BBC Radio 4’s You & Yours reports on three victims of a pension investment scam called Blackmore Global, two of whom were cold called by David Vilka of Square Mile International Financial.

The three victims were persuaded to transfer their funds from secure company pensions into QROPS (Qualifying Overseas Pension Schemes). The victims have since struggled to track or recoup their investments in the Blackmore Global fund.

Stephen Sefton, a driving instructor from Milton Keynes, was the main focus of the You & Your´s program. Most of his pension fund had been invested through the overseas pension scheme into a fund called Blackmore Global. The rest had gone into an investment fund in Malta. A year later disaster struck.

Stephen became a member of Pension Life after he was unable to track and evaluate his overseas pension investment. Upon calling the City regulator, the Financial Conduct Authority (FCA), he was informed that his adviser – David Vilka of Square Mile International Financial – was not regulated to give investment advice. Furthermore, the fund in Malta was a professional investor fund only and was not suitable for a retail investor like him.

Stephen, taking advantage of the new pension rules, had transferred £415,000 of his company pension scheme into a new pension in 2015. He wanted to access his money early and give some to his children. He had found the advisory firm online; seen the company’s FCA registration number of David Vilka’s firm (Square Mile International Financial based in Prague) at the bottom of the firm’s letters. What he did not realise, was that the firm was only regulated for insurance mediation, and not investment advice.

Stephen, managed to get most of his money back after pursuing his case for many months. However, he lost £30,000 of his investment as the fund in Malta dropped in value at the time of withdrawing his money.

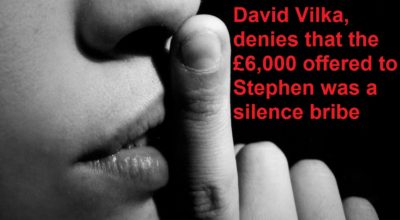

Having succeeded in recouping a good chunk of his money, he received an email from Square Mile International Financial offering him a bribe of £6,000 to cease all contact with outside sources. This included regulatory authorities and Action Fraud!

Having succeeded in recouping a good chunk of his money, he received an email from Square Mile International Financial offering him a bribe of £6,000 to cease all contact with outside sources. This included regulatory authorities and Action Fraud!

David Vilka, one of Square Mile International Financial’s directors, claims this to be incorrect. Instead suggesting the amount was a goodwill gesture to close the matter amicably.

Unfortunately Stephen Sefton’s recovery of his money is a minority case, many other victims of the Blackmore Global Pension Scam are finding it difficult to recover their money.

David Vilka insists that Square Mile International Financial is a completely legitimate firm. He claims the firm has been “inspected and verified in full by numerous regulators”. Furthermore, Stephen’s reports to Action Fraud were returned saying it had not identified any leads to follow up.

David Vilka insists that Square Mile International Financial is a completely legitimate firm. He claims the firm has been “inspected and verified in full by numerous regulators”. Furthermore, Stephen’s reports to Action Fraud were returned saying it had not identified any leads to follow up.

The BBC also reported about another victim called Paul (not his real name):

“Paul” agreed to have his £100,000 pension fund transferred into another pension scheme and then invested in the Blackmore Global fund. This was after being cold-called by another company called Aspinal Chase who offered him a free pension review.

The small print stated investments were locked in for 10 years, which was way beyond Paul’s 60th Birthday. This was not mentioned to Paul when he made the transfer. Fortunately he managed to escape the lock-in, however he has still been unable to access his funds.

Paul told You and Yours “I’ve got three grandchildren. I’d like to take them all to Disneyworld in America. I want to spend the money I’ve earned over the years. A bit of that money would pay off the last bit of my mortgage, so that is a big chunk of my future. I feel as though I’ve let the family down.”

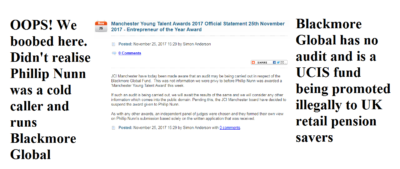

The perpetrators – Phillip Nunn and Patrick McCreesh – are listed as Blackmore Global’s directors in a fund document seen by Radio 4’s You & Yours program, which shows they each earn salaries of £20,000 a year.

David Vilka was also the financial adviser for Paul and also for the third victim reported, Jacqueline. Another cold-call victim of Aspinal Chase, Jacqueline has had no access to her funds.

Blackmore Global’s directors have refused to release the £50,000 she invested. You & Yours quoted, Phillip Nunn and Patrick McCreesh: who said, only allowed redemption´s in exceptional circumstances to “protect the integrity of the investment for its other stakeholders”.

Phillip Nunn and Patrick McCreesh deny that their company, would engage in cold calling or pension advice. They claimed that any advice must have been given by separate, regulated financial advisers.

Nunn and McCreesh also say they have no financial relationship with David Vilka or Square Mile International Financial. In fact, they state they are totally independent from them! However, there has to be a good reason why Vilka has invested so many of his victims’ pension funds in the Blackmore Global fund – and risked criminal prosecution because Blackmore Global is a UCIS (Unregulated, Collective, Investment Scheme) which is illegal to promote to UK residents.

Pension Life is aware of a further 38 victims cold called by Aspinal Chase, Nunn & McCreesh´s firm. Originally being advised to transfer their funds into a Hong Kong QROPS, the victims´ funds finally made their way to the Blackmore Global fund. The total amount of funds scammed from these UK resident victims amounts to nearly £1,000,000!

To listen to the broadcast on the BBC’s website, click here.

To read the news story based on the You & Yours report, click here.

**************************************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

I will, of course, be more than happy to help Deloittes see the whole picture – rather than just what the Fraudsters want them to see. I will happily buy a whole shed full of spades as well as several boxes of latex gloves and surgical masks. However, the most important way in which I can assist them is to give them details of the various scams which the Fraudsters have operated and facilitated.

I will, of course, be more than happy to help Deloittes see the whole picture – rather than just what the Fraudsters want them to see. I will happily buy a whole shed full of spades as well as several boxes of latex gloves and surgical masks. However, the most important way in which I can assist them is to give them details of the various scams which the Fraudsters have operated and facilitated. Deloittes will need to concentrate on at least three main areas: Trafalgar Multi-Asset Fund;

Deloittes will need to concentrate on at least three main areas: Trafalgar Multi-Asset Fund;

TPR had appointed Dalriada Trustees to the case, and with this ruling, they will be able to attempt to recoup the stolen money from the four scammers. Unfortunately it is unclear how much money is actually left to recoup as scammers are notoriously clever at hiding their ill-gotten gains offshore and presenting themselves as “men of straw”.

TPR had appointed Dalriada Trustees to the case, and with this ruling, they will be able to attempt to recoup the stolen money from the four scammers. Unfortunately it is unclear how much money is actually left to recoup as scammers are notoriously clever at hiding their ill-gotten gains offshore and presenting themselves as “men of straw”. One of the victims, Colin, from South Wales, had become the full-time carer for his partner when he was approached via text message. Promised investments in the now bust St Lucia Developments, a lump sum which he planned to spend on a holiday. Having heard about the pension scams, he tried to contact the scammers with no success.

One of the victims, Colin, from South Wales, had become the full-time carer for his partner when he was approached via text message. Promised investments in the now bust St Lucia Developments, a lump sum which he planned to spend on a holiday. Having heard about the pension scams, he tried to contact the scammers with no success. A couple, John and Samantha, both fell victim to this scam despite being advised by their pension provider that it could be a scam. They received their lump sum and were told their pension was invested in truffle trees. After reporting the case to the police, they were later informed that their lump sum was from their own funds and HMRC promptly served them with a large tax bill.

A couple, John and Samantha, both fell victim to this scam despite being advised by their pension provider that it could be a scam. They received their lump sum and were told their pension was invested in truffle trees. After reporting the case to the police, they were later informed that their lump sum was from their own funds and HMRC promptly served them with a large tax bill. Why has cold calling not been banned by the government?

Why has cold calling not been banned by the government?

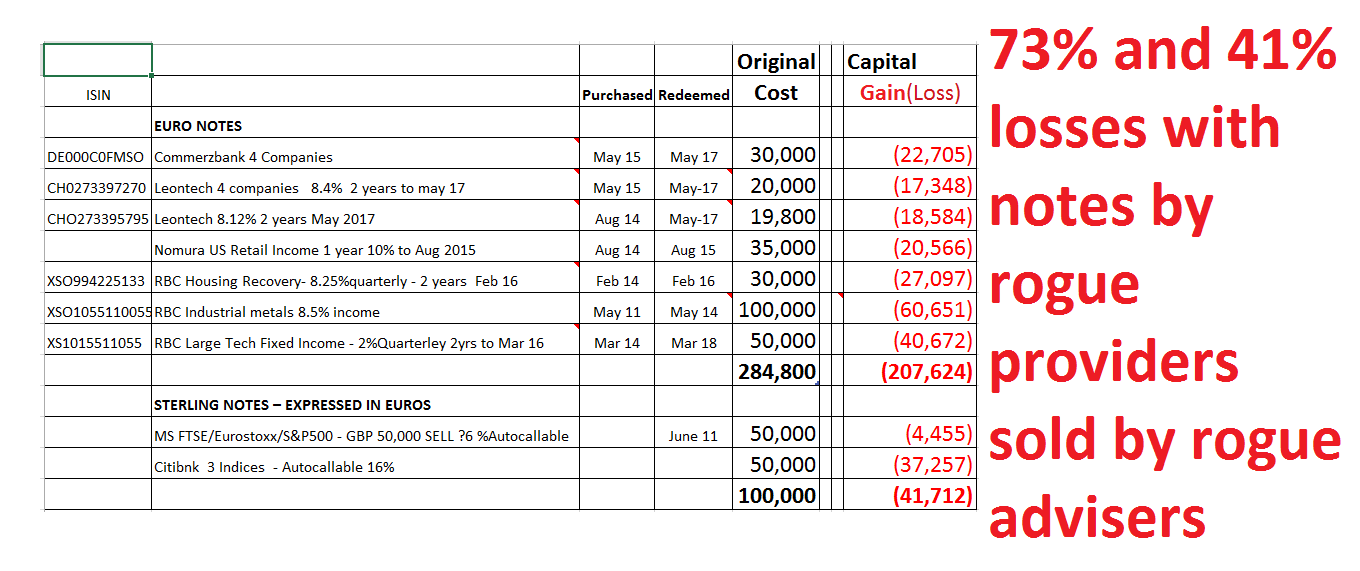

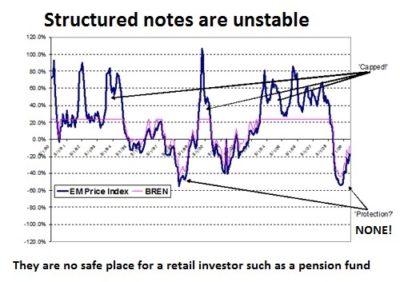

Structured notes – say NO to them if an adviser wants to invest your pension in them. They are high-risk investments which are for professional investors

Structured notes – say NO to them if an adviser wants to invest your pension in them. They are high-risk investments which are for professional investors  As in the above example, it is a disgrace that structured note providers such as Commerzbank, Nomura, RBC and Leonteq have allowed their toxic products to be used for retail pension savers. Even when these rotten products have nosedived repeatedly, these dishonest and dishonourable providers keep on flogging them to destroy victims’ retirement savings.

As in the above example, it is a disgrace that structured note providers such as Commerzbank, Nomura, RBC and Leonteq have allowed their toxic products to be used for retail pension savers. Even when these rotten products have nosedived repeatedly, these dishonest and dishonourable providers keep on flogging them to destroy victims’ retirement savings.

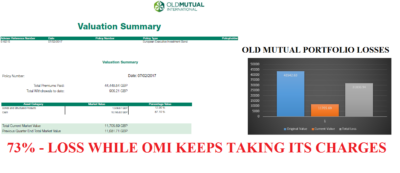

OMI – Old Mutual International (Quilter), SEB, ZURICH, GENERALI, FRIENDS PROVIDENT, ZURICH INTERNATIONAL, RL360 AND HANSARD INTERNATIONAL. They are all as bad as each other. They rip their clients off, charging them huge fees and commissions, tying them into useless, pointless products for years.

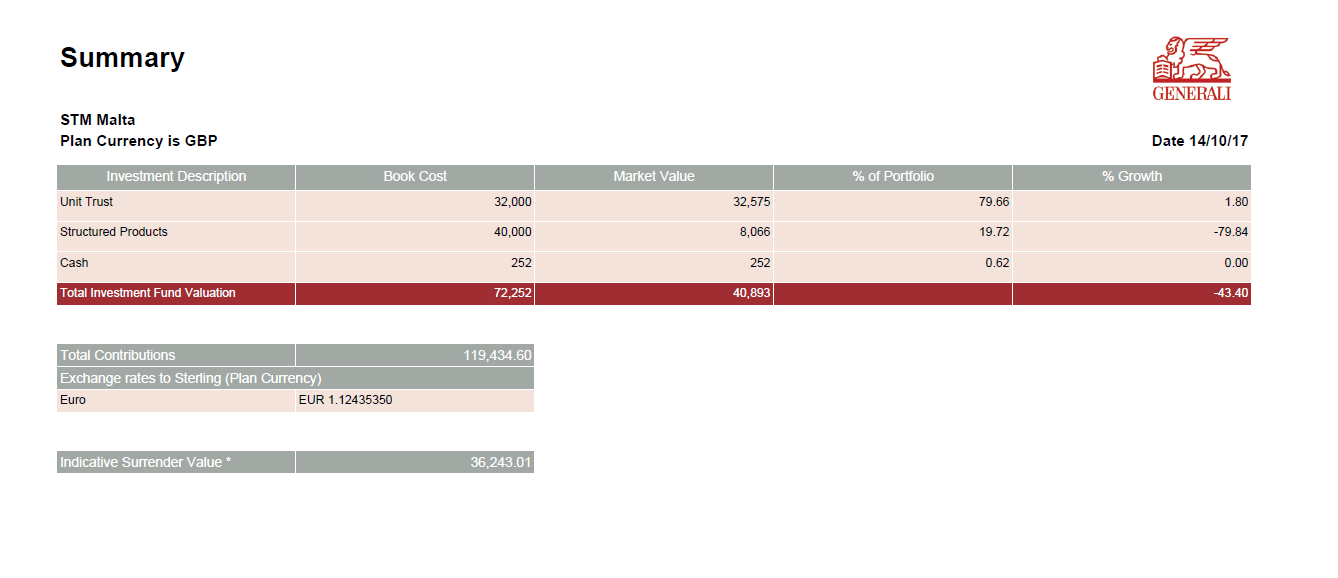

OMI – Old Mutual International (Quilter), SEB, ZURICH, GENERALI, FRIENDS PROVIDENT, ZURICH INTERNATIONAL, RL360 AND HANSARD INTERNATIONAL. They are all as bad as each other. They rip their clients off, charging them huge fees and commissions, tying them into useless, pointless products for years. One Generali victim saw her £119k pension fund plummet to £36k in five years.

One Generali victim saw her £119k pension fund plummet to £36k in five years. Pension scams are not the only arrangements that these life offices profit handsomely from. Another method they use to rinse extortionate fees out of unsuspecting victims is the LONG TERM SAVINGS PLAN. Clients think these are a good idea until they realise the huge hidden charges which decimate the funds they put towards these plans.

Pension scams are not the only arrangements that these life offices profit handsomely from. Another method they use to rinse extortionate fees out of unsuspecting victims is the LONG TERM SAVINGS PLAN. Clients think these are a good idea until they realise the huge hidden charges which decimate the funds they put towards these plans.

With assurances that the funds were in secure bank accounts which would not leave the UK, Arck LLP later forged statements to mislead investors about the losses.

With assurances that the funds were in secure bank accounts which would not leave the UK, Arck LLP later forged statements to mislead investors about the losses.

From: Old Mutual International mail:

From: Old Mutual International mail:

When a pension or investment scam implodes (as they always do), it is important to keep tabs on where the scammers go next, what they are doing next and who is helping them.

When a pension or investment scam implodes (as they always do), it is important to keep tabs on where the scammers go next, what they are doing next and who is helping them. Darren Kirby – allegedly hiding in Australia. Let’s hope he turns into a kangaroo and never gets a chance to scam any more victims out of their pensions

Darren Kirby – allegedly hiding in Australia. Let’s hope he turns into a kangaroo and never gets a chance to scam any more victims out of their pensions Dean Stogsdill – referred to as “Dogkill” by some – is an expert on how structured notes can decimate a pension fund

Dean Stogsdill – referred to as “Dogkill” by some – is an expert on how structured notes can decimate a pension fund Neil Hathaway – referred to as “Hadaway” by some – is another expert on the structured note scam

Neil Hathaway – referred to as “Hadaway” by some – is another expert on the structured note scam

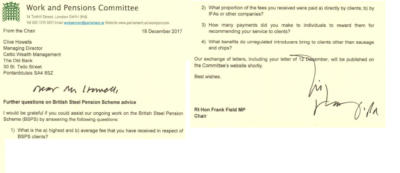

CHARLIE CHARLIE, SAUSAGE AND CHIPS – WATCH OUT BRITISH STEEL WORKERS!

CHARLIE CHARLIE, SAUSAGE AND CHIPS – WATCH OUT BRITISH STEEL WORKERS! What then struck me about Frank Field’s letter to Clive Howells of Celtic Wealth Management (the “introducer” who has been stalking the beleaguered British Steelworkers) was that Frank is a good sort – and I’d like to buy him lunch (although it won’t be sausages and chips!).

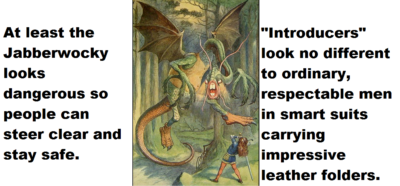

What then struck me about Frank Field’s letter to Clive Howells of Celtic Wealth Management (the “introducer” who has been stalking the beleaguered British Steelworkers) was that Frank is a good sort – and I’d like to buy him lunch (although it won’t be sausages and chips!). In the words of Lewis Carroll:

In the words of Lewis Carroll: