I read an interesting article recently which has prompted this blog, written by Blair duQuesnay, CFA®, CFP® – an investment adviser at Ritholtz Wealth Management, LLC. Blair suggests that the most important change needed in the financial industry is qualifications. Poorly qualified advisers give poor investment advice. Bad investments advice leads to loss of funds.

I read an interesting article recently which has prompted this blog, written by Blair duQuesnay, CFA®, CFP® – an investment adviser at Ritholtz Wealth Management, LLC. Blair suggests that the most important change needed in the financial industry is qualifications. Poorly qualified advisers give poor investment advice. Bad investments advice leads to loss of funds.

Blair has said one thing that underpins all the work we do at Pension Life:

“The bar to hold oneself out as a financial advisor is low, shockingly low. This is all the more shocking because the stakes are so high. Clients have only one chance to save and invest for retirement. If bad advice leads to the unnecessary loss of capital, there is no time to start over.”

Read Blair’s piece here:

http://blairbellecurve.com/substance/?fbclid=IwAR1or8YzCkxUNh_M5-o9e7WngaYJXXV_vjyWI92ZjXEXqG5x9DWzJMA8rgc

I have written many times in the past about unqualified financial advisers, leading victims blindly into wholly unsuitable investments. These unqualified “snake-oil salesmen” often put most (or sometimes all) of their clients funds into unregulated, toxic, illiquid, no-hoper rubbish which has high commissions for the broker to earn but leave the pension or investment portfolio with an unrecoverable dent.

If investors are unsure about what qualifications an adviser needs to give advice on investments then please have a read of this blog: “Qualified or not qualified? That is the question”

Blair (pictured) talks about substance and the need for higher standards among financial advisers. Whilst I love her thoughts, I know how difficult this might be to achieve. We see wholly unqualified scammers posing as fully qualified IFAs time and time again. These scammers are very good at acting the part and the victims have no idea they are dealing with a fraudster – and sometimes go on for years believing they are dealing with a proper financial adviser.

Blair (pictured) talks about substance and the need for higher standards among financial advisers. Whilst I love her thoughts, I know how difficult this might be to achieve. We see wholly unqualified scammers posing as fully qualified IFAs time and time again. These scammers are very good at acting the part and the victims have no idea they are dealing with a fraudster – and sometimes go on for years believing they are dealing with a proper financial adviser.

When accepting financial advice always ask the ‘adviser’ what financial qualifications they have. If it transpires they are not fully qualified to give investment or pension advice – walk away and find someone who is.

Blair’s words highlight this issue perfectly, stating, “What sort of education, credentials, and work experience do these people have? It depends. You cannot tell which type of firm, business model, or regulatory space in which they operate or if they have the right training and qualifications to give financial advice. One broker is a CFA charterholder, while another down the hall had three weeks of sales training and took the Series 7.”

Often the best scammers are the ones with the sales training – they know how to push the ‘hard sell’, make the victim think they are ‘missing out’ if they don’t sign straight away. In offshore firms – especially – we see job adverts for new ‘financial advisers’, which state that they are looking for people with sales backgrounds. All too often there is no mention of the necessity of a financial services background, let alone any financial qualifications. Often guys that used to sell cars or holiday apartments will end up selling pension transfers. These are the ones you definitely want to avoid.

Blair goes on to say, “There’s a common phrase that it takes 10,000 hours to master a skill. Working a 40-hour week with no holidays or vacation, that takes almost five years. I would argue this number is low. I practice ashtanga yoga, a method that adds one new posture when the previous one is mastered. I spent over four years on the same posture. In that daily work of making tiny incremental progress toward the end goal, I overcame fears, corrected weaknesses, and powered through with pure determination. That is substance.”

Blair highlights that we live in a time of instant gratification and almost laziness in regards to making money. From multi-million-pound Youtubers, rich from being stupid in videos, to big-bottomed rich girls selling their life stories to become famous – it is all about obtaining difficult things easily.

Twenty-first-century living is driven by the need for wealth and the need for that wealth to be earned FAST!

These desires are what the scammers use to their advantage. They tell their victims that their funds will be placed in high-return investments. Investments that will easily add great value to their pension fund, meaning they will be able to have a lavish retirement.

The thought of possibly doubling your pension fund in just ten years can seem like something of a dream come true. AND, unfortunately, a dream is usually what this is. Placing your funds in supposedly high-return investments – ALWAYS – means taking a high-risk.

Whilst some high-risk investments do pay off, they are no place for a pension fund – life savings are what people are depending on to keep them in their later years. A pension fund is not a fund to be risked: it should be placed in a broad spectrum of liquid, low-to-medium risk investments. Maybe a small proportion could go into a higher-risk investment but only if the investor’s risk profile says he is comfortable with that degree of risk. Most people – even high-net-worth clients – don’t want to lose ANY money.

A trustworthy and fully qualified financial adviser would know this and he would ensure the advice he gives you is in your best interests – not his. The unqualified salesman giving “advice”, will usually opt for the fund that gives the highest commissions. He can walk away with a fat wallet (probably never to be seen again) and the bleak future of your pension fund is not something he will lose sleep over. But you will, when the high-risk investment in which your entire fund is trapped starts to rapidly lose value.

If the gentle reader doubts these dire warnings, just look at the facts about investment losses that we highlighted in a recent blog:

Who killed the pension? Scammers; ceding providers; introducers; HMRC?

£236,000,000 London Capital & Finance fund (bond), but also:

£120,000,000 Axiom Legal Financing Fund

£456,000,000 LM Group of Funds

£207,000,000 Premier Group of Funds

£94,000,000 Leonteq structured notes

Without stating the blooming obvious, that is well over one billion pounds’ worth of AVOIDABLE losses – and still just the tip of the iceberg.

Blair finishes her article by saying, “We owe it to our future clients to raise the bar. People deserve the reassurance that the person giving investment advice on their life savings has a baseline of knowledge. Until then, clients must continue to do their research on advisors. Look for those who have put in the time to learn their craft and have degrees and credentials to prove it. Often these are not the best salespeople, but at least these advisers have substance behind them.”

What a lovely finish and what a very important statement. Financial advisers are not salesmen, they are financial advisers. Their work should be conducted in a way that best suits the needs of the individual – each individual, separately. And there is one way and one way only to invest a client’s money: do a proper, thorough, professional risk assessment and then invest strictly in accordance with that the resulting risk profile.

Slow, steady and fully qualified financial advice always wins the race.

Looking at International Adviser’s 2017 awards, I really think the judges were having a

Looking at International Adviser’s 2017 awards, I really think the judges were having a  I HAVE DECIDED TO INVITE MY FRIENDS AT INTERNATIONAL ADVISER TO LAUNCH A NEW AWARDS CEREMONY:

I HAVE DECIDED TO INVITE MY FRIENDS AT INTERNATIONAL ADVISER TO LAUNCH A NEW AWARDS CEREMONY:

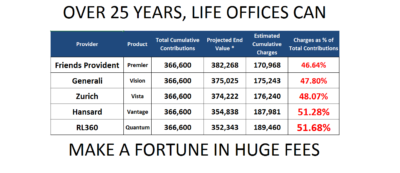

OMI – Old Mutual International (Quilter), SEB, ZURICH, GENERALI, FRIENDS PROVIDENT, ZURICH INTERNATIONAL, RL360 AND HANSARD INTERNATIONAL. They are all as bad as each other. They rip their clients off, charging them huge fees and commissions, tying them into useless, pointless products for years.

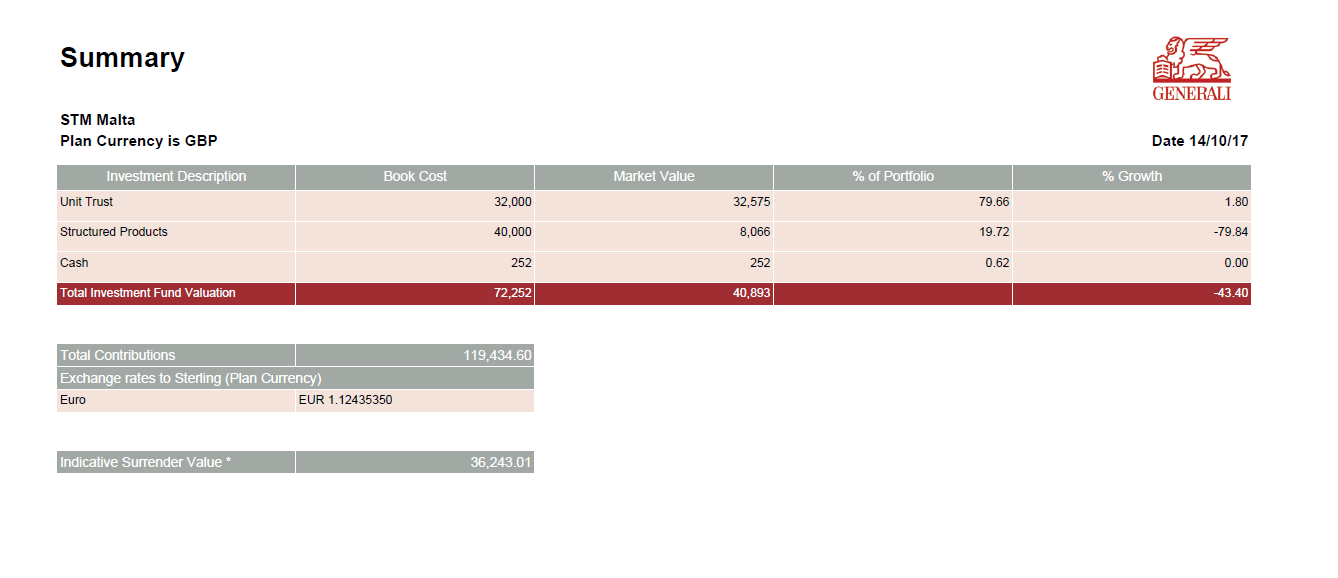

OMI – Old Mutual International (Quilter), SEB, ZURICH, GENERALI, FRIENDS PROVIDENT, ZURICH INTERNATIONAL, RL360 AND HANSARD INTERNATIONAL. They are all as bad as each other. They rip their clients off, charging them huge fees and commissions, tying them into useless, pointless products for years. One Generali victim saw her £119k pension fund plummet to £36k in five years.

One Generali victim saw her £119k pension fund plummet to £36k in five years. Pension scams are not the only arrangements that these life offices profit handsomely from. Another method they use to rinse extortionate fees out of unsuspecting victims is the LONG TERM SAVINGS PLAN. Clients think these are a good idea until they realise the huge hidden charges which decimate the funds they put towards these plans.

Pension scams are not the only arrangements that these life offices profit handsomely from. Another method they use to rinse extortionate fees out of unsuspecting victims is the LONG TERM SAVINGS PLAN. Clients think these are a good idea until they realise the huge hidden charges which decimate the funds they put towards these plans.