I don’t often disagree with highly-regarded pensions expert Henry Tapper. Too much respect and awe. But his recent blog: “The Balls of Old Bailey” (about Andrew Bailey) merits a polite argument. It has made me cross – not cross with Henry, per se. But cross with the failure of Britain’s culture, government, regulation and legal system to address justice justly (or at all).

Henry has questioned the point of revisiting the balls-up made by former FCA CEO Andrew Bailey and has suggested that “we need to move on”.

The point of examining Bailey’s sickening catalogue of balls-ups is that we must make sure it never happens again. Part of that mission is to follow the example of the criminal justice system: we don’t give convicted criminals a jolly good talking to – or even a good bollocking. We take away their liberty and put them in prison. This is called a “deterrent”.

What did Old Bailey do that was so bad? The answer is, indeed, a long list – starting with British Steel, Toby Whittaker’s Park First and Neil Woodford’s Fund, and moving on to London Capital & Finance and a long list of other mini-bond scams – including the Blackmore Bond. Bailey should have stopped that entire horrific catalogue of investment fraud if he’d been doing his job properly. He could – and should – have prevented hundreds of thousands of victims from losing their life savings and pensions in all of those investment scams.

The advantage to be had from putting the bollocks – and preferably the head – of Bailey on the block is to send out a warning to future FCA bosses. They all need to understand that they are public servants, and that with huge salaries come huge responsibilities. Current overpaid bosses Nikhil Rathi, Christopher Woolard and Charles Randall must be reminded that running the FCA is a serious public duty – and not just an easy stepping stone to an even bigger and better job (however badly they fail consumers).

Bailey’s numerous failures were rewarded with an eye-watering salary followed by promotion to governor of the Bank of England.

But Bailey’s balls-up is by no means unique. He’s in good company with a whole raft of over-paid public servants who have betrayed the public:

Post Office boss Paula Vennells was awarded a CBE for falsely prosecuting hundreds of innocent Post Office subpostmasters for fraud – even though she knew full well they were innocent. In arguably the biggest scandal of corruption and injustice in British history, Vennells oversaw the wrongful conviction and sometimes imprisonment of 700 victims. Many of these people were financially ruined, lost their homes and committed suicide. One pregnant woman was sent to jail, and many marriages and families were destroyed.

Former HMRC boss Lin Homer was rewarded for her vast catalogue of disasters and failures with another huge salary and a £2.2m pension

Paula Vennells (left), Dave Hartnett (middle), Lin Homer (right)

But to revert to the failings of Andrew Bailey, Henry has suggested that we need to “move on”. However, those who have lost their life savings and pensions because of the FCA’s defects will have great difficulty putting their losses and harrowing ordeals behind them. Living in abject poverty won’t help them forget. They will certainly never forgive the fact that Andrew Bailey could have prevented them becoming victims of investment scams such as mini bonds, Store First, Park First, the Woodford Fund and Blackmore Global etc.

Henry’s blog concludes that Andrew Bailey, as Governor of the Bank of England, has a great deal on his plate: cost of living crisis, looming recession and Brexit. But does anybody seriously think that such a negligent, lazy, incompetent person is capable of dealing with that lot – when he couldn’t even listen to frantic whistleblowers such as Paul Carlier, Mark Taber and Brev at Bond Review who were offering to do his job for him?

This silly twerp got caught looking at lewd images on his mobile in the House of Commons. His excuse was that he thought porn was spelled “tractor”. Parish has now resigned and his political career is almost certainly over. His wife might also be quite cross. He probably won’t be rewarded with a promotion, a CBE or any kind of public “moving on”.

What Parish did was foolish. But he didn’t cost thousands of people their pensions and life savings; he didn’t ruin hundreds of subpostmasters’ lives and send some of them to prison or to their deaths; he didn’t aid and abet hundreds of millions of pounds’ worth of tax evasion; he didn’t overcharge millions of taxpayers or lose their records.

Parish embarrassed himself and was caught doing something unbelievably silly – that hurt nobody except himself (and his own family). But the price he will pay for this will be crippling and may have ruined his life. Meanwhile, Bailey, Vennells, Hartnet and Homer have evaded any kind of sanction and gone on to glittering success, awards and eye-watering pensions.

The Pension Scams Industry Group (PSIG) has carried out a pilot survey on pension scams. The survey has identified seven key findings and concluded that most scams are carried out by rogue advisers and unregulated “introducers”. This is something we write about regularly, so it is great that PSIG has finally caught up.

“Another significant concern was member awareness of advice. PSIG stated, after they found in almost half (49 per cent) of cases, the member had limited understanding or appeared to be unaware who was providing the advice, the fees being charged, or the receiving scheme to which the transfer would be made.”

A lack of understanding of the way the financial industry works is something that the scammers play on.

Many of our blogs here at Pension Life focus on getting information across to the public. You owe it to yourself to understand how the pension system works. This understanding will empower you and your money, protecting it from the scammers. We provide the platform for this information, you just need to read it.

However, time and time again we find we hit brick walls when sharing information.

Our blogs are shared on lots of social media networks. I find in many cases – especially on Facebook – that the links to our blogs will get deleted after the admins refuse to approve them. Some readers state that the blogs we write about expat scams are not relevant to expat issues.

We have been told that our blogs which highlight what questions to ask your adviser are of a commercial and marketing nature. Yet in none of our blogs do we try to sell anything – we just offer knowledge and warnings about how to safeguard your pension.

When met with this negativity, how do we get the information out there? How do we educate the public?

Future unaware victims need to know what to look out for and how to avoid a scam. Otherwise, the cycle will continue. The scammers will outsmart the public and they will continue to get rich off the ignorance of the public. And the victims will continue to see their life savings vanish.

As the saying goes, “ignorance is bliss”. However, if the ignorance leads to you signing your life savings over to a rogue financial adviser – whose only interest is purloining as much of your fund as possible – ignorance is in fact negligence.

You may think you can trust a financial adviser, but we live in a world full of scammers and crooks – quite a few of which are financial advisers. Some of them are very greedy and will stop at nothing to fatten their bank balance at your expense. They have no conscience when it comes to living a lavish lifestyle funded from another’s grim fate.

At school, they teach us about history, geography, maths and more. There is no subject about how to look after your money. Basic education on how to look after our pennies or how to finance our future is not included in the curriculum.

Knowledge is important when it comes to your finances.

I can honestly say that before I started this job, I knew very little about pensions and how they work. I simply knew that a pension was something you get when you are ‘old’.

But ‘old’ comes round too quickly. Whilst working hard, building, saving and living your life. Time flies by.

It is all too easy for a rogue adviser to contact you out of the blue about a

Above all else – safeguard your pension from the scammers.

Don’t spend your life saving for your future, just to let a rogue adviser snatch it away and spend it on theirs.

We have put together ten essential standards that we believe every financial adviser and their firm should adhere to. Make sure you read the blog and ensure your financial adviser can meet these standards. If he can´t – find one that can.

Enormous respect for the gentlemanly and (IMHO) restrained manner in which Henry Tapper has written his blog about the FCA and Debbie Gupta. The latter is blaming IFAs for “failures to call out bad practice” and claims her “view of the industry is not as positive as it could be”.

Sick

DEBBIE GUPTA – FCA’S CO-DIRECTOR OF LIFE INSURANCE AND FINANCIAL ADVICE SUPERVISION

I have never come across Debbie Gupta before. I am wondering what planet she has been on for the past six years. Victims, concerned members of the financial services industry and I have literally been hammering at the FCA’s door repeatedly. And all we have to show for it are red knuckles and chipped teeth from excessive gnashing.

In his blog, Henry quite rightly points out that “The spirit of collaboration will win, confrontation won’t.” It is a well-known fact that one wins more battles with honey than with vinegar. But two terrible wrongs have to be righted: Gupta must learn not to spout utter garbage that she knows nothing about. And Andrew Bailey must be sacked.

Let us be clear: the FCA is an embarrassment to Britain.

The cost of the FCA’s many failures is borne by IFAs in terms of levies to the FSCS as well as soaring professional indemnity insurance premiums. And the thousands of victims whose lives have been destroyed by fraudsters operating under the very nose of the FCA.

Before Debbie Gupta sticks her big foot in her mouth any further, I would suggest she attempts to learn something about scams, scammers and scamees. She should come and spend a week with me. Sit up until midnight talking distraught victims out of suicide a couple of times. She should go to Port Talbot with Al Rush and talk to some steelworkers and hear their tragic stories for herself.

Finally, Gupta should take a long hard look at the number of FCA-registered firms that have facilitated or committed financial crime. And then she should not just take back her ill-conceived words, but apologise for the profound disrespect and contempt she has shown the British advisory profession.

I have experienced at first hand how difficult (impossible) it is to get through to the FCA. Last year, I wrote a blog about my last visit. I wonder what more I could have done to “collaborate” with somebody – anybody – at their magnificent offices. I came pretty close to taking all my clothes off and singing “Bonkers” by Dizzee Rascal while shaving my head and reading Tolley’s Pensions Taxation. But still the FCA refused to speak to me. Even the guy in the post room made it clear I was a blooming nuisance when I handed in my whistleblowing report. (Which was, of course, ignored – and probably shredded).

The FCA needs to do a number of things to become an effective regulator – and none of them is particularly difficult or challenging:

Stop paying ridiculous, offensively-high salaries to no-hoper executives like Andrew Bailey. Bailey has shown he has neither the inclination nor the ability to run a regulatory authority. Throwing away nearly £600k a year on such a failure isn’t going to make him want to change and start doing a bit of regulating from time to time. Bailey is laughing all the way to the bank as he sits in his luxurious office and does SFA at the FCA. At the industry’s and public’s expense.

Buy some ladders. Window cleaners known how to use them – so I’m sure the nitwits at the FCA could try to copy them. The fat, low-hanging fruit only account for a tiny percentage of the offenders – all the really bad guys are at the top of the tree.

Take action against FCA-registered scammers. One appalling example is Gerard Associates which helped Stephen Ward scam 100 victims out of their pensions in 2014 and into toxic, high-risk, high-commission investments such as imaginary eucalyptus plantations. The scam, London Quantum, was masterminded by Ward and used to ruin dozens of victims – including a police officer. Gerard Associates provided the FCA-regulated advice. And remains FCA authorised to this day (even though it is in liquidation).

Buy a bunch of hearing aids. And listen to people. To IFAs and the industry in the UK and offshore; to the public; to me.

Update the FCA’s Whistleblowing section on the website. It is three years out of date. Reach out and invite the industry and the public to report suspicious activity – make it easy for people who take the time to stick their necks out. Welcome them with open arms and show them you care. And actually do something about the whistleblowing reports (don’t just shred them like they did with mine).

Demote Debbie Gupta to Junior on the Whistleblowing team – and pay her £41k a year like the other 12. Make her learn what this industry is really about. And teach her to keep her mouth shut until she begins to understand the seriousness of what she is talking about. Once she has learned some sense and memorised the immortal words of Dizzee Rascal: “Everybody says I got to get a grip, but I let sanity give me the slip”. She might then be ready to do a bit of regulating.

All the above will save the FCA nearly three quarters of a million pounds a year.

It will only cost a couple of hundred quid for a few dozen hearing aids and ladders. Andy Agathangelou and his team will give their advice for free. I know several dozen victims who will happily help out. By getting rid of the dross at the FCA, and providing just a bit of training for staff in the reception area and post room (as well as all the way up to the board room). It should be possible to turn this embarrassing, limp failure into something half decent.

I do hope the FCA will like some of my above ideas – after all “There’s nothing crazy ’bout me”.

Henry Tapper has published an interesting article about the problem of the number of lost pensions. We live in an age where careers are much more fluid and many people move companies or retrain and change professions. This mean many people may have had five or six different jobs (if not more) throughout their working career. Keeping track and actually remembering who all their employers were is difficult, let alone remembering who the ceding provider of their pension was 30 years ago. Where’s my pension? is now a frequently asked question.

Henry writes:

‘According to the Pension Policy Institute , there is £20,000,000,000 of other people’s money swilling about in pension trusts, in the troughs of life insurance companies or “managed” in “self-invested” personal pensions.’

That is a huge amount of money that has been worked hard for and is to get someone through their later years. So how can we answer the question: Where’s my pension?

Well apparently, according to Henry’s intelligence, the DWP were going to do something about this situation back in March. However, – and really not that surprisingly – it’s now December and nothing has been done!

The DWP had proposed a pensions ‘dashboard’, a go-to for people who were stuck with the unanswered question of ‘Where’s my pension?’ But we are still waiting for this to be completed and explained.

Currently, you can use professional pension finding services like Origo or Experian to find your missing pension(s), although this is lengthy and not free of charge. Henry and the Sun newspaper have kindly put together this DIY dashboard pension finding advice.

So, in answer to the question: ‘Where is my pension?’ it is probably wise to DIY your pension dashboard. If you wait for the DWP you may be cold in the ground before their proposals are actually met! Meaning they get your money! No surprise, then, that they are being slow with their proposals.

We also need to remember that scammers are lurking in the undergrowth, so will this be the next scam tactic?

When it comes to finance, nothing in life comes for free. These free pension reviews are often followed by high commissions and even toxic, high-risk investments. Leaving you worse off than you were when you were stuck with the ‘Where’s my pension?’ question.

This week Henry Tapper wrote a blog entitled, “The wheels of the law turn (too) slowly”. He exposes the fact that when it comes to financial crime the justice system in place just isn´t enough. I think he was being generous with his title. The wheels of the law don’t just turn slowly – they just don’t turn at all. Friendly Pensions has been in the news this week.

In the case of Friendly Pensions, we know ringleader David Austin is guilty of setting up 11 fake schemes, with toxic investments including a truffle farm. We know that he and his partners in crime, Susan Dalton, Alan Barratt and Julian Hanson (also connected to the Ark Scam), are guilty of scamming 245 pension savers out of £13.7 million. We knew all of this back in January 2018, yet no arrests have been made!

“David Austin, 52, has been banned from serving as a pension trustee and disqualified from working as a company director for 12 years. His business partners Susan Dalton, Alan Barratt, and Julian Hanson have also been barred from trustee roles.

David Austin’s daughter, 25-year-old Camilla, has been banned from serving as a director for four years for helping him with the scheme.”

They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

Camilla Austin was a central part of the operational side of the Friendly Pensions scam. She and a number of her girlfriends went into nursing homes and approached elderly, frail and vulnerable elderly people. They easily conned them into signing transfer request forms – all that is required to get their hands on millions of pounds’ worth of pension funds. And, of course, we all know that the ceding providers do nothing to stop fraudulent transfers.

As Henry points out, banning these people from acting as trustees or directors, does little to deter past, present and future pension scammers. A ban is barely a slap on the wrist as far as we are concerned; these scammers can still launch any number of future dodgy schemes by simply finding the next crooked stooge – just as XXXX XXXX used the idiotic Karl Dunlop to be a director in the Capita Oak scam.

Keeping pension savers safe from financial crime should be at the top of the list – but, instead, it is at the bottom. Pension scammers are left free to commit their crimes over and over again. Take Julian Hanson: he was busily scamming dozens of Ark victims out of more than £5.3 million worth of pensions back in 2011 and 2012, yet he was not prosecuted or jailed. Hence, he was still able to get “friendly” with David Austin and go on to scam hundreds more victims out of their pensions.

Despite investigations being made into these schemes, Ward was still able to go on and create the CWM monster scheme that saw around 1,000 victims conned out of their pension funds. Ward is hovering somewhere between his collection of luxury villas in Florida and the Spanish Costa Blanca – but at least he is no longer doing pension transfers. Over the past nine years, Ward can be linked to dozens more pension scams that have left thousands of victims’ funds decimated.

These cases are just the tip of the iceberg. We must not forget Philip Nunn and Patrick McCreesh´s investment scam Blackmore Global. This was in the wake of them doing the lead generation for the Capita Oak and Henley Retirement Fund scams. The Insolvency Service has wound up these schemes, yet Nunn and McCreesh remain free to defraud more victims as they have never been brought to justice.

David Vilka of Square Mile International was one of the main promoters of the Blackmore Global Fund scam. He “advised” dozens – possibly hundreds – of victims to invest their pensions in this scam (despite the fact that he is neither qualified nor regulated to give investment advice). Again, he has never been prosecuted or jailed, so still remains at large – free to continue scamming people out of their pensions.

You can see a depressing pattern here: these words are about cold, hard facts. The authorities are leaving known scammers free to keep scamming.

Victims of these scams have been left in misery and financial ruin. Some have taken their own lives. Yet the perpetrators, those guilty of these repeated financial crimes, are free to do as they please.

This area of financial crime really is where the wheels of the law don´t seem to turn. Shame there aren’t any regulators capable of doing any regulating, or law enforcement agencies capable of enforcing the law.

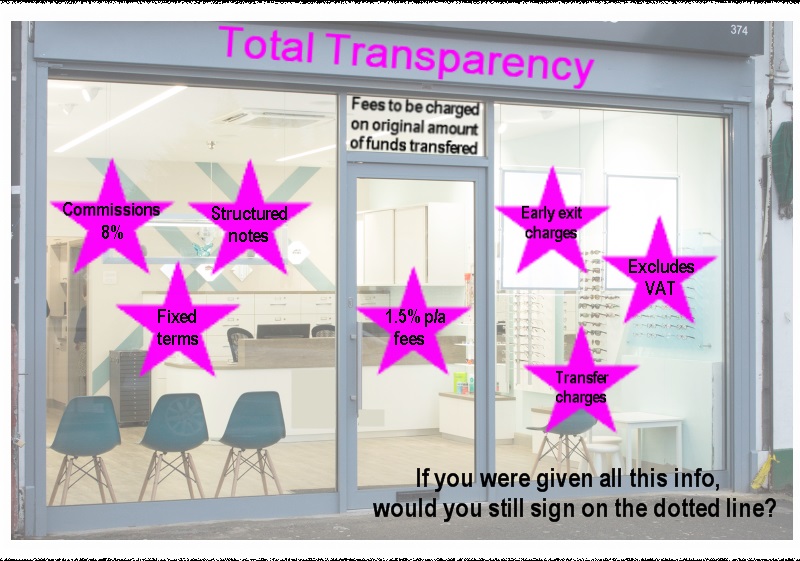

The financial services industry has failed with flyingcolours to achieve transparency – both offshore and in the UK. The single most important thing about any product or service is transparency – aka honesty. This is where the profession has tolerated – and even encouraged – bare-faced lying for years and continues to do so today.

There is nothing intrinsically wrong with overcharging – as long as the overcharger makes it clear he is openly trying to rip his customers off and the victim is consciously happy to be ripped off. Personally, I’d love to be able to sell my car for 25,000 EUR – but with its age, condition and mileage I know I’d struggle to get 5,000. However, a crafty, clever person could give it a makeover, a clockover, tell a few convincing porky pies – and some poor fool might pay over the odds for it.

Most of the victims I deal with tell me the same story:

the adviser said the “review” would be free

the adviser said the only charge I would pay would be 1.5% a year

the adviser said my fund would grow at 8% a year net of charges

the adviser never told me about the insurance bond

the adviser never told me he was going to invest my funds in high-risk, illiquid funds or structured notes

Most people describe their offshore adviser as being about as transparent as a pork chop and the “flying colours” of their achievements to be fifty shades of brown.

Champion campaigner against this sort of dishonesty is international king of transparency Andy Agathangelou – Founding Chair of the Transparency Task Force, the collaborative, campaigning community dedicated to driving up levels of transparency in financial services around the world. Andy writes for Investment Week and calls for total transparency from offshore advisory firms.

One of Andy’s key statements is: “the financial services industry as a whole has a moral, ethical and professional duty to behave transparently”. But I wonder if that is a bit like asking for World peace, an end to pollution, a cure for cancer or a reversal of global warming (and a solution to the Brexit problem).

In the UK, advisers are not allowed to charge commissions on the products they sell, meaning that they will (hopefully) choose the best investment for their client – as there is no financial incentive to chose one product over another. However, offshore advisers do not have these restrictions, meaning that when they are selling an investment they will inevitably choose the one that pays the most commission.

But are things really that squeaky clean in the UK? Does the “beady” eye of the FCA have any effect or is it merely a masking mechanism to cloak lack of transparency (aka lying) in a thin veneer of false security? Henry Tapper’s recent blog on the subject of the FCA’s investigation into 34 firms suspected of non-disclosure of investment charges reports:

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

One example was cited: Canaccord Genuity claimed its annual management fee was 1.25% plus a transaction commission of £30. But it turned out the 1.25% was just the beginning – then there were VAT and fund charges bringing the true cost nearer to 2.75%. Now, I know we women sometimes stretch the truth when it comes to our age, weight or clothes size – but Canaccord’s porky pie was that the real charges were actually twice what was claimed. That’s not just lack of transparency – that is naked dishonesty.

I had a browse through Canaccord’s funds and got bewildered by the range of costs – the annual charges seemed to range from 2.1% up to a whopping 4.34%. I’m just wondering whether an investor prepared to pay 4.34% for one of these funds might like to buy my car as well? After all, if they can throw their money away so easily, they surely can’t be bright enough to realise my rusty old heap isn’t worth 25k.

While I was in a browsing mood, I thought I’d have a wee look at Flying Colours. The company aims to provide super low-cost advice and investment funds and “negate the hidden costs in the market”. The website claims “I’m building a network of independent financial advisers with a shared vision – to improve the returns of UK investors. Join us.” But now I’ve got alarm bells ringing: a network? And who exactly is in the network?

A list of firms scattered across England from Bristol and Godalming to Liverpool and Skelmersdale – plus a few one-man bands. But they all claim to be “independent” financial advisers. How can they be independent if they are tied agents of Flying Colours? We are back to the “Wild West” offshore culture where members of a network are effectively “feral” and get up to all sorts of mischief due to lack of independence. And let us not forget that tied agents are illegal in Spain – and for good reason because the Spanish government knows that advisers simply cannot be independent if they are tied to one provider.

The Flying Colours network includes All Things Financial, Arch Financial Planning, CBG Financial Planning, Cullen Wealth Management, E-Crunch, Fit Financial Services, JAV Financial Planning, JBD Financial Planning, JRF Financial Planning, Lavelle Financial Services, Layfield Wealth Management, Mathew Burrows Financial Planning, NTW Financial Planning, Pepperells Wealth, S Fox Wealth Management, Sterling Financial Planning, The Royall Wealth Partnership and Tyrone Peters Financial Planning.

But how on earth does a coherent and effective compliance function work with 18 different firms scattered all across the country? (All of which are lying about their independence).

The Flying Colours website boasts: “We’re transparent about the charges you’ll pay for advice and investments. And there’ll be no hidden fees, ever.” But where are the fees and charges? I searched the whole website but couldn’t find out what they were. Because they were hidden.

Flying Colours recently made an ill-fated, abortive attempt to enter the offshore market (leaving considerable embarrassment and expense in its wake). Far from the claim of “starting strong relationships with a cultural fit and starting friendships“, Flying Colours ended up dumping the failure and retreating to UK-based “DIY” advice. Once Flying Colours’ offshore mess is cleared up, there will – no doubt – be a sigh of relief since Flying Colours was actually offering a more expensive version of the “cheap” investment advice process at 2% for investors with complex investments (so back to the same old, same old offshore “sophisticated” confidence trick).

What is there in Britain to protect consumers from lies; scams; lack of independence and transparency; weak compliance and unworkable investment offerings? Forget the FCA – they are permanently on a coffee break.

But what about the Insolvency Service? Isn’t that there to help protect victims from investment scams? More than a year ago, the IS commenced winding up proceedings against Store First for selling store pods to rogue SIPPS providers such as Berkeley Burke, Carey Pensions, Rowanmoor Pensions, London & Colonial and Stadia Trustees. So, we have thousands of victims of pension and investment fraud all left hanging – not knowing whether their investments are worthless or not. And this, of course, includes the Capita Oak and Henley scheme victims.

The lack of transparency about the store pods was, arguably, not the fault of Store First itself, but caused by the lies of the rogue promoters and “advisers” and the negligence of the SIPPS providers. A store pod is a great investment if the investor has a burning desire to invest in an illiquid, speculative asset – with the added benefit that he can also put his granny’s knick-knacks in there free of charge. While any honest adviser would have told the investors to invest their life savings in a low-cost, liquid, prudent fund – and any competent pension trustee or administrator would have refused to accept store pods as pension investments – the fact is that the backhanders set aside any common sense entirely.

Personally, I think the UK has a long way to go before it can claim to be entirely transparent. To get there, some sort of regulator would be helpful (forget the FCA – obviously) and an effective insolvency service would contribute to achieving meaningful reform. But while firms are still lying, obfuscating and cheating, we can’t really say that pension and investment scams only happen offshore. They are still very much on our doorstep.

Andy Agathangelou’s important work addresses many of the ills which blight offshore financial services. But he could do with a team of several hundred helpers to cover all the key expat jurisdictions. Offshore advisers – as well as UK-based firms – need to be 100% committed to their clients and take into consideration the future of the investments they make. They need to give their clients total transparency, not just on the commissions that will be applied but also on all other fees and charges.

Total transparency on all fees and commissions, before any transfers are made, would mean investors know exactly what they are getting into.The truth, the whole truth and nothing but the truth, is needed from day one! But it would also be exceedingly helpful if ALL UK-based advisers and fund managers adhered to this model.

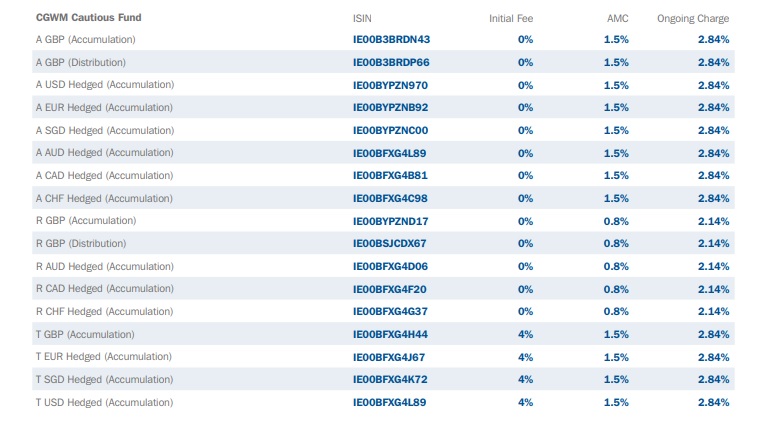

Going back to Canaccord Genuity’s opacity in the case of a client with a £700k portfolio, their non-disclosure of the VAT charges alone led to an additional cost of £10,500. £10,500 over 10 years amounts to £105,000 – quite a sizable chunk of the fund. You would have to have some very good investments to cover these costs AND increase the amount of the fund. Which, of course, is (or ought to be) the main aim of an investment!

Just for a laugh, have a look on Canaccord´s website at their list of fees, in particular, their cautious fund. 4.34% a year in charges. I wondered if this included VAT (being a “cautious” investor!).

So I decided I´d give them a call, just to clear up the confusion.

I was passed around various departments and ended up talking to a woman, who was – to put it plainly – pretty unhelpful. I asked about the charges and was told I would need to talk to a fund manager. I was asked how much I wanted to invest. I replied I´d need more information before I could commit to an amount. I was told there was a minimum investment of £250,00, but she still couldn´t tell me about the fees and charges.

I was put on hold, after she implied she might find out the answers to my questions. However, she must have forgotten me as no one came back and I was simply left hanging – listening to the sound of silence. Hopefully, Canaccord won’t forget me in the future.

Mind you, I didn’t have much luck with Flying Colours either. I chatted to their online “can I help you?” chap, Stephen Murphy, and asked him what the fund and advisory charges were. Murphy wanted to know why I wanted to know. I explained I was writing an article on Flying Colours’ fees. His reply was: “In regards to you writing an article around fund charges – we are not interested in featuring in an article as you are based in Spain – however, if you need further information around this you could contact Dani Greenfield on dgreenfield@flyingcolourswealth.com – she deals with the marketing side of our business.” Why so secretive I wonder?

Offshore advisers should be forced to put labels like these on their investments!

All this leaves us with a number of pressing, unanswered questions:

Is it acceptable that the financial services industry has failed with flyingcolours?

Is it tolerable that in some ways it is as bad in the UK as it is offshore?

Should consumers continue to tolerate unacceptably high charges from providers?

In the Royal London v Hughes case, Royal London suspected an attempted transfer was destined to go into a scam and blocked it. The member, Ms Hughes, complained to the Pensions Ombudsman – but he did not uphold her complaint. He said that Royal London was quite right to block the transfer. But Ms Hughes appealed the matter to the High Court and the judge overturned the Ombudsman’s determination.

The industry was, naturally, appalled. But this matter left many questions unanswered:

Why was a singing teacher so desperate to transfer her £8,000 pension and have it invested in Cape Verde property? (Had she developed a passion for collapsible flats?)

Where did she get the many thousands of pounds it must have cost her to have a barrister represent her in the High Court? (Considerably more than eight thousand quid I reckon).

How come the mighty Fenner Moeran QC (for Royal London) got so soundly defeated by a public access barrister? (Was his sharp stick a bit blunt that day?)

What happened to the several hundred people queuing up behind Ms Hughes to have their pensions invested in Cape Verde flats? (“Flat” being the operative word).

I could ask loads more pertinent and searching questions – like why did Ms Hughes’ public access barrister, Frances Ratcliffe of Radcliffe Chambers, think it was a good use of her considerable skills to defend an obvious pension scam? How drunk was the judge on the day? How many more people got scammed out of their pensions because of this abomination – and proof the law is not just an ass but a whole donkey farm?

Anyway, enough already. The damage was done in the Royal London v Hughes case. And now, hopefully, the door to justice has been opened in the Police Authority v Mr N case – as eloquently reported by Henry Tapper in his blog on 2.8.18. But there is a great deal more work to be done on this now: the scammers who organised and promoted the London Quantum scam need to be prosecuted and jailed; and the FCA-regulated firm – Gerard Associates – which gave the advice to the police officer (Mr N) needs to be sanctioned by the FCA. Gerard Associates – run by Stephen Ward’s associate Gary Barlow – also needs to refund the £5k they charged Mr N – and indeed all of the £220k they charged the 98 London Quantum victims.

Now is the time to bring to justice not only the pension scammers, but also the negligent ceding pension trustees who allowed the scammers to succeed – and facilitated financial crime.

At the time Mr N was scammed by Stephen Ward; Viva Costa International (the “introducers”); and FCA-regulated advisers Gerard Associates, the Pensions Regulator’s “Scorpion” campaign was in full flow. But it was unbelievably inept. It only really talked about liberation and ignored the many other kinds of fraud being perpetrated at the time – i.e. investment fraud.

The London Quantum pension scam came hard on the heels of the Capita Oak and Henley scams – which straddled the Scorpion watershed of February 2013. The transfer administration for Capita Oak was done by Stephen Ward of Premier Pension Solutions (Spain) and Premier Pension Transfers (Worsley, Manchester). Ward knew from first-hand experience how ceding trustees were starting – albeit agonisingly slowly and gradually – to resist transfer requests.

Here is evidence of the first tentative – and very inconsistent – moves to do some long-overdue diligence on pension transfer requests – as reported by Stephen Ward’s team of transfer administration scammers:

24.4.2013 – ReAssure Pensions – “The scheme now want the client’s application and new-dated screenshot emailed to Alan (Fowler – Ward’s pension lawyer chum) – on hold at Tom’s (Biggar – XXXX XXXX’s mate) request”.

11.4.2013 – Prudential – “Transfer canceled as per XXXX (XXXX XXXX’s wife)”

26.4.2013 – Zurich – “Unwilling to process – not sure why – need to cancel”

11.7.2013 – Zurich – “On hold as there may be an issue with Scorpion”

26.4.2013 – Friends Life – “Awaiting trust scheme rules – with Anthony (Salih – Ward’s mate) – need to cancel”

30.5.2013 – Aviva, NHS, Co-op, Friends Life – “Schemes are refusing to transfer”

11.6.2013 – Scottish Life – “Scheme contacting client – believed not transferring”

However, during this same period, there were plenty of transfers being made in defiance or ignorance of Scorpion. These included ceding schemes NHS (£43k), Scottish Widows (£25k), LGPS Newham (£47k), Aviva (£54k), Xerox £92k, Zurich (£21k), Prudential (£25k) and Standard Life (£53k).

But the most worrying was the Firefighters Pension Scheme: £69K after the following notes were made:

“Advised that the trustees committee are meeting to discuss cases and we are awaiting a call back next week. Transfer sent today 2.7.13 and paid on 16.8.13. Statement sent to XXXX and Tom (Biggar)”.

So the Firefighters were no better than the Police Authority in terms of ignoring the Scorpion warning.

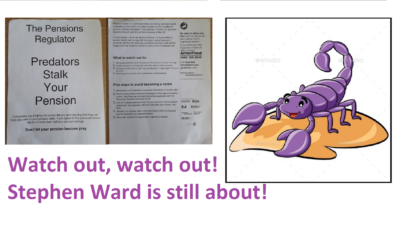

And here is what the Scorpion warning was saying from 2013 onwards – and, indeed, was still saying in 2016 when the last couple of hundred Continental Wealth Management victims were in the process of being scammed:

Predators Stalk Your Pension

Companies are singling out savers like you and claiming that they can help you cash in your pension early. If you agree to this you could face a tax bill of more than half your pension savings.

Don’t let your pension become prey.

Pension loans or cash incentives are being used alongside misleading information to entice savers as the number of pension scams increases. This activity is known as ‘pension liberation fraud’ and it’s on the increase in the UK.

In rare cases – such as terminal illness – it is possible to access funds before age 55 from your current pension scheme. But for the majority, promises of early cash will be bogus and are likely to result in serious tax consequences.

What to watch out for?

Being approached out of the blue, over the phone or via text message

Pushy advisers or ‘introducers’ who offer upfront cash incentives

Companies that offer a ‘loan’, ‘savings advance’ or cash back’ from your pension

Not being informed about the potential tax consequences

Five steps to avoid becoming a victim

Never give out financial or personal information to a cold caller

Find out about the company’s background through information online. Any financial advisers should be registered with the FCA

Ask for a statement showing how your pension will be paid at retirement and question who will look after your money until then

Speak to an adviser that is not associated with the proposal you’ve received, for unbiased advice

Never be rushed into agreeing to a pension transfer

If you think you may have been made an offer, contact Action Fraud.

But, the Scorpion warning failed tragically in so many different ways:

The warning only talked about liberation. Many victims thought this warning didn’t apply to them as they had no intention of liberating their pension fund

No information was given on how to find out about a company’s background – and how to establish whether it was regulated

The warning talked about advisers being FCA regulated – but ignored the question of offshore advisers who obviously wouldn’t be FCA regulated

The public was advised to contact Action Fraud – but did not disclose that Action Fraud would do absolutely nothing

In 2015, we went to see the Pensions Regulator to talk about the failings of the Scorpion campaign – as well as the failings of the Regulator. Two Ark victims and I met the then Executive Director for Regulatory Policy – Tinky Winky. Our intention was to explain to him how the Scorpion campaign had failed and how it needed to be made more robust and comprehensive.

Tinky Winky, flanked by two lawyers and a paralegal, told us to “hop it” – and warned us that if we tried to interfere with the authority of the powers of the regulator, our arse would be grass and he’d be a lawnmower. A year later the Scorpion warning had still not been updated or improved and hundreds more victims lost their life savings.

The Pensions Ombudsman is, naturally, the hero of the hour in the Mr N v Police Authority case. And hopefully, he will find for the rest of the victims if they all now bring complaints against their negligent ceding trustees in the London Quantum case. But we must remember that, contrary to what the Ombudsman’s service has said for the past few years, the industry did know about pension scams long before the Scorpion Campaign in February 2013.

In fact, a clear warning had been given in 2010. The Pensions Regulator had been fully aware that since 1999 pension scams were on the increase, and yet did not make it clear to ceding pension trustees what their statutory obligations were in respect of transferring victims into scams. On 13.7.2010, tPR Chair David Norgrove stated that: “Any administrator who simply ticks a box and allows the transfer, post July 2010, is failing in their duty as a trustee and as such are liable to compensate the beneficiary.”

But pension trustees claim they never read that message (let alone heeded it) and that it was neither publicised nor distributed. Further, in the same year Tony King, the Pensions Ombudsman, reported that he had “found that pension trustees failed in carrying out serious fiduciary responsibilities to others in circumstances in which the law specifically states that they should not be protected from liability.” And still tPR did nothing. And the Pension Schemes Act 1993 was not amended to reflect the urgent need to protect the public.

The Pensions Regulator’s predecessor – OPRA (Occupational Pensions Regulatory Authority) had warned about the dangers of pension scams years before 2013 – as had HMRC. The last thing I want to do is criticise the Ombudsman – as this must be his hour of glory and we must all be hugely grateful to him. Especially Mr N and his fellow London Quantum victims. But we must remember that the industry in general, and pension trustees in particular, should have been alert to pension scams long before Scorpion.

Now is the time to bring to justice not only the pension scammers, but also the negligent ceding pension trustees who allowed the scammers to succeed – and facilitated financial crime.

When I grow up, I want to be able to write blogs as eloquently as the Mighty Henry Tapper – the Pension Ploughman with a huge plough which furrows deeply through much of the bullshit on Twitter. He also tolerates Ros Altmann with grace and generosity – which is something I could never do no matter how grown up I get.

Henry´s recent blog is particularly pertinent as it draws attention to the small and irritating gaggle of willy wagglers who understand little but talk a lot about how knowledgeable they are. In fact, many of these know-alls grasp very little outside their own comfort zone – and some of them, like John Ralfe, have neither class nor manners. John and his fellow gaggle of wagglers are quick to belittle and insult, but slow to make the effort to understand complex matters in sufficient depth to be able to develop a balanced and intelligent view of the diverse details of human economics.

But first, let me talk a little about Henry. He is one of the small, elite group of professionals who have bothered to get their feet wet and their hands dirty and venture into my world: the arena of pension and investment scams and scammers. It takes a strong stomach to square up to the vile operators and facilitators of financial crime, and a lot of backbone to call out regulators and other authorities for their dismal failings.

Señor Tapper, over the past five years, has generously given his time, effort and expertise to the plight of the scam victims. Victims who have also been very active in campaigning and representing other victims – including airline pilots, bus and taxi drivers, nurses and doctors, architects, research chemists, a carp breeder, a driving instructor and people dying of life-threatening illnesses.

Then you’ve got the so-called professionals in the UK who think – and say – that none of what goes on in the scamming industry, or offshore, is anything to do with them. Some of these self-proclaimed experts also dismiss the victims as “stupid” or “complicit”. To say I have no time for these people would be a bit of an understatement. But to see some of these idiotic “experts” also being insulting to the very people I value so highly is a bit much for me – and the victims – to swallow.

Henry complains about the pesky “experts” on the following grounds:

They make you read their books

They willy waggle

They waggle each other’s willies

They get frustrated when you don’t agree with them

They are generally from the USA and Europe

I don’t really have a problem with number 1, because I also try to get people to read my book: Anatomy of a Pension Scam

I did try to make it free, but the cheapest selling price Amazon will let you use is $1.34.

I don’t do 2 or 3 (either actually or metaphorically) but I do 4 a lot. But that is because intelligent, knowledgeable people tend to understand the importance of tackling financial crime, while arrogant, ill-informed people don’t. Not that I am talking about agreeing with anything complex or requiring much knowledge – I am referring to the basic principals that scamming is wrong; being unqualified is wrong; being unregulated is wrong; being greedy is wrong.

I am not too sure about 5 because I know very few people from the USA. However, the people I tend to meet in Europe are mostly either victims or perpetrators – and they are both genuine experts in their field of expertise in equal measures (i.e. at being scammed or doing the scamming). I have met one or two good guys on the Continent, but they are pretty rare.

I’ve had a quick look at the willy waggling Tweets by John Ralfe (clearly a legend in his own mind) to which Henry is referring. Ralfe appears to be recommending that Henry should take up reading the work of Nobel Laureates. I have no doubt that should Henry ever feel the need for advice about what books he should read, he will know exactly where to go. And, of course, Henry is far too much of a gentleman to tell this ignorant twerp where to go. I, on the other hand, do not aspire to Henry’s high standards.

So, Mr Ralfe, take your willy and waggle it somewhere else.

International Investment has written a jolly good article about the recent action taken by the UAE Insurance Authority – headed up by His Excellency Ibrahim Al Zaabi. I quote from Gary Robinson’s article:

“In a statement on the Arabic version on its website the IA has issued a circular confirming the suspension (of Holborn Assets) for a period of three months or until it is satisfied that the company has improved its performance.

According to Dubai-based sources that International Investment has been speaking to, the IA has written to regulated insurance companies notifying them of their action.”

I have no doubt that Holborn Assets will rise to the challenge magnificently and in a dignified manner – and will recognise the fact that it is time for the routine misuse of all insurance bonds in offshore financial services to come to an end. I also doubt Holborn Assets will sell any more RL360 products.

The Continental Wealth Management debacle must surely serve as a perfect example of how and why insurance bonds should not be used at all – and indeed how and why structured notes should be banned altogether. And yet, despite the Malta FSC’s lukewarm change in regulations to ban advisers without an investment license and limit structured notes to 30% of a portfolio, useless/pointless insurance bonds and toxic structured notes are very much the norm across the offshore financial services landscape.

The Eagle-eyed Sheikh Al Zaabi has obviously spotted something that regulators in all jurisdictions which affect British expats have turned a deliberate blind eye to. Insurance products can, have been, and are routinely abused. And the abusers often cause heavy losses to thousands of unfortunate victims. His Eminence also obviously recognises that turning a blind eye damages not only the jurisdiction in question, but also the reputation of financial services in general.

The FCAtakes no action even when their nose is rubbed into obvious fraud – and let the British Steel disaster happen under their very noses. In fact it took public-spirited independent financial services professionals such as Al Rush, Darren Cooke and Henry Tapper to take it on themselves to try to rescue the steelworkers while the scammers hovered like vultures. I would like to be proud to be British, but the FCA is a national disgrace and an embarrassment to all British citizens. I wouldn’t mind if the FCA was just lazy, but it simply doesn’t care about the interests of those who get conned and scammed.

The Guernsey FSC allowed many frauds, including trustees Concept Trustees to sell UCIS fund EEA Life Settlements even after the FSA “toxic” warning. And, of course, EEA Life Settlements itself. Then the stable door shut with a resounding clang as an ombudsman was brought in, but told not to hear any complaints prior to July 2013. This effectively excluded all the worst scams which were being carried out in Guernsey by the likes of Concept Trustees – which took business from Stephen Ward’s Premier Pension Solutions which neither had regulation nor professional indemnity insurance.

The Gibraltar FSC appears to actively encourage outright scammers such STM Fidecs – and when financial crime is brought to their attention they go fishing for a few small, wet fish. Talking of fish, I think it is very fishy that Paul Garner, now of the Gibraltar FSC, used to work for scammer XXXX XXXX at Global Partners Ltd – the firm that “advised” hundreds of UK-resident victims to transfer their pensions to an STM Fidecs QROPS. Then STM Fidecs allowed XXXX XXXX to invest 100% of 100% of these victims’ funds into his own UCIS fund: Trafalgar Multi Asset (now in liquidation). I genuinely don’t know at which point Paul Garner moved over from Global Partners Limited to the Gibraltar FSC……but I have a feeling his leaving do will be an exceptionally (and uncharacteristically) lavish affair – and I am very much hoping to be invited. I hear there will be something fishy on the menu and Garner’s good fortune will be toasted with something bubbly. I have no doubt the cleaners will effectively brush all the crumbs under the carpet after the party.

The Central Bank of Ireland will be put to the test when scammers SEB (formerly Irish Life) are put in the spotlight. CBI has known for years that SEB – led by Peder Nateus and Conor McCarthy – has been facilitating financial crime. SEB took £ millions’ worth of business from unlicensed scammers Continental Wealth Management and allowed the whole lot to be invested in toxic structured notes: “for professional investors only”. These notes – including the fraudulent Leonteq ones (over which OMI is now suing Leonteq) clearly warned of the “danger of loss of part or all of your capital”. And yet SEB sat there and watched while hundreds of CWM‘s clients’ victims’ life savings were destroyed – and did nothing. This has left many victims in despair and poverty – with some contemplating suicide.

Against this backdrop of extreme ineptitude and collusion amongst this collection of chocolate teapots, motorbike ashtrays and fishnet willy warmers, let us all hope that the UAE Insurance Authority shows all these no-hopers what effective regulation should look, smell and feel like.

I like to have a good relationship with regulators. And believe me I have tried really really hard with the FCA. I didn’t have much of a relationship with the Pensions Regulator in the past. I asked for a meeting with Tinky Winky, tPR’s former executive director. He turned up with two lawyers (in case one blew away I guess) and a paralegal in an aptly-named conference room called the Warwick Suite at a hotel at Gatwick airport.

Winky accused me of bombarding him with emails (about the Capita Oak scam). I counted them: 16 over an 8-week period. My calculator said that was approximately two per week.

Then he threatened me for “tipping off” and said I could be prosecuted; then the uglier of his two lawyers threatened me with unspecified action if I didn’t wind my neck in. She said to me in a rather unpleasant manner “we can have you sent to the Tower you know – we have wide-ranging powers”.

Anyway, our little tea party in the stuffy room didn’t exactly make for a good spirit between us. So I sighed a huge sigh of relief when Winky departed tPR a year or so later and went to work for LGPS (one of the ceding providers who had performed so appallingly in Ark, Capita Oak and Westminster – handing over £ millions to the scammers without batting an eyelid).

I am happy to say I have a good relationship with Lesley Titcomb – Head of tPR – and am grateful to Henry Tapper for facilitating this.

But, back to the FCA. I went to see John Thorpe at the FCA a couple of years ago – with a rather thin colleague of mine who is a Chartered Financial Planner. John was very enthusiastic about working with us and asked me to give him any intel I had on scams and scammers. He said he would ensure all information would be passed on to the relevant people. However, he did warn me not to deluge him with emails and said: “not more than two or three a week please”.

But then John got moved to another department, which was disappointing. Since then I have sent dozens of complaints to the FCA – as have a number of my associates including IFAs, trustees, compliance officers, chartered financial planners and victims. But the firms in question are left unsanctioned. And the non-compliant practices continue unabated – and more victims are ruined on a daily basis.

In 2016, Jeremy Donaghy-Sutton (a senior airline captain and safety instructor) and I got together in London. He suggested we propose to the FCA an air-crash-style investigation and reporting system to analyse the causes of scams, prevent them from recurring and taking the appropriate action against those responsible for failures. Mostly his brilliant work, we finished and printed off our proposal and set off for the FCA offices.

I had called ahead and told them we would be coming and that we would like to hand our proposal, report and a series of complaints to an appropriate person. I said it was important that we had a brief chat so that we could explain the purpose of our visit (me plus an actual victim) and the accompanying documentation.

We got to the FCA’s North Colonnade office and went to reception. There I explained who I was, what I wanted, who and what I had with me. A very pleasant lady, flanked by two security guards, said “Oh, but we don’t see people here”. Her English wasn’t too bad, but I did wonder whether she hadn’t quite understood what I had said. So I tried again, and went into some detail about the fact that the person I had previously spoken to at the FCA had said that someone would indeed come down and see us.

But her English seemed to get worse the second time. And she still insisted that nobody would come to see us and accept the documents. I tried a third time, while Jeremy sat in the waiting area chuckling quietly as he could see and hear my fuse getting shorter and shorter.

This time the nice lady said she would get someone to speak to me on the phone and asked me to sit down for a few minutes while she got through to somebody. Jeremy and I sat watching the ghastly moving picture on the reception wall – and I wondered what on earth had inspired such a weird and inappropriate piece of “art” (and what the artist had been on at the time).

After about ten minutes, I was summoned back to the reception desk and the nice lady handed me a phone. I have no idea who the man on the other end of the line was, and not much idea whether he was speaking in English or some weird combination of Mandarin, Yiddish and Czech.

When I eventually got my head and ears around his weird accent, I realised he wanted me to explain – over the phone – who I was and what I wanted. By this time there were about twenty people hanging around in the reception area – so this extremely confidential complaint and report proposal was announced loudly and publicly as my voice got higher, squeakier and louder.

I had to spell out some words several times as the man’s English seemed to get worse as the agonisingly painful conversation dragged on and on. When I had finished, exhausted and wondering if this was all a bad dream, the man said “OK, hand your documents into the post room”. We duly dropped the bulging envelope into the tiny little room just outside the entrance to the FCA building. I assume it was all shredded as we never even got an acknowledgement.

Afterwards, over a quick lunch in a Thai restaurant just up the road from the FCA, Jeremy and I wondered if what had happened had all been just a bad dream. How could such a thing happen in a supposedly civilised and well-regulated country. But then Jeremy himself had spent the past five years wondering how the Ark “thing” had been allowed to happen.

The very things I warned about back in 2016 are still happening and victims’ pensions are being routinely destroyed – both in the UK and offshore. At the Transparency Task Force Symposium in November 2017, one victim stood up and related a remarkably similar story to mine about his treatment by FCA. The delegates – who included pension trustees, solicitors, police officers, victims and the wonderful Andy Agathangelou – were stunned and disgusted.

So, if anybody knows anyone at the FCA who might like to do a bit of regulating no more than twice a week, could they please let me know?

Here is the video Pension Life constructed with the help of Jeremy Donaghy-Sutton (a senior airline captain and safety instructor and Ark victim)

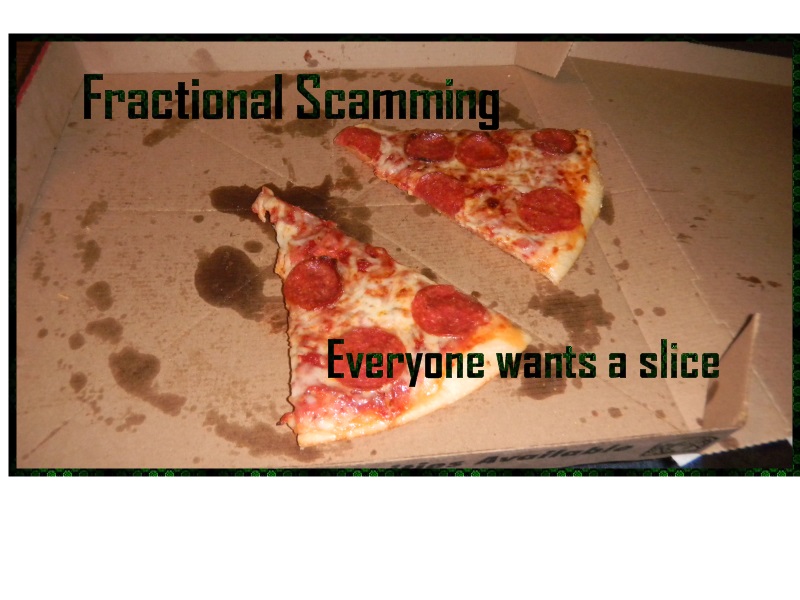

Having read Henry Tapper’s A Master Class in Fractional Scamming, here at Pension Life we feel we should share some facts with our readers about the “trending” investment and pension scam of 2018 – fractional scamming.

First of all here´s a bit about the fractional scam:

Today with new regulations, pension liberation has pretty much gone out of the window. Instead, victims are being offered to transfer their pension fund into a “new” scheme and invest in funds with promises of high returns and low risks. What is hidden in the small print is that whilst there MIGHT be high returns (possibly, if the wind is blowing in the right direction for long enough), the fund has to work its way through the hands of many parasitic introducers and advisers – each one taking their own fraction of the fund.

Henry Tapper uses a Pizza as a great example. Say you ordered a pizza which has been cut into eight slices. On its way to you, the pizza goes past 6 people, and each one takes a slice. Therefore 3/4 of the pizza has already been eaten by the time it gets to you. That does not leave much for you, the person whose pizza it was supposed to be.

This is what is happening to pension funds subjected to fractional scamming, they are being passed from one adviser to another and each one takes their slice.

So whilst the pension fund may well be going into a high-return investment, (when they finally arrive there), the fund has to recover from the percentage slices taken before any profit can be made. Using the pizza as an example, 75% of it was eaten before it arrived at its promised destination. 75% is a pretty high figure – even if the investment interest is 6.5%/7.5% – it is going to take another lifetime to get it back to its original value. Something the victims of fractional scamming don´t have.

The trending pension scam, fractional scamming – this image shows how the scammers skim their slice of the victims’ pension fund in this new wave of pension scam. Chip, chip, chipping away until the original pot is but a fragment of its original state.

What is most frustrating about the situation is that many of the people benefiting from the fractional scam are unregulated advisers. They are the unauthorised introducers who work with unauthorised – as well as authorised – IFAS who worked with Pension Trustees to transfer money into overseas funds. Each one taking their fraction of the fund.

Ways to avoid falling victim to fractional scamming are to ensure that the adviser you are proposing to use is fully authorised by the FCA in the UK. Or by the appropriate regulator in whichever jurisdiction you are resident. Do your own due diligence to ensure that you know all the facts about the transfer of your pension fund. What are the fees – as in ALL THE FEES – relating to the transfer; where will the fund be going and what exactly will it be invested in.

If you are cold called – HANG UP IMMEDIATELY

Do the adviser’s promises sound too good to be true? IF THEY DO, THEY PROBABLY ARE

High return/low risk investment – NO SUCH THING

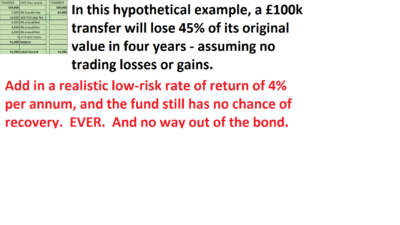

The illustration on the left is based on the Continental Wealth Management scam which saw nearly 1,000 people have around £100 million worth of retirement savings put at risk. The first year would have cost the victim at least 16% of the fund, and thereafter around 8% a year. So it never had any chance of growing – while the “advisers”, bond provider and structured note providers got fat and rich.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

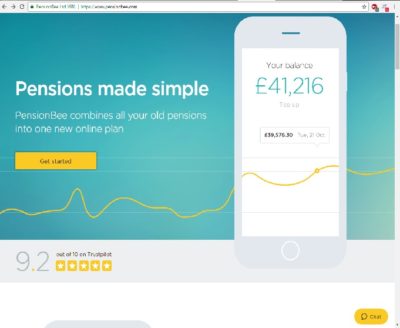

Having focused very much on bad pension investments, pension scams and how to avoid them, I´d like to talk a bit about PensionBee, a relatively new pension provider.

PensionBee offers the service of consolidating all your pension funds into one online fund. You are able to check your balance at any time and have a personal “Bee keeper” assigned to your account. The firm’s annual fees range from only 0.5% – 0.95% – significantly lower than the industry average.

Having explored PensionBee´s website, they are bright, modern and have a 9.2 out of 10 on trust pilot – not bad! You can use the PensionBee pension calculator to set a retirement goal and top up your savings to get on track. In our fast-paced, ever-changing online society, this is ideal for the busy working person.

Sounds great doesn´t it? Unfortunately, other pension providers wouldn´t agree, and it seems Aegon (formerly Scottish Equitable) isn´t impressed by their new competitor. Henry Tapper’s blog, ´PensionBee stands up to the bullies´ address the issue that Aegon are taking 38 days for a pension transfer to PensionBee. (The standard transfer time should be just 12 days). Fortunately, PensionBee is taking none of it, check out their video on “how to transfer your pension away from Aegon”.

In fact, Henry writes, ´Since 8 June 2017, customers wishing to transfer out of Aegon to PensionBee have faced barriers to switching, including multiple discharge forms, telephone calls and repetitive requests for information that has already been provided. There are various other steps that impede the customer’s right to switch pension provider easily (please see here). The average transfer out of Aegon for completed transfers now takes c.54 days – although the true scale of detriment remains unknown, since many people have been unable to overcome the barriers placed in front of them by Aegon in their attempts to switch or have simply given up.´

Upon doing some more digging I found that Professional Adviser, reported that nearly 900 customers were in fact ´stuck´ between Aegon and PensionBee. Going on to say, “So far, the longest transfer that has successfully completed is 176 days, or nearly six months.”

What we at Pension Life are struggling to grasp is, Why now?

Since 2011 big pension companies such as Aegon, Standard Life, Scottish Widows etc, have made transferring out of their pension scheme relatively easy. Even after the Scorpion campaign, which raised awareness about pension scams, these pension providers continued to release funds to bogus schemes. They have enabled the pension scammers to profit whilst the victims ended up being financially ruined.

In the Capita Oak scam – distributed by XXXX XXXX, promoted by Phillip Nunn and administered by Stephen Ward of Premier Pension Solutions – Aegon was one of the leading offending ceding providers. Aegon handed over at least 13 transfers totalling £263,271.71. Then, in the Westminster pension scam, Aegon was still up there with the worst offenders, facilitating a further eight transfers totalling at least £253,305.63.

In neither Capita Oak nor Westminster, did Aegon question why both schemes had the same sponsoring employer: R. P. Medplant (Cyprus). Nor did Aegon establish whether the schemes were genuine occupational schemes. They just handed over the transfers without heed to the Pensions Regulator’s dire Scorpion warning.

But now Aegon appears to be resisting genuine, bona fide transfers. When victims complained to Aegon about the callous and negligent manner in which pensions were handed over to the scammers, Aegon failed to uphold the complaints and refused to pay any compensation. And this despite the fact that many of the transfers were made AFTER the publication of the Scorpion warning.

I wonder – is this change due to a weight on their conscience or do they realise that PensionBee could possibly be the new long-term market competitor? A real threat to their business. PensionBee is modern, clear, fresh and online – appealing to the technology savvy generation. With the introduction of pension freedoms in 2015, savers are looking to find new alternatives with their new choices.

Fortunately, the Pensions Administration Standards Association (PASA) is aware of these issues and has created a work group to enable transferring members a faster outcome. This will hopefully make transferring pensions to legitimate schemes much easier.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

The Pension Scams Industry Group (PSIG) has carried out a pilot survey on pension scams. The survey has identified seven key findings and concluded that most scams are carried out by rogue advisers and unregulated “introducers”. This is something we write about regularly, so it is great that PSIG has finally caught up.

The Pension Scams Industry Group (PSIG) has carried out a pilot survey on pension scams. The survey has identified seven key findings and concluded that most scams are carried out by rogue advisers and unregulated “introducers”. This is something we write about regularly, so it is great that PSIG has finally caught up.

You may think you can trust a financial adviser, but we live in a world full of scammers and crooks – quite a few of which are financial advisers. Some of them are very greedy and will stop at nothing to fatten their bank balance at your expense. They have no conscience when it comes to living a lavish lifestyle funded from another’s grim fate.

You may think you can trust a financial adviser, but we live in a world full of scammers and crooks – quite a few of which are financial advisers. Some of them are very greedy and will stop at nothing to fatten their bank balance at your expense. They have no conscience when it comes to living a lavish lifestyle funded from another’s grim fate.

THE DIZZEE RASCALS AT THE FCA:

THE DIZZEE RASCALS AT THE FCA: Before Debbie Gupta sticks her big foot in her mouth any further, I would suggest she attempts to learn something about scams, scammers and scamees. She should come and spend a week with me. Sit up until midnight talking distraught victims out of suicide a couple of times. She should go to Port Talbot with Al Rush and talk to some steelworkers and hear their tragic stories for herself.

Before Debbie Gupta sticks her big foot in her mouth any further, I would suggest she attempts to learn something about scams, scammers and scamees. She should come and spend a week with me. Sit up until midnight talking distraught victims out of suicide a couple of times. She should go to Port Talbot with Al Rush and talk to some steelworkers and hear their tragic stories for herself. All the above will save the FCA nearly three quarters of a million pounds a year.

All the above will save the FCA nearly three quarters of a million pounds a year.

Henry Tapper has published an interesting article about the problem of the

Henry Tapper has published an interesting article about the problem of the

When it comes to finance, nothing in life comes for free. These free pension reviews are often followed by

When it comes to finance, nothing in life comes for free. These free pension reviews are often followed by

This week Henry Tapper wrote a blog entitled, “

This week Henry Tapper wrote a blog entitled, “ They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

Just for a laugh, have a look on

Just for a laugh, have a look on

Trustees have the power to block pension transfers if they suspect a scam – they must use it! Now the

Trustees have the power to block pension transfers if they suspect a scam – they must use it! Now the  Predators Stalk Your Pension

Predators Stalk Your Pension In 2015, we went to see the Pensions Regulator to talk about the failings of the Scorpion campaign – as well as the failings of the Regulator. Two Ark victims and I met the then

In 2015, we went to see the Pensions Regulator to talk about the failings of the Scorpion campaign – as well as the failings of the Regulator. Two Ark victims and I met the then

When I grow up, I want to be able to write blogs as eloquently as the Mighty Henry Tapper – the Pension Ploughman with a huge plough which furrows deeply through much of the bullshit on Twitter. He also tolerates Ros Altmann with grace and generosity – which is something I could never do no matter how grown up I get.

When I grow up, I want to be able to write blogs as eloquently as the Mighty Henry Tapper – the Pension Ploughman with a huge plough which furrows deeply through much of the bullshit on Twitter. He also tolerates Ros Altmann with grace and generosity – which is something I could never do no matter how grown up I get.

International Investment has written a jolly good article about the recent action taken by the UAE Insurance Authority – headed up by His Excellency Ibrahim Al Zaabi. I quote from

International Investment has written a jolly good article about the recent action taken by the UAE Insurance Authority – headed up by His Excellency Ibrahim Al Zaabi. I quote from  The Gibraltar FSC

The Gibraltar FSC

Winky accused me of bombarding him with emails (about the Capita Oak scam). I counted them: 16 over an 8-week period. My calculator said that was approximately two per week.

Winky accused me of bombarding him with emails (about the Capita Oak scam). I counted them: 16 over an 8-week period. My calculator said that was approximately two per week.

I had to spell out some words several times as the man’s English seemed to get worse as the agonisingly painful conversation dragged on and on. When I had finished, exhausted and wondering if this was all a bad dream, the man said “OK, hand your documents into the post room”. We duly dropped the bulging envelope into the tiny little room just outside the entrance to the FCA building. I assume it was all shredded as we never even got an acknowledgement.

I had to spell out some words several times as the man’s English seemed to get worse as the agonisingly painful conversation dragged on and on. When I had finished, exhausted and wondering if this was all a bad dream, the man said “OK, hand your documents into the post room”. We duly dropped the bulging envelope into the tiny little room just outside the entrance to the FCA building. I assume it was all shredded as we never even got an acknowledgement.

The illustration on the left is based on the

The illustration on the left is based on the

Having focused very much on bad pension investments, pension scams and how to avoid them, I´d like to talk a bit about PensionBee, a relatively new pension provider.

Having focused very much on bad pension investments, pension scams and how to avoid them, I´d like to talk a bit about PensionBee, a relatively new pension provider.