In 2018, Old Mutual International (now Utmost International) announced it was suing structured note provider Leonteq. This was over a series of rogue structured notes with an extra layer of secret commission paid to scammers without Utmost International’s knowledge (allegedly). These notes had failed because they were so enormously high risk. The result was thousands of Utmost’s victims losing huge amounts of their pensions and life savings.

On 28th May 2024, it was announced by QROPS trustees and Old Mutual (later renamed Quilter and now owned by Utmost International – formerly Generali) that Leonteq had settled out of court for the damages caused by these toxic structured notes to thousands of investors.

This announcement was reported by Momentum Pensions in Malta – among other QROPS trustees. Some victims of offshore pension scams facilitated by Old Mutual, Generali, Utmost, RL360, SEB and other life offices will get some compensation for a small part of their huge losses.

Old Mutual International, the life office responsible for thousands of ruined lives in Spain and beyond, announced in 2018 that it was suing structured-note provider Leonteq. There had been a series of extra toxic, high-risk notes for which Leonteq had been paying scammers additional commission “under the table” (i.e. not disclosed to Old Mutual). In early 2023 the matter was settled out of court for an undisclosed amount.

But this is no real compensation for the years of distress and poverty the many thousands of Utmost’s victims have gone through. Lives have been ruined. Families torn apart. Homes lost. Victims have died miserable, lonely deaths – leaving distraught and destitute spouses and partners.

It had originally been reported that Old Mutual had been suing Leonteq for somewhere between £94 million and £200 million. The basis for this action was undisclosed commissions – which is fraud. But Utmost (along with all other life offices) had been quite happy to pay millions in undisclosed commissions to the vast array of scammers who sell their offshore bonds and toxic investments (such as structured notes). But while Utmost had no problem with these outrageous commissions being kept secret from the victims, they objected to the Leonteq commissions being hidden from Utmost themselves.

Momentum is taking further advice on the legalities and tax implications of paying this compensation to pension scheme members. Presumably, STM, SEB and other QROPS providers who had facilitated this fraud will be doing likewise.

While this is indeed welcome news for the thousands of pension savers whose lives were ruined by these failed investments, it does leave many unanswered questions:

Why did the life offices such as Utmost give terms of business to the scammers in the first place?

Why didn’t Utmost ensure the scammers disclosed the commissions on the insurance bonds and also on the investments?

Why did Utmost allow retail investors’ money to be invested in professional-investor-only, high-risk investments?

Will Utmost be paying compensation for all the other structured notes which were toxic and which failed?

Utmost’s answer to these questions would, obviously, be: “We didn’t give investment advice”. And this is the excuse they will make when they testify in the Isle of Man court – where Signature Litigation and Forsters are suing them and Friends Provident International for £400 million for this very crime.

Utmost and all the other life offices did not – indeed – give investment advice. However, they did act on the investment instructions (often forged) of unlicensed scammers – and reported on the resulting crippling losses for thousands of policyholders. Despite being fully aware of these losses, Utmost continued accepting investment instructions (often with forged investor signatures) for years – paying the same undisclosed commissions to the same scammers, with the same resulting losses.

In fact, Utmost International continues with this fraud to this very day. And now there is evidence that they are paying even higher undisclosed commissions to the very same scammers who have already ruined so many lives for well over a dozen years.

Utmost had not been the only life office involved in the Leonteq structured note scandal. Friends Provident International, Generali, Investors Trust, Julius Baer, RL360 and SEB had all been similarly culpable. But it looks like Utmost had been the only one to sue Leonteq for this fraud.

And let us be clear, undisclosed commission does constitute fraud – irrespective of whether it is committed by the scammers, Leonteq or Utmost International.

Perhaps the biggest question which remains unanswered is why the regulator – the Isle of Man Financial Services Authority – has done nothing to sanction the likes of Quilter, Utmost, Friends Provident and RL360? The regulator’s Chair – Lillian Boyle – has been in place since 2015 so she must have known perfectly well how much fraud had been facilitated by the life offices.

Boyle had previously been the CEO, Director and Chair of Isle of Man international life companies and their overseas subsidiaries and branches. So she must have had intimate knowledge of how the secret-commission fraud worked. And yet she has stayed silent.

The IoM FSA’s Chief Executive is Bettina Roth. She has worked for the regulator in the Cayman Islands (that well-known jurisdiction for dodgy financial dealings – including the Trafalgar Multi Asset Fund investment scam). And yet she too has stayed silent. Both Boyle and Roth must know that the Isle of Man is under the spotlight with nearly half a billion pounds’ worth of claims against the death offices for fraud (and a billion more in the pipeline).

The IoMFSA’s own website claims it is “responsible for protecting consumers, reducing financial crime and maintaining confidence in the financial services sector through strong prudential supervision”. And yet the very financial crime that Old Mutual and Utmost International have been committing for more than a dozen years – under the very nose of the regulator – is ignored.

It is indeed great news that Leonteq has paid up. But, did that payment include all the extra-commission paid on the toxic structured notes? And any interest, damages and compensation for the losses and the fraud? And what about the other structured note providers whose toxic products caused just as much (and sometimes more) damage to thousands of victims?

Royal Bank of Canada, Nomura and Commerzbank also listed their toxic products on Utmost Internationals’ investment platforms. A multitude of scammers (who had terms of business with the life offices) used these to ruin their low-risk, retail victims. Did any of these big financial institutions care that they were facilitating financial crime on a massive scale – and ruining thousands of lives?

With the IoM regulator silent, this massive international fraud continues to this day. The life offices are still paying the scammers huge undisclosed commissions for both the insurance bonds and the investments listed on their platforms. In fact, the bond commission can be as high as 9% – for a product that nobody needs and which only serves to facilitate fraud against the policyholders.

In 2018, Utmost International commissioned a report on the Leonteq structured note scam from https://www.futurevc.co.uk/ – a consultancy firm which specialised in structured products systems and research analytics. Their Managing Director, T. M. Mortimer, analysed a test sample of 100 notes and reported the below fees and commission figures:

Fee Level

Number of Occurrences

Less than 6%

9

6% – 8%

4

8% – 12%

21

12% – 16%

26

16% – 20%

14

20% – 24%

12

24% – 28%

6

28% or more

8

100

Mortimer concluded: “In my view a total fee of 8% taken between Leonteq and its associates would be reasonable. This corresponds to the entries in the first two rows in the table.”

This means that only 13% were reasonably (i.e. viably) priced. The remaining 87% were vastly overpriced with extortionate commissions paid to the scammers.

The insurance bond scam continues to flourish in all the typical British expat destinations – from Spain and Portugal to Thailand and the Middle East. Life offices such as Utmost International and RL360 continue to fuel the global undisclosed commission fraud machine – with scammers posing as financial advisers and selling over-priced products rather than proper financial advice.

Leonteq is still doing a roaring trade – thanks to the offshore scammers and the life offices. The secret-commission fraud still flourishes unhindered. Utmost International and Friends Provident International are throwing millions at defending the Signature and Forsters actions brought by thousands of victims. The regulators remain silent.

Every day more victims are created. How many more victims need to be ruined before something is done to put a stop to this huge-scale offshore financial crime? Leonteq may have paid up – but now the life offices themselves (including Utmost International, RL360 and SEB) need to pay up too.

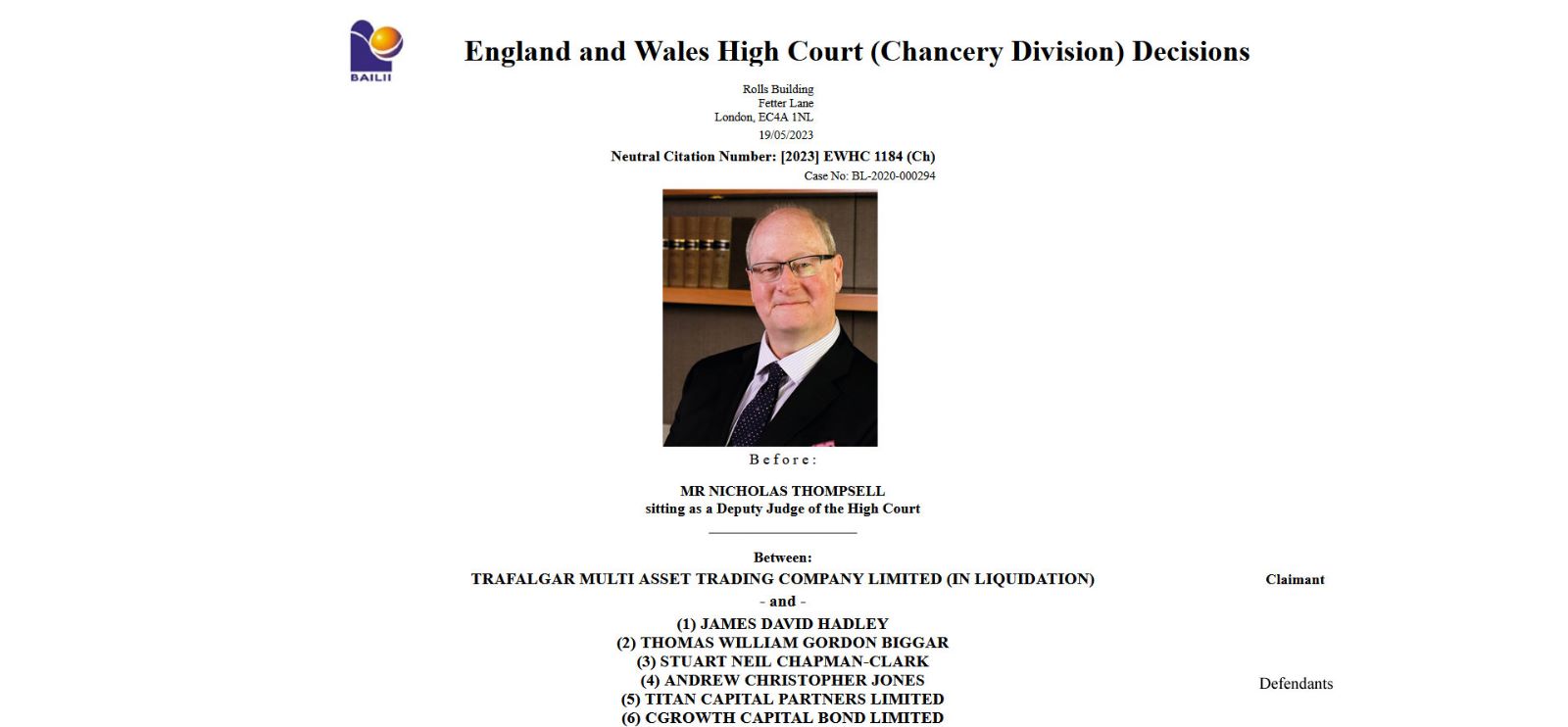

High Court Rules in Trafalgar Multi Asset Fund Case against James Hadley and associates.

In a recent High Court judgment, Judge Mr. Nicholas Thompsell found that the Cayman-Islands based Trafalgar Multi Asset Fund (TMAF) was involved in an illegal conspiracy to “extract commissions from the investments.” The defendants, who were also behind the 2013 Store First pension investment scam, were found guilty of acting together to establish TMAF and deceive investors.

The claimant, Doran & Minehane, the liquidator of TMAF, argued that the investments were uncommercial transactions, potentially fictitious, or involved undisclosed self-dealing benefiting the conspirators. The investments were designed to exploit and misappropriate pension funds for the defendants’ benefit.

The judge determined a deliberate intention to harm TMAF, stating that the arrangements aimed to generate commissions for the conspirators at the fund’s expense. The accused faced a range of serious accusations, including breach of financial services regulation, fiduciary duties, and involvement in unlawful means conspiracy.

The victims, who suffered significant losses due to these schemes, have our sympathy. The court’s judgment establishes solid principles of liability, which may lead to a faster receipt of claimed monies and reduced legal costs for the defendants.

For the full judgment, click here: High Court Rules in Trafalgar Multi Asset Fund Case against James Hadley and associates.

This is a helpful lesson for victims and potential victims of pension and investment scams. The FSCS compensation payments will be funded by levies on the decent, qualified and ethical IFAs who don’t operate scams. Justice and education combined in one bitter pill.

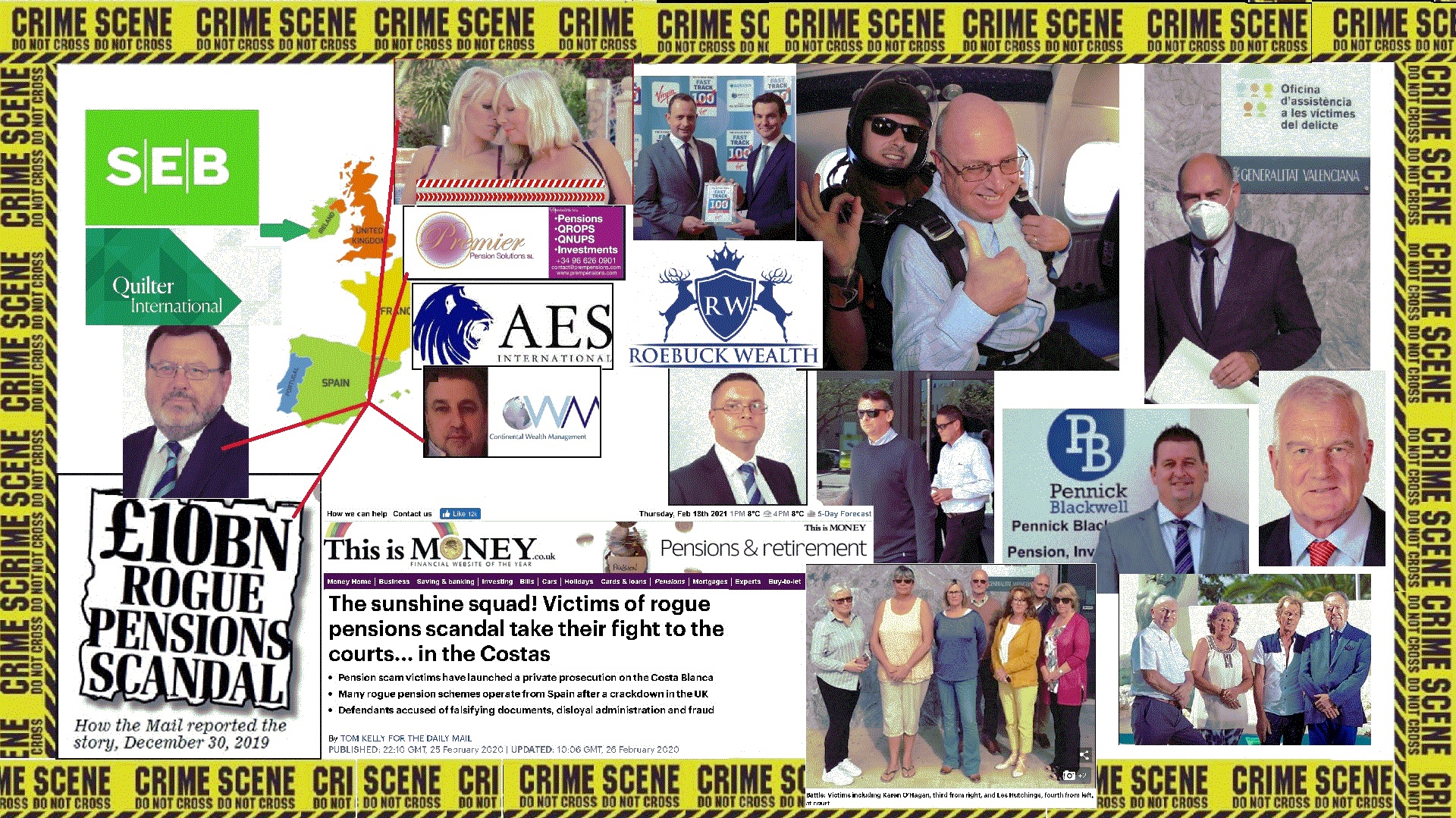

The Spanish criminal trial of so-called “financial advisers” in Denia has exposed the widespread fraud routinely committed in offshore financial services for over a decade.

This particular stage of this particular trial may be directed at just eight members of Continental Wealth Management and Premier Pension Solutions. For now. But the case – brought by Pension Life – needs to be extended to all parties who have committed similar offences in offshore financial services.

Spain is the second-largest expat jurisdiction in the world – after Australia. More than three quarters of a million British expats have settled in the Spanish sunshine. That’s over half the total in the whole of Australia. And these Spanish-resident expats are sitting targets for pension scammers.

It is not unusual for Brits to be suspicious of foreigners in any country. Expats typically veer towards their own countrymen. They are notorious for being suspicious of foreign food and customs. Hence, the depressing fact that it is British scammers who relieve British victims of their pensions and life savings.

And this is why so many British expats – especially in Spain – fall prey to bogus “financial advisers” flogging bogus life assurance policies provided by bogus insurance companies – like Quilter International headed up by Peter Kenny.

The facts of this criminal case are indisputable. One thousand victims were scammed by Continental Wealth Management. Between 2009 and 2017, these victims lost many millions of pounds’ worth of pensions and life savings. And much of this was facilitated by Quilter International (formerly Old Mutual International).

So how were these losses caused? What on earth went wrong? Financial services – in any country – should be a safe industry which investors can rely on. Depend on. Why have so many expats – not just the Continental Wealth Management victims – lost so much money?

Who and what is to blame for the loss of hundreds of millions of pounds?

The short version of the answer is: “COMMISSIONS”. Offshore advisers get rich by selling products for commissions. What they don’t sell is independent financial advice. Proper independent advice (provided by a correctly and properly qualified and licensed adviser) is about recommending an appropriate investment strategy which is in the best interests of the client. And, of course, charging a reasonable and commercially-viable fee for such advice.

But that rarely – if ever – happens in offshore, expat jurisdictions. What is cleverly presented as “advice” is generally just a dishonest ploy to sell a client unsuitable products which they don’t need and that will make the salesman the most commission.

The orchestrators, facilitators and architects of all this fraud are the “life offices”. In practice and in reality, these companies are more about death than life. Their business is about destroying life savings and pensions – while enriching the pockets of fraudsters.

There are various ways to combat this widespread fraud facilitated by the life offices:

Bring criminal proceedings against ALL those who have defrauded their clients – from bogus, unlicensed advisory firms to the life offices themselves

Ensure all so-called advisory firms (sometimes calling themselves “wealth managers”) are correctly licensed in the jurisdiction where they provide advice

Make it mandatory for all advisers to be properly qualified to provide financial advice

Ban all firms without an investment license from providing investment advice

Educate consumers to only use advisory firms which openly disclose their professional indemnity insurance on their website

The bald truth is that if the life offices – such as Quilter International, Friends Provident International and RL360 – were closed down, this widespread fraud would stop.

The only way this fraud keeps going so vigorously and relentlessly, is the terms of business given by the life offices to the scammers. And, of course, the fat commissions the life offices pay to them. As well as the toxic, risky, high-commission-paying investments the life offices put on their “platforms” for the scammers to use (and abuse).

You only have to look at Continental Wealth Management to see how quickly a scamming firm will collapse once life offices withdraw terms of business. The life offices are the life blood of scams and scammers.

Without the facilitation of the “death” offices (Quilter International, Generali, SEB etc.) frauds such as Continental Wealth Management could not have taken place. The blood of all those who have died wretched, lonely deaths – and those who are suicidal – is squarely on the hands of Peter Kenny and his various cronies.

The bank statements of Continental Wealth Management show the repeated amounts of fat commissions paid by Quilter International, Generali and SEB. And these amounts were paid willingly and cheerfully in the full knowledge that every payment meant more lives damaged; more funds destroyed; more miserable deaths.

Quilter and their associates had reported on the victims’ losses for a decade; produced valuations and transaction histories evidencing the repeated, relentless fraud. And yet Quilter (and the other death offices) did nothing – just kept on and on facilitating the same fraud: repeat, repeat, repeat.

While the “advisers” from Continental Wealth Management and Premier Pension Solutions stand trial – the hundreds of victims have to listen to the defendants’ offensive denials and excuses. But, worst of all, the distressed and impoverished victims know that the life (death) offices should also be on trial – standing shoulder to shoulder with the scammers themselves.

The cause of the investment losses in the Continental Wealth Management case was almost exclusively toxic, high-risk (and high-commission) structured notes. These are complex investment instruments called “derivatives” and should only ever be used for professional or sophisticated investors. They are certainly completely unsuitable for ordinary people (who are classed as retail investors) or for pension schemes.

High-risk structured notes are big business for the death offices. Quilter International (formerly Old Mutual International) has historically onboarded over 100 new structured products per month. In the case of the Continental Wealth Management fraud, it was the structured notes – from Leonteq, Commerzbank, Royal Bank of Canada and Nomura – which caused the terrible investment losses. These toxic, high-commission investment products – so beloved by the scammers because of the high commissions – were responsible for the destruction of millions of pounds’ worth of pensions and life savings.

Quilter International knew perfectly well that these toxic products – totally unsuitable for retail investors – paid 8% commission to the scammers and a further 8% to 10% to the “arrangers”. They knew perfectly well – and admitted internally to their “asset review committee” – that these products were risky and “not good value”. But they still allowed the scammers (to whom they gave terms of business) to keep selling them.

Quilter has also admitted that they had 2,047 structured products in total, and that the average holding per product was £243,654.03; that the smallest holding was £67.54 and the largest holding was £5,350,833.60. Quilter was concerned that there was a reputational risk to Quilter for allowing these structured products to be held within their offshore bonds. They also acknowledged that these products carried excessive commissions and were causing “suboptimal customer outcomes”. However, their concern for their own “reputational risk” did not extend to concern for their victims.

Quilter has tried to wriggle out of culpability for the victims’ losses by claiming that investment product “suitability” is the responsibility of advisers. And that these so-called advisers are participating in a “race to the bottom”.

However, the advisers are mostly scammers to whom Quilter has cheerfully given terms of business. And they are winning the race to the bottom by several lengths. If Quilter withdrew terms of business from all the scammers, the race wouldn’t even take place at all. In fact, all Quilter would have to do would be to ensure that all advisers are qualified and licensed – and that investors’ risk profiles are correctly respected – and the fraud would stop instantly.

But until Quilter and all the other death offices are put on trial for fraud themselves, this crime is going to continue. And victims are going to keep losing their pensions and life savings – and dying in abject poverty.

As an interesting post script, Quilter have posted a warning about scams on the internet. Their disingenuous claim that “Your security is our priority, so we have reacted quickly to help you and the financial advisers we work with to spot fraudsters” is ironic and cynical. Quilter themselves routinely work with fraudsters who pose as financial advisers – and who have no license or qualifications to provide financial advice.

January 28/29 2021 saw the cross examination of Stephen Ward in Pension Life’s criminal case in the Denia court. Ward gave the judge an elaborate explanation as to how and why none of the Continental Wealth Management pension and investment scams were his fault.

Ward provided the pension transfer “advice” to hundreds of Continental Wealth Management victims – facilitating the handing over of millions of pounds’ worth of personal and occupational pensions into the hands of well-known, firmly-established scammers. Once out of the relative safety of the UK, and into the offshore abyss, the scammers made millions out of undisclosed commissions on the victims’ life savings. The investments were, of course, largely worthless. Victims lost somewhere between a small percentage and a large percentage – with a few losing 100%. And a few more even going overdrawn on their pension accounts.

Ward’s Spanish firm Premier Pension Solutions, worked as “sister company” to Darren Kirby’s and Jody Smart’s Continental Wealth Management. After Ark in 2011, Ward moved straight onto the Evergreen New Zealand QROPS liberation scam. And CWM did the cold calling to sign up 300 victims to the toxic £10 million pension scam and so-called “loans” from Ward’s own finance company – Marazion.

Ark (and indeed Evergreen) victims may well want an answer to the question: why hasn’t Ward been prosecuted before now? The lack of any previous criminal proceedings against him, for the many other scams he was involved in, is – indeed – astonishing.

Capita Oak, Westminster, Southlands, Headforte, London Quantum et al – could all have been prevented had Ward been behind bars. Victims of all of those scams might still have their pensions had it not been for Ward.

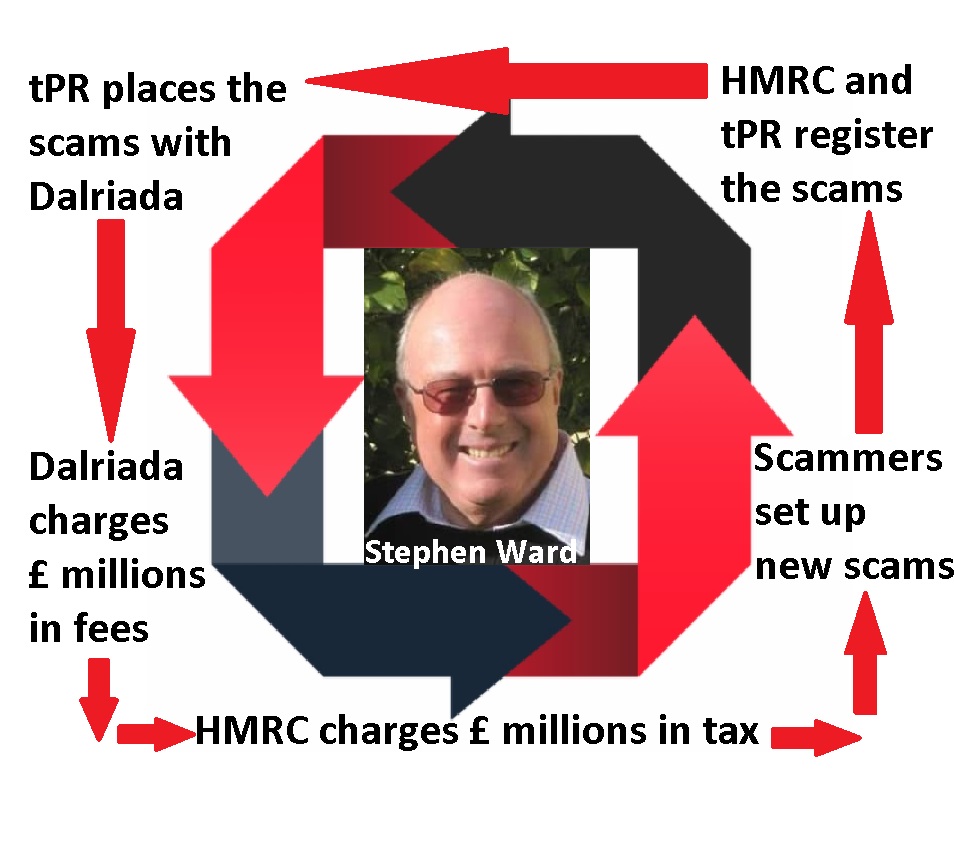

Part of the answer may lie with Dalriada Trustees. The firm was appointed by the Pensions Regulator to the Ark schemes as independent trustee on 31st May 2011. Over £27 million worth of pensions had been transferred from safe, professionally-run pension schemes into the six Ark schemes. Nearly 500 people are affected – many of whom had received reciprocal “loans” on the advice of Stephen Ward and his very convincing associates. Ward had assured all the victims that the loans would be “tax free”. But, of course, HMRC does not share that view – and the tax trial is starting in March 2021.

HMRC is looking to tax all those who did get “loans” and also all those who didn’t. HMRC’s argument is firstly that even if members didn’t get a loan, they had made the transfer with the intention of getting a loan, and secondly that they “made” a loan.

One of the first questions I ever asked Dalriada back in 2013 (appointed by the Pensions Regulator – who registered the Ark schemes in the first place) was:

“Why didn’t you bring criminal proceedings against Stephen Ward and all the other scammers who set up and ran Ark?”

Dalriada’s answer was:

“We didn’t think it was within our remit”.

So what is (or was) Dalriada’s remit? And has it fulfilled that remit? And how much has it cost?

DALRIADA’S REMIT:

To suspend the Ark schemes so that no further “loans” could be made; no further victims lost their pensions; no further toxic investments could be made

To investigate the schemes to find out how they had been run and where the money had gone

To recover the toxic investments and return the money to the schemes

To liaise with the members and keep them informed

To liaise with HMRC on the unauthorised payment tax liabilities

The above points are all guesses on my part. Certainly, Dalriada has admitted that they didn’t really know where to start at the beginning. They had no idea what they would find, once they started investigating, and no clue as to how much work was going to be involved.

Dalriada has, indeed, recovered some of the toxic investments in the Ark schemes. But communications with the members have been limp at best. Dalriada has spent a lot of time, effort and money on taking proceedings against the victims themselves to recover the “loans”, but seems to have spent zero time, effort or money on pursuing the scammers.

Most important of all, Dalriada has not invested any of the money left in the Ark schemes – so members (victims) have missed out on the longest investment bull run in history. Bottom line: there’s been no growth in the value of the Ark funds – only shrinkage. Had the funds been invested in something as simple as a low-cost tracker fund, they could have grown by some 330% at least.

Of the original £27 million in the Ark schemes, Dalriada has spent more than £7.4 million on trustees’ and lawyers’ fees between 31st May 2011 and 31st May 2020. But isn’t it reasonable to ask: “Why couldn’t Dalriada have spent some of that money on criminal proceedings against Stephen Ward and some (or all) of the other scammers?”

Dalriada Trustees have been appointed to more than 100 pension scams in the past ten years (by the Pensions Regulator). But there is no evidence that any of the scammers – especially the prolific Stephen Ward – have ever had any CRIMINAL action taken against them by Dalriada in an effort to prevent further scams.

Kelly reports that “Pension scam victims have lost millions of pounds more to the government-appointed trustees hired to get their money back.” and that “Victims say Dalriada Trustees ‘inexplicably’ held their recovered retirement savings for years and then only paid a fraction of their money back.”

Kelly has been to meet me in Spain several times. He attended the Denia court for the first set of cross examinations in 2020, and reports that “tens of thousands of savers had lost up to £10 billion in rogue schemes that looked safe because they were registered by HMRC and overseen by the Pensions Regulator”.

Kelly goes on to cite the case of one victim who waited seven years to have his £157,000 pension pot returned to him by Dalriada. But they deducted £90,000 in charges before handing it back to him. And this was after Dalriada had rescued the fund in full, before the scammers had managed to invest the money in toxic, commission-paying assets.

With 5,400 pension scam victims having Dalriada as their trustees, it is perhaps time to ask whether this is a tenable solution. Scammers could, realistically, be forgiven for thinking that once Dalriada takes charge, this is merely a license for the next scam, and the next one, and the next one…… Because, Dalriada is never going to report the scammers for fraud. So they are free to keep on scamming people out of their pensions repeatedly.

One of my all-time favourite comedy lines is Greg Davies describing his middle-aged love life as “like trying to stuff a marshmallow up a cat’s arse”. My second-favourite comedy line is “Andrew Bailey has been such a failure at the FCA, that we’re going to put him in charge of the Bank of England”. My third favourite is “the FCA’s practitioner panel is going to be headed up by Paul Feeney of Quilter”.

With the exception of Greg Davies’ somewhat risqué pun, the other two are both true and sickeningly serious.

Victims of Quilter (previously Old Mutual International and Skandia) will be appalled that such a pariah of financial services can be held up to be an example to financial services practitioners.

It might, of course, be that I am mistaken – and that Feeney is being brought in as an example of how financial services should NOT be run, and how financial advice should NOT be provided.

But, sadly, I think the “old boys’ network” has worked its magic and the FCA elite have closed ranks with Quilter’s elite, to dominate control over pension and investment scams. It is clear that neither the so-called “City Watchdog” nor the insurance giant – specialising in pointless insurance bonds and toxic investments – want to see financial services cleaned up.

If any financial services consumer is unclear about the FCA’s multiple failures in the matter of the collapsed London Capital & Finance “bond”, they only need to read Bond Review’s piece on the Dame Gloster report. Along with “The FCA told potential investors that LCF was not a fraud, and FSCS protected“, “the FCA took no follow-up action to verify that all LCF’s investors qualified as high-net-worth and sophisticated” and “The FCA consistently treated LCF’s unregulated bonds as not its problem“, Dame Gloster pulls no punches when she outlines the FCA’s many disgraceful and negligent failures.

From Andrew Bailey at the top, to the members of FCA staff who defecated on the men’s bathroom floor at the bottom, Dame Gloster’s report demonstrates that the FCA simply doesn’t understand pension and investment scams. Apparently, an FCA supervisor had admitted that “there is little training on how to identify financial crime within the FCA’s Supervision division”.

Put simply, if the FCA can’t keep its own bathrooms clean, how on earth can it help clean up the crap in the world of financial fraud?

The FCA clearly does not understand that unregulated, high-risk, toxic investments are simply not suitable for ordinary retail investors. And this is why the appointment of Quilter’s Paul Feeney is so anomalous: Quilter has for years specialised in peddling these kinds of high-risk investments to low-risk investors. The graveyards of thousands of Quilter victims’ investment portfolios is littered with the rotting remains of many funds and structured notes.

A regulator’s “Practitioner’s Panel” should ideally be headed up by someone who understands how financial services firms should be run; someone who eschews the fraudulent and disloyal practices of the “cowboys” and “chiringuitos”; someone who has shown the will to outlaw illegally-sold insurance bonds whose sole purpose is to make thousands of victims poor and dozens of scammers rich.

Instead, the FCA’s panel is going to be under the control of someone who has actively promoted high-risk investments to low-risk investors.

So, it would seem there is no hope that the FCA will ever be reformed – just as there is no hope that the top dogs at Quilter will ever brought to justice for facilitating so much financial crime. The two rogue organisations are going to jog along cosily, side by side, with no remorse for their own failures and culpability.

It is hard for pension and investment scam victims to comprehend the apathy towards reform of regulation in the UK. Experts such as Henry Tapper, Mick McAteer, Martin Hague, Paul Carlier and Gina Miller have long banged the “reform” drum. But this has largely fallen on deaf ears. And, of course, Dame Gloster’s report will be largely ignored.

This is all cronyism at its worst. And shows that neither the Treasury nor Parliament truly understand what is so very wrong with financial services in the UK (and also offshore). Select Committees, such as the Work and Pensions one chaired by Stephen Timms, can debate all day long – but until the FCA is scrapped and rogue “wealth” and “life” (in reality, poverty and death) companies like Quilter are shut down, nothing will change.

Dame Gloster has written about the “wickedness” of the FCA’s failures to protect the public (from investment scams such as London Capital & Finance). Part of this evil is the failure to recognise the dangers of unlicensed scammers – the motley assortment of unlicensed “introducers” – both onshore and offshore. But, of course, this is what Quilter’s business is based on – so the appointment of Quilter’s Paul Feeney will only protect and nurture this branch of financial crime.

Quilter has for many years given terms of business to assorted scammers, prostitutes, murderers, fraudsters and conmen (and women). With the acceptance of thousands of investment instructions from these unruly hordes of low-life, unlicensed, unqualified criminals, Quilter has built up a successful and profitable business based on ruining innocent victims’ lives (and killing some of them in the process).

Dame Gloster’s excellent, comprehensive and severely damning report provides almost 500 pages of details of the FCA’s disgraceful failings.

But if you haven’t got time to read it, just read FT Adviser’s one-page article on “Quilter boss Feeney to head up FCA panel”. Then zoom down to the bit that says: “Paul has served on the panel for a number of years and appreciates the important role it plays in ensuring our regulation is targeted and effective.”

Then go and have a good cry. And a packet of marshmallows.

In the past decade, millions of pounds of pensions and life savings have been destroyed in Spain. Much of this has involved insurance bonds (OMI, SEB and Generali) – as well as all other popular expat countries. Only by benefitting from lessons learned so painfully by those who’ve already been scammed, can new potential victims arm themselves against the scammers.

Pension scams always start with a so-called “financial adviser” or “wealth manager” or “retirement consultant”. Sadly, it is almost always British “advisers” which scam British expats.

Potential victims need to understand what to look out for – and avoid. Here are the essential “must haves” for proper, professional financial advisers (in other words people who sell advice, not products):

LICENCE – The firm must be licensed – both for insurance and for investment.

QUALIFICATIONS – The adviser must be qualified – and a link to proof of the qualification clearly visible on the firm’s website.

LEGACY – There must be no legacy of previous scamming within the firm.

INSURANCE – There must be a professional indemnity insurance policy in place.

NETWORK – If the firm is an agent of a network, there must be an up to date copy of the agency agreement freely available.

INSURANCE BONDS – The firm must not sell insurance bonds illegally.

UNREGULATED FUNDS AND STRUCTURED NOTES – The firm must not invest clients’ funds in unregulated or esoteric funds, or structured notes.

COMPLIANCE – There must be a proper compliance function in place.

MANAGEMENT AND TEAM – All members of the team must be clearly visible on the website – along with details of who is in charge and responsible for the firm’s activities and compliance.

COMMISSION POLICY – The firm’s policy on undisclosed commissions must be clearly visible.

When I Googled the term: “Financial Adviser Spain” just now, the top results that came up for me were:

Blacktower Wealth Management

Blevins Franks

Finance Spain – Patrick Macdonald

Spectrum IFA

Chorus Financial

Abbey Wealth

Alexander Peter

Axis Consultants

Logic Financial Consultants

Harrison Brook

Seagate Wealth

When I changed the search term to: “Pension Advisor Spain” or “Wealth Advisor Spain” I also got the following:

deVere Spain

Mathstone Financial Management

Pennick Blackwell

SJB Global

United Advisers Group

Indalo Partners

Trafalgar-International

Fiduciary Wealth Management

And one firm which won’t come up at all, no matter how hard you search, is:

Roebuck Wealth – run by Paul Clarke

Plus one which only comes up if you know what to search for:

So let’s take a look at some of these firms to see what we can learn from their websites and see if there are any warning signs for potential victims:

Blacktower Wealth Management – Always look at the bottom of a firm’s website to read the small print and see how the firm is licensed. Blacktower is licensed by the Gibraltar Financial services Commission for both insurance mediation and investment advice. Why Gibraltar? Why not Spain? Gibraltar has a long history of facilitating and licensing scams and scammers and the Commission even employs one itself. The website claims to have “Consultants throughout our offices in Europe” – and this worries me. What is a “consultant”? Why not talk about advice, not consultancy?

Looking at the directors and “international financial advisers” of the firm, there are quite a few. Associate Director Tim Govaerts claims to be qualified with the Chartered Institute of Insurers up to Level 3. But the CII register says they’ve never heard of him. Richard Mills claims to be qualified with both the CII and the CISI, but both registers say they’ve never heard of him. Quentin Sellar claims to be qualified with both the CII and the CISI, but only the latter has heard of him. Clifford Knezovich also claims to be qualified with the CISI but does not appear on the register. Lucia Melgarejo is another member of the team who also claims to be qualified. I met her a few years ago, when a colleague of hers had cold called me, and she told me that she was too busy selling to get qualified.

The member of the Blacktower team which worries me the most is Terry Tunmore – as he was one of the scammers at Stephen Ward’s Premier Pension Solutions. Tunmore certainly soils the reputation of this firm, and should not be employed by any firm holding itself out to be professional and to have integrity.

Under the Licensing section of the website, the firm is immediately getting potential clients warmed up to insurance bonds and “wrappers” – and states that it has permission to recommend them and provide investment advice on the underlying portfolios. This should worry any potential client – and ring loud alarm bells – as this indicates a clear intention to use bond providers such as Quilter, SEB, Generali or RL360 – and earn hidden commissions. These products are deemed to be invalid under Spanish law, and are routinely sold illegally in Spain.

Blacktower’s website makes no mention (that I can find) of compliance or their professional indemnity insurance policy. It also worries me that Blacktower has so many “agents” – and without hard evidence of a robust compliance function, I think there is a risk that some of these agents could well be acting as unsupervised “feral” salesmen, rather than bona fide financial advisers.

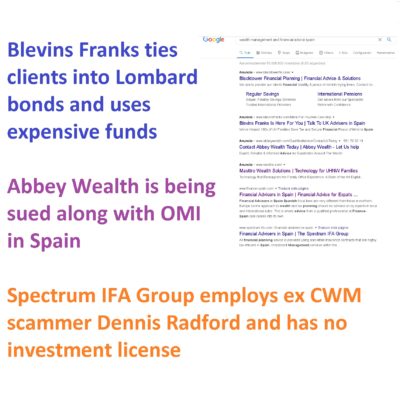

Blevins Franks – Well-known firm with offices in Spain, and other European countries. The team in Spain all have titles such as Partner, Private Client Manager or Regional Manager – and there is no mention of any of them being genuine financial advisers. In Spain, Partners Christopher McCann, Brett Hanson, Paul Montague, Andrew Southgate, Henry Rutherford and David Bowern all claim to be qualified with the London Institute of Banking & Finance, but none of them appears on the member register. Steven Langford claims to be CII qualified but does not appear on the register. With so many members of the team claiming – falsely – to be qualified, this should ring loud alarm bells with any potential victims. We know that Blevins Franks routinely puts all clients into a Lombard insurance bond – which means they are committing a criminal offence in Spain.

Insurance bonds are illegal and invalid for the purpose of holding investments in Spain, and the usual manner of selling them is also a criminal offence. An insurance bond provides no benefits or protection for investors – and should never ever be used inside a pension (QROPS). Blevins Franks also has a close tie with Russell funds – and routinely invests their clients’ funds in Russell. There’s nothing bad about Russell – but there’s nothing good about them either. A portfolio should always be a well-spread mixture of funds from the whole market – not a narrow selection of investments from one provider. I can’t see any information on the Blevins Franks website about their professional indemnity insurance, compliance or commission policy. All in all, I think there are too many risks with this firm and it should be avoided.

Finance Spain – Patrick Macdonald – This firm comes high up the Google rankings, so obviously spends a lot of money on SEO and/or Google Ads. The “Regulation” bit on the website states the firm is “part of a group who are regulated by the Financial Services Commission in Gibraltar”. But which “group” is it talking about? There’s a link to the GFSC website, but no evidence as to how the firm is licensed. The website also claims to consist of “qualified and regulated international wealth managers and members of the Chartered Institute for securities and Investment (CISI) in the UK”. But who are these so-called wealth managers? The only one named on the website is Patrick Macdonald – and the CISI register shows him as being employed by Blacktower. But the firm Finance Spain does not appear on the GFSC register as being one of Blacktower’s agents – so how is this firm licensed?

What worries me most about this website is that it is openly flogging insurance bonds. It promotes “Spanish Portfolio Bonds” – which are routinely sold illegally by the scammers. It claims these bonds are a “tax beneficial home for investments”. But that isn’t true in Spain, as the so-called tax benefits only work for UK residents. In the “Wealth” section of the website, you are met with a brazen offer of insurance bonds from Prudential, Old Mutual and SEB. The section on pension transfers is also very worrying as it gives misleading comparisons between UK pension providers and EU-based QROPS providers; it fails to provide warnings against transferring final salary pensions and – worst of all – states “There is greater investment choice”. This so-called choice is what so many scammers in Spain (in the past ten years) have used to destroy victims’ pensions with high-risk, high-commission, unregulated investments such as structured notes.

Ironically, the Finance Spain website has a section called “Top 5 Warnings” about pension scams. It recognises that the industry is rife with scammers and warns about cold calling, cashing in pensions, pension reviews and the promise of high returns. But it ignores the fact that Finance Spain is itself heavily promoting insurance bonds – which have been the biggest single cause of pension scams in Spain in the past decade. With no clear information about licensing, compliance, insurance or commission policy – and no idea who the firm is or by whom it is managed – I think it is safe to say this is one to avoid.

Spectrum IFA – Oh dear, where to begin! There are so many alarm bells here, it’s like being inside a busy fire station. No investment license, but openly giving investment advice, and flogging insurance bonds: “efficient investing (using Insurance wrappers”. And that’s just the home page. The website openly boasts: “Our internationally qualified, professional advisers make certain you receive the best possible advice for the following areas: Investment Advice in Spain – Pension planning in Spain. That’s a bold claim to make for a firm with no investment license.

The website goes on to boast: “All our advisers live in Spain, are experienced and qualified.” But who are they? What are their qualifications? One “financial adviser” is Dennis Radford who claims to be qualified with the CISI – but does not appear on the register. Aside from lying about his qualifications, he is one of the former Continental Wealth Management scammers responsible for defrauding many victims out of their pensions and life savings. I have brought this to Spectrum’s attention before, but they obviously don’t care – as Radford brings in a lot of business and commission (on illegally-sold insurance bonds and high-risk, inappropriate investments).

There is one adviser who is qualified with the CII – John Hayward. I believe he is a decent bloke – so what on earth he is doing with Spectrum is beyond me. Spain may be full of inadequately licensed firms which do nothing but flog insurance bonds to victims who don’t need them and can’t afford them, but there are some (admittedly not many) decent firms he could join.

Abbey Wealth – This firm has been around a long time – flogging insurance bonds to unsuspecting victims. The firm was an agent of well-known scammers Inter Alliance – the “network” of which Continental Wealth Management was also a member. Abbey Wealth is now licensed by the Central Bank of Ireland. If you’ve ever wondered why so many firms like Ireland, it’s because regulation there is as flaccid as a marshmallow. Another reason why Quilter International is so active there with its insurance bonds – so beloved of so many pension scammers. Abbey boasts a flock of “advisers” who claim to be passionate about financial services – including Ben Noifield who states he is CII qualified (the CII register says otherwise). The rest of the sorry team are an assortment of unqualified salesmen masquerading as advisers.

No mention of professional indemnity insurance, and no reference to their murky past as part of the Inter Alliance shambles.

Alexander Peter – No information about if or how the firm is licensed; who the advisers are and whether they are qualified; who is in charge, what professional indemnity insurance they hold.

Harrison Brook – This firm claims to be a member of the Nexus Global network. But there is no access to the agency agreement and no link to any professional indemnity insurance details or information about who is in charge and who the “advisers” are (and whether any of them are qualified). The question also has to be asked: why don’t firms get their own license rather than joining a network? Ding dong!

Seagate Wealth – No information about how (or if) this firm is licensed. It states on the website: “We work in conjunction with fully regulated and authorised companies”. So presumably that’s an admittance that they are not regulated or authorised. There’s no information about who controls and is responsible for the firm, and nothing to state how any of the team members are qualified. Perhaps one of the biggest alarm bells about this lot is that they are mostly ex AES International and stole the Spanish client book back in 2015.

The recent awards given to Quilter Cheviot and Quilter International by International Adviser (sponsored by Quilter) must have sickened and disgusted many Quilter (OMI/Skandia) victims. Editor Kirsten Hastings’ saccharine and gushing words of praise will have been seen as offensive in the extreme by the thousands of victims who have lost their pensions and life savings in Quilter International death bonds.

While there were, indeed, some very decent firms given well-deserved awards for excellent service and innovation, the prizes handed out to the sponsors of the event were just plain wrong. International Adviser Editor Kirsten Hastings should hang her head in profound shame. She knows full well how many people have been ruined by Quilter. She knows Quilter’s victims are dying – and some have died. She is fully aware that many more are contemplating suicide and that most are facing a bleak Christmas and poverty for the rest of their lives. And yet she can still publicly praise a company which she is fully aware has facilitated investment fraud on a massive scale; congratulate them warmly, and smile broadly while cocking a coquettish nod at the distraught victims as she played canned applause.

I’m going to add an award which was conspicuous by its absence; an award for a brave and determined woman who stood up in the flaccid jurisdiction of Guernsey to a negligent pension trustee: FNB International. Home to many scams and scammers, Guernsey had for many years hosted pension scams – until eventually de-listed by HMRC. A well-known tax haven, Guernsey does have an ombudsman for financial services (albeit a weak and ineffective one) – but he refuses to hear any complaints about matters relating to the height of Guernsey’s disgraceful past.

The heroine so who richly deserves a medal is Manita Khuller – victim of Quilter International, FNB International Trustees and Professional Portfolio International. Between them, these three negligent and culpable parties conspired to cause the destruction of her two final salary pensions worth £330,000 ($430,921/€386,574). The Guernsey Court denied Ms Khuller’s original claim for restitution – and, at first, all seemed lost and it looked like the scammers were going to get away with it. But, unprepared to go down without a fight, Khuller sought an appeal based on the gross negligence of the unregulated adviser – Professional Portfolio International, which FNB had used while she was living in Thailand.

Roger Berry of Concept Trustees in Guernsey, commented on this: “The trustee sought to show that they could rely on the delegation to the adviser/manager to remove or qualify its duties as trustee and in any event, to be liable, the trustees had to be shown to have acted with gross negligence.”

Mr. Berry spoke from significant first-hand experience – as he himself had been accepting investment instructions from AES International’s Stephen Ward (of Premier Pension Solutions in Spain) in the high-risk and toxic EEA Life Settlements fund as far back as 2010. So, he knows all about the catastrophic consequences of accepting business from known serial scammers into obviously unsuitable investments. Berry is also familiar with the art of gross and grotesque negligence.

How she lost two guaranteed DB pensions with strong employer covenants

Why PPI continues to operate throughout Asia under MD Eric Jordan

Why Old Mutual and Skandia (now Quilter International) have yet again been found wrapping dodgy investments

How a South African and now UK bank is owning a Guernsey Trust in the first place

What Geoff Gavey, Alan Glen and co were doing at FNB international to claim “trusteeship”.

Perhaps, in years to come, people in the financial industry will discuss in hushed tones the epic and cautionary tale of Manita vs. Quilter.

But What has Quilter got to do with a Guernsey-based pension trustee who accepted unregulated investment advice into toxic, high-risk, unregulated funds – LM and Mansion Student Accommodation?”

The answer is, of course, EVERYTHING. A Quilter insurance bond should never have been used in a QROPS at all in the first place – and was only there in order to provide scammers posing as independent financial advisers with hefty, undisclosed commissions.

This case was about FNB International, the guilty QROPS trustee who facilitated this scam. But, of course, this firm did not act alone. As in all the thousands of similar cases, the main protagonists started with the rogue advisory firm and ended with the rogue life (or, rather, death) office – in this case Quilter International. But similar cases involving this type of pension investment fraud involve SEB, Generali, FPI and RL360.

Manita Khuller was advised to transfer her defined-benefit pensions by Professional Portfolio International, an unlicensed advisory firm based in Bangkok – where she was living at the time – into the Plaiderie QROPS. Of course, the reality was that her pensions should never have been transferred at all and would have been much better left where they were – safe in the hands of professionals and far away from the grubby paws of unlicensed scammers posing as financial advisers.

Then, going down the well-trodden path of traditional pension and investment scams, PPI put their victim’s fund into a death bond for their undisclosed 7% or 8% commission, and then invested it entirely in high-risk, toxic, unregulated funds for further huge, undisclosed commissions. None of these three phases of the scam should ever happened: not the transfer out of her final salary pension scheme; not the purchase of the unnecessary, inflexible and expensive death bond; not the risky, inappropriate investments. But Quilter International facilitated it all – rewarding the scammers at PPI handsomely (as they do with so many unregulated scammers across the globe).

Professional Portfolio International – run by Eric Jordan and Colin Bloodworth – claim, on their website, to: “strive to help each client grow, protect and enjoy their wealth”. But this, of course, is completely untrue. If they had their clients’ interests at heart, they wouldn’t have put Manita Khuller into a Quilter International bond in the first place; and they wouldn’t have invested her precious pension in high risk toxic crap in the second place. Their only motivation was, of course, their own fat commissions.

Jordan and Bloodworth claim to have a “very knowledgeable and suitably qualified team of experienced advisers”. But this is clearly untrue – as any qualified adviser would know that an insurance bond serves no purpose inside a pension wrapper and wouldn’t be seen dead advising a valued client to invest in worthless rubbish such as LM and Mansion.

Jordan and Bloodworth’s website goes on to boast that “PPI is able to deliver the highest level of progressive financial planning and wealth management services”. And yet, it is clear this is not only a black lie, but that “planning and service” are the furthest things from their minds. The only things they care about, obviously, are fat commissions and conning victims like Manita Khuller out of their pensions and life savings.

So, Manita Khuller was failed and scammed by three parties:

Rogue advisory firm Professional Portfolio International in Bangkok – run by Eric Jordan in Thailand and Colin Bloodworth in Indonesia

Rogue QROPS trustee FNB International in Guernsey

Rogue death office Quilter International (previously Old Mutual International/Royal Skandia)

Manita Khuller – like thousands of other victims of Quilter International, QROPS trustees and unlicensed advisers – was a low-risk, retail investor – as is anyone investing a pension fund. But more than half of her pension – around £170,000 – was put into LM Managed Performance Fund, run by Australian-based LM Investment Management. This company is now in administration. Another big chunk was put into the Mansion Student Accommodation Fund which is now in liquidation.

Almost a third of her money had been invested in the Mansion Student Accommodation fund, and due to the fund’s liquidation her money had been frozen without her being able to access it at all. Speaking to This is Money, Manita commented:

And that, in a nutshell, is the crux of the situation. Quilter are far too willing to give terms of business to unlicensed scammers – with no relevant qualifications or regulations in place to ensure their professional obligations are not compromised by greed, lies and disloyalty. Quilter have been doing this for years now – and have made a fortune out of the sales of their expensive, unnecessary death bonds. They have perpetuated the myth for years that firms with only an insurance license (or even no license at all) can “advise” on investments as long as they flog their victims a death bond and then “pick” from the toxic investments on the death bond provider’s platform – obviously always choosing the investments that pay them the highest commissions (like LM and Mansion).

So here is the award that Kirsten Hastings of International Adviser should have given:

INTERNATIONAL CHALLENGER OF PENSION SCAMS

(especially those facilitated by Quilter International)

Recent data obtained by Quilter (formerly Old Mutual International and Royal Skandia) under a freedom of information request has further highlighted the issue of financial education, or rather the lack of it, with many casualties of fraud ‘unaware they may have fallen victim‘ to such a scheme.

The time has come to call out the thieves in their midst!

Scams, and the lack of an active regulator in place to ensure their non-proliferation, undermine the reputation of the industry itself – and of any decent advisers out there.

The supposed altruism behind the actions of Quilter, who have seen the story of their plucky attempt at standing up for the little guy circulated by almost every major financial publication available in the UK, and by a fair few online and overseas English-language webpages/articles besides, is questionable at the very best – and a downright attempt at pulling the famous ‘Kansas City Shuffle‘ (when everybody looks right, you go left) at worst. I would like to use this opportunity to call “bull-“, as I believe I have heard my American friends say when faced with a claim that is clearly one of the more than 50 shades of bovine excrement currently available from all major stockers of the substance.

Quilter has, in the past ten years, facilitated hundreds of millions of pounds’ worth of pension scams with their “fertilizer”-based products.

It seems that almost every shady offshore firm has been taking advantage of Quilter and other life offices just like them being asleep at the wheel, with hordes of unlicensed investment firms popping up with increasing frequency and success in virtually every expat jurisdiction (especially Spain: e.g. Darren Kirby and Jody Smart at Continental Wealth Management).

Quilter are (at least partially) to blame. The well-known asset management company’s lack of responsibility when it comes to selling inappropriate products to any suitor who comes a-calling is – at this point – bordering on criminal negligence. (And that’s if you remove the border…)

Quilter are fully aware that the statistics they’ve obtained (£30,857,329lost to UK pension scams since 2017) are downright misleading. They fall woefully short of demonstrating even the losses incurred by their own (Quilter’s) facilitation of financial crime in recent years generally – and the last three years particularly.

Yet when it comes to financial fraud and investment scams (particularly those that involve unsuspecting clients’ pension pots), there is almost no pre-emptive warning given to the public, except for massively underestimated figures produced by the very people who have been clearing the way for the scammers from day one. And by that, I do – of course – mean the life offices (like Quilter/OMI) themselves.

“Pension scams and other investment frauds are extremely complex, they can span multiple jurisdictions, and can often go uncovered for years before the victim realises their money is gone. This all makes investigating the scams incredibly time-consuming and expensive, which is why the police have to prioritise those few cases where they have a chance of success.

“The government has a perfect opportunity to bring the regulation into the 21st century by including financial harms within scope of the forthcoming Online Harms Bill. This will mean that, for the first time, search engines and social media platforms will be bound by a statutory duty of care to tackle harm caused as a result of content or activity on their services.”

As you can see Mr. Greer, and by association Quilter, talk a good fight and hit on almost every relevant point a consumer would want to hear from a company of their standing and stature within the financial industry; projecting themselves as a shining light – pouring their beacon out over the surrounding landscape and frightening any existing/would-be scammers out from their hiding places, while at the same time calling on the government for harsher penalties and swifter action to be taken (measures which Quilter themselves, and companies just like them, have blocked on numerous occasions).

And all this “bright light-shining” has served its purpose: leaving regulators, government and public alike too dazzled to notice the wrongdoing going on behind the source of the so-called light and within Quilter‘s very own doorstep!”

The grim reality is substantially different from the one that Quilter aim to project for themselves. That being said, it makes my reply to J. Greer’s well put comments even easier:

“Actions speak louder than words, and all we’re hearing is a deafening silence. If you truly believe the message your company has spent tens, if not hundreds, of thousands of pounds to tell us – by buying article space from any major financial publication that would have you, and getting them to run the story you wanted to put out there.

Covid 19 is having a terrible effect on millions of people across the globe. All walks of life are being affected. One important aspect of life in general is that of investments – life savings and pensions in particular.

Fraudsters are now using the Covid 19 pandemic as a weapon to encourage investors to fall for investment scams. The tactics used are similar to those deployed as scare tactics over Brexit:

“get your pensions out of the UK so you have more investment choice and control”

(What the scammers meant by this, of course, was that they would have choice and control – and fat commissions. The victims would just have less money).

There are many lessons to be learned from the pandemic – including the way different countries have dealt with lockdown procedures. But the lesson I want to examine, in parallel, is how governments deal with pension and investment fraud.

We’ve now seen that laws can be changed swiftly when there is an international crisis threatening millions of lives. Yet, for more than a decade, pension and investment scams have threatened even more lives, while laws and regulations have barely budged. Police can jump into action when a couple of people take a stroll in the park without observing social distancing laws, yet armies of scammers steal of millions of pounds from thousands of victims, and nobody in a police uniform lifts a finger.

The Covid 19 crisis will inevitably contribute to the effects of inappropriate investments – which teeter on the narrow verge between mis-selling and fraud. Where commission is king and investments have been chosen purely for the hidden (from the consumer) introduction revenue, the effects of this will now be felt acutely by many victims.

It has long been deeply frustrating that so many scammers can offend repeatedly – often for years on end – without any sanction. Victims of pension scams such as Ark, Capita Oak, Henley, Westminster, Evergreen, London Quantum, Fast Pensions and Continental Wealth Management have lost their pensions to the same scammers over a seven-year period.

Regulators, police and government ministers have taken not a bit of notice other than sometimes handing the pension schemes over to Dalriada Trustees – who also fail to report the blindingly-obvious frauds to the police authorities.

Mind you, I have some (limited) sympathy with Dalriada. They obviously know it is a complete waste of their precious (and very expensive) time reporting the scammers. Dalriada clearly knows full well that the Police, Insolvency Service and Serious Fraud Office are worse than useless.

Behind this failed law-enforcement network lies an even bigger scam: Action Fraud. This is a cynical effort to fool scam victims into believing that some action will be taken when fraud takes place. However, the reality is that Action Fraud is just a call centre which deliberately ignores the desperate pleas for help by fraud victims. In fact, the Action Fraud call centres are no different in nature than the boiler-room cold calling centres used by the scammers – the purpose is the same: to deceive victims.

We have now seen the hard evidence that whole continents can jump into radical action when necessary. So there is no longer any excuse for allowing the pension and investment scam pandemic to continue unchallenged.

Every country – especially ones where lots of British expats live – needs to recognise that pension and investment scams are – and always have been – a global pandemic. The apathy and laziness of regulators, law enforcement agencies and governments need to cease. And Britain’s shameful, embarrassing track record of ignoring – and even facilitating – scams needs to be reformed.

The early signs of a wind of change in the pension and investment scamming world are there. Spain and New Zealand are now actively progressing criminal proceedings against scammers. There are early signs that other jurisdictions are starting to wake up as well.

The scammers at Premier Pension Solutions and Continental Wealth Management are facing fraud and falsification charges in Spain.

The SFO in New Zealand is investigating the scammers in the $100m Penrich Macro Global investment fraud which was also linked to the Evergreen QROPS scam (run by Stephen Ward and promoted by Continental Wealth Management).

STM Fidecs in Gibraltar has issued a claim against thirteen defendants for the return of “misappropriated” money in the Trafalgar Multi Asset Fund case (also under investigation by the British SFO).

Police in the Cayman Islands are investigating a fraudulent investment company – and has warned potential investors into any companies in Cayman to carry out proper research and due diligence

The Isle of Man courts are preparing for a raft of civil proceedings against leading life offices which have facilitated financial crime on a massive scale internationally.

The Hong Kong fraud squad is taking a keen interest in the GFS Blackmore Global pension/investment scam.

Back home in the UK, there are serious complaints being filed against HMRC and the Pensions Regulator for facilitating pension scams and failing to warn the public. And a growing body of victims and professionals is looking at bringing the FCA to justice for their multiple failures.

Even if the tide is beginning to turn, it is – of course – way too late for thousands of victims whose lives have already been ruined by the scammers. Just as Covid 19 has killed hundreds of thousands of victims in just a few months, pension and investment scams have ruined hundreds of thousands of hard-working victims’ lives in the past decade.

While more than 200 countries are fighting against the spread of Coronavirus and trying to save the 300,000+ people who are sick, we now need key financial services jurisdictions to take the pension and investment scam pandemic seriously.

Renowned English Author James Hadley Chase once famously wrote:

“It’s better to be sick of life than not have a life”.

Pension and scam victims are not just sick of life, but they are also sick of the lack of action by authorities internationally – but above all in Britain. Let’s hope that current actions in place in Spain, Gibraltar, Cayman Islands, Isle of Man, Hong Kong and New Zealand will be replicated as swiftly and effectively as the Covid 19 protection measures.

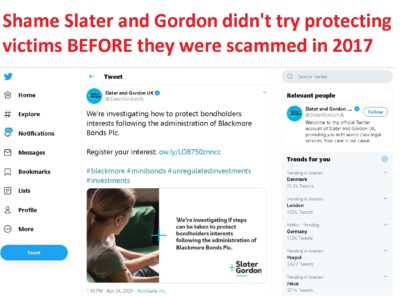

On July 18th 2017, Slater and Gordon Lawyers wrote me the below email. Lawyer Steve Kuncewicz clearly stated that Slater and Gordon acted for their client: Blackmore Global PCC Limited; Phillip Nunn and Patrick McCreesh. The full transcript is below – complete with my comments in bold. This is a 25-page document, so I don’t expect most people (except the most tenacious and determined) to read all of it. So I have put the basic highlights below.

It is clear that Slater and Gordon was a poacher back in July 2017 when the firm represented clients Blackmore, Nunn and McCreesh. And now in 2020, Slater and Gordon, is an even bigger poacher as it attempts to profit from the losses suffered by Blackmore Bond victims.

As Bond Review reported yesterday that the FCA knew all about the doomed Blackmore Bond three years ago, it is clear that Blackmore’s own lawyers – Slater and Gordon – also knew what Nunn and McCreesh were up to at the same time, but did not report their clients to the authorities as they should have done (not that it would have done any good). But both the FCA and Slater and Gordon could have prevented the Blackmore Bond tragedy and saved hundreds of victims from losing their life savings.

Meanwhile, Slater and Gordon is now advertising all over social media:

We’re investigating how to protect bondholders interests following the administration of Blackmore Bonds Plc.

Slater and Gordon is also denying that Blackmore, Nunn and McCreesh were ever their clients. Slater and Gordon is now trying to attract clients by promising:

“We’re keen to assist investors and help them understand their position. We’re investigating if any steps can be taken to protect their interest in the funds within Blackmore’s mini-bond schemes, following the administration of Blackmore Bonds Plc. These schemes promised a high rate of return to investors but continually failed to pay-out. If you invested in mini-bonds or an ISA through Blackmore, we’re keen to speak with you. “

Although the communication with Slater and Gordon is more about the Blackmore Global Fund scam than the mini-bond, it does cover a number of crucial issues including:

Slater and Gordon confirmed that they acted for their clients: Blackmore, Nunn and McCreesh in both a ” business and personal capacity “

Slater and Gordon was trying to shut me up so that their clients could keep scamming hundreds of victims out of their pensions and life savings

Slater and Gordon was falsely portraying their client as: “a prestigious, multi-asset investment house with over £60 million in assets under management, offering institutional and high net-worth clients access to a wide variety of investment products in order to maximise their returns”. This was completely false as Blackmore only targeted retail investors with small pension pots or personal savings – with their entirely unsuitable, illiquid, high-risk investments

Slater and Gordon claimed: “The Blackmore Group was founded on the core belief of putting the needs of its clients first, developing diverse portfolios backed by real assets containing a blend of capital growth and fixed income”. This is nonsense: Blackmore worked closely with known, serial scammers to promote their products and target naive, vulnerable victims. They locked pension savers into their fund scam for ten years without their knowledge and they spent the bondholders’ money on huge amounts of promotion fees (e.g. Surge Group) and commissions for the scammers who helped distribute their toxic wares.

But most serious of all is this next point:

5. Your only intention can be to divert business from them and to cause serious financial harm as a result.

I replied: “I have no interest in causing your clients financial harm – why would I? But I do think that vulnerable pension savers have a right to know the background of the people behind a fund which is being promoted to retail, UK-resident investors.”

A lot of the Blackmore Bond victims invested AFTER this letter. Slater and Gordon did NOTHING to warn the public about their client. All they did was to try to shut me up and prevent me from warning the public.

And now they want to make money out of the Blackmore Bond victims? Seriously?

Slater

Gordon

Lawyers

18 July 2017

URGENT

— IF YOU DO NOT RESPOND TO THIS CORRESPONDENCE, COURT

PROCEEDINGS MAY BE ISSUED AGAINST YOU WITHOUT FURTHER NOTICE

Ms Brooks t/a

Pension-Life.com

24 Calle Cuatro

Esquinas

Lanjaron

18420,

Granada

SPAIN

58 Mosley Street

Manchester

M2 3HZ

DX 14340

Manchester 1

Tel: 0161 383

3500 Fax: 0161 383 3636

wwwslatergordon.co.uk

Your Contact:

Steve Kuncewicz Assistant: Rebecca Young

Direct Tel:

01613833708

Email:

Steve.Kuncewicz@slatergordon.co.uk

Your Ref:

Our

Ref: RZY03/UM1389098

Our Clients: Blackmore Global PCC Limited, Philip Nunn and Patrick McCreesh Proposed Claim for Defamation and Malicious Falsehood

We act for the aforementioned clients in their business and personal capacity and have been instructed to contact you in relation to various untrue, defamatory and wholly unjustifiable allegations published on your website at httq://pension-life.com (the Website) relating to our clients, their products and services which are designed to (and in fact already have, as set out below) damage their respective reputations and financial interests.

Our client, Blackmore Global PCC Limited, is part of the Blackmore Group which is a prestigious, multi-asset investment house with over £60 million in assets under management, offering institutional and high net-worth clients access to a wide variety of investment products in order to maximise their returns.

If it is indeed true that Blackmore Group is a prestigious organisation, then I have no doubt the directors will be keen to ensure that the damage done to victims’ pensions is put right and that Blackmore’s purported “good name” is protected. However, when you Google Blackmore Group PCC nothing comes up about it being “prestigious” – but what does come up is a link to one of Offshore Alert’s warnings regarding Brian Weal – – and as you know at least one of the underlying assets was run by Weal.

Further, there are cautionary warnings on the Money Saving Expert forum which mentions that investors were given a “pension review” by Aspinal Chase (run by your clients) and promised 10% returns p.a.There is absolutely nothing available on Google which describes Blackmore Global as “prestigious”.

Further, the clients are not high

net-worth, under the FCA definition. Are you aware of the FCA

definition of “High net-worth”? Your clients, with 25 years’

experience, will know this. Just to remind you, a high net-worth

client, according to the FCA has-

an

annual income to

the value of £100,000

or more.

Annual income for these purposes does not include money withdrawn

from pension savings (except where the withdrawals are used directly

for income in retirement).

net assets to

the value of £250,000

or more.

The definition specifically excludes

pension savings. Yet, your clients are involved in the marketing,

processing and investing of retail pensions of those that are not

high net-worth clients. I would be interested to see if ANY

sophisticated or institutional investors are in the Blackmore Global

Funds. Surely, such experienced investors would demand audited

accounts.

“The Blackmore Group was founded on the core belief of putting the needs of its clients first, developing diverse portfolios backed by real assets containing a blend of capital growth and fixed income.” (Steve Kuncewicz of Slater and Gordon – 18.7.2017)

If the assets

are “real” – tell us what they are. Do you even know what they

are? Have you seen an independent audit or are you relying solely on

what your client is telling you?

Blackmore Global

PCC Limited offers a medium to long-term investment vehicle for its

clients with a diversified investment portfolio under one structure

which allocates investment between four distinct protected cells

which diversify assets between property, sustainable energy, private

equity and lifestyle. In order to take advantage of as wide a range

of investments as possible, it invests in a number of vehicles

including funds, companies, joint venture projects and equities.

I know all about

the cells as they are described in the factsheet and brochure.

However, based on the fact that we know some of the information

contained therein is untrue, I am not sure the cell information can

necessarily be relied on. What we really need to know is exactly

what the assets are. Steve, I mean no disrespect but your letter

contains 21,290 words – and not one word about what the assets

really are. You seem to be trying to claim your clients have done

nothing wrong – but you are providing no evidence.

Further, among

those many words, you refer to loss suffered by your clients multiple

times, but you never once refer to the considerable loss and distress

suffered by the Blackmore Global investors (or indeed the Capita Oak

and Henley ones).

Patrick McCreesh

and Philip Nunn founded the Blackmore Group (of which Blackmore

Global PCC forms part) in 2013,

That would be

just after the Capita Oak and Henley scams, which Nunn and McCreesh

were promoting, collapsed.

and jointly have

more than 25 years’ experience in the financial services sector,

growing their business to the extent of it having over £17m of

assets under management across multiple asset classes.

With

respect, if they have jointly more than 25 years’ experience in the

financial services sector, they should know that their fund is not

suitable for pension schemes – just as they should have known that

empty boxes (store pods) were not suitable investments for the Capita

Oak and Henley victims. And

I sincerely hope that (apart from the victims of which I am aware)

none of the remaining £17m represents pension investments.

By contrast, the

Website describes your activities as follows:

“Depending

on the type of pension or investment scam a victim has been involved

in, there are various things we can do to help. We charge annual

membership fees so that members know exactly what they will have to

pay and there will be no legal or accountancy fees on top.

Deal with

trustees, advisers and fund managers

Complain to

regulators and ombudsmen

Appeal tax

liabilities with HMRC and the Tax Tribunals

Analyse and

quantify investments, losses and fees/commissions

Instruct

solicitors to

make

a claim against negligent parties to obtain redress for losses and

liabilities (paid for by litigation funding)”

Am not sure what

the point is that you are trying to make here. You have used the

phrase “by contrast” which to me suggests you are trying to

ascertain that, unlike your clients, I have never been involved in

running or promoting a pension or investment scam. Which, of course,

I haven’t. Indeed, I vigorously oppose such crimes and am working

with the regulators, police and ombudsmen to help stamp out such

activities and bring those responsible to justice.

Notably, you refer

to yourself as “one

of the leading experts on pension liberation scams”.

Indeed, I am

widely acknowledged as such. Further, in your above statements, you

have now correctly identified the following problems associated with

Blackmore Global:

Problem no. 1: the victims were

neither “institutional” nor “high net-worth”. They should

never have had their pensions invested in the Blackmore Global fund

at all.

Problem no.2: you have said Blackmore

develops “diverse portfolios backed by real assets”. So what

are these “real” assets? Do you even know? Has Blackmore ever

told you or shown you proof? Because they won’t tell the victims

what the assets are. Nor will they tell the pension trustees.

Problem no. 3: Blackmore Global

offers a “medium to long-term investment vehicle”. So, not