Pension Scams Explained

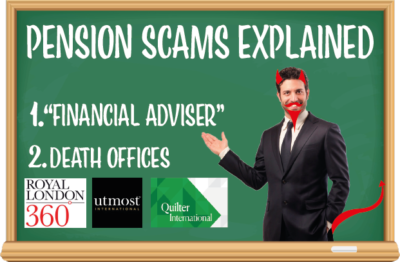

Every offshore pension scam starts with a “financial advisor”. Or, at least, a slick salesman posing as a financial adviser. This person can also call himself a “wealth consultant” or “senior associate”. After the scammer pretending to be an adviser, the next player is the life office. More accurately described as a “death” office, this

Boris on Crime (I see no fraud!)

At the end of January 2022, Boris Johnson claimed he had reduced crime by 14%. Boris shocked a lot of people with this figure. But, apparently, he wasn’t talking about fraud. He’d forgotten that even some of his own constituents had been defrauded into the Ark pension scam (and that he had promised to “sort

2021/22 Roundup for Pension Life

2021 was a tough year for everybody in the world. But for Pension Life it was especially frustrating because courts and law firms were severely held up as they got to grips with the challenges of Covid, travel restrictions and working remotely. Attending hearings and meetings by video conference was a hit-or-miss affair. The success

Pension Scam Investments

The world of pension and investment scams is dominated and driven by commissions on investments (usually unregulated). The scammers’ strategy is always identical: get the pensions away from the safety of a reputable pension provider and into the hands of a SIPP, a SSAS or a QROPS. One purported benefit of these types of schemes

CRIMINAL CASE AGAINST UNLICENSED FINANCIAL ADVISERS

haps “the end” will be just the beginning. A new dawn for an offshore financial services industry which sells proper financial advice – and not just commission-laden products.

FCA Investigates Ark and AES

The FCA seems to have woken up. It only took eleven years. Eleven years of laziness, torpor, disinterest and deliberately ignoring the problem. But, completely out of the blue, the FCA has suddenly got bored with crapping on bathroom floors and has decided to do a spot of rather belated regulating. The object of this