I don’t often disagree with highly-regarded pensions expert Henry Tapper. Too much respect and awe. But his recent blog: “The Balls of Old Bailey” (about Andrew Bailey) merits a polite argument. It has made me cross – not cross with Henry, per se. But cross with the failure of Britain’s culture, government, regulation and legal system to address justice justly (or at all).

Henry has questioned the point of revisiting the balls-up made by former FCA CEO Andrew Bailey and has suggested that “we need to move on”.

The point of examining Bailey’s sickening catalogue of balls-ups is that we must make sure it never happens again. Part of that mission is to follow the example of the criminal justice system: we don’t give convicted criminals a jolly good talking to – or even a good bollocking. We take away their liberty and put them in prison. This is called a “deterrent”.

What did Old Bailey do that was so bad? The answer is, indeed, a long list – starting with British Steel, Toby Whittaker’s Park First and Neil Woodford’s Fund, and moving on to London Capital & Finance and a long list of other mini-bond scams – including the Blackmore Bond. Bailey should have stopped that entire horrific catalogue of investment fraud if he’d been doing his job properly. He could – and should – have prevented hundreds of thousands of victims from losing their life savings and pensions in all of those investment scams.

The advantage to be had from putting the bollocks – and preferably the head – of Bailey on the block is to send out a warning to future FCA bosses. They all need to understand that they are public servants, and that with huge salaries come huge responsibilities. Current overpaid bosses Nikhil Rathi, Christopher Woolard and Charles Randall must be reminded that running the FCA is a serious public duty – and not just an easy stepping stone to an even bigger and better job (however badly they fail consumers).

Bailey’s numerous failures were rewarded with an eye-watering salary followed by promotion to governor of the Bank of England.

But Bailey’s balls-up is by no means unique. He’s in good company with a whole raft of over-paid public servants who have betrayed the public:

Post Office boss Paula Vennells was awarded a CBE for falsely prosecuting hundreds of innocent Post Office subpostmasters for fraud – even though she knew full well they were innocent. In arguably the biggest scandal of corruption and injustice in British history, Vennells oversaw the wrongful conviction and sometimes imprisonment of 700 victims. Many of these people were financially ruined, lost their homes and committed suicide. One pregnant woman was sent to jail, and many marriages and families were destroyed.

Former HMRC boss Lin Homer was rewarded for her vast catalogue of disasters and failures with another huge salary and a £2.2m pension

Paula Vennells (left), Dave Hartnett (middle), Lin Homer (right)

But to revert to the failings of Andrew Bailey, Henry has suggested that we need to “move on”. However, those who have lost their life savings and pensions because of the FCA’s defects will have great difficulty putting their losses and harrowing ordeals behind them. Living in abject poverty won’t help them forget. They will certainly never forgive the fact that Andrew Bailey could have prevented them becoming victims of investment scams such as mini bonds, Store First, Park First, the Woodford Fund and Blackmore Global etc.

Henry’s blog concludes that Andrew Bailey, as Governor of the Bank of England, has a great deal on his plate: cost of living crisis, looming recession and Brexit. But does anybody seriously think that such a negligent, lazy, incompetent person is capable of dealing with that lot – when he couldn’t even listen to frantic whistleblowers such as Paul Carlier, Mark Taber and Brev at Bond Review who were offering to do his job for him?

This silly twerp got caught looking at lewd images on his mobile in the House of Commons. His excuse was that he thought porn was spelled “tractor”. Parish has now resigned and his political career is almost certainly over. His wife might also be quite cross. He probably won’t be rewarded with a promotion, a CBE or any kind of public “moving on”.

What Parish did was foolish. But he didn’t cost thousands of people their pensions and life savings; he didn’t ruin hundreds of subpostmasters’ lives and send some of them to prison or to their deaths; he didn’t aid and abet hundreds of millions of pounds’ worth of tax evasion; he didn’t overcharge millions of taxpayers or lose their records.

Parish embarrassed himself and was caught doing something unbelievably silly – that hurt nobody except himself (and his own family). But the price he will pay for this will be crippling and may have ruined his life. Meanwhile, Bailey, Vennells, Hartnet and Homer have evaded any kind of sanction and gone on to glittering success, awards and eye-watering pensions.

The following blog was written by Stephen Sefton: a Blackmore Global Victim who cares about pension scams.

Stephen was scammed by David Vilka of Square Mile International Financial Services around six or seven years ago. Vilka, who had neither qualifications nor a license to provide pension or investment advice, arranged the transfer of Mr. Sefton’s substantial final salary pension.

Stephen’s pension was transferred to the Optimus QROPS in Malta.It was placed in an Investors Trust offshore bond in the Cayman Islands. Then it was invested in high-risk, high-commission, unregulated funds. One of these was Blackmore Global.

A determined fight on the part of the tenacious Mr. Sefton did eventually result in the recovery of a large part of his funds. But his case was a rare exception. He was, indeed, very fortunate that he didn’t lose the whole lot. Most victims suffer total loss in such circumstances.

It is now looking very likely that Phillip Nunn and Patrick McCreesh’s Blackmore Global Fund is going to be as worthless as their other investment scam: Blackmore Bond (now in administration).

Pension Scam victim Stephen Sefton writes:

Finally, after two months of radio silence, Angie Brooks once again pens an article. It’s about time!

I care. I don’t know why I should but I do. Maybe because I am seeing a media frenzy over the recent collapse of mini bonds in the UK. Especially LC&F and Blackmore Bonds plc to name just two. Meanwhile, victims of pension scams from the last decade are being forgotten and swept under the carpet. Much to the delight of many of those that oiled the wheels of the scams and helped them to happen – especially the QROPS and SIPPS!

There are many (especially the scammers) that really don’t like me. This is why they tried to offer me a paltry £6000 to silence me. Seriously?

There are many that don’t like my rhetoric and I regularly get blocked on Twitter, or thrown off Facebook. Here, I get to tell it like it is, however unpalatable the truth may be.

What I have learned over the years is that there’s an intricate web, woven around these scams. This interconnects a number of players whose names just keep on cropping up.

Malta was clearly the jurisdiction of choice for many pension scams. It seems to have hundreds, if not thousands, of victims. Many of these are not yet even aware that they face financial ruin in their retirement.

In my opinion, Malta has much to answer for and really should clean up its act. Journalists rarely focus their gaze on the real facilitators of pension scams: the Mickey Mouse jurisdictions that turn a blind eye and allow them on their patch.

Why are they not aware? QROPS Scheme Administrators are sending out fictitious statements implying members’ pensions are still intact. One member of STM Pensions Malta was sent a statement in Sep 2020 showing his pension still intact just one month after STM wrote to members invested in Blackmore Global – Nunn & McCreesh’s offshore unregulated collective – that in fact they (STM) have no idea what the value is!

As it happens, STM did manage to get Nunn & McCreesh to publish the underlying assets for Blackmore Global, in May 2020 (over 6 years since the fund was launched). Even with this list, there is little idea what the fund is worth because the underlying assets are themselves useless, opaque, private ventures in yet more Mickey Mouse jurisdictions. One offshore fund is already being pursued by Dalriada as part of other failed pension schemes from early in the last decade – but Dalriada are getting nowhere with it.

I am not convinced that “The Adams v Carey case is likely to herald a flood of similar claims …”.

Courageous Manita Khuller in front of the Guernsey courthouse

The Ombudsman case that went in favour of Mr. N against the Northumbria Police Authority (PO-12763) in July 2018, was also a landmark case against a negligent UK pension provider that had a tick box culture. The ceding provider transferred Mr. N’s pension without due regard for the Pensions Regulator’s requirements of 2013 for extra due diligence when handling transfers.

That decision doesn’t appear to have “herald[ed] a [likewise] flood of similar claims” three years on.

Firstly, the victims were targeted by scammers because they were “ignorant”. That’s not meant to be derogatory.

They knew diddly squat about pensions, regulations, investments – nothing! They trusted the “adviser” – the con man persuading them to transfer their pension. For a con to be successful you need the essential skill of gaining people’s trust. Scammers have this skill in abundance. The ignorant fall for it every time.

Victims not only knew nothing about pensions and investments, they didn’t even know how to spot they were being conned. They were the perfect mark for scammers. They didn’t know what they didn’t know. Like taking candy from a baby – although a baby knows it is being robbed and often screams quite loudly (so maybe not the best analogy).

Secondly, even if victims have now discovered they have lost their pension, they have absolutely no idea what next to do about it. The ones I have come across are like fish out of water. Completely at a loss of where to go.

On Angie’s facebook group, one person recently told of their father’s loss of pension to Nunn & McCreesh’s Blackmore Global. In an attempt to do “something” the person went to the FCA on behalf of their father only to be told that investing in unregulated funds on the advice of unregulated advisers bars them from the compensation scheme and Ombudsman service. The FCA suggested looking into the Malta compensation scheme – which is a joke! That was the extent of help from the FCA. As useful as a chocolate teapot.

It hadn’t occurred to this person that either the ceding provider is guilty of maladministration for the transfer in the first place, AND/OR the receiving scheme in Malta is in “breach of trust” because it too is bound by legislation controlling its activities.

So the best next step is to pursue one or other side of the transfer – or both.

Manita Khuller went after the receiving trustee through the courts and eventually won. However, such legal action isn’t for the faint hearted. It cost her huge sums of money, which she took out loans to fund. Losing was not an option. On top of already losing her pension. It was a nightmare for her. I know – I was with her every step of the way since 2018 when we were introduced by a journalist. This was her only option because the Mickey Mouse jurisdiction, Guernsey, had no “Ombudsman” service. Moreover, the incestuous nature in Guernsey meant law firms declined to represent her. She had to go it alone for the first trial, adding a layer of stress no person should be subjected to. There are few victims with this determination or courage willing to take this course of action – so they don’t, even though she has paved the way.

We in the UK, at least, have the Ombudsman and now – relatively recently – Malta also has one (the Office of the Arbiter for Financial Services (“OAFS”)).

Guernsey is a backward, biased, Mickey Mouse, incestuous jurisdiction – which is why scammers love it.

The Scheme administrators on both sides of the transfer will fight tooth and nail and argue the victim is wholly to blame for their losses. Many victims just have no idea how to go about presenting their case.

There is no “free” professional service available to help victims navigate this minefield. Mr. N (referenced earlier) paid lawyers £25k to make his case. But the Ombudsman did not award costs – saying that it is not necessary to engage lawyers. However, it is not easy to fight a pension scheme that will employ a top notch law firm to present its defence. So by and large, the victims I have come across are at a serious disadvantage because they have no idea how to seek justice and have nowhere to go and don’t know how to present their case. That’s why they were targeted by scammers in the first place. They were (and still are) easy pickings.

In the article above, Ms. Brooks quoted from the appeal. I will do same. A more appropriate section, §115(i),

“… while consumers can to an extent be expected to bear responsibility for their own decisions, there is a need for regulation, among other things to safeguard consumers from their own folly.”

Members of Staff (in shorts!) from Carey Olsen

These victims are indeed victims of their own folly, but they never realised what they were doing. On both sides of the equation (ceding providers and the receiving schemes) there were duties of care designed to protect these victims “from their own folly”. In all cases I have come across, neither side fulfilled those duties of care. On the UK side there was contempt for the Pensions Regulator’s requirements of 2013, despite growing industry concerns for pension scams. On the receiving side, the QROPS didn’t (and still don’t) care about their members – period. And neither did the authorities in these Mickey Mouse jurisdictions. It was the perfect match and thousands of vulnerable victims are paying the price.

Carey Pensions was started in 2009 by the Carey Group. The Group is controlled in Guernsey by ten partners and ex-partners of the Law Firm Carey Olsen. This is an amusing coincidence in my opinion. Carey Olsen, perhaps the top law firm in Guernsey, represented FNBIT against Manita Khuller – and LOST at appeal by the way.

Justin Caffery floating in the sea while preaching stress relief

Harbour Pensions was started by Justin Caffrey, in 2013 and says in the STM announcement, “Harbour was always a five year plan…”. Justin made his money and now runs meditation classes (seriously?). He should meditate on the misery, caused by Nunn & McCreesh, of hundreds – if not thousands – of vulnerable victims of Blackmore Global that he allowed into his pension scheme, in my opinion, willingly and knowing the consequences of such an unsuitable investment. He permitted 100% allocation of one member’s pension into a fund that has never published audited accounts. At the material time, knowing the fund was opaque and unregulated, Harbour (and other QROPS) were happily permitting transfers and 100% allocations.

The fund’s offer document, which Harbour had, says the investment has a ten year lock-in. That condition, which the QROPS knew and willingly accepted, effectively locked Harbour (and subsequently STM) into an asset they knew nothing about – and still don’t – for ten years, with absolutely no knowledge or control of what Nunn & McCreesh were doing with the money.

The Scheme administrators in these QROPS in Malta were, and still are, completely at the whim of Nunn & McCreesh – who could misappropriate the pensions as they wish and the administrators could do absolutely nothing about it. The QROPS effectively abdicated all powers they had to run the scheme and mitigate risks in the interest of members, to Nunn & McCreesh. They have been passive bystanders to the destruction of their members’ pensions ever since. This is, in my opinion, in breach of the Malta Trust and Trustees Act. They are also willingly and knowingly in breach of trust.

All this really begs the question whether STM go looking for dodgy pension schemes or are they just plain stupid? What on earth is going on and why hasn’t the MFSA taken them to task? They seem to attract scams like flies to a pile of dung.

Blackmore Global Victim who cares about pension scams – says victims are being forgotten

Victims are being forgotten by the media and authorities. Victims had no idea what they were doing or how to seek restitution. They are guilty of nothing but ignorance and ALL the actors in these scams have gotten away with it. They have ALL dipped their hand in the pension pots and kept the spoils – and now moved on, leaving the pension pots empty.

This is frustrating in the extreme because I see no evidence of any “flood of similar claims”. The victims are, for the most part, still ignorant and there is no one “helping” them. This site (Pension Life) once purported to “help” victims but I am not at all convinced it has done much and now has long periods of radio silence. The newbies in this scam space, the journalists claiming to be the heroes that “blew the whistle” or warned the FCA, are just chasing big headlines for their editor on today’s flavour of the month: mini bonds. Soon the mini bond victims will be forgotten just like the victims of Defined Benefit Pension transfers. The blood sucking journalists will move on to the next headline. I have no time for these insincere upstarts because they don’t stay in it for the long haul.

Victims are on their own by and large and still ignorant. No one seems to care and there is no help from any quarter. They face a retirement with a significantly reduced standard of living and that’s the hard truth of the matter. There will be no “flood of similar cases”.

On July 18th 2017, Slater and Gordon Lawyers wrote me the below email. Lawyer Steve Kuncewicz clearly stated that Slater and Gordon acted for their client: Blackmore Global PCC Limited; Phillip Nunn and Patrick McCreesh. The full transcript is below – complete with my comments in bold. This is a 25-page document, so I don’t expect most people (except the most tenacious and determined) to read all of it. So I have put the basic highlights below.

It is clear that Slater and Gordon was a poacher back in July 2017 when the firm represented clients Blackmore, Nunn and McCreesh. And now in 2020, Slater and Gordon, is an even bigger poacher as it attempts to profit from the losses suffered by Blackmore Bond victims.

As Bond Review reported yesterday that the FCA knew all about the doomed Blackmore Bond three years ago, it is clear that Blackmore’s own lawyers – Slater and Gordon – also knew what Nunn and McCreesh were up to at the same time, but did not report their clients to the authorities as they should have done (not that it would have done any good). But both the FCA and Slater and Gordon could have prevented the Blackmore Bond tragedy and saved hundreds of victims from losing their life savings.

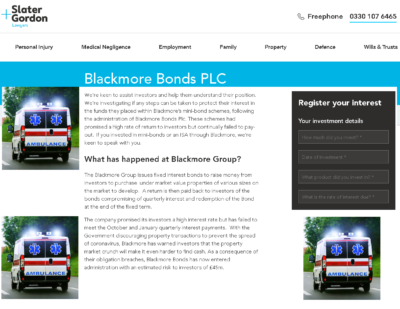

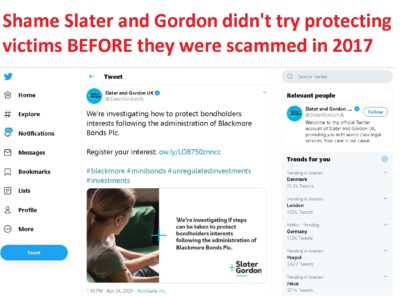

Meanwhile, Slater and Gordon is now advertising all over social media:

We’re investigating how to protect bondholders interests following the administration of Blackmore Bonds Plc.

Slater and Gordon is also denying that Blackmore, Nunn and McCreesh were ever their clients. Slater and Gordon is now trying to attract clients by promising:

“We’re keen to assist investors and help them understand their position. We’re investigating if any steps can be taken to protect their interest in the funds within Blackmore’s mini-bond schemes, following the administration of Blackmore Bonds Plc. These schemes promised a high rate of return to investors but continually failed to pay-out. If you invested in mini-bonds or an ISA through Blackmore, we’re keen to speak with you. “

Although the communication with Slater and Gordon is more about the Blackmore Global Fund scam than the mini-bond, it does cover a number of crucial issues including:

Slater and Gordon confirmed that they acted for their clients: Blackmore, Nunn and McCreesh in both a ” business and personal capacity “

Slater and Gordon was trying to shut me up so that their clients could keep scamming hundreds of victims out of their pensions and life savings

Slater and Gordon was falsely portraying their client as: “a prestigious, multi-asset investment house with over £60 million in assets under management, offering institutional and high net-worth clients access to a wide variety of investment products in order to maximise their returns”. This was completely false as Blackmore only targeted retail investors with small pension pots or personal savings – with their entirely unsuitable, illiquid, high-risk investments

Slater and Gordon claimed: “The Blackmore Group was founded on the core belief of putting the needs of its clients first, developing diverse portfolios backed by real assets containing a blend of capital growth and fixed income”. This is nonsense: Blackmore worked closely with known, serial scammers to promote their products and target naive, vulnerable victims. They locked pension savers into their fund scam for ten years without their knowledge and they spent the bondholders’ money on huge amounts of promotion fees (e.g. Surge Group) and commissions for the scammers who helped distribute their toxic wares.

But most serious of all is this next point:

5. Your only intention can be to divert business from them and to cause serious financial harm as a result.

I replied: “I have no interest in causing your clients financial harm – why would I? But I do think that vulnerable pension savers have a right to know the background of the people behind a fund which is being promoted to retail, UK-resident investors.”

A lot of the Blackmore Bond victims invested AFTER this letter. Slater and Gordon did NOTHING to warn the public about their client. All they did was to try to shut me up and prevent me from warning the public.

And now they want to make money out of the Blackmore Bond victims? Seriously?

Slater

Gordon

Lawyers

18 July 2017

URGENT

— IF YOU DO NOT RESPOND TO THIS CORRESPONDENCE, COURT

PROCEEDINGS MAY BE ISSUED AGAINST YOU WITHOUT FURTHER NOTICE

Ms Brooks t/a

Pension-Life.com

24 Calle Cuatro

Esquinas

Lanjaron

18420,

Granada

SPAIN

58 Mosley Street

Manchester

M2 3HZ

DX 14340

Manchester 1

Tel: 0161 383

3500 Fax: 0161 383 3636

wwwslatergordon.co.uk

Your Contact:

Steve Kuncewicz Assistant: Rebecca Young

Direct Tel:

01613833708

Email:

Steve.Kuncewicz@slatergordon.co.uk

Your Ref:

Our

Ref: RZY03/UM1389098

Our Clients: Blackmore Global PCC Limited, Philip Nunn and Patrick McCreesh Proposed Claim for Defamation and Malicious Falsehood

We act for the aforementioned clients in their business and personal capacity and have been instructed to contact you in relation to various untrue, defamatory and wholly unjustifiable allegations published on your website at httq://pension-life.com (the Website) relating to our clients, their products and services which are designed to (and in fact already have, as set out below) damage their respective reputations and financial interests.

Our client, Blackmore Global PCC Limited, is part of the Blackmore Group which is a prestigious, multi-asset investment house with over £60 million in assets under management, offering institutional and high net-worth clients access to a wide variety of investment products in order to maximise their returns.

If it is indeed true that Blackmore Group is a prestigious organisation, then I have no doubt the directors will be keen to ensure that the damage done to victims’ pensions is put right and that Blackmore’s purported “good name” is protected. However, when you Google Blackmore Group PCC nothing comes up about it being “prestigious” – but what does come up is a link to one of Offshore Alert’s warnings regarding Brian Weal – – and as you know at least one of the underlying assets was run by Weal.

Further, there are cautionary warnings on the Money Saving Expert forum which mentions that investors were given a “pension review” by Aspinal Chase (run by your clients) and promised 10% returns p.a.There is absolutely nothing available on Google which describes Blackmore Global as “prestigious”.

Further, the clients are not high

net-worth, under the FCA definition. Are you aware of the FCA

definition of “High net-worth”? Your clients, with 25 years’

experience, will know this. Just to remind you, a high net-worth

client, according to the FCA has-

an

annual income to

the value of £100,000

or more.

Annual income for these purposes does not include money withdrawn

from pension savings (except where the withdrawals are used directly

for income in retirement).

net assets to

the value of £250,000

or more.

The definition specifically excludes

pension savings. Yet, your clients are involved in the marketing,

processing and investing of retail pensions of those that are not

high net-worth clients. I would be interested to see if ANY

sophisticated or institutional investors are in the Blackmore Global

Funds. Surely, such experienced investors would demand audited

accounts.

“The Blackmore Group was founded on the core belief of putting the needs of its clients first, developing diverse portfolios backed by real assets containing a blend of capital growth and fixed income.” (Steve Kuncewicz of Slater and Gordon – 18.7.2017)

If the assets

are “real” – tell us what they are. Do you even know what they

are? Have you seen an independent audit or are you relying solely on

what your client is telling you?

Blackmore Global

PCC Limited offers a medium to long-term investment vehicle for its

clients with a diversified investment portfolio under one structure

which allocates investment between four distinct protected cells

which diversify assets between property, sustainable energy, private

equity and lifestyle. In order to take advantage of as wide a range

of investments as possible, it invests in a number of vehicles

including funds, companies, joint venture projects and equities.

I know all about

the cells as they are described in the factsheet and brochure.

However, based on the fact that we know some of the information

contained therein is untrue, I am not sure the cell information can

necessarily be relied on. What we really need to know is exactly

what the assets are. Steve, I mean no disrespect but your letter

contains 21,290 words – and not one word about what the assets

really are. You seem to be trying to claim your clients have done

nothing wrong – but you are providing no evidence.

Further, among

those many words, you refer to loss suffered by your clients multiple

times, but you never once refer to the considerable loss and distress

suffered by the Blackmore Global investors (or indeed the Capita Oak

and Henley ones).

Patrick McCreesh

and Philip Nunn founded the Blackmore Group (of which Blackmore

Global PCC forms part) in 2013,

That would be

just after the Capita Oak and Henley scams, which Nunn and McCreesh

were promoting, collapsed.

and jointly have

more than 25 years’ experience in the financial services sector,

growing their business to the extent of it having over £17m of

assets under management across multiple asset classes.

With

respect, if they have jointly more than 25 years’ experience in the

financial services sector, they should know that their fund is not

suitable for pension schemes – just as they should have known that

empty boxes (store pods) were not suitable investments for the Capita

Oak and Henley victims. And

I sincerely hope that (apart from the victims of which I am aware)

none of the remaining £17m represents pension investments.

By contrast, the

Website describes your activities as follows:

“Depending

on the type of pension or investment scam a victim has been involved

in, there are various things we can do to help. We charge annual

membership fees so that members know exactly what they will have to

pay and there will be no legal or accountancy fees on top.

Deal with

trustees, advisers and fund managers

Complain to

regulators and ombudsmen

Appeal tax

liabilities with HMRC and the Tax Tribunals

Analyse and

quantify investments, losses and fees/commissions

Instruct

solicitors to

make

a claim against negligent parties to obtain redress for losses and

liabilities (paid for by litigation funding)”

Am not sure what

the point is that you are trying to make here. You have used the

phrase “by contrast” which to me suggests you are trying to

ascertain that, unlike your clients, I have never been involved in

running or promoting a pension or investment scam. Which, of course,

I haven’t. Indeed, I vigorously oppose such crimes and am working

with the regulators, police and ombudsmen to help stamp out such

activities and bring those responsible to justice.

Notably, you refer

to yourself as “one

of the leading experts on pension liberation scams”.

Indeed, I am

widely acknowledged as such. Further, in your above statements, you

have now correctly identified the following problems associated with

Blackmore Global:

Problem no. 1: the victims were

neither “institutional” nor “high net-worth”. They should

never have had their pensions invested in the Blackmore Global fund

at all.

Problem no.2: you have said Blackmore

develops “diverse portfolios backed by real assets”. So what

are these “real” assets? Do you even know? Has Blackmore ever

told you or shown you proof? Because they won’t tell the victims

what the assets are. Nor will they tell the pension trustees.

Problem no. 3: Blackmore Global

offers a “medium to long-term investment vehicle”. So, not

suitable for pensions then. Members of a pension scheme have a

statutory right to a transfer as well as to be able to reach the age

of 55, or retire or die, so there must be liquidity. Also, at least

one victim was close to retirement age when he entered the scheme so

he should never have been put into long-term investments.

Problem no. 4: Blackmore Global has

£17m worth of assets – if these are all members of pension

schemes such as the victims who are members of the Pension Life

Group Action, then there is a very serious problem indeed for your

clients.

You

refer to my activities and expertise on pension liberation scams –

if you need any clarification or corroboration of this I am sure your

colleague Craig will be happy to fill you in.

The Website

contains a number of posts which refer, either directly or

indirectly, to our clients, specifically:

“Action Fraud

are nobody and have no authority”: John Ferguson, Square Mile

Financial Services: November 30, 2016;

Government

Consultation on Pension and Investment Scams (The Square Mile):

December 5, 2016;

“Scammers Are

Criminals” : April 11, 2017;

“Gambling

With Your Pension”: May 14, 2017;

“Serious

Fraud Office Requests Pension And Investment Scam Reports” :

May 24, 2017; and

“Blackmore

Global Fund — Asset Or Black Hole?”: July 7, 2017

Copies of these

posts are attached to this letter marked Annex 1.

The content of

these various posts (and the content of various other social media

posts and other direct communications with third-party professional

intermediaries who refer work and clients to our clients, which will

be adduced in evidence in due course), led our clients to write to

you on January 17 this year to put you on notice of their objection

to your various claims.

Forgive me, but

I am not sure what point

you are making. Ferguson did indeed write to a victim and state that

“Action Fraud are nobody and have no authority”. He even copied

in his lawyer to this. There was indeed a government consultation on

pension and investment scams. Scammers are indeed criminals (as

confirmed by

the Pensions Regulator). Gambling with your pension is not

advisable. The Serious Fraud Office has indeed requested reports on

a number of pension scams – some of which your clients were

involved with. Finally, we don’t know whether Blackmore Global is

an asset or a black hole because there is no independent audit.

Until and unless the long-awaited audit is forthcoming, the jury will

have to remain out on that.

As our clients

summarised, borne out by the contents of the Website, you purport to

act in a professional capacity for individuals who are beneficiaries

of trusts or pension schemes, who have been advised by independent

financial advisers (including, without limitation, Square Mile, who

are also referred to at various points in the posts referred to

above) to transfer some or all of their existing pension funds to the

Optimus Pension Scheme using an Investor Trust Wrapper.

As I am sure you

will realise, Slater and Gordon already did comprehensive due

diligence on me and the Group Actions several years ago, so there is

no need to “purport” – just ask Craig McAdam.

As our clients

stated, they understand that some of these individuals may have

invested certain of their pension fund assets into underlying

investments which may

include investments managed by our client. As you will be well aware

our client as an investment house has never, nor would they, ever

deal directly with any of your “clients”

as

beneficiaries.

I have never

said Blackmore Global (of which Messrs Nunn and McCreesh are

directors) did deal direct with the investors. However, they do run

a cold calling/lead generation business called Aspinal Chase which

dealt direct with the clients. See below the details of the Aspinal

Chase website:

I am not sure you understand how this

unpleasant, calculated and deliberate targeting of unsophisticated

retail pensions operated. Let me spell it out for you.

Your clients (again I refer to the

individuals – as I they cannot hide behind the corporate entity)

had websites offering pension reviews and cold-called members of the

public. Those that agreed to a review were introduced to what they

believed was an IFA (and IFA has a duty to look at the whole market

and act in the clients’ best interests). The “IFA” then

assessed the client’s needs and objectives and recommended

Blackmore Global. Then, your clients dealt with the processing of the

transfer from the ceding trustees into a pension and their own funds.

At no time was the client ever informed of the conflict of interest.

There was never an intention to provide the client with a pension

review, it was just a calculated ruse by your clients to get their

hands on the pension funds of gullible members of the public.

So effectively,

your clients were generating leads and introducing people to their

own fund via Aspinal Chase.

It is further evidenced that Messrs

Nunn and McCreesh’s firm Pension & Life were acting as pension

transfer administrators for the victims who were subsequently

invested in the Blackmore Global fund:

“Subject – Transfer from: Unisys

Pension Scheme Member name: Mr A B C Driver: Our reference: Transfer

Out – 9999999 Your reference: B00047 We have been advised by Pension

& Life UK Ltd to proceed with the transfer of this member’s

benefits from Unisys Pension Scheme to Optimus Retirement Benefit

Scheme No 1. We can confirm that the member has received appropriate

independent advice in respect of the transfer to the receiving

arrangement. The total transfer value amounts to £4xx,xxx.xx and has

been paid direct to your bank account.”

Please note, that your clients – in

their role as transfer administrators Pension & Life –

confirmed to the ceding provider that Mr. Driver had “received

appropriate independent advice”. However, with their 25 years’

experience Messrs Nunn and McCreesh should have known full well that

the advice had come from a firm which was not regulated for pension

and investment advice.

We now direct our

and your attention (to the extent that you were not fully aware of

their content, which we doubt), to the specific posts on your

Website, and how the same are both untrue and seriously defamatory of

our clients.

I am not sure

what you mean by this statement – how could I not be aware of the

content of the blogs on my website? I wrote them all personally.

Not a single one is untrue.

Below, in

accordance with the Pre-Action Protocol, we set out what we consider

to be the defamatory comments (Defamatory Comments)

“Action Fraud

are nobody and have no authority”: John Ferguson, Square Mile

Financial Services

And what is your

point? John Ferguson wrote this statement. I didn’t write it –

I only quoted it. There is nothing defamatory about repeating this –

it is a clearly evidenced fact.

The above post

contains the following statements:

“Mr.

Ferguson has invested a number of victims’ pensions in the Blackmore

Global and Symphony funds and was asked to provide a copy of the

audit for Blackmore Global which his firm has been promoting and

which appears to have some questionable assets — described as

“esoteric” and “alternative”. He was also asked

to provide evidence of his firm’s regulation to provide pension and

investment advice.”

Again, I am not

sure what your problem is with this – it is perfectly true and

clearly evidenced that Ferguson (and other unregulated advisers) have

indeed invested victims’ pensions in Blackmore Global. The assets

of the fund are indeed questionable – and will remain so until the

audit is produced. The fund is invested in esoteric and alternative

assets. Ferguson has been asked to provide evidence of his firm’s

regulation to provide pension and investment advice on several

occasions but he has never done so.

“One victim

had threatened to report the matter to Action Fraud when he

discovered multiple irregularities with his pension scheme”

Again, this is

perfectly true – and evidenced.

“The

factsheet for the Blackmore Global fund had falsely claimed a firm in

Barcelona was the Investment Manager for the fund — robustly denied

by the furious firm in question.”

And? Both the

factsheet and the brochure stated this – falsely.

Meaning

On any

consideration of the above two paragraphs, this post is intended to

cause damage to Blackmore Global PCC Ltd’s reputation and its

business by suggesting that our client’s underlying assets into which

funds are invested are “questionable”.

The questions

are “where is the audit” and “what are the assets”? There

was no intention to cause damage to anyone’s reputation and

business – but every intention to discover what the assets are.

There is compelling evidence that the assets are linked to very

suspicious investments and people with a track record of dealing in

investment scams. In fact, if you were genuinely interested in

protecting your clients’ reputation and good name, you would simply

send me a statement confirming what the assets are. The very fact

that you haven’t suggests you don’t know and your clients haven’t

told you. So how can you refute that the assets are questionable?

The natural and

ordinary meaning attached to the suggestion that an investment is

“questionable”

is

that it is disreputable, uncertain as to its credibility or validity,

and generally morally suspect. You seek to further compound the

damage to our client’s reputation by describing the assets as

“alternative”

and

“esoteric”.

For a pension

saver, the investment is indeed questionable. And the evidence is

that the assets are alternative and esoteric – and there is nothing

to prove otherwise. If you can prove that the fund is not

disreputable, I will happily apologise. But even if it turns out

that the underlying assets are low-risk, prudent, diverse and

suitable for pensions, the fact that there is a ten-year lock-in

precludes the fund from being suitable for pensions.

Even more

seriously, however, this post makes the most serious of defamatory

allegations in that it alleges that our client is involved in

investments which should be (reported?)

to the police, via Action Fraud, and that our client is therefore

engaged in unlawful, criminal activity.

Your client was

indeed engaged in unlawful, criminal activity in the Capita Oak and

Henley schemes as well as various SIPPS invested in Store First. I

cannot comment further on this because the matter is now in the hands

of the Serious Fraud Office.

Please

be clear that my motive and intention was not to cause damage to

Blackmore Global’s reputation, but to get the victims disinvested

as quickly as possible and further to warn the public that they too

might be in danger of being similarly invested in this fund by

unregulated “Chiringuitos”. The distress caused to the victims

who are invested in Blackmore Global has already been appalling and

as a solicitor you too have a duty to help protect the public.

You

have claimed I intended to cause damage by stating that the fund’s

underlying assets are “questionable”. So what are they? Prove

they are not questionable – of course you can’t, because there is

no audit. The audit was promised last summer, then xmas, then

Easter. Either Grant Thornton can’t find the assets or somebody

doesn’t want the audit made public because of what it will reveal.

You go on to state

that our client has produced Factsheets containing “false

information”. This

is strongly rejected by our client. Our client’s investments, and

their underlying asset classes, are wholly reputable and completely

transparent to investors.

I am sorry but

this is absolute nonsense. The factsheet did contain false

information. The investments and underlying assets are not at all

transparent – there has been no audit and your clients won’t tell

anybody what they are. And to be fair, you keep going on about the

assets, but you won’t say what they are – so you are being just

as opaque as your clients. We know what the asset classes are –

and the explanation of the sub classes are horrendous as they contain

all the usual asset types so beloved by investment scammers (gaming,

spread betting, wine, waste to energy etc.). One victim has written:

“All

I can offer, is to reiterate, that I have no recollection of any

correspondence with an IFA prior to signing up with Harbour Pensions

and Blackmore Global. It was always, Aspinal Chase and in particular

Marc Rees. He told me what a great move it all was, how it made sense

to have all my individual pension funds in one place, that having a

fund of over £250k, I’d get a personal manager that would work

specifically on my fund and keep me regularly updated. Needless to

say this never happened. In addition, Marc told me that investing in

Malta, with Harbour, would give me better returns and be tax

efficient. I took this all as “advice”. Only after a

few years, when I wasn’t getting updates and I had to ask for them,

and I asked him some questions about surrendering, did he say that

was bordering on advice which he wasn’t qualified to answer, and my

IFA, David Vilka, would contact me. He never did. I badgered Harbour

Pensions and got fobbed off. Then Vilka emailed me to say he

understood I was in discussion with Harbour Pension and he couldn’t

do anything more than what I was doing myself.”

Marc Rees- a name familiar to your

clients as he worked for them.

Go

to individuals and click on Previous Involvement…

It is correct to

describe the underlying asset classes as “alternative”

in

that they are not what would otherwise be classified as “mainstream”

investments

such as gilts or shares in publicly listed companies. Investments

into property or renewable energy sources are considered

“alternative”.

However,

the manner in which you seek to adopt this term is to the detriment

of our client by implying that the asset classes themselves are

irregular. An investment is “alternative”

where

it departs from the norm. Therefore, the threshold by which an

investment could be determined as “alternative”

is

low.

You are mixing

apples and oranges: asset classes

are one thing; actual assets are another thing. But again, I come

back to the simple resolution to this debate: provide me with a list

of the underlying assets and then we can put this issue to bed once

and for all. In fact, it is interesting to note that you have never

once stated what the assets are and I have to assume you simply don’t

know as your clients have not disclosed them to you.

I think we should get comment from

professional qualified advisers and actuaries to see if they think

the funds are irregular for retail pensions. I will happily be guided

by them on this matter. Remind me, what qualifications do your

clients hold that would prove they are competent to run such a fund?

We already know one of their colleagues, Brian Weal, was found to be

incompetent.

It is further

correct to describe the investments as being “esoteric,”

that

is, out of the ordinary and traditional model of investments. It is

common for investment portfolios to have an element of “esoteric”

asset

classes, as part of a wider diversification of assets and potentially

offering the higher returns that investors require to achieve their

objectives, based upon the input of independent financial advisers.

However, you seek to adopt this term, which you will be well placed

to understand as being regularly used within the media in a negative

sense, whilst referring to alleged “victims”

of

our client’s allegedly unlawful behaviour, as referred to above. It

is used frequently in a negative sense by the media and other

professionals within the context of financial services, hence why you

have chosen to do so.

I am afraid I

would have to correct you on the assertion that it is common for an

element of esoteric asset classes to be used as part of an investment

portfolio for

pensions.

Perhaps for sophisticated investors or HNW individuals who like a

bit of risk – but not pensions. The term “esoteric” is indeed

frequently used by the media in a negative sense – and there is a

good reason for that: many of the failed funds which have destroyed

victims’ life savings have been invested in esoteric assets.

You cannot possibly believe or claim

that alternative and esoteric assets are suitable for pensions. Why

not provide me with a definitive list of the assets and then we can

debate this properly. You must surely know that funds for pensions

must, by definition, be low-risk, liquid, prudent and diverse –

which Blackmore Global clearly is not.

To clarify the

position in regards to our client’s Factsheet, our client’s

investment manager in relation to the background to which this post

refers was one Gerald Rodriguez, who formerly operated the firm IIG

Financial Services before moving under the banner of Meriden Capital.

Mr. Rodriguez is no longer responsible for the management of this

fund.

I

did indeed state that your client has produced Factsheets containing

“false information”. This is true and clearly evidenced by both

the Blackmore Global factsheet and brochure. Both documents claim

that the Investment Manager for the fund is Meriden Capital Partners

in Barcelona. But the directors of Meriden state they have never

heard of Nunn, McCreesh, Ferguson or Vilka – or indeed Blackmore

Global. However, when I jogged their memory that they had actually

completed an application form to become the Investment Manager, their

English suddenly got worse. But they still insisted they had never

been the Investment Manager to the fund as they were not regulated to

carry out such a task.

Your

explanation about Gerald Rodriguez of IIG Financial Services being

the Investment Manager is, I am afraid, mistaken. I called Mr.

Rodriguez (19th

July) who now works for the Gibraltar International Bank. He

confirmed that he did once work for IIG but that it was many years

ago. He also confirmed that he had never been the investment manager

for Blackmore Global – indeed he had never even heard of it – and

that he had never worked for Meriden Capital Partners. Perhaps you

should ask your clients to conjure up another answer to that one.

2. Government

Consultation on Pension and Investment Scams (The Square Mile)

We direct your

attention to the entire blog posting at Annex 1, and below we set out

the extracts which are most concerning, and defamatory, to our

client.

“Blackmore

Global was full of toxic, illiquid, high-risk assets, had no audit

and as a UCIS (unregulated collective investment scheme) was illegal

to promote to a retail UK investor. The brochure made a fraudulent

claim as to who the investment manager was.”

“The

trouble is, while Mr Driver has fought hard to get some of his money

back, there are around 1,100 other victims stuck in this fund who may

yet have no idea their pensions are invested in —how shall I say

this- worthless crap”

Meaning

This post purports

to discuss alleged pension and/or investment “scams”.

By

including a

reference to our

client within this blog, the clear inference is that our client is

such a

“scammer”, that

is, behaving dishonestly and not in accordance with clear ethical and

regulatory guidelines, and in breach of its obligations (both express

and implied) to its stakeholders. Again, this is a most serious

allegation to make, and is repeated across the post, through repeated

and unjustified allegations that our client is involved in criminal

activity.

Our client,

Blackmore Global PCC Ltd, is an investment company based in the Isle

of Man. It was set up as an unregulated investment company under the

Companies Act 2006, to operate in that jurisdiction.

I am not at all sure what you mean by “unjustified allegations”. It is evidenced on the FCA website that it is illegal to promote UCIS funds to UK retail investors.

You

have kindly confirmed that your client is an unregulated investment

company – and there is no argument about the fact that it has been

promoted by, among others, associates of Nunn and McCreesh: Ferguson

and Vilka, (not regulated to provide investment or pension advice) to

retail, low-risk pension savers. And further, Nunn and McCreesh were

involved in the promotion of a number of pension scams which are now

under investigation by the Serious Fraud Office. What do you have a

problem with?

Your reference to

our client’s investment company being “toxic,

illiquid, (and containing) high risk assets” has

a natural and ordinary meaning that the product is harmful to an

individual’s pension, worthless and of little value as there is no

market within which it can be re-sold. You cannot have underestimated

the significance of calling the product in question “toxic”

to

our client and its reputation. You go on to describe it as being

“worthless

crap”, the

meaning of which we trust we need not set out in correspondence save

to confirm that the use of vulgar abuse does not offset or place into

favourable context your other allegations, as referred to above.

I see no merit

in further debating this point: you are aware of my position on the

assets of the fund but you repeatedly fail to provide any evidence to

prove me wrong. You cannot object to my references, descriptions and

allegations unless you disprove them. Tell me what the assets are,

provide independent

and credible valuations, and disprove what I have written. Your

repeated failure to disclose what the assets are merely serves to

reinforce the point that the fund is opaque and your clients are

failing to be transparent with the victims or the trustees – or,

indeed, you.

We understand that the value of Blackmore

Global PCC Ltd has increased some 11% since its inception.

Exactly how do you “understand”

this? Have you seen an audit? Have you seen the accounts? Have you

got evidence of 11% growth since inception? If you are right, then

11% since 1.5.14 isn’t actually that much at all – a simple

tracker fund would have done just as well, been cheaper, much lower

risk and not had the ten-year lock in. And further, if the fund has

grown, why did Mr Driver get less back than the scammers invested in

the fund in the first place?

We again note that you fail to make any

mention of this fact, which ultimately would not further your evident

intention to damage our client’s reputation and blatant attempt to

self-promote your own “business”.

What fact? Provide the facts.

I genuinely do not understand why

you think my intention is to damage your client’s reputation. What

benefit would that produce for anyone? Nunn and McCreesh do indeed

have a chequered history because of their involvement with Capita

Oak, Henley and multiple SIPPS invested 100% in Store First, but I

wouldn’t have a motive to take the slightest interest in their

reputation. But I would most definitely want to prevent more victims

from having their pensions invested in Blackmore Global – and I am

sure the existing victims would attest to that intention because of

the profound distress they have gone through. But I am not sure how

or why you think commenting on the unsuitability of your clients’

fund does anything to “self-promote” my business.

It is correct that

the product referred to in this post as “illiquid”.

Our

client offers a ten-year close- ended product that is not designed to

be liquid. It is entirely normal for illiquid products to be offered

for investment, where the investment opportunity is designed to be

long-term. In itself, the term illiquid is correct, however the

manner and context in which it is adopted by you, alongside the terms

“toxic”

and

“scam”

is

clearly designed to be harmful to our client’s reputation.

I am beginning

to realise you know little or nothing about investments in general or

investments for pensions in particular. It is also clear you are

relying entirely on what you “understand” from your clients –

and it has been evidenced that some of this is not true. Investors

who specifically want an illiquid investment into which they are

locked for ten years, would have no problem with Blackmore Global.

Or at least, they would have no problem if they knew what the assets

were (which clearly you don’t). Provided the assets were not toxic

or associated with known investment scammers, then a sophisticated,

HNW investor could do his own due diligence and decide for himself.

But illiquid funds are not suitable for pensions.

I would contend

that no one would lock up their funds for 10 years. I have spoken to

a number of Chartered advisers who all have this opinion.

One raised an

extremely good point. Among the spurious reasons that were used to

entice people out of perfectly sound pensions was the promise of

access from the age of 55. Yet, all the people that I have spoken to,

invested in Blackmore, are over 45 years of age. The sales pitch of

55 is meaningless. Of even greater concern is that their whole

pension fund is locked up to 10 years in some cases and this is an

outrage!

What if an

investor were to die within 10 years, how would the family get the

much needed funds? If you have any conscience at all, think about

that.

It is incorrect to

describe the product as “solely

high risk”. As

with any balanced investment portfolio, there will and should be

asset classes within it which fall within the definition of “high

risk”. Overall,

however, the overall apportionment of such “high

risk” assets

is low and, the portfolio in question is balanced.

Without knowing

what the assets are, neither you nor anyone else could make that

statement with any confidence. How can you state that the overall

apportionment of high risk assets is low and the portfolio in

question is balanced if you don’t know what the assets are and have

never seen an audit?

If it is so good, I am sure you have

invested all your own pension savings into the Blackmore Fund. I look

forward to seeing your investment statement.

The sweeping statements you make

regarding suitability, or any purported lack thereof, of our

corporate client’s close ended investment are of serious concern,

especially when made without any objective attempt at justification.

There can be no justification for your assertion that the products in

issue are wholly unsuitable for any pension fund or that its nature

as a 10-year, closed-ended product renders it “worthless

crap”.

If

you are so sure that I am wrong about Blackmore Global, give me the

evidence – and also provide me with evidence that confirms you

yourself have seen and know what the assets are. You cannot argue

that the Blackmore Global fund is not harmful to individuals’

pensions, because one has suffered loss upon redemption already

(£1,663.17)

and others are being

denied their statutory right to transfer out of their schemes because

no reputable pension trustee would accept an in specie transfer in

something so illiquid and with no audit.

I

will be able to get a considerable number of high profile, well-known

and respected advisers to assert that the product is wholly

unsuitable for retail pensions. And, since they were sold in the UK,

why was the commission filched from the funds not disclosed?

You

state that you “understand that the value of Blackmore Global has

increased 11% since inception”. How did you come to that

conclusion? Did you see an audit – or are you taking your clients’

word for it? If your client’s word on the value of the fund is

anything like their word on who the Investment Manager was, I would

think you are making a somewhat shaky assumption.

Blackmore Global

PCC Ltd is not a UCIS.

Yes it is.

Again, the

suggestion that our client “promotes”

itself

to consumers/customers and that such activity is illegal is a most

serious of allegations to make.

Your client

promotes itself to consumers through Aspinal Chase.

The product in

issue is a closed-ended investment and not a UCIS.

It is a UCIS

Furthermore, our

client’s customers are not “retail’

clients.

Instead, they are investment managers, professional pension trustees

or the like rather than investors in their own right.

This is a common

ruse employed by scammers to deflect attention from their negligent

or fraudulent advice or investments – and I am disappointed to see

you using it. You know very well that we are talking about ordinary

people with pensions so please don’t be obscure and opaque.

The trustees I have spoken to have

made it clear that they are not the clients. The investor is the

client and the recommendations for the investment was made to the

individual client. All the money going into the fund is from retail

clients’ pension funds. Of course the customer is a retail client,

it is the retail clients’ money that is invested.

We addressed above the position in

regards to the identity of the investment manager in question,

Yes you did – falsely. Can you

please tell me the truth now?

and again we are

gravely concerned as to your use of the word “fraudulent”

within

your blog.

It was indeed

fraudulent to state that Meriden Capital Partners was the Investment

Manager when it clearly was not. Then, the subsequent “explanation”

about Mr. Rodriguez of IIG being the Investment Manager was also

wholly untrue.

Your

conclusion that this implies “criminal, deceitful and dishonest

conduct seeking to scam people” is perfectly natural. Indeed, if

you would like to call Mr. Gerald Rodriguez at the Gibraltar

International Bank – +350 200 13900 I am sure he will confirm to you

himself that your client is lying. https://www.gibintbank.gi/contact

The natural and

ordinary meaning which our client attributes to it is that it is

involved in criminal, deceitful and dishonest conduct, through which

it seeks to “scam” people of their pensions.

Your client is

indeed involved; has clearly exhibited deceitful and dishonest

conduct, and people have been scammed out of their pensions.

I have explained how the deceit was organized, all verifiable.

Such a description of our client can only

seek to lower its reputation in the eyes of the reasonable reader,

without any exercise in strained construction.

If your client

helps the victims to redeem their Blackmore Global investments

without further delay, there is no reason why their reputation should

not recover. Your clients need to acknowledge that the fund should

never have been used for pensions and put right any loss or damage

suffered by the victims.

Our client is not

involved in the provision of financial advice to consumers/customers.

Its ultimate clients are pension trustees, and it has no direct

communication with underlying beneficiaries. Our client is not in any

way involved in the provision of advice to consumers who go on to

invest. There is no obligation upon our client to have their company

“audited”.

Despite

such, our corporate client has voluntarily sought an audit of its

business by Grant Thornton,

The

fund was indeed promoted to numerous UK residents – illegally. I

have their details and documentary evidence. The clients are not the

investment managers or the trustees – but the investors themselves.

This is a ruse frequently used by scammers to justify investing

clients’ pensions in high-risk, toxic, illiquid – sometimes

professional-investor-only – funds and instruments. Please be

clear, the “advice” was given to the clients – not investment

managers or trustees. This is clearly evidenced and confirmed by the

trustees.

Your

client was involved from the targeting of prospects, through to the

advice process and investment into their own funds.

which remains

underway and to which you refer. The product is administered through

registered regulated custodians and agents, who control all relevant

bank accounts.

And who are

these custodians and agents? The factsheet and brochure state they

are Corporate Options Ltd and OrmCo Ltd. Corporate Options (IoM)

claims to provide the following: company management and

administration; offshore company formation and management; ship and

yacht registration; e-gaming; bookkeeping and accountancy;

intellectual property rights; IoM relocation; services for IoM

businesses and individuals.

Based on these

claims, I see no reason why Corporate Options should not simply

provide a print out of the investments – if indeed they do the

bookkeeping and accountancy for Blackmore Global. How difficult

would it have been for them to simply provide a transaction report to

the victims, trustees, you and me? Instead of making vague,

unsubstantiated claims about the quality of the assets, and refuting

my fears about the toxicity of the fund, you could have simply

provided the evidence instead of demonstrating you have no idea what

the assets are.

OrmCo PLC is

staffed by qualified chartered accountants. So, again, there is no

reason why the accounts for Blackmore Global could not have been

easily produced. In fact, it is becoming more and more ludicrous

(and suspicious) that neither Corporate Options nor OrmCo nor Grant

Thornton nor Blackmore Global has produced a transaction history of

the investments.

We understand from

our clients that your references to Mr Driver are also factually

incorrect. Optimus was the entity who recommended Blackmore Global

PCC Limited, and who contracted with our corporate client, rather

than Mr Driver. Blackmore Global is, once again, a 10-year investment

and contractually there is no right to redeem before the end of that

10-year period. Any early redemption fee that would have applied to

that investment was in fact waived in full by our clients as a

gesture of goodwill, which would usually amount to 7% of the funds

invested.

Optimus was the

trustee, not the adviser. The adviser was Square Mile – a firm in

the Czech Republic which was not regulated for pension or investment

advice. I hope your

clients have made you aware that Mr Driver has this confirmed in

writing by the FCA. Mr.

Driver was not aware that his pension had been invested in a fund

with a 10-year lock in. The early redemption fee was not waived but

eventually refunded retrospectively.

There was no

financial detriment to Mr Driver. Yes

there was. The loss was only relatively small, but there should not

have been any loss – since according to you the fund has grown 11%

since inception. So Mr. Driver not only suffered an actual loss but

also lack of growth for the period his pension was invested in

Blackmore Global.

Additionally, he was advised to

transfer out of a final salary pension with no proper analysis.

Something that would result in a UK FCA registered adviser being

closed down. No doubt the poorly qualified and unregulated adviser

from Square Mile will say that there was no obligation for a non-UK

firm to provide this analysis at the time. However, the movement from

a final salary scheme will have resulted in substantial and, as yet,

unquantifiable detriment. How many others suffered the same fate? On

that note, does your client ensure that the advisers are all properly

qualified to undertake pension transfer activities?

The structures into

which his funds were invested are registered in a variety of

commonly-used and well-regulated financial jurisdictions subject to

appropriate trust and segregation arrangements, and far from the

“scam”,

“toxic fund’ or

“swamp”

to

which you refer. The allegation that our clients’ products are

“toxic”

is

simply the worst description which can be applied to a product in the

investment market, and cannot be justified on any basis, objective or

otherwise.

Given the recent spate of fund

failures in the Isle of Man, I would question the well-regulated

jurisdiction comment.

I absolutely

stand by the terms I used to describe the fund. Indeed, this is

borne out by the description of the cells in the Blackmore Global

documentation:

“Lifestyle

Cell”:

gaming, spread betting, sports events, construction of facilities,

travel solutions, fine wines, art and antiques.

These

are all categories of investments which are typical of the classic

investment scams and are certainly not suitable for pensions.

“Private

Equity Cell”:

venture capital, growth capital and leveraged buyouts.

Very

high risk and entirely unsuitable for pension investments.

“Property

Cell”:

commercial and residential property developments.

Illiquid,

speculative and high risk. Entirely unsuitable for pension

investments.

“Sustainable

Cell”:

renewable energy including biomass, solar, wind, hydro and waste to

energy projects.

Again,

illiquid, speculative and high risk. Entirely unsuitable for pension

investments.

3. Scammers are

Criminals

As the title to

this post suggests, herein you discuss the alleged lack of regulation

and activity taken by regulators and the police to prevent “scams”

and

to sanction those involved in the same. By including our client

within this post, the clear inference is that our client is involved

in fraudulent, criminal and deceptive conduct. You go to list a

number of “failed”

investments

including Capita Oak and Ark, and the implication of such is that our

corporate client is or was involved in those investments or seeking

to promote a similar product.

You need to be

clear about which clients you are referring to. You have three

clients (according to your own letter): 1. Blackmore Global 2.

Phillip Nunn 3. Patrick McCreesh. Blackmore Global is a corporate

entity so cannot of itself “do” or “say” anything – except

those in control of the entity, i.e. Messrs Nunn and McCreesh, can.

Messrs Nunn and McCreesh were involved in the promotion of Capita Oak

and Henley and numerous SIPPS – all of which were 100% invested in

Store First store pods. Store First is subject to a winding up

petition and the entire schemes and all parties involved in the

promotion, distribution and administration of the schemes are subject

to a Serious Fraud Office investigation.

The deceitful conduct of your clients

is clear and detailed above.

“This

so-called Malta-based pension trustee is running the Optimus

Retirement Benefit Scam No. 1 QROPS. it is illegally promoting UCIS

funds to UK residents and these include toxic, illiquid funds such as

Blackmore Global and Richard Reinert’s Symphony.”

A QROPS on its

own is merely a wrapper and on its own is relatively harmless –

except for the fact that should HMRC decide at some point it does not

meet the requirements, it can be removed from the QROPS list without

notice to the members of the scheme. However, it should not have

been promoted to UK residents at all, should not have accepted

transfers from advisers (Square Mile) who were not licensed for

pension advice, should not have allowed investments in entirely

unsuitable UCIS funds such as Blackmore Global – a high risk,

opaque fund with no tradable assets.

QROPS are sold to UK residents, in

these cases, for one reason. To get the funds away from the regulated

jurisdiction of the FCA where UCIS and undisclosed fees are rife. A

real IFA would recommend regulated funds in a UK pension at a

fraction of the cost, with no commissions being taken.

“Optimus

permitted UK residents to be put into a QROPS and then be invested in

Blackmore Global and Symphony UCIS funds: toxic, high risk, illiquid

and volatile. Blackmore Global is run by Nunn McCreesh: one of the

cold calling scammers behind Capita Oak, Henley and other scams

invested 100% in Store First — the promoters are now under

investigation by the Serious Fraud Office and Store First is subject

to five winding-up petitions.”

Correct.

Meaning

Again, you describe

our corporate client’s products as being “toxic,

illiquid funds”. Correct.

We address above

that, whilst it is correct to describe the product as “illiquid”

the

manner and context in which that term is used is designed to be

harmful to our client. My

intention is to warn the public against having their pensions

invested in the fund as it is indeed entirely unsuitable for pension

investments.

The funds are not liquid, hence the

term illiquid.

The product offered

is not worthless or “toxic”

as

you repeatedly seek to describe it as. So

prove it. You keep claiming it is not worthless and toxic, but you

provide no evidence and you clearly don’t even know what the assets

are.

The value of the

product has in fact increased since its inception and, again, is

designed as a long-term investment of 10 years. As

above: prove it.

For the sake of

clarity, Nunn McCreesh was a financial advisory firm established in

around 2008 to 2009 by our clients, Phillip Nunn and Patrick

McCreesh. Nunn McCreesh has been dormant since 2013, and is now wound

up. Both our clients Messrs Nunn and McCreesh were directors of this

firm. It was never involved in “cold

calling”.

Nunn McCreesh

was involved in cold calling and I have several witnesses prepared to

testify to this, and

are looking forward to their chance to do so.

For the sake of

clarity, I will also refer you to the Insolvency Service’s witness

statement dated 27.5.2015:

Documents and information received

from four members of CAPITA OAK indicated they were initially

contacted by Craig Mason or Patrick McCreesh of Nunn McCreesh of Its

Your Pension Ltd and offered pension review services prior to them

being referred to JACKSON FRANCIS or Sycamore for the transfer of

their pension to CAPITA OAK.

On 3.3.15 I received an undated

letter in which it was stated that Its Your Pension had not traded

and was a dormant company and that Nunn McCreesh had traded as an

insurance brokerage between 2009 and 2012 when they entered into a

verbal arrangement with TRANSEURO where in return for providing

pension leads to JACKSON FRANCIS they received a commission from

TRANSEURO.

Nunn McCreesh provided JACKSON

FRANCIS with 100-200 leads per month which were provided by email

and/or telephone for which they received £899,829.86 from TRANSEURO

during the period 26.3.12 to 14.5.14.

As your clients

clearly received a substantial sum of money from the Transeuro scam,

perhaps you would like to suggest they return this money to the

victims to help them with their profound distress, loss of their life

savings and tax liabilities? I am sure this would be much

appreciated and would mitigate some of their inevitably poor

reputation.

Rather, it

generated business through the purchase of leads through reputable

providers such as moneysupermarket.com.

This is a well-known and established practice that many businesses

engage in, and this business was largely an insurance brokerage, also

dealing in wealth management.

This

is also an established practiced used widely by scammers. Nunn

McCreesh only had a license for selling insurance so if it was also

dealing in wealth management, then it was doing so illegally. Also,

Nunn McCreesh was an appointed representative of Sage Financial

Services which had gone into administration by July 2012 – just

before the Capita Oak et al scams were launched.

As

part of that business’ operations, it inevitably generated leads for

mortgages or investments in respect of which it would give

customers/consumers the option to refer to another firm that may be

able to assist them. As

clearly evidenced by the Insolvency Service’s witness statement,

Nunn McCreesh and Its Your Pension were supplying up to 200 leads per

month to Jackson Francis – one of the cold calling scammers

involved in these schemes.

Our clients had no

control over what financial investment advice may have subsequently

been given to customers/consumers, and whether those

customers/consumers then acted upon that advice. Nonsense.

Your clients had already entered into an agreement with Transeuro

regarding the 100% investment of all 1,000+ victims’ pensions into

Store First store pods and would have shared some of the 46%

commission (of £120 million) – 16% of which had been

stolen/defrauded from the victims.

I have already proved your clients

gave the advice (Remember Marc Rees for example?) and they dealt with