Gibraltar’s most wanted man – Alan Kentish, CEO of STM Fidecs

STM Fidecs needed a safe Harbour. And now they’ve got one – but is it really safe?

LETTER TO ALAN KENTISH – CEO OF STM FIDECS:

Dear Al, hope you are well. I’m not anticipating a response to this because I know how difficult it must be to type emails when you’re wearing handcuffs. However, I thought I would drop you a line because I am genuinely worried about you.

STM’s harbour for investment scams

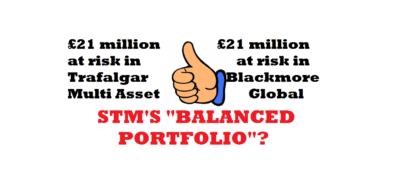

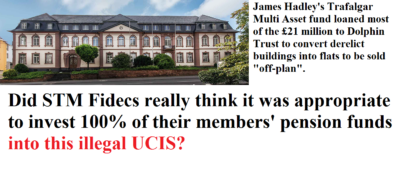

You see, I heard you’d bought Harbour Pensions for £1 million – a book of 1,600 members. But how many of these members will want to stay once they find out they are now in the hands of STM? If any of them have got any sense they will transfer out to a decent QROPS trustee who can be trusted to look after their pensions. STM Fidecs allowed hundreds of victims – advised by a known scammer running an unlicensed firm (XXXX XXXX) of the Pensions Reporter/Global Partners Limited) – to be 100% invested in XXXX’s own fund, Trafalgar Multi Asset (now suspended, under investigation by the SFO and being wound up).

The Trafalgar Multi Asset Fund was a sub-fund of the Nascent Platform – one of many operated by Custom House Global offering scammers a cost-effective place to waste pension pots. This provided a low-cost solution to wannabe fund managers to try their hand at playing musical money with victims’ life savings.

What surprises me, is that having proved that STM Fidecs is an incompetent firm run by inept – or perhaps even crooked – people, you would be splashing money around acquiring more victims and more toxic assets. Instead, you should have been paying compensation to your existing victims who may well have lost a substantial proportion of their retirement savings due to STM Fidecs’ own failings.

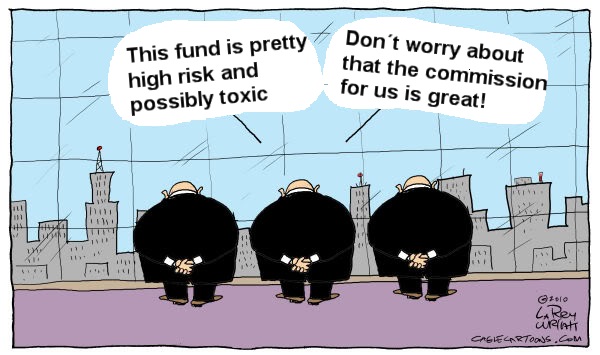

Having acquired Harbour, you have now added the toxic, illiquid, high-risk, un-audited Blackmore Global fund to your portfolio of worthless crap. Your balance sheet must need disinfectant and a good old scrub.

STM’s balanced portfolio of toxic investment scams – Trafalgar Multi Asset and Blackmore Global

Furthermore, you will now be in league with not one but TWO lots of scammers who are under investigation by the Serious Fraud Office. XXXX XXXX (Trafalgar Multi Asset) and Nunn McCreesh (Blackmore Global) were both behind the Capita Oak and Henley Retirement Benefit pension scams – all 100% invested in Store First store pods.

Seriously, Al, you should think about cleaning up your act – not making it dirtier and murkier. Hope those handcuffs don’t chafe too much.

STM Fidecs, the Gibraltar-based trustee firm used for the Trafalgar Multi Asset Scam, is now the subject of large numbers of complaints to the Gibraltar authorities. Hundreds of victims of XXXX XXXX’s unlicensed “advice” transferred safe UK pensions to a Gibraltar STM Fidecs QROPS and then he invested 100% of their funds into his own fund – Trafalgar Multi Asset (now under investigation by the Serious Fraud Office). These victims have now submitted evidence and testimony. These reports and complaints are against both XXXX XXXX and STM Fidecs for their part in this scam.

STM Fidecs are also being reported to the Gibraltar Financial Services Commission for the attention of:

Annette Perales, Head of Financial Crime

and

Zoe Westwood, Head of Enforcement, Legal, Enforcement and Policy

The Serious Fraud Office has been investigating this scam – in which STM Fidecs played an integral and crucial part – for some months. XXXX XXXX and one of the STM Fidecs directors have been arrested. XXXX’s office was searched and no doubt STM Fidecs’ offices were also searched. Obviously, the victims all want those responsible for this scam to serve maximum prison sentences.

The STM Fidecs website makes the following grand-sounding claim:

“The backbone of STM is its staff. We have people who have worked for us for 20 years who are the heart and soul of our business. If we didn’t have outstanding staff, we wouldn’t be able to do what we do.”

The only thing “outstanding” would be an immediate admission of their guilt and negligence, as well as an undertaking by STM Fidecs to compensate their victims for the £ millions of losses they are facing due to STM Fidecs’ complicity with this scam. Let’s examine some of these staff and see how much backbone they really have.

Alan Roy Kentish ACA ACII AIRM Role: Chief Executive Officer

Alan Kentish, CEO, claims to be a qualified chartered accountant specialising in the financial services industry. So you would have thought he would have known not to accept business from an unlicensed firm – XXXX XXXX’s Global Partners Limited (now Tourbillon). He ought to have known that UK residents should not be transferred to a QROPS at all. He would have known that members’ funds should not be 100% invested in one UCIS fund (illegal to be promoted to UK residents). And he should have recognised that it is a clear conflict of interest for members to be invested in a fund for which their adviser was also the investment manager.

What has Alan Kentish done to put this right? How much compensation has he offered to the hundreds of distressed investors? Has he engaged with the victims and assured them that STM Fidecs acknowledges their responsibility, liability and culpability? No – Alan Kentish has done nothing except pull up the drawbridge-like a spineless coward.

David Easton, Head of Pensions at STM Group PLC

“David Easton, Head of Pensions for STM Group PLC joined STM in October 2014 as Managing Director of the Gibraltar pensions business and is also a board member of the pensions businesses in Malta and the UK. Since 1990 David has worked in the financial services arena specialising in pensions administration. David is responsible for driving the expansion of STM Group’s international pensions division as well as personal and occupational pension schemes in Gibraltar and personal pensions in the UK.”

So, responsible for driving the expansion of STM’s pension business into an investment scam run by a known serial scammer? Well done David. Your “primary focus” was very clear: put UK residents into a QROPS and then allow all of them to be 100% invested into an illegal UCIS. And to what extent has he engaged with the hundreds of distressed victims of this scam? Zero. Another spineless coward who refuses to speak to these people. He will neither explain nor apologise.

A former employee of STM Fidecs sent me the following statement:

“We were told not to go to the Pension Life website so as not to give her any traffic and SEO rankings. I believed them. More fool me. This is why I am now checking it out and am amazed at what’s on there.

I was asked to dig the dirt on Angela Brooks and I did, believing STM had not been aware of the Trafalgar stuff but had instead been duped. It’s more than apparent now that they fully knew what they were doing. They have sent Angela lawyers letters insisting she cease from mentioning them on her website or will take legal action against her.

Glynis Broadfoot (a victim of Holborn Assets and Gower Pensions) who also used to work for STM Fidecs, was marched out. We had no anti-bullying policy in place at the time and Glynis was being bullied. They marched her out on trumped up charges.

If I had known this at the time I would have objected. Glynis won’t speak though. They must have frightened her to death.

Outstanding staff? I think not. The only thing the STM Fidecs staff excel at is bullying. And bullies are, of course, the biggest cowards of all.

Dolphin Trust – a UCIS which was illegal to be sold to UK residents

The Trafalgar Multi Asset Fund liquidators say this is the most obvious scam they have ever seen. Purely designed through ‘layering’ to misappropriate funds, the liquidators are just glad the administrators pulled the plug at £21m and not later. At the height of the success of this scam, STM Fidecs was accepting more than £1 million a month from UK residents (none of whom should have transferred into a QROPS at all) and allowing it all to be invested in XXXX XXXX’s illegal UCIS.

Apparently, Dolphin Trust (the German fund which borrows money to refurbish derelict government and listed buildings) has “cooperated” and the liquidators have found some other assets as well, although getting them may prove tricky since they will have been vigorously hidden. Dolphin Trust is typically found alongside car parking spaces, store pods, eucalyptus plantations, truffle trees and other toxic crap peddled by the scammers.

The liquidators reckon the victims might get 50% back less costs, so after the liquidators’ costs that would be nearer 30% net. But STM Fidecs know all this, but have deliberately hidden it from the victims.

It is human to err, and STM Fidecs is staffed by humans (albeit spineless ones). But what is not forgivable is to fail to come to the table and assure the victims they will be compensated for their losses and profound distress. STM Group has been bragging that it has plenty of money and will be buying up other trust companies to make their business bigger and more profitable.

None so blind….

STM Fidecs’ victims feel they shouldn’t be in the pension trustee business at all since they are clearly incompetent, dishonest and dishonorable. This belief is clearly correct since STM Fidecs also accepted transfers from Continental Wealth Management (unlicensed “chiringuitos”) and then allowed the victims’ pensions to be 100% invested in high-risk, professional-investor-only structured notes. As a result, the STM members are facing heavy losses.

Hundreds of victims have reported both XXXX XXXX and STM Fidecs to the SFO and the GFSC for fraud

The Gibraltar authorities must now show how “highly regulated and transparent” Gibraltar is. As things stand, the evidence is that Gibraltar is full of thieves, scammers and scoundrels. The chiringuitos love being there because the regulation is widely accepted as being as spineless as the staff and directors at STM Fidecs.

**********************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Continental Wealth Management (CWM) was a financial advisory firm based on the Costa Blanca in Spain. Headed up by Darren Kirby, there were – until earlier in 2017 – 35 people working at the firm. The firm claimed to have £50 million worth of assets under management and around 500 clients. The firm closed down on 29.9.2017.

It is feared that up to 40% of CWM’s clients may have been affected by this situation.

BACKGROUND TO CWM

CWM “advisers” acted as sharks

In mid-2011, Stephen Ward’s Premier Pension Solutions (PPS) lost the lucrative Ark pension liberation scam when the Pensions Regulator placed the scheme in the hands of Dalriada Trustees. Ward had advised 160 victims to transfer £10m worth of secure pensions into this scheme on the promise of having 50% of their pensions paid to them in cash. He also assured them these payments would not be repayable or taxable and that the pensions would be invested in “high-end London residential properties”.

In the event, neither of these assurances turned out to be true. Dalriada is now making claims to recover the 50% liberations and HMRC has issued tax demands at 55% of the cash received (and the tax will still be payable even if the liberations are repaid). The High Court called the Ark scheme a “fraud on the power of investment”.

Having ruined 160 lives, and made up to £1 million profit out of the Ark victims, Ward immediately turned his attention to his next scam: Evergreen New Zealand QROPS and his Marazion “loans”. Having seen how easily victims could be duped into transferring their safe pensions with the promise of 50% liberation, Ward appointed CWM as “introducers” to the scam.

Here is an actual account by one of the Evergreen/PPS/CWM victims of what happened to her:

Mrs. A: “I was first cold called by CWM in 2011. I first met Phil Kelman of CWM in January 2012. I was told only positive things about transferring my pensions and to be able to take 100% of my pension funds.

This, however, changed after the first meeting and I was then told that due to the government closing loopholes I would only be able to get 50% of my pension fund and that the other 50% would be in the Evergreen QROPS earning enough interest over the 5 years to cover the 50% that I could withdraw (before the age of 55) – a win win situation!

There was no mention of the 50% being given as a loan until much further down the line. This was supposed to have taken 6 weeks at the most, but it actually took nearly 10 months. I was told that the “loan application” was a paper exercise just to cover things – I obviously have no proof of these conversations! Due to the fact that in the beginning it was not a “loan” there was no talk of a 55% tax charge, also as it was QROPS I was told it wouldn’t have incurred a tax bill.

I was not given any opportunity to say what the consequences of losing my pension or gaining an extortionate tax bill would be – either in the short or long term. If I had known of the huge risk of losing everything then obviously I would not have gone ahead. I did not state that I was willing to risk everything to get the “loan”.

I was told that Evergreen was a safe place for my pension to be as Evergreen was “approved”. I was given a graph to show how my pension would not only make the 50% back up but make more on top of it.”

Marco Floreale – former CWM “adviser” – now MD of Carrick Wealth

Mrs. A’s case was handled by CWM’s Marco Floreale (now Managing Director of Carrick Wealth) who claimed to be the managing director of CWM. Her secure, final salary, £100k Royal Mail pension was transferred to Evergreen and she was forced to sign a five-year “lock in” before receiving her “loan”. The loan agreement issued by Stephen Ward included annual interest at 8.5% compound which would mean that her £50k loan would have increased to £75k at the end of the five-year term. She was also charged more than £10k in fees.

There are now around 300 victims trapped in Evergreen as they are not allowed to transfer out. Ever. Between them they have lost £10m worth of pensions. The CWM personnel involved in this scam claimed that PPS was their “sister” company and have offered no help or compensation for the victims’ losses and terrible distress. One victim died of cancer in February 2017 and her husband is convinced that the stress of the Evergreen situation brought on the disease.

Phil Kelman, Jon Meek, Robert Pearl, Gemma Broad and Anthony Downs were among the CWM personnel who assured the victims that the transfers were in their interests as well as safe and prudent. It was, of course, later discovered that the Evergreen fund was invested in illiquid, high-risk, toxic funds – including personal, unsecured loans. Evergreen was removed from the QROPS list in November 2012 and the victims have now been told they can never transfer out.

It is not known how many other Stephen Ward/Premier Pension Solutions scams CWM was involved in, but when Evergreen got shut down CWM started acting as “advisers” to British expats in Spain and France. They were still working with Stephen Ward of PPS who provided the transfer advice. It is now thought they advised more than 500 people and that around 40% of these have suffered crippling losses to their investments.

I do not know whether CWM ever disclosed their previous involvement with Stephen Ward’s scams to the clients – although it is doubtful that any people would have felt comfortable using CWM had they known they had been responsible for the 300 Evergreen victims. Certainly, CWM did not disclose their past activities to either Trafalgar International or Momentum Pensions – had they done so they would never have been given terms of business by either firm.

From 2013 onwards, CWM invested hundreds of low to medium risk clients’ investments in high-risk, illiquid assets. CWM completely ignored the suitability issue and paid no heed to the clients’ preference for safe, low-risk investments. Clients’ signatures were repeatedly copied and once the losses started to appear, CWM assured them that there was nothing to worry about and they were “only paper losses”.

When asked why so many clients were put into professional-investor-only investments, CWM replied that the investors themselves were not the clients; but the insurance companies were the clients. When I showed CWM evidence of forged signatures on dealing instructions several months ago, there was no response then and no further communication from them subsequently.

The most important thing now is the restitution of the victims’ funds. OMI, Trafalgar and Momentum Pensions, have come to the table to try to find a solution and restore of the victims’ pensions and investments. If we can achieve an equitable settlement, this will be a first in European financial services. However, the parties who have not come to the table are life offices Generali and SEB, as well as other pension trustees including Concept, Sovereign, Pantheon, Elmo and STM. It is no surprise that STM have not come to the table, because they pulled up the drawbridge in the Trafalgar Multi Asset Fund scam, run by XXXX XXXX – now under investigation by the Serious Fraud Office.

I would like to thank all the victims for their patience so far. But it has now finally run out – unsurprisingly. The mood has darkened and victims want action. A valuable information and commentary resource is the Repdigger forum. One interesting post recently reminded contributors that it was Stephen Ward of Premier Pension Solutions who provided the initial transfer advice. Nothing changes.

Beddoe proceedings: arguably (apparently) Dalriada could have been pursued by Ark victims without MPVAs for not pursuing repayment from those with MPVAs and conversely could have been pursued by Ark victims with MPVAs. So, to be on the safe side, they spent a quarter of a million quid of the victims’ funds on the Beddoe proceedings in the High Court.

And here we need to look at the meaning of the terms – MPVA and sharp stick:

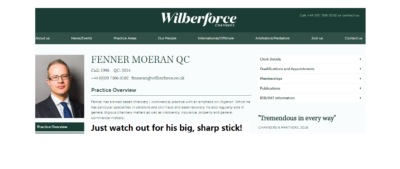

Sharp Stick: Fenner Moeran’s extremely offensive statement that Ark victims should be beaten with a sharp stick (upon which neither the judge, Sarah Asplin, admonished him nor upon which Keith Bryant, the Ark victims’ QC, challenged him)

MPVA

MPVA is an anacronym for “Maximising Pension Value Arrangements” – a euphemism for pension liberation. The rules are that if a person is under the age of 55, he or she can’t access any part of their pension without incurring an unauthorised payment tax charge of up to 55%. So all pension liberation scammers think up clever ways of fooling potential victims into believing there is a legal “loophole” to circumvent this rule.

The point of a pension liberation scam is not to provide members with a bona fide pension scheme designed to provide an income in retirement, but to make the scammers loads of money. First there is the transfer fee: in the Ark case it was relatively low at 5% – although Stephen Ward was charging an extra fee on top of that of up to £2k per transfer.

And then there are the investment kick-backs. We still don’t know how much the Ark scammers earned out of the speculative, illiquid, high-risk properties they purchased in various dodgy offshore jurisdictions. But it will have been very lucrative. In subsequent scams, the scammers earned huge commissions such as 20% from Dolphin Trust; 30% from Park First; 46% from Store First.

By the time the Ark victims realised they’d been scammed it was too late and there was no parachute

The scammers always promise spectacularly high returns on the investments with assurances such as “guaranteed 8% per annum”. In the case of Ark, the victims were told they would receive up to 9% a year on the growth of the value of “high-end London residential properties” in which the pensions would be invested. This, of course, was a lie. But by the time alarms started to ring and the victims realised there was no way out of this toxic flight with no parachute, it was too late.

But let us revert to the portion of a transfer which is liberated. This can range from 5% to 85% depending on the structure of the scam. And it is given various names or labels such as “cashback”; “thank you”; “refund of fees”; “trousers”; “loan”. The favourite word used is “loan” because the scammers claim that “loans are not taxable”. There is no intention for the money ever to be paid back – that isn’t the point of the exercise. The scammers know the victims would never be able to repay the funds.

The use of the word “loan” in some schemes is merely a marketing term used to fool people into believing they won’t be taxed on the money. And the scammers have no interest in whether the victims ever get taxed or not – because by the time HMRC gets around to sending out tax demands, the scheme will have collapsed and the scammers will be long gone and far ahead on their next scams. They never stick around to help mop up the train wreck left behind.

Often, the victims are surprised when they receive “loan” documentation and alarm bells start ringing. But the scammers assure the victims that this is “just a paper exercise” or “administration to make sure HMRC don’t try to tax the money – because loans aren’t taxable“.

In the Ark scheme, the victims were told the amounts liberated would not be taxable because they didn’t come from the members’ own scheme, but from another scheme. And this is why 14 schemes were set up to work in pairs so that up to 99 people in each pair of schemes could swap cash from their transfers. So this was an artificial mechanism structured purely to operate the liberation – using the label “MPVA” to dress the payments up as something more glamorous and bona fide than just a dollop of unauthorised cash in a person’s trousers.

Very few of the victims were told their cash would ever have to be paid back. The MPVA agreements never once mentioned the word “loan” but did mention the word “discharge” and suggested that the MPVA would be automatically “discharged” after a period of years.

Some victims were told the MPVA would be settled or repaid out of the growth that the Ark pension would enjoy (because of the wonderful investments!). It was explained that the MPVA would grow at 3% a year but the pension fund would grow at 9%. But the member would never have to pay the MPVA off out of their own pocket.

Other victims were told the MPVAs would never have to be paid at all because of the reciprocal nature of the transfer/payment structure. It was explained thus: two “paired” members in different schemes would each have a reciprocal MPVA of – say – £50k. If they both decided they never wanted to pay the MPVAs back, they would just treat them like equal IOUs and agree to simply tear them up.

The Tolleys authoritative manual on pensions taxation by Stephen Ward

Now remember, the victims weren’t told these things by any old spivs – they were told them by Stephen Ward of Premier Pension Solutions and his various accomplices (e.g. Fraser Collins, Terry Tunmore, Paul Clarke etc). Stephen Ward was back then – and still is now – a regulated financial adviser of many years’ experience, as well as the author of the Tolleys Pensions Taxation Manual, (and Level 6 CII qualified).

The same assurances were also given to numerous victims by George Frost, of Frost Financial, a regulated mortgage and insurance broker. And the victims who received the advice on the merits of entering into the Ark scheme believed they had every right to believe and trust professional, qualified and regulated advisers who assured them the MPVAs would never have to be repaid and that their pensions would be safe and secure.

HMRC does not care whether a sum of money accessed from a pension before the age of 55 is called a loan, thank you, cash back, fee refund, MPVA or any other euphemism for “liberation”. They don’t care whether it is repayable or whether it is ever repaid or not. They don’t care whether it comes directly from the member’s pension scheme, or from somebody else’s pension scheme, or via some convoluted arrangement designed to conceal the source of the money – such as Stephen Ward’s Evergreen/Marazion pension/loan scam. If a member makes a pension transfer and receives a sum of money as a result – irrespective of where it comes from – HMRC will issue a tax demand of up to 55%.

To illustrate how pension liberation scams range from the very simple and transparent to the highly complex and opaque, here is an example of one arrangement which Stephen Ward and his merry men, Alan Fowler and Bill Perkins, were involved with in 2013 – after Ark, Evergreen, Capita Oak and Westminster pension scams had all been suspended:

Thanks to you both for your understanding…. Am unused to non delivery! The arrangement I heard about today works like this as an example (ignoring fees) and this is the simplistic version …

Client borrows 16k or thereabouts (this is available in the package)

He gets a non recourse loan (which will not be repaid) of £84k

He buys shares in Xco for £100k. These are listed on the CISX (name is Elysian)

Transfers £100k to James Hay SIPP

SIPP pays member £100k for the shares

Member repays the 16k and trousers £84k

My IFA connection has done 40 of them so far. Advice to transfer to the SIPP is from an FCA regulated IFA. James Hay and Suffolk Life know the full structure and are happy with it.

Regards Stephen

The FCA-regulated IFA to whom he was referring was Angela South of Magna Wealth. She soon made a hasty exit from the collaboration with Stephen Ward when victims realised this was a scam and threatened to report her to the Serious Fraud Office. Victims who participated in this scam have now received tax demands from HMRC and Elysian Fuels is now worthless.

SHARP STICK

Dalriada’s QC, Fenner Moeran, seemed like a very sharp cookie. His skeleton argument (which we never got to see), and his opening speeches, started with the assumption that the MPVAs were definitely loans; that there was no question that they were loans and that the members knew and accepted that they were loans.

The judge, Sarah Asplin, accepted this without question and there was no debate on the subject. Kim Goldsmith’s QC, Keith Bryant, sat as quiet as a corpse and made not one single interjection or objection – even though he was sitting next to Kim who knew perfectly well – and must have told him – that the victims were not aware the MPVAs were loans. Indeed, they were categorically assured that the MPVAs would never have to be repaid.

Even more astonishing was the fact that Dalriada was aware the victims never knew the MPVAs were loans. Dalriada’s Sean Browes and Brian Spence, as well as Pinsent Masons’Ben Fairhead and Ian Hyde, had attended various meetings with the Ark Class Action and gone through this issue numerous times. They were also fully aware that one victim was horrified when she was subsequently told the MPVA was a loan and she immediately called Dalriada and asked to repay it. But Dalriada had refused.

Furthermore, dozens of Ark Class Action members had completed HMRC’s 10-point questionnaire (the Q10) which specifically asked about the arrangements and what they had been told about the need to repay the MPVAs. This is evidenced at HMRC’s question 8:

8: “DETAILS OF WHAT YOU WERE TOLD ABOUT THE NEED TO REPAY THE LOAN”

Here is a typical response to this question by one of the victims:

“I was told that although on paper it would be an official 25 year loan, that because of the nature of the way the loans were set up, i.e. the quid pro quo arrangement, whereby as one person received their monies from the other members scheme and vice versa, if there was a request for any monies to be repaid in the future from each member, each would tear up each other`s IOU and be quits, so to speak, as already stated.”

Stephen Ward – BA (Econ), ACII, APFS, APMI, ex examiner for the pensions management institute and for the CII, confirmed that the Ark scheme was designed by specialist pensions lawyer Alan Fowler – head of pensions at Stevens and Bolton.

Ward went on to explain how the MPVAs worked: “The best way to understand this is in terms of my lending you £100 and you lending me £100. If I do not repay you and you do not repay me then we are both in an equal position. Conversely, if I repay you and you repay me then the position is identical to that which would arise if neither party had repaid the other”.

These statements have been made to HMRC by Ark victims on countless occasions – and Dalriada has always been perfectly well aware of this. And yet Fenner Moeran used his sharp stick to knock these evidenced facts completely off the table – so that the judge was never made aware of them. Mind you, Keith Bryant QC was no better – because he didn’t bring them to the judge’s attention either.

I would go so far as to observe that Fenner Moeran should have used his sharp stick to point the judge to these evidenced facts – and Dalriada should have made sure he did so. By omitting to do so, both Fenner Moeran and Keith Bryant allowed the judge to come to the incorrect conclusion that:

“members who received the MPVA loans agreed to repay them. That’s the point of a loan. It’s not a gift. They cannot now complain about having to repay them. They can complain about having to repay them earlier, but that’s a cashflow issue which is vastly overwritten by the capital harm that is suffered by the non-recipient members”

Fenner Moeran merely leaned on his sharp stick and did nothing to correct the judge. As I was sitting behind him, I couldn’t see whether he was smirking – but I have a feeling he might have been. The judge was wrong on three counts:

The members with MPVAs did not agree to repay them – they were told they would never have to

They can most certainly now complain about being asked to repay them as they were never told they would have to and did not budget to do so

The capital harm suffered by members without MPVAs was mostly caused by Dalriada who did not reject their transfers after 31.5.11 but allowed transfers to continue right up until the end of August 2011

Having glossed over the facts smoothly, and directed the judge to her incorrect conclusion, Fenner Moeran then addressed the issue of ascertaining whether the Ark victims were in a position to be able to afford to repay the MPVAs. And then he produced, with a confident flourish, his pièce de résistance:

“The chances of getting ascertainably or enforceably more accurate information increases when you have the sharp stick of litigation behind it. If we want to see if we’re actually going to get any of this money back, the chances are that we’re going to have to wave a very large stick“

Fenner Moeran ought to be an intelligent person. In the full knowledge that a few feet to his right sat Kim Goldsmith, an Ark victim who had gone through six years of hell courtesy of Stephen Ward and George Frost and all the other scammers, and that a number of other victims were sitting at the back of the courtroom, he still made such an unbelievably stupid and offensive statement. He apologised later “I deeply and sincerely apologise for any misunderstanding or upset caused”.

But the damage had already been done – and you can’t un-say what has been said – especially when every word is recorded and transcribed. On behalf of Dalriada Trustees, he had deliberately misled the judge, and then proceeded to demonstrate clear contempt for the suffering of the Ark victims.

Interestingly, the judge had not remonstrated with Moeran for his crass comments – and Keith Bryant had not objected to the stupid and insensitive words. Throughout the rest of the proceedings, the judge remained – in my view – dominated and steered by Moeran. No attempt was ever made to disclose the truth about what the victims were told about repayment of the MPVAs by Stephen Ward, George Frost, Andrew Isles or Alan Fowler. And no explanation was ever given as to why Dalriada had not pursued these parties for having duped, misled and defrauded the Ark members.

This may seem like a completely off-topic piece of this report, but please stick with it – it will be worth it because it is the whole point of this report. Nearly 18 months before the Ark/Dalriada/Beddoe proceedings in the High Court, another case was heard: Royal London v Hughes. A pension scammer had tried to do exactly what the Ark scammers had done so successfully and profitably for nearly a year: transfer hundreds of secure pensions into a pension scam. But one ceding provider – Royal London – had blocked a transfer request. They strongly suspected the receiving scheme was a liberation scam – unlike the many ceding providers in the Ark case who handed over hundreds of transfers willy-nilly without question or due diligence – the worst of which was Standard Life.

Hughes complained to the Pensions Ombudsman that her transfer request had been blocked by Royal London. The Ombudsman did not uphold her complaint because he agreed with Royal London that the receiving scheme had all the classic hallmarks of being a scam – including the fact that the scheme had been registered as an occupational scheme and Hughes was not genuinely employed by the sponsoring employer. Exactly the same as Ark (and many of the subsequent scams).

Counsel for Royal London argued that “Hughes had to be an “earner” to be able to transfer”. He tried to support the Ombudsman’s view that the legislation required Hughes to be an earner in relation to a scheme employer”. This counsel obviously knew well that victims were made all sorts of promises and assurances and often not told the truth about the arrangements within pension scams.

Royal London’s QC would have been aware of the Ombudsman’s concerns that pension liberation may well have been behind Hughes’ enthusiasm to transfer her pension. And he will have known only too well that potential victims were systematically lied to and probably told that their “loans” (or whatever euphemism was used) were not repayable. And he would have known that the intended liberation “loans” were never intended to be repaid and that the victims would be told that the loans never needed to be repaid.

This QC will have been thoroughly briefed by his clients, Royal London, and may even have consulted with the Pensions Regulator who would have given him thorough details on how pension liberation scams worked.

So this particular QC had intimate, first-hand knowledge of how pension liberation schemes worked in general and represented Royal London in their quest to defend their right to prevent further victims of pension liberation scams. He also knew intimately how Ark worked in particular.

Fenner Moeran of Wilberforce Chambers

He knew perfectly well that the victims were told they never had to repay their loans (or MPVAs/cash backs/thank you’s/trousers). And he knew that the Ark MPVAs were supposed to be “discharged” from growth in the schemes and NOT from the victims’ own pockets – as reported by Justice Bean. But he failed to bring this to the judge’s attention.

Who was this QC? I will give you a clue – he had a big, sharp stick. Perhaps he should have gone to Specsavers and read the MPVA agreement where this was clearly stated.

Blackmore Global is a UCIS (unregulated collective investment scheme) which is illegal to be promoted to retail, UK investors. The fund is run by Philip Nunn and Patrick McCreesh (formerly of Nunn McCreesh – the lead generation and cold calling firm which introduced around 8,000 victims to the scammers who were running the Capita Oak and Henley pension scams in 2012/13).

It is perhaps more than a little ironic that a pair of cold-callers who were facilitating hundreds of victims being transferred into schemes 100% invested in Store First store pods are now running their own investment fund – Blackmore Global.

Slater and Gordon is a very large firm of no-win-no-fee solicitors with an office in Manchester. I met their National Practice Group Leader and specialist in financial litigation and pension mis-selling in April 2015. His name is Craig McAdam. After going through the various scams I was handling at the time, and the appalling damage done by the scammers to thousands of victims, Craig was thoroughly up to speed on how the scams worked. He was also deeply committed to helping the Ark Class Action and other group actions.

Nunn McCreesh was the introducer of contacts for the pension scammers

Craig McAdam confirmed by email on 16.4.15 that he was looking forward to working with me. A week later he sent a draft engagement letter and confirmed that Slater & Gordon’s success fee would be 15% – although he did revise this up to 18% a couple of days later.

The following month Craig McAdam confirmed he would be attending a meeting with Dalriada Trustees and Pinsent Masons with members of the Ark Class Action. He also confirmed he would be talking to one of Stephen Ward’s many victims: a member of the London Quantum scheme whose trustee was Ward’s firm Dorrixo Alliance.

A month later, Craig McAdam was examining the Capita Oak pension scam run by XXXX XXXX and administered by Stephen Ward, and asked me to put forward one of the victims as a creditor. The Insolvency Service had wound up the trustee of Capita Oak: Imperial Trustees Ltd. Craig then asked me if I was happy for Grant Thornton to be appointed as the insolvency practitioner and I confirmed that indeed I was. I felt that Grant Thornton was a competent and ethical firm and could finally unscramble the mess created by the scammers behind Capita Oak and bring some form of resolution to the victims who were all introduced and/or cold called by Nunn McCreesh.

I was delighted that the same day, one of the Capita Oak victims put herself forward willingly and eagerly as a creditor and Craig McAdam confirmed this to Grant Thornton the following day. At the same time, Craig confirmed that one of the London Quantum victims was a client of Slater and Gordon and made a complaint to FCA-regulated Gerard Associates who had acted as the adviser in that case.

Later in June 2015, Craig McAdam confirmed that Slater and Gordon was instructed by the Capita Oak victim who had volunteered to be the creditor in the liquidation of the trustee of the Capita Oak scam. Craig also sent out letters of engagement to other victims.

In July 2015 I sent a copy of the Insolvency Service’s Capita Oak/Imperial Trustee Services witness statement to Craig McAdam. This statement confirmed that Philip Nunn and Patrick McCreesh’s firm Nunn McCreesh had supplied up to 300 leads a month (for 28 months) to the scammers who promoted and operated the Capita Oak scam: Jackson Francis, Sycamore Crown, Sanderson Clarke, Barncroft Associates, Nationwide Benefits Consultants, Speke Admin, Timoran Capital.

The Insolvency Service witness statement mentioned Nunn McCreesh several times:

“Members of Capita Oak indicated they were initially contacted by Patrick McCreesh of Nunn McCreesh and referred to Jackson Francis or Sycamore for the transfer of their pension to Capita Oak. I wrote to Mr. McCreesh to request a copy of any sales and marketing agreement with Jackson Francis or Sycamore and details of commission received.” Nunn McCreesh and their solicitors admitted they had been involved with the scammers and also Transeuro Worldwide Holdings – one of the main operators of the Capita Oak and Henley scams.

However, Nunn McCreesh was unable to produce copies of invoices or sales ledgers for the money received for their part in these scams. Their solicitors also confirmed that Nunn McCreesh received a commission of 8% of sales and the Insolvency Service stated that there was a “lack of transparency” by Nunn McCreesh.

The Insolvency Service also confirmed that some of the victims had been cold called directly by Nunn McCreesh.

Being in possession of the Insolvency Service’s witness statement clearly galvanised Craig McAdam into an enthusiastic confidence to take on the Capita Oak case and asked me to send him through contact details of all the members. He obviously realised that now the scam was clearly documented and the promoters – including Nunn McCreesh – were now identified without any question of doubt. It was also documented in the witness statement that Nunn McCreesh had earned £900k out of providing at least 8,000 leads for the scam – 300+ of which ended up in Capita Oak and 200+ of which ended up in Henley. It is not clear whether the 8% sales commission was on top of this. 8% of £10.8 million would have been a handsome sum indeed.

I provided Craig McAdam with contact details for the Capita Oak Class Action members and on 21.7.15 he confirmed that cases were “being opened up smoothly”. At the end of 2015, Craig attended a meeting of Class Action members and got to meet a group of victims in person. There can be no doubt that Craig, by now, thoroughly understood the wickedness of the scammers and the profound distress and impending financial ruin of the victims.

So for most of 2015, it looked like Slater and Gordon was going to represent the Capita Oak members – all of whom were initially introduced by Nunn McCreesh. And it looked like Grant Thornton was going to be appointed as insolvency practitioner to Capita Oak’s trustee – Imperial Trustee Services Ltd.

In the event, neither happened. But Capita Oak is now in the hands of Dalriada Trustees – appointed by the Pensions Regulator. And the organisers, promoters and administrators of Capita Oak are all under investigation by the Serious Fraud Office.

Slater and Gordon now represents Nunn McCreesh

In a very curious twist, Philip Nunn and Patrick McCreesh are now running the Blackmore Global UCIS. They are doing the cold calling and the pension administration, as well as running the fund. And you will never guess who their solicitor is: Steve Kunziewicz of Slater and Gordon (Manchester office). And you will never guess who their auditor is: Grant Thornton. You really couldn’t make it up.

Victims of Blackmore Global are indeed extremely distressed. They have either managed to redeem out of the fund at a loss after a protracted struggle, or they are stuck in the fund with no prospect of getting out of it any time soon (if ever).

A year ago, the underlying assets of the fund were confirmed to one victim by Optimus Fiduciaries Ltd, an IoM domiciled company managing the Optimus Retirement Benefits #1 QROPS. Further research discovered these underlying assets were a load of toxic, illiquid, high-risk crap.

Neither Slater and Gordon nor Grant Thornton will confirm what the assets are or how much they are worth – despite Nunn and McCreesh claiming the fund has “£17m under management”. However, £17m is nothing more than a meaningless figure on a piece of paper until such time as the assets are independently verified and audited. Nunn & McCreesh have promised to publish audited accounts for over 12 months now, but failed to do so. One can only assume that to do so would instantly crystallise a true value far below the imaginary £17m and result in a sudden collapse of the fund.

Nunn and McCreesh claim Meriden Capital Partners are the investment manager to the fund

I have asked Steve Kunziewicz of Slater and Gordon on numerous occasions this past couple of months to tell me what the assets are, but presumably Nunn and McCreesh won’t tell their own solicitor – any more than they will tell their own auditors. Perhaps they told the Blackmore Global investment manager, Meriden Capital Partners in Barcelona? The trouble is that Meriden Capital Partners deny that they were ever investment manager to the fund and that Nunn and McCreesh are lying.

I hope the irony of this situation is not lost on the gentle reader: Slater and Gordon solicitors and Grant Thornton being “gamekeepers turned poachers”. My suggestion to both firms is that they should choose their clients carefully and protect their public image diligently. Both firms should decide whether they want to be like Bark and Co who openly represent fraudsters, murderers, insider dealers, hackers, race fixers and other criminals. Or whether they want to be on the side of justice for victims of pension and investment scammers. Because they can’t do both.

Regulators have got to do some effective regulating

Regulators and scammers; cops and robbers; cowboys and indians. Each has their role: cowboys fire their six shooters and dodge the injuns’ arrows valiantly; cops drive their police cars at breakneck speed to corner the robbers in a dark alley; regulators waggle their flaccid willies and watch the scammers walk all over them.

In the week my great friend had his appendix out (somewhat hurriedly as it happens) I thought I would write a slight variation on the Three Sausages poem:

Regulation, regulation, regulation, Three scammers went to the station, One got crushed, one got killed, And one got a huge operation.

The sizzling scammers need to be put behind bars – and the keys need to be thrown away.

Now, I am not suggesting I want the scammers crushed or killed – nor even that they suffer the same pain and discomfort that my mate has gone through in hospital this past week. But I do want them stopped from harming more victims and destroying more life savings. And, of course, put behind bars where the only thing they can scam is the soap on a rope.

WHAT DO REGULATORS NEED TO DO AS A MATTER OF URGENCY?

All regulators in all jurisdictions where has been a history of scamming and mis-selling need to work closely with governments, tax authorities, financial crime units, ombudsmen and the press. There has to be a “zero tolerance” attitude to scams and scammers – and all those responsible have to be brought to justice. And publicly so. It is clear that most regulators – including the FCA – are limp, lazy and useless and this has to change. Here are some examples of regulators’ failures in each jurisdiction:

Allowing unregulated firms to provide financial, pension and investment advice freely and without sanction in the UK. Sometimes these firms have an insurance license – sometimes none at all

Not sanctioning regulated firms for clear breaches and/or fraud – such as Gerard Associates which was introducing Ark victims to Stephen Ward of Premier Pension Solutions as far back as 2010, and was then providing “advice” to Ward’s London Quantum victims

Ignoring firms such as Fast Pensions who have defied 37 Pensions Ombudsmen’s determinations

Failing to coordinate criminal prosecutions against the scammers behind numerous scams who ruined thousands of lives and cost hundreds of millions of pounds’ worth of life savings

Failing to use existing legislation provided by FSMA 2000 to prosecute advisors (regulated and/or unregulated) overtly contravening the ban on communicating invitations to retail clients to invest in Unregulated Collective Investment Schemes

Announcing ineffective crack-down plans by newly-appointed government minsters who have failed to grasp the enormity of the pension scamming industry and the desperate plight of thousands of pension scam victims

Failing to police and sanction negligent pension trustees such as STM Fidecs for accepting members introduced by an unlicensed adviser: XXXX XXXX of Global Partners Ltd/The Pension Reporter – who was also the fund manager for the UCIS that all the victims had their pensions invested in and which is now being wound up

Refusing to communicate with members on the progress of the winding up of the Trafalgar Multi Asset Fund which had been run by XXXX XXXX

Omitting to take action against STM Fidecs for its role in the Cornerstone Friendly Society investment scam

Taking no action against Trustees, Integrated Capabilities Malta Ltd (ICML) for accepting retail members from an unlicensed firm in the Czech Republic and knowingly permitting investments in Nunn McCreesh’s UCIS: Blackmore Global, as well as Malta-licensed fund Symphony – a sub-fund of the Nascent Platform that is licensed only for professional investors

Not sanctioning Customs House Global, that runs the Nascent Platform, for inadequate due diligence and accepting unscrupulous sub-fund managers (such as XXXX XXXX, investment manager of failed TMAF and later, the recently wound up Symphony Fund) that exploit the platform for the sole purpose of pension scamming

Allowing an unlicensed firm – Square Mile Financial Services – to operate freely in the EU, providing pension and investment advice with only an insurance mediation license

Ignoring insurance companies which accept investments in UCIS funds and professional-investor-only instruments for retail investors

Failing to recognise those registered Closed-Ended Investment Companies whose true nature is as a Collective Investment irrespective of their form, such as Blackmore Global (registered number 010221V), that intentionally circumvent the stricter regulations imposed on collective investments, specifically to hide their financial accounts and the sub-funds which invariably include unsigned loan notes and high-risk hare-brained projects

Failing to act against a pension liberation scam – Evergreen Retirement Benefits Scheme – run by Simon Swallow who was working with Stephen Ward of Premier Pension Solutions and operating Marazion “loans”

Ignoring Concept Trustees (Guernsey) who offered retail investors the EEA Life Settlements UCIS and then accepted investment instructions from unlicensed, un-insured Stephen Ward of Premier Pension Solutions

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Laurence Goodman and the three wishes: please make 37 Fast Pensions Scam loans disappear JUST LIKE THAT!

Bridgebank Capital’s Laurence Badman Goodman has made 37 Fast Pensions Scam loans disappear as if by magic – while he was on holiday and too busy to engage with Pension Life or the distraught victims of Peter and Sara Moat.

Having discovered this was where some or all of the elusive Fast Pensions Scam funds were hiding, we all hoped this might finally result in some of the 18 Pensions Ombudsman’s determinations to allow victims to transfer out being complied with.

We all wanted to believe that Goodman was a good man, but now it would seem the opposite might be the case. So, one of the following is true:

All the borrowers of the 37 loans have simultaneously repaid their loans on 17th August 2017

The loans have been sold or transferred on to somewhere we can find them (yet)

Sara Moat had been claiming that Fast Pensions was merely the administrator of the pension schemes, and that it was ultimately the “responsibility of the trustees to decide whether the transfers could be made”. Of course, the Companies House records showed that the Bridgebank Capital loans were made in favour of Sara Moat as trustee (along with another stooge called Martin Peacock). This scuppered Sara Moat’s excuse and exposed her as a liar once again.

So, when Goodman has finished having a jolly time on the Costa Lot, necking his champers and writing his postcards to his mate Pete, perhaps he might find a moment to be sober enough to remember that I am meeting the Serious Fraud Office next week. And most of the Fast Pensions Scam victims have also submitted their reports to the SFO.

Frantic with worry – the Fast Pensions victims now know their pension funds are being used for property loans.

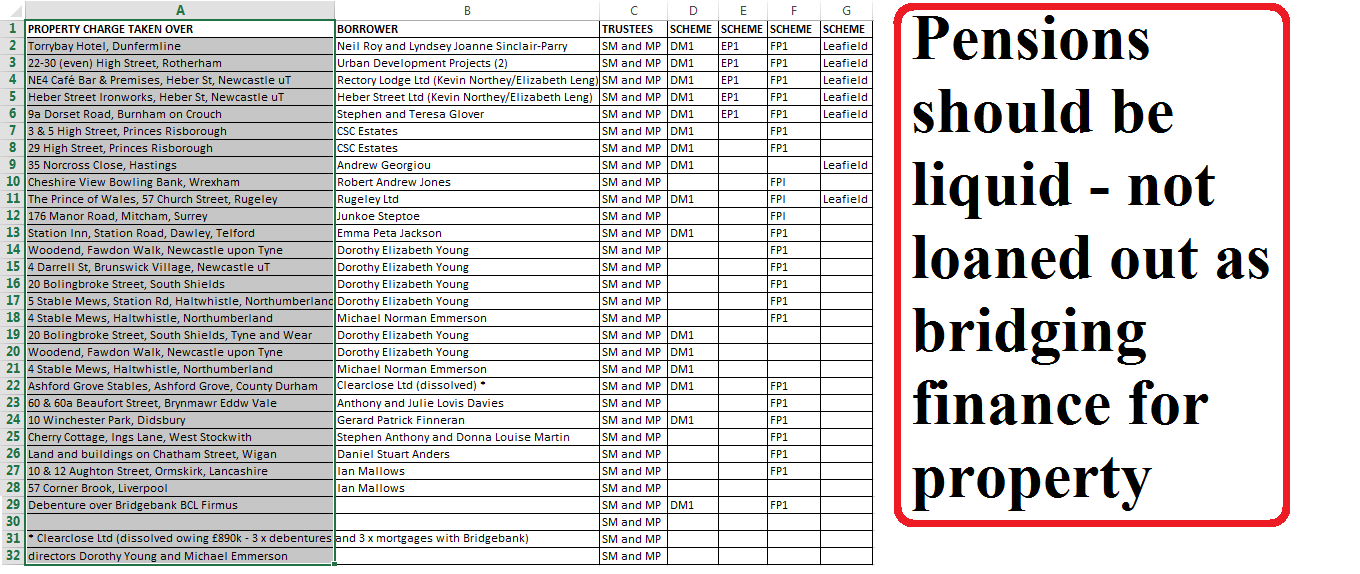

Bridgebank Capital seems to be a bona fide property loan company – providing bridging and development finance. Nothing wrong with that.

But Bridgebank Capital No. 5 seems to be full of Fast Pensions money and locked into term loans secured on a variety of domestic and commercial properties. Each charge refers to the trustees of four of the Fast Pensions schemes: DM1, FP1, EP1 and Leafield. The trustees of each of these schemes are clearly identified at Companies House as Sara Moat and Martin Peacock. (Interestingly, Sara Moat is telling victims that “the trustees” have to decide what happens to the pension monies – while hiding the fact that she is the trustee).

Of great concern is the fact that one of the borrowers, Clearclose, has gone bust owing the pension fund nearly £900k.

The Pensions Ombudsman has made 18 determinations against Fast Pensions – but Sara and Peter Moat of Fast Pensions have studiously ignored them. I sent links to all of the background to Fast Pensions to Laurence Goodman of Bridgebank Capital on 6th August 2017:

Dear Mr. Goodman

It was good to speak to you on Friday.

First of all, may I say that I recognise that Bridgebank Capital is a bona fide finance company and I mean no criticism against you or your company in the summary I am setting out below. I have tried to summarise the position in a bullet-point series of statements to make this as easy to understand as possible.

Once you have read and digested this, please can we start a dialogue about what happens next. What the members need to know, is how much do these various loans/charges/mortgages in favour of the four Fast Pensions schemes realise when they mature, and what will happen to the money. I realise you are restricted to an extent in terms of what you can tell me, but there are many Fast Pensions victims who will happily provide you with letters of authority as they are the beneficiaries of the pension schemes and have a legal right to know what has happened to their pension funds.

Best, Angie

—————-

* There are hundreds of members of various pension schemes (including DM1, FP1, EP1 and Leafield) run by Peter and Sara Moat of Fast Pensions – a pensions administration company.

* The Moats maintain they are not the trustees of the schemes. Peter Moat (masquerading as “James Porter”) told me the trustee was a company called FP Scheme Trustees, of which one Jane Wright is sole director. She was an employee of Moat’s at his former company Blu Properties in Javea which folded and it is believed she was paid to be the director of this company.

* The charges registered at Companies House for Bridgebank Capital No. 5 show all the loans as being in favour of Sara Moat and Martin Peacock (an associate of Peter Moat’s) as trustees of the Fast Pensions schemes.

* The various Fast Pensions schemes – including DM1, FP1, EP1 and Leafield – I believe are all bogus occupational schemes. When I say bogus, what I mean is that they were not set up to provide genuine pensions for employees of a company which intended to trade and create jobs, but merely as a vehicle for a pension liberation scam.

* Peter Moat told me (while he was masquerading as a “James Porter”) that the underlying assets of the Fast Pensions schemes were “invested in Bridgebank Capital” and also in another loan company called Pamplona Capital Partners. Clearly, having the underlying assets of a pension scheme solely “invested” in property loans is not acceptable. A pension scheme is required to have low-risk, liquid assets as members have a statutory right to a transfer and need to be able to take their 25% tax-free lump sum at age 55, or retire or die.

* The Moats have failed dismally to communicate with the members or respond to transfer requests for a long period of time – causing considerable distress to the victims. The Pensions Ombudsman has made a large number of determinations in response to complaints by the victims and has ordered Fast Pensions to allow the victims to transfer out and pay compensation for their distress. These 18 determinations have all been ignored by Fast Pensions:

Needless to say, there is no evidence that the Moats have complied with any of these determinations and the victims themselves report that they have not.

* Alongside the pension transfers and lending of the pension funds to Bridgebank Capital No. 5, the Moats were operating pension liberation in the form of loans from Moat’s companies Blu Debt Management and Umbrella Loans. Victims were told these loans were not connected to the pension transfers and would not be taxable. HMRC is now sending out tax demands in respect of these loans.

* There are grave concerns about the Bridgebank Capital No. 5 loans for the following reasons:

1. We do not know what the total amount lent to Bridgebank Capital is

2. There are multiple loans to the same parties

3. One borrower is in liquidation

4, We do not know what the terms of the loans or the interest payable are

* The greatest concern is that if any part of the money is recoverable and is paid back into the control of the Moats, it will simply “disappear” again and not be available for the benefit of the members who are the ultimate beneficiaries.

Investors are likely to have lost all their money in Premier New Earth Recycling fund – now in liquidation. The liquidator is Deloittes and they can’t say much, if anything, about what is happening as they are looking into the possibility of claims against third parties and don’t want to prejudice any possible action.

Rather than getting into the nitty gritty of the liquidation of this fund – and the appalling possibility that the investors may very well have lost everything – let us take a good look at the fund itself.

It is a UCIS. Nothing more to say – except:

“Specialist, qualifying, and qualifying-type experienced investor funds are unregulated collective investment schemes which are neither approved nor reviewed by IOMFSA. Once launched, the funds must be registered with the authority within 14 days. These types of funds cannot be sold to the retail public. Access to such funds is only available where investors confirm that they meet the fund type’s minimum entry criteria. This includes a statutory certification that they have read the scheme’s offering document and understand and accept the specific risks associated with that type of fund.”

So, instead of writing lots of fascinating stuff about the wonderful topic of generating energy from rubbish (which I am sure is really interesting and good for the planet), why don’t we stick with the unchallengeable fact that the fund was a UCIS and should not have been promoted to retail investors. End of. No argument. Non-negotiable. Talk to the hand. Stick your UCIS where the sun doesn’t shine.

In fact, the same was true (should have been true) of the Connaught bridging loan fund; EEA Life Settlements; LM; Store First, Park First, Trafalgar Multi-Asset Fund and Blackmore Global. So why did so many advisers promote them and invest their clients’ money in them? £$£$£$£$£!!! Commissions. Backhanders. Sandwiches. And the distressed investors are now paying the appalling price for rogue advisers’ greed and negligence.

And what does this look like from the investor’s point of view?

Appalling investment losses on Premier New Earth Recycling

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

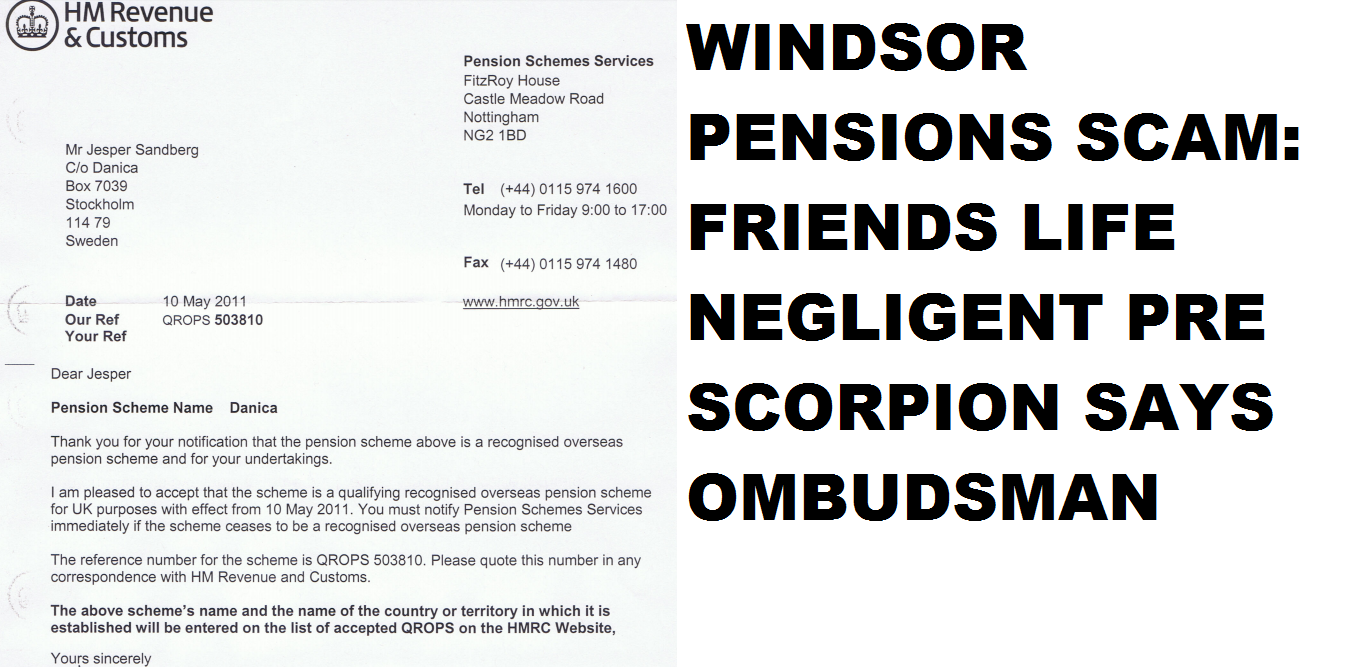

Friends Life negligent in Windsor Pensions “Danica” scam

FRIENDS LIFE – OR DEATH? WINDSOR PENSIONS QROPS SCAM (DANICA)

Since 2010, dozens of ceding pension providers have recklessly and negligently allowed transfers out to obvious pension scams. During the years of Ark, Capita Oak, Westminster and Henley, the worst offenders were Standard Life, Scottish Widows, Prudential and Aviva as personal providers, and Royal Mail as an occupational provider.

Both HMRC and the Pensions Regulator claim there were sufficient/ample warnings in the public domain to educate and inform ceding providers about pension scams since 2002. But the Pensions Ombudsman’s Service claims the cut-off date was February 2013 when the Pensions Regulator first published the “Scorpion Campaign”. According to the POS, before Scorpion all ceding providers walked around with paper bags over their heads and did no reading up on their professional and fiduciary obligations or any developments among scams and scammers.

However, a recent ruling on the negligence of a ceding provider – Friends Provident – may change the course of history. The case of “Mrs N” involved a transfer from FP administered by a company called Windsor Pensions run by one Steve Pimlott in Florida. In fact, I “secret shopped” Windsor and Pimlott in 2015, and he was still offering “transfers to Danica QROPS” with full liberation. He also claimed to have done 5,000 such transfers/liberations.

On 25 February 2015 at 10:37, STEVE PIMLOTT <stevepimlott@windsorpensions.com> wrote: Dear Ms Brooks

I cannot give you tax advice. If you cash out, it’s possible that HMRC will send you a tax bill. We assisted approximately 5,000 people who took that route and I would estimate that 200-300 did receive a tax bill. The rest to my knowledge did not. Of those that did, many just ignored it because they were resident in a different country and had no assets left in the UK.

Regards

Steve

The question is, however, does this set the bar for other negligent ceding trustees? This case is notable because it is “pre Scorpion”. But the POS found that irrespective of the date, Friends Provident should have done more due diligence and not just handed over a pension to a scheme which was no longer registered (and, de facto, to a fraudulently-set-up bank account).

Mrs N’s complaint is upheld and to put matters right Friends Life should pay her the unauthorised member payment tax charge and surcharge less the tax liability she would have paid had the full pension been taken as an uncrystallised funds pension lump sum (UFPLS). In addition it should pay Mrs N £1,000 for the significant distress and inconvenience caused by its error.

My reasons for reaching this decision are explained in more detail below.

Complaint summary

Mrs N complained that Friends Life undertook insufficient due diligence on the qualifying recognised overseas pension scheme (QROPS) into which she had requested a transfer. Had it acted appropriately it would not have accepted the transfer instruction.

Following the transfer Mrs N received the full value of her pension. At the time she was 53. As a result she is now liable to a 55% unauthorised member payment tax charge.

Mrs N has also said she has incurred costs whilst attempting to resolve the situation and Friends Life should pay these.

Background information, including submissions from the parties

On 10 May 2011, HMRC wrote to Danica, Stockholm, confirming undertakings had been received that Danica was a recognised overseas pension scheme, and that HMRC would accept the scheme as a QROPS with effect from 10 May 2011. It provided a QROPS reference number – QROPS 503810 – and confirmed that the scheme name and country would be added to the list of accepted QROPS on HMRC’s website.

Danica was added to the HMRC QROPS list, but then removed on 29 June 2011.

In October 2011 Mrs N completed a letter of authority for an unregulated financial intermediary; Insignia Financial Services. This was submitted to Friends Life which responded with a transfer illustration on 3 January 2012. QROPS illustrations were issued on 21 January 2012.

On 16 February 2016, Friends Life received an Overseas Transfer Out Payment form and Member Declaration, signed by Mrs N on 7 February 2012. Accompanying this was the HMRC letter confirming QROPS status.

QROPS discharge forms were issued to Mrs N shortly after.

The required forms were received by Friends Life on 9 March 2012. Friends Life says that the supplied QROPS number was checked against the QROPS list and found to be correct. Friends Life also checked the HM Treasury sanctions list.

The payment of £88,622.80 was processed on 13 March 2012. However, what the POS has not disclosed is that the funds were sent to a Barclays Bank account in the Isle of Man which was fraudulently set up by the scammers with the account name “Danica”. I understand the money was subsequently paid to Mrs N by the Danica arrangement and has since been spent. No it wasn’t. The money never went near the Danica pension scheme in Sweden. It went straight to the scammers’ bank account in IoM.

Friends Life were made aware of an issue with the Danica scheme, and Insignia Financial Services on 13 April 2012.

Mrs N has since been contacted by HMRC and informed that the transfer was an unauthorised payment, so it is subject to an unauthorised member payment tax charge and surcharge of approximately £49,000. I understand this has not been paid and remains outstanding, with interest accruing.

Mrs N raised a complaint about Friends Life’s actions. It did not uphold the complaint, and made the following summarised points.

Mrs N had a statutory right to transfer, and Friends Life had no reason to think that the information provided regarding the QROPS was false. Friends Life missed a rather obvious clue i.e. a QROPS in Sweden was purportedly using a Barclays bank account in the IoM – might that not have rung an alarm bell?

The QROPS number was checked against the QROPS list and found to be correct. Although the name Danica did not appear on the QROPS list, Danica Private Pension (Sweden) and Danica Pension (Sweden) did. In other words, similar but different.

The transfer happened prior to concerns about pensions liberation being widely recognised as an industry issue. The Pension Ombudsman has previously said that February 2013 was the point of change in good industry practice where knowledge of pension liberation and scams had increased. This is nonsense – both the Pensions Regulator (formerly known as OPRA) and HMRC had been warning the industry about pension scams for more than fifteen years. Friends Life had an absolute duty to be aware of and vigilant against pension scams.

The presence of a scheme on the QROPS list does not guarantee its QROPS status, and HMRC forms which would have been completed by Mrs N state: “The list should not be relied upon by you, the member in deciding whether a scheme is a QROPS.” Pretty confusing to be honest: HMRC publishes a list of QROPS but the member herself has to decide whether the scheme is a QROPS. How would a member decide that? Ask the scammers?

Friends Life suggested that Mrs N transferred her pension with full knowledge of a lump sum payment being made, which was not offered under her existing plan due to UK tax legislation. It was reasonable to expect that she would have sought independent financial advice before proceeding. Instead she proceeded through an unregulated financial adviser and did not seek advice from a regulated adviser. Indeed, the adviser was unregulated – but Mrs. N did not know this and wouldn’t have known how to check anyway. In fact, Friends Life ought to have brought this to her attention at the start.

There was an onus on Mrs N to check the legitimacy of her financial adviser. At the time there was no reason for Friends Life to think the financial adviser was unregulated. Friends Life didn’t even check.

Friends Life had highlighted that, ‘Tax penalties may apply following a transfer to a QROPS. It is important all implications are understood before transferring funds from the UK’, and Mrs N had received a copy of this statement.

Adjudicator’s Opinion

Mrs N’s complaint was considered by one of our Adjudicators who concluded that further action was required by Friends Life. The Adjudicator’s findings are summarised briefly below:-

Central to the complaint was whether Friends Life should have acted on Mrs N’s transfer request. Side issues relating to the legitimacy of the financial adviser involved or any declarations signed were not integral to the complaint.

The events complained of occurred prior to the Pension Regulator’s pension liberation warning campaign of February 2013, at a time when checks on receiving schemes were less rigorous. This may be correct – however, that doesn’t make it right. However there were reasonable basic checks that Friends Life ought to have completed before making the transfer, including checking HMRC’s QROPS list. They did check the QROPS list and were probably confused by the similar names of two other schemes containing the word “Danica”.

The Danica scheme had been on the list for a short period but was removed by the time Mrs N submitted the transfer request. Friends Life’s internal policy was not to transfer to schemes which were not on the QROPS list.

Although the QROPS list was checked the day before the transfer was put through and there were two similarly named schemes on the list, the Danica scheme was not on the list. At that point additional checks should have been undertaken to establish why the Danica scheme was not on the list, had it done so it would have established that the Danica scheme had been removed nine months prior.

In these circumstances Mrs N’s pension should not have been transferred, and had it not done so Mrs N would not now be subject to the unauthorised member payment tax charge and surcharge. One could argue against this point – perhaps Windsor Pensions and Insignia Financial Services would have found another obscure QROPS to use for the fraud.

To put matters right Friends Life should agree to meet the full cost of the unauthorised member payment tax charge and in addition pay Mrs N £500 for the distress and inconvenience suffered.

The Adjudicator did not consider Friends Life should be required to pay the costs Mrs N incurred when bringing the complaint. The complaint could have been referred to this Office and resolved without the involvement of her representative. I would not agree necessarily: Mrs. N had a very busy life running a business in the USA and she did need help and guidance with the complaint against Friends Life and the POS process. She was also fighting the tax demand at the same time and was extremely distressed.

Additionally, in relation to potential accountant’s fees she may incur, the Adjudicator concluded she would have needed to pay similar costs had the funds been received through legitimate means.

Mrs N did not accept the Adjudicator’s Opinion and the complaint was passed to me to consider. Mrs N and Friends Life provided further comments which are summarised below.

Friends Life said:-

Friends Life accepted the recommended redress in principle, but highlighted that it had already paid a 40% Scheme Sanction Charge and Mrs N was, under the Adjudicator’s recommendation, in effect being paid the fund value without any tax liability. Friends Life proposed to pay the unauthorised member charge less the notional tax Mrs N would have paid had she legitimately accessed the full fund value under the current rules. It calculated the tax she would have paid to be £15,294.34.

Friends Life also considered that given Mrs N’s position it was reasonable for her to have sought independent financial advice given its recommendation that she do so, and especially given her unfamiliarity with UK taxation laws. In not doing so Mrs N had contributed to the risk that her pension could be adversely impacted by the transfer.

Mrs N said:-

The proposed redress would have significant tax consequences for her as a U.S. resident. As a result the redress would not put her back into the position she should have been had the error not occurred.

She had incurred significant expenditure appointing a representative to pursue the complaint on her behalf. Those costs, and the cost of receiving appropriate cross border tax advice, would continue to rise. Given the complexity of the issues in the complaint, and the tax complications she could not have brought the complaint without specialist assistance.

The redress methodology used by Friends Life show a misunderstanding of Mrs N’s tax position. For instance it has suggested that she would be entitled to a personal allowance, when as a U.S. resident this is not the case.

The wording of the redress must be specifically tailored to avoid potential tax complications in the UK and U.S. Friends Life should pay the costs associated with drafting agreeable wording to avoid those tax complications.

Friends Life should provide an indemnity to cover the potential tax liability arising from the redress payment.

She was very distressed by the situation, has been unable to sleep and it has impacted her health.

On review of Friends Life’s and Mrs N’s responses to the Opinion the Adjudicator made the following points:-

* Friends Life’s offer to pay the unauthorised member payment tax charge and surcharge, less the tax Mrs N would have paid had the pension been paid as an UFPLS, was reasonable in the circumstances. The recommended redress was altered to reflect this.

* The redress was not intended to pay Mrs N’s tax liability. Mrs N was the party subject to the liability and would need to pay this. The redress was intended to make good a relevant proportion of that loss once it had been paid. Under this arrangement the reference to a personal allowance was only notional it did not appear that Mrs N would be subject to punitive tax charges as the redress was intended to make good Friends Life’s error.

* Given the significant impact on Mrs N’s health the Adjudicator increased the proposed distress and inconvenience award to £1,000, which Friends Life agreed to.

Having considered Mrs N’s arguments they do not change the outcome. I agree with the Adjudicator’s Opinion, summarised above, and I will therefore only respond to the key points made by Mrs N for completeness.

Ombudsman’s decision

Mrs N argues that she could not have brought the complaint without employing the assistance of tax and pensions specialist. I do not agree. In the first instance a complaint can be passed to the Pensions Advisory Service, who can guide an applicant through the Scheme’s complaint process and provide technical input where the applicant lacks an understanding of the issues involved. In this case TPAS considered it too late to intervene due to the potential time limits of referral to this Office. So it was not a lack of understanding that prevented TPAS from taking on the case.

Notwithstanding that, had Mrs N not accepted Friends Life’s response to the complaint she could have brought the complaint directly to this Office for review. Although Mrs N’s representative disagrees, I am confident that this Office has the expertise to investigate complaints about pension liberation. I would dispute that: the POS has repeatedly failed to uphold pre-Scorpion complaints on the basis that pension trustees had never heard of pension liberation fraud prior to February 2013 – which is absolute nonsense. The representative’s involvement has not brought any unknown evidence or arguments to the investigation. Mrs N was entitled to seek assistance in this matter, but that does not mean Friends Life are responsible for the costs incurred where there are free dispute resolution alternatives available to her. For that reason I do not consider Friends Life should pay the costs she is claiming. To be fair, I think Mrs N should have had her costs paid. She – and thousands of other victims in this situation – find themselves utterly overwhelmed by these types of cases and need support. Also, being based in the USA, she needed someone to deal with the case in the UK.

I understand that as a U.S. tax resident there may be complications in Mrs N’s tax situation on receipt of the redress payment. Her UK and U.S. accountants have said they will not provide advice on the matter because of the complications. The redress may cause her to have to seek specialist tax advice. However, tax is matter for Mrs N and the local tax authorities. It is not for me to determine any future tax liability she may have, and it may ultimately be that there is none.

I have also taken into account that had Mrs N taken her pension through legitimate means she would have needed to seek tax advice regardless, so in my view the position has not changed. Mrs N will have had to pay for tax advice at some time or another regardless of how the pension was accessed.

Friends Life has said it does not believe that the redress payment would be taxable, but that it would reconsider its position if at a later date it can be shown that Mrs N had suffered a tax liability, although it would not agree to an indemnity. This is a reasonable stance for Friends Life to take. Mrs N should establish any resultant tax liability due to the redress and communicate that to Friends Life if necessary.

Looking at the proposed redress methodology, Mrs N may disagree with certain assumptions made by Friends Life, but I consider they are reasonable assumptions. I note in particular that in relation to the personal allowance, under this notional methodology, she is better off for it being included than if Friends Life assumed no personal allowance.

The approach taken to offsetting the notional income tax that Mrs N would have paid had she taken the full fund value as an UFPLS is balanced and appropriate. This places Mrs N broadly in line with the position she would have been had the pension been taken in full under the current rules. I believe that is an appropriate remedy for the error caused by Friends Life.

Therefore, I uphold Mrs N’s complaint.

Directions

Within 28 days of this determination Friends Life should establish the unauthorised member payment tax charge and surcharge less the notional tax liability of £15,294.34 she would have paid had the full pension been taken as an uncrystallised funds and pay this to Mrs N. PO-9935 7 31. Additionally it should pay £1,000 for the significant distress and inconvenience suffered.

London Quantum is a pension scheme whose trustee was a firm called Dorrixo Alliance run by our old friend Stephen Ward. That name will, of course, send a chill down the spines of many pension scam victims. Since 2010, Ward had been involved – either at the top or the bottom of the pond – in numerous pension scams. He eventually decided to “go straight” and declared that Ark was history – although Ark was far from history for his hundreds of victims who are now facing financial ruin.