CRIMINAL CASE AGAINST UNLICENSED FINANCIAL ADVISERS:

Last month saw the first of the CWM pension scam victims testifying in the criminal court of Denia, Alicante. Nine brave people re-lived their ordeal in front of the judge. They answered the judge’s questions, and were then cross-examined by the defendants’ lawyers.

Darren Kirby in front of CWM office

The complainants who testified were all clients of Continental Wealth Management (CWM) run by Darren Kirby and Jody Smart (pictured below), as well as Premier Pension Solutions (PPS) run by Stephen Ward. PPS was an “agent” and “partner” of AES Financial Services run by Sam Instone. (PPS and AES are now under investigation for their role in the 2011 Ark Pension Liberation scam).

It is hard enough for a pension scam victim to be reminded of their ordeal at the hands of callous, greedy scammers. But to have to recount in graphic detail the methods used by the scammers was hard for them to bear.

The scammer’s typical arsenal of weapons comprises a series of lies – adeptly used to trick the unwary into handing over their pensions and life savings. The victims who testified in Denia know these lies all too well. And now, so too does the judge:

LIE NO. 1: “We’re fully regulated”. This, of course, was completely untrue. CWM operated, purportedly, as a member of the Inter Alliance “network”. And Inter Alliance was not only unregulated but had been fined by the Cyprus regulator for providing regulated services without legal authorisation.

Jody Smart of CWM

LIE NO. 2: “Yes, I’m fully qualified”. This, again, was untrue. Few – if any – of the people working for CWM had any financial qualifications. They were mostly poorly-educated salesmen with the gift of the gab. They had learned a well-used and very clever script which was designed to mislead and defraud their victims.

LIE NO. 3: “The case for transferring your pension into a QROPS is overwhelming”. In the case of final salary pensions, this was never true. A guaranteed income for life from a company pension final salary scheme can almost never be bettered. Most personal pensions should also have been left where they were. In fact, all pensions would have been better off avoiding ending up in the hands of CWM – even if a QROPS had been the right option.

LIE NO. 4: “Your pension needs to be in an insurance bond (Quilter, SEB or Utmost). This is for protection and tax efficiency”. This was never true. The bond provided no protection, no tax savings, no flexibility. The 7% commission paid to the “adviser” was not disclosed.

LIE NO. 5: “Your money will be invested in blue chip companies and you will get high returns and low risk.” High returns come with high risk – and the high commissions (paid to the scammers) were hidden from the victims. Toxic structured notes were used for all the victims – and these are complex investment products which were only suitable for professional investors.

There were, of course, many other lies – including the fact that when the toxic structured notes and unregulated funds failed, these were “only paper losses”. Plus the fact that the investors’ signatures were forged or copied on the investment dealing instructions.

Structured Note Providers

The second half of the complainants will be heard by the court on 9th and 10th December 2021. Once the court has heard from all these victims (minus Bob Bowden who sadly passed away recently), the fate of the defendants will be decided by the judge. Let us all hope this will herald an end to these types of pension and investment scams.

Perhaps “the end” will be just the beginning. A new dawn for an offshore financial services industry which sells proper financial advice – and not just commission-laden products.

CRIMINAL CASE AGAINST UNLICENSED FINANCIAL ADVISERS

The FCA seems to have woken up. It only took eleven years. Eleven years of laziness, torpor, disinterest and deliberately ignoring the problem. But, completely out of the blue, the FCA has suddenly got bored with crapping on bathroom floors and has decided to do a spot of rather belated regulating.

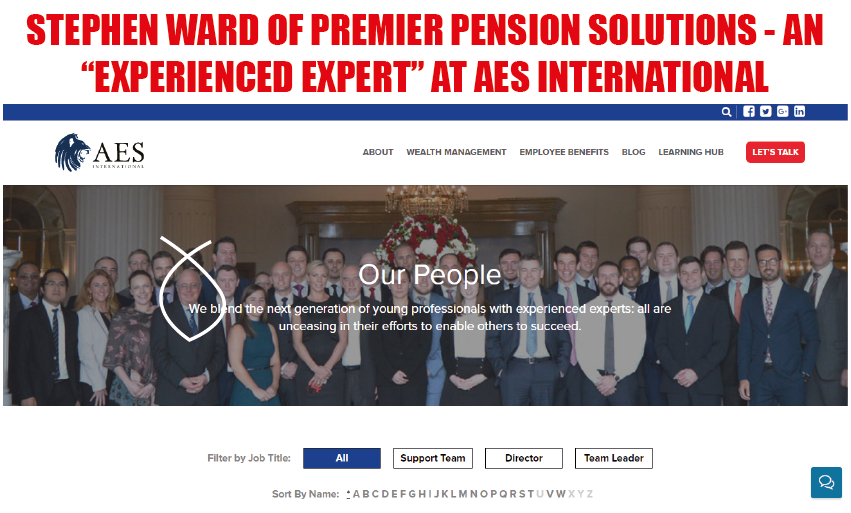

The object of this sudden fit of uncharacteristic activity, is the Ark pension scam. This was operated between 2010 and 2011 by a team of scammers. This team included so-called financial advisers, introducers, a pensions lawyer and an accountant. The principal architect of the six Ark schemes, however, was Stephen Ward of Premier Pension Solutions in Spain. His Spanish firm specialised in (pretty much what it said on the tin) pensions. In particular pension transfers.

Stephen Ward of Premier Pension Solutions

From August 2010, Ward’s company Premier Pension Solutions (PPS) was run as an agent of AES Financial Services – which was regulated by the FSA (now the FCA). Before this, Ward’s company was in the Inter-Alliance network in Cyprus. Coincidentally, the “sister” firm Continental Wealth Management (CWM) was also a member of the Inter-Alliance network. PPS and CWM worked together in close collaboration. CWM often did the cold calling and warm up act for Ward’s various pension scams – including the New Zealand Evergreen liberation scam.

An agency agreement was in place between Ward’s firm PPS and Sam Instone’s firm AES. But the agreement specifically excluded pension transfers. Which was pretty odd, bearing in mind pension transfers were PPS’ main activity. This resulted in Ward’s firm giving victims the false impression that the pension advice he provided was regulated. Which, of course, it wasn’t. The exclusion in the agency agreement between PPS and AES was, naturally, hidden from clients and victims.

Complaints directed at Ward about the various pension scams he had been operating over the years were always firmly rebutted. Ward always claimed that his own activities were the responsibility of AES as the regulated party – and that it was up to Instone to decide what PPS could and couldn’t do.

Kirsten Hastings from International Adviser has published some excerpts from the FCA’s questionnaire about Ark, PPS and AES:

A questionnaire has been sent by the FCA to customers of AES Financial Services (which also traded as International Pension Transfer Specialists (IPTS), Premier Pension Solutions (PPS) and Premier Pension Transfers (PPT).

These clients invested or transferred pensions into schemes managed by Ark Business Consulting and/or the Ark pension schemes.

The questionnaire was sent to consumers to gather more information about their dealings with these firms.

They have until 17 October to respond.

Director of AES Sam Instone told IA: “We are absolutely certain AES Financial Services Ltd has never provided any advice at all in relation to Ark schemes, so it seems like a strange questionnaire.”

Sam Instone seems to have forgotten that AES Spain was run by rogue “adviser” Paul Clarke for some years – after leaving unlicensed firm CWM in 2010. Clarke advised several victims to transfer into Ark. And good old Sam himself advised his own Dad to transfer into Ark. I guess three destroyed pensions – with accompanying tax penalties – can be easy to forget?

Kirsten Hastings goes on to talk about the history of Stephen Ward’s Ark scam:

TPR took action following concerns that the Ark schemes were being used for pension liberation.

According to Dalriada, such schemes generally have high charges and invest money in risky and esoteric vehicles.

They also put members at risk of having to pay large sums of tax.

The latest Dalriada update to members states it is “not able to place a value on any members’ benefits at the time and are therefore unable to make payments to members”.

Kirsten also mentions some further points in the FCA questionnaire:

Kirsten Hastings editor at International Adviser

Did the client (Ark victim) approach the firm or vice versa?

Where was the client based when these services were provided?

Would clients be willing to sign a witness statement?

What regulatory protections was the client told there were?

All Ark victims would certainly be more than happy to sign a witness statement to evidence what Stephen Ward, PPS and AES did, wrote, promised, assured and persuaded.

The regulatory protection, of course, for anyone advised by Stephen Ward’s Premier Pension Solutions (which was most of them) in the Ark scam, was Sam Instone’s AES Financial Services – according to all the documentation.

Ward promoted the Ark £27 million scam during 2010 and 2011 – cases being documented on PPS headed paper announcing that the firm was a “Partner” of AES and regulated through AES. Ward would have earned at least £1 million through the Ark scam – all of which would have been paid through AES.

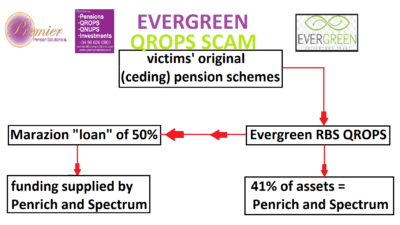

When Ark went tits up, Ward launched his next pension liberation scam: Evergreen Retirement Benefits QROPS in New Zealand – with his accompanying 50% Marazion “loans”. Again, all advice was given on PPS headed paper announcing that the firm was an AES partner and regulated through AES. This meant another 300 victims lost more than £10 million worth of pensions. It also meant that PPS and AES between them earned at least £1 million from the scam (10% of transfer values). These fees were paid direct to AES.

When Evergreen collapsed (as all PPS pension scams eventually did) in 2012, Ward set up the Capita Oak scam. Another 300 people lost over £10 million – all invested in Store First store pods. Again, all pension transfers were done by Ward. Alongside Capita Oak, Ward carried out all the transfers for Henley (another 250 victims losing £8 million in Store First) and Westminster (another 79 victims losing £3.3 million in other toxic, high-commission investments). All these schemes are currently under investigation by the Serious Fraud Office.

Throughout this era – during which all business done by PPS went through AES – Ward ran multiple, multi-£million pension scams – mostly involving liberation fraud:

Bollington Wood

Capita Oak

Dorrixo Alliance

Endeavour QROPS

Evergreen QROPS

Feldspar

Halkin

Hammerley

Headforte

Henley Retirement Benefits

London Quantum

Southlands

Randwick

Randwick Estates

Southern Star QROPS

Superlife QROPS

The above list comprises QROPS which were used abusively, and bogus occupational schemes.

All these PPS scams resulted in many hundreds more victims losing millions of pounds’ worth of pensions. Many of these unfortunate people were also persuaded by Ward to liberate their pensions, and so they would have faced crippling tax penalties as well.

Ward’s final triumph in his long-running pension scam campaign was London Quantum. He proudly announced this scheme saying that “Ark is history” and that he was now going straight. Still trading as an AES partner and agent, Ward conned 100 victims into the London Quantum scheme. This was invested in the usual high-risk, high-commission and entirely inappropriate assets (including Dolphin Trust loans and car parking spaces at Park First Glasgow). London Quantum ended up being classified by Dalriada Trustees as being “probably worthless”.

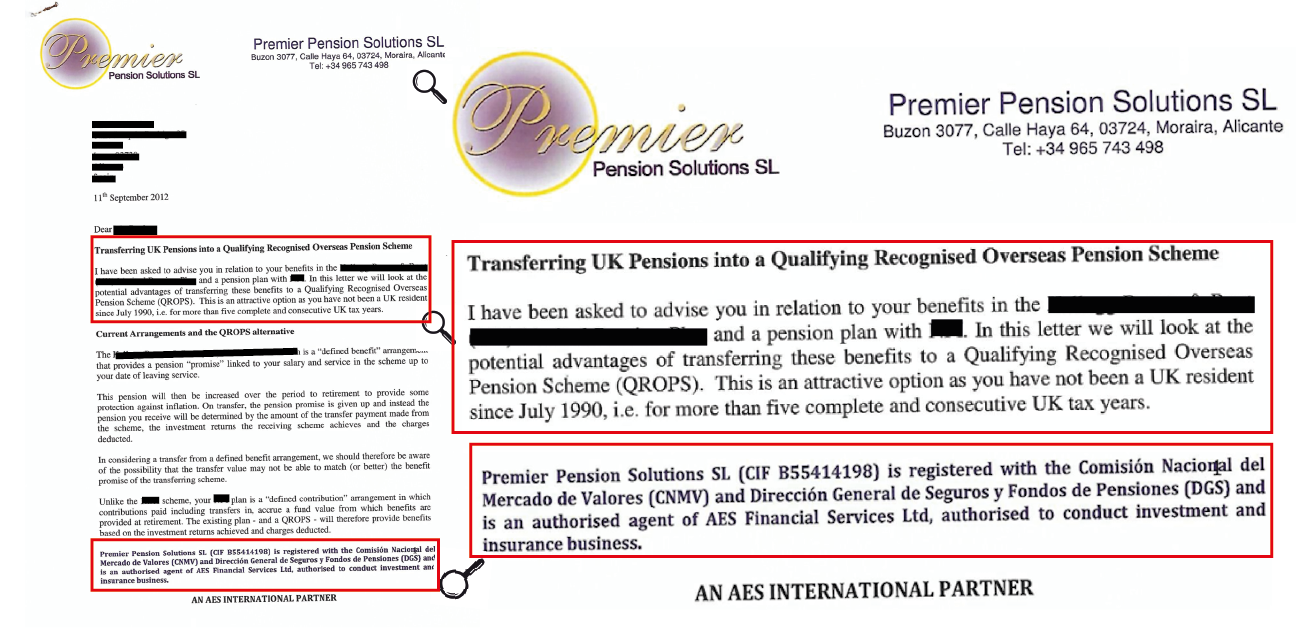

In the Ark Pensions scam, it is clear why so many victims thought PPS was a properly-regulated firm – AS AN AGENT AND “PARTNER” OF AES:

“Premier Pension Solutions SL …..is an authorised agent of AES Financial Services Ltd authorised to conduct investment and insurance business. AN AES INTERNATIONAL PARTNER.“

In the subsequent £100 million Continental Wealth Management pension and investment scam, Ward continued to “advise” hundreds of victims to transfer their precious pensions into the hands of known scammers – in the full knowledge that their pensions would be invested in high-risk, high-commission rubbish funds and structured notes:

But Stephen Ward was a bit more than just an “agent” and “partner” of AES. He was also an integral part of the AES management team – and boasted that he was Director of International Pensions. When all the pension scams finally collapsed, leaving thousands destitute and desperate – as well as hounded by HMRC – Ward and Instone set up IPTS: International Pension Transfer Specialists. This new venture was run from Ward’s office in Moraira – although they tried to hide this by using a PO Box at nearby LettersRUs. And so the misery continued…..

Stephen Ward in the front row of the AES team of “experienced experts”.

Utmost (formerly Generali) is proposing buying Quilter (formerly Old Mutual). The deal is due to be completed by December 2021. The agreed price is nearly half a billion pounds. It is reported that Margrethe Vestager, Vice President of the European Commission, has “approved” this acquisition.

Margrethe Vestager – EU Commissioner Executive Vice President

The “approval” by the European Commission of this deal is an insult to thousands of victims of pension and investment fraud. Widespread financial crime has been facilitated, encouraged and rewarded by Utmost and Quilter over the past decade. The appalling result has been the destruction of millions of pounds’ worth of life savings and pensions.

Margrethe Vestager, EU Commissioner Executive Vice President, has proved that the Commission hasn’t got a clue about Utmost’s and Quilter’s role in offshore financial services fraud. And this deal between these two death offices will create a monopoly over fraud against expats in Europe.

For death offices – such as Utmost and Quilter – fraud against expats is clearly a lucrative business with a huge market. The horrific damage – including distress, poverty and suicide – gives neither Utmost’s CEO Paul Thompson nor Quilter’s CEO Paul Feeney any cause for concern. Thompson has described the proposed acquisition as:

“highly attractive and in line with our growth strategy”.

But growing an industry based on fraud should neither be countenanced by the European Commission – nor the European Markets and Securities Authority.

Paul Feeney CEO of Quilter

Paul Thompson CEO of Utmost

Utmost Fraud approved by EU Commission

Utmost announced the planned takeover in April 2021. CEO Paul Thompson has bragged this would add £22 billion and 90,000 policies to its existing portfolio. This would give the Utmost/Quilter combo a total of £58 billion of funds. And much of this will have been acquired through fraud. It will also give them 600,000 “customers”. And many of these will have been victims of fraud – some of them currently on the verge of suicide.

The toxic assets and suicidal victims result from Utmost’s and Quilter’s long-standing practice of giving terms of business to unlicensed scammers. These death offices have paid huge, undeserved and undisclosed commissions to these scammers for more than a decade. And there is no sign that there is any intention to pay redress to the thousands of victims who have lost their life savings and pensions in death bonds.

The Commission’s approval of this iniquitous acquisition is a grave insult to Utmost’s and Quilter’s existing victims. It also puts thousands of British expats across Europe at risk of becoming future victims of the fraudsters to whom the death offices give terms of business.

There are three clear strands to the fraud with which both Utmost and Quilter are undeniably complicit:

1. The insurance bond – also known as a life, portfolio, or offshore bond. This is the core “product” routinely used and abused by the unethical sector of the offshore financial services market. This toxic sector – which includes many known scammers – sells products and not advice. Bonds can – under certain, limited circumstances – play a valid tax-mitigation role in the UK. But offshore, they serve zero purpose – other than to pay commissions to many unauthorised introducers and fraudsters posing as advisers. Insurance bonds should never be used with offshore pensions (QROPS) since the pension is already a tax “wrapper” in its own right.

2. The terms of the insurance bonds are clearly abusive to consumers as retail, inexperienced investors. The high charges are mostly for the purpose of clawing back the concealed commissions paid to the introducers (many of whom are unauthorised). Utmost and Quilter had known for years that large numbers of these introducers had no license to provide insurance mediation or investment advice. They had also known that these same introducers had long-established track records of mis-selling and fraud. And yet Utmost and Quilter continued to give them terms of business. They allowed them to invest thousands of victims’ pensions and life savings recklessly – and disastrously.

3. The toxic, illiquid, high-risk “investments” offered by the death offices. These products were offered on the death offices’ platforms for the scammers to sell to their victims. Investment products have included dozens of failed funds such as LM, Axiom, Premier New Earth, Quadris Forestry and Kijani. Worse still are the professional-investor-only structured notes supplied by Leonteq, Commerzbank, Royal Bank of Canada and Nomura.

This toxic “triptych” has resulted in horrific losses for thousands of victims over the past ten years. And if this iniquitous acquisition goes ahead, there will be just as many – if not more – casualties in the next ten years. The EU Commission – along with ESMA – will be complicit.

Of course, I might be entirely wrong: Utmost’s half a billion might have been subject to a sequestration deal enforced by the Commission. Perhaps this money is going to be used to repay all the victims the hard-earned money they have lost? And any surplus used to prosecute the dozens of fraudsters to whom the death offices had given terms of business? (Sadly, I am not often wrong).

Death offices Utmost and Quilter (as well as FPI and RL360) have routinely given terms of business to known scammers and unlicensed salesmen posing as advisers since 2010. They have created a toxic industry of selling dodgy products – not professional financial advice. The result has been predictably awful. Victims have paid the price with poverty and misery in retirement. Utmost’s acquisition of Quilter is likely to result in a huge increase in this widespread crime.

The facts behind this perilous situation are irrefutable. Quilter itself is suing Leonteq for £200 million for just one series of high-risk structured notes. This was for an extra 2% hidden commission on top of the 6% hidden commission allowed by Quilter. Chief Executives Peter Kenny and Paul Feeney know that these toxic products should never have been promoted to retail, naive investors. Kenny and Feeney are fully aware that their unlicensed introducers will sell any toxic and high-commission crap to their victims.

John Ferguson (left) & David Vilka (right) of Square Mile International

In 2016, Quilter provided hundreds of these toxic Leonteq structured notes (with total concealed commissions of up to 14.57%) to distributors such as Satori, Mayfields and Morgan Capital. Quilter also sold these notes to known, serial scammers Square Mile International. In the same year, Utmost sold the same Leonteq notes with hidden commissions of over 12%.

Utmost Fraud approved by EU Commission

The EU Commission needs to understand why Utmost’s proposed acquisition should not go ahead. In their Introducer Terms of Business Agreement, Utmost opens with a false statement:

“Following completion of due diligence we are pleased to confirm your terms of business have been authorised on the following commission basis”.

But there is no due diligence. There are no checks on how the firms are licensed, or whether any of the staff or sub agents are qualified to provide insurance or investment advice. And certainly no acknowledgement that the commissions must be openly disclosed to the victims.

The starting point for the hidden commissions is that 140% of the victims’ portfolio will form the basis for the payment. A fact which is never disclosed to the victims.

The Utmost Introducer Agreement requests details of the applicant’s experience and qualifications, in addition to membership of professional bodies or trade associations. The application form also asks for confirmation of regulatory status in the markets where the firm operates. They also ask for details and proof of professional indemnity insurance. Therefore, Utmost acknowledges that these are essential factors for a legitimate introducer. They willingly enter into terms of business with many unlicensed, unqualified scammers. These scammers have no experience, qualifications, membership of professional bodies or trade associations, and no essential regulatory status. They also have no professional indemnity insurance.

In 2014, Utmost accepted one bond application from a victim resident in Spain. Her “adviser” (introducer) had no license to provide either insurance mediation or investment advice anywhere in Europe. And yet Utmost gave this firm complete freedom to invest the victim’s funds – accepting 19 separate investment dealing instructions (mostly with forged client signatures) totalling 529,251.80 Euros. All of the investments were professional-investor-only, high-risk structured notes provided by Leonteq, Commerzbank, Royal Bank of Canada and Nomura. Between 2014 and 2018, Utmost and the scammer between them destroyed over 75% of the victim’s fund. The destruction was caused by repeated structured note failures and the inexorable high charges by Utmost. When the victim finally took out what little was left, Utmost charged her a hefty early-exit penalty. There was no recognition of the horrific destruction Utmost had facilitated.

Criminal proceedings against this, and other associated firms, are now in progress in Spain. However, the main lead complainant – also an Utmost victim who lost most of his portfolio – has recently died. Much of his life savings and pension – which started out at three quarters of a million pounds – were destroyed by Utmost and the scammer. The causes of the losses were not only the toxic structured notes but also some unregulated, professional-investor-only funds such as the Quadris Brazilian Teak Forestry Fund. The deceased victim’s disabled widow is now facing poverty on top of bereavement.

Of course, Quilter has performed just as atrociously as Utmost over the past decade. Thousands of Quilter’s victims are facing similar poverty and suffering at the hands of the same scammers. This fraud is facilitated and rewarded by hidden commissions and the freedom to invest portfolios without the victims’ knowledge, using forged client signatures. With similar callousness, Quilter has allowed the flotsam and jetsam of the offshore cowboys to commit the exact same type of fraud as Utmost has.

One such scammer – with Quilter terms of business – boasts that his qualification to work in financial services is working as a bar manager and managing a successful sales company:

(formerly an agent of AES International and now an agent of Abbey Wealth)

If I am wrong, and the Commission has already made arrangements to freeze Utmost’s half a billion pounds, then I apologise unreservedly for doubting you. But if I am right, then the European Commission is just as bad as the death offices and the scammers.

Today, 7th April 2020, was supposed to have been the second part of the Continental Wealth Management criminal trial. Obviously, due to Coronavirus, the hearing has been postponed. For now. As soon as the pandemic is under control and life in the courts (and elsewhere) gets back to “normal”, the hearings will be rescheduled. This is obviously a disappointment to the victims who are waiting anxiously to see the outcome of the trial – but it is only a relatively minor setback in the grand scheme of things. We will get these defendants into court, and the judge will give directions as to how to deal with the crimes committed.

The crimes involved are:

Fraud

Disloyal administration

Falsification of commercial documentation

The second batch of defendants comprises:

Stephen Ward of Premier Pension Solutions and Premier Pension Transfers, IPTS (International Pension Transfer Specialists), AES International, Dorrixo Alliance and Marazion

Paul Clarke of Continental Wealth Management, AES International and Roebuck Wealth

Jody Smart (alias Jody Bell) of Continental Wealth Trust, Jody Bell Fashion, Grant A Wish charity and Mercurio Conpro

Darren Kirby (partner of Jody Bell) of Continental Wealth Management and Continental Wealth Trust

The first batch of defendants were cross examined in the week of 24th February 2020 and comprised:

Patrick Kirby (brother of Darren Kirby)

Anthony Downs

Dean Stogsdill

Neil Hathaway (all of Continental Wealth Management)

When we first set out this case, we weren’t entirely sure the court would accept the charge of fraud – because it is difficult to prove as a complainant needs to establish intent. However, the court had no hesitation in accepting this charge, as well as the additional charges of disloyal administration and falsification of commercial documentation.

The evidence in the case is very clear and incontrovertible: seventeen lead complainants (out of more than 600) who all exhibit the exact same “symptoms”:

Low to medium risk investors placed in inappropriate, high-risk investments

Insurance bonds sold illegally

Investments churned repeatedly

No license to provide insurance or investment advice

No qualifications to provide financial advice

No adjustment to financial strategy when serious losses began to appear

It is tempting to think that perhaps Continental Wealth Management (which later became Continental Wealth Trust but still kept the original name) was an isolated case. But, sadly, that is not so. I have seen many examples (in Spain and other jurisdictions) of clients being placed into inappropriate investments, by other so-called advisers, which paid large, hidden commissions over the past six years. Stephen Ward was routinely flogging the EEA Life Settlements fund – putting some investors’ entire portfolios into this risky fund which paid up to 19% in commission. He was also flogging other high-risk funds such as Traded Life Policies, Axiom, Blackrock Gold and Aria – as well as selling bonds such as Skandia (OMI) illegally. And, naturally, Ward’s clients suffered crippling losses.

The above method, show-cased by Stephen Ward, has – of course – been rife in offshore financial services for years. It has made the advisers rich and the investors poor. In short, this is disloyalty at its worst: the adviser putting his own interests above those of his clients.

And that, in Spain and other European countries, is a criminal offence.

But Ward wasn’t alone: Paul Clarke did the same even after he left Continental Wealth Management and became an agent of AES International – exploiting the financial advisory market on the Costa Blanca as he decimated clients’ savings with more illegally-sold insurance bonds, structured notes and expensive, high-commission funds. Clarke regularly featured in whole-page spreads in Euro Weekly – spouting “expertise” and masquerading as a qualified, experienced financial adviser.

There are few firms in Spain – or indeed the rest of Europe and beyond – which do not rely heavily on the notorious insurance bond. The offshore market is dominated by the usual suspects: OMI (previously Skandia and now Quilter); Generali, SEB, RL360 and Investors Trust. And all these insurance companies encourage unregulated, unqualified advisors to sell these bonds illegally. There are few, if any, benefits to the consumer – and no insurance bond should ever be used inside a QROPS (unless there’s no lock-in and no commission).

I just Googled: “wealth management and financial advice Spain”. The top results came up as: Blacktower; Blevins Franks; Abbey Wealth; Masttro (a firm I’d never heard of before); Finance Spain (another firm I’d never heard of); Spectrum IFA Group; and Alexander Peter. I am not saying whether any of these firms are either good or bad – but I think it is safe to assume they are all selling insurance bonds illegally.

Of course, there’s nothing inherently wrong with an insurance bond. It is, after all, just a wrapper – or container for funds and investments. There are, arguably, some tax advantages in some jurisdictions – although they should never be used inside a QROPS.

The problem with an insurance bond – whether from OMI, SEB, Generali or RL360 – is that an investor is going to get one whether he wants or needs one or can afford one or not. The investor will get locked in for up to ten years and he won’t be aware that the adviser will get paid an 8% commission for selling the bond. This commission will get clawed back by the life office over the term of the bond.

Many investors are conned into believing that the bond provides some sort of protection. It doesn’t. Many investors are also conned into to thinking that the investments offered by the bond providers are “safe”. They aren’t necessarily – there may be some decent investments but there are also an awful lot of rubbish, expensive ones. But the biggest con of all is that the investor isn’t told that the annual bond charges (taken quarterly) will stay the same even if the portfolio value decreases. So, if the investor needs to withdraw some money from the bond, the charges will start to do some serious damage to the remaining fund. And if the investments fail – as many structured notes invariably do – and the portfolio value starts to decrease alarmingly – the bond charges will then erode what’s left very rapidly.

Some victims of serious mis-selling actually end up having the entire fund destroyed by irresponsible, fraudulent or disloyal investment advice by rogue advisers – and can still be paying the bond charges even after the entire portfolio has been destroyed.

The other half of the disloyalty and fraud by Continental Wealth Management (as well as some of the other well-known names in “wealth management”) is the practice of “churning”. This means that the same chunk of money is invested repeatedly to generate as much commission as possible – in as short a space of time as possible. This is easy to spot when looking at the bond statements (whether OMI/Quilter or RL360 or whatever):

“Buy £100k worth of rubbish (earn 6% commission); sell £100k worth of rubbish; buy another £100k worth of rubbish (earn another 6% commission); sell £100k worth of rubbish; buy”….and so on. This exercise can be repeated over and over again in any period – say one year – to mince two or three lots of commission out of the same sum of money. The investor may not notice – as long as his fund value isn’t falling too much – and, because the commissions are concealed, he may not realise he is being defrauded and that his adviser is committing a criminal offence by being “disloyal”.

The Continental Wealth Management case – being heard in the criminal court in Denia, Alicante – may not cure the ills of the offshore financial services industry overnight. But it will certainly send out a clear message to all financial advice firms that Spain, at least, will not tolerate such conduct. While British regulators, courts and police authorities are happy to leave fraudsters and scammers free to keep on operating and promoting financial scams, Spain is in the process of sending out a very clear message:

As we reach the halfway point in the criminal trial of the Continental Wealth Management and Premier Pension Solutions companies, I regret I am unable to give a detailed update on the case at this point. The first half of the eight defendants have been cross examined by the judge’s lawyer, and the second batch of four further defendants are due to be cross examined on 7th April 2020 (in the Denia Court of First Instruction).

This, of course, assumes there is no disruption to the proceedings caused by the Corona virus lockdown.

Dean Stogsdill and Neil Hathaway of CWM leaving the Denia Criminal Court on 25th February 2020 after being cross examined on charges of fraud, disloyal administration and falsification of commercial documents.

The first “batch” consisted of Patrick Kirby – Darren Kirby’s brother – who ran the CWM cold calling operation which sent so many hundreds of victims to their doom; Anthony Downs; Dean Stogsdill and Neil Hathaway who had various different titles at different times – ranging from Managing Director to Operations Director to Investment Director.

I can’t comment on the transcripts of the questions and answers on 24th and 25th February, and won’t be able to publish the full details of all cross examinations until all the defendants have appeared before the judge. The defendants on 7th April will be:

JodySmart – sole director and shareholder who paid herself over 1 million Euros in the last two years of the life of CWM – the money being paid into her two other businesses: property company Mercurio and fashion design company Jody Bell. In addition, she also paid money into her Grant A Wish “charity” and drew a hefty salary.

Paul Clarke – founder of the original CWM company in partnership with Darren Kirby; Clarke left a year later to run AES International Spain, where he scammed more victims out of their life savings with expensive, unnecessary, illegally-sold insurance bonds, and high-risk structured notes – all sold for the fat commissions (despite the even fatter losses suffered by the victims). He also advised two victims to go into Stephen Ward’s Ark scam. Clarke now runs a firm called Roebuck Wealth and has scrubbed the internet of all trace of his history.

Darren Kirby – founder along with Clarke and ultimate controller of the whole CWM operation throughout. Kirby made every attempt to divest himself of all legal responsibility for CWM. He gave away his shares in the company to his business/civil partner Jody Smart, and some of his employees. However, all the defendants (as well as victims) are bound to confirm Darren Kirby was the ultimate boss and controlling mind of the company.

Stephen Ward – owner of Premier Pension Solutions SL. He was the person who signed off all the CWM clients’ pension transfers (for a fat fee). He knowingly condemned all pension holders whose transfers he signed off to inevitable partial or total loss. He was fully aware of CWM’s modus operandi as he himself used a similar investment model to that of CWM (and had taught them how to do it). Ward was routinely investing his own clients’ funds in a toxic, disloyal and irresponsible manner which was as bad – and sometimes even worse – than in the CWM cases.

As soon as I can publish the cross examination transcripts and further directions, I will do so.

This landmark Continental Wealth Management criminal case will inevitably shine a much-needed spotlight on the issue of offshore financial services generally. CWM was just one example (albeit an extreme one) of an international financial services culture which generally disadvantages and/or defrauds consumers. The cause of this culture is a combination of the obsession with the insurance bond cartel: OMI, SEB, Generali, RL360 et al; the total reliance on (hidden) commission; the practice of churning (investing the same sum of money as often as possible to generate as much commission as possible) and the view that the client’s money and interests are secondary to the adviser’s.

CWM victims outside the Denia Criminal Court on 25.2.2020 waiting for Dean Stogsdill and Neil Hathaway to finish being questioned on charges of fraud, disloyal administration and falsification of commercial documents.

Most victims – whether parties to the criminal proceedings or not – are aware of the demise of CWM in September 2017. The company was slowly dying because of the number of victims the CWM scammers had ruined: the word was getting out (which was bad for business) so the victims who shouted loudest were getting paid off. This was having a seriously detrimental effect on CWM’s cashflow.

The financial strain on the business was, however, made even worse by the fact that every last bit of spare cash in the CWM bank account was being used to keep Jody Smart in houses, frilly frocks, shoes and champagne. In 2017, the CWM bank statements show 158,614 EUR was transferred into her Mercurio property company bank account, and 123,400 EUR into her Jody Bell fashion design company bank account. But this was significantly down on the previous year: 386,921 EUR to Mercurio and 164,000 EUR to Jody Bell. The year before, 2015, 124,500 EUR into Mercurio and 39,000.00 into Jody Bell fashion. That’s almost 1 million EUR in two years pocketed by Jody – not counting the money paid into her Grant A Wish “charity” and her generous “salary”.

During the same period, however, the revenue was at least 3,391,876.28 EUR in commissions from insurance bonds and structured notes. On top of this was a substantial amount of extra secret commission from the ultra-high-risk Leonteq structured notes, plus whatever Darren Kirby could con out of victims such as Mark Davison (who subsequently died penniless) and the other claimants pursuing Kirby and CWM through the criminal court in Denia in separate proceedings which pre-date our Pension Life proceedings.

Looking back to the dying days of CWM when cashflow was slowly grinding to a halt as the company was paying out compensation to some of the worst-affected victims (and any remaining cash was being spent by Jody Smart on first-class flights to New York and champagne in five-star hotels – despite her claim to be working 24/7 on her Grant A Wish charity), there was a plan to “reinvent” and re-launch CWM. It eventually dawned on the CWM scammers that they couldn’t scam enough new victims quickly enough to pay out all the existing victims – so the answer was to start afresh with a brand new approach. The new approach was essentially the same as the old approach – except they aimed to sell more “products” and ruin more victims.

The rest is history and CWM collapsed at the end of September 2017 – when all related parties withdrew terms of business. It is worth taking a careful look at the business plan which CWM had been intending to use to re-launch the business. This plan makes it clear that this was an unlicensed, insurance bond sales outfit which intended to continue to operate in contravention of the Spanish insurance regulations. If you read the plan carefully, you will see that CWM operating model was always based on a high-pressure sales target which ignored the interests of the clients (victims).

CWM’s promotion had always been centered around the iniquitous cold call – but in addition the business plan reveals that Jody Smart’s Grant A Wish “charity” events had been used to “harvest” potential victims at scamming sales parties posing as bona fide fundraising efforts.

Read the below CWM “Relaunch Business Plan” carefully and you will see how the scam works. If a victim transfers a £100,000 pension, it will fall in value in the hands of CWM to £91,976,000 by the end of year 1. This means the first year fees would have totalled £4,000 set up fee plus £1,000 annual management fee to CWM; £1,490 QROPS fee; £1,534 to fee OMI. It is interesting that Stogsdill has made the assumption in the plan that all clients will be put into an OMI bond – long before they’ve even met the client and found out if they actually need an insurance bond (which they never do as they are too expensive and lock investors in for up to ten years).

The CWM “plan” shows how a victim’s fund could recover back up to £97,495 if it grows by 6%. But this doesn’t take into account the investment costs of between 5% and 8% – so that was never going to happen. So Dean Stogsdill of CWM – despite all the lessons which should have been learned from years of destroying victims’ funds, still fully intended to keep on doing the same to as many new victims as possible.

Continental Wealth Management Business Plan 2017 (by Dean Stogsdill)

Continental Wealth Management is an independent financial advice firm specialising in wealth management advice to English speaking expatriates throughout Europe – this statement is the key to CWM’s future success.

CWM must focus on expanding our circle of influence and create new business through strategic placement of data gatherers. We must take on the business of “hard targets”, created to allow the best we have to flourish, whilst removing the weaker members of the team by natural selection. This is not a system for solely the sales force, but for all aspects of the team including call centre operators, administration and directors.

CWM will have clear defined roles within the sales force with the addition of achievable, measurable targets on top of generous salaries which is the cornerstone of our payroll ethos. The business will flow from our Partners meaning the business can be closed efficiently and serviced by an experienced adviser who is well trained, knowledgeable and most importantly a “hungry individual”.

There is a simple calculation on £100,000.00:

£100,000 invested over 6 years in capital protected products will provide £6,250.00 in gross revenue.

£100,000 invested over 6 years in a fund yielding 3% per annum growth will provide £10,690 in gross revenue.

BACKGROUND

CWM is a financial services company founded in 2007 on the Costa Blanca. It is a company specialising in pension transfers, portfolio bonds, offshore investments and single premium investments. It is a non-regulated company which is owned and operated by the directors / shareholders and founder Darren Kirby. Recent investors are Timothy Benjamin, and Mark Davison with share capital having been distributed amongst these investors.

Directors

/ Shareholders

Founder

/ Majority Shareholder – Darren Kirby

Chairman

– Neil Hathaway

CEO –

Dean Stogsdill

COO –

Anthony Downs

Key

Personnel

Darren

Kirby – He brings a wealth of experience in

financial services with a keen head for figures and sales techniques.

He has a strong view on the business and how it should be perceived

by the clients, while strengthening our position through strategic

investment decisions along with powerful leadership skills.

Neil

Hathaway – Decades of experience in

insurance and wealth management, he brings a strong personality and

great sales skills with the qualifications to match. He is a

knowledgeable asset to the management of the sales force and uses his

skills to bring through the less experienced members of the team.

Dean Stogsdill – Strong sales record and up to date qualifications – he can sell at the most technical level and has a strong grasp of the investment market, regulation and products. Strong views on company direction.

Anthony Downs – Organised, driven and a sales record to match. He drives through the issuing business and captures all revenues and commissions in the most efficient manner. Anthony is key to the efficient stream of payments required for this business model.

Directors:

Re-structure 2017

Darren

Kirby

The final decision maker as majority shareholder means critical decisions will fall to him. A mandate to find new investors and revenue streams for CWM. An ambassadorial role and a creative thinker for the company, bringing fresh ideas on many aspects of the business both operational and non-operational.

Neil

Hathaway

Key point of contact for the sales force. A remit to push the sales force to meet targets and close business. He will be in control of sales, possible bond lists as well as monitoring the business / LOA levels for each adviser. He will also have a key role in writing new business. This will be a target driven management position. All advisers will report directly to him.

Dean

Stogsdill

Complete oversight of the business operationally with a close working relationship with the Chairman and COO. I will manage the company direction and overall development planning, strategies and high level management with department heads reporting directly to me. I will chair board meetings and deal with technical and regulatory planning. I will also be heavily involved in the efficient management of the investment book.

Anthony

Downs

Full control of new business. A remit to drive through the revenues from written business to maximize the cashflow of the company. Target driven with targets based on company income needs, outstanding requirements and business written.

With the current admin levels and management restructure we should be able to easily handle up to 7 bonds per week, plus client after care, outstanding requirements, investment and re-investment. We do not hire any more administration in 2017. Although this will be adjusted if business levels exceed 7 bonds per week.

We are now a company where you perform, meet your

target or you are replaced.

Of the 9 bond writers, we have 1 in France, 1 in Turkey, 1 in Portugal and the other 6 are in Spain. I believe that we need to build up the business levels so that 9 bond writers can meet a target of 30 bonds per man for the year or an average of 3 a month, based on a 10 month / 40-week year. This would mean a company wide total of 270 bonds, at our target average of €10,000 commission per bond that would mean turnover of 2.7 million plus trail of €300,000 meaning a total of €3,000,000 for 2017.

Call Centres – Cold calling with appointments made and revenue generated through call centres and call centres paid for on performance only.

Market

history:

Historically we have concentrated on cold calling, Grant A Wish (“charity”) events, web videos, website and referrals from existing clients. The cold calling aspect is becoming more and more difficult and time consuming and other areas of marketing ourselves and our products must be found.

Victims of the Continental Wealth Management scam met Mail on Sunday’s Laura Shannon

Mail on Sunday’s Laura Shannon met a group of victims of the Continental Wealth Management scam in Denia in July 2019.

Here is a link to her excellent article Continental Wealth Management – “Plunder in paradise”: MAIL ON SUNDAY ARTICLE

All power to her, this young lady put all other would-be investigative journalists to shame. Laura jumped on a plane on 24th July 2019 when she and her editor heard about the Continental Wealth Management scandal. After a long, hot bus journey from Alicante airport, she got straight down to business. She spent all afternoon interviewing a large group of distressed investors. She then attended the memorial service for one victim who had been killed by the stress he suffered when he lost his pension – thanks to Continental Wealth Management’s Darren Kirby.

Laura Shannon – putting all other “investigative” journalists to shame

No other British journalist has bothered to do this. No other national newspaper has taken such an interest in this important story – about how British people have been scammed by British advisers in Europe’s leading expat destination.

Clearly shaken by the extent of the Continental Wealth Management scam, and the plight of the victims, Laura was deeply moved by the memorial service for victim Mark Davison who had died two weeks earlier. After a very long and tiring day, Laura retired to her hotel to write up her notes – ahead of another full day of meeting more victims.

So where had all the other so-called newspapers been all this time? Where were The Sun, The Times, The Telegraph, The Mirror, The Guardian, The Express? Too lazy – and clearly not concerned with this very British problem. These newspapers do indeed have some very fine journalists – but this widespread financial crime was too low on their priority list.

On the second day of her visit, Laura Shannon met another group of Continental Wealth’s victims and also spoke to a couple in France by Skype. Her final interview with an elderly lady (who had tried to commit suicide when she lost most of her life savings to the Continental Wealth Management scammers) left her in tears.

At lunch time, Laura headed back to Alicante airport. Four and a half months pregnant, this energetic and passionate young woman returned to her office in Birmingham to write and file her story. She left little out and covered most of the basic points. Her article left the reader in no doubt: financial crime has flourished in Spain for years.

There are both criminal and civil actions ongoing now – on the Costa Blanca and the Costa del Sol. The days of unqualified “chiringuitos” and unlicensed firms are hopefully over. While Britain’s feeble excuse for a regulator – the FCA run by lazy loser Andrew Bailey – fails to take any meaningful action, the Spanish regulator has at least ruled that failing to comply with Spanish regulations is a criminal offence.

The Malta regulator has tightened up rules to help stop firms operating similar scams from abusing QROPS, and deploying inappropriate investment policies. Multiple class actions in various jurisdictions are taking legal action against rogue insurance companies – such as Old Mutual International – who have encouraged and profited from widespread financial crime.

Ward’s luxury development at 64 Calle Haya, Moraira, Alicante

And this is the problem: crime pays. Stephen Ward of Premier Pension Solutions in Moraira is now adding to his ten mortgage-free luxury villa property portfolio in Florida by building a huge luxury villa next to his former office in Calle Haya in Moraira.

Paul Clarke – Darren Kirby’s former business partner (when Continental Wealth Management was first set up) has for years been seen zooming around the Costa Blanca in his Aston Martin. And Jody Smart (or Bell or Kirby) – Darren Kirby’s former girlfriend has boasted of the £13 million she earned as director of Continental Wealth Management.

Sipping champagne while publicising her fashion empire on Youtube

Jody now runs a swish ocean-front restaurant in Calpe with fiance Franco Pearson – seemingly untroubled by the appalling trail of devastation left behind her in the wake of the Continental Wealth Management tragedy.

But the millions made by the scammers at Continental Wealth Management pale into insignificance when compared to the fortunes made by life offices Old Mutual International, SEB and Generali.

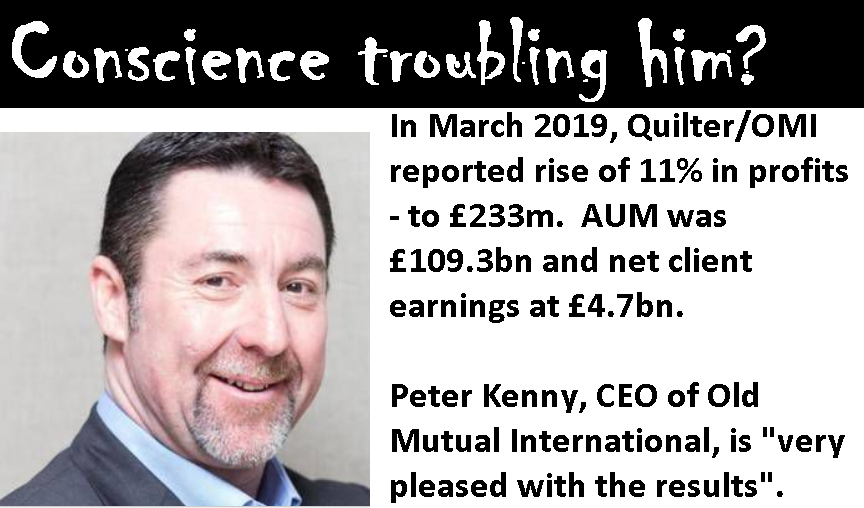

Not a hint of regret for OMI’s actions – or shame at his broken promises.

Peter Kenny did promise to pay compensation to OMI’s victims. But this was just a ruse to get me to take down my blogs about OMI so that the IPO would earn him and his accomplices more £ millions.

The Spanish regulator has made it clear it is a criminal offence to sell insurance “bonds”.

No firm with a conscience or any professional ethics should ever use OMI, SEB or Generali. Anyone caught mis-selling such insurance bonds in Spain is committing a criminal offence and can face jail. As most advisory firms in Spain are still doing so vigorously and unashamedly (with the same old lame excuse that such bonds are “tax efficient”), the Spanish jails are likely to get pretty crowded in the not-too-distant future.

But how do people avoid getting scammed from now on?

Part of the problem is knowing what questions to ask – and then being able to understand the answers. Unfortunately, Stephen Ward was the exception to the rule – since he was highly qualified and his firm – Premier Pension Solutions – was authorised to provide investment advice.

1. Check that the firm is authorised (regulated; licensed). If investment advice is given, make sure the firm has an investment license: don’t be fooled into believing that an insurance license is enough. It isn’t.

2. Check that the adviser is qualified to give financial advice. He or she must provide evidence of any qualifications claimed. If the relevant institute does not show the qualification, then the adviser is not qualified – no matter what exams may have been passed previously.

3. Don’t get talked into an insurance bond (aka “life bond” or portfolio bond). They are expensive and unnecessary – and only serve to pay the adviser a fat commission.

4. Don’t let an adviser invest your funds into expensive, risky assets which are only there to pay fat, undisclosed commissions FROM YOUR MONEY.

Lastly, make sure you get everything – all costs, fees, charges and commissions – in writing. DON’T GET SCAMMED LIKE THE CONTINENTAL WEALTH MANAGEMENT VICTIMS. They will all give you exactly the same advice.

TPR has been neither coy nor shy in its published determination against Ward and Salih – and has openly called the London Quantum pension scheme, and the risky investments which Ward made, a “scam”.

But to any reasonable person’s mind, tPR’s determination in relation to Ward and London Quantum raises more questions than it answers. In fact, I would go even further and say that HMRC’s and tPR’s incompetence – as well as Dalriada Trustees‘ own failings – should be examined in parallel with Ward’s multiple frauds.

Because, make no mistake, London Quantum was only one of many.

It all started long before the Ark Pensions scam. Ward set out his stall transferring pensions to New Zealand and liberating 100% “tax free”. He boasted in the local Costa Blanca press that he had “helped” thousands of clients liberate their pensions (legally). Of course, this may have been free of tax in New Zealand, but when the Spanish tax authorities catch up with these clients, there will be a very expensive disaster.

It is extremely worrying that IVCM – a “phoenix” of the Brooklands disaster – is also offering the same New Zealand liberation facility today. It always worries me when firms fail to learn the lessons of past scams and expose unsuspecting victims to the same catastrophes that past scammers orchestrated. Add to this the fact that IVCM is regulated out of Gibraltar – the jurisdiction of choice for scammers such as XXXX XXXX and STM Fidecs – and I think it is well worth giving IVCM a very wide berth.

Prior to 2010, Ward was a tied agent of Inter Alliance – a company based in Cyprus which had an insurance license. For Inter Alliance in Cyprus, Ward successfully created the illusion that this gave his company Premier Pension Solutions some sort of license. But, in reality, it did not – as the Cyprus license was only for Inter Alliance and not for any other entity. Plus tied agents were (and still are) illegal in Spain.

As a sideline, Ward was flogging EEA Life Settlements as he had discovered the delights of making huge commissions out of dodgy, risky, illiquid investments to his unsuspecting victims. In 2010, Ward was working closely with Concept Trustees in Guernsey – run by Roger Berry. Initially happy to see Concept Trustees’ QROPS members have 100% of their pensions invested by Ward in EEA, Berry eventually realised that Ward’s firm was not regulated as it had been dumped by Inter Alliance. Of course, even before it had been dumped, Premier Pension Solutions wasn’t regulated anyway. But Concept Trustees was too stupid to realise that.

Concept then wrote to all the members who were clients of Ward’s Premier Pension Solutions and warned them that Ward’s firm was neither regulated nor had any professional indemnity insurance cover. Berry claimed he would not be accepting any further investment instructions from Ward, but this was basically just a load of hot air (aka lying) as he continued to accept investment instructions into EEA by Ward.

In September 2010, Premier Pension Solutions was appointed as a tied agent of AES International – a firm based in London and Dubai. The agency agreement covered PPS for investment and insurance business – but not pension transfer business. Ward’s PPS letterheaded paper claimed that it was a “partner” of AES and that it was regulated by the DGS (Spanish insurance regulator) and CNMV (Spanish investment regulator). PPS also became a member of FEIFA – the Federation of European Independent Financial Advisers (although he was later dumped by them). You can understand why so many victims thought that PPS was a bona fide advisory firm.

Then came the first of Ward’s major pension scams: Ark. It is worth looking at the history of Ark because this sets the scene for how nearly 500 victims came to lose their pensions and face tax liabilities – as well as the dozens of further scams operated by Ward (including London Quantum).

A famous footballer and his mate – a football club owner – bought a plot of land in Larnaca in Cyprus with a view to turning it into a golf resort. They paid £1.1 million for the property, but then realised it wasn’t big enough for a whole golf course (neither of them was bright enough to be able to count up to 18) and so they tried to find some other investors. The chumps they tried to con into buying more land adjacent to the original plot either couldn’t come up with the money or were frightened off such a high-risk, illiquid investment.

So the sporty pair went to see the footballer’s accountant – Andrew Isles of Isles and Storer (now owned by LB Group). Isles soothed the sporty pair’s worries by telling them that securing more investors was simple: just start a pension fund! He introduced them to what he called “two leading pension experts”: Craig Tweedley and Stephen Ward. Tweedley was already operating the KJK Investments/G Loans pension liberation scam (later to be placed in the hands of Dalriada Trustees by the Pensions Regulator) and Ward was a highly-qualified pensions expert, examiner and author.

The rest is history as nearly 500 victims lost their pensions to the Ark scam. But the sporty pair did very nicely – they sold the land in Cyprus to the Ark scheme for £4 million and pocketed the profit. The footballer tried to hide the money in Dubai but got caught and turned Queens Evidence. He and the other original investor (the football club owner) fell out and they ended up in court against each other – with the footballer triumphing. Andrew Isles also did very nicely as he sold introductions to a number of his clients and earned fat commissions in doing so.

As Ark unfolded – between mid 2010 and mid 2011 – Ward initially acted as an introducer. There were various introducers – many recruited by Ward when he ran a series of seminars in various parts of the UK. But Ward himself was the biggest introducer – accounting for more than a third of the whole £27 million fund and earning approaching three quarters of a million pounds in fees (the Pensions Regulator’s report of £350k was way off the mark).

Ward and his sidekick – bent lawyer Alan Fowler of Stevens and Bolton Solicitors – acted as the controlling minds behind Ark. The scheme documentation and the “loan” contracts were drawn up and explained by Ward and Fowler. Of the 5% commission charged by Craig Tweedley, Ward got at least 2% plus a transfer fee. But Ward had his eye on a much bigger proportion of the fees. Towards the end of the life of Ark, Ward was preparing to take Ark over from Tweedley – along with an associate of his: Peter Moat (another pension crook who went on to operate the Fast Pensions scam – now also in the hands of Dalriada Trustees). In a way, it was a shame that didn’t happen, as Tweedley did at least try to help the Ark victims, whereas Ward never lifted a finger. In fact, he simply told the Ark victims to throw the tax demands away as “HMRC would never pursue them”.

In February 2011, HMRC met with Tweedley and Ward to discuss the “loans” – so HMRC knew perfectly well that Ward was the main brain behind the scam. It is, therefore, astonishing that they did nothing to stop him operating so many further pension scams.

Ark came to a shuddering halt on 31st May 2011, when tPR appointed Dalriada Trustees and the scheme was suspended. Dalriada went up to Yorkshire to confront Crag Tweedley and relieve him of all the evidence and files relating to the scam. Tweedley told Dalriada that all the records were held down at Ward’s Manchester office at 31, Memorial Road and he drove down to collect them from Anthony Salih. He arrived to find Salih removing all the Premier Pension Solutions fee agreements on the instructions of Ward (he managed to shred most of them – but did missed a few which I now have).

After Ark, Ward went on to run the Evergreen Retirement Benefits QROPS scam with accompanying 50% “loans” and a further 300 victims lost £10 million worth of pensions. HMRC removed Evergreen from the QROPS list when they realised it was a liberation scam and Ward fell back on two more UK-based, bogus occupational schemes: Southlands and Headforte. Plus, he registered a number of new schemes – including Capita Oak.

The Capita Oak scheme was another bogus occupational scheme registered by Ward with a fictitious sponsoring employer: RP Medplant (Cyprus). There is, however, a firm called RP Med Plant in Cyprus. The Capita Oak trust deed was written by Ward’s bent lawyer Alan Fowler. Ward took responsibility for the transfer administration – transferring valuable personal and final salary occupational pensions into this scam – in the full knowledge that he was condemning hundreds of victims to certain financial ruin and poverty in retirement. Capita Oak is now also in the hands of Dalriada Trustees.

Other pension scams that Ward was operating – in addition to Southlands and Headforte – from 2012 onwards included Feldspar, Hammerley, Meribel, Halkin, Randwick, Bollington Wood and Westminster. And, of course, Dorrixo Alliance which was the trustee for many of these scams. Capita Oak and Westminster are both under investigation by the Serious Fraud Office.

How much more evidence do they need?

In May 2014, HMRC was given evidence of all of Ward’s various scams – including Dorrixo Alliance. They were also given detailed testimony by me and a number of victims of what Ward had been up to in the pension liberation fraud industry since Ark. It would have been very easy for HMRC to look up to see what other pension schemes Dorrixo was trustee to. Had they done this, they would have seen that Dorrixo was the trustee for the London Quantum scheme. If HMRC had taken any action, they could have prevented Mr. N – a serving police officer – and 96 other victims from losing their pensions to Ward and his various dodgy, inappropriate investments (including loans to Dolphin Trust).

If we add to the above catalogue of scams the Continental Wealth Management scam – 1,000 victims facing the loss of £100 million worth of life savings – Ward has been responsible for the destruction of thousands of people’s pensions this past eight years. Plus several suicides and deaths from stress-related medical conditions.

SERIOUS QUESTIONS ARISING FROM THE PENSIONS REGULATOR’S DETERMINATION RE:

Mr Stephen Alexander Ward – The Pensions Regulator case ref: C46205159

Ward was a director of Dorrixo from 13 October 2011 to 28 April 2015. A company called Quantum Investment Management Solutions LLP (“QIMS”) has at all material times been the sole sponsoring employer of the Scheme. Dorrixo became the sole trustee of the Scheme on 19 April 2014. Dorrixo is also recorded as being the Scheme administrator.

HMRC AND TPR WERE GIVEN EVIDENCE OF WARD’S COMPANY, DORRIXO, IN MAY 2014. THEY WERE ALSO GIVEN EVIDENCE OF A LARGE NUMBER OF SCAMS WARD OPERATED AFTER ARK – ALL INVOLVING LIBERATION FRAUD. WHY WASN’T ACTION TAKEN TO PREVENT LONDON QUANTUM? ALL 97 VICTIMS – INCLUDING A SERVING POLICE OFFICER – COULD HAVE BEEN PREVENTED.

On 18 June 2015 the Regulator appointed Dalriada Trustees Limited (“Dalriada”) as an independent trustee to the Scheme, with exclusive powers.

HAS ONE SINGLE PENNY EVER BEEN RETURNED TO ANY OF THE PENSION SCAMS PLACED IN THE HANDS OF DALRIADA TRUSTEES? THERE ARE DOZENS OF THEM, AND FEW – IF ANY – OTHER INDEPENDENT TRUSTEES ARE EVER APPOINTED BY TPR. BUT THERE SEEMS TO BE NO RECORD OF ONE SINGLE MEMBER EVER GETTING ANY RETURN FROM ANY OF THE SCHEMES IN THE PAST EIGHT YEARS – DESPITE THE MANY MILLIONS DALRIADA HAVE PAID THEMSELVES FROM THESE SCHEMES.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

AS THIS EVIDENCES THAT THIS SCAM COULD EASILY HAVE DWARFED ARK IN A VERY SHORT SPACE OF TIME, DON’T HMRC AND TPR RECOGNISE THAT THEIR LAZINESS AND NEGLIGENCE NEED TO BE ADDRESSED? THEY LEARNED NOTHING FROM ARK – AND WHILE THERE ARE VALID CRITICISMS OF WARD FOR HAVING LEARNED NOTHING, HE IS JUST A COMMON SPIV WHILE HMRC AND TPR ARE SUPPOSED TO BE GOVERNMENT DEPARTMENTS WITH A RESPONSIBILITY TO PROTECT THE PUBLIC. THE SCALE OF THIS SCAM SHOWS THESE TWO ORGANISATIONS ARE NOTHING BUT HOPELESSLY INEPT AND AMATEURISH IN THEIR APPROACH TO DILIGENCE AND PUBLIC RESPONSIBILITY.

The Scheme was promoted to potential new members by introducers. These included the following entities: GoBMV; Baird Dunbar; What Partnership; the Resort Group PLC; Friendly Investments; Premier Mark Consultants and Quantum Wealth Management Solutions Limited.

THE DANGERS OF THE SCOURGE OF “INTRODUCERS” SHOULD HAVE BEEN LEARNED FROM THE ARK SCAM IN 2011. WARD RECRUITED DOZENS OF THEM ALL OVER THE COUNTRY. AND YET NONE OF THEM HAS EVER BEEN BROUGHT TO JUSTICE FOR THEIR PART IN ARK, AND HAVE GONE ON TO OPERATE AS INTRODUCERS AND EVEN HOLD KEY CENTRAL ROLES IN LATER SCAMS. THIS INCLUDES FRIENDLY INVESTMENTS AND JULIAN HANSON – WHOSE SCHEMES ARE NOW ALSO IN THE HANDS OF DALRIADA TRUSTEES.

Gerard was responsible for producing template risk letters, member application forms, pro forma declarations stating that the person signing them was a self-certified sophisticated investor, member booklets and the statement of investment principles (of which there were four versions). Gerard sent these documents to members once they had been introduced to the Scheme by an introducer.

GERARD ASSOCIATES, RUN BY GARY BARLOW, HAD ACTED AS AN INTRODUCER TO WARD IN THE ARK SCAM. AND YET HE WAS LEFT FREE TO OPERATE IN THE SAME CAPACITY IN THE LONDON QUANTUM SCAM – AND EVEN TAKE ON A MORE CENTRAL ROLE. GERARD ASSOCIATES WAS AT THE TIME AN FCA-REGULATED FIRM – AND REMAINS SO TO THIS DAY. THE FCA HAS TAKEN NO ACTION TO REMOVE THIS FIRM OR TAKE ANY ACTION AGAINST GARY BARLOW.

GERARD ASSOCIATES’ GARY BARLOW WAS PAID £253,000 FROM THE LONDON QUANTUM SCHEME FOR DEFRAUDING VICTIMS INTO SIGNING AGREEMENTS THAT THEY WERE “SOPHISTICATED” INVESTORS. SO WHY HASN’T BARLOW BEEN PROSECUTED AND JAILED – AND MADE TO PAY THIS MONEY BACK TO THE VICTIMS?

A material number of the new members had a low or medium appetite for investment risk and, in any event, were unaware that the Scheme’s investments were high-risk investments. The Panel was troubled by the apparent disconnect between members’ appetite for risk and the high risk nature of the investments made by Dorrixo. Mr Ward accepted that the Scheme’s investments were high risk, but claimed this was made clear to new members in the Member Booklet.

I DON’T KNOW WHAT SORT OF DRUNKEN DUMMIES MADE UP TPR’S “PANEL”, BUT DID THEY SERIOUSLY THINK THAT ANY PENSION FUNDS SHOULD EVER INVEST IN HIGH-RISK CRAP? INDIVIDUAL MEMBERS’ APPETITE FOR INVESTMENT RISK IS IRRELEVANT – THIS WAS A PENSION FUND, NOT A CASINO.

The case against Ward was based on failures of competence and capability, and also a lack of honesty and integrity as well as Ward’s involvement with “pension liberation” as an introducer of members to the “Ark” schemes.

BUT TPR AND HMRC KNEW ALL ABOUT THIS BACK IN 2010 AND 2011. WHY DID THEY DO NOTHING TO PREVENT WARD FROM SCAMMING MORE VICTIMS OUT OF MORE MILLIONS OF POUNDS. THEY STOOD BACK AND WATCHED – DESPITE HAVING HARD EVIDENCE THAT HE WAS STILL UP TO HIS CRIMINAL MISCHIEF.

Mr Ward did not dispute that a company of his (Premier Pensions Solutions SL) was involved in introducing members to the Ark Schemes, but states that the relevant activity pre-dated any finding by the courts of pensions liberation and that Mr Ward had no knowledge that the schemes were being used for such activity.

BUT HMRC, TPR AND DALRIADA ALL KNOW THIS ISN’T TRUE. THEY HAVE ALL SEEN EVIDENCE THAT WARD AND HIS BENT LAWYER ALAN FOWLER ACTUALLY PRODUCED THE “LOAN” (MPVA) DOCUMENTATION AND EXPLAINED THE LOANS IN SOME CONSIDERABLE DETAIL TO THE VICTIMS. THE MPVA CONTRACTS WERE DRAWN UP BY FOWLER. IS IT REALLY CREDIBLE THAT NEITHER HMRC NOR TPR WOULD HAVE OBJECTED TO THIS STATEMENT?

The Panel did not consider there was sufficient evidence of Ward having actual knowledge of, or turning a blind eye to, the illegal nature of the activity of the Ark Schemes when carrying out his role as introducer before.

SERIOUSLY? I HAVE GIVEN EVIDENCE OF THIS TO BOTH HMRC AND TPR ON MANY OCCASIONS. THIS HAS BEEN DISCUSSED AT MEETINGS WITH DALRIADA TRUSTEES ON MANY OCCASIONS. EVIDENCE OF THIS HAS BEEN GIVEN TO THE SERIOUS FRAUD OFFICE ON MANY OCCASIONS BY VARIOUS VICTIMS AND ME. WHAT FURTHER EVIDENCE DID THE PANEL WANT? EVERY ARK MEMBER’S FILE WAS FULL OF SUCH EVIDENCE. EITHER TPR IS LYING OR IT IS INCOMPETENT. OR BOTH.

The Case Team also relied on certain alleged failures in relation to other pension schemes (called Headforte and Halkin), of which Mr Ward was a trustee. These are denied by him (e.g. an allegation of failure to appoint an auditor to those schemes) and the Panel did not consider it necessary to make findings in respect of them.

SO WHAT ACTION HAS TPR TAKEN IN RELATION TO HEADFORTE AND HALKIN? BOTH WERE BEING USED FOR PENSION LIBERATION FRAUD BY WARD – AND YET THE VICTIMS PROBABLY STILL HAVE NO IDEA WHAT HAS HAPPENED TO THEIR MONEY. IT IS ABSOLUTELY ASTONISHING THAT NO ACTION HAS BEEN TAKEN IN RELATION TO THESE TWO SCHEMES, PLUS ALL THE OTHERS WARD HAS BEEN OPERATING OVER THE YEARS.

Stephen Alexander Ward (date of birth 11 July 1955) is hereby prohibited from being a trustee of trust schemes in general. This order has the effect of removing the above-named individual from all or any schemes of which he is a trustee. By section 6 of the Pensions Act 1995, any person who purports to act as a trustee of a trust scheme whilst prohibited under section 3 is guilty of an offence and liable (a) on summary conviction to a fine not exceeding the statutory maximum, and (b) on conviction on indictment to a fine or imprisonment or both.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

THIS IS NOT JUST THE DEATH OF TRUST, BUT OF ANY CONFIDENCE IN THE GOVERNMENT, REGULATORS AND CRIME PREVENTION AGENCIES TO PREVENT OR DEAL WITH PENSION SCAMS AND SCAMMERS.

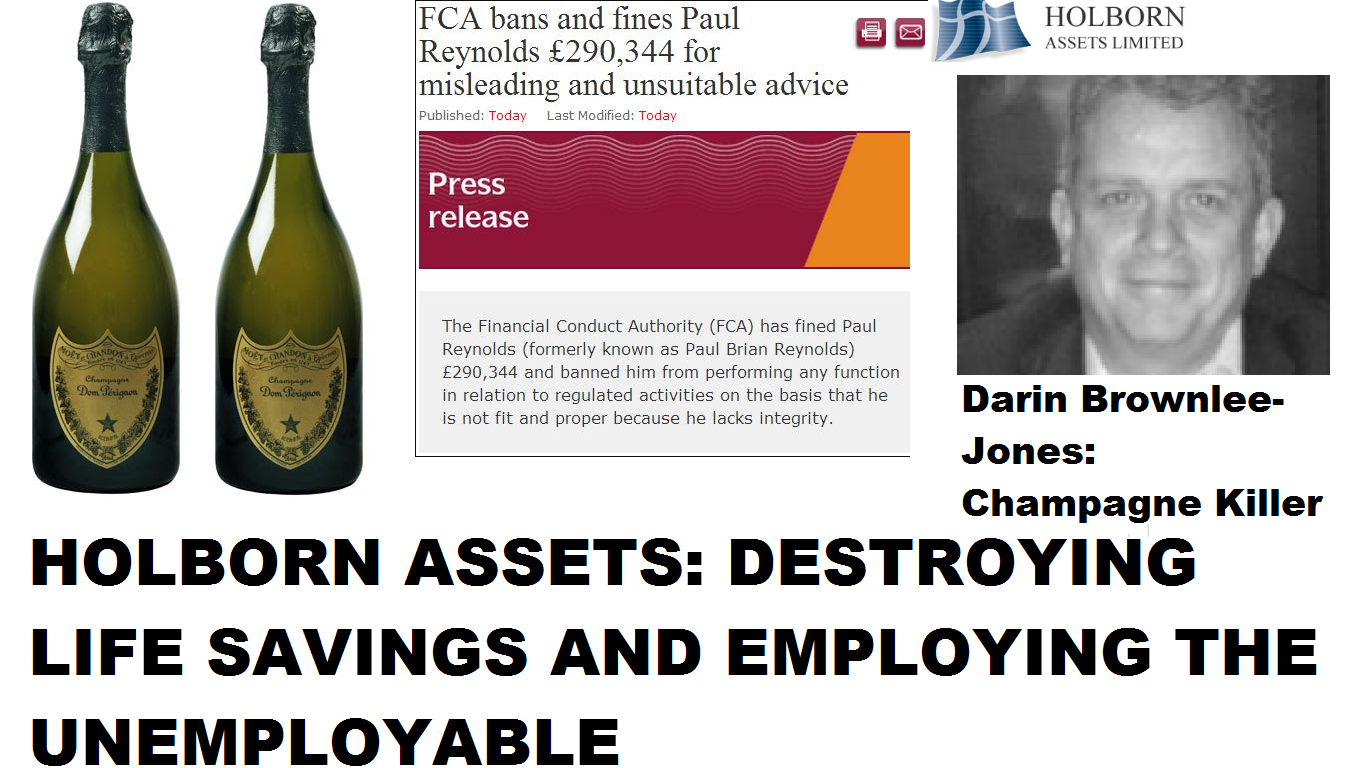

Holborn Assets mercilessly leaves its victims facing financial ruin

HOLBORN ASSETS “CHAMPAGNE KILLER” APPROACH TO FINANCIAL ADVICE IS DESTROYING VICTIMS’ LIFE SAVINGS

Holborn Assets “Champagne Killer” approach to financial advice is ruining victims. Holborn Assets is routinely destroying people’s pensions and life savings, and refusing to compensate the distraught victims facing poverty in retirement. The so-called “advisers” at Holborn Assets give investment advice (often unregulated) which entails investing victims’ funds in whatever toxic, illiquid, high-risk rubbish pays the highest commissions, and then leave the devastated investors hung out to dry. Neither the firm nor the “advisers” responsible for this outrage show any compassion or contrition. This is no different to the callous actions of a common drunk, hit-and-run driver.

As if this wasn’t bad enough, Holborn Assets also employs Darin Brownlee-Jones: the “Champagne Killer“. A drunk hit-and-run driver who killed an innocent man then walked away to drink champagne. He didn’t stop to try to help the victim he left dying in the road – or show any remorse for the horrible, painful death the poor man suffered.

Holborn Assets seems to make a habit out of employing the unemployable. First, there was Paul Reynolds who was banned by the FCA and fined nearly £300,000 for giving unsuitable and misleading financial advice. The FCA declared Reynolds was not a fit and proper person to give financial advice. But Uncle Bob Parker of Holborn Assets Dubai welcomed him with open arms – and Reynolds has since changed his name to try to conceal his unsavoury past. But I bumped into Reynolds when I was at the Holborn Assets office at the end of 2015 – so I know it is him despite trying to change his appearance as well as his name.

And now there is Darin Brownlee-Jones who is commissioning pension reports for more poor unfortunate victims. These people are transferring their defined benefit pension schemes to offshore QROPS in dodgy jurisdictions where negligent trustees peddle their toxic wares. In one case, Brownlee-Jones has employed a Spanish firm to sign off a DB transfer for a resident of France. The advice is covered (allegedly) by the Spanish insurance regulator (which doesn’t cover pension or investment advice) and not the French regulator or the FCA.

So why would Brownlee-Jones in Dubai get a Spanish firm to provide unregulated advice to an investor in France? In 2003, the FSA had refused an application from Brownlee Jones to perform investment and pension-transfer functions. The reason was that the FSA did not consider him to be a fit and proper person as he had indecently assaulted a woman, caused criminal damage and death by dangerous driving.

I think any reasonable person would agree that Brownlee-Jones was the last person you would want handling investment and pension advice. But Bob Parker at Holborn Assets clearly likes having misfits, FCA rejects, sex offenders, drunks and killers on his team.

Brownlee-Jones: after a belly full of beer in 1999, got into his car and hit a motor cyclist head on. He left the poor man dying in a pool of blood and went to celebrate at his favourite wine bar. He ordered two bottles of Dom Perignon champagne at £95 apiece. When he was arrested, he was quaffing his favourite bubbly – although he probably wasn’t smiling quite so broadly when he was jailed for four years.

The distraught father of the victim said that Brownlee-Jones had treated his dying son “like an animal“. And yet Bob Parker employs this callous killer and encourages him to provide unregulated pension advice to victims in France and Spain.

This routine callousness is shown by Bob Parker and many other Holborn Assets salesmen. Where their victims’ pensions and investments have been decimated by high-risk structured notes and unregulated, toxic, illiquid funds -such as Premier New Earth Recycling – Holborn Assets just shrugs and leaves the victims to face poverty in retirement. Once they have earned their fat commissions from the victims’ pension funds, Holborn Assets doesn’t want to know any more. Bob Parker and his merry men simply walk away without a backward glance.

Holborn Assets has been aggressively targeting new victims with a cold-calling campaign using a well-known boiler-room scam operation in Manchester. The cold calls to Spanish residents are followed up by salesmen such as Jason Ryder who claims that Holborn Assets have offices in Barcelona and Marbella. Of course, Holborn Assets is not licensed to operate in Spain – and once conned into letting these cowboys plunder their pensions for fat commissions and fees, there is no regulator to complain to.

Apart from Bob Parker, Paul Reynolds, Darin Brownlee-Jones and a bunch of other “snake oil salesmen”, there are some people at Holborn Assets who do have some ethics and a conscience. Surely, if these people had any sense they would distance themselves from this cesspit of financial disservice? Why stay with a firm with such an appalling track record?

Below is a list of all the people who work for Holborn Assets (excluding admin and finance). I wonder if a single one of them will feel some sense of disgrace at being a part of this “champagne killer” approach to financial services?

If not a single one of the above group of people is prepared to put ethics and principles at the top of their agenda and ensure their professional reputations are not sullied by the “champagne killer” approach to financial advice, then there truly is no hope for Holborn Assets.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

& David Vilka (right) splashing stolen pension funds in Vegas")

Then came the first of Ward’s

Then came the first of Ward’s  After Ark, Ward went on to run the

After Ark, Ward went on to run the

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member. SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.