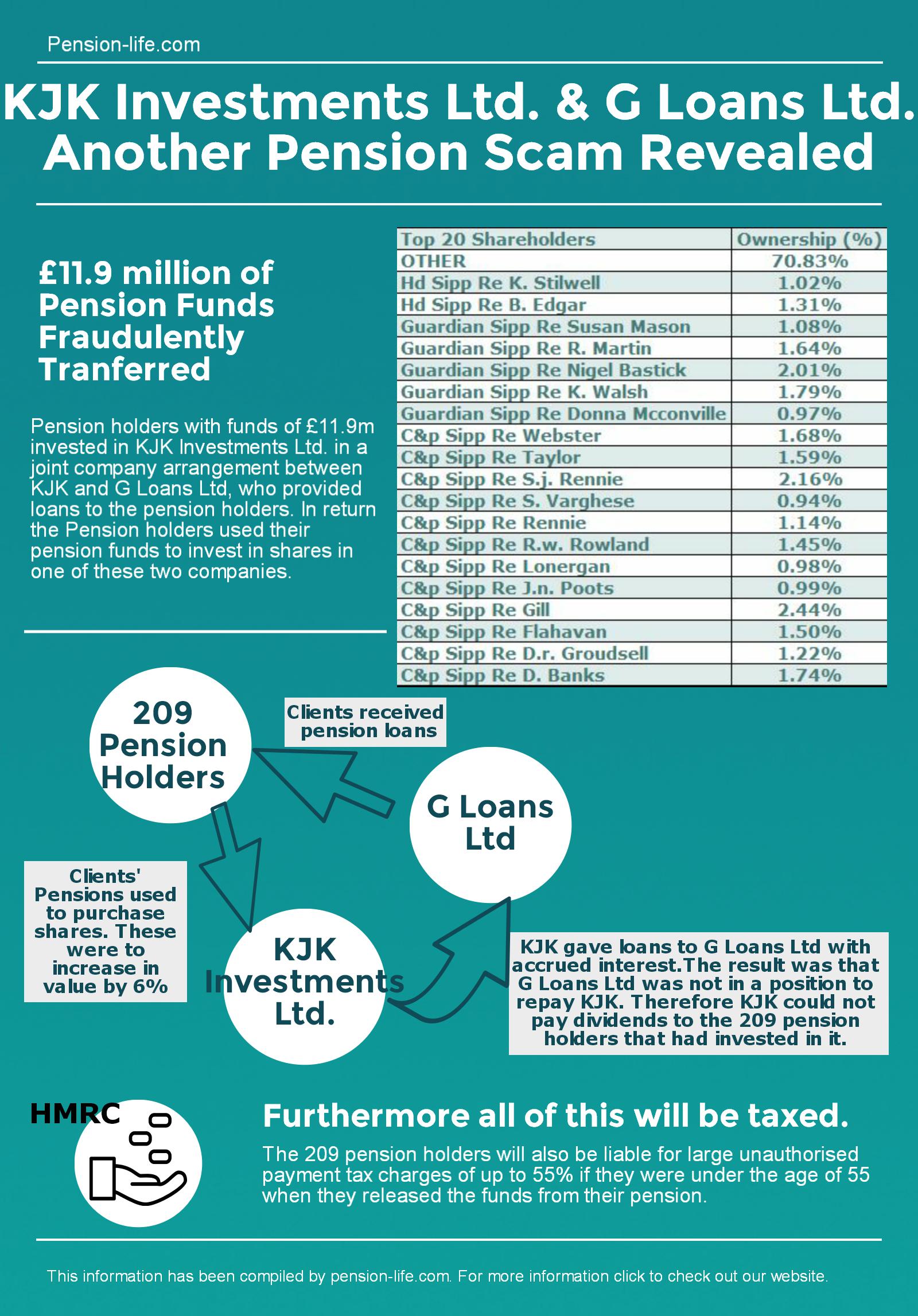

Pension scams have been a very clear and present danger since large-scale pension liberation fraud was unleashed on British pension holders on A day. Victims lose a life time of savings and face onerous unauthorised payment tax charges of up to 55% by HMRC. The latest one to come to our attention is a pension liberation scam involving two companies: KJK Investments and G Loans.

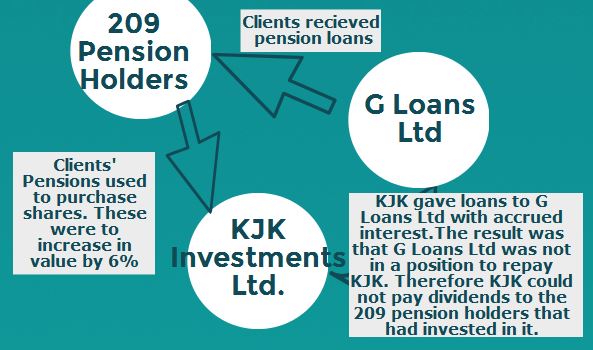

G Loans received loans from KJK Investments Ltd. The interest on the loans was accrued so G loans were never able to pay back the loans. The 209 pension holders were awarded loans from G Loans while their pension funds were used to purchase shares in KJK Investments. These shares were purportedly estimated to grow at 6%.

As loans to G Loans had their interest accrued, G Loans were unable to repay the loans. This meant the shares in KJK Investments did not grow by the estimated 6%. There were 209 pension holders who invested a total £11.9m in KJK Investments shares with the hope of 6% investment gain. They also liberated some of their pension under what they were told was a legitimate pension liberation. Furthermore because of the non-commercial nature of the loans, as well as the high fees and commissions paid there was never any possibility of regaining the pension funds which were initially invested.

This was a scam from start to finish and has now been wound up by the High Court. Furthermore the 209 pension holders who liberated funds from their pensions are now facing up to 55% unauthorised payment tax charges.

Pension-life.com is helping some of these victims and appealing the tax liabilities, as well as preparing to take action against the negligent parties.

These are the significant share holders of the KJK Investments Ltd. It is yet to be revealed if these significant shareholders released their pensions to buy shares.

Pension tax simplification, often simply referred to as “pension simplification” and taking effect from A-day on 6 April 2006 was a policy announced in 2004 by the Labourgovernment to rationalise the British tax system as applied to pension schemes.

The aim was to reduce the complicated patchwork of legislation built up by successive administrations which were seen as acting as a barrier to the public when considering retirement planning. The government wanted to encourage retirement provision by simplifying the previous eight tax regimes into one single regime for all individual and occupational pensions.

What happened after A day ?

The first thing to understand is that retrospective legislation is not desirable and would be open to challenge. In other words, many of the previous pension regimes provided better pension options than the new simplified rules. In these cases, investors were allowed to keep the previous benefits earned before 2006, with only their post 2006 benefits being automatically affected.

In practice, this means those with a foot on either side of 2006 can opt for the post 2006 on all their benefits if this suits them.

A word of caution

We would refer to A Day as adding a layer of simplification, not removing previous layers of complication. The interaction of the new rules and those with protected benefits – both pre 2006 and after – is extremely complex and the advice requirements are stiff.

Who are the players in pension transfers?

Outside the UK, any man and his dog can claim to be a pensions expert. Of course, there are genuine pension specialists outside the UK who have the necessary competencies to undertake pension transfer advice. The public need to undertake their own checks on their advisers to make sure they are regulated and qualified.

In the UK, this is straightforward. The FCA register shows the permissions of each firm.

Outside of the UK, advisers do not need any qualifications if they only undertake money purchase transfers or transfers with guaranteed benefits valued at lower than 30,000 GBP.

For transfers of schemes with guarantees (such as final salary schemes and policies with guaranteed annuity rates) that are valued over 30,000 GBP, then only a UK IFA with the correct FCA permissions can advise.

However, many money purchase schemes that do not require qualifications for transfer advice also straddle the pre 2006 and post 2006 rules. Namely, occupational money purchase schemes such as CIMPS/COMPS, Sec 32, EPP and SSASs. An unqualified adviser is unlikely to know all the rules and transfer advice may be inappropriate from such an individual.

Financial Conduct Authority – FCA – for personal pension schemes

The Pensions Regulator – TPR – for company pension schemes

Outside the UK, not all jurisdictions have pension regulators and, even if they do, if the pension is not a local pension it will not be of interest to the regulator (i.e. someone living in Spain with a pension in New Zealand, where the advice was given in Spain, is unlikely to get much help from the regulator in New Zealand).

Since A Day, the old HMRC approval system came to an end. Each scheme is now registered only and not approved in any way. Thousands have been registered, many of them being bona fide schemes, but also – because of the absence of due diligence by HMRC and tPR – many also being bogus and/or scams.

Pensions were also targeted for liberation scams. Here the promoters provided “loans” to members from their own scheme or from an associated source, or just cashed in part or all of their pension prior to the age of 55. Many thousands now face financial ruin as HMRC will tax them 55% of the funds they took early (unauthorised payment tax). Despite the fact that the investors acted in good faith and were the victims of fraud as well as negligence on the part of HMRC, tPR and the ceding providers, HMRC will still make every effort to enforce the tax.

Meanwhile, the government sits idly by and does nothing. Pensions Minister Ros Altmann merely says that the victims are “fools”.

Protected assessment: this is what thousands of pension liberation scam victims are receiving:

Pension Schemes Services

Fitz Roy House

Castle Meadow Road

Nottingham

NG2 1BD

PHONE 03000 564567

WEB www.gov.uk

Date 02 March 2016

Our Ref: UTR 99999 00000/XX/YYY – Ark

Dear Mr. J D

ARK PENSION RECIPROCATION SCHEMES

TAX LIABILITY – year ended 5 April 2012

During the year 2011/12 you were a member of The Tallton Place ARK Pension Scheme and according to the information I hold, an Unauthorised Payment (liberation/loan) was made either to you or in respect of you. I am currently liaising with the Trustees of the Pension Scheme and a list of Frequently Asked Questions (FAQs) have been prepared to help you understand the complex tax consequences and HMRC’s view. A copy of the FAQs is attached.

Following a change in legislation brought about by Schedule 39 Finance Act 2008 in relation to HRMC time limits for the issue of assessments and determinations, HMRC has issued an assessment in order to protect its position and ensure that any potential tax due for the year ended 5 April 2011 is not lost.

The assessment is based on the higher of the amount of MPVA loan you made or received from your pension scheme. Where you did not receive an MPVA we have based the assessment on the maximum amount of MPVA you coud have made (50% of the value you transferred rounded down to the nearest £2500) HMRC may consider other alternative arguments once their enquiries are complete.

Amount of unauthorised payment £ 57,500

Tax Due at 40% £23,000

Tax Due at 15%(surcharge) £8,625

Total Tax Due £31,625

HMRC will continue with its enquiries in order to establish the correct amount of tax due for the year ended 5 April 2011 and you should not, therefore, consider the assessment to signify the closure of HMRC’s enquiries.

If you have not already provided information to HMRC, please let me have the following information as soon as possible:

A copy of the signed Maximisining Pension Value Arrangements (MPVA) Agreement relating to the sum received by you under Agreement relating to the sum received by you under the Agreement (the MPV Amount)

A copy of your bank or building society statement showing the payment of the MPV Amount into your account

Copies of all documents and correspondence held by you relating to the MPVA arrangements entered into by you.

Details of how you were introduced to the MPVA arrangements

Details of the persons you dealt with concerning the MPVA arrangements.

An explanation as to why the unauthorised payment (the MPV Amount) was not declared in you 2012 Tax Return

You have the right to appeal against this assessment and, considering the circumstances, HMRC would not object to a postponement application of 100% of the tax due on the assessment until such time as our enquiries are finalised. Full details of how an appeal and postponement of tax can be made are enclosed.

I would also like to tell you that you may want to consider making an application for discharge of the unauthorised payments surcharge under Section 268 Finance Act 2004 if you think that you meet the ground set out in Section 268(3) Finance Act 2004. If you do want to make an application, this should be sent to me at the address shown above and you will need to set down the reasons why you meet the conditionset out in the legislation.

If you contact us, we can deal with you more quickly if you quote the reference number and provide a daytime telephone number. If you prefer you can email us at pension.compliance@hmrc.gsi.gov.uk. Please remember to include ARK in the subject line of your email.

A copy of this lette plus enclosures have been sent to your agent Angela Brooks.

Yours Sincerely

XXXXX XXXXXXXXXXXX

Compliance Officer

To find out what you can expect from us and what we expect from you go to www.gov.uk/hmrc/your-charter and have a look at ‘Your Charter’.

Pension Schemes Services

Fitz Roy House

Castle Meadow Road

Nottingham

NG2 1BD

PHONE 03000 564567

WEB www.gov.uk

Issuing Officers Name: XXXXXXXXXX XXXXXX

Reference: UTR 99999 00000/XX/YYY – Ark

Date: 02 April 2016

NOTICE OF ASSESSMENT FOR THE YEAR ENDED 05 April 2012

Amount charged by this assessment: £31, 999.00

I am sending this assessment to you because we have found that there is additional tax dur that was not previously shown on your tax return. It is now too late for us to amend your tax return so this assessment allows us to collect the additional tax. We have made this assessment under Section 29 of the Taxes Management Act 1970.

I enclose a copy of my calculation of the amount charged by this assessment. I have also included this amount on your Self Assessment statement, a copy of which is enclosed.

About your adviser

I have sent a copy of this notice to your adviser, Angela Brooks, Ark Class Action.

Paying what is due.

Please pay £34, 630.01 no later than 4 May 2015. This is the amount due for assessment. Please refer to your Self Assessment statement for details of the interest included in this amount, as well as details of any other items that you have not yet paid. Please also pay any other amounts that are due.

We have charged you late payment interest for the amount charged by this assessment. We will add more interest on a daily basis until you have paid all the tax due that is due, so we recommend that you pay straightaway.

If you do not pay all the tax that is due as a result of this assessment within 30 days of the date it should be paid, we will charge you late payment penalties. A late payment penalty is an additional amount of money that you will have to pay as well as the tax that is due. If your payment is:

30 days late, we will charge you an initial penalty – this will be an amount equal to 5% of the tax you owe at that date

6 months late, we will charge you a further penalty – this will be an amount to 5% of the tax that you owe at that date

12 months late, we will charge you a second further penalty – this will be an amount equal to 5% of the the tax that you owe at that date.

Interest we charge for paying tax late

We will charge you interest on any tax and/or penalties that you pay late. We will charge it from the date that the payment should have been made, until the date that it is paid. Any interest charges are shown your on your Self Assessment statement.

We will charge you interest from 31 January 2013 until the date it is paid. If you should have made Self Assessement payments on account by 31 January 2012 and 31 July 2012, we will charge you interest on what you should paid from those dates.

Changes to the Self Assessment tax that you are due to pay for one year, may affect the payments on account that you are due to make for later years.

How to pay

We recommend that you pay us electronically. You can find more details on out website. Go to www.hmrc.gov.uk/payinghmrc/index.htm

If you need to pay by post, please send a cheque to:

HM Revenue & Customs

Accounts Office Shipley

BRADFORD

BD98 1YY

Please make your checque payable to ‘HM Revenue & Customs’ followed by the reference ‘UTR99999 00000’.

If you disagree with the assessment, you can appeal. To do this, you need to write to us within 30 days of the date on this assessment, telling us why you think our desicion is wrong. We will then contact you to try to settle the matter. If we cannot come to an agreement, we will write to you and tell you why. You can then either:

have the matter reviewed by an HMRC officer who has not previously been involved in the case

ask an independent tribunal to decide the matter.

If you choose a review, you can still fo to the tribunal if you are not satisfied with the outcome.

If you appeal, you can ask for the payment of all or part of the tax in dispute to be postponed until the matter is resolved.

If you want to apply for a postponement, please tell us the amount of tax that you think you are being overcharged and the reasons why you think you should not have to pay this. We will continue to charge interest on any tax that we postpone. Once the dispute is settled, the interest will be payable if tax is found to be due.

You can find more information about your appeal and review rights in factsheet HMRC1 ‘HM Reveneue & Customs decisions – what to do if you disagree’. You can get this fact sheet from our website. Go to www.hmrc.gov.uk/factsheets/hmrc1.pdf or you can phone our orderline on 0300 200 3610.

On a rainy Tuesday, we wiggled our way round the back of Westminster Cathedral to the DWP which houses Pensions Minister Ros Altmann and also Work and Pensions minister Iain Duncan-Smith. As it turned out, it also housed a security guard called “Babs”.

We were a trio from Ark Class Action which represents victims of pension scams such as Ark, Capita Oak and Evergreen. With me were the vice chair (an Ark victim who lost her final salary pension along with her partner); and secretary (also an Ark victim who lost her final salary pension along with her husband). The previous evening, they had spent several hours comforting a very distressed Capita Oak victim who was worried sick that the assets of his pension – Store First store pods – were now worthless.

We had gone to meet recently appointed Altmann to urge her to ensure the government takes the action which is so desperately needed to tackle pension scams. Altmann, former adviser on pensions to the Labour government, had severely criticized George Osborne for his “cavalier” attitude to Britain’s 12 million pensioners – one of the most powerful voting blocks in the country. http://www.theguardian.com/money/2011/mar/27/george-osborne-ignore-pensioners-peril#comments

We had decided not to waste our time seeing Iain Duncan-Smith since a year previously he had promised support, action and meetings, but had turned out to be as dishonest as the scammers themselves. After his false promises, he had then gone on to “lose” one member’s entire file, including copies of bank statements and then lied about having returned it by recorded delivery.

Altmann had always come across to me as an honourable person and we had high hopes that she would take the time and trouble to understand the seriousness of the pension scam industry – which continues to flourish and ruin thousands of victims – costing billions of pounds’ worth of pensions every year. Having already met shadow Pensions Minister Nick Thomas Symonds, Mayor of London Boris Johnson and MP Wes Streeting, we felt sure Altmann would want to engage with the Class Action and spearhead an anti pension scam campaign without hesitation.

Having spent weeks trying to set up the meeting with Altmann, our mission was to ensure she understood that the system of policing and preventing pension scams was quite simply broken. We wanted her to become the champion who would take the credit for putting this disgraceful situation right while regulators, police authorities, HMRC and the government continue to fail to address the problem. With the Pensions Select committee aiming to treat pension scams as a spectator sport, http://www.publications.parliament.uk/pa/cm201516/cmselect/cmworpen/371/37106.html we thought Altmann might step up to the plate and launch a military-style, zero-tolerance initiative against pension scams and scammers.

We thought wrong. Babs the security guard informed us:

“You are not going to be seen and you need to leave the premises. This is not a Job Centre”.

Altmann has brought both the Cabinet and the House of Lords into disrepute by publicly turning her back on thousands of victims of pension scams. She would do well to remember that along with many frontline workers, there are Police officers and Armed Forces personnel losing their pensions every day.

MPs have already urged the government to take action against the embarrassing and disgraceful scandal of unchallenged pension fraud.

I suggest she puts rather more effort into doing her job properly and less effort into comparing the DWP with a Job Centre. Her responsibility is to champion the cause of thousands of victims of pension fraud – both helping existing victims and preventing future ones. Altmann should hark back to the warnings she herself made about George Osborne’s “cavalier attitude” to pensioners before she was appointed pensions minister. And also remember the criticisms she was making about the government four years ago. http://www.theguardian.com/money/2011/mar/27/george-osborne-ignore-pensioners-peril#comments And then search her conscience honestly.

Pension liberation fraud costs victims £millions every year. It ruins lives and causes desperate poverty in retirement. But the situation is made far worse because the State has badly miscalculated how much it will cost to support these victims for the rest of their lives. The amount of tax actually collected will be far outstripped by the cost of support and healthcare.

LETTER TO PRUDENTIAL’S CHAIRMAN RE TRANSFERS TO PENSION SCAMS

Dear Mr. Manduca

As you are the Chairman of Prudential, and in light of the recent POS determination in respect of a Capita Oak victim’s transfer out of Prudential and in to a scheme which was clearly a pension liberation scam, I feel it is important to bring to your attention the significance of the Ombudsman’s decision for Prudential, dozens of other ceding providers, and for the thousands of victims of pension liberation fraud.

The Pensions Ombudsman feels there should be a distinction between the culpability/negligence of transfers made by ceding providers pre-tPR Scorpion campaign and post. I disagree very strongly and believe that if you allow this precedent to impact on the defrauded members of Prudential, this will also allow other ceding providers (your competitors) to escape responsibility for failing the thousands of members who have fallen victim to scams such as Capita Oak. This will impact severely on the credibility of not just Prudential but the whole industry and Britain’s ethos of saving for a pension.

The Pensions Regulator was issuing warnings about pension liberation fraud back in 2009. But in 2010/11, Prudential allowed dozens (at least) of transfers into Ark. Following tPR’s action (placing the six Ark schemes into the hands of Dalriada in May 2011), and a high-profile High Court ruling by Justice Bean which declared Ark to be a “fraud on the power of investment”, Prudential do not appear to have improved their due diligence at all.

HMRC state that “members and pension providers would have been aware of warnings/tax consequences in early 2012 (to pension liberation scams) as there were sufficient warnings and publicity available within the public domain from regulator websites, such as HMRC’s, the Pensions Regulator and the Financial Conduct Authority and a number of pension provider websites.”

And yet, in 2012/13, Prudential transferred at least 28 members’ pensions totalling more than £829k to the Capita Oak pension liberation scam. Around half of these were post Scorpion. (Scottish Widows, by comparison, transferred more than £750k into Capita Oak and half of this was post Scorpion.)

Also in 2012/13, Prudential transferred at least £383k to another pension liberation scam: Westminster. Most of this was post Scorpion. Prudential was beaten only by Scottish Widows who transferred more than £485k to Westminster – all of it post Scorpion.

In none of the transfers did Prudential seek confirmation that the members were genuinely employed by the sponsors of Capita Oak and Westminster. Had they done so, they would have found that both schemes had the same spurious “employer” (a non-existent company in Cyprus) and the same administrator: Imperial Trustee Services Ltd.

Prudential also failed to spot that both these schemes’ transfer administration was handled by Stephen Ward’s company Premier Pension Transfers Ltd at 31 Memorial Road, Worsley (with Ward’s Spanish firm Premier Pension Solutions SL being a tied agent of AES Financial Services Ltd, an FCA-regulated firm). A little more gentle digging with a very small spade would have found that Ward was the principal promoter and administrator for Ark.

In researching the Ark, Capita Oak and Westminster members’ files, I can find no evidence that Prudential did any due diligence at all in respect of any of the transfers. Prudential asked no questions of the members or of the administrators of the schemes. Prudential asked for no copies of the trust deed or the scheme accounts or evidence of the sponsoring employer. There is no evidence in my possession that Prudential’s transfer due diligence improved at all post Scorpion.

In response to one of my complaints to Prudential in respect of a transfer to Ark, Prudential’s Customer Relations Specialist Yvonne Kewell wrote on 7.3.15: “I can assure you that all appropriate checks were done before we transferred the fund. We followed the correct process as required at that time”.

If Prudential’s “appropriate checks” and “correct process” between 2010 and 2013 were to fail to heed tPR’s warnings as far back as 2009 and beyond; ignore advice widely available in the public domain in early 2012 (according to HMRC); neglect to adhere to the Scorpion checklist in 2013, then what possible faith can the public have in Prudential or indeed the rest of the industry?

To my knowledge, Prudential have transferred well over £2m in members’ funds to pension liberation scams (and that’s just the ones I know about). Operated by the same scammers. In the same manner. To the same effect for the victims: poverty in retirement and crippling tax liabilities which may result in homelessness.

Prudential’s Ms Kewell’s concluding statement reads: “I hope my letter explains our position”. If Prudential’s position is that it is acceptable to fail its members and ignore warnings/advice widely available in the public domain over a four-year period, then perhaps that redefines the term “customer relations”?

Prudential has a once-only opportunity here to emerge from this series of debacles as a shining example of how a leading pension provider should respond to valid complaints of negligence. If Prudential sets a conscientious example and compensates the victims voluntarily (notwithstanding the POS determination above) then all the other providers will have no option other than to follow suit.

I have thrown down the gauntlet. I look forward to your early response. You and Prudential can either emerge as a hero or a villain since I can assure you there is a determined and highly-organised campaign to bring ALL negligent ceding providers to justice in respect of negligent transfers to pension liberation scams. With a compliance and legal team the size of Huddersfield, I sincerely hope that Prudential will now elect to become a hero amongst the depressing tide of ceding providers who have sought pathetically to justify their failings in thousands of negligent transfers to obvious scams.

Regards, Angela Brooks – Chairman, Ark Class Action and Pension Life

www.pension-life.com

Pension liberation fraud has been reported widely in the press, on t.v. and on radio for several years. The Inside Out documentary showed how easily victims are scammed by the teams of scammers. The Ark Class Action, led by Angela Brooks, filmed part of this programme at the BBC studios along with a financial adviser and solicitor.

Interestingly, Andrew Isles, the accountant who helped design and set up the Ark schemes, took part enthusiastically in the filming. The BBC team did some secret shopping of their own, and uncovered another pension liberation scheme run by George Frost – former Chairman of Canvey Island Football Club. Frost’s scheme invested victims’ pensions in “truffle trees”.

ARK PENSIONS DISASTER CLASS ACTION – MISSION STATEMENT

For members of the Ark Pensions schemes and any other similar schemes involving MPVA (Maximising Pension Value Arrangements) or PRP (Pension Reciprocation Payments) or Pension Liberation (releasing a proportion of your pension before the age of 55).

THE MISSION: There are a number of challenges facing the Ark Pensions victims. What they want and need is clarity, honesty, transparency, justice and action to get their pensions back and be put into the position they should have been in before their original pensions were transferred to Ark (or any other similar pension liberation schemes).

The Ark Pensions Class Action is taking up all the challenges required to do this and give the victims back their financial security in retirement. To do this, and more, there are five distinct but inextricably-linked aspects to the mission:

THE GOVERNMENT

DALRIADA TRUSTEES

HMRC

FINANCIAL ADVISERS WHO SOLD THE ARK SCHEMES

JUSTICE BEAN’S RULING (INTERPRETATION AND APPLICATION)

THE GOVERNMENT

The Government’s Pensions Regulator investigated the Ark schemes and made a full report detailing the areas where it did not feel the schemes complied with Pension Regulations: http://www.thepensionsregulator.gov.uk/docs/DN2116109.pdf.

When I say “full” I mean “full-ish”. The Pensions Regulator has blanked out the bits it doesn’t want the public to see.

The Pensions Regulator appointed Dalriada Trustees to take control of the Ark schemes and they were suspended in May 2011. Dalriada has been recovering the original investments made by the Ark schemes and have recovered the majority (despite originally declaring them to be worthless). They are now taking steps to recover the loans made to the Ark members.

The government is responsible for HMRC who are trying to tax the Ark loans even if they are repaid.

The government department – The Financial Conduct Authority – refused to take action against the financial advisers who sold the Ark schemes, saying that it was “not within their jurisdiction” – and anyway they get to pick and choose which cases to pursue.

The government is responsible for:

Pensions being frozen and 10% of the original Ark assets being spent on fees by Dalriada in the first two years

Secrecy over the who/where/what/how the Ark disaster was set up, investigated and “worked”

Failure by the FCA to take action against the negligent financial advisers who sold the schemes in the first place

Failure by HMRC to decide clearly how and where they intend to tax the loans at 55% despite having had three years to do this and honour their own “Taxpayers Charter” (help and support taxpayers to get things right). The loans could be taxed in three different places (depending on what HMRC can get away with).

Apathy. So far, only three MP’s out of the entire House of Commons have taken up their constituents’ cases. George Osborne has completely ignored the matter. David Gauke, Treasury Secretary, has brushed the matter aside in a “bothered?” letter without even asking about the welfare of the Ark victims or offering to do anything to help.

DALRIADA TRUSTEES

Dalriada were appointed by the Pensions Regulator in May 2011. The pensions remain frozen. After numerous bouts of legal action, two sets of audited accounts were sent out seven months after the end of the first two financial years. No news as to when Dalriada’s work will be concluded. Bulletins and updates sent out infrequently and Dalriada staff not great at returning Ark victims’ calls and emails. Some Ark victims have still heard absolutely nothing from Dalriada.

In the first two years since their appointment, Dalriada charged £665,039 in fees, spent £1,633,371 on legal fees and £47,695 on audit fees (10% of the total fund value). They refuse to declare how much has been spent in year three, stating that the Ark victims must wait until audited accounts are released in December 2014.

In three years, Dalriada have failed to resolve with HMRC whether the Ark loans are taxable or repayable. And failed to inform the members that – actually – they are both. Dalriada have been meeting with HMRC for some time, but claim it is nothing to do with them if HMRC tax the loans (just as HMRC are claiming it is nothing to do with them if the taxed loans are forcibly reclaimed by Dalriada).

There is still no clear idea of how safe the Ark pensions are. £11.8 million of Ark victims’ cash is held on deposit at Barclays Bank earning pitifully-low interest. (Let’s not forget that Barclays are being investigated by the Serious Fraud Office over a shady £322 million Qatar deal and have been fined £50 million by the FCA – so why chose Barclays?)

Dalriada are making a “Beddoe” application for court directions as to how to recover the Ark loans. They have stated they will not agree to Angela Brooks, representing numerous Ark victims, being present at the private hearing because the hearing is “private” and that she is an “unconnected party”.

Dalriada need to answer key questions about the future of the Ark pensions. Legal and financial professionals fear the “fee-earning machine” could roll on for years until there is nothing left of the pension funds. Unless Dalriada are challenged. And vigorously.

In the three years since Dalriada took over the Ark pensions, HMRC have done nothing – I repeat, NOTHING – to clarify the taxation of the Ark loans. They did not even sit down and have a meeting with “pensions experts” until the end of March 2014 i.e. more than two years after Justice Bean ruled in the High Court that the loans constituted unauthorised (i.e. taxable) payments.

It must be remembered that if HMRC had not registered the Ark schemes in the first place, the original pension providers would not have made the transfers and the Ark disaster WOULD NEVER HAVE HAPPENED. HMRC have since publicly stated that they were going to put an end to the “register now, ask questions later” negligent and sloppy approach. But they lied. Angela Brooks applied to register a pension online at the HMRC website, using her own name and private address in Spain at the beginning of January 2014. Two weeks later she received her HMRC-authorised pension certificate. No questions asked.

HMRC have informed the Ark Pensions Class Action that:

55% tax is payable at the receiving end or at the making end of the loans (the funds). Or both.

Dalriada have said that HMRC will also be taxing the members themselves for “making” the loans (even though they had nothing to do with it).

Even Ark members who did not receive loans will be taxed at 55%.

HMRC refused to be joined in the High Court proceedings in December 2011 because “it wasn’t a tax case”.

They declined to be bound by Justice Bean’s ruling. But are now relying on it.

They want all Ark members to complete tax returns so that an appealable decision can be issued and then the members have to appeal the tax before the tax tribunals – knowing full well that this is a lengthy, expensive and stressful process. But HMRC have deep pockets, and they don’t care.

If the Ark members don’t get an appealable decision, HMRC will issue a determination with no appeal.

Some Ark members have received demands to complete tax returns. Some haven’t. Some have already paid the tax “on account”. Some are so worried they can barely function.

HMRC state that the loans are still taxable even if they are repaid.

HMRC have to be taken to task. They have blatantly contravened their own “Taxpayers Charter”. They have not lifted a finger to sort out a clear and fair way to deal with this unclear and unfair situation which is inflicting so much stress, anxiety and potential financial ruin on so many Ark victims.

The tax demands have to be vigorously challenged and appealed in the tax tribunals and some sort of justice as well as closure sought to end the misery of the past three years.

FINANCIAL ADVISERS

Let’s get one thing 100% straight right from the start. Financial advisers have one thing and ONE THING ONLY to sell: financial advice. Not halal chicken or horse-meat burgers; not snake oil or penis enlargement cream. Pure and simple financial advice. And it is an easy enough job because all you have to do as a “financial adviser” is ask your clients three basic questions:

What is your risk profile?

What is your risk profile?

What is your risk profile?

Then all the financial adviser has to do is provide the client with three crucial bits of information:

Here’s a copy of my professional indemnity insurance

Here’s proof of my authorisation/regulation

Here’s my fee for your approval (plus anybody else’s fees in the “supply chain” for this transaction)

It is worth defining “risk profile” in order to establish just how easy it is to get it right:

First, ask the client if they are low, medium or high risk (in other words, how happy are they to lose their investment if things go tits up). If the investor says “very happy” – refer to a psychiatrist

Second, explain the underlying investment in plain English without any gobbledygook (i.e. property or shares or precious metals or an outsider in the 3.30 at Kempton Park)

Third, outline how the investment will be spread between a variety of different types and class of fund (after all, only a complete moron would put 100% of his client’s money into something as outrageously risky and toxic as a “death bond”!)

However, if – despite following all the basic, not-rocket-science rules of how to be a competent and successful financial adviser – things do go pear shaped, then the client can go back to the financial adviser and complain and ask for compensation and redress.

The good, professional, competent, conscientious, properly regulated and insured financial advisers will move heaven and earth to help, assist and support the aggrieved client and make every effort to resolve an investment which has turned sour. If the problem is not resolvable and the client ends up either losing money or gaining an unforeseen tax liability (or both), then the financial adviser will notify his professional indemnity insurers and ensure that the client is compensated.

As with all professions, however, there are the good, the bad and ugly. Unfortunately for the Ark members, they have been victims of financial advisers who are not only bad and ugly, but downright cowardly. In the face of their monumental cock ups, they have shown that not only do they have no conscience but they have no balls either.

The financial advisers responsible for the Ark disaster will be brought to justice. Many of the Ark victims have described them as “dead men walking”. However, the Ark Pensions Class Action wants them kept alive and healthy so that they can face both criminal and civil proceedings for justice and compensation for their victims.

HIGH COURT RULING

In December 2011, Justice Bean declared (Clause 57 of the ruling) that the Ark Pensions loans were “unauthorised payments” (i.e. taxable at 55%). In the same clause, he also ruled that they were “not unauthorised payments” (i.e. not taxable at 55%).

About as clear as mud. Either way, HMRC declined to be joined in the proceedings (or, to put it in layman’s language – they couldn’t be bothered to turn up). Their excuse was that “it wasn’t a tax case” – although they knew that tax was central to the issue. They also declined to be bound by the ruling – although they are subsequently relying on the ruling that the loans WERE unauthorised payments and ignoring the bit that says they WERE NOT unauthorised payments.

Many highly-qualified and experienced legal and tax professionals think Justice Bean was wrong. Equally, James Bulger’s family thought Justice Bean was wrong when he sentenced Jon Venables to two years in prison for distributing child pornography, and stated it was important to protect Venables’ secret identity.

However, the judge did say one very significant thing which seems to have escaped HMRC and that is at Clause 53 where he quotes the case of DCC Holdings v HMRC heard by Lord Walker of Gestingthorpe and a bunch of other judges who agreed with him about the principles of interpreting and applying laws (also known as “common sense”):

“…the correct approach in construing a deeming provision to be to give the words used their ordinary and natural meaning, consistent so far as possible with the policy of the Act and the purposes of the provisions so far as such policy and purposes can be ascertained; but if such construction would lead to injustice or absurdity, the application of the statutory fiction should be limited to the extent needed to avoid such injustice or absurdity…”

To put the above into layman’s terms, this means “if the law is an ass, don’t act like a donkey”.

The Ark Pensions Class Action puts it to His Honour Justice Bean, HMRC, The Pensions Regulator, Dalriada Trustees, the Treasury Secretary, the Pensions Minister, the Chancellor, the Prime Minister, the Financial Ombudsman, the Pensions Ombudsman, the Parliamentary Ombudsman (and any other Ombudsman you can think of) that the following position is both unjust and absurd:

Dalriada will be reclaiming the Ark loans

HMRC will be trying to tax the Ark loans – at least once, if not twice or three times if they can get away with it

The tax on the loans (whether 55%, 110% or 165%) will be repayable even if the loans are repaid

Even those Ark victims who did not receive a loan will be taxed at 55% because they “intended” getting a loan

Even those Ark victims who didn’t receive a loan because they didn’t want one will be taxed at 55% because they “made” a loan (presumably in their sleep)

The Class Action will be calling upon all involved in this disaster to interpret the law justly, and with intelligence rather than with downright stupidity.