Pension scammers are hidden all around us, often dressed in smart clothes, driving smart cars and carrying impressive leather folders. They offer what seems like smart investments, push through your pension fund transfer swiftly and seamlessly. However what you don´t see on the surface is their hidden parasitic ways. These scammers will drain the funds from your pension, investing in high-risk, toxic investments, that only they will profit from.

Here´s Pension Life´s, “Top 10 Pension Scammers”. (Please note: this information is correct as of the today´s date only, as pension scammers are evolving daily and as one falls another will rise!)

John (Gus) Ferguson’s firm Square Mile International promote unregulated toxic crap to pension savers and employs unqualified David Vilka. The so-called “advisers” promoted the Blackmore Global Fund.

It is still unclear what has actually happened to the money invested into the Blackmore Global Fund.

James Lau was a financial adviser with Wightman, Fletcher McCabe (FSA regulated) – part of the Clarkson Hill Group. Along with directors Peter Bradley and Andrew Meeson, of Tudor Capital Management (subsequently jailed for eight years for money laundering and tax fraud), James Lau conned 116 victims into transferring their pensions, investing in forex trading companies, and liberating up to 85% of their pensions. Lau is now rumoured to be in hiding in Hong Kong. The victims are now facing 55% tax charges by HMRC.

8 – Friendly Pensions

David Austen of Friendly Pensions, used cold-calling and high-pressure sales tactics to strong-arm 245 victims into investing in 11 fake schemes, including a truffle farm.

Dalton, Barratt and Hanson all served as trustees on the fake schemes set up by Austin – who is described as the mastermind – and were paid more than £550,000 between them. The four scammers who conned pension savers out of £13.7 million have now been banned from the industry but not imprisoned. The victims, however, lost everything.

One thousand people were relieved of up to £100 million worth of pension funds. Conned by a motley assortment of snake oil salesmen, the victims were promised high returns, but all they got was high losses. Old Mutual International (OMI) were the provider for the bulk of the insurance bonds in this scam. Funds were invested in risky, toxic structured notes which were clearly labelled as “for professional investors only”. Clients were lied to, as when they saw the value of their funds plunging dramatically, the Continental Wealth Management scammers assured the victims that the reported losses were “only paper losses”. Continental Wealth Management collapsed in September 2017.

6 -XXXX XXXX

XXXX XXXX was the “distributor” of the Capita Oak, Henley, Westminster and various SIPPS scams in 2012/13. He was also operating pension liberation fraud with his “loan” company: Thurlstone. When these schemes collapsed in 2013, he went on to launch an investment scam called Trafalgar Multi Asset Fund. Capita Oak, Henley, Westminster and Trafalgar Multi Asset Fund are now all under investigation by the Serious Fraud Office. XXXX XXXX has been arrested and his offices searched.

Phillip Nunn – along with his sidekick and partner in crime Patrick McCreesh – provided “lead generation” services to the Capita Oak and Henley scams. At up to 200 leads a month for more than two years, he was responsible for the destruction of £ millions of pension funds – and got paid nearly £1 million in fees for doing so. He then went on to set up an investment scam called Blackmore Global – a UCIS which is illegal to be promoted to retail pension savers. It is not known whether the investors have lost some, most or all of the funds in Blackmore Global as Phillip Nunn refuses to have an independent audit carried out on the fund.

Steve Pimlott has been running Windsor Pensions for at least seven years. He claims to have done around 5,000 pension liberations and assures victims that HMRC will be “unlikely” to catch up with them. Pimlott uses QROPS schemes such as Danica in Sweden and then sets up a fraudulent bank account in the Isle of Man. The transfer never goes anywhere near Danica, of course. But the transfer is sent to the IoM bank account – 85% is paid out to the victim and Pimlott trousers the other 15%. HMRC is now taxing the victims at 55% – although they have never taken action against Pimlott who is still operating happily in Florida (not far from where Stephen Ward has his six luxury villas).

Peter Moat and his wife Sara Moat were chums of Stephen Ward of Premier Pension Solutions. They ran a loan company called Blu Debt Management and also had several other businesses involving estate agency and pension administration. Hundreds of victims were transferred into the Moats’ Fast Pension schemes, and now the victims cannot access their pensions or transfer out. Peter and Sara Moat live in the Javea area of the Spanish Costa Blanca and have had 18 Pensions Ombudsman’s determinations against them for mal-administration of the pension schemes they are running. It is thought that around 400 victims are affected, although it is not known how much they have lost between them. It is known that several years ago, a substantial amount of the funds were loaned to Bridgebank Capital and then used as bridging loans for property developers. But the money has since been repaid and goodness only knows where it is now. Certainly not accessible to the members.

Capita Oak: 300 victims; £10 million at risk; tax penalties on XXXX XXXX’s Thurlstone “loans”

Westminster: 200 victims; £7 million at risk; tax penalties on “loans”

Southlands, Headforte, Feldspar, Hammerley, Maribel, Dorrixo Alliance, Halkin, Bollington Wood, Randwick Estates, Elysian Fuels, London Quantum – and many more. Stephen Ward remains active with DB transfers.

and in first position we have …..

1 – HMRC

Yes, you read correctly, HMRC is our number-one culprit in the Top 10 pension scammers list. And here’s why:

Since at least 2010, pension scams have been on the rise. That’s 8 years, yet regulations have not been changed, HMRC has not become vigilant or conscientious about registering pension scams, and new laws have not been put in place to stop scammers.

In fact, the scams are registered in the first place by HMRC, and in the case of occupational schemes also by tPR.

No notice is taken of whether the schemes are registered by known scammers and no questions are asked as to the purpose of the schemes.

In the case of James Lau’s Salmon Enterprises, the trustees – Meeson and Bradley – had been investigated by HMRC and arrested in March 2010 on suspicion of money laundering and tax fraud. However, HMRC did nothing to warn ceding providers or the public and Salmon Enterprises was left as an HMRC-registered, fully-operational occupational scheme.

Later that year, one ceding provider queried the legitimacy of the Salmon Enterprises scheme, but HMRC refused to elaborate on why the trustees had been arrested. A transfer went ahead – along with 115 others – while HMRC sat back in the full knowledge that all these victims would be bound to face unauthorised payment tax charges.

In the Ark case, HMRC spoke to the organisers and promoters (including Stephen Ward) of the six Ark schemes on several occasions. They then had a meeting with Craig Tweedley and Ward in February 2011 to discuss their concerns that the 50% “loans” paid out to scheme members constituted unauthorised payments. At this point there was a “mere” £7 million worth of transfers. Nothing was done to suspend the Ark schemes for another three months – during which time a further £20 million was transferred in. HMRC is now trying to tax both the members and the scheme for unauthorised payments.

In the full knowledge that Stephen Ward was behind Ark and numerous other scams, HMRC ignored evidence of his pension trustee/administrator firm – Dorrixo Alliance. In May 2014, they discussed prosecuting Ward, but did nothing about the London Quantum pension scam, and in August of the same year, a police officer lost his police pension to Ward’s scheme.

Therefore, HMRC takes 1st place, due to its downright lack of motivation to help stop the scams, yet speedy tax demands fly out for the unauthorised payments arising from the so-called “loans” operated from the very schemes that HMRC themselves registers.

Furthermore, HMRC taxes the victims of pension liberation scams – and not the perpetrators.

List of 10 deadliest parasites borrowed from listverse website for comparison.

**********************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

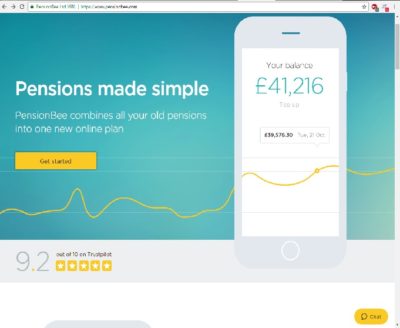

Having focused very much on bad pension investments, pension scams and how to avoid them, I´d like to talk a bit about PensionBee, a relatively new pension provider.

PensionBee offers the service of consolidating all your pension funds into one online fund. You are able to check your balance at any time and have a personal “Bee keeper” assigned to your account. The firm’s annual fees range from only 0.5% – 0.95% – significantly lower than the industry average.

Having explored PensionBee´s website, they are bright, modern and have a 9.2 out of 10 on trust pilot – not bad! You can use the PensionBee pension calculator to set a retirement goal and top up your savings to get on track. In our fast-paced, ever-changing online society, this is ideal for the busy working person.

Sounds great doesn´t it? Unfortunately, other pension providers wouldn´t agree, and it seems Aegon (formerly Scottish Equitable) isn´t impressed by their new competitor. Henry Tapper’s blog, ´PensionBee stands up to the bullies´ address the issue that Aegon are taking 38 days for a pension transfer to PensionBee. (The standard transfer time should be just 12 days). Fortunately, PensionBee is taking none of it, check out their video on “how to transfer your pension away from Aegon”.

In fact, Henry writes, ´Since 8 June 2017, customers wishing to transfer out of Aegon to PensionBee have faced barriers to switching, including multiple discharge forms, telephone calls and repetitive requests for information that has already been provided. There are various other steps that impede the customer’s right to switch pension provider easily (please see here). The average transfer out of Aegon for completed transfers now takes c.54 days – although the true scale of detriment remains unknown, since many people have been unable to overcome the barriers placed in front of them by Aegon in their attempts to switch or have simply given up.´

Upon doing some more digging I found that Professional Adviser, reported that nearly 900 customers were in fact ´stuck´ between Aegon and PensionBee. Going on to say, “So far, the longest transfer that has successfully completed is 176 days, or nearly six months.”

What we at Pension Life are struggling to grasp is, Why now?

Since 2011 big pension companies such as Aegon, Standard Life, Scottish Widows etc, have made transferring out of their pension scheme relatively easy. Even after the Scorpion campaign, which raised awareness about pension scams, these pension providers continued to release funds to bogus schemes. They have enabled the pension scammers to profit whilst the victims ended up being financially ruined.

In the Capita Oak scam – distributed by XXXX XXXX, promoted by Phillip Nunn and administered by Stephen Ward of Premier Pension Solutions – Aegon was one of the leading offending ceding providers. Aegon handed over at least 13 transfers totalling £263,271.71. Then, in the Westminster pension scam, Aegon was still up there with the worst offenders, facilitating a further eight transfers totalling at least £253,305.63.

In neither Capita Oak nor Westminster, did Aegon question why both schemes had the same sponsoring employer: R. P. Medplant (Cyprus). Nor did Aegon establish whether the schemes were genuine occupational schemes. They just handed over the transfers without heed to the Pensions Regulator’s dire Scorpion warning.

But now Aegon appears to be resisting genuine, bona fide transfers. When victims complained to Aegon about the callous and negligent manner in which pensions were handed over to the scammers, Aegon failed to uphold the complaints and refused to pay any compensation. And this despite the fact that many of the transfers were made AFTER the publication of the Scorpion warning.

I wonder – is this change due to a weight on their conscience or do they realise that PensionBee could possibly be the new long-term market competitor? A real threat to their business. PensionBee is modern, clear, fresh and online – appealing to the technology savvy generation. With the introduction of pension freedoms in 2015, savers are looking to find new alternatives with their new choices.

Fortunately, the Pensions Administration Standards Association (PASA) is aware of these issues and has created a work group to enable transferring members a faster outcome. This will hopefully make transferring pensions to legitimate schemes much easier.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

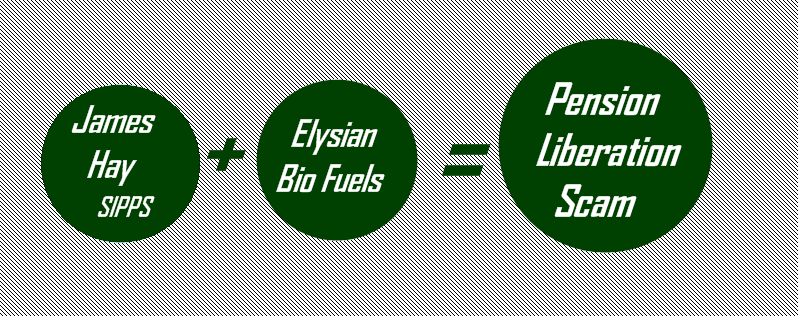

James Hay, the first UK SIPPS provider, could face tax charges of up to £20 million from HMRC, related to the Elysian Bio Fuel investment scam (sorry: scheme). Elysian Bio Fuels, which owned a bioethanol plant in the US and a renewable fuels refinery in the UK, was also used by other SIPPS providers such as Suffolk Life.

Money Marketing states : “Sipp investors are facing millions in write downs on a high-risk bio fuel investment, which has also been linked to a suspected pension liberation scam.”

Unsurprisingly, James Hay has launched an appeal against the tax charges AND as of January, has also slipped in a ban on non-standard investments including overseas commercial property, storage pods and carbon credits to be bought through its SIPPS platform.

We say to James Hay, “too little, too late, mate!”

Through SIPPS provided by James Hay, around 500 clients put £55m in to Elysian Bio Fuels. Yes, that´s 500 retail investors, placed into high-risk toxic investments, totally unsuitable for pensions. The business failed in 2015. James Hay claim that they did not advise their members AND limited their role to pension administration. Whilst they may not have directly advised their members, they did, however, allow crooked advisers to buy shares in Elysian Bio Fuels for the purpose of Pension Liberation.

The sheer act of letting crooked advisers advise their trusting members, whilst turning a blind eye to fraud, makes James Hay guilty in anybody´s book. How long can so called legitimate SIPPS providers continue to get away with this sheer negligence of their members´ funds?

Below is an email exchange between Stephen Ward of Premier Pension Solutions, his lawyer Alan Fowler and Angela South of Magna Wealth. This thread describes exactly how the Elysian Bio Fuels/James Hay liberation scam worked.

Interesting….but I’m amazed that reputable SIPP providers will countenance this. Who’s making the loans? I’m not sure I see how the SIPP pays the member (or anyone for that matter) £100k – with what/who’s money? And won’t the SIPP need to verify that the shares in Xco are actually worth £100k. That said, if the IFA is doing these, it seems the process works………..

From: Stephen Ward [mailto:SWard@ppsespana.com] Sent: 18 October 2013 10:01 To: Angela (South – Magna Wealth) Subject: FW: QROPS opportunity Importance: High

Morning Angela

I was not expecting such a fast green light !

But it seems to me that a green light is what we have

The next step is a test case I guess ….. ? I may have one but just need to check his fund value.

Putting my provider hat on I do not need to understand the details of the back end engineering, the fact its OK with James Hay is good enough for me.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

There are many different types of pension scam – just as there are many types of genuine pension scheme. This can sometimes make it difficult to tell the difference so we are her to help you inform you about, what is a pension scam.

Fortunately, there are some common tell-tale signs that mean you could spot a scam and avoid it:

Cold calling: always be suspicious of a cold caller. This can come as a text, phone call, email or even a smart-looking individual at your door!

Some cold callers may even imply that they are from the government or another government-backed organisation.

THIS WOULD NEVER HAPPEN!

Hard sell: when your smart-looking/sounding “adviser” won’t take “no” for an answer and pressurises you into an on-the-spot decision

No land-line contact phone number: the only contact they give consists of an email, mobile or PO Box address

Use of words like ‘pension liberation’, ‘loan’, ‘loophole’, ‘free pension review’ or ‘one-off investment’

Unrealistic claims:

You can unlock your pension before 55

Promises of tax advantages

investment is ‘unique’, ‘overseas’, ‘environmentally friendly’, ‘ethical’ or in a ‘new’ industry

Low risk but high return investments (THEY DON’T EXIST!!)

What the scammers don’t tell you is that taking any part of your pension early (before 55 years of age) DOES result in tax charges. These charges can be up to 55% of the amount you take – even if you were told it was a “loan”.

With HMRC on your back for this tax demand, it will be hard to remember the pleasure of the money you received. Plus, whilst you are distracted with your tax demand from HMRC, it is likely that the rest of your pension fund is taking a nasty tumble.

Pension scams can involve various types of pension arrangements from QROPS and QNUPS to occupational schemes and SIPPS. These arrangements are not, in their own right, bad. However, if they are used for unsuitable investments, they most certainly can be. Know about these investments means you will know about what is a pension scam.

The investments inside the schemes can range from high-risk, professional-investor-only structured notes to toxic, illiquid, risky UCIS funds (Unregulated Collective Investment Scheme – illegal to be promoted to UK residents). Whilst these types of investments are not illegal in their own right, they are only suitable for certain people with deep pockets and sound investment experience. Or, alternatively, they are totally unsuitable for pension funds – full stop.

When taking advice on transferring your pension fund you should always ensure the adviser you choose is either based in the UK OR in the country you reside/plan to reside in. Alternatively, you must make sure the adviser is regulated and qualified for pension and investment advice in the jurisdiction where you reside.

If you’ve already signed something you’re now unsure about, contact your pension provider straight away. They might be able to stop a transfer that hasn’t taken place yet.

If you think you’ve been targeted by an investment scam, please report it to the FCA using their reporting form.

If you have lost money to a suspected investment fraud, you should report it to Action Fraud on 0300 123 2040 or online at www.ActionFraud.police.uk.

If you have doubts about what to do, ask The Pensions Advisory Service (TPAS) for help. Call them on 0300 123 1047 or visit the TPAS website for free pensions advice and information.

Beware of being targeted in the future, particularly if you lost money to a scam. Fraudulent companies might take advantage of this and offer to help you get some or all of your money back.

*************************************

With out due diligence and knowledge you often won´t realise that you are the victim of a pension scam until its too late. Its best to have the knowledge so you can tell what is a pension scam and what is a genuine pension scheme.

Therefore, Pension Life has written a series of blogs about pensions, pension scammers and how to safe guard your pension fund from fraudsters. Please make sure you read as many as possible and ensure you know everything you should about your pension fund. If we can educated the masses about pension fraud we can stop the scammers in their tracks – worldwide.

Debbie Abrahams takes a stand in parliament, raising the question of, “how many more pensions scandals does she (Esther McVey, Secretary of State, Work and Pensions) need before she introduces the robust regulatory oversight needed to protect peoples’ pensions for the future?“

Debbie Abrahams (pictured) has been a Member of Parliament for Oldham East and Saddleworth since her by-election victory in January 2011. Debbie was a member of the Work & Pensions Select Committee from June 2011-March 2015 , where she led the call for an independent inquiry into the Government’s punitive New Sanctions Regime. In June 2016 she was appointed Shadow Secretary of State for Work and Pensions.

During Work & Pensions Questions, Debbie stated “100´s of 1000´s of ordinary working people have lost half of their retirement income.” Mentioning British Steel Pension Schemes (BSPS), Carillion, BHS and Capita, she goes on to highlight the government´s failure in tackling pensions governance.

BSPS were pushed into the Pension Protection Fund, the government lifeboat for failed schemes in December 2017. 122,000 members were given just months to make the decision of where to go with their precious pension funds. They had the choice to stay with the scheme, join a new one with reduced benefits set up by Tata Steel, or transfer to a personal pension plan. The Guardian reports further on this stating that, “those who do not make a decision will default into the PPF.”

The Independent released an article about the collapse of Carillion: Carillion was put into liquidation in January 2018 after racking up debts of around £900m and a pension deficit thought to be at least £587m.

The collapse of Carillion has left hundreds of workers redundant and their pension funds in tatters.

BHS had 19,000 members and a combined £571m deficit when the company went into administration in April 2016. Again reported by The Guardian, we can at least be thankful that:

Domonic Chappell is being prosecuted by The Pensions Regulator (TPR) in the latest fallout from the demise of BHS, which he bought for £1 from retail tycoon Sir Philip Green in 2015.

With all this pension turmoil, the path is paved with gold for the serial pension scammers, such as ex CWM employees.

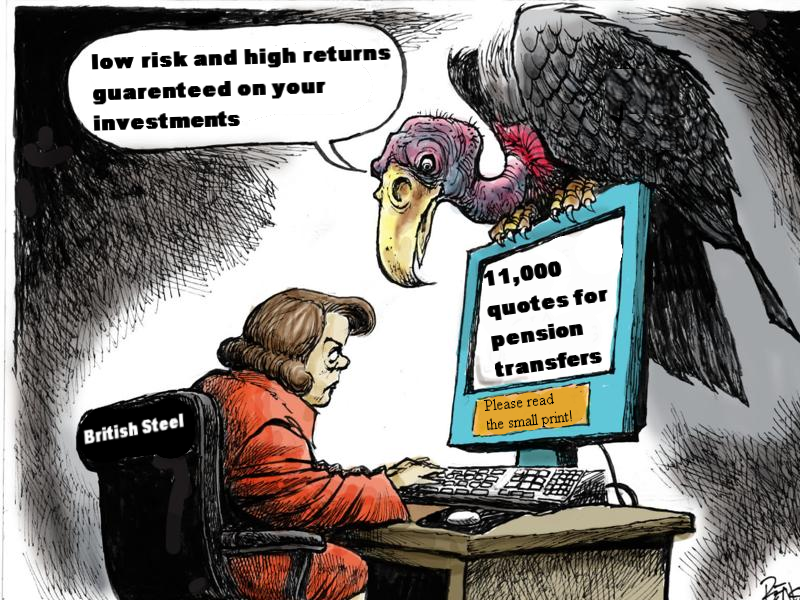

The Financial Times reported that: The Financial Conduct Authority is investigating allegations that steelworkers at Tata UK’s plant in Port Talbot were being targeted by unscrupulous pension transfer advisers. British Steel pension fund trustees have received requests for around 11,000 quotes for pension transfers. With promises of low risk and high returns on the investments, who knows how many peope have fallen victim to these vultures already?

We at Pension Life would also like to know why the government has not put in place tighter regulations on pensions to combat pension scammers. New laws need to be introduced so hard working and trusting citizens aren’t left with decimated pension funds.

We can at least be thankful that the SFO and the Pensions Regulator are pushing forward at the High Court and bringing some pension scammers to justice.

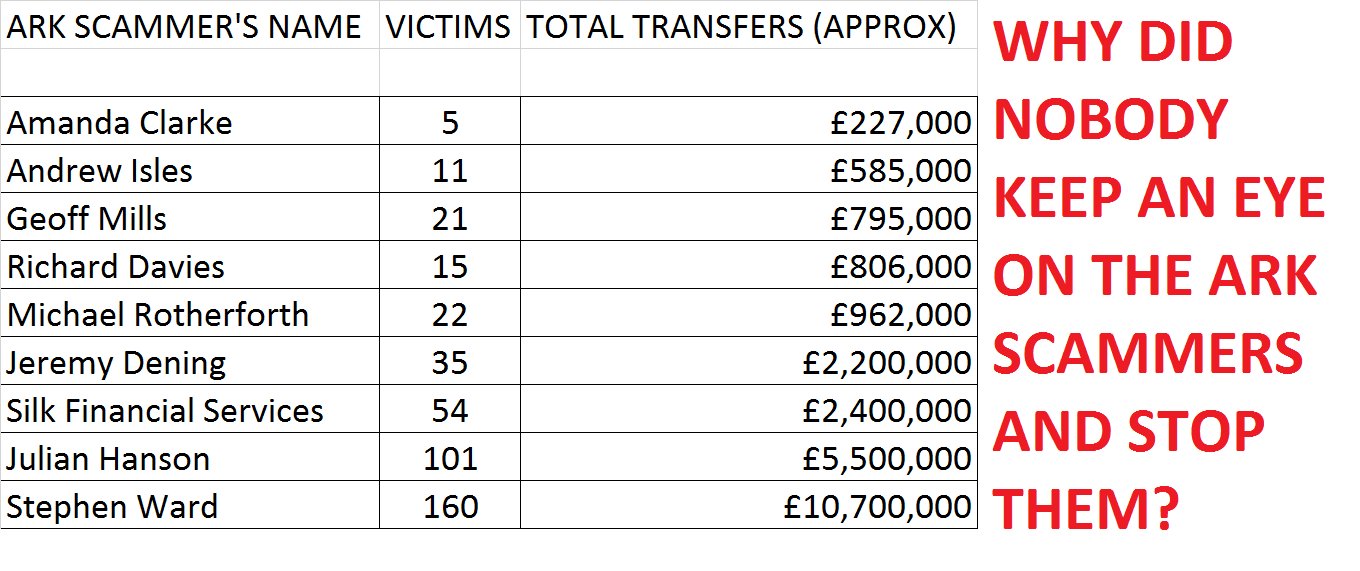

Why pension scammers such as Julian Hanson must be stopped before they burn more victims’ pension funds – such as in the Ark and Barratt and Dalton scams

Julian Hanson – why pension scammers must be prosecuted.

245 victims had their pension funds stolen by David Austin, Susan Dalton, Alan Barratt and Julian Hanson. Their company – Friendly Pensions Limited (FPL) – acquired the pension funds using cold calling techniques with promises of ‘tax-free’ payments.

The Pensions Regulator (TPR) had asked the High Court to order the defendants to repay the funds they dishonestly misused or misappropriated from the pension schemes – the first time such an order has been obtained.

But this clearly demonstrates that pension scammers should be prosecuted and jailed quickly before they go on to scam thousands more victims. Julian Hanson – an integral part of the Barratt and Dalton scamming team – was also an integral part of the Ark scam.

Julian Hanson acted as an introducer/adviser in the ARK case (also in the hands of Dalriada) in 2010/11. He scammed over 100 victims out of their pensions – totaling around £5.5 million worth of retirement savings. Hanson, in common with the many evil scammers creating scam after scam, was happy to push aside the appalling predicament of his Ark victims and stroll on to find new victims for the Barratt and Dalton scam.

Hanson had promised his Ark victims their pensions would be profitably invested in “high-end London residential property” and would grow sufficiently to discharge the 50% they were allowed to take from their funds. This, he assured the victims, would NOT be taxable.

As soon as the Pensions Regulator placed the Ark schemes into the hands of Dalriada Trustees, Julian Hanson should have been prosecuted and prevented from ever scamming pension savers again. But, sadly, he was left free to continue his evil trade. Hanson was one of a whole army of scammers peddling the Ark scam:

And hereby lies a basic flaw in the system: had Julian Hanson (along with his fellow scammers) been prosecuted and jailed for scamming the Ark victims, in 2011, the subsequent Barratt and Dalton victims might have been saved. However, it will hopefully be the last one that Julian Hanson is allowed to get away with, as his name will now be synonymous with pension scams.

The same is true for the other introducers/advisers peddling Ark who remain free to continue their trade:

Andrew Isles is still a practicing accountant at Isles and Storer

Stephen Ward went on to scam thousands more victims out of their pensions and into toxic investments as well as illegal liberation in the Evergreen QROPS; Capita Oak, Westminster, Southlands, Headforte, and London Quantum.

The mastermind behind the Barratt and Dalton scam was apparently David Austin – a former bankrupt with no experience of pension investments. He invested victims’ pension funds in truffle trees and St. Lucia timeshares, and then laundered the victims’ pension funds through relatives in the UK, Switzerland, and Andorra. Austin used a number of businesses he had set up in the UK, Cyprus and the Caribbean – including Friendly Pensions Ltd. Austin’s family clearly had no shame about where their money came from and flaunted their new-found wealth all over social media. Fortunately, this vulgar and heartless bragging made the job of gathering evidence for the High Court much easier for tPR

TPR had appointed Dalriada Trustees to the case, and with this ruling, they will be able to attempt to recoup the stolen money from the four scammers. Unfortunately it is unclear how much money is actually left to recoup as scammers are notoriously clever at hiding their ill-gotten gains offshore and presenting themselves as “men of straw”.

Nicola Parish,TPR’s Executive Director of Frontline Regulation, said: “The defendants siphoned off millions of pounds from the schemes on what they falsely claimed were fees and commissions.

“While Austin was the mastermind, all four took part in stripping the schemes almost bare. This left hardly anything behind from the savings their victims had set aside over decades of work to pay for their retirements.

“The High Court’s ruling means that Dalriada can now go after the assets and investments of those involved to try to recover at least some of the money that these corrupt people took. This case sends a clear message that we will take tough action against pension scammers.”

One the investments in the Barratt and Dalton scam was £2 million in an off-plan timeshare development in St Lucia called Freedom Bay. This same development also took millions of pounds’ worth of funds from the victims of the ARK scam. Freedom Bay is now in administration.

In this scam, operating between November 2011 and September 2014, 245 people were cold called, promises of a cash lump sum and compliant investments at 5% were promised.

The reality of what happened to the funds was:

More than £10.3 million was transferred to businesses owned or controlled by Mr Austin

Just £3.2 million of the funds was invested

False documents were made to cover these figures

Funds given back to the victims were a % of their actual funds and NOT profits

More than £1 million was paid to the “ introducers” or “agents” who conducted the cold calls

One of the victims, Colin, from South Wales, had become the full-time carer for his partner when he was approached via text message. Promised investments in the now bust St Lucia Developments, a lump sum which he planned to spend on a holiday. Having heard about the pension scams, he tried to contact the scammers with no success.

Colin, 48, said: “I should have known that it was too good to be true. I should have sought advice and asked more questions, but I didn’t.

“I had contributed towards my £50,000 pension pot, for which I had worked really hard, and now that has been taken from me.

“The loss of my pension will have a massive impact on my life. When my children finish school I will be around retirement age. There will be no money to draw down when I turn 55 and no pension savings for later life.

“I was greedy. I feel stupid for throwing away my financial future for £4,200.”

A couple, John and Samantha, both fell victim to this scam despite being advised by their pension provider that it could be a scam. They received their lump sum and were told their pension was invested in truffle trees. After reporting the case to the police, they were later informed that their lump sum was from their own funds and HMRC promptly served them with a large tax bill.

John, 46, said: “As a result of my dealings with Alan Barratt my final salary pension is in a scheme that I don’t understand the status of but which I have been told is a scam.

“As far as I know, the majority of my pension fund is invested in truffle trees but I doubt whether that is legitimate. My partner appears to have lost her pension too.

“I deeply regret ever listening to Mr Barratt.”

Why has cold calling not been banned by the government?

Why are ‘introducers’ still be used?

Why are the scammers in the Ark case not under criminal investigation?

Serial pension scammers like Julian Hanson and all the others need to be stopped now. New laws need to be introduced so hard working and trusting citizens aren’t left with decimated pension funds and huge tax bills they can’t pay.

Beddoe proceedings: arguably (apparently) Dalriada could have been pursued by Ark victims without MPVAs for not pursuing repayment from those with MPVAs and conversely could have been pursued by Ark victims with MPVAs. So, to be on the safe side, they spent a quarter of a million quid of the victims’ funds on the Beddoe proceedings in the High Court.

And here we need to look at the meaning of the terms – MPVA and sharp stick:

Sharp Stick: Fenner Moeran’s extremely offensive statement that Ark victims should be beaten with a sharp stick (upon which neither the judge, Sarah Asplin, admonished him nor upon which Keith Bryant, the Ark victims’ QC, challenged him)

MPVA

MPVA is an anacronym for “Maximising Pension Value Arrangements” – a euphemism for pension liberation. The rules are that if a person is under the age of 55, he or she can’t access any part of their pension without incurring an unauthorised payment tax charge of up to 55%. So all pension liberation scammers think up clever ways of fooling potential victims into believing there is a legal “loophole” to circumvent this rule.

The point of a pension liberation scam is not to provide members with a bona fide pension scheme designed to provide an income in retirement, but to make the scammers loads of money. First there is the transfer fee: in the Ark case it was relatively low at 5% – although Stephen Ward was charging an extra fee on top of that of up to £2k per transfer.

And then there are the investment kick-backs. We still don’t know how much the Ark scammers earned out of the speculative, illiquid, high-risk properties they purchased in various dodgy offshore jurisdictions. But it will have been very lucrative. In subsequent scams, the scammers earned huge commissions such as 20% from Dolphin Trust; 30% from Park First; 46% from Store First.

By the time the Ark victims realised they’d been scammed it was too late and there was no parachute

The scammers always promise spectacularly high returns on the investments with assurances such as “guaranteed 8% per annum”. In the case of Ark, the victims were told they would receive up to 9% a year on the growth of the value of “high-end London residential properties” in which the pensions would be invested. This, of course, was a lie. But by the time alarms started to ring and the victims realised there was no way out of this toxic flight with no parachute, it was too late.

But let us revert to the portion of a transfer which is liberated. This can range from 5% to 85% depending on the structure of the scam. And it is given various names or labels such as “cashback”; “thank you”; “refund of fees”; “trousers”; “loan”. The favourite word used is “loan” because the scammers claim that “loans are not taxable”. There is no intention for the money ever to be paid back – that isn’t the point of the exercise. The scammers know the victims would never be able to repay the funds.

The use of the word “loan” in some schemes is merely a marketing term used to fool people into believing they won’t be taxed on the money. And the scammers have no interest in whether the victims ever get taxed or not – because by the time HMRC gets around to sending out tax demands, the scheme will have collapsed and the scammers will be long gone and far ahead on their next scams. They never stick around to help mop up the train wreck left behind.

Often, the victims are surprised when they receive “loan” documentation and alarm bells start ringing. But the scammers assure the victims that this is “just a paper exercise” or “administration to make sure HMRC don’t try to tax the money – because loans aren’t taxable“.

In the Ark scheme, the victims were told the amounts liberated would not be taxable because they didn’t come from the members’ own scheme, but from another scheme. And this is why 14 schemes were set up to work in pairs so that up to 99 people in each pair of schemes could swap cash from their transfers. So this was an artificial mechanism structured purely to operate the liberation – using the label “MPVA” to dress the payments up as something more glamorous and bona fide than just a dollop of unauthorised cash in a person’s trousers.

Very few of the victims were told their cash would ever have to be paid back. The MPVA agreements never once mentioned the word “loan” but did mention the word “discharge” and suggested that the MPVA would be automatically “discharged” after a period of years.

Some victims were told the MPVA would be settled or repaid out of the growth that the Ark pension would enjoy (because of the wonderful investments!). It was explained that the MPVA would grow at 3% a year but the pension fund would grow at 9%. But the member would never have to pay the MPVA off out of their own pocket.

Other victims were told the MPVAs would never have to be paid at all because of the reciprocal nature of the transfer/payment structure. It was explained thus: two “paired” members in different schemes would each have a reciprocal MPVA of – say – £50k. If they both decided they never wanted to pay the MPVAs back, they would just treat them like equal IOUs and agree to simply tear them up.

The Tolleys authoritative manual on pensions taxation by Stephen Ward

Now remember, the victims weren’t told these things by any old spivs – they were told them by Stephen Ward of Premier Pension Solutions and his various accomplices (e.g. Fraser Collins, Terry Tunmore, Paul Clarke etc). Stephen Ward was back then – and still is now – a regulated financial adviser of many years’ experience, as well as the author of the Tolleys Pensions Taxation Manual, (and Level 6 CII qualified).

The same assurances were also given to numerous victims by George Frost, of Frost Financial, a regulated mortgage and insurance broker. And the victims who received the advice on the merits of entering into the Ark scheme believed they had every right to believe and trust professional, qualified and regulated advisers who assured them the MPVAs would never have to be repaid and that their pensions would be safe and secure.

HMRC does not care whether a sum of money accessed from a pension before the age of 55 is called a loan, thank you, cash back, fee refund, MPVA or any other euphemism for “liberation”. They don’t care whether it is repayable or whether it is ever repaid or not. They don’t care whether it comes directly from the member’s pension scheme, or from somebody else’s pension scheme, or via some convoluted arrangement designed to conceal the source of the money – such as Stephen Ward’s Evergreen/Marazion pension/loan scam. If a member makes a pension transfer and receives a sum of money as a result – irrespective of where it comes from – HMRC will issue a tax demand of up to 55%.

To illustrate how pension liberation scams range from the very simple and transparent to the highly complex and opaque, here is an example of one arrangement which Stephen Ward and his merry men, Alan Fowler and Bill Perkins, were involved with in 2013 – after Ark, Evergreen, Capita Oak and Westminster pension scams had all been suspended:

Thanks to you both for your understanding…. Am unused to non delivery! The arrangement I heard about today works like this as an example (ignoring fees) and this is the simplistic version …

Client borrows 16k or thereabouts (this is available in the package)

He gets a non recourse loan (which will not be repaid) of £84k

He buys shares in Xco for £100k. These are listed on the CISX (name is Elysian)

Transfers £100k to James Hay SIPP

SIPP pays member £100k for the shares

Member repays the 16k and trousers £84k

My IFA connection has done 40 of them so far. Advice to transfer to the SIPP is from an FCA regulated IFA. James Hay and Suffolk Life know the full structure and are happy with it.

Regards Stephen

The FCA-regulated IFA to whom he was referring was Angela South of Magna Wealth. She soon made a hasty exit from the collaboration with Stephen Ward when victims realised this was a scam and threatened to report her to the Serious Fraud Office. Victims who participated in this scam have now received tax demands from HMRC and Elysian Fuels is now worthless.

SHARP STICK

Dalriada’s QC, Fenner Moeran, seemed like a very sharp cookie. His skeleton argument (which we never got to see), and his opening speeches, started with the assumption that the MPVAs were definitely loans; that there was no question that they were loans and that the members knew and accepted that they were loans.

The judge, Sarah Asplin, accepted this without question and there was no debate on the subject. Kim Goldsmith’s QC, Keith Bryant, sat as quiet as a corpse and made not one single interjection or objection – even though he was sitting next to Kim who knew perfectly well – and must have told him – that the victims were not aware the MPVAs were loans. Indeed, they were categorically assured that the MPVAs would never have to be repaid.

Even more astonishing was the fact that Dalriada was aware the victims never knew the MPVAs were loans. Dalriada’s Sean Browes and Brian Spence, as well as Pinsent Masons’Ben Fairhead and Ian Hyde, had attended various meetings with the Ark Class Action and gone through this issue numerous times. They were also fully aware that one victim was horrified when she was subsequently told the MPVA was a loan and she immediately called Dalriada and asked to repay it. But Dalriada had refused.

Furthermore, dozens of Ark Class Action members had completed HMRC’s 10-point questionnaire (the Q10) which specifically asked about the arrangements and what they had been told about the need to repay the MPVAs. This is evidenced at HMRC’s question 8:

8: “DETAILS OF WHAT YOU WERE TOLD ABOUT THE NEED TO REPAY THE LOAN”

Here is a typical response to this question by one of the victims:

“I was told that although on paper it would be an official 25 year loan, that because of the nature of the way the loans were set up, i.e. the quid pro quo arrangement, whereby as one person received their monies from the other members scheme and vice versa, if there was a request for any monies to be repaid in the future from each member, each would tear up each other`s IOU and be quits, so to speak, as already stated.”

Stephen Ward – BA (Econ), ACII, APFS, APMI, ex examiner for the pensions management institute and for the CII, confirmed that the Ark scheme was designed by specialist pensions lawyer Alan Fowler – head of pensions at Stevens and Bolton.

Ward went on to explain how the MPVAs worked: “The best way to understand this is in terms of my lending you £100 and you lending me £100. If I do not repay you and you do not repay me then we are both in an equal position. Conversely, if I repay you and you repay me then the position is identical to that which would arise if neither party had repaid the other”.

These statements have been made to HMRC by Ark victims on countless occasions – and Dalriada has always been perfectly well aware of this. And yet Fenner Moeran used his sharp stick to knock these evidenced facts completely off the table – so that the judge was never made aware of them. Mind you, Keith Bryant QC was no better – because he didn’t bring them to the judge’s attention either.

I would go so far as to observe that Fenner Moeran should have used his sharp stick to point the judge to these evidenced facts – and Dalriada should have made sure he did so. By omitting to do so, both Fenner Moeran and Keith Bryant allowed the judge to come to the incorrect conclusion that:

“members who received the MPVA loans agreed to repay them. That’s the point of a loan. It’s not a gift. They cannot now complain about having to repay them. They can complain about having to repay them earlier, but that’s a cashflow issue which is vastly overwritten by the capital harm that is suffered by the non-recipient members”

Fenner Moeran merely leaned on his sharp stick and did nothing to correct the judge. As I was sitting behind him, I couldn’t see whether he was smirking – but I have a feeling he might have been. The judge was wrong on three counts:

The members with MPVAs did not agree to repay them – they were told they would never have to

They can most certainly now complain about being asked to repay them as they were never told they would have to and did not budget to do so

The capital harm suffered by members without MPVAs was mostly caused by Dalriada who did not reject their transfers after 31.5.11 but allowed transfers to continue right up until the end of August 2011

Having glossed over the facts smoothly, and directed the judge to her incorrect conclusion, Fenner Moeran then addressed the issue of ascertaining whether the Ark victims were in a position to be able to afford to repay the MPVAs. And then he produced, with a confident flourish, his pièce de résistance:

“The chances of getting ascertainably or enforceably more accurate information increases when you have the sharp stick of litigation behind it. If we want to see if we’re actually going to get any of this money back, the chances are that we’re going to have to wave a very large stick“

Fenner Moeran ought to be an intelligent person. In the full knowledge that a few feet to his right sat Kim Goldsmith, an Ark victim who had gone through six years of hell courtesy of Stephen Ward and George Frost and all the other scammers, and that a number of other victims were sitting at the back of the courtroom, he still made such an unbelievably stupid and offensive statement. He apologised later “I deeply and sincerely apologise for any misunderstanding or upset caused”.

But the damage had already been done – and you can’t un-say what has been said – especially when every word is recorded and transcribed. On behalf of Dalriada Trustees, he had deliberately misled the judge, and then proceeded to demonstrate clear contempt for the suffering of the Ark victims.

Interestingly, the judge had not remonstrated with Moeran for his crass comments – and Keith Bryant had not objected to the stupid and insensitive words. Throughout the rest of the proceedings, the judge remained – in my view – dominated and steered by Moeran. No attempt was ever made to disclose the truth about what the victims were told about repayment of the MPVAs by Stephen Ward, George Frost, Andrew Isles or Alan Fowler. And no explanation was ever given as to why Dalriada had not pursued these parties for having duped, misled and defrauded the Ark members.

This may seem like a completely off-topic piece of this report, but please stick with it – it will be worth it because it is the whole point of this report. Nearly 18 months before the Ark/Dalriada/Beddoe proceedings in the High Court, another case was heard: Royal London v Hughes. A pension scammer had tried to do exactly what the Ark scammers had done so successfully and profitably for nearly a year: transfer hundreds of secure pensions into a pension scam. But one ceding provider – Royal London – had blocked a transfer request. They strongly suspected the receiving scheme was a liberation scam – unlike the many ceding providers in the Ark case who handed over hundreds of transfers willy-nilly without question or due diligence – the worst of which was Standard Life.

Hughes complained to the Pensions Ombudsman that her transfer request had been blocked by Royal London. The Ombudsman did not uphold her complaint because he agreed with Royal London that the receiving scheme had all the classic hallmarks of being a scam – including the fact that the scheme had been registered as an occupational scheme and Hughes was not genuinely employed by the sponsoring employer. Exactly the same as Ark (and many of the subsequent scams).

Counsel for Royal London argued that “Hughes had to be an “earner” to be able to transfer”. He tried to support the Ombudsman’s view that the legislation required Hughes to be an earner in relation to a scheme employer”. This counsel obviously knew well that victims were made all sorts of promises and assurances and often not told the truth about the arrangements within pension scams.

Royal London’s QC would have been aware of the Ombudsman’s concerns that pension liberation may well have been behind Hughes’ enthusiasm to transfer her pension. And he will have known only too well that potential victims were systematically lied to and probably told that their “loans” (or whatever euphemism was used) were not repayable. And he would have known that the intended liberation “loans” were never intended to be repaid and that the victims would be told that the loans never needed to be repaid.

This QC will have been thoroughly briefed by his clients, Royal London, and may even have consulted with the Pensions Regulator who would have given him thorough details on how pension liberation scams worked.

So this particular QC had intimate, first-hand knowledge of how pension liberation schemes worked in general and represented Royal London in their quest to defend their right to prevent further victims of pension liberation scams. He also knew intimately how Ark worked in particular.

Fenner Moeran of Wilberforce Chambers

He knew perfectly well that the victims were told they never had to repay their loans (or MPVAs/cash backs/thank you’s/trousers). And he knew that the Ark MPVAs were supposed to be “discharged” from growth in the schemes and NOT from the victims’ own pockets – as reported by Justice Bean. But he failed to bring this to the judge’s attention.

Who was this QC? I will give you a clue – he had a big, sharp stick. Perhaps he should have gone to Specsavers and read the MPVA agreement where this was clearly stated.

Laurence Goodman and the three wishes: please make 37 Fast Pensions Scam loans disappear JUST LIKE THAT!

Bridgebank Capital’s Laurence Badman Goodman has made 37 Fast Pensions Scam loans disappear as if by magic – while he was on holiday and too busy to engage with Pension Life or the distraught victims of Peter and Sara Moat.

Having discovered this was where some or all of the elusive Fast Pensions Scam funds were hiding, we all hoped this might finally result in some of the 18 Pensions Ombudsman’s determinations to allow victims to transfer out being complied with.

We all wanted to believe that Goodman was a good man, but now it would seem the opposite might be the case. So, one of the following is true:

All the borrowers of the 37 loans have simultaneously repaid their loans on 17th August 2017

The loans have been sold or transferred on to somewhere we can find them (yet)

Sara Moat had been claiming that Fast Pensions was merely the administrator of the pension schemes, and that it was ultimately the “responsibility of the trustees to decide whether the transfers could be made”. Of course, the Companies House records showed that the Bridgebank Capital loans were made in favour of Sara Moat as trustee (along with another stooge called Martin Peacock). This scuppered Sara Moat’s excuse and exposed her as a liar once again.

So, when Goodman has finished having a jolly time on the Costa Lot, necking his champers and writing his postcards to his mate Pete, perhaps he might find a moment to be sober enough to remember that I am meeting the Serious Fraud Office next week. And most of the Fast Pensions Scam victims have also submitted their reports to the SFO.

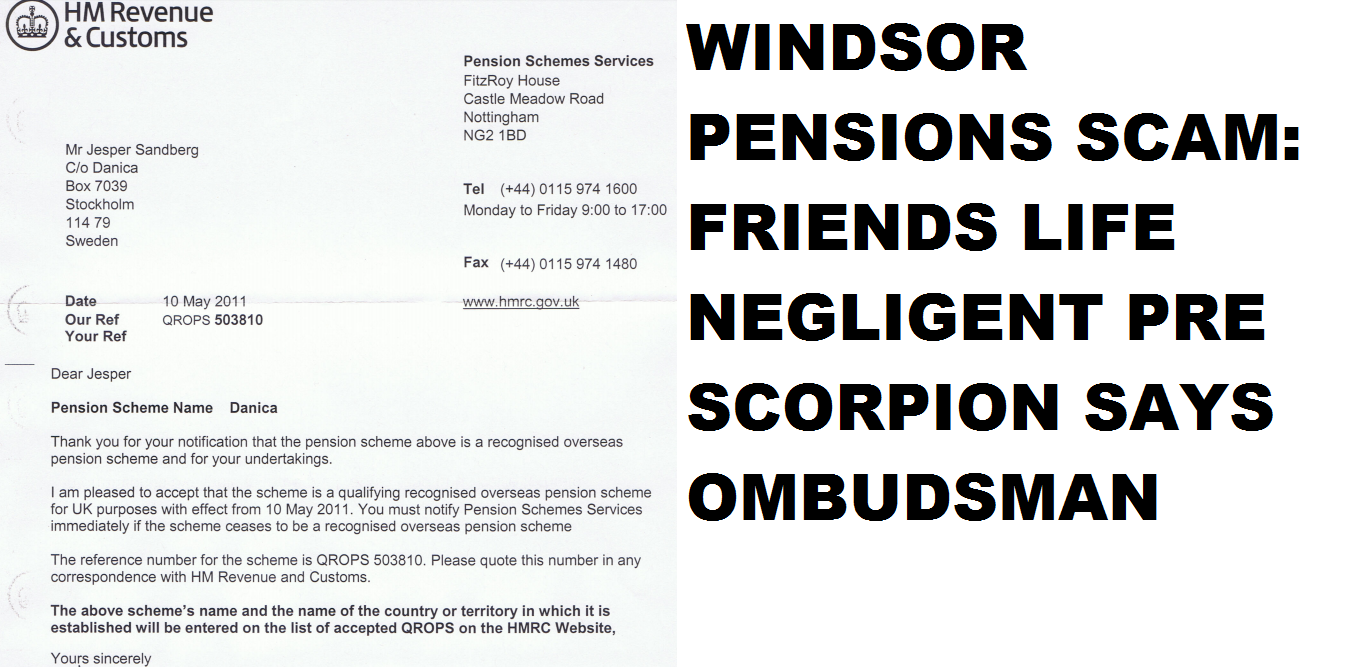

Friends Life negligent in Windsor Pensions “Danica” scam

FRIENDS LIFE – OR DEATH? WINDSOR PENSIONS QROPS SCAM (DANICA)

Since 2010, dozens of ceding pension providers have recklessly and negligently allowed transfers out to obvious pension scams. During the years of Ark, Capita Oak, Westminster and Henley, the worst offenders were Standard Life, Scottish Widows, Prudential and Aviva as personal providers, and Royal Mail as an occupational provider.

Both HMRC and the Pensions Regulator claim there were sufficient/ample warnings in the public domain to educate and inform ceding providers about pension scams since 2002. But the Pensions Ombudsman’s Service claims the cut-off date was February 2013 when the Pensions Regulator first published the “Scorpion Campaign”. According to the POS, before Scorpion all ceding providers walked around with paper bags over their heads and did no reading up on their professional and fiduciary obligations or any developments among scams and scammers.

However, a recent ruling on the negligence of a ceding provider – Friends Provident – may change the course of history. The case of “Mrs N” involved a transfer from FP administered by a company called Windsor Pensions run by one Steve Pimlott in Florida. In fact, I “secret shopped” Windsor and Pimlott in 2015, and he was still offering “transfers to Danica QROPS” with full liberation. He also claimed to have done 5,000 such transfers/liberations.

On 25 February 2015 at 10:37, STEVE PIMLOTT <stevepimlott@windsorpensions.com> wrote: Dear Ms Brooks

I cannot give you tax advice. If you cash out, it’s possible that HMRC will send you a tax bill. We assisted approximately 5,000 people who took that route and I would estimate that 200-300 did receive a tax bill. The rest to my knowledge did not. Of those that did, many just ignored it because they were resident in a different country and had no assets left in the UK.

Regards

Steve

The question is, however, does this set the bar for other negligent ceding trustees? This case is notable because it is “pre Scorpion”. But the POS found that irrespective of the date, Friends Provident should have done more due diligence and not just handed over a pension to a scheme which was no longer registered (and, de facto, to a fraudulently-set-up bank account).

Mrs N’s complaint is upheld and to put matters right Friends Life should pay her the unauthorised member payment tax charge and surcharge less the tax liability she would have paid had the full pension been taken as an uncrystallised funds pension lump sum (UFPLS). In addition it should pay Mrs N £1,000 for the significant distress and inconvenience caused by its error.

My reasons for reaching this decision are explained in more detail below.

Complaint summary

Mrs N complained that Friends Life undertook insufficient due diligence on the qualifying recognised overseas pension scheme (QROPS) into which she had requested a transfer. Had it acted appropriately it would not have accepted the transfer instruction.

Following the transfer Mrs N received the full value of her pension. At the time she was 53. As a result she is now liable to a 55% unauthorised member payment tax charge.

Mrs N has also said she has incurred costs whilst attempting to resolve the situation and Friends Life should pay these.

Background information, including submissions from the parties

On 10 May 2011, HMRC wrote to Danica, Stockholm, confirming undertakings had been received that Danica was a recognised overseas pension scheme, and that HMRC would accept the scheme as a QROPS with effect from 10 May 2011. It provided a QROPS reference number – QROPS 503810 – and confirmed that the scheme name and country would be added to the list of accepted QROPS on HMRC’s website.

Danica was added to the HMRC QROPS list, but then removed on 29 June 2011.

In October 2011 Mrs N completed a letter of authority for an unregulated financial intermediary; Insignia Financial Services. This was submitted to Friends Life which responded with a transfer illustration on 3 January 2012. QROPS illustrations were issued on 21 January 2012.

On 16 February 2016, Friends Life received an Overseas Transfer Out Payment form and Member Declaration, signed by Mrs N on 7 February 2012. Accompanying this was the HMRC letter confirming QROPS status.

QROPS discharge forms were issued to Mrs N shortly after.

The required forms were received by Friends Life on 9 March 2012. Friends Life says that the supplied QROPS number was checked against the QROPS list and found to be correct. Friends Life also checked the HM Treasury sanctions list.

The payment of £88,622.80 was processed on 13 March 2012. However, what the POS has not disclosed is that the funds were sent to a Barclays Bank account in the Isle of Man which was fraudulently set up by the scammers with the account name “Danica”. I understand the money was subsequently paid to Mrs N by the Danica arrangement and has since been spent. No it wasn’t. The money never went near the Danica pension scheme in Sweden. It went straight to the scammers’ bank account in IoM.

Friends Life were made aware of an issue with the Danica scheme, and Insignia Financial Services on 13 April 2012.

Mrs N has since been contacted by HMRC and informed that the transfer was an unauthorised payment, so it is subject to an unauthorised member payment tax charge and surcharge of approximately £49,000. I understand this has not been paid and remains outstanding, with interest accruing.

Mrs N raised a complaint about Friends Life’s actions. It did not uphold the complaint, and made the following summarised points.

Mrs N had a statutory right to transfer, and Friends Life had no reason to think that the information provided regarding the QROPS was false. Friends Life missed a rather obvious clue i.e. a QROPS in Sweden was purportedly using a Barclays bank account in the IoM – might that not have rung an alarm bell?

The QROPS number was checked against the QROPS list and found to be correct. Although the name Danica did not appear on the QROPS list, Danica Private Pension (Sweden) and Danica Pension (Sweden) did. In other words, similar but different.

The transfer happened prior to concerns about pensions liberation being widely recognised as an industry issue. The Pension Ombudsman has previously said that February 2013 was the point of change in good industry practice where knowledge of pension liberation and scams had increased. This is nonsense – both the Pensions Regulator (formerly known as OPRA) and HMRC had been warning the industry about pension scams for more than fifteen years. Friends Life had an absolute duty to be aware of and vigilant against pension scams.

The presence of a scheme on the QROPS list does not guarantee its QROPS status, and HMRC forms which would have been completed by Mrs N state: “The list should not be relied upon by you, the member in deciding whether a scheme is a QROPS.” Pretty confusing to be honest: HMRC publishes a list of QROPS but the member herself has to decide whether the scheme is a QROPS. How would a member decide that? Ask the scammers?

Friends Life suggested that Mrs N transferred her pension with full knowledge of a lump sum payment being made, which was not offered under her existing plan due to UK tax legislation. It was reasonable to expect that she would have sought independent financial advice before proceeding. Instead she proceeded through an unregulated financial adviser and did not seek advice from a regulated adviser. Indeed, the adviser was unregulated – but Mrs. N did not know this and wouldn’t have known how to check anyway. In fact, Friends Life ought to have brought this to her attention at the start.

There was an onus on Mrs N to check the legitimacy of her financial adviser. At the time there was no reason for Friends Life to think the financial adviser was unregulated. Friends Life didn’t even check.

Friends Life had highlighted that, ‘Tax penalties may apply following a transfer to a QROPS. It is important all implications are understood before transferring funds from the UK’, and Mrs N had received a copy of this statement.

Adjudicator’s Opinion

Mrs N’s complaint was considered by one of our Adjudicators who concluded that further action was required by Friends Life. The Adjudicator’s findings are summarised briefly below:-

Central to the complaint was whether Friends Life should have acted on Mrs N’s transfer request. Side issues relating to the legitimacy of the financial adviser involved or any declarations signed were not integral to the complaint.

The events complained of occurred prior to the Pension Regulator’s pension liberation warning campaign of February 2013, at a time when checks on receiving schemes were less rigorous. This may be correct – however, that doesn’t make it right. However there were reasonable basic checks that Friends Life ought to have completed before making the transfer, including checking HMRC’s QROPS list. They did check the QROPS list and were probably confused by the similar names of two other schemes containing the word “Danica”.

The Danica scheme had been on the list for a short period but was removed by the time Mrs N submitted the transfer request. Friends Life’s internal policy was not to transfer to schemes which were not on the QROPS list.

Although the QROPS list was checked the day before the transfer was put through and there were two similarly named schemes on the list, the Danica scheme was not on the list. At that point additional checks should have been undertaken to establish why the Danica scheme was not on the list, had it done so it would have established that the Danica scheme had been removed nine months prior.

In these circumstances Mrs N’s pension should not have been transferred, and had it not done so Mrs N would not now be subject to the unauthorised member payment tax charge and surcharge. One could argue against this point – perhaps Windsor Pensions and Insignia Financial Services would have found another obscure QROPS to use for the fraud.

To put matters right Friends Life should agree to meet the full cost of the unauthorised member payment tax charge and in addition pay Mrs N £500 for the distress and inconvenience suffered.

The Adjudicator did not consider Friends Life should be required to pay the costs Mrs N incurred when bringing the complaint. The complaint could have been referred to this Office and resolved without the involvement of her representative. I would not agree necessarily: Mrs. N had a very busy life running a business in the USA and she did need help and guidance with the complaint against Friends Life and the POS process. She was also fighting the tax demand at the same time and was extremely distressed.

Additionally, in relation to potential accountant’s fees she may incur, the Adjudicator concluded she would have needed to pay similar costs had the funds been received through legitimate means.

Mrs N did not accept the Adjudicator’s Opinion and the complaint was passed to me to consider. Mrs N and Friends Life provided further comments which are summarised below.

Friends Life said:-

Friends Life accepted the recommended redress in principle, but highlighted that it had already paid a 40% Scheme Sanction Charge and Mrs N was, under the Adjudicator’s recommendation, in effect being paid the fund value without any tax liability. Friends Life proposed to pay the unauthorised member charge less the notional tax Mrs N would have paid had she legitimately accessed the full fund value under the current rules. It calculated the tax she would have paid to be £15,294.34.

Friends Life also considered that given Mrs N’s position it was reasonable for her to have sought independent financial advice given its recommendation that she do so, and especially given her unfamiliarity with UK taxation laws. In not doing so Mrs N had contributed to the risk that her pension could be adversely impacted by the transfer.

Mrs N said:-

The proposed redress would have significant tax consequences for her as a U.S. resident. As a result the redress would not put her back into the position she should have been had the error not occurred.

She had incurred significant expenditure appointing a representative to pursue the complaint on her behalf. Those costs, and the cost of receiving appropriate cross border tax advice, would continue to rise. Given the complexity of the issues in the complaint, and the tax complications she could not have brought the complaint without specialist assistance.

The redress methodology used by Friends Life show a misunderstanding of Mrs N’s tax position. For instance it has suggested that she would be entitled to a personal allowance, when as a U.S. resident this is not the case.

The wording of the redress must be specifically tailored to avoid potential tax complications in the UK and U.S. Friends Life should pay the costs associated with drafting agreeable wording to avoid those tax complications.

Friends Life should provide an indemnity to cover the potential tax liability arising from the redress payment.

She was very distressed by the situation, has been unable to sleep and it has impacted her health.

On review of Friends Life’s and Mrs N’s responses to the Opinion the Adjudicator made the following points:-

* Friends Life’s offer to pay the unauthorised member payment tax charge and surcharge, less the tax Mrs N would have paid had the pension been paid as an UFPLS, was reasonable in the circumstances. The recommended redress was altered to reflect this.

* The redress was not intended to pay Mrs N’s tax liability. Mrs N was the party subject to the liability and would need to pay this. The redress was intended to make good a relevant proportion of that loss once it had been paid. Under this arrangement the reference to a personal allowance was only notional it did not appear that Mrs N would be subject to punitive tax charges as the redress was intended to make good Friends Life’s error.

* Given the significant impact on Mrs N’s health the Adjudicator increased the proposed distress and inconvenience award to £1,000, which Friends Life agreed to.

Having considered Mrs N’s arguments they do not change the outcome. I agree with the Adjudicator’s Opinion, summarised above, and I will therefore only respond to the key points made by Mrs N for completeness.

Ombudsman’s decision

Mrs N argues that she could not have brought the complaint without employing the assistance of tax and pensions specialist. I do not agree. In the first instance a complaint can be passed to the Pensions Advisory Service, who can guide an applicant through the Scheme’s complaint process and provide technical input where the applicant lacks an understanding of the issues involved. In this case TPAS considered it too late to intervene due to the potential time limits of referral to this Office. So it was not a lack of understanding that prevented TPAS from taking on the case.

Notwithstanding that, had Mrs N not accepted Friends Life’s response to the complaint she could have brought the complaint directly to this Office for review. Although Mrs N’s representative disagrees, I am confident that this Office has the expertise to investigate complaints about pension liberation. I would dispute that: the POS has repeatedly failed to uphold pre-Scorpion complaints on the basis that pension trustees had never heard of pension liberation fraud prior to February 2013 – which is absolute nonsense. The representative’s involvement has not brought any unknown evidence or arguments to the investigation. Mrs N was entitled to seek assistance in this matter, but that does not mean Friends Life are responsible for the costs incurred where there are free dispute resolution alternatives available to her. For that reason I do not consider Friends Life should pay the costs she is claiming. To be fair, I think Mrs N should have had her costs paid. She – and thousands of other victims in this situation – find themselves utterly overwhelmed by these types of cases and need support. Also, being based in the USA, she needed someone to deal with the case in the UK.

I understand that as a U.S. tax resident there may be complications in Mrs N’s tax situation on receipt of the redress payment. Her UK and U.S. accountants have said they will not provide advice on the matter because of the complications. The redress may cause her to have to seek specialist tax advice. However, tax is matter for Mrs N and the local tax authorities. It is not for me to determine any future tax liability she may have, and it may ultimately be that there is none.

I have also taken into account that had Mrs N taken her pension through legitimate means she would have needed to seek tax advice regardless, so in my view the position has not changed. Mrs N will have had to pay for tax advice at some time or another regardless of how the pension was accessed.

Friends Life has said it does not believe that the redress payment would be taxable, but that it would reconsider its position if at a later date it can be shown that Mrs N had suffered a tax liability, although it would not agree to an indemnity. This is a reasonable stance for Friends Life to take. Mrs N should establish any resultant tax liability due to the redress and communicate that to Friends Life if necessary.

Looking at the proposed redress methodology, Mrs N may disagree with certain assumptions made by Friends Life, but I consider they are reasonable assumptions. I note in particular that in relation to the personal allowance, under this notional methodology, she is better off for it being included than if Friends Life assumed no personal allowance.

The approach taken to offsetting the notional income tax that Mrs N would have paid had she taken the full fund value as an UFPLS is balanced and appropriate. This places Mrs N broadly in line with the position she would have been had the pension been taken in full under the current rules. I believe that is an appropriate remedy for the error caused by Friends Life.

Therefore, I uphold Mrs N’s complaint.

Directions

Within 28 days of this determination Friends Life should establish the unauthorised member payment tax charge and surcharge less the notional tax liability of £15,294.34 she would have paid had the full pension been taken as an uncrystallised funds and pay this to Mrs N. PO-9935 7 31. Additionally it should pay £1,000 for the significant distress and inconvenience suffered.

Scammers are loathed by victims, regulators, police, ombudsmen and financial services professionals whose professional reputations are compromised by the nefarious practices of the scam merchants. But however damning the hard evidence is about the scams and the various promoters, introducers, advisers, administrators behind them, the scammers still protest their innocence.

Even when there are announcements and articles in the public domain confirming criminal investigations, winding up petitions, arrests, Pensions Ombudsman’s determinations, regulatory intervention and sanctions, the scammers still try to protest that they are innocent and that the damage done to the victims is everybody else’s fault but theirs.

But as soon as I publish something on the Pension Life blog, to inform and warn the public, the scammers’ solicitors swoop like vultures with their cease and desist letters – threatening defamation proceedings. Never mind the £ millions lost to hundreds or even thousands of victims – many of whom are worried sick about losing their pensions; never mind the tax demands which are driving the victims to complete despair and could result in HMRC making them bankrupt; never mind the heart attacks, strokes and other fatal illnesses brought on by stress and sleepless nights. The scammers’ solicitors pull out all the stops – even going so far as to threaten the Pension Life web host and complain to Google about Pension Life’s website blogs.

I’ve been through this with – among others – Stephen Ward of Premier Pension Solutions – who actually took me to court for upsetting his “picky” clients (Ward didn’t even turn up); Paul Baxendale-Walker, the disgraced former barrister (struck off) and porn star; XXXX XXXX of Global Partners Ltd and The Pensions Reporter (now under investigation by the SFO);and now Peter Moat of Fast Pensions (see Sam Brodbeck’s article of 1.7.2017).

In fact all these solicitors – including DWF, Mishcon de Reya, Carter Ruck, Manleys Law, Molins & Silva et al, all bleat that the Pension Life blogs are harming their clients by “causing reputational damage generating huge financial damages and danger of losing business interests and opportunities”. But not so much a squeak about the huge financial damages the scammers they represent cause to the victims who are in danger of losing their homes.

And not a word about the crippling financial damages the scammers they represent cause to the victims who are in danger of losing their homes.

Below is the email exchange between Peter and Sara Moat’s solicitor Monica Caellas and me dated 27th June 2017. Worth noting she has not responded. Perhaps her website, email and telephones have been hit by the same virus as appears to afflict the Moats and Fast Pensions?

Ms. Brooks:

We hereby contact you in name and on behalf of our clients, Ms. Sara Grace Moat and Mr. Peter Daniel Moat, in connection with the statements set forth in the article “Peter Moat and Sara Moat – Fast Pensions” (hereinafter, the “Article”) included in the website https://pension-life.com/peter-moat-sara-moat-fast-pensions/ since May 18, 2017. I am enormously relieved that you have contacted me and would be most grateful if you would be kind enough to act as intermediary in relation to many hundreds of victims who have been scammed out of their pensions. As you can imagine, this is an extremely worrying time for these people and some of them are now receiving tax demands from HMRC as the Moats were operating pension liberation fraud as part of the “package”.

Some of the statements of the Article are extremely serious and could be constitutive of various crimes sanctioned by the Spanish Criminal Code; among them, serious offences of defamations and calumnies. I do not agree that the Moats’ actions include defamation and calumnies – but they certainly involve pension, tax and investment fraud.

FAST PENSIONS is a UK Limited Company licensed by HMRC. No it is not. HMRC do not license companies in the UK. HMRC registers pension schemes, but this implies no approval or license.

Ms. Sara Moat is the sole Director and the sole shareholder of FAST PENSIONS. Her husband, Mr. Peter Moat is the owner and administrator of Blue Property Group, a Group of corporations that has nothing to do with FAST PENSIONS. From a corporate point of view you are correct, however, Peter Moat was the controlling mind behind the company and has been masquerading as “James Porter” in his communications with the victims to attempt to conceal his involvement. Also, I think you will find that Blue Property Group has gone bust and owes money to creditors all over the Costa Blanca.

With the Article you have caused serious confusion against third parties and it is hurting my clients and their companies. I regret that neither the victims nor I will have any sympathy whatsoever with any hurt your clients are experiencing. They have hundreds of victims’ pensions in limbo – and despite numerous Pensions Ombudsman’s determinations, no transfers out (which is a UK citizen’s legal right) have been facilitated. The victims of this scam include several deaths whereby the deceased pension member’s family has not been able to benefit from the pension fund as required by law in the UK.

In particular, the Article expressly and roundly states “There have been a number of Pension Ombudsman determinations which expressed concerns about the maladministration of the unlicensed firm [Fast Pensions] owned by the Moats”. Yes. This is in the public domain on the Pensions Ombudsman’s website.

In this sense, you claimed that a number of very distressed and worried members of the Fast Pensions scheme had contacted you, while those four hundred worried members have not directly contacted FAST PENSIONS itself. I cannot comment on how many worried members have directly contacted Sara and Peter Moat (masquerading as “James Porter”) direct. Many may have attempted to do so but the Moats have made this impossible by disabling their website and emails and not answering their phones. Their claims that the website, email and phone number have all been hit by a “mystery virus” are simply not credible.

As a consequence of the alleged existing claims you contacted Mr. James Porter, the person in charge of leading with any pension queries for Fast Pensions and that has nothing to do with Mr. Moat, despite your suggestions of identifying them as the same person. That is not correct. Peter Moat contacted me, pretending to be “James Porter”.

Anyhow, and after being correctly assisted by Mr. Porter, you claimed that he takes days to respond and you interpreted that as a “deliberate attempt to make it difficult to contact anyone at Fast Pensions”, which is untrue, since all queries have been responded to and dealt with quickly. I am afraid you do not know the facts. Numerous victims have attested to the fact that their desperate pleas to transfer out have been ignored.

If there were clients with concerns they would contact FAST PENSIONS in the First instance to get these resolve. Why don’t you try contacting Fast Pensions and let me know how “fast” they respond? A journalist tried to contact them just now and got this response: Your message wasn’t delivered to james.porter@fastpensions.co.ukbecause the domain fastpensions.co.uk couldn’t be found.

Moreover, in the Article you have made several statements that make Mr. Peter Moat, Ms. Sara Moat, FAST PENSIONS and all of Mr. Peter Moats companies look like a scam. Then I have done my job properly. They are all a scam.

For example, by trying to link Mr. and Ms. Moat as well as FAST PENSIONS to Mr. Sthephen Ward. Also, and more seriously, you stated that you are afraid that the professional environment of Mr. and Ms. Moat “has undeniably got all the hallmarks of a typical, bog standard scam”. And you insisted: “It looks, feels, smells like a scam”. And I stand by all of that. And so does the Pensions Ombudsman.

As a consequence thereof, there are actually a huge number of parties affected by the Article, Peter Moat and his associated companies, Ms. Moat and FAST PENSIONS. The unjustified reputational damage caused by the Article is generating huge financial damages and is putting Mr. Peter Moat and his companies in danger of losing business interests and opportunities. Perhaps you would like to ask some of the victims how they feel about poor Mr. and Mrs. Moat losing business interests and opportunities?

Based on all the foregoing, and without prejudice to the express reservation of legal actions that correspond to my clients, through this communication you are FORMALLY REQUIRED TO IMMEDIATELY REMOVE THE ARTICLE FROM THE WEBSITE AND STOP DISSEMINATING IT THROUGH INTERNET. I will happily reach an agreement with you Monica: you get Sara and Peter Moat to return all the victims’ pensions to them immediately – in full plus interest – and I will remove the article.