CRIMINAL CASE AGAINST UNLICENSED FINANCIAL ADVISERS:

Last month saw the first of the CWM pension scam victims testifying in the criminal court of Denia, Alicante. Nine brave people re-lived their ordeal in front of the judge. They answered the judge’s questions, and were then cross-examined by the defendants’ lawyers.

The complainants who testified were all clients of Continental Wealth Management (CWM) run by Darren Kirby and Jody Smart (pictured below), as well as Premier Pension Solutions (PPS) run by Stephen Ward. PPS was an “agent” and “partner” of AES Financial Services run by Sam Instone. (PPS and AES are now under investigation for their role in the 2011 Ark Pension Liberation scam).

It is hard enough for a pension scam victim to be reminded of their ordeal at the hands of callous, greedy scammers. But to have to recount in graphic detail the methods used by the scammers was hard for them to bear.

The scammer’s typical arsenal of weapons comprises a series of lies – adeptly used to trick the unwary into handing over their pensions and life savings. The victims who testified in Denia know these lies all too well. And now, so too does the judge:

LIE NO. 1: “We’re fully regulated”. This, of course, was completely untrue. CWM operated, purportedly, as a member of the Inter Alliance “network”. And Inter Alliance was not only unregulated but had been fined by the Cyprus regulator for providing regulated services without legal authorisation.

LIE NO. 2: “Yes, I’m fully qualified”. This, again, was untrue. Few – if any – of the people working for CWM had any financial qualifications. They were mostly poorly-educated salesmen with the gift of the gab. They had learned a well-used and very clever script which was designed to mislead and defraud their victims.

LIE NO. 3: “The case for transferring your pension into a QROPS is overwhelming”. In the case of final salary pensions, this was never true. A guaranteed income for life from a company pension final salary scheme can almost never be bettered. Most personal pensions should also have been left where they were. In fact, all pensions would have been better off avoiding ending up in the hands of CWM – even if a QROPS had been the right option.

LIE NO. 4: “Your pension needs to be in an insurance bond (Quilter, SEB or Utmost). This is for protection and tax efficiency”. This was never true. The bond provided no protection, no tax savings, no flexibility. The 7% commission paid to the “adviser” was not disclosed.

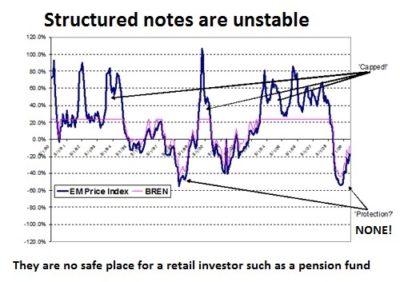

LIE NO. 5: “Your money will be invested in blue chip companies and you will get high returns and low risk.” High returns come with high risk – and the high commissions (paid to the scammers) were hidden from the victims. Toxic structured notes were used for all the victims – and these are complex investment products which were only suitable for professional investors.

There were, of course, many other lies – including the fact that when the toxic structured notes and unregulated funds failed, these were “only paper losses”. Plus the fact that the investors’ signatures were forged or copied on the investment dealing instructions.

The second half of the complainants will be heard by the court on 9th and 10th December 2021. Once the court has heard from all these victims (minus Bob Bowden who sadly passed away recently), the fate of the defendants will be decided by the judge. Let us all hope this will herald an end to these types of pension and investment scams.

I read an interesting article recently which has prompted this blog, written by

I read an interesting article recently which has prompted this blog, written by  Blair (pictured) talks about substance and the need for higher standards among financial advisers. Whilst I love her thoughts, I know how difficult this might be to achieve. We see wholly unqualified scammers posing as fully qualified IFAs time and time again. These scammers are very good at acting the part and the victims have no idea they are dealing with a fraudster – and sometimes go on for years believing they are dealing with a proper financial adviser.

Blair (pictured) talks about substance and the need for higher standards among financial advisers. Whilst I love her thoughts, I know how difficult this might be to achieve. We see wholly unqualified scammers posing as fully qualified IFAs time and time again. These scammers are very good at acting the part and the victims have no idea they are dealing with a fraudster – and sometimes go on for years believing they are dealing with a proper financial adviser.

In every pension scam there is one beginning, lots of middles, and always a wretched ending for the victim and a profitable ending for the scammers. The beginning is always a negligent, lazy, box-ticking transfer by a ceding provider – the worst of which always tend to be the likes of

In every pension scam there is one beginning, lots of middles, and always a wretched ending for the victim and a profitable ending for the scammers. The beginning is always a negligent, lazy, box-ticking transfer by a ceding provider – the worst of which always tend to be the likes of

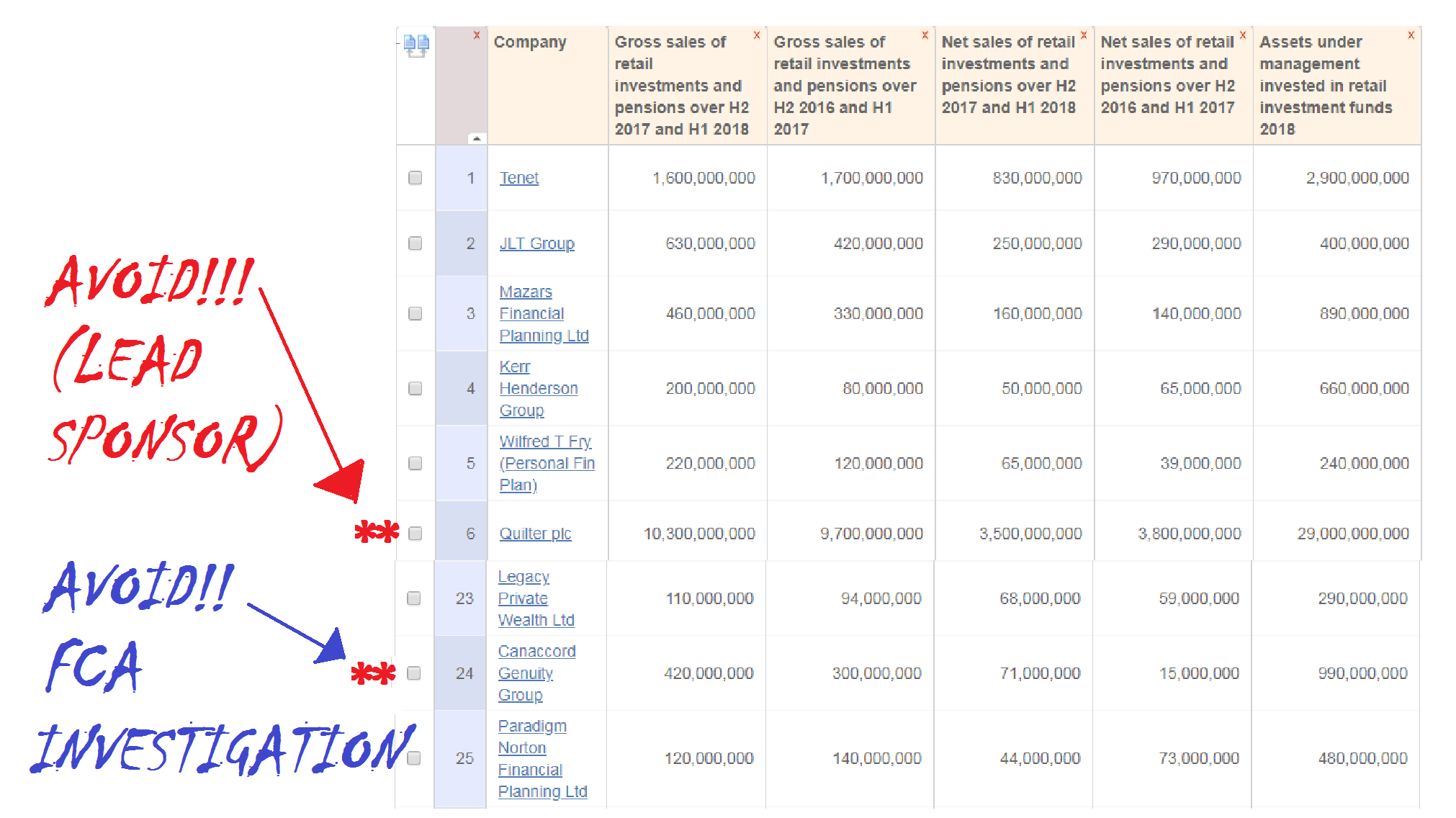

I have enormous respect for FT Adviser. Their articles are written by proper journalists and they generally write competently and professionally. FT Adviser puts

I have enormous respect for FT Adviser. Their articles are written by proper journalists and they generally write competently and professionally. FT Adviser puts  However, Canaccord Genuity Group’s porky pies do pale into a degree of insignificance when compared to Quilter plc which came sixth with £10.3 billion worth of sales and £29 billion worth of assets under management. Quilter plc is

However, Canaccord Genuity Group’s porky pies do pale into a degree of insignificance when compared to Quilter plc which came sixth with £10.3 billion worth of sales and £29 billion worth of assets under management. Quilter plc is  But, despite the embarrassing inclusion of these two dud firms, congratulations to FT Adviser for the hard work which must have gone into producing this hit parade. This is definitely one in the eye for the hopeless nitwits at

But, despite the embarrassing inclusion of these two dud firms, congratulations to FT Adviser for the hard work which must have gone into producing this hit parade. This is definitely one in the eye for the hopeless nitwits at  Looking at International Adviser’s 2017 awards, I really think the judges were having a

Looking at International Adviser’s 2017 awards, I really think the judges were having a  I HAVE DECIDED TO INVITE MY FRIENDS AT INTERNATIONAL ADVISER TO LAUNCH A NEW AWARDS CEREMONY:

I HAVE DECIDED TO INVITE MY FRIENDS AT INTERNATIONAL ADVISER TO LAUNCH A NEW AWARDS CEREMONY:

Kenny told International Adviser:

Kenny told International Adviser: Here at Pension Life, we do hope that even trainees at OMI are aware that pension fund members are retail investors and should be placed into low to medium risk, liquid investments. However, it seems that these details obviously don´t feature in OMI´s training manual.

Here at Pension Life, we do hope that even trainees at OMI are aware that pension fund members are retail investors and should be placed into low to medium risk, liquid investments. However, it seems that these details obviously don´t feature in OMI´s training manual. Regrettably for the investors who were victims of the CWM scammers and OMI, they most definitely did not possess the depth of knowledge required to fully understand the risks. They put their faith in the smartly- dressed scammers. With promises of high returns, the high risk of the investments and high fees to be charged were left unmentioned. OMI were supposed to protect the victims’ interests but failed dismally to lift a finger to help arrest the downward spiral of the funds.

Regrettably for the investors who were victims of the CWM scammers and OMI, they most definitely did not possess the depth of knowledge required to fully understand the risks. They put their faith in the smartly- dressed scammers. With promises of high returns, the high risk of the investments and high fees to be charged were left unmentioned. OMI were supposed to protect the victims’ interests but failed dismally to lift a finger to help arrest the downward spiral of the funds.

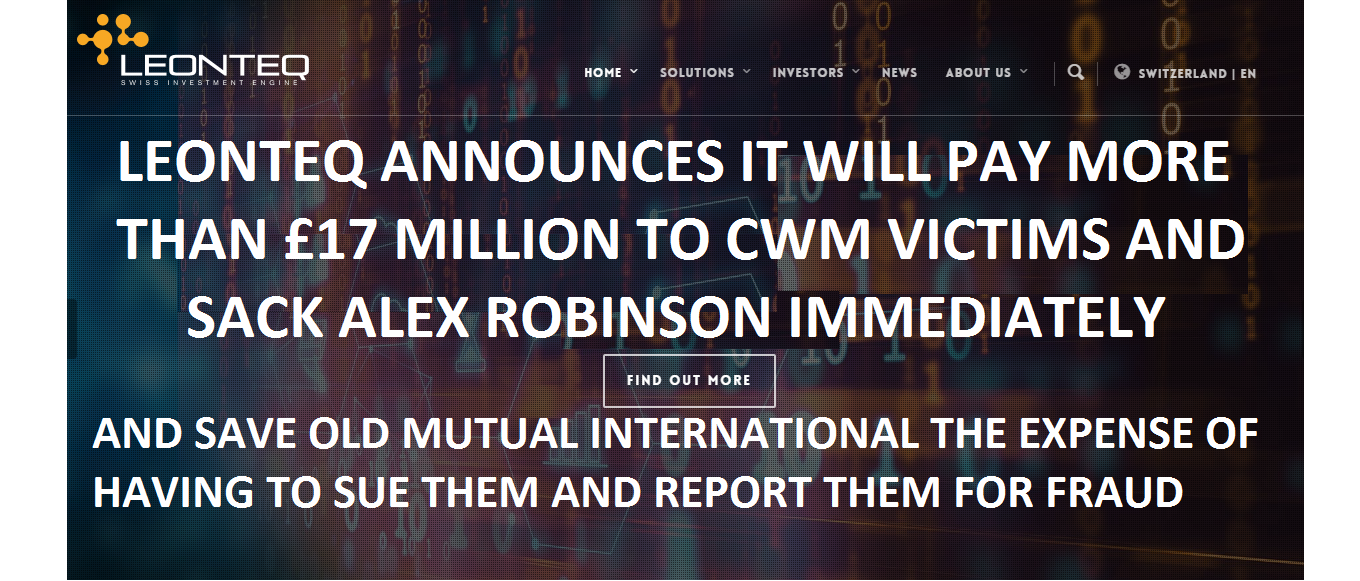

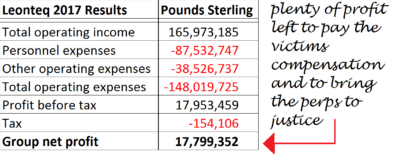

And Leonteq can, of course, afford to pay. Here are their 2017 results:

And Leonteq can, of course, afford to pay. Here are their 2017 results: Rogue life office,

Rogue life office,

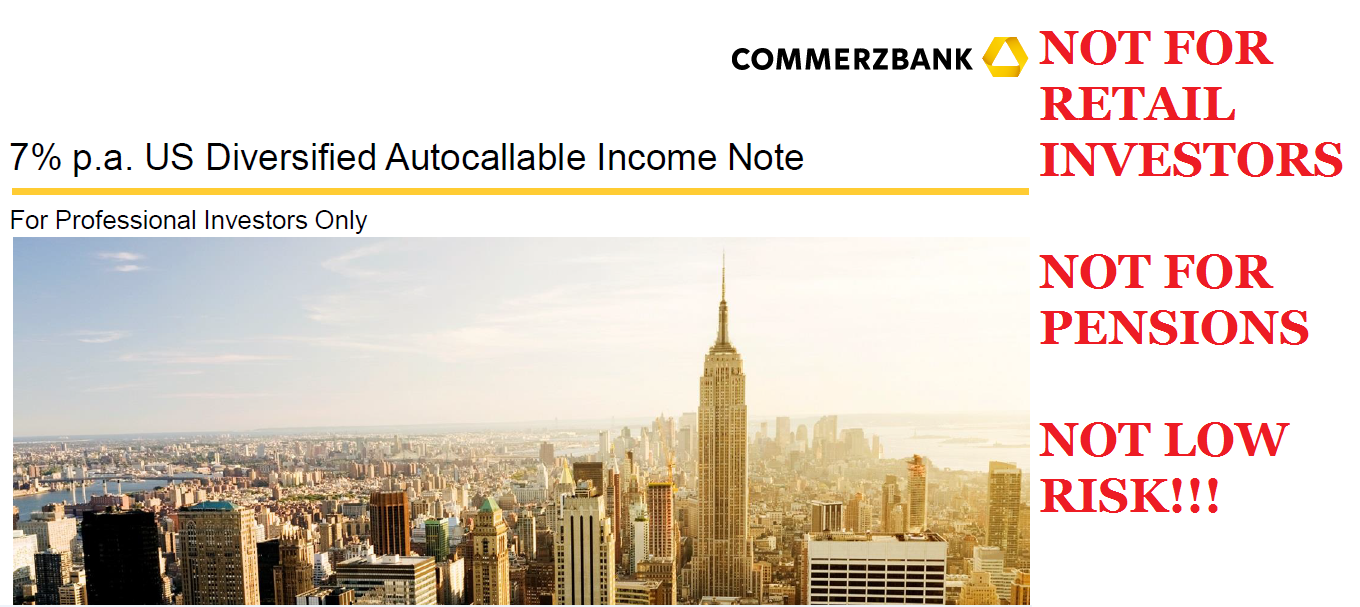

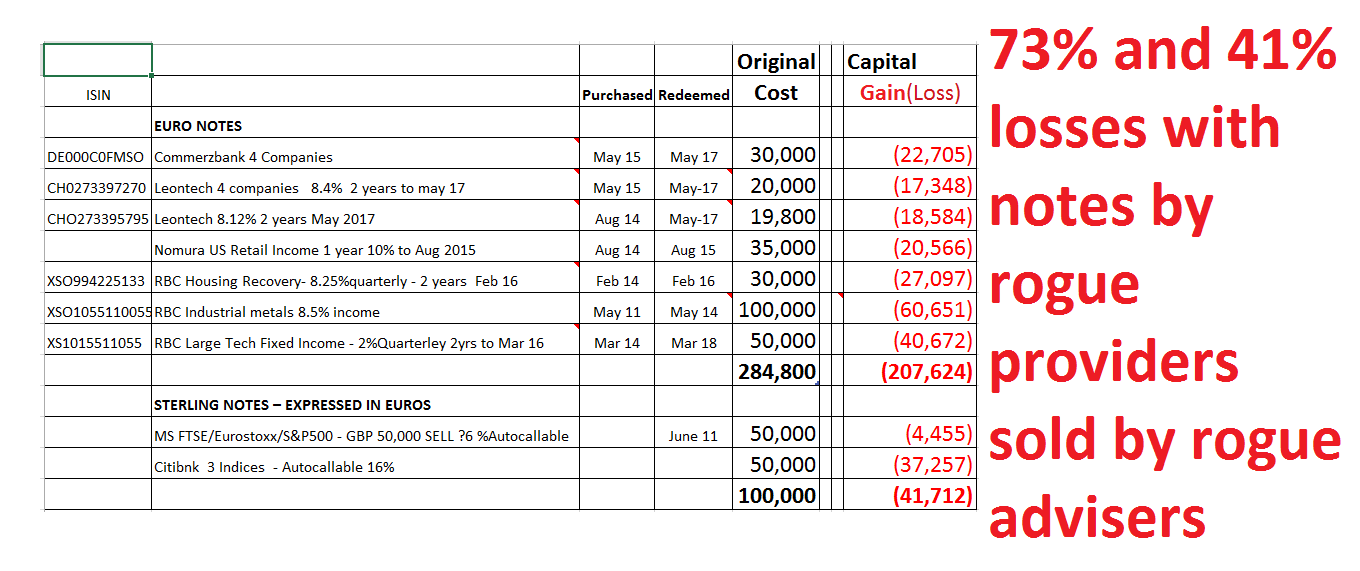

Structured notes – say NO to them if an adviser wants to invest your pension in them. They are high-risk investments which are for professional investors

Structured notes – say NO to them if an adviser wants to invest your pension in them. They are high-risk investments which are for professional investors  As in the above example, it is a disgrace that structured note providers such as Commerzbank, Nomura, RBC and Leonteq have allowed their toxic products to be used for retail pension savers. Even when these rotten products have nosedived repeatedly, these dishonest and dishonourable providers keep on flogging them to destroy victims’ retirement savings.

As in the above example, it is a disgrace that structured note providers such as Commerzbank, Nomura, RBC and Leonteq have allowed their toxic products to be used for retail pension savers. Even when these rotten products have nosedived repeatedly, these dishonest and dishonourable providers keep on flogging them to destroy victims’ retirement savings.

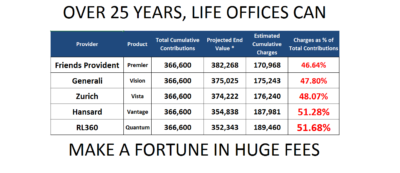

OMI – Old Mutual International (Quilter), SEB, ZURICH, GENERALI, FRIENDS PROVIDENT, ZURICH INTERNATIONAL, RL360 AND HANSARD INTERNATIONAL. They are all as bad as each other. They rip their clients off, charging them huge fees and commissions, tying them into useless, pointless products for years.

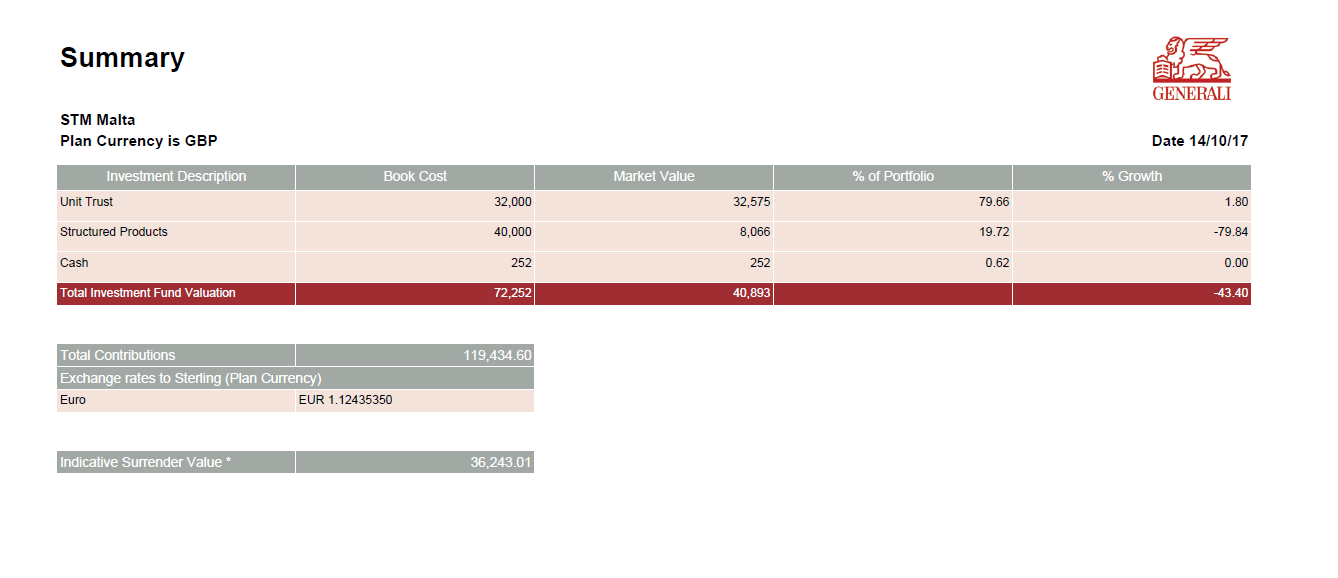

OMI – Old Mutual International (Quilter), SEB, ZURICH, GENERALI, FRIENDS PROVIDENT, ZURICH INTERNATIONAL, RL360 AND HANSARD INTERNATIONAL. They are all as bad as each other. They rip their clients off, charging them huge fees and commissions, tying them into useless, pointless products for years. One Generali victim saw her £119k pension fund plummet to £36k in five years.

One Generali victim saw her £119k pension fund plummet to £36k in five years. Pension scams are not the only arrangements that these life offices profit handsomely from. Another method they use to rinse extortionate fees out of unsuspecting victims is the LONG TERM SAVINGS PLAN. Clients think these are a good idea until they realise the huge hidden charges which decimate the funds they put towards these plans.

Pension scams are not the only arrangements that these life offices profit handsomely from. Another method they use to rinse extortionate fees out of unsuspecting victims is the LONG TERM SAVINGS PLAN. Clients think these are a good idea until they realise the huge hidden charges which decimate the funds they put towards these plans.