HOLBORN ASSETS “CHAMPAGNE KILLER” APPROACH TO FINANCIAL ADVICE IS DESTROYING VICTIMS’ LIFE SAVINGS

Holborn Assets “Champagne Killer” approach to financial advice is ruining victims. Holborn Assets is routinely destroying people’s pensions and life savings, and refusing to compensate the distraught victims facing poverty in retirement. The so-called “advisers” at Holborn Assets give investment advice (often unregulated) which entails investing victims’ funds in whatever toxic, illiquid, high-risk rubbish pays the highest commissions, and then leave the devastated investors hung out to dry. Neither the firm nor the “advisers” responsible for this outrage show any compassion or contrition. This is no different to the callous actions of a common drunk, hit-and-run driver.

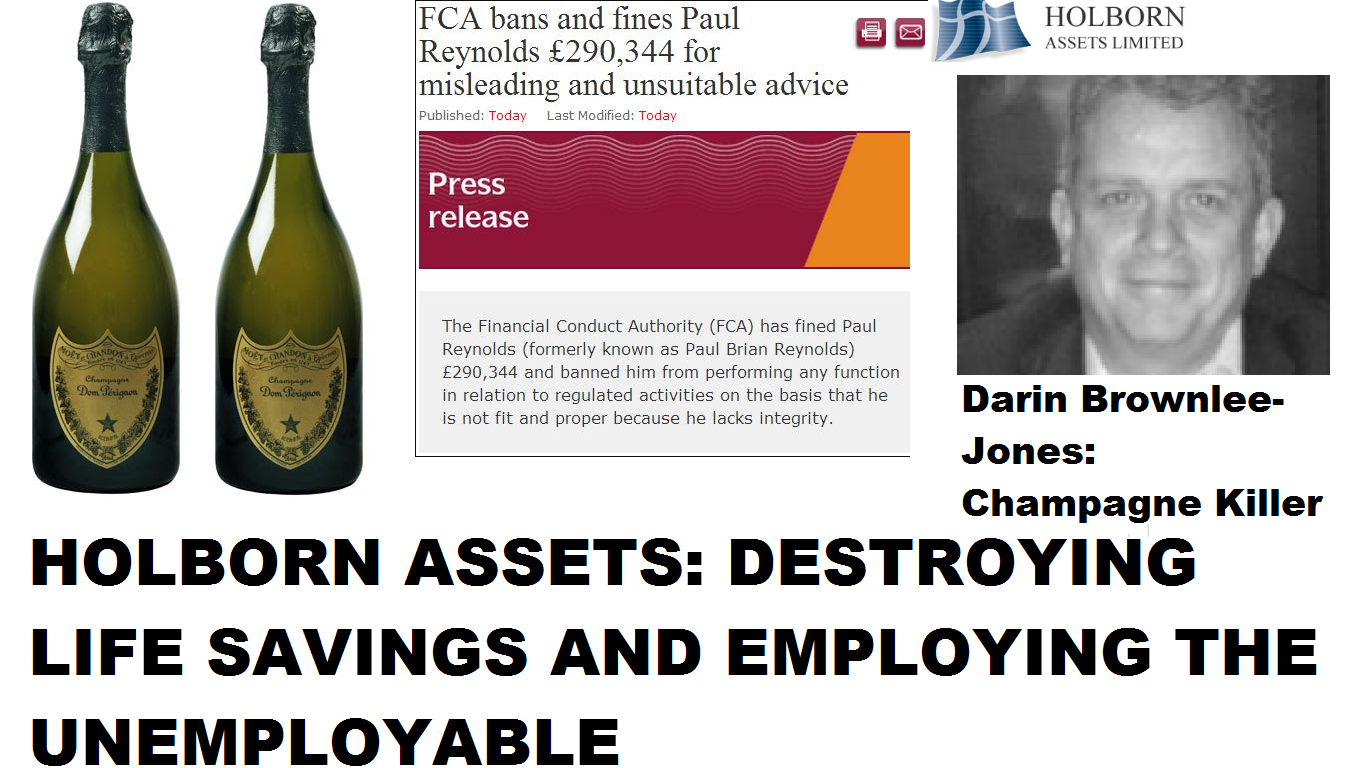

As if this wasn’t bad enough, Holborn Assets also employs Darin Brownlee-Jones: the “Champagne Killer“. A drunk hit-and-run driver who killed an innocent man then walked away to drink champagne. He didn’t stop to try to help the victim he left dying in the road – or show any remorse for the horrible, painful death the poor man suffered.

Holborn Assets seems to make a habit out of employing the unemployable. First, there was Paul Reynolds who was banned by the FCA and fined nearly £300,000 for giving unsuitable and misleading financial advice. The FCA declared Reynolds was not a fit and proper person to give financial advice. But Uncle Bob Parker of Holborn Assets Dubai welcomed him with open arms – and Reynolds has since changed his name to try to conceal his unsavoury past. But I bumped into Reynolds when I was at the Holborn Assets office at the end of 2015 – so I know it is him despite trying to change his appearance as well as his name.

And now there is Darin Brownlee-Jones who is commissioning pension reports for more poor unfortunate victims. These people are transferring their defined benefit pension schemes to offshore QROPS in dodgy jurisdictions where negligent trustees peddle their toxic wares. In one case, Brownlee-Jones has employed a Spanish firm to sign off a DB transfer for a resident of France. The advice is covered (allegedly) by the Spanish insurance regulator (which doesn’t cover pension or investment advice) and not the French regulator or the FCA.

So why would Brownlee-Jones in Dubai get a Spanish firm to provide unregulated advice to an investor in France? In 2003, the FSA had refused an application from Brownlee Jones to perform investment and pension-transfer functions. The reason was that the FSA did not consider him to be a fit and proper person as he had indecently assaulted a woman, caused criminal damage and death by dangerous driving.

I think any reasonable person would agree that Brownlee-Jones was the last person you would want handling investment and pension advice. But Bob Parker at Holborn Assets clearly likes having misfits, FCA rejects, sex offenders, drunks and killers on his team.

Brownlee-Jones: after a belly full of beer in 1999, got into his car and hit a motor cyclist head on. He left the poor man dying in a pool of blood and went to celebrate at his favourite wine bar. He ordered two bottles of Dom Perignon champagne at £95 apiece. When he was arrested, he was quaffing his favourite bubbly – although he probably wasn’t smiling quite so broadly when he was jailed for four years.

The distraught father of the victim said that Brownlee-Jones had treated his dying son “like an animal“. And yet Bob Parker employs this callous killer and encourages him to provide unregulated pension advice to victims in France and Spain.

This routine callousness is shown by Bob Parker and many other Holborn Assets salesmen. Where their victims’ pensions and investments have been decimated by high-risk structured notes and unregulated, toxic, illiquid funds -such as Premier New Earth Recycling – Holborn Assets just shrugs and leaves the victims to face poverty in retirement. Once they have earned their fat commissions from the victims’ pension funds, Holborn Assets doesn’t want to know any more. Bob Parker and his merry men simply walk away without a backward glance.

Holborn Assets has been aggressively targeting new victims with a cold-calling campaign using a well-known boiler-room scam operation in Manchester. The cold calls to Spanish residents are followed up by salesmen such as Jason Ryder who claims that Holborn Assets have offices in Barcelona and Marbella. Of course, Holborn Assets is not licensed to operate in Spain – and once conned into letting these cowboys plunder their pensions for fat commissions and fees, there is no regulator to complain to.

Apart from Bob Parker, Paul Reynolds, Darin Brownlee-Jones and a bunch of other “snake oil salesmen”, there are some people at Holborn Assets who do have some ethics and a conscience. Surely, if these people had any sense they would distance themselves from this cesspit of financial disservice? Why stay with a firm with such an appalling track record?

Below is a list of all the people who work for Holborn Assets (excluding admin and finance). I wonder if a single one of them will feel some sense of disgrace at being a part of this “champagne killer” approach to financial services?

Robert Parker, Phillip Parker, Simon Parker, Gerard Frew, Gerard J Leahy, Adrian Bliss, Alexander Herbert, Andrew Jarvis, Daniel Quinn, Joanne Phillips, Michele Carby, Nicholas Thompson, Rubina Khan, Ryan Quinn, Vince Truong, Paul Barrass, Kapil Mathur, Mark Powsney, Payal Trehan, Richard Hanna, Samuel Ebbs, Simon Burrass, Steve Lawton, Steven Downey, Usman Ahmed, Conor O’Shaughnessy, Anthony Murray, Colin Estlick, Creigh Classey, Jamie Arthur, Gavin Webster, Guillermo Martorell, Adrian Luscombe-Whyte, Tim Sant, Stuart Bichard, Richard Colburn, Kevin Curtis, Alison Sant, Ian Leigh, Darin Brownlee-Jones, Colin Kneale, Bryan Wawman, Vivian Van Eeden.

If not a single one of the above group of people is prepared to put ethics and principles at the top of their agenda and ensure their professional reputations are not sullied by the “champagne killer” approach to financial advice, then there truly is no hope for Holborn Assets.

**************************************************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Is it right to shame everyone in the company for what a few people have done?

Why exclude admin and finance employees from your list if you are going to make a comment like “there are some people at Holborn Assets who do have some ethics and a conscience. Surely, if these people had any sense they would distance themselves from this cesspit of financial disservice? Why stay with a firm with such an appalling track record?”

I know for a fact that not everyone has much choice of who they work for. The only choices are: work for the company or starve. Nor do all of these named employees focus on selling only Holborn Assets products.

Whoever you are, you have clearly been burnt with a bad experience with this company and you are taking it out on everyone instead of the person who burnt you.

My advise is to focus all your energies on that person rather than destroy the reputation of those who are not involved.

I aimed the blog at the front-line snake-oil salesmen who peddle their toxic wares. I know there are a few decent advisers, and I want them to come forward and help kick out the stinkers which Uncle Bob Parker really ought to have jettisoned.

Then why put the names and dirty the good guys? Not all of them can afford to leave or do what you want them to do. Not everyone has earned so much money taking advantage of people and so therefore have nothing to fall back on in the event of something going wrong. Those who have not taken advantage of others don’t have that extra money to fall back on.

Because they have the power to change things. The “good” guys must appreciate there are good clients who are going to be exposed to financial ruin. And some will commit suicide because they will never be able to retire because of Holborn’s “bad guys”. I have little sympathy with the “good” guys if, after reading this blog, they don’t up sticks and go to work somewhere else – somewhere where such bad practices are not routine and where the boss (i.e. Uncle Bob Parker) doesn’t tell the victims that the “case is closed” when they complain.

The “good guys” surely cannot be entirely oblivious of what a cesspit Holborn Assets is? How many innocent victims are ruined? How many times Bob Parker refuses to even consider the ruined victims’ life savings are destroyed by Holborn Assets’ rogue “snake oil salesmen” destroy people’s life savings. I hope that if there are a few of these people with a conscience or with some ethics they will up sticks and leave. This should sort out the men from the boys once and for all.

All well and good and very easy to do when you are in a position to leave. Jobs are very scarce in today’s world.

Hi Angie, I would like to state that I will be taking legal advice on this as you have sullied my good name in pursuit of your campaign of destruction. Financial advice is between the client and the adviser and you have over- stepped the mark on this one I’m afraid. If a large company like RBS (constantly in the press for law suits) is or has been seen to be doing wrong, should we besmirch the reputation of 10’s of thousands of staff? Do you think you would get away with that?

I hope that if you have received bad advice that you are properly compensated, as you are going to need the money to fight your next legal battle. How dare you tar and feather everyone with the same brush.

Just to clear things up, my name is Angie but I have a different surname to the person who has written the article.

Would you be kind enough to give me your full name then instead of changing it like some of the people you describe in your article please. Let’s let the legal process decide if you have anything to answer for. Promise I won’t try and convict you like you have done to me by association in your kangaroo court.

My name is Angie Brooks, Director of Pension Life. The website is http://www.pension-life.com and my landline is 0034858995645 and mobile is 0034674746663. I have had several calls from your colleagues today and they have asked me (courteously) to remove their names from the blog and I have done so. I have already offered to take your name off the blog but I need to know what your name is. Happy to speak or communicate by email: [email protected] or [email protected].

I would insist you remove my name from the article immediately. You did not ask me courteously to include my name and had I committed any of the crimes you have charged me with I would crawl under the nearest rock and keep my mouth shut.

I have spoken to my solicitor and he is aware of the matter. Do not post my reply or associate my name with any more of your publications my name is Gerard Frew and my record is unblemished. Should you continue to associate my name with your article you will hear from my solicitor in due course.

As I stated to you DO NOT post this reply.

Can you please confirm that you have checked that your name GERARD FREW has been removed from the blog post? Also, I am a little confused about where you are based and how you are regulated – it seems you are working out of Sweden. And why would a chartered financial adviser want to be associated with Holborn Assets Dubai in the first place? Surely you can’t be associated with Holborn Assets UK can you? Your colleague David Wells seems to be acting as your “agent” as he has emailed me about you – so I am puzzled as to why you couldn’t email me yourself.

Oh for goodness’ sake, what an own goal!

Hardly a great advert for chartered. A similar firm here says- The international financial marketplace needs professional standards, such as chartered status, to help expatriates like you identify who can be trusted to give financial advice.

Sorry mate, there is a long way to go before that happens.

Once again, doubts are raised about licences. If everyone put a list of their licences on their websites, explaining what they can sell and where they can sell them, then it would go a long way to restoring public confidence in advisers.

This industry keeps on shooting itself in the foot.

Angie,

Keep up the good work. This site is becoming a “must read” for professional trustees managing DC and DB schemes in the UK.

Holborn Assets is scamming people all over the world. The so called good guys would not join the firm on the basis of the FCA review and the crooks they employ

Sensationalist Journalism – slanderous at best – ” Bob Parker at Holborn Assets clearly likes having misfits, FCA rejects, sex offenders, drunks and killers on his team.”

Silly Girl!!

So let me be more specific: two FCA rejects; one sex offender; one drunk and one killer. Is that better?

Your wild remarks about %’s and ” decimated by high-risk structured notes and unregulated, toxic, illiquid funds ” – your evidence ?

Not wild at all and will happily send you the evidence if you give me your email (I don’t think “gigglemail” is going to work).

Why not submit this as part of your article, you’re happy to paste pictures and icons of your other remarks, seems remiss not to qualify all your statements with equal facts

Interesting, you remarks about Brown-Lee Jones are not complete or accurate, also 18 years out of date !

Always happy to be corrected Simon. If I have written anything you believe is incomplete or inaccurate I will gladly put it right.

Following your trail and doing just a little reading from reputable media it appears you have picked out the trash in a very old story, I m sure the parents and friends of the deceased are comforted by your article – you fail to present background and other facts relevant to the case – I have no interest in the bodies being discussed but I think we both know the reporting is very one sided !

Would be a more balanced article and Blog if you placed all the facts before us and allowed intelligent people to form an opinion based on fact, maybe something more uptodate, not 20 years old ?

Simon, with respect you are missing the point. The blog is about the approach of Holborn Assets: Some of the advisers destroy a victim’s life savings, then walk away without a backward glance. And Bob Parker does nothing about it. The reason for referring to the “Champagne Killer” is to draw the parallel between the callous actions of a drunk driver who flees the scene to drink champagne, and the callous actions of a minority of Holborn Assets’ advisers who invest their clients’ savings and pensions in toxic, high risk-rubbish, and then wash their hands of all responsibility. And Bob Parker lets them do it. He has spent three years cowering away and hiding from me – rather than standing up to his clear responsibilities. His failure to address these matters are neither professional nor Christian.

Are you suggesting that A – ‘advisers’ have access to and personally ‘invest’ a person’s money into ‘toxic, high risk rubbish’ ?

Or B – are you reporting on funds which are mass marketed, stamped and badged then presented to Brokers who offer them, amongst several hundreds of others, to clients to chose from, and subject to approval by the custodian of the scheme are ‘bought’ by the custodian on the ‘member’s’ instructions ?

Can we have some clarity – because if it is option A, then this is fraud – if it is Option B then this is a matter for the Ombudsmen and similar authorities because the fund managers are responsible to their ‘clients’, the adviser does not have any input or influence on what happens inside a fund.

I bought a CIS pension in late 90″s and lost over 119,000 in 2008/9 – was my Broker at fault? Was CIS at Fault, was this the collapse of the funds and markets?

Would a blog trashing the CEO of CIS have helped ?

Re your victims and their decimated savings/’loses’

Could you focus on the fund and the fund managers and ask what they did with the money entrusted to them?

Could you use your influence and push to ask questions of the regulator or authorities to explain why this is allowed to happen?

Could you use this forum to expose why no-one researches or recovers the millions of pounds that have been written off by the HMRC and DTI when these companies claim administration or insolvency?

Because my reading is that you blasting a broker for the collapse of a fund and this no better than blaming the girl who served you in Tesco for the toaster you bought that turns out to be faulty !

Simon, this is quite a long question so I am going to break it down into smaller sections. I have pasted your question below and put my answers in CAPS:

Are you suggesting that A – ‘advisers’ have access to and personally ‘invest’ a person’s money into ‘toxic, high risk rubbish’ ? YES – ABSOLUTELY

Or B – are you reporting on funds which are mass marketed, stamped and badged then presented to Brokers who offer them, amongst several hundreds of others, to clients to chose from, and subject to approval by the custodian of the scheme are ‘bought’ by the custodian on the ‘member’s’ instructions ? AGAIN, YES.

Can we have some clarity – because if it is option A, then this is fraud – if it is Option B then this is a matter for the Ombudsmen and similar authorities because the fund managers are responsible to their ‘clients’, the adviser does not have any input or influence on what happens inside a fund. YES TO BOTH. BUT IN OPTION B IT SHOULD BE ABOUT CHOOSING FUNDS WHICH MEET THE RISK PROFILE AND SUITABILITY REQUIREMENTS OF THE CLIENT – RATHER THAN GOING FOR THE FUND OR NOTE THAT PAYS THE HIGHEST COMMISSION.

I bought a CIS pension in late 90″s and lost over 119,000 in 2008/9 – was my Broker at fault? Was CIS at Fault, was this the collapse of the funds and markets? DEPENDS HOW YOUR PENSION WAS INVESTED AND BY WHOM

Would a blog trashing the CEO of CIS have helped ? HELPED WHOM? YOU, CIS? THE BROKER? KNOWLEDGE IS POWER AND TO SPREAD THE WORD THAT PENSIONS AND INVESTMENTS CAN COLLAPSED DUE TO A VARIETY OF CAUSES WOULD HAVE HELPED EDUCATE THE PUBLIC AND PERHAPS MADE A FEW PEOPLE MORE CAUTIOUS.

Re your victims and their decimated savings/’loses’

Could you focus on the fund and the fund managers and ask what they did with the money entrusted to them? I WOULDN’T WASTE MY TIME. IF THEY WERE HIGH-RISK, PROFESSIONAL INVESTOR ONLY FUNDS, THAT WOULD BE A POINTLESS EXERCISE. IT WAS ALL ABOUT THE ADVISER WHO PICKED THE FUNDS – FOR LOW RISK, CAUTIOUS INVESTORS.

Could you use your influence and push to ask questions of the regulator or authorities to explain why this is allowed to happen? YES – DOING THAT AS WE SPEAK.

Could you use this forum to expose why no-one researches or recovers the millions of pounds that have been written off by the HMRC and DTI when these companies claim administration or insolvency? COULD DO, BUT IT WOULDN’T GET US ANYWHERE.

Because my reading is that you blasting a broker for the collapse of a fund and this no better than blaming the girl who served you in Tesco for the toaster you bought that turns out to be faulty ! THE DIFFERENCE IS THAT TESCO IS “HELP YOURSELF”. THE CUSTOMER MAKES THE CHOICES AND THE GIRLS ON THE CHECKOUTS JUST READ THE BAR CODES. PROVIDING INVESTMENT ADVICE IS ENTIRELY DIFFERENT. BUT ALSO REMEMBER, IN TESCO AND ALL OTHER SHOPS, IT IS ILLEGAL TO SELL KNIVES, GLUE AND PORN MAGS TO UNDER 18S. SIMILARLY, IT SHOULD BE ILLEGAL TO SELL HIGH RISK ASSETS TO LOW RISK INVESTORS.

Short reply – No broker collects money from a client – Ponzi Schemes possibly – I am confident Holborn’s advisers do not collect or receive clients money

Trustees/Custodians double check and sign off all ‘trades’ on any policy – the risk profile and fund are very important – they are the clients ‘Police Officer or gatekeeper – if what you suggest has happened – who or where was the trustee ? Trustees and scheme administrators police all trades – risk profile, fees, charges and commissions are visible to them – are you suggesting the trustee was in on it ?

The markets collapsed in 2008/9 – loses across the world c.15 Trilliion – confident the Co Op pension scheme was professionally and ethically invested!

Re your comment about fund managers – we are back to your interpretation of the fund type and risk profile – brokers can not promote what they want to who they want – the industry is regulated – the Trustee/Custodian is policed and reports to the Ombudsman etc

Your remark re shops and prohibited goods goes back to the Trustee and their care of the client – question is … who signed off on the ‘business’. You have mentioned Gower Trustees – what communication have you had with them?

I know brokers don’t collect money from clients – but they do act as discretionary fund managers (even when they shouldn’t). I am afraid you are mistaken if you think trustees/custodians double check and sign off all trades on any policy – that simply is not what happens (although it jolly well ought to happen). Trustees and administrators do not police trades – although they should. I am not suggesting trustees were in on it – just that they did no due diligence on the investments. Brokers do indeed promote what they want to who they want – often they don’t even tell the investors. The industry may well be regulated, but many of the brokers are not regulated. Gower Trustees in Guernsey was accepting business from unregulated advisers such as Stephen Ward of Premier Pension Solutions in Moraira – even after Gower had warned the members against using Ward. But then they went ahead and accepted it anyway and allowed Ward to invest 100% of investors’ money in EEA Life Settlements – a professional-investor-only fund which had already had one FSA warning against it.

We need to ‘debate’ these and other points over Sangria …. I have worked with the industry for over 30 years and can confirm that these ‘shannigans’ are very rare and often blown up or exaggerated – I challenge you to find me a compliance team or officer in any registered regulated Trustees office that does not question a Trade – this is a basic requirement of their job and training – they are called sales prevention officers by the industry because they make a VAT inspection feel like a children’s Xmas party !

Which Broker firms or funds do you feel operate in the way you advocate ?

Mine’s a large one 😉 Will have to disagree with you over this being a “very rare” problem and I assure you I never exaggerate. Email me on [email protected] and will happily give you some redacted cases as examples.

I think Simon is living in a parallel universe, the mis-sale of UCIS (Normally wrapped in insurance bonds to stiff the clients even more) within offshore pensions is out of control.

Do the trustees check that the sales people (who are not IFAs whatever they may say) are properly regulated in the jurisdiction in which they and the client operates? Do they check that the sales people are even qualified to acceptable standards?

Do the trustees know, ask or even care, about the huge commissions being filched from the clients’ retirement under the guise of free advice?

Do they question every trade?

My suggestion is that they do none of this, based on what I have seen, which is why websites like this appear.

The industry needs to up its game and report and stop poor practice, otherwise there will be more sites like this. This site is an inevitable consequence of all of this and the blame should be on those that caused this to happen and not the messenger.

Mrs Brooks,

You are wasting your time arguing with dinosaurs like this in the UAE. The only people that are going to take issue with you will be the 80s style product floggers and the lawyers that fawn on them for fees. I refer to the initial comment from a guy that wears slip-ons and kipper ties.

As for Simon’s comments, refer him to the FCA commentary about this individual.

Everything I ever write is always backed up by hard evidence – including the FCA and various Ombudsmen. I don’t ever see it as a waste of time to expose bad practice. But slip-ons and kipper ties sound horrendous!

Payal Trehan was fired for gross misconduct and reported to the police and the authorities for technically what was theft. Subsequently she was welcomed with open arms to Holborn Assets despite being warned who she was and how she abused her position of trust with her clients.

Joe Capaldi unfortunately managed to remove the news article about his mis-selling fine https://mobile.twitter.com/williamehunter/status/118779713815711744

Which firm did Joe Capaldi work for at the time of the fine?

Yes, which firm please?

A friend of mine was advised to transfer 4 pensions (including a FS one) into a SIPP. Initial value was over £120k now worth less than £20k. No final salary transfer analysis was conducted. These guys are crooks. Avoid!!!

I am afraid this is typical behaviour of Holborn Assets. They do transfers irrespective of whether they are in the interests of the client – and then invest the victims in crap which pays maximum commissions.

A SIPP is a UK pension, name the SIPP firm involved. It sounds very much like non-standard investments were recommended and this needs flagging to the FCA.

Some of us are getting sick to the back teeth of funding the FSCS to cover the appalling advice into opaque funds that would not be allowed in any decently regulated environment.

Brooklands trustees were sipp provider . They went into administration and taken over by heritage pensions. They won’t even tell him the commission he paid because they are not required to!