Jody Smart (or Bell or Kirby or whatever name she uses now) appeared in the Criminal Court in Denia on 1st October 2019. As one of the group of defendants in the fraud trial – including her former partner Darren Kirby (who didn’t turn up) – she testified about her involvement in the £100 million Continental Wealth Management/Trust (CWM) investment scam.

CWM – of which Jody was shareholder and sole director – collapsed at the end of September 2017.

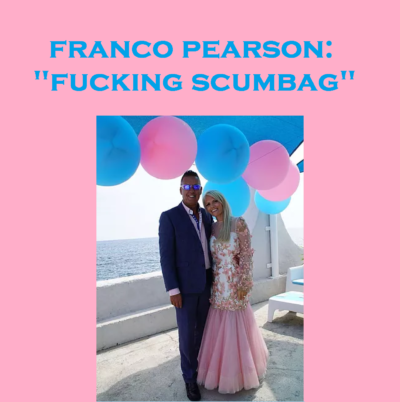

The event was covered by journalist Joshua Parfitt of The Olive Press newspaper https://issuu.com/theolivepress/docs/online_issue_a/1?e=1186741/73089185 and was a relatively low key affair in the Denia Court Number 3 . Jody’s ex boyfriend Darren failed to show (no surprise there). The only entertainment on offer for anyone watching (and hoping for some sign that justice will be done) was her current beau, Franco Pearson, shouting “fucking scumbag” in the court waiting room.

This particular criminal case involves not just the investment scam itself, but also some previously-unknown anciliary scams involving bogus property transactions and false promises of shares in CWM in exchange for hard cash.

One of the complainants – Mark D – had handed over his final salary Shell pension (worth £415,000) plus a further £140,000 to Jody’s company: CWM. Mark was told he would be given a 5% shareholding in the company and that it was worth £10,000,000. Jody’s then boyfriend, Darren Kirby, had promised Mark the shares in return for £400,000 – and told him the money was going to be used to prop up the ailing company and also be invested in Jody’s fashion business. Mark D – who lost not just his pension but his house – developed severe depression and diabetes which he struggled to manage. After being left penniless by Jody and Darren’s CWM scam, he died alone in August 2019.

In the Denia court, Jody confirmed she was the sole director of Continental Wealth Trust (formerly Continental Wealth Management). The company held no license to provide either insurance or investment advice – and was selling life (death) bonds illegally; provided by rogue companies such as Old Mutual International, SEB and Generali. She stated it had not been possible to close the company because there had been so many debts. This comes as no surprise as Darren had paid £1.3 million to victims as compensation for investment losses, and had also pumped £500,000 into the Jody Bell fashion business. The court was also told that Jody had been paid 12,000 Euros a month by CWM.

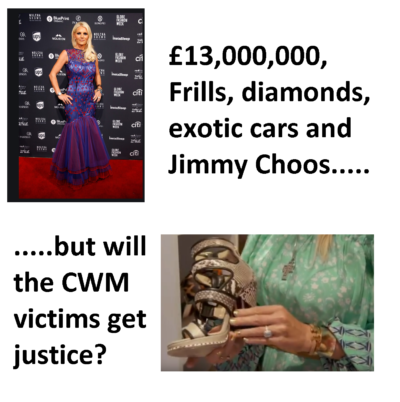

In court, Jody denied holding any position in CWM and stated that she had no financial qualifications. But here I start to wonder whether, perhaps, something got lost in translation. In previous interviews, Jody had openly boasted about running CWM and also the sister operation Female Wealth Management. She claimed to have made £13 million out of financial services.

Jody also stated in the Denia Court that she had never had anything to do with the company or the clients (perhaps she was paid 12,000 Euros a month just to look glamorous in reception?). However, in a previous t.v. interview she had stated that her role was “to expand the company and see where we could go forward. Bring the best people on board to work for us“.

In the same interview, Jody had expanded on CWM’s activities: “We offer the whole package for expats. Advising on the investment of funds. We also do a pension release. There is a scheme where we can release your pension from the UK. Obviously, we’ve been very successful with that. Being in the climate that we’re in at the moment, there are a lot of people, unfortunately, who can’t pay their mortgages or their private school fees.

Its like saying “we’re gonna give you money and its not gonna cost you anyfink. Obviously, we can just change your life really”.

She was clearly referring to the Evergreen pension liberation scam in which more than 300 people certainly had their lives changed by losing their pensions and getting 50% loans from Stephen Ward’s Delaware-registered finance company Marazion. CWM did all the cold calling and administration for this scam – from which Ward earned 10% of the overall £10 million worth of pensions transferred into the bogus New Zealand-based QROPS run by Simon Swallow and Kenji Stevens.

Far from not costing the victims “anyfink”, 300 people are now being pursued for repayment of the Marazion loans and have lost the other 50% of their pensions left in Evergreen, which is now being wound up. They also face 55% tax charges on the 50% loans as unauthorised payments.

Jody was apparently (according to the court transcript) asked in court if she knew anything about the CWM business of which she was the sole director. She replied “no” and that Darren told her she could be a director along with him as she spoke Spanish, that he wanted to protect her and that it was going to be good for her.

So this leaves me wondering: was Jody lying in her recorded interviews which she used to promote CWM and her Jody Bell fashion business, or was she lying in court?

After testifying that everything had been Darren’s fault, that he had manipulated her and killed her mum’s chickens, Jody refused to answer any further questions.

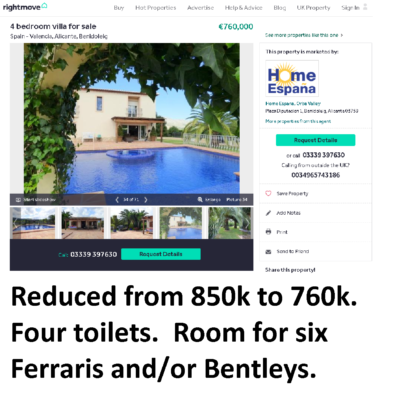

So with no further answers from Jody Smart/Bell/Kirby/Pearson, we can only listen to the evidenceprovided by her in her video interviews. She is portrayed as the director of the CWM wealth management company and is worth an estimated £13m. She has a stunning house in Spain (currently up for sale for 760,000 Euros), a fleet of fast cars, a diamond ring as big as a door knob worth 39,000 Euros, and an impressive limited edition Jimmy Choo collection.

In one video interview, Jody started to describe how she had invested a lot of money in her fashion business and that after only six months the sales were “phenomenal”; that with her hard work and sheer determination……(here she pauses as a waiter brings a bottle of champagne)….

Full of bubbly, Jody goes on to state that she didn’t doubt herself – that her ambition (which came from a burning desire inside her) would help her succeed. Her conclusion was that she just knew she was “gonna reach the stars”.

Of course, victim Mark D had no idea how quickly he was going to “reach the stars”. Furthermore, there are hundreds of other CWM victims who are afraid that they too will meet a similar fate: dying – starving and penniless.

But I have faith in Jody – because she is very enthusiastic about her charitable works. She is on record, in one of her t.v. interviews, as saying:

“We done a lotta charity work. I’m lucky. There aren’t a lotta people as fortunate as what I am.”

Jody’s magnificent house is on the market for 760,000 Euros – and I get a sneaking feeling that she is flogging this pile of real estate full of glamorous furniture in order to help the victims of the CWM scam. In her t.v. interview she stated: “I like to help people. It’s in me.” So, hopefully, the 760,000 Euros will go towards helping some of the people who have been financially ruined by her company.

It is, of course, too late for Mark D. One of the things that killed him was the fact that he couldn’t afford to eat properly – and this is particularly dangerous for people who are suffering from diabetes. But there is hope for others – Jody has set up a facility to feed those who can’t afford to eat because her company scammed them out of their life savings: The Oceana Club near Calpe.

Rather more glamorous than the run of the mill soup kitchen, those who have lost their life savings and are in need of a hot meal will – I feel sure – be warmly welcomed at The Oceana Club. Hopefully Jody’s boyfriend Franco will embrace this charitable initiative just as warmly as he welcomes the CWM victims with a greeting rather more gentlemanly than “fucking scumbag”.

Fighting pension scams needs to be done logically and methodically. Decent advisers need to use high standards to help fight scams. If these standards become the norm, the scammers won’t survive and flourish so easily.

Fighting pension scams – Qualifications

Most qualified advisers want nothing to do with pension scams. Many offshore firms employ advisers who have not passed the required exams. Even if an adviser has qualified, he or she must still be registered. We recently surveyed a number of offshore advisory firms:

The Chartered Institute for Securities & Investment (CISI) is the largest and most widely respected professional body for those who work in the securities. The Chartered Insurance Institute (CII) is a professional body dedicated to building trust in the insurance and financial planning profession.

All financial advisory firms should list their advisers, provide clear details of each adviser’s qualifications and a link to the institute’s register showing evidence of the qualifications.

“Qualifications are not the be all/end all. A certificate does not prove professional competence in the field , ethics or experience. But the public have to start their due diligence somewhere.”

and many others such as Westminster and London Quantum – ruining thousands of lives. Several of his schemes are under investigation by the Serious Fraud Office. He also provided the transfer advice in the Continental Wealth scam.

Any decent adviser will want to be fully qualified. And registered. The rest should go back to selling snake oil. But consumers must remember there are exceptions. Some regulated firms get it wrong. Qualified advisers can get it wrong.

Clients must have comprehensive fact finds and risk profiles

Firm must operate adequate compliance procedures

Advisers must not abuse insurance bonds

Clients must understand the investment policy

All fees, charges and commissions must be disclosed

Investors must know how their investments are performing

Firm must keep a log of all customer complaints

Fighting pension scams – why qualifications are so essential

If clients used only firms that tick all ten Standards boxes, it would be harder for the scammers to get business. Decent firms who care about their reputation should make sure there are clear links to all advisers’ qualifications. Make it easy for the consumer to understand how to check that the stated qualifications are genuine. And help educate people to understand what qualifications are required.

All too often, advisers claim to have qualifications that don’t exist – or that aren’t appropriate for investment advice. For example, some advisers who are assuring clients they can advise on pensions and investments, only have qualifications suitable for mortgages. Or worse still, no qualifications at all. Whatever the adviser says his qualifications are, the client must be able to double check.

You wouldn’t go to an unqualified solicitor would you? So don’t use an unqualified financial adviser. Being qualified goes hand in hand with being regulated.

If it was easy to stop pension scams, everyone would be doing it. Clearing up the mess left behind a pension scam is a huge challenge. This is why clear international standards need to be recognised and adopted. The scammers are like flocks of vultures. If people only used regulated firms, they could avoid a lot of scams.

Firm must be fully regulated – with licenses for insurance and investment advice

Advisers must be qualified to the right standard

Firm must have Professional Indemnity Insurance

Clients must have comprehensive fact finds and risk profiles

Firm must operate adequate compliance procedures

Advisers must not abuse insurance bonds

Clients must understand the investment policy

All fees, charges and commissions must be disclosed

Investors must know how their investments are performing

Firm must keep a log of all customer complaints

Why is regulation so important?:

If a firm sells insurance, it must have an insurance license.

If a firm gives investment advice, it must have an investment license.

Many advisers will claim that if they only have an insurance license, they can advise on investments if an insurance bond is used. This practice must be outlawed, because this is how so many scams happen.

Most countries have an insurance and an investment regulator. They provide licenses to firms. Some regulators are better than others. Most regulators do some research and only give licenses to decent firms.

History tells us that most pension scams start with unlicensed firms. Here are some examples:

Continental Wealth Management invested 1,000 clients’ funds in high-risk structured notes. Investors started with £100 million. Most have lost at least half. Some have lost everything. Continental Wealth Management had no license from any regulator in any country.

Serial scammers such as Peter Moat, Stephen Ward, Phillip Nunn, and XXXX XXXX all ran unlicensed firms. Peter Moat operated the Fast Pensions scam which cost victims over £21 million. Stephen Ward operated the Ark, Evergreen, Capita Oak, Westminster and London Quantum pension scams which cost victims over £50 million. XXXX XXXX operated the Trafalgar pension scam which cost victims over £21 million.

Phillip Nunn operates the Blackmore Global Fund which has cost victims over £40 million. Serial scammer David Vilka has been promoting this fund. Over 1,000 people may have lost their pensions.

Firms that give unlicensed advice are breaking the law. Unlicensed advisers often use insurance bonds. These bonds pay high commissions. The funds these advisers use also pay high commissions. The advisers get rich. The clients get fleeced. The funds get destroyed. Insurance bonds such as OMI, FPI, SEB and Generali are full of worthless unregulated funds, bonds and structured notes.

Unlicensed firms hide charges from their clients. Most victims say they would never have invested had they known how expensive it was going to be.

Hidden charges can destroy a fund – even without investment losses. Licensed advisers normally disclose all fees and commissions up front. This way, the client knows exactly how much the advice is going to cost.

People can avoid being victims of pension scammers. Using properly regulated firms is one way. An advisory firm should have both an insurance license and an investment license. Don’t fall for the line: “we don’t need an investment license if we use an insurance bond”. Bond providers such as OMI, FPI, SEB and Generali still offer high-risk investments. The insurance bond provides zero protection. And the bond charges will make investment losses much worse.

If you have been following Pension Life´s blogs, you will know that we have been conducting a series of investigations into qualified and registered financial advisers in various firms. Today is the turn of Callaghan QROPS Spain – qualified and registered?

IFAs and their clients are invited to add to it, correct it, improve it. Here’s a link to the three registers if you want to double check:

Please note that this data is correct as at today, 11/07/2018

**********

What Callaghan QROPS Spain say about themselves:

“Located in Cabo Roig, Alicante, GC QROPS has a long history of assisting UK Expats with their pension transfers. Our pensions advisors are all UK Qualified and Registered IFAs and give up-to-date informed evaluations with a no obligation policy running throughout the company.

Graeme Callaghan Pension Services has been successfully assisting UK expats in Spain with UK pension transfers for 9 years since 2006. We have assisted in over 500 successful UK pension transfers for UK Pensioners.”

Callaghan QROPS Spain claim they have been advising UK expats on their pension transfers for nine years – with this claim, let’s hope Callaghan QROPS Spain has advisers which are qualified and registered? Can this firm score a better percentage than some of the other companies of the past weeks?

Callaghan QROPS Spain – advisers qualified and registered?

Upon clicking on the ´Our Advisers´ tab on Graeme Callaghan´s website, I was presented with this statement:

´All our advisers are U.K qualified. We offer a free no obligation assessment on all your existing plans. Including your U.K pensions, your existing QROPS and ISA’s.

In some circumstances our advisers will travel to your country of residence. We can also arrange for your travelling requirements to one of our offices in Spain.´

With no links to any real person to represent this Callaghan QROPS Spain firm, it is very hard to make a judgement on who you are entrusting you valuable pension fund to. Callaghan QROPS Spain do little to give a true representation of their firm with no transparency about their staff or their qualifications – I was unable to even find a picture of Graeme Callaghan himself. They do however mention that they are looking for UK qualified financial advisers.

What I did find was a host of testimonials from Hollywood movie stars and professional sports persons etc etc assuring me that Callaghan QROPS Spain had supplied, ´Top Service´, and were ´Highly recommended´.

What I find hard to grasp is that Callaghan QROPS Spain managed to go to all the effort of giving a long list of testimonials, but were unable to take the time to put anyone in their ´Our Advisers´ tab. Surely a reputable financial advisory company would be proud to show their qualified and registered IFAs who give ´top service´ to pension holders?

As shown in the image above there were lots of links to social media, so I chose to follow the Facebook one first. Here I was able to find an image of Graeme Callaghan of Callaghan QROPS Spain (and I also found out they were Callaghan QROPS Portugal too).

On his facebook page dated 06/07/2018 he states: ´Find us ranked on page one by Google with an ”Evergreen QROPS” search. We are assisting multiple members of this scheme with transfering to a scheme recognised on the HMRC website. Contact us for a free no obligation assessment on your existing QROPS or UK pension´.

Those of you who are familiar with the CWM pension scam debacle and the Evergreen QROPS liberation scheme will know that this pension scam was hustled by unregulated and unqualified advisers and resulted in members losing massive percentages of their pension funds when CWM collapsed. Furthermore, the victims of this scam face large tax bills from HMRC after they received Stephen Ward’s Marazion “loans” on their pension transfers.

Graeme Callaghan is also using the threat of Brexit as a compelling reason for expats to move their pension fund into a QROPS. It is questionable whether Brexit will have any effect at all on expats’ pensions and many firms are using this as a “scare tactic” to get people to transfer into a QROPS – often entirely unnecessarily.

As I have no other staff to go on for Callaghan QROPS Spain, I am going to check the registers for Graeme Callaghan himself. Interestingly on his Facebook profile he states he studied at City University London, but he fails to mention what subject he studied there.

Graham Callaghan – Director? Sole financial adviser? Position unclear – however he seems to be the owner of Callaghan QROPS Spain – IS NOT LISTED ON ANY OF THE REGISTERS FOR FINANCIAL ADVISERS.

Callaghan QROPS Spain – qualified and registered? 0/1 – 0%

EDIT: a search through Linkedin of Callaghan QROPS Spain revealed that there is in fact another employee, Dylan Callaghan. Listed job role of UK Pension Adviser at Graeme Callaghan Pension Services, he too went to went to University of London where he apparently studied for an MBA.

Despite stating that he is a UK pension adviser for the company, he lists no financial qualifications and does not appear on any of the three registers. Therefore, Callaghan QROPS Spain – qualified and registered? 0/2 employees 0%.

Other claims by Callaghan QROPS Spain: Callaghan Financial Services can advise on the whole of the QROPS market and we are not tied to one jurisdiction. Really? And how do you manage that? You are an unregulated company, with zero qualifications.

“We believe part of our success is due to offering a free no obligation assessment on all your existing plans.” Here at Pension Life we are always supicious of the word ´free´.

If I was looking to swap my pension plan I would steer clear of Callaghan QROPS Spain.

Unqualified, unregistered, unregulated and non-transparent – this company is no place for your pension fund – even if Eric Roberts (Hollywood Actor) states they are an excellent company!

Welcome to my world – and the four letter word that sends a chill down most people’s spine: HMRC. A world where justice and taxation are not just in different countries, but on different continents. And, sadly, where thousands of British expats are living under the shadow of a ticking time bomb because of arrangements made with their pensions and life savings.

A few people are aware of the tax disaster that awaits them. But the majority have absolutely no idea and it is going to hit them as a devastating shock – whether from HMRC or their local tax authorities (or, in some cases, both).

Up to 2012, expats were routinely sending their pensions off to New Zealand – to the Superlife and Southern Star QROPS – and then busting 100% out. After the rules changed in April 2012, Stephen Ward set up the Evergreen QROPS/Marazion loan scam and up to 300 people bust 50% of their pensions out. It remains to be seen how the Spanish tax authorities will treat all these payments. It is unlikely to be pleasant for those affected.

For expats in Spain, the outlook can be grim. If there is a debt with HMRC for tax – say an unauthorised pension payment @ 55% – HMRC can send the debt to the Spanish Tributaria and they can then enforce the payment. If we think that HMRC is heartless, the Tributaria makes them look like the Sally Army. If a tax debt is unpaid, they will just have your bank account frozen and can also put your house up for auction.

In the Continental Wealth Management scam, large numbers of victims were paid compensation for the destruction of their pension funds by investing them in high-risk, toxic structured notes from firms such as Leonteq. But CWM had not bargained for the fact that in Spain the Tributaria would deem this to be taxable income – and the victims had a terrible surprise when the money they had used up to live on attracted a hefty tax bill for which they hadn’t budgeted.

Which brings me to Portfolio Bonds in general – and the SEB Life International “Spanish” one in particular. Many victims are fooled into thinking that because this product is heralded as “Spanish Compliant” that there is some degree of safety or security. There isn’t. SEB’s Spanish Portfolio bond is compliant from the Tributaria’s point of view because it reports annually on growth of the portfolio for tax purposes. However, that is all there is to it. And it is a waste of time anyway, because there often isn’t any growth – only loss. The huge quarterly charges by SEB erode any growth – and if toxic Leonteq structured notes have been used, there will be destruction of most or even all of the fund.

The Continental Wealth Management scandal – along with similar scams run by firms such as Holborn Assets – should have taught the industry conclusively that insurance bonds should not be used for pensions. They are too expensive and inflexible. The quarterly charges do increase when the fund value increases, but they don’t decrease when the fund is impaired – or even destroyed entirely. I have one member whose fund has gone from £250k to minus £57k as SEB simply kept taking their fees long after the fund was worthless.

An insurance bond (Personalised Portfolio Bond) can be used by an individual as an investment wrapper outside of the UK. This can be useful and tax efficient offshore. But when the investor goes back to the UK, there is a tax nightmare. Personalised Portfolio Bonds come under anti-avoidance legislation in the UK!

The horrible surprise that the investor will get upon returning to British soil is that HMRC can assume a deemed gain even if there is no gain at all, and charge tax on it. It is known often as the 15/15/15 rule and it leads to taxation even where the fund within the bond is losing money.

This situation only applies to investments within the Personalised Portfolio Bonds, selected by the policyholder, where the policyholder is a UK tax resident. The tax payable is at the policyholder’s highest rate. Even worse, the supposed tax efficiency of investment bonds does not work as top slicing relief (which normally lessens the blow and is often the cited reason for these bonds when sold to non-UK investors) does not apply to Personalised Portfolio Bonds.

Most people assume that tax is applied to actual gains made by the overall fund. And few offshore advisers have heard of the tax rules which apply in this situation (The Income Tax, Trading and other Income Act (ITTOIA) 2005 Sections 515 to 526). The devasting effect of this on an expat returning home is that the rules assume an annual gain of 15% of both the initial premium and the cumulative actual gains from the date the bond was established.

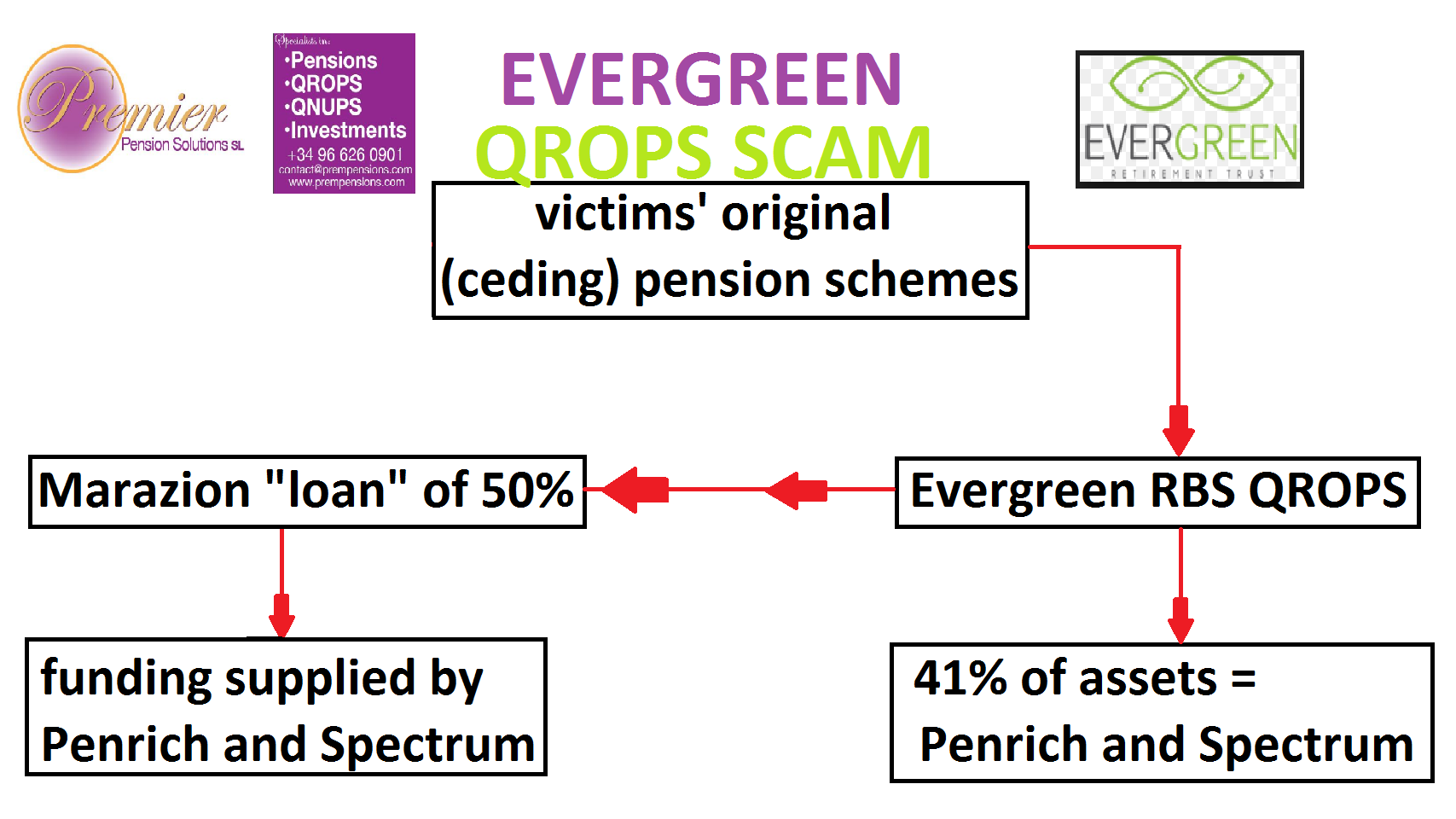

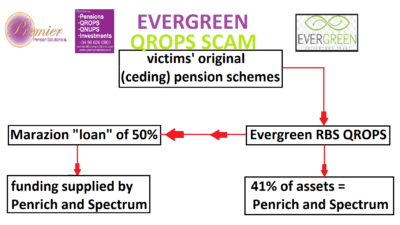

EVERGREEN RETIREMENT TRUST QROPS SCAM – HOW DID IT ALL WORK?

Victims were cold called by Continental Wealth Management (CWM) and duped into transferring their UK pensions into the Evergreen New Zealand QROPS on the promise that they could access 50% of their pension. CWM acted as the “sister” company to Stephen Ward’s Premier Pension Solutions (PPS).

Once the 300+ victims had been sold this idea – on the promise by pensions “expert” Stephen Ward of Premier Pension Solutions that the 50% in cash would not be taxable – the transfers went ahead. More than £10 million pounds’ worth.

CWM assured the victims that the 50% cash would not be taxable because the scheme was set up and run by international pensions expert and author of the Tolleys Pensions Taxation manual Stephen Ward of Premier Pension Solutions.

Once the transfer had gone ahead, and the victims were eagerly awaiting their 50% in cash (albeit having to pay 10% in fees for the privilege), they then started to chase up their cash. There were delays after delays.

After many weeks of frustration, the victims were then told they had to apply for a loan. They were told that this was merely a formality – paperwork to ensure that the cash would not be taxable by HMRC. And they were sent loan application forms from a company called Marazion – Stephen Ward’s company in Cyprus.

Victims were then forced to sign a five-year Marazion loan agreement. And forced to sign a five-year Evergreen “lock in”. Clearly, this was designed to stop victims from transferring out of Evergreen before their Marazion “loans” were paid off.

Evergreen recently sent out a notice to victims advising them the Evergreen Scheme is being wound up. (Surprise surprise!!). Here is the Evergreen notice with my comments in bold:

Evergreen Retirement Trust – closure and winding up

We are writing to inform you that the Evergreen Retirement Trust (“ERT”) is being closed and wound up with effect from Friday, 6 April 2018. So why, just days earlier, were you writing to victims to tell them could take their 30% tax-free lump sum and transfer out? You knew this day and the winding up would eventually take place – and why as well as when. And yet you have misled and distressed a large number of your victims knowingly and intentionally.

Why is ERT being wound up? We all know exactly why ERT is being wound up. HMRC realised that the scheme was operating pension liberation fraud in partnership with Stephen Ward of Premier Pension Solutions early on – in 2012 – so removed it from the QROPS list in November 2012. Your Manager’s Report for the year ended 31.3.16 refers to “concerns raised by HMRC” but you do not disclose the fact that you had been caught and the scheme removed from the QROPS list as a result. The other reason the fund is being wound up is that you have run out of excuses now the five-year lock-in period is up. In your Manager’s Report, you claim that service contracts were entered into by Evergreen Retirement Trust for admin, trustee and other services which have minimum fixed fees. But you have never provided evidence of these alleged “contracts” – nor have you explained why you have carried on paying these unaffordable costs. You have been trying to obscure the fact that 41% of the underlying assets of the fund were in Penrich and Spectrum and that this is where the loan funds came from. You have for years tried to pretend that you knew nothing about the Marazion loans. But the original trustee – Perpetual Trust – even had a virtually identical logo to Marazion!

We have been considering the future of ERT for some time. Despite our best efforts, ERT has not been as successful as we had originally hoped. This is the understatement of the century surely? Best efforts? I would really hate to see your worst efforts. You’ve spent the last five years telling members they can’t transfer out because of the five-year term Marazion loans – and knowing all along that you were always going to wind the scheme up because there was nothing to be done about at least 41% of the scheme being in illegal loans using Penrich and Spectrum funds – the underlying assets of the scheme.

The main reasons for this have been the inability to attract new membership into ERT and the increased compliance costs arising from transition to the new, more rigorous, Financial Markets Conduct Act regulatory framework that now applies to it. And what exactly did the “more rigorous regulatory framework” say about the scheme operating pension liberation fraud as part of the scheme?

Although we explored a number of avenues to resolve these issues, we ultimately determined that it would be in members’ best interests for ERT to be wound up and the scheme brought to a close. What would have been in the members’ best interests would have been to allow the members to transfer out several years ago when we first asked Evergreen for transfers. It is clear from your own accounts that you have indeed allowed 10 people to transfer out £500k worth of funds last year – presumably these were people without Marazion loans?

What happens next? Until 6 April 2018, ERT will continue as normal and you will have the same rights and benefits as before. On and from 6 April 2018, the assets in your member account will be realised and the proceeds paid into your nominated bank account after the deduction of applicable fees, expenses and any taxes in respect of the winding up process. So for people under the age of 55, you are proposing triggering an unauthorised payment which would be taxed at 55% by HMRC? Unbelievable.

A final set of scheme financial statements will be prepared, audited and sent to all members, and the relevant regulatory notifications will be filed. So how are you going to account for the Marazion loans? You must surely realise that this is a huge problem and you can’t just keep ignoring it and pretending you weren’t involved in this aspect of the scam.

To allow this process to occur in an orderly fashion, members will not be able to request transfers (except as set out below) or make further contributions, and benefit payments will be put on hold pending the final distribution of wind up proceeds. So how are you going to account for the Marazion loans? How will these be factored into the wind-up proceeds?

Some of the scheme’s assets are illiquid and as a consequence the winding up process could take some time. Why on earth are any of the assets illiquid? No pension scheme assets should be illiquid. You have been dealing with this matter for more than five years and you always knew that there was a purported five-year lock-in, timed to coincide with the five-year term of the Marazion loans. So why on earth invest in illiquid assets?

Based on current market conditions, we expect the winding-up process to be fully completed and a final distribution to be made around December 2019. So what you are saying is that you never intended to honour the five-year lock-in in the first place. You wanted a seven-year lock-in so that you could continue to hide the Marazion loans.

Prior to the final distribution of wind up proceeds, partial distributions may be made as assets are realised, provision for anticipated costs are made and as such funds become available to make those partial distributions. In 2016 you purchased £5.87 million worth of assets. Why – in the full knowledge that you were going to wind the fund up a couple of years later – did you buy illiquid assets?

What are my options? Unless you advise us otherwise by 6 June 2018, you will receive your winding up proceeds in cash to the bank account nominated in accordance with the requirements noted below once the winding up process above has been completed. For members under the age of 55, you cannot do this as it will trigger an unauthorised payment and the victims will get taxed at 55%.

For members who have not been tax resident outside the UK for five clear and consecutive UK tax years, receiving winding up proceeds in cash could have adverse UK tax consequences. We are therefore offering members the option of having their winding up proceeds transferred to another QROPS or registered UK pension scheme instead of being paid directly in cash. But you are asking other trustees to accept in specie transfers of unknown provenance (by your own admission at least half of the fund is illiquid) and with at least 40% of the fund subject to a fund which provided the Marazion loans.

These members are strongly encouraged to obtain professional tax advice from an independent and qualified UK tax adviser before making any decision. Of course they do – including tax advice on the 50% Marazion “loans” which you facilitated and of which you have always been not only aware but in which you have been complicit.

If you wish to have wind-up proceeds transferred to another scheme you will need to provide us with notification by 6 June 2018. And which “other scheme” is going to accept illiquid – possibly toxic – assets bought by a clearly inept and irresponsible trustee which has also facilitated pension liberation? Any members with a Marazion loan will be deemed to be “high risk” by any new pension trustee and a mechanism for repayment of the loan will need to be put in place.

Please note that transfer of the assets will occur over time, in line with the distribution of the funds to other members. What do I need to do? If you have been tax resident outside the UK for five or more clear and consecutive tax years then all you need to do is provide us with updated proof of identity and address documentation together with official bank documentation evidencing a nominated bank account held in your name (see the Appendix to this letter for more details about this requirement). But that only applies to those over the age of 55 and without a Marazion loan presumably?

Once that documentation has been provided, you will receive your winding up proceeds into your nominated bank account as funds become available through the winding up process. You will also receive copies of the final audited financial statements in due course. Do you mean once you have figured out how to account for the Marazion loans funded by Penrich and Spectrum?

If you have not been tax resident outside the UK for five complete and consecutive UK years, we strongly encourage you to seek professional tax advice from an independent qualified UK tax adviser. You should then advise us whether you wish to receive your winding up proceeds in cash, or transfer your member account to another QROPS or registered UK pension scheme. So what are you going to do if no trustee will accept an in specie transfer and the members are under the age of 55?

If you still wish to receive your proceeds in cash, you will need to provide us with the documentation (including official bank documentation evidencing a nominated bank account held in your name) referred to in the previous paragraph. In either case, if you wish to transfer your member account to another QROPS or registered UK pension scheme, please advise us before 6 June 2018 and we will send you the relevant transfer forms. It is now clear, beyond any shadow of a doubt, that you must immediately account for the Marazion loans and show how these are accounted for in the scheme accounts. You have avoided this question for several years and now is the time finally to come clean.

If the trustee of the other scheme agrees, a proportion of your transfer to that scheme might comprise a transfer of underlying investments of ERT, as well as cash. I doubt any receiving scheme will be thrilled at the thought of accepting any of ERT’s underlying investments in the full knowledge that approaching 50% of the original transfers were given out in fraudulent “loans”.

Please be aware that all payments made out of the scheme, including in the winding up process, are required to be reported to HM Revenue & Customs.

Who should I contact with questions? If you have any questions about the winding up process, you can contact our customer services team by email at transfers@evergreentrust.co.nz, by telephone on +64 3 974 1505 or by post to PO Box 36270, Merivale, Christchurch 8146. Please note that we do not provide financial advice or tax advice. Yours sincerely, The Directors Evergreen Capital Partners Limited So, will Evergreen finally answer the questions about the Marazion loans? Fully and transparently? I doubt it. And I would like to remind Evergreen that scammers are criminals.

Being scammed out of a big chunk of your pension once is bad enough. But TWICE is awful. Double pension scam victim Jessica M.J. talks about her experience and gives other victims advice about how to cope with the stress that results from being a pension scam victim.

Jessica was scammed by Continental Wealth Management – one of Pension Life’s top-ten worst scammers – into the Evergreen QROPS scheme. Continental Wealth Management was acting as the cold callers and lead generators to Stephen Ward’s firm Premier Pension Solutions. Evergreen was a New Zealand pension scheme which was being used for pension liberation fraud using Ward’s pension loan company, Marazion. Jessica did not get (and was not offered) a loan.

Jessica was brave and generous enough to share her own story – which, sadly, was so typical of hundreds of other cases. However, she was one of the few who were actually scammed twice by Continental Wealth Management. She spoke of her own feelings: “I was very angry. I felt betrayed, cheated.”

After losing a third of her pension, Jessica was then moved by Continental Wealth Management to a Malta QROPS and put into an Old Mutual International insurance bond (which she didn’t need and couldn’t afford – and only served to earn the scammers a hefty commission). By investing what was left of the fund in high-risk, professional-investor-only structured notes, half of what was left of Jessica’s pension was then destroyed. So she ended up losing two thirds of her hard-earned retirement savings.

Continental Wealth Management collapsed at the end of September 2017, leaving hundreds of victims with their pension funds in ruins and facing poverty in retirement. Old Mutual International, Generali and SEB – the life offices who allowed this devastation to happen and stood idly by while the structured notes destroyed the victims’ funds – have done nothing to compensate the victims for their losses.

Jessica has advised the public:

“There’s a lot of scammers out there – check ’em out!”

Sadly, if Jessica had known the questions to ask, the warning signs were there from the start. Continental Wealth Management was not licensed for investment advice. Few of the so-called advisers had any qualifications relevant to financial advice. The investments were professional-investor-only structured notes provided by RBC, Commerzbank, Nomura and Leonteq – among others. Continental Wealth Management used life bonds provided by Old Mutual International, Generali and SEB. These bonds served absolutely no purpose except to pay the scammers huge commissions. Dealing instructions had forged client signatures and the advisers lied about the losses when they were first reported claiming they were “only paper losses, and would recover”.

Beddoe proceedings: arguably (apparently) Dalriada could have been pursued by Ark victims without MPVAs for not pursuing repayment from those with MPVAs and conversely could have been pursued by Ark victims with MPVAs. So, to be on the safe side, they spent a quarter of a million quid of the victims’ funds on the Beddoe proceedings in the High Court.

And here we need to look at the meaning of the terms – MPVA and sharp stick:

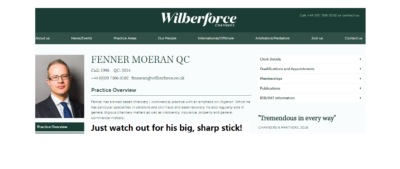

Sharp Stick: Fenner Moeran’s extremely offensive statement that Ark victims should be beaten with a sharp stick (upon which neither the judge, Sarah Asplin, admonished him nor upon which Keith Bryant, the Ark victims’ QC, challenged him)

MPVA

MPVA is an anacronym for “Maximising Pension Value Arrangements” – a euphemism for pension liberation. The rules are that if a person is under the age of 55, he or she can’t access any part of their pension without incurring an unauthorised payment tax charge of up to 55%. So all pension liberation scammers think up clever ways of fooling potential victims into believing there is a legal “loophole” to circumvent this rule.

The point of a pension liberation scam is not to provide members with a bona fide pension scheme designed to provide an income in retirement, but to make the scammers loads of money. First there is the transfer fee: in the Ark case it was relatively low at 5% – although Stephen Ward was charging an extra fee on top of that of up to £2k per transfer.

And then there are the investment kick-backs. We still don’t know how much the Ark scammers earned out of the speculative, illiquid, high-risk properties they purchased in various dodgy offshore jurisdictions. But it will have been very lucrative. In subsequent scams, the scammers earned huge commissions such as 20% from Dolphin Trust; 30% from Park First; 46% from Store First.

By the time the Ark victims realised they’d been scammed it was too late and there was no parachute

The scammers always promise spectacularly high returns on the investments with assurances such as “guaranteed 8% per annum”. In the case of Ark, the victims were told they would receive up to 9% a year on the growth of the value of “high-end London residential properties” in which the pensions would be invested. This, of course, was a lie. But by the time alarms started to ring and the victims realised there was no way out of this toxic flight with no parachute, it was too late.

But let us revert to the portion of a transfer which is liberated. This can range from 5% to 85% depending on the structure of the scam. And it is given various names or labels such as “cashback”; “thank you”; “refund of fees”; “trousers”; “loan”. The favourite word used is “loan” because the scammers claim that “loans are not taxable”. There is no intention for the money ever to be paid back – that isn’t the point of the exercise. The scammers know the victims would never be able to repay the funds.

The use of the word “loan” in some schemes is merely a marketing term used to fool people into believing they won’t be taxed on the money. And the scammers have no interest in whether the victims ever get taxed or not – because by the time HMRC gets around to sending out tax demands, the scheme will have collapsed and the scammers will be long gone and far ahead on their next scams. They never stick around to help mop up the train wreck left behind.

Often, the victims are surprised when they receive “loan” documentation and alarm bells start ringing. But the scammers assure the victims that this is “just a paper exercise” or “administration to make sure HMRC don’t try to tax the money – because loans aren’t taxable“.

In the Ark scheme, the victims were told the amounts liberated would not be taxable because they didn’t come from the members’ own scheme, but from another scheme. And this is why 14 schemes were set up to work in pairs so that up to 99 people in each pair of schemes could swap cash from their transfers. So this was an artificial mechanism structured purely to operate the liberation – using the label “MPVA” to dress the payments up as something more glamorous and bona fide than just a dollop of unauthorised cash in a person’s trousers.

Very few of the victims were told their cash would ever have to be paid back. The MPVA agreements never once mentioned the word “loan” but did mention the word “discharge” and suggested that the MPVA would be automatically “discharged” after a period of years.

Some victims were told the MPVA would be settled or repaid out of the growth that the Ark pension would enjoy (because of the wonderful investments!). It was explained that the MPVA would grow at 3% a year but the pension fund would grow at 9%. But the member would never have to pay the MPVA off out of their own pocket.

Other victims were told the MPVAs would never have to be paid at all because of the reciprocal nature of the transfer/payment structure. It was explained thus: two “paired” members in different schemes would each have a reciprocal MPVA of – say – £50k. If they both decided they never wanted to pay the MPVAs back, they would just treat them like equal IOUs and agree to simply tear them up.

The Tolleys authoritative manual on pensions taxation by Stephen Ward

Now remember, the victims weren’t told these things by any old spivs – they were told them by Stephen Ward of Premier Pension Solutions and his various accomplices (e.g. Fraser Collins, Terry Tunmore, Paul Clarke etc). Stephen Ward was back then – and still is now – a regulated financial adviser of many years’ experience, as well as the author of the Tolleys Pensions Taxation Manual, (and Level 6 CII qualified).

The same assurances were also given to numerous victims by George Frost, of Frost Financial, a regulated mortgage and insurance broker. And the victims who received the advice on the merits of entering into the Ark scheme believed they had every right to believe and trust professional, qualified and regulated advisers who assured them the MPVAs would never have to be repaid and that their pensions would be safe and secure.

HMRC does not care whether a sum of money accessed from a pension before the age of 55 is called a loan, thank you, cash back, fee refund, MPVA or any other euphemism for “liberation”. They don’t care whether it is repayable or whether it is ever repaid or not. They don’t care whether it comes directly from the member’s pension scheme, or from somebody else’s pension scheme, or via some convoluted arrangement designed to conceal the source of the money – such as Stephen Ward’s Evergreen/Marazion pension/loan scam. If a member makes a pension transfer and receives a sum of money as a result – irrespective of where it comes from – HMRC will issue a tax demand of up to 55%.

To illustrate how pension liberation scams range from the very simple and transparent to the highly complex and opaque, here is an example of one arrangement which Stephen Ward and his merry men, Alan Fowler and Bill Perkins, were involved with in 2013 – after Ark, Evergreen, Capita Oak and Westminster pension scams had all been suspended:

Thanks to you both for your understanding…. Am unused to non delivery! The arrangement I heard about today works like this as an example (ignoring fees) and this is the simplistic version …

Client borrows 16k or thereabouts (this is available in the package)

He gets a non recourse loan (which will not be repaid) of £84k

He buys shares in Xco for £100k. These are listed on the CISX (name is Elysian)

Transfers £100k to James Hay SIPP

SIPP pays member £100k for the shares

Member repays the 16k and trousers £84k

My IFA connection has done 40 of them so far. Advice to transfer to the SIPP is from an FCA regulated IFA. James Hay and Suffolk Life know the full structure and are happy with it.

Regards Stephen

The FCA-regulated IFA to whom he was referring was Angela South of Magna Wealth. She soon made a hasty exit from the collaboration with Stephen Ward when victims realised this was a scam and threatened to report her to the Serious Fraud Office. Victims who participated in this scam have now received tax demands from HMRC and Elysian Fuels is now worthless.

SHARP STICK

Dalriada’s QC, Fenner Moeran, seemed like a very sharp cookie. His skeleton argument (which we never got to see), and his opening speeches, started with the assumption that the MPVAs were definitely loans; that there was no question that they were loans and that the members knew and accepted that they were loans.

The judge, Sarah Asplin, accepted this without question and there was no debate on the subject. Kim Goldsmith’s QC, Keith Bryant, sat as quiet as a corpse and made not one single interjection or objection – even though he was sitting next to Kim who knew perfectly well – and must have told him – that the victims were not aware the MPVAs were loans. Indeed, they were categorically assured that the MPVAs would never have to be repaid.

Even more astonishing was the fact that Dalriada was aware the victims never knew the MPVAs were loans. Dalriada’s Sean Browes and Brian Spence, as well as Pinsent Masons’Ben Fairhead and Ian Hyde, had attended various meetings with the Ark Class Action and gone through this issue numerous times. They were also fully aware that one victim was horrified when she was subsequently told the MPVA was a loan and she immediately called Dalriada and asked to repay it. But Dalriada had refused.

Furthermore, dozens of Ark Class Action members had completed HMRC’s 10-point questionnaire (the Q10) which specifically asked about the arrangements and what they had been told about the need to repay the MPVAs. This is evidenced at HMRC’s question 8:

8: “DETAILS OF WHAT YOU WERE TOLD ABOUT THE NEED TO REPAY THE LOAN”

Here is a typical response to this question by one of the victims:

“I was told that although on paper it would be an official 25 year loan, that because of the nature of the way the loans were set up, i.e. the quid pro quo arrangement, whereby as one person received their monies from the other members scheme and vice versa, if there was a request for any monies to be repaid in the future from each member, each would tear up each other`s IOU and be quits, so to speak, as already stated.”

Stephen Ward – BA (Econ), ACII, APFS, APMI, ex examiner for the pensions management institute and for the CII, confirmed that the Ark scheme was designed by specialist pensions lawyer Alan Fowler – head of pensions at Stevens and Bolton.

Ward went on to explain how the MPVAs worked: “The best way to understand this is in terms of my lending you £100 and you lending me £100. If I do not repay you and you do not repay me then we are both in an equal position. Conversely, if I repay you and you repay me then the position is identical to that which would arise if neither party had repaid the other”.

These statements have been made to HMRC by Ark victims on countless occasions – and Dalriada has always been perfectly well aware of this. And yet Fenner Moeran used his sharp stick to knock these evidenced facts completely off the table – so that the judge was never made aware of them. Mind you, Keith Bryant QC was no better – because he didn’t bring them to the judge’s attention either.

I would go so far as to observe that Fenner Moeran should have used his sharp stick to point the judge to these evidenced facts – and Dalriada should have made sure he did so. By omitting to do so, both Fenner Moeran and Keith Bryant allowed the judge to come to the incorrect conclusion that:

“members who received the MPVA loans agreed to repay them. That’s the point of a loan. It’s not a gift. They cannot now complain about having to repay them. They can complain about having to repay them earlier, but that’s a cashflow issue which is vastly overwritten by the capital harm that is suffered by the non-recipient members”

Fenner Moeran merely leaned on his sharp stick and did nothing to correct the judge. As I was sitting behind him, I couldn’t see whether he was smirking – but I have a feeling he might have been. The judge was wrong on three counts:

The members with MPVAs did not agree to repay them – they were told they would never have to

They can most certainly now complain about being asked to repay them as they were never told they would have to and did not budget to do so

The capital harm suffered by members without MPVAs was mostly caused by Dalriada who did not reject their transfers after 31.5.11 but allowed transfers to continue right up until the end of August 2011

Having glossed over the facts smoothly, and directed the judge to her incorrect conclusion, Fenner Moeran then addressed the issue of ascertaining whether the Ark victims were in a position to be able to afford to repay the MPVAs. And then he produced, with a confident flourish, his pièce de résistance:

“The chances of getting ascertainably or enforceably more accurate information increases when you have the sharp stick of litigation behind it. If we want to see if we’re actually going to get any of this money back, the chances are that we’re going to have to wave a very large stick“

Fenner Moeran ought to be an intelligent person. In the full knowledge that a few feet to his right sat Kim Goldsmith, an Ark victim who had gone through six years of hell courtesy of Stephen Ward and George Frost and all the other scammers, and that a number of other victims were sitting at the back of the courtroom, he still made such an unbelievably stupid and offensive statement. He apologised later “I deeply and sincerely apologise for any misunderstanding or upset caused”.

But the damage had already been done – and you can’t un-say what has been said – especially when every word is recorded and transcribed. On behalf of Dalriada Trustees, he had deliberately misled the judge, and then proceeded to demonstrate clear contempt for the suffering of the Ark victims.

Interestingly, the judge had not remonstrated with Moeran for his crass comments – and Keith Bryant had not objected to the stupid and insensitive words. Throughout the rest of the proceedings, the judge remained – in my view – dominated and steered by Moeran. No attempt was ever made to disclose the truth about what the victims were told about repayment of the MPVAs by Stephen Ward, George Frost, Andrew Isles or Alan Fowler. And no explanation was ever given as to why Dalriada had not pursued these parties for having duped, misled and defrauded the Ark members.

This may seem like a completely off-topic piece of this report, but please stick with it – it will be worth it because it is the whole point of this report. Nearly 18 months before the Ark/Dalriada/Beddoe proceedings in the High Court, another case was heard: Royal London v Hughes. A pension scammer had tried to do exactly what the Ark scammers had done so successfully and profitably for nearly a year: transfer hundreds of secure pensions into a pension scam. But one ceding provider – Royal London – had blocked a transfer request. They strongly suspected the receiving scheme was a liberation scam – unlike the many ceding providers in the Ark case who handed over hundreds of transfers willy-nilly without question or due diligence – the worst of which was Standard Life.

Hughes complained to the Pensions Ombudsman that her transfer request had been blocked by Royal London. The Ombudsman did not uphold her complaint because he agreed with Royal London that the receiving scheme had all the classic hallmarks of being a scam – including the fact that the scheme had been registered as an occupational scheme and Hughes was not genuinely employed by the sponsoring employer. Exactly the same as Ark (and many of the subsequent scams).

Counsel for Royal London argued that “Hughes had to be an “earner” to be able to transfer”. He tried to support the Ombudsman’s view that the legislation required Hughes to be an earner in relation to a scheme employer”. This counsel obviously knew well that victims were made all sorts of promises and assurances and often not told the truth about the arrangements within pension scams.

Royal London’s QC would have been aware of the Ombudsman’s concerns that pension liberation may well have been behind Hughes’ enthusiasm to transfer her pension. And he will have known only too well that potential victims were systematically lied to and probably told that their “loans” (or whatever euphemism was used) were not repayable. And he would have known that the intended liberation “loans” were never intended to be repaid and that the victims would be told that the loans never needed to be repaid.

This QC will have been thoroughly briefed by his clients, Royal London, and may even have consulted with the Pensions Regulator who would have given him thorough details on how pension liberation scams worked.

So this particular QC had intimate, first-hand knowledge of how pension liberation schemes worked in general and represented Royal London in their quest to defend their right to prevent further victims of pension liberation scams. He also knew intimately how Ark worked in particular.

Fenner Moeran of Wilberforce Chambers

He knew perfectly well that the victims were told they never had to repay their loans (or MPVAs/cash backs/thank you’s/trousers). And he knew that the Ark MPVAs were supposed to be “discharged” from growth in the schemes and NOT from the victims’ own pockets – as reported by Justice Bean. But he failed to bring this to the judge’s attention.

Who was this QC? I will give you a clue – he had a big, sharp stick. Perhaps he should have gone to Specsavers and read the MPVA agreement where this was clearly stated.

My name is Nikki Mitchell. Lets peep behind the scenes at life at Pension Life, fighting pension scams. I’m the newest member of the team. I started in June 2016 – there was a lot to learn in six months. I am PA to Angie, but most importantly I handle a wide variety of tasks.

Angie has been defending people scammed out of their pensions since 2013. My colleague Sue Halfyard’s role is member administration. She completes all the essential documentation that we, HMRC, Dalriada Trustees and the solicitors need. Sue also liaises with HMRC on the unauthorised payment tax appeals and helps Angie prepare for the Tax Tribunals. Elizabeth is our website and blog-writer and is currently on maternity leave.

Our website is not only a place to inform people of the work we do, and how we can help people who have fallen foul of pension scammers, but it also serves as a platform to warn others about scammers, so that hopefully we can stop them losing their life savings.

We are currently dealing with over 30 different schemes:

Ark; Axiom UP; Barret and Dalton; Baxendale Walker; Capita Oak; Confiance; Continental Wealth Management; EEA/Concept Trustees; Elysian Fuels/SIPPS; Evergreen QROPS; Headforte; Henley; Holborn Assets/Gower Pensions; Holbrook Capital; KJK Investments; Ledger and Simmons; London Quantum; Malvern; Mendip; RL360; Hansard/Trafalgar; LM; Optimus Retirement Benefit Scheme No 1; Peak Performance; Pennines; Salmon Enterprises; Store First SIPPS; Trafalgar Multi Asset Fund/STM Fidecs; Tudor Capital Management; Westminster; Windsor Pensions.

Sadly, most months we hear about new ones.

Day to day work in the office consists of managing Angie’s crowded diary, keeping the accounts, liaising with members to keep them abreast of new developments, preparing scheme and member files for the legal teams, responding to the demands of HMRC and various trustees. I also work on campaigns to raise awareness of pension scams, or to campaign for changes in the law to protect pension investments.

My first few weeks passed in a whirl of new jargon and abbreviations – UTR, Q10, MPVA EIS, PCLS, etc. Some days I spend the day designing and completing databases with members’ information for the solicitors. Other days I’m number crunching the transfer and loan amounts for an individual scheme. Some days we all have to change direction as there has been an urgent development. A recent example of this was the Standstill Agreements sent out by Dalriada – the trustees of the Ark Pension schemes. Our first member received an agreement in August 2016. We have warned all the members that they will be receiving one, and worked with our solicitors to redraft the agreement to protect the members’ interests.

Being a small, busy team in a hectic office, there is never a dull moment. Aside from the daily nitty-gritty of the work, there are also the heart-breaking accounts of the members who have been scammed out of their pensions. Consequently, I have felt disbelief at the cruel contempt of the scammers. Reading members’ stories of how they were conned into investing their entire pensions or life savings into dodgy, illiquid schemes is utterly heart-breaking. Speaking to people who have lost everything – their homes, their marriages and their health – through the actions of these arrogant, greedy con-men fills me with horror.

The greatest shock to me since joining Pension Life has been how the scammers have continually got away with fraud and theft for years. Also, how ceding providers routinely transfer pensions with hardly even the most rudimentary checks. It has amazed me how so many different types of pension scams are allowed to be set up time and time again, with no thorough controls by HMRC or the regulators. Moreover, I can’t understand why it takes so long for the scams to be shut down – long after they have been identified.

We may be a small team here at Pension Life, but with the government’s recent realisation that cold calling needs to be outlawed and the consultation on pension scams:

EVERGREEN RETIREMENT TRUST QROPS PENSION SCAM AND MARAZION LOANS

THE WAY THE SCAM WORKED

When Ark got shut down in June 2011, Stephen Ward flew to New Zealand and set up the Evergreen NZ QROPS liberation scam with Simon Swallow of Charter Square. Ward also set up a “loan” company in Cyprus called Marazion. He also did a deal with two investment funds: Penrich and Spectrum. Expats would transfer their UK pensions to Evergreen and pay a 10% transfer fee. As soon as the transfer was complete, a loan – funded by either

Expat victims (mostly) would transfer their UK pensions to Evergreen and pay a 10% transfer fee. As soon as the transfer was complete, a loan – funded by either Penrich or Spectrum (to whom the loans were assigned) was arranged between Marazion and the member. The loan was for a fixed five-year term, and the member was made to sign a “lock in” agreement with Evergreen.

The loan interest was 8.5% compound (quarterly) and would mean that the original loan amount would increase by 50% by the end of the five years. Ergo, the maths worked like this at the outset: £100k transfer; £10k fees; £90k Evergreen fund; £50k loan. At the end of the five-year term, the Evergreen fund would either have increased, decreased or remained the same (in fact, it has decreased) and the loan would have increased to £75k. The member was offered the option to renew the loan for a further five-year term at a higher rate of interest.

For three years, Evergreen managed to avoid disclosing what the assets of the scheme actually were, but in 2015 they had no choice other than to disclose that 41% of the scheme’s assets consisted of Penrich and Spectrum. After a lengthy and detailed complaint to the NZ Ombudsman, the complaint against Evergreen was not upheld and the victims were originally left “locked in” until 2017. However, Evergreen has now moved the goal posts and the victims are locked in until they reach the age of 55. Evergreen was removed from the QROPS list by HMRC in November 2012.

THE IDENTITY OF THE MAIN PLAYERS

Stephen Ward of PPS/Marazion

Continental Wealth Management SL who acted as introducers

Simon Swallow of Charter Square

HOW THE MAIN PLAYERS WERE INVOLVED

Continental Wealth acted as introducers – and referred to the firm as the “sister” company to Ward’s company Premier Pension Solutions; PPS processed the transfers and loans; Swallow of Charter Square managed the scheme.

Fighting pension scams needs to be done logically and methodically. Decent advisers need to use high standards to help fight scams. If these standards become the norm, the scammers won’t survive and flourish so easily.

Fighting pension scams needs to be done logically and methodically. Decent advisers need to use high standards to help fight scams. If these standards become the norm, the scammers won’t survive and flourish so easily. Lots of offshore advisers

Lots of offshore advisers

and many others such as

and many others such as  Fighting pension scams – why qualifications are so essential

Fighting pension scams – why qualifications are so essential You wouldn’t go to an unqualified solicitor would you? So don’t use an unqualified financial adviser. Being qualified goes hand in hand with being regulated.

You wouldn’t go to an unqualified solicitor would you? So don’t use an unqualified financial adviser. Being qualified goes hand in hand with being regulated.

Fighting pension scams:

Fighting pension scams:  LCF Bond, Blackmore Bond, Blackmore Global Fund, LM, Axiom and Premier New Earth

LCF Bond, Blackmore Bond, Blackmore Global Fund, LM, Axiom and Premier New Earth

Serial

Serial  Firms that give unlicensed advice are breaking the law. Unlicensed advisers often use insurance bonds. These bonds pay high commissions. The funds these advisers use also pay high commissions. The advisers get rich. The clients get fleeced. The funds get destroyed. Insurance bonds such as

Firms that give unlicensed advice are breaking the law. Unlicensed advisers often use insurance bonds. These bonds pay high commissions. The funds these advisers use also pay high commissions. The advisers get rich. The clients get fleeced. The funds get destroyed. Insurance bonds such as  Unlicensed firms

Unlicensed firms  People can avoid being victims of

People can avoid being victims of

If you have been following Pension Life´s blogs, you will know that we have been conducting a series of investigations into

If you have been following Pension Life´s blogs, you will know that we have been conducting a series of investigations into

As shown in the image above there were lots of links to social media, so I chose to follow the Facebook one first. Here I was able to find an image of Graeme Callaghan of Callaghan QROPS Spain (and I also found out they were Callaghan QROPS Portugal too).

As shown in the image above there were lots of links to social media, so I chose to follow the Facebook one first. Here I was able to find an image of Graeme Callaghan of Callaghan QROPS Spain (and I also found out they were Callaghan QROPS Portugal too).

Welcome to my world – and the four letter word that sends a chill down most people’s spine:

Welcome to my world – and the four letter word that sends a chill down most people’s spine:  My friends at

My friends at

EVERGREEN RETIREMENT TRUST QROPS SCAM – HOW DID IT ALL WORK?

EVERGREEN RETIREMENT TRUST QROPS SCAM – HOW DID IT ALL WORK? CWM assured the victims that the 50% cash would not be taxable because the scheme was set up and run by international pensions expert and author of the Tolleys Pensions Taxation manual Stephen Ward of Premier Pension Solutions.

CWM assured the victims that the 50% cash would not be taxable because the scheme was set up and run by international pensions expert and author of the Tolleys Pensions Taxation manual Stephen Ward of Premier Pension Solutions. Victims were then forced to sign a five-year Marazion loan agreement. And forced to sign a five-year Evergreen “lock in”. Clearly, this was designed to stop victims from transferring out of Evergreen before their Marazion “loans” were paid off.

Victims were then forced to sign a five-year Marazion loan agreement. And forced to sign a five-year Evergreen “lock in”. Clearly, this was designed to stop victims from transferring out of Evergreen before their Marazion “loans” were paid off. Why is ERT being wound up? We all know exactly why ERT is being wound up. HMRC realised that the scheme was operating pension liberation fraud in partnership with Stephen Ward of Premier Pension Solutions early on – in 2012 – so removed it from the QROPS list in November 2012. Your Manager’s Report for the year ended 31.3.16 refers to “concerns raised by HMRC” but you do not disclose the fact that you had been caught and the scheme removed from the QROPS list as a result. The other reason the fund is being wound up is that you have run out of excuses now the five-year lock-in period is up. In your Manager’s Report, you claim that service contracts were entered into by Evergreen Retirement Trust for admin, trustee and other services which have minimum fixed fees. But you have never provided evidence of these alleged “contracts” – nor have you explained why you have carried on paying these unaffordable costs. You have been trying to obscure the fact that 41% of the underlying assets of the fund were in Penrich and Spectrum and that this is where the loan funds came from. You have for years tried to pretend that you knew nothing about the Marazion loans. But the original trustee –

Why is ERT being wound up? We all know exactly why ERT is being wound up. HMRC realised that the scheme was operating pension liberation fraud in partnership with Stephen Ward of Premier Pension Solutions early on – in 2012 – so removed it from the QROPS list in November 2012. Your Manager’s Report for the year ended 31.3.16 refers to “concerns raised by HMRC” but you do not disclose the fact that you had been caught and the scheme removed from the QROPS list as a result. The other reason the fund is being wound up is that you have run out of excuses now the five-year lock-in period is up. In your Manager’s Report, you claim that service contracts were entered into by Evergreen Retirement Trust for admin, trustee and other services which have minimum fixed fees. But you have never provided evidence of these alleged “contracts” – nor have you explained why you have carried on paying these unaffordable costs. You have been trying to obscure the fact that 41% of the underlying assets of the fund were in Penrich and Spectrum and that this is where the loan funds came from. You have for years tried to pretend that you knew nothing about the Marazion loans. But the original trustee –

After losing a third of her pension, Jessica was then moved by

After losing a third of her pension, Jessica was then moved by