There are many different types of pension scam – just as there are many types of genuine pension scheme. This can sometimes make it difficult to tell the difference so we are her to help you inform you about, what is a pension scam.

Fortunately, there are some common tell-tale signs that mean you could spot a scam and avoid it:

Cold calling: always be suspicious of a cold caller. This can come as a text, phone call, email or even a smart-looking individual at your door!

Some cold callers may even imply that they are from the government or another government-backed organisation.

THIS WOULD NEVER HAPPEN!

Hard sell: when your smart-looking/sounding “adviser” won’t take “no” for an answer and pressurises you into an on-the-spot decision

No land-line contact phone number: the only contact they give consists of an email, mobile or PO Box address

Use of words like ‘pension liberation’, ‘loan’, ‘loophole’, ‘free pension review’ or ‘one-off investment’

Unrealistic claims:

You can unlock your pension before 55

Promises of tax advantages

investment is ‘unique’, ‘overseas’, ‘environmentally friendly’, ‘ethical’ or in a ‘new’ industry

Low risk but high return investments (THEY DON’T EXIST!!)

What the scammers don’t tell you is that taking any part of your pension early (before 55 years of age) DOES result in tax charges. These charges can be up to 55% of the amount you take – even if you were told it was a “loan”.

With HMRC on your back for this tax demand, it will be hard to remember the pleasure of the money you received. Plus, whilst you are distracted with your tax demand from HMRC, it is likely that the rest of your pension fund is taking a nasty tumble.

Pension scams can involve various types of pension arrangements from QROPS and QNUPS to occupational schemes and SIPPS. These arrangements are not, in their own right, bad. However, if they are used for unsuitable investments, they most certainly can be. Know about these investments means you will know about what is a pension scam.

The investments inside the schemes can range from high-risk, professional-investor-only structured notes to toxic, illiquid, risky UCIS funds (Unregulated Collective Investment Scheme – illegal to be promoted to UK residents). Whilst these types of investments are not illegal in their own right, they are only suitable for certain people with deep pockets and sound investment experience. Or, alternatively, they are totally unsuitable for pension funds – full stop.

When taking advice on transferring your pension fund you should always ensure the adviser you choose is either based in the UK OR in the country you reside/plan to reside in. Alternatively, you must make sure the adviser is regulated and qualified for pension and investment advice in the jurisdiction where you reside.

If you’ve already signed something you’re now unsure about, contact your pension provider straight away. They might be able to stop a transfer that hasn’t taken place yet.

If you think you’ve been targeted by an investment scam, please report it to the FCA using their reporting form.

If you have lost money to a suspected investment fraud, you should report it to Action Fraud on 0300 123 2040 or online at www.ActionFraud.police.uk.

If you have doubts about what to do, ask The Pensions Advisory Service (TPAS) for help. Call them on 0300 123 1047 or visit the TPAS website for free pensions advice and information.

Beware of being targeted in the future, particularly if you lost money to a scam. Fraudulent companies might take advantage of this and offer to help you get some or all of your money back.

*************************************

With out due diligence and knowledge you often won´t realise that you are the victim of a pension scam until its too late. Its best to have the knowledge so you can tell what is a pension scam and what is a genuine pension scheme.

Therefore, Pension Life has written a series of blogs about pensions, pension scammers and how to safe guard your pension fund from fraudsters. Please make sure you read as many as possible and ensure you know everything you should about your pension fund. If we can educated the masses about pension fraud we can stop the scammers in their tracks – worldwide.

Debbie Abrahams takes a stand in parliament, raising the question of, “how many more pensions scandals does she (Esther McVey, Secretary of State, Work and Pensions) need before she introduces the robust regulatory oversight needed to protect peoples’ pensions for the future?“

Debbie Abrahams (pictured) has been a Member of Parliament for Oldham East and Saddleworth since her by-election victory in January 2011. Debbie was a member of the Work & Pensions Select Committee from June 2011-March 2015 , where she led the call for an independent inquiry into the Government’s punitive New Sanctions Regime. In June 2016 she was appointed Shadow Secretary of State for Work and Pensions.

During Work & Pensions Questions, Debbie stated “100´s of 1000´s of ordinary working people have lost half of their retirement income.” Mentioning British Steel Pension Schemes (BSPS), Carillion, BHS and Capita, she goes on to highlight the government´s failure in tackling pensions governance.

BSPS were pushed into the Pension Protection Fund, the government lifeboat for failed schemes in December 2017. 122,000 members were given just months to make the decision of where to go with their precious pension funds. They had the choice to stay with the scheme, join a new one with reduced benefits set up by Tata Steel, or transfer to a personal pension plan. The Guardian reports further on this stating that, “those who do not make a decision will default into the PPF.”

The Independent released an article about the collapse of Carillion: Carillion was put into liquidation in January 2018 after racking up debts of around £900m and a pension deficit thought to be at least £587m.

The collapse of Carillion has left hundreds of workers redundant and their pension funds in tatters.

BHS had 19,000 members and a combined £571m deficit when the company went into administration in April 2016. Again reported by The Guardian, we can at least be thankful that:

Domonic Chappell is being prosecuted by The Pensions Regulator (TPR) in the latest fallout from the demise of BHS, which he bought for £1 from retail tycoon Sir Philip Green in 2015.

With all this pension turmoil, the path is paved with gold for the serial pension scammers, such as ex CWM employees.

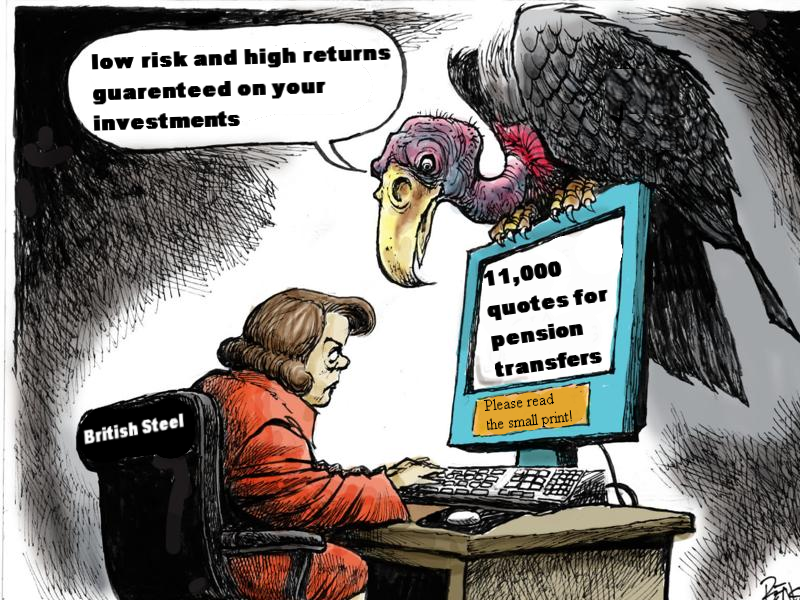

The Financial Times reported that: The Financial Conduct Authority is investigating allegations that steelworkers at Tata UK’s plant in Port Talbot were being targeted by unscrupulous pension transfer advisers. British Steel pension fund trustees have received requests for around 11,000 quotes for pension transfers. With promises of low risk and high returns on the investments, who knows how many peope have fallen victim to these vultures already?

We at Pension Life would also like to know why the government has not put in place tighter regulations on pensions to combat pension scammers. New laws need to be introduced so hard working and trusting citizens aren’t left with decimated pension funds.

We can at least be thankful that the SFO and the Pensions Regulator are pushing forward at the High Court and bringing some pension scammers to justice.

Why pension scammers such as Julian Hanson must be stopped before they burn more victims’ pension funds – such as in the Ark and Barratt and Dalton scams

Julian Hanson – why pension scammers must be prosecuted.

245 victims had their pension funds stolen by David Austin, Susan Dalton, Alan Barratt and Julian Hanson. Their company – Friendly Pensions Limited (FPL) – acquired the pension funds using cold calling techniques with promises of ‘tax-free’ payments.

The Pensions Regulator (TPR) had asked the High Court to order the defendants to repay the funds they dishonestly misused or misappropriated from the pension schemes – the first time such an order has been obtained.

But this clearly demonstrates that pension scammers should be prosecuted and jailed quickly before they go on to scam thousands more victims. Julian Hanson – an integral part of the Barratt and Dalton scamming team – was also an integral part of the Ark scam.

Julian Hanson acted as an introducer/adviser in the ARK case (also in the hands of Dalriada) in 2010/11. He scammed over 100 victims out of their pensions – totaling around £5.5 million worth of retirement savings. Hanson, in common with the many evil scammers creating scam after scam, was happy to push aside the appalling predicament of his Ark victims and stroll on to find new victims for the Barratt and Dalton scam.

Hanson had promised his Ark victims their pensions would be profitably invested in “high-end London residential property” and would grow sufficiently to discharge the 50% they were allowed to take from their funds. This, he assured the victims, would NOT be taxable.

As soon as the Pensions Regulator placed the Ark schemes into the hands of Dalriada Trustees, Julian Hanson should have been prosecuted and prevented from ever scamming pension savers again. But, sadly, he was left free to continue his evil trade. Hanson was one of a whole army of scammers peddling the Ark scam:

And hereby lies a basic flaw in the system: had Julian Hanson (along with his fellow scammers) been prosecuted and jailed for scamming the Ark victims, in 2011, the subsequent Barratt and Dalton victims might have been saved. However, it will hopefully be the last one that Julian Hanson is allowed to get away with, as his name will now be synonymous with pension scams.

The same is true for the other introducers/advisers peddling Ark who remain free to continue their trade:

Andrew Isles is still a practicing accountant at Isles and Storer

Stephen Ward went on to scam thousands more victims out of their pensions and into toxic investments as well as illegal liberation in the Evergreen QROPS; Capita Oak, Westminster, Southlands, Headforte, and London Quantum.

The mastermind behind the Barratt and Dalton scam was apparently David Austin – a former bankrupt with no experience of pension investments. He invested victims’ pension funds in truffle trees and St. Lucia timeshares, and then laundered the victims’ pension funds through relatives in the UK, Switzerland, and Andorra. Austin used a number of businesses he had set up in the UK, Cyprus and the Caribbean – including Friendly Pensions Ltd. Austin’s family clearly had no shame about where their money came from and flaunted their new-found wealth all over social media. Fortunately, this vulgar and heartless bragging made the job of gathering evidence for the High Court much easier for tPR

TPR had appointed Dalriada Trustees to the case, and with this ruling, they will be able to attempt to recoup the stolen money from the four scammers. Unfortunately it is unclear how much money is actually left to recoup as scammers are notoriously clever at hiding their ill-gotten gains offshore and presenting themselves as “men of straw”.

Nicola Parish,TPR’s Executive Director of Frontline Regulation, said: “The defendants siphoned off millions of pounds from the schemes on what they falsely claimed were fees and commissions.

“While Austin was the mastermind, all four took part in stripping the schemes almost bare. This left hardly anything behind from the savings their victims had set aside over decades of work to pay for their retirements.

“The High Court’s ruling means that Dalriada can now go after the assets and investments of those involved to try to recover at least some of the money that these corrupt people took. This case sends a clear message that we will take tough action against pension scammers.”

One the investments in the Barratt and Dalton scam was £2 million in an off-plan timeshare development in St Lucia called Freedom Bay. This same development also took millions of pounds’ worth of funds from the victims of the ARK scam. Freedom Bay is now in administration.

In this scam, operating between November 2011 and September 2014, 245 people were cold called, promises of a cash lump sum and compliant investments at 5% were promised.

The reality of what happened to the funds was:

More than £10.3 million was transferred to businesses owned or controlled by Mr Austin

Just £3.2 million of the funds was invested

False documents were made to cover these figures

Funds given back to the victims were a % of their actual funds and NOT profits

More than £1 million was paid to the “ introducers” or “agents” who conducted the cold calls

One of the victims, Colin, from South Wales, had become the full-time carer for his partner when he was approached via text message. Promised investments in the now bust St Lucia Developments, a lump sum which he planned to spend on a holiday. Having heard about the pension scams, he tried to contact the scammers with no success.

Colin, 48, said: “I should have known that it was too good to be true. I should have sought advice and asked more questions, but I didn’t.

“I had contributed towards my £50,000 pension pot, for which I had worked really hard, and now that has been taken from me.

“The loss of my pension will have a massive impact on my life. When my children finish school I will be around retirement age. There will be no money to draw down when I turn 55 and no pension savings for later life.

“I was greedy. I feel stupid for throwing away my financial future for £4,200.”

A couple, John and Samantha, both fell victim to this scam despite being advised by their pension provider that it could be a scam. They received their lump sum and were told their pension was invested in truffle trees. After reporting the case to the police, they were later informed that their lump sum was from their own funds and HMRC promptly served them with a large tax bill.

John, 46, said: “As a result of my dealings with Alan Barratt my final salary pension is in a scheme that I don’t understand the status of but which I have been told is a scam.

“As far as I know, the majority of my pension fund is invested in truffle trees but I doubt whether that is legitimate. My partner appears to have lost her pension too.

“I deeply regret ever listening to Mr Barratt.”

Why has cold calling not been banned by the government?

Why are ‘introducers’ still be used?

Why are the scammers in the Ark case not under criminal investigation?

Serial pension scammers like Julian Hanson and all the others need to be stopped now. New laws need to be introduced so hard working and trusting citizens aren’t left with decimated pension funds and huge tax bills they can’t pay.

London Quantum is a pension scheme whose trustee was a firm called Dorrixo Alliance run by our old friend Stephen Ward. That name will, of course, send a chill down the spines of many pension scam victims. Since 2010, Ward had been involved – either at the top or the bottom of the pond – in numerous pension scams. He eventually decided to “go straight” and declared that Ark was history – although Ark was far from history for his hundreds of victims who are now facing financial ruin.

Ward’s version of “going straight” was London Quantum. He had learned from the Capita Oak and Westminster scams that the value in getting involved in a pension scam comes from the investment introduction commissions. So he set about building a portfolio for the London Quantum victims which was based purely on how much wonga he could earn – rather than what was right, prudent and appropriate for an occupational pension scheme.

So what were the investments and why weren’t they right for a pension scheme?

The Scheme purchased shares in a unitised currency investment fund which traded in the top ten major currencies. The fund was regulated by the Central Bank of Ireland.

The fund was regulated but according to a regulated investment advisor the fund was inappropriate in terms of risk for the Scheme.

The fund prospectus did not specify a predicted rate of capital growth. However the scheme sponsor had previously stated a predicted return of 12%-15% per annum – an astonishing amount by any stands. But in practice, the fund performed poorly and fell over the period of the investment.

Dalriada Trustees (who replaced Stephen Ward’s Dorrixo Alliance and was appointed by the Pensions Regulator) received advice that, due to the high-risk nature of the fund and, notwithstanding the fall in the value of the investment, the Trustee should exit the fund at the earliest opportunity – irrespective of potentially heavy losses.

In 2014/15, the Scheme purchased nine corporate loan notes. Dolphin specialise in the purchasing of derelict and listed German property. The property is then sold off plan to German investors who take advantage of a specific German tax relief which allows for the recovery of renovation costs through tax allowances when purchasing units within a listed building.

The corporate loan notes were for a period of 5 years with no early exit options. The loans were due to be repaid at various dates between 9 October 2019 to 27 April 2020 depending on when the loans were made.

The loan notes had varied rates of return ranging from 12% to 13.8% per annum. All interest is rolled forward and paid at the end of the 5 year period.

This is an unregulated investment and is high risk in nature. There is no guarantee that the capital and interest will be fully repaid at the end of the relevant 5 year period. Dalriada had received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

London Quantum One Limited

The Scheme had purchased shares in London Quantum One Limited (“LQOL”). LQOL holds rights to a social media application called VIP Greetings which provides personalised messages with the use of celebrity endorsement. The original trustees paid for the LQOL shares from the scheme funds.

The underlying investment in VIP Greetings was long term and no returns were expected for several years. No early exit options exist and there is no evidence of a secondary market to sell the investment.

The returns from VIP Greeting application are highly speculative. These is no guaranteed minimum return or definitive payment date. Investors hold no security over any physical asset.

A number of valuations in relation to the VIP Greetings investment were received prior to the appointment of Dalriada Trustees. The valuations appeared highly speculative. In addition, the valuations were not made at the time that the Scheme purchased the investment.

Dalriada suspects that the investment holds little, or more likely, no value. They are not confident that any return will be made to the Scheme.

Between 2014 and 2015 the Scheme purportedly invested in 17 car parking spaces in a car park near Glasgow Airport. The investment was offered by Park First Glasgow Limited who lease parking spaces to investors, in this case the London Quantum, and then sub lease the parking space back.

The investor enters a lease for a period of 175 years (the maximum allowed under Scottish law). The parking spaces are then sub-leased back for a period of 6 years. The sub-leases can be terminated by Park First after 2 or 4 years, or at any time with not less than 10 days notice if it has found a substitute sub-tenant.

There is a ‘guaranteed buy back’ policy which outlines under what circumstance Park First will buy back the parking spaces. Park First has full discretion in this regard and is under no obligation to buy back the spaces at any point. In short, there is no guaranteed exit option.

The investment offers a guaranteed rate of return of 8% per annum for the first 2 years. To date payment in line with the 8% return had been received. £27,200 was received in February 2015 and a further £27,200 was received in February 2016. No payment was received for February 2017.

This is an unregulated investment. Park First operate the car parking space on behalf of the investor for an annual fee. The parking spaces generate income which is ultimately passed back to the investor each year.

Dalriada received advice that the investment was illiquid and inappropriate for the Scheme and early exit was recommended.

Dalriada have tried to recover the monies paid to Park First arguing that the legal documentation was never fully completed by the previous trustee and that the contracts were ineffective. Park First has rejected this request and is insisting that the contracts are valid and that there is no scope for Dalriada to be refunded.

On 20 August 2013 the Scheme invested in an unsecured loan note issued by the law firm Malletts Solicitors Limited.

The loan note had an investment period of 6 years with an obligation for the note holder to redeem 25% of the note per annum after year 2. No early exit options existed.

The loan note purported to return 8% per annum payable half yearly.

Interest or redemption payment have not been made by Mallets. To date the Scheme should have received payments totalling £3,280.00 as per the contractual documentation.

Loan notes have been issued by Mallets in an attempt to raise funding for an internal ‘legal hub’ project. The loan note was unsecured.

Dalriada contacted Malletts to obtain additional information in relation to the investment. Mallets have refused to explain how the Scheme came to be invested with them and have only provided minimum details

Dalriada had received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended. They sent Malletts a number of formal requests to exit the investment however Malletts did not respond.

Malletts Solicitors Limited went in liquidation on 11 November 2016. Dalriada submitted a proof of debt respect of the loan note but the fact it has gone into liquidation suggests prospects of recovery are poor.

On 31 January 2015 the Scheme invested in a corporate bond with Colonial Capital Group Plc. Colonial operates in the distressed US social housing market and have issued a number of bonds.

The corporate bond is for a period of 3 years. No early exit options exist. The bond has a fixed return of 12% per annum. Interest will be rolled forward and paid at the end of the 3 year investment period.

This is an unregulated investment. Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

Dalriada sent Colonial a formal request to exit the investment. Colonial responded and confirmed that an early exit was not available as Colonial may only redeem all or part of the bonds on a pro rata basis for all investors. It would therefore not be possible to facilitate an early exit for the Scheme.

Colonial Capital Group Plc was then placed into administration on 8 March 2017. Dalriada has issued a proof of debt in relation to the corporate bond but, again, the fact the company has gone into administration suggests prospects of recovery are unpromising.

The investment is in hotel rooms in a hotel development by The Resort Group. The hotel has recently been completed in Cape Verde and investors purchase a right to benefit from the profits and interests of specific pieces of the development. Investors do not own the land nor do they have a charge over it. An investor has simply a right to share in any profit generated from the hotel rooms.

The investment could not be exited prior to completion of the hotel rooms. Now that these have been completed they can be sold on the secondary market.

Before completion of the hotel rooms a guaranteed return is paid. After completion the return is based on room occupancy. The expected returns have been paid to the Scheme.

This is an unregulated investment. Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

The Resort Group offered to repay the amount transferred to it by the Scheme. That offer was to release one plot every two months from 31 October 2016 subject to completion of legal agreements. Dalriada agreed to this offer and signed the agreements in December 2016.

The Reforestation Group Limited

The purported nature of this investment is that the Scheme has purchased ‘land rights’ to 21 plots of Brazilian farm land that is to be used for growing eucalyptus trees. The investment term is 21 years as it covers three cycles of seven years, which is the projected time period to grow and harvest the trees. The investment purportedly offers returns of 28-32% compounded over each seven year cycle.

The crop cycle of the eucalyptus tree is seven years. Accordingly, with the investment being made in 2014, the first return on any of the Land Rights Agreements (”LRA”) would not be realised until around 2021.

The estimated return after 7 years is £19,000 per hectare, which is a 90% return. There are a number of issues with this development which Dalriada finds concerning and are being investigated.

Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

Dalriada, through the Scheme’s legal advisers, has written to Reforestation to seek further details regarding this investment and to seek justification for the apparent high level of returns promised.

The investment consists of 11 Bonds over three different series and made between 27 October 2014 and 15 May 2015. The Bonds mature after four years from issue but can be redeemed early after three years (upon six months’ notice) or otherwise with ‘the express consent of the directors of ABC Alpha Business Centres Limited’.

Investment returns depend on the series of the Bond and range from 8.11% to 8.25% with and additional bonus if the Bonds are not redeemed early.

In relation to the two series of Bonds, the Scheme has elected not to have ‘rolled up’ interest. This means that interest is due and payable to the Scheme on a quarterly basis. These payments were made until Q4 2016 but stopped when ABC Alpha Business Centres UK Limited and ABC Alpha Business Centres VI UK Limited went into administration on 20 January 2017.

The Bonds are corporate bonds in ANC UK Limited. ABC UK Limited is the capital raising vehicle for the investments. ABC UK Limited is wholly owned by a United Arab Emirates (UAE) entity, ABC LLC. ABC LLC owns and operates the investment portfolio of real estate investments.

ABC LLC is wholly owned by another UAE entity, the Property Store. The Property Store purportedly provides security of 200% of the value of the invested funds.

Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended. An offer was made to buy back the Bonds subject to a 10% reduction. As noted above, interest payments stopped, and the offer was withdrawn when ABC Alpha Business Centres UK Limited, and ABC Alpha Business Centres VI UK Limited, were put into administration on 20 January 2017. Dalriada has prepared a proof of debt in relation to the investment but, as with others above, there is a risk that recovery prospects will be poor.

This unregulated investment consists of a “lease” on 7 car parking spaces in a new office development in Dubai taken out between 1 October 2014 and 17 April 2015. Under the Operator’s Agreement, there is 5 years guaranteed rental income

The Scheme is liable to pay the car park operator, The Property Store, 10% of any income greater than the guaranteed rental income. Once the guaranteed income period comes to an end the Scheme must pay The Property Store 10% of any income that is received from the car parking spaces.

The guaranteed rental income is paid monthly. It had been paid on time up to Q4 2016 when an issue with car park operator meant payments were stopped.

All of the car parking spaces that the Scheme has leased are located at Churchill Towers, Dubai. NCP Ltd owns the freehold of these car parking spaces. The contractual position is not clear due to incomplete documentation however it would appear that the investment operates as follows:

NCP Ltd owns the freehold and has assigned full commercial rights over the car park spaces to Horizon Properties SA; Horizon Properties SA has granted the Scheme a 99 year lease over each of the seven car park spaces; the Scheme has entered into an Operator’s Agreement with The Property Store with no set term for each of the seven car parking spaces.

Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

An offer was made to buy back the car parking spaces subject to a 10% reduction. The £189,000.00 investment would return £170,100.00 plus the income received (£13,165.20 – 6.97% return). The offer was within a range that might have been acceptable however before it could be accepted Best Asset Management Limited removed the offer from the table. Dalriada is corresponding with Best in relation to the options for the investment.

So, in other words, a load of old rubbish. But then what would you expect from Stephen Ward who has destroyed thousands of victims’ life savings since 2010. He may be a highly qualified “pensions expert”, and the author of the Tolley’s Pensions Taxation Manual, but that doesn’t mean that he should ever be allowed anywhere near people’s pension savings.

The other questions that should be asked are:

why did HMRC allow the pension scheme to operate in the full knowledge that Stephen Ward was the trustee?

why has FCA-registered Gerard Associates, who were “advising” the victims not been removed from the register and sanctioned?

why did the ceding providers (including the trustee of the Police Pension Scheme) not do their due diligence and question the transfer requests?

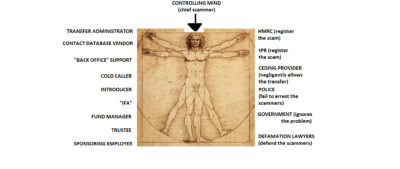

Scammers are loathed by victims, regulators, police, ombudsmen and financial services professionals whose professional reputations are compromised by the nefarious practices of the scam merchants. But however damning the hard evidence is about the scams and the various promoters, introducers, advisers, administrators behind them, the scammers still protest their innocence.

Even when there are announcements and articles in the public domain confirming criminal investigations, winding up petitions, arrests, Pensions Ombudsman’s determinations, regulatory intervention and sanctions, the scammers still try to protest that they are innocent and that the damage done to the victims is everybody else’s fault but theirs.

But as soon as I publish something on the Pension Life blog, to inform and warn the public, the scammers’ solicitors swoop like vultures with their cease and desist letters – threatening defamation proceedings. Never mind the £ millions lost to hundreds or even thousands of victims – many of whom are worried sick about losing their pensions; never mind the tax demands which are driving the victims to complete despair and could result in HMRC making them bankrupt; never mind the heart attacks, strokes and other fatal illnesses brought on by stress and sleepless nights. The scammers’ solicitors pull out all the stops – even going so far as to threaten the Pension Life web host and complain to Google about Pension Life’s website blogs.

I’ve been through this with – among others – Stephen Ward of Premier Pension Solutions – who actually took me to court for upsetting his “picky” clients (Ward didn’t even turn up); Paul Baxendale-Walker, the disgraced former barrister (struck off) and porn star; XXXX XXXX of Global Partners Ltd and The Pensions Reporter (now under investigation by the SFO);and now Peter Moat of Fast Pensions (see Sam Brodbeck’s article of 1.7.2017).

In fact all these solicitors – including DWF, Mishcon de Reya, Carter Ruck, Manleys Law, Molins & Silva et al, all bleat that the Pension Life blogs are harming their clients by “causing reputational damage generating huge financial damages and danger of losing business interests and opportunities”. But not so much a squeak about the huge financial damages the scammers they represent cause to the victims who are in danger of losing their homes.

And not a word about the crippling financial damages the scammers they represent cause to the victims who are in danger of losing their homes.

Below is the email exchange between Peter and Sara Moat’s solicitor Monica Caellas and me dated 27th June 2017. Worth noting she has not responded. Perhaps her website, email and telephones have been hit by the same virus as appears to afflict the Moats and Fast Pensions?

Ms. Brooks:

We hereby contact you in name and on behalf of our clients, Ms. Sara Grace Moat and Mr. Peter Daniel Moat, in connection with the statements set forth in the article “Peter Moat and Sara Moat – Fast Pensions” (hereinafter, the “Article”) included in the website https://pension-life.com/peter-moat-sara-moat-fast-pensions/ since May 18, 2017. I am enormously relieved that you have contacted me and would be most grateful if you would be kind enough to act as intermediary in relation to many hundreds of victims who have been scammed out of their pensions. As you can imagine, this is an extremely worrying time for these people and some of them are now receiving tax demands from HMRC as the Moats were operating pension liberation fraud as part of the “package”.

Some of the statements of the Article are extremely serious and could be constitutive of various crimes sanctioned by the Spanish Criminal Code; among them, serious offences of defamations and calumnies. I do not agree that the Moats’ actions include defamation and calumnies – but they certainly involve pension, tax and investment fraud.

FAST PENSIONS is a UK Limited Company licensed by HMRC. No it is not. HMRC do not license companies in the UK. HMRC registers pension schemes, but this implies no approval or license.

Ms. Sara Moat is the sole Director and the sole shareholder of FAST PENSIONS. Her husband, Mr. Peter Moat is the owner and administrator of Blue Property Group, a Group of corporations that has nothing to do with FAST PENSIONS. From a corporate point of view you are correct, however, Peter Moat was the controlling mind behind the company and has been masquerading as “James Porter” in his communications with the victims to attempt to conceal his involvement. Also, I think you will find that Blue Property Group has gone bust and owes money to creditors all over the Costa Blanca.

With the Article you have caused serious confusion against third parties and it is hurting my clients and their companies. I regret that neither the victims nor I will have any sympathy whatsoever with any hurt your clients are experiencing. They have hundreds of victims’ pensions in limbo – and despite numerous Pensions Ombudsman’s determinations, no transfers out (which is a UK citizen’s legal right) have been facilitated. The victims of this scam include several deaths whereby the deceased pension member’s family has not been able to benefit from the pension fund as required by law in the UK.

In particular, the Article expressly and roundly states “There have been a number of Pension Ombudsman determinations which expressed concerns about the maladministration of the unlicensed firm [Fast Pensions] owned by the Moats”. Yes. This is in the public domain on the Pensions Ombudsman’s website.

In this sense, you claimed that a number of very distressed and worried members of the Fast Pensions scheme had contacted you, while those four hundred worried members have not directly contacted FAST PENSIONS itself. I cannot comment on how many worried members have directly contacted Sara and Peter Moat (masquerading as “James Porter”) direct. Many may have attempted to do so but the Moats have made this impossible by disabling their website and emails and not answering their phones. Their claims that the website, email and phone number have all been hit by a “mystery virus” are simply not credible.

As a consequence of the alleged existing claims you contacted Mr. James Porter, the person in charge of leading with any pension queries for Fast Pensions and that has nothing to do with Mr. Moat, despite your suggestions of identifying them as the same person. That is not correct. Peter Moat contacted me, pretending to be “James Porter”.

Anyhow, and after being correctly assisted by Mr. Porter, you claimed that he takes days to respond and you interpreted that as a “deliberate attempt to make it difficult to contact anyone at Fast Pensions”, which is untrue, since all queries have been responded to and dealt with quickly. I am afraid you do not know the facts. Numerous victims have attested to the fact that their desperate pleas to transfer out have been ignored.

If there were clients with concerns they would contact FAST PENSIONS in the First instance to get these resolve. Why don’t you try contacting Fast Pensions and let me know how “fast” they respond? A journalist tried to contact them just now and got this response: Your message wasn’t delivered to james.porter@fastpensions.co.ukbecause the domain fastpensions.co.uk couldn’t be found.

Moreover, in the Article you have made several statements that make Mr. Peter Moat, Ms. Sara Moat, FAST PENSIONS and all of Mr. Peter Moats companies look like a scam. Then I have done my job properly. They are all a scam.

For example, by trying to link Mr. and Ms. Moat as well as FAST PENSIONS to Mr. Sthephen Ward. Also, and more seriously, you stated that you are afraid that the professional environment of Mr. and Ms. Moat “has undeniably got all the hallmarks of a typical, bog standard scam”. And you insisted: “It looks, feels, smells like a scam”. And I stand by all of that. And so does the Pensions Ombudsman.

As a consequence thereof, there are actually a huge number of parties affected by the Article, Peter Moat and his associated companies, Ms. Moat and FAST PENSIONS. The unjustified reputational damage caused by the Article is generating huge financial damages and is putting Mr. Peter Moat and his companies in danger of losing business interests and opportunities. Perhaps you would like to ask some of the victims how they feel about poor Mr. and Mrs. Moat losing business interests and opportunities?

Based on all the foregoing, and without prejudice to the express reservation of legal actions that correspond to my clients, through this communication you are FORMALLY REQUIRED TO IMMEDIATELY REMOVE THE ARTICLE FROM THE WEBSITE AND STOP DISSEMINATING IT THROUGH INTERNET. I will happily reach an agreement with you Monica: you get Sara and Peter Moat to return all the victims’ pensions to them immediately – in full plus interest – and I will remove the article.

Otherwise, we will be forced to exercise the corresponding judicial actions, especially criminal ones, to protect our clients in defense of his freedom and other rights that protect them. I hope you will exercise criminal judicial actions against your clients who have scammed hundreds of victims out of their pensions. Meanwhile, a little friendly advice – as a Spanish lawyer you clearly do not understand UK law, so please tread very carefully. You clearly do not know the facts and are in danger of defending a party which has clearly contravened UK law and compromising your own standing as a legal practitioner in Spain.

The Ark victims’ QC rolls over as he is quashed by Dalriada’s counsel

DALRIADA V ARK VICTIMS: “ABUSE OF VULNERABLE MEMBERS OF THE PUBLIC”

The Beddoe proceedings of Dalriada (tPR-appointed independent trustees) v Goldsmith (representative beneficiary for the Ark members) kicked off on 20th June 2017 in the High Court. It was a sweltering day in central London – humid and dusty at the same time. The Ark victims were about to discover that the warning about anomalous and unjust outcomes made by Justice Bean in the High Court in November 2011 was going to be ignored.

Dalriada and their solicitors, Pinsent Masons, and their QC Fenner Moeran sat on the left in the airless courtroom. Mrs Goldsmith and our solicitors, Trowers and Hamlins and QC Keith Bryant, sat on the right. Justice Asplin sat on the bench and prepared to rule on whether 348 Ark victims would have to repay their MPVA loans – and whether Dalriada could use the members’ funds to pay for the recovery proceedings. A group of Ark, Capita Oak and Salmon Enterprises victims and I sat at the back. The only thing we all had in common was that everybody was sweating profusely from the heat.

To put this into context, the Ark victims did indeed all sign loan agreements. However, the loans were intended to be paid back out of the members’ 25% tax-free lump sums available at age 55 – so the term of each loan agreement was calculated to be for the number of years it would take each member to reach 55. By which time, the pension was predicted to have grown by at least 8% per year and would be sufficient to repay the loans. Or so the story went.

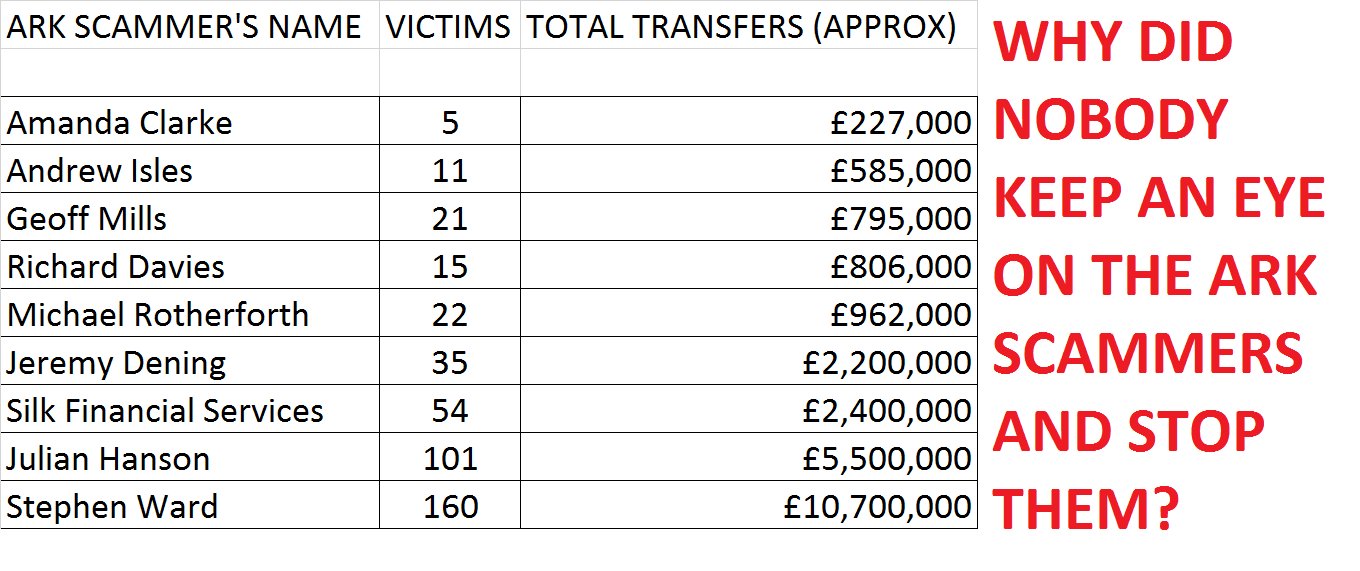

Conspicuous by their absence were the various introducers and advisers who sold the Ark schemes and accompanying MPVA (Maximising Pension Value Arrangements) “loans”. By far the most assertive and prolific of these was Stephen Ward of Premier Pension Solutions who sold over £10 million worth of transfers to more than 160 victims. Ward was followed by those who aspired to be as successful as him and these included:

Julian Hanson £5.3m

James Hobson (Silk Financial) £2.3m

Jeremy Dening £2.2m

Michael Rotherforth £961k

Richard Davies £805k

Geoff Mills £794k

Andrew Isles £584k

Amanda Clark £227k

Many of these went on to operate further pension liberation scams – some of which are now also in the hands of Dalriada Trustees. Andrew Isles of Isles and Storer Accountants is still in practice. Stephen Ward still authors the Tolley’s Pensions Taxation Manual.

The definitive pensions taxation manual by leading pension liberator Ward

Interestingly, Stephen Ward, who used Ark to launch a whole series of further pension scams – including several currently under investigation by the SFO and in the hands of Dalriada – claimed in 2014 that “The Ark thing is history now and my involvement with that was administrative”. Of course, neither of those statements was true: Ark is far from being history as, in the wake of the Beddoe proceedings, a whole new chapter of wretched challenges for the Ark victims has only just begun. Ward was the leading promoter, evangelist and advisor to Ark. He had sold over a third of all the transfers – with a total transfer value of more than £10 million.

In fact, Ward and his herd of “introducers” he had recruited from up and down the country (including FCA-registered Gerard Associates which went on to collaborate with Ward in the London Quantum pension scam) – also now in the hands of Dalriada – often assured the victims they would never have to repay the loans.

Fenner Moeran QC, for Dalriada, opened with the lusty confidence of a dashing matador – and who could possibly have failed to be charmed by his persuasive, eloquent, star quality? He reminded me of an actor at the Oscars who knew he was the favourite to win. With his extravagant hand gestures and polished, word-perfect performance, he got into his stride and stayed there – holding court for the whole day with barely a feeble squeak out of our QC.

Moeran’s confidence, however, veered a little too close to cockiness, and he strayed occasionally into the realms of being callously offensive to the Ark victims when he talked about using a “sharp stick” to beat them into submission with threats of bankruptcy. At that moment, he stopped looking like a polished QC and started to look like a mere back-street bully. In fact, it was astonishing that the judge didn’t pull him up on that “foot and mouth” moment, but she appeared to be far too mesmerised by his charming performance to notice – or care.

While I was taking notes, it was really interesting to watch the players’ body language. One can tell an awful lot about what is really going on in people’s heads by what they do with their various body parts. When Moeran was on his feet, Justice Asplin was coquettish, smiley, full of chuckles and did this wiggly thing with her shoulders (like we women do when we are trying to get a bra straight). But when our QC Keith Bryant was on his feet, she sat as still as a statue and peered down at him with a combination of indifference and pity as if he was a dying bull in the afternoon sun.

Mrs Goldsmith sat quietly and showed not a shred of distress as Moeran referred to her and all the other Ark victims as though they were just names on a list, as opposed to human beings – or indeed anything with a pulse. Knowing her well, I am sure she will have felt profound pain and anguish during the whole three days, but not once did either her composure or her dignity slip.

So here is my transcript of the notes I took on what the various parties said during the proceedings – with my comments in bold.

The last thing I personally want to say on the matter, is that something good has to come out of this and my fervent hope is that all those involved in the promotion, sale, administration, introduction, advice, purchase of assets, execution of loans and various other functions will now face justice sooner rather than later. And here, I am actually grateful to my learned fiend’s suggestion of a sharp stick and would propose something more akin to what Vlad The Impaler would have done to these criminals.

TRANSCRIPT OF MY NOTES AT THE HEARING

DAY ONE

Never forget that legal proceedings are nothing to do with justice

Justice Asplin opened with the words “This was a tragedy and an abuse of vulnerable members of the public”. That got us off to a really good start, but curiously the following day she vehemently denied ever having said it. She also denied ever having mentioned Ark and didn’t even seem to know that collectively, the six schemes (Tallton, Grosvenor, Woodcroft, Cranbourne, Lancaster and Portman) were the Ark schemes. Bearing in mind she had had – and been paid for – a whole day’s reading, one would have thought she would have been a little better prepared.

Ark’s Craig Tweedley was quoted as having made a statement that Ark was “designed to unlock amounts of money from people’s pensions in a way which was not taxable”. This is perfectly true – but it went further: it was promoted to the public (both introducers and potential members alike) as an innovative structure which was lawful and tax free. And the principal promoter and recruiter was Stephen Ward. Ward is also a CII Level 6 qualified former pensions examiner and government consultant on pensions and QROPS – so who wouldn’t have believed him?

One of the Ark schemes’ assets – the South Horizon land option in Larnaca, Cyprus – was brought up and reported as having been purchased by Ark for £4 million. But what was not mentioned was that the option had originally been purchased by two football celebrities for £1.1 million and then sold on to Ark for £4 million. And that this pair had gone to accountant Andrew Isles of Isles and Storer to get advice on how to procure further investors in the Cyprus land project. Isles had introduced them to Craig Tweedley and Stephen Ward. In fact, Isles subsequently introduced at least eleven cases to Ark.

It was stated that Craig Tweedley’s associates Andrew Hields and Julian Hanson had purchased all the assets of the schemes and that the sales documentation claimed that some of the funds were “guaranteed “funds and protected by “re-insurance”. Hields and Hanson may well have purchased some of the assets but they will certainly have benefited from handsome investment introduction commissions along the way.

It was also reported that one of the other Ark assets, Freedom Bay, the St. Lucia timeshare development, is now in administration and that none of the investments made met the statements and claims made in the sales documentation. In fact, it did not come out that few – if any – of the victims were ever shown the sales documentation. Most of Stephen Ward’s victims were told the assets would be “high-end residential London property”.

The matter turned to the recovery effort. It was reported that Tweedley had been pursued for the 5% fees taken from scheme members and that although Dalriada had won their claim, of the approx. £1.5 million taken in fees, they only ever actually managed to recover about £20k. This does beg the question as to just how successful Dalriada will actually be in recovering the £9 million in MPVA loans.

In taking steps to recover the loans, it was reported that Dalriada intends to consider the cost vs benefit situation and decide on the approach on a case by case basis, taking each individual case on its merits. It was acknowledged that the chances of recovery were slim and that the costs could be disproportionate to the likely return. The judge asked how many members had received MPVAs and it was disclosed that 348 had and 138 had not. However, nobody raised the question of why such a large number of members had not received an MPVA loan – had they done so it ought to have been disclosed that a significant proportion of transfers were not rejected after Dalriada were appointed.

It was at this point, while examining the possible avenues to recovery, that Moeran’s confidence bubbled over into bald cockiness and he started bragging about using the threat of bankruptcy as a “sharp stick with which to beat the victims into paying back their MPVA loans”. In fact, by now the judge seemed to be very firmly on his side and stated that the members had already agreed to repay the loans and that their only loss was having to repay early. It seemed clear that neither Moeran nor the judge understood – nor had made any attempt to understand – how the loans were sold to the victims. They were told, by Ward and all the others involved in promoting the scheme, that the loans would be repaid out of their pension pots and not out of their own funds. In fact, some people were told they would never have to repay the loans and that each person on either end of the loan transaction would simply agree to tear up their “IOUs”.

Moeran then went on to claim that by repaying the loans, members could avoid the tax charge. Perhaps the HMRC fairy had whispered this in his ear? Or perhaps he was deliberately ignoring the fact that it is HMRC’s position that the loans will remain taxable even if they are repaid.

Towards the end of day one, it was clear that Moeran was confident they were going to win and that the judge would clearly find in favour of Dalriada and against the members. It was also clear that he had the full support of the judge. In fact, Moeran even went so far as to pretty much read out what our QC, Keith Bryant, would be arguing and told the judge what she ought to find against the case he would be putting forward. At some point, I wondered whether Moeran and the judge would be swapping places.

Moeran talked about the methods and costs of taking recovery action against the Ark members. He itemised three issues to take into consideration:

Merits of taking recovery action

Cost vs benefit of taking recovery action

Consequences of not taking recovery action

He then went on to report that Dalriada had 144 signed Standstill agreements and said that Dalriada was intending spending £2,925 per member on court recovery action. The judge declared that that was on the low side as that cost could only happen if the claim was uncomplicated and resulted in a quick and easy repayment. She also said she was not confident that bankruptcy proceedings were necessarily appropriate.

She did, however, firmly declare that the Ark members had all shared the “mistaken belief” that the MPVA loans were valid, non-taxable and only repayable by the end of the originally-agreed loan term. She broke this “mistaken belief” down into four points:

The members’ “mistaken beliefs”:

The trustees had the power to make the loans

The loans were capable of being made valid

The trustee could transfer beneficial ownership of these monies

The loans were not unauthorised payments and would not trigger a tax charge

The judge appeared to consider that somehow the members had come to these conclusions all on their own. The reality was, of course, that this was exactly what they were told by Stephen Ward and the herd of introducers and advisers – including a couple of FCA-registered ones. But reality did not seem to concern either the judge or Moeran overly.

The last thing that Moeran said on Day One was to make reference to the revised Standstill agreement – the focus of which was to ensure that criminal proceedings are now taken against all those who were involved in defrauding the Ark victims. The judge read the document herself, giving us a welcome rest from listening to Moeran.

As the first day came to a close, I was beginning to wonder whether I had dreamed the fact that a High Court judge had clearly stated in the High Court that Ark had involved an abuse of members of the public. Her statement had been made in front of a dozen or more witnesses and she had then gone on to deny that she had ever said it in front of the same witnesses who all clearly heard her words. Moeran and the judge had both agreed the Ark sales documentation was false and yet I heard neither of them conclude spontaneously that criminal complaints were now essential.

DAY TWO

Moeran opened with: “We are in the process of agreeing six test cases at the First Tier Tribunal” in relation to the personal tax appeals resulting from HMRC’s treatment of the loans (whether repaid or not) as unauthorised payments. The judge questioned whether members put forward for this role might not be happy. Moeran confidently assured her that there had already been five volunteers. I am not aware that any of these purported volunteers have come from the Class Action. Also, at the last meeting that Mrs Goldsmith, Mr Walters (Salmon Enterprises) and I had with HMRC, we agreed two Ark test cases – one with a loan and one without. Moeran did not appear to be aware of this.

Skating quickly over the tax issue for the members – and studiously ignoring the fact that according to HMRC the tax will remain payable even if the MPVA loans are repaid – Moeran and the judge got back to pondering recovery measures. The judge expressed reservations about bankruptcy proceedings because she said that that would merely release members from liability to the scheme rather than help recovery.

Moeran and the judge then started to discuss which members might not be worth pursuing at all for a variety of reasons. Between them, they concluded that those with very small MPVA loans should be ignored and that they might also have to ignore those outside the jurisdiction of the UK. Moeran reported that there were four members in Northern Ireland; 22 in Scotland, 24 in the EU and four outside the EU – USA, Jersey, Bulgaria and Australia.

Neither Moeran nor the judge were sure whether Bulgaria was in the EU (in fact, of course, it is an EU member). The members and I having complained in the strongest possible terms about Moeran’s use of the term “beating the victims with a sharp stick” the previous day, Moeran then went on to publicly apologise for that statement. To be fair to him, he made a good job of the apology and I am sure that Mrs Goldsmith and other members present appreciated it.

I really don’t remember whether our QC said much or anything at all that day – if he did it was not very memorable, or perhaps I couldn’t hear him terribly well because he muttered apologetically and miserably rather than speaking in Moeran’s strident voice.

The MPVA loans were summarised thus:

50 members with loans between £5k and £9,999

124 members with loans between £10k and £19,999

132 members with loans between £20k and £44,999 (totalling £4m+)

40 members with loans of £50k upwards (totalling £3m+)

The judge opined that the bigger the loan, the bigger the original pension must have been, and therefore the wealthier the member was likely to be. She concluded that these would be the easiest targets for recovery.

Then the judge handed down her judgement. She summarised the claim by Dalriada for Beddoe relief (money to be taken from the members’ funds) for the recovery of the MPVA loans and also to challenge the scheme sanction charge in the Tax Tribunals. She approved both of these, but did not agree that Dalriada should use funds to help the members with their individual tax appeals.

She reported that 152 claims had been written to date and that 12 consent orders had been received. She declared that she believed the claims were strong but expressed reservation as to whether the members were in reality good for the money. She reminded the court that there were 138 members without loans and that Dalriada had a duty to protect their position by recovering loans from as many of the other 348 members as possible.

She determined that it was appropriate that the trustees should be granted the relief they sought – albeit not the entire amount sought. She advised Dalriada to take stock of each individual situation and use their discretion as to whether it was appropriate to continue with the action. She also urged them to take into account relevant factors including the aggressive stance being taken by HMRC and to act as a reasonable trustee.

Finally, she said Dalriada should bear in mind that the individual cost of recovery per member would rise from £2.9k to £3.6k (plus VAT) if bankruptcy proceedings were issued and that those with the very smallest loans ought not to be pursued because of the disproportionate cost of doing do. She said it was difficult to decide where exactly the “watermark” might be and reiterated that bankruptcy might not be appropriate and should not be the first refuge sought and could be used as a “second string to their bow”. She suggested that further directions might need to be sought by Dalriada.

Regarding the scheme sanction tax charge appeal matter, she said it was appropriate to give the relief sought and for Dalriada to take steps to challenge the assessments. She recommended a “ceiling” on the amount to be spent and said that to challenge the £4m in tax sought by HMRC, the amount of £350k + VAT was appropriate.

On the question of paying a further £50k to fund legal representations for members against personal tax assessments, she recommended that the scheme sanction charge and the personal tax appeals should be coordinated. But she expressed a reservation about granting this relief to Dalriada as she felt it was excessive “because of the vagueness of what might take place”. She did not consider that for them to pay a barrister was necessarily a reasonable step to take. Therefore, she did not grant the relief sought.

In summary, therefore, the judge’s determination was as follows:

Yes to recovering the MPVA loans from as many of the members as possible/practicable

Yes to paying for the recovery costs out of the members’ funds – at the ideal rate of £2.9k + VAT per member (possibly rising to £3.6k + VAT per member if bankruptcy proceedings were issued)

Yes to taking £350k + VAT out of the members’ funds to pay for the appeal against the scheme sanction charge

No to paying £50k + VAT towards the members’ personal tax liability appeals

At the start of the proceedings, Moeran had reminded the court that Dalriada, as the trustee, already had the legal right to recover the loans if they chose to. But they were seeking the necessary relief and directions to do so from the court to protect their position.

DAY THREE

The final day was all about the nitty gritty of how the recovery costs should be apportioned between the six schemes. Moeran and Bryant put forward different suggestions as to whether this should be done on the basis of the value of the assets or the value of the MPVA loans within each scheme, and whether this should be done equally or on a pro rata basis.

The members at the back of the court were by now numb and none of them really paid much attention to what was basically “housekeeping” in terms of internal accounting procedures by Dalriada. One of the judge’s last points seemed to be that Dalriada should take all and any reasonable steps to recover the MPVA loans – but that the only question was what was reasonable. She cautioned that some options should not be taken, but stopped short of saying what they were.

Shedding a tear or two at the departure of tPR’s Head of Willy Waggling

Bye bye Tinky Winky. Good luck and have fun at LGPS!

His next challenge will be to lead by example and ensure negligent ceding providers compensate their victims whose pensions were transferred into scams. And he can start with LGPS as a shining example so the rest can follow.

As Tinky Winky sails off into the sunset and leaves his regulatory willy waggling duties behind, his first mission is to understand the other side of the coin: the transfer of £millions from secure pensions into the trousers of the scammers. He will now see with a fresh pair of eyes how ineffective tPR has been – and how negligent the ceding providers were.

Winky is going to have quite a mess to clean up when he gets to LGPS – so he had better make sure he takes Noo Noo with him.

Will probably need more than 1 Noo Noo – in different sizes for all the mess at LGPS

And I am sure he is going to be cheerfully looking forward to working even more closely with me from now on.

On June 19th, the Secretary of the Ark Class Action – Mrs. G – will be in the High Court as the Representative Beneficiary for the Ark victims challenging Dalriada Trustees’ Beddoe application. Dalriada, appointed by tPR in May 2011, have already spent around 15% of the £30 million Ark fund. They are now seeking the court’s permission and directions to use even more of the victims’ funds to take legal action against them to recover £11 million worth of liberation loans. This will result in financial ruin for most of the victims – many of whom will lose their homes. HMRC say the loans will remain taxable even if they are repaid so there is the real possibility that members will face two sets of crippling proceedings.

Mrs. G and the other Ark victims – originally 487 of them but now significantly fewer as some have died (some as a result of taking their own lives) – became victims because HMRC and tPR took way too long to take action to suspend the schemes. Also, the schemes were registered negligently in the first place – tPR allowed fourteen occupational Ark schemes to be registered by the same person without there being evidence of any intention or chance of the sponsoring employer being a bona fide employer.

Between August 2010 and August 2011, dozens of personal and occupational pension providers cheerfully handed over £30 million to the scammers with utter incompetence, no due diligence and complete disregard for all the dozens of warnings which had been put out by HMRC and tPR for many years.

In particular, these negligent ceding providers ignored this one issued by tPR Chair David Norgrove on 13.7.2010 just before Ark was launched: “Any administrator who simply ticks a box and allows the transfer, post July 2010, is failing in their duty as a trustee and as such are liable to compensate the beneficiary.”

I shall be looking forward to my next meeting with Tinky Winky because he will be able to bring a wealth of first-hand knowledge and experience to the table. I will probably be bringing Mrs. G to the meeting with me. Because guess who her negligent ceding provider was? Yep, you guessed – LGPS.

BACKGROUND TO THE NEGLIGENCE OF CEDING PROVIDERS SUCH AS LGPS:

The Ark schemes were launched in 2010 by – among others – Stephen Ward of Premier Pension Solutions S.L. and Premier Pension Transfers Ltd. The six Ark schemes had been registered by HMRC and the Pensions Regulator with no due diligence by either to establish whether the schemes had been set up with the specific purpose of operating pension liberation; whether they were bona fide occupational pension schemes set up by a sponsoring employer which intended to trade and provide employment; whether there was a competent trustee and board of trustees in place; whether there was a clear Statement of Investment Principles or whether there was ever any realistic prospect of the schemes providing member benefits.

At around the same time, a multi-million pound occupational pension scam was being vigorously promoted by James Lau of Wightman Fletcher McCabe while the administrators/trustees of the scheme, Andrew Meeson and Peter Bradley, were under criminal investigation for cheating the Public Revenue (and were subsequently jailed). Also, former barrister, solicitor and porn star Paul Baxendale-Walker was promoting a whole series of liberation scams unhindered by the authorities – despite having been firmly in the spotlight since 2007 as a passionate advocate of liberation. And KJK Investments/G Loans was a further liberation scheme flourishing at around the same time, having been started in 2009.

By the time Ark was getting well underway, tPR (formerly OPRA) was fully aware that liberation scams were proliferating and that the feeble warnings they had made back in 2002 about scams which had been operating as far back as 1997 had reached neither the public nor the industry effectively. In 1999, tPR had been investigating two scammers – Stephen Russell and William Ferguson – for a £6m pension fraud. The pair were jailed for five years in 2003.

In fact, tPR were fully aware that since 1999 pension scams were on the increase, and yet did not make it clear to ceding pension trustees what their statutory obligations were in respect of transferring victims into scams. On 13.7.2010, tPR Chair David Norgrove stated that: “Any administrator who simply ticks a box and allows the transfer, post July 2010, is failing in their duty as a trustee and as such are liable to compensate the beneficiary.” But pension trustees claim they never read that message (let alone heeded it) and that it was neither publicised nor distributed. Further, in the same year Tony King, the Pensions Ombudsman, reported that he had “found that pension trustees failed in carrying out serious fiduciary responsibilities to others in circumstances in which the law specifically states that they should not be protected from liability.” And still tPR did nothing. And the Pension Schemes Act 1993 was not amended to reflect the urgent need to protect the public.

The Scorpion Campaign was launched by tPR in 2013 after fifteen years of failing to warn the public sufficiently, and omitting to make it clear to trustees what their statutory obligations were to pension scheme members. During this period, the pension scam industry matured into a deadly serious and well organised large-scale operation in the UK, with many new “players” coming into the arena having been trained by Stephen Ward and other founders and pioneers of early scams.

It was – by the time Scorpion dribbled weakly and ineffectually into the arena – well known to tPR what the typical characteristics of pension scams were and what phrases and claims were habitually being made by the scammers to dupe their victims into signing over their gold-plated pensions into worthless, toxic schemes and being financial ruined. Among the many key phrases (such as “your pension is frozen”; “tax-free loan”; “guaranteed 8% returns” etc.), was the most powerful of all: “the scheme is HMRC approved”. There was, of course, no such thing as HMRC were as guilty of lazy, box-ticking negligence as the culpable ceding provider trustees. But to this day, tPR has done nothing to dispel this myth, and in fact even continues to help the scammers by using the same incorrect phrase on its own website: “If you are required to register a scheme with TPR that does not require HMRC approval, please contact us.”

Even by the time tPR had published the feeble Scorpion campaign in February 2013, the scammers acknowledged this was having a negligible effect on their various scams, and merely moved the goalposts a little to avoid detection. Capita Oak, Henley and Westminster continued to operate successfully beyond February 2013, but only a few ceding pension trustees either noticed Scorpion at all or took any steps to put into practice the minimal due diligence suggested by Scorpion.

In the full knowledge that Stephen Ward was one of the most prolific pension liberation scammers, tPR took no action to suspend any schemes in which he was involved. As a consequence, in August 2014, a Police officer was scammed out of his Police Pension by Ward’s Dorrixo Alliance and into the toxic London Quantum scheme. In fact, far from having any widespread effect, the multitude of scams continue to this day unaffected by tPR’s dismal attempts to protect and inform the public.

PENSIONS REGULATOR’S OBLIGATIONS AND OBJECTIVES:

According to their own website, tPR’s statutory objectives are set out in legislation and include promoting and improving understanding of the good administration of work-based pensions to protect member benefits. These objectives are detailed below with notes in bold.

to protect the benefits of members of occupational pension schemes tPR has failed to do this and as a result of repeated failures over a period of more than fifteen years has facilitated the scamming of thousands of victims out of millions of pounds’ worth of occupational pensions and into millions of pounds’ worth of tax liabilities

to promote, and to improve understanding of the good administration of work-based pension schemes tPR made no effort to work with administrators and trustees of schemes such as Royal Mail; local authorities; the NHS, the Police etc., to help them improve their understanding of how to avoid transferring victims into scams

to reduce the risk of situations arising which may lead to compensation being payable from the Pension Protection Fund (PPF) Through multiple failings over a period of more than fifteen years, tPR has exposed the PPF to huge amounts of compensation claims. This is paid for by the ethical, compliant sector of the financial services industry who are understandably deeply unhappy that they have to bear the cost of tPR’s negligence and omissions

to maximise employer compliance with employer duties and the employment safeguards introduced by the Pensions Act 2008 tPR has done nothing to ensure that occupational pension schemes have a bona fide employer that either trades or employs anybody – or even exists at all

One thing which tPR omits to state as being one of its obligations or objectives, is to take action to prevent pension scams in the first place by carrying out due diligence on the trustees, administrators or sponsors of a scam before registering it. In fact, it is clear from evidenced facts, that what should have been simple common sense in terms of basic, obvious vigilance and diligence, was not done. No questions were asked; no checks were made; no basic suspicions were raised. There is no evidence that anybody at tPR ever had the intelligence to ask questions such as whether schemes repeatedly administered by Stephen Ward or his accomplice Anthony Salih and registered to 31 Memorial Road posed any risks to the public.

Over the past couple of years, numerous “whistle blowing” reports have been made to tPR by members of the Class Action but they have been studiously ignored. At a meeting in April 2015, tPR were invited to work with (rather than against) the Class Action, but this too was ignored. Also at this meeting, the Capita Oak case was discussed. The Insolvency Service subsequently wound up the trustee of Capita Oak, Imperial, but tPR has taken no action to protect the members’ interests and has left 300 victims facing the loss of £10.8 million worth of pension transfers which were 100% invested in Store First store pods (now arguably worthless). The Henley and Westminster victims are facing a similar fate with zero intervention by tPR.

In 2014, evidence of Stephen Ward’s pension scam portfolio was handed to HMRC – including numerous occupational schemes and a pension trustee company: Dorrixo Alliance (registered at 31 Memorial Road, Worsley). However, neither HMRC nor tPR carried out any due diligence to see how many scams were under the trusteeship of Dorrixo and the toxic London Quantum scheme slipped through yet another gaping hole in the net, leading to dozens of victims losing £ millions of pension funds (including final salary ones).

Reverting back to 2010 when the most damning of tPR’s multiple failings started, hundreds of people were left to be scammed into the Salmon Enterprises scheme with no warnings by tPR that the administrators were under investigation for fraud, and thousands of people were left to be scammed into the various Baxendale-Walker and KJK Investments schemes. Along with Ark, 2010/11 alone accounted for well over a quarter of a billion pounds’ worth of pension fund losses and crippling tax liabilities. And this excludes the dozens of scams still being run by Stephen Ward to this day and which tPR continues to ignore. In fact, it has recently been reported that pension scams are by now accounting for over £10 billion worth of losses so the 2010/11 figure may well be substantially higher in reality.

The Pensions Regulator’s plans to start regulating

The Pensions Regulator has sent out a clear message in the Johnsons Shoes case where an employer failed to comply with its legal obligations regarding workplace pensions:

This was clearly the right course of action for the regulator to take and will both encourage some employers to be compliant and discourage others to avoid compliance failures.

But here is a curiously anomalous situation: I can find no evidence that the company just fined £40k by the regulator has ever scammed thousands of victims out of millions of pounds’ worth of pensions and left them with crippling tax liabilities. Many of these victims have had heart attacks and strokes as a result of the stress of being scammed. The employer, Johnsons Shoes, sanctioned by tPR, has been in business for 25 years and it is possible that one or two customers might have experienced the odd blister if the hand-made shoes were too tight. But my search for skeletons, scams or scandals came up with nothing more serious than the fact that they can’t spell the word “paid” on their website.

A little birdie has tipped me the wink that LaLa has had a quiet word in TinkyWinky’s shell like and told him that now he has got a taste for a spot of regulating, he really ought to up his game and sanction some of the outright scammers (i.e. criminals). There is a touch of embarrassment now that a long-established family business has received such a high-profile and high-value fine, while the worst sanction that has ever been handed out to criminals is the odd flaccid waggle.

Tinky Winky’s first dilemma is how to catch the scammers. Shoe shops are easy because they don’t tend to fly away to exotic places like Gibraltar and Malta but stay neatly sandwiched between a travel agent and a book store. The Insolvency Service very helpfully named 18 of the scammers in the Capita Oak, Henley and Store First SIPP investment scams which cost over 1,000 victims over £100 million worth of pensions plus tax liabilities. And I am sure all these criminals will be relatively easy to find in their various magnificent country mansions.

Once caught, the next dilemma will be to work out how much to fine them. My suggestion would be to simply divide £100 million by 18 – interestingly that comes out to £5,555,555.55 each. On top of that, the scammers should be made to pay the victims’ tax liabilities.

Speed is now of the essence to avoid the embarrassment that it took the Pensions Regulator more than four years to ban 5G Futures trustees Williams and Huxley and that the only action ever taken against Stephen Ward was a “severe dressing gown”.

If the shoe fits….

Tinky Winky has got to realise why there is the word “Regulator” in the Pensions Regulator – and if the shoe fits, he has got to wear it.

Another reason for the urgency of taking some long-overdue action against the criminals, is the part played in the financial ruin of so many thousands of victims by tPR itself. 14 Ark schemes, now in the hands of Dalriada Trustees, were registered by tPR; Capita Oak now in the hands of Dalriada Trustees, was registered by tPR; Westminster now in the hands of Dalriada Trustees, was registered by tPR (and tPR failed to spot that both Capita and Westminster shared the same non-existent sponsoring employer); London Quantum, now in the hands of Dalriada Trustees, was registered by tPR and its trustee was Stephen Ward who was behind Ark, Capita Oak and Westminster…….etc. etc.

The Pensions Regulator has warned employers not to ignore their automatic enrolment duties. It would be good to see the regulator’s duties clarified and restore some public confidence in the performance of this public body that is supposed to protect workplace pensions so that people can save safely for their retirement.

Every time I think this book about pension scams is done and I can put it away, a new scam or scammer pops up and I have to rethink it. And every time I add in a new sentence or paragraph, the formatting and pagination need to be adjusted. But, however imperfect and unfinished it may be, it is available on Amazon:

It has been much harder to write than I ever thought it would be. But nowhere near as hard as it is for the victims who have to live with the consequences of losing their pensions and investments – and gaining tax liabilities.

The purpose of this book is to warn the public against current scams and scammers (the same ones who have been doing it since 2010) and encourage the police and regulators to criminalise all forms of scams. The Pensions Regulator’s Lesley Titcombe has clearly stated that scammers are “criminals” and it is hoped they will all be prosecuted. The victims and the ethical members of the financial services industry want to see a zero-tolerance policy and a military-style campaign to stamp out this horrendous crime wave.