Holborn Assets: This Toxic Dubai Firm Comes with a Health Warning

Holborn Assets can seriously damage your life savings – and indeed your health and even life.

Holborn Assets does have a few decent advisers. When I published the “Champagne Killer” blog last week, I was contacted by over a dozen advisers who asked me (courteously and respectfully) to remove their names and profile links from the blog. This I did immediately in all cases except Gerard Frew who was simply rude and abusive.

Quite a few of these advisers had had no idea they worked in such a cess pit. None of them seemed to have had any idea about Paul Reynolds and Darin Brownlee-Jones. They appeared unaware that the FCA had ruled both individuals unsuitable to be financial advisers. And they didn’t seem to know that some advisers at Holborn Assets are routinely destroying victims’ life savings – and Bob Parker simply shrugs the complaints off.

A couple of the “good guys” raised the point that if one person at Barclays had done something wrong, it did not necessarily mean that all the other staff at Barclays were rotten. A valid point, perhaps, but if there was a rotten apple at Barclays, they would get sacked – whereas Bob Parker deliberately goes out and picks rotten apples because they have no principles, no scruples, no hesitation in scamming people out of their pensions and investments. And they make Uncle Bob lots of money.

The advisers who contacted me claimed to have unblemished records (which they didn’t want to be besmirched by the likes of Reynolds and Brownlee-Jones). But the question is: if they have good records, what on earth are they doing working at Holborn Assets? If they care about their professional reputations, why not go and work for another firm which is not full of cowboys and run by a man who cares not a jot for the distress his firm causes to innocent victims.

Let’s have the drains up on how Holborn Assets really works and see how and why it is so “successful”.

HOLBORN ASSETS KUALA LUMPUR:

Holborn Assets has a team of about 50 “contact generators” based in Kuala Lumpur (where labour is cheap). They trawl social media for names and contact details.

The leads are passed to a company in the UK set up by Holborn Assets to run as a cold calling “boiler room”. They used to use a boiler room in Manchester for their cold calls, but now they’ve got their own: The Retirement Shop. The company was set up in September 2016 and has two directors: James Patrick Parker and John Cornelius Parker who was arrested and charged after extreme violence against fans and police at a football match in 2002. Presumably, they are relatives of Bob Parker – James lives in the UK and John in Dubai. In fact, when you call The Retirement Shop, James Parker answers the phone.

Holborn Assets’ cold calling boiler room, The Retirement Shop, has around 40 callers – mostly young, poorly-educated people desperate for work. Bob Parker pretends this company is in Bournemouth, but it is actually based in Sale, Cheshire. The cold callers basically bombard people throughout the UK and offshore with calls designed to book a telephone call and/or meeting appointments with Holborn Assets advisers.

Bob Parker is enthusiastic about this “lead generation” scam as the cold calls come from a UK number, so it’s less likely the potential victims are going to drop the call. Holborn Assets also uses a voice-over IT system that can change the number so that victims in – say – Saudi will see a Saudi number come up even though the call is actually coming from the UK.

Holborn Assets openly admits to doing cold calling in Saudi but in Dubai Bob Parker wants to conceal the company’s cold calling operation so he pretends the calls come from an allegedly entirely separate and independent company (The Retirement Shop) – which is, of course, controlled and run by Bob Parker himself. This is what Parker calls “warm calling”.

The way that Holborn Assets’ cold (or warm) calling operation works is that they have 16 to 20 year olds calling from The Retirement Shop to potential victims in the UK or anywhere in the world. Working from a prepared script, the caller asks the person if they’ve got a pension, and if they keep up to date with it. The caller is instructed to tell the victims the company works alongside HMRC, then to ask them loads of questions such as whether they know about legislative changes. Then the caller says he will get a “specialist” to call – so the lead is now “warmed up”. Bob Parker thinks this is “quite clever really”.

How does The Retirement Shop “package” itself? The company claims that: “We have assisted thousands of clients all over the world to transfer their frozen UK pensions and plan for their retirement. To date, we have helped successfully transfer over 500 million Pounds worth of frozen UK pensions. We are amongst the best at what we do.” But as the company was only registered in September 2016, how can it possibly have “assisted thousands” of clients since then? But the thought of Holborn Assets handling £500m worth of pension transfers is utterly blood curdling.

The Retirement Shop‘s website further claims to be “UK Qualified”, “Experts in UK Tax Law”, have “Knowledge in UK Pension Transfers” and “We also link you up with UK qualified pension specialists across the globe”. In fact, none of these claims is true – especially the last one as the only “pension specialists” they link people up with are those at Holborn Assets Dubai. And that firm is not licensed to provide advice in many jurisdictions.

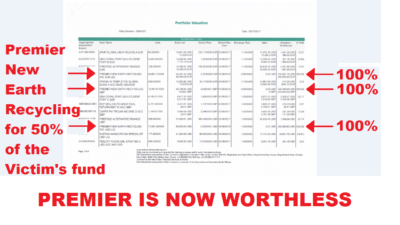

Having been cold called and “warmed up” by Holborn Assets’ boiler room scammers, what sort of investment advice is the victim likely to receive? Various victims have seen heavy losses due to negligent, unregulated, unqualified advice into entirely inappropriate, high-risk, illiquid assets. This includes one victim’s $600k life savings – half of which were invested in New Earth Recycling (which, of course, was paying the best investment introduction commissions).

So why would decent, ethical, conscientious advisers choose to stay at Holborn Assets? Do they really want all this toxic, unethical practice to rub off on them? Do they want their leads to come from Bob Parker’s boiler room scammers in Kuala Lumpur and “Bournemouth”?

Lastly, why don’t they all get together and tie Bob Parker to a chair then slap him with a wet fish and a copy of the Bible until he agrees to pay proper compensation to the Holborn Assets victims?

This Bob Parker sounds like a real piece of work. Noting his remarks in UAE newspaper The National regarding “financial cowboys”, and in view of what we all now know about Holborn Assets, I wonder whether he would care to re-clarify his position on the topic?

Whilst much of the above may be roughly accurate, one does wonder why this company in particular is so firmly in your crosshairs? Clearly you have done some research so you are no doubt aware that the above criticisms could equally be levelled at many firms in the industry, not least of which the biggest fish of all deVere, yet you don’t seem to mention them. The articles against Holborn are written with such vitriol one has to wonder if there is a personal agenda here….

No personal agenda – but I have watched the damage done to Glynis Broadfoot when a huge chunk of her pension was destroyed by Holborn Assets. But I watched in horror the utter disdain and disinterest on the part of Bob Parker who simply wrote “case closed” and walked away. I even met his PA in his office and she promised someone would get back to me, but no-one did. I accept mistakes can be made – but an honourable firm would put them right and compensate victims for distress caused.

I am sure others in Dubai will appear on here. The fact that your comment was allowed to stay, and responded to, suggests there is possibly no agenda as you suggest.

I have commented on supposed independent forums and the comments do not get past the “independent” moderators as there is an agenda on many sites. Independent Adviser online magazine is a prime case in point. Better not upset the sponsors.

Question to Ms Brookes “Do you moderate all comments and allow them to stay. Or, if there is a reason you cannot allow the comment will you make the reason known? After all, you want transparency”

Hi Mark, yes I allow all comments to stay. I would only delete a comment if it was abusive. I don’t have sponsors and don’t do advertising so there is nobody to upset. I do get emails and phone calls asking me to delete individuals’ names from blogs, and provided these are courteous I always comply. There has only been one exception. I also get lots of solicitors letters – such as a recent one from Slater and Gordon on the Blackmore Global investment scam. But that’s ok – it keeps them off the streets. BTW, there is no “e” in Brooks 🙂

The office is in bournemouth, used to be a boiler room caller there myself.

So who do we go to? Holborn has been pursuing me for over 2 years to transfer my pensions? surely if it was a scam they would have given up by now?

My accountant, says I should not look at them and he wants me to head to a big firm like Irish Life.

I just don’t know where to go or what to do!!

Irish Life is one of the biggest scammers around. They use life insurance bonds to hold single-premium investments; pay huge commissions to the scammers which they then claw back from the victims and then allow the scammers to fill the bonds with toxic, expensive, illiquid, risky crap. They will accept business from any old unregulated so-called advisers (called chiringuitos here in Spain). And then accept dealing instructions for structured notes which are supposed to be only for professional investors only – and when the structured notes fail and the victims lose 10, 20, 30, 40, 50, 60, 70, 80 and even 90% of their original fund, Irish Life will just shrug their shoulders and say it was not their fault. It was the victim’s fault for appointing the adviser in the first place.