Spongebob Parker Squarepants of Holborn Assets has apparently been telling his salesmen that he has paid Glynis Broadfoot £150,000 in compensation for the destruction of her pension by Holborn Assets.

Not only is this a big porky pie (she hasn’t had a penny) but it is a cynical and dishonest tactic used to placate and dupe the Holborn Assets salesmen into wrongly believing that Spongebob has ethics. He doesn’t. If he had any morals, ethics or principles, he would come to the table and sort this appalling mess out.

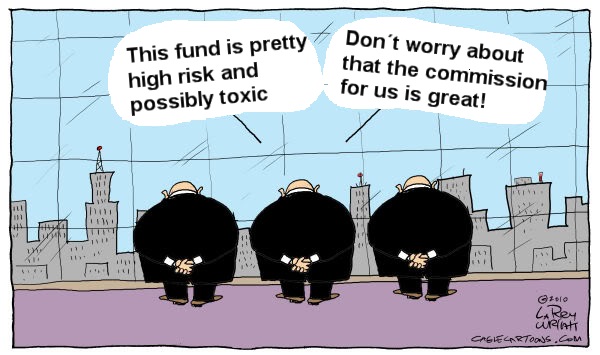

Spongebob effectively stole Glynis’ life savings – a final salary scheme. Then invested her pension into an expensive and unnecessary insurance bond and purchased toxic, high-risk, professional-investor-only structured notes. He did all this to earn the maximum amount of commission – in the full knowledge that this would put her pension fund at risk. In fact, tactics identical to the Continental Wealth Management scam.

Glynis has now gone through more than five years of hell as she watched the systematic destruction of her pension. And now you can imagine how she feels reading reports of Holborn Assets’ vulgar and disgusting “jolly” in Tanzania which cost half a million quid. Despite making a series of totally inadequate offers, Spongebob has still to pay her a penny.

I hear on the grapevine that Spongebob is paranoid about any of his staff talking to me. He has even sacked one adviser – Claudia Shaw – on suspicion of communicating with me. It is true that quite a few Holborn Assets people have indeed communicated with me. These include – inter alia – Jerry Leahy, Joe Capaldi, Benjamin Thompson, Matthew Newman, James McMullen, Michael Cunningham, Ben Buckley, Marlon Bruges, Keren Bobker, Michele Carby and Syeda Al Iqtadar. Also, I’ve met Paul Reynolds and Chimaa Mefta at Holborn Assets’ Dubai offices. Also, Darin Brownlee-Jones tried to befriend me on Linkedin. Why hasn’t Spongebob sacked all of these people? He harbours a convicted killer and someone who was struck off and fined by the FCA. I’ve also been approached by various people claiming to work for Holborn Assets and offered a bribe to stop blogging about the company’s nefarious practices.

So, Uncle Spongebob – here’s my invitation. Stop sponging off Holborn Assets’ victims, come to the table and talk to me. Negotiate a decent redress package for Glynis and the others. Then, undertake to do business in an ethical, professional and compliant manner moving forward. Stop hosting binge-drinking, drug-snorting binges, and put in a place a proper compliance department.

Seriously, I don’t bite. I came to your office a couple of years back. You have ignored me since. So maybe now it is time for you to come to my office?

Simples! And then I can write nice blogs about you and the other Parkers saying what heroes you have been and what a good firm Holborn Assets is.

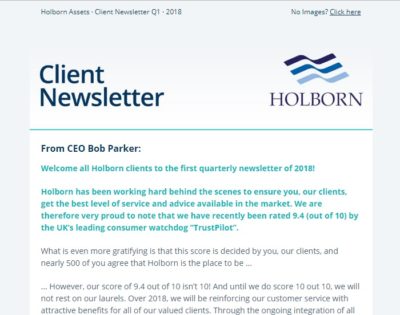

Seems we can´t get enough of Holborn Assets’ cheek this week. CEO Bob Parker has sent out a Q1 2018 newsletter and included on his mailing list a very unsatisfied and traumatised client who, through Holborn Assets’ negligence, has suffered a significant loss to her pension fund, with no compensation – or even apology.

Glynis Broadfoot was a victim of Holborn Assets’ rotten advice and service in 2011 and which resulted in her losing a significant portion of what had originally been a final-salary pension which should never have been transferred in the first place. Holborn Assets refused to help her, and simply kept taking their extortionate fees from her ever-shrinking pension pot. They had invested her in high-risk, professional-investor-only structured notes which were totally inappropriate for a low-risk investor.

You can imagine Mrs. Broadfoot’s fury and disgust when this message popped up in her inbox.

In summary, despite the expensive advice given to Mrs. Broadfoot by Holborn Assets, and assurances that her pension would grow at 8% per annum, she ended up losing nearly a third of her fund. Despite the fund’s losses, Holborn Assets continued to apply their fees to the fund, totaling somewhere in the region of £11k!

Holborn Assets informed her, at the height of her distress over her losses, that they “had closed the case, and would not enter into any further correspondence”.Yet now, several years on, it appears she’s still on their mailing list – despite knowing full well they have left this victim’s retirement prospects in tatters.

Mrs. Broadfoot’s case was typical of “fractional scams“: expensive and unnecessary insurance bond (only purpose was to pay a fat commission to the scammers); expensive, high-risk, professional-investor-only structured notes (again, high commissions for the scammers and heavy losses for the victim); hefty advisor fees. This was a very obvious scam which caused great suffering for the victim who is resident in Spain – but Holborn Assets was not licensed to provide investment advice in Spain.

In the years since Mrs. Broadfoot was scammed, Bob Parker did start to engage half-heartedly with a process of negotiating compensation for her losses. But so far she has not received one penny. Her local government final salary pension scheme – which she was conned into sacrificing by these unlicensed scammers – would have provided her with a guaranteed, index-linked pension for life and she could have retired comfortably. Instead, she has a seriously damaged fund which is unlikely to ever recover and provide her with the retirement income she needed and deserved.

So, far from getting the “best level of service and advice available” as boasted by Bob Parker, Mrs. Broadfoot was conned, scammed, fleeced and then dumped by Holborn Assets.

Which brings me on to the Trust Pilot reviews. Only 2% scored Holborn Assets as average or poor. Which is very surprising – given the number of people who report similar stories to Mrs. Broadfoot’s. But I think it is likely that those who gave four or five stars, haven’t yet found out what their losses are. In fact, some of these reviewers admit they were cold called by Holborn Assets. We know for sure Claudia Shaw was flogging the high-risk Premier New Earth Recycling UCIS fund to her victims and that there have been heavy investment losses.

I don’t believe anyone from Holborn has contacted me since September last year. In August 2016 I was contacted and advised to switch my policy which seemed ridiculous considering the additional charges I would incur, the fact it was even suggested causes me concern.

Then in September 2016, I was contacted to recommend my wealth manager for an award, again the audacity of this makes me wonder.

I have no idea on what your investment performance to date is over the past 12 months and I have not been given any confidence how my investments will be managed going forward now that I have finished paying your fees and Iactually begin to get money invested.

I do plan to visit within the next month and hopefully by that stage you in a position to assure me I did not make a big mistake investing my money with you. Regards Ian Norton

Another victim has complained directly to Pension Life about the appalling treatment he has had at the hands of Holborn Assets:

“Since 2013, the fund has not done anything at all. The fees are much too high, excessive transactions have been made to earn themselves money on my account and the investments went down in value. There is no communication with Holborn Assets and they are unwilling to discuss this matter with me or to do anything about it.”

So, as the cheeky Bob Parker is aiming to infiltrate South Africa with his new weapon – the bright-eyed and bushy-chinned Lourens Reichert – I thought now would be a good time to make friends with Reichert and see if he can put some pressure on Uncle Bob. Reichert will, no doubt, be very pleased to help me sort these victims out – as he has a big bulging lump in his trousers courtesy of Bob’s golden handshake.

I might even nip down to Johannesburg and have a cup of tea and a cheeky biscuit with him. No doubt, he won’t want the sordid details of Holborn Assets’ scams to compromise his quest to conquer South Africa. If the natives find out just what his colleagues have been up to, he might find himself on the wrong end of a Zulu spear.

Investors are likely to have lost all their money in Premier New Earth Recycling fund – now in liquidation. The liquidator is Deloittes and they can’t say much, if anything, about what is happening as they are looking into the possibility of claims against third parties and don’t want to prejudice any possible action.

Rather than getting into the nitty gritty of the liquidation of this fund – and the appalling possibility that the investors may very well have lost everything – let us take a good look at the fund itself.

It is a UCIS. Nothing more to say – except:

“Specialist, qualifying, and qualifying-type experienced investor funds are unregulated collective investment schemes which are neither approved nor reviewed by IOMFSA. Once launched, the funds must be registered with the authority within 14 days. These types of funds cannot be sold to the retail public. Access to such funds is only available where investors confirm that they meet the fund type’s minimum entry criteria. This includes a statutory certification that they have read the scheme’s offering document and understand and accept the specific risks associated with that type of fund.”

So, instead of writing lots of fascinating stuff about the wonderful topic of generating energy from rubbish (which I am sure is really interesting and good for the planet), why don’t we stick with the unchallengeable fact that the fund was a UCIS and should not have been promoted to retail investors. End of. No argument. Non-negotiable. Talk to the hand. Stick your UCIS where the sun doesn’t shine.

In fact, the same was true (should have been true) of the Connaught bridging loan fund; EEA Life Settlements; LM; Store First, Park First, Trafalgar Multi-Asset Fund and Blackmore Global. So why did so many advisers promote them and invest their clients’ money in them? £$£$£$£$£!!! Commissions. Backhanders. Sandwiches. And the distressed investors are now paying the appalling price for rogue advisers’ greed and negligence.

And what does this look like from the investor’s point of view?

Appalling investment losses on Premier New Earth Recycling

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Holborn Assets mercilessly leaves its victims facing financial ruin

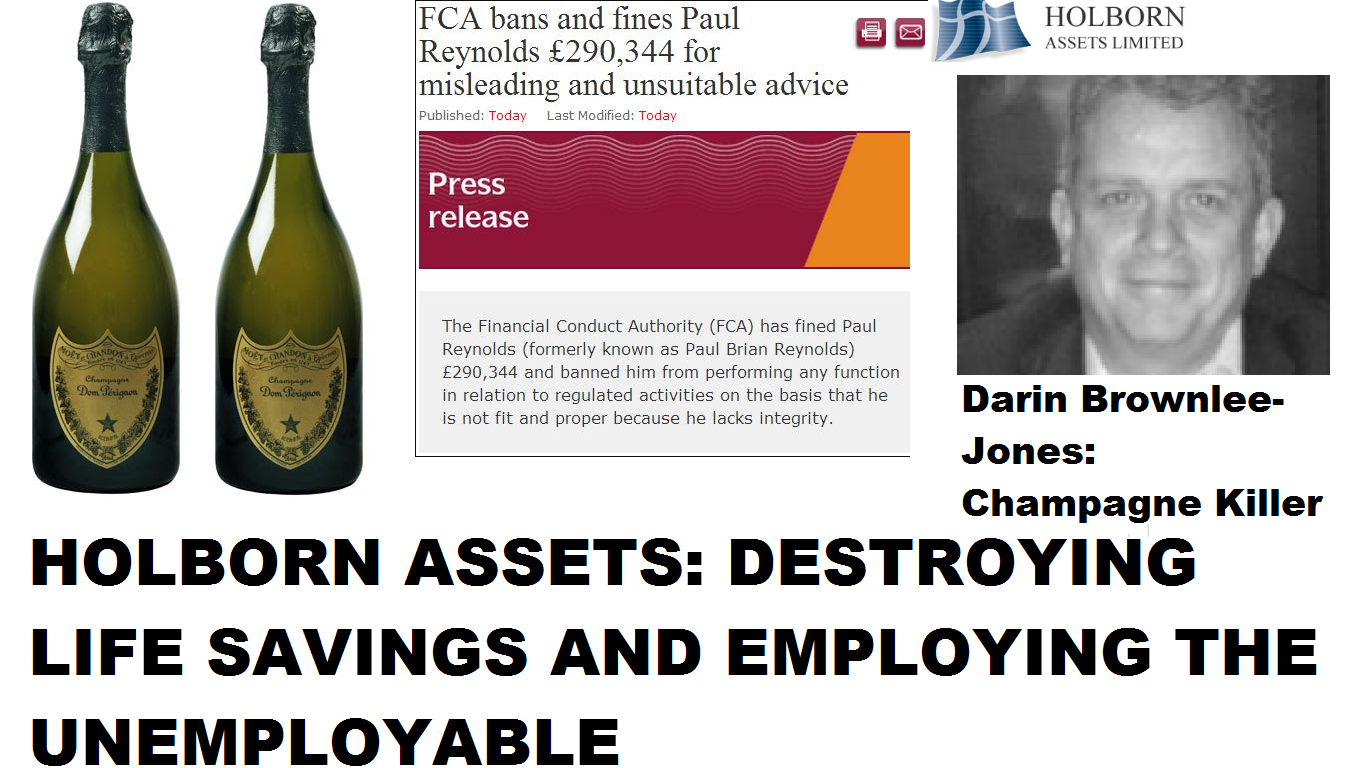

HOLBORN ASSETS “CHAMPAGNE KILLER” APPROACH TO FINANCIAL ADVICE IS DESTROYING VICTIMS’ LIFE SAVINGS

Holborn Assets “Champagne Killer” approach to financial advice is ruining victims. Holborn Assets is routinely destroying people’s pensions and life savings, and refusing to compensate the distraught victims facing poverty in retirement. The so-called “advisers” at Holborn Assets give investment advice (often unregulated) which entails investing victims’ funds in whatever toxic, illiquid, high-risk rubbish pays the highest commissions, and then leave the devastated investors hung out to dry. Neither the firm nor the “advisers” responsible for this outrage show any compassion or contrition. This is no different to the callous actions of a common drunk, hit-and-run driver.

As if this wasn’t bad enough, Holborn Assets also employs Darin Brownlee-Jones: the “Champagne Killer“. A drunk hit-and-run driver who killed an innocent man then walked away to drink champagne. He didn’t stop to try to help the victim he left dying in the road – or show any remorse for the horrible, painful death the poor man suffered.

Holborn Assets seems to make a habit out of employing the unemployable. First, there was Paul Reynolds who was banned by the FCA and fined nearly £300,000 for giving unsuitable and misleading financial advice. The FCA declared Reynolds was not a fit and proper person to give financial advice. But Uncle Bob Parker of Holborn Assets Dubai welcomed him with open arms – and Reynolds has since changed his name to try to conceal his unsavoury past. But I bumped into Reynolds when I was at the Holborn Assets office at the end of 2015 – so I know it is him despite trying to change his appearance as well as his name.

And now there is Darin Brownlee-Jones who is commissioning pension reports for more poor unfortunate victims. These people are transferring their defined benefit pension schemes to offshore QROPS in dodgy jurisdictions where negligent trustees peddle their toxic wares. In one case, Brownlee-Jones has employed a Spanish firm to sign off a DB transfer for a resident of France. The advice is covered (allegedly) by the Spanish insurance regulator (which doesn’t cover pension or investment advice) and not the French regulator or the FCA.

So why would Brownlee-Jones in Dubai get a Spanish firm to provide unregulated advice to an investor in France? In 2003, the FSA had refused an application from Brownlee Jones to perform investment and pension-transfer functions. The reason was that the FSA did not consider him to be a fit and proper person as he had indecently assaulted a woman, caused criminal damage and death by dangerous driving.

I think any reasonable person would agree that Brownlee-Jones was the last person you would want handling investment and pension advice. But Bob Parker at Holborn Assets clearly likes having misfits, FCA rejects, sex offenders, drunks and killers on his team.

Brownlee-Jones: after a belly full of beer in 1999, got into his car and hit a motor cyclist head on. He left the poor man dying in a pool of blood and went to celebrate at his favourite wine bar. He ordered two bottles of Dom Perignon champagne at £95 apiece. When he was arrested, he was quaffing his favourite bubbly – although he probably wasn’t smiling quite so broadly when he was jailed for four years.

The distraught father of the victim said that Brownlee-Jones had treated his dying son “like an animal“. And yet Bob Parker employs this callous killer and encourages him to provide unregulated pension advice to victims in France and Spain.

This routine callousness is shown by Bob Parker and many other Holborn Assets salesmen. Where their victims’ pensions and investments have been decimated by high-risk structured notes and unregulated, toxic, illiquid funds -such as Premier New Earth Recycling – Holborn Assets just shrugs and leaves the victims to face poverty in retirement. Once they have earned their fat commissions from the victims’ pension funds, Holborn Assets doesn’t want to know any more. Bob Parker and his merry men simply walk away without a backward glance.

Holborn Assets has been aggressively targeting new victims with a cold-calling campaign using a well-known boiler-room scam operation in Manchester. The cold calls to Spanish residents are followed up by salesmen such as Jason Ryder who claims that Holborn Assets have offices in Barcelona and Marbella. Of course, Holborn Assets is not licensed to operate in Spain – and once conned into letting these cowboys plunder their pensions for fat commissions and fees, there is no regulator to complain to.

Apart from Bob Parker, Paul Reynolds, Darin Brownlee-Jones and a bunch of other “snake oil salesmen”, there are some people at Holborn Assets who do have some ethics and a conscience. Surely, if these people had any sense they would distance themselves from this cesspit of financial disservice? Why stay with a firm with such an appalling track record?

Below is a list of all the people who work for Holborn Assets (excluding admin and finance). I wonder if a single one of them will feel some sense of disgrace at being a part of this “champagne killer” approach to financial services?

If not a single one of the above group of people is prepared to put ethics and principles at the top of their agenda and ensure their professional reputations are not sullied by the “champagne killer” approach to financial advice, then there truly is no hope for Holborn Assets.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Spongebob Parker Squarepants of Holborn Assets has apparently been telling his salesmen that he has paid Glynis Broadfoot £150,000 in compensation for the destruction of her pension by Holborn Assets.

Spongebob Parker Squarepants of Holborn Assets has apparently been telling his salesmen that he has paid Glynis Broadfoot £150,000 in compensation for the destruction of her pension by Holborn Assets. Glynis has now gone through more than five years of hell as she watched the systematic destruction of her pension. And now you can imagine how she feels reading reports of Holborn Assets’ vulgar and disgusting “jolly” in Tanzania which cost half a million quid. Despite making a series of totally inadequate offers, Spongebob has still to pay her a penny.

Glynis has now gone through more than five years of hell as she watched the systematic destruction of her pension. And now you can imagine how she feels reading reports of Holborn Assets’ vulgar and disgusting “jolly” in Tanzania which cost half a million quid. Despite making a series of totally inadequate offers, Spongebob has still to pay her a penny. Simples! And then I can write nice blogs about you and the other Parkers saying what heroes you have been and what a good firm Holborn Assets is.

Simples! And then I can write nice blogs about you and the other Parkers saying what heroes you have been and what a good firm Holborn Assets is. Seems we can´t get enough of Holborn Assets’ cheek this week. CEO Bob Parker has sent out a Q1 2018 newsletter and included on his mailing list a very unsatisfied and traumatised client who, through Holborn Assets’ negligence, has suffered a significant loss to her pension fund, with no compensation – or even apology.

Seems we can´t get enough of Holborn Assets’ cheek this week. CEO Bob Parker has sent out a Q1 2018 newsletter and included on his mailing list a very unsatisfied and traumatised client who, through Holborn Assets’ negligence, has suffered a significant loss to her pension fund, with no compensation – or even apology.

I might even nip down to Johannesburg and have a cup of tea and a cheeky biscuit with him. No doubt, he won’t want the sordid details of Holborn Assets’ scams to compromise his quest to conquer South Africa. If the natives find out just what his colleagues have been up to, he might find himself on the wrong end of a Zulu spear.

I might even nip down to Johannesburg and have a cup of tea and a cheeky biscuit with him. No doubt, he won’t want the sordid details of Holborn Assets’ scams to compromise his quest to conquer South Africa. If the natives find out just what his colleagues have been up to, he might find himself on the wrong end of a Zulu spear.

Investors are likely to have lost all their money in

Investors are likely to have lost all their money in