David Vilka of Square Mile International Financial Services has exactly the sort of lawyer one would expect: a scammer’s lawyer. Unsurprisingly, this dope can’t even spell Vilka’s victim’s name and has referred to him as “Mr Sexton” as opposed to “Mr Sefton”. But, again, this is no surprise.

David Vilka of Square Mile International Financial Services has exactly the sort of lawyer one would expect: a scammer’s lawyer. Unsurprisingly, this dope can’t even spell Vilka’s victim’s name and has referred to him as “Mr Sexton” as opposed to “Mr Sefton”. But, again, this is no surprise.

What I must challenge, however, is the fact that Mr. Sefton has referred to this clown as a “two-bit lawyer”. I really don’t think this is true – as he is a one-bit lawyer at best. He has a couple of glowing client testimonials going back to 2016 and 2015 on his amateurish website, and displays no evidence of experience or expertise in the arena of British pensions (and why would he? – he’s purportedly practising US law in the US).

One might forgive Mr. Davies for not understanding anything about UK pensions in general and pension scammers like David Vilka in particular, but to immediately jump into a firm conclusion that there has been defamation against his client shows that he hasn’t even made a one-bit attempt to understand what his client has been up to – or how many lives (like Mr Sefton’s) Vilka has ruined.

I must admit I am used to dealing with a much better class of scammers’ lawyer. Take DWF, for example: this large firm carelessly lost a team of 20 lawyers to rival Trowers and Hamlins a couple of years ago. This wasn’t long after they were caught representing both sides in a case: the Insolvency Service in the winding up of Capita Oak, and Stephen Ward who handled the transfer administration in the same scheme. But at least they dealt with the embarrassment of acting for both the poacher and the gamekeeper with a degree of dignity and elegance – a class act indeed. DWF comes into the same league as my other legal chums – including Carter Ruck and Mishcon de Reya. So, you can see I am more used to dealing with professional firms rather than twerps like this Mr Davies.

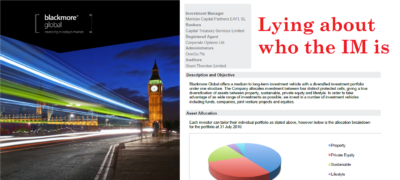

Mr. Davies is referring to the UCIS investment scam, Blackmore Global, which was illegally promoted to retail investors – and which is a fraud from start to finish.

Mr. Davies is referring to the UCIS investment scam, Blackmore Global, which was illegally promoted to retail investors – and which is a fraud from start to finish.

Anyway, I have answered his absurd email below with my usual comments in bold.

————————————————————————————————-

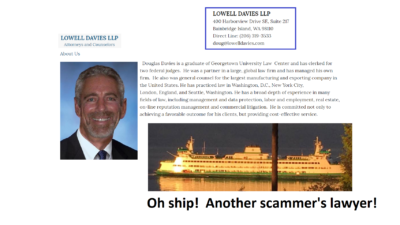

LOWELL DAVIES LLP

July 14, 2018

Ms. Angela Brooks, Director of Pension Life

Re: Defamation of Mr. David Vilka and Square Mile International

Dear Ms. Brooks:

I am an attorney You may well be, but you are clearly a US attorney – and that does not qualify you to deal with a matter which involves UK pensions

and represent Mr. David Vilka Bad luck

with respect to the defamatory article I never write defamatory articles – I only write the truth

published on your on-line site. Specifically, this complaint relates to the misstatements and misrepresentations made on

the following site:

If I might sum up, each and every defamatory allegation with regard to Mr. Vilka and Square Mile International you assert are sourced to one disgruntled individual, Stephen Sexton, none of which allegations are supported by any evidence whatsoever. Wrong. Mr. Sefton is one of a number of victims of Vilka’s scams – many of which were invested in the same toxic, illegal UCIS fund as Mr. Sefton – Blackmore Global – and others were invested in other similar investment scams. Blackmore Global is run by another scammer, Phillip Nunn, who – along with his partner in crime Patrick McCreesh – ran the cold calling and lead generation services for the Capita Oak and Henley pension scams, now under investigation by the Serious Fraud Office.

Mr. Sexton was an unsolicited client of Mr. Vilka and Square Mile who had a substantial pension and for personal reasons of his own wanted to switch his pension and draw down sums for his personal use. When he says “unsolicited” he means not cold called, as was usually the case with Vilka. Vilka lied about being regulated to provide pension and investment advice, and the rest is history: Mr Sefton’s life savings were invested in two UCIS funds which were habitually promoted by Vilka: Blackmore Global and Symphony.

The switch in pension plans resulted in what Mr. Sexton felt were unreasonable fees (None of which went to Mr. Vilka or Square Mile). I wonder if this idiot would like to explain why Mr Sefton was put into a QROPS when he was a UK resident?

And despite the fact that Mr. Vilka was able to personally intervene and get Mr. Sexton’s monies returned less a nominal fee, Mr. Sexton continued to complain and when Square Mile attempted to make up even this nominal fee on its own part, Mr. Sexton continued to complain because he refused to sign a boilerplate settlement agreement containing a standard confidentiality agreement. It is true that Mr Sefton did, eventually, get around 85% of his original investment back – but only after a dogged fight which was backed up by the pension trustees Integrated Capabilities. There was no intervention by Vilka.

In your post on the Blackmore Fund you have the temerity to cast defamatory aspersions on Mr. Vilka and Square Mile based on your “strong suspicion” and you go on to assert they must have a “strong vested interest in promoting this black hole of a fund.” Why else would scammers such as Vilka promote such a fund? It is a UCIS, with no independent audit to verify whether the purported assets even exist.

Really? What proof of that would you have? Vilka must have had a very strong reason to promote the Blackmore Global investment fraud – why else would he have invested a further 64 victims’ pensions in this UCIS? This was a bunch of people he scammed into transferring their pensions to a Hong Kong QROPS.

And since you have none, we demand you remove this article and/or any reference to Mr. Vilka or Square Mile. I have plenty of evidence thank you.

Let me advise you that Mr. Vilka and Square Mile, contrary to your specious aspersions, are heavily regulated as is the industry. “Heavily”? What you actually mean is that neither Vilka nor Square Mile is regulated for pension or investment advice – only insurance mediation.

The Sexton matter was thoroughly investigated at the time by the appropriate regulators who found no irregularities. You don’t know that.

Mr. Sexton is not nor was he a perplexed victim of Mr. Vilka or Square Mile. He most certainly was – as Vilka and his accomplice John Ferguson know full well.

His pension is worth well over half a million pounds. No it isn’t. Did you do maths at school?

He read and signed multiple acknowledgements before he switched pensions showing very clearly that he knew what he was investing in and the inherent risks involved. No he didn’t. It was never disclosed that the scammers were going to invest his pension in a UCIS fund which is illegal to be promoted to retail UK investors.

And again, significantly, he was not cold-called. He sought out Mr. Vilka and Square Mile. Nor did Mr. Vilka or Square Mile receive any payment from the Blackmore fund or its partner firms regarding Mr. Sexton’s transaction as confirmed by the Czech National Bank which has direct access to Square Mile’s company bank accounts via an electronic data box. Are you talking about the accounts which haven’t been updated since 2014?

And again, significantly, he was not cold-called. He sought out Mr. Vilka and Square Mile. Nor did Mr. Vilka or Square Mile receive any payment from the Blackmore fund or its partner firms regarding Mr. Sexton’s transaction as confirmed by the Czech National Bank which has direct access to Square Mile’s company bank accounts via an electronic data box. Are you talking about the accounts which haven’t been updated since 2014?

In sum, there is no bases whatsoever for the specious and actionable statements you make in your referenced post with regard to Mr. Vilka and Square Mile International. I think you mean basis – and yes, there is a solid basis for all the statements I made in my post and not a single one of them is “specious” (although I am amazed you have even heard of the word).

Your comments have caused Mr. Vilka and Square Mile reputational damage, among others, and you are hereby instructed to delete the post immediately. I sincerely hope that the impact of my blog has caused Vilka and his accomplice Ferguson to turn over a new leaf and arrange to pay compensation for Mr. Sefton and all their other victims who have lost part or all of their pensions to the Square Mile scams.

Your failure to do so will result in further damages to Mr. Vilka and Square Mile International, the accrual of further legal fees and costs, and the likelihood of litigation, all of which damages and costs we will recover from you. Good luck with that.

If you have any questions or concerns or require further information, please don’t hesitate to contact me directly at (206) 319-3533. I look forward to confirmation of the removal of the identified defamatory materials. Thank you in advance for resolving this matter expeditiously. I have no questions, other than to enquire as to when your client intends to pay redress for the losses caused by his fraud.

Best regards,

LOWELL DAVIES LLP

LOWELL DAVIES LLP

Douglas Davies Attorney at Law

8497 Hemlock Drive

Bainbridge Island, WA 98110

Direct Line: (206) 319-3533

doug@lowelldavies.com

At Pension Life we believe that all financial advisers should be appropriately qualified as well as registered with the institute from which they gained their qualifications. If they are a good, trustworthy FA then why would they object to these requirements? With so many rogues out there, and the figures of financial fraud totting up to millions, an honest FA should be proud for their name to appear on all the professional institutes’ registers to which they claim they are qualified.

At Pension Life we believe that all financial advisers should be appropriately qualified as well as registered with the institute from which they gained their qualifications. If they are a good, trustworthy FA then why would they object to these requirements? With so many rogues out there, and the figures of financial fraud totting up to millions, an honest FA should be proud for their name to appear on all the professional institutes’ registers to which they claim they are qualified.

If you have been following Pension Life´s blogs, you will know that we have been conducting a series of investigations into

If you have been following Pension Life´s blogs, you will know that we have been conducting a series of investigations into

And thus it always is: the perpetrators of financial scams fight back hard against their victims with fancy, overpaid lawyers (in fact, one pension scam victim calls them “bloodsuckers”). In my view, these lawyers are just as bad as their guilty clients. Any self-respecting lawyer ought to refuse to represent those who facilitate scams which ruin innocent victims. And any self-respecting judge should see through such obfuscation tactics in court.

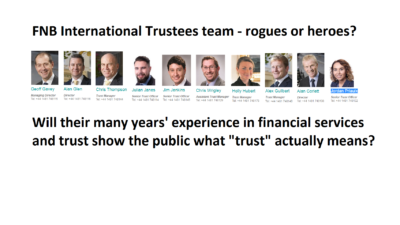

And thus it always is: the perpetrators of financial scams fight back hard against their victims with fancy, overpaid lawyers (in fact, one pension scam victim calls them “bloodsuckers”). In my view, these lawyers are just as bad as their guilty clients. Any self-respecting lawyer ought to refuse to represent those who facilitate scams which ruin innocent victims. And any self-respecting judge should see through such obfuscation tactics in court. Let us be clear: FNB is not any old dodgy trustee in a corrupt jurisdiction where the regulator, ombudsman and financial crime unit all play golf and quaff champagne with the perpetrators of financial crime. The firm holds itself out to be a responsible, professional and competent pension trustee. The so-called “key” people have, between them, many years of purported experience in financial services, trusts, banking and investments.

Let us be clear: FNB is not any old dodgy trustee in a corrupt jurisdiction where the regulator, ombudsman and financial crime unit all play golf and quaff champagne with the perpetrators of financial crime. The firm holds itself out to be a responsible, professional and competent pension trustee. The so-called “key” people have, between them, many years of purported experience in financial services, trusts, banking and investments.

Still, neither the regulators nor law enforcement agencies lifted a finger to stop the Moats: FAST PENSIONS – SLOW LAW ENFORCEMENT – STATIONARY REGULATORS, is the basis of this case.

Still, neither the regulators nor law enforcement agencies lifted a finger to stop the Moats: FAST PENSIONS – SLOW LAW ENFORCEMENT – STATIONARY REGULATORS, is the basis of this case. I’ve been very concerned about Dolphin Trust GmbH for some time. There’s an awful lot of pension money being loaned to this company – and I don’t get to hear of many (in fact any) people who have had their loans repaid. That doesn’t mean they haven’t been repaid – it just means I haven’t heard about it.

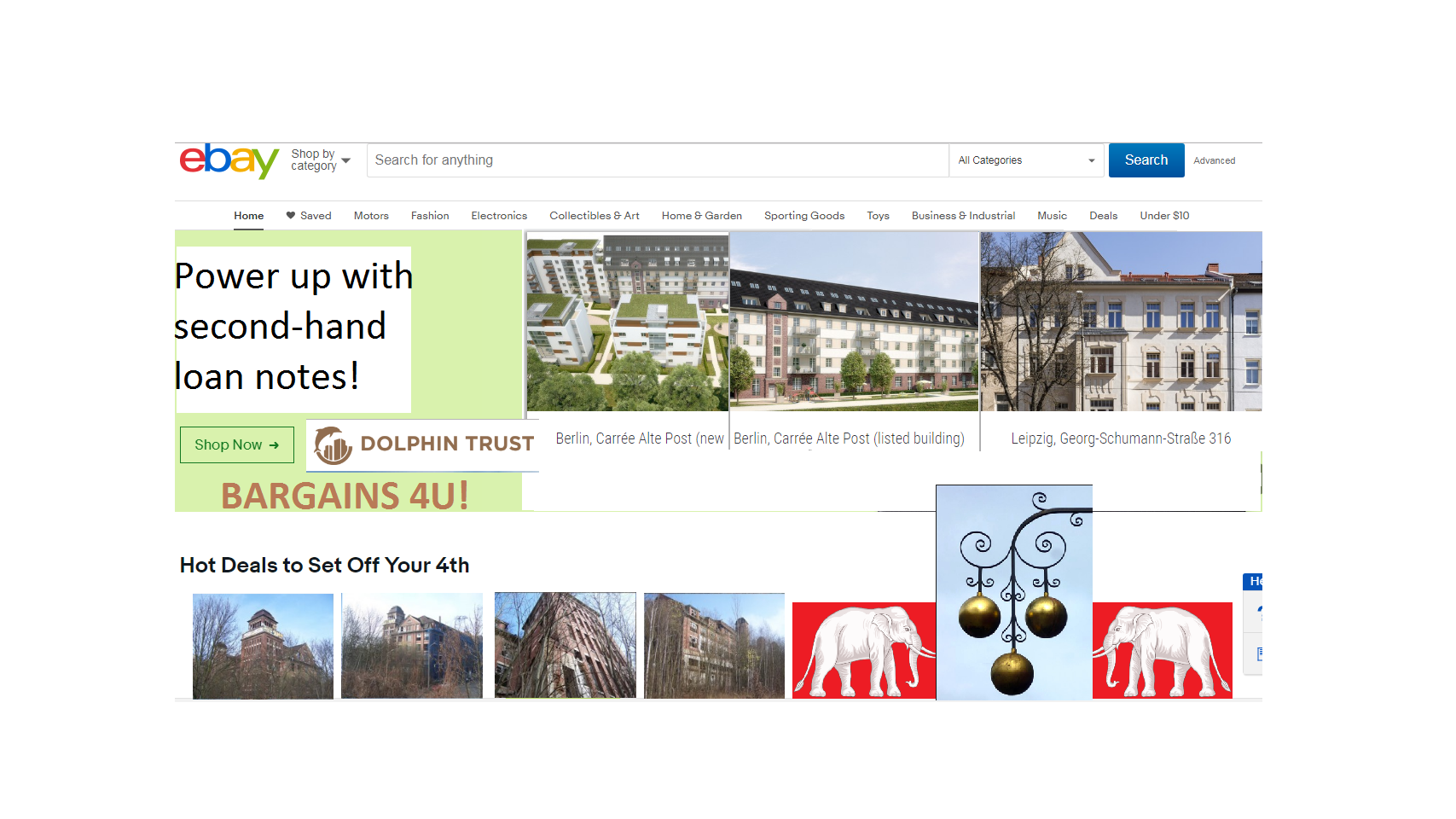

I’ve been very concerned about Dolphin Trust GmbH for some time. There’s an awful lot of pension money being loaned to this company – and I don’t get to hear of many (in fact any) people who have had their loans repaid. That doesn’t mean they haven’t been repaid – it just means I haven’t heard about it. Without the benefit of any assurances from the nice men at Dolphin Trust – Charles Smethurst, Helmut Freitag, Axel Krechberger and Matthias Ruhl – we will just have to hope that Mr Doran manages to offload the second-hand loan notes that STM Fidecs allowed 400+ victims’ life savings to be invested in. Perhaps I’ll drop him a friendly note and suggest he tries ebay.

Without the benefit of any assurances from the nice men at Dolphin Trust – Charles Smethurst, Helmut Freitag, Axel Krechberger and Matthias Ruhl – we will just have to hope that Mr Doran manages to offload the second-hand loan notes that STM Fidecs allowed 400+ victims’ life savings to be invested in. Perhaps I’ll drop him a friendly note and suggest he tries ebay.

Holborn Assets’ Kensington Fund –

Holborn Assets’ Kensington Fund –  Back to the

Back to the  There are no details of costs, no fact sheets, no details of who is making the investment decisions. The directors are Scott Balsdon, Director of Holborn Assets, Globaleye and Adamou Riyad, CCO of Holborn Assets (and Noel Ford). So the fund is run by the same cowboys who run Holborn Assets – yeehaa!

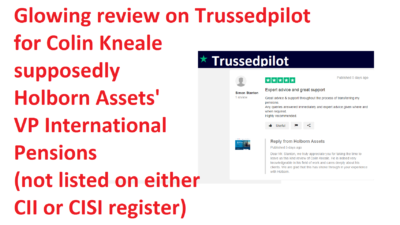

There are no details of costs, no fact sheets, no details of who is making the investment decisions. The directors are Scott Balsdon, Director of Holborn Assets, Globaleye and Adamou Riyad, CCO of Holborn Assets (and Noel Ford). So the fund is run by the same cowboys who run Holborn Assets – yeehaa! And, finally, Holborn Assets forge five-star Trustpilot reviews. How sad is that?

And, finally, Holborn Assets forge five-star Trustpilot reviews. How sad is that?

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.