When I grow up, I want to be a hairdresser. Not a care in the World other than how short/long/blonde/purple/curly/straight my clients want their Barnets. And nothing to talk about other than where they will go on holiday: Torremolinos, Benidorm or Amsterdam (wink wink…).

World First – so boring you’ll never lose any money using it.

But for now, I’m stuck in the real World – the one where all I see is scams from morning ’til night. All my clients are heartbroken, worried sick, traumatised and devastated. Few of them can afford holidays – much less frequent trips to the hairdresser.

I am regularly asked whether I can recommend a financial adviser. Not just any financial adviser – but one with a magic wand who can somehow rescue whatever is left after a greedy scammer has destroyed most of their victims’ life savings. Bearing in mind most offshore advisers are still stuck in the offshore bond-of-death rut (Old Mutual, RL360, Friends Provident etc.), I rarely make recommendations.

There are a few financial institutions that people can’t live without: bank; insurer; pension provider; mortgage lender and credit card issuer. Then a few more that make life smoother: currency exchanger; tax adviser; financial adviser.

I can make some recommendations about the first batch. My bank – CaixaBank – is the one I recommend because it is the one closest to my house (takes me 90 seconds to walk there). It is next to the barber and opposite the fruit shop – so couldn’t be handier. I also get my insurance, pension and plastic there – so no need ever to go anywhere else.

I used to be a tax adviser so tend to do tax stuff myself, and don’t need a financial adviser because in Spain banks tend to do a pretty good job with money. Most people in Spain who escape the clutches of the chiringuitos (scammers) just tend to use their trusted – or nearest – bank. (In fact, the Spanish look on with astonishment at the British expats who get regularly scammed by British expats – and wonder why Brits don’t just use properly-regulated and qualified Spanish advisers).

The only money thing I contract out is currency transfer. And for this I use a company called World First – and have done for ten years. Don’t get me wrong – this isn’t an advert. But if World First chose to send me a “thank you” for this blog in the shape of a large box of chocolates I would be unashamedly delighted.

Chocolates gratefully received from World First!

So what do I like about World First? Well, er, nothing – actually. It is really boring. It does what it says on the tin: currency transfers. It charges what it says it will charge (also in big letters on the tin). It is as transparent as it is dull. When I move Sterling from my UK bank and get Euros in my Spanish bank, I get the right amount. To the penny (or, rather, cent). On time. No dramas.

There are no frills. Nothing exciting ever happens. No nasty surprises – but no nice ones either. I’m never promised three for the price of two, or that I will lose a stone in a week, or that I will meet my handsome prince and live happily ever after. But most important of all, I am never promised a “guaranteed 8% return”.

Paul has listed some of the recent scams which have destroyed thousands of victims’ savings by promising the magic 8% bait: Mederco; London Capital & Finance; HAB. There are, of course, dozens more such as Axiom Legal Financing, Premier New Earth, various student accommodation and nursing home funds, car parks, store pods and derelict German sheds. Plus thousands of toxic structured notes like those provided by Commerzbank, Royal Bank of Canada, Nomura and Leonteq – and distributed by the bond-of-death providers themselves: Old Mutual International, Friends Provident International, RL360, SEB, Generali, Hansard etc. And sold by unscrupulous “advisers”.

All this does beg the question: why does an FCA-regulated company such as World First never cross the line – while so many others are happy and eager to do so regularly? What is it about a boring old currency transfer service that sets it apart from “advisers” who routinely sign off DB pension transfers or who openly provide regulated services without being regulated?

We know from the British Steel debacle that out and out scams can easily be perpetrated right under the very nose of the FCA – with Active Wealth and Celtic Wealth having earned fortunes out of flogging collapsible flats in Cape Verde to the steelworkers for their pension investents. We know that Gerard Associates openly aided and abetted serial scammer Stephen Ward in the London Quantum scam – investing victims’ pension funds in all sorts of crap such as Dolphin and eucalyptus forests. (Gary Barlow’s Gerard Associates is still on the FCA register btw!).

More recently we know that the FCA deliberately turned a blind eye to the obvious investment scam London Capital & Finance, and that Hargreaves Lansdown was openly and brazenly promoting Neil Woodford’s high-risk and illiquid Woodford Equity and Income fund (now suspended). It is public knowledge that the FCA’s obscenely overpaid chief Andrew Bailey has long since lost interest in the boring task of regulating as he only has eyes for the top spot at the Bank of England (God help us!).

I think the answer is that the rogue, greedy, irresponsible firms who flout the regulations see an eye-watering opportunity to make a lot of money. So caution is not just thrown to the winds but also flushed down the loo. The golden opportunity won’t last long, but these opportunists don’t care how many people get ruined in the process – they will just make hay while the sun shines and then shrug their shoulders when it all goes tits up. After all, what is the worst that will happen? The FCA might rummage around in someone’s drawers and find a wet fish; or someone at ministry level might get cross enough to wag a finger or two.

A fund manager once said to me that he was astonished at how many financial services professionals get involved in scams and dodgy schemes. He said that this is an industry where practitioners can make a very respectable living, and keep their reputation and conscience intact. He also speculated that the huge pile of money that could be made from opportunistic bad practice (naked euphemism!) is only ever short term – and that it is bound to come crashing down eventually. And then, if the offender wants to keep trading, they have to start all over again with the next gig. And the next. And….(etc). They know that the regulators and the police are way too slow, lazy and stupid to do anything about it all – so it is a fertile hunting ground for the unscrupulous and inventive.

So back to my World: my only two financial services providers are CaixaBank and World First. Both pretty boring and predictable. Day in day out; year in year out – they do what they say they will do and charge me the standard rate for the privilege of routinely boring the pants off me. I know I will never be rich – and my life will never be exciting. But I also know I will never be either penniless or surprised (unless a fat box of chocolates rocks up next week!).

Boring pays

Being boring and straight does pay off. Chinese giant Alibaba recently bought a 40% stake in World First for a figure reported to be around $700m. Watch and learn ye scammers, opportunists and greedy bad guys.

The problem with money is that it blows away if you don’t hold it down, tie it up or stuff it down your knickers. That’s why you need to put it somewhere safe: in a shoe box on top of the wardrobe; under your mattress; in the safe or – if you’re feeling really brave – in the bank. Trouble is, left in cash, money shrinks (inflation, charges, moths). This is why so many advisers recommend a platform – aka “somewhere safe” to keep your money.

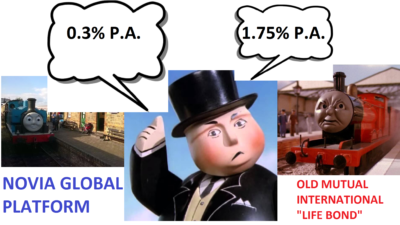

I’ve met Bill Vasilieff who runs Novia Global. He serves Earl Grey and nice biscuits. A man of few words, and even fewer syllables, he gave me a quick rundown on how the Novia Global platform works – and how much it costs.

I haven’t met Peter Kenny of Old Mutual International (OMI) – although I have spoken to him several times. As broadly Irish as Bill is Scottish, Peter Kenny also comes across as a softly-spoken and sincere chap. But there the similarity seems to end. Peter stood me up – I got a view of his office waiting room but wasn’t offered a cup of tea (let alone a biscuit).

Mind you, there isn’t much I don’t know about the Old Mutual International bonds. I’ve seen thousands of their policyholders’ statements – and they are frighteningly ugly and depressing. They accurately, faithfully and unemotionally report the destruction of their victims’ atrocious losses. And OMI regularly (like clockwork!) take their quarterly fees – irrespective of how deep the destruction of the policyholders’ funds is. In fact, some victims even find themselves in negative figures as OMI continue to account for their fees long after the whole blooming lot has gone.

Anyway, back to Bill and his welcoming teapot….I can’t really compare him to Pete but I can compare the two products. So here is a brief and brutal side-by-side line up of what the two “platforms” offer. And how much they cost. And how difficult they are to get out of. And how much financial crime they are associated with.

So the OMI “life bond” costs almost six times as much as the Novia Global platform. But that is if you are locked in for five years. You can get it cheaper – 1.15% – if you get locked in for ten years. But you must remember that if you are scammed, then OMI will have paid the scammer an 8% commission and you could get stuck with paying the quarterly fees for the next ten years, even if you’ve figured out you’ve been scammed. And the quarterly fees are based on your original investment – not on the impaired amount. If you’ve been scammed, and your fund value drops inexorably, the 1.15% will become bigger and bigger. And even if you lose your whole fund, OMI will keep taking their charges and pushing you further and further into debt.

A bit like the lyrics to Hotel California, with an OMI “bond”, you can’t check out any time you want, and you can only leave after between five and ten years. OMI will take that number of years to claw back the commission paid to your adviser – even if you have long since learned that your adviser was an unregulated scammer and has conned you into unsuitable, high-risk, high-commission investments that have badly damaged your fund. You are stuck with paying the quarterly fees to OMI – even after your whole fund has gone. One victim went from plus £300k to minus £25k – and counting. As your funds inside the OMI bond shrink, the 1.15% grows and helps destroy what is left of your fund even faster. But with the Novia Global platform, you can leave any time you want. No exit penalties. No hard feelings.

In Spain, the Supreme Court has ruled that bogus life assurance policies – such as those provided by Old Mutual International – used to hold investments are illegal. This is because they are neither proper insurance policies (which take risk in the interests of the consumer) nor are they proper investment platforms. The Spanish aren’t stupid – they can spot a scam much more easily than other jurisdictions and take action to prevent them from ruining future victims. This is in stark contrast to the likes of the Isle of Man and Gibraltar – which seem to revel in encouraging scams and protecting firms such as Old Mutual International (and STM Group) which facilitate financial crime on a massive scale.

Carl Melvin BA (Hons), MSc, CFP, FPFS, Chartered FCSI

Certified & Chartered Financial Planner, Affiliate of the Society of Trust & Estate Practitioners, Chartered Wealth Manager.

Somethings don’t change!

A new model challenge to the offshore sharks

The arrival of wraps allows fee-based financial planners in the UK to offer a sound, client-focused service to expats, who up until recently have been easy prey to unscrupulous offshore IFAs.

High charges – the total costs for such plans are huge but because they are layered between multiple charge types, such as those above, the investor does not fully understand how expensive the plan is.

In short, these plans are designed to make the product provider and the offshore IFA money, rather than serve the client. Their purpose is to hide big commissions for the salesperson and the massive penalties should the client stop the plan early.

One ploy that continues is the ‘extended term’ swindle. Here, the salesman sets up the offshore ‘regular savings plan’ with a term of, say, 20 years or more, even though the expat investor may only have a work contract for three to five years in the country in question.

So why not set the plan term to three or five years? Because the longer the term, the bigger the commission. Unfortunately, if the client stops the plan or reduces the contribution level, there are often very severe penalties or administration costs. It is not uncommon for the first two or three years’ contributions to be taken in charges, leaving the investor with nothing after saving for years – outrageous!

No redress

But then, how are you going to obtain redress? The provider will say the advice was given by the adviser firm, who in turn will blame the individual adviser who happens to have left the company or country. Nor is there any effective ombudsman service to enable the client to be compensated.

The offshore IFA sector demonstrates the following qualities:

Lack of professional standards regarding

commission disclosure and treating customers fairly rules l Low levels of professional qualification

A sales-led approach rather than a client-centric, service-based approach l Dubious integrity and honesty

Expats often have high tax-free salaries but no UK pension scheme benefits, so there is a real need for them to engage in financial planning and invest for the future. They are vulnerable to offshore IFAs, many of whom do not behave ethically.

There is a real need for the New Model Adviser® to engage with the expat community. Such clients would benefit from the higher professional standards, transparency and lack of commission bias that is provided by a fee-only approach.

Technology now makes it possible for UK financial planners to service expat clients wherever they may be. Email and web conferencing have dissolved the barriers to service that existed before.

The emergence of wrap platforms will be the final nail in the coffin of the offshore products pedalled by offshore IFAs. Wraps offer a simple, transparent, flexible and comprehensive wealth management service for expat investors.

Offshore salesmen move aside – the new model expat adviser has arrived!

Carl Melvin (CFP) is managing director of Affluent

TPR has been neither coy nor shy in its published determination against Ward and Salih – and has openly called the London Quantum pension scheme, and the risky investments which Ward made, a “scam”.

But to any reasonable person’s mind, tPR’s determination in relation to Ward and London Quantum raises more questions than it answers. In fact, I would go even further and say that HMRC’s and tPR’s incompetence – as well as Dalriada Trustees‘ own failings – should be examined in parallel with Ward’s multiple frauds.

Because, make no mistake, London Quantum was only one of many.

It all started long before the Ark Pensions scam. Ward set out his stall transferring pensions to New Zealand and liberating 100% “tax free”. He boasted in the local Costa Blanca press that he had “helped” thousands of clients liberate their pensions (legally). Of course, this may have been free of tax in New Zealand, but when the Spanish tax authorities catch up with these clients, there will be a very expensive disaster.

It is extremely worrying that IVCM – a “phoenix” of the Brooklands disaster – is also offering the same New Zealand liberation facility today. It always worries me when firms fail to learn the lessons of past scams and expose unsuspecting victims to the same catastrophes that past scammers orchestrated. Add to this the fact that IVCM is regulated out of Gibraltar – the jurisdiction of choice for scammers such as XXXX XXXX and STM Fidecs – and I think it is well worth giving IVCM a very wide berth.

Prior to 2010, Ward was a tied agent of Inter Alliance – a company based in Cyprus which had an insurance license. For Inter Alliance in Cyprus, Ward successfully created the illusion that this gave his company Premier Pension Solutions some sort of license. But, in reality, it did not – as the Cyprus license was only for Inter Alliance and not for any other entity. Plus tied agents were (and still are) illegal in Spain.

As a sideline, Ward was flogging EEA Life Settlements as he had discovered the delights of making huge commissions out of dodgy, risky, illiquid investments to his unsuspecting victims. In 2010, Ward was working closely with Concept Trustees in Guernsey – run by Roger Berry. Initially happy to see Concept Trustees’ QROPS members have 100% of their pensions invested by Ward in EEA, Berry eventually realised that Ward’s firm was not regulated as it had been dumped by Inter Alliance. Of course, even before it had been dumped, Premier Pension Solutions wasn’t regulated anyway. But Concept Trustees was too stupid to realise that.

Concept then wrote to all the members who were clients of Ward’s Premier Pension Solutions and warned them that Ward’s firm was neither regulated nor had any professional indemnity insurance cover. Berry claimed he would not be accepting any further investment instructions from Ward, but this was basically just a load of hot air (aka lying) as he continued to accept investment instructions into EEA by Ward.

In September 2010, Premier Pension Solutions was appointed as a tied agent of AES International – a firm based in London and Dubai. The agency agreement covered PPS for investment and insurance business – but not pension transfer business. Ward’s PPS letterheaded paper claimed that it was a “partner” of AES and that it was regulated by the DGS (Spanish insurance regulator) and CNMV (Spanish investment regulator). PPS also became a member of FEIFA – the Federation of European Independent Financial Advisers (although he was later dumped by them). You can understand why so many victims thought that PPS was a bona fide advisory firm.

Then came the first of Ward’s major pension scams: Ark. It is worth looking at the history of Ark because this sets the scene for how nearly 500 victims came to lose their pensions and face tax liabilities – as well as the dozens of further scams operated by Ward (including London Quantum).

A famous footballer and his mate – a football club owner – bought a plot of land in Larnaca in Cyprus with a view to turning it into a golf resort. They paid £1.1 million for the property, but then realised it wasn’t big enough for a whole golf course (neither of them was bright enough to be able to count up to 18) and so they tried to find some other investors. The chumps they tried to con into buying more land adjacent to the original plot either couldn’t come up with the money or were frightened off such a high-risk, illiquid investment.

So the sporty pair went to see the footballer’s accountant – Andrew Isles of Isles and Storer (now owned by LB Group). Isles soothed the sporty pair’s worries by telling them that securing more investors was simple: just start a pension fund! He introduced them to what he called “two leading pension experts”: Craig Tweedley and Stephen Ward. Tweedley was already operating the KJK Investments/G Loans pension liberation scam (later to be placed in the hands of Dalriada Trustees by the Pensions Regulator) and Ward was a highly-qualified pensions expert, examiner and author.

The rest is history as nearly 500 victims lost their pensions to the Ark scam. But the sporty pair did very nicely – they sold the land in Cyprus to the Ark scheme for £4 million and pocketed the profit. The footballer tried to hide the money in Dubai but got caught and turned Queens Evidence. He and the other original investor (the football club owner) fell out and they ended up in court against each other – with the footballer triumphing. Andrew Isles also did very nicely as he sold introductions to a number of his clients and earned fat commissions in doing so.

As Ark unfolded – between mid 2010 and mid 2011 – Ward initially acted as an introducer. There were various introducers – many recruited by Ward when he ran a series of seminars in various parts of the UK. But Ward himself was the biggest introducer – accounting for more than a third of the whole £27 million fund and earning approaching three quarters of a million pounds in fees (the Pensions Regulator’s report of £350k was way off the mark).

Ward and his sidekick – bent lawyer Alan Fowler of Stevens and Bolton Solicitors – acted as the controlling minds behind Ark. The scheme documentation and the “loan” contracts were drawn up and explained by Ward and Fowler. Of the 5% commission charged by Craig Tweedley, Ward got at least 2% plus a transfer fee. But Ward had his eye on a much bigger proportion of the fees. Towards the end of the life of Ark, Ward was preparing to take Ark over from Tweedley – along with an associate of his: Peter Moat (another pension crook who went on to operate the Fast Pensions scam – now also in the hands of Dalriada Trustees). In a way, it was a shame that didn’t happen, as Tweedley did at least try to help the Ark victims, whereas Ward never lifted a finger. In fact, he simply told the Ark victims to throw the tax demands away as “HMRC would never pursue them”.

In February 2011, HMRC met with Tweedley and Ward to discuss the “loans” – so HMRC knew perfectly well that Ward was the main brain behind the scam. It is, therefore, astonishing that they did nothing to stop him operating so many further pension scams.

Ark came to a shuddering halt on 31st May 2011, when tPR appointed Dalriada Trustees and the scheme was suspended. Dalriada went up to Yorkshire to confront Crag Tweedley and relieve him of all the evidence and files relating to the scam. Tweedley told Dalriada that all the records were held down at Ward’s Manchester office at 31, Memorial Road and he drove down to collect them from Anthony Salih. He arrived to find Salih removing all the Premier Pension Solutions fee agreements on the instructions of Ward (he managed to shred most of them – but did missed a few which I now have).

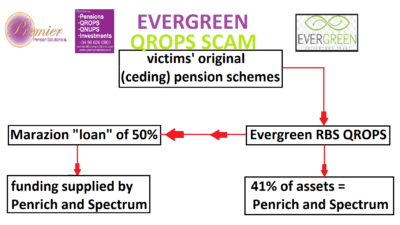

After Ark, Ward went on to run the Evergreen Retirement Benefits QROPS scam with accompanying 50% “loans” and a further 300 victims lost £10 million worth of pensions. HMRC removed Evergreen from the QROPS list when they realised it was a liberation scam and Ward fell back on two more UK-based, bogus occupational schemes: Southlands and Headforte. Plus, he registered a number of new schemes – including Capita Oak.

The Capita Oak scheme was another bogus occupational scheme registered by Ward with a fictitious sponsoring employer: RP Medplant (Cyprus). There is, however, a firm called RP Med Plant in Cyprus. The Capita Oak trust deed was written by Ward’s bent lawyer Alan Fowler. Ward took responsibility for the transfer administration – transferring valuable personal and final salary occupational pensions into this scam – in the full knowledge that he was condemning hundreds of victims to certain financial ruin and poverty in retirement. Capita Oak is now also in the hands of Dalriada Trustees.

Other pension scams that Ward was operating – in addition to Southlands and Headforte – from 2012 onwards included Feldspar, Hammerley, Meribel, Halkin, Randwick, Bollington Wood and Westminster. And, of course, Dorrixo Alliance which was the trustee for many of these scams. Capita Oak and Westminster are both under investigation by the Serious Fraud Office.

How much more evidence do they need?

In May 2014, HMRC was given evidence of all of Ward’s various scams – including Dorrixo Alliance. They were also given detailed testimony by me and a number of victims of what Ward had been up to in the pension liberation fraud industry since Ark. It would have been very easy for HMRC to look up to see what other pension schemes Dorrixo was trustee to. Had they done this, they would have seen that Dorrixo was the trustee for the London Quantum scheme. If HMRC had taken any action, they could have prevented Mr. N – a serving police officer – and 96 other victims from losing their pensions to Ward and his various dodgy, inappropriate investments (including loans to Dolphin Trust).

If we add to the above catalogue of scams the Continental Wealth Management scam – 1,000 victims facing the loss of £100 million worth of life savings – Ward has been responsible for the destruction of thousands of people’s pensions this past eight years. Plus several suicides and deaths from stress-related medical conditions.

SERIOUS QUESTIONS ARISING FROM THE PENSIONS REGULATOR’S DETERMINATION RE:

Mr Stephen Alexander Ward – The Pensions Regulator case ref: C46205159

Ward was a director of Dorrixo from 13 October 2011 to 28 April 2015. A company called Quantum Investment Management Solutions LLP (“QIMS”) has at all material times been the sole sponsoring employer of the Scheme. Dorrixo became the sole trustee of the Scheme on 19 April 2014. Dorrixo is also recorded as being the Scheme administrator.

HMRC AND TPR WERE GIVEN EVIDENCE OF WARD’S COMPANY, DORRIXO, IN MAY 2014. THEY WERE ALSO GIVEN EVIDENCE OF A LARGE NUMBER OF SCAMS WARD OPERATED AFTER ARK – ALL INVOLVING LIBERATION FRAUD. WHY WASN’T ACTION TAKEN TO PREVENT LONDON QUANTUM? ALL 97 VICTIMS – INCLUDING A SERVING POLICE OFFICER – COULD HAVE BEEN PREVENTED.

On 18 June 2015 the Regulator appointed Dalriada Trustees Limited (“Dalriada”) as an independent trustee to the Scheme, with exclusive powers.

HAS ONE SINGLE PENNY EVER BEEN RETURNED TO ANY OF THE PENSION SCAMS PLACED IN THE HANDS OF DALRIADA TRUSTEES? THERE ARE DOZENS OF THEM, AND FEW – IF ANY – OTHER INDEPENDENT TRUSTEES ARE EVER APPOINTED BY TPR. BUT THERE SEEMS TO BE NO RECORD OF ONE SINGLE MEMBER EVER GETTING ANY RETURN FROM ANY OF THE SCHEMES IN THE PAST EIGHT YEARS – DESPITE THE MANY MILLIONS DALRIADA HAVE PAID THEMSELVES FROM THESE SCHEMES.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

AS THIS EVIDENCES THAT THIS SCAM COULD EASILY HAVE DWARFED ARK IN A VERY SHORT SPACE OF TIME, DON’T HMRC AND TPR RECOGNISE THAT THEIR LAZINESS AND NEGLIGENCE NEED TO BE ADDRESSED? THEY LEARNED NOTHING FROM ARK – AND WHILE THERE ARE VALID CRITICISMS OF WARD FOR HAVING LEARNED NOTHING, HE IS JUST A COMMON SPIV WHILE HMRC AND TPR ARE SUPPOSED TO BE GOVERNMENT DEPARTMENTS WITH A RESPONSIBILITY TO PROTECT THE PUBLIC. THE SCALE OF THIS SCAM SHOWS THESE TWO ORGANISATIONS ARE NOTHING BUT HOPELESSLY INEPT AND AMATEURISH IN THEIR APPROACH TO DILIGENCE AND PUBLIC RESPONSIBILITY.

The Scheme was promoted to potential new members by introducers. These included the following entities: GoBMV; Baird Dunbar; What Partnership; the Resort Group PLC; Friendly Investments; Premier Mark Consultants and Quantum Wealth Management Solutions Limited.

THE DANGERS OF THE SCOURGE OF “INTRODUCERS” SHOULD HAVE BEEN LEARNED FROM THE ARK SCAM IN 2011. WARD RECRUITED DOZENS OF THEM ALL OVER THE COUNTRY. AND YET NONE OF THEM HAS EVER BEEN BROUGHT TO JUSTICE FOR THEIR PART IN ARK, AND HAVE GONE ON TO OPERATE AS INTRODUCERS AND EVEN HOLD KEY CENTRAL ROLES IN LATER SCAMS. THIS INCLUDES FRIENDLY INVESTMENTS AND JULIAN HANSON – WHOSE SCHEMES ARE NOW ALSO IN THE HANDS OF DALRIADA TRUSTEES.

Gerard was responsible for producing template risk letters, member application forms, pro forma declarations stating that the person signing them was a self-certified sophisticated investor, member booklets and the statement of investment principles (of which there were four versions). Gerard sent these documents to members once they had been introduced to the Scheme by an introducer.

GERARD ASSOCIATES, RUN BY GARY BARLOW, HAD ACTED AS AN INTRODUCER TO WARD IN THE ARK SCAM. AND YET HE WAS LEFT FREE TO OPERATE IN THE SAME CAPACITY IN THE LONDON QUANTUM SCAM – AND EVEN TAKE ON A MORE CENTRAL ROLE. GERARD ASSOCIATES WAS AT THE TIME AN FCA-REGULATED FIRM – AND REMAINS SO TO THIS DAY. THE FCA HAS TAKEN NO ACTION TO REMOVE THIS FIRM OR TAKE ANY ACTION AGAINST GARY BARLOW.

GERARD ASSOCIATES’ GARY BARLOW WAS PAID £253,000 FROM THE LONDON QUANTUM SCHEME FOR DEFRAUDING VICTIMS INTO SIGNING AGREEMENTS THAT THEY WERE “SOPHISTICATED” INVESTORS. SO WHY HASN’T BARLOW BEEN PROSECUTED AND JAILED – AND MADE TO PAY THIS MONEY BACK TO THE VICTIMS?

A material number of the new members had a low or medium appetite for investment risk and, in any event, were unaware that the Scheme’s investments were high-risk investments. The Panel was troubled by the apparent disconnect between members’ appetite for risk and the high risk nature of the investments made by Dorrixo. Mr Ward accepted that the Scheme’s investments were high risk, but claimed this was made clear to new members in the Member Booklet.

I DON’T KNOW WHAT SORT OF DRUNKEN DUMMIES MADE UP TPR’S “PANEL”, BUT DID THEY SERIOUSLY THINK THAT ANY PENSION FUNDS SHOULD EVER INVEST IN HIGH-RISK CRAP? INDIVIDUAL MEMBERS’ APPETITE FOR INVESTMENT RISK IS IRRELEVANT – THIS WAS A PENSION FUND, NOT A CASINO.

The case against Ward was based on failures of competence and capability, and also a lack of honesty and integrity as well as Ward’s involvement with “pension liberation” as an introducer of members to the “Ark” schemes.

BUT TPR AND HMRC KNEW ALL ABOUT THIS BACK IN 2010 AND 2011. WHY DID THEY DO NOTHING TO PREVENT WARD FROM SCAMMING MORE VICTIMS OUT OF MORE MILLIONS OF POUNDS. THEY STOOD BACK AND WATCHED – DESPITE HAVING HARD EVIDENCE THAT HE WAS STILL UP TO HIS CRIMINAL MISCHIEF.

Mr Ward did not dispute that a company of his (Premier Pensions Solutions SL) was involved in introducing members to the Ark Schemes, but states that the relevant activity pre-dated any finding by the courts of pensions liberation and that Mr Ward had no knowledge that the schemes were being used for such activity.

BUT HMRC, TPR AND DALRIADA ALL KNOW THIS ISN’T TRUE. THEY HAVE ALL SEEN EVIDENCE THAT WARD AND HIS BENT LAWYER ALAN FOWLER ACTUALLY PRODUCED THE “LOAN” (MPVA) DOCUMENTATION AND EXPLAINED THE LOANS IN SOME CONSIDERABLE DETAIL TO THE VICTIMS. THE MPVA CONTRACTS WERE DRAWN UP BY FOWLER. IS IT REALLY CREDIBLE THAT NEITHER HMRC NOR TPR WOULD HAVE OBJECTED TO THIS STATEMENT?

The Panel did not consider there was sufficient evidence of Ward having actual knowledge of, or turning a blind eye to, the illegal nature of the activity of the Ark Schemes when carrying out his role as introducer before.

SERIOUSLY? I HAVE GIVEN EVIDENCE OF THIS TO BOTH HMRC AND TPR ON MANY OCCASIONS. THIS HAS BEEN DISCUSSED AT MEETINGS WITH DALRIADA TRUSTEES ON MANY OCCASIONS. EVIDENCE OF THIS HAS BEEN GIVEN TO THE SERIOUS FRAUD OFFICE ON MANY OCCASIONS BY VARIOUS VICTIMS AND ME. WHAT FURTHER EVIDENCE DID THE PANEL WANT? EVERY ARK MEMBER’S FILE WAS FULL OF SUCH EVIDENCE. EITHER TPR IS LYING OR IT IS INCOMPETENT. OR BOTH.

The Case Team also relied on certain alleged failures in relation to other pension schemes (called Headforte and Halkin), of which Mr Ward was a trustee. These are denied by him (e.g. an allegation of failure to appoint an auditor to those schemes) and the Panel did not consider it necessary to make findings in respect of them.

SO WHAT ACTION HAS TPR TAKEN IN RELATION TO HEADFORTE AND HALKIN? BOTH WERE BEING USED FOR PENSION LIBERATION FRAUD BY WARD – AND YET THE VICTIMS PROBABLY STILL HAVE NO IDEA WHAT HAS HAPPENED TO THEIR MONEY. IT IS ABSOLUTELY ASTONISHING THAT NO ACTION HAS BEEN TAKEN IN RELATION TO THESE TWO SCHEMES, PLUS ALL THE OTHERS WARD HAS BEEN OPERATING OVER THE YEARS.

Stephen Alexander Ward (date of birth 11 July 1955) is hereby prohibited from being a trustee of trust schemes in general. This order has the effect of removing the above-named individual from all or any schemes of which he is a trustee. By section 6 of the Pensions Act 1995, any person who purports to act as a trustee of a trust scheme whilst prohibited under section 3 is guilty of an offence and liable (a) on summary conviction to a fine not exceeding the statutory maximum, and (b) on conviction on indictment to a fine or imprisonment or both.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

THIS IS NOT JUST THE DEATH OF TRUST, BUT OF ANY CONFIDENCE IN THE GOVERNMENT, REGULATORS AND CRIME PREVENTION AGENCIES TO PREVENT OR DEAL WITH PENSION SCAMS AND SCAMMERS.

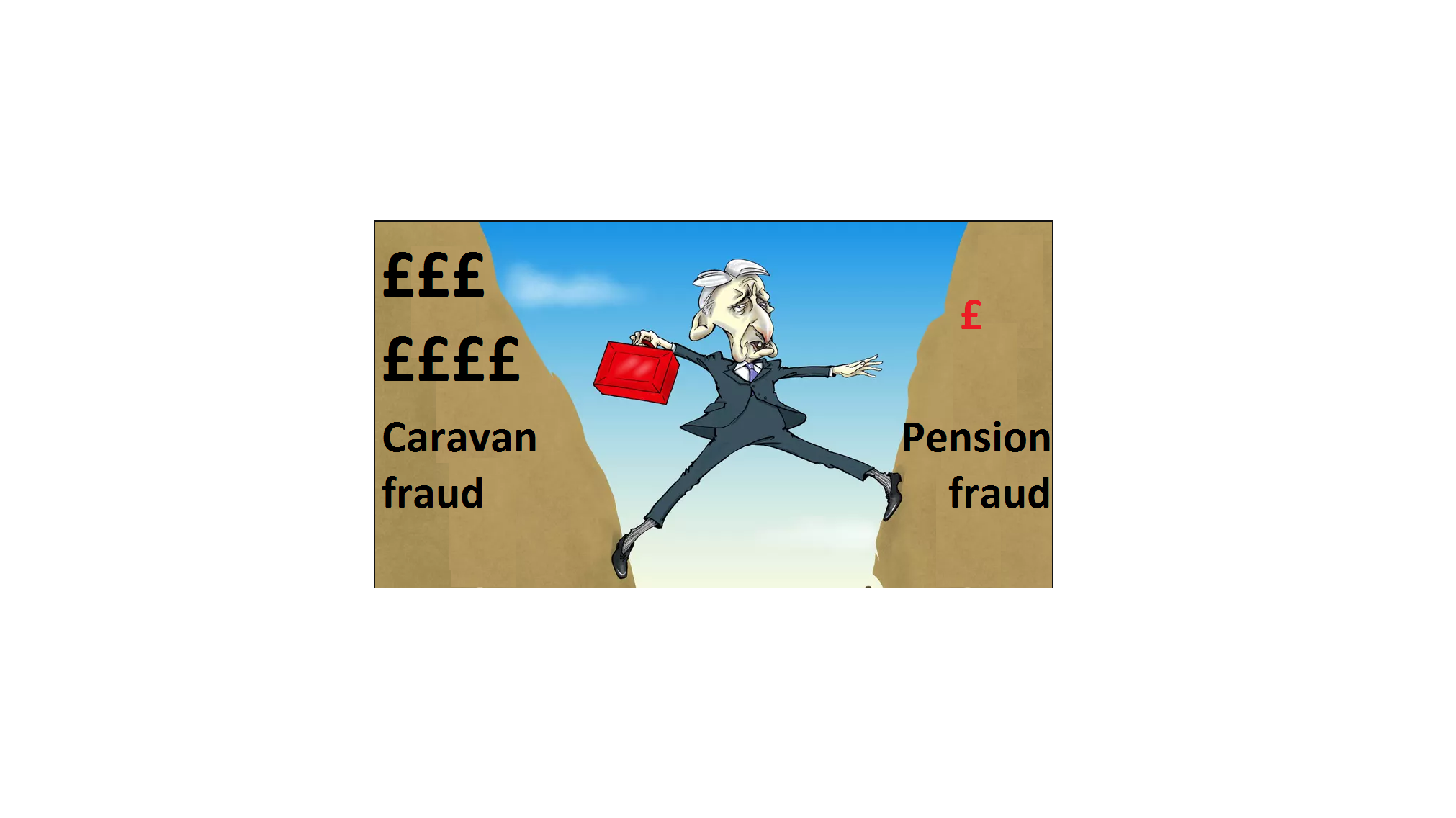

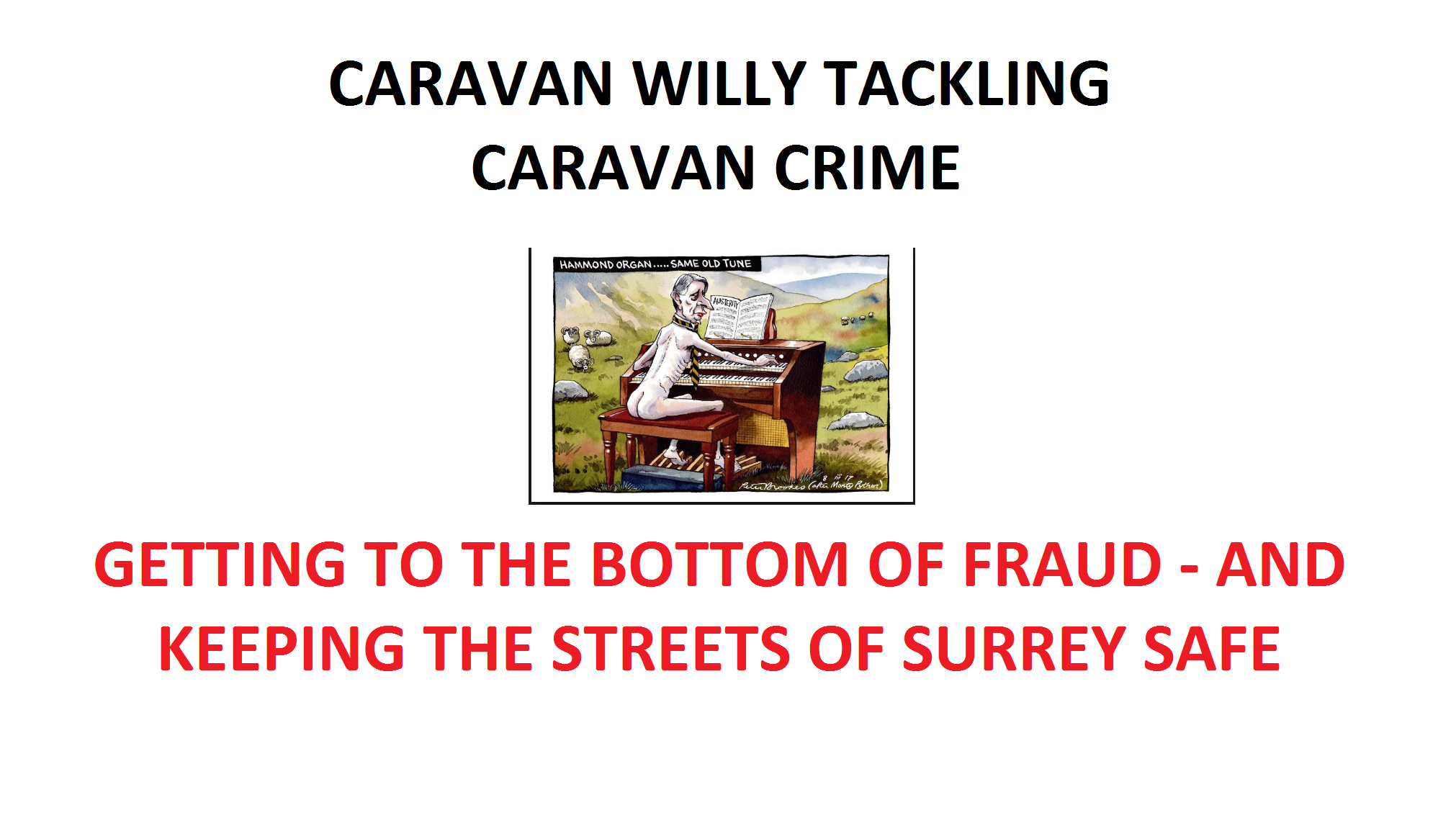

Tackling Caravan Crime – Chancellor Philip Hammond. Victims of pension fraud in scams such as Ark, Capita Oak, Westminster, London Quantum, Friendly Pensions and Salmon Enterprises – will not be surprised to hear that even the Crown Prosecution Service acknowledges that the fraudsters have defeated the system. Alison Saunders, head of the CPS, has stated publicly that the British justice system can’t cope. She is stepping down and is clearly disheartened by Britain’s failure to tackle crime – especially fraud. She has vented her frustration in an interview:

But look hard enough, and you will see how tackling crime can be done successfully. As someone who constantly writes about the failure of our police and courts to bring criminals to justice, I was surprised to hear of a spectacular success story in leafy Surrey recently.

Mr. and Mrs. Shore of Thorpe, in Surrey, were successfully prosecuted and jailed for proceeds of crime. Residing in Runnymede Borough Council – presided over by Chancellor Phillip Hammond – this dastardly pair (in their sixties) were both sent down for a heinous crime under the Proceeds of Crime Act 2002 (“POCA”).

After many years of detailed investigation, the successful prosecution will send out a resounding warning to all such criminals and will no doubt discourage others from profiting from the same hideous crimes. And the crime was…….?

Housing homeless families in caravans without planning consent.

Let that sink in for a moment – vulnerable people with young children who had a choice between living on the streets or living in a caravan. And this crime was committed in Runnymede Borough where there was insufficient housing for the many poor families who could not afford private accommodation and had not been offered council homes.

This spectacular success story on the part of Hammond, Runnymede Borough Council and the CPS has left the good citizens of Surrey relieved that these dangerous caravan owners are now behind bars and dozens of homeless families are now living on the streets. Jobdone; justice served; well done Cutty Sark!

Hailing from Surrey myself, I am pleased that the county will now be a safer place. The successful prosecution was in respect of 14 breaches of six enforcement notices issued since 1999 by Runnymede Borough Council, following a seven-day trial at Guildford Crown Court. The jury heard how the farm owners had not only stationed the caravans on their own land, but had also failed to demolish a shower room. Unbelievable!

Hammond must be strutting the halls of Westminster bursting with pride and patrolling the fields of Runnymede with a sense of upholding the social and civil justice with which King John would have been delighted. In the House of Commons bar, Chancellor Hammond is probably boasting that there is a reason why he is named after a large organ. In fact, after his spectacular success with the Shores’ caravans, he will probably go down in history as “Caravan Willy” for presiding over such a coup.

I am sure that the many thousands of people who have lost millions of pounds’ worth of life savings to scammers such as Stephen Ward, Julian Hanson, George Frost, XXXX XXXX, Phillip Nunn, Patrick McCreesh, Stuart Chapman-Clarke, David Vilka, David Austin, Darren Kirby, Dean Stogsdill, Anthony Downs and James Lau will now understand why the CPS couldn’t dedicate any resources to prosecuting them. And they will, no doubt, be glad that the priority of the judiciary was removing unauthorised caravans in Surrey.

As in most of my blogs, there is an important postscript: Caravan Willy is a keen property owner and is reported to be worth over £9 million. The Shores’ land has now been confiscated by Runnymede Borough Council. And it is worth at least £27 million once planning permission for a housing estate is granted. I wonder who will be lucky enough to scoop that one up?………

When I grow up, I want to be able to write blogs as eloquently as the Mighty Henry Tapper – the Pension Ploughman with a huge plough which furrows deeply through much of the bullshit on Twitter. He also tolerates Ros Altmann with grace and generosity – which is something I could never do no matter how grown up I get.

Henry´s recent blog is particularly pertinent as it draws attention to the small and irritating gaggle of willy wagglers who understand little but talk a lot about how knowledgeable they are. In fact, many of these know-alls grasp very little outside their own comfort zone – and some of them, like John Ralfe, have neither class nor manners. John and his fellow gaggle of wagglers are quick to belittle and insult, but slow to make the effort to understand complex matters in sufficient depth to be able to develop a balanced and intelligent view of the diverse details of human economics.

But first, let me talk a little about Henry. He is one of the small, elite group of professionals who have bothered to get their feet wet and their hands dirty and venture into my world: the arena of pension and investment scams and scammers. It takes a strong stomach to square up to the vile operators and facilitators of financial crime, and a lot of backbone to call out regulators and other authorities for their dismal failings.

Señor Tapper, over the past five years, has generously given his time, effort and expertise to the plight of the scam victims. Victims who have also been very active in campaigning and representing other victims – including airline pilots, bus and taxi drivers, nurses and doctors, architects, research chemists, a carp breeder, a driving instructor and people dying of life-threatening illnesses.

Then you’ve got the so-called professionals in the UK who think – and say – that none of what goes on in the scamming industry, or offshore, is anything to do with them. Some of these self-proclaimed experts also dismiss the victims as “stupid” or “complicit”. To say I have no time for these people would be a bit of an understatement. But to see some of these idiotic “experts” also being insulting to the very people I value so highly is a bit much for me – and the victims – to swallow.

Henry complains about the pesky “experts” on the following grounds:

They make you read their books

They willy waggle

They waggle each other’s willies

They get frustrated when you don’t agree with them

They are generally from the USA and Europe

I don’t really have a problem with number 1, because I also try to get people to read my book: Anatomy of a Pension Scam

I did try to make it free, but the cheapest selling price Amazon will let you use is $1.34.

I don’t do 2 or 3 (either actually or metaphorically) but I do 4 a lot. But that is because intelligent, knowledgeable people tend to understand the importance of tackling financial crime, while arrogant, ill-informed people don’t. Not that I am talking about agreeing with anything complex or requiring much knowledge – I am referring to the basic principals that scamming is wrong; being unqualified is wrong; being unregulated is wrong; being greedy is wrong.

I am not too sure about 5 because I know very few people from the USA. However, the people I tend to meet in Europe are mostly either victims or perpetrators – and they are both genuine experts in their field of expertise in equal measures (i.e. at being scammed or doing the scamming). I have met one or two good guys on the Continent, but they are pretty rare.

I’ve had a quick look at the willy waggling Tweets by John Ralfe (clearly a legend in his own mind) to which Henry is referring. Ralfe appears to be recommending that Henry should take up reading the work of Nobel Laureates. I have no doubt that should Henry ever feel the need for advice about what books he should read, he will know exactly where to go. And, of course, Henry is far too much of a gentleman to tell this ignorant twerp where to go. I, on the other hand, do not aspire to Henry’s high standards.

So, Mr Ralfe, take your willy and waggle it somewhere else.

I’D RATHER HAVE A CUP OF TEA THAN SEX – Boy George

BG had a point. A cuppa can be enjoyed without taking your clothes off or getting your hair messed up. Plus you can easily do it with people you haven’t quite made up your mind about.

This is my dilemma. I am enormously popular with solicitors and I have two potential new best friends: Carter Ruck and DWF Solicitors. They both want to be my friends but I have to chose both of them, half of them or neither of them.

So I’ve decided to invite them both to my kitchen for a cup of tea and a few fruity tarts. Firstly, I will make it clear that it is my kitchen – my rules. And I shall expect good manners and elegant waggling of their pinkies.

Secondly, I will impress upon both of them that while I can friend them, I can just as easily unfriend them. The rules of my kitchen include: no smoking; no belching and no farting.

I have had many friends among the legal community over the past few years. You can see why they enjoy writing to me – scammers pay them huge amounts to engage with me. (Rather than the fact that they enjoy being my pal).

Assisting me in my quest to decide whether to accept either of these guys as my “new bestie” will be my Toy Poodle Tigga, who will hump the leg of the one he likes best. It is not so much what Tigga does, but how the lawyers react – and whether they deal with such a situation with elegance and class.

It must be declared that, actually, DWF does start out with a huge disadvantage. In 2015 they were acting for the Insolvency Service in the winding up of Imperial Trustees in the matter of the Capita Oak scam. But they were also acting for Stephen Ward of Premier Pension Solutions – the transfer administrator for the Capita Oak scam. I did point out that this was a bit of a conflict of interests (to various parties). Shortly after, DWF was dropped as legal representative to the Insolvency Service.

Another thing against DWF is that a couple of years back, a group of 20 lawyers left the firm for Trowers and Hamlins. Not exactly a confidence-inspiring event in the reputation of the (DWF) firm.

As we are an all-girls’ team at Pension Life (except for Tigga) we only have one loo. And that has framed letters from a number of my other favourite lawyer chums on the walls. It remains to be seen which of these two new candidates will end up on the toilet wall and which will be told to “Ruck” off.

The problem with money is that it blows away if you don’t hold it down, tie it up or stuff it down your knickers. That’s why you need to put it somewhere safe: in a shoe box on top of the wardrobe; under your mattress; in the safe or – if you’re feeling really brave – in the bank. Trouble is, left in cash, money shrinks (inflation, charges, moths). This is why so many advisers recommend a platform – aka “somewhere safe” to keep your money.

The problem with money is that it blows away if you don’t hold it down, tie it up or stuff it down your knickers. That’s why you need to put it somewhere safe: in a shoe box on top of the wardrobe; under your mattress; in the safe or – if you’re feeling really brave – in the bank. Trouble is, left in cash, money shrinks (inflation, charges, moths). This is why so many advisers recommend a platform – aka “somewhere safe” to keep your money.

A bit like the lyrics to Hotel California, with an OMI “bond”, you can’t check out any time you want, and you can only leave after between five and ten years. OMI will take that number of years to claw back the commission paid to your adviser – even if you have long since learned that your adviser was an unregulated scammer and has conned you into unsuitable, high-risk, high-commission investments that have badly damaged your fund. You are stuck with paying the quarterly fees to OMI – even after your whole fund has gone. One victim went from plus

A bit like the lyrics to Hotel California, with an OMI “bond”, you can’t check out any time you want, and you can only leave after between five and ten years. OMI will take that number of years to claw back the commission paid to your adviser – even if you have long since learned that your adviser was an unregulated scammer and has conned you into unsuitable, high-risk, high-commission investments that have badly damaged your fund. You are stuck with paying the quarterly fees to OMI – even after your whole fund has gone. One victim went from plus  In Spain, the Supreme Court has ruled that bogus life assurance policies – such as those provided by

In Spain, the Supreme Court has ruled that bogus life assurance policies – such as those provided by

The arrival of wraps allows fee-based financial planners in the UK to offer a sound, client-focused service to expats, who up until recently have been easy prey to

The arrival of wraps allows fee-based financial planners in the UK to offer a sound, client-focused service to expats, who up until recently have been easy prey to

Then came the first of Ward’s

Then came the first of Ward’s  After Ark, Ward went on to run the

After Ark, Ward went on to run the

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member. SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

But look hard enough, and you will see how tackling crime can be done successfully. As someone who constantly writes about the failure of our police and courts to bring criminals to justice, I was surprised to hear of a spectacular success story in leafy Surrey recently.

But look hard enough, and you will see how tackling crime can be done successfully. As someone who constantly writes about the failure of our police and courts to bring criminals to justice, I was surprised to hear of a spectacular success story in leafy Surrey recently. Mr. and Mrs. Shore of Thorpe, in Surrey, were successfully prosecuted and jailed for proceeds of crime. Residing in Runnymede Borough Council – presided over by Chancellor Phillip Hammond – this dastardly pair (in their sixties) were both sent down for a heinous crime under the Proceeds of Crime Act 2002 (“POCA”).

Mr. and Mrs. Shore of Thorpe, in Surrey, were successfully prosecuted and jailed for proceeds of crime. Residing in Runnymede Borough Council – presided over by Chancellor Phillip Hammond – this dastardly pair (in their sixties) were both sent down for a heinous crime under the Proceeds of Crime Act 2002 (“POCA”). This spectacular success story on the part of Hammond, Runnymede Borough Council and the CPS has left the good citizens of Surrey relieved that these dangerous caravan owners are now behind bars and dozens of homeless families are now living on the streets.

This spectacular success story on the part of Hammond, Runnymede Borough Council and the CPS has left the good citizens of Surrey relieved that these dangerous caravan owners are now behind bars and dozens of homeless families are now living on the streets.  I am sure that the many thousands of people who have lost millions of pounds’ worth of life savings to scammers such as Stephen Ward, Julian Hanson, George Frost, XXXX XXXX, Phillip Nunn, Patrick McCreesh, Stuart Chapman-Clarke, David Vilka, David Austin, Darren Kirby, Dean Stogsdill, Anthony Downs and James Lau will now understand why the CPS couldn’t dedicate any resources to prosecuting them. And they will, no doubt, be glad that the priority of the judiciary was removing unauthorised caravans in Surrey.

I am sure that the many thousands of people who have lost millions of pounds’ worth of life savings to scammers such as Stephen Ward, Julian Hanson, George Frost, XXXX XXXX, Phillip Nunn, Patrick McCreesh, Stuart Chapman-Clarke, David Vilka, David Austin, Darren Kirby, Dean Stogsdill, Anthony Downs and James Lau will now understand why the CPS couldn’t dedicate any resources to prosecuting them. And they will, no doubt, be glad that the priority of the judiciary was removing unauthorised caravans in Surrey.

When I grow up, I want to be able to write blogs as eloquently as the Mighty Henry Tapper – the Pension Ploughman with a huge plough which furrows deeply through much of the bullshit on Twitter. He also tolerates Ros Altmann with grace and generosity – which is something I could never do no matter how grown up I get.

When I grow up, I want to be able to write blogs as eloquently as the Mighty Henry Tapper – the Pension Ploughman with a huge plough which furrows deeply through much of the bullshit on Twitter. He also tolerates Ros Altmann with grace and generosity – which is something I could never do no matter how grown up I get.

I’D RATHER HAVE A CUP OF TEA THAN SEX – Boy George

I’D RATHER HAVE A CUP OF TEA THAN SEX – Boy George your mind about.

your mind about.