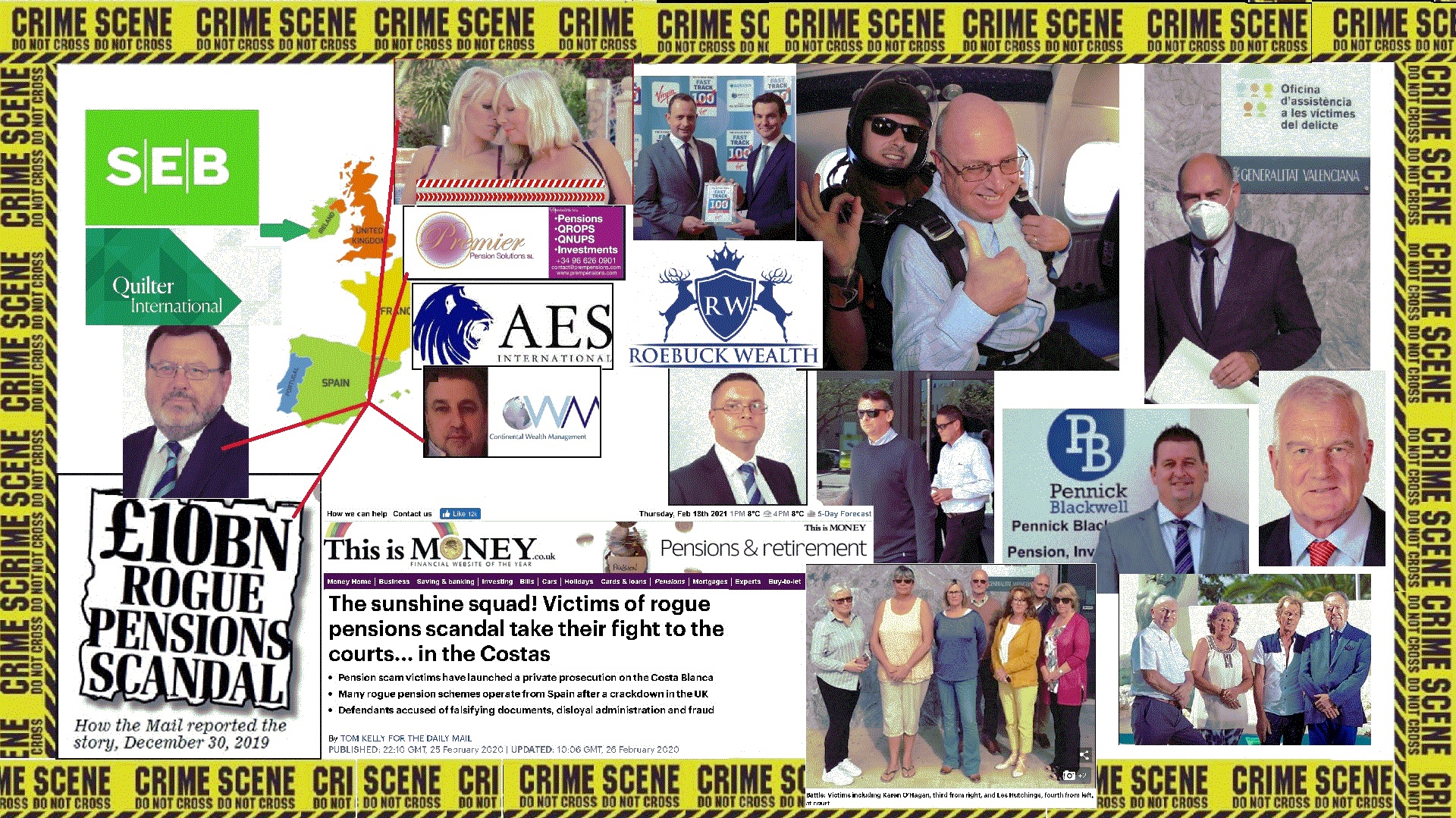

The Spanish criminal trial of so-called “financial advisers” in Denia has exposed the widespread fraud routinely committed in offshore financial services for over a decade.

This particular stage of this particular trial may be directed at just eight members of Continental Wealth Management and Premier Pension Solutions. For now. But the case – brought by Pension Life – needs to be extended to all parties who have committed similar offences in offshore financial services.

Spain is the second-largest expat jurisdiction in the world – after Australia. More than three quarters of a million British expats have settled in the Spanish sunshine. That’s over half the total in the whole of Australia. And these Spanish-resident expats are sitting targets for pension scammers.

It is not unusual for Brits to be suspicious of foreigners in any country. Expats typically veer towards their own countrymen. They are notorious for being suspicious of foreign food and customs. Hence, the depressing fact that it is British scammers who relieve British victims of their pensions and life savings.

And this is why so many British expats – especially in Spain – fall prey to bogus “financial advisers” flogging bogus life assurance policies provided by bogus insurance companies – like Quilter International headed up by Peter Kenny.

The facts of this criminal case are indisputable. One thousand victims were scammed by Continental Wealth Management. Between 2009 and 2017, these victims lost many millions of pounds’ worth of pensions and life savings. And much of this was facilitated by Quilter International (formerly Old Mutual International).

So how were these losses caused? What on earth went wrong? Financial services – in any country – should be a safe industry which investors can rely on. Depend on. Why have so many expats – not just the Continental Wealth Management victims – lost so much money?

Who and what is to blame for the loss of hundreds of millions of pounds?

The short version of the answer is: “COMMISSIONS”. Offshore advisers get rich by selling products for commissions. What they don’t sell is independent financial advice. Proper independent advice (provided by a correctly and properly qualified and licensed adviser) is about recommending an appropriate investment strategy which is in the best interests of the client. And, of course, charging a reasonable and commercially-viable fee for such advice.

But that rarely – if ever – happens in offshore, expat jurisdictions. What is cleverly presented as “advice” is generally just a dishonest ploy to sell a client unsuitable products which they don’t need and that will make the salesman the most commission.

The orchestrators, facilitators and architects of all this fraud are the “life offices”. In practice and in reality, these companies are more about death than life. Their business is about destroying life savings and pensions – while enriching the pockets of fraudsters.

There are various ways to combat this widespread fraud facilitated by the life offices:

Bring criminal proceedings against ALL those who have defrauded their clients – from bogus, unlicensed advisory firms to the life offices themselves

Ensure all so-called advisory firms (sometimes calling themselves “wealth managers”) are correctly licensed in the jurisdiction where they provide advice

Make it mandatory for all advisers to be properly qualified to provide financial advice

Ban all firms without an investment license from providing investment advice

Educate consumers to only use advisory firms which openly disclose their professional indemnity insurance on their website

The bald truth is that if the life offices – such as Quilter International, Friends Provident International and RL360 – were closed down, this widespread fraud would stop.

The only way this fraud keeps going so vigorously and relentlessly, is the terms of business given by the life offices to the scammers. And, of course, the fat commissions the life offices pay to them. As well as the toxic, risky, high-commission-paying investments the life offices put on their “platforms” for the scammers to use (and abuse).

You only have to look at Continental Wealth Management to see how quickly a scamming firm will collapse once life offices withdraw terms of business. The life offices are the life blood of scams and scammers.

Without the facilitation of the “death” offices (Quilter International, Generali, SEB etc.) frauds such as Continental Wealth Management could not have taken place. The blood of all those who have died wretched, lonely deaths – and those who are suicidal – is squarely on the hands of Peter Kenny and his various cronies.

The bank statements of Continental Wealth Management show the repeated amounts of fat commissions paid by Quilter International, Generali and SEB. And these amounts were paid willingly and cheerfully in the full knowledge that every payment meant more lives damaged; more funds destroyed; more miserable deaths.

Quilter and their associates had reported on the victims’ losses for a decade; produced valuations and transaction histories evidencing the repeated, relentless fraud. And yet Quilter (and the other death offices) did nothing – just kept on and on facilitating the same fraud: repeat, repeat, repeat.

While the “advisers” from Continental Wealth Management and Premier Pension Solutions stand trial – the hundreds of victims have to listen to the defendants’ offensive denials and excuses. But, worst of all, the distressed and impoverished victims know that the life (death) offices should also be on trial – standing shoulder to shoulder with the scammers themselves.

The cause of the investment losses in the Continental Wealth Management case was almost exclusively toxic, high-risk (and high-commission) structured notes. These are complex investment instruments called “derivatives” and should only ever be used for professional or sophisticated investors. They are certainly completely unsuitable for ordinary people (who are classed as retail investors) or for pension schemes.

High-risk structured notes are big business for the death offices. Quilter International (formerly Old Mutual International) has historically onboarded over 100 new structured products per month. In the case of the Continental Wealth Management fraud, it was the structured notes – from Leonteq, Commerzbank, Royal Bank of Canada and Nomura – which caused the terrible investment losses. These toxic, high-commission investment products – so beloved by the scammers because of the high commissions – were responsible for the destruction of millions of pounds’ worth of pensions and life savings.

Quilter International knew perfectly well that these toxic products – totally unsuitable for retail investors – paid 8% commission to the scammers and a further 8% to 10% to the “arrangers”. They knew perfectly well – and admitted internally to their “asset review committee” – that these products were risky and “not good value”. But they still allowed the scammers (to whom they gave terms of business) to keep selling them.

Quilter has also admitted that they had 2,047 structured products in total, and that the average holding per product was £243,654.03; that the smallest holding was £67.54 and the largest holding was £5,350,833.60. Quilter was concerned that there was a reputational risk to Quilter for allowing these structured products to be held within their offshore bonds. They also acknowledged that these products carried excessive commissions and were causing “suboptimal customer outcomes”. However, their concern for their own “reputational risk” did not extend to concern for their victims.

Quilter has tried to wriggle out of culpability for the victims’ losses by claiming that investment product “suitability” is the responsibility of advisers. And that these so-called advisers are participating in a “race to the bottom”.

However, the advisers are mostly scammers to whom Quilter has cheerfully given terms of business. And they are winning the race to the bottom by several lengths. If Quilter withdrew terms of business from all the scammers, the race wouldn’t even take place at all. In fact, all Quilter would have to do would be to ensure that all advisers are qualified and licensed – and that investors’ risk profiles are correctly respected – and the fraud would stop instantly.

But until Quilter and all the other death offices are put on trial for fraud themselves, this crime is going to continue. And victims are going to keep losing their pensions and life savings – and dying in abject poverty.

As an interesting post script, Quilter have posted a warning about scams on the internet. Their disingenuous claim that “Your security is our priority, so we have reacted quickly to help you and the financial advisers we work with to spot fraudsters” is ironic and cynical. Quilter themselves routinely work with fraudsters who pose as financial advisers – and who have no license or qualifications to provide financial advice.

January 28/29 2021 saw the cross examination of Stephen Ward in Pension Life’s criminal case in the Denia court. Ward gave the judge an elaborate explanation as to how and why none of the Continental Wealth Management pension and investment scams were his fault.

Ward provided the pension transfer “advice” to hundreds of Continental Wealth Management victims – facilitating the handing over of millions of pounds’ worth of personal and occupational pensions into the hands of well-known, firmly-established scammers. Once out of the relative safety of the UK, and into the offshore abyss, the scammers made millions out of undisclosed commissions on the victims’ life savings. The investments were, of course, largely worthless. Victims lost somewhere between a small percentage and a large percentage – with a few losing 100%. And a few more even going overdrawn on their pension accounts.

Ward’s Spanish firm Premier Pension Solutions, worked as “sister company” to Darren Kirby’s and Jody Smart’s Continental Wealth Management. After Ark in 2011, Ward moved straight onto the Evergreen New Zealand QROPS liberation scam. And CWM did the cold calling to sign up 300 victims to the toxic £10 million pension scam and so-called “loans” from Ward’s own finance company – Marazion.

Ark (and indeed Evergreen) victims may well want an answer to the question: why hasn’t Ward been prosecuted before now? The lack of any previous criminal proceedings against him, for the many other scams he was involved in, is – indeed – astonishing.

Capita Oak, Westminster, Southlands, Headforte, London Quantum et al – could all have been prevented had Ward been behind bars. Victims of all of those scams might still have their pensions had it not been for Ward.

Part of the answer may lie with Dalriada Trustees. The firm was appointed by the Pensions Regulator to the Ark schemes as independent trustee on 31st May 2011. Over £27 million worth of pensions had been transferred from safe, professionally-run pension schemes into the six Ark schemes. Nearly 500 people are affected – many of whom had received reciprocal “loans” on the advice of Stephen Ward and his very convincing associates. Ward had assured all the victims that the loans would be “tax free”. But, of course, HMRC does not share that view – and the tax trial is starting in March 2021.

HMRC is looking to tax all those who did get “loans” and also all those who didn’t. HMRC’s argument is firstly that even if members didn’t get a loan, they had made the transfer with the intention of getting a loan, and secondly that they “made” a loan.

One of the first questions I ever asked Dalriada back in 2013 (appointed by the Pensions Regulator – who registered the Ark schemes in the first place) was:

“Why didn’t you bring criminal proceedings against Stephen Ward and all the other scammers who set up and ran Ark?”

Dalriada’s answer was:

“We didn’t think it was within our remit”.

So what is (or was) Dalriada’s remit? And has it fulfilled that remit? And how much has it cost?

DALRIADA’S REMIT:

To suspend the Ark schemes so that no further “loans” could be made; no further victims lost their pensions; no further toxic investments could be made

To investigate the schemes to find out how they had been run and where the money had gone

To recover the toxic investments and return the money to the schemes

To liaise with the members and keep them informed

To liaise with HMRC on the unauthorised payment tax liabilities

The above points are all guesses on my part. Certainly, Dalriada has admitted that they didn’t really know where to start at the beginning. They had no idea what they would find, once they started investigating, and no clue as to how much work was going to be involved.

Dalriada has, indeed, recovered some of the toxic investments in the Ark schemes. But communications with the members have been limp at best. Dalriada has spent a lot of time, effort and money on taking proceedings against the victims themselves to recover the “loans”, but seems to have spent zero time, effort or money on pursuing the scammers.

Most important of all, Dalriada has not invested any of the money left in the Ark schemes – so members (victims) have missed out on the longest investment bull run in history. Bottom line: there’s been no growth in the value of the Ark funds – only shrinkage. Had the funds been invested in something as simple as a low-cost tracker fund, they could have grown by some 330% at least.

Of the original £27 million in the Ark schemes, Dalriada has spent more than £7.4 million on trustees’ and lawyers’ fees between 31st May 2011 and 31st May 2020. But isn’t it reasonable to ask: “Why couldn’t Dalriada have spent some of that money on criminal proceedings against Stephen Ward and some (or all) of the other scammers?”

Dalriada Trustees have been appointed to more than 100 pension scams in the past ten years (by the Pensions Regulator). But there is no evidence that any of the scammers – especially the prolific Stephen Ward – have ever had any CRIMINAL action taken against them by Dalriada in an effort to prevent further scams.

Kelly reports that “Pension scam victims have lost millions of pounds more to the government-appointed trustees hired to get their money back.” and that “Victims say Dalriada Trustees ‘inexplicably’ held their recovered retirement savings for years and then only paid a fraction of their money back.”

Kelly has been to meet me in Spain several times. He attended the Denia court for the first set of cross examinations in 2020, and reports that “tens of thousands of savers had lost up to £10 billion in rogue schemes that looked safe because they were registered by HMRC and overseen by the Pensions Regulator”.

Kelly goes on to cite the case of one victim who waited seven years to have his £157,000 pension pot returned to him by Dalriada. But they deducted £90,000 in charges before handing it back to him. And this was after Dalriada had rescued the fund in full, before the scammers had managed to invest the money in toxic, commission-paying assets.

With 5,400 pension scam victims having Dalriada as their trustees, it is perhaps time to ask whether this is a tenable solution. Scammers could, realistically, be forgiven for thinking that once Dalriada takes charge, this is merely a license for the next scam, and the next one, and the next one…… Because, Dalriada is never going to report the scammers for fraud. So they are free to keep on scamming people out of their pensions repeatedly.

The recent awards given to Quilter Cheviot and Quilter International by International Adviser (sponsored by Quilter) must have sickened and disgusted many Quilter (OMI/Skandia) victims. Editor Kirsten Hastings’ saccharine and gushing words of praise will have been seen as offensive in the extreme by the thousands of victims who have lost their pensions and life savings in Quilter International death bonds.

While there were, indeed, some very decent firms given well-deserved awards for excellent service and innovation, the prizes handed out to the sponsors of the event were just plain wrong. International Adviser Editor Kirsten Hastings should hang her head in profound shame. She knows full well how many people have been ruined by Quilter. She knows Quilter’s victims are dying – and some have died. She is fully aware that many more are contemplating suicide and that most are facing a bleak Christmas and poverty for the rest of their lives. And yet she can still publicly praise a company which she is fully aware has facilitated investment fraud on a massive scale; congratulate them warmly, and smile broadly while cocking a coquettish nod at the distraught victims as she played canned applause.

I’m going to add an award which was conspicuous by its absence; an award for a brave and determined woman who stood up in the flaccid jurisdiction of Guernsey to a negligent pension trustee: FNB International. Home to many scams and scammers, Guernsey had for many years hosted pension scams – until eventually de-listed by HMRC. A well-known tax haven, Guernsey does have an ombudsman for financial services (albeit a weak and ineffective one) – but he refuses to hear any complaints about matters relating to the height of Guernsey’s disgraceful past.

The heroine so who richly deserves a medal is Manita Khuller – victim of Quilter International, FNB International Trustees and Professional Portfolio International. Between them, these three negligent and culpable parties conspired to cause the destruction of her two final salary pensions worth £330,000 ($430,921/€386,574). The Guernsey Court denied Ms Khuller’s original claim for restitution – and, at first, all seemed lost and it looked like the scammers were going to get away with it. But, unprepared to go down without a fight, Khuller sought an appeal based on the gross negligence of the unregulated adviser – Professional Portfolio International, which FNB had used while she was living in Thailand.

Roger Berry of Concept Trustees in Guernsey, commented on this: “The trustee sought to show that they could rely on the delegation to the adviser/manager to remove or qualify its duties as trustee and in any event, to be liable, the trustees had to be shown to have acted with gross negligence.”

Mr. Berry spoke from significant first-hand experience – as he himself had been accepting investment instructions from AES International’s Stephen Ward (of Premier Pension Solutions in Spain) in the high-risk and toxic EEA Life Settlements fund as far back as 2010. So, he knows all about the catastrophic consequences of accepting business from known serial scammers into obviously unsuitable investments. Berry is also familiar with the art of gross and grotesque negligence.

How she lost two guaranteed DB pensions with strong employer covenants

Why PPI continues to operate throughout Asia under MD Eric Jordan

Why Old Mutual and Skandia (now Quilter International) have yet again been found wrapping dodgy investments

How a South African and now UK bank is owning a Guernsey Trust in the first place

What Geoff Gavey, Alan Glen and co were doing at FNB international to claim “trusteeship”.

Perhaps, in years to come, people in the financial industry will discuss in hushed tones the epic and cautionary tale of Manita vs. Quilter.

But What has Quilter got to do with a Guernsey-based pension trustee who accepted unregulated investment advice into toxic, high-risk, unregulated funds – LM and Mansion Student Accommodation?”

The answer is, of course, EVERYTHING. A Quilter insurance bond should never have been used in a QROPS at all in the first place – and was only there in order to provide scammers posing as independent financial advisers with hefty, undisclosed commissions.

This case was about FNB International, the guilty QROPS trustee who facilitated this scam. But, of course, this firm did not act alone. As in all the thousands of similar cases, the main protagonists started with the rogue advisory firm and ended with the rogue life (or, rather, death) office – in this case Quilter International. But similar cases involving this type of pension investment fraud involve SEB, Generali, FPI and RL360.

Manita Khuller was advised to transfer her defined-benefit pensions by Professional Portfolio International, an unlicensed advisory firm based in Bangkok – where she was living at the time – into the Plaiderie QROPS. Of course, the reality was that her pensions should never have been transferred at all and would have been much better left where they were – safe in the hands of professionals and far away from the grubby paws of unlicensed scammers posing as financial advisers.

Then, going down the well-trodden path of traditional pension and investment scams, PPI put their victim’s fund into a death bond for their undisclosed 7% or 8% commission, and then invested it entirely in high-risk, toxic, unregulated funds for further huge, undisclosed commissions. None of these three phases of the scam should ever happened: not the transfer out of her final salary pension scheme; not the purchase of the unnecessary, inflexible and expensive death bond; not the risky, inappropriate investments. But Quilter International facilitated it all – rewarding the scammers at PPI handsomely (as they do with so many unregulated scammers across the globe).

Professional Portfolio International – run by Eric Jordan and Colin Bloodworth – claim, on their website, to: “strive to help each client grow, protect and enjoy their wealth”. But this, of course, is completely untrue. If they had their clients’ interests at heart, they wouldn’t have put Manita Khuller into a Quilter International bond in the first place; and they wouldn’t have invested her precious pension in high risk toxic crap in the second place. Their only motivation was, of course, their own fat commissions.

Jordan and Bloodworth claim to have a “very knowledgeable and suitably qualified team of experienced advisers”. But this is clearly untrue – as any qualified adviser would know that an insurance bond serves no purpose inside a pension wrapper and wouldn’t be seen dead advising a valued client to invest in worthless rubbish such as LM and Mansion.

Jordan and Bloodworth’s website goes on to boast that “PPI is able to deliver the highest level of progressive financial planning and wealth management services”. And yet, it is clear this is not only a black lie, but that “planning and service” are the furthest things from their minds. The only things they care about, obviously, are fat commissions and conning victims like Manita Khuller out of their pensions and life savings.

So, Manita Khuller was failed and scammed by three parties:

Rogue advisory firm Professional Portfolio International in Bangkok – run by Eric Jordan in Thailand and Colin Bloodworth in Indonesia

Rogue QROPS trustee FNB International in Guernsey

Rogue death office Quilter International (previously Old Mutual International/Royal Skandia)

Manita Khuller – like thousands of other victims of Quilter International, QROPS trustees and unlicensed advisers – was a low-risk, retail investor – as is anyone investing a pension fund. But more than half of her pension – around £170,000 – was put into LM Managed Performance Fund, run by Australian-based LM Investment Management. This company is now in administration. Another big chunk was put into the Mansion Student Accommodation Fund which is now in liquidation.

Almost a third of her money had been invested in the Mansion Student Accommodation fund, and due to the fund’s liquidation her money had been frozen without her being able to access it at all. Speaking to This is Money, Manita commented:

And that, in a nutshell, is the crux of the situation. Quilter are far too willing to give terms of business to unlicensed scammers – with no relevant qualifications or regulations in place to ensure their professional obligations are not compromised by greed, lies and disloyalty. Quilter have been doing this for years now – and have made a fortune out of the sales of their expensive, unnecessary death bonds. They have perpetuated the myth for years that firms with only an insurance license (or even no license at all) can “advise” on investments as long as they flog their victims a death bond and then “pick” from the toxic investments on the death bond provider’s platform – obviously always choosing the investments that pay them the highest commissions (like LM and Mansion).

So here is the award that Kirsten Hastings of International Adviser should have given:

INTERNATIONAL CHALLENGER OF PENSION SCAMS

(especially those facilitated by Quilter International)

Covid 19 is having a terrible effect on millions of people across the globe. All walks of life are being affected. One important aspect of life in general is that of investments – life savings and pensions in particular.

Fraudsters are now using the Covid 19 pandemic as a weapon to encourage investors to fall for investment scams. The tactics used are similar to those deployed as scare tactics over Brexit:

“get your pensions out of the UK so you have more investment choice and control”

(What the scammers meant by this, of course, was that they would have choice and control – and fat commissions. The victims would just have less money).

There are many lessons to be learned from the pandemic – including the way different countries have dealt with lockdown procedures. But the lesson I want to examine, in parallel, is how governments deal with pension and investment fraud.

We’ve now seen that laws can be changed swiftly when there is an international crisis threatening millions of lives. Yet, for more than a decade, pension and investment scams have threatened even more lives, while laws and regulations have barely budged. Police can jump into action when a couple of people take a stroll in the park without observing social distancing laws, yet armies of scammers steal of millions of pounds from thousands of victims, and nobody in a police uniform lifts a finger.

The Covid 19 crisis will inevitably contribute to the effects of inappropriate investments – which teeter on the narrow verge between mis-selling and fraud. Where commission is king and investments have been chosen purely for the hidden (from the consumer) introduction revenue, the effects of this will now be felt acutely by many victims.

It has long been deeply frustrating that so many scammers can offend repeatedly – often for years on end – without any sanction. Victims of pension scams such as Ark, Capita Oak, Henley, Westminster, Evergreen, London Quantum, Fast Pensions and Continental Wealth Management have lost their pensions to the same scammers over a seven-year period.

Regulators, police and government ministers have taken not a bit of notice other than sometimes handing the pension schemes over to Dalriada Trustees – who also fail to report the blindingly-obvious frauds to the police authorities.

Mind you, I have some (limited) sympathy with Dalriada. They obviously know it is a complete waste of their precious (and very expensive) time reporting the scammers. Dalriada clearly knows full well that the Police, Insolvency Service and Serious Fraud Office are worse than useless.

Behind this failed law-enforcement network lies an even bigger scam: Action Fraud. This is a cynical effort to fool scam victims into believing that some action will be taken when fraud takes place. However, the reality is that Action Fraud is just a call centre which deliberately ignores the desperate pleas for help by fraud victims. In fact, the Action Fraud call centres are no different in nature than the boiler-room cold calling centres used by the scammers – the purpose is the same: to deceive victims.

We have now seen the hard evidence that whole continents can jump into radical action when necessary. So there is no longer any excuse for allowing the pension and investment scam pandemic to continue unchallenged.

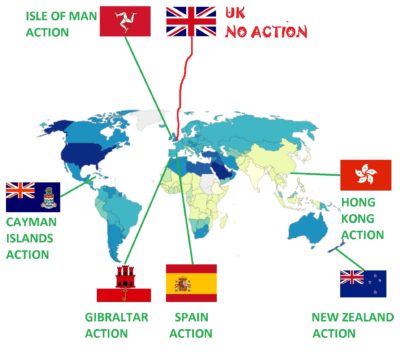

Every country – especially ones where lots of British expats live – needs to recognise that pension and investment scams are – and always have been – a global pandemic. The apathy and laziness of regulators, law enforcement agencies and governments need to cease. And Britain’s shameful, embarrassing track record of ignoring – and even facilitating – scams needs to be reformed.

The early signs of a wind of change in the pension and investment scamming world are there. Spain and New Zealand are now actively progressing criminal proceedings against scammers. There are early signs that other jurisdictions are starting to wake up as well.

The scammers at Premier Pension Solutions and Continental Wealth Management are facing fraud and falsification charges in Spain.

The SFO in New Zealand is investigating the scammers in the $100m Penrich Macro Global investment fraud which was also linked to the Evergreen QROPS scam (run by Stephen Ward and promoted by Continental Wealth Management).

STM Fidecs in Gibraltar has issued a claim against thirteen defendants for the return of “misappropriated” money in the Trafalgar Multi Asset Fund case (also under investigation by the British SFO).

Police in the Cayman Islands are investigating a fraudulent investment company – and has warned potential investors into any companies in Cayman to carry out proper research and due diligence

The Isle of Man courts are preparing for a raft of civil proceedings against leading life offices which have facilitated financial crime on a massive scale internationally.

The Hong Kong fraud squad is taking a keen interest in the GFS Blackmore Global pension/investment scam.

Back home in the UK, there are serious complaints being filed against HMRC and the Pensions Regulator for facilitating pension scams and failing to warn the public. And a growing body of victims and professionals is looking at bringing the FCA to justice for their multiple failures.

Even if the tide is beginning to turn, it is – of course – way too late for thousands of victims whose lives have already been ruined by the scammers. Just as Covid 19 has killed hundreds of thousands of victims in just a few months, pension and investment scams have ruined hundreds of thousands of hard-working victims’ lives in the past decade.

While more than 200 countries are fighting against the spread of Coronavirus and trying to save the 300,000+ people who are sick, we now need key financial services jurisdictions to take the pension and investment scam pandemic seriously.

Renowned English Author James Hadley Chase once famously wrote:

“It’s better to be sick of life than not have a life”.

Pension and scam victims are not just sick of life, but they are also sick of the lack of action by authorities internationally – but above all in Britain. Let’s hope that current actions in place in Spain, Gibraltar, Cayman Islands, Isle of Man, Hong Kong and New Zealand will be replicated as swiftly and effectively as the Covid 19 protection measures.

On July 18th 2017, Slater and Gordon Lawyers wrote me the below email. Lawyer Steve Kuncewicz clearly stated that Slater and Gordon acted for their client: Blackmore Global PCC Limited; Phillip Nunn and Patrick McCreesh. The full transcript is below – complete with my comments in bold. This is a 25-page document, so I don’t expect most people (except the most tenacious and determined) to read all of it. So I have put the basic highlights below.

It is clear that Slater and Gordon was a poacher back in July 2017 when the firm represented clients Blackmore, Nunn and McCreesh. And now in 2020, Slater and Gordon, is an even bigger poacher as it attempts to profit from the losses suffered by Blackmore Bond victims.

As Bond Review reported yesterday that the FCA knew all about the doomed Blackmore Bond three years ago, it is clear that Blackmore’s own lawyers – Slater and Gordon – also knew what Nunn and McCreesh were up to at the same time, but did not report their clients to the authorities as they should have done (not that it would have done any good). But both the FCA and Slater and Gordon could have prevented the Blackmore Bond tragedy and saved hundreds of victims from losing their life savings.

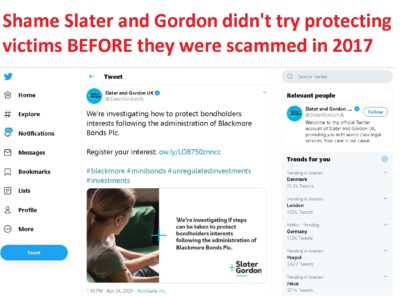

Meanwhile, Slater and Gordon is now advertising all over social media:

We’re investigating how to protect bondholders interests following the administration of Blackmore Bonds Plc.

Slater and Gordon is also denying that Blackmore, Nunn and McCreesh were ever their clients. Slater and Gordon is now trying to attract clients by promising:

“We’re keen to assist investors and help them understand their position. We’re investigating if any steps can be taken to protect their interest in the funds within Blackmore’s mini-bond schemes, following the administration of Blackmore Bonds Plc. These schemes promised a high rate of return to investors but continually failed to pay-out. If you invested in mini-bonds or an ISA through Blackmore, we’re keen to speak with you. “

Although the communication with Slater and Gordon is more about the Blackmore Global Fund scam than the mini-bond, it does cover a number of crucial issues including:

Slater and Gordon confirmed that they acted for their clients: Blackmore, Nunn and McCreesh in both a ” business and personal capacity “

Slater and Gordon was trying to shut me up so that their clients could keep scamming hundreds of victims out of their pensions and life savings

Slater and Gordon was falsely portraying their client as: “a prestigious, multi-asset investment house with over £60 million in assets under management, offering institutional and high net-worth clients access to a wide variety of investment products in order to maximise their returns”. This was completely false as Blackmore only targeted retail investors with small pension pots or personal savings – with their entirely unsuitable, illiquid, high-risk investments

Slater and Gordon claimed: “The Blackmore Group was founded on the core belief of putting the needs of its clients first, developing diverse portfolios backed by real assets containing a blend of capital growth and fixed income”. This is nonsense: Blackmore worked closely with known, serial scammers to promote their products and target naive, vulnerable victims. They locked pension savers into their fund scam for ten years without their knowledge and they spent the bondholders’ money on huge amounts of promotion fees (e.g. Surge Group) and commissions for the scammers who helped distribute their toxic wares.

But most serious of all is this next point:

5. Your only intention can be to divert business from them and to cause serious financial harm as a result.

I replied: “I have no interest in causing your clients financial harm – why would I? But I do think that vulnerable pension savers have a right to know the background of the people behind a fund which is being promoted to retail, UK-resident investors.”

A lot of the Blackmore Bond victims invested AFTER this letter. Slater and Gordon did NOTHING to warn the public about their client. All they did was to try to shut me up and prevent me from warning the public.

And now they want to make money out of the Blackmore Bond victims? Seriously?

Slater

Gordon

Lawyers

18 July 2017

URGENT

— IF YOU DO NOT RESPOND TO THIS CORRESPONDENCE, COURT

PROCEEDINGS MAY BE ISSUED AGAINST YOU WITHOUT FURTHER NOTICE

Ms Brooks t/a

Pension-Life.com

24 Calle Cuatro

Esquinas

Lanjaron

18420,

Granada

SPAIN

58 Mosley Street

Manchester

M2 3HZ

DX 14340

Manchester 1

Tel: 0161 383

3500 Fax: 0161 383 3636

wwwslatergordon.co.uk

Your Contact:

Steve Kuncewicz Assistant: Rebecca Young

Direct Tel:

01613833708

Email:

Steve.Kuncewicz@slatergordon.co.uk

Your Ref:

Our

Ref: RZY03/UM1389098

Our Clients: Blackmore Global PCC Limited, Philip Nunn and Patrick McCreesh Proposed Claim for Defamation and Malicious Falsehood

We act for the aforementioned clients in their business and personal capacity and have been instructed to contact you in relation to various untrue, defamatory and wholly unjustifiable allegations published on your website at httq://pension-life.com (the Website) relating to our clients, their products and services which are designed to (and in fact already have, as set out below) damage their respective reputations and financial interests.

Our client, Blackmore Global PCC Limited, is part of the Blackmore Group which is a prestigious, multi-asset investment house with over £60 million in assets under management, offering institutional and high net-worth clients access to a wide variety of investment products in order to maximise their returns.

If it is indeed true that Blackmore Group is a prestigious organisation, then I have no doubt the directors will be keen to ensure that the damage done to victims’ pensions is put right and that Blackmore’s purported “good name” is protected. However, when you Google Blackmore Group PCC nothing comes up about it being “prestigious” – but what does come up is a link to one of Offshore Alert’s warnings regarding Brian Weal – – and as you know at least one of the underlying assets was run by Weal.

Further, there are cautionary warnings on the Money Saving Expert forum which mentions that investors were given a “pension review” by Aspinal Chase (run by your clients) and promised 10% returns p.a.There is absolutely nothing available on Google which describes Blackmore Global as “prestigious”.

Further, the clients are not high

net-worth, under the FCA definition. Are you aware of the FCA

definition of “High net-worth”? Your clients, with 25 years’

experience, will know this. Just to remind you, a high net-worth

client, according to the FCA has-

an

annual income to

the value of £100,000

or more.

Annual income for these purposes does not include money withdrawn

from pension savings (except where the withdrawals are used directly

for income in retirement).

net assets to

the value of £250,000

or more.

The definition specifically excludes

pension savings. Yet, your clients are involved in the marketing,

processing and investing of retail pensions of those that are not

high net-worth clients. I would be interested to see if ANY

sophisticated or institutional investors are in the Blackmore Global

Funds. Surely, such experienced investors would demand audited

accounts.

“The Blackmore Group was founded on the core belief of putting the needs of its clients first, developing diverse portfolios backed by real assets containing a blend of capital growth and fixed income.” (Steve Kuncewicz of Slater and Gordon – 18.7.2017)

If the assets

are “real” – tell us what they are. Do you even know what they

are? Have you seen an independent audit or are you relying solely on

what your client is telling you?

Blackmore Global

PCC Limited offers a medium to long-term investment vehicle for its

clients with a diversified investment portfolio under one structure

which allocates investment between four distinct protected cells

which diversify assets between property, sustainable energy, private

equity and lifestyle. In order to take advantage of as wide a range

of investments as possible, it invests in a number of vehicles

including funds, companies, joint venture projects and equities.

I know all about

the cells as they are described in the factsheet and brochure.

However, based on the fact that we know some of the information

contained therein is untrue, I am not sure the cell information can

necessarily be relied on. What we really need to know is exactly

what the assets are. Steve, I mean no disrespect but your letter

contains 21,290 words – and not one word about what the assets

really are. You seem to be trying to claim your clients have done

nothing wrong – but you are providing no evidence.

Further, among

those many words, you refer to loss suffered by your clients multiple

times, but you never once refer to the considerable loss and distress

suffered by the Blackmore Global investors (or indeed the Capita Oak

and Henley ones).

Patrick McCreesh

and Philip Nunn founded the Blackmore Group (of which Blackmore

Global PCC forms part) in 2013,

That would be

just after the Capita Oak and Henley scams, which Nunn and McCreesh

were promoting, collapsed.

and jointly have

more than 25 years’ experience in the financial services sector,

growing their business to the extent of it having over £17m of

assets under management across multiple asset classes.

With

respect, if they have jointly more than 25 years’ experience in the

financial services sector, they should know that their fund is not

suitable for pension schemes – just as they should have known that

empty boxes (store pods) were not suitable investments for the Capita

Oak and Henley victims. And

I sincerely hope that (apart from the victims of which I am aware)

none of the remaining £17m represents pension investments.

By contrast, the

Website describes your activities as follows:

“Depending

on the type of pension or investment scam a victim has been involved

in, there are various things we can do to help. We charge annual

membership fees so that members know exactly what they will have to

pay and there will be no legal or accountancy fees on top.

Deal with

trustees, advisers and fund managers

Complain to

regulators and ombudsmen

Appeal tax

liabilities with HMRC and the Tax Tribunals

Analyse and

quantify investments, losses and fees/commissions

Instruct

solicitors to

make

a claim against negligent parties to obtain redress for losses and

liabilities (paid for by litigation funding)”

Am not sure what

the point is that you are trying to make here. You have used the

phrase “by contrast” which to me suggests you are trying to

ascertain that, unlike your clients, I have never been involved in

running or promoting a pension or investment scam. Which, of course,

I haven’t. Indeed, I vigorously oppose such crimes and am working

with the regulators, police and ombudsmen to help stamp out such

activities and bring those responsible to justice.

Notably, you refer

to yourself as “one

of the leading experts on pension liberation scams”.

Indeed, I am

widely acknowledged as such. Further, in your above statements, you

have now correctly identified the following problems associated with

Blackmore Global:

Problem no. 1: the victims were

neither “institutional” nor “high net-worth”. They should

never have had their pensions invested in the Blackmore Global fund

at all.

Problem no.2: you have said Blackmore

develops “diverse portfolios backed by real assets”. So what

are these “real” assets? Do you even know? Has Blackmore ever

told you or shown you proof? Because they won’t tell the victims

what the assets are. Nor will they tell the pension trustees.

Problem no. 3: Blackmore Global

offers a “medium to long-term investment vehicle”. So, not

suitable for pensions then. Members of a pension scheme have a

statutory right to a transfer as well as to be able to reach the age

of 55, or retire or die, so there must be liquidity. Also, at least

one victim was close to retirement age when he entered the scheme so

he should never have been put into long-term investments.

Problem no. 4: Blackmore Global has

£17m worth of assets – if these are all members of pension

schemes such as the victims who are members of the Pension Life

Group Action, then there is a very serious problem indeed for your

clients.

You

refer to my activities and expertise on pension liberation scams –

if you need any clarification or corroboration of this I am sure your

colleague Craig will be happy to fill you in.

The Website

contains a number of posts which refer, either directly or

indirectly, to our clients, specifically:

“Action Fraud

are nobody and have no authority”: John Ferguson, Square Mile

Financial Services: November 30, 2016;

Government

Consultation on Pension and Investment Scams (The Square Mile):

December 5, 2016;

“Scammers Are

Criminals” : April 11, 2017;

“Gambling

With Your Pension”: May 14, 2017;

“Serious

Fraud Office Requests Pension And Investment Scam Reports” :

May 24, 2017; and

“Blackmore

Global Fund — Asset Or Black Hole?”: July 7, 2017

Copies of these

posts are attached to this letter marked Annex 1.

The content of

these various posts (and the content of various other social media

posts and other direct communications with third-party professional

intermediaries who refer work and clients to our clients, which will

be adduced in evidence in due course), led our clients to write to

you on January 17 this year to put you on notice of their objection

to your various claims.

Forgive me, but

I am not sure what point

you are making. Ferguson did indeed write to a victim and state that

“Action Fraud are nobody and have no authority”. He even copied

in his lawyer to this. There was indeed a government consultation on

pension and investment scams. Scammers are indeed criminals (as

confirmed by

the Pensions Regulator). Gambling with your pension is not

advisable. The Serious Fraud Office has indeed requested reports on

a number of pension scams – some of which your clients were

involved with. Finally, we don’t know whether Blackmore Global is

an asset or a black hole because there is no independent audit.

Until and unless the long-awaited audit is forthcoming, the jury will

have to remain out on that.

As our clients

summarised, borne out by the contents of the Website, you purport to

act in a professional capacity for individuals who are beneficiaries

of trusts or pension schemes, who have been advised by independent

financial advisers (including, without limitation, Square Mile, who

are also referred to at various points in the posts referred to

above) to transfer some or all of their existing pension funds to the

Optimus Pension Scheme using an Investor Trust Wrapper.

As I am sure you

will realise, Slater and Gordon already did comprehensive due

diligence on me and the Group Actions several years ago, so there is

no need to “purport” – just ask Craig McAdam.

As our clients

stated, they understand that some of these individuals may have

invested certain of their pension fund assets into underlying

investments which may

include investments managed by our client. As you will be well aware

our client as an investment house has never, nor would they, ever

deal directly with any of your “clients”

as

beneficiaries.

I have never

said Blackmore Global (of which Messrs Nunn and McCreesh are

directors) did deal direct with the investors. However, they do run

a cold calling/lead generation business called Aspinal Chase which

dealt direct with the clients. See below the details of the Aspinal

Chase website:

I am not sure you understand how this

unpleasant, calculated and deliberate targeting of unsophisticated

retail pensions operated. Let me spell it out for you.

Your clients (again I refer to the

individuals – as I they cannot hide behind the corporate entity)

had websites offering pension reviews and cold-called members of the

public. Those that agreed to a review were introduced to what they

believed was an IFA (and IFA has a duty to look at the whole market

and act in the clients’ best interests). The “IFA” then

assessed the client’s needs and objectives and recommended

Blackmore Global. Then, your clients dealt with the processing of the

transfer from the ceding trustees into a pension and their own funds.

At no time was the client ever informed of the conflict of interest.

There was never an intention to provide the client with a pension

review, it was just a calculated ruse by your clients to get their

hands on the pension funds of gullible members of the public.

So effectively,

your clients were generating leads and introducing people to their

own fund via Aspinal Chase.

It is further evidenced that Messrs

Nunn and McCreesh’s firm Pension & Life were acting as pension

transfer administrators for the victims who were subsequently

invested in the Blackmore Global fund:

“Subject – Transfer from: Unisys

Pension Scheme Member name: Mr A B C Driver: Our reference: Transfer

Out – 9999999 Your reference: B00047 We have been advised by Pension

& Life UK Ltd to proceed with the transfer of this member’s

benefits from Unisys Pension Scheme to Optimus Retirement Benefit

Scheme No 1. We can confirm that the member has received appropriate

independent advice in respect of the transfer to the receiving

arrangement. The total transfer value amounts to £4xx,xxx.xx and has

been paid direct to your bank account.”

Please note, that your clients – in

their role as transfer administrators Pension & Life –

confirmed to the ceding provider that Mr. Driver had “received

appropriate independent advice”. However, with their 25 years’

experience Messrs Nunn and McCreesh should have known full well that

the advice had come from a firm which was not regulated for pension

and investment advice.

We now direct our

and your attention (to the extent that you were not fully aware of

their content, which we doubt), to the specific posts on your

Website, and how the same are both untrue and seriously defamatory of

our clients.

I am not sure

what you mean by this statement – how could I not be aware of the

content of the blogs on my website? I wrote them all personally.

Not a single one is untrue.

Below, in

accordance with the Pre-Action Protocol, we set out what we consider

to be the defamatory comments (Defamatory Comments)

“Action Fraud

are nobody and have no authority”: John Ferguson, Square Mile

Financial Services

And what is your

point? John Ferguson wrote this statement. I didn’t write it –

I only quoted it. There is nothing defamatory about repeating this –

it is a clearly evidenced fact.

The above post

contains the following statements:

“Mr.

Ferguson has invested a number of victims’ pensions in the Blackmore

Global and Symphony funds and was asked to provide a copy of the

audit for Blackmore Global which his firm has been promoting and

which appears to have some questionable assets — described as

“esoteric” and “alternative”. He was also asked

to provide evidence of his firm’s regulation to provide pension and

investment advice.”

Again, I am not

sure what your problem is with this – it is perfectly true and

clearly evidenced that Ferguson (and other unregulated advisers) have

indeed invested victims’ pensions in Blackmore Global. The assets

of the fund are indeed questionable – and will remain so until the

audit is produced. The fund is invested in esoteric and alternative

assets. Ferguson has been asked to provide evidence of his firm’s

regulation to provide pension and investment advice on several

occasions but he has never done so.

“One victim

had threatened to report the matter to Action Fraud when he

discovered multiple irregularities with his pension scheme”

Again, this is

perfectly true – and evidenced.

“The

factsheet for the Blackmore Global fund had falsely claimed a firm in

Barcelona was the Investment Manager for the fund — robustly denied

by the furious firm in question.”

And? Both the

factsheet and the brochure stated this – falsely.

Meaning

On any

consideration of the above two paragraphs, this post is intended to

cause damage to Blackmore Global PCC Ltd’s reputation and its

business by suggesting that our client’s underlying assets into which

funds are invested are “questionable”.

The questions

are “where is the audit” and “what are the assets”? There

was no intention to cause damage to anyone’s reputation and

business – but every intention to discover what the assets are.

There is compelling evidence that the assets are linked to very

suspicious investments and people with a track record of dealing in

investment scams. In fact, if you were genuinely interested in

protecting your clients’ reputation and good name, you would simply

send me a statement confirming what the assets are. The very fact

that you haven’t suggests you don’t know and your clients haven’t

told you. So how can you refute that the assets are questionable?

The natural and

ordinary meaning attached to the suggestion that an investment is

“questionable”

is

that it is disreputable, uncertain as to its credibility or validity,

and generally morally suspect. You seek to further compound the

damage to our client’s reputation by describing the assets as

“alternative”

and

“esoteric”.

For a pension

saver, the investment is indeed questionable. And the evidence is

that the assets are alternative and esoteric – and there is nothing

to prove otherwise. If you can prove that the fund is not

disreputable, I will happily apologise. But even if it turns out

that the underlying assets are low-risk, prudent, diverse and

suitable for pensions, the fact that there is a ten-year lock-in

precludes the fund from being suitable for pensions.

Even more

seriously, however, this post makes the most serious of defamatory

allegations in that it alleges that our client is involved in

investments which should be (reported?)

to the police, via Action Fraud, and that our client is therefore

engaged in unlawful, criminal activity.

Your client was

indeed engaged in unlawful, criminal activity in the Capita Oak and

Henley schemes as well as various SIPPS invested in Store First. I

cannot comment further on this because the matter is now in the hands

of the Serious Fraud Office.

Please

be clear that my motive and intention was not to cause damage to

Blackmore Global’s reputation, but to get the victims disinvested

as quickly as possible and further to warn the public that they too

might be in danger of being similarly invested in this fund by

unregulated “Chiringuitos”. The distress caused to the victims

who are invested in Blackmore Global has already been appalling and

as a solicitor you too have a duty to help protect the public.

You

have claimed I intended to cause damage by stating that the fund’s

underlying assets are “questionable”. So what are they? Prove

they are not questionable – of course you can’t, because there is

no audit. The audit was promised last summer, then xmas, then

Easter. Either Grant Thornton can’t find the assets or somebody

doesn’t want the audit made public because of what it will reveal.

You go on to state

that our client has produced Factsheets containing “false

information”. This

is strongly rejected by our client. Our client’s investments, and

their underlying asset classes, are wholly reputable and completely

transparent to investors.

I am sorry but

this is absolute nonsense. The factsheet did contain false

information. The investments and underlying assets are not at all

transparent – there has been no audit and your clients won’t tell

anybody what they are. And to be fair, you keep going on about the

assets, but you won’t say what they are – so you are being just

as opaque as your clients. We know what the asset classes are –

and the explanation of the sub classes are horrendous as they contain

all the usual asset types so beloved by investment scammers (gaming,

spread betting, wine, waste to energy etc.). One victim has written:

“All

I can offer, is to reiterate, that I have no recollection of any

correspondence with an IFA prior to signing up with Harbour Pensions

and Blackmore Global. It was always, Aspinal Chase and in particular

Marc Rees. He told me what a great move it all was, how it made sense

to have all my individual pension funds in one place, that having a

fund of over £250k, I’d get a personal manager that would work

specifically on my fund and keep me regularly updated. Needless to

say this never happened. In addition, Marc told me that investing in

Malta, with Harbour, would give me better returns and be tax

efficient. I took this all as “advice”. Only after a

few years, when I wasn’t getting updates and I had to ask for them,

and I asked him some questions about surrendering, did he say that

was bordering on advice which he wasn’t qualified to answer, and my

IFA, David Vilka, would contact me. He never did. I badgered Harbour

Pensions and got fobbed off. Then Vilka emailed me to say he

understood I was in discussion with Harbour Pension and he couldn’t

do anything more than what I was doing myself.”

Marc Rees- a name familiar to your

clients as he worked for them.

Go

to individuals and click on Previous Involvement…

It is correct to

describe the underlying asset classes as “alternative”

in

that they are not what would otherwise be classified as “mainstream”

investments

such as gilts or shares in publicly listed companies. Investments

into property or renewable energy sources are considered

“alternative”.

However,

the manner in which you seek to adopt this term is to the detriment

of our client by implying that the asset classes themselves are

irregular. An investment is “alternative”

where

it departs from the norm. Therefore, the threshold by which an

investment could be determined as “alternative”

is

low.

You are mixing

apples and oranges: asset classes

are one thing; actual assets are another thing. But again, I come

back to the simple resolution to this debate: provide me with a list

of the underlying assets and then we can put this issue to bed once

and for all. In fact, it is interesting to note that you have never

once stated what the assets are and I have to assume you simply don’t

know as your clients have not disclosed them to you.

I think we should get comment from

professional qualified advisers and actuaries to see if they think

the funds are irregular for retail pensions. I will happily be guided

by them on this matter. Remind me, what qualifications do your

clients hold that would prove they are competent to run such a fund?

We already know one of their colleagues, Brian Weal, was found to be

incompetent.

It is further

correct to describe the investments as being “esoteric,”

that

is, out of the ordinary and traditional model of investments. It is

common for investment portfolios to have an element of “esoteric”

asset

classes, as part of a wider diversification of assets and potentially

offering the higher returns that investors require to achieve their

objectives, based upon the input of independent financial advisers.

However, you seek to adopt this term, which you will be well placed

to understand as being regularly used within the media in a negative

sense, whilst referring to alleged “victims”

of

our client’s allegedly unlawful behaviour, as referred to above. It

is used frequently in a negative sense by the media and other

professionals within the context of financial services, hence why you

have chosen to do so.

I am afraid I

would have to correct you on the assertion that it is common for an

element of esoteric asset classes to be used as part of an investment

portfolio for

pensions.

Perhaps for sophisticated investors or HNW individuals who like a

bit of risk – but not pensions. The term “esoteric” is indeed

frequently used by the media in a negative sense – and there is a

good reason for that: many of the failed funds which have destroyed

victims’ life savings have been invested in esoteric assets.

You cannot possibly believe or claim

that alternative and esoteric assets are suitable for pensions. Why

not provide me with a definitive list of the assets and then we can

debate this properly. You must surely know that funds for pensions

must, by definition, be low-risk, liquid, prudent and diverse –

which Blackmore Global clearly is not.

To clarify the

position in regards to our client’s Factsheet, our client’s

investment manager in relation to the background to which this post

refers was one Gerald Rodriguez, who formerly operated the firm IIG

Financial Services before moving under the banner of Meriden Capital.

Mr. Rodriguez is no longer responsible for the management of this

fund.

I

did indeed state that your client has produced Factsheets containing

“false information”. This is true and clearly evidenced by both

the Blackmore Global factsheet and brochure. Both documents claim

that the Investment Manager for the fund is Meriden Capital Partners

in Barcelona. But the directors of Meriden state they have never

heard of Nunn, McCreesh, Ferguson or Vilka – or indeed Blackmore

Global. However, when I jogged their memory that they had actually

completed an application form to become the Investment Manager, their

English suddenly got worse. But they still insisted they had never

been the Investment Manager to the fund as they were not regulated to

carry out such a task.

Your

explanation about Gerald Rodriguez of IIG Financial Services being

the Investment Manager is, I am afraid, mistaken. I called Mr.

Rodriguez (19th

July) who now works for the Gibraltar International Bank. He

confirmed that he did once work for IIG but that it was many years

ago. He also confirmed that he had never been the investment manager

for Blackmore Global – indeed he had never even heard of it – and

that he had never worked for Meriden Capital Partners. Perhaps you

should ask your clients to conjure up another answer to that one.

2. Government

Consultation on Pension and Investment Scams (The Square Mile)

We direct your

attention to the entire blog posting at Annex 1, and below we set out

the extracts which are most concerning, and defamatory, to our

client.

“Blackmore

Global was full of toxic, illiquid, high-risk assets, had no audit

and as a UCIS (unregulated collective investment scheme) was illegal

to promote to a retail UK investor. The brochure made a fraudulent

claim as to who the investment manager was.”

“The

trouble is, while Mr Driver has fought hard to get some of his money

back, there are around 1,100 other victims stuck in this fund who may

yet have no idea their pensions are invested in —how shall I say

this- worthless crap”

Meaning

This post purports

to discuss alleged pension and/or investment “scams”.

By

including a

reference to our

client within this blog, the clear inference is that our client is

such a

“scammer”, that

is, behaving dishonestly and not in accordance with clear ethical and

regulatory guidelines, and in breach of its obligations (both express

and implied) to its stakeholders. Again, this is a most serious

allegation to make, and is repeated across the post, through repeated

and unjustified allegations that our client is involved in criminal

activity.

Our client,

Blackmore Global PCC Ltd, is an investment company based in the Isle

of Man. It was set up as an unregulated investment company under the

Companies Act 2006, to operate in that jurisdiction.

I am not at all sure what you mean by “unjustified allegations”. It is evidenced on the FCA website that it is illegal to promote UCIS funds to UK retail investors.

You

have kindly confirmed that your client is an unregulated investment

company – and there is no argument about the fact that it has been

promoted by, among others, associates of Nunn and McCreesh: Ferguson

and Vilka, (not regulated to provide investment or pension advice) to

retail, low-risk pension savers. And further, Nunn and McCreesh were

involved in the promotion of a number of pension scams which are now

under investigation by the Serious Fraud Office. What do you have a

problem with?

Your reference to

our client’s investment company being “toxic,

illiquid, (and containing) high risk assets” has

a natural and ordinary meaning that the product is harmful to an

individual’s pension, worthless and of little value as there is no

market within which it can be re-sold. You cannot have underestimated

the significance of calling the product in question “toxic”

to

our client and its reputation. You go on to describe it as being

“worthless

crap”, the

meaning of which we trust we need not set out in correspondence save

to confirm that the use of vulgar abuse does not offset or place into

favourable context your other allegations, as referred to above.

I see no merit

in further debating this point: you are aware of my position on the

assets of the fund but you repeatedly fail to provide any evidence to

prove me wrong. You cannot object to my references, descriptions and

allegations unless you disprove them. Tell me what the assets are,

provide independent

and credible valuations, and disprove what I have written. Your

repeated failure to disclose what the assets are merely serves to

reinforce the point that the fund is opaque and your clients are

failing to be transparent with the victims or the trustees – or,

indeed, you.

We understand that the value of Blackmore

Global PCC Ltd has increased some 11% since its inception.

Exactly how do you “understand”

this? Have you seen an audit? Have you seen the accounts? Have you

got evidence of 11% growth since inception? If you are right, then

11% since 1.5.14 isn’t actually that much at all – a simple

tracker fund would have done just as well, been cheaper, much lower

risk and not had the ten-year lock in. And further, if the fund has

grown, why did Mr Driver get less back than the scammers invested in

the fund in the first place?

We again note that you fail to make any

mention of this fact, which ultimately would not further your evident

intention to damage our client’s reputation and blatant attempt to

self-promote your own “business”.

What fact? Provide the facts.

I genuinely do not understand why

you think my intention is to damage your client’s reputation. What

benefit would that produce for anyone? Nunn and McCreesh do indeed

have a chequered history because of their involvement with Capita

Oak, Henley and multiple SIPPS invested 100% in Store First, but I

wouldn’t have a motive to take the slightest interest in their

reputation. But I would most definitely want to prevent more victims

from having their pensions invested in Blackmore Global – and I am

sure the existing victims would attest to that intention because of

the profound distress they have gone through. But I am not sure how

or why you think commenting on the unsuitability of your clients’

fund does anything to “self-promote” my business.

It is correct that

the product referred to in this post as “illiquid”.

Our

client offers a ten-year close- ended product that is not designed to

be liquid. It is entirely normal for illiquid products to be offered

for investment, where the investment opportunity is designed to be

long-term. In itself, the term illiquid is correct, however the

manner and context in which it is adopted by you, alongside the terms

“toxic”

and

“scam”

is

clearly designed to be harmful to our client’s reputation.

I am beginning

to realise you know little or nothing about investments in general or

investments for pensions in particular. It is also clear you are

relying entirely on what you “understand” from your clients –

and it has been evidenced that some of this is not true. Investors

who specifically want an illiquid investment into which they are

locked for ten years, would have no problem with Blackmore Global.

Or at least, they would have no problem if they knew what the assets

were (which clearly you don’t). Provided the assets were not toxic

or associated with known investment scammers, then a sophisticated,

HNW investor could do his own due diligence and decide for himself.

But illiquid funds are not suitable for pensions.

I would contend

that no one would lock up their funds for 10 years. I have spoken to

a number of Chartered advisers who all have this opinion.

One raised an

extremely good point. Among the spurious reasons that were used to

entice people out of perfectly sound pensions was the promise of

access from the age of 55. Yet, all the people that I have spoken to,

invested in Blackmore, are over 45 years of age. The sales pitch of

55 is meaningless. Of even greater concern is that their whole

pension fund is locked up to 10 years in some cases and this is an

outrage!

What if an

investor were to die within 10 years, how would the family get the

much needed funds? If you have any conscience at all, think about

that.

It is incorrect to

describe the product as “solely

high risk”. As

with any balanced investment portfolio, there will and should be

asset classes within it which fall within the definition of “high

risk”. Overall,

however, the overall apportionment of such “high

risk” assets

is low and, the portfolio in question is balanced.

Without knowing

what the assets are, neither you nor anyone else could make that

statement with any confidence. How can you state that the overall

apportionment of high risk assets is low and the portfolio in

question is balanced if you don’t know what the assets are and have

never seen an audit?

If it is so good, I am sure you have

invested all your own pension savings into the Blackmore Fund. I look

forward to seeing your investment statement.

The sweeping statements you make

regarding suitability, or any purported lack thereof, of our

corporate client’s close ended investment are of serious concern,

especially when made without any objective attempt at justification.

There can be no justification for your assertion that the products in

issue are wholly unsuitable for any pension fund or that its nature

as a 10-year, closed-ended product renders it “worthless

crap”.

If

you are so sure that I am wrong about Blackmore Global, give me the

evidence – and also provide me with evidence that confirms you

yourself have seen and know what the assets are. You cannot argue

that the Blackmore Global fund is not harmful to individuals’

pensions, because one has suffered loss upon redemption already

(£1,663.17)

and others are being

denied their statutory right to transfer out of their schemes because

no reputable pension trustee would accept an in specie transfer in

something so illiquid and with no audit.

I

will be able to get a considerable number of high profile, well-known

and respected advisers to assert that the product is wholly

unsuitable for retail pensions. And, since they were sold in the UK,

why was the commission filched from the funds not disclosed?

You

state that you “understand that the value of Blackmore Global has

increased 11% since inception”. How did you come to that

conclusion? Did you see an audit – or are you taking your clients’

word for it? If your client’s word on the value of the fund is

anything like their word on who the Investment Manager was, I would

think you are making a somewhat shaky assumption.

Blackmore Global

PCC Ltd is not a UCIS.

Yes it is.

Again, the

suggestion that our client “promotes”

itself

to consumers/customers and that such activity is illegal is a most

serious of allegations to make.

Your client

promotes itself to consumers through Aspinal Chase.

The product in

issue is a closed-ended investment and not a UCIS.

It is a UCIS

Furthermore, our

client’s customers are not “retail’

clients.

Instead, they are investment managers, professional pension trustees

or the like rather than investors in their own right.

This is a common

ruse employed by scammers to deflect attention from their negligent

or fraudulent advice or investments – and I am disappointed to see

you using it. You know very well that we are talking about ordinary

people with pensions so please don’t be obscure and opaque.

The trustees I have spoken to have

made it clear that they are not the clients. The investor is the

client and the recommendations for the investment was made to the

individual client. All the money going into the fund is from retail

clients’ pension funds. Of course the customer is a retail client,

it is the retail clients’ money that is invested.

We addressed above the position in

regards to the identity of the investment manager in question,

Yes you did – falsely. Can you

please tell me the truth now?

and again we are

gravely concerned as to your use of the word “fraudulent”

within

your blog.

It was indeed

fraudulent to state that Meriden Capital Partners was the Investment

Manager when it clearly was not. Then, the subsequent “explanation”

about Mr. Rodriguez of IIG being the Investment Manager was also

wholly untrue.

Your

conclusion that this implies “criminal, deceitful and dishonest

conduct seeking to scam people” is perfectly natural. Indeed, if

you would like to call Mr. Gerald Rodriguez at the Gibraltar

International Bank – +350 200 13900 I am sure he will confirm to you

himself that your client is lying. https://www.gibintbank.gi/contact

The natural and

ordinary meaning which our client attributes to it is that it is

involved in criminal, deceitful and dishonest conduct, through which

it seeks to “scam” people of their pensions.

Your client is

indeed involved; has clearly exhibited deceitful and dishonest

conduct, and people have been scammed out of their pensions.

I have explained how the deceit was organized, all verifiable.

Such a description of our client can only

seek to lower its reputation in the eyes of the reasonable reader,

without any exercise in strained construction.

If your client

helps the victims to redeem their Blackmore Global investments

without further delay, there is no reason why their reputation should

not recover. Your clients need to acknowledge that the fund should

never have been used for pensions and put right any loss or damage

suffered by the victims.

Our client is not

involved in the provision of financial advice to consumers/customers.

Its ultimate clients are pension trustees, and it has no direct

communication with underlying beneficiaries. Our client is not in any

way involved in the provision of advice to consumers who go on to

invest. There is no obligation upon our client to have their company

“audited”.

Despite

such, our corporate client has voluntarily sought an audit of its

business by Grant Thornton,

The

fund was indeed promoted to numerous UK residents – illegally. I

have their details and documentary evidence. The clients are not the

investment managers or the trustees – but the investors themselves.

This is a ruse frequently used by scammers to justify investing

clients’ pensions in high-risk, toxic, illiquid – sometimes

professional-investor-only – funds and instruments. Please be

clear, the “advice” was given to the clients – not investment

managers or trustees. This is clearly evidenced and confirmed by the

trustees.

Your

client was involved from the targeting of prospects, through to the

advice process and investment into their own funds.

which remains

underway and to which you refer. The product is administered through

registered regulated custodians and agents, who control all relevant

bank accounts.

And who are

these custodians and agents? The factsheet and brochure state they

are Corporate Options Ltd and OrmCo Ltd. Corporate Options (IoM)

claims to provide the following: company management and