Laurence Goodman and the three wishes: please make 37 Fast Pensions Scam loans disappear JUST LIKE THAT!

Bridgebank Capital’s Laurence Badman Goodman has made 37 Fast Pensions Scam loans disappear as if by magic – while he was on holiday and too busy to engage with Pension Life or the distraught victims of Peter and Sara Moat.

Having discovered this was where some or all of the elusive Fast Pensions Scam funds were hiding, we all hoped this might finally result in some of the 18 Pensions Ombudsman’s determinations to allow victims to transfer out being complied with.

We all wanted to believe that Goodman was a good man, but now it would seem the opposite might be the case. So, one of the following is true:

All the borrowers of the 37 loans have simultaneously repaid their loans on 17th August 2017

The loans have been sold or transferred on to somewhere we can find them (yet)

Sara Moat had been claiming that Fast Pensions was merely the administrator of the pension schemes, and that it was ultimately the “responsibility of the trustees to decide whether the transfers could be made”. Of course, the Companies House records showed that the Bridgebank Capital loans were made in favour of Sara Moat as trustee (along with another stooge called Martin Peacock). This scuppered Sara Moat’s excuse and exposed her as a liar once again.

So, when Goodman has finished having a jolly time on the Costa Lot, necking his champers and writing his postcards to his mate Pete, perhaps he might find a moment to be sober enough to remember that I am meeting the Serious Fraud Office next week. And most of the Fast Pensions Scam victims have also submitted their reports to the SFO.

Frantic with worry – the Fast Pensions victims now know their pension funds are being used for property loans.

Bridgebank Capital seems to be a bona fide property loan company – providing bridging and development finance. Nothing wrong with that.

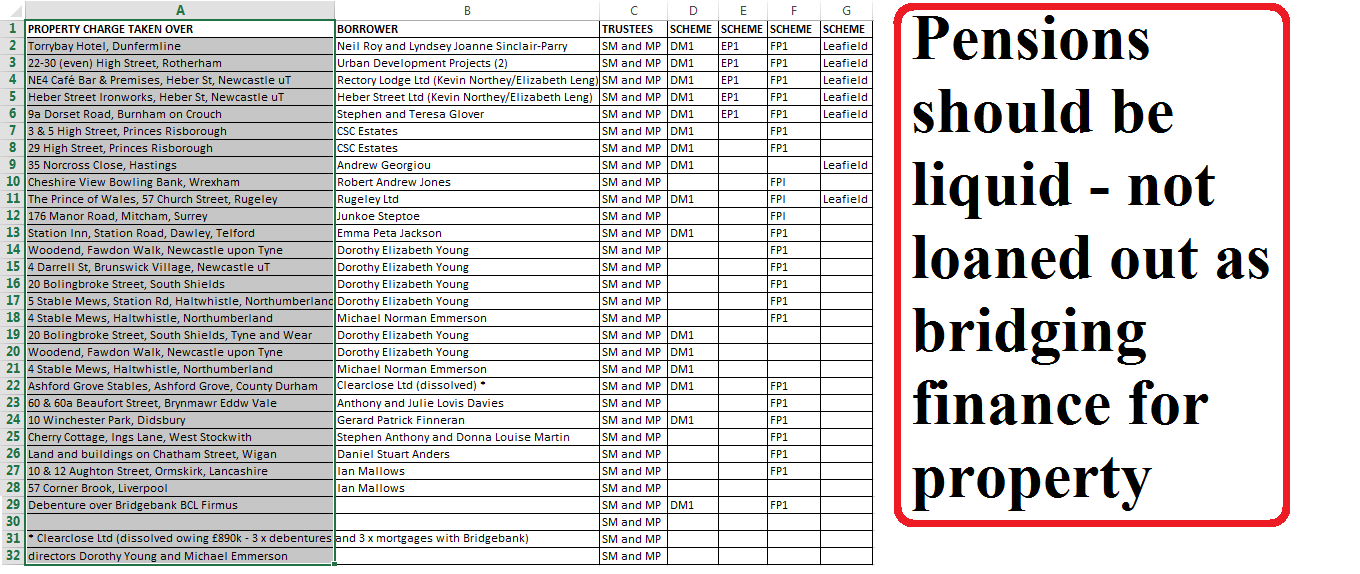

But Bridgebank Capital No. 5 seems to be full of Fast Pensions money and locked into term loans secured on a variety of domestic and commercial properties. Each charge refers to the trustees of four of the Fast Pensions schemes: DM1, FP1, EP1 and Leafield. The trustees of each of these schemes are clearly identified at Companies House as Sara Moat and Martin Peacock. (Interestingly, Sara Moat is telling victims that “the trustees” have to decide what happens to the pension monies – while hiding the fact that she is the trustee).

Of great concern is the fact that one of the borrowers, Clearclose, has gone bust owing the pension fund nearly £900k.

The Pensions Ombudsman has made 18 determinations against Fast Pensions – but Sara and Peter Moat of Fast Pensions have studiously ignored them. I sent links to all of the background to Fast Pensions to Laurence Goodman of Bridgebank Capital on 6th August 2017:

Dear Mr. Goodman

It was good to speak to you on Friday.

First of all, may I say that I recognise that Bridgebank Capital is a bona fide finance company and I mean no criticism against you or your company in the summary I am setting out below. I have tried to summarise the position in a bullet-point series of statements to make this as easy to understand as possible.

Once you have read and digested this, please can we start a dialogue about what happens next. What the members need to know, is how much do these various loans/charges/mortgages in favour of the four Fast Pensions schemes realise when they mature, and what will happen to the money. I realise you are restricted to an extent in terms of what you can tell me, but there are many Fast Pensions victims who will happily provide you with letters of authority as they are the beneficiaries of the pension schemes and have a legal right to know what has happened to their pension funds.

Best, Angie

—————-

* There are hundreds of members of various pension schemes (including DM1, FP1, EP1 and Leafield) run by Peter and Sara Moat of Fast Pensions – a pensions administration company.

* The Moats maintain they are not the trustees of the schemes. Peter Moat (masquerading as “James Porter”) told me the trustee was a company called FP Scheme Trustees, of which one Jane Wright is sole director. She was an employee of Moat’s at his former company Blu Properties in Javea which folded and it is believed she was paid to be the director of this company.

* The charges registered at Companies House for Bridgebank Capital No. 5 show all the loans as being in favour of Sara Moat and Martin Peacock (an associate of Peter Moat’s) as trustees of the Fast Pensions schemes.

* The various Fast Pensions schemes – including DM1, FP1, EP1 and Leafield – I believe are all bogus occupational schemes. When I say bogus, what I mean is that they were not set up to provide genuine pensions for employees of a company which intended to trade and create jobs, but merely as a vehicle for a pension liberation scam.

* Peter Moat told me (while he was masquerading as a “James Porter”) that the underlying assets of the Fast Pensions schemes were “invested in Bridgebank Capital” and also in another loan company called Pamplona Capital Partners. Clearly, having the underlying assets of a pension scheme solely “invested” in property loans is not acceptable. A pension scheme is required to have low-risk, liquid assets as members have a statutory right to a transfer and need to be able to take their 25% tax-free lump sum at age 55, or retire or die.

* The Moats have failed dismally to communicate with the members or respond to transfer requests for a long period of time – causing considerable distress to the victims. The Pensions Ombudsman has made a large number of determinations in response to complaints by the victims and has ordered Fast Pensions to allow the victims to transfer out and pay compensation for their distress. These 18 determinations have all been ignored by Fast Pensions:

Needless to say, there is no evidence that the Moats have complied with any of these determinations and the victims themselves report that they have not.

* Alongside the pension transfers and lending of the pension funds to Bridgebank Capital No. 5, the Moats were operating pension liberation in the form of loans from Moat’s companies Blu Debt Management and Umbrella Loans. Victims were told these loans were not connected to the pension transfers and would not be taxable. HMRC is now sending out tax demands in respect of these loans.

* There are grave concerns about the Bridgebank Capital No. 5 loans for the following reasons:

1. We do not know what the total amount lent to Bridgebank Capital is

2. There are multiple loans to the same parties

3. One borrower is in liquidation

4, We do not know what the terms of the loans or the interest payable are

* The greatest concern is that if any part of the money is recoverable and is paid back into the control of the Moats, it will simply “disappear” again and not be available for the benefit of the members who are the ultimate beneficiaries.