FRIENDS LIFE – OR DEATH? WINDSOR PENSIONS QROPS SCAM (DANICA)

Since 2010, dozens of ceding pension providers have recklessly and negligently allowed transfers out to obvious pension scams. During the years of Ark, Capita Oak, Westminster and Henley, the worst offenders were Standard Life, Scottish Widows, Prudential and Aviva as personal providers, and Royal Mail as an occupational provider.

Both HMRC and the Pensions Regulator claim there were sufficient/ample warnings in the public domain to educate and inform ceding providers about pension scams since 2002. But the Pensions Ombudsman’s Service claims the cut-off date was February 2013 when the Pensions Regulator first published the “Scorpion Campaign”. According to the POS, before Scorpion all ceding providers walked around with paper bags over their heads and did no reading up on their professional and fiduciary obligations or any developments among scams and scammers.

However, a recent ruling on the negligence of a ceding provider – Friends Provident – may change the course of history. The case of “Mrs N” involved a transfer from FP administered by a company called Windsor Pensions run by one Steve Pimlott in Florida. In fact, I “secret shopped” Windsor and Pimlott in 2015, and he was still offering “transfers to Danica QROPS” with full liberation. He also claimed to have done 5,000 such transfers/liberations.

On 25 February 2015 at 10:37, STEVE PIMLOTT <stevepimlott@windsorpensions.com> wrote:

Dear Ms Brooks

I cannot give you tax advice. If you cash out, it’s possible that HMRC will send you a tax bill. We assisted approximately 5,000 people who took that route and I would estimate that 200-300 did receive a tax bill. The rest to my knowledge did not. Of those that did, many just ignored it because they were resident in a different country and had no assets left in the UK.

Regards

Steve

The question is, however, does this set the bar for other negligent ceding trustees? This case is notable because it is “pre Scorpion”. But the POS found that irrespective of the date, Friends Provident should have done more due diligence and not just handed over a pension to a scheme which was no longer registered (and, de facto, to a fraudulently-set-up bank account).

You decide:

PO-9935 1 Ombudsman’s Determination Applicant Mrs N Respondent Friends Life Limited

Outcome

- Mrs N’s complaint is upheld and to put matters right Friends Life should pay her the unauthorised member payment tax charge and surcharge less the tax liability she would have paid had the full pension been taken as an uncrystallised funds pension lump sum (UFPLS). In addition it should pay Mrs N £1,000 for the significant distress and inconvenience caused by its error.

- My reasons for reaching this decision are explained in more detail below.

Complaint summary

- Mrs N complained that Friends Life undertook insufficient due diligence on the qualifying recognised overseas pension scheme (QROPS) into which she had requested a transfer. Had it acted appropriately it would not have accepted the transfer instruction.

- Following the transfer Mrs N received the full value of her pension. At the time she was 53. As a result she is now liable to a 55% unauthorised member payment tax charge.

- Mrs N has also said she has incurred costs whilst attempting to resolve the situation and Friends Life should pay these.

Background information, including submissions from the parties

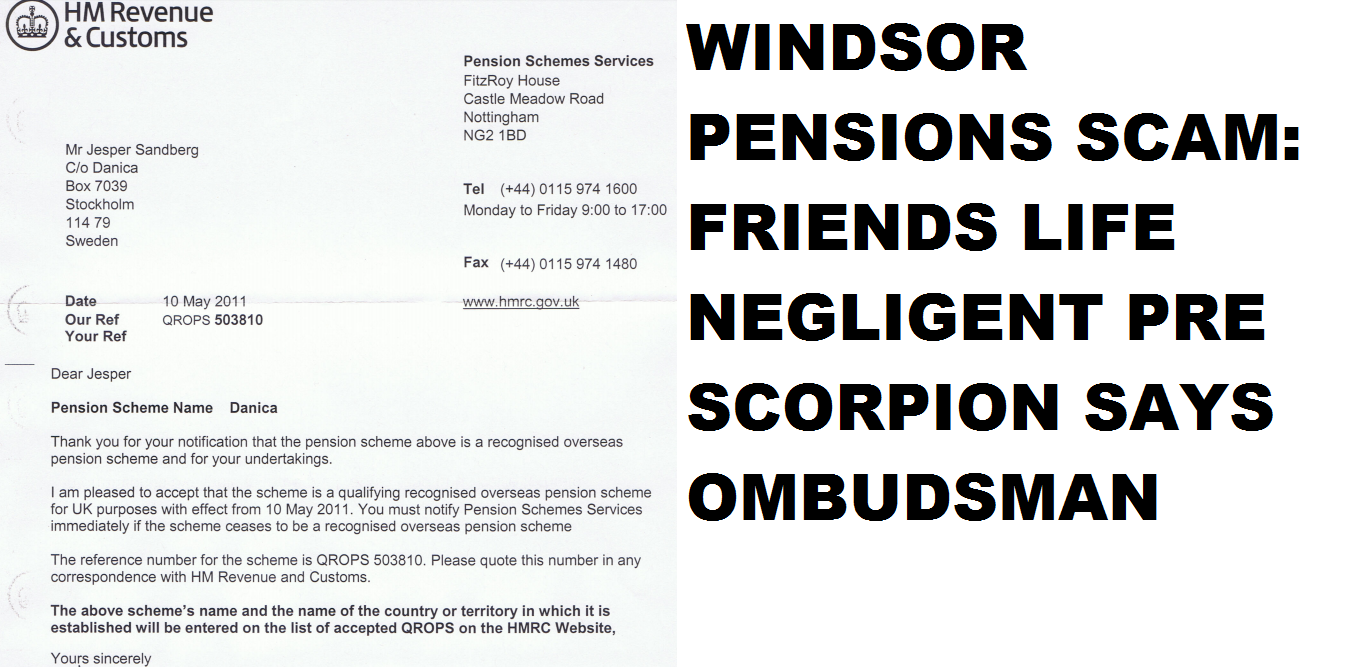

- On 10 May 2011, HMRC wrote to Danica, Stockholm, confirming undertakings had been received that Danica was a recognised overseas pension scheme, and that HMRC would accept the scheme as a QROPS with effect from 10 May 2011. It provided a QROPS reference number – QROPS 503810 – and confirmed that the scheme name and country would be added to the list of accepted QROPS on HMRC’s website.

- Danica was added to the HMRC QROPS list, but then removed on 29 June 2011.

- In October 2011 Mrs N completed a letter of authority for an unregulated financial intermediary; Insignia Financial Services. This was submitted to Friends Life which responded with a transfer illustration on 3 January 2012. QROPS illustrations were issued on 21 January 2012.

- On 16 February 2016, Friends Life received an Overseas Transfer Out Payment form and Member Declaration, signed by Mrs N on 7 February 2012. Accompanying this was the HMRC letter confirming QROPS status.

- QROPS discharge forms were issued to Mrs N shortly after.

- The required forms were received by Friends Life on 9 March 2012. Friends Life says that the supplied QROPS number was checked against the QROPS list and found to be correct. Friends Life also checked the HM Treasury sanctions list.

- The payment of £88,622.80 was processed on 13 March 2012. However, what the POS has not disclosed is that the funds were sent to a Barclays Bank account in the Isle of Man which was fraudulently set up by the scammers with the account name “Danica”. I understand the money was subsequently paid to Mrs N by the Danica arrangement and has since been spent. No it wasn’t. The money never went near the Danica pension scheme in Sweden. It went straight to the scammers’ bank account in IoM.

- Friends Life were made aware of an issue with the Danica scheme, and Insignia Financial Services on 13 April 2012.

- Mrs N has since been contacted by HMRC and informed that the transfer was an unauthorised payment, so it is subject to an unauthorised member payment tax charge and surcharge of approximately £49,000. I understand this has not been paid and remains outstanding, with interest accruing.

- Mrs N raised a complaint about Friends Life’s actions. It did not uphold the complaint, and made the following summarised points.

- Mrs N had a statutory right to transfer, and Friends Life had no reason to think that the information provided regarding the QROPS was false. Friends Life missed a rather obvious clue i.e. a QROPS in Sweden was purportedly using a Barclays bank account in the IoM – might that not have rung an alarm bell?

- The QROPS number was checked against the QROPS list and found to be correct. Although the name Danica did not appear on the QROPS list, Danica Private Pension (Sweden) and Danica Pension (Sweden) did. In other words, similar but different.

- The transfer happened prior to concerns about pensions liberation being widely recognised as an industry issue. The Pension Ombudsman has previously said that February 2013 was the point of change in good industry practice where knowledge of pension liberation and scams had increased. This is nonsense – both the Pensions Regulator (formerly known as OPRA) and HMRC had been warning the industry about pension scams for more than fifteen years. Friends Life had an absolute duty to be aware of and vigilant against pension scams.

- The presence of a scheme on the QROPS list does not guarantee its QROPS status, and HMRC forms which would have been completed by Mrs N state: “The list should not be relied upon by you, the member in deciding whether a scheme is a QROPS.” Pretty confusing to be honest: HMRC publishes a list of QROPS but the member herself has to decide whether the scheme is a QROPS. How would a member decide that? Ask the scammers?

- Friends Life suggested that Mrs N transferred her pension with full knowledge of a lump sum payment being made, which was not offered under her existing plan due to UK tax legislation. It was reasonable to expect that she would have sought independent financial advice before proceeding. Instead she proceeded through an unregulated financial adviser and did not seek advice from a regulated adviser. Indeed, the adviser was unregulated – but Mrs. N did not know this and wouldn’t have known how to check anyway. In fact, Friends Life ought to have brought this to her attention at the start.

- There was an onus on Mrs N to check the legitimacy of her financial adviser. At the time there was no reason for Friends Life to think the financial adviser was unregulated. Friends Life didn’t even check.

- Friends Life had highlighted that, ‘Tax penalties may apply following a transfer to a QROPS. It is important all implications are understood before transferring funds from the UK’, and Mrs N had received a copy of this statement.

Adjudicator’s Opinion

- Mrs N’s complaint was considered by one of our Adjudicators who concluded that further action was required by Friends Life. The Adjudicator’s findings are summarised briefly below:-

- Central to the complaint was whether Friends Life should have acted on Mrs N’s transfer request. Side issues relating to the legitimacy of the financial adviser involved or any declarations signed were not integral to the complaint.

- The events complained of occurred prior to the Pension Regulator’s pension liberation warning campaign of February 2013, at a time when checks on receiving schemes were less rigorous. This may be correct – however, that doesn’t make it right. However there were reasonable basic checks that Friends Life ought to have completed before making the transfer, including checking HMRC’s QROPS list. They did check the QROPS list and were probably confused by the similar names of two other schemes containing the word “Danica”.

- The Danica scheme had been on the list for a short period but was removed by the time Mrs N submitted the transfer request. Friends Life’s internal policy was not to transfer to schemes which were not on the QROPS list.

- Although the QROPS list was checked the day before the transfer was put through and there were two similarly named schemes on the list, the Danica scheme was not on the list. At that point additional checks should have been undertaken to establish why the Danica scheme was not on the list, had it done so it would have established that the Danica scheme had been removed nine months prior.

- In these circumstances Mrs N’s pension should not have been transferred, and had it not done so Mrs N would not now be subject to the unauthorised member payment tax charge and surcharge. One could argue against this point – perhaps Windsor Pensions and Insignia Financial Services would have found another obscure QROPS to use for the fraud.

- To put matters right Friends Life should agree to meet the full cost of the unauthorised member payment tax charge and in addition pay Mrs N £500 for the distress and inconvenience suffered.

- The Adjudicator did not consider Friends Life should be required to pay the costs Mrs N incurred when bringing the complaint. The complaint could have been referred to this Office and resolved without the involvement of her representative. I would not agree necessarily: Mrs. N had a very busy life running a business in the USA and she did need help and guidance with the complaint against Friends Life and the POS process. She was also fighting the tax demand at the same time and was extremely distressed.

- Additionally, in relation to potential accountant’s fees she may incur, the Adjudicator concluded she would have needed to pay similar costs had the funds been received through legitimate means.

- Mrs N did not accept the Adjudicator’s Opinion and the complaint was passed to me to consider. Mrs N and Friends Life provided further comments which are summarised below.

- Friends Life said:-

- Friends Life accepted the recommended redress in principle, but highlighted that it had already paid a 40% Scheme Sanction Charge and Mrs N was, under the Adjudicator’s recommendation, in effect being paid the fund value without any tax liability. Friends Life proposed to pay the unauthorised member charge less the notional tax Mrs N would have paid had she legitimately accessed the full fund value under the current rules. It calculated the tax she would have paid to be £15,294.34.

- Friends Life also considered that given Mrs N’s position it was reasonable for her to have sought independent financial advice given its recommendation that she do so, and especially given her unfamiliarity with UK taxation laws. In not doing so Mrs N had contributed to the risk that her pension could be adversely impacted by the transfer.

Mrs N said:-

- The proposed redress would have significant tax consequences for her as a U.S. resident. As a result the redress would not put her back into the position she should have been had the error not occurred.

- She had incurred significant expenditure appointing a representative to pursue the complaint on her behalf. Those costs, and the cost of receiving appropriate cross border tax advice, would continue to rise. Given the complexity of the issues in the complaint, and the tax complications she could not have brought the complaint without specialist assistance.

- The redress methodology used by Friends Life show a misunderstanding of Mrs N’s tax position. For instance it has suggested that she would be entitled to a personal allowance, when as a U.S. resident this is not the case.

- The wording of the redress must be specifically tailored to avoid potential tax complications in the UK and U.S. Friends Life should pay the costs associated with drafting agreeable wording to avoid those tax complications.

- Friends Life should provide an indemnity to cover the potential tax liability arising from the redress payment.

- She was very distressed by the situation, has been unable to sleep and it has impacted her health.

- On review of Friends Life’s and Mrs N’s responses to the Opinion the Adjudicator made the following points:-

* Friends Life’s offer to pay the unauthorised member payment tax charge and surcharge, less the tax Mrs N would have paid had the pension been paid as an UFPLS, was reasonable in the circumstances. The recommended redress was altered to reflect this.

* The redress was not intended to pay Mrs N’s tax liability. Mrs N was the party subject to the liability and would need to pay this. The redress was intended to make good a relevant proportion of that loss once it had been paid. Under this arrangement the reference to a personal allowance was only notional it did not appear that Mrs N would be subject to punitive tax charges as the redress was intended to make good Friends Life’s error.

* Given the significant impact on Mrs N’s health the Adjudicator increased the proposed distress and inconvenience award to £1,000, which Friends Life agreed to.

- Having considered Mrs N’s arguments they do not change the outcome. I agree with the Adjudicator’s Opinion, summarised above, and I will therefore only respond to the key points made by Mrs N for completeness.

Ombudsman’s decision

- Mrs N argues that she could not have brought the complaint without employing the assistance of tax and pensions specialist. I do not agree. In the first instance a complaint can be passed to the Pensions Advisory Service, who can guide an applicant through the Scheme’s complaint process and provide technical input where the applicant lacks an understanding of the issues involved. In this case TPAS considered it too late to intervene due to the potential time limits of referral to this Office. So it was not a lack of understanding that prevented TPAS from taking on the case.

- Notwithstanding that, had Mrs N not accepted Friends Life’s response to the complaint she could have brought the complaint directly to this Office for review. Although Mrs N’s representative disagrees, I am confident that this Office has the expertise to investigate complaints about pension liberation. I would dispute that: the POS has repeatedly failed to uphold pre-Scorpion complaints on the basis that pension trustees had never heard of pension liberation fraud prior to February 2013 – which is absolute nonsense. The representative’s involvement has not brought any unknown evidence or arguments to the investigation. Mrs N was entitled to seek assistance in this matter, but that does not mean Friends Life are responsible for the costs incurred where there are free dispute resolution alternatives available to her. For that reason I do not consider Friends Life should pay the costs she is claiming. To be fair, I think Mrs N should have had her costs paid. She – and thousands of other victims in this situation – find themselves utterly overwhelmed by these types of cases and need support. Also, being based in the USA, she needed someone to deal with the case in the UK.

- I understand that as a U.S. tax resident there may be complications in Mrs N’s tax situation on receipt of the redress payment. Her UK and U.S. accountants have said they will not provide advice on the matter because of the complications. The redress may cause her to have to seek specialist tax advice. However, tax is matter for Mrs N and the local tax authorities. It is not for me to determine any future tax liability she may have, and it may ultimately be that there is none.

- I have also taken into account that had Mrs N taken her pension through legitimate means she would have needed to seek tax advice regardless, so in my view the position has not changed. Mrs N will have had to pay for tax advice at some time or another regardless of how the pension was accessed.

- Friends Life has said it does not believe that the redress payment would be taxable, but that it would reconsider its position if at a later date it can be shown that Mrs N had suffered a tax liability, although it would not agree to an indemnity. This is a reasonable stance for Friends Life to take. Mrs N should establish any resultant tax liability due to the redress and communicate that to Friends Life if necessary.

- Looking at the proposed redress methodology, Mrs N may disagree with certain assumptions made by Friends Life, but I consider they are reasonable assumptions. I note in particular that in relation to the personal allowance, under this notional methodology, she is better off for it being included than if Friends Life assumed no personal allowance.

- The approach taken to offsetting the notional income tax that Mrs N would have paid had she taken the full fund value as an UFPLS is balanced and appropriate. This places Mrs N broadly in line with the position she would have been had the pension been taken in full under the current rules. I believe that is an appropriate remedy for the error caused by Friends Life.

- Therefore, I uphold Mrs N’s complaint.

Directions

- Within 28 days of this determination Friends Life should establish the unauthorised member payment tax charge and surcharge less the notional tax liability of £15,294.34 she would have paid had the full pension been taken as an uncrystallised funds and pay this to Mrs N. PO-9935 7 31. Additionally it should pay £1,000 for the significant distress and inconvenience suffered.

Anthony Arter Pensions Ombudsman 27 June 2017

Does this basically mean HMRC will stop pursuing people thus has happened to ..or done the same as Mrs N …or that the HMRC will continue to track down these cases ..and each case will have to be gone through the ombudsman or court like this case has ?

Thoughts anyone ?