In the wake of hundreds of victims fearing heavy pension losses in the Blackmore Global fund, we now have another disaster waiting to happen: Blackmore Bond.

This new threat to unwary investors has been analysed by Bond Review. Just to be clear, many people were duped into investing their pensions in the Blackmore Global UCIS fund – which has never published an independent audit. We now have a second threat offered by Phillip Nunn and Patrick McCreesh. Blackmore Bond PLC is promoting these unregulated, capital-at-risk bonds which purport to pay up to 8.5% per annum – but with potential for total loss. How many more people will this high-risk bond ruin financially?

BLACKMORE BOND – SHAKEN OR STIRRED – CARELESS OR STUPID?

Bond Review raises an intriguing question: how come Paul Careless and Surge Group have got involved with Nunn and McCreesh? Unless he has been careless (pun intended), Careless looks to have an unblemished past and Surge (in Brighton) looks to be a bona fide company.

In 2017, Careless’ company Surge Group offered £3,000 in sponsorship to the Kent Police rugby team. This was accepted, but then he tried to change the sponsor from Surge Group to Blackmore Bond. And Blackmore Global started claiming on their website to be “Proud supporters of Kent Police Rugby Team”. So why would Careless – himself an ex-police officer – try to con the police and also get into bed with Nunn and McCreesh?

Let us just remind ourselves that Messrs Nunn and McCreesh were the cold callers/lead generators in the Capita Oak and Henley Retirement Benefits scams which are now under investigation by the Serious Fraud Office. Nunn and McCreesh scammed/attempted to scam up to 300 victims a month for more than two years. Unsurprisingly, Kent Police declined the toxic offer to have any association between a law-enforcement agency and known scammers.

But here’s another puzzle: a geezer called Kenneth “Buzz” West also appears at first glance to be relatively harmless. He is a director of numerous companies – including European Wealth. The only stain on his reputation that I can find is that his former company, Ashcourt Rowan, was fined £412k by the FSA in 2012 for dodgy investments in his other company: Savoy Group. But Ashcourt Rowan held its hands up and paid the fine.

So why on earth would “Buzz” risk getting tangled up with Nunn and McCreesh? Buzz is now Chairman of two of their companies: Blackmore Group and Blackmore Bond. Unless his brains are shaken as well as stirred, he is committing professional suicide – knowingly and deliberately.

Or perhaps I am being too harsh. Maybe he has taken on the role of Chairman so that he can ensure that Blackmore Bond does not sell any toxic, high-risk products to low-risk victims; and also so that he can get the long-overdue Blackmore Global fund audit done. Maybe he also has plans to get the Blackmore Global victims compensated for their losses and distress suffered in the past couple of years.

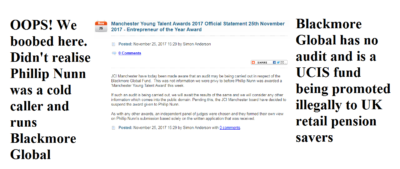

We need to be very clear about Blackmore Global: it is a UCIS fund that was illegally promoted to retail investors in the UK and which unregulated David Vilka of Square Mile International was flogging to UK victims in the Hong Kong QROPS scam. This accounted for 64 victims with a combined transfer value of £1.6 million – all introduced by cold-calling firm Aspinall Chase – run by Nunn and McCreesh.

It just so happens that I am going to Cyprus in a couple of weeks – so hopefully he will invite me for a wee drop of Zivania and Halloumi on toast. And once our whistles are whetted, we can discuss the Blackmore Global audit and compensation.

Pension scammers are hidden all around us, often dressed in smart clothes, driving smart cars and carrying impressive leather folders. They offer what seems like smart investments, push through your pension fund transfer swiftly and seamlessly. However what you don´t see on the surface is their hidden parasitic ways. These scammers will drain the funds from your pension, investing in high-risk, toxic investments, that only they will profit from.

Here´s Pension Life´s, “Top 10 Pension Scammers”. (Please note: this information is correct as of the today´s date only, as pension scammers are evolving daily and as one falls another will rise!)

John (Gus) Ferguson’s firm Square Mile International promote unregulated toxic crap to pension savers and employs unqualified David Vilka. The so-called “advisers” promoted the Blackmore Global Fund.

It is still unclear what has actually happened to the money invested into the Blackmore Global Fund.

James Lau was a financial adviser with Wightman, Fletcher McCabe (FSA regulated) – part of the Clarkson Hill Group. Along with directors Peter Bradley and Andrew Meeson, of Tudor Capital Management (subsequently jailed for eight years for money laundering and tax fraud), James Lau conned 116 victims into transferring their pensions, investing in forex trading companies, and liberating up to 85% of their pensions. Lau is now rumoured to be in hiding in Hong Kong. The victims are now facing 55% tax charges by HMRC.

8 – Friendly Pensions

David Austen of Friendly Pensions, used cold-calling and high-pressure sales tactics to strong-arm 245 victims into investing in 11 fake schemes, including a truffle farm.

Dalton, Barratt and Hanson all served as trustees on the fake schemes set up by Austin – who is described as the mastermind – and were paid more than £550,000 between them. The four scammers who conned pension savers out of £13.7 million have now been banned from the industry but not imprisoned. The victims, however, lost everything.

One thousand people were relieved of up to £100 million worth of pension funds. Conned by a motley assortment of snake oil salesmen, the victims were promised high returns, but all they got was high losses. Old Mutual International (OMI) were the provider for the bulk of the insurance bonds in this scam. Funds were invested in risky, toxic structured notes which were clearly labelled as “for professional investors only”. Clients were lied to, as when they saw the value of their funds plunging dramatically, the Continental Wealth Management scammers assured the victims that the reported losses were “only paper losses”. Continental Wealth Management collapsed in September 2017.

6 -XXXX XXXX

XXXX XXXX was the “distributor” of the Capita Oak, Henley, Westminster and various SIPPS scams in 2012/13. He was also operating pension liberation fraud with his “loan” company: Thurlstone. When these schemes collapsed in 2013, he went on to launch an investment scam called Trafalgar Multi Asset Fund. Capita Oak, Henley, Westminster and Trafalgar Multi Asset Fund are now all under investigation by the Serious Fraud Office. XXXX XXXX has been arrested and his offices searched.

Phillip Nunn – along with his sidekick and partner in crime Patrick McCreesh – provided “lead generation” services to the Capita Oak and Henley scams. At up to 200 leads a month for more than two years, he was responsible for the destruction of £ millions of pension funds – and got paid nearly £1 million in fees for doing so. He then went on to set up an investment scam called Blackmore Global – a UCIS which is illegal to be promoted to retail pension savers. It is not known whether the investors have lost some, most or all of the funds in Blackmore Global as Phillip Nunn refuses to have an independent audit carried out on the fund.

Steve Pimlott has been running Windsor Pensions for at least seven years. He claims to have done around 5,000 pension liberations and assures victims that HMRC will be “unlikely” to catch up with them. Pimlott uses QROPS schemes such as Danica in Sweden and then sets up a fraudulent bank account in the Isle of Man. The transfer never goes anywhere near Danica, of course. But the transfer is sent to the IoM bank account – 85% is paid out to the victim and Pimlott trousers the other 15%. HMRC is now taxing the victims at 55% – although they have never taken action against Pimlott who is still operating happily in Florida (not far from where Stephen Ward has his six luxury villas).

Peter Moat and his wife Sara Moat were chums of Stephen Ward of Premier Pension Solutions. They ran a loan company called Blu Debt Management and also had several other businesses involving estate agency and pension administration. Hundreds of victims were transferred into the Moats’ Fast Pension schemes, and now the victims cannot access their pensions or transfer out. Peter and Sara Moat live in the Javea area of the Spanish Costa Blanca and have had 18 Pensions Ombudsman’s determinations against them for mal-administration of the pension schemes they are running. It is thought that around 400 victims are affected, although it is not known how much they have lost between them. It is known that several years ago, a substantial amount of the funds were loaned to Bridgebank Capital and then used as bridging loans for property developers. But the money has since been repaid and goodness only knows where it is now. Certainly not accessible to the members.

Capita Oak: 300 victims; £10 million at risk; tax penalties on XXXX XXXX’s Thurlstone “loans”

Westminster: 200 victims; £7 million at risk; tax penalties on “loans”

Southlands, Headforte, Feldspar, Hammerley, Maribel, Dorrixo Alliance, Halkin, Bollington Wood, Randwick Estates, Elysian Fuels, London Quantum – and many more. Stephen Ward remains active with DB transfers.

and in first position we have …..

1 – HMRC

Yes, you read correctly, HMRC is our number-one culprit in the Top 10 pension scammers list. And here’s why:

Since at least 2010, pension scams have been on the rise. That’s 8 years, yet regulations have not been changed, HMRC has not become vigilant or conscientious about registering pension scams, and new laws have not been put in place to stop scammers.

In fact, the scams are registered in the first place by HMRC, and in the case of occupational schemes also by tPR.

No notice is taken of whether the schemes are registered by known scammers and no questions are asked as to the purpose of the schemes.

In the case of James Lau’s Salmon Enterprises, the trustees – Meeson and Bradley – had been investigated by HMRC and arrested in March 2010 on suspicion of money laundering and tax fraud. However, HMRC did nothing to warn ceding providers or the public and Salmon Enterprises was left as an HMRC-registered, fully-operational occupational scheme.

Later that year, one ceding provider queried the legitimacy of the Salmon Enterprises scheme, but HMRC refused to elaborate on why the trustees had been arrested. A transfer went ahead – along with 115 others – while HMRC sat back in the full knowledge that all these victims would be bound to face unauthorised payment tax charges.

In the Ark case, HMRC spoke to the organisers and promoters (including Stephen Ward) of the six Ark schemes on several occasions. They then had a meeting with Craig Tweedley and Ward in February 2011 to discuss their concerns that the 50% “loans” paid out to scheme members constituted unauthorised payments. At this point there was a “mere” £7 million worth of transfers. Nothing was done to suspend the Ark schemes for another three months – during which time a further £20 million was transferred in. HMRC is now trying to tax both the members and the scheme for unauthorised payments.

In the full knowledge that Stephen Ward was behind Ark and numerous other scams, HMRC ignored evidence of his pension trustee/administrator firm – Dorrixo Alliance. In May 2014, they discussed prosecuting Ward, but did nothing about the London Quantum pension scam, and in August of the same year, a police officer lost his police pension to Ward’s scheme.

Therefore, HMRC takes 1st place, due to its downright lack of motivation to help stop the scams, yet speedy tax demands fly out for the unauthorised payments arising from the so-called “loans” operated from the very schemes that HMRC themselves registers.

Furthermore, HMRC taxes the victims of pension liberation scams – and not the perpetrators.

List of 10 deadliest parasites borrowed from listverse website for comparison.

**********************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

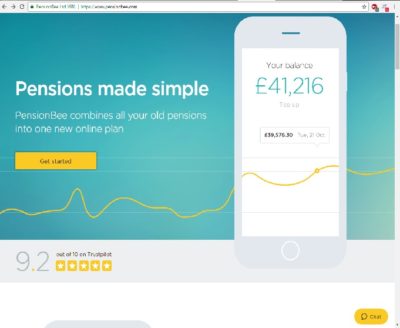

Having focused very much on bad pension investments, pension scams and how to avoid them, I´d like to talk a bit about PensionBee, a relatively new pension provider.

PensionBee offers the service of consolidating all your pension funds into one online fund. You are able to check your balance at any time and have a personal “Bee keeper” assigned to your account. The firm’s annual fees range from only 0.5% – 0.95% – significantly lower than the industry average.

Having explored PensionBee´s website, they are bright, modern and have a 9.2 out of 10 on trust pilot – not bad! You can use the PensionBee pension calculator to set a retirement goal and top up your savings to get on track. In our fast-paced, ever-changing online society, this is ideal for the busy working person.

Sounds great doesn´t it? Unfortunately, other pension providers wouldn´t agree, and it seems Aegon (formerly Scottish Equitable) isn´t impressed by their new competitor. Henry Tapper’s blog, ´PensionBee stands up to the bullies´ address the issue that Aegon are taking 38 days for a pension transfer to PensionBee. (The standard transfer time should be just 12 days). Fortunately, PensionBee is taking none of it, check out their video on “how to transfer your pension away from Aegon”.

In fact, Henry writes, ´Since 8 June 2017, customers wishing to transfer out of Aegon to PensionBee have faced barriers to switching, including multiple discharge forms, telephone calls and repetitive requests for information that has already been provided. There are various other steps that impede the customer’s right to switch pension provider easily (please see here). The average transfer out of Aegon for completed transfers now takes c.54 days – although the true scale of detriment remains unknown, since many people have been unable to overcome the barriers placed in front of them by Aegon in their attempts to switch or have simply given up.´

Upon doing some more digging I found that Professional Adviser, reported that nearly 900 customers were in fact ´stuck´ between Aegon and PensionBee. Going on to say, “So far, the longest transfer that has successfully completed is 176 days, or nearly six months.”

What we at Pension Life are struggling to grasp is, Why now?

Since 2011 big pension companies such as Aegon, Standard Life, Scottish Widows etc, have made transferring out of their pension scheme relatively easy. Even after the Scorpion campaign, which raised awareness about pension scams, these pension providers continued to release funds to bogus schemes. They have enabled the pension scammers to profit whilst the victims ended up being financially ruined.

In the Capita Oak scam – distributed by XXXX XXXX, promoted by Phillip Nunn and administered by Stephen Ward of Premier Pension Solutions – Aegon was one of the leading offending ceding providers. Aegon handed over at least 13 transfers totalling £263,271.71. Then, in the Westminster pension scam, Aegon was still up there with the worst offenders, facilitating a further eight transfers totalling at least £253,305.63.

In neither Capita Oak nor Westminster, did Aegon question why both schemes had the same sponsoring employer: R. P. Medplant (Cyprus). Nor did Aegon establish whether the schemes were genuine occupational schemes. They just handed over the transfers without heed to the Pensions Regulator’s dire Scorpion warning.

But now Aegon appears to be resisting genuine, bona fide transfers. When victims complained to Aegon about the callous and negligent manner in which pensions were handed over to the scammers, Aegon failed to uphold the complaints and refused to pay any compensation. And this despite the fact that many of the transfers were made AFTER the publication of the Scorpion warning.

I wonder – is this change due to a weight on their conscience or do they realise that PensionBee could possibly be the new long-term market competitor? A real threat to their business. PensionBee is modern, clear, fresh and online – appealing to the technology savvy generation. With the introduction of pension freedoms in 2015, savers are looking to find new alternatives with their new choices.

Fortunately, the Pensions Administration Standards Association (PASA) is aware of these issues and has created a work group to enable transferring members a faster outcome. This will hopefully make transferring pensions to legitimate schemes much easier.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

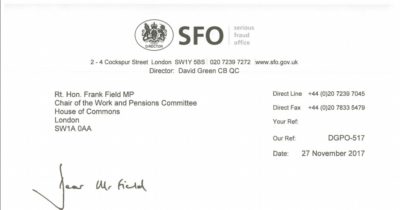

The Serious Fraud Office has written to Frank Field – Chairman of the Pensions Select Committee. The SFO was responding to Frank’s request for details about pension fraud cases prosecuted by the SFO and about the fraudsters’ various scamming techniques.

It is obviously essential to recognise and understand these techniques so that police authorities, regulators, HMRC, the Insolvency Service and the government understand how these crimes work. They need to know how the criminals think, plan, scheme and execute their crimes. It is even more important to publish these details to educate and warn the public as to how to avoid becoming victim to existing and future scams.

The SFO reported two cases and described how they worked:

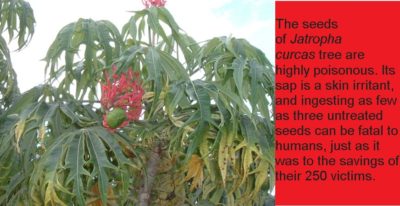

Sustainable Agroenergy (SAE) Plc, investors were told their investments were in biofuel products, that land was owned in Cambodia and planted with Jatropha trees – a tree with highly toxic fruit that could be used to produce biofuel.

Investors were told there was an insurance policy in place to protect the investments if the crops failed. There was already documented research to show that the Jatropha tree, was not as fruitful as originally thought. Gary West, James Whale and Stuart Stone, were convicted of fraud and bribery offences and sentenced to a total of 28 years imprisonment. They were given confiscation orders totaling £1.36m – most of which has now been paid and distributed on a pro-rata basis to investors eligible for compensation. Details of compensation.

In the Arck LLP case (not to be confused with the ARK pension liberation scam) the fraudsters promised investments would be used for a scheme to develop holiday resorts in Cape Verde. With assurances that the funds were in secure bank accounts which would not leave the UK, Arck LLP later forged statements to mislead investors about the losses.

Clay and Clark – the Arck fraudsters – pleaded guilty to charges of fraud and forgery. Clay was sentenced to 10 years and 10 months in prison, while Clark, was sentenced to two years in prison. Confiscation Orders of £344,244.07 and £178,522 were made against Clay and Clark respectively. To date, the SFO has recovered over £500,000 and is currently identifying potential victims for compensation.

The SFO is also conducting investigations into Capita Oak Pension and Henley Retirement Benefit Scheme, various Self-Invested Personal Pensions (SIPPS) as well as other storage pod investment schemes. This investigation also includes the Westminister Pension Scheme and the Trafalgar Multi Asset Fund.

It is thought that over a thousand individual investors have been affected by this alleged fraud.

The amounts invested in these scams totals over £120m.

Around 300 victims of the Capita Oak scheme were given “Thurlstone” loans operated by scammer XXXX XXXX. Now victims face crippling tax bills from HMRC as the loans are deemed to be unauthorised payments.

The Henley Retirement Benefit scheme is the sister scheme to Capita Oak. Both schemes were administered by Stephen Ward of Premier Pension Solutions and Premier Pension transfers.

Trafalgar Multi Asset Fund: hundreds of victims have been affected by this toxic, high risk UCIS fund (Unregulated Collective Investment Scheme) which is illegal to be promoted to UK residents. All these victims were “advised” by unlicensed XXXX XXXX to transfer into an STM Fidecs QROPS and then invest 100% of their funds in Trafalgar – his own fund.

How, you may be asking, are these people getting away with scam after scam? Especially Stephen Ward. His company, Premier Pension Solutions(PPS) has close connections with ARK, Evergreen Retirement Trust Qrops, CWM, Headforte, Southlands, London Quantum to name just a few. Ward is a clever “chameleon”, hiding his past scams and reinventing himself each time with ever changing new skins.

A common feature in a number of these frauds is the offer to investors of an unrealistically higher or secured rate of return. Pension Life has many members who have suffered at the hands of not just the schemes listed above but also the repeat fraudsters operating them.

Some victims are facing more than a 73% LOSS! on their pension investments. Others are facing huge tax bills from HMRC.

The BSPS dilemma for steelworkers is clearly difficult with very little time to consider options and make a wise decision which will affect them for the rest of their lives.

There’s a whole team of willing voluntary professional advisers trying to provide some guidance to help people avoid making the wrong decision. This team includes eminent pensions experts including Henry Tapper (The Pension Ploughman), Al Rush, Darren Cooke and many more.

I’d like to contribute to this excellent initiative to help the scheme members – but I can’t advise how to do things right; I can only advise how not to do things wrong.

Henry Tapper, Al Rush and Darren Cooke – plus other qualified, licensed advisers generously giving their time to help the BSPS members – will give sound guidance as to the right decision to make. The Pensions Advisory Service will also help.

Here are some pointers from me – someone who represents hundreds of victims of pensions scams and has seen all the tricks, lies, false promises and smoke/mirrors in the pension scamming business.

Check that a proper adviser is licensed – in other words: regulated. You can check this out on the FCA register. Here is an example: check out Darren Cooke’s firm, Red Circle. You will see that his firm is regulated (or licensed by the FCA – Financial Conduct Authority) to carry out personal pension and stakeholder pension advice. Remember, unregulated means SNAKE OIL SALESMAN. And beware the “introducer” – which is another word for snake oil salesman. If you find the so-called adviser is not regulated – run like hell!

Beware “free” financial advice. Go to Tesco and ask if they have any free milk. Go to the Post Office and ask if there are any free stamps. Go to an accountant and ask if he will do your accounts for free. Go to your local car dealer and ask if there are any free cars. There ain’t no such thing as free. Everything has to be paid for – but make sure that all the charges, fees, commissions etc., are openly declared. If someone promises you free financial advice – run like hell!

Run a mile from “get rich quick” investment schemes. Your pension has to be invested in boring, safe, traditional assets which will grow steadily and safely. If you are offered something exciting and sexy – like eucalyptus plantations; car parks; football betting; overseas property “opportunities” and truffle trees – run like hell. If you are told that your pension will get “guaranteed returns” of 8%, 10% or 12% – run like hell!

If you are told you can have some cash out of your pension other than your 25% tax free at age 55 – or the rest at the marginal tax rate – run like hell!

If you are cold called – run like hell!

Remember, you are a sitting duck – and it is open season. Also remember, the good guys like Henry Tapper, Darren Cooke and Al Rush – as well as all the other decent, honourable, ethical advisers who are volunteering their time free to help you avoid the scammers – can give you some invaluable, generic guidance. But someone who is offering to transfer your pension into another scheme is giving you advice.

So what is the difference between actual advice and general guidance? Let us take the example of a medical practitioner: you know a doctor – say a GP – at your local tennis club. You are concerned about your health in general and the fact that you are putting on weight and get breathless going upstairs. The doctor might suggest – as in suggest – that you consider going on a diet and taking some exercise, but that you also consult your GP. That is an informal and friendly (as well as well-meaning and common sense) suggestion. But it does not constitute formal advice. A specialist would look for deeper issues such as blood pressure, signs of diabetes and any other underlying conditions to be investigated – and would prescribe specific treatment.

If all else fails, drop me an email and I will try to help: angiebrooks@pension-life.com – but meanwhile, please buy some good running shoes!

Meanwhile, take a look at just a few of the schemes for which Pension Life is representing groups of victims who have lost their life savings to the same – or very similar – scammers who will inevitably be targeting you now:

Pension Scammer Phillip Nunn receiving an award for “Entrepreneur of the Year”

Phillip Nunn has been reported to Action Fraud – which John Ferguson of Square Mile Financial Services describes as being “nobody and with no authority” – on numerous occasions by victims of various scams.

Phillip Nunn, cold caller and “fund manager” of the Blackmore Global investment scam, was given the Entrepreneur of the Year Award by JCI Manchester, but this was reversed shortly afterwards:

“JCI Manchester have today been made aware that an audit may be being carried out in respect of the Blackmore Global Fund. This was not information we were privy to before Phillip Nunn was awarded a ‘Manchester Young Talent Award’ this week.

If such an audit is being carried out, we will await the results of the same and we will consider any other information which comes into the public domain. Pending this, the JCI Manchester board have decided to suspend the award given to Phillip Nunn.”

MYT Phillip Nunn Award Retraction

“An independent panel of judges formed their own view on Phillip Nunn’s submission based solely on the written application received.”

I would love to read Phillip Nunn’s submission. It would certainly make very interesting reading. I doubt it would have included the fact that Nunn and his accomplice Patrick McCreesh were cold callers and lead generators in the Capita Oak/Henley Retirement Benefits/multiple SIPPS/Store First scam – which led to well over 1,000 victims losing over £120 million worth of pensions.

The Insolvency Service produced a witness statement which stated:

“Members of CAPITA OAK indicated they were initially contacted by Craig Mason or Patrick McCreesh of Nunn McCreesh of Its Your Pension Ltd and offered pension review services prior to them being referred to JACKSON FRANCIS or Sycamore for the transfer of their pension to CAPITA OAK.

On 3.3.15 I received an undated letter in which it was stated that Its Your Pension had not traded and was a dormant company and that Nunn McCreesh had traded as an insurance brokerage between 2009 and 2012 when they entered into a verbal arrangement with TRANSEURO where in return for providing pension leads to JACKSON FRANCIS they received a commission from TRANSEURO.

Nunn McCreesh provided JACKSON FRANCIS with 100-200 leads per month which were provided by email and/or telephone for which they received £899,829.86 from TRANSEURO during the period 26.3.12 to 14.5.14.”

Phillip Nunn’s lawyers, Slater and Gordon (funny that, also nominated for an award) tried to claim that Nunn McCreesh’s involvement in the Capita Oak scam was “minimal”. But I wouldn’t describe generating 5,000 leads, cold calling thousands of victims and being paid nearly £900k “minimal”.

On the subject of Slater and Gordon, earlier this year they threatened me with defamation proceedings for exposing Nunn’s scamtivities. It was curious that they couldn’t see any conflict of interest in representing Phillip Nunn when they were also representing the very victims (of Capita Oak) whom he had cold called in the first place.

Slater and Gordon’s Steve Kunziewicz claimed that “Blackmore Global is a prestigious, multi-asset investment house with over £60 million in assets under management, offering institutional and high net-worth clients access to a wide variety of investment products in order to maximise their returns.”

But there is no audit for Blackmore Global and only evidence suggesting the fund is invested in toxic, high-risk, illiquid crap including:

Swan Holding PCC

Kingston Capital Partners (Belize private equity vehicle controlled by Nunn & McCreesh)

GRRE Invest

Spinaris 90 ( UK sports spread betting)

The Blackmore Global audit was promised more than a year ago but never materialised. The audit has now been promised “by the end of the year” – but Grant Thornton won’t specify which year.

However, far from the Blackmore Global fund being aimed at “institutional and high net worth clients”, Phillip Nunn targets low-risk pension savers using a variety of unregulated so-called “advisers” such as David Vilka of Square Mile Financial Services. Many of the Blackmore Global victims were cold-called and/or introduced by Phillip Nunn’s cold-calling outfit, Aspinall Chase. Some were transferred to Maltese QROPS run by Integrated Capabilities and Harbour (now taken over by STM) and to Hong Kong.

Blackmore Global is a UCIS fund – unregulated collective investment scheme. And it is illegal to promote these to UK retail investors as this was banned by the FCA in 2014.

I doubt the other nominees and award recipients will appreciate having been listed alongside Phillip Nunn who has a history of promoting other scammers’ pension scams and is now running one himself. Perhaps JCI Manchester ought to vet candidates for the Manchester Young Talent Awards more carefully in the future.

Pension and investment scams and scandals are a blight on financial services and saving for retirement. The energetic and inspired campaign by Darren Cooke of Red Circle successfully raised awareness of the problems of cold calling. But the snap general election scuppered serious traction on this and the most the government has achieved so far is to make a vague promise to talk about talking about it. But still it is not illegal, and still the scammers are scamming away merrily.

Chair of The Transparency Task Force

The Scams and Scandals team was formed as a result of inspiration by the Transparency Task Force’s Andy Agathangelou. It has attracted a group of like-minded professionals who believe passionately that a concerted effort should go into coordinating a zero-tolerance approach to scams and scandals. All members of the team are committed to producing a White Paper which can focus the minds of government ministers, regulators and law enforcement agencies on the whole problem – not just the cold calling bit.

Irrespective of which version of which political party we are talking about, the ultimate object of a successful and fulfilled life is to be happy, healthy and solvent. And this includes getting a decent education, leading a responsible and law-abiding life, and saving for a comfortable retirement. Millions of British citizens manage to achieve this goal, but sadly many thousands of them lose part of all of their retirement savings to the armies of scammers.

XXXX XXXX, one of the many pension scammers ruining thousands of victims’ lives

All these scams and scammers have caused thousands of victims to lose hundreds of millions of pounds’ worth of retirement savings. And caused untold misery – in many cases exacerbated by HMRC punishing the victims rather than the perpetrators.

The Scams and Scandals Team has a clear five-point goal:

Ban UK cold calling and fraudulent calling

We must not let this disappear off the agenda and must keep up pressure on MPs and Ministers – as well as the regulators. But this must also be extended to overseas as we already know that the UK-based cold calling outfits have made arrangements to move their operations or merely facilitate re-routing of phone numbers. However, the twilight industry of “introducing” must also be examined as this is a serious source of scam facilitation.

Support Lesley Titcomb “Scammers are Criminals”

Ms Titcomb has publicly declared scammers to be criminals

We must work with the regulators, government and law enforcement agencies to enhance existing and introduce new regulation and legislation to prevent new scams, close down known existing scams and bring those involved in conceiving, operating and promoting both to account.

Revitalise Scorpion Campaign

Fundamental to preventing scams is communication to the public of the dangers of cold calls and pension/investment scams which would include the Scorpion Campaign – but so much more as well. A key part of this exercise is the use of social media and the plan to produce a documentary and Youtube channel giving real-life examples of past and current scams. Explaining the mechanics of a scam is one thing – but showing an actual example of a victim and the scammer is bound to have even greater impact.

Write off HMRC debt where scams are proven

HMRC celebrating the tax they collect from victims of pension liberation fraud

We need the help of the government here and could do with an actuary to help us work out what the cost to the State is of taxing victims of scams. If we can demonstrate that by ruining a scam victim (who has already probably lost part or all of his pension) with the tax charge, the long-term cost of supporting the victim and his family will far outstrip the tax collected. This is especially well demonstrated in the Ark case where the victims have got to both repay the “loans” and pay the 55% tax even if the loans are repaid.

Ensure AML regs include pension scamming

TOBY WHITTAKER’S TOXIC EMPIRE WILL FINALLY BE HUFFED AND PUFFED AWAY

I would widen this to include investment scams. This is because at the heart of every pension scam there is a fraudulent investment (and/or loan). The actual pension itself is harmless as it is essentially just a box with a label on it and only becomes toxic and dangerous once you put the scorpions, snakes and cockroaches inside it. You could equally put fluffy kittens in it. It is the mis-use of the pension “box” which is the scam.

Beddoe proceedings: arguably (apparently) Dalriada could have been pursued by Ark victims without MPVAs for not pursuing repayment from those with MPVAs and conversely could have been pursued by Ark victims with MPVAs. So, to be on the safe side, they spent a quarter of a million quid of the victims’ funds on the Beddoe proceedings in the High Court.

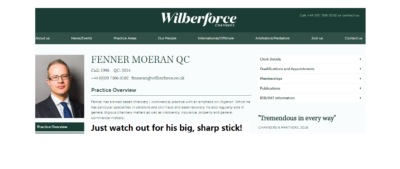

And here we need to look at the meaning of the terms – MPVA and sharp stick:

Sharp Stick: Fenner Moeran’s extremely offensive statement that Ark victims should be beaten with a sharp stick (upon which neither the judge, Sarah Asplin, admonished him nor upon which Keith Bryant, the Ark victims’ QC, challenged him)

MPVA

MPVA is an anacronym for “Maximising Pension Value Arrangements” – a euphemism for pension liberation. The rules are that if a person is under the age of 55, he or she can’t access any part of their pension without incurring an unauthorised payment tax charge of up to 55%. So all pension liberation scammers think up clever ways of fooling potential victims into believing there is a legal “loophole” to circumvent this rule.

The point of a pension liberation scam is not to provide members with a bona fide pension scheme designed to provide an income in retirement, but to make the scammers loads of money. First there is the transfer fee: in the Ark case it was relatively low at 5% – although Stephen Ward was charging an extra fee on top of that of up to £2k per transfer.

And then there are the investment kick-backs. We still don’t know how much the Ark scammers earned out of the speculative, illiquid, high-risk properties they purchased in various dodgy offshore jurisdictions. But it will have been very lucrative. In subsequent scams, the scammers earned huge commissions such as 20% from Dolphin Trust; 30% from Park First; 46% from Store First.

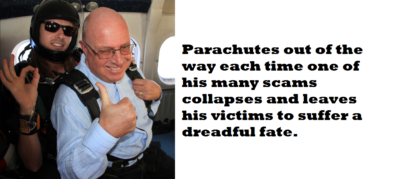

By the time the Ark victims realised they’d been scammed it was too late and there was no parachute

The scammers always promise spectacularly high returns on the investments with assurances such as “guaranteed 8% per annum”. In the case of Ark, the victims were told they would receive up to 9% a year on the growth of the value of “high-end London residential properties” in which the pensions would be invested. This, of course, was a lie. But by the time alarms started to ring and the victims realised there was no way out of this toxic flight with no parachute, it was too late.

But let us revert to the portion of a transfer which is liberated. This can range from 5% to 85% depending on the structure of the scam. And it is given various names or labels such as “cashback”; “thank you”; “refund of fees”; “trousers”; “loan”. The favourite word used is “loan” because the scammers claim that “loans are not taxable”. There is no intention for the money ever to be paid back – that isn’t the point of the exercise. The scammers know the victims would never be able to repay the funds.

The use of the word “loan” in some schemes is merely a marketing term used to fool people into believing they won’t be taxed on the money. And the scammers have no interest in whether the victims ever get taxed or not – because by the time HMRC gets around to sending out tax demands, the scheme will have collapsed and the scammers will be long gone and far ahead on their next scams. They never stick around to help mop up the train wreck left behind.

Often, the victims are surprised when they receive “loan” documentation and alarm bells start ringing. But the scammers assure the victims that this is “just a paper exercise” or “administration to make sure HMRC don’t try to tax the money – because loans aren’t taxable“.

In the Ark scheme, the victims were told the amounts liberated would not be taxable because they didn’t come from the members’ own scheme, but from another scheme. And this is why 14 schemes were set up to work in pairs so that up to 99 people in each pair of schemes could swap cash from their transfers. So this was an artificial mechanism structured purely to operate the liberation – using the label “MPVA” to dress the payments up as something more glamorous and bona fide than just a dollop of unauthorised cash in a person’s trousers.

Very few of the victims were told their cash would ever have to be paid back. The MPVA agreements never once mentioned the word “loan” but did mention the word “discharge” and suggested that the MPVA would be automatically “discharged” after a period of years.

Some victims were told the MPVA would be settled or repaid out of the growth that the Ark pension would enjoy (because of the wonderful investments!). It was explained that the MPVA would grow at 3% a year but the pension fund would grow at 9%. But the member would never have to pay the MPVA off out of their own pocket.

Other victims were told the MPVAs would never have to be paid at all because of the reciprocal nature of the transfer/payment structure. It was explained thus: two “paired” members in different schemes would each have a reciprocal MPVA of – say – £50k. If they both decided they never wanted to pay the MPVAs back, they would just treat them like equal IOUs and agree to simply tear them up.

The Tolleys authoritative manual on pensions taxation by Stephen Ward

Now remember, the victims weren’t told these things by any old spivs – they were told them by Stephen Ward of Premier Pension Solutions and his various accomplices (e.g. Fraser Collins, Terry Tunmore, Paul Clarke etc). Stephen Ward was back then – and still is now – a regulated financial adviser of many years’ experience, as well as the author of the Tolleys Pensions Taxation Manual, (and Level 6 CII qualified).

The same assurances were also given to numerous victims by George Frost, of Frost Financial, a regulated mortgage and insurance broker. And the victims who received the advice on the merits of entering into the Ark scheme believed they had every right to believe and trust professional, qualified and regulated advisers who assured them the MPVAs would never have to be repaid and that their pensions would be safe and secure.

HMRC does not care whether a sum of money accessed from a pension before the age of 55 is called a loan, thank you, cash back, fee refund, MPVA or any other euphemism for “liberation”. They don’t care whether it is repayable or whether it is ever repaid or not. They don’t care whether it comes directly from the member’s pension scheme, or from somebody else’s pension scheme, or via some convoluted arrangement designed to conceal the source of the money – such as Stephen Ward’s Evergreen/Marazion pension/loan scam. If a member makes a pension transfer and receives a sum of money as a result – irrespective of where it comes from – HMRC will issue a tax demand of up to 55%.

To illustrate how pension liberation scams range from the very simple and transparent to the highly complex and opaque, here is an example of one arrangement which Stephen Ward and his merry men, Alan Fowler and Bill Perkins, were involved with in 2013 – after Ark, Evergreen, Capita Oak and Westminster pension scams had all been suspended:

Thanks to you both for your understanding…. Am unused to non delivery! The arrangement I heard about today works like this as an example (ignoring fees) and this is the simplistic version …

Client borrows 16k or thereabouts (this is available in the package)

He gets a non recourse loan (which will not be repaid) of £84k

He buys shares in Xco for £100k. These are listed on the CISX (name is Elysian)

Transfers £100k to James Hay SIPP

SIPP pays member £100k for the shares

Member repays the 16k and trousers £84k

My IFA connection has done 40 of them so far. Advice to transfer to the SIPP is from an FCA regulated IFA. James Hay and Suffolk Life know the full structure and are happy with it.

Regards Stephen

The FCA-regulated IFA to whom he was referring was Angela South of Magna Wealth. She soon made a hasty exit from the collaboration with Stephen Ward when victims realised this was a scam and threatened to report her to the Serious Fraud Office. Victims who participated in this scam have now received tax demands from HMRC and Elysian Fuels is now worthless.

SHARP STICK

Dalriada’s QC, Fenner Moeran, seemed like a very sharp cookie. His skeleton argument (which we never got to see), and his opening speeches, started with the assumption that the MPVAs were definitely loans; that there was no question that they were loans and that the members knew and accepted that they were loans.

The judge, Sarah Asplin, accepted this without question and there was no debate on the subject. Kim Goldsmith’s QC, Keith Bryant, sat as quiet as a corpse and made not one single interjection or objection – even though he was sitting next to Kim who knew perfectly well – and must have told him – that the victims were not aware the MPVAs were loans. Indeed, they were categorically assured that the MPVAs would never have to be repaid.

Even more astonishing was the fact that Dalriada was aware the victims never knew the MPVAs were loans. Dalriada’s Sean Browes and Brian Spence, as well as Pinsent Masons’Ben Fairhead and Ian Hyde, had attended various meetings with the Ark Class Action and gone through this issue numerous times. They were also fully aware that one victim was horrified when she was subsequently told the MPVA was a loan and she immediately called Dalriada and asked to repay it. But Dalriada had refused.

Furthermore, dozens of Ark Class Action members had completed HMRC’s 10-point questionnaire (the Q10) which specifically asked about the arrangements and what they had been told about the need to repay the MPVAs. This is evidenced at HMRC’s question 8:

8: “DETAILS OF WHAT YOU WERE TOLD ABOUT THE NEED TO REPAY THE LOAN”

Here is a typical response to this question by one of the victims:

“I was told that although on paper it would be an official 25 year loan, that because of the nature of the way the loans were set up, i.e. the quid pro quo arrangement, whereby as one person received their monies from the other members scheme and vice versa, if there was a request for any monies to be repaid in the future from each member, each would tear up each other`s IOU and be quits, so to speak, as already stated.”

Stephen Ward – BA (Econ), ACII, APFS, APMI, ex examiner for the pensions management institute and for the CII, confirmed that the Ark scheme was designed by specialist pensions lawyer Alan Fowler – head of pensions at Stevens and Bolton.

Ward went on to explain how the MPVAs worked: “The best way to understand this is in terms of my lending you £100 and you lending me £100. If I do not repay you and you do not repay me then we are both in an equal position. Conversely, if I repay you and you repay me then the position is identical to that which would arise if neither party had repaid the other”.

These statements have been made to HMRC by Ark victims on countless occasions – and Dalriada has always been perfectly well aware of this. And yet Fenner Moeran used his sharp stick to knock these evidenced facts completely off the table – so that the judge was never made aware of them. Mind you, Keith Bryant QC was no better – because he didn’t bring them to the judge’s attention either.

I would go so far as to observe that Fenner Moeran should have used his sharp stick to point the judge to these evidenced facts – and Dalriada should have made sure he did so. By omitting to do so, both Fenner Moeran and Keith Bryant allowed the judge to come to the incorrect conclusion that:

“members who received the MPVA loans agreed to repay them. That’s the point of a loan. It’s not a gift. They cannot now complain about having to repay them. They can complain about having to repay them earlier, but that’s a cashflow issue which is vastly overwritten by the capital harm that is suffered by the non-recipient members”

Fenner Moeran merely leaned on his sharp stick and did nothing to correct the judge. As I was sitting behind him, I couldn’t see whether he was smirking – but I have a feeling he might have been. The judge was wrong on three counts:

The members with MPVAs did not agree to repay them – they were told they would never have to

They can most certainly now complain about being asked to repay them as they were never told they would have to and did not budget to do so

The capital harm suffered by members without MPVAs was mostly caused by Dalriada who did not reject their transfers after 31.5.11 but allowed transfers to continue right up until the end of August 2011

Having glossed over the facts smoothly, and directed the judge to her incorrect conclusion, Fenner Moeran then addressed the issue of ascertaining whether the Ark victims were in a position to be able to afford to repay the MPVAs. And then he produced, with a confident flourish, his pièce de résistance:

“The chances of getting ascertainably or enforceably more accurate information increases when you have the sharp stick of litigation behind it. If we want to see if we’re actually going to get any of this money back, the chances are that we’re going to have to wave a very large stick“

Fenner Moeran ought to be an intelligent person. In the full knowledge that a few feet to his right sat Kim Goldsmith, an Ark victim who had gone through six years of hell courtesy of Stephen Ward and George Frost and all the other scammers, and that a number of other victims were sitting at the back of the courtroom, he still made such an unbelievably stupid and offensive statement. He apologised later “I deeply and sincerely apologise for any misunderstanding or upset caused”.

But the damage had already been done – and you can’t un-say what has been said – especially when every word is recorded and transcribed. On behalf of Dalriada Trustees, he had deliberately misled the judge, and then proceeded to demonstrate clear contempt for the suffering of the Ark victims.

Interestingly, the judge had not remonstrated with Moeran for his crass comments – and Keith Bryant had not objected to the stupid and insensitive words. Throughout the rest of the proceedings, the judge remained – in my view – dominated and steered by Moeran. No attempt was ever made to disclose the truth about what the victims were told about repayment of the MPVAs by Stephen Ward, George Frost, Andrew Isles or Alan Fowler. And no explanation was ever given as to why Dalriada had not pursued these parties for having duped, misled and defrauded the Ark members.

This may seem like a completely off-topic piece of this report, but please stick with it – it will be worth it because it is the whole point of this report. Nearly 18 months before the Ark/Dalriada/Beddoe proceedings in the High Court, another case was heard: Royal London v Hughes. A pension scammer had tried to do exactly what the Ark scammers had done so successfully and profitably for nearly a year: transfer hundreds of secure pensions into a pension scam. But one ceding provider – Royal London – had blocked a transfer request. They strongly suspected the receiving scheme was a liberation scam – unlike the many ceding providers in the Ark case who handed over hundreds of transfers willy-nilly without question or due diligence – the worst of which was Standard Life.

Hughes complained to the Pensions Ombudsman that her transfer request had been blocked by Royal London. The Ombudsman did not uphold her complaint because he agreed with Royal London that the receiving scheme had all the classic hallmarks of being a scam – including the fact that the scheme had been registered as an occupational scheme and Hughes was not genuinely employed by the sponsoring employer. Exactly the same as Ark (and many of the subsequent scams).

Counsel for Royal London argued that “Hughes had to be an “earner” to be able to transfer”. He tried to support the Ombudsman’s view that the legislation required Hughes to be an earner in relation to a scheme employer”. This counsel obviously knew well that victims were made all sorts of promises and assurances and often not told the truth about the arrangements within pension scams.

Royal London’s QC would have been aware of the Ombudsman’s concerns that pension liberation may well have been behind Hughes’ enthusiasm to transfer her pension. And he will have known only too well that potential victims were systematically lied to and probably told that their “loans” (or whatever euphemism was used) were not repayable. And he would have known that the intended liberation “loans” were never intended to be repaid and that the victims would be told that the loans never needed to be repaid.

This QC will have been thoroughly briefed by his clients, Royal London, and may even have consulted with the Pensions Regulator who would have given him thorough details on how pension liberation scams worked.

So this particular QC had intimate, first-hand knowledge of how pension liberation schemes worked in general and represented Royal London in their quest to defend their right to prevent further victims of pension liberation scams. He also knew intimately how Ark worked in particular.

Fenner Moeran of Wilberforce Chambers

He knew perfectly well that the victims were told they never had to repay their loans (or MPVAs/cash backs/thank you’s/trousers). And he knew that the Ark MPVAs were supposed to be “discharged” from growth in the schemes and NOT from the victims’ own pockets – as reported by Justice Bean. But he failed to bring this to the judge’s attention.

Who was this QC? I will give you a clue – he had a big, sharp stick. Perhaps he should have gone to Specsavers and read the MPVA agreement where this was clearly stated.

Blackmore Global is a UCIS (unregulated collective investment scheme) which is illegal to be promoted to retail, UK investors. The fund is run by Philip Nunn and Patrick McCreesh (formerly of Nunn McCreesh – the lead generation and cold calling firm which introduced around 8,000 victims to the scammers who were running the Capita Oak and Henley pension scams in 2012/13).

It is perhaps more than a little ironic that a pair of cold-callers who were facilitating hundreds of victims being transferred into schemes 100% invested in Store First store pods are now running their own investment fund – Blackmore Global.

Slater and Gordon is a very large firm of no-win-no-fee solicitors with an office in Manchester. I met their National Practice Group Leader and specialist in financial litigation and pension mis-selling in April 2015. His name is Craig McAdam. After going through the various scams I was handling at the time, and the appalling damage done by the scammers to thousands of victims, Craig was thoroughly up to speed on how the scams worked. He was also deeply committed to helping the Ark Class Action and other group actions.

Nunn McCreesh was the introducer of contacts for the pension scammers

Craig McAdam confirmed by email on 16.4.15 that he was looking forward to working with me. A week later he sent a draft engagement letter and confirmed that Slater & Gordon’s success fee would be 15% – although he did revise this up to 18% a couple of days later.

The following month Craig McAdam confirmed he would be attending a meeting with Dalriada Trustees and Pinsent Masons with members of the Ark Class Action. He also confirmed he would be talking to one of Stephen Ward’s many victims: a member of the London Quantum scheme whose trustee was Ward’s firm Dorrixo Alliance.

A month later, Craig McAdam was examining the Capita Oak pension scam run by XXXX XXXX and administered by Stephen Ward, and asked me to put forward one of the victims as a creditor. The Insolvency Service had wound up the trustee of Capita Oak: Imperial Trustees Ltd. Craig then asked me if I was happy for Grant Thornton to be appointed as the insolvency practitioner and I confirmed that indeed I was. I felt that Grant Thornton was a competent and ethical firm and could finally unscramble the mess created by the scammers behind Capita Oak and bring some form of resolution to the victims who were all introduced and/or cold called by Nunn McCreesh.

I was delighted that the same day, one of the Capita Oak victims put herself forward willingly and eagerly as a creditor and Craig McAdam confirmed this to Grant Thornton the following day. At the same time, Craig confirmed that one of the London Quantum victims was a client of Slater and Gordon and made a complaint to FCA-regulated Gerard Associates who had acted as the adviser in that case.

Later in June 2015, Craig McAdam confirmed that Slater and Gordon was instructed by the Capita Oak victim who had volunteered to be the creditor in the liquidation of the trustee of the Capita Oak scam. Craig also sent out letters of engagement to other victims.

In July 2015 I sent a copy of the Insolvency Service’s Capita Oak/Imperial Trustee Services witness statement to Craig McAdam. This statement confirmed that Philip Nunn and Patrick McCreesh’s firm Nunn McCreesh had supplied up to 300 leads a month (for 28 months) to the scammers who promoted and operated the Capita Oak scam: Jackson Francis, Sycamore Crown, Sanderson Clarke, Barncroft Associates, Nationwide Benefits Consultants, Speke Admin, Timoran Capital.

The Insolvency Service witness statement mentioned Nunn McCreesh several times:

“Members of Capita Oak indicated they were initially contacted by Patrick McCreesh of Nunn McCreesh and referred to Jackson Francis or Sycamore for the transfer of their pension to Capita Oak. I wrote to Mr. McCreesh to request a copy of any sales and marketing agreement with Jackson Francis or Sycamore and details of commission received.” Nunn McCreesh and their solicitors admitted they had been involved with the scammers and also Transeuro Worldwide Holdings – one of the main operators of the Capita Oak and Henley scams.

However, Nunn McCreesh was unable to produce copies of invoices or sales ledgers for the money received for their part in these scams. Their solicitors also confirmed that Nunn McCreesh received a commission of 8% of sales and the Insolvency Service stated that there was a “lack of transparency” by Nunn McCreesh.

The Insolvency Service also confirmed that some of the victims had been cold called directly by Nunn McCreesh.

Being in possession of the Insolvency Service’s witness statement clearly galvanised Craig McAdam into an enthusiastic confidence to take on the Capita Oak case and asked me to send him through contact details of all the members. He obviously realised that now the scam was clearly documented and the promoters – including Nunn McCreesh – were now identified without any question of doubt. It was also documented in the witness statement that Nunn McCreesh had earned £900k out of providing at least 8,000 leads for the scam – 300+ of which ended up in Capita Oak and 200+ of which ended up in Henley. It is not clear whether the 8% sales commission was on top of this. 8% of £10.8 million would have been a handsome sum indeed.

I provided Craig McAdam with contact details for the Capita Oak Class Action members and on 21.7.15 he confirmed that cases were “being opened up smoothly”. At the end of 2015, Craig attended a meeting of Class Action members and got to meet a group of victims in person. There can be no doubt that Craig, by now, thoroughly understood the wickedness of the scammers and the profound distress and impending financial ruin of the victims.

So for most of 2015, it looked like Slater and Gordon was going to represent the Capita Oak members – all of whom were initially introduced by Nunn McCreesh. And it looked like Grant Thornton was going to be appointed as insolvency practitioner to Capita Oak’s trustee – Imperial Trustee Services Ltd.

In the event, neither happened. But Capita Oak is now in the hands of Dalriada Trustees – appointed by the Pensions Regulator. And the organisers, promoters and administrators of Capita Oak are all under investigation by the Serious Fraud Office.

Slater and Gordon now represents Nunn McCreesh

In a very curious twist, Philip Nunn and Patrick McCreesh are now running the Blackmore Global UCIS. They are doing the cold calling and the pension administration, as well as running the fund. And you will never guess who their solicitor is: Steve Kunziewicz of Slater and Gordon (Manchester office). And you will never guess who their auditor is: Grant Thornton. You really couldn’t make it up.

Victims of Blackmore Global are indeed extremely distressed. They have either managed to redeem out of the fund at a loss after a protracted struggle, or they are stuck in the fund with no prospect of getting out of it any time soon (if ever).

A year ago, the underlying assets of the fund were confirmed to one victim by Optimus Fiduciaries Ltd, an IoM domiciled company managing the Optimus Retirement Benefits #1 QROPS. Further research discovered these underlying assets were a load of toxic, illiquid, high-risk crap.

Neither Slater and Gordon nor Grant Thornton will confirm what the assets are or how much they are worth – despite Nunn and McCreesh claiming the fund has “£17m under management”. However, £17m is nothing more than a meaningless figure on a piece of paper until such time as the assets are independently verified and audited. Nunn & McCreesh have promised to publish audited accounts for over 12 months now, but failed to do so. One can only assume that to do so would instantly crystallise a true value far below the imaginary £17m and result in a sudden collapse of the fund.

Nunn and McCreesh claim Meriden Capital Partners are the investment manager to the fund

I have asked Steve Kunziewicz of Slater and Gordon on numerous occasions this past couple of months to tell me what the assets are, but presumably Nunn and McCreesh won’t tell their own solicitor – any more than they will tell their own auditors. Perhaps they told the Blackmore Global investment manager, Meriden Capital Partners in Barcelona? The trouble is that Meriden Capital Partners deny that they were ever investment manager to the fund and that Nunn and McCreesh are lying.

I hope the irony of this situation is not lost on the gentle reader: Slater and Gordon solicitors and Grant Thornton being “gamekeepers turned poachers”. My suggestion to both firms is that they should choose their clients carefully and protect their public image diligently. Both firms should decide whether they want to be like Bark and Co who openly represent fraudsters, murderers, insider dealers, hackers, race fixers and other criminals. Or whether they want to be on the side of justice for victims of pension and investment scammers. Because they can’t do both.

SAIL FINANCIAL AND TRAFALGAR MULTI ASSET FUND: What is the connection?

Who is behind Sail Financial? And what is the connection to Trafalgar Multi Asset Fund? We know Trafalgar Multi Asset Fund was originally run by XXXX XXXX as “Victory Asset Management” and that XXXX had also been behind the Capita Oak, Henley Retirement Benefits Scheme and Westminster pension scams: wound up by the Insolvency Service; now in the hands of Dalriada Trustees and under investigation by the Serious Fraud Office.

We also know that the £120 million of store pods purchased for Capita Oak, Henley RBS and hundreds of SIPPS are now probably worthless and Store First is subject to a winding up petition due to be heard on 1st August in Manchester.

In addition to being the Investment Manager of the Trafalgar Multi Asset Fund, XXXX was also the “financial adviser” in the form of his firms Global Partners Limited and The Pension Reporter – a “trading style” of XXXX’s Nationwide Benefit Consultants. But none of these firms were licensed for pension or investment advice.

However, Joseph Oliver’s Marcus Groombridge has stated:

“I can confirm that XXXX XXXX and Nationwide Benefit Consultants Ltd were appointed on the 29th of May 2014 and terminated on the 8th of April 2016. The permission for insurance mediation covers pension advice.”

Phew! What a relief. I am now looking forward to Mr Groombridge’s full cooperation with putting XXXX XXXX’s victims back into the position they should have been in had they not been scammed into investing their pensions in the Trafalgar Multi Asset Fund in the first place. I will also probably remind Mr Groombridge that the Trafalgar matter is under investigation by the Serious Fraud Office – along with other pension scams “distributed” by XXXX XXXX in 2012/13.

If there hadn’t already been enough misery for the hundreds of victims of the Capita Oak and Henley Retirement Benefit schemes run back in 2012/13 – XXXX had also been operating pension liberation in the form of “loans” from his company Thurlstone, based in the Seychelles. The victims have now been sent tax demands. But XXXX and his solicitor, Mark Manley of Manleys Law, have ignored pleas to indemnify the victims from these crippling tax liabilities.

I have often wondered what people like XXXX do after their latest scheme collapses or implodes. History tells us that they simply get straight on with their next one – and in fact had probably started it already. XXXX has been a director of seven companies (according to Companies House):

Nationwide Benefit Consultants (active)

Nationwide Corporate Benefits (active)

Proactive Administration Solutions (active)

Nationwide Trustee Services (dissolved)

Ashton Abbott (dissolved)

Nationwide Tax Administration (dissolved)

Admin Protection (dissolved)

XXXX has resigned from Nationwide Benefit Consultants and Nationwide Corporate Benefits – and appointed someone called Raymond Hampton as a director. But XXXX remains a director of Proactive Administration Solutions. So perhaps that is one to watch.

XXXX’s background is in the “distribution of pension schemes” (his words). He has worked closely with the cold-calling and lead generation firms (such as Jackson Francis, Sanderson Clarke and Barncroft Associates run by XXXX´s mates Ben Fox and Stuart Chapman-Clarke) who were involved in the Capita Oak and Henley scams.

So what is XXXX doing now? Perhaps whatever project he is working on involves trying to make enough money to compensate the victims of Capita Oak, Henley, Westminster and the Trafalgar Multi Asset Fund – all of the schemes are now under investigation by the Serious Fraud Office. It is also probable that Gibraltar Trustees STM Fidecs no longer want terms of business with XXXX XXXX now that so many of his schemes are subject to criminal investigations. STM Fidecs also probably now realises it was a serious conflict of interest taking business from an adviser who was also the Investment Manager to the Trafalgar Multi Asset Fund – which is now in the process of being wound up.

While I was idly puzzling over what XXXX´s next scheme might be, I started hearing reports about a firm called Sail Financial doing the rounds of firms in Europe – touting offering to do “introducing” and cold calling. Looking at the Sail Financial website, it is impossible to see who is involved in the business – no names, no address, no regulation. According to the Companies House register, Sail Financial – incorporated on 8.5.2015 – has two directors: Robert Hathaway and Brian Westhead. Neither of those names rang any bells with me.

Hathaway has no other directorships listed. However, Westhead does: he is listed as a director of a dissolved company called BIGB22 (08559856). This company’s previous names were Portia Financial and The Pension Reporter: XXXX XXXX’s firms. These firms have a history of being involved in pension and investment scams, cold calling and unregulated financial advice. The victims of the Trafalgar Multi Asset/STM Fidecs pension and investment scam were introduced and “advised” by Portia Financial, GPL (Global Partners Ltd) and The Pension Reporter, with advice letters signed by XXXX XXXX and Tom Biggar.

So clearly there is a connection between Sail Financial and various firms and schemes run by XXXX XXXX – including Trafalgar Multi Asset Fund. Perhaps XXXX XXXX is sailing round the Mediterranean now? I just hope he doesn’t have one glass of champagne too many and fall overboard.

A fund like Blackmore Global really ought to be audited as soon as possible – to make sure it isn’t simply a “black hole” into which victims’ hard-earned pensions have sunk. Numerous worried pension savers are stuck in the Blackmore Global Fund and finding it difficult – if not impossible – to get out. They are seemingly “locked in” for ten years.

I WOULD LIKE TO EXPRESS MY SINCERE THANKS TO THOSE – INCLUDING IFAs, PENSION TRUSTEE FIRMS AND BLACKMORE GLOBAL VICTIMS – WHO HAVE CONTACTED ME AND SUGGESTED IMPROVEMENTS, CORRECTIONS AND ADDITIONS.

Allegedly, Grant Thornton is working on an audit – and has been doing so since September 2016. They could probably have audited Microsoft in that time – and squeezed in Amazon on the side during the lunch breaks. Just how difficult can it be to audit a fund which only has a handful of assets in it?

Originally, the directors of Blackmore Global were Brian Weal, Patrick McCreesh, and Phillip Nunn.

Brian Weal – sanctioned by the FSC in 2014 – was also a director of Swan Holdings – the only investment that the Advalorem Value Asset Fund made. Brian Weal was also a director of Advalorem. Advalorem lost most of its money because the investments in Swan Holdings were overvalued. The valuations were supplied by Stuart Black who also provided valuations for a Hedge Fund called Heather Capital which lost $300 million because of overvaluations. Swan Holdings had invested a chunk of cash in Etaireia Investments. Stuart Black was a director of Etaireia Investments. Brian Weal owns a controlling number of shares in Etaireia Investments. So, make up your own mind as to whether having Weal as a director of Blackmore Global is a good thing or a bad thing – or a “black hole” thing.

As for Nunn and McCreesh, I will let Leonard Fenton of the Insolvency Service do the talking:

Documents and information received from members of CAPITA OAK indicated they were initially contacted by Craig Mason or Patrick McCreesh of Nunn McCreesh of Its Your Pension Ltd and offered pension review services prior to them being referred to JACKSON FRANCIS or Sycamore for the transfer of their pension to CAPITA OAK.

On 3.3.15 I received an undated letter in which it was stated that Its Your Pension had not traded and was a dormant company and that Nunn McCreesh had traded as an insurance brokerage between 2009 and 2012 when they entered into a verbal arrangement with TRANSEURO where in return for providing pension leads to JACKSON FRANCIS they received a commission from TRANSEURO.

Nunn McCreesh provided JACKSON FRANCIS with 100-200 leads per month which were provided by email and/or telephone for which they received £899,829.86 from TRANSEURO during the period 26.3.12 to 14.5.14.

So, again, draw your own conclusions about those connected with Blackmore Global. Nunn and McCreesh generated up to 200 leads a month to pension scammers in relation to a series of pension/investment scams which are now under investigation by the Serious Fraud Office. This entailed £120 million worth of pensions being invested in Store First store pods which are now the subject of a winding up petition – and arguably worthless.

When I first started investigating the Blackmore Global fund in 2016, I started with the brochure which makes all sorts of grand claims: “medium to long-term investment vehicle with a diversified investment portfolio under one structure. The Company allocates investment between four distinct protected cells, giving a true diversification of assets between property, sustainable, private equity and lifestyle”. Yeah, right. But what are the underlying assets? Where is the audit?

The Fact Sheet goes on to claim the fund’s NAV is £17.65 million and was launched on 1st May 2014. So why no audit? It also claims that the Investment Manager is a firm in Barcelona called Meriden Capital Partners. I thought it a bit strange that a fund based in the Isle of Man would appoint an investment manager in Spain – especially one without a website. So I called Meriden Capital Partners and asked them to confirm that they were the investment manager. They claimed they had never heard of Blackmore Global. Then one of the partners called me back and told me that some man who didn’t give his name had come to their office and asked them whether they would be interested in being the investment manager for Blackmore Global.

The partner at Meriden Capital explained that they had declined because they were not licensed to provide investment management advice to a fund – only to private individuals.

But then I discovered that that hadn’t been entirely true either. Meriden Capital had actually completed an application form to apply to become the investment manager to the fund on 4th April 2014. So either Meriden Capital was lying or Blackmore Global was lying – or both.

The Blackmore Global NAV Factsheet also states that there is a ten-year lock-in to the fund. So why would anyone invest a pension in such a fund? A pension saver has a statutory right to a transfer and might want to take his PCLS – 25% tax free withdrawal at age 55 – or retire, or even die. What on earth is the point in using Blackmore Global for a pension at all? Ever.

As Grant Thorton is clearly having a little trouble with the audit of a five-cell investment fund, I will lay a wee trail of bread crumbs for them to look at. Clearly they can’t even find the underlying assets – let alone value them:

Spinaris 90 – UK sports spread betting (invisible – and what happened to Aria Invest?)

Most of the victims of the Blackmore Global fund were initially cold-called by a firm called Aspinal Chase. And all the victims were advised by unregulated investment advisers Square Mile Financial Services (an insurance license does not cover regulated investment advice). But more worryingly, all of them were put into a QROPS in Malta or the Isle of Man. So why were UK residents transferred to an offshore pension at all, and why were most or all of their pension funds invested in a UCIS which is illegal to be promoted to UK residents?

The list of questions goes on and on. And here, we get back to whether the unscrambling of these pension and investment scams is more about who you know rather than what you know. One victim had his pension invested 75% in Blackmore Global and 25% in Symphony. Symphony was a fund invested in derivatives and highly leveraged. It was also a sub fund of the Nascent Fund run by Richard Reinert. Under the Nascent “umbrella” (a structure for wannabe fund managers) was also the Trafalgar Multi Asset fund which was run by XXXX XXXX who was one of the main distributors behind Capita Oak, Henley and Westminster – all of which are being investigated by the Serious Fraud Office.

Now we have gone round in a complete circle. A catalogue of lies, deception, fraud, mis-selling, negligence and incompetence.

I don’t envy Grant Thornton (if indeed they are the auditors) because they have got to unscramble this unholy mess. And I strongly suspect that, behind the scenes, there are certain parties who are busting a gut to ensure the audit is never published. Two of these may well be John Ferguson and David Vilka of Square Mile in the Czech Republic who seem to have a strong vested interest in promoting this black hole of a fund.

Meanwhile, the longer the victims are held back from transferring out of this toxic swamp of a fund, the more serious the complaints against the various parties involved will be. These will include the cold-calling scammers; introducers; advisers; pension trustees and insurance companies such as Investors Trust who allowed this investment and the pensions transfers from unlicensed advisers.

Finally, on the subject of Investors Trust, they showed not a shred of interest in the fact that they had facilitated financial crime in allowing UK residents to have their pensions invested in this UCIS, but when I published a photo of John Ferguson and David Vilka posing as a couple of gaudily-dressed spivs in Las Vegas, Investors Trust objected on the grounds the photograph was their property.

This story was first published by International Investment journalist Helen Burgraff on 22.5.17 and heralds a welcome start to the much-needed initiative to bring pension scammers to justice.

Unfortunately, the pension landscape – both in the UK and offshore – is no better now than in the days of the Wild West. Back then, first the Sheriff’s Fraud Officer had to catch his horse; check the horse wasn’t lame; saddle up; then whistle for his tame injun to help him track the thief. Finally, once his water bottle was filled, the brave sheriff set off with his companion, Raging Bull, by around lunch time. Usually, they had tracked the thief down drinking whisky in a saloon by tea time, and after a dusty skirmish, he was thrown in jail by supper time.

Almost exactly two years ago, on 27.5.2015, the Insolvency Service published a witness statement on the £120 million Store First fraud which saw more than 1,000 victims lose their pensions and gain tax liabilities. The statement clearly named 18 scammers involved in these cases – many of whom had been visited at their offices. And yet, not a single one of these criminals was prosecuted or jailed.

Of course the blooming obvious happened – all the scammers went on to operate further scams and ruin thousands more victims’ lives. The cold calling firm, Nunn McCreesh, went on to operate the toxic UCIS fund, Blackmore Global; many of the cold callers upgraded their operations to “introducers” and the Ginger Scammer promoted himself to fund investment manager in the Trafalgar Multi Asset Fund (£21 million now suspended).

Whatever all the rest of the scammers are doing, it won’t be making good the damage they caused back in 2012/13. And Group First is now launching a new Park First car park at Luton Airport. Doubtless there will be healthy investment introduction commissions for the scammers to con hundreds of investors and pension savers into losing their life savings. Perhaps Toby will name this new venture “Lootin’ Airport”.

Meanwhile, I have discovered one of the advantages of having police officers among the members of the Pension Life Groups. You get the benefit of a wee bit of inside information and I hear that a bunch of the scammers have been arrested. About time!

Meanwhile, the Ginger Scammer’s lawyer is complaining about an image on the Pension Life website. Trouble is, I can’t work out which one it is – I’ve searched and searched and I can’t find a single offensive photo. But then what is offensive to one person is inoffensive to another. I called the Ginger Scammer’s lawyer a “dick” once – maybe it should have been “tick”.

In the wake of hundreds of victims fearing heavy pension losses in the Blackmore Global fund, we now have another disaster waiting to happen: Blackmore Bond.

In the wake of hundreds of victims fearing heavy pension losses in the Blackmore Global fund, we now have another disaster waiting to happen: Blackmore Bond. But here’s another puzzle: a geezer called Kenneth “Buzz” West also appears at first glance to be relatively harmless. He is a director of numerous companies – including European Wealth. The only stain on his reputation that I can find is that his former company, Ashcourt Rowan, was fined £412k by the FSA in 2012 for dodgy investments in his other company: Savoy Group. But Ashcourt Rowan held its hands up and paid the fine.