Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders:

The life offices take business from any old known scammers – firms without proper licenses and with a known history of defrauding the public

The life offices will offer toxic, illiquid, risky funds – including UCIS funds – such as LM and Mansion on their platform (without doing any proper due diligence as to how quickly these funds can eradicate the life offices’ victims’ life savings)

The life offices will accept investment instructions from unqualified scammers who work for firms with no investment license – and, in some cases, with no insurance license either

The life offices will accept dealing instructions – often with fraudulently-copied or forged signatures – on dealing instructions for toxic assets such as professional-investor-only structured notes

A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

Mr. S’ pension fund was then placed in a “life bond” with Investors Trust in the Cayman Islands. This was an entirely gratuitous transaction, as he had absolutely no need of such a bond – known to be a spurious life assurance policy used for what is called a “single premium” insurance contract. These bonds are illegal in Spain, since the Spanish Supreme Court has ruled that they are being used to hold investments in contravention of the nature of what insurance is supposed to be (i.e. risk for the insurer).

The entire fund – which represented Mr. S’ retirement savings – was then invested in two toxic UCIS funds (illegal to be promoted to UK-resident, retail investors) called Symphony and Blackmore Global. Investors Trust negligently accepted these investments from Square Mile – in the full knowledge that this was absolutely against the interests of the policyholder and that the “advisory” firm had no investment license.

After a protracted battle, waged with great tenacity and dogged determination, Mr S did indeed get back a large proportion of his fund. But he still suffered what can only be described as a harrowing experience which resulted in a total loss of a significant chunk of his pension to the scammers (who will have profited handsomely from scamming him in the first place).

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer Douglas Davies of Lowell Davies LLP.

But what of the Cayman Islands-based life office – Investors Trust? Did they try to help Mr. S recover his serious losses? Did they offer him compensation for the significant distress he suffered at the hands of the scammers at Square Mile? Did they publish a statement demonstrating recognition of the damage done to victims’ life savings by investing in toxic crap like Blackmore Global on the instructions of scammers like David Vilka?

The answer, of course, is a resounding “no”. Investors Trust could have done so much to reform these illegal practices and expose the likes of scammer David Vilka who scammed not only Mr. S out of a big part of his pension, but also scammed hundreds of victims into the Hong Kong QROPS scam (many of which got invested in Blackmore Global).

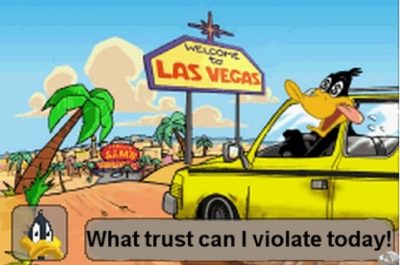

Instead of showing any contrition or regret for facilitating financial crime, an idiot at Investors Trust called Lindsay Paris emailed me threatening to sue me for using a picture of David Vilka and John Ferguson posing as vulgar spivs at Las Vegas. This revolting photograph is, apparently, the property of Investors Trust:

“This is my second attempt to reach you regarding the copyright infringement on your website. Please have the image removed immediately or we will have no other choice but to seek legal action.

This is not the first time you have fraudulently misused private images and copyrights without authorization. You are imposing on our ownership rights and we would appreciate it if you would refrain from any future use of Investors Trust-owned materials. It is a serious violation which we will continue to pursue.

Lindsay Paris, Media and Communications Manager, Investors Trust Administration

lparis@investors-trust.com”

So, no apology for destroying victims’ life savings; no apology for taking business from a firm which was not regulated to give investment advice; no apology for investing a victim’s pension in a toxic UCIS fund run by known scammer Philip Nunn….just a complaint about a violation of their ownership rights of a picture of the scammers bearing the Investors Trust logo.

It is reported that Old Mutual International has put aside £69 million to pay compensation for their victims’ losses. May I suggest that Investors Trust should do the same thing – and then I will happily take down the vile picture of Vilka and Ferguson. But until then, it stays up. And if you want to sue me – go ahead: make my day.

I have read the report about what happened to the scammers at STM Fidecs in the wake of the Gibraltar FSC’s investigation and Deloitte’s so-called “expert report”.

Frankly, I am stunned. I have members who are victims of the Trafalgar Multi-Asset Fund and STM Fidecs and they are, understandably, stunned as well. I have met the people at the Gibraltar FSC and they had seemed decent guys |(but WTF do I know?!). Maybe they’ve all left, because the people I met appeared enthusiastic and conscientious. But perhaps they’ve been replaced by a bunch of malfunctioning robots, or ex-scammers or – much worse – ex STM Fidecs employees.

Serious Fraud Office investigating XXXX XXXX

The bottom line is that STM Fidecs scammed hundreds of victims out of their pensions. STM Fidecs took business from unlicensed scammer XXXX XXXX of Global Partners Limited (only had an insurance license with Marcus Groombridge’s firm Joseph Oliver) and then invested 100% of the victims’ funds into an illegal UCIS fund – run by XXXX XXXX (now under investigation by the Serious Fraud Office – although I really don’t know what they are playing at because XXXX still isn’t behind bars).

The rest is history. The Trafalgar Multi-Asset Fund is being wound up, and after paying the liquidation costs to Stephen Doran, of Doran + Minehane, there is unlikely to be much – if anything – left. Deloittes spent weeks supposedly investigating STM Fidecs’ books. I reckon the chumps at Deloittes probably spent most of that time on the golf course with Alan Kentish having a chuckle and a side bet about how feeble the Gibraltar FSC was likely to be. And, of course, they were right.

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.

Neither STM Fidecs nor the Gibraltar FSC has said a word about redress for the Trafalgar Multi-Asset Fund victims.

The only words spoken are that the Gibraltar Regulator has told STM Fidecs to “improve its compliance”. Improve?? How can you improve something that doesn’t even exist at all? We know that one victim (of scammers Holborn Assets) was bullied by STM Fidecs for trying to improve compliance and harassed for trying to stop obviously non-compliant transactions when she was employed by them. She was subsequently “paid off” and threatened with a gagging order.

“STM is now expected to engage with the Gibraltar FSC in order to discuss the Recommendations of the report, and agree a plan of action to implement them.” (according to the report by FT Adviser). Recommendations? Where are the sanctions? Where are the appropriate fines? Where are the bans to stop Alan Kentish and David Easton from ever practising in financial services again? Where is the cancellation of STM Fidecs‘ license?

With this in mind, here are some idiots’ guides as to how to become a pension trustee, and how to become a regulator. Both are equally easypeasylemonsqueasy – any old idiot or scammer could do it.

HOW TO BE A PENSION TRUSTEE IN EASY STEPS

Think of a catchy name: obviously inspired by the acronym STD, Alan Kentish came up with the name STM. FIDEC is an acronym for “Fighting Infectious Diseases in Emerging Countries”. Here’s my suggestion: Trussed4U – wadya fink?

Think of a jurisdiction with the most ineffective, pathetic and corrupt regulation – such as Gibraltar

Find an unlicensed scammer like XXXX XXXX who will transfer lots of UK-resident victims into an offshore QROPS and invest their life savings in whatever crap will pay him the highest commissions

Sit back and rake in the profits

Forget fiduciary obligations or anything with the word “trust” in it – only concentrate on the word “trussed“

Play golf with the regulator

HOW TO BE A REGULATOR

Join a golf club (that isn’t too picky about who it lets in)

Give licenses to as many scammers as possible – the more the merrier

Buy lots of blindfolds (to help turn a blind eye to scams and scammers)

Play lots of golf with the scammers and bent pension trustees who facilitate financial crime

When an advisory firm or a trustee firm gets caught scamming, slap a few people on the wrist with a wet fish

Write meaningless reports about robust compliance

HOW TO BE A SCAMMER

Find yourself a bent jurisdiction (such as Gibraltar)

Find a bent trustee who will accept business from any old unlicensed scammer (such as STD FIDEC)

Find a bent “umbrella” fund which will facilitate financial crime – such as Richard Reinert’s Nascent Fund

Find a Ponzi scheme such as Dolphin Trust which will issue “loan notes” at 10% interest per annum (and up to 25% in introduction commission)

Transfer hundreds of UK residents to a Gibraltar QROPS scam

Get the trustee to agree to invest 100% of 100% of the victims’ retirement savings in … your own fund!

See how easy it is to be either a trustee, a regulator or a scammer? But, equally, remember how easy it is to be a victim!

Quite frankly, Gibraltar should be towed out to sea and sunk. It is a disgrace to the British nation. Just give it back to the Spanish and let them clean it up – they would soon kick the likes of STM Fidecs out and stop any further scams and scammers from operating on Spanish soil. Soil being the operating word.

Rather than going on about how utterly disgusted I am with the Gibraltar regulator, I will leave it to the eloquent words of one of the STM Fidecs/Trafalgar Multi-Asset victims to put this sickening disgrace into perspective.

Firstly, do Gibraltar FSC actually realise over 1,000 individuals and their families are affected by the Trafalgar fiasco, who will potentially all suffer negatively in many different ways during their retirement years? On a personal level, I should haveknown better but was caught out by cleverness at a weak moment in my life, but many others I have spoken to had no understanding at all of financial affairs and put all of their trust in the hands of STM and all connected parties due to their apparent convincing knowledge and lies – shocking!!!!!

Due to my own personal research, I know of several other financial institutions who were offered and were involved in discussions regarding Trafalgar. But due to having correct procedures in place (unlike STM), they clearly ”smelled a rat”, and were far more ”ROBUST” in their approach. The only rat STM smelled was some form of hopeful ”Magic Money Tree” with no concern for its clients’ wellbeing – apart from its own pound note signs.

As you already know I have previously discussed this matter with my local MP and with your permission would like to highlight again the manner in which Gibraltar FSC have dealt with and inadequately reacted to STM’s performance. STM’s website highlights their glowing history and expertise, but at no point mentions their clearly poor basic audit and compliance mechanisms.

Hopefully, at some point in the future all the evil parties – including STM – in this matter are dragged through the courts, eventually embarrassed and humiliated by the press, and made to pay both financially and personally for their hideous crimes – I can only dream.

Still angry and in despair.

STM Fidecs/Trafalgar Multi Asset Fund Victim

That victim may well have lost her entire life savings thanks to XXXX XXXX and STM Fidecs. I am sickened and disgusted with our own onshore regulator’s pathetic failings: the FCA. But, quite frankly, the Gibraltar FSC makes the FCA look like Superman with TWO pairs of pants on outside their tights!

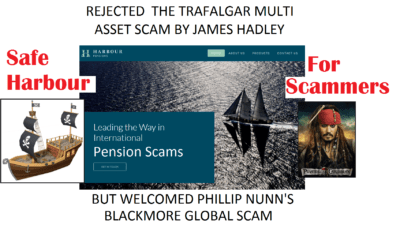

Interestingly, Justin Caffrey – who used to run Harbour Pensions in Malta – told me a year or so ago that he had been approached by XXXX XXXX who wanted to flog his toxic Trafalgar Multi Asset crap.

Caffrey claimed to have sent XXXX packing with a flea in his ear because he twigged straight away that XXXX was a no-good spiv. However, he had no such ethics when he invested victims’ pensions in Phillip Nunn’s Blackmore Global crap.

But now STD FIDEC has bought Harbour and Caffrey has been given the heave-ho. You couldn’t make it up!

Gibraltar’s most wanted man – Alan Kentish, CEO of STM Fidecs

STM Fidecs needed a safe Harbour. And now they’ve got one – but is it really safe?

LETTER TO ALAN KENTISH – CEO OF STM FIDECS:

Dear Al, hope you are well. I’m not anticipating a response to this because I know how difficult it must be to type emails when you’re wearing handcuffs. However, I thought I would drop you a line because I am genuinely worried about you.

STM’s harbour for investment scams

You see, I heard you’d bought Harbour Pensions for £1 million – a book of 1,600 members. But how many of these members will want to stay once they find out they are now in the hands of STM? If any of them have got any sense they will transfer out to a decent QROPS trustee who can be trusted to look after their pensions. STM Fidecs allowed hundreds of victims – advised by a known scammer running an unlicensed firm (XXXX XXXX) of the Pensions Reporter/Global Partners Limited) – to be 100% invested in XXXX’s own fund, Trafalgar Multi Asset (now suspended, under investigation by the SFO and being wound up).

The Trafalgar Multi Asset Fund was a sub-fund of the Nascent Platform – one of many operated by Custom House Global offering scammers a cost-effective place to waste pension pots. This provided a low-cost solution to wannabe fund managers to try their hand at playing musical money with victims’ life savings.

What surprises me, is that having proved that STM Fidecs is an incompetent firm run by inept – or perhaps even crooked – people, you would be splashing money around acquiring more victims and more toxic assets. Instead, you should have been paying compensation to your existing victims who may well have lost a substantial proportion of their retirement savings due to STM Fidecs’ own failings.

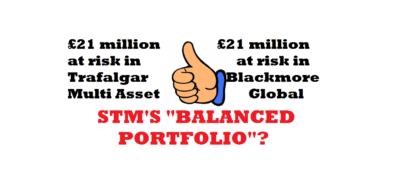

Having acquired Harbour, you have now added the toxic, illiquid, high-risk, un-audited Blackmore Global fund to your portfolio of worthless crap. Your balance sheet must need disinfectant and a good old scrub.

STM’s balanced portfolio of toxic investment scams – Trafalgar Multi Asset and Blackmore Global

Furthermore, you will now be in league with not one but TWO lots of scammers who are under investigation by the Serious Fraud Office. XXXX XXXX (Trafalgar Multi Asset) and Nunn McCreesh (Blackmore Global) were both behind the Capita Oak and Henley Retirement Benefit pension scams – all 100% invested in Store First store pods.

Seriously, Al, you should think about cleaning up your act – not making it dirtier and murkier. Hope those handcuffs don’t chafe too much.

Gambling is a very strictly controlled industry – and rightly so. Every individual jurisdiction has its own gambling or casino licenses which are usually very expensive and onerous to obtain and keep. Where large amounts of cash change hands every minute, it is obviously important to impose strict conditions and ensure that regulations are complied with.

The city of Las Vegas sprang up in the middle of a desert in 1905 in the hottest part of the world and has since flourished into a sparkling and magnificent centre for world-class gambling.

In the words of Rudyard Kipling: “If you can make one heap of all your winnings, and risk it on one turn of pitch-and-toss, and lose, and start again at your beginnings, and never breathe a word about your loss…..you’ll be a man my son!”

Kipling’s advice is clearly aimed at someone young; someone who has years ahead of him to get lucky; recoup his losses; start again; do a phoenix; learn from his mistakes and do better next time. But with pensions, a life-time of savings can be wiped out so easily on “one turn of pitch-and-toss” by entrusting an unlicensed adviser.

Here in Spain, the investment regulator – the CNMV – refers to unlicensed pensions and investments advisers as “chiringuitos” (which translates as “bar flies”). The CNMV helpfully publishes a well-written warning booklet to alert the public to the nefarious tactics of these scoundrels – copied below for the information of the gentle reader. However, in Britain we tend to be rather more direct and call them scammers. And Lesley Titcomb of the Pensions Regulator has come right out and said it: “scammers are criminals”.

So, make sure you only use an advisory firm which is licensed to provide pension and investment advice. And avoid the chiringuitos, scammers and criminals. I have no idea who the jolly pair of gamblers are in the photo on this blog, but I am sure no informed person would entrust them with a pension and I reckon Kipling would have had a thing or two to say about them.

Away from the fun fun fun of Vegas, these two amiable-looking scallywags could probably scrub up and look like respectable independent financial advisers with a business-like suit and a leather portfolio full of impressive documentation about funds with imaginative names such as “Symphony” and “Blackmore Global”. But if they did so without a license, they would be criminals.

SPANISH REGULATOR’S (CNMV) GUIDE (translated)

FINANCIAL CHIRINGUITOS (“IFA” FLY BOYS/SCAMMERS)

“CHIRINGUITOS” means entities offering and providing pensions/investment and advisory services without being authorized to do so. They are dangerous because in most cases the apparent provision of such services is just a cover for fooling victims into believing they are making a highly profitable investment. It is important to understand that high yields offered are often too good to be true: the bait to con ill-informed (naïve) investors to hand over their savings or pensions. When exposed, the “CHIRINGUITOS” simply disappear or change their names. They are simply swindlers.

Companies authorized to provide investment services (brokers, portfolio managers, IFAs, banks etc.) are subject to the rules governing the securities markets and strict controls by the supervisory bodies (CNMV and BanK of Spain). Only CNMV-registered companies are authorized to provide pension/investment services, after demonstrating compliance with specific legal requirements and standards.

CHIRINGUITOS are not attached to the Investment Guarantee Fund, so that investors are not protected in the event of insolvency of the entity (authorized entities contribute to these protection funds through compulsory subscriptions).

There is no particular type of victim because often scams are very elaborate. Victims can be small businesses, individuals or professionals who fall for credible-sounding false promises of quick wealth and easy gains.

In short, to trust a CHIRINGUITO is a sure way to lose capital, with no investor protection under the laws. How CHIRINGUITOS work

The channels used by scammers and boiler rooms to contact potential victims are no different from those that can be used legally by legitimate entities i.e. telephone, letters, e-mail, web pages etc. The difference lies in the way the scammers use these channels, the type of messages they convey and the general approach to achieving their goals.

The CHIRINGUITOS use databases (often obtained fraudulently) of people who, for example, have purchased a particular financial product, publication – or on occasion answered a survey about their tastes, interests and financial situation. Phone calls

Cold calling is one of the CHIRINGUITOS’ favourite contact methods. It allows them to directly exercise psychological pressure techniques. Cold calling is by definition unexpected but is legal, and in fact authorized entities often use it as part of their promotional campaigns. However, in the case of authorized entities, it is normal practice to call existing customers, so people know their data has been obtained legitimately. If the answer to what is being offered is “no” this is accepted politely. By contrast, the CHIRINGUITOS do not usually settle for a NO.

Mail

High-quality leaflets which are sophisticated, inviting and promising. These often request the recipients to contact them by filling out a form, calling by phone or by visiting their website. Internet, e-mail

The great success of the Internet as a direct marketing tool allows advertisers to access a wide mass of recipients more cheaply than traditional media (phone, mail). This fact, coupled with the possibility of anonymity, has led to abuse of the medium, such as spam or indiscriminate emailing of unsolicited products bordering on illegality. Recipient lists are often obtained unlawfully, in breach of data protection rules. Also, the address of origin of the messages are usually false, and also the subject headings are deliberately misleading. Spanish law decrees that commercial communications should be identified as such and prohibits sending emails unless they have previously been requested or expressly authorized by the recipient. No serious company would ever spam the public, as that would be invading consumer privacy.

When it comes to financial products and services, we must be very cautious about offers and information received, even if they have been requested or consented to. Financial fraud on the Internet can be carried out by more sophisticated means. Spam is just one of the possible mechanisms, because the Internet offers various tools to disseminate potentially fraudulent or questionable deals: boards, newsgroups, chats, or even sophisticated web pages.

Phishing

Another danger is “phishing”: emails that appear to come from legitimate financial institutions, which request personal passwords. These messages often lead to a website that imitates an authentic entity (although it may have spelling mistakes), which fools people into entering their personal data or passwords.

Pharming

Even more sophisticated is “pharming”: people who visit fraudulently-cloned websites can have their personal, confidential data collected by criminals. Never surrender personal or confidential business information to unknown persons. If a request for personal data appears legitimate, use an established phone number to double check. Also, don’t access websites via links, but type in the full URL and, if possible, install antiphishing and antipharming tools. Adverts

CHIRINGUITOS also advertise in newspapers, magazines or other media (such as television teletext) to offer opportunities which are much more attractive than traditional investments and promising to provide attractive opportunities (which, of course, are not so in reality).

Personal referrals

It is common for people to make their investment decisions based on recommendations from acquaintances or relatives whom they trust. Knowing this, sometimes the CHIRINGUITOS pay great benefits to the first customers, using their own money or from other investors; this is what is called a Ponzi scheme. In fact, those investors who unwittingly act as bait are only going to get limited performance at first and successive investments begin to generate losses. Then, the company will not respond to requests for repayment of capital and finally disappear with all the money invested.

Personalized investment recommendations should always be made by a professional entity authorized to do so, because what is good for one investor may not be for another, depending on their different personal and financial circumstances. Persuasion techniques

The list of boiler-room persuasion techniques cannot be exhaustive, since the arguments and methods are increasingly sophisticated. Therefore it is important to stay alert to any financial offer that is not from a known, registered party. Accurate predictions

A simple but very effective technique – using a large number of calls to impress potential victims with their knowledge of financial markets – half of which confidently predict the rise of a certain investment value and the other half predicting decrease of the same value. In the following days this exercise is repeated several time. Those targets who were given a series of successful predictions are contacted again. Now convinced of the infallibility of a company that has hit all its forecasts for several consecutive days, these people are willing to surrender their savings to the CHIRINGUITOS. Appearance of respectability and success

CHIRINGUITOS know it is essential to look respectable and seem like financial market experts. So they dress smartly and elegantly and rent luxury offices. Sometimes it is difficult to get an appointment to meet them because they want to give the impression of being busy and in high demand. Incomprehensible explanations and use of technical jargon

CHIRINGUITOS promoting fraudulent investments talk with confidence and mastery of technicalities that make them look like experts on the subject. In fact, the aim is that the potential victim does not understand anything and chooses to trust those who seem to be experts who know what they are talking about. Offering large profits with little risk

CHIRINGUITOS promise much higher returns than can be obtained from a conventional investment with minimal risk. A basic principle that all investors should bear in mind is that profitability and risk go together inseparably. The possibility of obtaining high yields always involves taking high risks. Be wary of any offer that ensures high returns without risk. Insistence on an immediate decision

Urgency is a major factor, not only because they want to get their hands on your money asap and with the least possible effort, but because they know that if the investor has time to think properly about the offer, or seeks professional and reliable advice, he will probably reject the offer. So, CHIRINGUITOS use tricks aimed at achieving an immediate decision to try to convince the victim that they are offering a unique opportunity that will expire soon. Investors should be aware that this is not true: there is always time to assess the characteristics of a financial offer and to make sure it is suitable. Psychological pressure

The conversation, either by phone or by any other means, usually begins in a cordial fashion, but if the targeted victim shows some potential resistance the scammer can become more aggressive. This constitutes a fundamental difference between the CHIRINGUITOS and the authorized entities, who always respect a prospect’s right to not be interested.

Although psychological pressure can take many forms, here are some common tricks:

Not taking no for an answer

Being repeatedly insistent

Becoming increasingly aggressive

Questioning the intelligence or ability of the investor to make a decision

Conveying the idea they are doing the victim a big favor by offering exceptional gains

Making it clear it would be absurd to question the promises made

Using warnings such as: “you’ll regret it if you don’t go ahead” or “you’ll never get rich if you ignore my advice”

When to be suspicious of a financial offer

Most of the techniques used by CHIRINGUITOS would not be used by authorized firms, since they are subject to strict rules of conduct. Authorized firms are required to keep customers properly informed and to provide information to investors fairly and clearly. In particular, they must provide information about their services and financial instruments, so that the client knows the nature and risks of the investment service that it is going to provide and the characteristics and risks of financial instruments offered.

It is therefore important to understand the difference between people or entities who are authorized to provide investment services and those who only intend to carry out a scam. When an authorized firm sells a product, the customer must request information on their knowledge and experience in this product, in order to assess for himself whether it is suitable for him. This is called a suitability test.

When a broker is going to provide investment advice or manage an investment portfolio, in addition to asking about the client’s investment knowledge and experience, he should request additional information such as the financial situation and investment objectives of the client (risk profile, time-frame etc.) – as proper financial advice is always personalized.

The boiler room scammers’ only aim is to attract money from their victims, so they do not care about their clients’ expertise in investments and financial circumstances – all they need to know is that they are willing to invest. The contact must have been requested by the prospect

Authorised entities have to work with personal data in a legally-compliant manner, and the client must have given them permission to make commercial offers. But if an entity of which we have never heard contacted us to offer an investment, you have to take extra precautions because this is probably a scam. Authorized entities never pressurise customers

Any investment should be approached with sufficient knowledge of the characteristics and risks of the product. It is important to do thorough research before committing. The investor needs time to decide and get answers to all their questions. However, scammers pressure the victim to get an immediate yes, without giving them a chance to reflect. How to protect yourself against a possible CHIRINGUITO

Promises of exceptional returns without risk should make us suspicious immediately. Never trust an unknown entity until they have been able to verify that they are properly authorized to provide investment services. The investor has available the following protection mechanisms which should always be used before handing over capital:

Request information from the supervisory body, in this case the CNMV

Identify any peculiarities about the investment proposal

Demand concrete answers and make sure they are fully understood

Ask for information from the CNMV

The Investor Assistance Office of the CNMV is at your disposal to inform you whether entities are authorised to provide investment services or not. If you have been advised to deal with a company that has been referred/recommended, you should call the CNMV for assurance that it is an entity which is authorized, registered and supervised. Public records are also available through the website of the CNMV (www.cnmv.es). Investors can also visit the website of the International Organization of Securities Commissions IOSCO, (www.iosco.org) where there are warnings and advice available.

The CNMV regularly issues warnings about entities which are suspected of providing investment services without authorization. These warnings may come from the CNMV (when it is aware of the existence of possible CHIRINGUITOS through inquiries or complaints from investors) or which have been supplied by a foreign regulator (bear in mind that CHIRINGUITOS may operate their fraudulent activities in more than one country).

To make it easier for investors to identify entities operating without authorization, the website of the CNMV provides a search engine that can locate them quickly and easily. Entities that have not been placed on the warning list may not yet have been detected by the supervisory bodies. It is important to remember that although most of the victims of fraud contact the CNMV after losing their money, it is always preferable and much less expensive to conduct this consultation in advance, i.e. before handing any funds over.

Identify the characteristics of the proposal

Sometimes, the activities of the CHIRINGUITOS are masked under the guise of consulting services, in which in the client is charged a high commission on their investment (which also often adds to the total loss of the capital). However, all entities making personalized investment advice must be registered on a public registry, so that potential victims can see whether or not a firm or person is authorized to provide this service.

Generally, CHIRINGUITOS require funds to be transferred to a current account (sometimes abroad) on behalf of a non-Spanish company. In general, any offshore entities are not authorised or regulated. The investments tend to be complex financial products in unknown foreign markets.

There are often entities or websites that offer investors the opportunity to invest in foreign exchange derivative products (CFD, futures, rolling spot contracts etc.). The forex market (foreign exchange) is very complex, so any access to this should only be done by authorized entities.

Scammers are often reluctant to provide updated information or respond to questions from the investor, although they promise that they are offering a relationship based on mutual trust. But remember that trust is something that must be earned, the more so when it comes to giving your money to organizations or persons who have failed to establish their legality, professional integrity or solvency.

Insist that any adviser provides clear answers to questions. The investor not only has the right but also the duty to know in advance all relevant aspects of the proposed investment. One of the main differences between authorized financial institutions and CHIRINGUITOS is that the former invite investors to ask questions and then provide all necessary answers and information, while the scammers try to make their targets feel ignorant, and to trust them blindly.

Below are some questions to ask the advisers to see whether they are CHIRINGUITOS. In fact, many of these questions, particularly those relating to the characteristics and risks of the investment should also be made when dealing with authorized entities. The difference is that scammers will be unwilling to provide clear answers:

How did you get my name and contact details?

Why are you making contact with me?

Is your firm registered with the CNMV and the Bank of Spain?

Is your firm supervised by any public authority?

Are you a member of any investment protection/guarantee scheme?

How long have you been with the firm?

What is your professional experience?

Is there any financial entity which can give you or your firm a reference?

Does the investment you are proposing match my objectives and is it suitable for me?

What are the risks of this investment? How much could I lose and under what circumstances?

How would I profit from this investment?

What has to happen for the value of this investment to increase? (i.e. interest rate or stock market rises?)

For how long do I need to keep the investment?

What is the liquidity of the investment i.e. how and under what conditions can I get my capital back if I need it?

What commissions are payable? How are they calculated? Can I have a copy of the fees/rates?

Can I have a copy of the documents/contracts that I have to sign (to read carefully before signing them)?

Is there any official document regarding the investment at the CNMV regulator? Can I see it?

Can you give me a written detailed explanation of the investment to read/digest carefully and a second opinion?

Can we discuss the proposed investment with my lawyer or with a trusted financial expert?

If anything goes wrong with my investment, what avenues of redress or compensation do I have?

Just asking these questions is not enough. CHIRINGUITOS are expert at being persuasive and evading answering questions with plausible excuses. This is why it is essential to check out any person, firm or investment with the CNMV before handing over any funds.

What a wag that Michael Howard was on Saturday. But his timing is brilliant as we do have one little “mess” which needs sorting out urgently, and a bit of a hole – about the size of Howard’s mouth – in regulation and financial crime prevention in Gibraltar: the STM Fidecs/Trafalgar Multi-Asset Fund pension scam.

Known for many years as a haven for crooks, tax evaders, swindlers, fraudsters, money launderers, drug traffickers and assorted rascally turds, Gibraltar is also home to STM Fidecs. Allegedly a pension “trustee” firm. So, this blog is addressed directly and unashamedly to STM Fidec’s Alan Kentish and David Easton.

“Alan and David, the word “trustee” has got the “trust” bit in it for a reason. Members are supposed to be able to trust a pension trustee to ensure that investors are not advised by a two-bit, unregulated, serial scammer. And further, that they are not advised by a two-bit, unregulated, serial scammer who is also the investment manager of the very UCIS scam he is promoting to UK residents who should never have been put in a QROPS in the first place. And further still, that the investors’ pensions are not 100% invested in that high-risk, toxic rubbish which is illegal to be promoted to UK residents.

Talking of words, I was curious as to what “Fidecs” actually means and when I Googled it, I got “fighting infectious diseases in emerging countries”. Well, that’s about right if you ask me. And who asked me? Victims of the Trafalgar Multi-Asset Fraud (£21 million suspended and arguably worthless). And a dying elderly man to whom you caused immense anguish by refusing to release a portion of his pension so he could have life-saving cancer treatment – and whom you gagged when eventually you did relent (although he had told me all about before you gagged him).

And talking of gagging, what about the woman you gagged because she worked for you and objected strongly to the amount of business you were signing off which was non-compliant and would put investors at risk? She happened to know what she was talking about because she had been a victim of the scammers at Holborn Assets in Dubai who came close to losing her all of her pension – so she knew her stuff. So you gagged her too – but not before she had told me every detail – as she is a member of the Pension Life Group Action.

So, Al and Dave, I am sure it goes without saying that you won’t be gagging me, and a detailed report is being prepared for Messrs. Coles, Crossman, Tricker, Ashton, Barrass and Garner. It would be nice if you came forward, admitted your negligence like men and put your professional indemnity insurers on notice without squirming and slithering around.

Let’s see if you are men; whether you can put the “trust” back in “trustee”, take the turd out of Saturday and kick the rot out of Gibraltar. Then Lord Howard can take his foot out of his mouth and Gib might have a chance of rescuing its tarnished imagine as the harbourer of financial crime.”

Seriously–is this yet another wind up? STM want to be voted as “National Public Champion”?

All of STM’s allegedly world-leading people will have known that it was illegal to promote a UCIS to retail UK residents. Unless STM’s claims about their excellent pensions team are just a wind up?

After International Investor’s expose of the wind up of the failed £21 millionTrafalgar Multi-Asset fund:

not many of the hundreds of victims who may stand to lose part or all of their pensions will be voting for STM. International Investment’s Helen Burggraf reported that the Trafalgar fund’s investors were advised of the wind up on 13th January 2017 by Richard Reinert of the Nascent Fund (an umbrella fund containing the Trafalgar fund).

STM, who failed to provide details about how the wind-up is likely to work, have apparently whined that they had been “unfairly singled out” as a well-known trustee because they had kept their victims “informed about the fund’s problems”

STM, whose stake in Trafalgar accounted for 75% of the total fund value, failed to answer urgent questions about their role in the victims’ impending losses in the fund which, according to International Investment was “managed by Victory Asset Management, run by two of the people involved in the Capita Oak pension scam.”

.

STM claim to have over 50 “dedicated and highly-skilled” people in their pensions team and that their level of expertise has made them world leaders in the field of QROPS. Perhaps one of these wonderful people can explain why hundreds of UK-domiciled investors were transferred into a Gibraltar QROPS on the advice of an unregulated adviser who was also the Trafalgar fund manager into which 100% of these pensions were invested.

STM will surely have no trouble providing an explanation as to why victims’ pensions were 100% invested into one UCIS which was 100% invested in loans to a German property developer.

All of STM’s allegedly world-leading people will have known that it was illegal to promote a UCIS to retail UK residents. Unless STM’s claims about their excellent pensions team are just a wind up?

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders:

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders: A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer Douglas Davies of Lowell Davies LLP.

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer Douglas Davies of Lowell Davies LLP.

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.