This week Henry Tapper wrote a blog entitled, “The wheels of the law turn (too) slowly”. He exposes the fact that when it comes to financial crime the justice system in place just isn´t enough. I think he was being generous with his title. The wheels of the law don’t just turn slowly – they just don’t turn at all. Friendly Pensions has been in the news this week.

In the case of Friendly Pensions, we know ringleader David Austin is guilty of setting up 11 fake schemes, with toxic investments including a truffle farm. We know that he and his partners in crime, Susan Dalton, Alan Barratt and Julian Hanson (also connected to the Ark Scam), are guilty of scamming 245 pension savers out of £13.7 million. We knew all of this back in January 2018, yet no arrests have been made!

“David Austin, 52, has been banned from serving as a pension trustee and disqualified from working as a company director for 12 years. His business partners Susan Dalton, Alan Barratt, and Julian Hanson have also been barred from trustee roles.

David Austin’s daughter, 25-year-old Camilla, has been banned from serving as a director for four years for helping him with the scheme.”

They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

Camilla Austin was a central part of the operational side of the Friendly Pensions scam. She and a number of her girlfriends went into nursing homes and approached elderly, frail and vulnerable elderly people. They easily conned them into signing transfer request forms – all that is required to get their hands on millions of pounds’ worth of pension funds. And, of course, we all know that the ceding providers do nothing to stop fraudulent transfers.

As Henry points out, banning these people from acting as trustees or directors, does little to deter past, present and future pension scammers. A ban is barely a slap on the wrist as far as we are concerned; these scammers can still launch any number of future dodgy schemes by simply finding the next crooked stooge – just as XXXX XXXX used the idiotic Karl Dunlop to be a director in the Capita Oak scam.

Keeping pension savers safe from financial crime should be at the top of the list – but, instead, it is at the bottom. Pension scammers are left free to commit their crimes over and over again. Take Julian Hanson: he was busily scamming dozens of Ark victims out of more than £5.3 million worth of pensions back in 2011 and 2012, yet he was not prosecuted or jailed. Hence, he was still able to get “friendly” with David Austin and go on to scam hundreds more victims out of their pensions.

Despite investigations being made into these schemes, Ward was still able to go on and create the CWM monster scheme that saw around 1,000 victims conned out of their pension funds. Ward is hovering somewhere between his collection of luxury villas in Florida and the Spanish Costa Blanca – but at least he is no longer doing pension transfers. Over the past nine years, Ward can be linked to dozens more pension scams that have left thousands of victims’ funds decimated.

These cases are just the tip of the iceberg. We must not forget Philip Nunn and Patrick McCreesh´s investment scam Blackmore Global. This was in the wake of them doing the lead generation for the Capita Oak and Henley Retirement Fund scams. The Insolvency Service has wound up these schemes, yet Nunn and McCreesh remain free to defraud more victims as they have never been brought to justice.

David Vilka of Square Mile International was one of the main promoters of the Blackmore Global Fund scam. He “advised” dozens – possibly hundreds – of victims to invest their pensions in this scam (despite the fact that he is neither qualified nor regulated to give investment advice). Again, he has never been prosecuted or jailed, so still remains at large – free to continue scamming people out of their pensions.

You can see a depressing pattern here: these words are about cold, hard facts. The authorities are leaving known scammers free to keep scamming.

Victims of these scams have been left in misery and financial ruin. Some have taken their own lives. Yet the perpetrators, those guilty of these repeated financial crimes, are free to do as they please.

This area of financial crime really is where the wheels of the law don´t seem to turn. Shame there aren’t any regulators capable of doing any regulating, or law enforcement agencies capable of enforcing the law.

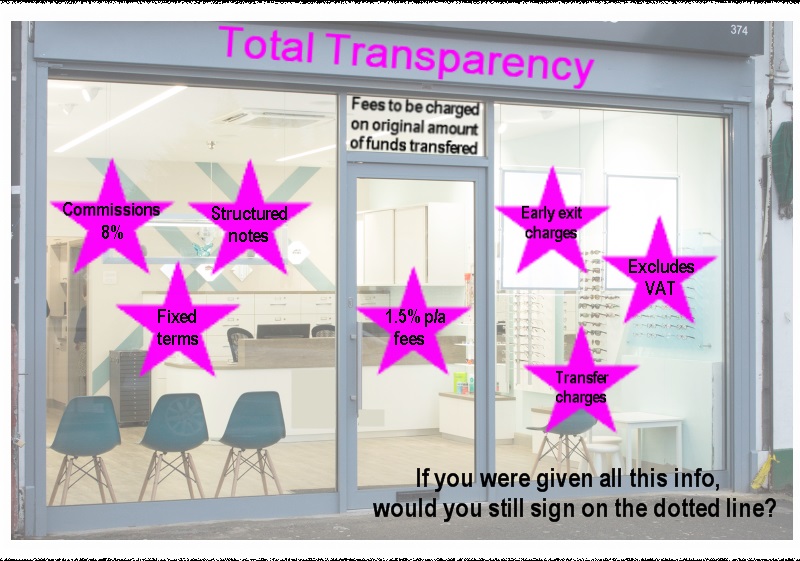

The financial services industry has failed with flyingcolours to achieve transparency – both offshore and in the UK. The single most important thing about any product or service is transparency – aka honesty. This is where the profession has tolerated – and even encouraged – bare-faced lying for years and continues to do so today.

There is nothing intrinsically wrong with overcharging – as long as the overcharger makes it clear he is openly trying to rip his customers off and the victim is consciously happy to be ripped off. Personally, I’d love to be able to sell my car for 25,000 EUR – but with its age, condition and mileage I know I’d struggle to get 5,000. However, a crafty, clever person could give it a makeover, a clockover, tell a few convincing porky pies – and some poor fool might pay over the odds for it.

Most of the victims I deal with tell me the same story:

the adviser said the “review” would be free

the adviser said the only charge I would pay would be 1.5% a year

the adviser said my fund would grow at 8% a year net of charges

the adviser never told me about the insurance bond

the adviser never told me he was going to invest my funds in high-risk, illiquid funds or structured notes

Most people describe their offshore adviser as being about as transparent as a pork chop and the “flying colours” of their achievements to be fifty shades of brown.

Champion campaigner against this sort of dishonesty is international king of transparency Andy Agathangelou – Founding Chair of the Transparency Task Force, the collaborative, campaigning community dedicated to driving up levels of transparency in financial services around the world. Andy writes for Investment Week and calls for total transparency from offshore advisory firms.

One of Andy’s key statements is: “the financial services industry as a whole has a moral, ethical and professional duty to behave transparently”. But I wonder if that is a bit like asking for World peace, an end to pollution, a cure for cancer or a reversal of global warming (and a solution to the Brexit problem).

In the UK, advisers are not allowed to charge commissions on the products they sell, meaning that they will (hopefully) choose the best investment for their client – as there is no financial incentive to chose one product over another. However, offshore advisers do not have these restrictions, meaning that when they are selling an investment they will inevitably choose the one that pays the most commission.

But are things really that squeaky clean in the UK? Does the “beady” eye of the FCA have any effect or is it merely a masking mechanism to cloak lack of transparency (aka lying) in a thin veneer of false security? Henry Tapper’s recent blog on the subject of the FCA’s investigation into 34 firms suspected of non-disclosure of investment charges reports:

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

One example was cited: Canaccord Genuity claimed its annual management fee was 1.25% plus a transaction commission of £30. But it turned out the 1.25% was just the beginning – then there were VAT and fund charges bringing the true cost nearer to 2.75%. Now, I know we women sometimes stretch the truth when it comes to our age, weight or clothes size – but Canaccord’s porky pie was that the real charges were actually twice what was claimed. That’s not just lack of transparency – that is naked dishonesty.

I had a browse through Canaccord’s funds and got bewildered by the range of costs – the annual charges seemed to range from 2.1% up to a whopping 4.34%. I’m just wondering whether an investor prepared to pay 4.34% for one of these funds might like to buy my car as well? After all, if they can throw their money away so easily, they surely can’t be bright enough to realise my rusty old heap isn’t worth 25k.

While I was in a browsing mood, I thought I’d have a wee look at Flying Colours. The company aims to provide super low-cost advice and investment funds and “negate the hidden costs in the market”. The website claims “I’m building a network of independent financial advisers with a shared vision – to improve the returns of UK investors. Join us.” But now I’ve got alarm bells ringing: a network? And who exactly is in the network?

A list of firms scattered across England from Bristol and Godalming to Liverpool and Skelmersdale – plus a few one-man bands. But they all claim to be “independent” financial advisers. How can they be independent if they are tied agents of Flying Colours? We are back to the “Wild West” offshore culture where members of a network are effectively “feral” and get up to all sorts of mischief due to lack of independence. And let us not forget that tied agents are illegal in Spain – and for good reason because the Spanish government knows that advisers simply cannot be independent if they are tied to one provider.

The Flying Colours network includes All Things Financial, Arch Financial Planning, CBG Financial Planning, Cullen Wealth Management, E-Crunch, Fit Financial Services, JAV Financial Planning, JBD Financial Planning, JRF Financial Planning, Lavelle Financial Services, Layfield Wealth Management, Mathew Burrows Financial Planning, NTW Financial Planning, Pepperells Wealth, S Fox Wealth Management, Sterling Financial Planning, The Royall Wealth Partnership and Tyrone Peters Financial Planning.

But how on earth does a coherent and effective compliance function work with 18 different firms scattered all across the country? (All of which are lying about their independence).

The Flying Colours website boasts: “We’re transparent about the charges you’ll pay for advice and investments. And there’ll be no hidden fees, ever.” But where are the fees and charges? I searched the whole website but couldn’t find out what they were. Because they were hidden.

Flying Colours recently made an ill-fated, abortive attempt to enter the offshore market (leaving considerable embarrassment and expense in its wake). Far from the claim of “starting strong relationships with a cultural fit and starting friendships“, Flying Colours ended up dumping the failure and retreating to UK-based “DIY” advice. Once Flying Colours’ offshore mess is cleared up, there will – no doubt – be a sigh of relief since Flying Colours was actually offering a more expensive version of the “cheap” investment advice process at 2% for investors with complex investments (so back to the same old, same old offshore “sophisticated” confidence trick).

What is there in Britain to protect consumers from lies; scams; lack of independence and transparency; weak compliance and unworkable investment offerings? Forget the FCA – they are permanently on a coffee break.

But what about the Insolvency Service? Isn’t that there to help protect victims from investment scams? More than a year ago, the IS commenced winding up proceedings against Store First for selling store pods to rogue SIPPS providers such as Berkeley Burke, Carey Pensions, Rowanmoor Pensions, London & Colonial and Stadia Trustees. So, we have thousands of victims of pension and investment fraud all left hanging – not knowing whether their investments are worthless or not. And this, of course, includes the Capita Oak and Henley scheme victims.

The lack of transparency about the store pods was, arguably, not the fault of Store First itself, but caused by the lies of the rogue promoters and “advisers” and the negligence of the SIPPS providers. A store pod is a great investment if the investor has a burning desire to invest in an illiquid, speculative asset – with the added benefit that he can also put his granny’s knick-knacks in there free of charge. While any honest adviser would have told the investors to invest their life savings in a low-cost, liquid, prudent fund – and any competent pension trustee or administrator would have refused to accept store pods as pension investments – the fact is that the backhanders set aside any common sense entirely.

Personally, I think the UK has a long way to go before it can claim to be entirely transparent. To get there, some sort of regulator would be helpful (forget the FCA – obviously) and an effective insolvency service would contribute to achieving meaningful reform. But while firms are still lying, obfuscating and cheating, we can’t really say that pension and investment scams only happen offshore. They are still very much on our doorstep.

Andy Agathangelou’s important work addresses many of the ills which blight offshore financial services. But he could do with a team of several hundred helpers to cover all the key expat jurisdictions. Offshore advisers – as well as UK-based firms – need to be 100% committed to their clients and take into consideration the future of the investments they make. They need to give their clients total transparency, not just on the commissions that will be applied but also on all other fees and charges.

Total transparency on all fees and commissions, before any transfers are made, would mean investors know exactly what they are getting into.The truth, the whole truth and nothing but the truth, is needed from day one! But it would also be exceedingly helpful if ALL UK-based advisers and fund managers adhered to this model.

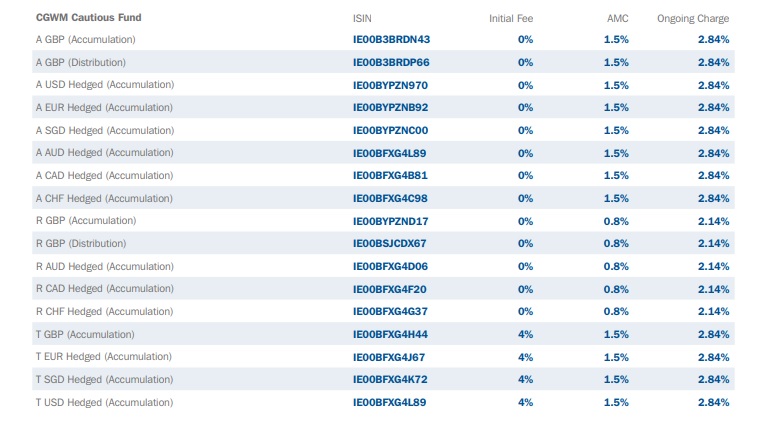

Going back to Canaccord Genuity’s opacity in the case of a client with a £700k portfolio, their non-disclosure of the VAT charges alone led to an additional cost of £10,500. £10,500 over 10 years amounts to £105,000 – quite a sizable chunk of the fund. You would have to have some very good investments to cover these costs AND increase the amount of the fund. Which, of course, is (or ought to be) the main aim of an investment!

Just for a laugh, have a look on Canaccord´s website at their list of fees, in particular, their cautious fund. 4.34% a year in charges. I wondered if this included VAT (being a “cautious” investor!).

So I decided I´d give them a call, just to clear up the confusion.

I was passed around various departments and ended up talking to a woman, who was – to put it plainly – pretty unhelpful. I asked about the charges and was told I would need to talk to a fund manager. I was asked how much I wanted to invest. I replied I´d need more information before I could commit to an amount. I was told there was a minimum investment of £250,00, but she still couldn´t tell me about the fees and charges.

I was put on hold, after she implied she might find out the answers to my questions. However, she must have forgotten me as no one came back and I was simply left hanging – listening to the sound of silence. Hopefully, Canaccord won’t forget me in the future.

Mind you, I didn’t have much luck with Flying Colours either. I chatted to their online “can I help you?” chap, Stephen Murphy, and asked him what the fund and advisory charges were. Murphy wanted to know why I wanted to know. I explained I was writing an article on Flying Colours’ fees. His reply was: “In regards to you writing an article around fund charges – we are not interested in featuring in an article as you are based in Spain – however, if you need further information around this you could contact Dani Greenfield on dgreenfield@flyingcolourswealth.com – she deals with the marketing side of our business.” Why so secretive I wonder?

Offshore advisers should be forced to put labels like these on their investments!

All this leaves us with a number of pressing, unanswered questions:

Is it acceptable that the financial services industry has failed with flyingcolours?

Is it tolerable that in some ways it is as bad in the UK as it is offshore?

Should consumers continue to tolerate unacceptably high charges from providers?

2,000 victims of fraudulent pension firms may be in with a chance of getting their funds back. In November, the FCA pushed for legal proceedings to go ahead against collapsed firm Avacade Limited, trading as Avacade Investment Options; and Alexandra Associates (UK) Limited, trading as Avacade Future Solutions.

Past prosecutions made by the FCA:

In 2016, the FCA proposed Alistar Burns of TaylorMade International should face a fine of £233,600, along with a ban. Earlier this year the case was seen in the Upper Tribunal, whilst upholding the ban, they chosen to lower the fine to £60,000. Here I believe the FCA made a good strong decision, but the Upper Tribunal then let them down by reducing the fine.

Court proceedings against Capital Alternatives have been taking place since July 2013. The FCA alleged that Capital Alternatives used “false, misleading and deceptive statements” to lure unsuspecting investors into four toxic, high-risk investments (scams) between 2009 and 2013. Despite the High Court deciding in February 2014 that the schemes/scams were collective investment schemes, only two out of the sixteen defendants in this case have made settlements. Since this date, the other defendants have been appealing the decision and no other monies has been recouped.

This case demonstrates the problems surrounding prosecutions made, often the funds that have been scammed can not be located. Or the scammers hire good lawyers and squander money away by appealing the decisions again and again, causing massive delays on payback. Victims of Fast Pensions are also stuck with this problem.

It is not yet know how much of the pensioners´ money has been lost. However, it is clear that Alexandra Associates was not licensed to carry out the advice given.

Craig Lummis, Lee Lummis and Raymond Fox are named in the legal proceedings for being “knowingly concerned” in the alleged wrongdoing of Avacade and Alexandra Associates. The court has ordered that any wealth held by the companies should be used to compensate the victims.

Once again, this case highlights unregulated introducers – Alexandra Associates – posing as qualified financial advisory firms, offering “free pensions advice” to lure in unsuspecting victims. In many of my blogs, I try to raise awareness of this trick: nothing in life comes for free. Often, firms offering this “free review”, will be rogue firms. Whilst the review may well come for free, there are often undisclosed fees and costs that will be imposed on the value of your pension fund – often making a large dent in your savings.

Unfortunately for the victims, they will not notice these – usually higher than average – fees until it is too late. Pension Life has many blogs that can help you to avoid being scammed, recommending the right questions to ask your adviser – before you sign your precious pension fund over.

You can also read blogs that will help you know what qualifications your adviser should have in order to be in an educated and qualified position to legally advise you on a pension transfer and pension investments. If in doubt, you can say “NO” and walk away from the deal, providing you have not signed anything (although there should be a 30-day cooling off period). Try reading up on past scams and becoming familiar with the names of scammers working in the pensions field.

Mark Steward, director of enforcement at the City regulator, said:

“The FCA is seeking injunctions, declarations and restitution orders to prevent further breaches in schemes which were unlawfully promoted to the public using false, misleading and deceptive statements.”

What a relief to hear this statement being made by an employee of the FCA (about blooming time!). Pension Life has long been waiting for the FCA to pull their finger out and start prosecuting pension scammes. With positive action like this, we could have had all the pension scammers locked up by Christmas and the victims´ monies returned to them. I’m sure that those who have lost so much to these crooks would be over the moon to be able to tell their families that they are once again financially secure (rather than financially ruined).

I have a long list of fraudulent pension firms and serial scammers that I plan to forward to the FCA (yet again). However, in reality, I do wonder how many cases the FCA can actually deal with in one year. Given their past track record, I’d say this is their annual big bust. The other scammers are safe and the victims will be left to wait and wonder when their cases will be dealt with.

On the plus side, the FCA have certainly had a busy month. Alongside their prosecutions, they have launched their ScamSmart campaign, teaming up with The Pensions Regulator. The campaign encourages people who are concerned that they may have been approached by fraudsters to report it via the ScamSmart website. It also raises awareness about checking that the firms consumers are using are regulated to provide the advice they are offering.

Here at Pension Life, we are constantly trying to raise awareness about pension scams. The Financial Conduct Authority – FCA – has also been busy. Pairing up with the Pensions Regulator – tPR – they have published the ScamSmart campaign with the slogan – Be ScamSmart with your pension.

With the ScamSmart campaign, they have also made a video and published it on YouTube. Here is the video for you to watch:

Whilst I think it is great that they are publishing videos as part of the ScamSmart campaign, I can´t help but feel that they spent a large chunk of their budget on some bloke whizzing around on a jet ski.

The video does highlight what people need to look out for to be ScamSmart, but the repeated flashes back to the jet skier whooping loudly are, in my opinion, very distracting. I feel they deviate from the message they are trying to get across.

However, the FCA has done nothing to stop these scammers, nor other well-known ones and no prosecutions have been made. Whilst we are fully in support of educating the masses worldwide to ensure consumers can avoid falling victim to pension scams, this does beg the question:

WHY ARE THE FCA DOING NOTHING ABOUT THE KNOWN SCAMMERS?!?

If the industry was to put a stop to the masterminds, (like Stephen Ward), then surely that would be a giant leap in the right direction for deterring new-comers. As it stands, however, the “award-winning” scammers just seem to set a precedent. If you are good at what you do, your scams can be pushed under the carpet and you can live a life of luxury on the hard-earned cash of the scam victims, escaping punishment.

Victims of the unregulated property scheme Harlequin, may be disheartened to know that Alistair Burns has escaped with a reduced fine for his role as chief executive of TailorMade International.

The FCA originally proposed Burns should face a fine of £233,600, along with a ban back in December 2016. However, the Upper Tribunal, whilst upholding the ban, has chosen to lower this to £60,000.

FCA executive director of enforcement and market oversight Mark Steward said: “Mr Burns failed to ensure that TailorMade International managed its conflicts of interest, benefiting financially from his role as shareholder and director at an unregulated introducer alongside his regulated role, to the detriment of his customers.”

Burns co-owned and co-directed the unregulated introducer company operating as ‘TailorMade’. For three years TailorMade provided advice to 1,661 customers transferring them into the unregulated property scheme Harlequin.

Burns received “significant amounts of commission” from Harlequin for the customers that were advised into the scheme through TailorMade. It was found that pension holders were offered totally unsuitable advice to enter into the SIPPS scheme, which lined Burns´ pockets but saw victims´ funds invested into risky overseas property.

The FCA stated “Our action sends a strong message that failing to manage conflicts of interest fairly and disclose them clearly is completely unacceptable.“

To date, compensation totaling more than £55.6m has been paid by the Financial Services Compensation Scheme (FSCS) in relation to claims upheld against TailorMade. This does not cover all the losses suffered by investors, which the FSCS assesses at more than £106.5m.”

This is a welcome prosecution in the battle against unregulated pension scammers. However, this does beg the question as to why the Upper Tribunal reduced Burns´fine. It does seem that Burns has got off lightly, given the compensation being paid out by the FSCS and the enormity of his crime.

Here in the Pension Life office, we believe scammers should be locked up for their crimes and the keys thrown away. A light sentence seems to spell out to scammers that they may get caught but will get off with a slap on the wrist – leaving these criminals free to scam again and again.

49-year-old Freddy David of Elstree, Borehamwood, of North London, faces six years in jail for conning millions of pounds out of people in his community through an investment scam.

David, once a well-respected member of his community and former financial adviser, obtained money by deception to fund his gambling habit. Figures of his scam are said to be a staggering £15.6m ($20.5m, €17.5m). Many of his victims are elderly and unable to recover the money they have lost. Some investments were as much as £750,000.

David told his 55 clients their funds were being held in a high-interest bank account in his company HBFS Financial Services. The reality of it was, that he used the funds to feed his gambling addiction, including £240,000 in one day!

Fortunately, the FCA became suspicious and were able to collaborate with the City of London Police. This resulted in David admitting to his crime and receiving a six-year jail sentence as well as a ten-year ban from holding a directorship.

Police staff investigator Katie Watkins said: “David was a well-respected member of his community who exploited this in his position as a managing director of a recommended financial advisory firm to gain trust from unsuspecting investors.

“This fraud has caused significant emotional distress and financial harm to the victims involved, many of whom invested their life savings in HBFS. Some victims are retired and are not in a position to recover the money lost.”

This goes to show that investment scammers lurk everywhere and are very good at disguising themselves. Even respected, qualified and registered advisers can turn crooked when they need a bit of extra cash (or even a lot of extra cash).

When choosing to make any financial transfer, ensure that the transaction is your own decision and that the adviser is working in your best interests. Make sure you ask all the relevant questions.

Make sure you receive all the investment information in writing – DO NOT just trust the words of the adviser.

Once you have all the relevant paperwork – DO make sure that you have read over the proposal several times and that you understand it fully.

If in doubt, just walk away. If the offer sounds too good to be true, then it probably is!

International Investment has written a jolly good article about the recent action taken by the UAE Insurance Authority – headed up by His Excellency Ibrahim Al Zaabi. I quote from Gary Robinson’s article:

“In a statement on the Arabic version on its website the IA has issued a circular confirming the suspension (of Holborn Assets) for a period of three months or until it is satisfied that the company has improved its performance.

According to Dubai-based sources that International Investment has been speaking to, the IA has written to regulated insurance companies notifying them of their action.”

I have no doubt that Holborn Assets will rise to the challenge magnificently and in a dignified manner – and will recognise the fact that it is time for the routine misuse of all insurance bonds in offshore financial services to come to an end. I also doubt Holborn Assets will sell any more RL360 products.

The Continental Wealth Management debacle must surely serve as a perfect example of how and why insurance bonds should not be used at all – and indeed how and why structured notes should be banned altogether. And yet, despite the Malta FSC’s lukewarm change in regulations to ban advisers without an investment license and limit structured notes to 30% of a portfolio, useless/pointless insurance bonds and toxic structured notes are very much the norm across the offshore financial services landscape.

The Eagle-eyed Sheikh Al Zaabi has obviously spotted something that regulators in all jurisdictions which affect British expats have turned a deliberate blind eye to. Insurance products can, have been, and are routinely abused. And the abusers often cause heavy losses to thousands of unfortunate victims. His Eminence also obviously recognises that turning a blind eye damages not only the jurisdiction in question, but also the reputation of financial services in general.

The FCAtakes no action even when their nose is rubbed into obvious fraud – and let the British Steel disaster happen under their very noses. In fact it took public-spirited independent financial services professionals such as Al Rush, Darren Cooke and Henry Tapper to take it on themselves to try to rescue the steelworkers while the scammers hovered like vultures. I would like to be proud to be British, but the FCA is a national disgrace and an embarrassment to all British citizens. I wouldn’t mind if the FCA was just lazy, but it simply doesn’t care about the interests of those who get conned and scammed.

The Guernsey FSC allowed many frauds, including trustees Concept Trustees to sell UCIS fund EEA Life Settlements even after the FSA “toxic” warning. And, of course, EEA Life Settlements itself. Then the stable door shut with a resounding clang as an ombudsman was brought in, but told not to hear any complaints prior to July 2013. This effectively excluded all the worst scams which were being carried out in Guernsey by the likes of Concept Trustees – which took business from Stephen Ward’s Premier Pension Solutions which neither had regulation nor professional indemnity insurance.

The Gibraltar FSC appears to actively encourage outright scammers such STM Fidecs – and when financial crime is brought to their attention they go fishing for a few small, wet fish. Talking of fish, I think it is very fishy that Paul Garner, now of the Gibraltar FSC, used to work for scammer XXXX XXXX at Global Partners Ltd – the firm that “advised” hundreds of UK-resident victims to transfer their pensions to an STM Fidecs QROPS. Then STM Fidecs allowed XXXX XXXX to invest 100% of 100% of these victims’ funds into his own UCIS fund: Trafalgar Multi Asset (now in liquidation). I genuinely don’t know at which point Paul Garner moved over from Global Partners Limited to the Gibraltar FSC……but I have a feeling his leaving do will be an exceptionally (and uncharacteristically) lavish affair – and I am very much hoping to be invited. I hear there will be something fishy on the menu and Garner’s good fortune will be toasted with something bubbly. I have no doubt the cleaners will effectively brush all the crumbs under the carpet after the party.

The Central Bank of Ireland will be put to the test when scammers SEB (formerly Irish Life) are put in the spotlight. CBI has known for years that SEB – led by Peder Nateus and Conor McCarthy – has been facilitating financial crime. SEB took £ millions’ worth of business from unlicensed scammers Continental Wealth Management and allowed the whole lot to be invested in toxic structured notes: “for professional investors only”. These notes – including the fraudulent Leonteq ones (over which OMI is now suing Leonteq) clearly warned of the “danger of loss of part or all of your capital”. And yet SEB sat there and watched while hundreds of CWM‘s clients’ victims’ life savings were destroyed – and did nothing. This has left many victims in despair and poverty – with some contemplating suicide.

Against this backdrop of extreme ineptitude and collusion amongst this collection of chocolate teapots, motorbike ashtrays and fishnet willy warmers, let us all hope that the UAE Insurance Authority shows all these no-hopers what effective regulation should look, smell and feel like.

I like to have a good relationship with regulators. And believe me I have tried really really hard with the FCA. I didn’t have much of a relationship with the Pensions Regulator in the past. I asked for a meeting with Tinky Winky, tPR’s former executive director. He turned up with two lawyers (in case one blew away I guess) and a paralegal in an aptly-named conference room called the Warwick Suite at a hotel at Gatwick airport.

Winky accused me of bombarding him with emails (about the Capita Oak scam). I counted them: 16 over an 8-week period. My calculator said that was approximately two per week.

Then he threatened me for “tipping off” and said I could be prosecuted; then the uglier of his two lawyers threatened me with unspecified action if I didn’t wind my neck in. She said to me in a rather unpleasant manner “we can have you sent to the Tower you know – we have wide-ranging powers”.

Anyway, our little tea party in the stuffy room didn’t exactly make for a good spirit between us. So I sighed a huge sigh of relief when Winky departed tPR a year or so later and went to work for LGPS (one of the ceding providers who had performed so appallingly in Ark, Capita Oak and Westminster – handing over £ millions to the scammers without batting an eyelid).

I am happy to say I have a good relationship with Lesley Titcomb – Head of tPR – and am grateful to Henry Tapper for facilitating this.

But, back to the FCA. I went to see John Thorpe at the FCA a couple of years ago – with a rather thin colleague of mine who is a Chartered Financial Planner. John was very enthusiastic about working with us and asked me to give him any intel I had on scams and scammers. He said he would ensure all information would be passed on to the relevant people. However, he did warn me not to deluge him with emails and said: “not more than two or three a week please”.

But then John got moved to another department, which was disappointing. Since then I have sent dozens of complaints to the FCA – as have a number of my associates including IFAs, trustees, compliance officers, chartered financial planners and victims. But the firms in question are left unsanctioned. And the non-compliant practices continue unabated – and more victims are ruined on a daily basis.

In 2016, Jeremy Donaghy-Sutton (a senior airline captain and safety instructor) and I got together in London. He suggested we propose to the FCA an air-crash-style investigation and reporting system to analyse the causes of scams, prevent them from recurring and taking the appropriate action against those responsible for failures. Mostly his brilliant work, we finished and printed off our proposal and set off for the FCA offices.

I had called ahead and told them we would be coming and that we would like to hand our proposal, report and a series of complaints to an appropriate person. I said it was important that we had a brief chat so that we could explain the purpose of our visit (me plus an actual victim) and the accompanying documentation.

We got to the FCA’s North Colonnade office and went to reception. There I explained who I was, what I wanted, who and what I had with me. A very pleasant lady, flanked by two security guards, said “Oh, but we don’t see people here”. Her English wasn’t too bad, but I did wonder whether she hadn’t quite understood what I had said. So I tried again, and went into some detail about the fact that the person I had previously spoken to at the FCA had said that someone would indeed come down and see us.

But her English seemed to get worse the second time. And she still insisted that nobody would come to see us and accept the documents. I tried a third time, while Jeremy sat in the waiting area chuckling quietly as he could see and hear my fuse getting shorter and shorter.

This time the nice lady said she would get someone to speak to me on the phone and asked me to sit down for a few minutes while she got through to somebody. Jeremy and I sat watching the ghastly moving picture on the reception wall – and I wondered what on earth had inspired such a weird and inappropriate piece of “art” (and what the artist had been on at the time).

After about ten minutes, I was summoned back to the reception desk and the nice lady handed me a phone. I have no idea who the man on the other end of the line was, and not much idea whether he was speaking in English or some weird combination of Mandarin, Yiddish and Czech.

When I eventually got my head and ears around his weird accent, I realised he wanted me to explain – over the phone – who I was and what I wanted. By this time there were about twenty people hanging around in the reception area – so this extremely confidential complaint and report proposal was announced loudly and publicly as my voice got higher, squeakier and louder.

I had to spell out some words several times as the man’s English seemed to get worse as the agonisingly painful conversation dragged on and on. When I had finished, exhausted and wondering if this was all a bad dream, the man said “OK, hand your documents into the post room”. We duly dropped the bulging envelope into the tiny little room just outside the entrance to the FCA building. I assume it was all shredded as we never even got an acknowledgement.

Afterwards, over a quick lunch in a Thai restaurant just up the road from the FCA, Jeremy and I wondered if what had happened had all been just a bad dream. How could such a thing happen in a supposedly civilised and well-regulated country. But then Jeremy himself had spent the past five years wondering how the Ark “thing” had been allowed to happen.

The very things I warned about back in 2016 are still happening and victims’ pensions are being routinely destroyed – both in the UK and offshore. At the Transparency Task Force Symposium in November 2017, one victim stood up and related a remarkably similar story to mine about his treatment by FCA. The delegates – who included pension trustees, solicitors, police officers, victims and the wonderful Andy Agathangelou – were stunned and disgusted.

So, if anybody knows anyone at the FCA who might like to do a bit of regulating no more than twice a week, could they please let me know?

Here is the video Pension Life constructed with the help of Jeremy Donaghy-Sutton (a senior airline captain and safety instructor and Ark victim)

Pension Life is pleased to report that the FCA has woken up long enough to do a spot of regulating and has won an important case over the promotion of unregulated investment schemes. The firm flogging the schemes, Capital Alternatives, must pay back nearly £17m to investors.

The FCA alleged that Capital Alternatives used “false, misleading and deceptive statements” to lure unsuspecting investors into four toxic, high-risk investments (scams) between 2009 and 2013. Capital Alternatives, ran investment schemes/scams involving rice farm harvests in Sierra Leone and carbon credits across Sierra Leone, Brazil and Australia.

In reality, Capital Alternatives sold more land to investors than it actually owned.

Court proceedings have been taking place since July 2013, with The High Court deciding in February 2014 that the schemes/scams were collective investment schemes which could not be lawfully operated by the defendants. Since this date defendants have been appealing the decision.

It must be highlighted that Capital Alternatives are not the only defendants involved in this case. This is perhaps why proceedings have taken so long. In fact, the FCA stated that there are a staggering 15 more defendants involved in this case.

The FCA lists the defendants:

Capital Alternatives Limited

Capital Secretarial Limited

Capital Organisation Limited

Capital Administration Services Limited

MH Trustees Limited

Marcia Hargous

Renwick Haddow

Richard Henstock (case settled)

African Land Limited

Robert McKendrick

Alan Meadowcroft

Regency Capital Limited

Reforestation Projects Limited

Mark Ayres/Eyres

Mark Gibbs

the estate of David Waygood (case settled).

The eighth and sixteenth defendants settled their cases previously and have paid £33,000 and £200,000 towards compensation for the investors. The FCA has received this money and will hold it until the Court issue further directions to the FCA about the return of money to victims.

The bad news for investors in Capital Alternatives, is that the High Court’s decision is still open to appeal. The FCA can proceed to obtain monies from the Defendants only when no further appeals are made. In the meantime, the FCA is seeking new injunctions restraining the assets of some of the defendants. We sincerely hope this means there will be some funds left to be returned to the victims of this scam.

But it would be better news if the other 14 defendants find it in their conscience to settle out of court and put the victims out of their misery. It is terrible to find out that you have put hard-earned money into high-risk, illiquid or even worthless investments.

FCA Director of Enforcement Mark Steward has been reported as saying:

“This judgment should send a clear message to all of those who use corporate facades to sell dubious investments. We will do what it takes to hold them to account for their misconduct.

We are acutely aware from experience that the risk to investors who deal with unauthorised firms is that most, if not all, investors are likely only to get a fraction of their money back.

Consumers should recognise that there are huge risks involved when investing with unauthorised businesses.”

Investors should be aware that investments into sustainable/renewable energies, farming and recycling schemes are favorites of scammers. They entice you in with promises of your investment being good for the environment. However, they are rarely good for your pocket. James Hay and Elysian Bio fuel is one example of toxic investment using biofuels as a lure.

In Novemeber 2017 we also wrote about the SFOs letter to Frank Field. The letter highlighted cases of prosecutions against pensions fraud.

Sustainable Agroenergy (SAE) Plc: investors were told their investments were in biofuel products, that land was owned in Cambodia and planted with Jatropha trees – a tree with highly toxic fruit that could be used to produce biofuel. At the time of sale, there was already evidence to show that the product was neither sustainable nor profitable.

The BARRATT AND DALTON PENSION SCAM: – one couple fell victim to this scam despite being advised by their pension provider that it could be a scam. They received a lump sum and were told their pension was invested in truffle trees. After reporting the case to the police, they were later informed that their lump sum was from their own funds and HMRC promptly served them with a large tax bill.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

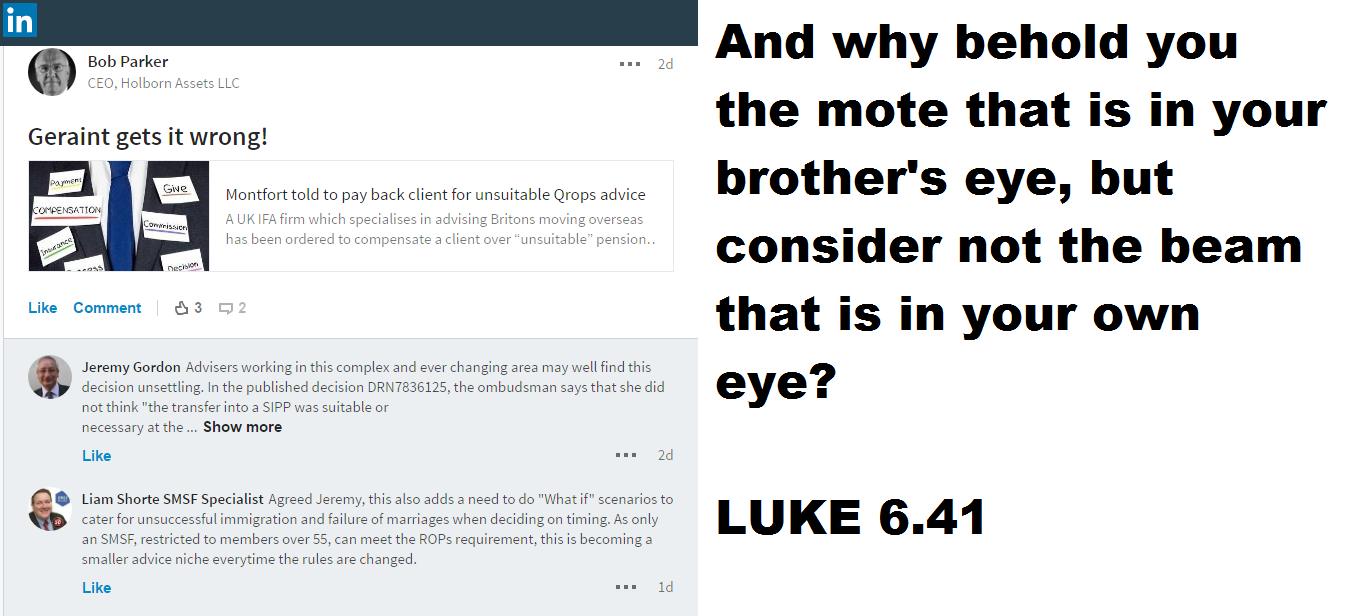

Holborn Assets’ Bob Parker commits a gloat too far.

Holborn Assets Dubai – under the questionable leadership of Bob Parker – has been responsible for ruining quite a number of victims’ pensions. With a deft waggle of the Holborn Assets magic wand, a pension transferred from a gold-plated final salary scheme can be reduced by at least 50% in just a couple of years. Trouble is, the magic kind of runs out of steam if asked to work in reverse.

Glynis Broadfoot and various other victims in Spain were “advised” by dodgy Holborn Assets’ advisers to transfer their pensions into a QROPS with Gower Pensions in Guernsey. Then the victims’ pensions were invested in toxic, illiquid, high-risk, professional-investor-only funds and shrank relentlessly. The problem was that Holborn Assets had no license to provide pension or investment advice in Spain. This is the sort of scam that the CNMV, the Spanish investment regulator, refers to as being operated by “chiringuitos” (bar flies) which translates as “scammers”. And the UK Pensions Regulator clearly refers to scammers as criminals.

Holborn Assets’ home – a low-rise advisory firm amongst the high-rise buildings

So why is Bob Parker – from Dubai – gloating over Geraint Davies from Surrey? OK, Geraint’s firm Montfort International has been sanctioned – and very publicly so. And, knowing Geraint I believe he will take his punishment pragmatically and stoically. He has fought back from other challenges in the past and he will fight back from this. But at the end of the day, whatever other faults he may have, he does have respect for the establishment, the law, the regulators and the ethical sector of the financial advisory profession.

I suspect – if Geraint saw Bob the Knob’s post on the LinkedIn QROPS group – he will have had an ironic chuckle at the Bible-thumper’s hypocrisy. And if he had known that Bob’s response to his various victims’ distress and pleas for help had been “buzz off – case closed” he would most probably have been enraged that Parker the Not-So-Magic Marker should remark on the mote in Geraint’s eye and cynically gloss over the socking great forest in his own.

Of course, Geraint himself will certainly know that Parker’s top salesman is Paul Reynolds who has been sanctioned by the FCA (banned from regulated activities due to lack integrity and fined nearly £300k) and may even have had a wry smile to himself that a man who professes to be a devout Christian is prepared to employ a publicly-condemned pariah of the profession. But, of course, Reynolds is Holborn Assets’ best salesman – flogging toxic assets to ruin their clients – so it is worth keeping him in order to keep the wheels of Parker’s Rolls Royce well oiled.

So, am just wondering how the devout Christian Bob Parker is getting Holborn Assets’ DB pension transfers done now? What dodgy outfit is he using? Because it won’t be anything ethical or honourable. And whichever firm it is, it will be helping Holborn Assets ruin hundreds – or even thousands – of victims have their pensions decimated by execrable, unregulated investment advice.

Despite Parker’s hypocritical post on LinkedIn, I think Geraint Davies’ firm Montfort comes out of this considerably better than Holborn Assets. I have no doubt Geraint will have more success in plucking the mote out of his eye than Parker will in taking a whole sawmill out of his.

Steve Pimlott of Windsor Pensions is still scamming people out of their pensions. And seeking new victims on LinkedIn. Inviting people to:

Transfer your frozen UK pensions to a QROPS

Still scamming after all these years

He will charge between 10% and 20% and will use forged documentation from an obscure QROPS such as Danica and BSEC and then fool the ceding provider into transferring a pension into a fraudulently-set-up bank account in a dodgy jurisdiction such as the Isle of Man.

Pimlott – who may also go by the name of Steve Derrick Pimlott – claims to have done many thousands of these transactions and states that only a couple of hundred people have ever got caught by HMRC. And even then, he says, as most of the people live offshore they ignore the tax demands of 55% on the amount liberated. HMRC’s version of events is somewhat different and tell me that in some cases Pimlott made off with the whole transfer and the victim never even got the 80% or 90% that was left.

Pimlott involved a firm allegedly called Insignia Financial Services in some of the cases. Although this gave some of the victims an illusion of respectability, the firm was in fact a clone of an FCA-registered entity.

Dozens of properties as opposed to Ward’s mere six

Pimlott is reportedly in Florida – not too far from Stephen Ward’s Indian Point holiday villa empire. Ward also told his victims to throw the tax demands in the bin. However, Pimlott’s property portfolio is considerably larger than Ward’s. If Pimlott is telling the truth about having done 5,000 liberations, then HMRC will be pretty busy. If we assume the average pension pot size was, say, £50,000 and Windsor Pensions charged 15% fees for each one, then Pimlott earned a cool £37.5 million. And herein lies the problem: while these scammers are earning such huge amounts of money, they are hardly likely to give it all up voluntarily.

I hark back to the Pensions Regulator’s Lesley Titcomb’s statement that “scammers are criminals”. Steve Pimlott and his associates are criminals. They need prosecuting, given maximum jail sentences and their assets confiscating. The industry needs to get behind this and support the pressure that must be put on law enforcement agencies in the UK, USA and beyond.

Ceding Pension Providers ignored warnings about scams

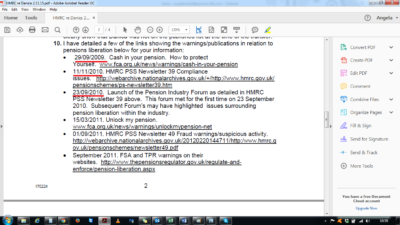

HMRC say there were sufficient warnings about pension scams in the public domain for years. In 2009, the FCA warned about a rogue firm called Cash In Your Pension operating liberation scams; HMRC warned about pension liberation scams involving rogue IFAs. Yet still the ceding pension providers carried out zero due diligence. For years they just kept handing over thousands of pension pots to the scammers without a thought to the financial ruin they were inflicting on the victims.

Hopefully, now the Pensions Regulator’s Andrew Warwick-Thompson is going to work for one of these negligent pension providers – LGPS – he will help bring these companies to justice as well.

Readers may have seen the HMRC News Release on 22 June 2009 which confirmed 11 people, including some independent financial advisers, were arrested following raids in the North West and Midlands. These arrests were linked to an estimated £2.5 million suspected tax relief fraud involving bogus pension schemes. Enquiries are continuing in that case.

Pension Schemes Services (PSS) and other areas of HMRC are continuing to work closely with our regulatory colleagues to ensure that the interests of members are properly protected through bona fide pension schemes and that the generous tax reliefs available through employer/member contributions are not abused. We will vigorously pursue those who deliberately attempt to defraud the public purse.

“James Hay was ONLY the pension administrator”. My hat!

JAMES HAY AND ELYSIAN BIOFUELS SCAM

I always say that pension and investment scams happen because people, firms and authorities allow them to happen. This was very true in the Elysian Fuels pension liberation scam. Jack Gilbert of New Model Adviser broke the news today, 9.5.2017, of James Hay’s involvement in this:

Sipp and platform provider James Hay is facing an HM Revenue & Customs tax charge of £1.8 million over the non-standard biofuel investment Elysian Fuels. James Hay today said it has 500 clients who have invested around £55 million in Elysian Fuels and HMRC is investigating this scheme.

And the firm added it is now appealing a tax charge from HMRC over this investment.

‘James Hay did not advise investors in relation to these investments; it acted solely as pension administrator. James Hay has received, in April 2017, assessment notices for sanction charges from HMRC for the tax years 2011/2012 and 2012/2013 in total for £1.8 million. These have been appealed and are the subject of ongoing discussions with HMRC.’

The investors themselves, whose SIPP investments are now worthless, will undoubtedly be interested to know the real story behind this disgraceful scam – which also involved other FCA-regulated SIPP providers such as Suffolk Life:

The arrangement I heard about today works like this as an example ( ignoring fees) and this is the simplistic version

Client borrows 16k or thereabouts (this is available in the package)

He gets a non-recourse loan (which will not be repaid) of £84k

He buys shares in Xco for £100k. These are listed on the CISX (name is Elysian)

Transfers £100k to James Hay SIPP

SIPP pays member £100k for the shares .,,,

Member repays the 16k and trousers £84k

My IFA connection has done 40 of them so far. Advice to transfer to the SIPP is from an FCA regulated IFA. James Hay and Suffolk Life know the full structure and are happy with it ….Fees ….. On transfer to SIPP (need to agree the commercials with the IFA)

Regards

Stephen

The FCA-registered IFA was Angela South’s Magna Wealth. We’ve had quite a good old chin-wag over this and while she said she did suspect I had hacked her emails, she denied she had done 40 of these transactions. In fact, the only hacking I have ever done was plodding round Windsor Great Park on an elderly horse when I was a teenager.

But don’t you just love James Hay’s protestation: “we acted solely as pension administrator”? Solely? Pull the other one. Come on FCA – wake up! Perhaps we could have a competition between tPR and FCA to see which one could start doing some actual regulating first? Tortoise and tortoise race?

This week Henry Tapper wrote a blog entitled, “The wheels of the law turn (too) slowly”. He exposes the fact that when it comes to financial crime the justice system in place just isn´t enough. I think he was being generous with his title. The wheels of the law don’t just turn slowly – they just don’t turn at all. Friendly Pensions has been in the news this week.

This week Henry Tapper wrote a blog entitled, “The wheels of the law turn (too) slowly”. He exposes the fact that when it comes to financial crime the justice system in place just isn´t enough. I think he was being generous with his title. The wheels of the law don’t just turn slowly – they just don’t turn at all. Friendly Pensions has been in the news this week. They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

Just for a laugh, have a look on

Just for a laugh, have a look on

2,000 victims of fraudulent pension firms may be in with a chance of getting their funds back. In November, the FCA pushed for legal proceedings to go ahead against collapsed firm Avacade Limited, trading as Avacade Investment Options; and Alexandra Associates (UK) Limited, trading as Avacade Future Solutions.

2,000 victims of fraudulent pension firms may be in with a chance of getting their funds back. In November, the FCA pushed for legal proceedings to go ahead against collapsed firm Avacade Limited, trading as Avacade Investment Options; and Alexandra Associates (UK) Limited, trading as Avacade Future Solutions.

I have a long list of fraudulent pension firms and serial scammers that I plan to forward to the FCA (yet again). However, in reality, I do wonder how many cases the FCA can actually deal with in one year. Given their past track record, I’d say this is their annual big bust. The other scammers are safe and the victims will be left to wait and wonder when their cases will be dealt with.

I have a long list of fraudulent pension firms and serial scammers that I plan to forward to the FCA (yet again). However, in reality, I do wonder how many cases the FCA can actually deal with in one year. Given their past track record, I’d say this is their annual big bust. The other scammers are safe and the victims will be left to wait and wonder when their cases will be dealt with. On the plus side, the FCA have certainly had a busy month. Alongside their prosecutions, they have launched their

On the plus side, the FCA have certainly had a busy month. Alongside their prosecutions, they have launched their  I would like to highlight that the rider of the jet ski does bear a remarkable resemblance to Phillip Nunn, cold caller and “fund manager” of the

I would like to highlight that the rider of the jet ski does bear a remarkable resemblance to Phillip Nunn, cold caller and “fund manager” of the

Victims of the unregulated

Victims of the unregulated

49-year-old Freddy David of Elstree, Borehamwood, of North London, faces six years in jail for conning millions of pounds out of people in his community through an investment scam.

49-year-old Freddy David of Elstree, Borehamwood, of North London, faces six years in jail for conning millions of pounds out of people in his community through an investment scam. Police staff investigator Katie Watkins said: “David was a well-respected member of his community who exploited this in his position as a managing director of a recommended financial advisory firm to gain trust from unsuspecting investors.

Police staff investigator Katie Watkins said: “David was a well-respected member of his community who exploited this in his position as a managing director of a recommended financial advisory firm to gain trust from unsuspecting investors.

International Investment has written a jolly good article about the recent action taken by the UAE Insurance Authority – headed up by His Excellency Ibrahim Al Zaabi. I quote from

International Investment has written a jolly good article about the recent action taken by the UAE Insurance Authority – headed up by His Excellency Ibrahim Al Zaabi. I quote from  The Gibraltar FSC

The Gibraltar FSC

Winky accused me of bombarding him with emails (about the Capita Oak scam). I counted them: 16 over an 8-week period. My calculator said that was approximately two per week.

Winky accused me of bombarding him with emails (about the Capita Oak scam). I counted them: 16 over an 8-week period. My calculator said that was approximately two per week.

I had to spell out some words several times as the man’s English seemed to get worse as the agonisingly painful conversation dragged on and on. When I had finished, exhausted and wondering if this was all a bad dream, the man said “OK, hand your documents into the post room”. We duly dropped the bulging envelope into the tiny little room just outside the entrance to the FCA building. I assume it was all shredded as we never even got an acknowledgement.

I had to spell out some words several times as the man’s English seemed to get worse as the agonisingly painful conversation dragged on and on. When I had finished, exhausted and wondering if this was all a bad dream, the man said “OK, hand your documents into the post room”. We duly dropped the bulging envelope into the tiny little room just outside the entrance to the FCA building. I assume it was all shredded as we never even got an acknowledgement.

The bad news for investors in Capital Alternatives, is that the High Court’s decision is still open to appeal. The FCA can proceed to obtain monies from the Defendants only when no further appeals are made. In the meantime, the FCA is seeking new injunctions restraining the assets of some of the defendants. We sincerely hope this means there will be some funds left to be returned to the victims of this scam.

The bad news for investors in Capital Alternatives, is that the High Court’s decision is still open to appeal. The FCA can proceed to obtain monies from the Defendants only when no further appeals are made. In the meantime, the FCA is seeking new injunctions restraining the assets of some of the defendants. We sincerely hope this means there will be some funds left to be returned to the victims of this scam.