Laurence Goodman and the three wishes: please make 37 Fast Pensions Scam loans disappear JUST LIKE THAT!

Bridgebank Capital’s Laurence Badman Goodman has made 37 Fast Pensions Scam loans disappear as if by magic – while he was on holiday and too busy to engage with Pension Life or the distraught victims of Peter and Sara Moat.

Having discovered this was where some or all of the elusive Fast Pensions Scam funds were hiding, we all hoped this might finally result in some of the 18 Pensions Ombudsman’s determinations to allow victims to transfer out being complied with.

We all wanted to believe that Goodman was a good man, but now it would seem the opposite might be the case. So, one of the following is true:

All the borrowers of the 37 loans have simultaneously repaid their loans on 17th August 2017

The loans have been sold or transferred on to somewhere we can find them (yet)

Sara Moat had been claiming that Fast Pensions was merely the administrator of the pension schemes, and that it was ultimately the “responsibility of the trustees to decide whether the transfers could be made”. Of course, the Companies House records showed that the Bridgebank Capital loans were made in favour of Sara Moat as trustee (along with another stooge called Martin Peacock). This scuppered Sara Moat’s excuse and exposed her as a liar once again.

So, when Goodman has finished having a jolly time on the Costa Lot, necking his champers and writing his postcards to his mate Pete, perhaps he might find a moment to be sober enough to remember that I am meeting the Serious Fraud Office next week. And most of the Fast Pensions Scam victims have also submitted their reports to the SFO.

Frantic with worry – the Fast Pensions victims now know their pension funds are being used for property loans.

Bridgebank Capital seems to be a bona fide property loan company – providing bridging and development finance. Nothing wrong with that.

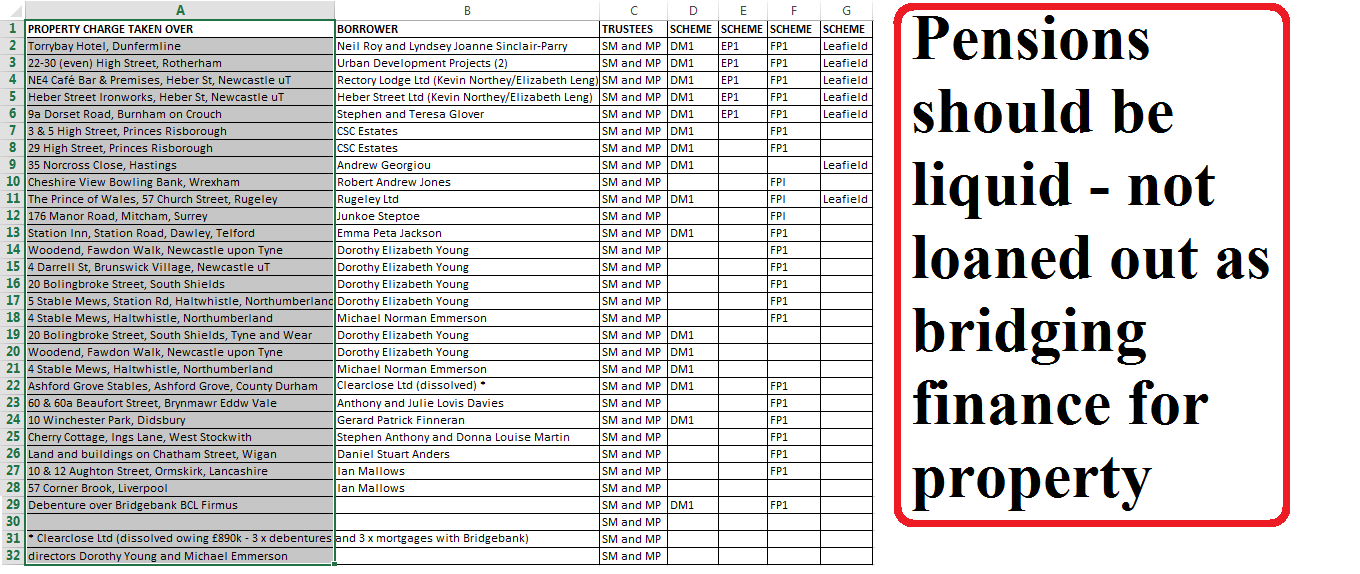

But Bridgebank Capital No. 5 seems to be full of Fast Pensions money and locked into term loans secured on a variety of domestic and commercial properties. Each charge refers to the trustees of four of the Fast Pensions schemes: DM1, FP1, EP1 and Leafield. The trustees of each of these schemes are clearly identified at Companies House as Sara Moat and Martin Peacock. (Interestingly, Sara Moat is telling victims that “the trustees” have to decide what happens to the pension monies – while hiding the fact that she is the trustee).

Of great concern is the fact that one of the borrowers, Clearclose, has gone bust owing the pension fund nearly £900k.

The Pensions Ombudsman has made 18 determinations against Fast Pensions – but Sara and Peter Moat of Fast Pensions have studiously ignored them. I sent links to all of the background to Fast Pensions to Laurence Goodman of Bridgebank Capital on 6th August 2017:

Dear Mr. Goodman

It was good to speak to you on Friday.

First of all, may I say that I recognise that Bridgebank Capital is a bona fide finance company and I mean no criticism against you or your company in the summary I am setting out below. I have tried to summarise the position in a bullet-point series of statements to make this as easy to understand as possible.

Once you have read and digested this, please can we start a dialogue about what happens next. What the members need to know, is how much do these various loans/charges/mortgages in favour of the four Fast Pensions schemes realise when they mature, and what will happen to the money. I realise you are restricted to an extent in terms of what you can tell me, but there are many Fast Pensions victims who will happily provide you with letters of authority as they are the beneficiaries of the pension schemes and have a legal right to know what has happened to their pension funds.

Best, Angie

—————-

* There are hundreds of members of various pension schemes (including DM1, FP1, EP1 and Leafield) run by Peter and Sara Moat of Fast Pensions – a pensions administration company.

* The Moats maintain they are not the trustees of the schemes. Peter Moat (masquerading as “James Porter”) told me the trustee was a company called FP Scheme Trustees, of which one Jane Wright is sole director. She was an employee of Moat’s at his former company Blu Properties in Javea which folded and it is believed she was paid to be the director of this company.

* The charges registered at Companies House for Bridgebank Capital No. 5 show all the loans as being in favour of Sara Moat and Martin Peacock (an associate of Peter Moat’s) as trustees of the Fast Pensions schemes.

* The various Fast Pensions schemes – including DM1, FP1, EP1 and Leafield – I believe are all bogus occupational schemes. When I say bogus, what I mean is that they were not set up to provide genuine pensions for employees of a company which intended to trade and create jobs, but merely as a vehicle for a pension liberation scam.

* Peter Moat told me (while he was masquerading as a “James Porter”) that the underlying assets of the Fast Pensions schemes were “invested in Bridgebank Capital” and also in another loan company called Pamplona Capital Partners. Clearly, having the underlying assets of a pension scheme solely “invested” in property loans is not acceptable. A pension scheme is required to have low-risk, liquid assets as members have a statutory right to a transfer and need to be able to take their 25% tax-free lump sum at age 55, or retire or die.

* The Moats have failed dismally to communicate with the members or respond to transfer requests for a long period of time – causing considerable distress to the victims. The Pensions Ombudsman has made a large number of determinations in response to complaints by the victims and has ordered Fast Pensions to allow the victims to transfer out and pay compensation for their distress. These 18 determinations have all been ignored by Fast Pensions:

Needless to say, there is no evidence that the Moats have complied with any of these determinations and the victims themselves report that they have not.

* Alongside the pension transfers and lending of the pension funds to Bridgebank Capital No. 5, the Moats were operating pension liberation in the form of loans from Moat’s companies Blu Debt Management and Umbrella Loans. Victims were told these loans were not connected to the pension transfers and would not be taxable. HMRC is now sending out tax demands in respect of these loans.

* There are grave concerns about the Bridgebank Capital No. 5 loans for the following reasons:

1. We do not know what the total amount lent to Bridgebank Capital is

2. There are multiple loans to the same parties

3. One borrower is in liquidation

4, We do not know what the terms of the loans or the interest payable are

* The greatest concern is that if any part of the money is recoverable and is paid back into the control of the Moats, it will simply “disappear” again and not be available for the benefit of the members who are the ultimate beneficiaries.

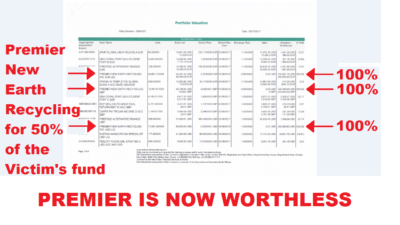

Investors are likely to have lost all their money in Premier New Earth Recycling fund – now in liquidation. The liquidator is Deloittes and they can’t say much, if anything, about what is happening as they are looking into the possibility of claims against third parties and don’t want to prejudice any possible action.

Rather than getting into the nitty gritty of the liquidation of this fund – and the appalling possibility that the investors may very well have lost everything – let us take a good look at the fund itself.

It is a UCIS. Nothing more to say – except:

“Specialist, qualifying, and qualifying-type experienced investor funds are unregulated collective investment schemes which are neither approved nor reviewed by IOMFSA. Once launched, the funds must be registered with the authority within 14 days. These types of funds cannot be sold to the retail public. Access to such funds is only available where investors confirm that they meet the fund type’s minimum entry criteria. This includes a statutory certification that they have read the scheme’s offering document and understand and accept the specific risks associated with that type of fund.”

So, instead of writing lots of fascinating stuff about the wonderful topic of generating energy from rubbish (which I am sure is really interesting and good for the planet), why don’t we stick with the unchallengeable fact that the fund was a UCIS and should not have been promoted to retail investors. End of. No argument. Non-negotiable. Talk to the hand. Stick your UCIS where the sun doesn’t shine.

In fact, the same was true (should have been true) of the Connaught bridging loan fund; EEA Life Settlements; LM; Store First, Park First, Trafalgar Multi-Asset Fund and Blackmore Global. So why did so many advisers promote them and invest their clients’ money in them? £$£$£$£$£!!! Commissions. Backhanders. Sandwiches. And the distressed investors are now paying the appalling price for rogue advisers’ greed and negligence.

And what does this look like from the investor’s point of view?

Appalling investment losses on Premier New Earth Recycling

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

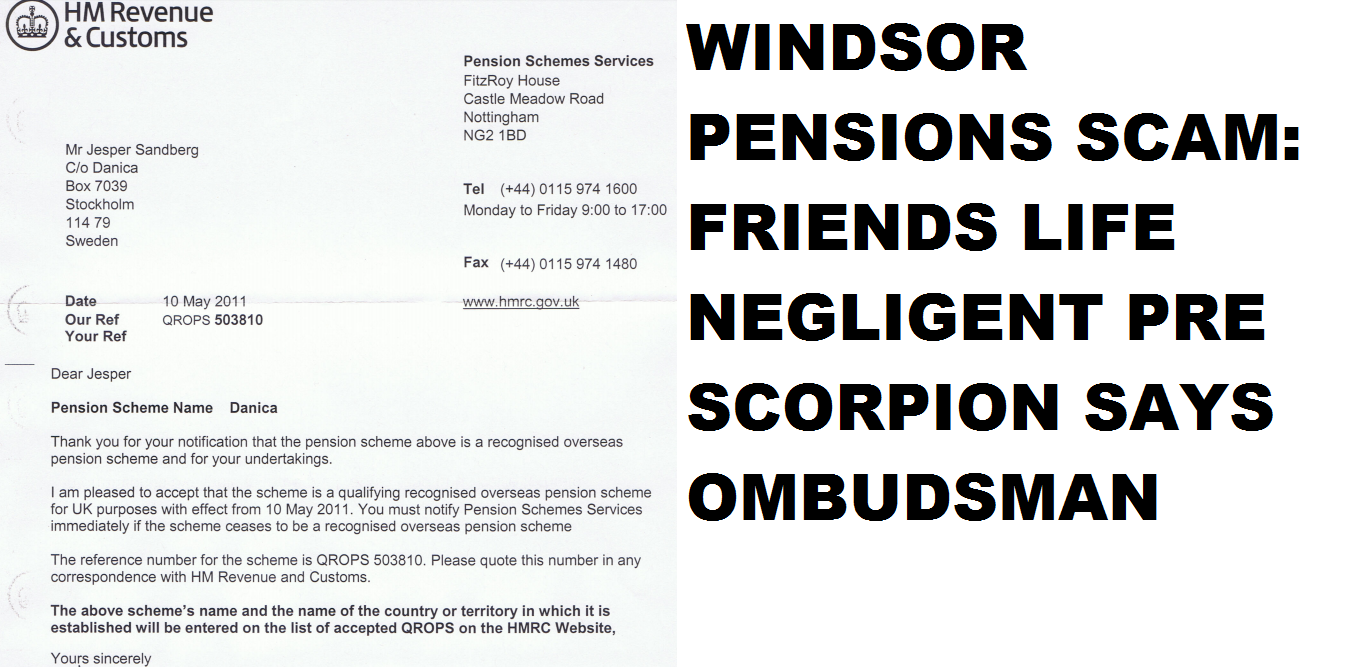

Friends Life negligent in Windsor Pensions “Danica” scam

FRIENDS LIFE – OR DEATH? WINDSOR PENSIONS QROPS SCAM (DANICA)

Since 2010, dozens of ceding pension providers have recklessly and negligently allowed transfers out to obvious pension scams. During the years of Ark, Capita Oak, Westminster and Henley, the worst offenders were Standard Life, Scottish Widows, Prudential and Aviva as personal providers, and Royal Mail as an occupational provider.

Both HMRC and the Pensions Regulator claim there were sufficient/ample warnings in the public domain to educate and inform ceding providers about pension scams since 2002. But the Pensions Ombudsman’s Service claims the cut-off date was February 2013 when the Pensions Regulator first published the “Scorpion Campaign”. According to the POS, before Scorpion all ceding providers walked around with paper bags over their heads and did no reading up on their professional and fiduciary obligations or any developments among scams and scammers.

However, a recent ruling on the negligence of a ceding provider – Friends Provident – may change the course of history. The case of “Mrs N” involved a transfer from FP administered by a company called Windsor Pensions run by one Steve Pimlott in Florida. In fact, I “secret shopped” Windsor and Pimlott in 2015, and he was still offering “transfers to Danica QROPS” with full liberation. He also claimed to have done 5,000 such transfers/liberations.

On 25 February 2015 at 10:37, STEVE PIMLOTT <stevepimlott@windsorpensions.com> wrote: Dear Ms Brooks

I cannot give you tax advice. If you cash out, it’s possible that HMRC will send you a tax bill. We assisted approximately 5,000 people who took that route and I would estimate that 200-300 did receive a tax bill. The rest to my knowledge did not. Of those that did, many just ignored it because they were resident in a different country and had no assets left in the UK.

Regards

Steve

The question is, however, does this set the bar for other negligent ceding trustees? This case is notable because it is “pre Scorpion”. But the POS found that irrespective of the date, Friends Provident should have done more due diligence and not just handed over a pension to a scheme which was no longer registered (and, de facto, to a fraudulently-set-up bank account).

Mrs N’s complaint is upheld and to put matters right Friends Life should pay her the unauthorised member payment tax charge and surcharge less the tax liability she would have paid had the full pension been taken as an uncrystallised funds pension lump sum (UFPLS). In addition it should pay Mrs N £1,000 for the significant distress and inconvenience caused by its error.

My reasons for reaching this decision are explained in more detail below.

Complaint summary

Mrs N complained that Friends Life undertook insufficient due diligence on the qualifying recognised overseas pension scheme (QROPS) into which she had requested a transfer. Had it acted appropriately it would not have accepted the transfer instruction.

Following the transfer Mrs N received the full value of her pension. At the time she was 53. As a result she is now liable to a 55% unauthorised member payment tax charge.

Mrs N has also said she has incurred costs whilst attempting to resolve the situation and Friends Life should pay these.

Background information, including submissions from the parties

On 10 May 2011, HMRC wrote to Danica, Stockholm, confirming undertakings had been received that Danica was a recognised overseas pension scheme, and that HMRC would accept the scheme as a QROPS with effect from 10 May 2011. It provided a QROPS reference number – QROPS 503810 – and confirmed that the scheme name and country would be added to the list of accepted QROPS on HMRC’s website.

Danica was added to the HMRC QROPS list, but then removed on 29 June 2011.

In October 2011 Mrs N completed a letter of authority for an unregulated financial intermediary; Insignia Financial Services. This was submitted to Friends Life which responded with a transfer illustration on 3 January 2012. QROPS illustrations were issued on 21 January 2012.

On 16 February 2016, Friends Life received an Overseas Transfer Out Payment form and Member Declaration, signed by Mrs N on 7 February 2012. Accompanying this was the HMRC letter confirming QROPS status.

QROPS discharge forms were issued to Mrs N shortly after.

The required forms were received by Friends Life on 9 March 2012. Friends Life says that the supplied QROPS number was checked against the QROPS list and found to be correct. Friends Life also checked the HM Treasury sanctions list.

The payment of £88,622.80 was processed on 13 March 2012. However, what the POS has not disclosed is that the funds were sent to a Barclays Bank account in the Isle of Man which was fraudulently set up by the scammers with the account name “Danica”. I understand the money was subsequently paid to Mrs N by the Danica arrangement and has since been spent. No it wasn’t. The money never went near the Danica pension scheme in Sweden. It went straight to the scammers’ bank account in IoM.

Friends Life were made aware of an issue with the Danica scheme, and Insignia Financial Services on 13 April 2012.

Mrs N has since been contacted by HMRC and informed that the transfer was an unauthorised payment, so it is subject to an unauthorised member payment tax charge and surcharge of approximately £49,000. I understand this has not been paid and remains outstanding, with interest accruing.

Mrs N raised a complaint about Friends Life’s actions. It did not uphold the complaint, and made the following summarised points.

Mrs N had a statutory right to transfer, and Friends Life had no reason to think that the information provided regarding the QROPS was false. Friends Life missed a rather obvious clue i.e. a QROPS in Sweden was purportedly using a Barclays bank account in the IoM – might that not have rung an alarm bell?

The QROPS number was checked against the QROPS list and found to be correct. Although the name Danica did not appear on the QROPS list, Danica Private Pension (Sweden) and Danica Pension (Sweden) did. In other words, similar but different.

The transfer happened prior to concerns about pensions liberation being widely recognised as an industry issue. The Pension Ombudsman has previously said that February 2013 was the point of change in good industry practice where knowledge of pension liberation and scams had increased. This is nonsense – both the Pensions Regulator (formerly known as OPRA) and HMRC had been warning the industry about pension scams for more than fifteen years. Friends Life had an absolute duty to be aware of and vigilant against pension scams.

The presence of a scheme on the QROPS list does not guarantee its QROPS status, and HMRC forms which would have been completed by Mrs N state: “The list should not be relied upon by you, the member in deciding whether a scheme is a QROPS.” Pretty confusing to be honest: HMRC publishes a list of QROPS but the member herself has to decide whether the scheme is a QROPS. How would a member decide that? Ask the scammers?

Friends Life suggested that Mrs N transferred her pension with full knowledge of a lump sum payment being made, which was not offered under her existing plan due to UK tax legislation. It was reasonable to expect that she would have sought independent financial advice before proceeding. Instead she proceeded through an unregulated financial adviser and did not seek advice from a regulated adviser. Indeed, the adviser was unregulated – but Mrs. N did not know this and wouldn’t have known how to check anyway. In fact, Friends Life ought to have brought this to her attention at the start.

There was an onus on Mrs N to check the legitimacy of her financial adviser. At the time there was no reason for Friends Life to think the financial adviser was unregulated. Friends Life didn’t even check.

Friends Life had highlighted that, ‘Tax penalties may apply following a transfer to a QROPS. It is important all implications are understood before transferring funds from the UK’, and Mrs N had received a copy of this statement.

Adjudicator’s Opinion

Mrs N’s complaint was considered by one of our Adjudicators who concluded that further action was required by Friends Life. The Adjudicator’s findings are summarised briefly below:-

Central to the complaint was whether Friends Life should have acted on Mrs N’s transfer request. Side issues relating to the legitimacy of the financial adviser involved or any declarations signed were not integral to the complaint.

The events complained of occurred prior to the Pension Regulator’s pension liberation warning campaign of February 2013, at a time when checks on receiving schemes were less rigorous. This may be correct – however, that doesn’t make it right. However there were reasonable basic checks that Friends Life ought to have completed before making the transfer, including checking HMRC’s QROPS list. They did check the QROPS list and were probably confused by the similar names of two other schemes containing the word “Danica”.

The Danica scheme had been on the list for a short period but was removed by the time Mrs N submitted the transfer request. Friends Life’s internal policy was not to transfer to schemes which were not on the QROPS list.

Although the QROPS list was checked the day before the transfer was put through and there were two similarly named schemes on the list, the Danica scheme was not on the list. At that point additional checks should have been undertaken to establish why the Danica scheme was not on the list, had it done so it would have established that the Danica scheme had been removed nine months prior.

In these circumstances Mrs N’s pension should not have been transferred, and had it not done so Mrs N would not now be subject to the unauthorised member payment tax charge and surcharge. One could argue against this point – perhaps Windsor Pensions and Insignia Financial Services would have found another obscure QROPS to use for the fraud.

To put matters right Friends Life should agree to meet the full cost of the unauthorised member payment tax charge and in addition pay Mrs N £500 for the distress and inconvenience suffered.

The Adjudicator did not consider Friends Life should be required to pay the costs Mrs N incurred when bringing the complaint. The complaint could have been referred to this Office and resolved without the involvement of her representative. I would not agree necessarily: Mrs. N had a very busy life running a business in the USA and she did need help and guidance with the complaint against Friends Life and the POS process. She was also fighting the tax demand at the same time and was extremely distressed.

Additionally, in relation to potential accountant’s fees she may incur, the Adjudicator concluded she would have needed to pay similar costs had the funds been received through legitimate means.

Mrs N did not accept the Adjudicator’s Opinion and the complaint was passed to me to consider. Mrs N and Friends Life provided further comments which are summarised below.

Friends Life said:-

Friends Life accepted the recommended redress in principle, but highlighted that it had already paid a 40% Scheme Sanction Charge and Mrs N was, under the Adjudicator’s recommendation, in effect being paid the fund value without any tax liability. Friends Life proposed to pay the unauthorised member charge less the notional tax Mrs N would have paid had she legitimately accessed the full fund value under the current rules. It calculated the tax she would have paid to be £15,294.34.

Friends Life also considered that given Mrs N’s position it was reasonable for her to have sought independent financial advice given its recommendation that she do so, and especially given her unfamiliarity with UK taxation laws. In not doing so Mrs N had contributed to the risk that her pension could be adversely impacted by the transfer.

Mrs N said:-

The proposed redress would have significant tax consequences for her as a U.S. resident. As a result the redress would not put her back into the position she should have been had the error not occurred.

She had incurred significant expenditure appointing a representative to pursue the complaint on her behalf. Those costs, and the cost of receiving appropriate cross border tax advice, would continue to rise. Given the complexity of the issues in the complaint, and the tax complications she could not have brought the complaint without specialist assistance.

The redress methodology used by Friends Life show a misunderstanding of Mrs N’s tax position. For instance it has suggested that she would be entitled to a personal allowance, when as a U.S. resident this is not the case.

The wording of the redress must be specifically tailored to avoid potential tax complications in the UK and U.S. Friends Life should pay the costs associated with drafting agreeable wording to avoid those tax complications.

Friends Life should provide an indemnity to cover the potential tax liability arising from the redress payment.

She was very distressed by the situation, has been unable to sleep and it has impacted her health.

On review of Friends Life’s and Mrs N’s responses to the Opinion the Adjudicator made the following points:-

* Friends Life’s offer to pay the unauthorised member payment tax charge and surcharge, less the tax Mrs N would have paid had the pension been paid as an UFPLS, was reasonable in the circumstances. The recommended redress was altered to reflect this.

* The redress was not intended to pay Mrs N’s tax liability. Mrs N was the party subject to the liability and would need to pay this. The redress was intended to make good a relevant proportion of that loss once it had been paid. Under this arrangement the reference to a personal allowance was only notional it did not appear that Mrs N would be subject to punitive tax charges as the redress was intended to make good Friends Life’s error.

* Given the significant impact on Mrs N’s health the Adjudicator increased the proposed distress and inconvenience award to £1,000, which Friends Life agreed to.

Having considered Mrs N’s arguments they do not change the outcome. I agree with the Adjudicator’s Opinion, summarised above, and I will therefore only respond to the key points made by Mrs N for completeness.

Ombudsman’s decision

Mrs N argues that she could not have brought the complaint without employing the assistance of tax and pensions specialist. I do not agree. In the first instance a complaint can be passed to the Pensions Advisory Service, who can guide an applicant through the Scheme’s complaint process and provide technical input where the applicant lacks an understanding of the issues involved. In this case TPAS considered it too late to intervene due to the potential time limits of referral to this Office. So it was not a lack of understanding that prevented TPAS from taking on the case.

Notwithstanding that, had Mrs N not accepted Friends Life’s response to the complaint she could have brought the complaint directly to this Office for review. Although Mrs N’s representative disagrees, I am confident that this Office has the expertise to investigate complaints about pension liberation. I would dispute that: the POS has repeatedly failed to uphold pre-Scorpion complaints on the basis that pension trustees had never heard of pension liberation fraud prior to February 2013 – which is absolute nonsense. The representative’s involvement has not brought any unknown evidence or arguments to the investigation. Mrs N was entitled to seek assistance in this matter, but that does not mean Friends Life are responsible for the costs incurred where there are free dispute resolution alternatives available to her. For that reason I do not consider Friends Life should pay the costs she is claiming. To be fair, I think Mrs N should have had her costs paid. She – and thousands of other victims in this situation – find themselves utterly overwhelmed by these types of cases and need support. Also, being based in the USA, she needed someone to deal with the case in the UK.

I understand that as a U.S. tax resident there may be complications in Mrs N’s tax situation on receipt of the redress payment. Her UK and U.S. accountants have said they will not provide advice on the matter because of the complications. The redress may cause her to have to seek specialist tax advice. However, tax is matter for Mrs N and the local tax authorities. It is not for me to determine any future tax liability she may have, and it may ultimately be that there is none.

I have also taken into account that had Mrs N taken her pension through legitimate means she would have needed to seek tax advice regardless, so in my view the position has not changed. Mrs N will have had to pay for tax advice at some time or another regardless of how the pension was accessed.

Friends Life has said it does not believe that the redress payment would be taxable, but that it would reconsider its position if at a later date it can be shown that Mrs N had suffered a tax liability, although it would not agree to an indemnity. This is a reasonable stance for Friends Life to take. Mrs N should establish any resultant tax liability due to the redress and communicate that to Friends Life if necessary.

Looking at the proposed redress methodology, Mrs N may disagree with certain assumptions made by Friends Life, but I consider they are reasonable assumptions. I note in particular that in relation to the personal allowance, under this notional methodology, she is better off for it being included than if Friends Life assumed no personal allowance.

The approach taken to offsetting the notional income tax that Mrs N would have paid had she taken the full fund value as an UFPLS is balanced and appropriate. This places Mrs N broadly in line with the position she would have been had the pension been taken in full under the current rules. I believe that is an appropriate remedy for the error caused by Friends Life.

Therefore, I uphold Mrs N’s complaint.

Directions

Within 28 days of this determination Friends Life should establish the unauthorised member payment tax charge and surcharge less the notional tax liability of £15,294.34 she would have paid had the full pension been taken as an uncrystallised funds and pay this to Mrs N. PO-9935 7 31. Additionally it should pay £1,000 for the significant distress and inconvenience suffered.

London Quantum is a pension scheme whose trustee was a firm called Dorrixo Alliance run by our old friend Stephen Ward. That name will, of course, send a chill down the spines of many pension scam victims. Since 2010, Ward had been involved – either at the top or the bottom of the pond – in numerous pension scams. He eventually decided to “go straight” and declared that Ark was history – although Ark was far from history for his hundreds of victims who are now facing financial ruin.

Ward’s version of “going straight” was London Quantum. He had learned from the Capita Oak and Westminster scams that the value in getting involved in a pension scam comes from the investment introduction commissions. So he set about building a portfolio for the London Quantum victims which was based purely on how much wonga he could earn – rather than what was right, prudent and appropriate for an occupational pension scheme.

So what were the investments and why weren’t they right for a pension scheme?

The Scheme purchased shares in a unitised currency investment fund which traded in the top ten major currencies. The fund was regulated by the Central Bank of Ireland.

The fund was regulated but according to a regulated investment advisor the fund was inappropriate in terms of risk for the Scheme.

The fund prospectus did not specify a predicted rate of capital growth. However the scheme sponsor had previously stated a predicted return of 12%-15% per annum – an astonishing amount by any stands. But in practice, the fund performed poorly and fell over the period of the investment.

Dalriada Trustees (who replaced Stephen Ward’s Dorrixo Alliance and was appointed by the Pensions Regulator) received advice that, due to the high-risk nature of the fund and, notwithstanding the fall in the value of the investment, the Trustee should exit the fund at the earliest opportunity – irrespective of potentially heavy losses.

In 2014/15, the Scheme purchased nine corporate loan notes. Dolphin specialise in the purchasing of derelict and listed German property. The property is then sold off plan to German investors who take advantage of a specific German tax relief which allows for the recovery of renovation costs through tax allowances when purchasing units within a listed building.

The corporate loan notes were for a period of 5 years with no early exit options. The loans were due to be repaid at various dates between 9 October 2019 to 27 April 2020 depending on when the loans were made.

The loan notes had varied rates of return ranging from 12% to 13.8% per annum. All interest is rolled forward and paid at the end of the 5 year period.

This is an unregulated investment and is high risk in nature. There is no guarantee that the capital and interest will be fully repaid at the end of the relevant 5 year period. Dalriada had received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

London Quantum One Limited

The Scheme had purchased shares in London Quantum One Limited (“LQOL”). LQOL holds rights to a social media application called VIP Greetings which provides personalised messages with the use of celebrity endorsement. The original trustees paid for the LQOL shares from the scheme funds.

The underlying investment in VIP Greetings was long term and no returns were expected for several years. No early exit options exist and there is no evidence of a secondary market to sell the investment.

The returns from VIP Greeting application are highly speculative. These is no guaranteed minimum return or definitive payment date. Investors hold no security over any physical asset.

A number of valuations in relation to the VIP Greetings investment were received prior to the appointment of Dalriada Trustees. The valuations appeared highly speculative. In addition, the valuations were not made at the time that the Scheme purchased the investment.

Dalriada suspects that the investment holds little, or more likely, no value. They are not confident that any return will be made to the Scheme.

Between 2014 and 2015 the Scheme purportedly invested in 17 car parking spaces in a car park near Glasgow Airport. The investment was offered by Park First Glasgow Limited who lease parking spaces to investors, in this case the London Quantum, and then sub lease the parking space back.

The investor enters a lease for a period of 175 years (the maximum allowed under Scottish law). The parking spaces are then sub-leased back for a period of 6 years. The sub-leases can be terminated by Park First after 2 or 4 years, or at any time with not less than 10 days notice if it has found a substitute sub-tenant.

There is a ‘guaranteed buy back’ policy which outlines under what circumstance Park First will buy back the parking spaces. Park First has full discretion in this regard and is under no obligation to buy back the spaces at any point. In short, there is no guaranteed exit option.

The investment offers a guaranteed rate of return of 8% per annum for the first 2 years. To date payment in line with the 8% return had been received. £27,200 was received in February 2015 and a further £27,200 was received in February 2016. No payment was received for February 2017.

This is an unregulated investment. Park First operate the car parking space on behalf of the investor for an annual fee. The parking spaces generate income which is ultimately passed back to the investor each year.

Dalriada received advice that the investment was illiquid and inappropriate for the Scheme and early exit was recommended.

Dalriada have tried to recover the monies paid to Park First arguing that the legal documentation was never fully completed by the previous trustee and that the contracts were ineffective. Park First has rejected this request and is insisting that the contracts are valid and that there is no scope for Dalriada to be refunded.

On 20 August 2013 the Scheme invested in an unsecured loan note issued by the law firm Malletts Solicitors Limited.

The loan note had an investment period of 6 years with an obligation for the note holder to redeem 25% of the note per annum after year 2. No early exit options existed.

The loan note purported to return 8% per annum payable half yearly.

Interest or redemption payment have not been made by Mallets. To date the Scheme should have received payments totalling £3,280.00 as per the contractual documentation.

Loan notes have been issued by Mallets in an attempt to raise funding for an internal ‘legal hub’ project. The loan note was unsecured.

Dalriada contacted Malletts to obtain additional information in relation to the investment. Mallets have refused to explain how the Scheme came to be invested with them and have only provided minimum details

Dalriada had received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended. They sent Malletts a number of formal requests to exit the investment however Malletts did not respond.

Malletts Solicitors Limited went in liquidation on 11 November 2016. Dalriada submitted a proof of debt respect of the loan note but the fact it has gone into liquidation suggests prospects of recovery are poor.

On 31 January 2015 the Scheme invested in a corporate bond with Colonial Capital Group Plc. Colonial operates in the distressed US social housing market and have issued a number of bonds.

The corporate bond is for a period of 3 years. No early exit options exist. The bond has a fixed return of 12% per annum. Interest will be rolled forward and paid at the end of the 3 year investment period.

This is an unregulated investment. Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

Dalriada sent Colonial a formal request to exit the investment. Colonial responded and confirmed that an early exit was not available as Colonial may only redeem all or part of the bonds on a pro rata basis for all investors. It would therefore not be possible to facilitate an early exit for the Scheme.

Colonial Capital Group Plc was then placed into administration on 8 March 2017. Dalriada has issued a proof of debt in relation to the corporate bond but, again, the fact the company has gone into administration suggests prospects of recovery are unpromising.

The investment is in hotel rooms in a hotel development by The Resort Group. The hotel has recently been completed in Cape Verde and investors purchase a right to benefit from the profits and interests of specific pieces of the development. Investors do not own the land nor do they have a charge over it. An investor has simply a right to share in any profit generated from the hotel rooms.

The investment could not be exited prior to completion of the hotel rooms. Now that these have been completed they can be sold on the secondary market.

Before completion of the hotel rooms a guaranteed return is paid. After completion the return is based on room occupancy. The expected returns have been paid to the Scheme.

This is an unregulated investment. Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

The Resort Group offered to repay the amount transferred to it by the Scheme. That offer was to release one plot every two months from 31 October 2016 subject to completion of legal agreements. Dalriada agreed to this offer and signed the agreements in December 2016.

The Reforestation Group Limited

The purported nature of this investment is that the Scheme has purchased ‘land rights’ to 21 plots of Brazilian farm land that is to be used for growing eucalyptus trees. The investment term is 21 years as it covers three cycles of seven years, which is the projected time period to grow and harvest the trees. The investment purportedly offers returns of 28-32% compounded over each seven year cycle.

The crop cycle of the eucalyptus tree is seven years. Accordingly, with the investment being made in 2014, the first return on any of the Land Rights Agreements (”LRA”) would not be realised until around 2021.

The estimated return after 7 years is £19,000 per hectare, which is a 90% return. There are a number of issues with this development which Dalriada finds concerning and are being investigated.

Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

Dalriada, through the Scheme’s legal advisers, has written to Reforestation to seek further details regarding this investment and to seek justification for the apparent high level of returns promised.

The investment consists of 11 Bonds over three different series and made between 27 October 2014 and 15 May 2015. The Bonds mature after four years from issue but can be redeemed early after three years (upon six months’ notice) or otherwise with ‘the express consent of the directors of ABC Alpha Business Centres Limited’.

Investment returns depend on the series of the Bond and range from 8.11% to 8.25% with and additional bonus if the Bonds are not redeemed early.

In relation to the two series of Bonds, the Scheme has elected not to have ‘rolled up’ interest. This means that interest is due and payable to the Scheme on a quarterly basis. These payments were made until Q4 2016 but stopped when ABC Alpha Business Centres UK Limited and ABC Alpha Business Centres VI UK Limited went into administration on 20 January 2017.

The Bonds are corporate bonds in ANC UK Limited. ABC UK Limited is the capital raising vehicle for the investments. ABC UK Limited is wholly owned by a United Arab Emirates (UAE) entity, ABC LLC. ABC LLC owns and operates the investment portfolio of real estate investments.

ABC LLC is wholly owned by another UAE entity, the Property Store. The Property Store purportedly provides security of 200% of the value of the invested funds.

Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended. An offer was made to buy back the Bonds subject to a 10% reduction. As noted above, interest payments stopped, and the offer was withdrawn when ABC Alpha Business Centres UK Limited, and ABC Alpha Business Centres VI UK Limited, were put into administration on 20 January 2017. Dalriada has prepared a proof of debt in relation to the investment but, as with others above, there is a risk that recovery prospects will be poor.

This unregulated investment consists of a “lease” on 7 car parking spaces in a new office development in Dubai taken out between 1 October 2014 and 17 April 2015. Under the Operator’s Agreement, there is 5 years guaranteed rental income

The Scheme is liable to pay the car park operator, The Property Store, 10% of any income greater than the guaranteed rental income. Once the guaranteed income period comes to an end the Scheme must pay The Property Store 10% of any income that is received from the car parking spaces.

The guaranteed rental income is paid monthly. It had been paid on time up to Q4 2016 when an issue with car park operator meant payments were stopped.

All of the car parking spaces that the Scheme has leased are located at Churchill Towers, Dubai. NCP Ltd owns the freehold of these car parking spaces. The contractual position is not clear due to incomplete documentation however it would appear that the investment operates as follows:

NCP Ltd owns the freehold and has assigned full commercial rights over the car park spaces to Horizon Properties SA; Horizon Properties SA has granted the Scheme a 99 year lease over each of the seven car park spaces; the Scheme has entered into an Operator’s Agreement with The Property Store with no set term for each of the seven car parking spaces.

Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

An offer was made to buy back the car parking spaces subject to a 10% reduction. The £189,000.00 investment would return £170,100.00 plus the income received (£13,165.20 – 6.97% return). The offer was within a range that might have been acceptable however before it could be accepted Best Asset Management Limited removed the offer from the table. Dalriada is corresponding with Best in relation to the options for the investment.

So, in other words, a load of old rubbish. But then what would you expect from Stephen Ward who has destroyed thousands of victims’ life savings since 2010. He may be a highly qualified “pensions expert”, and the author of the Tolley’s Pensions Taxation Manual, but that doesn’t mean that he should ever be allowed anywhere near people’s pension savings.

The other questions that should be asked are:

why did HMRC allow the pension scheme to operate in the full knowledge that Stephen Ward was the trustee?

why has FCA-registered Gerard Associates, who were “advising” the victims not been removed from the register and sanctioned?

why did the ceding providers (including the trustee of the Police Pension Scheme) not do their due diligence and question the transfer requests?

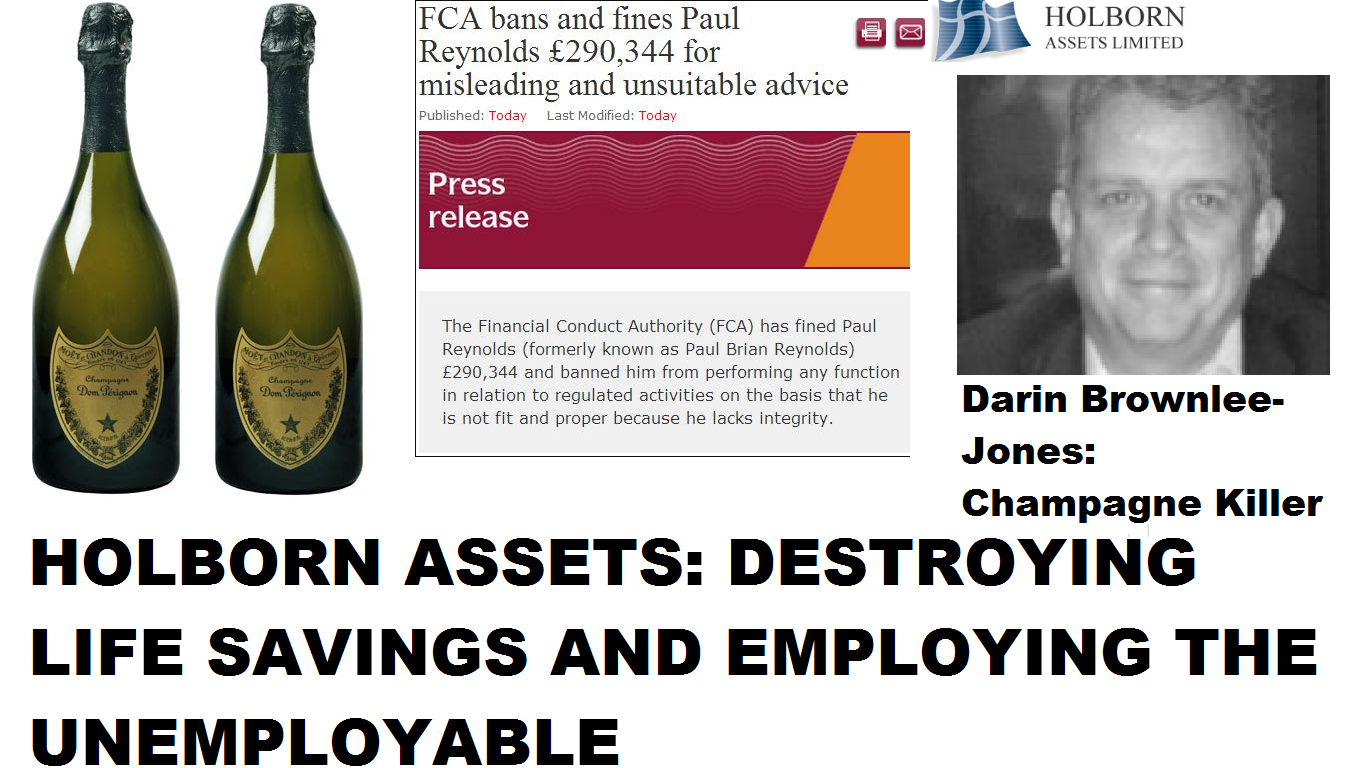

Holborn Assets Warning: their rogue advisers can seriously damage your life savings – and your life

Holborn Assets: This Toxic Dubai Firm Comes with a Health Warning

Holborn Assets can seriously damage your life savings – and indeed your health and even life.

Holborn Assets does have a few decent advisers. When I published the “Champagne Killer” blog last week, I was contacted by over a dozen advisers who asked me (courteously and respectfully) to remove their names and profile links from the blog. This I did immediately in all cases except Gerard Frew who was simply rude and abusive.

Quite a few of these advisers had had no idea they worked in such a cess pit. None of them seemed to have had any idea about Paul Reynolds and Darin Brownlee-Jones. They appeared unaware that the FCA had ruled both individuals unsuitable to be financial advisers. And they didn’t seem to know that some advisers at Holborn Assets are routinely destroying victims’ life savings – and Bob Parker simply shrugs the complaints off.

A couple of the “good guys” raised the point that if one person at Barclays had done something wrong, it did not necessarily mean that all the other staff at Barclays were rotten. A valid point, perhaps, but if there was a rotten apple at Barclays, they would get sacked – whereas Bob Parker deliberately goes out and picks rotten apples because they have no principles, no scruples, no hesitation in scamming people out of their pensions and investments. And they make Uncle Bob lots of money.

The advisers who contacted me claimed to have unblemished records (which they didn’t want to be besmirched by the likes of Reynolds and Brownlee-Jones). But the question is: if they have good records, what on earth are they doing working at Holborn Assets? If they care about their professional reputations, why not go and work for another firm which is not full of cowboys and run by a man who cares not a jot for the distress his firm causes to innocent victims.

Let’s have the drains up on how Holborn Assets really works and see how and why it is so “successful”.

HOLBORN ASSETS KUALA LUMPUR:

Holborn Assets has a team of about 50 “contact generators” based in Kuala Lumpur (where labour is cheap). They trawl social media for names and contact details.

The leads are passed to a company in the UK set up by Holborn Assets to run as a cold calling “boiler room”. They used to use a boiler room in Manchester for their cold calls, but now they’ve got their own: The Retirement Shop. The company was set up in September 2016 and has two directors: James Patrick Parker and John Cornelius Parker who was arrested and charged after extreme violence against fans and police at a football match in 2002. Presumably, they are relatives of Bob Parker – James lives in the UK and John in Dubai. In fact, when you call The Retirement Shop, James Parker answers the phone.

Holborn Assets’ cold calling boiler room, The Retirement Shop, has around 40 callers – mostly young, poorly-educated people desperate for work. Bob Parker pretends this company is in Bournemouth, but it is actually based in Sale, Cheshire. The cold callers basically bombard people throughout the UK and offshore with calls designed to book a telephone call and/or meeting appointments with Holborn Assets advisers.

Bob Parker is enthusiastic about this “lead generation” scam as the cold calls come from a UK number, so it’s less likely the potential victims are going to drop the call. Holborn Assets also uses a voice-over IT system that can change the number so that victims in – say – Saudi will see a Saudi number come up even though the call is actually coming from the UK.

Holborn Assets openly admits to doing cold calling in Saudi but in Dubai Bob Parker wants to conceal the company’s cold calling operation so he pretends the calls come from an allegedly entirely separate and independent company (The Retirement Shop) – which is, of course, controlled and run by Bob Parker himself. This is what Parker calls “warm calling”.

The way that Holborn Assets’ cold (or warm) calling operation works is that they have 16 to 20 year olds calling from The Retirement Shop to potential victims in the UK or anywhere in the world. Working from a prepared script, the caller asks the person if they’ve got a pension, and if they keep up to date with it. The caller is instructed to tell the victims the company works alongside HMRC, then to ask them loads of questions such as whether they know about legislative changes. Then the caller says he will get a “specialist” to call – so the lead is now “warmed up”. Bob Parker thinks this is “quite clever really”.

How does The Retirement Shop “package” itself? The company claims that: “We have assisted thousands of clients all over the world to transfer their frozen UK pensions and plan for their retirement. To date, we have helped successfully transfer over 500 million Pounds worth of frozen UK pensions. We are amongst the best at what we do.”But as the company was only registered in September 2016, how can it possibly have “assisted thousands” of clients since then? But the thought of Holborn Assets handling £500m worth of pension transfers is utterly blood curdling.

The Retirement Shop‘s website further claims to be “UK Qualified”, “Experts in UK Tax Law”, have “Knowledge in UK Pension Transfers” and “We also link you up with UK qualified pension specialists across the globe”. In fact, none of these claims is true – especially the last one as the only “pension specialists” they link people up with are those at Holborn Assets Dubai. And that firm is not licensed to provide advice in many jurisdictions.

Holborn Assets rogue advisers can wipe out at least half your life savings in a heartbeat.

Having been cold called and “warmed up” by Holborn Assets’ boiler room scammers, what sort of investment advice is the victim likely to receive? Various victims have seen heavy losses due to negligent, unregulated, unqualified advice into entirely inappropriate, high-risk, illiquid assets. This includes one victim’s $600k life savings – half of which were invested in New Earth Recycling (which, of course, was paying the best investment introduction commissions).

So why would decent, ethical, conscientious advisers choose to stay at Holborn Assets? Do they really want all this toxic, unethical practice to rub off on them? Do they want their leads to come from Bob Parker’s boiler room scammers in Kuala Lumpur and “Bournemouth”?

Lastly, why don’t they all get together and tie Bob Parker to a chair then slap him with a wet fish and a copy of the Bible until he agrees to pay proper compensation to the Holborn Assets victims?

I got into an interesting debate with Frances Coppola on Twitter last night (a very auspicious date: 17.7.17). Frances is a very knowledgeable and capable pension person – with whom I don’t always agree – but she always conducts herself with me in a dignified and respectful fashion and I much admire her expertise.

She said “You were never told you were entitled to a pension at 60. You may have believed that, but that’s not the same as being told.”

If that is true, then this was one of the greatest magic tricks of the last century – all women born in the 50’s thinking/imagining/dreaming they had been told the same thing; at the same time; in the same way; entirely independently. And then all thinking/imagining/dreaming they hadn’t received the letters the DWP alleged they had sent advising the cohort – of which I am one – that the imaginary dream we had all had about receiving our State Pension at 60 was going to be changed to 65, 66, 67 or 68.

This does, of course, beg the question: if we had never been told we were paying our NI contributions so we could receive our State Pension at age 60, why did the DWP subsequently claim they had moved the goalposts to age 66? Surely, if they had never told us in the first place, they wouldn’t have needed to tell us otherwise? And who can provide any evidence that from an early age we Cohorts had paid our NI contributions so we could receive our State Pension at some undetermined age from middle to late sixties – or beyond? Wouldn’t one or two of us have queried this state of affairs?

But the point of this blog is not to scratch the scab of the whole WASPI debate, but to look at the thorny question of “equality”. WASPI opponents bang the drum that we don’t want equality – but are seeking “preferential treatment” over men. I can’t speak for WASPI members, but here is my take on this equality/inequality issue:

As little girls, we were generally segregated from little boys in many different ways – and treated differently because it was accepted that our lives would be different when we grew up. At school we did needlework, domestic science (including ironing, cooking, cleaning the silver) and in general our whole academic and sporting education and development were geared towards our femininity. The boys were steered towards metal work, carpentry, football, rough and tumble and engineering.

As we got older, our education, families and society in general taught us that we needed an “interim” career to prepare us for being wives and mothers. In many different social classes, large numbers of young women prepared to be nurses, secretaries, shop workers so we could have a job we could return to once we had married and brought up our children. We were taught that it was a man’s job to go out to work and bring home a wage for the family, and the woman’s job to keep a good home, put a decent meal on the table, and bring up the children.

I remember being a first-time mother in Edinburgh in 1980 and going back to work a few weeks after my baby was born. And I was treated like a pariah. Many mothers were so treated in Scotland, England and Wales (and undoubtedly Northern Ireland). In fact, I had been unceremoniously sacked by my employer when I announced my pregnancy as they didn’t think I was capable of continuing to work either throughout my pregnancy or after my baby was born. I do not believe this was entirely untypical back then.

We women earned considerably less than our male counterparts and were not entitled to occupational pensions. So we never had the opportunity to build up pensions of our own – and for those of us who were widowed or divorced, we were left hung out to dry in later years. In fact, many of us also had the additional responsibility of looking after and supporting our elderly parents or parents in law.

Does anyone remember the term “housewife” being replaced by “domestic engineer”? I do, and I remember the challenges of looking after and juggling the multiple responsibilities of young children, a home, a husband who was often tired and grumpy, and my own health/well-being/emotional stability. It wasn’t easy. And when my father died and my mother developed dementia it got harder still.

This isn’t about me – but this will be a situation with which many WASPI members will be entirely familiar. And here’s where we come to the “equality” bit. How many men gave birth to a number of children? How many men never had the opportunity of occupational pensions? How many men never had their own income but relied on the dregs left over after the bills were paid and the children supported? Yes, I know many men worked their backsides off in a wide variety of different jobs and professions. But there was a clear distinction between the situations and opportunities afforded to men and women in the 60’s and 70’s.

We women gave our lives to supporting our husbands, families, children, homes – and working as much as would could depending on our domestic circumstances. And now we’ve been shafted, are being told to “get over it” and accused of not wanting equality. We weren’t equal back in the 60’s, and we can’t backdate equality now.

So whether we were told, or we believed, or we imagined, or we hoped we would receive our State Pension at age 60, we didn’t. We haven’t. We won’t. And this gimpy government with which we are unfortunately saddled can make all the excuses in the World, but it won’t change the fact that a major part of the backbone of British society – 1950’s women – were told we would receive our State Pension at age 60.

Many of us gave up career and pension opportunities to look after our families. None of us entered into marriages and families assuming we would become widowed or divorced. None of us imagined that in addition to looking after our children we would also have to look after our parents.

But perhaps the most sinister and incomprehensible part of the whole WASPI matter is the number of MPs and ministers who have refused to acknowledge the WASPI problem on the basis that the State could not afford to introduce transitional arrangements. WASPI women are not asking for an unfair advantage over men – they are asking for something which approaches and addresses (albeit inadequately) the inequitable position of women who were not given the opportunity to make revisions to their retirement arrangements.

Our only crime is that we are living too long. We refuse to die on time. Despite the demands on our bodies of child birth and domestic industry, we have failed to pop off on time. My posturing will make not a blind bit of difference, of course.

Frances Coppola can keep on saying we were told that our SPA would be increased and that we were never told we could expect to receive our SP at age 60 all day long. But that does not change the fact that there is very considerable hardship for many 1950’s-born women who did believe they could expect to receive their SP at age 60 and who are now unable to get jobs to support themselves. Many of these women are in desperate need of transitional arrangements. These women paid their NI contributions all their working lives, brought up their children, supported their husbands and lived an unequal life. But now the State wants to backdate equality.

Holborn Assets mercilessly leaves its victims facing financial ruin

HOLBORN ASSETS “CHAMPAGNE KILLER” APPROACH TO FINANCIAL ADVICE IS DESTROYING VICTIMS’ LIFE SAVINGS

Holborn Assets “Champagne Killer” approach to financial advice is ruining victims. Holborn Assets is routinely destroying people’s pensions and life savings, and refusing to compensate the distraught victims facing poverty in retirement. The so-called “advisers” at Holborn Assets give investment advice (often unregulated) which entails investing victims’ funds in whatever toxic, illiquid, high-risk rubbish pays the highest commissions, and then leave the devastated investors hung out to dry. Neither the firm nor the “advisers” responsible for this outrage show any compassion or contrition. This is no different to the callous actions of a common drunk, hit-and-run driver.

As if this wasn’t bad enough, Holborn Assets also employs Darin Brownlee-Jones: the “Champagne Killer“. A drunk hit-and-run driver who killed an innocent man then walked away to drink champagne. He didn’t stop to try to help the victim he left dying in the road – or show any remorse for the horrible, painful death the poor man suffered.

Holborn Assets seems to make a habit out of employing the unemployable. First, there was Paul Reynolds who was banned by the FCA and fined nearly £300,000 for giving unsuitable and misleading financial advice. The FCA declared Reynolds was not a fit and proper person to give financial advice. But Uncle Bob Parker of Holborn Assets Dubai welcomed him with open arms – and Reynolds has since changed his name to try to conceal his unsavoury past. But I bumped into Reynolds when I was at the Holborn Assets office at the end of 2015 – so I know it is him despite trying to change his appearance as well as his name.

And now there is Darin Brownlee-Jones who is commissioning pension reports for more poor unfortunate victims. These people are transferring their defined benefit pension schemes to offshore QROPS in dodgy jurisdictions where negligent trustees peddle their toxic wares. In one case, Brownlee-Jones has employed a Spanish firm to sign off a DB transfer for a resident of France. The advice is covered (allegedly) by the Spanish insurance regulator (which doesn’t cover pension or investment advice) and not the French regulator or the FCA.

So why would Brownlee-Jones in Dubai get a Spanish firm to provide unregulated advice to an investor in France? In 2003, the FSA had refused an application from Brownlee Jones to perform investment and pension-transfer functions. The reason was that the FSA did not consider him to be a fit and proper person as he had indecently assaulted a woman, caused criminal damage and death by dangerous driving.

I think any reasonable person would agree that Brownlee-Jones was the last person you would want handling investment and pension advice. But Bob Parker at Holborn Assets clearly likes having misfits, FCA rejects, sex offenders, drunks and killers on his team.

Brownlee-Jones: after a belly full of beer in 1999, got into his car and hit a motor cyclist head on. He left the poor man dying in a pool of blood and went to celebrate at his favourite wine bar. He ordered two bottles of Dom Perignon champagne at £95 apiece. When he was arrested, he was quaffing his favourite bubbly – although he probably wasn’t smiling quite so broadly when he was jailed for four years.

The distraught father of the victim said that Brownlee-Jones had treated his dying son “like an animal“. And yet Bob Parker employs this callous killer and encourages him to provide unregulated pension advice to victims in France and Spain.

This routine callousness is shown by Bob Parker and many other Holborn Assets salesmen. Where their victims’ pensions and investments have been decimated by high-risk structured notes and unregulated, toxic, illiquid funds -such as Premier New Earth Recycling – Holborn Assets just shrugs and leaves the victims to face poverty in retirement. Once they have earned their fat commissions from the victims’ pension funds, Holborn Assets doesn’t want to know any more. Bob Parker and his merry men simply walk away without a backward glance.

Holborn Assets has been aggressively targeting new victims with a cold-calling campaign using a well-known boiler-room scam operation in Manchester. The cold calls to Spanish residents are followed up by salesmen such as Jason Ryder who claims that Holborn Assets have offices in Barcelona and Marbella. Of course, Holborn Assets is not licensed to operate in Spain – and once conned into letting these cowboys plunder their pensions for fat commissions and fees, there is no regulator to complain to.

Apart from Bob Parker, Paul Reynolds, Darin Brownlee-Jones and a bunch of other “snake oil salesmen”, there are some people at Holborn Assets who do have some ethics and a conscience. Surely, if these people had any sense they would distance themselves from this cesspit of financial disservice? Why stay with a firm with such an appalling track record?

Below is a list of all the people who work for Holborn Assets (excluding admin and finance). I wonder if a single one of them will feel some sense of disgrace at being a part of this “champagne killer” approach to financial services?

If not a single one of the above group of people is prepared to put ethics and principles at the top of their agenda and ensure their professional reputations are not sullied by the “champagne killer” approach to financial advice, then there truly is no hope for Holborn Assets.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

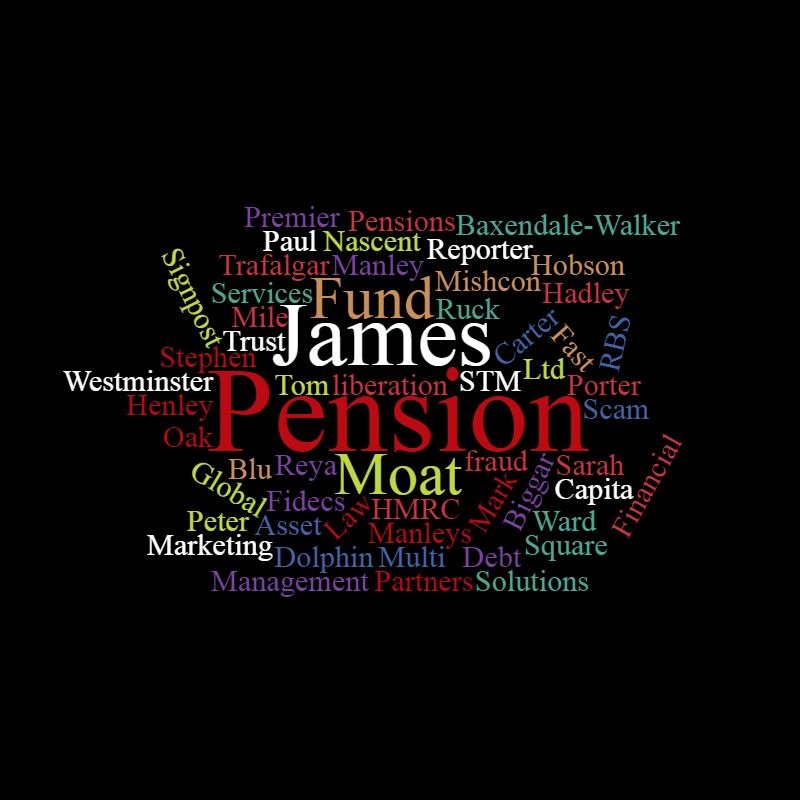

SAIL FINANCIAL AND TRAFALGAR MULTI ASSET FUND: What is the connection?

Who is behind Sail Financial? And what is the connection to Trafalgar Multi Asset Fund? We know Trafalgar Multi Asset Fund was originally run by XXXX XXXX as “Victory Asset Management” and that XXXX had also been behind the Capita Oak, Henley Retirement Benefits Scheme and Westminster pension scams: wound up by the Insolvency Service; now in the hands of Dalriada Trustees and under investigation by the Serious Fraud Office.

We also know that the £120 million of store pods purchased for Capita Oak, Henley RBS and hundreds of SIPPS are now probably worthless and Store First is subject to a winding up petition due to be heard on 1st August in Manchester.

In addition to being the Investment Manager of the Trafalgar Multi Asset Fund, XXXX was also the “financial adviser” in the form of his firms Global Partners Limited and The Pension Reporter – a “trading style” of XXXX’s Nationwide Benefit Consultants. But none of these firms were licensed for pension or investment advice.

However, Joseph Oliver’s Marcus Groombridge has stated:

“I can confirm that XXXX XXXX and Nationwide Benefit Consultants Ltd were appointed on the 29th of May 2014 and terminated on the 8th of April 2016. The permission for insurance mediation covers pension advice.”

Phew! What a relief. I am now looking forward to Mr Groombridge’s full cooperation with putting XXXX XXXX’s victims back into the position they should have been in had they not been scammed into investing their pensions in the Trafalgar Multi Asset Fund in the first place. I will also probably remind Mr Groombridge that the Trafalgar matter is under investigation by the Serious Fraud Office – along with other pension scams “distributed” by XXXX XXXX in 2012/13.

If there hadn’t already been enough misery for the hundreds of victims of the Capita Oak and Henley Retirement Benefit schemes run back in 2012/13 – XXXX had also been operating pension liberation in the form of “loans” from his company Thurlstone, based in the Seychelles. The victims have now been sent tax demands. But XXXX and his solicitor, Mark Manley of Manleys Law, have ignored pleas to indemnify the victims from these crippling tax liabilities.

I have often wondered what people like XXXX do after their latest scheme collapses or implodes. History tells us that they simply get straight on with their next one – and in fact had probably started it already. XXXX has been a director of seven companies (according to Companies House):

Nationwide Benefit Consultants (active)

Nationwide Corporate Benefits (active)

Proactive Administration Solutions (active)

Nationwide Trustee Services (dissolved)

Ashton Abbott (dissolved)

Nationwide Tax Administration (dissolved)

Admin Protection (dissolved)

XXXX has resigned from Nationwide Benefit Consultants and Nationwide Corporate Benefits – and appointed someone called Raymond Hampton as a director. But XXXX remains a director of Proactive Administration Solutions. So perhaps that is one to watch.

XXXX’s background is in the “distribution of pension schemes” (his words). He has worked closely with the cold-calling and lead generation firms (such as Jackson Francis, Sanderson Clarke and Barncroft Associates run by XXXX´s mates Ben Fox and Stuart Chapman-Clarke) who were involved in the Capita Oak and Henley scams.

So what is XXXX doing now? Perhaps whatever project he is working on involves trying to make enough money to compensate the victims of Capita Oak, Henley, Westminster and the Trafalgar Multi Asset Fund – all of the schemes are now under investigation by the Serious Fraud Office. It is also probable that Gibraltar Trustees STM Fidecs no longer want terms of business with XXXX XXXX now that so many of his schemes are subject to criminal investigations. STM Fidecs also probably now realises it was a serious conflict of interest taking business from an adviser who was also the Investment Manager to the Trafalgar Multi Asset Fund – which is now in the process of being wound up.

While I was idly puzzling over what XXXX´s next scheme might be, I started hearing reports about a firm called Sail Financial doing the rounds of firms in Europe – touting offering to do “introducing” and cold calling. Looking at the Sail Financial website, it is impossible to see who is involved in the business – no names, no address, no regulation. According to the Companies House register, Sail Financial – incorporated on 8.5.2015 – has two directors: Robert Hathaway and Brian Westhead. Neither of those names rang any bells with me.

Hathaway has no other directorships listed. However, Westhead does: he is listed as a director of a dissolved company called BIGB22 (08559856). This company’s previous names were Portia Financial and The Pension Reporter: XXXX XXXX’s firms. These firms have a history of being involved in pension and investment scams, cold calling and unregulated financial advice. The victims of the Trafalgar Multi Asset/STM Fidecs pension and investment scam were introduced and “advised” by Portia Financial, GPL (Global Partners Ltd) and The Pension Reporter, with advice letters signed by XXXX XXXX and Tom Biggar.

So clearly there is a connection between Sail Financial and various firms and schemes run by XXXX XXXX – including Trafalgar Multi Asset Fund. Perhaps XXXX XXXX is sailing round the Mediterranean now? I just hope he doesn’t have one glass of champagne too many and fall overboard.

A fund like Blackmore Global really ought to be audited as soon as possible – to make sure it isn’t simply a “black hole” into which victims’ hard-earned pensions have sunk. Numerous worried pension savers are stuck in the Blackmore Global Fund and finding it difficult – if not impossible – to get out. They are seemingly “locked in” for ten years.

I WOULD LIKE TO EXPRESS MY SINCERE THANKS TO THOSE – INCLUDING IFAs, PENSION TRUSTEE FIRMS AND BLACKMORE GLOBAL VICTIMS – WHO HAVE CONTACTED ME AND SUGGESTED IMPROVEMENTS, CORRECTIONS AND ADDITIONS.

Allegedly, Grant Thornton is working on an audit – and has been doing so since September 2016. They could probably have audited Microsoft in that time – and squeezed in Amazon on the side during the lunch breaks. Just how difficult can it be to audit a fund which only has a handful of assets in it?

Originally, the directors of Blackmore Global were Brian Weal, Patrick McCreesh, and Phillip Nunn.

Brian Weal – sanctioned by the FSC in 2014 – was also a director of Swan Holdings – the only investment that the Advalorem Value Asset Fund made. Brian Weal was also a director of Advalorem. Advalorem lost most of its money because the investments in Swan Holdings were overvalued. The valuations were supplied by Stuart Black who also provided valuations for a Hedge Fund called Heather Capital which lost $300 million because of overvaluations. Swan Holdings had invested a chunk of cash in Etaireia Investments. Stuart Black was a director of Etaireia Investments. Brian Weal owns a controlling number of shares in Etaireia Investments. So, make up your own mind as to whether having Weal as a director of Blackmore Global is a good thing or a bad thing – or a “black hole” thing.

As for Nunn and McCreesh, I will let Leonard Fenton of the Insolvency Service do the talking:

Documents and information received from members of CAPITA OAK indicated they were initially contacted by Craig Mason or Patrick McCreesh of Nunn McCreesh of Its Your Pension Ltd and offered pension review services prior to them being referred to JACKSON FRANCIS or Sycamore for the transfer of their pension to CAPITA OAK.

On 3.3.15 I received an undated letter in which it was stated that Its Your Pension had not traded and was a dormant company and that Nunn McCreesh had traded as an insurance brokerage between 2009 and 2012 when they entered into a verbal arrangement with TRANSEURO where in return for providing pension leads to JACKSON FRANCIS they received a commission from TRANSEURO.

Nunn McCreesh provided JACKSON FRANCIS with 100-200 leads per month which were provided by email and/or telephone for which they received £899,829.86 from TRANSEURO during the period 26.3.12 to 14.5.14.

So, again, draw your own conclusions about those connected with Blackmore Global. Nunn and McCreesh generated up to 200 leads a month to pension scammers in relation to a series of pension/investment scams which are now under investigation by the Serious Fraud Office. This entailed £120 million worth of pensions being invested in Store First store pods which are now the subject of a winding up petition – and arguably worthless.

When I first started investigating the Blackmore Global fund in 2016, I started with the brochure which makes all sorts of grand claims: “medium to long-term investment vehicle with a diversified investment portfolio under one structure. The Company allocates investment between four distinct protected cells, giving a true diversification of assets between property, sustainable, private equity and lifestyle”. Yeah, right. But what are the underlying assets? Where is the audit?

The Fact Sheet goes on to claim the fund’s NAV is £17.65 million and was launched on 1st May 2014. So why no audit? It also claims that the Investment Manager is a firm in Barcelona called Meriden Capital Partners. I thought it a bit strange that a fund based in the Isle of Man would appoint an investment manager in Spain – especially one without a website. So I called Meriden Capital Partners and asked them to confirm that they were the investment manager. They claimed they had never heard of Blackmore Global. Then one of the partners called me back and told me that some man who didn’t give his name had come to their office and asked them whether they would be interested in being the investment manager for Blackmore Global.

The partner at Meriden Capital explained that they had declined because they were not licensed to provide investment management advice to a fund – only to private individuals.

But then I discovered that that hadn’t been entirely true either. Meriden Capital had actually completed an application form to apply to become the investment manager to the fund on 4th April 2014. So either Meriden Capital was lying or Blackmore Global was lying – or both.

The Blackmore Global NAV Factsheet also states that there is a ten-year lock-in to the fund. So why would anyone invest a pension in such a fund? A pension saver has a statutory right to a transfer and might want to take his PCLS – 25% tax free withdrawal at age 55 – or retire, or even die. What on earth is the point in using Blackmore Global for a pension at all? Ever.

As Grant Thorton is clearly having a little trouble with the audit of a five-cell investment fund, I will lay a wee trail of bread crumbs for them to look at. Clearly they can’t even find the underlying assets – let alone value them:

Spinaris 90 – UK sports spread betting (invisible – and what happened to Aria Invest?)

Most of the victims of the Blackmore Global fund were initially cold-called by a firm called Aspinal Chase. And all the victims were advised by unregulated investment advisers Square Mile Financial Services (an insurance license does not cover regulated investment advice). But more worryingly, all of them were put into a QROPS in Malta or the Isle of Man. So why were UK residents transferred to an offshore pension at all, and why were most or all of their pension funds invested in a UCIS which is illegal to be promoted to UK residents?

The list of questions goes on and on. And here, we get back to whether the unscrambling of these pension and investment scams is more about who you know rather than what you know. One victim had his pension invested 75% in Blackmore Global and 25% in Symphony. Symphony was a fund invested in derivatives and highly leveraged. It was also a sub fund of the Nascent Fund run by Richard Reinert. Under the Nascent “umbrella” (a structure for wannabe fund managers) was also the Trafalgar Multi Asset fund which was run by XXXX XXXX who was one of the main distributors behind Capita Oak, Henley and Westminster – all of which are being investigated by the Serious Fraud Office.

Now we have gone round in a complete circle. A catalogue of lies, deception, fraud, mis-selling, negligence and incompetence.

I don’t envy Grant Thornton (if indeed they are the auditors) because they have got to unscramble this unholy mess. And I strongly suspect that, behind the scenes, there are certain parties who are busting a gut to ensure the audit is never published. Two of these may well be John Ferguson and David Vilka of Square Mile in the Czech Republic who seem to have a strong vested interest in promoting this black hole of a fund.

Meanwhile, the longer the victims are held back from transferring out of this toxic swamp of a fund, the more serious the complaints against the various parties involved will be. These will include the cold-calling scammers; introducers; advisers; pension trustees and insurance companies such as Investors Trust who allowed this investment and the pensions transfers from unlicensed advisers.

Finally, on the subject of Investors Trust, they showed not a shred of interest in the fact that they had facilitated financial crime in allowing UK residents to have their pensions invested in this UCIS, but when I published a photo of John Ferguson and David Vilka posing as a couple of gaudily-dressed spivs in Las Vegas, Investors Trust objected on the grounds the photograph was their property.

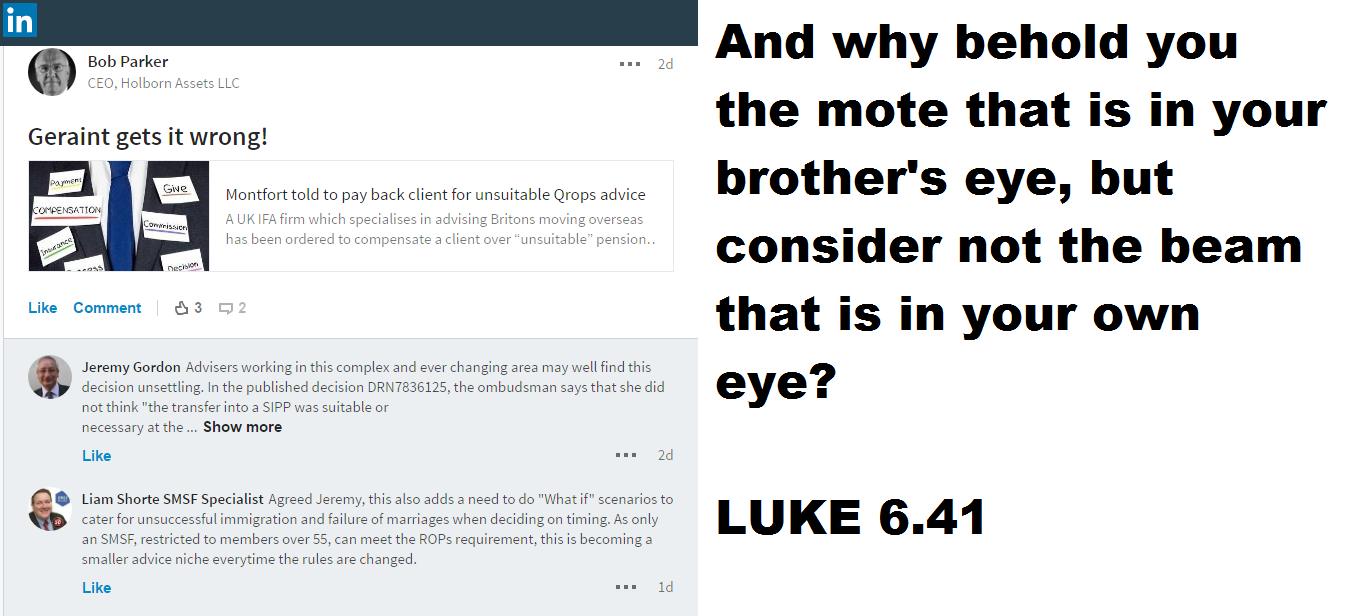

Holborn Assets’ Bob Parker commits a gloat too far.

Holborn Assets Dubai – under the questionable leadership of Bob Parker – has been responsible for ruining quite a number of victims’ pensions. With a deft waggle of the Holborn Assets magic wand, a pension transferred from a gold-plated final salary scheme can be reduced by at least 50% in just a couple of years. Trouble is, the magic kind of runs out of steam if asked to work in reverse.

Glynis Broadfoot and various other victims in Spain were “advised” by dodgy Holborn Assets’ advisers to transfer their pensions into a QROPS with Gower Pensions in Guernsey. Then the victims’ pensions were invested in toxic, illiquid, high-risk, professional-investor-only funds and shrank relentlessly. The problem was that Holborn Assets had no license to provide pension or investment advice in Spain. This is the sort of scam that the CNMV, the Spanish investment regulator, refers to as being operated by “chiringuitos” (bar flies) which translates as “scammers”. And the UK Pensions Regulator clearly refers to scammers as criminals.

Holborn Assets’ home – a low-rise advisory firm amongst the high-rise buildings

So why is Bob Parker – from Dubai – gloating over Geraint Davies from Surrey? OK, Geraint’s firm Montfort International has been sanctioned – and very publicly so. And, knowing Geraint I believe he will take his punishment pragmatically and stoically. He has fought back from other challenges in the past and he will fight back from this. But at the end of the day, whatever other faults he may have, he does have respect for the establishment, the law, the regulators and the ethical sector of the financial advisory profession.