Since 2013, thousands of clients of Planet Pensions – previously known as Aktiva Wealth Management and Square Mile International Financial Services – have been scammed out of their pensions.

John Ferguson and David Vilka of Planet Pensions (Square Mile/Aktiva) advised UK residents to transfer their pensions into QROPS including:

- GFS SCHEME 2 SUPERANNUATION SCHEME 2 (HONG KONG)

- QUARTERMAINE (HONG KONG)

- EFPG (GIBRALTAR)

- OPTIMUS (MALTA)

- KRESTON (ISLE OF MAN)

- HARBOUR PENSIONS (MALTA)

- PANTHEON (GIBRALTAR)

- CORINTHIAN (GIBRALTAR)

The clients were conned into these transfers on the basis that it would be in the interests of making their pensions perform better. It was also claimed that the clients would pay less tax. None of the promises, assurances and advice was true:

| LIES TOLD TO VICTIMS BY PLANET PENSIONS | THE TRUTH |

| “A QROPS falls outside the Lifetime Allowance rules for UK pension schemes. If your pension grows to above 1.25m you will suffer a 55 percent extra tax charge” | Most of Planet Pensions’ victims had pensions which were below £50k in value and were never likely to reach anywhere near £1.25m in value – so this would never apply. |

| “At age 55 you will be able to access a cash lump sum” | Had the victims left their pensions in the UK, they’d have accessed the 25% tax-free lump at age 55 |

| “The QROPS is of course approved by HMRC” | HMRC never “approves” any QROPS schemes. They register them – there is no approval. |

| “Your pension will be invested in funds which are not traditionally available in the UK, giving you access to a broad range of asset classes” | There is a good reason why risky, unregulated assets are not available in the UK – it is illegal to promote them to retail investors. Victims would be likely to lose their pensions (which is exactly what happened) |

| “With a wide range of high growth asset classes utilised, the high performance funds chosen by our investment team are ideally suited to your pension investment” | None of the high-risk/high-commission assets were suitable for pension investments – and they all failed (destroying thousands of victims’ pensions) |

| “The investment enables you to invest in investment funds which will contain a carefully managed risk assessed portfolio” | There was nothing to “manage” – once the pension money was invested in the assets, the money was trapped and would inevitably be lost |

| “A QROPS allows a wider choice of investments, which gives you the potential to grow the fund further than your current scheme” | This is true! Many QROPS allow fraudulent investments such as those chosen specifically for the high commissions paid to the scammers |

Of course, none of this – either the transfer (by a UK resident) to a Hong Kong QROPS – or the subsequent high-risk investments, was in the interests of the victims. This was only in the interests of the scammers who earned commissions from the unregulated investments. These included:

- Blackmore Global PCC Ltd

- Swan Holding PCC Ltd

- Christianson Property Capital Ltd

- SN Granite Investments Global

- Drake Incubator PCC – GRRE

- EcoVista PLC

- Curzon Alternative

In the GFS QROPS scheme in Hong Kong, Planet Pensions worked with a variety of unregulated “introducers” to help recruit victims. These included Scott Campbell of 3V Financial, Andrew Blackburn of St James International, and Aled Williams of Nicholas Street Tax.

The QROPS application forms, which showed which adviser each victim had appointed, were forged to show the name of the introducer rather than the name of the adviser. This was done by removing the adviser declaration page, and inserting a new page showing the introducer as the adviser – rather than Aktiva Wealth Management (one of Planet Pensions’ former names).

Planet Pensions also often claimed that Aktiva Wealth Management was acting under the regulation of Paul Brown’s Worldwide Broker – using the Dutch AFM as the regulator. Paul Brown has strenuously denied that he ever allowed Aktiva (Planet Pensions) to act as an Appointed Representative of Worldwide Broker.

John Ferguson and David Vilka of Planet Pensions (aka Aktiva, aka Square Mile) have clearly worked closely with Phillip Nunn and Patrick McCreesh of Blackmore Bond and Blackmore Global infamy. Both Blackmores are being wound up – causing hundreds of victims to lose over £90 million of pensions and life savings. It is clear both investments were run fraudulently by Nunn and McCreesh (both of whom have now been bankrupted).

Ferguson and Vilka also worked closely with Manish Gambhir of MG Finance and Christianson Property Capital (yet another failed mini bond). Another associate of Ferguson and Vilka was Tom Fraser of EFPG in Gibraltar, as well as Mark Donnelly of Brite Advisors in Australia, South Africa and the USA.

Ali Hussain of The Sunday Times covered the Mark Donnelly and Brite Advisors story in 2024:

“Missing expat pensions: Some 10,000 people put their money into a financial firm run by advisers who investigators say have transferred millions to their own accounts. Bosses at Brite – led by Mark Donnelly – transferred millions of pounds to their personal accounts or other companies.”

Ali Hussain – Saturday April 27 2024, 6.00pm, The Sunday Times – wrote that:

“The savers are victims of a network of financial advisers working for a firm called Brite Advisory Group, which is run by Mark Donnelly, a convicted fraudster who stole football merchandise relating to David Beckham. Donnelly’s right-hand man was a financial adviser who fled UK after duping a 91-year-old dementia sufferer out of £170,00. Investigators claim that instead of investing savers’ money in pensions, bosses at Brite took millions of pounds and transferred it to their personal accounts or other companies they ran around the world. Some of it is alleged to have been used to buy rival businesses; some was used for personal loans to directors and their wives. About £250,000 was allegedly used to buy two Porsches.”

Fighting pension scams needs to be done logically and methodically. Decent advisers need to use high standards to help fight scams. If these standards become the norm, the scammers won’t survive and flourish so easily.

Fighting pension scams needs to be done logically and methodically. Decent advisers need to use high standards to help fight scams. If these standards become the norm, the scammers won’t survive and flourish so easily. Lots of offshore advisers

Lots of offshore advisers

and many others such as

and many others such as  Fighting pension scams – why qualifications are so essential

Fighting pension scams – why qualifications are so essential You wouldn’t go to an unqualified solicitor would you? So don’t use an unqualified financial adviser. Being qualified goes hand in hand with being regulated.

You wouldn’t go to an unqualified solicitor would you? So don’t use an unqualified financial adviser. Being qualified goes hand in hand with being regulated.

HOW DO PENSION SCAMS WORK?

HOW DO PENSION SCAMS WORK?

“Information on scams is not readily available at an organisational level”.

“Information on scams is not readily available at an organisational level”. “The Scams Code is seen as a good basis for due diligence”

“The Scams Code is seen as a good basis for due diligence” “Significant time and effort goes into protecting members from scams”

“Significant time and effort goes into protecting members from scams” “The more detailed the due diligence, the more suspicious traits are identified”

“The more detailed the due diligence, the more suspicious traits are identified” SIPPS (including international SIPPS) are the vehicle of choice by scammers

SIPPS (including international SIPPS) are the vehicle of choice by scammers “Quality of adviser tops the list of practitioner concerns, with member awareness a close second”

“Quality of adviser tops the list of practitioner concerns, with member awareness a close second” “Sharing of intelligence would help avoid duplication of effort”

“Sharing of intelligence would help avoid duplication of effort”

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based

Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based  Capabilities and Harbour (n

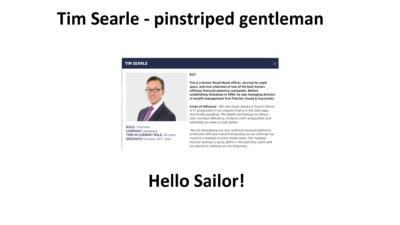

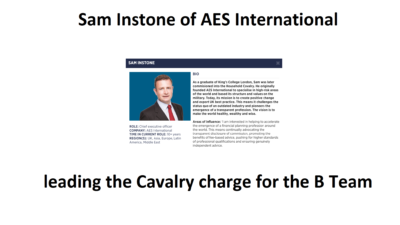

Capabilities and Harbour (n Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

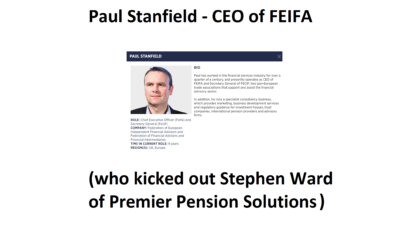

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated

This new pension arrangement locked me in for 10 years – definitely a “long-term relationship” – giving all parties the opportunity to drain my pension dry in fees. Credit where credit is due, however. Once I discovered I was in a scam, the director Andy Dawson (bottom row, 3rd from the left) did make an extraordinary effort not only to redeem the investments but successfully persuaded most parties to waive their early exit penalties and refund their fees. Only the greedy Symphony Fund chose to keep the penalties and that’s after mysteriously dropping in value 30% just before redemption. Thanks to Andy Dawson and his team, I did manage to get back 92% of my pension. But the BIG QUESTION is what has happened to the other 1,100+ members? It is inconceivable I was the only one transferred into this scheme via Vilka et al.

This new pension arrangement locked me in for 10 years – definitely a “long-term relationship” – giving all parties the opportunity to drain my pension dry in fees. Credit where credit is due, however. Once I discovered I was in a scam, the director Andy Dawson (bottom row, 3rd from the left) did make an extraordinary effort not only to redeem the investments but successfully persuaded most parties to waive their early exit penalties and refund their fees. Only the greedy Symphony Fund chose to keep the penalties and that’s after mysteriously dropping in value 30% just before redemption. Thanks to Andy Dawson and his team, I did manage to get back 92% of my pension. But the BIG QUESTION is what has happened to the other 1,100+ members? It is inconceivable I was the only one transferred into this scheme via Vilka et al.

I would like to highlight that the rider of the jet ski does bear a remarkable resemblance to Phillip Nunn, cold caller and “fund manager” of the

I would like to highlight that the rider of the jet ski does bear a remarkable resemblance to Phillip Nunn, cold caller and “fund manager” of the

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders:

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders: A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

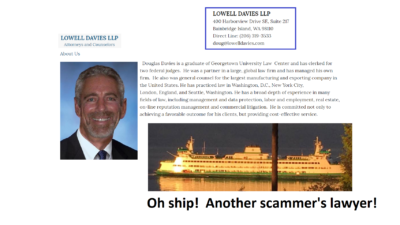

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer

David Vilka of

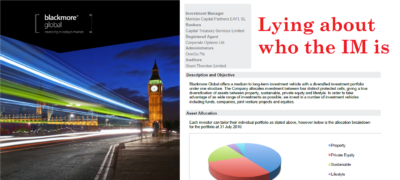

David Vilka of  Mr. Davies is referring to the UCIS investment scam, Blackmore Global, which was illegally promoted to retail investors – and which is a fraud from start to finish.

Mr. Davies is referring to the UCIS investment scam, Blackmore Global, which was illegally promoted to retail investors – and which is a fraud from start to finish. And again, significantly, he was not cold-called. He sought out Mr. Vilka and Square Mile. Nor did Mr. Vilka or Square Mile receive any payment from the Blackmore fund or its partner firms regarding Mr. Sexton’s transaction as confirmed by the Czech National Bank which has direct access to Square Mile’s company bank accounts via an electronic data box. Are you talking about the accounts which haven’t been updated since 2014?

And again, significantly, he was not cold-called. He sought out Mr. Vilka and Square Mile. Nor did Mr. Vilka or Square Mile receive any payment from the Blackmore fund or its partner firms regarding Mr. Sexton’s transaction as confirmed by the Czech National Bank which has direct access to Square Mile’s company bank accounts via an electronic data box. Are you talking about the accounts which haven’t been updated since 2014? LOWELL DAVIES LLP

LOWELL DAVIES LLP