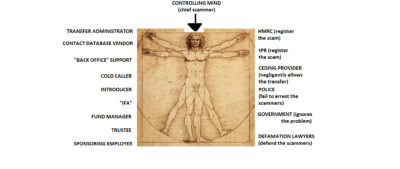

Pension scammers have a “code”. Rather like pirates, they are not to be trusted. They pick their words carefully, revealing little; they are sneaky and lack any morals. They are good at disguises and if they fear they may be rumbled, they will disappear over the horizon, never to be seen again. They certainly won’t hang around to help pick up the pieces after their victims have been ruined. Rest assured, they will take as much as they can get and show no remorse. Living the Life of Riley on your hard-earned money is their reward.

“Yo ho, yo, ho! A scammer’s life for me”.

Those of you who follow Pension Life, will know that we want to put a stop to pension scammers and are trying our hardest to get as much information as possible out to the public about how to avoid being scammed. We want to educate the masses and stop pension scammers worldwide.

Those of you who are new readers, may not be aware of how common pension and investment scams are, or how easily you could fall victim to a pension scam. But never fear, we have constructed a series of blogs, videos and cartoons for you to read and watch, so you can swot up on the dos and don’ts when it comes to safeguarding your precious pension fund.

This video has been constructed to show you the pension scammers’ code of conduct. By familiarising yourself with their techniques, you will be better prepared to spot the scammers and avoid falling victim to their schemes.

Please look through our archives and read about past scams, serial scammers and failures of the regulators and police to bring them to justice for their crimes. Make sure you know all there is to know about the evil and seemingly unstoppable world of pension scammers.

Above all, read the Trolley’s guide, and see how scammers learn their highly-profitable and destructive trade. Scammers learn from the best – including theauthor of this guide. And then they bring their own individual touch to the art of scamming.

Since 2010, £millions have been lost to pension scams, thousands of victims have lost their retirement savings, large-scale misery and poverty are the terrible results. One common factor connects many of these scams: one man – Stephen Ward.

Here at Pension Life we have made a video – based on the Mastermind quiz. Lessons must be learned from the dozens of scams, headed by Stephen Ward, which ruined thousands of lives and destroyed hundreds of millions of pounds’ worth of pensions.

Premier Pension Solutions, Stephen Ward’s company in Moraira on the Costa Blanca, was responsible for the Ark pension liberation scam. Ward had advised 160 victims to transfer £10m worth of secure pensions into this scheme on the promise of having 50% of their pensions paid to them in cash. 2011 saw the Pensions Regulator place the scheme in the hands of Dalriada Trustees. The High Court called the Ark scheme a “fraud on the power of investment”.

Ward then went on to his next scam: Evergreen New Zealand QROPS and the Marazion “loans”. The “sister company”, Continental Wealth Management, was running the cold-calling operation to lure victims in – and some of the CWM salesmen were hanging around outside supermarkets to try to trap people into this scam. When Evergreen was removed from the QROPS list, Ward continued to work with CWM. It is not known how many other Stephen Ward/Premier Pension Solutions scams CWM was involved in.

Mastermind – Stephen Ward

1. Who is the owner and director of the Spanish firm Premier Pension Solutions based in Moraira on the Costa Blanca in Spain?

Stephen Ward

2. In 2010, who was running road shows in the United Kingdom to promote the Ark pension liberation schemes and recruit introducers?

Stephen Ward

3. In the Ark pension scam, which operated in 2010/11, who was the biggest introducer with more than £10m worth of transfers?

Stephen Ward

4. Who is the author of the Tolley’s Pensions Taxation Manual described as an essential reference source for all tax practitioners?

Stephen Ward

5. Who administered the pension transfer administration in the Capita Oak scam which saw 300 victims lose £10m worth of pensions and is now under investigation by the Serious Fraud Office?

Stephen Ward

6. Who handled the pension transfer administration of the Westminster pension scam which saw 79 victims lose over £3.3 million pounds to worthless investments: now also under investigation by the Serious Fraud Office?

Stephen Ward

7. Who was the trustee for the London Quantum pension scheme now in the hands of Dalriada Trustees and invested in high-risk, illiquid investments such as Dolphin Trust which paid investment introduction commissions of up to 30%?

Stephen Ward

8. Which Level 6 qualified former pensions examiner and IFA in 2014 was famously quoted as saying: “The schemes with which we are involved are completely above board. The Ark thing is history now.”

Stephen Ward

9. Who was promoting the Elysian Fuels SIPPS liberation scheme which he described as allowing members to “trouser” most of their pension fund in cash?

Stephen Ward

10. Who was the owner of the loan company Marazion which operated pension liberation loans in the Evergreen QROPS scam which saw around 300 people lose £10 million worth of pension funds?

Continental Wealth Management (CWM) was a financial advisory firm based on the Costa Blanca in Spain. Headed up by Darren Kirby, there were – until earlier in 2017 – 35 people working at the firm. The firm claimed to have £50 million worth of assets under management and around 500 clients. The firm closed down on 29.9.2017.

It is feared that up to 40% of CWM’s clients may have been affected by this situation.

BACKGROUND TO CWM

CWM “advisers” acted as sharks

In mid-2011, Stephen Ward’s Premier Pension Solutions (PPS) lost the lucrative Ark pension liberation scam when the Pensions Regulator placed the scheme in the hands of Dalriada Trustees. Ward had advised 160 victims to transfer £10m worth of secure pensions into this scheme on the promise of having 50% of their pensions paid to them in cash. He also assured them these payments would not be repayable or taxable and that the pensions would be invested in “high-end London residential properties”.

In the event, neither of these assurances turned out to be true. Dalriada is now making claims to recover the 50% liberations and HMRC has issued tax demands at 55% of the cash received (and the tax will still be payable even if the liberations are repaid). The High Court called the Ark scheme a “fraud on the power of investment”.

Having ruined 160 lives, and made up to £1 million profit out of the Ark victims, Ward immediately turned his attention to his next scam: Evergreen New Zealand QROPS and his Marazion “loans”. Having seen how easily victims could be duped into transferring their safe pensions with the promise of 50% liberation, Ward appointed CWM as “introducers” to the scam.

Here is an actual account by one of the Evergreen/PPS/CWM victims of what happened to her:

Mrs. A: “I was first cold called by CWM in 2011. I first met Phil Kelman of CWM in January 2012. I was told only positive things about transferring my pensions and to be able to take 100% of my pension funds.

This, however, changed after the first meeting and I was then told that due to the government closing loopholes I would only be able to get 50% of my pension fund and that the other 50% would be in the Evergreen QROPS earning enough interest over the 5 years to cover the 50% that I could withdraw (before the age of 55) – a win win situation!

There was no mention of the 50% being given as a loan until much further down the line. This was supposed to have taken 6 weeks at the most, but it actually took nearly 10 months. I was told that the “loan application” was a paper exercise just to cover things – I obviously have no proof of these conversations! Due to the fact that in the beginning it was not a “loan” there was no talk of a 55% tax charge, also as it was QROPS I was told it wouldn’t have incurred a tax bill.

I was not given any opportunity to say what the consequences of losing my pension or gaining an extortionate tax bill would be – either in the short or long term. If I had known of the huge risk of losing everything then obviously I would not have gone ahead. I did not state that I was willing to risk everything to get the “loan”.

I was told that Evergreen was a safe place for my pension to be as Evergreen was “approved”. I was given a graph to show how my pension would not only make the 50% back up but make more on top of it.”

Marco Floreale – former CWM “adviser” – now MD of Carrick Wealth

Mrs. A’s case was handled by CWM’s Marco Floreale (now Managing Director of Carrick Wealth) who claimed to be the managing director of CWM. Her secure, final salary, £100k Royal Mail pension was transferred to Evergreen and she was forced to sign a five-year “lock in” before receiving her “loan”. The loan agreement issued by Stephen Ward included annual interest at 8.5% compound which would mean that her £50k loan would have increased to £75k at the end of the five-year term. She was also charged more than £10k in fees.

There are now around 300 victims trapped in Evergreen as they are not allowed to transfer out. Ever. Between them they have lost £10m worth of pensions. The CWM personnel involved in this scam claimed that PPS was their “sister” company and have offered no help or compensation for the victims’ losses and terrible distress. One victim died of cancer in February 2017 and her husband is convinced that the stress of the Evergreen situation brought on the disease.

Phil Kelman, Jon Meek, Robert Pearl, Gemma Broad and Anthony Downs were among the CWM personnel who assured the victims that the transfers were in their interests as well as safe and prudent. It was, of course, later discovered that the Evergreen fund was invested in illiquid, high-risk, toxic funds – including personal, unsecured loans. Evergreen was removed from the QROPS list in November 2012 and the victims have now been told they can never transfer out.

It is not known how many other Stephen Ward/Premier Pension Solutions scams CWM was involved in, but when Evergreen got shut down CWM started acting as “advisers” to British expats in Spain and France. They were still working with Stephen Ward of PPS who provided the transfer advice. It is now thought they advised more than 500 people and that around 40% of these have suffered crippling losses to their investments.

I do not know whether CWM ever disclosed their previous involvement with Stephen Ward’s scams to the clients – although it is doubtful that any people would have felt comfortable using CWM had they known they had been responsible for the 300 Evergreen victims. Certainly, CWM did not disclose their past activities to either Trafalgar International or Momentum Pensions – had they done so they would never have been given terms of business by either firm.

From 2013 onwards, CWM invested hundreds of low to medium risk clients’ investments in high-risk, illiquid assets. CWM completely ignored the suitability issue and paid no heed to the clients’ preference for safe, low-risk investments. Clients’ signatures were repeatedly copied and once the losses started to appear, CWM assured them that there was nothing to worry about and they were “only paper losses”.

When asked why so many clients were put into professional-investor-only investments, CWM replied that the investors themselves were not the clients; but the insurance companies were the clients. When I showed CWM evidence of forged signatures on dealing instructions several months ago, there was no response then and no further communication from them subsequently.

The most important thing now is the restitution of the victims’ funds. OMI, Trafalgar and Momentum Pensions, have come to the table to try to find a solution and restore of the victims’ pensions and investments. If we can achieve an equitable settlement, this will be a first in European financial services. However, the parties who have not come to the table are life offices Generali and SEB, as well as other pension trustees including Concept, Sovereign, Pantheon, Elmo and STM. It is no surprise that STM have not come to the table, because they pulled up the drawbridge in the Trafalgar Multi Asset Fund scam, run by XXXX XXXX – now under investigation by the Serious Fraud Office.

I would like to thank all the victims for their patience so far. But it has now finally run out – unsurprisingly. The mood has darkened and victims want action. A valuable information and commentary resource is the Repdigger forum. One interesting post recently reminded contributors that it was Stephen Ward of Premier Pension Solutions who provided the initial transfer advice. Nothing changes.

Every time I think this book about pension scams is done and I can put it away, a new scam or scammer pops up and I have to rethink it. And every time I add in a new sentence or paragraph, the formatting and pagination need to be adjusted. But, however imperfect and unfinished it may be, it is available on Amazon:

It has been much harder to write than I ever thought it would be. But nowhere near as hard as it is for the victims who have to live with the consequences of losing their pensions and investments – and gaining tax liabilities.

The purpose of this book is to warn the public against current scams and scammers (the same ones who have been doing it since 2010) and encourage the police and regulators to criminalise all forms of scams. The Pensions Regulator’s Lesley Titcombe has clearly stated that scammers are “criminals” and it is hoped they will all be prosecuted. The victims and the ethical members of the financial services industry want to see a zero-tolerance policy and a military-style campaign to stamp out this horrendous crime wave.

Evidence suggests that in the past seven years, there have been many £ billions lost to pension and investment scams – there are no precise “official” figures. But the dreadful fact is that the scammers who were targeting victims back in 2010, continued doing it in 2011; and 2012; and 2013; and 2014; and 2015, and 2016. And they are still doing it today. Happily and profitably. And nobody has stopped them or brought them to account for the horrific financial damage and distress they have caused.

It is hard to decide which is worse: the vicious, greedy, cold-hearted scammers or three sets of inept government or the feeble authorities who let them get away with it. Repeatedly. But it has to stop. A military-style, zero tolerance campaign has to be waged against all the guilty parties until every last one of them is brought to justice.

The tragic thing about these scams and the misery and financial ruin caused to so many thousands of victims is that this disaster was preventable. HMRC were warned by the industry about the potential for scams if the role of compulsory professional trustee was removed pre 2006. In a letter of March 2004 a specialist pension solicitor warned:

“It is essential that schemes offering self-administration and wide investment choice should have in place an independent person who has sufficient control of scheme assets to prevent abuse and sufficient knowledge and experience to know abuse when he sees it.

That does not necessarily mean that the system of pensioneer trustees should be retained in its current form but, if it is abolished without an effective replacement, we envisage that within the next 5 years the degree of abuse of such schemes by both incompetent and dishonest individuals will:

further stain the reputation of pensions generally; and

severely embarrass the government responsible for letting it happen.

Reputable professionals in the industry and the Government share a common aim of building a system of tax rules that is simple but is robust enough to last for a working lifetime without major overhaul. Such a system needs to contain adequate protections against abuse.”

The warning was ignored. And precisely what was predicted would happen, happened. And it will go on happening until and unless government, HMRC, regulators and police take responsibility for their failings and put in place robust measures to clean up the mess of the past/present and prevent future disasters.

This clear warning was brought to my attention by Martin Tilley who is director of technical services at Dentons Pension Management. Martin has written some excellent blogs and articles on the subject of pension scams and my favourite has to be this one:

I know the government is jolly busy at the moment with Brexit. But earlier this year there was a government consultation on pension scams – and still no word about what the battle plan is. In fact, neither Damian Green (Secretary of the DWP) nor Richard Harrington (Pensions Minister) will engage at the moment as they claim there is no point until after the consultation.

But they didn’t say how long after: three months? three years? With every day that they dither about, more victims will lose their life savings; more damage will be done to the reputation of the industry; more expensive will it become for the State to support those who have no retirement income; louder will be the ticking of the pension scam time bomb.

Richard Harrington recently stated that Britain can’t afford to implement transitional arrangements for 1950s-born women who weren’t notified their State pension age was going to be increased from 60 to 67. He reckons this would cost the country around £30 billion. With scams reportedly costing the British public £11 billion a year, the cost of supporting these thousands of victims throughout their retirement will be staggering. Plus the cost to the NHS (because of the amount of mental and physical health damaged caused by the stress of being scammed) will add to this enormous cost.

If you have read this blog from start to finish, it will have taken you seven minutes. During that time at least one person will have been scammed out of their life savings. If you read the Anatomy of a Pension Scam ebook from beginning to end, it could take you up to five hours if you read slowly and carefully. Think how many people could be scammed in that time. Avoidably.

The Scorpion Campaign was the Pensions Regulator’s attempt to warn the public and the industry against pension liberation scams. It wasn’t a bad try, but it failed. It was a bit like trying to stop a herd of stampeding elephants with a whoopee cushion.

Henry Tapper, pensions actuary and dedicated blogger on pensions, posted this:

The problem is that many pension trustees don’t take any notice. They didn’t back in 1999 when HMRC and tPR (then OPRA) first warned trustees about pension liberation fraud. They didn’t in 2003 when the first two liberation fraudsters – Steve Russell and William Ferguson – were jailed. They didn’t in 2010 and 2011 when the huge tide of Ark and Tudor Capital Management transfer requests into bogus occupational schemes were processed without so much the tiniest flicker of curiosity or interest. They didn’t in 2012 when 300 transfers into Capita Oak were made – even though the sponsoring employer didn’t exist. When the Scorpion Campaign was launched in February 2013, the trustees carried on making transfers into Capita Oak and the sister scam, Westminster (with the same non-existent sponsoring employer).

Now here’s the puzzling thing: didn’t the Pensions Regulator notice that their Scorpion Campaign was failing? Usually, when time, effort and money are invested in an important project, there is some sort of measuring process deployed to see how effective and successful the project is and to examine whether any improvements or reinforcements are needed. Clearly not in the case of tPR and Scorpion, because the same old same old scammers were allowed to keep registering pension schemes and becoming trustees and administrators of “occupational” scams obviously designed to defraud innocent victims.

In particular, the regulator issued a damning assessment of the scheme’s former trustee, Dorrixo Alliance, and its director Stephen Ward.

So, didn’t anybody at the Pensions Regulator (or HMRC for that matter) notice that Stephen Ward had become trustee of the doomed London Quantum “occupational” scheme (now in the hands of Dalriada Trustees)? Didn’t the memory of Ark, Evergreen, Capita Oak, Westminster and dozens of other liberation scams run by Ward and Dorrixo ring any bells? Didn’t London Quantum’s address: 31 Memorial Road, Worsley cause a sharp intake of breath?

The answer to all of the above is, of course, a resounding “no”. The Scorpion Campaign’s warnings were ignored 96 times in 2014 in the London Quantum case. Negligent, lazy and incompetent trustees handed over a total of £6.8 million to an obvious scam which had all the hallmarks of Ward’s handiwork – including the fact that it was registered to Ward’s UK address. But not a single one of the trustees heeded tPR’s Scorpion warning – including the trustees of the Police pension scheme.

My advice to the Pensions Regulator, is to put the whoopee cushion away. It doesn’t work. The stampeding elephants are too big and too determined. And don’t just knit a bigger whoopee cushion either – ban cold calling and put the scammers behind bars. Then spend some money on advertising (after all, the government found £10m to spend on the Remain campaign – which was arguably a complete waste of money).

And by the way, the Regulator’s “dressing down” was a complete waste of time. It might just as well have been a formal dressing gown for all the effect it had.

EVERGREEN RETIREMENT TRUST QROPS PENSION SCAM AND MARAZION LOANS

THE WAY THE SCAM WORKED

When Ark got shut down in June 2011, Stephen Ward flew to New Zealand and set up the Evergreen NZ QROPS liberation scam with Simon Swallow of Charter Square. Ward also set up a “loan” company in Cyprus called Marazion. He also did a deal with two investment funds: Penrich and Spectrum. Expats would transfer their UK pensions to Evergreen and pay a 10% transfer fee. As soon as the transfer was complete, a loan – funded by either

Expat victims (mostly) would transfer their UK pensions to Evergreen and pay a 10% transfer fee. As soon as the transfer was complete, a loan – funded by either Penrich or Spectrum (to whom the loans were assigned) was arranged between Marazion and the member. The loan was for a fixed five-year term, and the member was made to sign a “lock in” agreement with Evergreen.

The loan interest was 8.5% compound (quarterly) and would mean that the original loan amount would increase by 50% by the end of the five years. Ergo, the maths worked like this at the outset: £100k transfer; £10k fees; £90k Evergreen fund; £50k loan. At the end of the five-year term, the Evergreen fund would either have increased, decreased or remained the same (in fact, it has decreased) and the loan would have increased to £75k. The member was offered the option to renew the loan for a further five-year term at a higher rate of interest.

For three years, Evergreen managed to avoid disclosing what the assets of the scheme actually were, but in 2015 they had no choice other than to disclose that 41% of the scheme’s assets consisted of Penrich and Spectrum. After a lengthy and detailed complaint to the NZ Ombudsman, the complaint against Evergreen was not upheld and the victims were originally left “locked in” until 2017. However, Evergreen has now moved the goal posts and the victims are locked in until they reach the age of 55. Evergreen was removed from the QROPS list by HMRC in November 2012.

THE IDENTITY OF THE MAIN PLAYERS

Stephen Ward of PPS/Marazion

Continental Wealth Management SL who acted as introducers

Simon Swallow of Charter Square

HOW THE MAIN PLAYERS WERE INVOLVED

Continental Wealth acted as introducers – and referred to the firm as the “sister” company to Ward’s company Premier Pension Solutions; PPS processed the transfers and loans; Swallow of Charter Square managed the scheme.

Pension liberation fraud costs victims £millions every year. It ruins lives and causes desperate poverty in retirement. But the situation is made far worse because the State has badly miscalculated how much it will cost to support these victims for the rest of their lives. The amount of tax actually collected will be far outstripped by the cost of support and healthcare.

An Ark victim has suggested it would be a good idea to do a full update so everybody knows the entire story so far. I agree that’s a good idea so here is a brief outline of where we are and how we got here. If anyone has any questions or wants further information the Ark Class Action can be contacted on arkmarazion@gmail.com.

2010: a group of investors got together and purchased a plot of land in Larnaca, Cyprus for 1 million pounds. With the intention to try to turn it into a golf course. Only they needed more land and more money. So they consulted a group of “experts” who came up with the idea of attracting investment by starting a pension scheme. Now, pensions are supposed to be LOW RISK. And diverse. Speculative land development projects are NOT a good idea for a pension (due to being high risk). Financial advisers are supposed to know this and are not supposed to advise their clients to put their hard-earned pensions into a scheme based on a potentially worthless piece of land.

OFFICIAL TIME-LINE 2010: Ark was formed by a group of “experts” and the worthless piece of land originally bought for 1 million was sold to Ark for 4 million.

August 2010: Ark’s “Master Pension Schemes” (MPS’s) were aggressively promoted and sold by a clutch of financial advisers in Spain and the UK using pension liberation (also known as pension cracking or unlocking) in a scheme described by the promoters as “not traditionally available” (in other words unlawful). This “unique” process was called Maximising Pension Value Arrangements (MPVA) and facilitated a loan to the participant of up to 50% of the value of the transferred pension (after deduction of fees which ranged from between 5% and 15%).

2010 to 2011: The Ark schemes began advertising and were sold through newspaper ads, websites, calls from financial advisers, seminars and advertisements posted on toilet doors.

May 2011: The Pensions Regulator were actively shutting down pension liberation scams such as Ark and placed the six Ark schemes in the hands of Dalriada Trustees and the whole lot was suspended. The Regulator was actively promoting its “Scorpion” campaign to warn people about the dangers of pension liberation fraud. http://www.hmrc.gov.uk/pensionschemes/investments-tax.htm. HMRC also set up “Project Bloom” to help stop these scams due to the fact that the victims stood to lose their pensions AND get 55% plus tax bills on their pension loans. http://www.hmrc.gov.uk/pensionschemes/liberationud.pdf

December 15th 2011: Justice Bean ruled in the High Court that the Ark schemes (MPS’s and MPVA’s i.e. pension transfers and reciprocal loans) were a “fraud on the power of investment” and that the loans constituted “unauthorised payments” (i.e. taxable at 55%). The ruling can be read here – note Clause 57: http://www.professionalpensions.com/digital_assets/3826/4568_001.pdf

December 20th 2011: Marazion was incorporated in Nicosia, Cyprus.

June 2012 Evergreen Pension Scheme commenced trading – making a loss in the first year and attracting 426 members

August 2012 Marazion started selling five-year term loans and corresponding five-year “lock ins” to Evergreen pension transfers

19th November 2012 HMRC suspended Evergreen from their QROPS list http://www.evergreentrust.co.nz/uk-pension-transfers/

December 2012 Dalriada published the first year’s audited accounts (for the period May 2011 to May 2012) for the six MPS’s: Cranbourne Star, Tallton Place, Grosvenor, Lancaster, Portman and Woodcroft Dalriada’s audited accounts for the six Ark schemes for the first two years can be found here: http://dalriadatrustees.co.uk/ark/

September 2013: The Ark Class Action was set up to help inform the Ark victims and negotiate and appeal their tax liabilities so that these (together with their pension losses) can be reclaimed from the negligent financial advisers who sold the Ark schemes to the victims .

March 2014: HMRC finally agreed to confirm their full intentions regarding taxing the Ark loans.

April 2014: HMRC finally confirmed their intention to try to tax the loans at both ends i.e. 55% at the receiving end AND 55% at the making end. They also confirmed that Ark members who did not receive a loan would still be taxed at 55% for making a loan or intending to make a loan, and/or intending to receive a loan.

Between 2012 and 2014 (to date), some Ark members have received demands by HMRC to complete Self Assessment returns declaring the Ark unauthorized payments for tax purposes; some members have received demands for the tax; some have received nothing at all, but HMRC have confirmed that the letters and demands are now on their way. However, there really has been no consistency in their approach to the whole Ark matter, but they do now appear to be getting their act together.

June 2014: Evidence regarding the Marazion/Evergreen pension liberation fraud was handed to the British authorities in London.

June 2014: HMRC has issued a deadline of 30th of June for return of the 10 point questionnaire required in respect of the Ark loans.

Pension scammers have a “code”. Rather like pirates, they are not to be trusted. They pick their words carefully, revealing little; they are sneaky and lack any morals. They are good at disguises and if they fear they may be rumbled, they will disappear over the horizon, never to be seen again. They certainly won’t hang around to help pick up the pieces after their victims have been ruined. Rest assured, they will take as much as they can get and show no remorse. Living the Life of Riley on your hard-earned money is their reward.

Pension scammers have a “code”. Rather like pirates, they are not to be trusted. They pick their words carefully, revealing little; they are sneaky and lack any morals. They are good at disguises and if they fear they may be rumbled, they will disappear over the horizon, never to be seen again. They certainly won’t hang around to help pick up the pieces after their victims have been ruined. Rest assured, they will take as much as they can get and show no remorse. Living the Life of Riley on your hard-earned money is their reward. Those of you who follow Pension Life, will know that we want to put a stop to pension scammers and are trying our hardest to get as much information as possible out to the public about how to avoid being scammed. We want to educate the masses and stop pension scammers worldwide.

Those of you who follow Pension Life, will know that we want to put a stop to pension scammers and are trying our hardest to get as much information as possible out to the public about how to avoid being scammed. We want to educate the masses and stop pension scammers worldwide.

Mrs. A: “I was first cold called by CWM in 2011. I first met Phil Kelman of CWM in January 2012. I was told only positive things about transferring my pensions and to be able to take 100% of my pension funds.

Mrs. A: “I was first cold called by CWM in 2011. I first met Phil Kelman of CWM in January 2012. I was told only positive things about transferring my pensions and to be able to take 100% of my pension funds.