The sophistication of investment scams has reached new levels in Singapore

The sophistication of investment scams has reached new levels in Singapore

I “borrowed” this blog from my Twitter friend in Singapore who clearly understands and cares about investment scams – and the inability of the inept authorities to do anything about them. This is true not just in Singapore but throughout the world – particularly the UK, the Isle of Man, Gibraltar, the Cayman Islands, Guernsey, Ireland, Dubai, and Hong Kong.

I could not improve upon his excellent blog, but I have put some comments in red in the body of the text (with apologies to Lee!).

This is a story about how scammers have used the loopholes within the law to fleece hundreds of millions of dollars (and pounds and Euros in other jurisdictions) from an unsuspecting public. Many of whom are retirees and young people venturing into alternative investments for the first time in their lives.

This is a story about how scammers have used the loopholes within the law to fleece hundreds of millions of dollars (and pounds and Euros in other jurisdictions) from an unsuspecting public. Many of whom are retirees and young people venturing into alternative investments for the first time in their lives.

In Singapore, there are two primary agencies that are set up to ensure a safe investment environment for its people. The Monetary Authority of Singapore (MAS) that regulates the financial industry and the Commercial Affairs Department (CAD) of the Singapore Police Force that investigates commercial crime and Fraud.

Just wanted to add a few more: chia seeds, eucalyptus plantations, truffle trees, forex trading, life assurance policies, football betting, property loans, rubbish recycling, litigation funding, timeshares, films, claims management companies etc.

In support of innovation (Lee uses the word “innovation” – but I would have used the word “opportunism”) in the financial industry, Alternative Investment Offers have been allowed to thrive. Non-traditional Products are being offered to the lay public, advertised widely on social media and even in the mainstream media with barely any restrictions. (In the UK, we would refer to many of these as UCIS – unregulated collective investment schemes – which are illegal to promote to retail investors). Many vendors of these make wild claims of double-digit percentage returns per annum, sometimes coupled with apparent full capital protection that targetted investors would just swallow wholesale.

These companies are not regulated by MAS and will often be listed as such in the MAS-issued Investor Alert List. But being on the Investor Alert List simply means Caveat Emptor … nothing more. Legitimate companies, as well as unscrupulous ones, are similarly listed there without distinction. So in most cases, the attractive returns and false assurance of safety are just too irresistible to the average investors who would be pulled in by the hundreds, if not thousands. I reckon few people ever think to look at the MAS website – just as few ever look at the FCA website where well-hidden warnings lurk deep below the surface.

While not all Alternative Investments are dodgy, many of them are because the current law offers a fairly wide window (between 3 to 8 years) for them to operate before the law catches up. Why? Because the law enforcement agency that investigates fraud only starts to investigate after many victims have reported their loss. There are victims who do not report because of fear, because of embarrassment, because of unrealistic, hopeful optimism and a variety of other reasons so by the time CAD gets involved, it would have added more years and more new victims. A lot more people, sadly, would have been hurt by then. This is the most significant factor in stopping financial fraud – if the first whistle were to prompt action by the authorities, more victims could be prevented. The feet of clay by regulators and law enforcers help the scammers and facilitate the crimes.

Ponzi schemes are chief among these and as with all Ponzis, the early investors are taken in by the promised high returns being achieved. This pool of satisfied investors will go on to sink in additional funds. But more than that, they are often trotted out on stage at investment seminars to be the best spokespersons for their “safe and profitable” investments. Some are even recruited to be sub-agents who earn referral commissions.

A very common scam I see over recent years involves companies that may own some land in a distant country, directly or indirectly via their selected “Developer Partners” who have cleared their “rigorous” due diligence process and deemed safe. Money is borrowed from the lay public by an intermediary set up for that specific fundraising purpose. This intermediary is supposed to channel the funds out to the said Developers for the purpose of infrastructure development or some construction activities on the property. In return, the intermediary company, freshly created, probably a limited liability entity registered in some opaque tax-free haven, signs an IOU agreement with the investor detailing scheduled repayments of interests and full capital at the end of 2 or 3 or 4-year terms. He’s just described Dolphin Trust and similar investment “loan-note” scams perfectly.

The IOU agreement or promissory note does not accord the investors (or more accurately the lenders), any say on how the funds are utilised. There is also nothing to stop these unscrupulous vendors from using that same plot of land as their “collateral” to draw in funds from other investors in other markets.

Theoretically, that same piece of land could be used multiple times to borrow new money as long as the investors were not aware of it and had no legal title on that property. The number of times this “asset” is leveraged is limited only to the diabolical ingenuity of those vendors and the trusting innocence of an investing client pool. Am getting a bit worried now, as I think some of the scammers – who hadn’t already thought of this – might be getting very excited!

Other fundraising schemes can be created… perhaps through the issuance of minibonds in countries like the UK or in Europe. Or through commercial paper described as Development Funds that pay generous coupon rates over medium term, offered to selected high net worth clients. (And low-net-worth clients – the scammers aren’t fussy!).

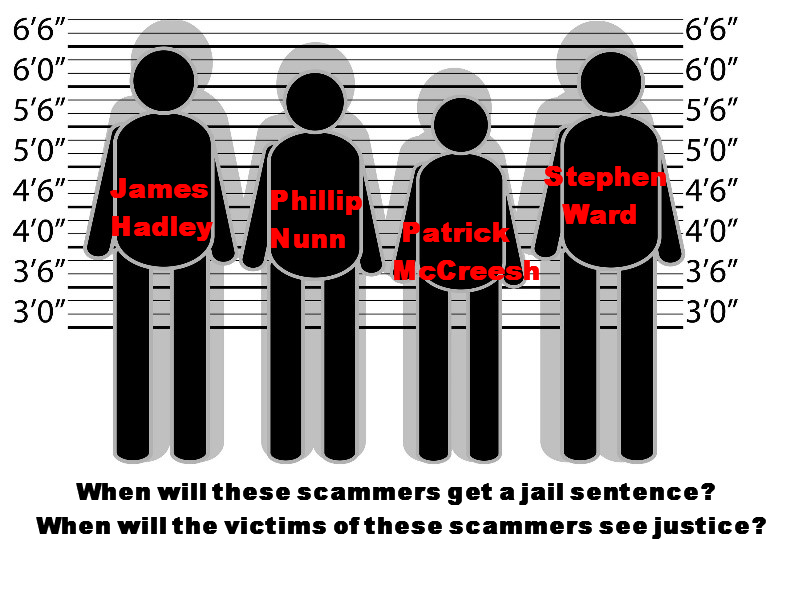

Different company names are formed but the directors may be the same. The product brief is almost always similar and the advertising media material professionally done and is always flashy. Invariably these vendors will hold charity events and engage media celebrities or host politicians to lend credibility to their cause. They would list fake awards and renowned organisations as their business partners on their websites. All these with the sole intent of creating an image of legitimacy. This perfectly describes Phillip Nunn and his Blackmore Global investment scams – promoted by David Vilka.

Sometimes they may even attempt to raise public funds via a back door listing through an acquisition of a public listed entity that had fallen under judicial management.

Who are these people who are capable of such an elaborate scheme that spans international borders? Will the law catch up with them before they escape with their ill-gotten loot? Will justice be served in time and make an example of how fraud should not be excused as business failure?

Alas, only time will tell. Lee doesn’t seem optimistic. And I most certainly am not. The scammers make far too much money from such investment scams – and pension savers are ridiculously easy targets. The cold-calling ban will have negligible effect, and the ceding pension providers will keep on keeping on handing over pensions to the scammers willy-nilly.

A firm with advisers who are unwilling to answer all of the questions you ask them is clearly a firm to be avoided.

A firm with advisers who are unwilling to answer all of the questions you ask them is clearly a firm to be avoided.

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

AND to rub salt into the wounds of the Trafalgar victims,

AND to rub salt into the wounds of the Trafalgar victims,

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based

Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based  Capabilities and Harbour (n

Capabilities and Harbour (n Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated

This new pension arrangement locked me in for 10 years – definitely a “long-term relationship” – giving all parties the opportunity to drain my pension dry in fees. Credit where credit is due, however. Once I discovered I was in a scam, the director Andy Dawson (bottom row, 3rd from the left) did make an extraordinary effort not only to redeem the investments but successfully persuaded most parties to waive their early exit penalties and refund their fees. Only the greedy Symphony Fund chose to keep the penalties and that’s after mysteriously dropping in value 30% just before redemption. Thanks to Andy Dawson and his team, I did manage to get back 92% of my pension. But the BIG QUESTION is what has happened to the other 1,100+ members? It is inconceivable I was the only one transferred into this scheme via Vilka et al.

This new pension arrangement locked me in for 10 years – definitely a “long-term relationship” – giving all parties the opportunity to drain my pension dry in fees. Credit where credit is due, however. Once I discovered I was in a scam, the director Andy Dawson (bottom row, 3rd from the left) did make an extraordinary effort not only to redeem the investments but successfully persuaded most parties to waive their early exit penalties and refund their fees. Only the greedy Symphony Fund chose to keep the penalties and that’s after mysteriously dropping in value 30% just before redemption. Thanks to Andy Dawson and his team, I did manage to get back 92% of my pension. But the BIG QUESTION is what has happened to the other 1,100+ members? It is inconceivable I was the only one transferred into this scheme via Vilka et al.

This week Henry Tapper wrote a blog entitled, “

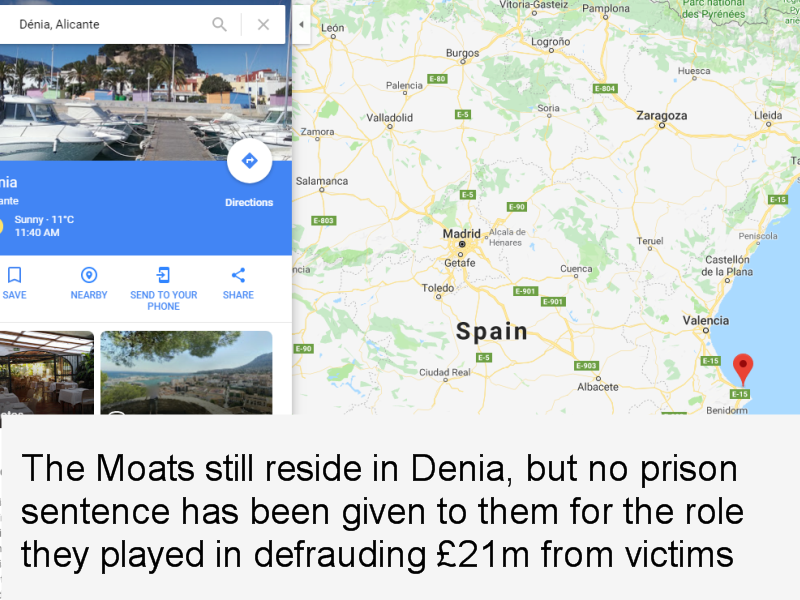

This week Henry Tapper wrote a blog entitled, “ They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

I would like to highlight that the rider of the jet ski does bear a remarkable resemblance to Phillip Nunn, cold caller and “fund manager” of the

I would like to highlight that the rider of the jet ski does bear a remarkable resemblance to Phillip Nunn, cold caller and “fund manager” of the

Interestingly,

Interestingly,

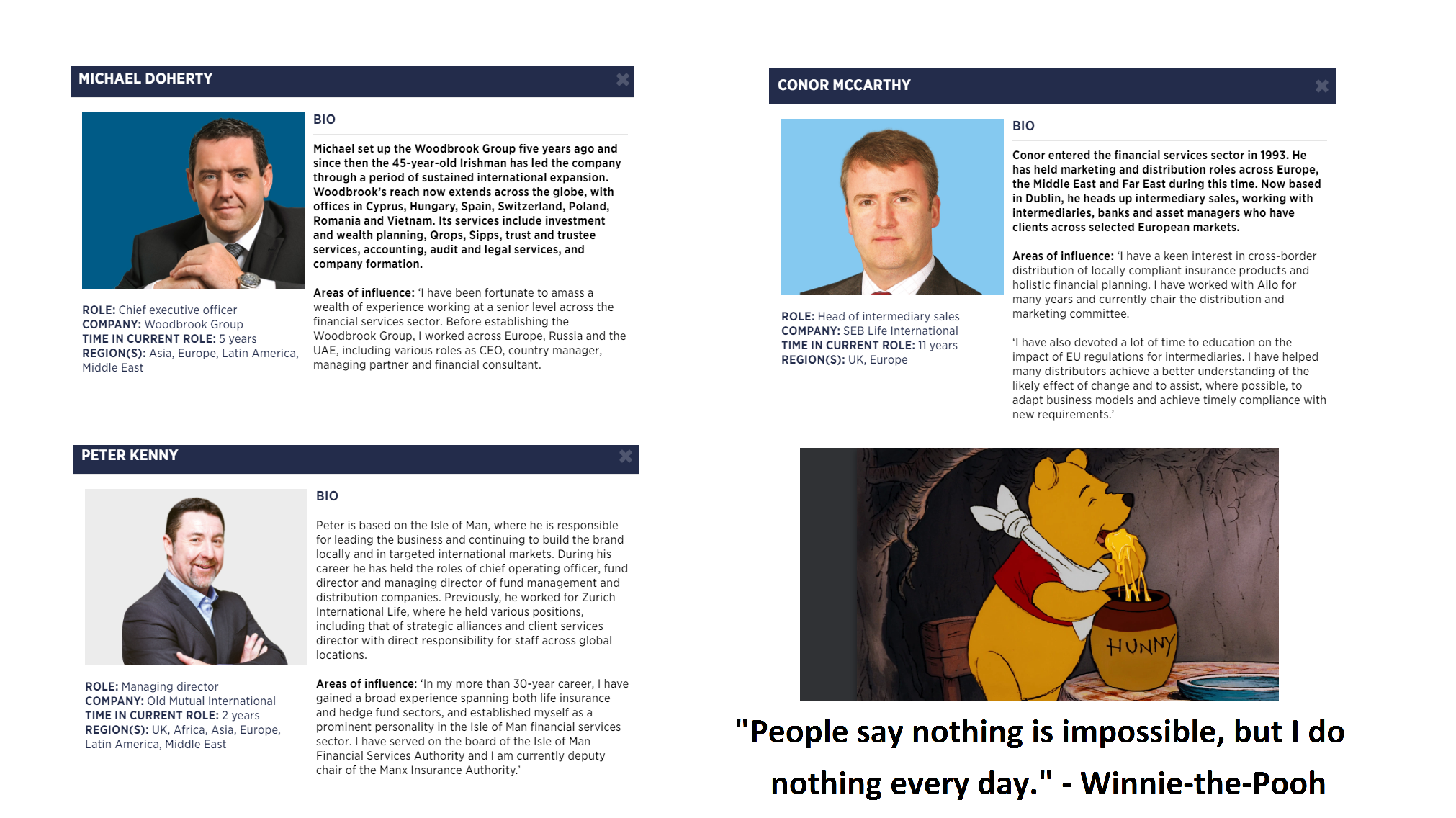

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders:

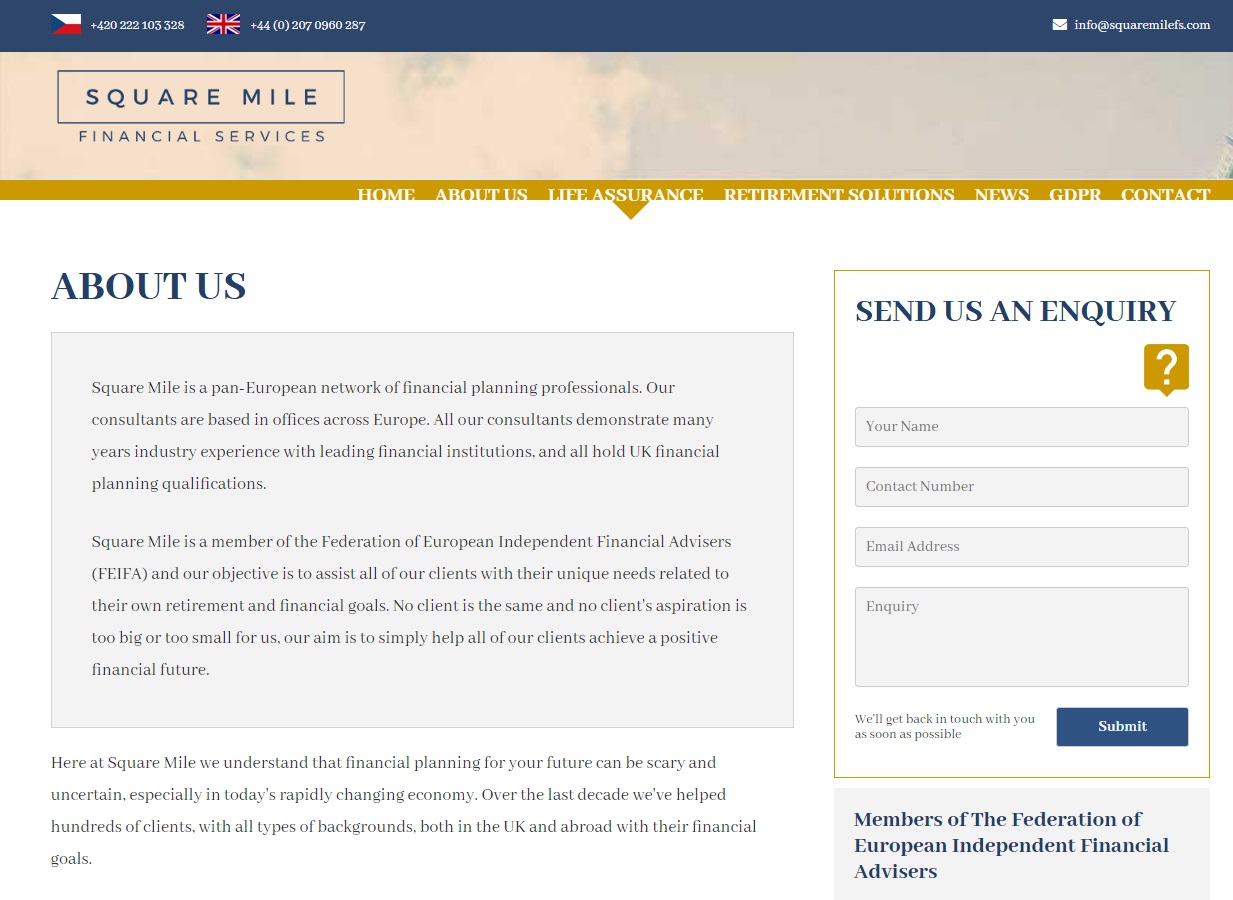

Investors’ trust is what gets violated in so many cases by irresponsible and negligent insurance companies such as Old Mutual International, SEB, Generali, RL360, Friends Provident International – and, of course, the firm in the Cayman Islands: Investors Trust. These companies – also known as “life offices” (although we prefer to call them “death offices” because they help destroy victims’ life savings – and sometimes cause the death of their distraught victims) – have a number of lethal practices which result in financial ruin for thousands of policyholders: A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

A prime example of these vile practices was in the case of Mr. S – a driving instructor from Milton Keynes. His final salary pension scheme was transferred to a QROPS in Malta despite the fact that he was a UK resident and had no need for his pension to be transferred offshore. His “adviser” was David Vilka from a firm called Square Mile International Financial Services. This firm had an insurance license but no investment license. Therefore, Square Mile could legally sell insurance products such as dog insurance – but could certainly not provide investment advice.

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer

Far from being contrite or apologetic, however, the scammer who risked Mr. S’ pension in the first place – David Vilka of Square Mile International Financial Services in the Czech Republic – showed no shame and made no attempt to recover the remainder of his victim’s pension. In fact, when I exposed Vilka’s vile scam, I was threatened by his two-bit American lawyer

Mr. Davies is referring to the UCIS investment scam, Blackmore Global, which was illegally promoted to retail investors – and which is a fraud from start to finish.

Mr. Davies is referring to the UCIS investment scam, Blackmore Global, which was illegally promoted to retail investors – and which is a fraud from start to finish. And again, significantly, he was not cold-called. He sought out Mr. Vilka and Square Mile. Nor did Mr. Vilka or Square Mile receive any payment from the Blackmore fund or its partner firms regarding Mr. Sexton’s transaction as confirmed by the Czech National Bank which has direct access to Square Mile’s company bank accounts via an electronic data box. Are you talking about the accounts which haven’t been updated since 2014?

And again, significantly, he was not cold-called. He sought out Mr. Vilka and Square Mile. Nor did Mr. Vilka or Square Mile receive any payment from the Blackmore fund or its partner firms regarding Mr. Sexton’s transaction as confirmed by the Czech National Bank which has direct access to Square Mile’s company bank accounts via an electronic data box. Are you talking about the accounts which haven’t been updated since 2014? LOWELL DAVIES LLP

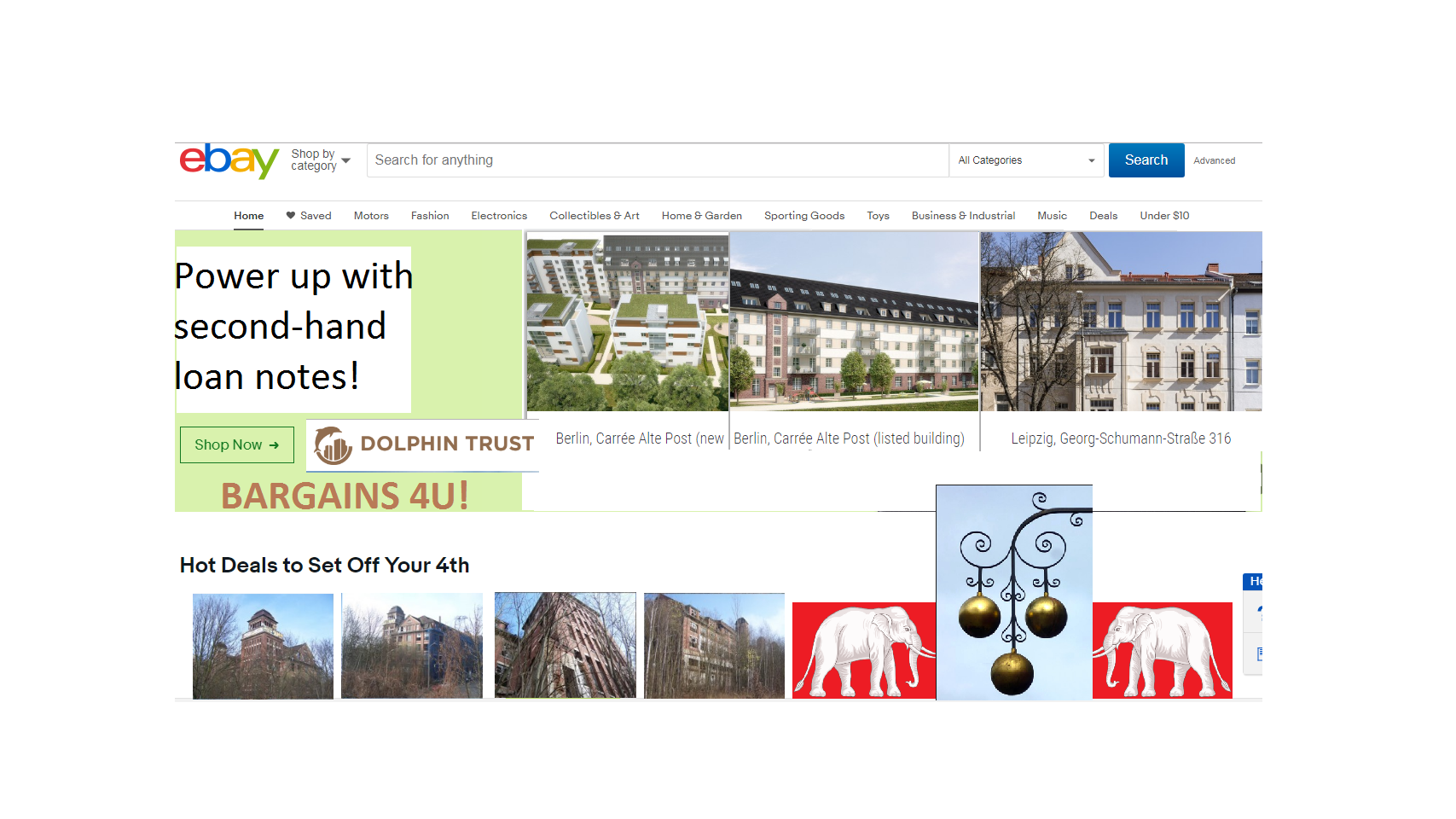

LOWELL DAVIES LLP I’ve been very concerned about Dolphin Trust GmbH for some time. There’s an awful lot of pension money being loaned to this company – and I don’t get to hear of many (in fact any) people who have had their loans repaid. That doesn’t mean they haven’t been repaid – it just means I haven’t heard about it.

I’ve been very concerned about Dolphin Trust GmbH for some time. There’s an awful lot of pension money being loaned to this company – and I don’t get to hear of many (in fact any) people who have had their loans repaid. That doesn’t mean they haven’t been repaid – it just means I haven’t heard about it. Without the benefit of any assurances from the nice men at Dolphin Trust – Charles Smethurst, Helmut Freitag, Axel Krechberger and Matthias Ruhl – we will just have to hope that Mr Doran manages to offload the second-hand loan notes that STM Fidecs allowed 400+ victims’ life savings to be invested in. Perhaps I’ll drop him a friendly note and suggest he tries ebay.

Without the benefit of any assurances from the nice men at Dolphin Trust – Charles Smethurst, Helmut Freitag, Axel Krechberger and Matthias Ruhl – we will just have to hope that Mr Doran manages to offload the second-hand loan notes that STM Fidecs allowed 400+ victims’ life savings to be invested in. Perhaps I’ll drop him a friendly note and suggest he tries ebay.

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.