Al Rush, Henry Tapper, Darren Cooke, Steve Webb and Michelle Cracknell

Knowing how to spot a scammer is half the battle in the fight against pension and investment scams. And my idol and hero in this fight is Darren Cooke of Red Circle Financial Planning. Armed with his petition calling for a cold-calling ban, he quickly became a t.v. star and National celebrity.

UPDATE: Cold-calling has still not been fully banned!! (20/11/2018)

Last week, on Monday 19th June 2017 (the week of the dreaded Ark trial) I had the privilege to attend the Great Pension Transfer Debate in Peterborough – organised by the amazing Al Rush and chaired by the awesome Henry Tapper. There I met a few people I already knew but also got to meet Darren Cooke in person and tried hard not to graze my knees as I groveled humbly before him. I also met some other wonderful professionals and heard some wonderful speakers – not the least of which were Sir Steve Webb and Michelle Cracknell.

But – and I mean no disrespect to the event and it’s organisers – all the excellent things which were said during the presentations depended entirely on the quality and honourability of the advice given. With only one notable exception, the event was attended by the ethical, qualified, regulated cohort of the profession. But, of course, out in the field there are sharks and shysters by the dozen – both in the UK and offshore.

In fact, this event was a world away from the world I live and work in. The attendees of this event were the cream of the financial services profession; those who pride themselves in being ethical, honest and conscientious. Most of the people there already had reputations for maintaining the highest possible standards of professional excellence, respecting the law and regulations, and actually caring about their clients. But I felt like a fish out of water, because generally I am dealing with criminals who have deliberately and callously ruined thousands of lives – some of whom are now, thank goodness, under official investigation by the SFO.

So, those in the know probably understand how to check qualification and regulation at the drop of a hat – but how does the ordinary man in the street – or on the Clapham Omnibus – know how to do that? Does the public know that there are a few – very few I would add – regulated and qualified firms and individuals in the UK who are scammers? (Ok, there are masses offshore, but let’s concentrate just on our mainland for the time being).

And even if a member of the public does know how to do that, do they have any idea what else to check or verify? Again, the answer is: of course not. So why don’t we start with the basics: the FCA register. That ought to tell the enquirer whether a firm is regulated – but that is part of the problem: regulated for what exactly? A firm which is regulated for insurance mediation is not regulated for pension or investment advice. But the ordinary man in the street does not understand that. Then you’ve got qualifications; looking up an individual on the CII register might show up a “student” member, but a member of the public might not know that is not the same thing as a qualified member.

But then you have firms which are FCA regulated but which are still scammers – albeit very few to my knowledge (but still enough to cause sufficient damage to large numbers of victims). And, of course, offshore it is simply “open season”.

The creepy crawlies of the financial services world (ugh!)

Rather than trying to figure out how to spot a scammer, perhaps we should have a go at deciding what constitutes a scam and work backwards from there. The Cambridge dictionary defines a scam as “an illegal plan for making money, especially one that involves tricking people“

The Business Dictionary defines a scam as “A fraudulent scheme performed by a dishonest individual, group, or company in an attempt to obtain money or something else of value. Scams traditionally resided in confidence tricks, where an individual would misrepresent themselves as someone with skill or authority, i.e. a doctor, lawyer, investor”

There are many variations on this theme – and many peripheral scammers providing cold-calling, lead generation and marketing services and loan facilities as well as spurious “introducers” which pose as quasi advisers. And then there are the accountants who sell tax-avoidance investment schemes and employee benefit trusts – resulting in heavy losses and tax liabilities. And then there are the UCIS providers peddling such rubbish such as collapsible holiday flats in an obscure part of Africa; oblong bits of tarmac not too far from an airport; truffle tree plantations; recycling inventions and empty tin cans.

If we keep it simple for now: how does the ordinary man in the street or on the Bakerloo Line check out a UK-based financial adviser? First check his qualifications; second check out that his firm is regulated by the FCA to provide the service being sought i.e. pension and/or investment advice; third ask for evidence of professional indemnity insurance; fourth check the solvency of the firm.

If the advisory firm goes bust and the client loses a large amount of money, the maximum the client can claim from the Financial Services Compensation Scheme is £50,000 for investments. The best place to check solvency is Companies House where you can look up a company’s accounts and see how profitable and solvent it is. And then ask yourself whether you want to take financial advice from a firm which can’t even look after it’s own finances.

One example is an advisory firm in Guildford which has been trading for 21 years. For twelve of those years the company has made a loss. On total turnover of £11 million since it started trading, it has made a total profit of £36 thousand during the entire period. Would you want that firm to advise you on your finances?

So, my advice is check, check and check again. And when you think you have exhausted all the checks, get a second opinion. The information is out there – it is just a question of knowing where and how to look for it; what questions to ask and how to understand the answers. And then you’ll be a man, my friend. SMILEY FACE 🙂

The Ark victims’ QC rolls over as he is quashed by Dalriada’s counsel

DALRIADA V ARK VICTIMS: “ABUSE OF VULNERABLE MEMBERS OF THE PUBLIC”

The Beddoe proceedings of Dalriada (tPR-appointed independent trustees) v Goldsmith (representative beneficiary for the Ark members) kicked off on 20th June 2017 in the High Court. It was a sweltering day in central London – humid and dusty at the same time. The Ark victims were about to discover that the warning about anomalous and unjust outcomes made by Justice Bean in the High Court in November 2011 was going to be ignored.

Dalriada and their solicitors, Pinsent Masons, and their QC Fenner Moeran sat on the left in the airless courtroom. Mrs Goldsmith and our solicitors, Trowers and Hamlins and QC Keith Bryant, sat on the right. Justice Asplin sat on the bench and prepared to rule on whether 348 Ark victims would have to repay their MPVA loans – and whether Dalriada could use the members’ funds to pay for the recovery proceedings. A group of Ark, Capita Oak and Salmon Enterprises victims and I sat at the back. The only thing we all had in common was that everybody was sweating profusely from the heat.

To put this into context, the Ark victims did indeed all sign loan agreements. However, the loans were intended to be paid back out of the members’ 25% tax-free lump sums available at age 55 – so the term of each loan agreement was calculated to be for the number of years it would take each member to reach 55. By which time, the pension was predicted to have grown by at least 8% per year and would be sufficient to repay the loans. Or so the story went.

Conspicuous by their absence were the various introducers and advisers who sold the Ark schemes and accompanying MPVA (Maximising Pension Value Arrangements) “loans”. By far the most assertive and prolific of these was Stephen Ward of Premier Pension Solutions who sold over £10 million worth of transfers to more than 160 victims. Ward was followed by those who aspired to be as successful as him and these included:

Julian Hanson £5.3m

James Hobson (Silk Financial) £2.3m

Jeremy Dening £2.2m

Michael Rotherforth £961k

Richard Davies £805k

Geoff Mills £794k

Andrew Isles £584k

Amanda Clark £227k

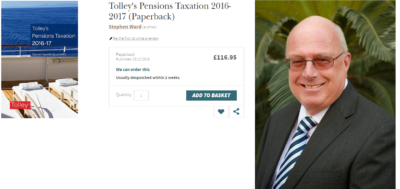

Many of these went on to operate further pension liberation scams – some of which are now also in the hands of Dalriada Trustees. Andrew Isles of Isles and Storer Accountants is still in practice. Stephen Ward still authors the Tolley’s Pensions Taxation Manual.

The definitive pensions taxation manual by leading pension liberator Ward

Interestingly, Stephen Ward, who used Ark to launch a whole series of further pension scams – including several currently under investigation by the SFO and in the hands of Dalriada – claimed in 2014 that “The Ark thing is history now and my involvement with that was administrative”. Of course, neither of those statements was true: Ark is far from being history as, in the wake of the Beddoe proceedings, a whole new chapter of wretched challenges for the Ark victims has only just begun. Ward was the leading promoter, evangelist and advisor to Ark. He had sold over a third of all the transfers – with a total transfer value of more than £10 million.

In fact, Ward and his herd of “introducers” he had recruited from up and down the country (including FCA-registered Gerard Associates which went on to collaborate with Ward in the London Quantum pension scam) – also now in the hands of Dalriada – often assured the victims they would never have to repay the loans.

Fenner Moeran QC, for Dalriada, opened with the lusty confidence of a dashing matador – and who could possibly have failed to be charmed by his persuasive, eloquent, star quality? He reminded me of an actor at the Oscars who knew he was the favourite to win. With his extravagant hand gestures and polished, word-perfect performance, he got into his stride and stayed there – holding court for the whole day with barely a feeble squeak out of our QC.

Moeran’s confidence, however, veered a little too close to cockiness, and he strayed occasionally into the realms of being callously offensive to the Ark victims when he talked about using a “sharp stick” to beat them into submission with threats of bankruptcy. At that moment, he stopped looking like a polished QC and started to look like a mere back-street bully. In fact, it was astonishing that the judge didn’t pull him up on that “foot and mouth” moment, but she appeared to be far too mesmerised by his charming performance to notice – or care.

While I was taking notes, it was really interesting to watch the players’ body language. One can tell an awful lot about what is really going on in people’s heads by what they do with their various body parts. When Moeran was on his feet, Justice Asplin was coquettish, smiley, full of chuckles and did this wiggly thing with her shoulders (like we women do when we are trying to get a bra straight). But when our QC Keith Bryant was on his feet, she sat as still as a statue and peered down at him with a combination of indifference and pity as if he was a dying bull in the afternoon sun.

Mrs Goldsmith sat quietly and showed not a shred of distress as Moeran referred to her and all the other Ark victims as though they were just names on a list, as opposed to human beings – or indeed anything with a pulse. Knowing her well, I am sure she will have felt profound pain and anguish during the whole three days, but not once did either her composure or her dignity slip.

So here is my transcript of the notes I took on what the various parties said during the proceedings – with my comments in bold.

The last thing I personally want to say on the matter, is that something good has to come out of this and my fervent hope is that all those involved in the promotion, sale, administration, introduction, advice, purchase of assets, execution of loans and various other functions will now face justice sooner rather than later. And here, I am actually grateful to my learned fiend’s suggestion of a sharp stick and would propose something more akin to what Vlad The Impaler would have done to these criminals.

TRANSCRIPT OF MY NOTES AT THE HEARING

DAY ONE

Never forget that legal proceedings are nothing to do with justice

Justice Asplin opened with the words “This was a tragedy and an abuse of vulnerable members of the public”. That got us off to a really good start, but curiously the following day she vehemently denied ever having said it. She also denied ever having mentioned Ark and didn’t even seem to know that collectively, the six schemes (Tallton, Grosvenor, Woodcroft, Cranbourne, Lancaster and Portman) were the Ark schemes. Bearing in mind she had had – and been paid for – a whole day’s reading, one would have thought she would have been a little better prepared.

Ark’s Craig Tweedley was quoted as having made a statement that Ark was “designed to unlock amounts of money from people’s pensions in a way which was not taxable”. This is perfectly true – but it went further: it was promoted to the public (both introducers and potential members alike) as an innovative structure which was lawful and tax free. And the principal promoter and recruiter was Stephen Ward. Ward is also a CII Level 6 qualified former pensions examiner and government consultant on pensions and QROPS – so who wouldn’t have believed him?

One of the Ark schemes’ assets – the South Horizon land option in Larnaca, Cyprus – was brought up and reported as having been purchased by Ark for £4 million. But what was not mentioned was that the option had originally been purchased by two football celebrities for £1.1 million and then sold on to Ark for £4 million. And that this pair had gone to accountant Andrew Isles of Isles and Storer to get advice on how to procure further investors in the Cyprus land project. Isles had introduced them to Craig Tweedley and Stephen Ward. In fact, Isles subsequently introduced at least eleven cases to Ark.

It was stated that Craig Tweedley’s associates Andrew Hields and Julian Hanson had purchased all the assets of the schemes and that the sales documentation claimed that some of the funds were “guaranteed “funds and protected by “re-insurance”. Hields and Hanson may well have purchased some of the assets but they will certainly have benefited from handsome investment introduction commissions along the way.

It was also reported that one of the other Ark assets, Freedom Bay, the St. Lucia timeshare development, is now in administration and that none of the investments made met the statements and claims made in the sales documentation. In fact, it did not come out that few – if any – of the victims were ever shown the sales documentation. Most of Stephen Ward’s victims were told the assets would be “high-end residential London property”.

The matter turned to the recovery effort. It was reported that Tweedley had been pursued for the 5% fees taken from scheme members and that although Dalriada had won their claim, of the approx. £1.5 million taken in fees, they only ever actually managed to recover about £20k. This does beg the question as to just how successful Dalriada will actually be in recovering the £9 million in MPVA loans.

In taking steps to recover the loans, it was reported that Dalriada intends to consider the cost vs benefit situation and decide on the approach on a case by case basis, taking each individual case on its merits. It was acknowledged that the chances of recovery were slim and that the costs could be disproportionate to the likely return. The judge asked how many members had received MPVAs and it was disclosed that 348 had and 138 had not. However, nobody raised the question of why such a large number of members had not received an MPVA loan – had they done so it ought to have been disclosed that a significant proportion of transfers were not rejected after Dalriada were appointed.

It was at this point, while examining the possible avenues to recovery, that Moeran’s confidence bubbled over into bald cockiness and he started bragging about using the threat of bankruptcy as a “sharp stick with which to beat the victims into paying back their MPVA loans”. In fact, by now the judge seemed to be very firmly on his side and stated that the members had already agreed to repay the loans and that their only loss was having to repay early. It seemed clear that neither Moeran nor the judge understood – nor had made any attempt to understand – how the loans were sold to the victims. They were told, by Ward and all the others involved in promoting the scheme, that the loans would be repaid out of their pension pots and not out of their own funds. In fact, some people were told they would never have to repay the loans and that each person on either end of the loan transaction would simply agree to tear up their “IOUs”.

Moeran then went on to claim that by repaying the loans, members could avoid the tax charge. Perhaps the HMRC fairy had whispered this in his ear? Or perhaps he was deliberately ignoring the fact that it is HMRC’s position that the loans will remain taxable even if they are repaid.

Towards the end of day one, it was clear that Moeran was confident they were going to win and that the judge would clearly find in favour of Dalriada and against the members. It was also clear that he had the full support of the judge. In fact, Moeran even went so far as to pretty much read out what our QC, Keith Bryant, would be arguing and told the judge what she ought to find against the case he would be putting forward. At some point, I wondered whether Moeran and the judge would be swapping places.

Moeran talked about the methods and costs of taking recovery action against the Ark members. He itemised three issues to take into consideration:

Merits of taking recovery action

Cost vs benefit of taking recovery action

Consequences of not taking recovery action

He then went on to report that Dalriada had 144 signed Standstill agreements and said that Dalriada was intending spending £2,925 per member on court recovery action. The judge declared that that was on the low side as that cost could only happen if the claim was uncomplicated and resulted in a quick and easy repayment. She also said she was not confident that bankruptcy proceedings were necessarily appropriate.

She did, however, firmly declare that the Ark members had all shared the “mistaken belief” that the MPVA loans were valid, non-taxable and only repayable by the end of the originally-agreed loan term. She broke this “mistaken belief” down into four points:

The members’ “mistaken beliefs”:

The trustees had the power to make the loans

The loans were capable of being made valid

The trustee could transfer beneficial ownership of these monies

The loans were not unauthorised payments and would not trigger a tax charge

The judge appeared to consider that somehow the members had come to these conclusions all on their own. The reality was, of course, that this was exactly what they were told by Stephen Ward and the herd of introducers and advisers – including a couple of FCA-registered ones. But reality did not seem to concern either the judge or Moeran overly.

The last thing that Moeran said on Day One was to make reference to the revised Standstill agreement – the focus of which was to ensure that criminal proceedings are now taken against all those who were involved in defrauding the Ark victims. The judge read the document herself, giving us a welcome rest from listening to Moeran.

As the first day came to a close, I was beginning to wonder whether I had dreamed the fact that a High Court judge had clearly stated in the High Court that Ark had involved an abuse of members of the public. Her statement had been made in front of a dozen or more witnesses and she had then gone on to deny that she had ever said it in front of the same witnesses who all clearly heard her words. Moeran and the judge had both agreed the Ark sales documentation was false and yet I heard neither of them conclude spontaneously that criminal complaints were now essential.

DAY TWO

Moeran opened with: “We are in the process of agreeing six test cases at the First Tier Tribunal” in relation to the personal tax appeals resulting from HMRC’s treatment of the loans (whether repaid or not) as unauthorised payments. The judge questioned whether members put forward for this role might not be happy. Moeran confidently assured her that there had already been five volunteers. I am not aware that any of these purported volunteers have come from the Class Action. Also, at the last meeting that Mrs Goldsmith, Mr Walters (Salmon Enterprises) and I had with HMRC, we agreed two Ark test cases – one with a loan and one without. Moeran did not appear to be aware of this.

Skating quickly over the tax issue for the members – and studiously ignoring the fact that according to HMRC the tax will remain payable even if the MPVA loans are repaid – Moeran and the judge got back to pondering recovery measures. The judge expressed reservations about bankruptcy proceedings because she said that that would merely release members from liability to the scheme rather than help recovery.

Moeran and the judge then started to discuss which members might not be worth pursuing at all for a variety of reasons. Between them, they concluded that those with very small MPVA loans should be ignored and that they might also have to ignore those outside the jurisdiction of the UK. Moeran reported that there were four members in Northern Ireland; 22 in Scotland, 24 in the EU and four outside the EU – USA, Jersey, Bulgaria and Australia.

Neither Moeran nor the judge were sure whether Bulgaria was in the EU (in fact, of course, it is an EU member). The members and I having complained in the strongest possible terms about Moeran’s use of the term “beating the victims with a sharp stick” the previous day, Moeran then went on to publicly apologise for that statement. To be fair to him, he made a good job of the apology and I am sure that Mrs Goldsmith and other members present appreciated it.

I really don’t remember whether our QC said much or anything at all that day – if he did it was not very memorable, or perhaps I couldn’t hear him terribly well because he muttered apologetically and miserably rather than speaking in Moeran’s strident voice.

The MPVA loans were summarised thus:

50 members with loans between £5k and £9,999

124 members with loans between £10k and £19,999

132 members with loans between £20k and £44,999 (totalling £4m+)

40 members with loans of £50k upwards (totalling £3m+)

The judge opined that the bigger the loan, the bigger the original pension must have been, and therefore the wealthier the member was likely to be. She concluded that these would be the easiest targets for recovery.

Then the judge handed down her judgement. She summarised the claim by Dalriada for Beddoe relief (money to be taken from the members’ funds) for the recovery of the MPVA loans and also to challenge the scheme sanction charge in the Tax Tribunals. She approved both of these, but did not agree that Dalriada should use funds to help the members with their individual tax appeals.

She reported that 152 claims had been written to date and that 12 consent orders had been received. She declared that she believed the claims were strong but expressed reservation as to whether the members were in reality good for the money. She reminded the court that there were 138 members without loans and that Dalriada had a duty to protect their position by recovering loans from as many of the other 348 members as possible.

She determined that it was appropriate that the trustees should be granted the relief they sought – albeit not the entire amount sought. She advised Dalriada to take stock of each individual situation and use their discretion as to whether it was appropriate to continue with the action. She also urged them to take into account relevant factors including the aggressive stance being taken by HMRC and to act as a reasonable trustee.

Finally, she said Dalriada should bear in mind that the individual cost of recovery per member would rise from £2.9k to £3.6k (plus VAT) if bankruptcy proceedings were issued and that those with the very smallest loans ought not to be pursued because of the disproportionate cost of doing do. She said it was difficult to decide where exactly the “watermark” might be and reiterated that bankruptcy might not be appropriate and should not be the first refuge sought and could be used as a “second string to their bow”. She suggested that further directions might need to be sought by Dalriada.

Regarding the scheme sanction tax charge appeal matter, she said it was appropriate to give the relief sought and for Dalriada to take steps to challenge the assessments. She recommended a “ceiling” on the amount to be spent and said that to challenge the £4m in tax sought by HMRC, the amount of £350k + VAT was appropriate.

On the question of paying a further £50k to fund legal representations for members against personal tax assessments, she recommended that the scheme sanction charge and the personal tax appeals should be coordinated. But she expressed a reservation about granting this relief to Dalriada as she felt it was excessive “because of the vagueness of what might take place”. She did not consider that for them to pay a barrister was necessarily a reasonable step to take. Therefore, she did not grant the relief sought.

In summary, therefore, the judge’s determination was as follows:

Yes to recovering the MPVA loans from as many of the members as possible/practicable

Yes to paying for the recovery costs out of the members’ funds – at the ideal rate of £2.9k + VAT per member (possibly rising to £3.6k + VAT per member if bankruptcy proceedings were issued)

Yes to taking £350k + VAT out of the members’ funds to pay for the appeal against the scheme sanction charge

No to paying £50k + VAT towards the members’ personal tax liability appeals

At the start of the proceedings, Moeran had reminded the court that Dalriada, as the trustee, already had the legal right to recover the loans if they chose to. But they were seeking the necessary relief and directions to do so from the court to protect their position.

DAY THREE

The final day was all about the nitty gritty of how the recovery costs should be apportioned between the six schemes. Moeran and Bryant put forward different suggestions as to whether this should be done on the basis of the value of the assets or the value of the MPVA loans within each scheme, and whether this should be done equally or on a pro rata basis.

The members at the back of the court were by now numb and none of them really paid much attention to what was basically “housekeeping” in terms of internal accounting procedures by Dalriada. One of the judge’s last points seemed to be that Dalriada should take all and any reasonable steps to recover the MPVA loans – but that the only question was what was reasonable. She cautioned that some options should not be taken, but stopped short of saying what they were.

In the famous poem extolling Victorian virtues – Kipling advises: “if you can watch the things you gave your life to, broken, and stoop and build ’em up with worn-out tools, you’ll be a man my son!”

Investment Fraud Victims’ Group Action and Task Force:

“Fighting Investment Fraud – Supporting Victims”

What Kipling did not take into consideration was that today’s investment fraud victims are punished by HMRC while the fraudsters escape prosecution and are simply left to continue re-offending. Therefore, the victims cannot afford to build up their life savings again because they have to pay crippling tax liabilities to HMRC.

Summary

The Investment Fraud Victims Group Action and Task Force aims to unite investment fraud victims, industry experts, lawyers and politicians to tackle the serious and growing problem of Investment Fraud.

We aim to raise awareness of this all too often overlooked crime and to campaign for positive reform. We advocate victims’ rights.

We are campaigning for a change in the law. Our fair tax treatment for fraud victims campaign aims to encourage the investigation of Investment Fraud and to introduce tax exemptions for victims which are astonishingly currently not in place.

We are forming a professional, influential and passionate Task Force to research and investigate this issue and make sound, sensible and workable recommendations to Parliament which we hope will result in positive legislative reform.

IF Task Force

Members of the Task Force are being appointed to help highlight the flaws and weaknesses in the current system which allows investment fraud to proliferate, leaves victims at the mercy of HMRC and also leaves the perpetrators free to commit further crimes and ruin further lives.

Task Force Agenda

A summary of a large cross-section of victims will be analysed by the Task Force. The results of this survey, including stories and case studies of our members, the financial damage summarised, the scams and scammers which have ruined so many lives and the impact and working practice of the current system and laws on the victims will be compiled into a report.

The Task Force will then consider the results and make recommendations to the government based on their research. The recommendation report will be circulated to the press, government, regulators and police authorities in the UK and also in other key jurisdictions involved.

We aim to achieve positive reform by parading the problem that the current status quo is unacceptable and highly damaging to our society on a number of levels.

The Campaign

Investigate the Fraudsters and Stop punishing the Victims

Fair Tax Laws for Investment Fraud Victims

UK tax laws currently unfairly penalise investment fraud victims who are suffering onerous tax liabilities for the actions of criminals who in turn are largely escaping investigation or punishment.

Our outdated and unfair legislation needs to be brought in line with other countries which tackle this issue head on and in a manner which avoids anomalous and unjust results.

The Cause

Investment Fraud is a very serious and growing problem. It is a disgraceful and unacceptable fact that individuals become victims of investment fraud every day. Victims have nowhere to turn as the police, regulators and government do nothing to stem the tide of this widespread, international crime. Many victims make reports to Action Fraud but no action is taken. Not even serving police officers themselves who have been defrauded can get criminal investigations launched.

Investment fraud impacts a huge number of people each year across a broad range of financial products and markets. According to reports, more than 5 million people a year in the U.K. are victims of scams and one in ten people in the UK have fallen victim to investment fraud in the past five years. This is costing in excess of £6 billion every year.

Fraud is now the UK’s most prevalent crime. Fraud and online crimes make up almost half of UK’s 11.8m total financial losses to financial criminals.

Since the new pension freedoms were introduced in April 2015, giving over-55s access to their entire pension fund, there has been an explosion of fraudulent investments in the UK. Billions of pounds of “unlocked” pension cash is a golden opportunity for con artists.

Raising awareness of Investment Fraud and encouraging the regulators, HMRC, police forces and the government to tackle Investment Fraud prevention

The current laws and system are unfair and unjust. HMRC pursue victims rather than perpetrators for tax liabilities. This does not happen in other countries like the US, as exemptions are available there for fraud victims.

Many victims of fraud, who have been mis-sold investment and pension schemes are being aggressively pursued by HM Revenue and Customs for resulting tax liabilities. Many victims have not made much, if any, financial gain and in most cases have actually lost funds, with some being very large sums. In contrast, those perpetrating the fraud, have made huge amounts of profit at the expense of the victims – much or all of which is not declared for tax purposes.

Calling on the Government to introduce a tax exemption for victims of fraud in respect of liabilities arising as a result of investment fraud

Few crimes are being investigated or prosecuted in this area – the fraudsters are escaping penalty whilst the victims are penalised. Investment fraud is a “Cinderella Crime”: in the shadows and overlooked, with the chances of prosecution of the perpetrators being minuscule.

Countless victims who have reported incidents to Action Fraud (the government’s designated facility for dealing with such matters) have been told that no action will be taken, despite very costly and devastating crimes having been committed against them.

In practice, when complaints are filed victims typically wait six weeks or more before their case is passed on to another police department to investigate. This gives criminals plenty of time to move money offshore, escape and continue to trick other savers, often under a different guise.

Those who defraud investors in the UK often suffer little more than a slap on the wrist. Police are often unwilling to investigate allegations of complex financial crimes, especially when cases involve smaller financial frauds that don’t attract media attention.

Even if the police do manage to tackle more fraud cases, Crown prosecutors need to make the issue a higher priority in order to put more fraudsters in jail.

Sentences for defrauding the public are non-existent or feeble – while sentences for defrauding HMRC are much more appropriate (e.g. eight years for the directors of pension trustees Tudor Capital Management).

In the US, fraudster Bernie Madoff revived a sentence of 150 years in prison – a sentence usually reserved for serial killers, such was the recognition of the devastation he had caused and the abuse of trust. In the U.K., prison sentences are rarely more than a few years. This is little deterrence to the unscrupulous fraudsters who stand to gain millions of pounds from conning investors

Fraud victims are also often reluctant to come forward. Some refuse to believe they have been swindled, and others are so embarrassed they can’t bring themselves to tell a spouse, let alone a police officer. The stigma needs to be broken and victims encouraged and supported in coming forward.

The double injustice of failures to investigate coupled with tax laws that penalise the victims has led to the suicide of good, honest, hardworking taxpayers, multiple families losing their homes, welfare issues, depression and family breakdowns. This is completely unacceptable and the law must be changed immediately to stop this devastating double victimisation

Investment fraud victims have already committed suicide over this issue – and more are still contemplating suicide as they contemplate the loss of everything they have ever worked for.

The victims’ lives are changed forever; savings and pensions which have taken a lifetime to accumulate can be gone in an instant. Victims may have to delay or even cancel retirement if they are defrauded out of their pensions or life savings.

Multiple victims have lost their family homes and some face homelessness. Fraud doesn’t just affect the victim. It affects a whole family. Partners need to take on extra jobs and victims may struggle to pay for food or clothing for their children.

Despite the complexity of the frauds committed, victims often feel blamed for having been defrauded. Many victims say they feel panic, anger, fear, anxiety, shame and guilty themselves after being defrauded.

Fraud can undermine the victims’ self confidence and make them feel that they are incapable of running their day to day life. Some victims report feeling vulnerable, lonely, violated and depressed. In the most extreme cases, suicidal, as a result of the fraud they experienced. These emotional and psychological impacts relate to both the stress of financial loss and the HMRC liabilities they are now facing following the fraud.

Investment Fraud is a devastating breach of trust. The experience was also reported to have affected relationships with others, making it difficult for victims to trust anyone again.

Victims are losing faith in the government and systems that should be protecting them rather than penalising them. Whether it is direct or indirect, investment fraud’s effects are profound – financially, emotionally and psychologically.

What needs to change?

Our laws and systems MUST be reformed. They are broken and unjustly penalise the wrong parties. This is a problem that will affect more and more hardworking families throughout the UK and offshore as fraud levels continue to rise.

More must be done to raise awareness of this growing area of criminal activity and preventative measures taken. HMRC must exercise their discretion against fraud victims more sensitively until the law is changed and stop enforcing liabilities against victims in cases where fraud can be proven.

The law must be changed to introduce a fair and robust system of tax exemptions for fraud victims to align our treatment of fraud victims with other countries

Investment Fraud must become a priority policing issue. There must be increased priority given to investigating and prosecuting Investment Fraud. Investment Fraud must no longer be a “Cinderella Crime” – in the shadows and overlooked.

Criminal sentences must reflect the impact and devastation caused by investment fraud. Tougher penalties for the perpetrators must send out a ZERO TOLERANCE to this iniquitous crime.

Holborn Assets’ Bob Parker needs a bit of help with his ‘rithmetic

Holborn Assets has been trying to calculate how much victim Glynis Broadfoot is due in compensation for loss to her pension fund invested by them for the past five years. But it is an uphill struggle and I am not entirely sure that poor old Bob Parker hasn’t either lost his marbles altogether, or never actually did maths in the first place. Either way I’ve decided to buy him a new calculator.

Let’s look at the maths – they are quite straightforward. When Holborn Assets first approached Mrs. Broadfoot, they promised her a “free” pension transfer from her final salary scheme with her local authority employer into a QROPS with Gower Pensions. They assured her this was in her best interests.

Five years and thousands of sleepless nights later, Mrs. Broadfoot has watched the value of her pension fund sink relentlessly while Holborn Assets has showed not a drop of concern and even refused to talk to her about it. They have said “the case is closed”.

To give them their due, Holborn Assets has now at last started coming to the table and have been making offers of compensation for Mrs. Braodfoot’s losses. They started at thruppence and have now upped their offer to £35,000. But let’s have a look at the maths:

Original cash equivalent transfer = £195,105

Actual transfer = £146,379

Big chunk of money inexplicably got lost = £48,726

At a cautious low-risk growth of 4% per year, pension should now be worth £178,000

But Mrs. Broadfoot has £106,730 left of her pension thanks to Holborn Assets

So, even forgetting the £48k that Holborn “lost”, Mrs. Broadfoot needs £71,270 to put her back to where she should be. And then there is compensation for the damage this has done to her health for five years.

So come on Bob, do the maths! We all know Paul Reynolds is making you a fortune so you can afford to pay proper compensation to your victim.

And another thing, Holborn Assets is using cold-calling scammers in Manchester to sign up more victims. Here in Spain, the leads generated by this scam are followed up by Holborn Assets salesman Jason Ryder who purports to have an office in Barcelona and another one in Marbella.

Just hope it is not bank of Dunlop!

Now, come on Uncle Bob, you know Holborn Assets has no license to operate in Spain or provide financial, pension or investment advice here. That is how Mrs. Broadfoot got scammed in the first place and lost such a huge chunk of her pension. So cold calling, scamming, destroying pensions, offering derisory compensation, ignoring a victim’s pleas for help…..not very nice. Get your chequebook out mate!

Finally, how is Paul Reynolds doing? I met him at your office in 2015 you know. He is quite handsome. I hear he is your best salesmen which is why you won’t get rid of him – he is making you so much money.

And what about your 40+ other “consultants”? Don’t any of them care about your firm’s professional reputation?

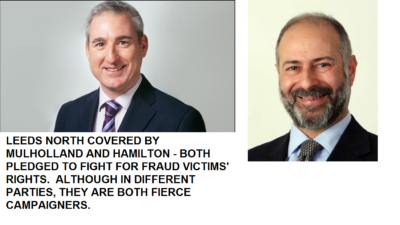

It takes balls to stand as a parliamentary candidate. It takes even bigger balls (or cojones as they say here in Spain) to champion a thorny cause and table an early day motion.Please vote for Greg if you are in Leeds North West. If you are in another constituency, please post and re-post this; tell any of your friends, relatives, colleagues, customers or bosses to vote for Greg. I would vote for him irrespective of whether he was Labour, Tory, Lib Dem or Monster Raving Looney Party.

If you are a victim of a pension or investment scam, you should be aware that Greg has championed the cause of victims and was one of the very few MPs who was ever prepared to put his head above the parapet and openly parade this problem.

Greg has a long history of championing victims and has actively campaigned against a number of issues involving injustice.

Mulholland’s EDM just before parliament was dissolved

Greg has tabled Early Day Motions on various subjects including support for small breweries, winter fuel payments for the severely disabled under 60, and biometric data collection in schools. He has spoken on dementia during a Health Hotel session at the 2009 Liberal Democrat Party Conference.

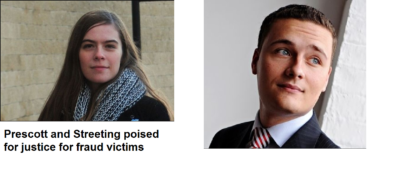

Two more champions for the fraud victims

Before the dissolution of Parliament, MPs Fabian Hamilton and Beth Prescott supported the motion and pledged to get involved in the campaign against pension and investment fraud if they were elected. Labour MP Wes Streeting has been involved in the Ark Class Action for some years and has a large number of victims of pension scams in his constituency.

It is rare for me to say nothing. On this occasion, STM Group has stated they are going to stick their heads in the sand and zip their lips. They have facilitated a financial crime…….OK, enough said. For now. I will leave it to STM Group/Fidecs to decide what goes into this blog. They have until close of play tomorrow, Friday 26th May. Then we can either deal with this discreetly and privately – or we can do it all publicly. With every sordid detail exposed in the public domain, to the regulators, the police (who are already investigating, with victims making their reports to the Serious Fraud Office) and the press. And, of course, the Stock Market. Your call STM. Silence is not golden. It is distinctly brown. Get your lawyers to talk to me if you want, but let these victims have some answers if you have any conscience.

This story was first published by International Investment journalist Helen Burgraff on 22.5.17 and heralds a welcome start to the much-needed initiative to bring pension scammers to justice.

Unfortunately, the pension landscape – both in the UK and offshore – is no better now than in the days of the Wild West. Back then, first the Sheriff’s Fraud Officer had to catch his horse; check the horse wasn’t lame; saddle up; then whistle for his tame injun to help him track the thief. Finally, once his water bottle was filled, the brave sheriff set off with his companion, Raging Bull, by around lunch time. Usually, they had tracked the thief down drinking whisky in a saloon by tea time, and after a dusty skirmish, he was thrown in jail by supper time.

Almost exactly two years ago, on 27.5.2015, the Insolvency Service published a witness statement on the £120 million Store First fraud which saw more than 1,000 victims lose their pensions and gain tax liabilities. The statement clearly named 18 scammers involved in these cases – many of whom had been visited at their offices. And yet, not a single one of these criminals was prosecuted or jailed.

Of course the blooming obvious happened – all the scammers went on to operate further scams and ruin thousands more victims’ lives. The cold calling firm, Nunn McCreesh, went on to operate the toxic UCIS fund, Blackmore Global; many of the cold callers upgraded their operations to “introducers” and the Ginger Scammer promoted himself to fund investment manager in the Trafalgar Multi Asset Fund (£21 million now suspended).

Whatever all the rest of the scammers are doing, it won’t be making good the damage they caused back in 2012/13. And Group First is now launching a new Park First car park at Luton Airport. Doubtless there will be healthy investment introduction commissions for the scammers to con hundreds of investors and pension savers into losing their life savings. Perhaps Toby will name this new venture “Lootin’ Airport”.

Meanwhile, I have discovered one of the advantages of having police officers among the members of the Pension Life Groups. You get the benefit of a wee bit of inside information and I hear that a bunch of the scammers have been arrested. About time!

Meanwhile, the Ginger Scammer’s lawyer is complaining about an image on the Pension Life website. Trouble is, I can’t work out which one it is – I’ve searched and searched and I can’t find a single offensive photo. But then what is offensive to one person is inoffensive to another. I called the Ginger Scammer’s lawyer a “dick” once – maybe it should have been “tick”.

There is growing concern about Peter Moat and Sara Moat of Fast Pensions. There have been a number of Pensions Ombudsman’s determinations which expressed concerns about the maladministration of the unlicensed firm owned/run by the Moats.

One of these was reported by FT Adviser on 10th May 2017:

The article stated the Pensions Ombudsman had told Fast Pensions it must pay out a death benefit to the widow of a former client after the company was accused of purposely delaying payments and quoted the Ombudsman as saying: “We have dealt with a number of other cases recently involving Fast Pensions, where there have been continued failures to respond to requests.”

The Ombudsman went on to cite delays and maladministration on the part of Fast Pensions which caused much distress and inconvenience to the complainant. Apparently, Fast Pensions has failed to comment and Karen Johnston, Deputy Pensions Ombudsman, has said: “We have dealt with a number of other cases recently involving Fast Pensions, where there have been continued failures to respond to requests and payment/transfer applications. Fast Pensions has also failed to communicate effectively with this office.”

A number of very distressed and worried members of the Fast Pensions scheme have contacted me and asked me to help them find out why they can’t transfer their pensions out (as is their statutory right). I filled in the contact form on the Fast Pensions website (there was no address, email or contact number on the site) and was contacted by James Porter. He told me that after some administrative problems in 2016, he had been appointed in January 2017 to look after the pension queries for Fast Pensions.

He also said he was dealing with all the members and the Ombudsman. However, the members have claimed Porter takes days to respond and that Fast Pensions have failed to pay compensation they were awarded and to facilitate transfers out.

CONTACT DETAILS

Porter’s email address is james.porter@fastpensions.co.uk and Fast Pensions have just changed their postal address from PO Box 4385 08121954: Companies House Default Address Cardiff CF14 8LH to Crown House 27 Old Gloucester Street London WC1N 3AX on 18 May 2017. This is a virtual office with thousands of companies registered there and nowhere near where Porter appears to be based in Manchester or where Moat is based in Javea, Alicante, Spain. There is nothing wrong with using a virtual address – I use a UK one myself as I am resident in Spain. But then I don’t run a pension scheme and the members suspect – perfectly understandably – there has been a deliberate attempt to make it difficult to contact anyone at Fast Pensions.

When we spoke a week or so ago, Porter – a very personable gentleman – assured me he was dealing with everything assiduously and that there would soon be a contact number and address so that worried members could contact the company. He told me there were about 400 members in total and he reassured me that the assets of the schemes were unregulated long-term loans held within bonds. What I relief! He said he would be sending out a newsletter to update all those who are so anxious to know whether their pensions are safe and are desperate for news as to when they can transfer out. Unsurprisingly, nobody has any confidence in the custodianship of their pensions.

There are a few worrying things about Fast Pensions – apart from the various Ombudsman’s determinations, the numerous worried members and reports of liberation and tax demands – and that is that Sara Moat resigned as a director on 17.3.17 and then a Sara Grace Moat (with the same date of birth) was appointed as a director on 6.4.17. Sara, or Sara Grace, is also director of Fast Enrolment of Gilbert Wakefield House Bewsey Street Warrington WA2 7JQ.

Would you buy a second-hand house from the Moats?

Peter Daniel Moat and Sara Grace Moat have been involved in a string of businesses called Blu somethingsomething… Blu Debt, Blu Property, Blu Property Group, Blu Financial Services of Cinnamon House, Cinnamon Park, Crab Lane, Fearnhead, Warrington WA2 0XP etc. As director of Blu Debt, Peter Moat introduced one victim to Stephen Ward’s Ark pension scam – and charged him £500 for “advice”.

The Moats also have a business in Javea called DEYSE INVESTMENTS SL plus Blu Holding Group, Desinplot, Desysins, Deysecomunic, Deyserents, El Arenal de Deyse, Property Exchange. I feel exhausted just thinking about running so many businesses and think I can understand why Fast Pensions has not received the attention it deserves when the Moats have so many other ventures – all based in Javea, Spain. The address for some of these businesses is Avenida la Llibertat 31, Javea 03730, Alicante. But who knows – it could equally be somewhere in Moraira at Stephen Ward’s office, or at LettersRUs next to Barclays Bank.

I have asked James Porter who the trustees are and for a complete schedule of the scheme assets. Many of the members suspect that Mr. Porter is actually Peter Moat. If this is true, then it is hard to understand why he would hide behind his pregnant wife. When their baby is born – and I do of course wish them well – I hope they will be more decisive about names than Sara Moat is with her directorships on Companies House.

Meanwhile, there are 400 people worried sick about their pensions. And I am concerned that the track record which is in the public domain in both the UK and Spain does not inspire confidence – neither does the Moats’ inability to spell the word “blue”. Further, the fact that the underlying assets of the scheme are unregulated loans and that the trustees are an unknown entity.

Nice as James Porter was when we spoke by phone, and sincere/reassuring as he sounded, I am afraid this has undeniably got all the hallmarks of a typical, bog standard scam. It looks, sounds, feels, smells like a scam. The victims are not stupid. Neither is the Pensions Ombudsman. The jury is out on the Pensions Regulator. I still wish and hope that it is not a scam and that the victims will be able to safely transfer out their pensions and receive their awarded compensation without further delay.

THE PENSION LIFE TICK CAMPAIGN: now that Andrew Warwick-Thompson, Executive Director for Regulatory Policy at the Pensions Regulator is joining LGPS Central as CEO, it is time for him to help us to ensure all negligent ceding providers compensate their victims. No doubt Andrew will engage enthusiastically with this campaign and lead by example.

tPR Chair David Norgrove stated on 13.7.2010:

“Any administrator who simply ticks a box and allows the transfer, post July 2010, is failing in their duty as a trustee and as such are liable to compensate the beneficiary.”

But on 29.12.2010, LGPS simply ticked a box, failed in their duty as a trustee, handed over a nurse’s pension to a bogus occupational scheme operating pension liberation, and is now liable to compensate her for her losses. The victim in question, Mrs. G, will be in the High Court as Representative Beneficiary of the Ark schemes to challenge Dalriada Trustees’ application to recover the loans on 19.6.2017.

Although LGPS did indeed perform badly in the case of Ark – handing over many thousands of pounds’ worth of pensions – the worst performing personal pension provider was Standard Life (by a mile). And Standard Life have rejected all the complaints made by their victims and refused to compensate them for their losses due to Standard Life’s failings.

STANDARD LIFE

The 2016 Report states: “During 2016 we engaged directly with our customers, investors and employees to review our strategy and ensure we continue to focus on the right areas. We asked these stakeholders to provide their views on what is important to them across our four sustainability priorities. This review highlighted a number of areas that matter most to our stakeholders including trust and transparency, governance, sustainable economic growth, cyber-crime, climate change, responsible stewardship, financial inclusion and decent work and pay. This input will also help focus our activity in 2017 and beyond.

If Standard Life are going to claim transparency and want customers to trust them, they have to prove they are capable of responsible stewardship. Handing over millions of pounds worth of pensions to obvious scammers neither inspires trust nor evidences responsible stewardship.

Standard Life declared a profit of £723 million in 2016 – after paying its four directors salaries in excess of £10.8 million – 40% of which was in bonuses. It is ridiculous, offensive and disgusting for Standard Life to fail to compensate the victims of fraud who are facing financial ruin due to Standard Life’s own failings.

There are only three questions to ask about Standard Life’s obligation to compensate its victims:

Did Standard Life simply tick a box and allow a transfer? TICK

Did Standard Life fail in their duty as trustee? TICK

Are Standard Life liable to compensate their beneficiaries? TICK

Don’t use Standard Life until they compensate their victims. Don’t put money in the pockets of these negligent people who pay their directors obscene salaries and lie about their company’s ethics.

Gambling is a very strictly controlled industry – and rightly so. Every individual jurisdiction has its own gambling or casino licenses which are usually very expensive and onerous to obtain and keep. Where large amounts of cash change hands every minute, it is obviously important to impose strict conditions and ensure that regulations are complied with.

The city of Las Vegas sprang up in the middle of a desert in 1905 in the hottest part of the world and has since flourished into a sparkling and magnificent centre for world-class gambling.

In the words of Rudyard Kipling: “If you can make one heap of all your winnings, and risk it on one turn of pitch-and-toss, and lose, and start again at your beginnings, and never breathe a word about your loss…..you’ll be a man my son!”

Kipling’s advice is clearly aimed at someone young; someone who has years ahead of him to get lucky; recoup his losses; start again; do a phoenix; learn from his mistakes and do better next time. But with pensions, a life-time of savings can be wiped out so easily on “one turn of pitch-and-toss” by entrusting an unlicensed adviser.

Here in Spain, the investment regulator – the CNMV – refers to unlicensed pensions and investments advisers as “chiringuitos” (which translates as “bar flies”). The CNMV helpfully publishes a well-written warning booklet to alert the public to the nefarious tactics of these scoundrels – copied below for the information of the gentle reader. However, in Britain we tend to be rather more direct and call them scammers. And Lesley Titcomb of the Pensions Regulator has come right out and said it: “scammers are criminals”.

So, make sure you only use an advisory firm which is licensed to provide pension and investment advice. And avoid the chiringuitos, scammers and criminals. I have no idea who the jolly pair of gamblers are in the photo on this blog, but I am sure no informed person would entrust them with a pension and I reckon Kipling would have had a thing or two to say about them.

Away from the fun fun fun of Vegas, these two amiable-looking scallywags could probably scrub up and look like respectable independent financial advisers with a business-like suit and a leather portfolio full of impressive documentation about funds with imaginative names such as “Symphony” and “Blackmore Global”. But if they did so without a license, they would be criminals.

SPANISH REGULATOR’S (CNMV) GUIDE (translated)

FINANCIAL CHIRINGUITOS (“IFA” FLY BOYS/SCAMMERS)

“CHIRINGUITOS” means entities offering and providing pensions/investment and advisory services without being authorized to do so. They are dangerous because in most cases the apparent provision of such services is just a cover for fooling victims into believing they are making a highly profitable investment. It is important to understand that high yields offered are often too good to be true: the bait to con ill-informed (naïve) investors to hand over their savings or pensions. When exposed, the “CHIRINGUITOS” simply disappear or change their names. They are simply swindlers.

Companies authorized to provide investment services (brokers, portfolio managers, IFAs, banks etc.) are subject to the rules governing the securities markets and strict controls by the supervisory bodies (CNMV and BanK of Spain). Only CNMV-registered companies are authorized to provide pension/investment services, after demonstrating compliance with specific legal requirements and standards.

CHIRINGUITOS are not attached to the Investment Guarantee Fund, so that investors are not protected in the event of insolvency of the entity (authorized entities contribute to these protection funds through compulsory subscriptions).

There is no particular type of victim because often scams are very elaborate. Victims can be small businesses, individuals or professionals who fall for credible-sounding false promises of quick wealth and easy gains.

In short, to trust a CHIRINGUITO is a sure way to lose capital, with no investor protection under the laws. How CHIRINGUITOS work

The channels used by scammers and boiler rooms to contact potential victims are no different from those that can be used legally by legitimate entities i.e. telephone, letters, e-mail, web pages etc. The difference lies in the way the scammers use these channels, the type of messages they convey and the general approach to achieving their goals.

The CHIRINGUITOS use databases (often obtained fraudulently) of people who, for example, have purchased a particular financial product, publication – or on occasion answered a survey about their tastes, interests and financial situation. Phone calls

Cold calling is one of the CHIRINGUITOS’ favourite contact methods. It allows them to directly exercise psychological pressure techniques. Cold calling is by definition unexpected but is legal, and in fact authorized entities often use it as part of their promotional campaigns. However, in the case of authorized entities, it is normal practice to call existing customers, so people know their data has been obtained legitimately. If the answer to what is being offered is “no” this is accepted politely. By contrast, the CHIRINGUITOS do not usually settle for a NO.

Mail

High-quality leaflets which are sophisticated, inviting and promising. These often request the recipients to contact them by filling out a form, calling by phone or by visiting their website. Internet, e-mail

The great success of the Internet as a direct marketing tool allows advertisers to access a wide mass of recipients more cheaply than traditional media (phone, mail). This fact, coupled with the possibility of anonymity, has led to abuse of the medium, such as spam or indiscriminate emailing of unsolicited products bordering on illegality. Recipient lists are often obtained unlawfully, in breach of data protection rules. Also, the address of origin of the messages are usually false, and also the subject headings are deliberately misleading. Spanish law decrees that commercial communications should be identified as such and prohibits sending emails unless they have previously been requested or expressly authorized by the recipient. No serious company would ever spam the public, as that would be invading consumer privacy.

When it comes to financial products and services, we must be very cautious about offers and information received, even if they have been requested or consented to. Financial fraud on the Internet can be carried out by more sophisticated means. Spam is just one of the possible mechanisms, because the Internet offers various tools to disseminate potentially fraudulent or questionable deals: boards, newsgroups, chats, or even sophisticated web pages.

Phishing

Another danger is “phishing”: emails that appear to come from legitimate financial institutions, which request personal passwords. These messages often lead to a website that imitates an authentic entity (although it may have spelling mistakes), which fools people into entering their personal data or passwords.

Pharming

Even more sophisticated is “pharming”: people who visit fraudulently-cloned websites can have their personal, confidential data collected by criminals. Never surrender personal or confidential business information to unknown persons. If a request for personal data appears legitimate, use an established phone number to double check. Also, don’t access websites via links, but type in the full URL and, if possible, install antiphishing and antipharming tools. Adverts

CHIRINGUITOS also advertise in newspapers, magazines or other media (such as television teletext) to offer opportunities which are much more attractive than traditional investments and promising to provide attractive opportunities (which, of course, are not so in reality).

Personal referrals

It is common for people to make their investment decisions based on recommendations from acquaintances or relatives whom they trust. Knowing this, sometimes the CHIRINGUITOS pay great benefits to the first customers, using their own money or from other investors; this is what is called a Ponzi scheme. In fact, those investors who unwittingly act as bait are only going to get limited performance at first and successive investments begin to generate losses. Then, the company will not respond to requests for repayment of capital and finally disappear with all the money invested.

Personalized investment recommendations should always be made by a professional entity authorized to do so, because what is good for one investor may not be for another, depending on their different personal and financial circumstances. Persuasion techniques

The list of boiler-room persuasion techniques cannot be exhaustive, since the arguments and methods are increasingly sophisticated. Therefore it is important to stay alert to any financial offer that is not from a known, registered party. Accurate predictions

A simple but very effective technique – using a large number of calls to impress potential victims with their knowledge of financial markets – half of which confidently predict the rise of a certain investment value and the other half predicting decrease of the same value. In the following days this exercise is repeated several time. Those targets who were given a series of successful predictions are contacted again. Now convinced of the infallibility of a company that has hit all its forecasts for several consecutive days, these people are willing to surrender their savings to the CHIRINGUITOS. Appearance of respectability and success

CHIRINGUITOS know it is essential to look respectable and seem like financial market experts. So they dress smartly and elegantly and rent luxury offices. Sometimes it is difficult to get an appointment to meet them because they want to give the impression of being busy and in high demand. Incomprehensible explanations and use of technical jargon

CHIRINGUITOS promoting fraudulent investments talk with confidence and mastery of technicalities that make them look like experts on the subject. In fact, the aim is that the potential victim does not understand anything and chooses to trust those who seem to be experts who know what they are talking about. Offering large profits with little risk

CHIRINGUITOS promise much higher returns than can be obtained from a conventional investment with minimal risk. A basic principle that all investors should bear in mind is that profitability and risk go together inseparably. The possibility of obtaining high yields always involves taking high risks. Be wary of any offer that ensures high returns without risk. Insistence on an immediate decision

Urgency is a major factor, not only because they want to get their hands on your money asap and with the least possible effort, but because they know that if the investor has time to think properly about the offer, or seeks professional and reliable advice, he will probably reject the offer. So, CHIRINGUITOS use tricks aimed at achieving an immediate decision to try to convince the victim that they are offering a unique opportunity that will expire soon. Investors should be aware that this is not true: there is always time to assess the characteristics of a financial offer and to make sure it is suitable. Psychological pressure

The conversation, either by phone or by any other means, usually begins in a cordial fashion, but if the targeted victim shows some potential resistance the scammer can become more aggressive. This constitutes a fundamental difference between the CHIRINGUITOS and the authorized entities, who always respect a prospect’s right to not be interested.

Although psychological pressure can take many forms, here are some common tricks:

Not taking no for an answer

Being repeatedly insistent

Becoming increasingly aggressive

Questioning the intelligence or ability of the investor to make a decision

Conveying the idea they are doing the victim a big favor by offering exceptional gains

Making it clear it would be absurd to question the promises made

Using warnings such as: “you’ll regret it if you don’t go ahead” or “you’ll never get rich if you ignore my advice”

When to be suspicious of a financial offer

Most of the techniques used by CHIRINGUITOS would not be used by authorized firms, since they are subject to strict rules of conduct. Authorized firms are required to keep customers properly informed and to provide information to investors fairly and clearly. In particular, they must provide information about their services and financial instruments, so that the client knows the nature and risks of the investment service that it is going to provide and the characteristics and risks of financial instruments offered.

It is therefore important to understand the difference between people or entities who are authorized to provide investment services and those who only intend to carry out a scam. When an authorized firm sells a product, the customer must request information on their knowledge and experience in this product, in order to assess for himself whether it is suitable for him. This is called a suitability test.

When a broker is going to provide investment advice or manage an investment portfolio, in addition to asking about the client’s investment knowledge and experience, he should request additional information such as the financial situation and investment objectives of the client (risk profile, time-frame etc.) – as proper financial advice is always personalized.

The boiler room scammers’ only aim is to attract money from their victims, so they do not care about their clients’ expertise in investments and financial circumstances – all they need to know is that they are willing to invest. The contact must have been requested by the prospect

Authorised entities have to work with personal data in a legally-compliant manner, and the client must have given them permission to make commercial offers. But if an entity of which we have never heard contacted us to offer an investment, you have to take extra precautions because this is probably a scam. Authorized entities never pressurise customers

Any investment should be approached with sufficient knowledge of the characteristics and risks of the product. It is important to do thorough research before committing. The investor needs time to decide and get answers to all their questions. However, scammers pressure the victim to get an immediate yes, without giving them a chance to reflect. How to protect yourself against a possible CHIRINGUITO

Promises of exceptional returns without risk should make us suspicious immediately. Never trust an unknown entity until they have been able to verify that they are properly authorized to provide investment services. The investor has available the following protection mechanisms which should always be used before handing over capital:

Request information from the supervisory body, in this case the CNMV

Identify any peculiarities about the investment proposal

Demand concrete answers and make sure they are fully understood

Ask for information from the CNMV

The Investor Assistance Office of the CNMV is at your disposal to inform you whether entities are authorised to provide investment services or not. If you have been advised to deal with a company that has been referred/recommended, you should call the CNMV for assurance that it is an entity which is authorized, registered and supervised. Public records are also available through the website of the CNMV (www.cnmv.es). Investors can also visit the website of the International Organization of Securities Commissions IOSCO, (www.iosco.org) where there are warnings and advice available.

The CNMV regularly issues warnings about entities which are suspected of providing investment services without authorization. These warnings may come from the CNMV (when it is aware of the existence of possible CHIRINGUITOS through inquiries or complaints from investors) or which have been supplied by a foreign regulator (bear in mind that CHIRINGUITOS may operate their fraudulent activities in more than one country).

To make it easier for investors to identify entities operating without authorization, the website of the CNMV provides a search engine that can locate them quickly and easily. Entities that have not been placed on the warning list may not yet have been detected by the supervisory bodies. It is important to remember that although most of the victims of fraud contact the CNMV after losing their money, it is always preferable and much less expensive to conduct this consultation in advance, i.e. before handing any funds over.

Identify the characteristics of the proposal

Sometimes, the activities of the CHIRINGUITOS are masked under the guise of consulting services, in which in the client is charged a high commission on their investment (which also often adds to the total loss of the capital). However, all entities making personalized investment advice must be registered on a public registry, so that potential victims can see whether or not a firm or person is authorized to provide this service.

Generally, CHIRINGUITOS require funds to be transferred to a current account (sometimes abroad) on behalf of a non-Spanish company. In general, any offshore entities are not authorised or regulated. The investments tend to be complex financial products in unknown foreign markets.

There are often entities or websites that offer investors the opportunity to invest in foreign exchange derivative products (CFD, futures, rolling spot contracts etc.). The forex market (foreign exchange) is very complex, so any access to this should only be done by authorized entities.

Scammers are often reluctant to provide updated information or respond to questions from the investor, although they promise that they are offering a relationship based on mutual trust. But remember that trust is something that must be earned, the more so when it comes to giving your money to organizations or persons who have failed to establish their legality, professional integrity or solvency.

Insist that any adviser provides clear answers to questions. The investor not only has the right but also the duty to know in advance all relevant aspects of the proposed investment. One of the main differences between authorized financial institutions and CHIRINGUITOS is that the former invite investors to ask questions and then provide all necessary answers and information, while the scammers try to make their targets feel ignorant, and to trust them blindly.

Below are some questions to ask the advisers to see whether they are CHIRINGUITOS. In fact, many of these questions, particularly those relating to the characteristics and risks of the investment should also be made when dealing with authorized entities. The difference is that scammers will be unwilling to provide clear answers:

How did you get my name and contact details?

Why are you making contact with me?

Is your firm registered with the CNMV and the Bank of Spain?

Is your firm supervised by any public authority?

Are you a member of any investment protection/guarantee scheme?

How long have you been with the firm?

What is your professional experience?

Is there any financial entity which can give you or your firm a reference?

Does the investment you are proposing match my objectives and is it suitable for me?

What are the risks of this investment? How much could I lose and under what circumstances?

How would I profit from this investment?

What has to happen for the value of this investment to increase? (i.e. interest rate or stock market rises?)

For how long do I need to keep the investment?

What is the liquidity of the investment i.e. how and under what conditions can I get my capital back if I need it?

What commissions are payable? How are they calculated? Can I have a copy of the fees/rates?

Can I have a copy of the documents/contracts that I have to sign (to read carefully before signing them)?

Is there any official document regarding the investment at the CNMV regulator? Can I see it?

Can you give me a written detailed explanation of the investment to read/digest carefully and a second opinion?

Can we discuss the proposed investment with my lawyer or with a trusted financial expert?

If anything goes wrong with my investment, what avenues of redress or compensation do I have?

Just asking these questions is not enough. CHIRINGUITOS are expert at being persuasive and evading answering questions with plausible excuses. This is why it is essential to check out any person, firm or investment with the CNMV before handing over any funds.

Steve Pimlott of Windsor Pensions is still scamming people out of their pensions. And seeking new victims on LinkedIn. Inviting people to:

Transfer your frozen UK pensions to a QROPS

Still scamming after all these years

He will charge between 10% and 20% and will use forged documentation from an obscure QROPS such as Danica and BSEC and then fool the ceding provider into transferring a pension into a fraudulently-set-up bank account in a dodgy jurisdiction such as the Isle of Man.

Pimlott – who may also go by the name of Steve Derrick Pimlott – claims to have done many thousands of these transactions and states that only a couple of hundred people have ever got caught by HMRC. And even then, he says, as most of the people live offshore they ignore the tax demands of 55% on the amount liberated. HMRC’s version of events is somewhat different and tell me that in some cases Pimlott made off with the whole transfer and the victim never even got the 80% or 90% that was left.

Pimlott involved a firm allegedly called Insignia Financial Services in some of the cases. Although this gave some of the victims an illusion of respectability, the firm was in fact a clone of an FCA-registered entity.

Dozens of properties as opposed to Ward’s mere six

Pimlott is reportedly in Florida – not too far from Stephen Ward’s Indian Point holiday villa empire. Ward also told his victims to throw the tax demands in the bin. However, Pimlott’s property portfolio is considerably larger than Ward’s. If Pimlott is telling the truth about having done 5,000 liberations, then HMRC will be pretty busy. If we assume the average pension pot size was, say, £50,000 and Windsor Pensions charged 15% fees for each one, then Pimlott earned a cool £37.5 million. And herein lies the problem: while these scammers are earning such huge amounts of money, they are hardly likely to give it all up voluntarily.

I hark back to the Pensions Regulator’s Lesley Titcomb’s statement that “scammers are criminals”. Steve Pimlott and his associates are criminals. They need prosecuting, given maximum jail sentences and their assets confiscating. The industry needs to get behind this and support the pressure that must be put on law enforcement agencies in the UK, USA and beyond.

Ceding Pension Providers ignored warnings about scams