Investors are likely to have lost all their money in Premier New Earth Recycling fund – now in liquidation. The liquidator is Deloittes and they can’t say much, if anything, about what is happening as they are looking into the possibility of claims against third parties and don’t want to prejudice any possible action.

Investors are likely to have lost all their money in Premier New Earth Recycling fund – now in liquidation. The liquidator is Deloittes and they can’t say much, if anything, about what is happening as they are looking into the possibility of claims against third parties and don’t want to prejudice any possible action.

Rather than getting into the nitty gritty of the liquidation of this fund – and the appalling possibility that the investors may very well have lost everything – let us take a good look at the fund itself.

It is a UCIS. Nothing more to say – except:

“Specialist, qualifying, and qualifying-type experienced investor funds are unregulated collective investment schemes which are neither approved nor reviewed by IOMFSA. Once launched, the funds must be registered with the authority within 14 days. These types of funds cannot be sold to the retail public. Access to such funds is only available where investors confirm that they meet the fund type’s minimum entry criteria. This includes a statutory certification that they have read the scheme’s offering document and understand and accept the specific risks associated with that type of fund.”

So, instead of writing lots of fascinating stuff about the wonderful topic of generating energy from rubbish (which I am sure is really interesting and good for the planet), why don’t we stick with the unchallengeable fact that the fund was a UCIS and should not have been promoted to retail investors. End of. No argument. Non-negotiable. Talk to the hand. Stick your UCIS where the sun doesn’t shine.

In fact, the same was true (should have been true) of the Connaught bridging loan fund; EEA Life Settlements; LM; Store First, Park First, Trafalgar Multi-Asset Fund and Blackmore Global. So why did so many advisers promote them and invest their clients’ money in them? £$£$£$£$£!!! Commissions. Backhanders. Sandwiches. And the distressed investors are now paying the appalling price for rogue advisers’ greed and negligence.

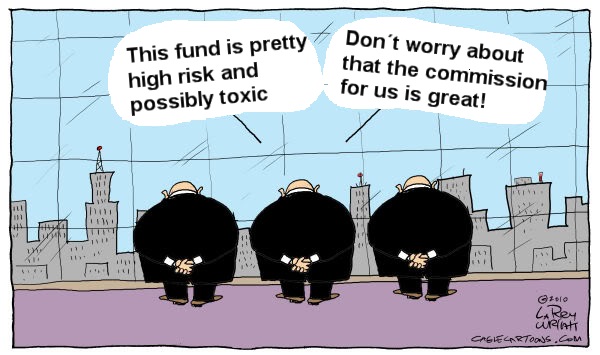

And what does this look like from the investor’s point of view?

**************************************************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

FOLLOW PENSION LIFE ON TWITTER TO KEEP UP WITH ALL THINGS PENSION RELATED, GOOD AND BAD.

Was that a sponsored champagne junket? If it was, do you know who sponsored it?

Reverse image search and you will find the answer.

https://www.facebook.com/forthpluspensions/photos/rpp.845103005602747/1231383896974654/?type=3&theater

That is either a blind link or it was pulled down by Forthplus Pensions(if that is the case, why take it down?).

Majority shareholder of Forthplus Pensions is interesting, Clare Hughes. She took over the holdings of Richard Ian Hughes in 2014.

https://www.ft.com/content/1b800be9-6791-307f-9e30-bfbcf2945d4d?mhq5j=e1

OLD NEWS -AGAIN – this was first reported in quality press/media over a year ago and is based on articles from 2014!

However – Are you suggesting that this adviser knowingly put clients money into a collapsed fund?

Is the statement from one clients portfolio …. if so, which Trustee or Life company signed it off?

Incidentally, Commissions in the industry are standard across all funds, you know this – unlikely to have been any extra ‘Commissions. Backhanders. Sandwiches.’

Do your homework and check into Premier – you will find their funds have been sold across the industry for some 15 years, this fund was in difficulty in 2013, would be interesting to know if this information was available to the adviser/broker or if the fund was still being marketed as normal so the adviser/broker was oblivious. In this case your recourse could be via the Life company who allowed the purchase of an Unregulated fund that was suspended or in trouble!

http://www.premiernewearthfund.com

So, which PPB/OIB do these investments sit in ? The Life company would have to approve a trade – where was their compliance check?

I don’t believe any adviser/broker would knowingly advise any client to put any money into a fund that has collapsed, is going to lose money or simply illegal as you suggest.

I am confident that even if this could be the case, once, the Life Company Bond provider would put a stop to it and remove their terms of business for their own protection – I could cite many examples.

I would spend a little more time checking the background to these statements and go to the Bond Provider and regulatory bodies for their input – they are ultimately responsible, not the broker.

Trust your phone will be hot today …..

Have to go out and buy a new phone!

No replies to the points raised ?

All parties involved are culpable: the broker for providing pension and investment advice – often unqualified and unregulated; the insurance company for accepting UCIS funds for retail investors; the pension trustee (where appropriate) for accepting business from any old Tom, Dick, Harry, Claudia or Adrian.

I guess you have read the relevant bodies qualifications – they are appropriately qualified and have many years experience in their chosen field – please note the definition of a Retail investor – A retail investor is an individual investor who buys and sells securities for their personal account, and not for another company or organization. Also known as an “individual investor” or “small investor”.

Clearly not the case here – I am confident the trustee in question would have had assurances from their own compliance team that the adviser/broker and fund were appropriate for the policy – the client has to sign every document to confirm each step of the way – are you claiming these people did not agree to and sign the relevant documents ?

I think the press need to see this discussion, this is very worrying. An individual, who has a pension fund, suddenly finds out that he(or she) is not the investor after all. This is not institutional money, it is the retirement fund of an individual. You are saying that the trustee has no regard for the beneficiary and the fact that the beneficiaries, as individuals, are not the investors despite this being their pension fund.

What a convenient way of getting around the fact that these are UCIS and should not be sold to retail clients. I bet if the investor were to contact these trustees, the trustees would say that it was the investor that took advice as the individual and they have no responsibility. I would put money on it!

I would be interested to see if there was a printed set of recommendations given to these investors. If such a report existed, the recommendations would no doubt be aimed at the individuals and not the trustees, leading the investors to believe the recommendations are to them as individual clients.

I think this blog is turning into an extremely important discussion.

https://www.ftadviser.com/2016/05/13/ifa-industry/companies-and-people/adviser-must-repay-client-for-recycling-investment-advice-4JWtOXAhRnTT4pEF2Y2UpJ/article.html The UK has a different view, but then that is properly regulated.

Finally, an investor may sign something on trust but this does not let the adviser off the hook when it turns out the advice was bad. There is no doubt that it was in this case, especially given the sums involved.

http://www.international-adviser.com/news/1037384/eco-fund-liquidator-replaced-blow-isle-regulator

A sad indictment of regulation in the Isle of Man.

It is not just investors in Dubai that have been affected by Premier

http://erva.es/2014/01/21/the-premier-group-isle-of-man-limited-operating-clandestinely/

I am surprised that there has not been more press comment about all of this. How many lives have been ruined?

Thousands apparently. And all because of the greed and callousness of the advisers.

I have been to every government body to try and get help and nobody is willing to help me, the ombudsman on the Isle of Man, FCA,FSA, Action Fraud UK, and FPI.

In 2011 I invested 310KGBP into a whole of life bond with FPI through one of their advisers( agents) I told him I wanted No Risk, little did I know the investments he put me into where only for sophisticated investors FPI done no check on me to see who I am (motor mechanic) FPI sold those investments to me in a country that they had no license to sell them in, also the agent that sold them to me had No work permits No license to sell financial products and No indemnity insurance. FPI allowed fraudulent funds on their platform with No due diligence (Ponzi Schemes) I wrote to FP about this and told me it’s my own fault for investing in those funds they where selling, FPI lost all of my life’s savings by iligally letting agents sell their products and I want something done about it, it’s ruined my life my families life and thousands of Expats and retirees around the world.

I’m am 54 years old and No pension to live on looking after my family abroad and unable to seek employment in the country I’m living in,if I come back to the U.K. I will be homeless living on the streets, I really need some HELP with this situation I’ve been put into by a house hold name that I trusted with confidence and they have allowed my life’s savings to be stolen from me by fraud that they aided and abetted, I have lots of evidence to back up my case.

My phone number is 0066(0)806975140

My email is garymainhood@googlemail.com

Please can someone contact me and help try to get out of this situation I’ve been put into by financial crooks.

Kind regards Gary Mainhood

I think a certain commentator on here is deliberately missing the point. This was a UCIS fund and should not have been recommended to someone who would be a retail customer. Why was so much of this portfolio put into the UCIS? I guess it must be the industry standard commission on top of the industry standard commission from the insurance firm.

Blame the life insurance company for choosing it? I have seen that excuse before with the EEA fund, “Mr Customer, it is their fault as they accepted my instruction to buy it”

These clients are not Retail Investors

Life companies do not get cooks for the funds in their bond !

We all know what he means double dipping is taking commission from the bond provider and then taking it again from the investment ………..poor pratise.

Poor Joe the Public does not see that coming……….. 8% from one and 5% from the other…….. salesman trousers this commission not the life company.

If you think life companies get nowt from the funds………. you are living in a parallel universe.

@Pension Life …….there are some good guys here…….. this is affecting the rest of us who try to do the right thing and some of us agree….. ..with (someof) what you say. Could you also talk about the positives of getting decent advice…. it would be appreciated.

This is the problem – the “chiringuitos” spoil it for the good guys. It needs to change – most advisers are not just out to “rape” the investors but to give good service. Trouble is, investors don’t know the difference – until it is too late.

Comms !

The EEA Life fund was over 6 years ago …. and completely different

And?

The fact remains that we put money into an investment that was recommended to us as “safe” by an advisor we trusted. Did we research the fund carefully and read the small print minutely before signing? No, we didn’t – I am an engineer, my wife is an ex hairdresser, makeup lady – THATS WHY WE HAD A F&CKING ADVISOR!!!! The clue is in the title FINANCIAL ADVISOR You “financial advisors” are swimming with the sharks – just wait till your car breaks down and you need it fixing – ! Our “financial advisor” has ‘retired’ and is living the life her clients can’t afford because of her “advice”.