At the end of January 2022, Boris Johnson claimed he had reduced crime by 14%.

Boris shocked a lot of people with this figure. But, apparently, he wasn’t talking about fraud. He’d forgotten that even some of his own constituents had been defrauded into the Ark pension scam (and that he had promised to “sort it out” back when he was Mayor of London).

Norgrove headed up the Pensions Regulator (which used to be known as OPRA) from 2005 to 2011. He had issued dire warnings to pension providers against handing over pensions to scammers – saying that just ticking boxes (without checking the receiving scheme was bona fide) would lead to a huge rise in pension fraud. He was, of course, ignored – especially by Standard Life, Aviva, Scottish Widows and Prudential.

Norgrove’s correction of Blonde Boris’ clumsy gaff is not surprising at all. This government’s attention and time spent into looking into fraud has been somewhere between minimal and non-existent. Combine that with putting an utter nitwit in charge of the FCA, and you have the perfect breeding ground for an explosion of fraud and scams.

It is disgraceful to know that this government’s focus on crime ignores fraud as though it were irrelevant. This huge aspect has been – and is still – affecting hundreds of thousands of people. I suppose our ill-informed P.M. thinks the person in the black balaclava seems a lot more dangerous than the one in the designer suit and tie.

But we know the damage these fraudsters can cause. Such misinformation being spread is highly dangerous; leaving consumers with a false sense of security, and making them even more likely to be scammed.

Terence Wright & his wife

Let’s take Terence Wright for example. Wright’s activities in the pension scam world flourished in 2014 and 2015. Although he most definitely didn’t look like a typical burglar, he caused the destruction of millions of pounds of pensions across the UK.

Wright had an unregulated Spanish firm called Commercial Land & Property Brokers (CL&P) which introduced hundreds of people to the pension SIPP provider Carey Pensions. From here he invested the victims’ money into Store First and Australian farmland via Gas Verdant where the money will have dwindled away into nothing.

One victim, Russell Adams, got his destroyed pension reinstated in the Appeal Court. But thousands more are still left stranded with illiquid and sometimes worthless pension assets.

There are many more examples: Trafalgar Multi Asset Fund (in an STM QROPS and invested in Dolphin Trust); Blackmore Bond, Blackmore Global (in STM, Optimus, EFPG, Quartermaine and GFS QROPS); Forthplus SIPP which has just gone bust and is full of toxic investments. The list is endless.

This type of fraud is committed against British victims routinely. The crime goes on (and on!) in the UK and offshore. By destroying pension funds with toxic investments, the fraudsters earn millions in hidden commissions. Which is supposed to be illegal. Perhaps Boris the Johnson will wake up to this fact one of these days. Or perhaps this is as unlikely as him using a hairbrush.

Pension scams have been destroying lives for more than a decade. The scammers cause poverty, marriage breakdowns and even death. Death caused by stress-related illness. And death by suicide.

A typical pension scam involves an unlicensed person pretending to be a financial adviser. This is illegal. But it goes on all the time, in the UK and offshore.

All pension scams result in the loss of part or all of the pension. And, sometimes, crippling tax liabilities on top.

Most pension scams start with a pension transfer that should never have happened. And finish with investments which are unsuitable and risky.

One particular pension scam involved an unlicensed introducer called Terence Wright (i.e. a scammer posing as a financial adviser). Wright ran a business in Spain called CLP (Commercial Land and Property).

Professor Gerard McMeel QC of Quadrant Chambers

In 2012, Wright conned hundreds of victims into transferring their pensions into a Carey SIPPS (SIPPS stands for Self Invested Personal Pension Scheme). The sole purpose for these transfers was to invest the pension funds in assets which paid the highest commissions to Wright and the other scammers involved.

One of these victims, a lorry driver called Russell Adams, felt so strongly that he had been defrauded, that he took his case to the High Court. But, in the first round, he lost.

In the landmark High Court appeal ruling, the Adams v Carey case resulted in SIPP provider Carey being ordered to put things right. After the previous judge failed to give Mr. Adams the justice he deserved, a victory was obtained which should help prevent future pension scams.

In the appeal, the judge – Justice Andrews – ruled that the case involved:

Justice Geraldine Andrews

“opportunities for unscrupulous entities to target the gullible”

She ordered Carey Pensions to refund Mr. Adams his pension. She mentioned “financial crime” and placed much of the blame squarely at the door of the unlicensed introducer – Terence Wright of CLP – who gave investment advice illegally.

The Adams v Carey case is likely to herald a flood of similar claims against pension providers like Carey. So let’s have the drains up on this case – and break down the main ingredients. Then we’ll see what lessons can be learned. And how similar pension scams could be avoided in the future.

SO HOW DO PENSION SCAMS WORK?

It all starts with HMRC.

A British pension scheme (whether a personal or occupational one) starts with an HMRC registration number. The good, the bad, the ugly – and the downright stinky – pension schemes are all registered by HMRC. And in the case of occupational schemes, by the Pensions Regulator as well.

HMRC makes no distinction between schemes set up for bona fide reasons, and those which are set up for scamming. HMRC doesn’t care – and anyway they say that consumer protection isn’t their responsibility.

WHAT IS A PENSION SCHEME?

A pension scheme is just a wrapper – like a cardboard box or a paper bag. On its own, a pension scheme can’t do any harm. Try looking at an empty cardboard box for a moment and ask yourself how much damage it could do. Watch it carefully – and see if you can spot it doing anything dangerous or sinister. I reckon that however closely you watch it, nothing untoward will happen (although your cat might curl up inside it and take a nap).

Christine Hallett CEO of Carey Pensions

Remember that it isn’t the box itself that could be dangerous, but the people handling it and putting things inside it. An empty box could become a delightful xmas present if filled with mince pies and chocolate. Or, if filled with dynamite and nails, it could become a deadly bomb which could kill and maim hundreds of people.

Whether a pension scheme is a personal or occupational pension, a SIPP, a SSAS, a QROPS or a QNUPS, it is just an empty wrapper. A harmless container which can be used responsibly by good people, or recklessly and even maliciously by bad people.

The lesson is that the cardboard box itself doesn’t do the damage – it is the people who handle it.

The Adams v Carey case will inevitably be a turning point for the pension industry – both in the UK and offshore. There will now be a big question mark over the word “self” in the phrase “self invested”. This phrase may have to be upgraded to “sort of self invested”. This is because the successful appeal makes it clear there is still a duty by the trustee to make sure nothing happens to pension funds which is clearly bonkers.

Mr. Adams was one of 580 Carey SIPP members who were all invested solely in store pods in the space of one year. And none of them had a licensed financial adviser. To put this into context, nearly 50 people a month transferred their pensions into a Carey SIPP and voluntarily invested the whole lot in store pods.

A reasonable person might ask why Carey didn’t ask themselves why there was this sudden stampede coming out of the blue? Why so many people wanted to invest their entire pension funds into the same illiquid property asset? Why so many different people were advised and represented by an unlicensed introducer in Spain?

Perhaps after the first month, Carey might have raised a bit of an eyebrow. After the second and third months, Carey’s CEO Christine Hallett might have decided to question whether Terence Wright of CLP in Spain was a suitable person to advise so many different people to invest in the exact same asset.

But she didn’t. She let the torrent of victims of Terence Wright’s unlicensed “advice” continue unchecked. Hallett is described on her LinkedIn profile as:

“one of the country’s most knowledgeable experts in the SIPP world and a highly respected leader in the financial services industry”

And yet she didn’t check the FCA website to see whether Terence Wright was legit. Had she done so, she would have found a clear warning that he was providing financial advice without a license. And that is a criminal offence.

Terence Wright was involved in both the pension transfer process and the investment process. And yet he had no qualifications or license to do either – and there was a clear FCA warning against him.

The ordinary man in the street may routinely check their emails, Facebook and Twitter, but would be unlikely to check the FCA website. However, a “highly respected leader in the financial services industry” ought to have checked the FCA website as routinely as any normal person would check their social media.

The Carey “Key Features” document stated that the member was responsible for investment decisions. And that is where the “self” bit comes from in “Self Invested Personal Pension”. But Carey also recommended that a suitably-qualified adviser ought to be used – to make sure that the pension transfer was in their best interests.

There is nothing wrong with having some illiquid commercial property in a pension portfolio. But the key to all investment decisions is “diversity” and not putting all one’s eggs in one basket (or cardboard box – or indeed pension wrapper). Had Russell Adams been advised by a proper, qualified, licensed adviser, he would have been warned against investing his whole fund in any one asset. To put everything into one single investment is always high risk and irresponsible – no matter how solid and safe the asset may be.

To be fair to Carey, they did eventually sever terms of business with CLP. But for some extraordinary reason they still acted on CLP’s investment recommendations until eventually deciding they were no longer suitable in April 2013 – nearly a year later.

The appeal judgement concluded that the Carey SIPP was recommended by Terence Wright solely for the purpose of investing in the store pods (and the accompanying introducer commissions). And that all the “advice” given by CLP was part of an inextricably-linked bundle of transactions which included the transfer and the investment.

This “bundle” of advice consisted of the transfer out of the original pension scheme; the transfer into the Carey SIPP; the investments (in the store pods). And the whole kit and caboodle was in contravention of article 53 of the FCA regulations.

Carey’s own documentation admitted that investments of less than £50k in a Full SIPP were not economically viable. This should have alerted Carey itself to the fact that many of the 580 people advised by CLP would inevitably suffer from disproportionately high fees.

The judges in Russel Adams’ case summarised the reasons for allowing the appeal:

i) Dealing with an unregulated intermediary

ii) Admitting an asset which could not be valued

iii) Proceeding with the store pod investment despite concerns in May 2012

Carey, now called Options, may come back for round 3 if they are given leave to appeal this judgement. Whether they are allowed to do this or not, this leaves the pension industry with a 100% crystal-clear message:

DO NOT DEAL WITH UNLICENSED INTRODUCERS

Most of the things that have gone wrong, in the past decade, are because of advice given by unscrupulous, unqualified, unlicensed “introducers”. And their mission is clear: to encourage victims to do what earns the introducer the most money – even though it will inevitably cause loss and damage to the victim.

The pensions industry worldwide must now get behind a coherent and determined campaign to stamp out the scourge of the unlicensed introducer. Confidence needs to be rebuilt in British and overseas pensions. And that can only be done by outlawing the rogues and scammers who have done so much damage to so many thousands of victims.

Terence Wright’s luxury mansion in France

It is, indeed, ironic that Terence Wright of CLP was operating from Spain – the capital of the world of pension and investment scams. He was able to ruin UK-residents’ lives all the way from the Costa del Sol. He was given access to a harmless pension wrapper, and managed to transfer hundreds of pensions which should have been left where they were.

But the real story is that Terence Wright and his wife Lesley made a fortune out of scamming Russel Adams and hundreds of other victims. And he is still at it from his new luxury home in France: a stunning mansion in the Dordogne region of France:

With his own private plane and stables for his wife Lesley’s collection of horses, he now lives a life of luxury and commutes to Dubai to pursue his lucrative “business” activities.

Terence Wright and his wife Lesley

This is what is so sad and disgusting about all the scammers behind the many hundreds of pension and investment frauds this past decade or so. They reap eye-watering rewards. Despite a few limp attempts by the SFO to bring scammers to justice they rarely face jail sentences.

The pensions industry needs to get behind a solid campaign to bring these criminals to justice. Lorry driver Russel Adams did his bit to kick this initiative off. It is now up to the pension providers themselves to take this to the next level. And finally restore confidence in British and overseas pensions.

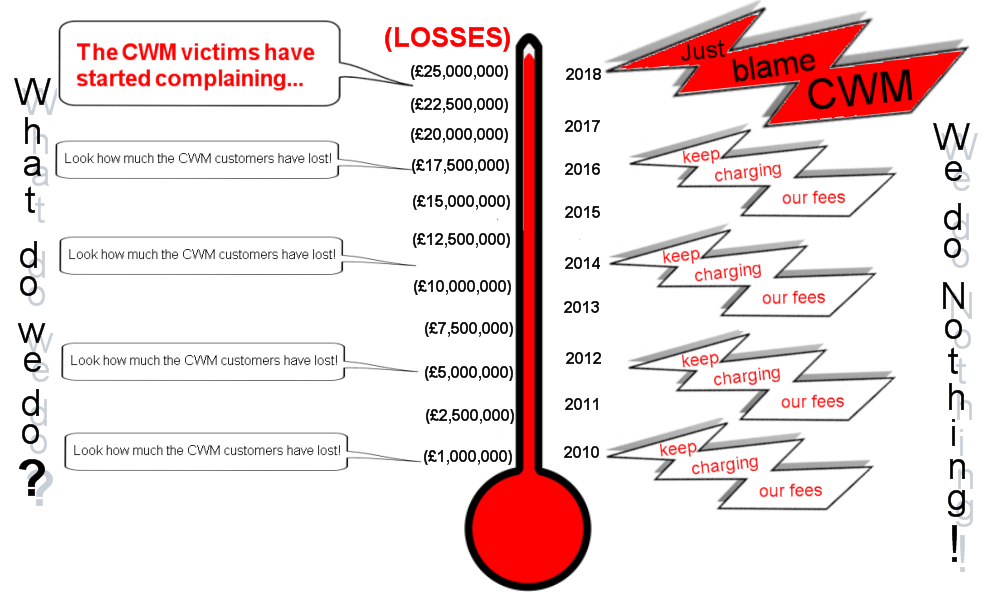

April 2019 sees the battle between Store First and the Insolvency Service. On April 15th, the High Court proceedings will kick off. As a result, the Store First v Insolvency Service will determine how many people will lose their pensions permanently. Two sets of very expensive lawyers – DWF and Eversheds Sutherland – will battle it out to see if Store First can continue trading. In the end, if the Insolvency Service wins the war, then both law firms and an insolvency practitioner will get rich.

As a result of the Insolvency Service winning, 1,200 pension scam victims will probably lose the majority of their investments in Store First. In most insolvencies, there is little left after the various snouts in the insolvency trough have had their fill. Investors will be lucky to get 10p in the pound. If there’s an “R” in the month. And if it is snowing. And if Brexit has a “happy ever after” ending.

The Insolvency Service says it is “in the public interest” to wind up Store First. But are they right? Isn’t winding up the company going to do even more unnecessary damage?

One very important issue is that the Insolvency Service’s witness statement dated 27.5.2015 (by Leonard Fenton) is so full of inaccuracies, misunderstandings, incomplete facts and an obvious failure to understand how the scam worked – as to be utterly laughable. The Insolvency Service and the High Court will rely heavily on this witness statement – and yet it has so many holes and errors that it is misleading, incomplete and meaningless. I asked the Insolvency Service questions about the incorrect and incomplete statements and made numerous comments on the failings contained within the statement. But the Insolvency Service did not even have the courtesy to reply or even acknowledge my contribution. In my view, this is arrogance and incompetence in the extreme.

This impending legal battle (which will cost the taxpayer £millions) is riddled with many more questions than answers. Here are a couple of my questions:

QUESTIONS RE STORE FIRST V INSOLVENCY SERVICE BATTLE

Why did HMRC and tPR register Capita Oak and Henley Retirement Benefits Scheme as pension schemes in the first place?

How many of the many scammers behind Capita Oak and Henley have been prosecuted?

The reason for my questions is that both HMRC and tPR were negligent in registering the two occupational pension schemes. This was because the schemes were obvious scams from the outset. They both had non-existent sponsoring employers which had never traded or employed anybody. And they weren’t even in the UK.

HMRC was blind, stupid and lazy at the start – when these two schemes were registered by known scammers. But several years later, HMRC woke up pretty smartly and sent out tax demands for the “loans” the victims received. The Store First v Insolvency Service Battle is probably doomed to ignore HMRC’s negligence in causing this disaster in the first place.

James Hay and Suffolk Life had been facilitating the Elysian Fuels investment scam at around the same time. And this was with the considerable “help” of serial scammer Stephen Ward. So, this was a prime time for scams and scammers. However, both HMRC and tPR failed the public back then and have continued to do so ever since.

In 2015, the Insolvency Service identified and interviewed most of the scammers behind the Store First pension scam. In their witness statement dated 27th May 2015, Insolvency Service Investigator Leonard Fenton cited statements and evidence from all the key players.

KEY PLAYERS IN THE STORE FIRST PENSION SCAM:

Ben Fox

Stuart Chapman-Clarke

Michael Talbot

Sarah Duffell

Bill Perkins

XXXX XXXX

Alan Fowler

Jason Holmes

Karl Dunlop

Christopher Payne

Keith Ryder

Craig Mason

Patrick McCreesh (of Nunn McCreesh – along with Phillip Nunn)

Tom Biggar

Paul Cooper (Metis Law Solicitors)

That is fifteen scammers who have never been prosecuted. They have not only never been brought to justice, but many of them went on to operate further scams and ruin thousands more lives – destroying more £ millions of hard-earned pension funds.

And what of Toby Whittaker’s Store First? There is no question that store pods are not suitable investments for pension fund investments. Car parking spaces are unsuitable for pensions as well. There are, in fact, a long list of inappropriate investments for pensions – including anything high-risk, illiquid and expensive or commission-laden.

All the above are routinely used and abused by pension scammers as “investments” for some dodgy scheme. Invariably, the above investments come with pension liberation fraud and/or huge introduction commissions and hidden charges. However, it is rarely the fault of the artist, wine maker, start-up entrepreneur, truffle farmer or property developer that the scammers profit so handsomely from abusing their products.

Store First v Insolvency Service Battle

I hope Store First defeats the Insolvency Service in the forthcoming battle in the High Court this month. And I hope that the public and British government will finally get to see what embarrassingly inept, corrupt, lazy regulators and government agencies we have. I will publish the Insolvency Service’s witness statement separately for anyone who wants to read the Full Monty.

Let us not forget that the solicitors acting for the Insolvency Service – DWF LLP – also act for serial scammer Stephen Ward. It was Ward who was responsible for the pension transfers which subsequently invested in Store First. Had it not been for him, 1,200 victims’ pensions totaling £120 million wouldn’t now be at risk. But, somehow, DWF LLP doesn’t think that is a conflict of interest?!?

Let us be clear: if the Insolvency Service wins the court case, the investors will get nothing. This will mean that, yet again, the victims will get punished. If Store First wins, the investors will get at the very least half their money back. If they are patient, they may even get it all back.

In every pension scam there is one beginning, lots of middles, and always a wretched ending for the victim and a profitable ending for the scammers. The beginning is always a negligent, lazy, box-ticking transfer by a ceding provider – the worst of which always tend to be the likes of Standard Life, Prudential, Scottish Widows, Aviva, Scottish Life, Aegon, Zurich etc.

Pension scams are rarely simple and there are many different culprits to blame for the losses. The one common theme though, is that not one of the parties involved is prepared to take the blame for the victims’ losses – EVER. It was always someone else’s fault.

The pension scam trail is rather like a game of Cluedo. The question is: “who murdered the pension fund?”. We travel around the board trying to decipher who is to blame: at which point was the pension fund truly put at risk? – and with what weapon was the pension fund murdered?

While the pension fund transfer always starts with the negligent ceding provider, there are financial crime facilitators long before this: our old friends HMRC and the Pensions Regulator. HMRC registers the scams – often to repeat, known scammers. HMRC does no basic due diligence and deliberately ignores obvious signs that the scheme is an out and out scam. Then HMRC does nothing to warn the public when they discover there are dastardly deeds afoot. In the case of an occupational scheme, the Pensions Regulator allows the scheme to be registered and is slow to take any action even when obvious signs of financial crime emerge.

In recent cases, we have seen complaints – by the victims of scams – upheld against the ceding provider’s negligence in releasing the pension funds to the scammers and financial crime facilitators. And yet neither HMRC nor the Pensions Regulator is ever brought to account. The biggest problem is that – in the case of pension liberation – HMRC will pursue the victims and not the perpetrators. This then compounds the appalling damage done to thousands of people’s life savings.

We have often seen serial scammers like Stephen Ward behind scams such as Ark, Capita Oak, Westminster, London Quantum etc., and yet neither HMRC nor tPR take any action (except to pursue the victims for unauthorised payment tax charges). This is neither just nor reasonable – and yet this practice continues unchallenged.

Any half-decent detective would then turn his attention to the “introducers” and cold callers. These people draw in the victims with unrealistic promises of fat returns and “free” pension reviews. In the case of the London Capital & Finance investment scam, we have seen hard evidence of how lucrative introducing and lead generation has become. Surge Group earned over £50 million promoting the scam which saw 12,000 victims lose £236 million worth of life savings. Surge boasts that it has over 100 staff and that they are treated very well: “We have our own in-house Barista who makes the best flat whites in Brighton. Every day you will find healthy breakfasts, fridges brimming with drinks and snacks, weekly massages and haircuts provided onsite.”

In the case of the Continental Wealth Management scam, there was a further trio of suspects: life assurance companies – Generali and SEB and OMI. These providers of expensive “life bonds” pay the scammers 7% commission and facilitate the crime of defrauding victims into investing into high-risk, expensive, unsuitable investments that earn the scammers further fat commissions. Even when the portfolios have been partially or even fully destroyed (murdered), the life offices still take the huge fees and blame the advisers such as CWM – or even the victims themselves.

We also have the so-called regulators – such as the FCA (Facilitating Crime Agency) and tPR (the Pension Rogues), who are supposed to help protect the public from becoming pension scam victims. But these limp and lazy organisations are so slow off the mark, that the scammers have long since vanished by the time they take any action. This is evident in the recent London Capital and Finance investment scam; the FCA was warned back in 2015 but – of course – did nothing.

Another suspect in the pension murder crime scene is the Insolvency Service. Back in May 2015, the Insolvency Service published their witness statement in the case of a large cluster of pension scams – including Capita Oak, Henley Retirement Benefits, Berkeley Burke and Careys SIPPS – all invested in Store First store pods. The total scammed out of 1,200 victims was £120 million – and yet the only action that the Insolvency Service has taken has been to try to wind up Store First. Four years later. And all this will do is punish the victims even further – on top of HMRC punishing the victims by issuing tax demands.

The burning question is:

How long can all the parties involved in these pension scams, go on letting this happen and say it has nothing to do with them? In some cases we have the ceding providers blaming the victims for their losses!

Still, to this day, we see victims’ life savings invested in toxic and expensive assets. Nothing meaningful is being done to put a stop to it. The victims lose their money and the scammers escape with bulging pockets full of cash.

In the offshore advisory space, regulation is still hit and miss – with some firms providing investment advice with only an insurance license. And many providing advice with no license at all. But still QROPS and SIPP trustees routinely accept business from these “chiringuitos”. But even the properly-regulated ones still routinely use expensive, unnecessary “life” bonds – and we now have hard evidence that this is a criminal matter in Spain after our recent DGS ruling against Continental Wealth Management and all associated parties.

The saddest footnote to this blog is that many so-called “experts” seem to think that the real culprit is the victim himself. They state that people who fall for scams were “stupid” or “greedy” or “should have known better. The well-worn trite phrase: “if it sounds too good to be true, it probably is” gets trotted out all too frequently. But when even regulated and qualified firms and individuals have convincing sales patters that effectively con people into expensive, high-risk arrangements with hidden commissions and fake promises of “healthy” returns, is it any wonder that so many pensions are murdered every day? And when large institutions like Old Mutual International and Friends Provident International facilitate such pension and investment scams, is it any wonder that so many highly-intelligent, well-educated people get scammed?

Ask the victims of not just the £236,000,000 London Capital & Finance fund (bond), but also:

Axiom Legal Financing Fund – £120,000,000 (most of which offered by OMI and Friends Provident International)

LM Group of Funds – £456,000,000 (most of which offered by OMI and Friends Provident International)

Premier Group of Funds – £207,000,000 (most of which offered by OMI and Friends Provident International) – including Premier New Earth and Premier Eco Resources

Leonteq structured notes – £94,000,000 (all of which offered by OMI)

Another victim of Berkeley Burke SIPPS investments into Store First storage pods has come forward. 55-year-old factory worker Robert McCarthy, of Ebbw Vale, said he has lost more than £30,000 through a Self-Invested Personal Pension (SIPP). He was duped into the transfer and investment by unregulated firm Jackson Francis which was liquidated in 2014. His investment may or may not be worthless – depending on whether Store First is wound up later in 2019.

Robert McCarthy – who is one of 500 Store First investors who used Berkeley Burke as their SIPP provider – made a serious complaint against Berkeley Burke – and spoke to BBC News on the matter.

McCarthy said:

“Basically I’ve lost my private pension. Thirteen years of hard work, they’ve taken it, it’s gone.

I’ll never trust anyone again. And I can’t believe that they can get away with what they’ve done.”

The BBC has reported Store First as saying that: “In McCarthy’s case, Berkeley Burke failed to instruct Store First on how to manage the pods they purchased as part of a SIPPS. This means that the store pods have stood empty since their purchase. With returns based on rent paid for using the pods purchased, no returns have been made on these empty pods.”

This scam follows the same path as so many other scams we see: an unregulated advisory firm, Liverpool-based company Jackson Francis, introduced the victims to Berkely Burke and the Store First investment. (Jackson Francis was wound up in 2014). With promises of the investment being ‘the next best thing’ and also guaranteed high returns, 500 people signed their pensions over to the SIPPS provider Berkeley Burke.

Berkeley Burke then invested the SIPPS into the store pods, but failed to give permission for Store First to rent the pods out on behalf of the investors – meaning they stood empty. Store First said they were never contracted to manage, advertise or let the storage pods. That responsibility, they say, lies with the pension trustee, Berkeley Burke.

This is not the first time Berkeley Burke have been accused of negligence. In the High Court last October, Berkeley Burke was found to have failed to show due diligence in vetting unregulated investments for another client. The company are currently seeking to appeal against the decision. But with a further 14 individuals, based in Wales alone, making complaints against them, there is definitely no smoke without fire.

Whilst Capita Oak tuned out to be a scam (currently under investigation by the Serious Fraud Office) and victims have lost huge chunks of their pensions, the initial presentation they were given made the scheme look 100% genuine.

I spend a lot of time sharing our blogs over Facebook into different groups, trying to get the message across about pension scams. Interestingly, many of my posts are met with negative comments.

Last week in a comment on an expat forum, I was told that my blog about expats being targeted by scammers was “irrelevant”. I have also had comments like: “I would never fall for a scam.” However, there is clear evidence that falling for a scam doesn´t make you stupid or naive – especially when the scammers are so good at disguising their sham schemes as genuine investments.

Therefore, when it comes to the crunch, it is incredibly easy to fall for a pension scam – especially when it is registered by HMRC and promoted by a qualified financial adviser. It is hard to tell the difference between the good guys and the bad guys (who are so good at clever disguises). Pension scam victims include airline pilots, doctors and nurses, teachers, scientists, bankers and even a solicitor or two. Anyone can fall for a cleverly-sold scam – and they frequently do.

Toby Whittaker, owner of Store First, as you can see from his Twitter page, is still promoting Group First and Store First as going concerns. He is also fighting the winding-up petition by the Insolvency Service against Store First.

Despite the fact that the Capita Oak scam now lies in the hands of Dalriada Trustees (appointed by the Pensions Regulator) and the ongoing petition to have Store First wound up (purportedly in the “public interest”), Toby Whittaker still stands proud and says he had no idea that his company was being used as part of a scam.

No one knows where the money went, but it certainly didn´t go to the victims of this scam. We can bet it lined the pockets of the scamming salesmen who incorrectly invested over 1,000 victims’ pensions into Store First.

If the UK government succeeds in its petition to wind Store First up, the hundreds of victims will lose all the funds in their pensions.

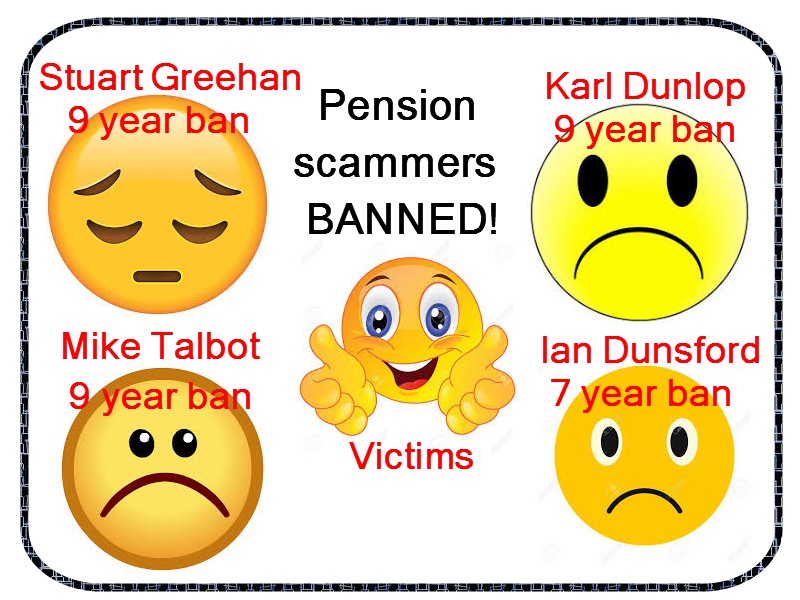

Articles like New Model Adviser’s report on some of the scammers behind the Capita Oak/Henley/Store First scam getting banned always makes me smile. Knowing that a few pension scammers (four in this case), are being named and shamed – as well as banned from being directors – motivates me to share information about these evil scams with the public.

“An investigation led by the Insolvency Service revealed the directors were connected with Transeuro Worldwide Holdings, which helped fund two introducer firms Sycamore Crown and Jackson Francis. The firms were involved in the transfer of £57 million of pension savings.

Sycamore Crown director Stuart Greehan agreed to a nine-year voluntary ban as a result of false and misleading statements to encourage investors to transfer their pensions.

Karl Dunlop, director of Imperial Trustee Services, and Ian Dunsford, director of Omni Trustees, agreed to bans of nine and seven years, respectively, for failing to act in the best interests of members and ‘failing to ensure investments were adequately diverse’.

While not a formally appointed director of Transeuro Worldwide Holdings, Mike Talbot (AKA Stephen Talbot) accepted a nine-year disqualification undertaking for failing to disclose what happened to the millions of pounds of pension assets.”

BUT, IN ADDITION TO THESE EVIL SCAMMERS, THERE WERE OTHER PLAYERS IN THIS APPALLING TRAGEDY AND THEY WERE NOT MENTIONED. SO HERE ARE THE OTHER PEOPLE WHO PLAYED LEADING PARTS IN THIS FOUL PLAY:

Stephen Ward of Premier Pension Solutions SL and Premier Pension Transfers Ltd – he handled the transfer administration from the original (ceding) pension providers. He was, apparently, paid £300 per Capita Oak transfer – and would have known that he was condemning each member to certain loss of his or her pension.

XXXX XXXX of Nationwide Benefit Consultants, The Pension Reporter, Victory Asset Management and Tourbillon, was clearly the “controlling mind” behind Capita Oak. He also ran the Thurlstone loan scheme which paid 5% in cash to the Capita Oak victims as a “bonus” or “thank you”. HMRC is now taxing these payments at 55% as they qualify as unauthorised payments. XXXX XXXX then went on to launch the successful Trafalgar Multi Asset Fund scam which saw over 400 victims lose their pensions to high-risk toxic loans to Dolphin Trust in an STM Fidecs Gibraltar QROPS. XXXX – as with most pension scammers – subsequently ignores the plight of the victims when the schemes eventually and inevitably collapse. XXXX is under investigation by the Serious Fraud Office and was also responsible for the Westminster pension scam.

Mark Manley of Manleys Solicitors – acting for XXXX XXXX.

Stuart Chapman-Clarke, Christopher Payne, Ben Fox, Bill Perkins, Alan Fowler, Karen Burton, Tom Biggar, Sarah Duffell, Jason Holmes, Metis Law Solicitors, Roger Chant, Brian Downs, Phillip Nunn and Patrick McCreesh all played further prominent roles in this series of scams and profited to a greater or lesser degree.

It is believed that cold calling techniques were used to lure unsuspecting victims into this series of unregulated investment scams. Victims’ pension savings were transferred into bogus occupational pension schemes whose trustees/administrators were Omni Trustees and Imperial Trustee Services. The schemes were Henley Retirement Benefit Scheme (HRBS) and Capita Oak Pension Scheme (COPS). But the scammers also used a variety of SIPPS which included Berkeley Burke, Careys Pensions, Rowanmoor, London and Colonial and Stadia Trustees.

As is often the case in scams like these, the victims were lured in with promises of so-called guaranteed high returns by spivs masquerading as advisers, who were also unqualified and unregulated to give financial advice.

The unqualified advisers were able to transfer millions of pounds’ worth of pension savings into these schemes which included investments in unregulated storage units and over £10 million into COPS (Capita Oak) and over £8 million into HRBS (Henley). The promised high returns were never paid to the investors – but handed over to the scammers instead. The pension funds are now suspended with the funds trapped in these illiquid investments.

The company directors have received a total ban of 34 years collectively. Here at Pension Life we would have liked to have seen lifetime bans all round.

The Serious Fraud Office (SFO) is now moving forward with their investigations against Omni and Imperial. They urge people who are members of HRBS (Henley) and COPS (Capita Oak) to contribute to criminal evidence against the scammers via a questionnaire.

As always, the team at Pension Life urges pension holders to be wary of pension scammers. Never accept a cold call offer, be aware that scammers lurk everywhere and if it seems to good to be true it probably is!

Pension Scammer Phillip Nunn receiving an award for “Entrepreneur of the Year”

Phillip Nunn has been reported to Action Fraud – which John Ferguson of Square Mile Financial Services describes as being “nobody and with no authority” – on numerous occasions by victims of various scams.

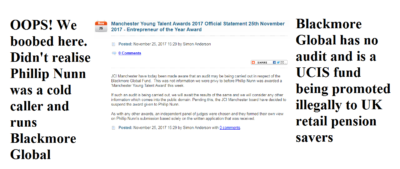

Phillip Nunn, cold caller and “fund manager” of the Blackmore Global investment scam, was given the Entrepreneur of the Year Award by JCI Manchester, but this was reversed shortly afterwards:

“JCI Manchester have today been made aware that an audit may be being carried out in respect of the Blackmore Global Fund. This was not information we were privy to before Phillip Nunn was awarded a ‘Manchester Young Talent Award’ this week.

If such an audit is being carried out, we will await the results of the same and we will consider any other information which comes into the public domain. Pending this, the JCI Manchester board have decided to suspend the award given to Phillip Nunn.”

MYT Phillip Nunn Award Retraction

“An independent panel of judges formed their own view on Phillip Nunn’s submission based solely on the written application received.”

I would love to read Phillip Nunn’s submission. It would certainly make very interesting reading. I doubt it would have included the fact that Nunn and his accomplice Patrick McCreesh were cold callers and lead generators in the Capita Oak/Henley Retirement Benefits/multiple SIPPS/Store First scam – which led to well over 1,000 victims losing over £120 million worth of pensions.

The Insolvency Service produced a witness statement which stated:

“Members of CAPITA OAK indicated they were initially contacted by Craig Mason or Patrick McCreesh of Nunn McCreesh of Its Your Pension Ltd and offered pension review services prior to them being referred to JACKSON FRANCIS or Sycamore for the transfer of their pension to CAPITA OAK.

On 3.3.15 I received an undated letter in which it was stated that Its Your Pension had not traded and was a dormant company and that Nunn McCreesh had traded as an insurance brokerage between 2009 and 2012 when they entered into a verbal arrangement with TRANSEURO where in return for providing pension leads to JACKSON FRANCIS they received a commission from TRANSEURO.

Nunn McCreesh provided JACKSON FRANCIS with 100-200 leads per month which were provided by email and/or telephone for which they received £899,829.86 from TRANSEURO during the period 26.3.12 to 14.5.14.”

Phillip Nunn’s lawyers, Slater and Gordon (funny that, also nominated for an award) tried to claim that Nunn McCreesh’s involvement in the Capita Oak scam was “minimal”. But I wouldn’t describe generating 5,000 leads, cold calling thousands of victims and being paid nearly £900k “minimal”.

On the subject of Slater and Gordon, earlier this year they threatened me with defamation proceedings for exposing Nunn’s scamtivities. It was curious that they couldn’t see any conflict of interest in representing Phillip Nunn when they were also representing the very victims (of Capita Oak) whom he had cold called in the first place.

Slater and Gordon’s Steve Kunziewicz claimed that “Blackmore Global is a prestigious, multi-asset investment house with over £60 million in assets under management, offering institutional and high net-worth clients access to a wide variety of investment products in order to maximise their returns.”

But there is no audit for Blackmore Global and only evidence suggesting the fund is invested in toxic, high-risk, illiquid crap including:

Swan Holding PCC

Kingston Capital Partners (Belize private equity vehicle controlled by Nunn & McCreesh)

GRRE Invest

Spinaris 90 ( UK sports spread betting)

The Blackmore Global audit was promised more than a year ago but never materialised. The audit has now been promised “by the end of the year” – but Grant Thornton won’t specify which year.

However, far from the Blackmore Global fund being aimed at “institutional and high net worth clients”, Phillip Nunn targets low-risk pension savers using a variety of unregulated so-called “advisers” such as David Vilka of Square Mile Financial Services. Many of the Blackmore Global victims were cold-called and/or introduced by Phillip Nunn’s cold-calling outfit, Aspinall Chase. Some were transferred to Maltese QROPS run by Integrated Capabilities and Harbour (now taken over by STM) and to Hong Kong.

Blackmore Global is a UCIS fund – unregulated collective investment scheme. And it is illegal to promote these to UK retail investors as this was banned by the FCA in 2014.

I doubt the other nominees and award recipients will appreciate having been listed alongside Phillip Nunn who has a history of promoting other scammers’ pension scams and is now running one himself. Perhaps JCI Manchester ought to vet candidates for the Manchester Young Talent Awards more carefully in the future.

SAIL FINANCIAL AND TRAFALGAR MULTI ASSET FUND: What is the connection?

Who is behind Sail Financial? And what is the connection to Trafalgar Multi Asset Fund? We know Trafalgar Multi Asset Fund was originally run by XXXX XXXX as “Victory Asset Management” and that XXXX had also been behind the Capita Oak, Henley Retirement Benefits Scheme and Westminster pension scams: wound up by the Insolvency Service; now in the hands of Dalriada Trustees and under investigation by the Serious Fraud Office.

We also know that the £120 million of store pods purchased for Capita Oak, Henley RBS and hundreds of SIPPS are now probably worthless and Store First is subject to a winding up petition due to be heard on 1st August in Manchester.

In addition to being the Investment Manager of the Trafalgar Multi Asset Fund, XXXX was also the “financial adviser” in the form of his firms Global Partners Limited and The Pension Reporter – a “trading style” of XXXX’s Nationwide Benefit Consultants. But none of these firms were licensed for pension or investment advice.

However, Joseph Oliver’s Marcus Groombridge has stated:

“I can confirm that XXXX XXXX and Nationwide Benefit Consultants Ltd were appointed on the 29th of May 2014 and terminated on the 8th of April 2016. The permission for insurance mediation covers pension advice.”

Phew! What a relief. I am now looking forward to Mr Groombridge’s full cooperation with putting XXXX XXXX’s victims back into the position they should have been in had they not been scammed into investing their pensions in the Trafalgar Multi Asset Fund in the first place. I will also probably remind Mr Groombridge that the Trafalgar matter is under investigation by the Serious Fraud Office – along with other pension scams “distributed” by XXXX XXXX in 2012/13.

If there hadn’t already been enough misery for the hundreds of victims of the Capita Oak and Henley Retirement Benefit schemes run back in 2012/13 – XXXX had also been operating pension liberation in the form of “loans” from his company Thurlstone, based in the Seychelles. The victims have now been sent tax demands. But XXXX and his solicitor, Mark Manley of Manleys Law, have ignored pleas to indemnify the victims from these crippling tax liabilities.

I have often wondered what people like XXXX do after their latest scheme collapses or implodes. History tells us that they simply get straight on with their next one – and in fact had probably started it already. XXXX has been a director of seven companies (according to Companies House):

Nationwide Benefit Consultants (active)

Nationwide Corporate Benefits (active)

Proactive Administration Solutions (active)

Nationwide Trustee Services (dissolved)

Ashton Abbott (dissolved)

Nationwide Tax Administration (dissolved)

Admin Protection (dissolved)

XXXX has resigned from Nationwide Benefit Consultants and Nationwide Corporate Benefits – and appointed someone called Raymond Hampton as a director. But XXXX remains a director of Proactive Administration Solutions. So perhaps that is one to watch.

XXXX’s background is in the “distribution of pension schemes” (his words). He has worked closely with the cold-calling and lead generation firms (such as Jackson Francis, Sanderson Clarke and Barncroft Associates run by XXXX´s mates Ben Fox and Stuart Chapman-Clarke) who were involved in the Capita Oak and Henley scams.

So what is XXXX doing now? Perhaps whatever project he is working on involves trying to make enough money to compensate the victims of Capita Oak, Henley, Westminster and the Trafalgar Multi Asset Fund – all of the schemes are now under investigation by the Serious Fraud Office. It is also probable that Gibraltar Trustees STM Fidecs no longer want terms of business with XXXX XXXX now that so many of his schemes are subject to criminal investigations. STM Fidecs also probably now realises it was a serious conflict of interest taking business from an adviser who was also the Investment Manager to the Trafalgar Multi Asset Fund – which is now in the process of being wound up.

While I was idly puzzling over what XXXX´s next scheme might be, I started hearing reports about a firm called Sail Financial doing the rounds of firms in Europe – touting offering to do “introducing” and cold calling. Looking at the Sail Financial website, it is impossible to see who is involved in the business – no names, no address, no regulation. According to the Companies House register, Sail Financial – incorporated on 8.5.2015 – has two directors: Robert Hathaway and Brian Westhead. Neither of those names rang any bells with me.

Hathaway has no other directorships listed. However, Westhead does: he is listed as a director of a dissolved company called BIGB22 (08559856). This company’s previous names were Portia Financial and The Pension Reporter: XXXX XXXX’s firms. These firms have a history of being involved in pension and investment scams, cold calling and unregulated financial advice. The victims of the Trafalgar Multi Asset/STM Fidecs pension and investment scam were introduced and “advised” by Portia Financial, GPL (Global Partners Ltd) and The Pension Reporter, with advice letters signed by XXXX XXXX and Tom Biggar.

So clearly there is a connection between Sail Financial and various firms and schemes run by XXXX XXXX – including Trafalgar Multi Asset Fund. Perhaps XXXX XXXX is sailing round the Mediterranean now? I just hope he doesn’t have one glass of champagne too many and fall overboard.

In every pension scam there is one beginning, lots of middles, and always a wretched ending for the victim and a profitable ending for the scammers. The beginning is always a negligent, lazy, box-ticking transfer by a ceding provider – the worst of which always tend to be the likes of

In every pension scam there is one beginning, lots of middles, and always a wretched ending for the victim and a profitable ending for the scammers. The beginning is always a negligent, lazy, box-ticking transfer by a ceding provider – the worst of which always tend to be the likes of

Another victim of Berkeley Burke SIPPS investments into Store First storage pods has come forward. 55-year-old factory worker Robert McCarthy, of Ebbw Vale, said he has lost more than £30,000 through a Self-Invested Personal Pension (SIPP). He was duped into the transfer and investment by unregulated firm Jackson Francis which was liquidated in 2014. His investment may or may not be worthless – depending on whether Store First is wound up later in 2019.

Another victim of Berkeley Burke SIPPS investments into Store First storage pods has come forward. 55-year-old factory worker Robert McCarthy, of Ebbw Vale, said he has lost more than £30,000 through a Self-Invested Personal Pension (SIPP). He was duped into the transfer and investment by unregulated firm Jackson Francis which was liquidated in 2014. His investment may or may not be worthless – depending on whether Store First is wound up later in 2019.

Victims were also invested into the Store First storage pods via

Victims were also invested into the Store First storage pods via  Stephen Ward

Stephen Ward

Stephen Ward of Premier Pension Solutions SL and Premier Pension Transfers Ltd

Stephen Ward of Premier Pension Solutions SL and Premier Pension Transfers Ltd Mark Manley of Manleys Solicitors – acting for XXXX XXXX.

Mark Manley of Manleys Solicitors – acting for XXXX XXXX. It is believed that cold calling techniques were used to lure unsuspecting victims into this series of unregulated investment scams. Victims’ pension savings were transferred into bogus occupational pension schemes whose trustees/administrators were Omni Trustees and Imperial Trustee Services. The schemes were

It is believed that cold calling techniques were used to lure unsuspecting victims into this series of unregulated investment scams. Victims’ pension savings were transferred into bogus occupational pension schemes whose trustees/administrators were Omni Trustees and Imperial Trustee Services. The schemes were