Our last blog in this series recreated the offshore pension scam process. We covered the set up and hard sell. The slick salesman prepared the unwitting victim and convinced him his pension would be better off out of the UK.

The silver-tongued spiv, Darren, posing as an adviser, conned his new client with no problem at all. The poor victim was duped into believing he should transfer his pension into a QROPS – an overseas pension scheme. The con worked because the experienced scammer pressed all the right buttons:

Your pension will be looked after better, it will be cheaper to manage, you’ll pay less tax, you won’t lose half of it when you die, you’ll get to choose your own pension investments!

Of course, the scammer, didn’t point out that once out of the UK, John’s pension would have no protection. Complete control of the money would be squandered will now lie in the hands of the unqualified, unlicensed scammers.

The victim, John had stressed:

I’ve paid tax all my life, so I feel I’ve paid my dues. I definitely don’t want to pay too much once I’m retired because every penny is going to count.

But sadly he’s played right into the scammer’s hands. His precious pension will be transferred into a QROPS and then into an insurance death bond:

John: I worked for thirty years to build up that pension and I don’t want anything to happen to it.

Darren: So, let’s look at all the ways you can improve your pension and make sure its protected.

But far, far from improving or protecting the investor’s pension, the scammer has removed the precious retirement fund from the safety of the UK. He’s sent it off to Malta or Gibraltar and then on to the Isle of Man or Guernsey. The money is now well beyond the protection of British regulation or compensation.

John had stressed how he wanted low risk, but has now signed dozens of forms – and this will guarantee that his pension will be exposed to high risk. Darren didn’t give him a chance to read or understand these long and complex forms. And the most important form of all was a blank investment dealing instruction. Once this has been signed by John, the scammer can copy it dozens of times and invest the pension money in whatever pays the highest commission.

The whole point of this scam is for the scammer to make money out of the victim by a whole series of hidden commissions.

Darren: My firm would charge you a small fee for setting up the transfer and then looking after your pension investments moving forwards.

But what will actually happen is that the scammer will openly charge three or four – or more – percent in set-up fees, plus one or two percent a year service charge. But, under the table, he will earn a further 7% hidden commission from the death office – such as Quilter International, Utmost International, RL360 or Friends Provident.

Darren: Right. And then we can start investing your pension and making it grow – so you’ll be able to have a happy and healthy retirement.

John, and all the other victims, will be a long way from being happy or healthy. Because the death office has a platform that the scammer will use to pick the highest-commission investments. So John’s pension fund will be used to line the scammer’s pockets for the next ten years – as he will be stuck in the death bond for that long.

Investments that pay the highest commissions – such as structured notes and unregulated collective investment schemes – are also the highest in terms of risk. John’s pension can now only lose money. And as the value of his hard-earned retirement savings goes down and down, the scammer’s commissions will keep on going up and up.

John, along with all the other victims, will end up losing part – or all – of his pension. He may well lose his home, see his marriage break up, develop depression or a life-threatening illness. He may even take his own life.

But John and his dire poverty will be long forgotten by the slick, silver-tongued scammer. He’ll be busy rubbing his hands with glee at his next batch of victims. Because there’s plenty of them and this form of pension fraud is showing no sign of slowing down any time soon.

I don’t often disagree with highly-regarded pensions expert Henry Tapper. Too much respect and awe. But his recent blog: “The Balls of Old Bailey” (about Andrew Bailey) merits a polite argument. It has made me cross – not cross with Henry, per se. But cross with the failure of Britain’s culture, government, regulation and legal system to address justice justly (or at all).

Henry has questioned the point of revisiting the balls-up made by former FCA CEO Andrew Bailey and has suggested that “we need to move on”.

The point of examining Bailey’s sickening catalogue of balls-ups is that we must make sure it never happens again. Part of that mission is to follow the example of the criminal justice system: we don’t give convicted criminals a jolly good talking to – or even a good bollocking. We take away their liberty and put them in prison. This is called a “deterrent”.

What did Old Bailey do that was so bad? The answer is, indeed, a long list – starting with British Steel, Toby Whittaker’s Park First and Neil Woodford’s Fund, and moving on to London Capital & Finance and a long list of other mini-bond scams – including the Blackmore Bond. Bailey should have stopped that entire horrific catalogue of investment fraud if he’d been doing his job properly. He could – and should – have prevented hundreds of thousands of victims from losing their life savings and pensions in all of those investment scams.

The advantage to be had from putting the bollocks – and preferably the head – of Bailey on the block is to send out a warning to future FCA bosses. They all need to understand that they are public servants, and that with huge salaries come huge responsibilities. Current overpaid bosses Nikhil Rathi, Christopher Woolard and Charles Randall must be reminded that running the FCA is a serious public duty – and not just an easy stepping stone to an even bigger and better job (however badly they fail consumers).

Bailey’s numerous failures were rewarded with an eye-watering salary followed by promotion to governor of the Bank of England.

But Bailey’s balls-up is by no means unique. He’s in good company with a whole raft of over-paid public servants who have betrayed the public:

Post Office boss Paula Vennells was awarded a CBE for falsely prosecuting hundreds of innocent Post Office subpostmasters for fraud – even though she knew full well they were innocent. In arguably the biggest scandal of corruption and injustice in British history, Vennells oversaw the wrongful conviction and sometimes imprisonment of 700 victims. Many of these people were financially ruined, lost their homes and committed suicide. One pregnant woman was sent to jail, and many marriages and families were destroyed.

Former HMRC boss Lin Homer was rewarded for her vast catalogue of disasters and failures with another huge salary and a £2.2m pension

Paula Vennells (left), Dave Hartnett (middle), Lin Homer (right)

But to revert to the failings of Andrew Bailey, Henry has suggested that we need to “move on”. However, those who have lost their life savings and pensions because of the FCA’s defects will have great difficulty putting their losses and harrowing ordeals behind them. Living in abject poverty won’t help them forget. They will certainly never forgive the fact that Andrew Bailey could have prevented them becoming victims of investment scams such as mini bonds, Store First, Park First, the Woodford Fund and Blackmore Global etc.

Henry’s blog concludes that Andrew Bailey, as Governor of the Bank of England, has a great deal on his plate: cost of living crisis, looming recession and Brexit. But does anybody seriously think that such a negligent, lazy, incompetent person is capable of dealing with that lot – when he couldn’t even listen to frantic whistleblowers such as Paul Carlier, Mark Taber and Brev at Bond Review who were offering to do his job for him?

This silly twerp got caught looking at lewd images on his mobile in the House of Commons. His excuse was that he thought porn was spelled “tractor”. Parish has now resigned and his political career is almost certainly over. His wife might also be quite cross. He probably won’t be rewarded with a promotion, a CBE or any kind of public “moving on”.

What Parish did was foolish. But he didn’t cost thousands of people their pensions and life savings; he didn’t ruin hundreds of subpostmasters’ lives and send some of them to prison or to their deaths; he didn’t aid and abet hundreds of millions of pounds’ worth of tax evasion; he didn’t overcharge millions of taxpayers or lose their records.

Parish embarrassed himself and was caught doing something unbelievably silly – that hurt nobody except himself (and his own family). But the price he will pay for this will be crippling and may have ruined his life. Meanwhile, Bailey, Vennells, Hartnet and Homer have evaded any kind of sanction and gone on to glittering success, awards and eye-watering pensions.

On the web of pension scams It seems as though criminal convictions against pension scammers might be getting popular. More than a decade has gone by with virtually none of the usual suspects getting jailed – despite a few criminal investigations (that, so far, have not resulted in convictions). Is the system really that hopeless or do these criminals just know how to work it? Probably, both. But is it getting any better?

Almost all scammers and scams are, in some way, related or connected. If the earliest scammers (circa 2010) had been prosecuted and put behind bars, much of today’s damage could have been prevented.

Now that there is an intricate web of them passing around their tricks of the trade, it’s no wonder they’ve all been able to bypass the laws and regulations.

Two scammers have, however, recently been brought to justice:

Much of the £13m ended up in the hands of well-known scammer David Austin – who committed suicide after being caught in another pension scam (using his daughter Camilla as the “front man”).

Susan Dalton & Alan Barratt

The Barratt and Dalton scheme, was also promoted by Julian Hanson – one of the main promoters of the £27m Ark pension scam in 2010/11. Hanson’s vigorous promotion efforts resulted in £5.5m worth of Ark victims (100 in total). One of Hanson’s co-scammers was the notorious Stephen Ward of Premier Pension Solutions who was the “architect” behind the Ark scheme – along with Andrew Isles of Isles and Storer Accountants. Hanson, Ward and Isles were never prosecuted and so went on to operate and promote millions of pounds’ worth of further pension scams – ruining many thousands more lives.

Ryan Playford

Sue Dalton, after moving on from the Barratt and Dalton scheme, went to work at Continental Wealth Management in Spain – reporting to head scammer Darren Kirby and his partner Jody Smart (who was the sole director of the company). Dalton’s extensive experience in pension scamming made her a hit at CWM. Ironically, Hanson has not been jailed along with Barratt and Dalton.

Playford got 15 years for supplying cocaine and canabis. Clearly a wrong-un, and someone who has no respect for the law or for the wellbeing of people’s lives who would inevitably be ruined by drug abuse.

But what does Playford’s drug conviction have to do with pension scams – you may ask? We have to go back a decade to discover the answer:

In 2008, Playford and an associate – Natasha Beesley – registered a drug company inCyprus:R. P. Med Plant. Presumably, the authorities were convinced that by “drugs”, this meant legitimate drugs for medicinal purposes.

Stephen Ward

In 2012, however, the pension scammers pounced on this Cyprus company as being the ideal sponsoring employer for another one of Stephen Ward’s pension scams: Capita Oak. Ward and his pension-lawyer friend Alan Fowler, used R. P. Med Plant Limited (Cyprus) as the so-called employer for an occupational scheme – registered by HMRC and the Pensions Regulator.

Ward and Fowler forged signatures on a trust deed for their new pension scam, and slightly changed the name of the employer to R. P. Medplant Limited (so that nobody could find it easily on the Cyprus Companies House register). It seems likely that Ward and Fowler must have known Ryan Playford somehow, in order to be able to get their hands on his drug company.

Patrick McCreesh

Capita Oak then became the vehicle for the scamming of 300 victims into investing their entire pensions in Store First store pods. Ward took charge of all the victims’ pension transfers, while another group of scammers took care of the cold calling of thousands of potential victims and signing up of the actual 300 victims.

Capita Oak’s 300 members were not the only victims invested in Store First store pods. There were thousands more in the Henley Retirement Benefits Scheme and various SIPPS including Carey (now Options and owned by STM), as well as Berkeley Burke and Rowanmoor. There have so far been no convictions – other than Playford’s for drug dealing.

This interconnected web of lies and deceit will keep on spreading unless these criminals actually fear the consequences of their actions. Let’s keep the convictions coming and not just save them for drug lords.

The world of pension and investment scams is dominated and driven by commissions on investments (usually unregulated). The scammers’ strategy is always identical: get the pensions away from the safety of a reputable pension provider and into the hands of a SIPP, a SSAS or a QROPS. One purported benefit of these types of schemes is that the member has control over where the funds are invested. This means that the scammers have control over where the funds are invested. These types of schemes are open to abuse by unscrupulous commission hunters whose only mission is to fill their own pockets – at the expense of the victim. Once transferred, the victims’ retirement funds are controlled by the scammers and invested in unsuitable, unregulated investments which pay fat introduction commissions.

It could be argued, however, that not all the investments are necessarily bad. There are some basic rules for pension investments – so let’s take a look at the different types and how they could (or should) fit into a pension portfolio.

Funds. Funds come in all shapes, sizes, flavours and types. As long as the funds are regulated, have a good track record, are appropriate to the risk profile of the individual investor and are competently managed by qualified investment professionals, they can be appropriate for a pension. However, pension scheme members must not be locked into any funds, and the charges must be transparent and affordable. There must not be any hidden commissions, and any one fund should form part of a diverse portfolio.

Bonds. Bonds are term loans with supposed “guaranteed” returns or interest. They are not regulated investment products, so there is no guarantee or protection in the event that they fail (as they often do). Typically, they are sold to victims as being “asset backed” and with unrealistically high returns or interest. They also typically pay high commissions to the scammers who promote them. These should be avoided at all costs as they are entirely unsuitable, risky and illiquid for retail investors – and so many of them are out and out scams.

Structured Notes. These are “derivatives” and are very complex instruments which are only suitable for sophisticated or professional investors. They also pay hefty commissions to the scammers who use them indiscriminately to “churn” their victims’ funds. Churning means investing the same sum of money multiple times in different structured notes to generate the maximum amount of (hidden) commissions. An experienced and sophisticated investor might want to consider having a small part of a pension portfolio invested in structured notes – as long as the commission taken by the “adviser” is low enough (or preferably non-existent).

Property. Residential property cannot form part of a pension’s underlying assets. However, commercial or agricultural land or property is acceptable. The main problem with property, however, is that it is illiquid – so it should only be used with extreme caution as part of a diverse portfolio of well-spread assets. Property also typically attracts high commissions and can frequently be used and abused by scammers. Store pods and car parking spaces fall into this category, along with holiday accommodation, forestry and industrial units.

The key to building a sensible and appropriate portfolio of assets for a pension is to ensure that only a licensed and qualified adviser is used to recommend the investments. Such professionals should only be charging for advice – and should not be earning commission on the investment products which are sold. If an adviser is receiving commission from the investment provider, then he cannot be independent – and should not be giving advice at all.

The key to making sure that the whole pension investment package is in the interests of the investor – rather than purely in the interests of someone posing (often fraudulently) as an adviser – is to look at each stage in the process.

What I mean by the “package” is this:

A. The transfer out of the existing pension scheme should be in the interests of the investor

B. The transfer in to the new pension scheme should be in the interests of the investor

C. The investment of the pension fund should be in the interests of the investor – and not just the adviser (or introducer)

D. There must be no offers of “loans” or “cashback”

The timeline of the past eleven years is littered with sordid and tragic examples of the whole “package” being nothing but a scam. But often this is true even when one of the component parts is legitimate or even harmless. It is the combination of all the elements which can, together, produce a fatal result: loss (to the investor).

In the UK, every pension scheme member has a statutory right to a transfer from one HMRC-registered scheme to another HMRC-registered scheme. However, this can often be a terrible move if it results in the investment of the money falling under the control of a commission-hungry scammer who has no regard for the interests of the victim.

The most risky part of any pension transfer “package” is always the investment. Here are some examples:

Bogus occupational scheme set up by a squad of known, serial scammers with a mythical sponsoring employer (in Cyprus). Promoted and distributed by boiler-room cold callers and “introducers”. 300 victims’ pensions transferred into the Capita Oak scheme, and all £10 million of their funds invested in Store First. The scammers behind the scheme earned up to 46% in commission. The scheme was placed in the hands of Dalriada by the Pension Regulator. Dalriada reported that the investments were worthless and Store First was placed into liquidation in 2019.

Hundreds of victims’ pensions were transferred to the Carey SIPP scheme purely so their funds could be invested in Store First. With the same result as in the Capita Oak scam, victims found that the “guaranteed” returns of 16% did not materialise. This was because the 16% had been paid “accidentally” to the scammers. One such victim – Russell Adams – took his case to the High Court and lost. But the judgement was overturned in the Court of Appeal and Carey must now reinstate his original pension. Other SIPP providers involved were Berkeley Burke, Montpelier (Curtis Banks) and Lifetime (Hartley).

Another bogus occupational scheme – run by the notorious Stephen Ward. 100 victims were scammed out of their pensions for the sole purpose of investing their funds in high-commission, unregulated funds and bonds. Investments included Quantum PYX – a forex trading fund; Dolphin Trust – now in liquidation; Park First Glasgow; Colonial Capital Loan Notes; The Resort Group holiday flats in Cape Verde and The Reforestation Group in Brazil. The scheme was placed in the hands of Dalriada by the Pension Regulator. Dalriada reports that most of the investments are worthless.

A group of known unlicensed scammers – including Square Mile in the Czech Republic – advised hundreds of UK residents to transfer their pensions to this Hong Kong scheme. All the victims had their pensions invested in worthless, high-commission, unregulated funds and bonds such as Blackmore Global, Swan, GRRE, Granite and Christianson Property Capital. The scheme is now being re-registered by the Hong Kong regulator – and the funds are deemed to be worthless.

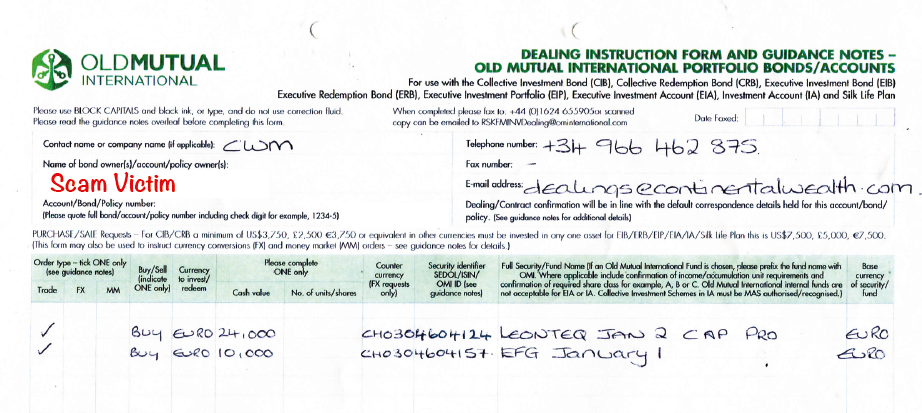

Unlicensed CWM, based on the Costa Blanca in Spain, defrauded 1,000 British expats out of £100 million worth of pensions and life savings. Victims had their funds invested in high-risk (and high-commission) structured notes which were only suitable for professional investors. The clients’ signatures were forged on the investment dealing instructions. Most of the structured notes suffered catastrophic losses, and what little remained of the victims’ funds were further eroded by the high fees on the illegally-sold insurance bonds provided by Quilter, Utmost and SEB. The CWM crew – along with Stephen Ward of Premier Pension Solutions (who signed off all the pension transfers) – are now facing criminal charges of fraud and forgery in Spain.

A pension scheme is a bit like a store pod. It is a container – no different to a cardboard box or shopping trolley. By itself, the scheme (or the pod) is harmless. The harmful ingredient is the greedy, unlicensed introducer or “adviser”. Fill a shopping trolley with unhealthy foods, alcohol and cigarettes and you have a recipe for an untimely death. Fill a store pod with flammable chemicals, and you risk an explosion. Fill a pension scheme with high-risk, high-commission, toxic investments, and you have the perfect recipe for poverty in retirement.

The FCA seems to have woken up. It only took eleven years. Eleven years of laziness, torpor, disinterest and deliberately ignoring the problem. But, completely out of the blue, the FCA has suddenly got bored with crapping on bathroom floors and has decided to do a spot of rather belated regulating.

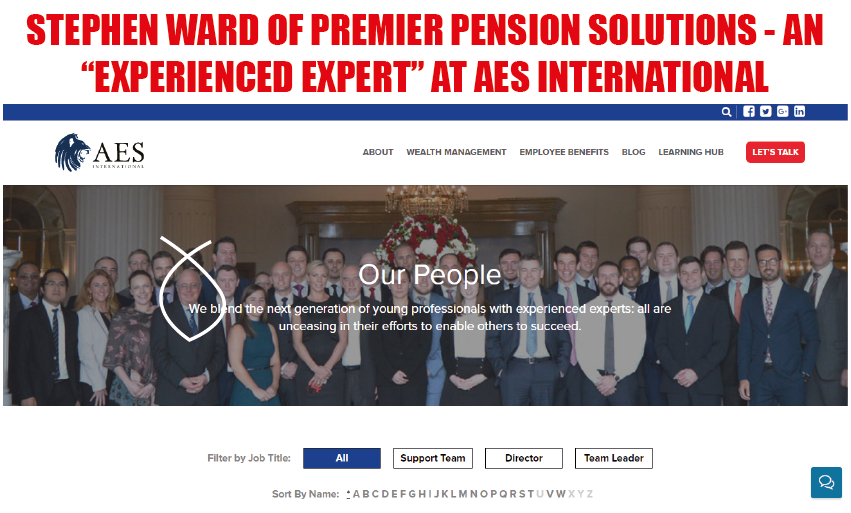

The object of this sudden fit of uncharacteristic activity, is the Ark pension scam. This was operated between 2010 and 2011 by a team of scammers. This team included so-called financial advisers, introducers, a pensions lawyer and an accountant. The principal architect of the six Ark schemes, however, was Stephen Ward of Premier Pension Solutions in Spain. His Spanish firm specialised in (pretty much what it said on the tin) pensions. In particular pension transfers.

Stephen Ward of Premier Pension Solutions

From August 2010, Ward’s company Premier Pension Solutions (PPS) was run as an agent of AES Financial Services – which was regulated by the FSA (now the FCA). Before this, Ward’s company was in the Inter-Alliance network in Cyprus. Coincidentally, the “sister” firm Continental Wealth Management (CWM) was also a member of the Inter-Alliance network. PPS and CWM worked together in close collaboration. CWM often did the cold calling and warm up act for Ward’s various pension scams – including the New Zealand Evergreen liberation scam.

An agency agreement was in place between Ward’s firm PPS and Sam Instone’s firm AES. But the agreement specifically excluded pension transfers. Which was pretty odd, bearing in mind pension transfers were PPS’ main activity. This resulted in Ward’s firm giving victims the false impression that the pension advice he provided was regulated. Which, of course, it wasn’t. The exclusion in the agency agreement between PPS and AES was, naturally, hidden from clients and victims.

Complaints directed at Ward about the various pension scams he had been operating over the years were always firmly rebutted. Ward always claimed that his own activities were the responsibility of AES as the regulated party – and that it was up to Instone to decide what PPS could and couldn’t do.

Kirsten Hastings from International Adviser has published some excerpts from the FCA’s questionnaire about Ark, PPS and AES:

A questionnaire has been sent by the FCA to customers of AES Financial Services (which also traded as International Pension Transfer Specialists (IPTS), Premier Pension Solutions (PPS) and Premier Pension Transfers (PPT).

These clients invested or transferred pensions into schemes managed by Ark Business Consulting and/or the Ark pension schemes.

The questionnaire was sent to consumers to gather more information about their dealings with these firms.

They have until 17 October to respond.

Director of AES Sam Instone told IA: “We are absolutely certain AES Financial Services Ltd has never provided any advice at all in relation to Ark schemes, so it seems like a strange questionnaire.”

Sam Instone seems to have forgotten that AES Spain was run by rogue “adviser” Paul Clarke for some years – after leaving unlicensed firm CWM in 2010. Clarke advised several victims to transfer into Ark. And good old Sam himself advised his own Dad to transfer into Ark. I guess three destroyed pensions – with accompanying tax penalties – can be easy to forget?

Kirsten Hastings goes on to talk about the history of Stephen Ward’s Ark scam:

TPR took action following concerns that the Ark schemes were being used for pension liberation.

According to Dalriada, such schemes generally have high charges and invest money in risky and esoteric vehicles.

They also put members at risk of having to pay large sums of tax.

The latest Dalriada update to members states it is “not able to place a value on any members’ benefits at the time and are therefore unable to make payments to members”.

Kirsten also mentions some further points in the FCA questionnaire:

Kirsten Hastings editor at International Adviser

Did the client (Ark victim) approach the firm or vice versa?

Where was the client based when these services were provided?

Would clients be willing to sign a witness statement?

What regulatory protections was the client told there were?

All Ark victims would certainly be more than happy to sign a witness statement to evidence what Stephen Ward, PPS and AES did, wrote, promised, assured and persuaded.

The regulatory protection, of course, for anyone advised by Stephen Ward’s Premier Pension Solutions (which was most of them) in the Ark scam, was Sam Instone’s AES Financial Services – according to all the documentation.

Ward promoted the Ark £27 million scam during 2010 and 2011 – cases being documented on PPS headed paper announcing that the firm was a “Partner” of AES and regulated through AES. Ward would have earned at least £1 million through the Ark scam – all of which would have been paid through AES.

When Ark went tits up, Ward launched his next pension liberation scam: Evergreen Retirement Benefits QROPS in New Zealand – with his accompanying 50% Marazion “loans”. Again, all advice was given on PPS headed paper announcing that the firm was an AES partner and regulated through AES. This meant another 300 victims lost more than £10 million worth of pensions. It also meant that PPS and AES between them earned at least £1 million from the scam (10% of transfer values). These fees were paid direct to AES.

When Evergreen collapsed (as all PPS pension scams eventually did) in 2012, Ward set up the Capita Oak scam. Another 300 people lost over £10 million – all invested in Store First store pods. Again, all pension transfers were done by Ward. Alongside Capita Oak, Ward carried out all the transfers for Henley (another 250 victims losing £8 million in Store First) and Westminster (another 79 victims losing £3.3 million in other toxic, high-commission investments). All these schemes are currently under investigation by the Serious Fraud Office.

Throughout this era – during which all business done by PPS went through AES – Ward ran multiple, multi-£million pension scams – mostly involving liberation fraud:

Bollington Wood

Capita Oak

Dorrixo Alliance

Endeavour QROPS

Evergreen QROPS

Feldspar

Halkin

Hammerley

Headforte

Henley Retirement Benefits

London Quantum

Southlands

Randwick

Randwick Estates

Southern Star QROPS

Superlife QROPS

The above list comprises QROPS which were used abusively, and bogus occupational schemes.

All these PPS scams resulted in many hundreds more victims losing millions of pounds’ worth of pensions. Many of these unfortunate people were also persuaded by Ward to liberate their pensions, and so they would have faced crippling tax penalties as well.

Ward’s final triumph in his long-running pension scam campaign was London Quantum. He proudly announced this scheme saying that “Ark is history” and that he was now going straight. Still trading as an AES partner and agent, Ward conned 100 victims into the London Quantum scheme. This was invested in the usual high-risk, high-commission and entirely inappropriate assets (including Dolphin Trust loans and car parking spaces at Park First Glasgow). London Quantum ended up being classified by Dalriada Trustees as being “probably worthless”.

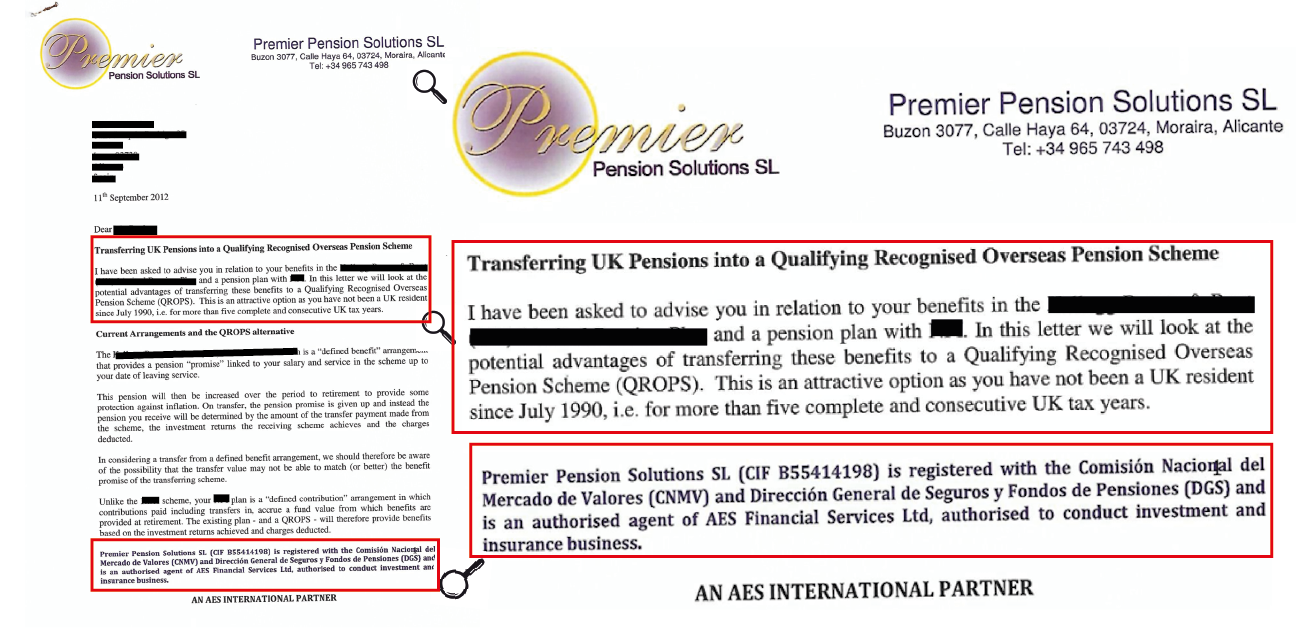

In the Ark Pensions scam, it is clear why so many victims thought PPS was a properly-regulated firm – AS AN AGENT AND “PARTNER” OF AES:

“Premier Pension Solutions SL …..is an authorised agent of AES Financial Services Ltd authorised to conduct investment and insurance business. AN AES INTERNATIONAL PARTNER.“

In the subsequent £100 million Continental Wealth Management pension and investment scam, Ward continued to “advise” hundreds of victims to transfer their precious pensions into the hands of known scammers – in the full knowledge that their pensions would be invested in high-risk, high-commission rubbish funds and structured notes:

But Stephen Ward was a bit more than just an “agent” and “partner” of AES. He was also an integral part of the AES management team – and boasted that he was Director of International Pensions. When all the pension scams finally collapsed, leaving thousands destitute and desperate – as well as hounded by HMRC – Ward and Instone set up IPTS: International Pension Transfer Specialists. This new venture was run from Ward’s office in Moraira – although they tried to hide this by using a PO Box at nearby LettersRUs. And so the misery continued…..

Stephen Ward in the front row of the AES team of “experienced experts”.

I’ve been asked by a number of Park First investors to help them decide how to vote in the forthcoming vote – 25th November 2019.

There are many options and decisions, with communications coming out from various related and interested parties. It is understandable that investors have some difficult choices and are being given conflicting and often confusing information. So I am going to try to put the decision into context to help people to decide.

Putting aside the rights, wrongs and merits for the moment, there are two options that investors have to decide on by the 25th November. But this is just the first of many decisions which will have to be made in the coming months. So here’s a diagram to put it as simply as possible:

Park First investors need to vote for Administration or Liquidation

In a nutshell, if investors vote for the Administration there is a range of options – including liquidation if that is what the investors vote for once the Administration has presented all the facts and figures. And the £33 million set aside (put on the table) by Toby Whittaker will be used to give the Buyback investors their money back. If the investors vote for the Liquidation instead of the Administration on 25th November, the £33 million comes off the table and the Buyback investors will not get their money back.

The liquidation option is being offered by Quantuma and Dow Schofield Watts. If the investors opt for the liquidation choice and reject the administration by Smith & Williamson, the costs will be paid out of the assets which will be sold off to pay the professional fees. The businesses will also probably cease trading.

The administration is currently in place with Smith & Williamson and the costs are being paid for by Toby Whittaker at no cost to the investors.

I have spent a few weeks talking to Quantuma, Smith & Williamson and their solicitors Mishcon de Reya, as well as Park First and their solicitors’ Paul Hastings. I have also spoken to investors and associates of mine who are professionally interested in what is going on. I can see that there are is dilemma for the investors and unfortunately, not a lot of time to make up their minds about which way to vote.

The bottom line is that if investors vote for the administration, they will be offered liquidation as a subsequent option. If they vote for the liquidation, there are no subsequent options. I have encouraged Quantuma to hang back and put forward their liquidation proposal once the administration is further forward and the investors know more about the finances of Park First.

I see a close similarity between the Park First dilemma and the Brexit one. If British citizens had known more about Brexit or Remain, perhaps millions would have voted differently. Many people regretted their first decision because they only found out afterwards how many different versions of Brexit there would be (a wide range of deals, no deal, long-term economic impacts etc). A large proportion of the British population wish they had known more about their options before the referendum. And this is more or less where the Park First investors are.

The vote on Monday 25th November will also decide between two people who will be at the helm: Finbarr O’Connell of Smith & Williamson or Carl Jackson of Quantuma.

Smith & Williamson’s Finbarr O’Connell is a chartered accountant and licensed insolvency practitioner. He is a past president of the Insolvency Practitioners’ Association. He has recently been appointed as administrator to London Capital & Finance. His track record of successful administrations includes gold mines, Ukrainian wheat farms, a nuclear power plant and the Caterham Formula 1 team. Even with my sharpest spade, I haven’t been able to uncover any skeletons in his cupboard.

Quantuma’s Carl Jackson is also a chartered accountant and licensed insolvency practitioner. However, I haven’t been able to find out anything more about his track record except the fact that he was ordered by the ICAEW to pay a fine of £5,000 and costs of £83,557 after he admitted failing to collect £330,000 of creditors’ funds in a liquidation.

The ICAEW Tribunal reported that Jackson failed to collect £330,000 from an agent on behalf of a liquidated company’s creditors and that he hadn’t made a full and proper disclosure to the creditors. The £330k had gone to a bank account in Monaco rather than to Jackson’s solicitors’ bank account. The Tribunal also found that Jackson had not disclosed the full amount recovered from directors; payments remitted to the agent; fees the agent was claiming and seeking to offset against the funds; and the extent of the difficulties in recovering the funds wrongly retained by the agent.

I make no judgement for or against either O’Connell or Jackson and am entirely neutral on this issue. But O’Connell has a long track record of recovering and protecting hundreds of millions of pounds’ worth of creditors’ funds. While Jackson doesn’t.

In the past couple of weeks, I cannot fault the parties for their willingness to communicate and provide information on the proposals moving forward. But when I attended the creditors’ meeting on 1st October, I was struck by the strong feelings of anger and confusion in equal measure. The investors need to see some clarity and they want to understand just two things:

What their investments are worth

What refunds and returns they will get

At the first Park First creditors’ meeting, there was little talk of the intervention by the FCA in the Park First matter – and the role they have played in the uncertainty currently experienced by more than 4,000 investors. I do hope that a thorough investigation of this matter will disclose the FCA’s actions in full. All being well, heads will roll – hopefully the right heads.

One thing the FCA did get right, however, was that it reminded investors that liquidation should always be a LAST RESORT. Liquidation is the equivalent of a “fire sale”. The liquidator gets paid first; then the taxman; then the investors get whatever crumbs are left over. An administration involves all creditors (investors) getting a fair slice of the whole cake. In the FCA’s own words: “It is the administrators’ task to explore whether it is possible to rescue the companies and thereby achieve a better outcome for creditors than liquidation.”

“Best of times. Worst of times. Age of wisdom and foolishness. Epoch of belief and incredulity. Season of light and darkness. Spring of hope; winter of despair.”

You would be forgiven for thinking the above was written about the world of pensions and investments (by someone far more eloquent than me). However, it was written by the mighty Charles Dickens on the subject of the French Revolution in the late 1700s.

There are strong parallels between both events: in the French Revolution, many thousands of lives were destroyed and society broken down in an era when turmoil and terror reigned. Since 2010 in the UK and offshore, a similar breakdown in the stability of society has taken place – with even more lives being destroyed.

Investment abuse.

Investment abuse is one of the biggest causes of darkness and despair in modern times. Thousands of victims are seeing their life savings put at risk every year – the causes range from outright fraud and mis-selling to negligence and greed (on the part of advisers, introducers and promoters). But what makes this abuse even more sinister, is that the FCA does nothing to help. And, even worse, sometimes it does something to hinder.

Regulators in the UK and offshore do nothing to help. But sometimes they do something to hinder. Unnecessarily.

Let’s compare two investments which have been in the spotlight in 2019: MANAGED FUNDS and AIRPORTCAR PARKS.

Citywire’s Bottom Performers Chart for 2019

In the case of the former, the FCA’s track record is appalling – it was slow and did nothing in the case of two funds: Neil Woodford’s Equity Income Fund and Mark Barnett’s Invesco funds. As a result, more than 300,000 investors face suspension of the funds – so they can’t get their money out, and will suffer inevitable heavy losses when they can.

In the case of the latter, the FCA has taken two lots of contradictory actions – it agreed a restructuring of Toby Whittaker’s Park First in 2017, then in 2019 it reneged on the agreement and forced the company into administration. Investors – somewhat understandably – believe that Whittaker has failed to make payments he agreed to make back in 2017. However, in reality it is the FCA which has prevented him from doing so as a result of disruptive and contradictory regulatory action.

Both sets of investments had their own strengths and weaknesses. There’s no such thing as the perfect investment and all investments carry a degree of risk. The problem lay with the promotion of the investments.

In the case of the Woodford Equity Income fund, there was Hargreaves Lansdown promoting it heavily – right up until immediately before the fund was suspended. One Trust Pilot reviewer said: “H and L are always pushing funds (presumably because you get commissions etc) but you were made to look devious over WOODFORD, so I think impartiality has to be addressed with regards to FUNDS”. Another reports liquidity issues: “Fabulous while you are investing with them. But try to get your money out – that’s a different matter. Still waiting for them to transfer my funds after 3 months. The delay is totally unacceptable.” A third reviewer is even more disgusted: “Another Woodford/Lansdown victim left nursing losses due to taking on board their advice. This wasnt just a case of poor performance, this was a former reputable company using its name to push an income fund heavily invested in illiquid stocks up to the point of it folding, a move that has cost investors millions. An untrustworthy company with lots of questions to answer.”

In the case of Park First, there were large numbers of advisers all over the World who advised their clients to put too much of their money into the investment. A more prudent approach would have been to spread the money over a variety of different assets (and avoid the “eggs in one basket” syndrome). It is also clear that these same advisers have often encouraged their clients to blame Park First’s Toby Whittaker for the current uncertainty in the run up to the creditors’ vote for the administration scheduled for 25th November 2019. The reality is that the advisers and the FCA have a lot of blame to shoulder. There’s nothing wrong with the car parks themselves: the planes are still flying (with the exception of Thomas Cook); the passengers are still driving their cars to the airport; the car parks are still doing a roaring trade. And this is set to continue unabated for years to come.

Investors in both the managed investment funds (Woodford and Invesco) are rightly peeved – their investments have not performed well; and they didn’t understand the degrees of liquidity, diversity and risk. It is now a matter of public record that both Woodford and Barnett suffered from the same syndrome: they were legends in their own lunchboxes. They took unacceptable risks – gambling with investors’ life savings; throwing caution and prudence to the winds.

Having successfully strayed into high-risk strategies in the past, they thought they would always be so lucky. But their luck ran out. Now they are having to unload the worst of the illiquid, risky stuff (crap) and are advertising: “Please will somebody (anybody) buy our unlisted shares – we desperately need the cash. We thought they were under valued. Seems we were wrong. Any takers? We’re in a bit of a hurry!”

Not exactly a position of strength from which to bargain. Neither of them will have a future in anything to do with investments other than perhaps serving as a reminder that: “past performance may not be indicative of future results”!

By comparison, Toby Whittaker’s Park First looks a much better bet. The only things that could possibly go wrong are that Glasgow, Gatwick and Luton airports get shut down, or that Elon Musk will invent a Tesla that will drive itself home alone from the airport.

The good thing about Park First is that it is a tangible, known, concrete (tarmac) asset. The car parks exist and are in no way speculative – there’s a proven and growing market for the car parks. There are no bad debts (nobody ever says “sorry I can’t pay – can I have 90 days please?”). Personally, I would never use a Park First airport car park – but only because I don’t have a driving license or a car. And even if I did, I live in Spain.

So, from investment funds and bonds, to airport car parks, the real problem seems to be who promotes them and what the regulator does (or doesn’t do) when it looks like things aren’t going to plan. The FCA first investigated the Woodford fund’s performance three years ago – but took no action (despite clear evidence that Woodford was investing heavily in “hard-to-value, unlisted, illiquid assets”). The most that Andrew Bailey could bring himself to say at the time was that he felt “uncomfortable”.

So no evidence of anything more serious than wearing his Y-fronts back to front.

The Woodford fund is now being liquidated by Link Fund Solutions – and the investors have no say in the future of their investments. It will be a “fire sale” – with the liquidator getting first dibs on the cash. The investors – as is always the case – will be at the back of the queue.

Park First investors are in a better position, as the administrator is Finbarr O’Connell of Smith and Williamson. A licensed insolvency practitioner and chartered accountant, Finbarr has been involved in restructuring and insolvency assignments for the last 33 years and is a past president of the Insolvency Practitioners’ Association. He engaged enthusiastically with investors at the creditors’ meeting in London on 1st October, and will be in the chair again on 25th November. He is offering investors a wide range of options in order to either get their money back or see their investment in safe hands and producing healthy returns.

Finbarr is also joint administrator of London Capital & Finance which has seen 11,600 investors dismayed at the collapsed of this ultra-high-risk “mini bond”. In March 2019, there were four arrests made by the Serious Fraud Office in connection with this case – and the man behind Surge Group (Paul Careless) was also arrested for promoting it. London Capital & Finance shows the extreme end of investing: outright fraud. Neither the Woodford fund nor Park First are – or ever were – frauds. However, they were both undoubtedly widely mis-sold.

While the Woodford investors have no voice in the liquidation of the Woodford fund, at least Park First investors have a vote – and the chance to avoid liquidation.

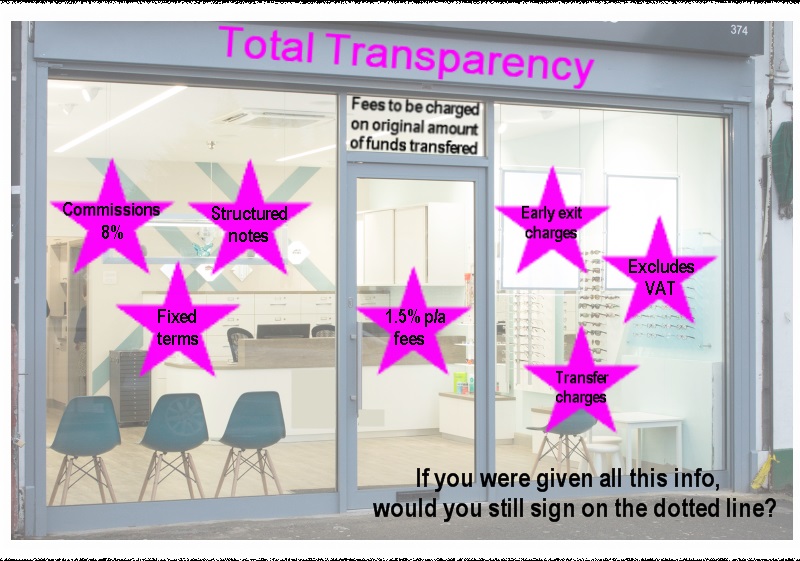

The financial services industry has failed with flyingcolours to achieve transparency – both offshore and in the UK. The single most important thing about any product or service is transparency – aka honesty. This is where the profession has tolerated – and even encouraged – bare-faced lying for years and continues to do so today.

There is nothing intrinsically wrong with overcharging – as long as the overcharger makes it clear he is openly trying to rip his customers off and the victim is consciously happy to be ripped off. Personally, I’d love to be able to sell my car for 25,000 EUR – but with its age, condition and mileage I know I’d struggle to get 5,000. However, a crafty, clever person could give it a makeover, a clockover, tell a few convincing porky pies – and some poor fool might pay over the odds for it.

Most of the victims I deal with tell me the same story:

the adviser said the “review” would be free

the adviser said the only charge I would pay would be 1.5% a year

the adviser said my fund would grow at 8% a year net of charges

the adviser never told me about the insurance bond

the adviser never told me he was going to invest my funds in high-risk, illiquid funds or structured notes

Most people describe their offshore adviser as being about as transparent as a pork chop and the “flying colours” of their achievements to be fifty shades of brown.

Champion campaigner against this sort of dishonesty is international king of transparency Andy Agathangelou – Founding Chair of the Transparency Task Force, the collaborative, campaigning community dedicated to driving up levels of transparency in financial services around the world. Andy writes for Investment Week and calls for total transparency from offshore advisory firms.

One of Andy’s key statements is: “the financial services industry as a whole has a moral, ethical and professional duty to behave transparently”. But I wonder if that is a bit like asking for World peace, an end to pollution, a cure for cancer or a reversal of global warming (and a solution to the Brexit problem).

In the UK, advisers are not allowed to charge commissions on the products they sell, meaning that they will (hopefully) choose the best investment for their client – as there is no financial incentive to chose one product over another. However, offshore advisers do not have these restrictions, meaning that when they are selling an investment they will inevitably choose the one that pays the most commission.

But are things really that squeaky clean in the UK? Does the “beady” eye of the FCA have any effect or is it merely a masking mechanism to cloak lack of transparency (aka lying) in a thin veneer of false security? Henry Tapper’s recent blog on the subject of the FCA’s investigation into 34 firms suspected of non-disclosure of investment charges reports:

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

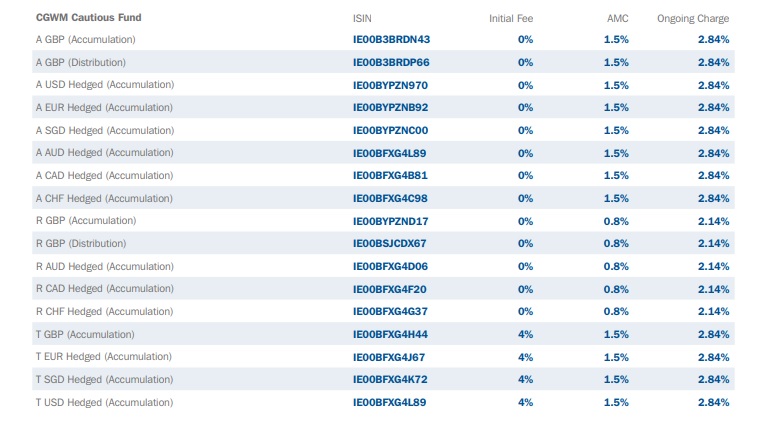

One example was cited: Canaccord Genuity claimed its annual management fee was 1.25% plus a transaction commission of £30. But it turned out the 1.25% was just the beginning – then there were VAT and fund charges bringing the true cost nearer to 2.75%. Now, I know we women sometimes stretch the truth when it comes to our age, weight or clothes size – but Canaccord’s porky pie was that the real charges were actually twice what was claimed. That’s not just lack of transparency – that is naked dishonesty.

I had a browse through Canaccord’s funds and got bewildered by the range of costs – the annual charges seemed to range from 2.1% up to a whopping 4.34%. I’m just wondering whether an investor prepared to pay 4.34% for one of these funds might like to buy my car as well? After all, if they can throw their money away so easily, they surely can’t be bright enough to realise my rusty old heap isn’t worth 25k.

While I was in a browsing mood, I thought I’d have a wee look at Flying Colours. The company aims to provide super low-cost advice and investment funds and “negate the hidden costs in the market”. The website claims “I’m building a network of independent financial advisers with a shared vision – to improve the returns of UK investors. Join us.” But now I’ve got alarm bells ringing: a network? And who exactly is in the network?

A list of firms scattered across England from Bristol and Godalming to Liverpool and Skelmersdale – plus a few one-man bands. But they all claim to be “independent” financial advisers. How can they be independent if they are tied agents of Flying Colours? We are back to the “Wild West” offshore culture where members of a network are effectively “feral” and get up to all sorts of mischief due to lack of independence. And let us not forget that tied agents are illegal in Spain – and for good reason because the Spanish government knows that advisers simply cannot be independent if they are tied to one provider.

The Flying Colours network includes All Things Financial, Arch Financial Planning, CBG Financial Planning, Cullen Wealth Management, E-Crunch, Fit Financial Services, JAV Financial Planning, JBD Financial Planning, JRF Financial Planning, Lavelle Financial Services, Layfield Wealth Management, Mathew Burrows Financial Planning, NTW Financial Planning, Pepperells Wealth, S Fox Wealth Management, Sterling Financial Planning, The Royall Wealth Partnership and Tyrone Peters Financial Planning.

But how on earth does a coherent and effective compliance function work with 18 different firms scattered all across the country? (All of which are lying about their independence).

The Flying Colours website boasts: “We’re transparent about the charges you’ll pay for advice and investments. And there’ll be no hidden fees, ever.” But where are the fees and charges? I searched the whole website but couldn’t find out what they were. Because they were hidden.

Flying Colours recently made an ill-fated, abortive attempt to enter the offshore market (leaving considerable embarrassment and expense in its wake). Far from the claim of “starting strong relationships with a cultural fit and starting friendships“, Flying Colours ended up dumping the failure and retreating to UK-based “DIY” advice. Once Flying Colours’ offshore mess is cleared up, there will – no doubt – be a sigh of relief since Flying Colours was actually offering a more expensive version of the “cheap” investment advice process at 2% for investors with complex investments (so back to the same old, same old offshore “sophisticated” confidence trick).

What is there in Britain to protect consumers from lies; scams; lack of independence and transparency; weak compliance and unworkable investment offerings? Forget the FCA – they are permanently on a coffee break.

But what about the Insolvency Service? Isn’t that there to help protect victims from investment scams? More than a year ago, the IS commenced winding up proceedings against Store First for selling store pods to rogue SIPPS providers such as Berkeley Burke, Carey Pensions, Rowanmoor Pensions, London & Colonial and Stadia Trustees. So, we have thousands of victims of pension and investment fraud all left hanging – not knowing whether their investments are worthless or not. And this, of course, includes the Capita Oak and Henley scheme victims.

The lack of transparency about the store pods was, arguably, not the fault of Store First itself, but caused by the lies of the rogue promoters and “advisers” and the negligence of the SIPPS providers. A store pod is a great investment if the investor has a burning desire to invest in an illiquid, speculative asset – with the added benefit that he can also put his granny’s knick-knacks in there free of charge. While any honest adviser would have told the investors to invest their life savings in a low-cost, liquid, prudent fund – and any competent pension trustee or administrator would have refused to accept store pods as pension investments – the fact is that the backhanders set aside any common sense entirely.

Personally, I think the UK has a long way to go before it can claim to be entirely transparent. To get there, some sort of regulator would be helpful (forget the FCA – obviously) and an effective insolvency service would contribute to achieving meaningful reform. But while firms are still lying, obfuscating and cheating, we can’t really say that pension and investment scams only happen offshore. They are still very much on our doorstep.

Andy Agathangelou’s important work addresses many of the ills which blight offshore financial services. But he could do with a team of several hundred helpers to cover all the key expat jurisdictions. Offshore advisers – as well as UK-based firms – need to be 100% committed to their clients and take into consideration the future of the investments they make. They need to give their clients total transparency, not just on the commissions that will be applied but also on all other fees and charges.

Total transparency on all fees and commissions, before any transfers are made, would mean investors know exactly what they are getting into.The truth, the whole truth and nothing but the truth, is needed from day one! But it would also be exceedingly helpful if ALL UK-based advisers and fund managers adhered to this model.

Going back to Canaccord Genuity’s opacity in the case of a client with a £700k portfolio, their non-disclosure of the VAT charges alone led to an additional cost of £10,500. £10,500 over 10 years amounts to £105,000 – quite a sizable chunk of the fund. You would have to have some very good investments to cover these costs AND increase the amount of the fund. Which, of course, is (or ought to be) the main aim of an investment!

Just for a laugh, have a look on Canaccord´s website at their list of fees, in particular, their cautious fund. 4.34% a year in charges. I wondered if this included VAT (being a “cautious” investor!).

So I decided I´d give them a call, just to clear up the confusion.

I was passed around various departments and ended up talking to a woman, who was – to put it plainly – pretty unhelpful. I asked about the charges and was told I would need to talk to a fund manager. I was asked how much I wanted to invest. I replied I´d need more information before I could commit to an amount. I was told there was a minimum investment of £250,00, but she still couldn´t tell me about the fees and charges.

I was put on hold, after she implied she might find out the answers to my questions. However, she must have forgotten me as no one came back and I was simply left hanging – listening to the sound of silence. Hopefully, Canaccord won’t forget me in the future.

Mind you, I didn’t have much luck with Flying Colours either. I chatted to their online “can I help you?” chap, Stephen Murphy, and asked him what the fund and advisory charges were. Murphy wanted to know why I wanted to know. I explained I was writing an article on Flying Colours’ fees. His reply was: “In regards to you writing an article around fund charges – we are not interested in featuring in an article as you are based in Spain – however, if you need further information around this you could contact Dani Greenfield on dgreenfield@flyingcolourswealth.com – she deals with the marketing side of our business.” Why so secretive I wonder?

Offshore advisers should be forced to put labels like these on their investments!

All this leaves us with a number of pressing, unanswered questions:

Is it acceptable that the financial services industry has failed with flyingcolours?

Is it tolerable that in some ways it is as bad in the UK as it is offshore?

Should consumers continue to tolerate unacceptably high charges from providers?

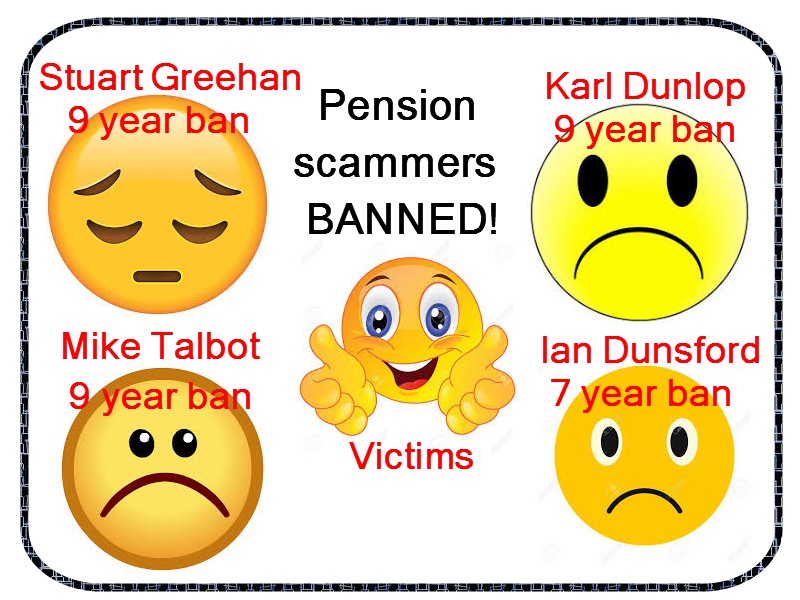

Articles like New Model Adviser’s report on some of the scammers behind the Capita Oak/Henley/Store First scam getting banned always makes me smile. Knowing that a few pension scammers (four in this case), are being named and shamed – as well as banned from being directors – motivates me to share information about these evil scams with the public.

“An investigation led by the Insolvency Service revealed the directors were connected with Transeuro Worldwide Holdings, which helped fund two introducer firms Sycamore Crown and Jackson Francis. The firms were involved in the transfer of £57 million of pension savings.

Sycamore Crown director Stuart Greehan agreed to a nine-year voluntary ban as a result of false and misleading statements to encourage investors to transfer their pensions.

Karl Dunlop, director of Imperial Trustee Services, and Ian Dunsford, director of Omni Trustees, agreed to bans of nine and seven years, respectively, for failing to act in the best interests of members and ‘failing to ensure investments were adequately diverse’.

While not a formally appointed director of Transeuro Worldwide Holdings, Mike Talbot (AKA Stephen Talbot) accepted a nine-year disqualification undertaking for failing to disclose what happened to the millions of pounds of pension assets.”

BUT, IN ADDITION TO THESE EVIL SCAMMERS, THERE WERE OTHER PLAYERS IN THIS APPALLING TRAGEDY AND THEY WERE NOT MENTIONED. SO HERE ARE THE OTHER PEOPLE WHO PLAYED LEADING PARTS IN THIS FOUL PLAY:

Stephen Ward of Premier Pension Solutions SL and Premier Pension Transfers Ltd – he handled the transfer administration from the original (ceding) pension providers. He was, apparently, paid £300 per Capita Oak transfer – and would have known that he was condemning each member to certain loss of his or her pension.

XXXX XXXX of Nationwide Benefit Consultants, The Pension Reporter, Victory Asset Management and Tourbillon, was clearly the “controlling mind” behind Capita Oak. He also ran the Thurlstone loan scheme which paid 5% in cash to the Capita Oak victims as a “bonus” or “thank you”. HMRC is now taxing these payments at 55% as they qualify as unauthorised payments. XXXX XXXX then went on to launch the successful Trafalgar Multi Asset Fund scam which saw over 400 victims lose their pensions to high-risk toxic loans to Dolphin Trust in an STM Fidecs Gibraltar QROPS. XXXX – as with most pension scammers – subsequently ignores the plight of the victims when the schemes eventually and inevitably collapse. XXXX is under investigation by the Serious Fraud Office and was also responsible for the Westminster pension scam.

Mark Manley of Manleys Solicitors – acting for XXXX XXXX.

Stuart Chapman-Clarke, Christopher Payne, Ben Fox, Bill Perkins, Alan Fowler, Karen Burton, Tom Biggar, Sarah Duffell, Jason Holmes, Metis Law Solicitors, Roger Chant, Brian Downs, Phillip Nunn and Patrick McCreesh all played further prominent roles in this series of scams and profited to a greater or lesser degree.

It is believed that cold calling techniques were used to lure unsuspecting victims into this series of unregulated investment scams. Victims’ pension savings were transferred into bogus occupational pension schemes whose trustees/administrators were Omni Trustees and Imperial Trustee Services. The schemes were Henley Retirement Benefit Scheme (HRBS) and Capita Oak Pension Scheme (COPS). But the scammers also used a variety of SIPPS which included Berkeley Burke, Careys Pensions, Rowanmoor, London and Colonial and Stadia Trustees.

As is often the case in scams like these, the victims were lured in with promises of so-called guaranteed high returns by spivs masquerading as advisers, who were also unqualified and unregulated to give financial advice.

The unqualified advisers were able to transfer millions of pounds’ worth of pension savings into these schemes which included investments in unregulated storage units and over £10 million into COPS (Capita Oak) and over £8 million into HRBS (Henley). The promised high returns were never paid to the investors – but handed over to the scammers instead. The pension funds are now suspended with the funds trapped in these illiquid investments.

The company directors have received a total ban of 34 years collectively. Here at Pension Life we would have liked to have seen lifetime bans all round.

The Serious Fraud Office (SFO) is now moving forward with their investigations against Omni and Imperial. They urge people who are members of HRBS (Henley) and COPS (Capita Oak) to contribute to criminal evidence against the scammers via a questionnaire.

As always, the team at Pension Life urges pension holders to be wary of pension scammers. Never accept a cold call offer, be aware that scammers lurk everywhere and if it seems to good to be true it probably is!

Katar Investments say they give UK and overseas investment advice in a simple way. However, the types of investment opportunities they are offering are, unfortunately, once again, making my red beacon flash. So, with Déjà vu, let me tell you why. Please make sure you are comfy, this might take a while!

Firstly, I had a quick look into their team. In my opinion, you would hope that some of the people advertising about giving you advice on investments would hold some sort of financial qualification. However, out of the five team members listed only one mentions a background in finance, the others only list sales experience.

I had a quick check on the registers to see if the one team member who states she has 10 years´ experience in the financial sector, holds any qualifications with the CII, CISI etc. – she did not appear to have any registered financial qualifications.

Now, forgive me if I am slightly biased and ever so critical when it comes to firms giving investment advice, but I would hope that any firm giving me advice on what to invest in, would have a team of fully qualified financial advisers. Not just sales experts. Or am I just being fussy?

Katar Investments state:

“Whether you are looking for a steady income investment, a property investment with high capital growth and a quick turn around of your capital or an opportunity in the latest emerging market, we have something to offer you.

We are highly committed to our investors and are focussed (their spelling mistake – not mine) on delivering a level of customer service which is above and beyond. So rest assured our agents will strive to provide you a class A service when you Invest with Katar Investments.”

I feel that the salespeople who work for Katar Investments may well be driven solely by earning high commissions when it comes to offering class A services. But, again, maybe I am biased! Let’s move on to what investments they offer.

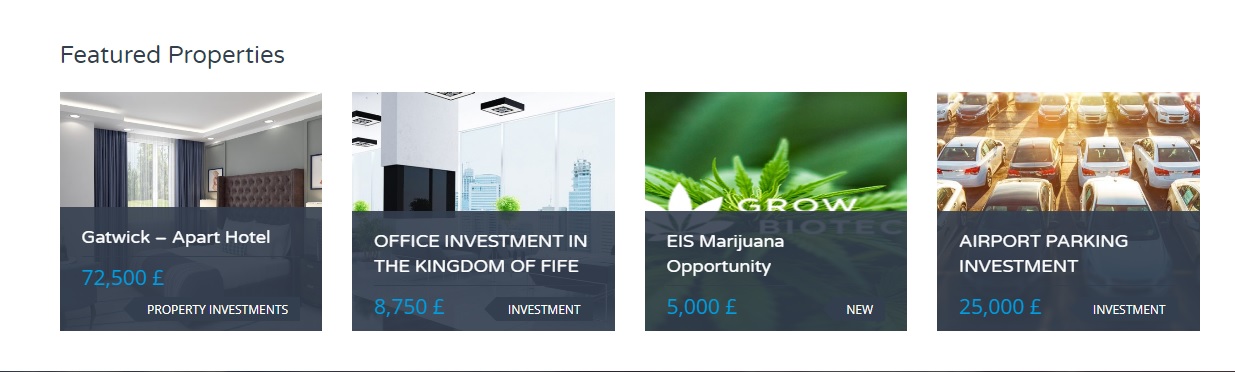

Gatwick – Apart Hotel – This is a serviced apartment/Hotel investment with a minimum investment of 72,500 GBP. The figure states “from”, so I assume you can throw a bit more in for good measure. The promised outcomes:

12 Months rental paid in advance

Rental protected by Insurance

5 Years Rental 8%

2% profit paid on exchange deposit during refurbishment

7 days free stay subject to 1 months notice

Buy back at 110% after 10 years

40% Finance on units over £140,000

Luxury furniture pack included with every purchase

Completion date: March 2019

This is a fixed term investment of 10 years and it has not been built yet (check the completion date). To me, an investment like this would ring alarm bells, as you are purchasing property that has yet to be completed. All sorts of hiccups could occur before the investment was up and running. An illiquid, high-risk investment, only for those who can afford a potential loss on the funds used.

This means your money is trapped for an awfully long time. If the market sways, you could be set for a loss and often with fixed-term structured investments there are fees and charges. Investments like this can, if they go wrong, result in you, the investor, falling into negative equity.

EIS marijuana opportunity – Grow Biotec, there is a lot of press going around at the moment into the medical uses of marijuana and possibilities of a change in legislation in the UK. In many states of America, the use of marijuana for medical use has been decriminalized. As an avid supporter of natural remedies and healing through nature, the use of CBD extracted from the marijuana plant interests me immensely, the idea of investing in this potentially lifesaving product does have a certain draw.

But, there is always a but! Since working for Pension Life, any investment opportunity that quotes the word ´bio´ gives me the heebie-jeebies. We have only to look back and remember the Elysian Bio Fuels liberation scam promoted by James Hay. The victims of this scam have been left penniless AND with huge tax bills from HMRC.

Another ´bio´investment disaster was Sustainable Agroenergy (SAE) Plc, investors were told their investments were in biofuel products, that land was owned in Cambodia and planted with Jatropha trees – a tree with highly toxic fruit that could be used to produce biofuel. Unfortunately, the Jatropa trees were not as fruitful as originally thought. The perpetrators, were thankfully convicted of fraud and bribery offenses.

The reasons I doubt this as a good investment are the vague promises and the over promises.

´It is a private offer raising £5 million to develop one of the world’s most valuable portfolios of cannabis-IP assets by 2022.´

What will be the outcome should this £5 million not be made? A possibility of loss of all or part of your investment.

´We are seeking to develop one of the world’s most valuable portfolios of cannabis-IP assets by 2022.´

Meaning this is a fixed-term investment, with potentially no return for at least 4 years, if not longer, AND only if successful.

Projected high returns: Target return of £50 per £1 invested (not guaranteed)

EIS Tax relief: up to 50% income tax and capital gains tax relief. Remember tax rules can change and benefits depend on circumstances.

If it sounds too good to be true – it probably is. Plus this figure is not guaranteed and seems to me like it was just plucked out of the sky, nice and high, to lure investors in.

These investments are what we in the industry call illiquid. Once your money is in, then it´s pretty hard to get it out quick AND unless the venture does well there will be no return. With regards to pension investments, these are the very worst, toxic assets to invest in.

Unfortunately, they are often the assets which pay handsome investment introduction commissions to the salesperson, and this is why serial scammers, like Ward, love them. They go in with the ´eco-bio´ sale pitch or the glamorous property ownership – withholding the high-risk, fixed-term rules surrounding the investment.

A pension fund is a retail investment that should be placed in a low to medium-risk asset. Fixed terms, high-risk and illiquid investments should be avoided at all costs.

The types of investments offered by Katar Investments are high-risk and illiquid, if you have a spare five grand that you can afford to lose, then go for it: have a cheeky punt on Bio Grow. You may be pleasantly surprised and get the target return of £50 per £1 invested (just remember to duck smartly when those pink things with curly tails fly a bit too close!). However, if your money is dear to you and you cannot afford to lose it, please stay away from shiny pink and green investments like this.

When it comes to your precious pension fund it is always best to air on the side of caution and go for the safe bet. It might not pay the highest interest, however, slow and steady wins the race. Meaning you will be able to enjoy your hard earned pennies in your retirement – stress free.

The BSPS dilemma for steelworkers is clearly difficult with very little time to consider options and make a wise decision which will affect them for the rest of their lives.

There’s a whole team of willing voluntary professional advisers trying to provide some guidance to help people avoid making the wrong decision. This team includes eminent pensions experts including Henry Tapper (The Pension Ploughman), Al Rush, Darren Cooke and many more.

I’d like to contribute to this excellent initiative to help the scheme members – but I can’t advise how to do things right; I can only advise how not to do things wrong.

Henry Tapper, Al Rush and Darren Cooke – plus other qualified, licensed advisers generously giving their time to help the BSPS members – will give sound guidance as to the right decision to make. The Pensions Advisory Service will also help.

Here are some pointers from me – someone who represents hundreds of victims of pensions scams and has seen all the tricks, lies, false promises and smoke/mirrors in the pension scamming business.

Check that a proper adviser is licensed – in other words: regulated. You can check this out on the FCA register. Here is an example: check out Darren Cooke’s firm, Red Circle. You will see that his firm is regulated (or licensed by the FCA – Financial Conduct Authority) to carry out personal pension and stakeholder pension advice. Remember, unregulated means SNAKE OIL SALESMAN. And beware the “introducer” – which is another word for snake oil salesman. If you find the so-called adviser is not regulated – run like hell!

Beware “free” financial advice. Go to Tesco and ask if they have any free milk. Go to the Post Office and ask if there are any free stamps. Go to an accountant and ask if he will do your accounts for free. Go to your local car dealer and ask if there are any free cars. There ain’t no such thing as free. Everything has to be paid for – but make sure that all the charges, fees, commissions etc., are openly declared. If someone promises you free financial advice – run like hell!

Run a mile from “get rich quick” investment schemes. Your pension has to be invested in boring, safe, traditional assets which will grow steadily and safely. If you are offered something exciting and sexy – like eucalyptus plantations; car parks; football betting; overseas property “opportunities” and truffle trees – run like hell. If you are told that your pension will get “guaranteed returns” of 8%, 10% or 12% – run like hell!

If you are told you can have some cash out of your pension other than your 25% tax free at age 55 – or the rest at the marginal tax rate – run like hell!

If you are cold called – run like hell!

Remember, you are a sitting duck – and it is open season. Also remember, the good guys like Henry Tapper, Darren Cooke and Al Rush – as well as all the other decent, honourable, ethical advisers who are volunteering their time free to help you avoid the scammers – can give you some invaluable, generic guidance. But someone who is offering to transfer your pension into another scheme is giving you advice.

So what is the difference between actual advice and general guidance? Let us take the example of a medical practitioner: you know a doctor – say a GP – at your local tennis club. You are concerned about your health in general and the fact that you are putting on weight and get breathless going upstairs. The doctor might suggest – as in suggest – that you consider going on a diet and taking some exercise, but that you also consult your GP. That is an informal and friendly (as well as well-meaning and common sense) suggestion. But it does not constitute formal advice. A specialist would look for deeper issues such as blood pressure, signs of diabetes and any other underlying conditions to be investigated – and would prescribe specific treatment.

If all else fails, drop me an email and I will try to help: angiebrooks@pension-life.com – but meanwhile, please buy some good running shoes!

Meanwhile, take a look at just a few of the schemes for which Pension Life is representing groups of victims who have lost their life savings to the same – or very similar – scammers who will inevitably be targeting you now:

Pension and investment scams and scandals are a blight on financial services and saving for retirement. The energetic and inspired campaign by Darren Cooke of Red Circle successfully raised awareness of the problems of cold calling. But the snap general election scuppered serious traction on this and the most the government has achieved so far is to make a vague promise to talk about talking about it. But still it is not illegal, and still the scammers are scamming away merrily.

Chair of The Transparency Task Force

The Scams and Scandals team was formed as a result of inspiration by the Transparency Task Force’s Andy Agathangelou. It has attracted a group of like-minded professionals who believe passionately that a concerted effort should go into coordinating a zero-tolerance approach to scams and scandals. All members of the team are committed to producing a White Paper which can focus the minds of government ministers, regulators and law enforcement agencies on the whole problem – not just the cold calling bit.

Irrespective of which version of which political party we are talking about, the ultimate object of a successful and fulfilled life is to be happy, healthy and solvent. And this includes getting a decent education, leading a responsible and law-abiding life, and saving for a comfortable retirement. Millions of British citizens manage to achieve this goal, but sadly many thousands of them lose part of all of their retirement savings to the armies of scammers.

XXXX XXXX, one of the many pension scammers ruining thousands of victims’ lives

All these scams and scammers have caused thousands of victims to lose hundreds of millions of pounds’ worth of retirement savings. And caused untold misery – in many cases exacerbated by HMRC punishing the victims rather than the perpetrators.

The Scams and Scandals Team has a clear five-point goal:

Ban UK cold calling and fraudulent calling

We must not let this disappear off the agenda and must keep up pressure on MPs and Ministers – as well as the regulators. But this must also be extended to overseas as we already know that the UK-based cold calling outfits have made arrangements to move their operations or merely facilitate re-routing of phone numbers. However, the twilight industry of “introducing” must also be examined as this is a serious source of scam facilitation.

Support Lesley Titcomb “Scammers are Criminals”

Ms Titcomb has publicly declared scammers to be criminals

We must work with the regulators, government and law enforcement agencies to enhance existing and introduce new regulation and legislation to prevent new scams, close down known existing scams and bring those involved in conceiving, operating and promoting both to account.

Revitalise Scorpion Campaign

Fundamental to preventing scams is communication to the public of the dangers of cold calls and pension/investment scams which would include the Scorpion Campaign – but so much more as well. A key part of this exercise is the use of social media and the plan to produce a documentary and Youtube channel giving real-life examples of past and current scams. Explaining the mechanics of a scam is one thing – but showing an actual example of a victim and the scammer is bound to have even greater impact.

Write off HMRC debt where scams are proven

HMRC celebrating the tax they collect from victims of pension liberation fraud

We need the help of the government here and could do with an actuary to help us work out what the cost to the State is of taxing victims of scams. If we can demonstrate that by ruining a scam victim (who has already probably lost part or all of his pension) with the tax charge, the long-term cost of supporting the victim and his family will far outstrip the tax collected. This is especially well demonstrated in the Ark case where the victims have got to both repay the “loans” and pay the 55% tax even if the loans are repaid.

Ensure AML regs include pension scamming

TOBY WHITTAKER’S TOXIC EMPIRE WILL FINALLY BE HUFFED AND PUFFED AWAY

I would widen this to include investment scams. This is because at the heart of every pension scam there is a fraudulent investment (and/or loan). The actual pension itself is harmless as it is essentially just a box with a label on it and only becomes toxic and dangerous once you put the scorpions, snakes and cockroaches inside it. You could equally put fluffy kittens in it. It is the mis-use of the pension “box” which is the scam.

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

Just for a laugh, have a look on

Just for a laugh, have a look on

Stephen Ward of Premier Pension Solutions SL and Premier Pension Transfers Ltd

Stephen Ward of Premier Pension Solutions SL and Premier Pension Transfers Ltd Mark Manley of Manleys Solicitors – acting for XXXX XXXX.