Back due to popular demand, qualified and registered company blogs. Today, I am looking into Belgravia Wealth, a Swiss based company. Belgravia Wealth – qualified and registered? Lets see if you are.

Belgravia Wealth has an impressive list of services offered. However, those who follow our blogs will know that the terms “structured products” and pensions together, makes us shudder with horror. We have seen so many pensions ruined by being invested in high-risk, fixed-term, for-professional- investor-only structured products.

Whilst I have a queue of trolls telling me that structured notes are “not all that bad”, take a look at this video we created about John Rodgers and the ´blue chip notes´ that destroyed his pension fund. He was a victim of a pension scam courtesy of Continental Wealth Management, which affected around 1,000 members.

What Belgravia say on their website:

“Belgravia Wealth Management is a Swiss-established and regulated company founded to fill the advice gap that currently exists between the retail financial companies and the services available to the UHNW clients. As an independent company, we ensure that you benefit from impartial advice and access to offerings from all the financial providers available in the market.”

It is great to read that Belgravia Wealth is regulated. Many firms I have written about fail to meet this simple – but essential – requirement. They claim to be independent and suggest that their advice is impartial. I wonder, though, with all this transparency in their blurb – are their staff qualified and registered to give this “impartial” advice?

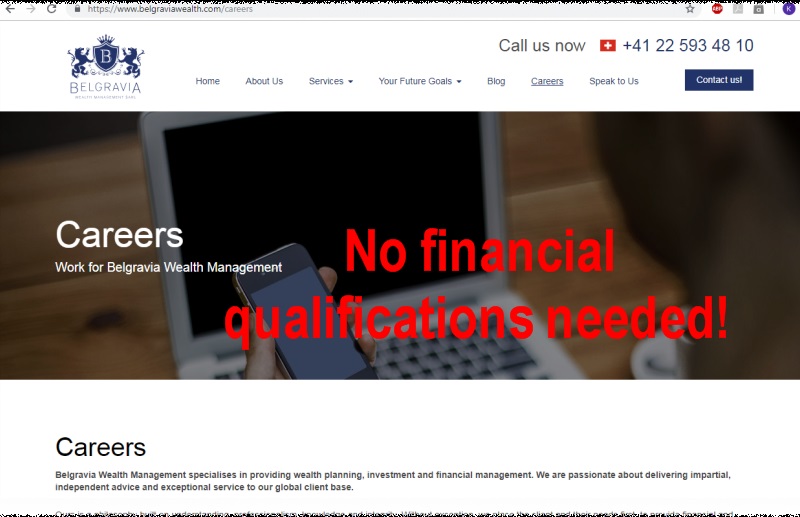

Whilst their website offers a tab entitled “Careers”, it does not offer a list of staff that actually work for Belgravia Wealth. So, over to Linkedin to see if Belgravia Wealth staff advertise their employment with the company.

As with all these blogs, we only go by the information we can find, which is the same information potential clients would be able to access.

IFAs and their clients are invited to add to this blog, correct it, improve it. We will gladly edit our information if proof of qualification certificates can be supplied. Here’s a link to the three registers if you want to double check for yourself:

http://www.cii.co.uk/web/app/membersearch/MemberSearch.aspx

https://www.cisi.org/cisiweb2/cisi-website/join-us/cisi-member-directory

https://www.libf.ac.uk/members-and-alumni/sps-and-cpd-register – Claim to a DipFA

- Spencer Freeman-Haynes – Director Zurich and Basel region at Belgravia Wealth Management – claims CISI – DOES not appear on the register

-

Emmanuel Obi, Jr. LL.M – Head of Compliance – Switzerland at Belgravia Wealth Management – no financial qualifications claimed (but how can he oversee the compliance function if he isn’t qualified?)

-

Regional Manager – Geneva Area, Switzerland – lists various CII qualifications – DOES NOT appear on the register

-

Director at Belgravia Wealth Management SARL – Claims CISI – DOES NOT appear on the register

-

Belgravia Wealth Management – Basel Area, Switzerland – No financial qualifications claimed

- Mystery Man (I do not have access to the profile) – Manager of Business Development – Belgravia Wealth Management – without a name I can not check his qualifications

Belgravia Wealth Switzerland has 6 members of staff listed as working for them, and from what I can tell NONE of them are qualified or registered to give financial advice.

Belgravia Wealth- qualified and registered 0%

Angela oh Angela where do I start with Belgravia, what better place than the first two on the list. The toxic twins as they are known in the profession Spencer Freeman Haynes and his drug dealer Emanuel Obi. The new breed of advisers strutting their stuff in downtown Geneva. Only the best champagne and class A narcotics for this band of idiots who talk billions not millions, billions! Their elaborate lifestyles all paid for through pilaging expats pensions. Emanuel Obi is a published fiction writer and if anyone cares to look his books up, they are a great cure from insomnia. The best work of fiction however is his CV, he does not have a qualification in law of any sort and is merely mirroring someone with the same name who does have a qualification. Old trick of a conman there which has paid off for him till this point. So let me tell you with absolute certainty he is not qualified to be head of compliance anywhere on this planet and the only reason he got the role was Spencer’s love of cocaine.

Without a doubt Belgavia will be making headlines for all the wrong reasons soon and it will be up to you Angela to deal with the broken dreams of pensioners who trusted this new breed of advisers. Do your due diligence people don’t become the next boardroom conquest of drug addled advisers selling high commission structured products.

Oh dear, here we go again…. “However, those who follow our blogs will know that the terms “structured products” and pensions together, makes us shudder with horror.” followed by this “Whilst I have a queue of trolls telling me that structured notes are “not all that bad”

I can’t say I have ever been described as a “troll” and I have to say I am shocked!! One thing I have over the writers of this blog is I can relate to the victims – been there, done it and got the scars!! But I am obsessed by “accuracy” in reporting and I keep saying the FCA permit structured products to be promoted to retail clients by – oh, here is the key to this, wait for it… – [UN]REGULATED IFA’s.

Oh wait, maybe this is the common denominator – it’s not the ASSET that’s the problem, it’s the bar stewards promoting them! You keep dissing the asset when in fact it’s the unregulated scum persuading the victims to invest in the high risk “asset” – whatever it may be!

Property is considered a safe asset – except when it’s not. For example, Cape Verde ( https://www.lovemoney.com/news/51956/action-fraud-warning-cape-verde-investment-pension-scam ). I don’t see you dissing “property” as an investment! However, when property is sold “fraudulently” by unregulated “advisers” then that becomes the scam – not the asset. ALL scams have some th,ings in common – unregulated advisers and “fraudulent misrepresentation” about the asset and the HIGH RISK structured product is yet another example of fraudulent misrepresentation marketing. But there are also “ok” structured products, legally promoted by regulated IFA’s in the UK in the same way there are legally promoted “property investments” recommended as assets in pension portfolios.

Your ignorance in this area does not give these blogs any credibility. In fact quite the opposite! And your only defence for your ignorance seems to be to call anyone that disagrees with you a troll rather than research your material correctly! Shocking!!!

I guess I need to stop coming here. Not good for my blood pressure.