Since 2010, £millions have been lost to pension scams, thousands of victims have lost their retirement savings, large-scale misery and poverty are the terrible results. One common factor connects many of these scams: one man – Stephen Ward.

Here at Pension Life we have made a video – based on the Mastermind quiz. Lessons must be learned from the dozens of scams, headed by Stephen Ward, which ruined thousands of lives and destroyed hundreds of millions of pounds’ worth of pensions.

Premier Pension Solutions, Stephen Ward’s company in Moraira on the Costa Blanca, was responsible for the Ark pension liberation scam. Ward had advised 160 victims to transfer £10m worth of secure pensions into this scheme on the promise of having 50% of their pensions paid to them in cash. 2011 saw the Pensions Regulator place the scheme in the hands of Dalriada Trustees. The High Court called the Ark scheme a “fraud on the power of investment”.

Ward then went on to his next scam: Evergreen New Zealand QROPS and the Marazion “loans”. The “sister company”, Continental Wealth Management, was running the cold-calling operation to lure victims in – and some of the CWM salesmen were hanging around outside supermarkets to try to trap people into this scam. When Evergreen was removed from the QROPS list, Ward continued to work with CWM. It is not known how many other Stephen Ward/Premier Pension Solutions scams CWM was involved in.

Mastermind – Stephen Ward

1. Who is the owner and director of the Spanish firm Premier Pension Solutions based in Moraira on the Costa Blanca in Spain?

Stephen Ward

2. In 2010, who was running road shows in the United Kingdom to promote the Ark pension liberation schemes and recruit introducers?

Stephen Ward

3. In the Ark pension scam, which operated in 2010/11, who was the biggest introducer with more than £10m worth of transfers?

Stephen Ward

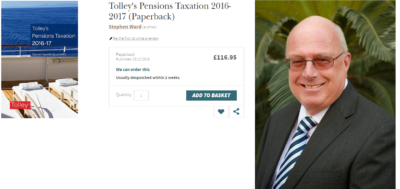

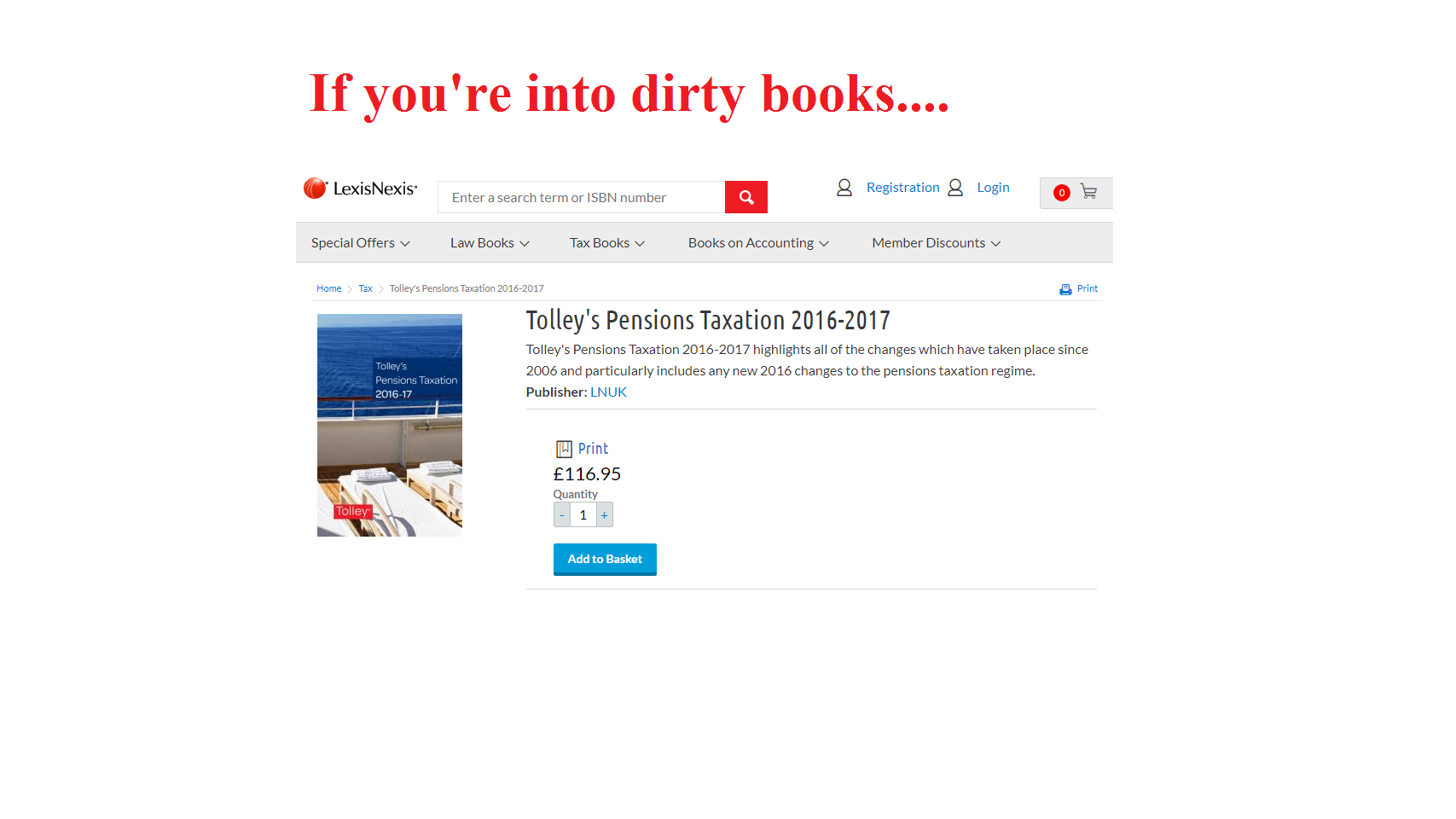

4. Who is the author of the Tolley’s Pensions Taxation Manual described as an essential reference source for all tax practitioners?

Stephen Ward

5. Who administered the pension transfer administration in the Capita Oak scam which saw 300 victims lose £10m worth of pensions and is now under investigation by the Serious Fraud Office?

Stephen Ward

6. Who handled the pension transfer administration of the Westminster pension scam which saw 79 victims lose over £3.3 million pounds to worthless investments: now also under investigation by the Serious Fraud Office?

Stephen Ward

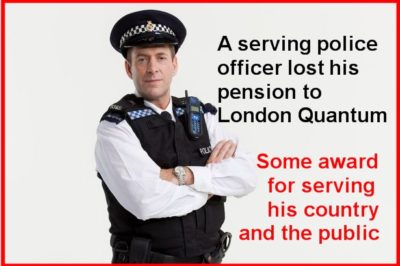

7. Who was the trustee for the London Quantum pension scheme now in the hands of Dalriada Trustees and invested in high-risk, illiquid investments such as Dolphin Trust which paid investment introduction commissions of up to 30%?

Stephen Ward

8. Which Level 6 qualified former pensions examiner and IFA in 2014 was famously quoted as saying: “The schemes with which we are involved are completely above board. The Ark thing is history now.”

Stephen Ward

9. Who was promoting the Elysian Fuels SIPPS liberation scheme which he described as allowing members to “trouser” most of their pension fund in cash?

Stephen Ward

10. Who was the owner of the loan company Marazion which operated pension liberation loans in the Evergreen QROPS scam which saw around 300 people lose £10 million worth of pension funds?

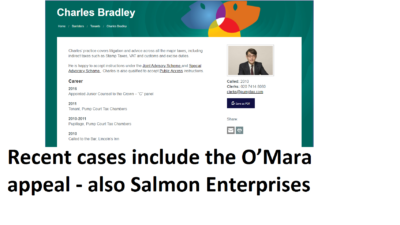

The Salmon Enterprises victims will have to wait until after Easter for the verdict on the Salmon Enterprises Tax Tribunal appeal. This will be a very anxious time for the victims of James Lau – currently under criminal investigation – and the directors of Tudor Capital Management currently serving eight-year jail sentences for cheating the Public Revenue and money laundering offences.

The anxiety will inevitably be shared by the Ark victims – as HMRC now want to push ahead with the Tax Tribunal appeals as well (after seven years of dithering). The Salmon Enterprises determination may well have an impact on the Ark appeal so there will be hundreds of people desperate for news after Easter.

In the Salmon Enterprises appeal heard in London on Tuesday 20th March, HMRC was represented by Charles Bradley of Pump Court Tax Chambers. A distinguished and gentlemanly young barrister with a double first in history at Cambridge, it remains to be seen whether his arguments for HMRC’s case based on interpretation of legislation and authorities will outweigh our arguments for justice and morality. Perhaps history will surprise us all after Easter.

I would like to pay tribute to the dignity and courage of the appellants at the Salmon Enterprises hearing. Having traveled down from the north of England, and spent many days preparing themselves mentally and intellectually for the ordeal before them, my heart went out to them both. A teacher and an IT analyst, both victims had worked hard all their lives and led exemplary lives before falling victim to this scam at the hands of criminals.

These two appellants – like the Ark victims – have endured years of worry and damage to their health since they were scammed in 2011. I was immensely proud of them as they stood in the witness box and represented, effectively, all victims of the Salmon Enterprises and Ark cases.

As I listened to the case put forward by HMRC, and the testimony of their witness, the words of Margaret Snowdon (speaking at the Transparency Task Force Symposium in November 2017) kept ringing in my ears:

“It is morally wrong to impose tax penalties on victims of fraud”.

Margaret was appointed an OBE in 2010 and has, uniquely, for six years running been named as one of the Top 50 Influential People in Pensions and was awarded for her outstanding contribution to the pensions industry by the PMI in 2012.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Pension scammers are hidden all around us, often dressed in smart clothes, driving smart cars and carrying impressive leather folders. They offer what seems like smart investments, push through your pension fund transfer swiftly and seamlessly. However what you don´t see on the surface is their hidden parasitic ways. These scammers will drain the funds from your pension, investing in high-risk, toxic investments, that only they will profit from.

Here´s Pension Life´s, “Top 10 Pension Scammers”. (Please note: this information is correct as of the today´s date only, as pension scammers are evolving daily and as one falls another will rise!)

John (Gus) Ferguson’s firm Square Mile International promote unregulated toxic crap to pension savers and employs unqualified David Vilka. The so-called “advisers” promoted the Blackmore Global Fund.

It is still unclear what has actually happened to the money invested into the Blackmore Global Fund.

James Lau was a financial adviser with Wightman, Fletcher McCabe (FSA regulated) – part of the Clarkson Hill Group. Along with directors Peter Bradley and Andrew Meeson, of Tudor Capital Management (subsequently jailed for eight years for money laundering and tax fraud), James Lau conned 116 victims into transferring their pensions, investing in forex trading companies, and liberating up to 85% of their pensions. Lau is now rumoured to be in hiding in Hong Kong. The victims are now facing 55% tax charges by HMRC.

8 – Friendly Pensions

David Austen of Friendly Pensions, used cold-calling and high-pressure sales tactics to strong-arm 245 victims into investing in 11 fake schemes, including a truffle farm.

Dalton, Barratt and Hanson all served as trustees on the fake schemes set up by Austin – who is described as the mastermind – and were paid more than £550,000 between them. The four scammers who conned pension savers out of £13.7 million have now been banned from the industry but not imprisoned. The victims, however, lost everything.

One thousand people were relieved of up to £100 million worth of pension funds. Conned by a motley assortment of snake oil salesmen, the victims were promised high returns, but all they got was high losses. Old Mutual International (OMI) were the provider for the bulk of the insurance bonds in this scam. Funds were invested in risky, toxic structured notes which were clearly labelled as “for professional investors only”. Clients were lied to, as when they saw the value of their funds plunging dramatically, the Continental Wealth Management scammers assured the victims that the reported losses were “only paper losses”. Continental Wealth Management collapsed in September 2017.

6 -XXXX XXXX

XXXX XXXX was the “distributor” of the Capita Oak, Henley, Westminster and various SIPPS scams in 2012/13. He was also operating pension liberation fraud with his “loan” company: Thurlstone. When these schemes collapsed in 2013, he went on to launch an investment scam called Trafalgar Multi Asset Fund. Capita Oak, Henley, Westminster and Trafalgar Multi Asset Fund are now all under investigation by the Serious Fraud Office. XXXX XXXX has been arrested and his offices searched.

Phillip Nunn – along with his sidekick and partner in crime Patrick McCreesh – provided “lead generation” services to the Capita Oak and Henley scams. At up to 200 leads a month for more than two years, he was responsible for the destruction of £ millions of pension funds – and got paid nearly £1 million in fees for doing so. He then went on to set up an investment scam called Blackmore Global – a UCIS which is illegal to be promoted to retail pension savers. It is not known whether the investors have lost some, most or all of the funds in Blackmore Global as Phillip Nunn refuses to have an independent audit carried out on the fund.

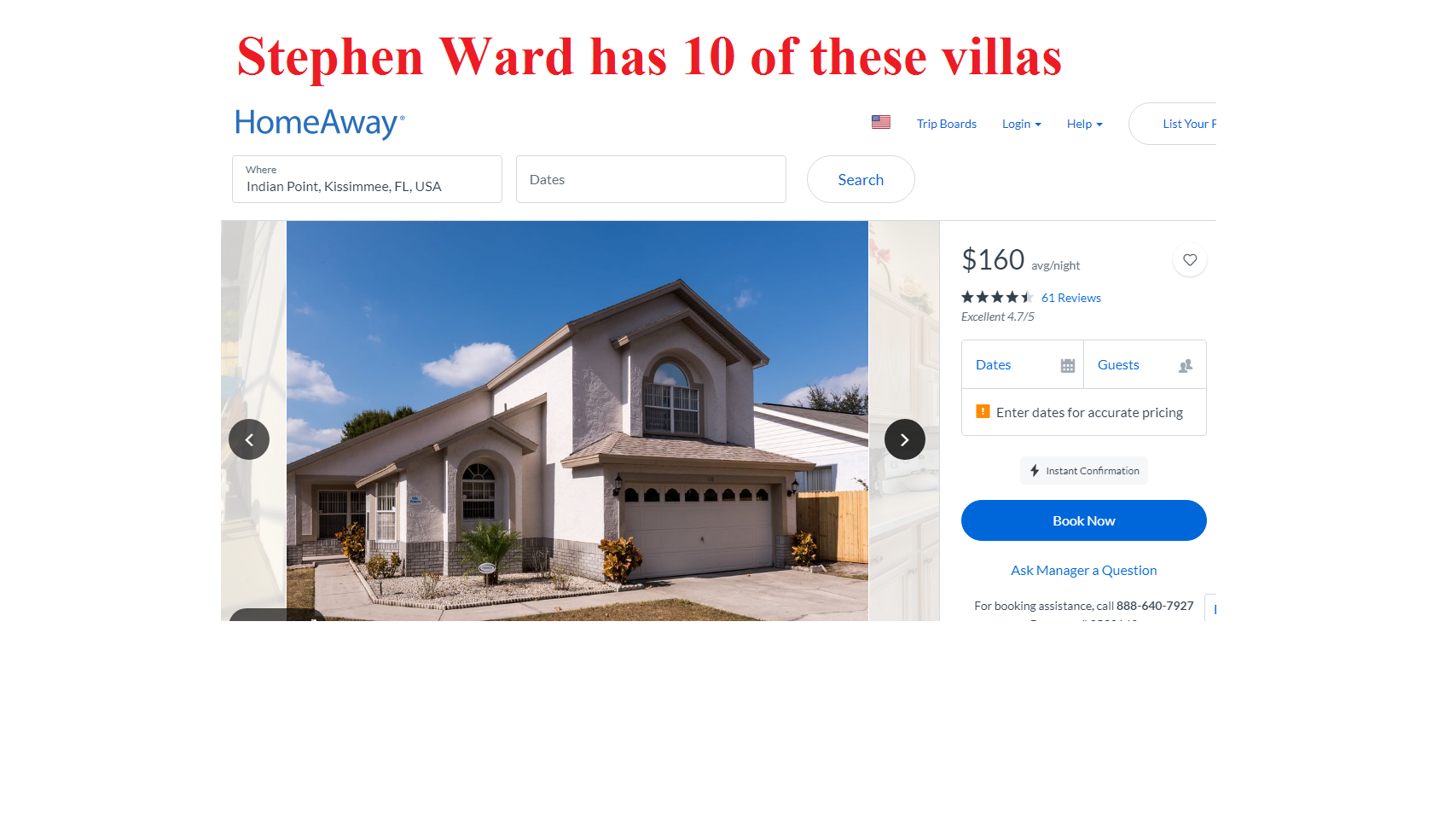

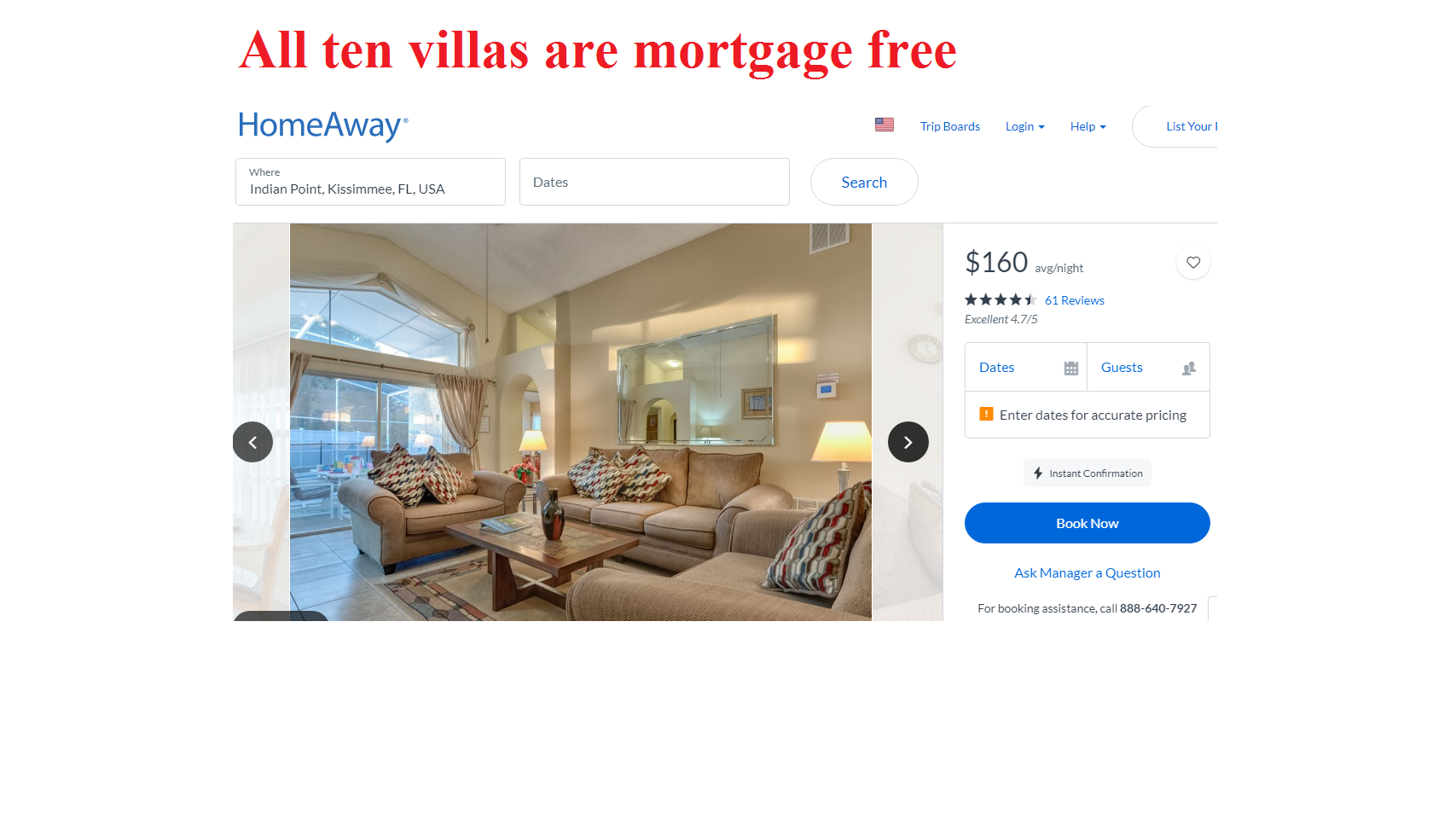

Steve Pimlott has been running Windsor Pensions for at least seven years. He claims to have done around 5,000 pension liberations and assures victims that HMRC will be “unlikely” to catch up with them. Pimlott uses QROPS schemes such as Danica in Sweden and then sets up a fraudulent bank account in the Isle of Man. The transfer never goes anywhere near Danica, of course. But the transfer is sent to the IoM bank account – 85% is paid out to the victim and Pimlott trousers the other 15%. HMRC is now taxing the victims at 55% – although they have never taken action against Pimlott who is still operating happily in Florida (not far from where Stephen Ward has his six luxury villas).

Peter Moat and his wife Sara Moat were chums of Stephen Ward of Premier Pension Solutions. They ran a loan company called Blu Debt Management and also had several other businesses involving estate agency and pension administration. Hundreds of victims were transferred into the Moats’ Fast Pension schemes, and now the victims cannot access their pensions or transfer out. Peter and Sara Moat live in the Javea area of the Spanish Costa Blanca and have had 18 Pensions Ombudsman’s determinations against them for mal-administration of the pension schemes they are running. It is thought that around 400 victims are affected, although it is not known how much they have lost between them. It is known that several years ago, a substantial amount of the funds were loaned to Bridgebank Capital and then used as bridging loans for property developers. But the money has since been repaid and goodness only knows where it is now. Certainly not accessible to the members.

Capita Oak: 300 victims; £10 million at risk; tax penalties on XXXX XXXX’s Thurlstone “loans”

Westminster: 200 victims; £7 million at risk; tax penalties on “loans”

Southlands, Headforte, Feldspar, Hammerley, Maribel, Dorrixo Alliance, Halkin, Bollington Wood, Randwick Estates, Elysian Fuels, London Quantum – and many more. Stephen Ward remains active with DB transfers.

and in first position we have …..

1 – HMRC

Yes, you read correctly, HMRC is our number-one culprit in the Top 10 pension scammers list. And here’s why:

Since at least 2010, pension scams have been on the rise. That’s 8 years, yet regulations have not been changed, HMRC has not become vigilant or conscientious about registering pension scams, and new laws have not been put in place to stop scammers.

In fact, the scams are registered in the first place by HMRC, and in the case of occupational schemes also by tPR.

No notice is taken of whether the schemes are registered by known scammers and no questions are asked as to the purpose of the schemes.

In the case of James Lau’s Salmon Enterprises, the trustees – Meeson and Bradley – had been investigated by HMRC and arrested in March 2010 on suspicion of money laundering and tax fraud. However, HMRC did nothing to warn ceding providers or the public and Salmon Enterprises was left as an HMRC-registered, fully-operational occupational scheme.

Later that year, one ceding provider queried the legitimacy of the Salmon Enterprises scheme, but HMRC refused to elaborate on why the trustees had been arrested. A transfer went ahead – along with 115 others – while HMRC sat back in the full knowledge that all these victims would be bound to face unauthorised payment tax charges.

In the Ark case, HMRC spoke to the organisers and promoters (including Stephen Ward) of the six Ark schemes on several occasions. They then had a meeting with Craig Tweedley and Ward in February 2011 to discuss their concerns that the 50% “loans” paid out to scheme members constituted unauthorised payments. At this point there was a “mere” £7 million worth of transfers. Nothing was done to suspend the Ark schemes for another three months – during which time a further £20 million was transferred in. HMRC is now trying to tax both the members and the scheme for unauthorised payments.

In the full knowledge that Stephen Ward was behind Ark and numerous other scams, HMRC ignored evidence of his pension trustee/administrator firm – Dorrixo Alliance. In May 2014, they discussed prosecuting Ward, but did nothing about the London Quantum pension scam, and in August of the same year, a police officer lost his police pension to Ward’s scheme.

Therefore, HMRC takes 1st place, due to its downright lack of motivation to help stop the scams, yet speedy tax demands fly out for the unauthorised payments arising from the so-called “loans” operated from the very schemes that HMRC themselves registers.

Furthermore, HMRC taxes the victims of pension liberation scams – and not the perpetrators.

List of 10 deadliest parasites borrowed from listverse website for comparison.

**********************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

There are many different types of pension scam – just as there are many types of genuine pension scheme. This can sometimes make it difficult to tell the difference so we are her to help you inform you about, what is a pension scam.

Fortunately, there are some common tell-tale signs that mean you could spot a scam and avoid it:

Cold calling: always be suspicious of a cold caller. This can come as a text, phone call, email or even a smart-looking individual at your door!

Some cold callers may even imply that they are from the government or another government-backed organisation.

THIS WOULD NEVER HAPPEN!

Hard sell: when your smart-looking/sounding “adviser” won’t take “no” for an answer and pressurises you into an on-the-spot decision

No land-line contact phone number: the only contact they give consists of an email, mobile or PO Box address

Use of words like ‘pension liberation’, ‘loan’, ‘loophole’, ‘free pension review’ or ‘one-off investment’

Unrealistic claims:

You can unlock your pension before 55

Promises of tax advantages

investment is ‘unique’, ‘overseas’, ‘environmentally friendly’, ‘ethical’ or in a ‘new’ industry

Low risk but high return investments (THEY DON’T EXIST!!)

What the scammers don’t tell you is that taking any part of your pension early (before 55 years of age) DOES result in tax charges. These charges can be up to 55% of the amount you take – even if you were told it was a “loan”.

With HMRC on your back for this tax demand, it will be hard to remember the pleasure of the money you received. Plus, whilst you are distracted with your tax demand from HMRC, it is likely that the rest of your pension fund is taking a nasty tumble.

Pension scams can involve various types of pension arrangements from QROPS and QNUPS to occupational schemes and SIPPS. These arrangements are not, in their own right, bad. However, if they are used for unsuitable investments, they most certainly can be. Know about these investments means you will know about what is a pension scam.

The investments inside the schemes can range from high-risk, professional-investor-only structured notes to toxic, illiquid, risky UCIS funds (Unregulated Collective Investment Scheme – illegal to be promoted to UK residents). Whilst these types of investments are not illegal in their own right, they are only suitable for certain people with deep pockets and sound investment experience. Or, alternatively, they are totally unsuitable for pension funds – full stop.

When taking advice on transferring your pension fund you should always ensure the adviser you choose is either based in the UK OR in the country you reside/plan to reside in. Alternatively, you must make sure the adviser is regulated and qualified for pension and investment advice in the jurisdiction where you reside.

If you’ve already signed something you’re now unsure about, contact your pension provider straight away. They might be able to stop a transfer that hasn’t taken place yet.

If you think you’ve been targeted by an investment scam, please report it to the FCA using their reporting form.

If you have lost money to a suspected investment fraud, you should report it to Action Fraud on 0300 123 2040 or online at www.ActionFraud.police.uk.

If you have doubts about what to do, ask The Pensions Advisory Service (TPAS) for help. Call them on 0300 123 1047 or visit the TPAS website for free pensions advice and information.

Beware of being targeted in the future, particularly if you lost money to a scam. Fraudulent companies might take advantage of this and offer to help you get some or all of your money back.

*************************************

With out due diligence and knowledge you often won´t realise that you are the victim of a pension scam until its too late. Its best to have the knowledge so you can tell what is a pension scam and what is a genuine pension scheme.

Therefore, Pension Life has written a series of blogs about pensions, pension scammers and how to safe guard your pension fund from fraudsters. Please make sure you read as many as possible and ensure you know everything you should about your pension fund. If we can educated the masses about pension fraud we can stop the scammers in their tracks – worldwide.

The BSPS dilemma for steelworkers is clearly difficult with very little time to consider options and make a wise decision which will affect them for the rest of their lives.

There’s a whole team of willing voluntary professional advisers trying to provide some guidance to help people avoid making the wrong decision. This team includes eminent pensions experts including Henry Tapper (The Pension Ploughman), Al Rush, Darren Cooke and many more.

I’d like to contribute to this excellent initiative to help the scheme members – but I can’t advise how to do things right; I can only advise how not to do things wrong.

Henry Tapper, Al Rush and Darren Cooke – plus other qualified, licensed advisers generously giving their time to help the BSPS members – will give sound guidance as to the right decision to make. The Pensions Advisory Service will also help.

Here are some pointers from me – someone who represents hundreds of victims of pensions scams and has seen all the tricks, lies, false promises and smoke/mirrors in the pension scamming business.

Check that a proper adviser is licensed – in other words: regulated. You can check this out on the FCA register. Here is an example: check out Darren Cooke’s firm, Red Circle. You will see that his firm is regulated (or licensed by the FCA – Financial Conduct Authority) to carry out personal pension and stakeholder pension advice. Remember, unregulated means SNAKE OIL SALESMAN. And beware the “introducer” – which is another word for snake oil salesman. If you find the so-called adviser is not regulated – run like hell!

Beware “free” financial advice. Go to Tesco and ask if they have any free milk. Go to the Post Office and ask if there are any free stamps. Go to an accountant and ask if he will do your accounts for free. Go to your local car dealer and ask if there are any free cars. There ain’t no such thing as free. Everything has to be paid for – but make sure that all the charges, fees, commissions etc., are openly declared. If someone promises you free financial advice – run like hell!

Run a mile from “get rich quick” investment schemes. Your pension has to be invested in boring, safe, traditional assets which will grow steadily and safely. If you are offered something exciting and sexy – like eucalyptus plantations; car parks; football betting; overseas property “opportunities” and truffle trees – run like hell. If you are told that your pension will get “guaranteed returns” of 8%, 10% or 12% – run like hell!

If you are told you can have some cash out of your pension other than your 25% tax free at age 55 – or the rest at the marginal tax rate – run like hell!

If you are cold called – run like hell!

Remember, you are a sitting duck – and it is open season. Also remember, the good guys like Henry Tapper, Darren Cooke and Al Rush – as well as all the other decent, honourable, ethical advisers who are volunteering their time free to help you avoid the scammers – can give you some invaluable, generic guidance. But someone who is offering to transfer your pension into another scheme is giving you advice.

So what is the difference between actual advice and general guidance? Let us take the example of a medical practitioner: you know a doctor – say a GP – at your local tennis club. You are concerned about your health in general and the fact that you are putting on weight and get breathless going upstairs. The doctor might suggest – as in suggest – that you consider going on a diet and taking some exercise, but that you also consult your GP. That is an informal and friendly (as well as well-meaning and common sense) suggestion. But it does not constitute formal advice. A specialist would look for deeper issues such as blood pressure, signs of diabetes and any other underlying conditions to be investigated – and would prescribe specific treatment.

If all else fails, drop me an email and I will try to help: angiebrooks@pension-life.com – but meanwhile, please buy some good running shoes!

Meanwhile, take a look at just a few of the schemes for which Pension Life is representing groups of victims who have lost their life savings to the same – or very similar – scammers who will inevitably be targeting you now:

Beddoe proceedings: arguably (apparently) Dalriada could have been pursued by Ark victims without MPVAs for not pursuing repayment from those with MPVAs and conversely could have been pursued by Ark victims with MPVAs. So, to be on the safe side, they spent a quarter of a million quid of the victims’ funds on the Beddoe proceedings in the High Court.

And here we need to look at the meaning of the terms – MPVA and sharp stick:

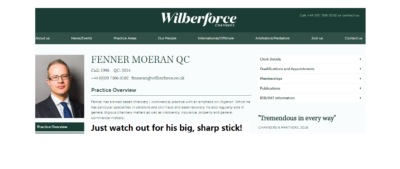

Sharp Stick: Fenner Moeran’s extremely offensive statement that Ark victims should be beaten with a sharp stick (upon which neither the judge, Sarah Asplin, admonished him nor upon which Keith Bryant, the Ark victims’ QC, challenged him)

MPVA

MPVA is an anacronym for “Maximising Pension Value Arrangements” – a euphemism for pension liberation. The rules are that if a person is under the age of 55, he or she can’t access any part of their pension without incurring an unauthorised payment tax charge of up to 55%. So all pension liberation scammers think up clever ways of fooling potential victims into believing there is a legal “loophole” to circumvent this rule.

The point of a pension liberation scam is not to provide members with a bona fide pension scheme designed to provide an income in retirement, but to make the scammers loads of money. First there is the transfer fee: in the Ark case it was relatively low at 5% – although Stephen Ward was charging an extra fee on top of that of up to £2k per transfer.

And then there are the investment kick-backs. We still don’t know how much the Ark scammers earned out of the speculative, illiquid, high-risk properties they purchased in various dodgy offshore jurisdictions. But it will have been very lucrative. In subsequent scams, the scammers earned huge commissions such as 20% from Dolphin Trust; 30% from Park First; 46% from Store First.

By the time the Ark victims realised they’d been scammed it was too late and there was no parachute

The scammers always promise spectacularly high returns on the investments with assurances such as “guaranteed 8% per annum”. In the case of Ark, the victims were told they would receive up to 9% a year on the growth of the value of “high-end London residential properties” in which the pensions would be invested. This, of course, was a lie. But by the time alarms started to ring and the victims realised there was no way out of this toxic flight with no parachute, it was too late.

But let us revert to the portion of a transfer which is liberated. This can range from 5% to 85% depending on the structure of the scam. And it is given various names or labels such as “cashback”; “thank you”; “refund of fees”; “trousers”; “loan”. The favourite word used is “loan” because the scammers claim that “loans are not taxable”. There is no intention for the money ever to be paid back – that isn’t the point of the exercise. The scammers know the victims would never be able to repay the funds.

The use of the word “loan” in some schemes is merely a marketing term used to fool people into believing they won’t be taxed on the money. And the scammers have no interest in whether the victims ever get taxed or not – because by the time HMRC gets around to sending out tax demands, the scheme will have collapsed and the scammers will be long gone and far ahead on their next scams. They never stick around to help mop up the train wreck left behind.

Often, the victims are surprised when they receive “loan” documentation and alarm bells start ringing. But the scammers assure the victims that this is “just a paper exercise” or “administration to make sure HMRC don’t try to tax the money – because loans aren’t taxable“.

In the Ark scheme, the victims were told the amounts liberated would not be taxable because they didn’t come from the members’ own scheme, but from another scheme. And this is why 14 schemes were set up to work in pairs so that up to 99 people in each pair of schemes could swap cash from their transfers. So this was an artificial mechanism structured purely to operate the liberation – using the label “MPVA” to dress the payments up as something more glamorous and bona fide than just a dollop of unauthorised cash in a person’s trousers.

Very few of the victims were told their cash would ever have to be paid back. The MPVA agreements never once mentioned the word “loan” but did mention the word “discharge” and suggested that the MPVA would be automatically “discharged” after a period of years.

Some victims were told the MPVA would be settled or repaid out of the growth that the Ark pension would enjoy (because of the wonderful investments!). It was explained that the MPVA would grow at 3% a year but the pension fund would grow at 9%. But the member would never have to pay the MPVA off out of their own pocket.

Other victims were told the MPVAs would never have to be paid at all because of the reciprocal nature of the transfer/payment structure. It was explained thus: two “paired” members in different schemes would each have a reciprocal MPVA of – say – £50k. If they both decided they never wanted to pay the MPVAs back, they would just treat them like equal IOUs and agree to simply tear them up.

The Tolleys authoritative manual on pensions taxation by Stephen Ward

Now remember, the victims weren’t told these things by any old spivs – they were told them by Stephen Ward of Premier Pension Solutions and his various accomplices (e.g. Fraser Collins, Terry Tunmore, Paul Clarke etc). Stephen Ward was back then – and still is now – a regulated financial adviser of many years’ experience, as well as the author of the Tolleys Pensions Taxation Manual, (and Level 6 CII qualified).

The same assurances were also given to numerous victims by George Frost, of Frost Financial, a regulated mortgage and insurance broker. And the victims who received the advice on the merits of entering into the Ark scheme believed they had every right to believe and trust professional, qualified and regulated advisers who assured them the MPVAs would never have to be repaid and that their pensions would be safe and secure.

HMRC does not care whether a sum of money accessed from a pension before the age of 55 is called a loan, thank you, cash back, fee refund, MPVA or any other euphemism for “liberation”. They don’t care whether it is repayable or whether it is ever repaid or not. They don’t care whether it comes directly from the member’s pension scheme, or from somebody else’s pension scheme, or via some convoluted arrangement designed to conceal the source of the money – such as Stephen Ward’s Evergreen/Marazion pension/loan scam. If a member makes a pension transfer and receives a sum of money as a result – irrespective of where it comes from – HMRC will issue a tax demand of up to 55%.

To illustrate how pension liberation scams range from the very simple and transparent to the highly complex and opaque, here is an example of one arrangement which Stephen Ward and his merry men, Alan Fowler and Bill Perkins, were involved with in 2013 – after Ark, Evergreen, Capita Oak and Westminster pension scams had all been suspended:

Thanks to you both for your understanding…. Am unused to non delivery! The arrangement I heard about today works like this as an example (ignoring fees) and this is the simplistic version …

Client borrows 16k or thereabouts (this is available in the package)

He gets a non recourse loan (which will not be repaid) of £84k

He buys shares in Xco for £100k. These are listed on the CISX (name is Elysian)

Transfers £100k to James Hay SIPP

SIPP pays member £100k for the shares

Member repays the 16k and trousers £84k

My IFA connection has done 40 of them so far. Advice to transfer to the SIPP is from an FCA regulated IFA. James Hay and Suffolk Life know the full structure and are happy with it.

Regards Stephen

The FCA-regulated IFA to whom he was referring was Angela South of Magna Wealth. She soon made a hasty exit from the collaboration with Stephen Ward when victims realised this was a scam and threatened to report her to the Serious Fraud Office. Victims who participated in this scam have now received tax demands from HMRC and Elysian Fuels is now worthless.

SHARP STICK

Dalriada’s QC, Fenner Moeran, seemed like a very sharp cookie. His skeleton argument (which we never got to see), and his opening speeches, started with the assumption that the MPVAs were definitely loans; that there was no question that they were loans and that the members knew and accepted that they were loans.

The judge, Sarah Asplin, accepted this without question and there was no debate on the subject. Kim Goldsmith’s QC, Keith Bryant, sat as quiet as a corpse and made not one single interjection or objection – even though he was sitting next to Kim who knew perfectly well – and must have told him – that the victims were not aware the MPVAs were loans. Indeed, they were categorically assured that the MPVAs would never have to be repaid.

Even more astonishing was the fact that Dalriada was aware the victims never knew the MPVAs were loans. Dalriada’s Sean Browes and Brian Spence, as well as Pinsent Masons’Ben Fairhead and Ian Hyde, had attended various meetings with the Ark Class Action and gone through this issue numerous times. They were also fully aware that one victim was horrified when she was subsequently told the MPVA was a loan and she immediately called Dalriada and asked to repay it. But Dalriada had refused.

Furthermore, dozens of Ark Class Action members had completed HMRC’s 10-point questionnaire (the Q10) which specifically asked about the arrangements and what they had been told about the need to repay the MPVAs. This is evidenced at HMRC’s question 8:

8: “DETAILS OF WHAT YOU WERE TOLD ABOUT THE NEED TO REPAY THE LOAN”

Here is a typical response to this question by one of the victims:

“I was told that although on paper it would be an official 25 year loan, that because of the nature of the way the loans were set up, i.e. the quid pro quo arrangement, whereby as one person received their monies from the other members scheme and vice versa, if there was a request for any monies to be repaid in the future from each member, each would tear up each other`s IOU and be quits, so to speak, as already stated.”

Stephen Ward – BA (Econ), ACII, APFS, APMI, ex examiner for the pensions management institute and for the CII, confirmed that the Ark scheme was designed by specialist pensions lawyer Alan Fowler – head of pensions at Stevens and Bolton.

Ward went on to explain how the MPVAs worked: “The best way to understand this is in terms of my lending you £100 and you lending me £100. If I do not repay you and you do not repay me then we are both in an equal position. Conversely, if I repay you and you repay me then the position is identical to that which would arise if neither party had repaid the other”.

These statements have been made to HMRC by Ark victims on countless occasions – and Dalriada has always been perfectly well aware of this. And yet Fenner Moeran used his sharp stick to knock these evidenced facts completely off the table – so that the judge was never made aware of them. Mind you, Keith Bryant QC was no better – because he didn’t bring them to the judge’s attention either.

I would go so far as to observe that Fenner Moeran should have used his sharp stick to point the judge to these evidenced facts – and Dalriada should have made sure he did so. By omitting to do so, both Fenner Moeran and Keith Bryant allowed the judge to come to the incorrect conclusion that:

“members who received the MPVA loans agreed to repay them. That’s the point of a loan. It’s not a gift. They cannot now complain about having to repay them. They can complain about having to repay them earlier, but that’s a cashflow issue which is vastly overwritten by the capital harm that is suffered by the non-recipient members”

Fenner Moeran merely leaned on his sharp stick and did nothing to correct the judge. As I was sitting behind him, I couldn’t see whether he was smirking – but I have a feeling he might have been. The judge was wrong on three counts:

The members with MPVAs did not agree to repay them – they were told they would never have to

They can most certainly now complain about being asked to repay them as they were never told they would have to and did not budget to do so

The capital harm suffered by members without MPVAs was mostly caused by Dalriada who did not reject their transfers after 31.5.11 but allowed transfers to continue right up until the end of August 2011

Having glossed over the facts smoothly, and directed the judge to her incorrect conclusion, Fenner Moeran then addressed the issue of ascertaining whether the Ark victims were in a position to be able to afford to repay the MPVAs. And then he produced, with a confident flourish, his pièce de résistance:

“The chances of getting ascertainably or enforceably more accurate information increases when you have the sharp stick of litigation behind it. If we want to see if we’re actually going to get any of this money back, the chances are that we’re going to have to wave a very large stick“

Fenner Moeran ought to be an intelligent person. In the full knowledge that a few feet to his right sat Kim Goldsmith, an Ark victim who had gone through six years of hell courtesy of Stephen Ward and George Frost and all the other scammers, and that a number of other victims were sitting at the back of the courtroom, he still made such an unbelievably stupid and offensive statement. He apologised later “I deeply and sincerely apologise for any misunderstanding or upset caused”.

But the damage had already been done – and you can’t un-say what has been said – especially when every word is recorded and transcribed. On behalf of Dalriada Trustees, he had deliberately misled the judge, and then proceeded to demonstrate clear contempt for the suffering of the Ark victims.

Interestingly, the judge had not remonstrated with Moeran for his crass comments – and Keith Bryant had not objected to the stupid and insensitive words. Throughout the rest of the proceedings, the judge remained – in my view – dominated and steered by Moeran. No attempt was ever made to disclose the truth about what the victims were told about repayment of the MPVAs by Stephen Ward, George Frost, Andrew Isles or Alan Fowler. And no explanation was ever given as to why Dalriada had not pursued these parties for having duped, misled and defrauded the Ark members.

This may seem like a completely off-topic piece of this report, but please stick with it – it will be worth it because it is the whole point of this report. Nearly 18 months before the Ark/Dalriada/Beddoe proceedings in the High Court, another case was heard: Royal London v Hughes. A pension scammer had tried to do exactly what the Ark scammers had done so successfully and profitably for nearly a year: transfer hundreds of secure pensions into a pension scam. But one ceding provider – Royal London – had blocked a transfer request. They strongly suspected the receiving scheme was a liberation scam – unlike the many ceding providers in the Ark case who handed over hundreds of transfers willy-nilly without question or due diligence – the worst of which was Standard Life.

Hughes complained to the Pensions Ombudsman that her transfer request had been blocked by Royal London. The Ombudsman did not uphold her complaint because he agreed with Royal London that the receiving scheme had all the classic hallmarks of being a scam – including the fact that the scheme had been registered as an occupational scheme and Hughes was not genuinely employed by the sponsoring employer. Exactly the same as Ark (and many of the subsequent scams).

Counsel for Royal London argued that “Hughes had to be an “earner” to be able to transfer”. He tried to support the Ombudsman’s view that the legislation required Hughes to be an earner in relation to a scheme employer”. This counsel obviously knew well that victims were made all sorts of promises and assurances and often not told the truth about the arrangements within pension scams.

Royal London’s QC would have been aware of the Ombudsman’s concerns that pension liberation may well have been behind Hughes’ enthusiasm to transfer her pension. And he will have known only too well that potential victims were systematically lied to and probably told that their “loans” (or whatever euphemism was used) were not repayable. And he would have known that the intended liberation “loans” were never intended to be repaid and that the victims would be told that the loans never needed to be repaid.

This QC will have been thoroughly briefed by his clients, Royal London, and may even have consulted with the Pensions Regulator who would have given him thorough details on how pension liberation scams worked.

So this particular QC had intimate, first-hand knowledge of how pension liberation schemes worked in general and represented Royal London in their quest to defend their right to prevent further victims of pension liberation scams. He also knew intimately how Ark worked in particular.

Fenner Moeran of Wilberforce Chambers

He knew perfectly well that the victims were told they never had to repay their loans (or MPVAs/cash backs/thank you’s/trousers). And he knew that the Ark MPVAs were supposed to be “discharged” from growth in the schemes and NOT from the victims’ own pockets – as reported by Justice Bean. But he failed to bring this to the judge’s attention.

Who was this QC? I will give you a clue – he had a big, sharp stick. Perhaps he should have gone to Specsavers and read the MPVA agreement where this was clearly stated.

The Ark victims’ QC rolls over as he is quashed by Dalriada’s counsel

DALRIADA V ARK VICTIMS: “ABUSE OF VULNERABLE MEMBERS OF THE PUBLIC”

The Beddoe proceedings of Dalriada (tPR-appointed independent trustees) v Goldsmith (representative beneficiary for the Ark members) kicked off on 20th June 2017 in the High Court. It was a sweltering day in central London – humid and dusty at the same time. The Ark victims were about to discover that the warning about anomalous and unjust outcomes made by Justice Bean in the High Court in November 2011 was going to be ignored.

Dalriada and their solicitors, Pinsent Masons, and their QC Fenner Moeran sat on the left in the airless courtroom. Mrs Goldsmith and our solicitors, Trowers and Hamlins and QC Keith Bryant, sat on the right. Justice Asplin sat on the bench and prepared to rule on whether 348 Ark victims would have to repay their MPVA loans – and whether Dalriada could use the members’ funds to pay for the recovery proceedings. A group of Ark, Capita Oak and Salmon Enterprises victims and I sat at the back. The only thing we all had in common was that everybody was sweating profusely from the heat.

To put this into context, the Ark victims did indeed all sign loan agreements. However, the loans were intended to be paid back out of the members’ 25% tax-free lump sums available at age 55 – so the term of each loan agreement was calculated to be for the number of years it would take each member to reach 55. By which time, the pension was predicted to have grown by at least 8% per year and would be sufficient to repay the loans. Or so the story went.

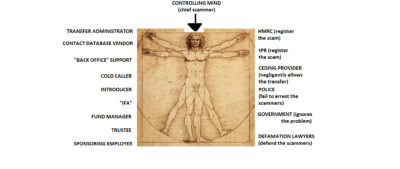

Conspicuous by their absence were the various introducers and advisers who sold the Ark schemes and accompanying MPVA (Maximising Pension Value Arrangements) “loans”. By far the most assertive and prolific of these was Stephen Ward of Premier Pension Solutions who sold over £10 million worth of transfers to more than 160 victims. Ward was followed by those who aspired to be as successful as him and these included:

Julian Hanson £5.3m

James Hobson (Silk Financial) £2.3m

Jeremy Dening £2.2m

Michael Rotherforth £961k

Richard Davies £805k

Geoff Mills £794k

Andrew Isles £584k

Amanda Clark £227k

Many of these went on to operate further pension liberation scams – some of which are now also in the hands of Dalriada Trustees. Andrew Isles of Isles and Storer Accountants is still in practice. Stephen Ward still authors the Tolley’s Pensions Taxation Manual.

The definitive pensions taxation manual by leading pension liberator Ward

Interestingly, Stephen Ward, who used Ark to launch a whole series of further pension scams – including several currently under investigation by the SFO and in the hands of Dalriada – claimed in 2014 that “The Ark thing is history now and my involvement with that was administrative”. Of course, neither of those statements was true: Ark is far from being history as, in the wake of the Beddoe proceedings, a whole new chapter of wretched challenges for the Ark victims has only just begun. Ward was the leading promoter, evangelist and advisor to Ark. He had sold over a third of all the transfers – with a total transfer value of more than £10 million.

In fact, Ward and his herd of “introducers” he had recruited from up and down the country (including FCA-registered Gerard Associates which went on to collaborate with Ward in the London Quantum pension scam) – also now in the hands of Dalriada – often assured the victims they would never have to repay the loans.

Fenner Moeran QC, for Dalriada, opened with the lusty confidence of a dashing matador – and who could possibly have failed to be charmed by his persuasive, eloquent, star quality? He reminded me of an actor at the Oscars who knew he was the favourite to win. With his extravagant hand gestures and polished, word-perfect performance, he got into his stride and stayed there – holding court for the whole day with barely a feeble squeak out of our QC.

Moeran’s confidence, however, veered a little too close to cockiness, and he strayed occasionally into the realms of being callously offensive to the Ark victims when he talked about using a “sharp stick” to beat them into submission with threats of bankruptcy. At that moment, he stopped looking like a polished QC and started to look like a mere back-street bully. In fact, it was astonishing that the judge didn’t pull him up on that “foot and mouth” moment, but she appeared to be far too mesmerised by his charming performance to notice – or care.

While I was taking notes, it was really interesting to watch the players’ body language. One can tell an awful lot about what is really going on in people’s heads by what they do with their various body parts. When Moeran was on his feet, Justice Asplin was coquettish, smiley, full of chuckles and did this wiggly thing with her shoulders (like we women do when we are trying to get a bra straight). But when our QC Keith Bryant was on his feet, she sat as still as a statue and peered down at him with a combination of indifference and pity as if he was a dying bull in the afternoon sun.

Mrs Goldsmith sat quietly and showed not a shred of distress as Moeran referred to her and all the other Ark victims as though they were just names on a list, as opposed to human beings – or indeed anything with a pulse. Knowing her well, I am sure she will have felt profound pain and anguish during the whole three days, but not once did either her composure or her dignity slip.

So here is my transcript of the notes I took on what the various parties said during the proceedings – with my comments in bold.

The last thing I personally want to say on the matter, is that something good has to come out of this and my fervent hope is that all those involved in the promotion, sale, administration, introduction, advice, purchase of assets, execution of loans and various other functions will now face justice sooner rather than later. And here, I am actually grateful to my learned fiend’s suggestion of a sharp stick and would propose something more akin to what Vlad The Impaler would have done to these criminals.

TRANSCRIPT OF MY NOTES AT THE HEARING

DAY ONE

Never forget that legal proceedings are nothing to do with justice

Justice Asplin opened with the words “This was a tragedy and an abuse of vulnerable members of the public”. That got us off to a really good start, but curiously the following day she vehemently denied ever having said it. She also denied ever having mentioned Ark and didn’t even seem to know that collectively, the six schemes (Tallton, Grosvenor, Woodcroft, Cranbourne, Lancaster and Portman) were the Ark schemes. Bearing in mind she had had – and been paid for – a whole day’s reading, one would have thought she would have been a little better prepared.

Ark’s Craig Tweedley was quoted as having made a statement that Ark was “designed to unlock amounts of money from people’s pensions in a way which was not taxable”. This is perfectly true – but it went further: it was promoted to the public (both introducers and potential members alike) as an innovative structure which was lawful and tax free. And the principal promoter and recruiter was Stephen Ward. Ward is also a CII Level 6 qualified former pensions examiner and government consultant on pensions and QROPS – so who wouldn’t have believed him?

One of the Ark schemes’ assets – the South Horizon land option in Larnaca, Cyprus – was brought up and reported as having been purchased by Ark for £4 million. But what was not mentioned was that the option had originally been purchased by two football celebrities for £1.1 million and then sold on to Ark for £4 million. And that this pair had gone to accountant Andrew Isles of Isles and Storer to get advice on how to procure further investors in the Cyprus land project. Isles had introduced them to Craig Tweedley and Stephen Ward. In fact, Isles subsequently introduced at least eleven cases to Ark.

It was stated that Craig Tweedley’s associates Andrew Hields and Julian Hanson had purchased all the assets of the schemes and that the sales documentation claimed that some of the funds were “guaranteed “funds and protected by “re-insurance”. Hields and Hanson may well have purchased some of the assets but they will certainly have benefited from handsome investment introduction commissions along the way.

It was also reported that one of the other Ark assets, Freedom Bay, the St. Lucia timeshare development, is now in administration and that none of the investments made met the statements and claims made in the sales documentation. In fact, it did not come out that few – if any – of the victims were ever shown the sales documentation. Most of Stephen Ward’s victims were told the assets would be “high-end residential London property”.

The matter turned to the recovery effort. It was reported that Tweedley had been pursued for the 5% fees taken from scheme members and that although Dalriada had won their claim, of the approx. £1.5 million taken in fees, they only ever actually managed to recover about £20k. This does beg the question as to just how successful Dalriada will actually be in recovering the £9 million in MPVA loans.

In taking steps to recover the loans, it was reported that Dalriada intends to consider the cost vs benefit situation and decide on the approach on a case by case basis, taking each individual case on its merits. It was acknowledged that the chances of recovery were slim and that the costs could be disproportionate to the likely return. The judge asked how many members had received MPVAs and it was disclosed that 348 had and 138 had not. However, nobody raised the question of why such a large number of members had not received an MPVA loan – had they done so it ought to have been disclosed that a significant proportion of transfers were not rejected after Dalriada were appointed.

It was at this point, while examining the possible avenues to recovery, that Moeran’s confidence bubbled over into bald cockiness and he started bragging about using the threat of bankruptcy as a “sharp stick with which to beat the victims into paying back their MPVA loans”. In fact, by now the judge seemed to be very firmly on his side and stated that the members had already agreed to repay the loans and that their only loss was having to repay early. It seemed clear that neither Moeran nor the judge understood – nor had made any attempt to understand – how the loans were sold to the victims. They were told, by Ward and all the others involved in promoting the scheme, that the loans would be repaid out of their pension pots and not out of their own funds. In fact, some people were told they would never have to repay the loans and that each person on either end of the loan transaction would simply agree to tear up their “IOUs”.

Moeran then went on to claim that by repaying the loans, members could avoid the tax charge. Perhaps the HMRC fairy had whispered this in his ear? Or perhaps he was deliberately ignoring the fact that it is HMRC’s position that the loans will remain taxable even if they are repaid.

Towards the end of day one, it was clear that Moeran was confident they were going to win and that the judge would clearly find in favour of Dalriada and against the members. It was also clear that he had the full support of the judge. In fact, Moeran even went so far as to pretty much read out what our QC, Keith Bryant, would be arguing and told the judge what she ought to find against the case he would be putting forward. At some point, I wondered whether Moeran and the judge would be swapping places.

Moeran talked about the methods and costs of taking recovery action against the Ark members. He itemised three issues to take into consideration:

Merits of taking recovery action

Cost vs benefit of taking recovery action

Consequences of not taking recovery action

He then went on to report that Dalriada had 144 signed Standstill agreements and said that Dalriada was intending spending £2,925 per member on court recovery action. The judge declared that that was on the low side as that cost could only happen if the claim was uncomplicated and resulted in a quick and easy repayment. She also said she was not confident that bankruptcy proceedings were necessarily appropriate.

She did, however, firmly declare that the Ark members had all shared the “mistaken belief” that the MPVA loans were valid, non-taxable and only repayable by the end of the originally-agreed loan term. She broke this “mistaken belief” down into four points:

The members’ “mistaken beliefs”:

The trustees had the power to make the loans

The loans were capable of being made valid

The trustee could transfer beneficial ownership of these monies

The loans were not unauthorised payments and would not trigger a tax charge

The judge appeared to consider that somehow the members had come to these conclusions all on their own. The reality was, of course, that this was exactly what they were told by Stephen Ward and the herd of introducers and advisers – including a couple of FCA-registered ones. But reality did not seem to concern either the judge or Moeran overly.

The last thing that Moeran said on Day One was to make reference to the revised Standstill agreement – the focus of which was to ensure that criminal proceedings are now taken against all those who were involved in defrauding the Ark victims. The judge read the document herself, giving us a welcome rest from listening to Moeran.

As the first day came to a close, I was beginning to wonder whether I had dreamed the fact that a High Court judge had clearly stated in the High Court that Ark had involved an abuse of members of the public. Her statement had been made in front of a dozen or more witnesses and she had then gone on to deny that she had ever said it in front of the same witnesses who all clearly heard her words. Moeran and the judge had both agreed the Ark sales documentation was false and yet I heard neither of them conclude spontaneously that criminal complaints were now essential.

DAY TWO

Moeran opened with: “We are in the process of agreeing six test cases at the First Tier Tribunal” in relation to the personal tax appeals resulting from HMRC’s treatment of the loans (whether repaid or not) as unauthorised payments. The judge questioned whether members put forward for this role might not be happy. Moeran confidently assured her that there had already been five volunteers. I am not aware that any of these purported volunteers have come from the Class Action. Also, at the last meeting that Mrs Goldsmith, Mr Walters (Salmon Enterprises) and I had with HMRC, we agreed two Ark test cases – one with a loan and one without. Moeran did not appear to be aware of this.

Skating quickly over the tax issue for the members – and studiously ignoring the fact that according to HMRC the tax will remain payable even if the MPVA loans are repaid – Moeran and the judge got back to pondering recovery measures. The judge expressed reservations about bankruptcy proceedings because she said that that would merely release members from liability to the scheme rather than help recovery.

Moeran and the judge then started to discuss which members might not be worth pursuing at all for a variety of reasons. Between them, they concluded that those with very small MPVA loans should be ignored and that they might also have to ignore those outside the jurisdiction of the UK. Moeran reported that there were four members in Northern Ireland; 22 in Scotland, 24 in the EU and four outside the EU – USA, Jersey, Bulgaria and Australia.

Neither Moeran nor the judge were sure whether Bulgaria was in the EU (in fact, of course, it is an EU member). The members and I having complained in the strongest possible terms about Moeran’s use of the term “beating the victims with a sharp stick” the previous day, Moeran then went on to publicly apologise for that statement. To be fair to him, he made a good job of the apology and I am sure that Mrs Goldsmith and other members present appreciated it.

I really don’t remember whether our QC said much or anything at all that day – if he did it was not very memorable, or perhaps I couldn’t hear him terribly well because he muttered apologetically and miserably rather than speaking in Moeran’s strident voice.

The MPVA loans were summarised thus:

50 members with loans between £5k and £9,999

124 members with loans between £10k and £19,999

132 members with loans between £20k and £44,999 (totalling £4m+)

40 members with loans of £50k upwards (totalling £3m+)

The judge opined that the bigger the loan, the bigger the original pension must have been, and therefore the wealthier the member was likely to be. She concluded that these would be the easiest targets for recovery.

Then the judge handed down her judgement. She summarised the claim by Dalriada for Beddoe relief (money to be taken from the members’ funds) for the recovery of the MPVA loans and also to challenge the scheme sanction charge in the Tax Tribunals. She approved both of these, but did not agree that Dalriada should use funds to help the members with their individual tax appeals.

She reported that 152 claims had been written to date and that 12 consent orders had been received. She declared that she believed the claims were strong but expressed reservation as to whether the members were in reality good for the money. She reminded the court that there were 138 members without loans and that Dalriada had a duty to protect their position by recovering loans from as many of the other 348 members as possible.

She determined that it was appropriate that the trustees should be granted the relief they sought – albeit not the entire amount sought. She advised Dalriada to take stock of each individual situation and use their discretion as to whether it was appropriate to continue with the action. She also urged them to take into account relevant factors including the aggressive stance being taken by HMRC and to act as a reasonable trustee.

Finally, she said Dalriada should bear in mind that the individual cost of recovery per member would rise from £2.9k to £3.6k (plus VAT) if bankruptcy proceedings were issued and that those with the very smallest loans ought not to be pursued because of the disproportionate cost of doing do. She said it was difficult to decide where exactly the “watermark” might be and reiterated that bankruptcy might not be appropriate and should not be the first refuge sought and could be used as a “second string to their bow”. She suggested that further directions might need to be sought by Dalriada.

Regarding the scheme sanction tax charge appeal matter, she said it was appropriate to give the relief sought and for Dalriada to take steps to challenge the assessments. She recommended a “ceiling” on the amount to be spent and said that to challenge the £4m in tax sought by HMRC, the amount of £350k + VAT was appropriate.

On the question of paying a further £50k to fund legal representations for members against personal tax assessments, she recommended that the scheme sanction charge and the personal tax appeals should be coordinated. But she expressed a reservation about granting this relief to Dalriada as she felt it was excessive “because of the vagueness of what might take place”. She did not consider that for them to pay a barrister was necessarily a reasonable step to take. Therefore, she did not grant the relief sought.

In summary, therefore, the judge’s determination was as follows:

Yes to recovering the MPVA loans from as many of the members as possible/practicable

Yes to paying for the recovery costs out of the members’ funds – at the ideal rate of £2.9k + VAT per member (possibly rising to £3.6k + VAT per member if bankruptcy proceedings were issued)

Yes to taking £350k + VAT out of the members’ funds to pay for the appeal against the scheme sanction charge

No to paying £50k + VAT towards the members’ personal tax liability appeals

At the start of the proceedings, Moeran had reminded the court that Dalriada, as the trustee, already had the legal right to recover the loans if they chose to. But they were seeking the necessary relief and directions to do so from the court to protect their position.

DAY THREE

The final day was all about the nitty gritty of how the recovery costs should be apportioned between the six schemes. Moeran and Bryant put forward different suggestions as to whether this should be done on the basis of the value of the assets or the value of the MPVA loans within each scheme, and whether this should be done equally or on a pro rata basis.

The members at the back of the court were by now numb and none of them really paid much attention to what was basically “housekeeping” in terms of internal accounting procedures by Dalriada. One of the judge’s last points seemed to be that Dalriada should take all and any reasonable steps to recover the MPVA loans – but that the only question was what was reasonable. She cautioned that some options should not be taken, but stopped short of saying what they were.

Shedding a tear or two at the departure of tPR’s Head of Willy Waggling

Bye bye Tinky Winky. Good luck and have fun at LGPS!

His next challenge will be to lead by example and ensure negligent ceding providers compensate their victims whose pensions were transferred into scams. And he can start with LGPS as a shining example so the rest can follow.

As Tinky Winky sails off into the sunset and leaves his regulatory willy waggling duties behind, his first mission is to understand the other side of the coin: the transfer of £millions from secure pensions into the trousers of the scammers. He will now see with a fresh pair of eyes how ineffective tPR has been – and how negligent the ceding providers were.

Winky is going to have quite a mess to clean up when he gets to LGPS – so he had better make sure he takes Noo Noo with him.

Will probably need more than 1 Noo Noo – in different sizes for all the mess at LGPS

And I am sure he is going to be cheerfully looking forward to working even more closely with me from now on.

On June 19th, the Secretary of the Ark Class Action – Mrs. G – will be in the High Court as the Representative Beneficiary for the Ark victims challenging Dalriada Trustees’ Beddoe application. Dalriada, appointed by tPR in May 2011, have already spent around 15% of the £30 million Ark fund. They are now seeking the court’s permission and directions to use even more of the victims’ funds to take legal action against them to recover £11 million worth of liberation loans. This will result in financial ruin for most of the victims – many of whom will lose their homes. HMRC say the loans will remain taxable even if they are repaid so there is the real possibility that members will face two sets of crippling proceedings.

Mrs. G and the other Ark victims – originally 487 of them but now significantly fewer as some have died (some as a result of taking their own lives) – became victims because HMRC and tPR took way too long to take action to suspend the schemes. Also, the schemes were registered negligently in the first place – tPR allowed fourteen occupational Ark schemes to be registered by the same person without there being evidence of any intention or chance of the sponsoring employer being a bona fide employer.

Between August 2010 and August 2011, dozens of personal and occupational pension providers cheerfully handed over £30 million to the scammers with utter incompetence, no due diligence and complete disregard for all the dozens of warnings which had been put out by HMRC and tPR for many years.

In particular, these negligent ceding providers ignored this one issued by tPR Chair David Norgrove on 13.7.2010 just before Ark was launched: “Any administrator who simply ticks a box and allows the transfer, post July 2010, is failing in their duty as a trustee and as such are liable to compensate the beneficiary.”

I shall be looking forward to my next meeting with Tinky Winky because he will be able to bring a wealth of first-hand knowledge and experience to the table. I will probably be bringing Mrs. G to the meeting with me. Because guess who her negligent ceding provider was? Yep, you guessed – LGPS.

BACKGROUND TO THE NEGLIGENCE OF CEDING PROVIDERS SUCH AS LGPS:

The Ark schemes were launched in 2010 by – among others – Stephen Ward of Premier Pension Solutions S.L. and Premier Pension Transfers Ltd. The six Ark schemes had been registered by HMRC and the Pensions Regulator with no due diligence by either to establish whether the schemes had been set up with the specific purpose of operating pension liberation; whether they were bona fide occupational pension schemes set up by a sponsoring employer which intended to trade and provide employment; whether there was a competent trustee and board of trustees in place; whether there was a clear Statement of Investment Principles or whether there was ever any realistic prospect of the schemes providing member benefits.

At around the same time, a multi-million pound occupational pension scam was being vigorously promoted by James Lau of Wightman Fletcher McCabe while the administrators/trustees of the scheme, Andrew Meeson and Peter Bradley, were under criminal investigation for cheating the Public Revenue (and were subsequently jailed). Also, former barrister, solicitor and porn star Paul Baxendale-Walker was promoting a whole series of liberation scams unhindered by the authorities – despite having been firmly in the spotlight since 2007 as a passionate advocate of liberation. And KJK Investments/G Loans was a further liberation scheme flourishing at around the same time, having been started in 2009.

By the time Ark was getting well underway, tPR (formerly OPRA) was fully aware that liberation scams were proliferating and that the feeble warnings they had made back in 2002 about scams which had been operating as far back as 1997 had reached neither the public nor the industry effectively. In 1999, tPR had been investigating two scammers – Stephen Russell and William Ferguson – for a £6m pension fraud. The pair were jailed for five years in 2003.

In fact, tPR were fully aware that since 1999 pension scams were on the increase, and yet did not make it clear to ceding pension trustees what their statutory obligations were in respect of transferring victims into scams. On 13.7.2010, tPR Chair David Norgrove stated that: “Any administrator who simply ticks a box and allows the transfer, post July 2010, is failing in their duty as a trustee and as such are liable to compensate the beneficiary.” But pension trustees claim they never read that message (let alone heeded it) and that it was neither publicised nor distributed. Further, in the same year Tony King, the Pensions Ombudsman, reported that he had “found that pension trustees failed in carrying out serious fiduciary responsibilities to others in circumstances in which the law specifically states that they should not be protected from liability.” And still tPR did nothing. And the Pension Schemes Act 1993 was not amended to reflect the urgent need to protect the public.

The Scorpion Campaign was launched by tPR in 2013 after fifteen years of failing to warn the public sufficiently, and omitting to make it clear to trustees what their statutory obligations were to pension scheme members. During this period, the pension scam industry matured into a deadly serious and well organised large-scale operation in the UK, with many new “players” coming into the arena having been trained by Stephen Ward and other founders and pioneers of early scams.

It was – by the time Scorpion dribbled weakly and ineffectually into the arena – well known to tPR what the typical characteristics of pension scams were and what phrases and claims were habitually being made by the scammers to dupe their victims into signing over their gold-plated pensions into worthless, toxic schemes and being financial ruined. Among the many key phrases (such as “your pension is frozen”; “tax-free loan”; “guaranteed 8% returns” etc.), was the most powerful of all: “the scheme is HMRC approved”. There was, of course, no such thing as HMRC were as guilty of lazy, box-ticking negligence as the culpable ceding provider trustees. But to this day, tPR has done nothing to dispel this myth, and in fact even continues to help the scammers by using the same incorrect phrase on its own website: “If you are required to register a scheme with TPR that does not require HMRC approval, please contact us.”

Even by the time tPR had published the feeble Scorpion campaign in February 2013, the scammers acknowledged this was having a negligible effect on their various scams, and merely moved the goalposts a little to avoid detection. Capita Oak, Henley and Westminster continued to operate successfully beyond February 2013, but only a few ceding pension trustees either noticed Scorpion at all or took any steps to put into practice the minimal due diligence suggested by Scorpion.

In the full knowledge that Stephen Ward was one of the most prolific pension liberation scammers, tPR took no action to suspend any schemes in which he was involved. As a consequence, in August 2014, a Police officer was scammed out of his Police Pension by Ward’s Dorrixo Alliance and into the toxic London Quantum scheme. In fact, far from having any widespread effect, the multitude of scams continue to this day unaffected by tPR’s dismal attempts to protect and inform the public.

PENSIONS REGULATOR’S OBLIGATIONS AND OBJECTIVES:

According to their own website, tPR’s statutory objectives are set out in legislation and include promoting and improving understanding of the good administration of work-based pensions to protect member benefits. These objectives are detailed below with notes in bold.

to protect the benefits of members of occupational pension schemes tPR has failed to do this and as a result of repeated failures over a period of more than fifteen years has facilitated the scamming of thousands of victims out of millions of pounds’ worth of occupational pensions and into millions of pounds’ worth of tax liabilities

to promote, and to improve understanding of the good administration of work-based pension schemes tPR made no effort to work with administrators and trustees of schemes such as Royal Mail; local authorities; the NHS, the Police etc., to help them improve their understanding of how to avoid transferring victims into scams

to reduce the risk of situations arising which may lead to compensation being payable from the Pension Protection Fund (PPF) Through multiple failings over a period of more than fifteen years, tPR has exposed the PPF to huge amounts of compensation claims. This is paid for by the ethical, compliant sector of the financial services industry who are understandably deeply unhappy that they have to bear the cost of tPR’s negligence and omissions

to maximise employer compliance with employer duties and the employment safeguards introduced by the Pensions Act 2008 tPR has done nothing to ensure that occupational pension schemes have a bona fide employer that either trades or employs anybody – or even exists at all

One thing which tPR omits to state as being one of its obligations or objectives, is to take action to prevent pension scams in the first place by carrying out due diligence on the trustees, administrators or sponsors of a scam before registering it. In fact, it is clear from evidenced facts, that what should have been simple common sense in terms of basic, obvious vigilance and diligence, was not done. No questions were asked; no checks were made; no basic suspicions were raised. There is no evidence that anybody at tPR ever had the intelligence to ask questions such as whether schemes repeatedly administered by Stephen Ward or his accomplice Anthony Salih and registered to 31 Memorial Road posed any risks to the public.

Over the past couple of years, numerous “whistle blowing” reports have been made to tPR by members of the Class Action but they have been studiously ignored. At a meeting in April 2015, tPR were invited to work with (rather than against) the Class Action, but this too was ignored. Also at this meeting, the Capita Oak case was discussed. The Insolvency Service subsequently wound up the trustee of Capita Oak, Imperial, but tPR has taken no action to protect the members’ interests and has left 300 victims facing the loss of £10.8 million worth of pension transfers which were 100% invested in Store First store pods (now arguably worthless). The Henley and Westminster victims are facing a similar fate with zero intervention by tPR.

In 2014, evidence of Stephen Ward’s pension scam portfolio was handed to HMRC – including numerous occupational schemes and a pension trustee company: Dorrixo Alliance (registered at 31 Memorial Road, Worsley). However, neither HMRC nor tPR carried out any due diligence to see how many scams were under the trusteeship of Dorrixo and the toxic London Quantum scheme slipped through yet another gaping hole in the net, leading to dozens of victims losing £ millions of pension funds (including final salary ones).

Reverting back to 2010 when the most damning of tPR’s multiple failings started, hundreds of people were left to be scammed into the Salmon Enterprises scheme with no warnings by tPR that the administrators were under investigation for fraud, and thousands of people were left to be scammed into the various Baxendale-Walker and KJK Investments schemes. Along with Ark, 2010/11 alone accounted for well over a quarter of a billion pounds’ worth of pension fund losses and crippling tax liabilities. And this excludes the dozens of scams still being run by Stephen Ward to this day and which tPR continues to ignore. In fact, it has recently been reported that pension scams are by now accounting for over £10 billion worth of losses so the 2010/11 figure may well be substantially higher in reality.

The Pensions Regulator’s plans to start regulating

The Pensions Regulator has sent out a clear message in the Johnsons Shoes case where an employer failed to comply with its legal obligations regarding workplace pensions:

This was clearly the right course of action for the regulator to take and will both encourage some employers to be compliant and discourage others to avoid compliance failures.

But here is a curiously anomalous situation: I can find no evidence that the company just fined £40k by the regulator has ever scammed thousands of victims out of millions of pounds’ worth of pensions and left them with crippling tax liabilities. Many of these victims have had heart attacks and strokes as a result of the stress of being scammed. The employer, Johnsons Shoes, sanctioned by tPR, has been in business for 25 years and it is possible that one or two customers might have experienced the odd blister if the hand-made shoes were too tight. But my search for skeletons, scams or scandals came up with nothing more serious than the fact that they can’t spell the word “paid” on their website.

A little birdie has tipped me the wink that LaLa has had a quiet word in TinkyWinky’s shell like and told him that now he has got a taste for a spot of regulating, he really ought to up his game and sanction some of the outright scammers (i.e. criminals). There is a touch of embarrassment now that a long-established family business has received such a high-profile and high-value fine, while the worst sanction that has ever been handed out to criminals is the odd flaccid waggle.

Tinky Winky’s first dilemma is how to catch the scammers. Shoe shops are easy because they don’t tend to fly away to exotic places like Gibraltar and Malta but stay neatly sandwiched between a travel agent and a book store. The Insolvency Service very helpfully named 18 of the scammers in the Capita Oak, Henley and Store First SIPP investment scams which cost over 1,000 victims over £100 million worth of pensions plus tax liabilities. And I am sure all these criminals will be relatively easy to find in their various magnificent country mansions.

Once caught, the next dilemma will be to work out how much to fine them. My suggestion would be to simply divide £100 million by 18 – interestingly that comes out to £5,555,555.55 each. On top of that, the scammers should be made to pay the victims’ tax liabilities.

Speed is now of the essence to avoid the embarrassment that it took the Pensions Regulator more than four years to ban 5G Futures trustees Williams and Huxley and that the only action ever taken against Stephen Ward was a “severe dressing gown”.

If the shoe fits….

Tinky Winky has got to realise why there is the word “Regulator” in the Pensions Regulator – and if the shoe fits, he has got to wear it.

Another reason for the urgency of taking some long-overdue action against the criminals, is the part played in the financial ruin of so many thousands of victims by tPR itself. 14 Ark schemes, now in the hands of Dalriada Trustees, were registered by tPR; Capita Oak now in the hands of Dalriada Trustees, was registered by tPR; Westminster now in the hands of Dalriada Trustees, was registered by tPR (and tPR failed to spot that both Capita and Westminster shared the same non-existent sponsoring employer); London Quantum, now in the hands of Dalriada Trustees, was registered by tPR and its trustee was Stephen Ward who was behind Ark, Capita Oak and Westminster…….etc. etc.