ALL PENSION SCAMS START WITH A TRANSFER BY A CEDING PENSION PROVIDER.

It is interesting that PSIG chose three particular providers to give their answers to the questionnaire sent out: XPS Pensions Group, Phoenix Life Assurance Company and Standard Life Assurance Company. I have no doubt they chose these three providers because of their extensive first-hand expertise at facilitating financial crime. In the Capita Oak and Westminster scams – distributed and administered by serial scammers XXXX and Stephen Ward – and now under investigation by the Serious Fraud Office – Phoenix Life and Standard Life handed over dozens of pensions to the scammers. In Phoenix Life’s case, the total came to nearly half a million pounds’ worth, and in Standard Life’s case it was well over one million.

While there is, of course, substantial hard evidence that both the Pensions Regulator (formerly OPRA) and HMRC had been giving the industry plenty of warnings about scams long before the Scorpion Campaign was published on Valentine’s Day in 2013, it is also true that providers such as Phoenix Life, Standard Life – and other favourite financial crime facilitators such as Aegon, Friends Life, Legal & General, Prudential, Royal London, Scottish Life and Scottish Widows – carried on handing over millions to the scammers well into 2014, 2015 and beyond. And, in fact, they are still at it today.

The “Key Findings” do throw up some interesting facts:

“Information on scams is not readily available at an organisational level”.

Seriously? Don’t these organisations know how to do research? Do they really not know what to look for? They’ve had enough experience over the years – and have had enough examples of spending vast amounts of time trying to cook up reasons to deny complaints against their incompetence for handing over pensions to scammers – to write a whole encyclopedia about scams.

Organisations (such as Phoenix Life and Standard Life) could try talking to TPAS, or tPR, or the FCA, or the SFO, or Dalriada Trustees, or regulators in Malta, the IoM, Gibraltar, Dubai or Hong Kong. Or some of the thousands of victims – who have lost their pensions due to the incompetence and callousness of the ceding providers – who would readily fill in the blanks. There really is no shortage of readily-available, free information. They just need to take the time and trouble to ask for it. It really isn’t difficult. They just have to put their box-ticking pencils down for a few minutes.

“The Scams Code is seen as a good basis for due diligence”

I agree – it is really great. But it is also 78 pages long. Few people have to the time to read, understand or remember such long documents (with too many long words and not enough pictures). What would be helpful would be to get a few of the worst offenders: Aegon, Aviva, Friends Life, Legal & General, Phoenix, Prudential, Royal London, Scottish Life, Scottish Widows, Standard Life and Zurich, in a room at the same time – and bang their heads together. And threaten them that if they don’t get their acts together and stop handing over pensions to the scammers, they will be made to read and memorise the 78-page Scams Code and recite it every morning before coffee break. Twice. Then snap all their box-ticking pencils in half, and JOB DONE! It really isn’t rocket science – there are usually some hints which are as subtle as a brick, such as: the sponsoring employer doesn’t exist; or the member lives in Scunthorpe and is transferring to a scheme whose sponsoring employer is based in Cyprus. Or Hong Kong. Now, I know there was a bit of a hiccup with the Royal London v Hughes case when Justice Morgan overturned the Ombudsman’s determination. But dear old Hughes had probably had a few Babychams too many – and it had slipped his mind that the law is supposed to be about justice and common sense. And that just because a particular piece of legislation has been written by an ass, it doesn’t have to be interpreted with stupidity.

“Significant time and effort goes into protecting members from scams”

This, of course, may be true. I only get to see the cases where the negligent ceding providers dohand over the pensions to the scammers. I rarely get to see the ones that have a narrow escape. But what worries me is that I am in the process of making complaints to the ceding providers who have handed over pensions to the scammers, and not a single one of them thinks they have done anything wrong. So, if they do spend “significant time and effort” doing the protecting bit, how come so many of them still fail so badly? And then try to deny they failed. These providers spend very significant amounts of time and effort writing long, boring letters about how they did nothing wrong – letters which must have taken them at least an hour to write. And yet they won’t spent two minutes checking – and stopping – transfers to obvious scams.

“The more detailed the due diligence, the more suspicious traits are identified”

I am a bit suspicious that this indicates a touch of porky pies here. I’ve never seen any evidence of ANY due diligence by the ceding providers. A bloke at Aviva once told me that they spent thousands on research and due diligence – but I see no evidence of it. The problem is, the ceding providers don’t know what they don’t know. And, to coin one of my favourite phrases: “they don’t know the questions to ask, and even if they did then they wouldn’t understand the answers”.

Interestingly, if – instead of repeatedly spending hours denying they did anything wrong when they handed over millions of pounds’ worth of pensions to the scammers – they spent some time talking to me and the victims trying to learn what went wrong and what due diligence should have gone into preventing a dodgy transfer, they might learn how to stop failing so badly.

SIPPS (including international SIPPS) are the vehicle of choice by scammers

Agreed. But the scammers still love the good old QROPS. But whether it is a SIPPS or a QROPS – both of which are just “wrappers” at the end of the day, it is about what goes inside the wrappers. Where the scammers make their money is in the kickbacks: 8% on the pointless, expensive insurance bond from OMI, SEB, Generali, RL360, Friends Provident etc., and then more fat commissions on the expensive funds or structured notes.

“Quality of adviser tops the list of practitioner concerns, with member awareness a close second”

And hereby lies one of the main problems: ceding providers don’t know who the good guys are and who the bad guys are. And that is because they don’t ask. And they don’t learn from their mistakes when they get it wrong. And they don’t care when they hand the pensions over to the bad guys and their former member is now financially ruined and contemplating suicide. Instead of trying to use their appalling mistakes to improve their performance and understand what “quality” actually means, and how to tell the difference between good and bad quality, they only care about avoiding responsibility for their own failings.

The problem about “member awareness” is that most people assume their ceding provider will do some sort of due diligence. They think that words like “Phoenix Life”, “Prudential” and “Standard Life” convey some sort of professionalism or duty of care. Most members are simply unaware of the appalling track record of these providers – and the extraordinary and exhaustive lengths to which they will go to avoid being brought to justice for their negligence and laziness.

“Sharing of intelligence would help avoid duplication of effort”

Oh, how heartily I agree! I remember a year or so ago, I shared some intelligence and a few beers with a nice chap from Scottish Widows. We met at one of Andy Agathangelou’s symposiums in London – the subject of which was pension scams. The Pensions Regulator was there, Dalriada Trustees were there, Pension Bee were there, lots of interested parties were there (including an American insurer from Singapore), and a couple of victims. I gave a joint presentation with one of the victims who described how he had been scammed and how his provider had handed over his pension so easily – well after the Scorpion watershed. The nice chap from Scottish Widows asked the victim why he hadn’t called the Police. The victim replied: “I am the Police”.

It was very telling that the room wasn’t full of delegates from Aviva, Phoenix Life, Prudential, Standard Life etc. None of them were interested.

Not a single provider has ever phoned me up to ask for advice, or to arrange to speak to some victims to learn something about how they were scammed and how and why their ceding providers had failed them so badly. There are so many victims all over the UK and the rest of the world. And what they all share is a passion to try to prevent other people from being scammed by the bad guys and failed by the bad pension providers. So this invaluable intelligence is freely available.

Until and unless the providers develop a conscience, they are going to continue to fuel the pension scam industry – and nothing will change. And the 79-page code might just as well be consigned to the bathrooms of Aegon, Aviva, Friends Life, Legal & General, Phoenix, Prudential, Royal London, Scottish Life, Scottish Widows, Standard Life and Zurich.

Every year we are seeing an increase in the number of victims falling for pension and investment scams. Despite warnings in the public domain and a huge array of information about how to avoid falling victim to a scam, it seems the scammers are so skilled at their sales techniques, that even the cleverest of people can fall for their slick pitches. Often the scammers use cold-calling techniques to initiate these pitches: using emails, texts, mail shots and the good ol’ phone.

We finally saw the introduction of the cold calling ban come into place in January 2019, with huge fines being threatened to firms using these techniques to promote pension sales. We have already written about the firms who have changed their scripts to escape the fines: Cadde Wealth Management is one of these firms. On top of this, we now find that the cold-calling ban has just encouraged the scammers to divert their efforts to British expats.

BBC4 You and Yours recently discussed how the cold-calling ban in the UK has seen a change in the scammers’ behaviour. Unfortunately, this is not a change for the better. As the ban only applies to the UK, scammers are targeting expats instead. This means UK pension holders are still the main target for pension scammers and are at greater risk than ever.

Interviewed in the programme, Jamie Jenkins says he has noticed this change. He is Head of Global Saving Policy at Standard Life. He states in the report, “In recent months we have known that the cold-calling ban is coming in and criminals know that too. So we have seen a switch from cold calls originating in the UK to UK customers, to overseas calls to expat customers living abroad.”

Ironically, Standard Life has been one of the worst performers in terms of ceding pension providers who have recklessly and negligently handed over millions of pounds’ worth of pensions to the scammers. Completely ignoring the Pensions Regulator’s warnings in 2010, they shoveled £millions across to pension scams such as Ark, Capita Oak, Westminster, Continental Wealth Management, Global Fiduciary Services and many other QROPS scams.

Here at Pension Life, we know that expats are not just a new target of cold callers – many expats have already fallen victim to horrific pension scams, like those who lost large chunks of their pension funds to CWM. Continental Wealth Management fraudsters like Darren Kirby, cold-called victims, then followed through with repeat house calls and persuaded around 1,000 UK pension holders to transfer out of safe DB pensions into QROPS and illegally-sold life insurance bonds (such as OMI, Generali, SEB, RL360). With promises of high returns, a lump sum in cash and greater freedoms, many professional and well-educated people fell for the scam.

Here is our cartoon video reconstruction of how the Continental Wealth Management scam worked:

The BBC programme also talks to a Continental Wealth Management victim, Rebecca Cooke, who lost £75,000 after transferring out of an NHS pension and other secure investments.

“We were approached in 2012/13 by a company based in Spain (Continental Wealth Management) who were offering us advice about moving our private pension from the UK into another investment scheme based in the EU. We went with them, but it became blatantly obvious that we had suffered catastrophic losses in our pension and chased them up about what was happening. They had actually invested our funds badly and put them in high-risk rather in low to medium risk funds. Consequently, we had lost that amount of money (£75,000).”

She said she feels stupid for falling for the scam, but she is not alone in believing the shiny sales pitch of these scamming criminals.

It seems the only way to escape the scammers – anywhere in the world – is not to fall for their lies. But the challenge is to know what is true and what is false. And that isn’t easy – the scammers are very clever and can adapt quickly to invalidate public warnings and even use them to their advantage. In addition to the scammers, there are now offshore claims management companies circling like vultures and conning people into believing that complaints against offshore firms can be upheld by UK-based ombudsmen – and that claims can be made against the FSCS (Financial Services Compensation Scheme) in respect of Maltese trustees.

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

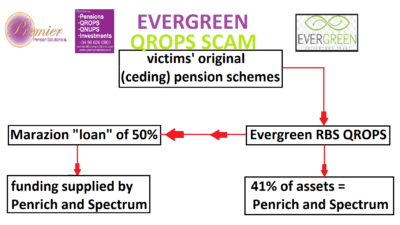

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

TPR has been neither coy nor shy in its published determination against Ward and Salih – and has openly called the London Quantum pension scheme, and the risky investments which Ward made, a “scam”.

But to any reasonable person’s mind, tPR’s determination in relation to Ward and London Quantum raises more questions than it answers. In fact, I would go even further and say that HMRC’s and tPR’s incompetence – as well as Dalriada Trustees‘ own failings – should be examined in parallel with Ward’s multiple frauds.

Because, make no mistake, London Quantum was only one of many.

It all started long before the Ark Pensions scam. Ward set out his stall transferring pensions to New Zealand and liberating 100% “tax free”. He boasted in the local Costa Blanca press that he had “helped” thousands of clients liberate their pensions (legally). Of course, this may have been free of tax in New Zealand, but when the Spanish tax authorities catch up with these clients, there will be a very expensive disaster.

It is extremely worrying that IVCM – a “phoenix” of the Brooklands disaster – is also offering the same New Zealand liberation facility today. It always worries me when firms fail to learn the lessons of past scams and expose unsuspecting victims to the same catastrophes that past scammers orchestrated. Add to this the fact that IVCM is regulated out of Gibraltar – the jurisdiction of choice for scammers such as XXXX XXXX and STM Fidecs – and I think it is well worth giving IVCM a very wide berth.

Prior to 2010, Ward was a tied agent of Inter Alliance – a company based in Cyprus which had an insurance license. For Inter Alliance in Cyprus, Ward successfully created the illusion that this gave his company Premier Pension Solutions some sort of license. But, in reality, it did not – as the Cyprus license was only for Inter Alliance and not for any other entity. Plus tied agents were (and still are) illegal in Spain.

As a sideline, Ward was flogging EEA Life Settlements as he had discovered the delights of making huge commissions out of dodgy, risky, illiquid investments to his unsuspecting victims. In 2010, Ward was working closely with Concept Trustees in Guernsey – run by Roger Berry. Initially happy to see Concept Trustees’ QROPS members have 100% of their pensions invested by Ward in EEA, Berry eventually realised that Ward’s firm was not regulated as it had been dumped by Inter Alliance. Of course, even before it had been dumped, Premier Pension Solutions wasn’t regulated anyway. But Concept Trustees was too stupid to realise that.

Concept then wrote to all the members who were clients of Ward’s Premier Pension Solutions and warned them that Ward’s firm was neither regulated nor had any professional indemnity insurance cover. Berry claimed he would not be accepting any further investment instructions from Ward, but this was basically just a load of hot air (aka lying) as he continued to accept investment instructions into EEA by Ward.

In September 2010, Premier Pension Solutions was appointed as a tied agent of AES International – a firm based in London and Dubai. The agency agreement covered PPS for investment and insurance business – but not pension transfer business. Ward’s PPS letterheaded paper claimed that it was a “partner” of AES and that it was regulated by the DGS (Spanish insurance regulator) and CNMV (Spanish investment regulator). PPS also became a member of FEIFA – the Federation of European Independent Financial Advisers (although he was later dumped by them). You can understand why so many victims thought that PPS was a bona fide advisory firm.

Then came the first of Ward’s major pension scams: Ark. It is worth looking at the history of Ark because this sets the scene for how nearly 500 victims came to lose their pensions and face tax liabilities – as well as the dozens of further scams operated by Ward (including London Quantum).

A famous footballer and his mate – a football club owner – bought a plot of land in Larnaca in Cyprus with a view to turning it into a golf resort. They paid £1.1 million for the property, but then realised it wasn’t big enough for a whole golf course (neither of them was bright enough to be able to count up to 18) and so they tried to find some other investors. The chumps they tried to con into buying more land adjacent to the original plot either couldn’t come up with the money or were frightened off such a high-risk, illiquid investment.

So the sporty pair went to see the footballer’s accountant – Andrew Isles of Isles and Storer (now owned by LB Group). Isles soothed the sporty pair’s worries by telling them that securing more investors was simple: just start a pension fund! He introduced them to what he called “two leading pension experts”: Craig Tweedley and Stephen Ward. Tweedley was already operating the KJK Investments/G Loans pension liberation scam (later to be placed in the hands of Dalriada Trustees by the Pensions Regulator) and Ward was a highly-qualified pensions expert, examiner and author.

The rest is history as nearly 500 victims lost their pensions to the Ark scam. But the sporty pair did very nicely – they sold the land in Cyprus to the Ark scheme for £4 million and pocketed the profit. The footballer tried to hide the money in Dubai but got caught and turned Queens Evidence. He and the other original investor (the football club owner) fell out and they ended up in court against each other – with the footballer triumphing. Andrew Isles also did very nicely as he sold introductions to a number of his clients and earned fat commissions in doing so.

As Ark unfolded – between mid 2010 and mid 2011 – Ward initially acted as an introducer. There were various introducers – many recruited by Ward when he ran a series of seminars in various parts of the UK. But Ward himself was the biggest introducer – accounting for more than a third of the whole £27 million fund and earning approaching three quarters of a million pounds in fees (the Pensions Regulator’s report of £350k was way off the mark).

Ward and his sidekick – bent lawyer Alan Fowler of Stevens and Bolton Solicitors – acted as the controlling minds behind Ark. The scheme documentation and the “loan” contracts were drawn up and explained by Ward and Fowler. Of the 5% commission charged by Craig Tweedley, Ward got at least 2% plus a transfer fee. But Ward had his eye on a much bigger proportion of the fees. Towards the end of the life of Ark, Ward was preparing to take Ark over from Tweedley – along with an associate of his: Peter Moat (another pension crook who went on to operate the Fast Pensions scam – now also in the hands of Dalriada Trustees). In a way, it was a shame that didn’t happen, as Tweedley did at least try to help the Ark victims, whereas Ward never lifted a finger. In fact, he simply told the Ark victims to throw the tax demands away as “HMRC would never pursue them”.

In February 2011, HMRC met with Tweedley and Ward to discuss the “loans” – so HMRC knew perfectly well that Ward was the main brain behind the scam. It is, therefore, astonishing that they did nothing to stop him operating so many further pension scams.

Ark came to a shuddering halt on 31st May 2011, when tPR appointed Dalriada Trustees and the scheme was suspended. Dalriada went up to Yorkshire to confront Crag Tweedley and relieve him of all the evidence and files relating to the scam. Tweedley told Dalriada that all the records were held down at Ward’s Manchester office at 31, Memorial Road and he drove down to collect them from Anthony Salih. He arrived to find Salih removing all the Premier Pension Solutions fee agreements on the instructions of Ward (he managed to shred most of them – but did missed a few which I now have).

After Ark, Ward went on to run the Evergreen Retirement Benefits QROPS scam with accompanying 50% “loans” and a further 300 victims lost £10 million worth of pensions. HMRC removed Evergreen from the QROPS list when they realised it was a liberation scam and Ward fell back on two more UK-based, bogus occupational schemes: Southlands and Headforte. Plus, he registered a number of new schemes – including Capita Oak.

The Capita Oak scheme was another bogus occupational scheme registered by Ward with a fictitious sponsoring employer: RP Medplant (Cyprus). There is, however, a firm called RP Med Plant in Cyprus. The Capita Oak trust deed was written by Ward’s bent lawyer Alan Fowler. Ward took responsibility for the transfer administration – transferring valuable personal and final salary occupational pensions into this scam – in the full knowledge that he was condemning hundreds of victims to certain financial ruin and poverty in retirement. Capita Oak is now also in the hands of Dalriada Trustees.

Other pension scams that Ward was operating – in addition to Southlands and Headforte – from 2012 onwards included Feldspar, Hammerley, Meribel, Halkin, Randwick, Bollington Wood and Westminster. And, of course, Dorrixo Alliance which was the trustee for many of these scams. Capita Oak and Westminster are both under investigation by the Serious Fraud Office.

How much more evidence do they need?

In May 2014, HMRC was given evidence of all of Ward’s various scams – including Dorrixo Alliance. They were also given detailed testimony by me and a number of victims of what Ward had been up to in the pension liberation fraud industry since Ark. It would have been very easy for HMRC to look up to see what other pension schemes Dorrixo was trustee to. Had they done this, they would have seen that Dorrixo was the trustee for the London Quantum scheme. If HMRC had taken any action, they could have prevented Mr. N – a serving police officer – and 96 other victims from losing their pensions to Ward and his various dodgy, inappropriate investments (including loans to Dolphin Trust).

If we add to the above catalogue of scams the Continental Wealth Management scam – 1,000 victims facing the loss of £100 million worth of life savings – Ward has been responsible for the destruction of thousands of people’s pensions this past eight years. Plus several suicides and deaths from stress-related medical conditions.

SERIOUS QUESTIONS ARISING FROM THE PENSIONS REGULATOR’S DETERMINATION RE:

Mr Stephen Alexander Ward – The Pensions Regulator case ref: C46205159

Ward was a director of Dorrixo from 13 October 2011 to 28 April 2015. A company called Quantum Investment Management Solutions LLP (“QIMS”) has at all material times been the sole sponsoring employer of the Scheme. Dorrixo became the sole trustee of the Scheme on 19 April 2014. Dorrixo is also recorded as being the Scheme administrator.

HMRC AND TPR WERE GIVEN EVIDENCE OF WARD’S COMPANY, DORRIXO, IN MAY 2014. THEY WERE ALSO GIVEN EVIDENCE OF A LARGE NUMBER OF SCAMS WARD OPERATED AFTER ARK – ALL INVOLVING LIBERATION FRAUD. WHY WASN’T ACTION TAKEN TO PREVENT LONDON QUANTUM? ALL 97 VICTIMS – INCLUDING A SERVING POLICE OFFICER – COULD HAVE BEEN PREVENTED.

On 18 June 2015 the Regulator appointed Dalriada Trustees Limited (“Dalriada”) as an independent trustee to the Scheme, with exclusive powers.

HAS ONE SINGLE PENNY EVER BEEN RETURNED TO ANY OF THE PENSION SCAMS PLACED IN THE HANDS OF DALRIADA TRUSTEES? THERE ARE DOZENS OF THEM, AND FEW – IF ANY – OTHER INDEPENDENT TRUSTEES ARE EVER APPOINTED BY TPR. BUT THERE SEEMS TO BE NO RECORD OF ONE SINGLE MEMBER EVER GETTING ANY RETURN FROM ANY OF THE SCHEMES IN THE PAST EIGHT YEARS – DESPITE THE MANY MILLIONS DALRIADA HAVE PAID THEMSELVES FROM THESE SCHEMES.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

AS THIS EVIDENCES THAT THIS SCAM COULD EASILY HAVE DWARFED ARK IN A VERY SHORT SPACE OF TIME, DON’T HMRC AND TPR RECOGNISE THAT THEIR LAZINESS AND NEGLIGENCE NEED TO BE ADDRESSED? THEY LEARNED NOTHING FROM ARK – AND WHILE THERE ARE VALID CRITICISMS OF WARD FOR HAVING LEARNED NOTHING, HE IS JUST A COMMON SPIV WHILE HMRC AND TPR ARE SUPPOSED TO BE GOVERNMENT DEPARTMENTS WITH A RESPONSIBILITY TO PROTECT THE PUBLIC. THE SCALE OF THIS SCAM SHOWS THESE TWO ORGANISATIONS ARE NOTHING BUT HOPELESSLY INEPT AND AMATEURISH IN THEIR APPROACH TO DILIGENCE AND PUBLIC RESPONSIBILITY.

The Scheme was promoted to potential new members by introducers. These included the following entities: GoBMV; Baird Dunbar; What Partnership; the Resort Group PLC; Friendly Investments; Premier Mark Consultants and Quantum Wealth Management Solutions Limited.

THE DANGERS OF THE SCOURGE OF “INTRODUCERS” SHOULD HAVE BEEN LEARNED FROM THE ARK SCAM IN 2011. WARD RECRUITED DOZENS OF THEM ALL OVER THE COUNTRY. AND YET NONE OF THEM HAS EVER BEEN BROUGHT TO JUSTICE FOR THEIR PART IN ARK, AND HAVE GONE ON TO OPERATE AS INTRODUCERS AND EVEN HOLD KEY CENTRAL ROLES IN LATER SCAMS. THIS INCLUDES FRIENDLY INVESTMENTS AND JULIAN HANSON – WHOSE SCHEMES ARE NOW ALSO IN THE HANDS OF DALRIADA TRUSTEES.

Gerard was responsible for producing template risk letters, member application forms, pro forma declarations stating that the person signing them was a self-certified sophisticated investor, member booklets and the statement of investment principles (of which there were four versions). Gerard sent these documents to members once they had been introduced to the Scheme by an introducer.

GERARD ASSOCIATES, RUN BY GARY BARLOW, HAD ACTED AS AN INTRODUCER TO WARD IN THE ARK SCAM. AND YET HE WAS LEFT FREE TO OPERATE IN THE SAME CAPACITY IN THE LONDON QUANTUM SCAM – AND EVEN TAKE ON A MORE CENTRAL ROLE. GERARD ASSOCIATES WAS AT THE TIME AN FCA-REGULATED FIRM – AND REMAINS SO TO THIS DAY. THE FCA HAS TAKEN NO ACTION TO REMOVE THIS FIRM OR TAKE ANY ACTION AGAINST GARY BARLOW.

GERARD ASSOCIATES’ GARY BARLOW WAS PAID £253,000 FROM THE LONDON QUANTUM SCHEME FOR DEFRAUDING VICTIMS INTO SIGNING AGREEMENTS THAT THEY WERE “SOPHISTICATED” INVESTORS. SO WHY HASN’T BARLOW BEEN PROSECUTED AND JAILED – AND MADE TO PAY THIS MONEY BACK TO THE VICTIMS?

A material number of the new members had a low or medium appetite for investment risk and, in any event, were unaware that the Scheme’s investments were high-risk investments. The Panel was troubled by the apparent disconnect between members’ appetite for risk and the high risk nature of the investments made by Dorrixo. Mr Ward accepted that the Scheme’s investments were high risk, but claimed this was made clear to new members in the Member Booklet.

I DON’T KNOW WHAT SORT OF DRUNKEN DUMMIES MADE UP TPR’S “PANEL”, BUT DID THEY SERIOUSLY THINK THAT ANY PENSION FUNDS SHOULD EVER INVEST IN HIGH-RISK CRAP? INDIVIDUAL MEMBERS’ APPETITE FOR INVESTMENT RISK IS IRRELEVANT – THIS WAS A PENSION FUND, NOT A CASINO.

The case against Ward was based on failures of competence and capability, and also a lack of honesty and integrity as well as Ward’s involvement with “pension liberation” as an introducer of members to the “Ark” schemes.

BUT TPR AND HMRC KNEW ALL ABOUT THIS BACK IN 2010 AND 2011. WHY DID THEY DO NOTHING TO PREVENT WARD FROM SCAMMING MORE VICTIMS OUT OF MORE MILLIONS OF POUNDS. THEY STOOD BACK AND WATCHED – DESPITE HAVING HARD EVIDENCE THAT HE WAS STILL UP TO HIS CRIMINAL MISCHIEF.

Mr Ward did not dispute that a company of his (Premier Pensions Solutions SL) was involved in introducing members to the Ark Schemes, but states that the relevant activity pre-dated any finding by the courts of pensions liberation and that Mr Ward had no knowledge that the schemes were being used for such activity.

BUT HMRC, TPR AND DALRIADA ALL KNOW THIS ISN’T TRUE. THEY HAVE ALL SEEN EVIDENCE THAT WARD AND HIS BENT LAWYER ALAN FOWLER ACTUALLY PRODUCED THE “LOAN” (MPVA) DOCUMENTATION AND EXPLAINED THE LOANS IN SOME CONSIDERABLE DETAIL TO THE VICTIMS. THE MPVA CONTRACTS WERE DRAWN UP BY FOWLER. IS IT REALLY CREDIBLE THAT NEITHER HMRC NOR TPR WOULD HAVE OBJECTED TO THIS STATEMENT?

The Panel did not consider there was sufficient evidence of Ward having actual knowledge of, or turning a blind eye to, the illegal nature of the activity of the Ark Schemes when carrying out his role as introducer before.

SERIOUSLY? I HAVE GIVEN EVIDENCE OF THIS TO BOTH HMRC AND TPR ON MANY OCCASIONS. THIS HAS BEEN DISCUSSED AT MEETINGS WITH DALRIADA TRUSTEES ON MANY OCCASIONS. EVIDENCE OF THIS HAS BEEN GIVEN TO THE SERIOUS FRAUD OFFICE ON MANY OCCASIONS BY VARIOUS VICTIMS AND ME. WHAT FURTHER EVIDENCE DID THE PANEL WANT? EVERY ARK MEMBER’S FILE WAS FULL OF SUCH EVIDENCE. EITHER TPR IS LYING OR IT IS INCOMPETENT. OR BOTH.

The Case Team also relied on certain alleged failures in relation to other pension schemes (called Headforte and Halkin), of which Mr Ward was a trustee. These are denied by him (e.g. an allegation of failure to appoint an auditor to those schemes) and the Panel did not consider it necessary to make findings in respect of them.

SO WHAT ACTION HAS TPR TAKEN IN RELATION TO HEADFORTE AND HALKIN? BOTH WERE BEING USED FOR PENSION LIBERATION FRAUD BY WARD – AND YET THE VICTIMS PROBABLY STILL HAVE NO IDEA WHAT HAS HAPPENED TO THEIR MONEY. IT IS ABSOLUTELY ASTONISHING THAT NO ACTION HAS BEEN TAKEN IN RELATION TO THESE TWO SCHEMES, PLUS ALL THE OTHERS WARD HAS BEEN OPERATING OVER THE YEARS.

Stephen Alexander Ward (date of birth 11 July 1955) is hereby prohibited from being a trustee of trust schemes in general. This order has the effect of removing the above-named individual from all or any schemes of which he is a trustee. By section 6 of the Pensions Act 1995, any person who purports to act as a trustee of a trust scheme whilst prohibited under section 3 is guilty of an offence and liable (a) on summary conviction to a fine not exceeding the statutory maximum, and (b) on conviction on indictment to a fine or imprisonment or both.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

THIS IS NOT JUST THE DEATH OF TRUST, BUT OF ANY CONFIDENCE IN THE GOVERNMENT, REGULATORS AND CRIME PREVENTION AGENCIES TO PREVENT OR DEAL WITH PENSION SCAMS AND SCAMMERS.

Tackling Caravan Crime – Chancellor Philip Hammond. Victims of pension fraud in scams such as Ark, Capita Oak, Westminster, London Quantum, Friendly Pensions and Salmon Enterprises – will not be surprised to hear that even the Crown Prosecution Service acknowledges that the fraudsters have defeated the system. Alison Saunders, head of the CPS, has stated publicly that the British justice system can’t cope. She is stepping down and is clearly disheartened by Britain’s failure to tackle crime – especially fraud. She has vented her frustration in an interview:

But look hard enough, and you will see how tackling crime can be done successfully. As someone who constantly writes about the failure of our police and courts to bring criminals to justice, I was surprised to hear of a spectacular success story in leafy Surrey recently.

Mr. and Mrs. Shore of Thorpe, in Surrey, were successfully prosecuted and jailed for proceeds of crime. Residing in Runnymede Borough Council – presided over by Chancellor Phillip Hammond – this dastardly pair (in their sixties) were both sent down for a heinous crime under the Proceeds of Crime Act 2002 (“POCA”).

After many years of detailed investigation, the successful prosecution will send out a resounding warning to all such criminals and will no doubt discourage others from profiting from the same hideous crimes. And the crime was…….?

Housing homeless families in caravans without planning consent.

Let that sink in for a moment – vulnerable people with young children who had a choice between living on the streets or living in a caravan. And this crime was committed in Runnymede Borough where there was insufficient housing for the many poor families who could not afford private accommodation and had not been offered council homes.

This spectacular success story on the part of Hammond, Runnymede Borough Council and the CPS has left the good citizens of Surrey relieved that these dangerous caravan owners are now behind bars and dozens of homeless families are now living on the streets. Jobdone; justice served; well done Cutty Sark!

Hailing from Surrey myself, I am pleased that the county will now be a safer place. The successful prosecution was in respect of 14 breaches of six enforcement notices issued since 1999 by Runnymede Borough Council, following a seven-day trial at Guildford Crown Court. The jury heard how the farm owners had not only stationed the caravans on their own land, but had also failed to demolish a shower room. Unbelievable!

Hammond must be strutting the halls of Westminster bursting with pride and patrolling the fields of Runnymede with a sense of upholding the social and civil justice with which King John would have been delighted. In the House of Commons bar, Chancellor Hammond is probably boasting that there is a reason why he is named after a large organ. In fact, after his spectacular success with the Shores’ caravans, he will probably go down in history as “Caravan Willy” for presiding over such a coup.

I am sure that the many thousands of people who have lost millions of pounds’ worth of life savings to scammers such as Stephen Ward, Julian Hanson, George Frost, XXXX XXXX, Phillip Nunn, Patrick McCreesh, Stuart Chapman-Clarke, David Vilka, David Austin, Darren Kirby, Dean Stogsdill, Anthony Downs and James Lau will now understand why the CPS couldn’t dedicate any resources to prosecuting them. And they will, no doubt, be glad that the priority of the judiciary was removing unauthorised caravans in Surrey.

As in most of my blogs, there is an important postscript: Caravan Willy is a keen property owner and is reported to be worth over £9 million. The Shores’ land has now been confiscated by Runnymede Borough Council. And it is worth at least £27 million once planning permission for a housing estate is granted. I wonder who will be lucky enough to scoop that one up?………

The BSPS dilemma for steelworkers is clearly difficult with very little time to consider options and make a wise decision which will affect them for the rest of their lives.

There’s a whole team of willing voluntary professional advisers trying to provide some guidance to help people avoid making the wrong decision. This team includes eminent pensions experts including Henry Tapper (The Pension Ploughman), Al Rush, Darren Cooke and many more.

I’d like to contribute to this excellent initiative to help the scheme members – but I can’t advise how to do things right; I can only advise how not to do things wrong.

Henry Tapper, Al Rush and Darren Cooke – plus other qualified, licensed advisers generously giving their time to help the BSPS members – will give sound guidance as to the right decision to make. The Pensions Advisory Service will also help.

Here are some pointers from me – someone who represents hundreds of victims of pensions scams and has seen all the tricks, lies, false promises and smoke/mirrors in the pension scamming business.

Check that a proper adviser is licensed – in other words: regulated. You can check this out on the FCA register. Here is an example: check out Darren Cooke’s firm, Red Circle. You will see that his firm is regulated (or licensed by the FCA – Financial Conduct Authority) to carry out personal pension and stakeholder pension advice. Remember, unregulated means SNAKE OIL SALESMAN. And beware the “introducer” – which is another word for snake oil salesman. If you find the so-called adviser is not regulated – run like hell!

Beware “free” financial advice. Go to Tesco and ask if they have any free milk. Go to the Post Office and ask if there are any free stamps. Go to an accountant and ask if he will do your accounts for free. Go to your local car dealer and ask if there are any free cars. There ain’t no such thing as free. Everything has to be paid for – but make sure that all the charges, fees, commissions etc., are openly declared. If someone promises you free financial advice – run like hell!

Run a mile from “get rich quick” investment schemes. Your pension has to be invested in boring, safe, traditional assets which will grow steadily and safely. If you are offered something exciting and sexy – like eucalyptus plantations; car parks; football betting; overseas property “opportunities” and truffle trees – run like hell. If you are told that your pension will get “guaranteed returns” of 8%, 10% or 12% – run like hell!

If you are told you can have some cash out of your pension other than your 25% tax free at age 55 – or the rest at the marginal tax rate – run like hell!

If you are cold called – run like hell!

Remember, you are a sitting duck – and it is open season. Also remember, the good guys like Henry Tapper, Darren Cooke and Al Rush – as well as all the other decent, honourable, ethical advisers who are volunteering their time free to help you avoid the scammers – can give you some invaluable, generic guidance. But someone who is offering to transfer your pension into another scheme is giving you advice.

So what is the difference between actual advice and general guidance? Let us take the example of a medical practitioner: you know a doctor – say a GP – at your local tennis club. You are concerned about your health in general and the fact that you are putting on weight and get breathless going upstairs. The doctor might suggest – as in suggest – that you consider going on a diet and taking some exercise, but that you also consult your GP. That is an informal and friendly (as well as well-meaning and common sense) suggestion. But it does not constitute formal advice. A specialist would look for deeper issues such as blood pressure, signs of diabetes and any other underlying conditions to be investigated – and would prescribe specific treatment.

If all else fails, drop me an email and I will try to help: angiebrooks@pension-life.com – but meanwhile, please buy some good running shoes!

Meanwhile, take a look at just a few of the schemes for which Pension Life is representing groups of victims who have lost their life savings to the same – or very similar – scammers who will inevitably be targeting you now:

The Ark victims’ QC rolls over as he is quashed by Dalriada’s counsel

DALRIADA V ARK VICTIMS: “ABUSE OF VULNERABLE MEMBERS OF THE PUBLIC”

The Beddoe proceedings of Dalriada (tPR-appointed independent trustees) v Goldsmith (representative beneficiary for the Ark members) kicked off on 20th June 2017 in the High Court. It was a sweltering day in central London – humid and dusty at the same time. The Ark victims were about to discover that the warning about anomalous and unjust outcomes made by Justice Bean in the High Court in November 2011 was going to be ignored.

Dalriada and their solicitors, Pinsent Masons, and their QC Fenner Moeran sat on the left in the airless courtroom. Mrs Goldsmith and our solicitors, Trowers and Hamlins and QC Keith Bryant, sat on the right. Justice Asplin sat on the bench and prepared to rule on whether 348 Ark victims would have to repay their MPVA loans – and whether Dalriada could use the members’ funds to pay for the recovery proceedings. A group of Ark, Capita Oak and Salmon Enterprises victims and I sat at the back. The only thing we all had in common was that everybody was sweating profusely from the heat.

To put this into context, the Ark victims did indeed all sign loan agreements. However, the loans were intended to be paid back out of the members’ 25% tax-free lump sums available at age 55 – so the term of each loan agreement was calculated to be for the number of years it would take each member to reach 55. By which time, the pension was predicted to have grown by at least 8% per year and would be sufficient to repay the loans. Or so the story went.

Conspicuous by their absence were the various introducers and advisers who sold the Ark schemes and accompanying MPVA (Maximising Pension Value Arrangements) “loans”. By far the most assertive and prolific of these was Stephen Ward of Premier Pension Solutions who sold over £10 million worth of transfers to more than 160 victims. Ward was followed by those who aspired to be as successful as him and these included:

Julian Hanson £5.3m

James Hobson (Silk Financial) £2.3m

Jeremy Dening £2.2m

Michael Rotherforth £961k

Richard Davies £805k

Geoff Mills £794k

Andrew Isles £584k

Amanda Clark £227k

Many of these went on to operate further pension liberation scams – some of which are now also in the hands of Dalriada Trustees. Andrew Isles of Isles and Storer Accountants is still in practice. Stephen Ward still authors the Tolley’s Pensions Taxation Manual.

The definitive pensions taxation manual by leading pension liberator Ward

Interestingly, Stephen Ward, who used Ark to launch a whole series of further pension scams – including several currently under investigation by the SFO and in the hands of Dalriada – claimed in 2014 that “The Ark thing is history now and my involvement with that was administrative”. Of course, neither of those statements was true: Ark is far from being history as, in the wake of the Beddoe proceedings, a whole new chapter of wretched challenges for the Ark victims has only just begun. Ward was the leading promoter, evangelist and advisor to Ark. He had sold over a third of all the transfers – with a total transfer value of more than £10 million.

In fact, Ward and his herd of “introducers” he had recruited from up and down the country (including FCA-registered Gerard Associates which went on to collaborate with Ward in the London Quantum pension scam) – also now in the hands of Dalriada – often assured the victims they would never have to repay the loans.

Fenner Moeran QC, for Dalriada, opened with the lusty confidence of a dashing matador – and who could possibly have failed to be charmed by his persuasive, eloquent, star quality? He reminded me of an actor at the Oscars who knew he was the favourite to win. With his extravagant hand gestures and polished, word-perfect performance, he got into his stride and stayed there – holding court for the whole day with barely a feeble squeak out of our QC.

Moeran’s confidence, however, veered a little too close to cockiness, and he strayed occasionally into the realms of being callously offensive to the Ark victims when he talked about using a “sharp stick” to beat them into submission with threats of bankruptcy. At that moment, he stopped looking like a polished QC and started to look like a mere back-street bully. In fact, it was astonishing that the judge didn’t pull him up on that “foot and mouth” moment, but she appeared to be far too mesmerised by his charming performance to notice – or care.

While I was taking notes, it was really interesting to watch the players’ body language. One can tell an awful lot about what is really going on in people’s heads by what they do with their various body parts. When Moeran was on his feet, Justice Asplin was coquettish, smiley, full of chuckles and did this wiggly thing with her shoulders (like we women do when we are trying to get a bra straight). But when our QC Keith Bryant was on his feet, she sat as still as a statue and peered down at him with a combination of indifference and pity as if he was a dying bull in the afternoon sun.

Mrs Goldsmith sat quietly and showed not a shred of distress as Moeran referred to her and all the other Ark victims as though they were just names on a list, as opposed to human beings – or indeed anything with a pulse. Knowing her well, I am sure she will have felt profound pain and anguish during the whole three days, but not once did either her composure or her dignity slip.

So here is my transcript of the notes I took on what the various parties said during the proceedings – with my comments in bold.

The last thing I personally want to say on the matter, is that something good has to come out of this and my fervent hope is that all those involved in the promotion, sale, administration, introduction, advice, purchase of assets, execution of loans and various other functions will now face justice sooner rather than later. And here, I am actually grateful to my learned fiend’s suggestion of a sharp stick and would propose something more akin to what Vlad The Impaler would have done to these criminals.

TRANSCRIPT OF MY NOTES AT THE HEARING

DAY ONE

Never forget that legal proceedings are nothing to do with justice

Justice Asplin opened with the words “This was a tragedy and an abuse of vulnerable members of the public”. That got us off to a really good start, but curiously the following day she vehemently denied ever having said it. She also denied ever having mentioned Ark and didn’t even seem to know that collectively, the six schemes (Tallton, Grosvenor, Woodcroft, Cranbourne, Lancaster and Portman) were the Ark schemes. Bearing in mind she had had – and been paid for – a whole day’s reading, one would have thought she would have been a little better prepared.

Ark’s Craig Tweedley was quoted as having made a statement that Ark was “designed to unlock amounts of money from people’s pensions in a way which was not taxable”. This is perfectly true – but it went further: it was promoted to the public (both introducers and potential members alike) as an innovative structure which was lawful and tax free. And the principal promoter and recruiter was Stephen Ward. Ward is also a CII Level 6 qualified former pensions examiner and government consultant on pensions and QROPS – so who wouldn’t have believed him?

One of the Ark schemes’ assets – the South Horizon land option in Larnaca, Cyprus – was brought up and reported as having been purchased by Ark for £4 million. But what was not mentioned was that the option had originally been purchased by two football celebrities for £1.1 million and then sold on to Ark for £4 million. And that this pair had gone to accountant Andrew Isles of Isles and Storer to get advice on how to procure further investors in the Cyprus land project. Isles had introduced them to Craig Tweedley and Stephen Ward. In fact, Isles subsequently introduced at least eleven cases to Ark.

It was stated that Craig Tweedley’s associates Andrew Hields and Julian Hanson had purchased all the assets of the schemes and that the sales documentation claimed that some of the funds were “guaranteed “funds and protected by “re-insurance”. Hields and Hanson may well have purchased some of the assets but they will certainly have benefited from handsome investment introduction commissions along the way.

It was also reported that one of the other Ark assets, Freedom Bay, the St. Lucia timeshare development, is now in administration and that none of the investments made met the statements and claims made in the sales documentation. In fact, it did not come out that few – if any – of the victims were ever shown the sales documentation. Most of Stephen Ward’s victims were told the assets would be “high-end residential London property”.

The matter turned to the recovery effort. It was reported that Tweedley had been pursued for the 5% fees taken from scheme members and that although Dalriada had won their claim, of the approx. £1.5 million taken in fees, they only ever actually managed to recover about £20k. This does beg the question as to just how successful Dalriada will actually be in recovering the £9 million in MPVA loans.

In taking steps to recover the loans, it was reported that Dalriada intends to consider the cost vs benefit situation and decide on the approach on a case by case basis, taking each individual case on its merits. It was acknowledged that the chances of recovery were slim and that the costs could be disproportionate to the likely return. The judge asked how many members had received MPVAs and it was disclosed that 348 had and 138 had not. However, nobody raised the question of why such a large number of members had not received an MPVA loan – had they done so it ought to have been disclosed that a significant proportion of transfers were not rejected after Dalriada were appointed.

It was at this point, while examining the possible avenues to recovery, that Moeran’s confidence bubbled over into bald cockiness and he started bragging about using the threat of bankruptcy as a “sharp stick with which to beat the victims into paying back their MPVA loans”. In fact, by now the judge seemed to be very firmly on his side and stated that the members had already agreed to repay the loans and that their only loss was having to repay early. It seemed clear that neither Moeran nor the judge understood – nor had made any attempt to understand – how the loans were sold to the victims. They were told, by Ward and all the others involved in promoting the scheme, that the loans would be repaid out of their pension pots and not out of their own funds. In fact, some people were told they would never have to repay the loans and that each person on either end of the loan transaction would simply agree to tear up their “IOUs”.

Moeran then went on to claim that by repaying the loans, members could avoid the tax charge. Perhaps the HMRC fairy had whispered this in his ear? Or perhaps he was deliberately ignoring the fact that it is HMRC’s position that the loans will remain taxable even if they are repaid.

Towards the end of day one, it was clear that Moeran was confident they were going to win and that the judge would clearly find in favour of Dalriada and against the members. It was also clear that he had the full support of the judge. In fact, Moeran even went so far as to pretty much read out what our QC, Keith Bryant, would be arguing and told the judge what she ought to find against the case he would be putting forward. At some point, I wondered whether Moeran and the judge would be swapping places.

Moeran talked about the methods and costs of taking recovery action against the Ark members. He itemised three issues to take into consideration:

Merits of taking recovery action

Cost vs benefit of taking recovery action

Consequences of not taking recovery action

He then went on to report that Dalriada had 144 signed Standstill agreements and said that Dalriada was intending spending £2,925 per member on court recovery action. The judge declared that that was on the low side as that cost could only happen if the claim was uncomplicated and resulted in a quick and easy repayment. She also said she was not confident that bankruptcy proceedings were necessarily appropriate.

She did, however, firmly declare that the Ark members had all shared the “mistaken belief” that the MPVA loans were valid, non-taxable and only repayable by the end of the originally-agreed loan term. She broke this “mistaken belief” down into four points:

The members’ “mistaken beliefs”:

The trustees had the power to make the loans

The loans were capable of being made valid

The trustee could transfer beneficial ownership of these monies

The loans were not unauthorised payments and would not trigger a tax charge

The judge appeared to consider that somehow the members had come to these conclusions all on their own. The reality was, of course, that this was exactly what they were told by Stephen Ward and the herd of introducers and advisers – including a couple of FCA-registered ones. But reality did not seem to concern either the judge or Moeran overly.

The last thing that Moeran said on Day One was to make reference to the revised Standstill agreement – the focus of which was to ensure that criminal proceedings are now taken against all those who were involved in defrauding the Ark victims. The judge read the document herself, giving us a welcome rest from listening to Moeran.

As the first day came to a close, I was beginning to wonder whether I had dreamed the fact that a High Court judge had clearly stated in the High Court that Ark had involved an abuse of members of the public. Her statement had been made in front of a dozen or more witnesses and she had then gone on to deny that she had ever said it in front of the same witnesses who all clearly heard her words. Moeran and the judge had both agreed the Ark sales documentation was false and yet I heard neither of them conclude spontaneously that criminal complaints were now essential.

DAY TWO

Moeran opened with: “We are in the process of agreeing six test cases at the First Tier Tribunal” in relation to the personal tax appeals resulting from HMRC’s treatment of the loans (whether repaid or not) as unauthorised payments. The judge questioned whether members put forward for this role might not be happy. Moeran confidently assured her that there had already been five volunteers. I am not aware that any of these purported volunteers have come from the Class Action. Also, at the last meeting that Mrs Goldsmith, Mr Walters (Salmon Enterprises) and I had with HMRC, we agreed two Ark test cases – one with a loan and one without. Moeran did not appear to be aware of this.

Skating quickly over the tax issue for the members – and studiously ignoring the fact that according to HMRC the tax will remain payable even if the MPVA loans are repaid – Moeran and the judge got back to pondering recovery measures. The judge expressed reservations about bankruptcy proceedings because she said that that would merely release members from liability to the scheme rather than help recovery.

Moeran and the judge then started to discuss which members might not be worth pursuing at all for a variety of reasons. Between them, they concluded that those with very small MPVA loans should be ignored and that they might also have to ignore those outside the jurisdiction of the UK. Moeran reported that there were four members in Northern Ireland; 22 in Scotland, 24 in the EU and four outside the EU – USA, Jersey, Bulgaria and Australia.

Neither Moeran nor the judge were sure whether Bulgaria was in the EU (in fact, of course, it is an EU member). The members and I having complained in the strongest possible terms about Moeran’s use of the term “beating the victims with a sharp stick” the previous day, Moeran then went on to publicly apologise for that statement. To be fair to him, he made a good job of the apology and I am sure that Mrs Goldsmith and other members present appreciated it.

I really don’t remember whether our QC said much or anything at all that day – if he did it was not very memorable, or perhaps I couldn’t hear him terribly well because he muttered apologetically and miserably rather than speaking in Moeran’s strident voice.

The MPVA loans were summarised thus:

50 members with loans between £5k and £9,999

124 members with loans between £10k and £19,999

132 members with loans between £20k and £44,999 (totalling £4m+)

40 members with loans of £50k upwards (totalling £3m+)

The judge opined that the bigger the loan, the bigger the original pension must have been, and therefore the wealthier the member was likely to be. She concluded that these would be the easiest targets for recovery.

Then the judge handed down her judgement. She summarised the claim by Dalriada for Beddoe relief (money to be taken from the members’ funds) for the recovery of the MPVA loans and also to challenge the scheme sanction charge in the Tax Tribunals. She approved both of these, but did not agree that Dalriada should use funds to help the members with their individual tax appeals.

She reported that 152 claims had been written to date and that 12 consent orders had been received. She declared that she believed the claims were strong but expressed reservation as to whether the members were in reality good for the money. She reminded the court that there were 138 members without loans and that Dalriada had a duty to protect their position by recovering loans from as many of the other 348 members as possible.

She determined that it was appropriate that the trustees should be granted the relief they sought – albeit not the entire amount sought. She advised Dalriada to take stock of each individual situation and use their discretion as to whether it was appropriate to continue with the action. She also urged them to take into account relevant factors including the aggressive stance being taken by HMRC and to act as a reasonable trustee.

Finally, she said Dalriada should bear in mind that the individual cost of recovery per member would rise from £2.9k to £3.6k (plus VAT) if bankruptcy proceedings were issued and that those with the very smallest loans ought not to be pursued because of the disproportionate cost of doing do. She said it was difficult to decide where exactly the “watermark” might be and reiterated that bankruptcy might not be appropriate and should not be the first refuge sought and could be used as a “second string to their bow”. She suggested that further directions might need to be sought by Dalriada.

Regarding the scheme sanction tax charge appeal matter, she said it was appropriate to give the relief sought and for Dalriada to take steps to challenge the assessments. She recommended a “ceiling” on the amount to be spent and said that to challenge the £4m in tax sought by HMRC, the amount of £350k + VAT was appropriate.

On the question of paying a further £50k to fund legal representations for members against personal tax assessments, she recommended that the scheme sanction charge and the personal tax appeals should be coordinated. But she expressed a reservation about granting this relief to Dalriada as she felt it was excessive “because of the vagueness of what might take place”. She did not consider that for them to pay a barrister was necessarily a reasonable step to take. Therefore, she did not grant the relief sought.

In summary, therefore, the judge’s determination was as follows:

Yes to recovering the MPVA loans from as many of the members as possible/practicable

Yes to paying for the recovery costs out of the members’ funds – at the ideal rate of £2.9k + VAT per member (possibly rising to £3.6k + VAT per member if bankruptcy proceedings were issued)

Yes to taking £350k + VAT out of the members’ funds to pay for the appeal against the scheme sanction charge

No to paying £50k + VAT towards the members’ personal tax liability appeals

At the start of the proceedings, Moeran had reminded the court that Dalriada, as the trustee, already had the legal right to recover the loans if they chose to. But they were seeking the necessary relief and directions to do so from the court to protect their position.

DAY THREE

The final day was all about the nitty gritty of how the recovery costs should be apportioned between the six schemes. Moeran and Bryant put forward different suggestions as to whether this should be done on the basis of the value of the assets or the value of the MPVA loans within each scheme, and whether this should be done equally or on a pro rata basis.

The members at the back of the court were by now numb and none of them really paid much attention to what was basically “housekeeping” in terms of internal accounting procedures by Dalriada. One of the judge’s last points seemed to be that Dalriada should take all and any reasonable steps to recover the MPVA loans – but that the only question was what was reasonable. She cautioned that some options should not be taken, but stopped short of saying what they were.

I am writing to explain the rather confusing “assessment” and “further assessment” appeal situation in relation to HMRC’s “pension loan wolf” situation. Although this is specifically aimed at the Ark case, it will also apply in most – if not all – other cases.

In a nutshell, the assessments are for the 55% unauthorised payment tax charges on the loans. The further assessments are for the “benefit” that the member has “enjoyed” through not having paid interest on the loans.

Here is HMRC’s explanation of their reasoning to try to tax the absence of interest on the “loans”:

“If the assessments are for small amounts these are to protect HMRC against the alternative argument that the loan is a benefit under S173 FA 2004. So for members who received loans in 2010/11, under the alternative argument a benefit in kind charge arises for 2011/12 (and every year thereafter until the loan is repaid/written off) based on the Benefit in Kind calculation ie 4% of the MPVA (loan) received each year. This is taxed at 40%.

Roughly translated into ordinary language, this means that HMRC do not know what the Tax Tribunals will let them get away with, so they are going to try to tax the loans everywhere – front, back, side, top, bottom. Ark is a bit more complicated because of the “reciprocal” situation, but HMRC will inevitably try to use the same approach with other schemes.

My defense and appeal argument against the Ark further assessments is as follows:

Dalriada Trustees will be taking legal action to recover the loan which may result in profound financial loss for the member

This member’s pension fund is severely depleted as a result of £11 million worth of unsecured personal loans which may or may not be recoverable, and in respect of which no interest has been received by the member’s scheme

This member’s pension fund is further seriously prejudiced as a result of five years’ worth of trustees’ and legal fees – largely fueled by HMRC’s protracted prevarication over how, when and where to tax various aspects of the transfers/loans.

There appears to be no end in sight to the overall financial loss this member will continue to face in the run up to the appeals being referred to the Tax Tribunals.

Any “benefit in kind” which the member is arguably “enjoying” due to below market-rate interest payments, is more than eclipsed by the financial damage caused by the combination of HMRC’s and Dalriada’s actions over the last five years. The net result, therefore, far from being a benefit in kind is a significant “loss in kind”.