International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors Old Mutual International, or a marketing machine. I read with interest the recent IA Industry Most Influential Top 100 described by IA thus: “we at International Adviser decided to shine a light on the movers and shakers that have helped this industry get to where it is today”.

But where exactly is the industry today? And have the so-called top 100 moved and shaken the industry in a helpful way or a detrimental way? To find out, why don’t we have a look at a few of the “influencers”. To get the measure of them, let’s put them into a game of “Have I Got News For You”:

Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based Investors Trust until recently appointed chair of the Association of International Life Offices, the trade body for international life offices. During his 35 years of experience in financial services, he facilitated the scam run by Phillip Nunn of Blackmore Global and David Vilka of Square Mile International Financial Services. Investors Trust accepted over 1,000 investments into illegal UCIS funds for UK-based victims scammed into QROPS with Integrated Capabilities and Harbour (now STM).

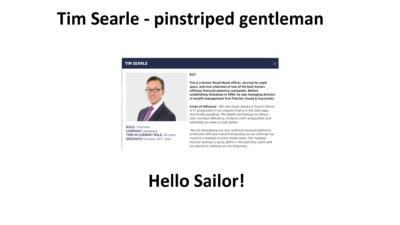

As Captain of the Navel Team, let’s have dashing Tim Searle – Chairman of Dubai-based Globaleye. With his eight-year Naval history, he should make an ideal leader and would come in particularly useful in the event of icebergs, torpedos or sharks.

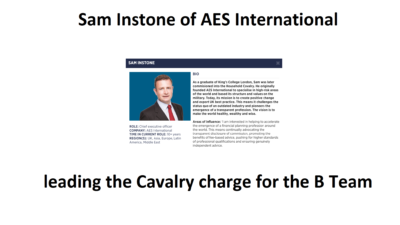

Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

On the Army Team, we’ll have international wealth and regulatory specialist, Phil Billingham. Phil must be utterly disgusted with the likes of Stephen Ward (another fully-qualified adviser) messing up the reputation of the profession by running a long series of pension scams and ruining thousands of lives.

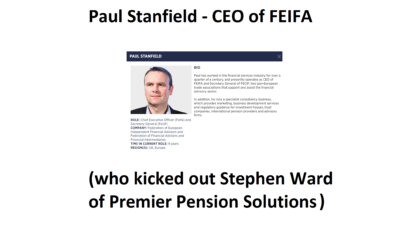

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated Stephen Ward of Premier Pension Solutions from FEIFA to loud cheers from victims and industry professionals alike. (My only gripe with him would be that he still hasn’t kicked out Square Mile Financial Services run by scammers John Ferguson and David Vilka).

On the Navel Team we’ll have Geraint Davies of Montfort International – an expert IFA specialising in international financial services, and Roger Berry of Concept Group Trustees in Guernsey. These two chaps also have, between them, extensive experience of Stephen Ward in their own ways and will, no doubt, have much to talk about.

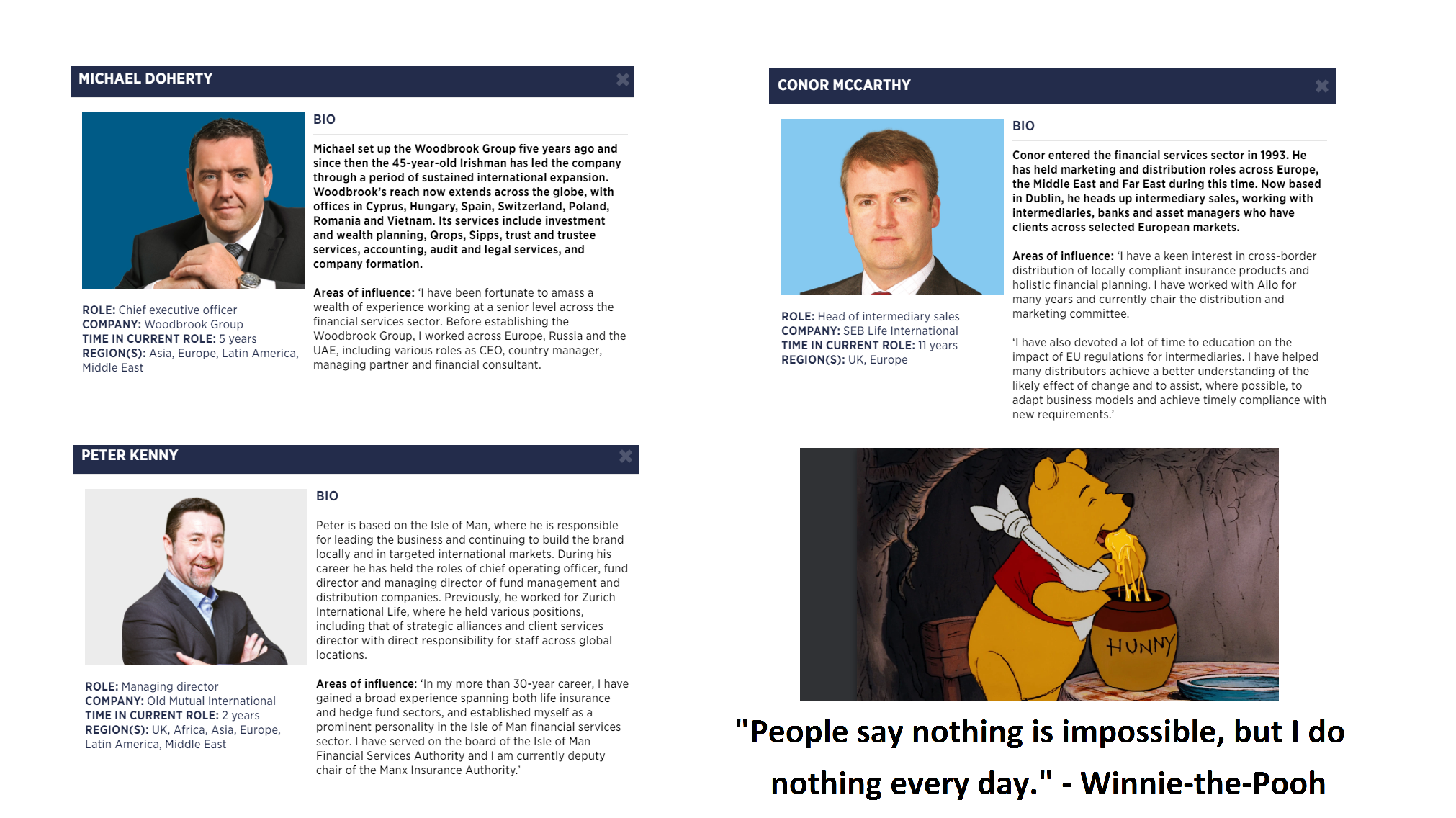

The contest will be to spot the “odd one out”: Michael Doherty of Woodbrook Group, Conor McCarthy of SEB, Peter Kenny of OMI and Winnie-the-Pooh.

Tim Searle: “They’re all Irish, except Winnie-the-Pooh who’s English?”

Geraint Davies: “They all hate Angie except Winnie-the-Pooh who’s never heard of her?”

Roger Berry: “They all love Angie except Winnie-the-Pooh who’s never heard of her?”

Sam Instone: “They’ve all got names that end in Y except Winnie-the-Pooh?”

Phil Billingham: “They’re all involved in money except Winnie-the-Pooh who’s involved in honey?”

Paul Stanfield: “None of them have applied to be members of FEIFA except Winnie-the-Pooh?”

Bob Pain: “No, you’re all wrong. The answer is Peter Kenny of OMI. The other three have been doing “nothing”: Michael Doherty was employing ex CWM scammers Dean Stogsdill and Neil Hathaway (known as Dog Kill and Hadaway) but claimed he was paying them nothing; Conor McCarthy of SEB has been asked numerous times for his comments on why SEB allowed the scammers at CWM to invest most of their victims’ funds in toxic structured notes, but McCarthy is saying nothing and won’t reply; and Winnie-the-Pool is doing nothing all the time.

The odd one out is Peter Kenny who is doing “something” and is suing Leonteq for the £94 million worth of fraudulent structured notes they sold to OMI.

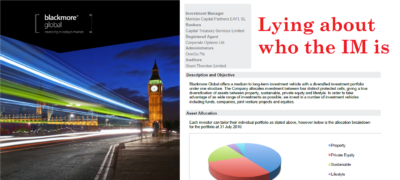

Integrated Capabilities – a Trust Company based in Malta have created their own Pension Scheme – Azure Pensions. On the face of it, however, the management team do not appear to have learned anything from their previous experience with Optimus Retirement Benefit Scheme No.1 and their association with David Vilka of Square Mile International Financial. It appears they have now teamed up with some very dubious friends – the result of which is very likely to create more victims of UK pension scams.

I AM GRATEFUL TO STEVE – ONE OF THE BLACKMORE GLOBAL/DAVID VILKA VICTIMS – FOR RE-WRITING THIS BLOG AT THE REQUEST OF INTEGRATED CAPABILITIES’ LAWYER.

The Azure website states: “We believe that trust is built and earned. As such we have an ingrained and sustained desire to develop long-term relationships with our clients”. These are just words and words are easy. It’s what you do that counts.

In 2015, the Optimus scheme started out with 26 members and by the end finished up with 1,176 – that’s a gain of almost 100 new members per month! I was one such member conned into transferring my pension by fraudulent misrepresentations made by David Vilka of Square Mile Financial Services.

This new pension arrangement locked me in for 10 years – definitely a “long-term relationship” – giving all parties the opportunity to drain my pension dry in fees. Credit where credit is due, however. Once I discovered I was in a scam, the director Andy Dawson (bottom row, 3rd from the left) did make an extraordinary effort not only to redeem the investments but successfully persuaded most parties to waive their early exit penalties and refund their fees. Only the greedy Symphony Fund chose to keep the penalties and that’s after mysteriously dropping in value 30% just before redemption. Thanks to Andy Dawson and his team, I did manage to get back 92% of my pension. But the BIG QUESTION is what has happened to the other 1,100+ members? It is inconceivable I was the only one transferred into this scheme via Vilka et al.

Another claim made by Azure Pensions is: “Our people are highly experienced, knowledgeable and motivated to do their utmost to ensure that they deliver a superior, professional and hassle-free service.” But this firm, and the people in it, have a history of working with scammers and investing members’ retirement funds in investment scams such as Phillip Nunn’s Blackmore Global and Richard Reinert’s Symphony Fund. So I would take issue with claims like “highly experienced” and “knowledgeable”.

If they were highly experienced and knowledgeable they would have known that, at the time I was being advised by Vilka in January 2015, Aktiva Wealth Management (later changed to Square Mile and now called Michalska Holding) was NOT regulated by the Czech National Bank. According to the CNB records, this didn’t happen until 5th May 2015 and then, only for insurance mediation and not for transferring pensions!

If Integrated Capabilities had been “highly experienced and knowledgeable” then they would have known the Symphony Fund – regulated in their own jurisdiction by their own regulator, the MFSA – was NOT permitted to be offered to me, a retail client. And they knew this because they had the Symphony documentation which clearly prohibited its promotion to UK retail clients.

I complained to the MFSA but they didn’t care and Malta’s “Ombudsman” equivalent – what they call the Office of the Arbiter for Financial Services – deters complaints because they have this small print that says if you lose, the other side can be awarded legal costs!

If Integrated Capabilities had been “highly experienced and knowledgeable” they would have known the Blackmore Global fund had never published audited accounts and still hasn’t to this day (December 2018). Something that in January 2015 caused Kreston (pension provider on the Isle of Man) to write to its members explaining their concerns over Blackmore Global and also stopped taking new members from Vilka.

So if they were “highly experienced and knowledgeable” then why did they allow all this to happen? It certainly had nothing to do with “motivation to do their utmost”. It is clear their only motivation was to take on as many members as possible – irrespective of which scammer introduced them and what unsuitable investments were made for them. Also, they claim to have a “long history and proven track record of providing expert and value for money multi-jurisdictional fiduciary solutions, so our clients and partners can have great peace of mind in the knowledge that our board of directors has over 100 years combined expertise in this field.” The proven track record is that they have taken on hundreds of new members per month from a known scammer – and the last thing their members have is peace of mind – far from it.

Angie has referred to these people at Integrated Capabilities/Azure Pensions as a “bunch of cowboys” and their lawyer recently wrote to her and objected to the phrase. You make your own mind up.

How do they earn trust when they have accepted transfers and investment instructions from known unregulated scammers Square Mile and David Vilka? Why would victims “desire” to have a long-term relationship with Azure when funds were previously placed in an unnecessary, expensive insurance bond by Investors Trust in the Cayman Islands (the only purpose for which is to pay commission to the scammers)?

Azure Pensions also claims that one of its partners is Carey Pensions UK LLC. Carey is facing a legal battle for investing a member into unregulated collectives in Australia through a Carey Pensions SIPP.

Carey is in hot water for allowing investments into high-risk scams, and is also now part of STM – undoubtedly the biggest scammers in the offshore pension trust industry. It would seem the Azure team have not learned anything from their previous experience.

If, as they say “We believe that trust is built and earned …”, then you actually have to do some “trust building” with actions – not just weasel words. The indisputable facts seem to indicate “business as usual” but with a different name.

It is highly probable that Integrated Capabilities still has at least 1,100 victims invested in scam funds such as Blackmore Global by scammers such as David Vilka of Square Mile. It looks like most – if not all – of these victims were UK residents who should never have gone into a QROPS at all in the first place. The only reason for transferring these pension funds to a QROPS was to get the money away from UK regulation so that the scammers could invest them in commission-paying UCIS funds – such as Blackmore Global.

The public should be very wary of Azure in the first instance, do a lot of due diligence and make sure their pension funds don’t go anywhere near offshore unregulated collectives wrapped in an assurance bond that can suck your pension dry.

Azure states on their website that: “Notwithstanding your appointment of a Financial Adviser, ICML has an overriding right to refuse to make investments, or to disinvest, where it believes that a particular investment proposal may not be consistent with the Scheme’s Investment Policy or any investment restriction applicable under Retirement Scheme Law.”

Is this a change in policy? Are they going to put their “knowledge and experience” to meaningful use by exercising some due diligence? Is this a statement that means they have sorted the 1,100+ members in the Optimus Scheme that are most likely locked into “investments … not consistent with the Scheme’s … Policy?” Or are these just more weasel words with no substance?

Reformed management team or a “bunch of cowboys”? The jury is still out. The association with Carey & STM doesn’t appear to show a reformed team. What has happened to the 1,100+ members in the previous Optimus Scheme? Has anything been done to remedy the situation?

I believed, and still do, that this team was unwittingly drawn into facilitating a scam by David Vilka of Square Mile, and that in essence Integrated Capabilities/Azure Pensions are a respectable team. However, if they want to be seen as having learned from their past failings they could take some actions. First, help the 1,100+ members to avoid financial ruin and secondly assist in the prosecution of the architects of the scam facilitated by Integrated Capabilities. I am sure they will have a considerable body of evidence that could be used to show fraudulent misrepresentation and thirdly drop the association with companies with an already poor reputation for their involvement with scams or unregulated collectives being promoted to retail clients.

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders:

The life offices take business from any old known scammers – firms without proper licenses and with a known history of defrauding the public

The life offices will offer toxic, illiquid, risky funds – including UCIS funds – such as LM and Mansion on their platform (without doing any proper due diligence as to how quickly these funds can eradicate the life offices’ victims’ life savings)

The life offices will accept investment instructions from unqualified scammers who work for firms with no investment license – and, in some cases, with no insurance license either

The life offices will accept dealing instructions – often with fraudulently-copied or forged signatures – on dealing instructions for toxic assets such as professional-investor-only structured notes

A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

Mr. S’ pension fund was then placed in a “life bond” with Investors Trust in the Cayman Islands. This was an entirely gratuitous transaction, as he had absolutely no need of such a bond – known to be a spurious life assurance policy used for what is called a “single premium” insurance contract. These bonds are illegal in Spain, since the Spanish Supreme Court has ruled that they are being used to hold investments in contravention of the nature of what insurance is supposed to be (i.e. risk for the insurer).

The entire fund – which represented Mr. S’ retirement savings – was then invested in two toxic UCIS funds (illegal to be promoted to UK-resident, retail investors) called Symphony and Blackmore Global. Investors Trust negligently accepted these investments from Square Mile – in the full knowledge that this was absolutely against the interests of the policyholder and that the “advisory” firm had no investment license.

After a protracted battle, waged with great tenacity and dogged determination, Mr S did indeed get back a large proportion of his fund. But he still suffered what can only be described as a harrowing experience which resulted in a total loss of a significant chunk of his pension to the scammers (who will have profited handsomely from scamming him in the first place).

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer Douglas Davies of Lowell Davies LLP.

But what of the Cayman Islands-based life office – Investors Trust? Did they try to help Mr. S recover his serious losses? Did they offer him compensation for the significant distress he suffered at the hands of the scammers at Square Mile? Did they publish a statement demonstrating recognition of the damage done to victims’ life savings by investing in toxic crap like Blackmore Global on the instructions of scammers like David Vilka?

The answer, of course, is a resounding “no”. Investors Trust could have done so much to reform these illegal practices and expose the likes of scammer David Vilka who scammed not only Mr. S out of a big part of his pension, but also scammed hundreds of victims into the Hong Kong QROPS scam (many of which got invested in Blackmore Global).

Instead of showing any contrition or regret for facilitating financial crime, an idiot at Investors Trust called Lindsay Paris emailed me threatening to sue me for using a picture of David Vilka and John Ferguson posing as vulgar spivs at Las Vegas. This revolting photograph is, apparently, the property of Investors Trust:

“This is my second attempt to reach you regarding the copyright infringement on your website. Please have the image removed immediately or we will have no other choice but to seek legal action.

This is not the first time you have fraudulently misused private images and copyrights without authorization. You are imposing on our ownership rights and we would appreciate it if you would refrain from any future use of Investors Trust-owned materials. It is a serious violation which we will continue to pursue.

Lindsay Paris, Media and Communications Manager, Investors Trust Administration

lparis@investors-trust.com”

So, no apology for destroying victims’ life savings; no apology for taking business from a firm which was not regulated to give investment advice; no apology for investing a victim’s pension in a toxic UCIS fund run by known scammer Philip Nunn….just a complaint about a violation of their ownership rights of a picture of the scammers bearing the Investors Trust logo.

It is reported that Old Mutual International has put aside £69 million to pay compensation for their victims’ losses. May I suggest that Investors Trust should do the same thing – and then I will happily take down the vile picture of Vilka and Ferguson. But until then, it stays up. And if you want to sue me – go ahead: make my day.

David Vilka of Square Mile International Financial Services has exactly the sort of lawyer one would expect: a scammer’s lawyer. Unsurprisingly, this dope can’t even spell Vilka’s victim’s name and has referred to him as “Mr Sexton” as opposed to “Mr Sefton”. But, again, this is no surprise.

What I must challenge, however, is the fact that Mr. Sefton has referred to this clown as a “two-bit lawyer”. I really don’t think this is true – as he is a one-bit lawyer at best. He has a couple of glowing client testimonials going back to 2016 and 2015 on his amateurish website, and displays no evidence of experience or expertise in the arena of British pensions (and why would he? – he’s purportedly practising US law in the US).

One might forgive Mr. Davies for not understanding anything about UK pensions in general and pension scammers like David Vilka in particular, but to immediately jump into a firm conclusion that there has been defamation against his client shows that he hasn’t even made a one-bit attempt to understand what his client has been up to – or how many lives (like Mr Sefton’s) Vilka has ruined.

I must admit I am used to dealing with a much better class of scammers’ lawyer. Take DWF, for example: this large firm carelessly lost a team of 20 lawyers to rival Trowers and Hamlins a couple of years ago. This wasn’t long after they were caught representing both sides in a case: the Insolvency Service in the winding up of Capita Oak, and Stephen Ward who handled the transfer administration in the same scheme. But at least they dealt with the embarrassment of acting for both the poacher and the gamekeeper with a degree of dignity and elegance – a class act indeed. DWF comes into the same league as my other legal chums – including Carter Ruck and Mishcon de Reya. So, you can see I am more used to dealing with professional firms rather than twerps like this Mr Davies.

Mr. Davies is referring to the UCIS investment scam, Blackmore Global, which was illegally promoted to retail investors – and which is a fraud from start to finish.

Anyway, I have answered his absurd email below with my usual comments in bold.

————————————————————————————————-

LOWELL DAVIES LLP

July 14, 2018

Ms. Angela Brooks, Director of Pension Life

Re: Defamation of Mr. David Vilka and Square Mile International

Dear Ms. Brooks:

I am an attorney You may well be, but you are clearly a US attorney – and that does not qualify you to deal with a matter which involves UK pensions

and represent Mr. David Vilka Bad luck

with respect to the defamatory article I never write defamatory articles – I only write the truth

published on your on-line site. Specifically, this complaint relates to the misstatements and misrepresentations made on

If I might sum up, each and every defamatory allegation with regard to Mr. Vilka and Square Mile International you assert are sourced to one disgruntled individual, Stephen Sexton, none of which allegations are supported by any evidence whatsoever. Wrong. Mr. Sefton is one of a number of victims of Vilka’s scams – many of which were invested in the same toxic, illegal UCIS fund as Mr. Sefton – Blackmore Global – and others were invested in other similar investment scams. Blackmore Global is run by another scammer, Phillip Nunn, who – along with his partner in crime Patrick McCreesh – ran the cold calling and lead generation services for the Capita Oak and Henley pension scams, now under investigation by the Serious Fraud Office.

Mr. Sexton was an unsolicited client of Mr. Vilka and Square Mile who had a substantial pension and for personal reasons of his own wanted to switch his pension and draw down sums for his personal use. When he says “unsolicited” he means not cold called, as was usually the case with Vilka. Vilka lied about being regulated to provide pension and investment advice, and the rest is history: Mr Sefton’s life savings were invested in two UCIS funds which were habitually promoted by Vilka: Blackmore Global and Symphony.

The switch in pension plans resulted in what Mr. Sexton felt were unreasonable fees (None of which went to Mr. Vilka or Square Mile). I wonder if this idiot would like to explain why Mr Sefton was put into a QROPS when he was a UK resident?

And despite the fact that Mr. Vilka was able to personally intervene and get Mr. Sexton’s monies returned less a nominal fee, Mr. Sexton continued to complain and when Square Mile attempted to make up even this nominal fee on its own part, Mr. Sexton continued to complain because he refused to sign a boilerplate settlement agreement containing a standard confidentiality agreement. It is true that Mr Sefton did, eventually, get around 85% of his original investment back – but only after a dogged fight which was backed up by the pension trustees Integrated Capabilities. There was no intervention by Vilka.

In your post on the Blackmore Fund you have the temerity to cast defamatory aspersions on Mr. Vilka and Square Mile based on your “strong suspicion” and you go on to assert they must have a “strong vested interest in promoting this black hole of a fund.” Why else would scammers such as Vilka promote such a fund? It is a UCIS, with no independent audit to verify whether the purported assets even exist.

Really? What proof of that would you have? Vilka must have had a very strong reason to promote the Blackmore Global investment fraud – why else would he have invested a further 64 victims’ pensions in this UCIS? This was a bunch of people he scammed into transferring their pensions to a Hong Kong QROPS.

And since you have none, we demand you remove this article and/or any reference to Mr. Vilka or Square Mile. I have plenty of evidence thank you.

Let me advise you that Mr. Vilka and Square Mile, contrary to your specious aspersions, are heavily regulated as is the industry. “Heavily”? What you actually mean is that neither Vilka nor Square Mile is regulated for pension or investment advice – only insurance mediation.

The Sexton matter was thoroughly investigated at the time by the appropriate regulators who found no irregularities. You don’t know that.

Mr. Sexton is not nor was he a perplexed victim of Mr. Vilka or Square Mile. He most certainly was – as Vilka and his accomplice John Ferguson know full well.

His pension is worth well over half a million pounds. No it isn’t. Did you do maths at school?

He read and signed multiple acknowledgements before he switched pensions showing very clearly that he knew what he was investing in and the inherent risks involved. No he didn’t. It was never disclosed that the scammers were going to invest his pension in a UCIS fund which is illegal to be promoted to retail UK investors.

And again, significantly, he was not cold-called. He sought out Mr. Vilka and Square Mile. Nor did Mr. Vilka or Square Mile receive any payment from the Blackmore fund or its partner firms regarding Mr. Sexton’s transaction as confirmed by the Czech National Bank which has direct access to Square Mile’s company bank accounts via an electronic data box. Are you talking about the accounts which haven’t been updated since 2014?

In sum, there is no bases whatsoever for the specious and actionable statements you make in your referenced post with regard to Mr. Vilka and Square Mile International. I think you mean basis – and yes, there is a solid basis for all the statements I made in my post and not a single one of them is “specious” (although I am amazed you have even heard of the word).

Your comments have caused Mr. Vilka and Square Mile reputational damage, among others, and you are hereby instructed to delete the post immediately. I sincerely hope that the impact of my blog has caused Vilka and his accomplice Ferguson to turn over a new leaf and arrange to pay compensation for Mr. Sefton and all their other victims who have lost part or all of their pensions to the Square Mile scams.

Your failure to do so will result in further damages to Mr. Vilka and Square Mile International, the accrual of further legal fees and costs, and the likelihood of litigation, all of which damages and costs we will recover from you. Good luck with that.

If you have any questions or concerns or require further information, please don’t hesitate to contact me directly at (206) 319-3533. I look forward to confirmation of the removal of the identified defamatory materials. Thank you in advance for resolving this matter expeditiously. I have no questions, other than to enquire as to when your client intends to pay redress for the losses caused by his fraud.

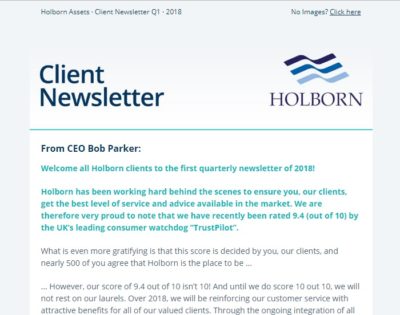

Seems we can´t get enough of Holborn Assets’ cheek this week. CEO Bob Parker has sent out a Q1 2018 newsletter and included on his mailing list a very unsatisfied and traumatised client who, through Holborn Assets’ negligence, has suffered a significant loss to her pension fund, with no compensation – or even apology.

Glynis Broadfoot was a victim of Holborn Assets’ rotten advice and service in 2011 and which resulted in her losing a significant portion of what had originally been a final-salary pension which should never have been transferred in the first place. Holborn Assets refused to help her, and simply kept taking their extortionate fees from her ever-shrinking pension pot. They had invested her in high-risk, professional-investor-only structured notes which were totally inappropriate for a low-risk investor.

You can imagine Mrs. Broadfoot’s fury and disgust when this message popped up in her inbox.

In summary, despite the expensive advice given to Mrs. Broadfoot by Holborn Assets, and assurances that her pension would grow at 8% per annum, she ended up losing nearly a third of her fund. Despite the fund’s losses, Holborn Assets continued to apply their fees to the fund, totaling somewhere in the region of £11k!

Holborn Assets informed her, at the height of her distress over her losses, that they “had closed the case, and would not enter into any further correspondence”.Yet now, several years on, it appears she’s still on their mailing list – despite knowing full well they have left this victim’s retirement prospects in tatters.

Mrs. Broadfoot’s case was typical of “fractional scams“: expensive and unnecessary insurance bond (only purpose was to pay a fat commission to the scammers); expensive, high-risk, professional-investor-only structured notes (again, high commissions for the scammers and heavy losses for the victim); hefty advisor fees. This was a very obvious scam which caused great suffering for the victim who is resident in Spain – but Holborn Assets was not licensed to provide investment advice in Spain.

In the years since Mrs. Broadfoot was scammed, Bob Parker did start to engage half-heartedly with a process of negotiating compensation for her losses. But so far she has not received one penny. Her local government final salary pension scheme – which she was conned into sacrificing by these unlicensed scammers – would have provided her with a guaranteed, index-linked pension for life and she could have retired comfortably. Instead, she has a seriously damaged fund which is unlikely to ever recover and provide her with the retirement income she needed and deserved.

So, far from getting the “best level of service and advice available” as boasted by Bob Parker, Mrs. Broadfoot was conned, scammed, fleeced and then dumped by Holborn Assets.

Which brings me on to the Trust Pilot reviews. Only 2% scored Holborn Assets as average or poor. Which is very surprising – given the number of people who report similar stories to Mrs. Broadfoot’s. But I think it is likely that those who gave four or five stars, haven’t yet found out what their losses are. In fact, some of these reviewers admit they were cold called by Holborn Assets. We know for sure Claudia Shaw was flogging the high-risk Premier New Earth Recycling UCIS fund to her victims and that there have been heavy investment losses.

I don’t believe anyone from Holborn has contacted me since September last year. In August 2016 I was contacted and advised to switch my policy which seemed ridiculous considering the additional charges I would incur, the fact it was even suggested causes me concern.

Then in September 2016, I was contacted to recommend my wealth manager for an award, again the audacity of this makes me wonder.

I have no idea on what your investment performance to date is over the past 12 months and I have not been given any confidence how my investments will be managed going forward now that I have finished paying your fees and Iactually begin to get money invested.

I do plan to visit within the next month and hopefully by that stage you in a position to assure me I did not make a big mistake investing my money with you. Regards Ian Norton

Another victim has complained directly to Pension Life about the appalling treatment he has had at the hands of Holborn Assets:

“Since 2013, the fund has not done anything at all. The fees are much too high, excessive transactions have been made to earn themselves money on my account and the investments went down in value. There is no communication with Holborn Assets and they are unwilling to discuss this matter with me or to do anything about it.”

So, as the cheeky Bob Parker is aiming to infiltrate South Africa with his new weapon – the bright-eyed and bushy-chinned Lourens Reichert – I thought now would be a good time to make friends with Reichert and see if he can put some pressure on Uncle Bob. Reichert will, no doubt, be very pleased to help me sort these victims out – as he has a big bulging lump in his trousers courtesy of Bob’s golden handshake.

I might even nip down to Johannesburg and have a cup of tea and a cheeky biscuit with him. No doubt, he won’t want the sordid details of Holborn Assets’ scams to compromise his quest to conquer South Africa. If the natives find out just what his colleagues have been up to, he might find himself on the wrong end of a Zulu spear.

John (Gus) Ferguson’s firm, Square Mile International, is clearly not exactly square – and Lillywhite is a grubby shade of black.

For once, I don’t have to write a blog myself – as Mr. Ferguson of Square Mile has written it for me. I did, however, have to resist the temptation to correct Fatty’s appalling grammar and spelling.

Fatty’s partner in crime is, of course, “adviser” David Vilka – who put retail, UK-domiciled victims into QROPS and then invested most or all of their pensions in Nunn and McCreesh’s toxic, illiquid, high-risk Blackmore Global fund.

So, if you have ever wondered how to promote unregulated toxic crap to pension savers, read on…..

Hi – yes good to meet you too, and glad you had a safe trip back.

As you said it would have perhaps been nice to have longer with you and we both felt there was areas in which we could work together and once we are all back from our various holidays no doubt we will be looking at ideas that we could explore together.

We intend to be in Dubai at end of November and have a busy schedule (already) so wouldn’t be able (this time) to build in a HK detour but if you are able to be in Dubai that time then perhaps it could be a good opportunity to spend longer discussing opportunities.

The relationships with our Introducers as we explained is relatively straight forward but to recap – Lillywhite International acts as a ‘hub’ co-ordinating the flow of business between ‘introducers’ (unregulated and unauthorised entities such as Manish’s operation) who are often looking to fund their own product (again such as Manish and Christianson) and the regulated IFA firms, and the Pension Trustees.

I think confusion probably lies in that historically GFS could take direct business or business from unregulated firms. In the UK for some years now, it has not been possible for a firm such as Manish’s or Aspinal Chase etc to give advice, get information from a ceding scheme, submit business to a QROPS or to earn fees from anything that could constitute ‘a regulated activity’ under the FSMA.

Lillywhites controls a number of regulated IFA firms, and has string links with Life Offices (providing bond wrappers) and Trustees (providing QROPS).

We offer a service to the Manish’s / Aspinal Chase’s of the world and our IFA’s will sign off the business, provide the advice, deal with the pension and invest a proportion of the fund into the investments these introducers are trying to raise subscriptions on. We have bespoke Bond arrangements at NIL commission to comply with RDR in the UK, and the funds don’t pay the IFA any commissions – again to comply with RDR.

In terms of fees etc, I’m sure in the same way your agreements are private we have various agreements with our introducers and they are confidential.

So as i said relatively open and simple relationship – nothing can be submitted to our panel of QROPS without being signed off by our IFAs and so EVERY piece of business you receive from these guys is actually via a Lillywhites Adviser – The majority will be via either Aktiva Wealth Management or Square Mile International.

Where i do think we could have a very serious chat is using your distribution in Asia for a couple of funds that we can split the distribution fees with you on, and thats definitely where id like to have a further discussion. our two main brands are www.atsgfunds.com and www.lillywhiteint.com

Speak soon

Gus

*****************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Quilter – Old Mutual International – new name to try to hide past crimes

QUILTER – A NEW HOBBY FOR OMI? OMI – Old Mutual International – needs to compensate thousands of victims of financial crime which they facilitated. I can’t make up my mind whether they are adopting the brand “Quilter” to attempt to shake off their sordid and toxic past, or whether they are actually taking up quilting.

If OMI really is going to become a quilter, it needs to make a quilt depicting all the criminals whose crimes it has facilitated for so many years. And all the victims who have lost part of or all of their life savings.

What OMI really needs to do is to get firmly behind the prosecution of the criminals – from whom they profited for many years. OMI must contribute to the cost of denouncing these criminals and ensuring they are given maximum prison sentences.

Also, OMI – Old Mutual – must stop allowing toxic, professional-investor-0nly structured notes in their bonds. Typically, these were provided by Commerzbank, Nomura, Leonteq and RBC. If Old Mutual International wants to gamble away its own money on these crap products, then be my guest. But don’t expose retail pension savers to these sordid, high-risk instruments – used by the scammers as mere tiles in a game of Scrabble.

Al Rush championing the British Steelworkers who have been scammed

Al Rush has suggested the wording which victims can use to report those who scammed – or attempted to scam – them. And all of what Al and his colleagues have done has been done at their own expense and out of a sense of decency.

Hard to tell the difference between OMI and Quilter and Jabba The Hut

This is in stark and stinky contrast to OMI – Old Mutual International. Since 2011, OMI has sat and watched – like a cross between Jabba The Hut and a Black Widow Spider – while thousands of victims have seen their life savings dwindle away to very little or even nothing. And all the while, taking extortionate fees and paying commissions to the very scammers who ruined the victims in the first place.

So does OMI really think that adopting the name “Quilter” will make future victims fail to make the connection – that this is the same firm that took business from dozens of unregulated scammers such as Continental Wealth Management, Abbey Financial Solutions, Holborn Assets, Guardian Wealth Management, and other “chiringuitos”?

Perhaps the worst crime committed by OMI is not that they took business from unlicensed scammers; not that they allowed 100% of victims’ pension funds to be invested in professional-investor-only, high-risk structured notes; not that they sat there idly and negligently while the clients’ pensions and investments shrank inexorably……

Old Mutual International – the rubbish end of financial services

the worst of OMI’s crimes has been that when there are only a few crumbs left of a life-time’s retirement savings, they will still charge crippling early-exit penalties. OMI, or Skandia, or Quilter or Jabba The Hut or whatever the hell this toxic, evil shower call themselves, have no place in financial services. They have facilitated and profited from financial crime for years and benefited from the misery and ruin of thousands of victims.

In an attempt to emulate Al Rush’s suggested police report for British Steel victims at the hands of the various scammers who targeted, stalked and scammed them, here is my suggested report for OMI victims to make to the police and the regulators. Naturally, this will work equally well for victims of Generali, SEB, RL360, Friends Provident, Hansard, Investors Trust etc.

OMI must be sanctioned for facilitating financial crime

‘I was advised to transfer out of my personal/occupational (delete as appropriate) pension scheme and was lied to when I asked about how much money would be taken from me. I think, over time especially, I will lose/have already lost many tens of thousands of pounds (probably, hundreds of thousands of pounds) in fees which were hidden from me.

This will bleed my pot dry, leave me exposed to poverty in old age and create a burden on the local council.

I was specifically told there would be no penalties or lock-in periods.

Can you help me please, I would like to make a formal statement and help you bring charges against those who did this, and those who helped them’.

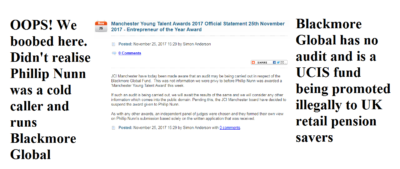

Pension Scammer Phillip Nunn receiving an award for “Entrepreneur of the Year”

Phillip Nunn has been reported to Action Fraud – which John Ferguson of Square Mile Financial Services describes as being “nobody and with no authority” – on numerous occasions by victims of various scams.

Phillip Nunn, cold caller and “fund manager” of the Blackmore Global investment scam, was given the Entrepreneur of the Year Award by JCI Manchester, but this was reversed shortly afterwards:

“JCI Manchester have today been made aware that an audit may be being carried out in respect of the Blackmore Global Fund. This was not information we were privy to before Phillip Nunn was awarded a ‘Manchester Young Talent Award’ this week.

If such an audit is being carried out, we will await the results of the same and we will consider any other information which comes into the public domain. Pending this, the JCI Manchester board have decided to suspend the award given to Phillip Nunn.”

MYT Phillip Nunn Award Retraction

“An independent panel of judges formed their own view on Phillip Nunn’s submission based solely on the written application received.”

I would love to read Phillip Nunn’s submission. It would certainly make very interesting reading. I doubt it would have included the fact that Nunn and his accomplice Patrick McCreesh were cold callers and lead generators in the Capita Oak/Henley Retirement Benefits/multiple SIPPS/Store First scam – which led to well over 1,000 victims losing over £120 million worth of pensions.

The Insolvency Service produced a witness statement which stated:

“Members of CAPITA OAK indicated they were initially contacted by Craig Mason or Patrick McCreesh of Nunn McCreesh of Its Your Pension Ltd and offered pension review services prior to them being referred to JACKSON FRANCIS or Sycamore for the transfer of their pension to CAPITA OAK.

On 3.3.15 I received an undated letter in which it was stated that Its Your Pension had not traded and was a dormant company and that Nunn McCreesh had traded as an insurance brokerage between 2009 and 2012 when they entered into a verbal arrangement with TRANSEURO where in return for providing pension leads to JACKSON FRANCIS they received a commission from TRANSEURO.

Nunn McCreesh provided JACKSON FRANCIS with 100-200 leads per month which were provided by email and/or telephone for which they received £899,829.86 from TRANSEURO during the period 26.3.12 to 14.5.14.”

Phillip Nunn’s lawyers, Slater and Gordon (funny that, also nominated for an award) tried to claim that Nunn McCreesh’s involvement in the Capita Oak scam was “minimal”. But I wouldn’t describe generating 5,000 leads, cold calling thousands of victims and being paid nearly £900k “minimal”.

On the subject of Slater and Gordon, earlier this year they threatened me with defamation proceedings for exposing Nunn’s scamtivities. It was curious that they couldn’t see any conflict of interest in representing Phillip Nunn when they were also representing the very victims (of Capita Oak) whom he had cold called in the first place.

Slater and Gordon’s Steve Kunziewicz claimed that “Blackmore Global is a prestigious, multi-asset investment house with over £60 million in assets under management, offering institutional and high net-worth clients access to a wide variety of investment products in order to maximise their returns.”

But there is no audit for Blackmore Global and only evidence suggesting the fund is invested in toxic, high-risk, illiquid crap including:

Swan Holding PCC

Kingston Capital Partners (Belize private equity vehicle controlled by Nunn & McCreesh)

GRRE Invest

Spinaris 90 ( UK sports spread betting)

The Blackmore Global audit was promised more than a year ago but never materialised. The audit has now been promised “by the end of the year” – but Grant Thornton won’t specify which year.

However, far from the Blackmore Global fund being aimed at “institutional and high net worth clients”, Phillip Nunn targets low-risk pension savers using a variety of unregulated so-called “advisers” such as David Vilka of Square Mile Financial Services. Many of the Blackmore Global victims were cold-called and/or introduced by Phillip Nunn’s cold-calling outfit, Aspinall Chase. Some were transferred to Maltese QROPS run by Integrated Capabilities and Harbour (now taken over by STM) and to Hong Kong.

Blackmore Global is a UCIS fund – unregulated collective investment scheme. And it is illegal to promote these to UK retail investors as this was banned by the FCA in 2014.

I doubt the other nominees and award recipients will appreciate having been listed alongside Phillip Nunn who has a history of promoting other scammers’ pension scams and is now running one himself. Perhaps JCI Manchester ought to vet candidates for the Manchester Young Talent Awards more carefully in the future.

Pension and investment scams and scandals are a blight on financial services and saving for retirement. The energetic and inspired campaign by Darren Cooke of Red Circle successfully raised awareness of the problems of cold calling. But the snap general election scuppered serious traction on this and the most the government has achieved so far is to make a vague promise to talk about talking about it. But still it is not illegal, and still the scammers are scamming away merrily.

Chair of The Transparency Task Force

The Scams and Scandals team was formed as a result of inspiration by the Transparency Task Force’s Andy Agathangelou. It has attracted a group of like-minded professionals who believe passionately that a concerted effort should go into coordinating a zero-tolerance approach to scams and scandals. All members of the team are committed to producing a White Paper which can focus the minds of government ministers, regulators and law enforcement agencies on the whole problem – not just the cold calling bit.

Irrespective of which version of which political party we are talking about, the ultimate object of a successful and fulfilled life is to be happy, healthy and solvent. And this includes getting a decent education, leading a responsible and law-abiding life, and saving for a comfortable retirement. Millions of British citizens manage to achieve this goal, but sadly many thousands of them lose part of all of their retirement savings to the armies of scammers.

XXXX XXXX, one of the many pension scammers ruining thousands of victims’ lives

All these scams and scammers have caused thousands of victims to lose hundreds of millions of pounds’ worth of retirement savings. And caused untold misery – in many cases exacerbated by HMRC punishing the victims rather than the perpetrators.

The Scams and Scandals Team has a clear five-point goal:

Ban UK cold calling and fraudulent calling

We must not let this disappear off the agenda and must keep up pressure on MPs and Ministers – as well as the regulators. But this must also be extended to overseas as we already know that the UK-based cold calling outfits have made arrangements to move their operations or merely facilitate re-routing of phone numbers. However, the twilight industry of “introducing” must also be examined as this is a serious source of scam facilitation.

Support Lesley Titcomb “Scammers are Criminals”

Ms Titcomb has publicly declared scammers to be criminals

We must work with the regulators, government and law enforcement agencies to enhance existing and introduce new regulation and legislation to prevent new scams, close down known existing scams and bring those involved in conceiving, operating and promoting both to account.

Revitalise Scorpion Campaign

Fundamental to preventing scams is communication to the public of the dangers of cold calls and pension/investment scams which would include the Scorpion Campaign – but so much more as well. A key part of this exercise is the use of social media and the plan to produce a documentary and Youtube channel giving real-life examples of past and current scams. Explaining the mechanics of a scam is one thing – but showing an actual example of a victim and the scammer is bound to have even greater impact.

Write off HMRC debt where scams are proven

HMRC celebrating the tax they collect from victims of pension liberation fraud

We need the help of the government here and could do with an actuary to help us work out what the cost to the State is of taxing victims of scams. If we can demonstrate that by ruining a scam victim (who has already probably lost part or all of his pension) with the tax charge, the long-term cost of supporting the victim and his family will far outstrip the tax collected. This is especially well demonstrated in the Ark case where the victims have got to both repay the “loans” and pay the 55% tax even if the loans are repaid.

Ensure AML regs include pension scamming

TOBY WHITTAKER’S TOXIC EMPIRE WILL FINALLY BE HUFFED AND PUFFED AWAY

I would widen this to include investment scams. This is because at the heart of every pension scam there is a fraudulent investment (and/or loan). The actual pension itself is harmless as it is essentially just a box with a label on it and only becomes toxic and dangerous once you put the scorpions, snakes and cockroaches inside it. You could equally put fluffy kittens in it. It is the mis-use of the pension “box” which is the scam.

Regulators have got to do some effective regulating

Regulators and scammers; cops and robbers; cowboys and indians. Each has their role: cowboys fire their six shooters and dodge the injuns’ arrows valiantly; cops drive their police cars at breakneck speed to corner the robbers in a dark alley; regulators waggle their flaccid willies and watch the scammers walk all over them.

In the week my great friend had his appendix out (somewhat hurriedly as it happens) I thought I would write a slight variation on the Three Sausages poem:

Regulation, regulation, regulation, Three scammers went to the station, One got crushed, one got killed, And one got a huge operation.

The sizzling scammers need to be put behind bars – and the keys need to be thrown away.

Now, I am not suggesting I want the scammers crushed or killed – nor even that they suffer the same pain and discomfort that my mate has gone through in hospital this past week. But I do want them stopped from harming more victims and destroying more life savings. And, of course, put behind bars where the only thing they can scam is the soap on a rope.

WHAT DO REGULATORS NEED TO DO AS A MATTER OF URGENCY?

All regulators in all jurisdictions where has been a history of scamming and mis-selling need to work closely with governments, tax authorities, financial crime units, ombudsmen and the press. There has to be a “zero tolerance” attitude to scams and scammers – and all those responsible have to be brought to justice. And publicly so. It is clear that most regulators – including the FCA – are limp, lazy and useless and this has to change. Here are some examples of regulators’ failures in each jurisdiction:

Allowing unregulated firms to provide financial, pension and investment advice freely and without sanction in the UK. Sometimes these firms have an insurance license – sometimes none at all

Not sanctioning regulated firms for clear breaches and/or fraud – such as Gerard Associates which was introducing Ark victims to Stephen Ward of Premier Pension Solutions as far back as 2010, and was then providing “advice” to Ward’s London Quantum victims

Ignoring firms such as Fast Pensions who have defied 37 Pensions Ombudsmen’s determinations

Failing to coordinate criminal prosecutions against the scammers behind numerous scams who ruined thousands of lives and cost hundreds of millions of pounds’ worth of life savings

Failing to use existing legislation provided by FSMA 2000 to prosecute advisors (regulated and/or unregulated) overtly contravening the ban on communicating invitations to retail clients to invest in Unregulated Collective Investment Schemes

Announcing ineffective crack-down plans by newly-appointed government minsters who have failed to grasp the enormity of the pension scamming industry and the desperate plight of thousands of pension scam victims

Failing to police and sanction negligent pension trustees such as STM Fidecs for accepting members introduced by an unlicensed adviser: XXXX XXXX of Global Partners Ltd/The Pension Reporter – who was also the fund manager for the UCIS that all the victims had their pensions invested in and which is now being wound up

Refusing to communicate with members on the progress of the winding up of the Trafalgar Multi Asset Fund which had been run by XXXX XXXX

Omitting to take action against STM Fidecs for its role in the Cornerstone Friendly Society investment scam

Taking no action against Trustees, Integrated Capabilities Malta Ltd (ICML) for accepting retail members from an unlicensed firm in the Czech Republic and knowingly permitting investments in Nunn McCreesh’s UCIS: Blackmore Global, as well as Malta-licensed fund Symphony – a sub-fund of the Nascent Platform that is licensed only for professional investors

Not sanctioning Customs House Global, that runs the Nascent Platform, for inadequate due diligence and accepting unscrupulous sub-fund managers (such as XXXX XXXX, investment manager of failed TMAF and later, the recently wound up Symphony Fund) that exploit the platform for the sole purpose of pension scamming

Allowing an unlicensed firm – Square Mile Financial Services – to operate freely in the EU, providing pension and investment advice with only an insurance mediation license

Ignoring insurance companies which accept investments in UCIS funds and professional-investor-only instruments for retail investors

Failing to recognise those registered Closed-Ended Investment Companies whose true nature is as a Collective Investment irrespective of their form, such as Blackmore Global (registered number 010221V), that intentionally circumvent the stricter regulations imposed on collective investments, specifically to hide their financial accounts and the sub-funds which invariably include unsigned loan notes and high-risk hare-brained projects

Failing to act against a pension liberation scam – Evergreen Retirement Benefits Scheme – run by Simon Swallow who was working with Stephen Ward of Premier Pension Solutions and operating Marazion “loans”

Ignoring Concept Trustees (Guernsey) who offered retail investors the EEA Life Settlements UCIS and then accepted investment instructions from unlicensed, un-insured Stephen Ward of Premier Pension Solutions

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

A fund like Blackmore Global really ought to be audited as soon as possible – to make sure it isn’t simply a “black hole” into which victims’ hard-earned pensions have sunk. Numerous worried pension savers are stuck in the Blackmore Global Fund and finding it difficult – if not impossible – to get out. They are seemingly “locked in” for ten years.

I WOULD LIKE TO EXPRESS MY SINCERE THANKS TO THOSE – INCLUDING IFAs, PENSION TRUSTEE FIRMS AND BLACKMORE GLOBAL VICTIMS – WHO HAVE CONTACTED ME AND SUGGESTED IMPROVEMENTS, CORRECTIONS AND ADDITIONS.

Allegedly, Grant Thornton is working on an audit – and has been doing so since September 2016. They could probably have audited Microsoft in that time – and squeezed in Amazon on the side during the lunch breaks. Just how difficult can it be to audit a fund which only has a handful of assets in it?

Originally, the directors of Blackmore Global were Brian Weal, Patrick McCreesh, and Phillip Nunn.

Brian Weal – sanctioned by the FSC in 2014 – was also a director of Swan Holdings – the only investment that the Advalorem Value Asset Fund made. Brian Weal was also a director of Advalorem. Advalorem lost most of its money because the investments in Swan Holdings were overvalued. The valuations were supplied by Stuart Black who also provided valuations for a Hedge Fund called Heather Capital which lost $300 million because of overvaluations. Swan Holdings had invested a chunk of cash in Etaireia Investments. Stuart Black was a director of Etaireia Investments. Brian Weal owns a controlling number of shares in Etaireia Investments. So, make up your own mind as to whether having Weal as a director of Blackmore Global is a good thing or a bad thing – or a “black hole” thing.

As for Nunn and McCreesh, I will let Leonard Fenton of the Insolvency Service do the talking:

Documents and information received from members of CAPITA OAK indicated they were initially contacted by Craig Mason or Patrick McCreesh of Nunn McCreesh of Its Your Pension Ltd and offered pension review services prior to them being referred to JACKSON FRANCIS or Sycamore for the transfer of their pension to CAPITA OAK.

On 3.3.15 I received an undated letter in which it was stated that Its Your Pension had not traded and was a dormant company and that Nunn McCreesh had traded as an insurance brokerage between 2009 and 2012 when they entered into a verbal arrangement with TRANSEURO where in return for providing pension leads to JACKSON FRANCIS they received a commission from TRANSEURO.

Nunn McCreesh provided JACKSON FRANCIS with 100-200 leads per month which were provided by email and/or telephone for which they received £899,829.86 from TRANSEURO during the period 26.3.12 to 14.5.14.

So, again, draw your own conclusions about those connected with Blackmore Global. Nunn and McCreesh generated up to 200 leads a month to pension scammers in relation to a series of pension/investment scams which are now under investigation by the Serious Fraud Office. This entailed £120 million worth of pensions being invested in Store First store pods which are now the subject of a winding up petition – and arguably worthless.

When I first started investigating the Blackmore Global fund in 2016, I started with the brochure which makes all sorts of grand claims: “medium to long-term investment vehicle with a diversified investment portfolio under one structure. The Company allocates investment between four distinct protected cells, giving a true diversification of assets between property, sustainable, private equity and lifestyle”. Yeah, right. But what are the underlying assets? Where is the audit?

The Fact Sheet goes on to claim the fund’s NAV is £17.65 million and was launched on 1st May 2014. So why no audit? It also claims that the Investment Manager is a firm in Barcelona called Meriden Capital Partners. I thought it a bit strange that a fund based in the Isle of Man would appoint an investment manager in Spain – especially one without a website. So I called Meriden Capital Partners and asked them to confirm that they were the investment manager. They claimed they had never heard of Blackmore Global. Then one of the partners called me back and told me that some man who didn’t give his name had come to their office and asked them whether they would be interested in being the investment manager for Blackmore Global.

The partner at Meriden Capital explained that they had declined because they were not licensed to provide investment management advice to a fund – only to private individuals.

But then I discovered that that hadn’t been entirely true either. Meriden Capital had actually completed an application form to apply to become the investment manager to the fund on 4th April 2014. So either Meriden Capital was lying or Blackmore Global was lying – or both.

The Blackmore Global NAV Factsheet also states that there is a ten-year lock-in to the fund. So why would anyone invest a pension in such a fund? A pension saver has a statutory right to a transfer and might want to take his PCLS – 25% tax free withdrawal at age 55 – or retire, or even die. What on earth is the point in using Blackmore Global for a pension at all? Ever.

As Grant Thorton is clearly having a little trouble with the audit of a five-cell investment fund, I will lay a wee trail of bread crumbs for them to look at. Clearly they can’t even find the underlying assets – let alone value them:

Spinaris 90 – UK sports spread betting (invisible – and what happened to Aria Invest?)

Most of the victims of the Blackmore Global fund were initially cold-called by a firm called Aspinal Chase. And all the victims were advised by unregulated investment advisers Square Mile Financial Services (an insurance license does not cover regulated investment advice). But more worryingly, all of them were put into a QROPS in Malta or the Isle of Man. So why were UK residents transferred to an offshore pension at all, and why were most or all of their pension funds invested in a UCIS which is illegal to be promoted to UK residents?

The list of questions goes on and on. And here, we get back to whether the unscrambling of these pension and investment scams is more about who you know rather than what you know. One victim had his pension invested 75% in Blackmore Global and 25% in Symphony. Symphony was a fund invested in derivatives and highly leveraged. It was also a sub fund of the Nascent Fund run by Richard Reinert. Under the Nascent “umbrella” (a structure for wannabe fund managers) was also the Trafalgar Multi Asset fund which was run by XXXX XXXX who was one of the main distributors behind Capita Oak, Henley and Westminster – all of which are being investigated by the Serious Fraud Office.

Now we have gone round in a complete circle. A catalogue of lies, deception, fraud, mis-selling, negligence and incompetence.

I don’t envy Grant Thornton (if indeed they are the auditors) because they have got to unscramble this unholy mess. And I strongly suspect that, behind the scenes, there are certain parties who are busting a gut to ensure the audit is never published. Two of these may well be John Ferguson and David Vilka of Square Mile in the Czech Republic who seem to have a strong vested interest in promoting this black hole of a fund.

Meanwhile, the longer the victims are held back from transferring out of this toxic swamp of a fund, the more serious the complaints against the various parties involved will be. These will include the cold-calling scammers; introducers; advisers; pension trustees and insurance companies such as Investors Trust who allowed this investment and the pensions transfers from unlicensed advisers.

Finally, on the subject of Investors Trust, they showed not a shred of interest in the fact that they had facilitated financial crime in allowing UK residents to have their pensions invested in this UCIS, but when I published a photo of John Ferguson and David Vilka posing as a couple of gaudily-dressed spivs in Las Vegas, Investors Trust objected on the grounds the photograph was their property.

Gambling is a very strictly controlled industry – and rightly so. Every individual jurisdiction has its own gambling or casino licenses which are usually very expensive and onerous to obtain and keep. Where large amounts of cash change hands every minute, it is obviously important to impose strict conditions and ensure that regulations are complied with.

The city of Las Vegas sprang up in the middle of a desert in 1905 in the hottest part of the world and has since flourished into a sparkling and magnificent centre for world-class gambling.

In the words of Rudyard Kipling: “If you can make one heap of all your winnings, and risk it on one turn of pitch-and-toss, and lose, and start again at your beginnings, and never breathe a word about your loss…..you’ll be a man my son!”

Kipling’s advice is clearly aimed at someone young; someone who has years ahead of him to get lucky; recoup his losses; start again; do a phoenix; learn from his mistakes and do better next time. But with pensions, a life-time of savings can be wiped out so easily on “one turn of pitch-and-toss” by entrusting an unlicensed adviser.

Here in Spain, the investment regulator – the CNMV – refers to unlicensed pensions and investments advisers as “chiringuitos” (which translates as “bar flies”). The CNMV helpfully publishes a well-written warning booklet to alert the public to the nefarious tactics of these scoundrels – copied below for the information of the gentle reader. However, in Britain we tend to be rather more direct and call them scammers. And Lesley Titcomb of the Pensions Regulator has come right out and said it: “scammers are criminals”.

So, make sure you only use an advisory firm which is licensed to provide pension and investment advice. And avoid the chiringuitos, scammers and criminals. I have no idea who the jolly pair of gamblers are in the photo on this blog, but I am sure no informed person would entrust them with a pension and I reckon Kipling would have had a thing or two to say about them.

Away from the fun fun fun of Vegas, these two amiable-looking scallywags could probably scrub up and look like respectable independent financial advisers with a business-like suit and a leather portfolio full of impressive documentation about funds with imaginative names such as “Symphony” and “Blackmore Global”. But if they did so without a license, they would be criminals.

SPANISH REGULATOR’S (CNMV) GUIDE (translated)

FINANCIAL CHIRINGUITOS (“IFA” FLY BOYS/SCAMMERS)

“CHIRINGUITOS” means entities offering and providing pensions/investment and advisory services without being authorized to do so. They are dangerous because in most cases the apparent provision of such services is just a cover for fooling victims into believing they are making a highly profitable investment. It is important to understand that high yields offered are often too good to be true: the bait to con ill-informed (naïve) investors to hand over their savings or pensions. When exposed, the “CHIRINGUITOS” simply disappear or change their names. They are simply swindlers.

Companies authorized to provide investment services (brokers, portfolio managers, IFAs, banks etc.) are subject to the rules governing the securities markets and strict controls by the supervisory bodies (CNMV and BanK of Spain). Only CNMV-registered companies are authorized to provide pension/investment services, after demonstrating compliance with specific legal requirements and standards.

CHIRINGUITOS are not attached to the Investment Guarantee Fund, so that investors are not protected in the event of insolvency of the entity (authorized entities contribute to these protection funds through compulsory subscriptions).

There is no particular type of victim because often scams are very elaborate. Victims can be small businesses, individuals or professionals who fall for credible-sounding false promises of quick wealth and easy gains.

In short, to trust a CHIRINGUITO is a sure way to lose capital, with no investor protection under the laws. How CHIRINGUITOS work

The channels used by scammers and boiler rooms to contact potential victims are no different from those that can be used legally by legitimate entities i.e. telephone, letters, e-mail, web pages etc. The difference lies in the way the scammers use these channels, the type of messages they convey and the general approach to achieving their goals.

The CHIRINGUITOS use databases (often obtained fraudulently) of people who, for example, have purchased a particular financial product, publication – or on occasion answered a survey about their tastes, interests and financial situation. Phone calls

Cold calling is one of the CHIRINGUITOS’ favourite contact methods. It allows them to directly exercise psychological pressure techniques. Cold calling is by definition unexpected but is legal, and in fact authorized entities often use it as part of their promotional campaigns. However, in the case of authorized entities, it is normal practice to call existing customers, so people know their data has been obtained legitimately. If the answer to what is being offered is “no” this is accepted politely. By contrast, the CHIRINGUITOS do not usually settle for a NO.

Mail

High-quality leaflets which are sophisticated, inviting and promising. These often request the recipients to contact them by filling out a form, calling by phone or by visiting their website. Internet, e-mail

The great success of the Internet as a direct marketing tool allows advertisers to access a wide mass of recipients more cheaply than traditional media (phone, mail). This fact, coupled with the possibility of anonymity, has led to abuse of the medium, such as spam or indiscriminate emailing of unsolicited products bordering on illegality. Recipient lists are often obtained unlawfully, in breach of data protection rules. Also, the address of origin of the messages are usually false, and also the subject headings are deliberately misleading. Spanish law decrees that commercial communications should be identified as such and prohibits sending emails unless they have previously been requested or expressly authorized by the recipient. No serious company would ever spam the public, as that would be invading consumer privacy.

When it comes to financial products and services, we must be very cautious about offers and information received, even if they have been requested or consented to. Financial fraud on the Internet can be carried out by more sophisticated means. Spam is just one of the possible mechanisms, because the Internet offers various tools to disseminate potentially fraudulent or questionable deals: boards, newsgroups, chats, or even sophisticated web pages.

Phishing

Another danger is “phishing”: emails that appear to come from legitimate financial institutions, which request personal passwords. These messages often lead to a website that imitates an authentic entity (although it may have spelling mistakes), which fools people into entering their personal data or passwords.

Pharming

Even more sophisticated is “pharming”: people who visit fraudulently-cloned websites can have their personal, confidential data collected by criminals. Never surrender personal or confidential business information to unknown persons. If a request for personal data appears legitimate, use an established phone number to double check. Also, don’t access websites via links, but type in the full URL and, if possible, install antiphishing and antipharming tools. Adverts

CHIRINGUITOS also advertise in newspapers, magazines or other media (such as television teletext) to offer opportunities which are much more attractive than traditional investments and promising to provide attractive opportunities (which, of course, are not so in reality).

Personal referrals

It is common for people to make their investment decisions based on recommendations from acquaintances or relatives whom they trust. Knowing this, sometimes the CHIRINGUITOS pay great benefits to the first customers, using their own money or from other investors; this is what is called a Ponzi scheme. In fact, those investors who unwittingly act as bait are only going to get limited performance at first and successive investments begin to generate losses. Then, the company will not respond to requests for repayment of capital and finally disappear with all the money invested.

Personalized investment recommendations should always be made by a professional entity authorized to do so, because what is good for one investor may not be for another, depending on their different personal and financial circumstances. Persuasion techniques

The list of boiler-room persuasion techniques cannot be exhaustive, since the arguments and methods are increasingly sophisticated. Therefore it is important to stay alert to any financial offer that is not from a known, registered party. Accurate predictions

A simple but very effective technique – using a large number of calls to impress potential victims with their knowledge of financial markets – half of which confidently predict the rise of a certain investment value and the other half predicting decrease of the same value. In the following days this exercise is repeated several time. Those targets who were given a series of successful predictions are contacted again. Now convinced of the infallibility of a company that has hit all its forecasts for several consecutive days, these people are willing to surrender their savings to the CHIRINGUITOS. Appearance of respectability and success

CHIRINGUITOS know it is essential to look respectable and seem like financial market experts. So they dress smartly and elegantly and rent luxury offices. Sometimes it is difficult to get an appointment to meet them because they want to give the impression of being busy and in high demand. Incomprehensible explanations and use of technical jargon

CHIRINGUITOS promoting fraudulent investments talk with confidence and mastery of technicalities that make them look like experts on the subject. In fact, the aim is that the potential victim does not understand anything and chooses to trust those who seem to be experts who know what they are talking about. Offering large profits with little risk

CHIRINGUITOS promise much higher returns than can be obtained from a conventional investment with minimal risk. A basic principle that all investors should bear in mind is that profitability and risk go together inseparably. The possibility of obtaining high yields always involves taking high risks. Be wary of any offer that ensures high returns without risk. Insistence on an immediate decision

Urgency is a major factor, not only because they want to get their hands on your money asap and with the least possible effort, but because they know that if the investor has time to think properly about the offer, or seeks professional and reliable advice, he will probably reject the offer. So, CHIRINGUITOS use tricks aimed at achieving an immediate decision to try to convince the victim that they are offering a unique opportunity that will expire soon. Investors should be aware that this is not true: there is always time to assess the characteristics of a financial offer and to make sure it is suitable. Psychological pressure

The conversation, either by phone or by any other means, usually begins in a cordial fashion, but if the targeted victim shows some potential resistance the scammer can become more aggressive. This constitutes a fundamental difference between the CHIRINGUITOS and the authorized entities, who always respect a prospect’s right to not be interested.

Although psychological pressure can take many forms, here are some common tricks:

Not taking no for an answer

Being repeatedly insistent

Becoming increasingly aggressive

Questioning the intelligence or ability of the investor to make a decision

Conveying the idea they are doing the victim a big favor by offering exceptional gains

Making it clear it would be absurd to question the promises made

Using warnings such as: “you’ll regret it if you don’t go ahead” or “you’ll never get rich if you ignore my advice”

When to be suspicious of a financial offer

Most of the techniques used by CHIRINGUITOS would not be used by authorized firms, since they are subject to strict rules of conduct. Authorized firms are required to keep customers properly informed and to provide information to investors fairly and clearly. In particular, they must provide information about their services and financial instruments, so that the client knows the nature and risks of the investment service that it is going to provide and the characteristics and risks of financial instruments offered.

It is therefore important to understand the difference between people or entities who are authorized to provide investment services and those who only intend to carry out a scam. When an authorized firm sells a product, the customer must request information on their knowledge and experience in this product, in order to assess for himself whether it is suitable for him. This is called a suitability test.

When a broker is going to provide investment advice or manage an investment portfolio, in addition to asking about the client’s investment knowledge and experience, he should request additional information such as the financial situation and investment objectives of the client (risk profile, time-frame etc.) – as proper financial advice is always personalized.

The boiler room scammers’ only aim is to attract money from their victims, so they do not care about their clients’ expertise in investments and financial circumstances – all they need to know is that they are willing to invest. The contact must have been requested by the prospect

Authorised entities have to work with personal data in a legally-compliant manner, and the client must have given them permission to make commercial offers. But if an entity of which we have never heard contacted us to offer an investment, you have to take extra precautions because this is probably a scam. Authorized entities never pressurise customers

Any investment should be approached with sufficient knowledge of the characteristics and risks of the product. It is important to do thorough research before committing. The investor needs time to decide and get answers to all their questions. However, scammers pressure the victim to get an immediate yes, without giving them a chance to reflect. How to protect yourself against a possible CHIRINGUITO