Our last blog in this series recreated the offshore pension scam process. We covered the set up and hard sell. The slick salesman prepared the unwitting victim and convinced him his pension would be better off out of the UK.

The silver-tongued spiv, Darren, posing as an adviser, conned his new client with no problem at all. The poor victim was duped into believing he should transfer his pension into a QROPS – an overseas pension scheme. The con worked because the experienced scammer pressed all the right buttons:

Your pension will be looked after better, it will be cheaper to manage, you’ll pay less tax, you won’t lose half of it when you die, you’ll get to choose your own pension investments!

Of course, the scammer, didn’t point out that once out of the UK, John’s pension would have no protection. Complete control of the money would be squandered will now lie in the hands of the unqualified, unlicensed scammers.

The victim, John had stressed:

I’ve paid tax all my life, so I feel I’ve paid my dues. I definitely don’t want to pay too much once I’m retired because every penny is going to count.

But sadly he’s played right into the scammer’s hands. His precious pension will be transferred into a QROPS and then into an insurance death bond:

John: I worked for thirty years to build up that pension and I don’t want anything to happen to it.

Darren: So, let’s look at all the ways you can improve your pension and make sure its protected.

But far, far from improving or protecting the investor’s pension, the scammer has removed the precious retirement fund from the safety of the UK. He’s sent it off to Malta or Gibraltar and then on to the Isle of Man or Guernsey. The money is now well beyond the protection of British regulation or compensation.

John had stressed how he wanted low risk, but has now signed dozens of forms – and this will guarantee that his pension will be exposed to high risk. Darren didn’t give him a chance to read or understand these long and complex forms. And the most important form of all was a blank investment dealing instruction. Once this has been signed by John, the scammer can copy it dozens of times and invest the pension money in whatever pays the highest commission.

The whole point of this scam is for the scammer to make money out of the victim by a whole series of hidden commissions.

Darren: My firm would charge you a small fee for setting up the transfer and then looking after your pension investments moving forwards.

But what will actually happen is that the scammer will openly charge three or four – or more – percent in set-up fees, plus one or two percent a year service charge. But, under the table, he will earn a further 7% hidden commission from the death office – such as Quilter International, Utmost International, RL360 or Friends Provident.

Darren: Right. And then we can start investing your pension and making it grow – so you’ll be able to have a happy and healthy retirement.

John, and all the other victims, will be a long way from being happy or healthy. Because the death office has a platform that the scammer will use to pick the highest-commission investments. So John’s pension fund will be used to line the scammer’s pockets for the next ten years – as he will be stuck in the death bond for that long.

Investments that pay the highest commissions – such as structured notes and unregulated collective investment schemes – are also the highest in terms of risk. John’s pension can now only lose money. And as the value of his hard-earned retirement savings goes down and down, the scammer’s commissions will keep on going up and up.

John, along with all the other victims, will end up losing part – or all – of his pension. He may well lose his home, see his marriage break up, develop depression or a life-threatening illness. He may even take his own life.

But John and his dire poverty will be long forgotten by the slick, silver-tongued scammer. He’ll be busy rubbing his hands with glee at his next batch of victims. Because there’s plenty of them and this form of pension fraud is showing no sign of slowing down any time soon.

I don’t often disagree with highly-regarded pensions expert Henry Tapper. Too much respect and awe. But his recent blog: “The Balls of Old Bailey” (about Andrew Bailey) merits a polite argument. It has made me cross – not cross with Henry, per se. But cross with the failure of Britain’s culture, government, regulation and legal system to address justice justly (or at all).

Henry has questioned the point of revisiting the balls-up made by former FCA CEO Andrew Bailey and has suggested that “we need to move on”.

The point of examining Bailey’s sickening catalogue of balls-ups is that we must make sure it never happens again. Part of that mission is to follow the example of the criminal justice system: we don’t give convicted criminals a jolly good talking to – or even a good bollocking. We take away their liberty and put them in prison. This is called a “deterrent”.

What did Old Bailey do that was so bad? The answer is, indeed, a long list – starting with British Steel, Toby Whittaker’s Park First and Neil Woodford’s Fund, and moving on to London Capital & Finance and a long list of other mini-bond scams – including the Blackmore Bond. Bailey should have stopped that entire horrific catalogue of investment fraud if he’d been doing his job properly. He could – and should – have prevented hundreds of thousands of victims from losing their life savings and pensions in all of those investment scams.

The advantage to be had from putting the bollocks – and preferably the head – of Bailey on the block is to send out a warning to future FCA bosses. They all need to understand that they are public servants, and that with huge salaries come huge responsibilities. Current overpaid bosses Nikhil Rathi, Christopher Woolard and Charles Randall must be reminded that running the FCA is a serious public duty – and not just an easy stepping stone to an even bigger and better job (however badly they fail consumers).

Bailey’s numerous failures were rewarded with an eye-watering salary followed by promotion to governor of the Bank of England.

But Bailey’s balls-up is by no means unique. He’s in good company with a whole raft of over-paid public servants who have betrayed the public:

Post Office boss Paula Vennells was awarded a CBE for falsely prosecuting hundreds of innocent Post Office subpostmasters for fraud – even though she knew full well they were innocent. In arguably the biggest scandal of corruption and injustice in British history, Vennells oversaw the wrongful conviction and sometimes imprisonment of 700 victims. Many of these people were financially ruined, lost their homes and committed suicide. One pregnant woman was sent to jail, and many marriages and families were destroyed.

Former HMRC boss Lin Homer was rewarded for her vast catalogue of disasters and failures with another huge salary and a £2.2m pension

Paula Vennells (left), Dave Hartnett (middle), Lin Homer (right)

But to revert to the failings of Andrew Bailey, Henry has suggested that we need to “move on”. However, those who have lost their life savings and pensions because of the FCA’s defects will have great difficulty putting their losses and harrowing ordeals behind them. Living in abject poverty won’t help them forget. They will certainly never forgive the fact that Andrew Bailey could have prevented them becoming victims of investment scams such as mini bonds, Store First, Park First, the Woodford Fund and Blackmore Global etc.

Henry’s blog concludes that Andrew Bailey, as Governor of the Bank of England, has a great deal on his plate: cost of living crisis, looming recession and Brexit. But does anybody seriously think that such a negligent, lazy, incompetent person is capable of dealing with that lot – when he couldn’t even listen to frantic whistleblowers such as Paul Carlier, Mark Taber and Brev at Bond Review who were offering to do his job for him?

This silly twerp got caught looking at lewd images on his mobile in the House of Commons. His excuse was that he thought porn was spelled “tractor”. Parish has now resigned and his political career is almost certainly over. His wife might also be quite cross. He probably won’t be rewarded with a promotion, a CBE or any kind of public “moving on”.

What Parish did was foolish. But he didn’t cost thousands of people their pensions and life savings; he didn’t ruin hundreds of subpostmasters’ lives and send some of them to prison or to their deaths; he didn’t aid and abet hundreds of millions of pounds’ worth of tax evasion; he didn’t overcharge millions of taxpayers or lose their records.

Parish embarrassed himself and was caught doing something unbelievably silly – that hurt nobody except himself (and his own family). But the price he will pay for this will be crippling and may have ruined his life. Meanwhile, Bailey, Vennells, Hartnet and Homer have evaded any kind of sanction and gone on to glittering success, awards and eye-watering pensions.

On the web of pension scams It seems as though criminal convictions against pension scammers might be getting popular. More than a decade has gone by with virtually none of the usual suspects getting jailed – despite a few criminal investigations (that, so far, have not resulted in convictions). Is the system really that hopeless or do these criminals just know how to work it? Probably, both. But is it getting any better?

Almost all scammers and scams are, in some way, related or connected. If the earliest scammers (circa 2010) had been prosecuted and put behind bars, much of today’s damage could have been prevented.

Now that there is an intricate web of them passing around their tricks of the trade, it’s no wonder they’ve all been able to bypass the laws and regulations.

Two scammers have, however, recently been brought to justice:

Much of the £13m ended up in the hands of well-known scammer David Austin – who committed suicide after being caught in another pension scam (using his daughter Camilla as the “front man”).

Susan Dalton & Alan Barratt

The Barratt and Dalton scheme, was also promoted by Julian Hanson – one of the main promoters of the £27m Ark pension scam in 2010/11. Hanson’s vigorous promotion efforts resulted in £5.5m worth of Ark victims (100 in total). One of Hanson’s co-scammers was the notorious Stephen Ward of Premier Pension Solutions who was the “architect” behind the Ark scheme – along with Andrew Isles of Isles and Storer Accountants. Hanson, Ward and Isles were never prosecuted and so went on to operate and promote millions of pounds’ worth of further pension scams – ruining many thousands more lives.

Ryan Playford

Sue Dalton, after moving on from the Barratt and Dalton scheme, went to work at Continental Wealth Management in Spain – reporting to head scammer Darren Kirby and his partner Jody Smart (who was the sole director of the company). Dalton’s extensive experience in pension scamming made her a hit at CWM. Ironically, Hanson has not been jailed along with Barratt and Dalton.

Playford got 15 years for supplying cocaine and canabis. Clearly a wrong-un, and someone who has no respect for the law or for the wellbeing of people’s lives who would inevitably be ruined by drug abuse.

But what does Playford’s drug conviction have to do with pension scams – you may ask? We have to go back a decade to discover the answer:

In 2008, Playford and an associate – Natasha Beesley – registered a drug company inCyprus:R. P. Med Plant. Presumably, the authorities were convinced that by “drugs”, this meant legitimate drugs for medicinal purposes.

Stephen Ward

In 2012, however, the pension scammers pounced on this Cyprus company as being the ideal sponsoring employer for another one of Stephen Ward’s pension scams: Capita Oak. Ward and his pension-lawyer friend Alan Fowler, used R. P. Med Plant Limited (Cyprus) as the so-called employer for an occupational scheme – registered by HMRC and the Pensions Regulator.

Ward and Fowler forged signatures on a trust deed for their new pension scam, and slightly changed the name of the employer to R. P. Medplant Limited (so that nobody could find it easily on the Cyprus Companies House register). It seems likely that Ward and Fowler must have known Ryan Playford somehow, in order to be able to get their hands on his drug company.

Patrick McCreesh

Capita Oak then became the vehicle for the scamming of 300 victims into investing their entire pensions in Store First store pods. Ward took charge of all the victims’ pension transfers, while another group of scammers took care of the cold calling of thousands of potential victims and signing up of the actual 300 victims.

Capita Oak’s 300 members were not the only victims invested in Store First store pods. There were thousands more in the Henley Retirement Benefits Scheme and various SIPPS including Carey (now Options and owned by STM), as well as Berkeley Burke and Rowanmoor. There have so far been no convictions – other than Playford’s for drug dealing.

This interconnected web of lies and deceit will keep on spreading unless these criminals actually fear the consequences of their actions. Let’s keep the convictions coming and not just save them for drug lords.

At the end of January 2022, Boris Johnson claimed he had reduced crime by 14%.

Boris shocked a lot of people with this figure. But, apparently, he wasn’t talking about fraud. He’d forgotten that even some of his own constituents had been defrauded into the Ark pension scam (and that he had promised to “sort it out” back when he was Mayor of London).

Norgrove headed up the Pensions Regulator (which used to be known as OPRA) from 2005 to 2011. He had issued dire warnings to pension providers against handing over pensions to scammers – saying that just ticking boxes (without checking the receiving scheme was bona fide) would lead to a huge rise in pension fraud. He was, of course, ignored – especially by Standard Life, Aviva, Scottish Widows and Prudential.

Norgrove’s correction of Blonde Boris’ clumsy gaff is not surprising at all. This government’s attention and time spent into looking into fraud has been somewhere between minimal and non-existent. Combine that with putting an utter nitwit in charge of the FCA, and you have the perfect breeding ground for an explosion of fraud and scams.

It is disgraceful to know that this government’s focus on crime ignores fraud as though it were irrelevant. This huge aspect has been – and is still – affecting hundreds of thousands of people. I suppose our ill-informed P.M. thinks the person in the black balaclava seems a lot more dangerous than the one in the designer suit and tie.

But we know the damage these fraudsters can cause. Such misinformation being spread is highly dangerous; leaving consumers with a false sense of security, and making them even more likely to be scammed.

Terence Wright & his wife

Let’s take Terence Wright for example. Wright’s activities in the pension scam world flourished in 2014 and 2015. Although he most definitely didn’t look like a typical burglar, he caused the destruction of millions of pounds of pensions across the UK.

Wright had an unregulated Spanish firm called Commercial Land & Property Brokers (CL&P) which introduced hundreds of people to the pension SIPP provider Carey Pensions. From here he invested the victims’ money into Store First and Australian farmland via Gas Verdant where the money will have dwindled away into nothing.

One victim, Russell Adams, got his destroyed pension reinstated in the Appeal Court. But thousands more are still left stranded with illiquid and sometimes worthless pension assets.

There are many more examples: Trafalgar Multi Asset Fund (in an STM QROPS and invested in Dolphin Trust); Blackmore Bond, Blackmore Global (in STM, Optimus, EFPG, Quartermaine and GFS QROPS); Forthplus SIPP which has just gone bust and is full of toxic investments. The list is endless.

This type of fraud is committed against British victims routinely. The crime goes on (and on!) in the UK and offshore. By destroying pension funds with toxic investments, the fraudsters earn millions in hidden commissions. Which is supposed to be illegal. Perhaps Boris the Johnson will wake up to this fact one of these days. Or perhaps this is as unlikely as him using a hairbrush.

The FCA seems to have woken up. It only took eleven years. Eleven years of laziness, torpor, disinterest and deliberately ignoring the problem. But, completely out of the blue, the FCA has suddenly got bored with crapping on bathroom floors and has decided to do a spot of rather belated regulating.

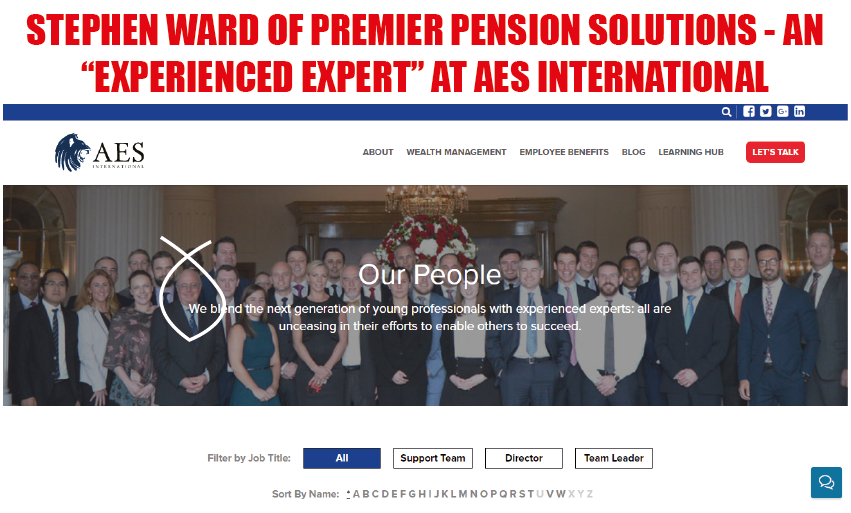

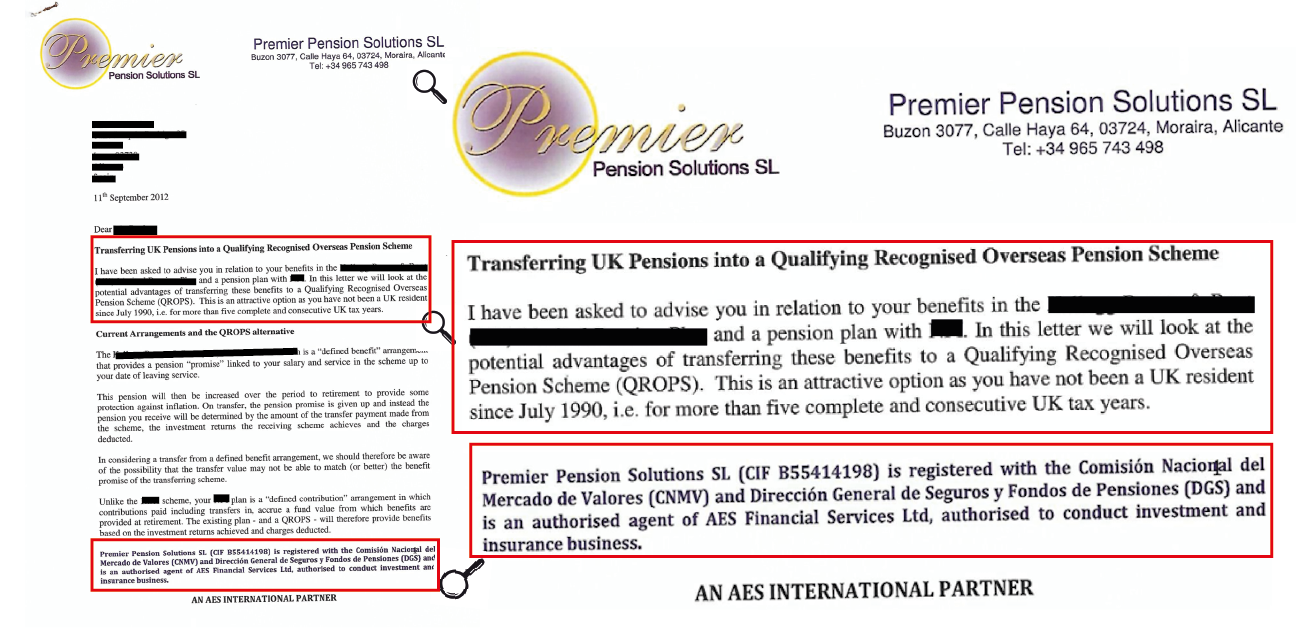

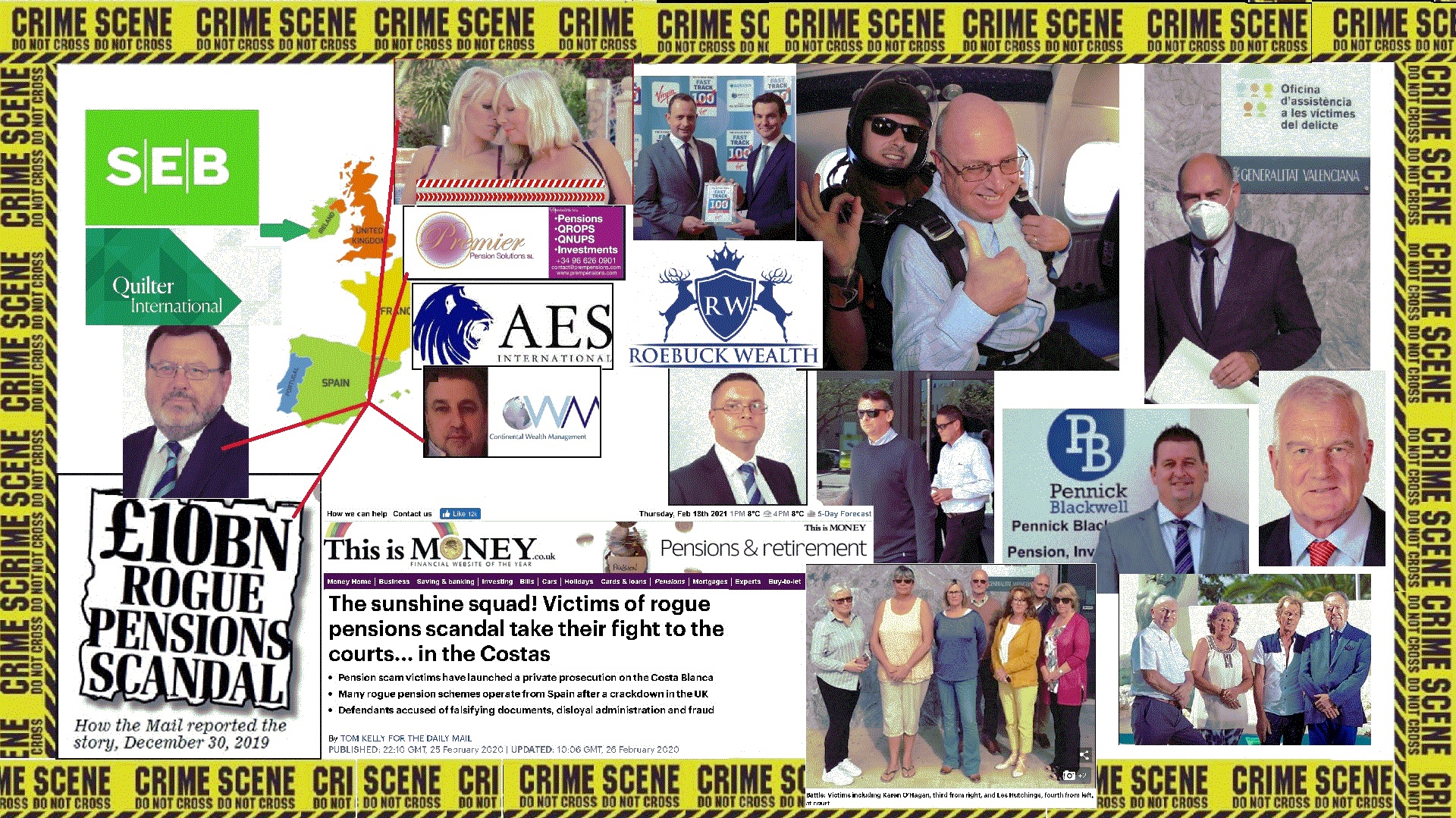

The object of this sudden fit of uncharacteristic activity, is the Ark pension scam. This was operated between 2010 and 2011 by a team of scammers. This team included so-called financial advisers, introducers, a pensions lawyer and an accountant. The principal architect of the six Ark schemes, however, was Stephen Ward of Premier Pension Solutions in Spain. His Spanish firm specialised in (pretty much what it said on the tin) pensions. In particular pension transfers.

Stephen Ward of Premier Pension Solutions

From August 2010, Ward’s company Premier Pension Solutions (PPS) was run as an agent of AES Financial Services – which was regulated by the FSA (now the FCA). Before this, Ward’s company was in the Inter-Alliance network in Cyprus. Coincidentally, the “sister” firm Continental Wealth Management (CWM) was also a member of the Inter-Alliance network. PPS and CWM worked together in close collaboration. CWM often did the cold calling and warm up act for Ward’s various pension scams – including the New Zealand Evergreen liberation scam.

An agency agreement was in place between Ward’s firm PPS and Sam Instone’s firm AES. But the agreement specifically excluded pension transfers. Which was pretty odd, bearing in mind pension transfers were PPS’ main activity. This resulted in Ward’s firm giving victims the false impression that the pension advice he provided was regulated. Which, of course, it wasn’t. The exclusion in the agency agreement between PPS and AES was, naturally, hidden from clients and victims.

Complaints directed at Ward about the various pension scams he had been operating over the years were always firmly rebutted. Ward always claimed that his own activities were the responsibility of AES as the regulated party – and that it was up to Instone to decide what PPS could and couldn’t do.

Kirsten Hastings from International Adviser has published some excerpts from the FCA’s questionnaire about Ark, PPS and AES:

A questionnaire has been sent by the FCA to customers of AES Financial Services (which also traded as International Pension Transfer Specialists (IPTS), Premier Pension Solutions (PPS) and Premier Pension Transfers (PPT).

These clients invested or transferred pensions into schemes managed by Ark Business Consulting and/or the Ark pension schemes.

The questionnaire was sent to consumers to gather more information about their dealings with these firms.

They have until 17 October to respond.

Director of AES Sam Instone told IA: “We are absolutely certain AES Financial Services Ltd has never provided any advice at all in relation to Ark schemes, so it seems like a strange questionnaire.”

Sam Instone seems to have forgotten that AES Spain was run by rogue “adviser” Paul Clarke for some years – after leaving unlicensed firm CWM in 2010. Clarke advised several victims to transfer into Ark. And good old Sam himself advised his own Dad to transfer into Ark. I guess three destroyed pensions – with accompanying tax penalties – can be easy to forget?

Kirsten Hastings goes on to talk about the history of Stephen Ward’s Ark scam:

TPR took action following concerns that the Ark schemes were being used for pension liberation.

According to Dalriada, such schemes generally have high charges and invest money in risky and esoteric vehicles.

They also put members at risk of having to pay large sums of tax.

The latest Dalriada update to members states it is “not able to place a value on any members’ benefits at the time and are therefore unable to make payments to members”.

Kirsten also mentions some further points in the FCA questionnaire:

Kirsten Hastings editor at International Adviser

Did the client (Ark victim) approach the firm or vice versa?

Where was the client based when these services were provided?

Would clients be willing to sign a witness statement?

What regulatory protections was the client told there were?

All Ark victims would certainly be more than happy to sign a witness statement to evidence what Stephen Ward, PPS and AES did, wrote, promised, assured and persuaded.

The regulatory protection, of course, for anyone advised by Stephen Ward’s Premier Pension Solutions (which was most of them) in the Ark scam, was Sam Instone’s AES Financial Services – according to all the documentation.

Ward promoted the Ark £27 million scam during 2010 and 2011 – cases being documented on PPS headed paper announcing that the firm was a “Partner” of AES and regulated through AES. Ward would have earned at least £1 million through the Ark scam – all of which would have been paid through AES.

When Ark went tits up, Ward launched his next pension liberation scam: Evergreen Retirement Benefits QROPS in New Zealand – with his accompanying 50% Marazion “loans”. Again, all advice was given on PPS headed paper announcing that the firm was an AES partner and regulated through AES. This meant another 300 victims lost more than £10 million worth of pensions. It also meant that PPS and AES between them earned at least £1 million from the scam (10% of transfer values). These fees were paid direct to AES.

When Evergreen collapsed (as all PPS pension scams eventually did) in 2012, Ward set up the Capita Oak scam. Another 300 people lost over £10 million – all invested in Store First store pods. Again, all pension transfers were done by Ward. Alongside Capita Oak, Ward carried out all the transfers for Henley (another 250 victims losing £8 million in Store First) and Westminster (another 79 victims losing £3.3 million in other toxic, high-commission investments). All these schemes are currently under investigation by the Serious Fraud Office.

Throughout this era – during which all business done by PPS went through AES – Ward ran multiple, multi-£million pension scams – mostly involving liberation fraud:

Bollington Wood

Capita Oak

Dorrixo Alliance

Endeavour QROPS

Evergreen QROPS

Feldspar

Halkin

Hammerley

Headforte

Henley Retirement Benefits

London Quantum

Southlands

Randwick

Randwick Estates

Southern Star QROPS

Superlife QROPS

The above list comprises QROPS which were used abusively, and bogus occupational schemes.

All these PPS scams resulted in many hundreds more victims losing millions of pounds’ worth of pensions. Many of these unfortunate people were also persuaded by Ward to liberate their pensions, and so they would have faced crippling tax penalties as well.

Ward’s final triumph in his long-running pension scam campaign was London Quantum. He proudly announced this scheme saying that “Ark is history” and that he was now going straight. Still trading as an AES partner and agent, Ward conned 100 victims into the London Quantum scheme. This was invested in the usual high-risk, high-commission and entirely inappropriate assets (including Dolphin Trust loans and car parking spaces at Park First Glasgow). London Quantum ended up being classified by Dalriada Trustees as being “probably worthless”.

In the Ark Pensions scam, it is clear why so many victims thought PPS was a properly-regulated firm – AS AN AGENT AND “PARTNER” OF AES:

“Premier Pension Solutions SL …..is an authorised agent of AES Financial Services Ltd authorised to conduct investment and insurance business. AN AES INTERNATIONAL PARTNER.“

In the subsequent £100 million Continental Wealth Management pension and investment scam, Ward continued to “advise” hundreds of victims to transfer their precious pensions into the hands of known scammers – in the full knowledge that their pensions would be invested in high-risk, high-commission rubbish funds and structured notes:

But Stephen Ward was a bit more than just an “agent” and “partner” of AES. He was also an integral part of the AES management team – and boasted that he was Director of International Pensions. When all the pension scams finally collapsed, leaving thousands destitute and desperate – as well as hounded by HMRC – Ward and Instone set up IPTS: International Pension Transfer Specialists. This new venture was run from Ward’s office in Moraira – although they tried to hide this by using a PO Box at nearby LettersRUs. And so the misery continued…..

Stephen Ward in the front row of the AES team of “experienced experts”.

The following blog was written by Stephen Sefton: a Blackmore Global Victim who cares about pension scams.

Stephen was scammed by David Vilka of Square Mile International Financial Services around six or seven years ago. Vilka, who had neither qualifications nor a license to provide pension or investment advice, arranged the transfer of Mr. Sefton’s substantial final salary pension.

Stephen’s pension was transferred to the Optimus QROPS in Malta.It was placed in an Investors Trust offshore bond in the Cayman Islands. Then it was invested in high-risk, high-commission, unregulated funds. One of these was Blackmore Global.

A determined fight on the part of the tenacious Mr. Sefton did eventually result in the recovery of a large part of his funds. But his case was a rare exception. He was, indeed, very fortunate that he didn’t lose the whole lot. Most victims suffer total loss in such circumstances.

It is now looking very likely that Phillip Nunn and Patrick McCreesh’s Blackmore Global Fund is going to be as worthless as their other investment scam: Blackmore Bond (now in administration).

Pension Scam victim Stephen Sefton writes:

Finally, after two months of radio silence, Angie Brooks once again pens an article. It’s about time!

I care. I don’t know why I should but I do. Maybe because I am seeing a media frenzy over the recent collapse of mini bonds in the UK. Especially LC&F and Blackmore Bonds plc to name just two. Meanwhile, victims of pension scams from the last decade are being forgotten and swept under the carpet. Much to the delight of many of those that oiled the wheels of the scams and helped them to happen – especially the QROPS and SIPPS!

There are many (especially the scammers) that really don’t like me. This is why they tried to offer me a paltry £6000 to silence me. Seriously?

There are many that don’t like my rhetoric and I regularly get blocked on Twitter, or thrown off Facebook. Here, I get to tell it like it is, however unpalatable the truth may be.

What I have learned over the years is that there’s an intricate web, woven around these scams. This interconnects a number of players whose names just keep on cropping up.

Malta was clearly the jurisdiction of choice for many pension scams. It seems to have hundreds, if not thousands, of victims. Many of these are not yet even aware that they face financial ruin in their retirement.

In my opinion, Malta has much to answer for and really should clean up its act. Journalists rarely focus their gaze on the real facilitators of pension scams: the Mickey Mouse jurisdictions that turn a blind eye and allow them on their patch.

Why are they not aware? QROPS Scheme Administrators are sending out fictitious statements implying members’ pensions are still intact. One member of STM Pensions Malta was sent a statement in Sep 2020 showing his pension still intact just one month after STM wrote to members invested in Blackmore Global – Nunn & McCreesh’s offshore unregulated collective – that in fact they (STM) have no idea what the value is!

As it happens, STM did manage to get Nunn & McCreesh to publish the underlying assets for Blackmore Global, in May 2020 (over 6 years since the fund was launched). Even with this list, there is little idea what the fund is worth because the underlying assets are themselves useless, opaque, private ventures in yet more Mickey Mouse jurisdictions. One offshore fund is already being pursued by Dalriada as part of other failed pension schemes from early in the last decade – but Dalriada are getting nowhere with it.

I am not convinced that “The Adams v Carey case is likely to herald a flood of similar claims …”.

Courageous Manita Khuller in front of the Guernsey courthouse

The Ombudsman case that went in favour of Mr. N against the Northumbria Police Authority (PO-12763) in July 2018, was also a landmark case against a negligent UK pension provider that had a tick box culture. The ceding provider transferred Mr. N’s pension without due regard for the Pensions Regulator’s requirements of 2013 for extra due diligence when handling transfers.

That decision doesn’t appear to have “herald[ed] a [likewise] flood of similar claims” three years on.

Firstly, the victims were targeted by scammers because they were “ignorant”. That’s not meant to be derogatory.

They knew diddly squat about pensions, regulations, investments – nothing! They trusted the “adviser” – the con man persuading them to transfer their pension. For a con to be successful you need the essential skill of gaining people’s trust. Scammers have this skill in abundance. The ignorant fall for it every time.

Victims not only knew nothing about pensions and investments, they didn’t even know how to spot they were being conned. They were the perfect mark for scammers. They didn’t know what they didn’t know. Like taking candy from a baby – although a baby knows it is being robbed and often screams quite loudly (so maybe not the best analogy).

Secondly, even if victims have now discovered they have lost their pension, they have absolutely no idea what next to do about it. The ones I have come across are like fish out of water. Completely at a loss of where to go.

On Angie’s facebook group, one person recently told of their father’s loss of pension to Nunn & McCreesh’s Blackmore Global. In an attempt to do “something” the person went to the FCA on behalf of their father only to be told that investing in unregulated funds on the advice of unregulated advisers bars them from the compensation scheme and Ombudsman service. The FCA suggested looking into the Malta compensation scheme – which is a joke! That was the extent of help from the FCA. As useful as a chocolate teapot.

It hadn’t occurred to this person that either the ceding provider is guilty of maladministration for the transfer in the first place, AND/OR the receiving scheme in Malta is in “breach of trust” because it too is bound by legislation controlling its activities.

So the best next step is to pursue one or other side of the transfer – or both.

Manita Khuller went after the receiving trustee through the courts and eventually won. However, such legal action isn’t for the faint hearted. It cost her huge sums of money, which she took out loans to fund. Losing was not an option. On top of already losing her pension. It was a nightmare for her. I know – I was with her every step of the way since 2018 when we were introduced by a journalist. This was her only option because the Mickey Mouse jurisdiction, Guernsey, had no “Ombudsman” service. Moreover, the incestuous nature in Guernsey meant law firms declined to represent her. She had to go it alone for the first trial, adding a layer of stress no person should be subjected to. There are few victims with this determination or courage willing to take this course of action – so they don’t, even though she has paved the way.

We in the UK, at least, have the Ombudsman and now – relatively recently – Malta also has one (the Office of the Arbiter for Financial Services (“OAFS”)).

Guernsey is a backward, biased, Mickey Mouse, incestuous jurisdiction – which is why scammers love it.

The Scheme administrators on both sides of the transfer will fight tooth and nail and argue the victim is wholly to blame for their losses. Many victims just have no idea how to go about presenting their case.

There is no “free” professional service available to help victims navigate this minefield. Mr. N (referenced earlier) paid lawyers £25k to make his case. But the Ombudsman did not award costs – saying that it is not necessary to engage lawyers. However, it is not easy to fight a pension scheme that will employ a top notch law firm to present its defence. So by and large, the victims I have come across are at a serious disadvantage because they have no idea how to seek justice and have nowhere to go and don’t know how to present their case. That’s why they were targeted by scammers in the first place. They were (and still are) easy pickings.

In the article above, Ms. Brooks quoted from the appeal. I will do same. A more appropriate section, §115(i),

“… while consumers can to an extent be expected to bear responsibility for their own decisions, there is a need for regulation, among other things to safeguard consumers from their own folly.”

Members of Staff (in shorts!) from Carey Olsen

These victims are indeed victims of their own folly, but they never realised what they were doing. On both sides of the equation (ceding providers and the receiving schemes) there were duties of care designed to protect these victims “from their own folly”. In all cases I have come across, neither side fulfilled those duties of care. On the UK side there was contempt for the Pensions Regulator’s requirements of 2013, despite growing industry concerns for pension scams. On the receiving side, the QROPS didn’t (and still don’t) care about their members – period. And neither did the authorities in these Mickey Mouse jurisdictions. It was the perfect match and thousands of vulnerable victims are paying the price.

Carey Pensions was started in 2009 by the Carey Group. The Group is controlled in Guernsey by ten partners and ex-partners of the Law Firm Carey Olsen. This is an amusing coincidence in my opinion. Carey Olsen, perhaps the top law firm in Guernsey, represented FNBIT against Manita Khuller – and LOST at appeal by the way.

Justin Caffery floating in the sea while preaching stress relief

Harbour Pensions was started by Justin Caffrey, in 2013 and says in the STM announcement, “Harbour was always a five year plan…”. Justin made his money and now runs meditation classes (seriously?). He should meditate on the misery, caused by Nunn & McCreesh, of hundreds – if not thousands – of vulnerable victims of Blackmore Global that he allowed into his pension scheme, in my opinion, willingly and knowing the consequences of such an unsuitable investment. He permitted 100% allocation of one member’s pension into a fund that has never published audited accounts. At the material time, knowing the fund was opaque and unregulated, Harbour (and other QROPS) were happily permitting transfers and 100% allocations.

The fund’s offer document, which Harbour had, says the investment has a ten year lock-in. That condition, which the QROPS knew and willingly accepted, effectively locked Harbour (and subsequently STM) into an asset they knew nothing about – and still don’t – for ten years, with absolutely no knowledge or control of what Nunn & McCreesh were doing with the money.

The Scheme administrators in these QROPS in Malta were, and still are, completely at the whim of Nunn & McCreesh – who could misappropriate the pensions as they wish and the administrators could do absolutely nothing about it. The QROPS effectively abdicated all powers they had to run the scheme and mitigate risks in the interest of members, to Nunn & McCreesh. They have been passive bystanders to the destruction of their members’ pensions ever since. This is, in my opinion, in breach of the Malta Trust and Trustees Act. They are also willingly and knowingly in breach of trust.

All this really begs the question whether STM go looking for dodgy pension schemes or are they just plain stupid? What on earth is going on and why hasn’t the MFSA taken them to task? They seem to attract scams like flies to a pile of dung.

Blackmore Global Victim who cares about pension scams – says victims are being forgotten

Victims are being forgotten by the media and authorities. Victims had no idea what they were doing or how to seek restitution. They are guilty of nothing but ignorance and ALL the actors in these scams have gotten away with it. They have ALL dipped their hand in the pension pots and kept the spoils – and now moved on, leaving the pension pots empty.

This is frustrating in the extreme because I see no evidence of any “flood of similar claims”. The victims are, for the most part, still ignorant and there is no one “helping” them. This site (Pension Life) once purported to “help” victims but I am not at all convinced it has done much and now has long periods of radio silence. The newbies in this scam space, the journalists claiming to be the heroes that “blew the whistle” or warned the FCA, are just chasing big headlines for their editor on today’s flavour of the month: mini bonds. Soon the mini bond victims will be forgotten just like the victims of Defined Benefit Pension transfers. The blood sucking journalists will move on to the next headline. I have no time for these insincere upstarts because they don’t stay in it for the long haul.

Victims are on their own by and large and still ignorant. No one seems to care and there is no help from any quarter. They face a retirement with a significantly reduced standard of living and that’s the hard truth of the matter. There will be no “flood of similar cases”.

Pension scams have been destroying lives for more than a decade. The scammers cause poverty, marriage breakdowns and even death. Death caused by stress-related illness. And death by suicide.

A typical pension scam involves an unlicensed person pretending to be a financial adviser. This is illegal. But it goes on all the time, in the UK and offshore.

All pension scams result in the loss of part or all of the pension. And, sometimes, crippling tax liabilities on top.

Most pension scams start with a pension transfer that should never have happened. And finish with investments which are unsuitable and risky.

One particular pension scam involved an unlicensed introducer called Terence Wright (i.e. a scammer posing as a financial adviser). Wright ran a business in Spain called CLP (Commercial Land and Property).

Professor Gerard McMeel QC of Quadrant Chambers

In 2012, Wright conned hundreds of victims into transferring their pensions into a Carey SIPPS (SIPPS stands for Self Invested Personal Pension Scheme). The sole purpose for these transfers was to invest the pension funds in assets which paid the highest commissions to Wright and the other scammers involved.

One of these victims, a lorry driver called Russell Adams, felt so strongly that he had been defrauded, that he took his case to the High Court. But, in the first round, he lost.

In the landmark High Court appeal ruling, the Adams v Carey case resulted in SIPP provider Carey being ordered to put things right. After the previous judge failed to give Mr. Adams the justice he deserved, a victory was obtained which should help prevent future pension scams.

In the appeal, the judge – Justice Andrews – ruled that the case involved:

Justice Geraldine Andrews

“opportunities for unscrupulous entities to target the gullible”

She ordered Carey Pensions to refund Mr. Adams his pension. She mentioned “financial crime” and placed much of the blame squarely at the door of the unlicensed introducer – Terence Wright of CLP – who gave investment advice illegally.

The Adams v Carey case is likely to herald a flood of similar claims against pension providers like Carey. So let’s have the drains up on this case – and break down the main ingredients. Then we’ll see what lessons can be learned. And how similar pension scams could be avoided in the future.

SO HOW DO PENSION SCAMS WORK?

It all starts with HMRC.

A British pension scheme (whether a personal or occupational one) starts with an HMRC registration number. The good, the bad, the ugly – and the downright stinky – pension schemes are all registered by HMRC. And in the case of occupational schemes, by the Pensions Regulator as well.

HMRC makes no distinction between schemes set up for bona fide reasons, and those which are set up for scamming. HMRC doesn’t care – and anyway they say that consumer protection isn’t their responsibility.

WHAT IS A PENSION SCHEME?

A pension scheme is just a wrapper – like a cardboard box or a paper bag. On its own, a pension scheme can’t do any harm. Try looking at an empty cardboard box for a moment and ask yourself how much damage it could do. Watch it carefully – and see if you can spot it doing anything dangerous or sinister. I reckon that however closely you watch it, nothing untoward will happen (although your cat might curl up inside it and take a nap).

Christine Hallett CEO of Carey Pensions

Remember that it isn’t the box itself that could be dangerous, but the people handling it and putting things inside it. An empty box could become a delightful xmas present if filled with mince pies and chocolate. Or, if filled with dynamite and nails, it could become a deadly bomb which could kill and maim hundreds of people.

Whether a pension scheme is a personal or occupational pension, a SIPP, a SSAS, a QROPS or a QNUPS, it is just an empty wrapper. A harmless container which can be used responsibly by good people, or recklessly and even maliciously by bad people.

The lesson is that the cardboard box itself doesn’t do the damage – it is the people who handle it.

The Adams v Carey case will inevitably be a turning point for the pension industry – both in the UK and offshore. There will now be a big question mark over the word “self” in the phrase “self invested”. This phrase may have to be upgraded to “sort of self invested”. This is because the successful appeal makes it clear there is still a duty by the trustee to make sure nothing happens to pension funds which is clearly bonkers.

Mr. Adams was one of 580 Carey SIPP members who were all invested solely in store pods in the space of one year. And none of them had a licensed financial adviser. To put this into context, nearly 50 people a month transferred their pensions into a Carey SIPP and voluntarily invested the whole lot in store pods.

A reasonable person might ask why Carey didn’t ask themselves why there was this sudden stampede coming out of the blue? Why so many people wanted to invest their entire pension funds into the same illiquid property asset? Why so many different people were advised and represented by an unlicensed introducer in Spain?

Perhaps after the first month, Carey might have raised a bit of an eyebrow. After the second and third months, Carey’s CEO Christine Hallett might have decided to question whether Terence Wright of CLP in Spain was a suitable person to advise so many different people to invest in the exact same asset.

But she didn’t. She let the torrent of victims of Terence Wright’s unlicensed “advice” continue unchecked. Hallett is described on her LinkedIn profile as:

“one of the country’s most knowledgeable experts in the SIPP world and a highly respected leader in the financial services industry”

And yet she didn’t check the FCA website to see whether Terence Wright was legit. Had she done so, she would have found a clear warning that he was providing financial advice without a license. And that is a criminal offence.

Terence Wright was involved in both the pension transfer process and the investment process. And yet he had no qualifications or license to do either – and there was a clear FCA warning against him.

The ordinary man in the street may routinely check their emails, Facebook and Twitter, but would be unlikely to check the FCA website. However, a “highly respected leader in the financial services industry” ought to have checked the FCA website as routinely as any normal person would check their social media.

The Carey “Key Features” document stated that the member was responsible for investment decisions. And that is where the “self” bit comes from in “Self Invested Personal Pension”. But Carey also recommended that a suitably-qualified adviser ought to be used – to make sure that the pension transfer was in their best interests.

There is nothing wrong with having some illiquid commercial property in a pension portfolio. But the key to all investment decisions is “diversity” and not putting all one’s eggs in one basket (or cardboard box – or indeed pension wrapper). Had Russell Adams been advised by a proper, qualified, licensed adviser, he would have been warned against investing his whole fund in any one asset. To put everything into one single investment is always high risk and irresponsible – no matter how solid and safe the asset may be.

To be fair to Carey, they did eventually sever terms of business with CLP. But for some extraordinary reason they still acted on CLP’s investment recommendations until eventually deciding they were no longer suitable in April 2013 – nearly a year later.

The appeal judgement concluded that the Carey SIPP was recommended by Terence Wright solely for the purpose of investing in the store pods (and the accompanying introducer commissions). And that all the “advice” given by CLP was part of an inextricably-linked bundle of transactions which included the transfer and the investment.

This “bundle” of advice consisted of the transfer out of the original pension scheme; the transfer into the Carey SIPP; the investments (in the store pods). And the whole kit and caboodle was in contravention of article 53 of the FCA regulations.

Carey’s own documentation admitted that investments of less than £50k in a Full SIPP were not economically viable. This should have alerted Carey itself to the fact that many of the 580 people advised by CLP would inevitably suffer from disproportionately high fees.

The judges in Russel Adams’ case summarised the reasons for allowing the appeal:

i) Dealing with an unregulated intermediary

ii) Admitting an asset which could not be valued

iii) Proceeding with the store pod investment despite concerns in May 2012

Carey, now called Options, may come back for round 3 if they are given leave to appeal this judgement. Whether they are allowed to do this or not, this leaves the pension industry with a 100% crystal-clear message:

DO NOT DEAL WITH UNLICENSED INTRODUCERS

Most of the things that have gone wrong, in the past decade, are because of advice given by unscrupulous, unqualified, unlicensed “introducers”. And their mission is clear: to encourage victims to do what earns the introducer the most money – even though it will inevitably cause loss and damage to the victim.

The pensions industry worldwide must now get behind a coherent and determined campaign to stamp out the scourge of the unlicensed introducer. Confidence needs to be rebuilt in British and overseas pensions. And that can only be done by outlawing the rogues and scammers who have done so much damage to so many thousands of victims.

Terence Wright’s luxury mansion in France

It is, indeed, ironic that Terence Wright of CLP was operating from Spain – the capital of the world of pension and investment scams. He was able to ruin UK-residents’ lives all the way from the Costa del Sol. He was given access to a harmless pension wrapper, and managed to transfer hundreds of pensions which should have been left where they were.

But the real story is that Terence Wright and his wife Lesley made a fortune out of scamming Russel Adams and hundreds of other victims. And he is still at it from his new luxury home in France: a stunning mansion in the Dordogne region of France:

With his own private plane and stables for his wife Lesley’s collection of horses, he now lives a life of luxury and commutes to Dubai to pursue his lucrative “business” activities.

Terence Wright and his wife Lesley

This is what is so sad and disgusting about all the scammers behind the many hundreds of pension and investment frauds this past decade or so. They reap eye-watering rewards. Despite a few limp attempts by the SFO to bring scammers to justice they rarely face jail sentences.

The pensions industry needs to get behind a solid campaign to bring these criminals to justice. Lorry driver Russel Adams did his bit to kick this initiative off. It is now up to the pension providers themselves to take this to the next level. And finally restore confidence in British and overseas pensions.

The Spanish criminal trial of so-called “financial advisers” in Denia has exposed the widespread fraud routinely committed in offshore financial services for over a decade.

This particular stage of this particular trial may be directed at just eight members of Continental Wealth Management and Premier Pension Solutions. For now. But the case – brought by Pension Life – needs to be extended to all parties who have committed similar offences in offshore financial services.

Spain is the second-largest expat jurisdiction in the world – after Australia. More than three quarters of a million British expats have settled in the Spanish sunshine. That’s over half the total in the whole of Australia. And these Spanish-resident expats are sitting targets for pension scammers.

It is not unusual for Brits to be suspicious of foreigners in any country. Expats typically veer towards their own countrymen. They are notorious for being suspicious of foreign food and customs. Hence, the depressing fact that it is British scammers who relieve British victims of their pensions and life savings.

And this is why so many British expats – especially in Spain – fall prey to bogus “financial advisers” flogging bogus life assurance policies provided by bogus insurance companies – like Quilter International headed up by Peter Kenny.

The facts of this criminal case are indisputable. One thousand victims were scammed by Continental Wealth Management. Between 2009 and 2017, these victims lost many millions of pounds’ worth of pensions and life savings. And much of this was facilitated by Quilter International (formerly Old Mutual International).

So how were these losses caused? What on earth went wrong? Financial services – in any country – should be a safe industry which investors can rely on. Depend on. Why have so many expats – not just the Continental Wealth Management victims – lost so much money?

Who and what is to blame for the loss of hundreds of millions of pounds?

The short version of the answer is: “COMMISSIONS”. Offshore advisers get rich by selling products for commissions. What they don’t sell is independent financial advice. Proper independent advice (provided by a correctly and properly qualified and licensed adviser) is about recommending an appropriate investment strategy which is in the best interests of the client. And, of course, charging a reasonable and commercially-viable fee for such advice.

But that rarely – if ever – happens in offshore, expat jurisdictions. What is cleverly presented as “advice” is generally just a dishonest ploy to sell a client unsuitable products which they don’t need and that will make the salesman the most commission.

The orchestrators, facilitators and architects of all this fraud are the “life offices”. In practice and in reality, these companies are more about death than life. Their business is about destroying life savings and pensions – while enriching the pockets of fraudsters.

There are various ways to combat this widespread fraud facilitated by the life offices:

Bring criminal proceedings against ALL those who have defrauded their clients – from bogus, unlicensed advisory firms to the life offices themselves

Ensure all so-called advisory firms (sometimes calling themselves “wealth managers”) are correctly licensed in the jurisdiction where they provide advice

Make it mandatory for all advisers to be properly qualified to provide financial advice

Ban all firms without an investment license from providing investment advice

Educate consumers to only use advisory firms which openly disclose their professional indemnity insurance on their website

The bald truth is that if the life offices – such as Quilter International, Friends Provident International and RL360 – were closed down, this widespread fraud would stop.

The only way this fraud keeps going so vigorously and relentlessly, is the terms of business given by the life offices to the scammers. And, of course, the fat commissions the life offices pay to them. As well as the toxic, risky, high-commission-paying investments the life offices put on their “platforms” for the scammers to use (and abuse).

You only have to look at Continental Wealth Management to see how quickly a scamming firm will collapse once life offices withdraw terms of business. The life offices are the life blood of scams and scammers.

Without the facilitation of the “death” offices (Quilter International, Generali, SEB etc.) frauds such as Continental Wealth Management could not have taken place. The blood of all those who have died wretched, lonely deaths – and those who are suicidal – is squarely on the hands of Peter Kenny and his various cronies.

The bank statements of Continental Wealth Management show the repeated amounts of fat commissions paid by Quilter International, Generali and SEB. And these amounts were paid willingly and cheerfully in the full knowledge that every payment meant more lives damaged; more funds destroyed; more miserable deaths.

Quilter and their associates had reported on the victims’ losses for a decade; produced valuations and transaction histories evidencing the repeated, relentless fraud. And yet Quilter (and the other death offices) did nothing – just kept on and on facilitating the same fraud: repeat, repeat, repeat.

While the “advisers” from Continental Wealth Management and Premier Pension Solutions stand trial – the hundreds of victims have to listen to the defendants’ offensive denials and excuses. But, worst of all, the distressed and impoverished victims know that the life (death) offices should also be on trial – standing shoulder to shoulder with the scammers themselves.

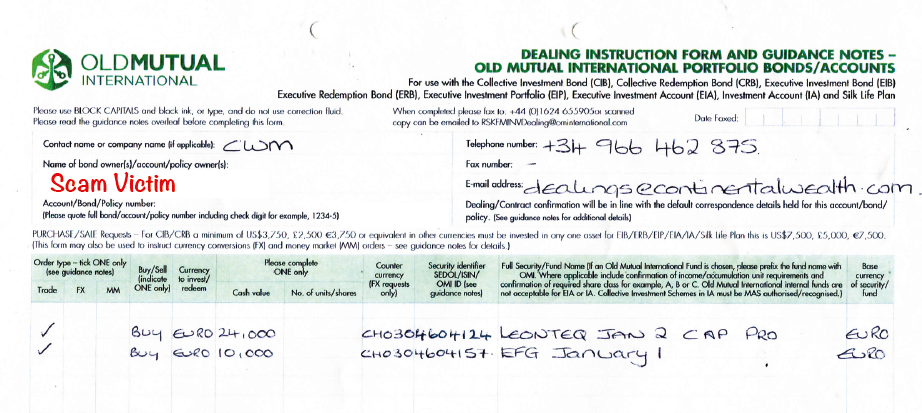

The cause of the investment losses in the Continental Wealth Management case was almost exclusively toxic, high-risk (and high-commission) structured notes. These are complex investment instruments called “derivatives” and should only ever be used for professional or sophisticated investors. They are certainly completely unsuitable for ordinary people (who are classed as retail investors) or for pension schemes.

High-risk structured notes are big business for the death offices. Quilter International (formerly Old Mutual International) has historically onboarded over 100 new structured products per month. In the case of the Continental Wealth Management fraud, it was the structured notes – from Leonteq, Commerzbank, Royal Bank of Canada and Nomura – which caused the terrible investment losses. These toxic, high-commission investment products – so beloved by the scammers because of the high commissions – were responsible for the destruction of millions of pounds’ worth of pensions and life savings.

Quilter International knew perfectly well that these toxic products – totally unsuitable for retail investors – paid 8% commission to the scammers and a further 8% to 10% to the “arrangers”. They knew perfectly well – and admitted internally to their “asset review committee” – that these products were risky and “not good value”. But they still allowed the scammers (to whom they gave terms of business) to keep selling them.

Quilter has also admitted that they had 2,047 structured products in total, and that the average holding per product was £243,654.03; that the smallest holding was £67.54 and the largest holding was £5,350,833.60. Quilter was concerned that there was a reputational risk to Quilter for allowing these structured products to be held within their offshore bonds. They also acknowledged that these products carried excessive commissions and were causing “suboptimal customer outcomes”. However, their concern for their own “reputational risk” did not extend to concern for their victims.

Quilter has tried to wriggle out of culpability for the victims’ losses by claiming that investment product “suitability” is the responsibility of advisers. And that these so-called advisers are participating in a “race to the bottom”.

However, the advisers are mostly scammers to whom Quilter has cheerfully given terms of business. And they are winning the race to the bottom by several lengths. If Quilter withdrew terms of business from all the scammers, the race wouldn’t even take place at all. In fact, all Quilter would have to do would be to ensure that all advisers are qualified and licensed – and that investors’ risk profiles are correctly respected – and the fraud would stop instantly.

But until Quilter and all the other death offices are put on trial for fraud themselves, this crime is going to continue. And victims are going to keep losing their pensions and life savings – and dying in abject poverty.

As an interesting post script, Quilter have posted a warning about scams on the internet. Their disingenuous claim that “Your security is our priority, so we have reacted quickly to help you and the financial advisers we work with to spot fraudsters” is ironic and cynical. Quilter themselves routinely work with fraudsters who pose as financial advisers – and who have no license or qualifications to provide financial advice.

January 28/29 2021 saw the cross examination of Stephen Ward in Pension Life’s criminal case in the Denia court. Ward gave the judge an elaborate explanation as to how and why none of the Continental Wealth Management pension and investment scams were his fault.

Ward provided the pension transfer “advice” to hundreds of Continental Wealth Management victims – facilitating the handing over of millions of pounds’ worth of personal and occupational pensions into the hands of well-known, firmly-established scammers. Once out of the relative safety of the UK, and into the offshore abyss, the scammers made millions out of undisclosed commissions on the victims’ life savings. The investments were, of course, largely worthless. Victims lost somewhere between a small percentage and a large percentage – with a few losing 100%. And a few more even going overdrawn on their pension accounts.

Ward’s Spanish firm Premier Pension Solutions, worked as “sister company” to Darren Kirby’s and Jody Smart’s Continental Wealth Management. After Ark in 2011, Ward moved straight onto the Evergreen New Zealand QROPS liberation scam. And CWM did the cold calling to sign up 300 victims to the toxic £10 million pension scam and so-called “loans” from Ward’s own finance company – Marazion.

Ark (and indeed Evergreen) victims may well want an answer to the question: why hasn’t Ward been prosecuted before now? The lack of any previous criminal proceedings against him, for the many other scams he was involved in, is – indeed – astonishing.

Capita Oak, Westminster, Southlands, Headforte, London Quantum et al – could all have been prevented had Ward been behind bars. Victims of all of those scams might still have their pensions had it not been for Ward.

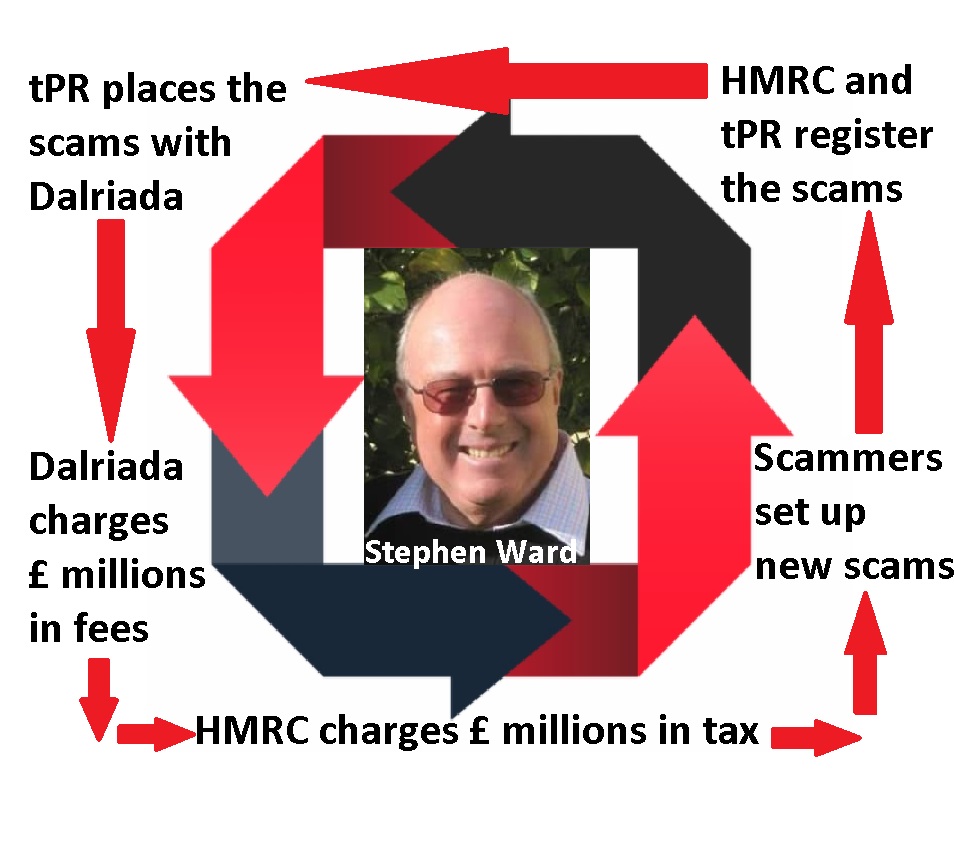

Part of the answer may lie with Dalriada Trustees. The firm was appointed by the Pensions Regulator to the Ark schemes as independent trustee on 31st May 2011. Over £27 million worth of pensions had been transferred from safe, professionally-run pension schemes into the six Ark schemes. Nearly 500 people are affected – many of whom had received reciprocal “loans” on the advice of Stephen Ward and his very convincing associates. Ward had assured all the victims that the loans would be “tax free”. But, of course, HMRC does not share that view – and the tax trial is starting in March 2021.

HMRC is looking to tax all those who did get “loans” and also all those who didn’t. HMRC’s argument is firstly that even if members didn’t get a loan, they had made the transfer with the intention of getting a loan, and secondly that they “made” a loan.

One of the first questions I ever asked Dalriada back in 2013 (appointed by the Pensions Regulator – who registered the Ark schemes in the first place) was:

“Why didn’t you bring criminal proceedings against Stephen Ward and all the other scammers who set up and ran Ark?”

Dalriada’s answer was:

“We didn’t think it was within our remit”.

So what is (or was) Dalriada’s remit? And has it fulfilled that remit? And how much has it cost?

DALRIADA’S REMIT:

To suspend the Ark schemes so that no further “loans” could be made; no further victims lost their pensions; no further toxic investments could be made

To investigate the schemes to find out how they had been run and where the money had gone

To recover the toxic investments and return the money to the schemes

To liaise with the members and keep them informed

To liaise with HMRC on the unauthorised payment tax liabilities

The above points are all guesses on my part. Certainly, Dalriada has admitted that they didn’t really know where to start at the beginning. They had no idea what they would find, once they started investigating, and no clue as to how much work was going to be involved.

Dalriada has, indeed, recovered some of the toxic investments in the Ark schemes. But communications with the members have been limp at best. Dalriada has spent a lot of time, effort and money on taking proceedings against the victims themselves to recover the “loans”, but seems to have spent zero time, effort or money on pursuing the scammers.

Most important of all, Dalriada has not invested any of the money left in the Ark schemes – so members (victims) have missed out on the longest investment bull run in history. Bottom line: there’s been no growth in the value of the Ark funds – only shrinkage. Had the funds been invested in something as simple as a low-cost tracker fund, they could have grown by some 330% at least.

Of the original £27 million in the Ark schemes, Dalriada has spent more than £7.4 million on trustees’ and lawyers’ fees between 31st May 2011 and 31st May 2020. But isn’t it reasonable to ask: “Why couldn’t Dalriada have spent some of that money on criminal proceedings against Stephen Ward and some (or all) of the other scammers?”

Dalriada Trustees have been appointed to more than 100 pension scams in the past ten years (by the Pensions Regulator). But there is no evidence that any of the scammers – especially the prolific Stephen Ward – have ever had any CRIMINAL action taken against them by Dalriada in an effort to prevent further scams.

Kelly reports that “Pension scam victims have lost millions of pounds more to the government-appointed trustees hired to get their money back.” and that “Victims say Dalriada Trustees ‘inexplicably’ held their recovered retirement savings for years and then only paid a fraction of their money back.”

Kelly has been to meet me in Spain several times. He attended the Denia court for the first set of cross examinations in 2020, and reports that “tens of thousands of savers had lost up to £10 billion in rogue schemes that looked safe because they were registered by HMRC and overseen by the Pensions Regulator”.

Kelly goes on to cite the case of one victim who waited seven years to have his £157,000 pension pot returned to him by Dalriada. But they deducted £90,000 in charges before handing it back to him. And this was after Dalriada had rescued the fund in full, before the scammers had managed to invest the money in toxic, commission-paying assets.

With 5,400 pension scam victims having Dalriada as their trustees, it is perhaps time to ask whether this is a tenable solution. Scammers could, realistically, be forgiven for thinking that once Dalriada takes charge, this is merely a license for the next scam, and the next one, and the next one…… Because, Dalriada is never going to report the scammers for fraud. So they are free to keep on scamming people out of their pensions repeatedly.

One of my all-time favourite comedy lines is Greg Davies describing his middle-aged love life as “like trying to stuff a marshmallow up a cat’s arse”. My second-favourite comedy line is “Andrew Bailey has been such a failure at the FCA, that we’re going to put him in charge of the Bank of England”. My third favourite is “the FCA’s practitioner panel is going to be headed up by Paul Feeney of Quilter”.

With the exception of Greg Davies’ somewhat risqué pun, the other two are both true and sickeningly serious.

Victims of Quilter (previously Old Mutual International and Skandia) will be appalled that such a pariah of financial services can be held up to be an example to financial services practitioners.

It might, of course, be that I am mistaken – and that Feeney is being brought in as an example of how financial services should NOT be run, and how financial advice should NOT be provided.

But, sadly, I think the “old boys’ network” has worked its magic and the FCA elite have closed ranks with Quilter’s elite, to dominate control over pension and investment scams. It is clear that neither the so-called “City Watchdog” nor the insurance giant – specialising in pointless insurance bonds and toxic investments – want to see financial services cleaned up.

If any financial services consumer is unclear about the FCA’s multiple failures in the matter of the collapsed London Capital & Finance “bond”, they only need to read Bond Review’s piece on the Dame Gloster report. Along with “The FCA told potential investors that LCF was not a fraud, and FSCS protected“, “the FCA took no follow-up action to verify that all LCF’s investors qualified as high-net-worth and sophisticated” and “The FCA consistently treated LCF’s unregulated bonds as not its problem“, Dame Gloster pulls no punches when she outlines the FCA’s many disgraceful and negligent failures.

From Andrew Bailey at the top, to the members of FCA staff who defecated on the men’s bathroom floor at the bottom, Dame Gloster’s report demonstrates that the FCA simply doesn’t understand pension and investment scams. Apparently, an FCA supervisor had admitted that “there is little training on how to identify financial crime within the FCA’s Supervision division”.

Put simply, if the FCA can’t keep its own bathrooms clean, how on earth can it help clean up the crap in the world of financial fraud?

The FCA clearly does not understand that unregulated, high-risk, toxic investments are simply not suitable for ordinary retail investors. And this is why the appointment of Quilter’s Paul Feeney is so anomalous: Quilter has for years specialised in peddling these kinds of high-risk investments to low-risk investors. The graveyards of thousands of Quilter victims’ investment portfolios is littered with the rotting remains of many funds and structured notes.

A regulator’s “Practitioner’s Panel” should ideally be headed up by someone who understands how financial services firms should be run; someone who eschews the fraudulent and disloyal practices of the “cowboys” and “chiringuitos”; someone who has shown the will to outlaw illegally-sold insurance bonds whose sole purpose is to make thousands of victims poor and dozens of scammers rich.

Instead, the FCA’s panel is going to be under the control of someone who has actively promoted high-risk investments to low-risk investors.

So, it would seem there is no hope that the FCA will ever be reformed – just as there is no hope that the top dogs at Quilter will ever brought to justice for facilitating so much financial crime. The two rogue organisations are going to jog along cosily, side by side, with no remorse for their own failures and culpability.

It is hard for pension and investment scam victims to comprehend the apathy towards reform of regulation in the UK. Experts such as Henry Tapper, Mick McAteer, Martin Hague, Paul Carlier and Gina Miller have long banged the “reform” drum. But this has largely fallen on deaf ears. And, of course, Dame Gloster’s report will be largely ignored.

This is all cronyism at its worst. And shows that neither the Treasury nor Parliament truly understand what is so very wrong with financial services in the UK (and also offshore). Select Committees, such as the Work and Pensions one chaired by Stephen Timms, can debate all day long – but until the FCA is scrapped and rogue “wealth” and “life” (in reality, poverty and death) companies like Quilter are shut down, nothing will change.

Dame Gloster has written about the “wickedness” of the FCA’s failures to protect the public (from investment scams such as London Capital & Finance). Part of this evil is the failure to recognise the dangers of unlicensed scammers – the motley assortment of unlicensed “introducers” – both onshore and offshore. But, of course, this is what Quilter’s business is based on – so the appointment of Quilter’s Paul Feeney will only protect and nurture this branch of financial crime.

Quilter has for many years given terms of business to assorted scammers, prostitutes, murderers, fraudsters and conmen (and women). With the acceptance of thousands of investment instructions from these unruly hordes of low-life, unlicensed, unqualified criminals, Quilter has built up a successful and profitable business based on ruining innocent victims’ lives (and killing some of them in the process).

Dame Gloster’s excellent, comprehensive and severely damning report provides almost 500 pages of details of the FCA’s disgraceful failings.

But if you haven’t got time to read it, just read FT Adviser’s one-page article on “Quilter boss Feeney to head up FCA panel”. Then zoom down to the bit that says: “Paul has served on the panel for a number of years and appreciates the important role it plays in ensuring our regulation is targeted and effective.”

Then go and have a good cry. And a packet of marshmallows.

In the past decade, millions of pounds of pensions and life savings have been destroyed in Spain. Much of this has involved insurance bonds (OMI, SEB and Generali) – as well as all other popular expat countries. Only by benefitting from lessons learned so painfully by those who’ve already been scammed, can new potential victims arm themselves against the scammers.

Pension scams always start with a so-called “financial adviser” or “wealth manager” or “retirement consultant”. Sadly, it is almost always British “advisers” which scam British expats.

Potential victims need to understand what to look out for – and avoid. Here are the essential “must haves” for proper, professional financial advisers (in other words people who sell advice, not products):

LICENCE – The firm must be licensed – both for insurance and for investment.

QUALIFICATIONS – The adviser must be qualified – and a link to proof of the qualification clearly visible on the firm’s website.

LEGACY – There must be no legacy of previous scamming within the firm.

INSURANCE – There must be a professional indemnity insurance policy in place.

NETWORK – If the firm is an agent of a network, there must be an up to date copy of the agency agreement freely available.

INSURANCE BONDS – The firm must not sell insurance bonds illegally.

UNREGULATED FUNDS AND STRUCTURED NOTES – The firm must not invest clients’ funds in unregulated or esoteric funds, or structured notes.

COMPLIANCE – There must be a proper compliance function in place.

MANAGEMENT AND TEAM – All members of the team must be clearly visible on the website – along with details of who is in charge and responsible for the firm’s activities and compliance.

COMMISSION POLICY – The firm’s policy on undisclosed commissions must be clearly visible.

When I Googled the term: “Financial Adviser Spain” just now, the top results that came up for me were:

Blacktower Wealth Management

Blevins Franks

Finance Spain – Patrick Macdonald

Spectrum IFA

Chorus Financial

Abbey Wealth

Alexander Peter

Axis Consultants

Logic Financial Consultants

Harrison Brook

Seagate Wealth

When I changed the search term to: “Pension Advisor Spain” or “Wealth Advisor Spain” I also got the following:

deVere Spain

Mathstone Financial Management

Pennick Blackwell

SJB Global

United Advisers Group

Indalo Partners

Trafalgar-International

Fiduciary Wealth Management

And one firm which won’t come up at all, no matter how hard you search, is:

Roebuck Wealth – run by Paul Clarke

Plus one which only comes up if you know what to search for:

So let’s take a look at some of these firms to see what we can learn from their websites and see if there are any warning signs for potential victims:

Blacktower Wealth Management – Always look at the bottom of a firm’s website to read the small print and see how the firm is licensed. Blacktower is licensed by the Gibraltar Financial services Commission for both insurance mediation and investment advice. Why Gibraltar? Why not Spain? Gibraltar has a long history of facilitating and licensing scams and scammers and the Commission even employs one itself. The website claims to have “Consultants throughout our offices in Europe” – and this worries me. What is a “consultant”? Why not talk about advice, not consultancy?

Looking at the directors and “international financial advisers” of the firm, there are quite a few. Associate Director Tim Govaerts claims to be qualified with the Chartered Institute of Insurers up to Level 3. But the CII register says they’ve never heard of him. Richard Mills claims to be qualified with both the CII and the CISI, but both registers say they’ve never heard of him. Quentin Sellar claims to be qualified with both the CII and the CISI, but only the latter has heard of him. Clifford Knezovich also claims to be qualified with the CISI but does not appear on the register. Lucia Melgarejo is another member of the team who also claims to be qualified. I met her a few years ago, when a colleague of hers had cold called me, and she told me that she was too busy selling to get qualified.

The member of the Blacktower team which worries me the most is Terry Tunmore – as he was one of the scammers at Stephen Ward’s Premier Pension Solutions. Tunmore certainly soils the reputation of this firm, and should not be employed by any firm holding itself out to be professional and to have integrity.

Under the Licensing section of the website, the firm is immediately getting potential clients warmed up to insurance bonds and “wrappers” – and states that it has permission to recommend them and provide investment advice on the underlying portfolios. This should worry any potential client – and ring loud alarm bells – as this indicates a clear intention to use bond providers such as Quilter, SEB, Generali or RL360 – and earn hidden commissions. These products are deemed to be invalid under Spanish law, and are routinely sold illegally in Spain.

Blacktower’s website makes no mention (that I can find) of compliance or their professional indemnity insurance policy. It also worries me that Blacktower has so many “agents” – and without hard evidence of a robust compliance function, I think there is a risk that some of these agents could well be acting as unsupervised “feral” salesmen, rather than bona fide financial advisers.

Blevins Franks – Well-known firm with offices in Spain, and other European countries. The team in Spain all have titles such as Partner, Private Client Manager or Regional Manager – and there is no mention of any of them being genuine financial advisers. In Spain, Partners Christopher McCann, Brett Hanson, Paul Montague, Andrew Southgate, Henry Rutherford and David Bowern all claim to be qualified with the London Institute of Banking & Finance, but none of them appears on the member register. Steven Langford claims to be CII qualified but does not appear on the register. With so many members of the team claiming – falsely – to be qualified, this should ring loud alarm bells with any potential victims. We know that Blevins Franks routinely puts all clients into a Lombard insurance bond – which means they are committing a criminal offence in Spain.

Insurance bonds are illegal and invalid for the purpose of holding investments in Spain, and the usual manner of selling them is also a criminal offence. An insurance bond provides no benefits or protection for investors – and should never ever be used inside a pension (QROPS). Blevins Franks also has a close tie with Russell funds – and routinely invests their clients’ funds in Russell. There’s nothing bad about Russell – but there’s nothing good about them either. A portfolio should always be a well-spread mixture of funds from the whole market – not a narrow selection of investments from one provider. I can’t see any information on the Blevins Franks website about their professional indemnity insurance, compliance or commission policy. All in all, I think there are too many risks with this firm and it should be avoided.