Spain is, sadly, the World’s capital of wealth scamming. For more than a decade, wealth planning has been perverted and converted into a commission-laden fraud. This financial crime has relieved thousands of victims of their pensions and life savings.

Originally a private Swiss bank, Julius Baer now wants to diversify into the Spanish wealth market. Hopefully, this is very good news. To date, Spain has been dominated by the dross of the commission churning machine. Some genuine, professional, qualified, fee-based financial advice in Spain would be welcome and also essential to clean up this crime-ridden territory.

Julius Baer has created a new team which includes Claudio Beretta and Claudia Linares. So just to give them a few friendly, helpful tips, here’s my message to them – which I hope they will accept in the spirit in which it is given.

If this newcomer to the Spanish market can bring proper fee-based financial advice to British expats in Spain, Julius Baer could change financial services the World over. The absurdly-stupid EU regulator: ESMA allows firms with only an insurance-mediation license to provide investment advice on portfolios held within insurance bonds. This, of course, facilitates most of the financial crime in Spain and the rest of Europe.

This widespread fraud – encouraged and handsomely rewarded by the death offices – oils the wheels of the illegal commission machine. These freely-spinning wheels result in herds of unqualified “advisers” (including drug addicts, convicted killers, prostitutes and fraudsters) conning thousands of victims out of their pensions.

This team is looking to provide services in the fields of wealth planning and wealth management. Julius Baer reports this constitutes;

“the overall Bank’s strategic conviction to further strengthen their presence in Western Europe and particularly in Spain.”

Hopefully, Julius Baer will avoid death offices and unlicensed spivs. And, even more essential to the fraud-saturated Spanish market, Julius Baer must make it clear there will be no secret or half-secret commissions involved – and concentrate purely on proper fee-based advice which is qualified and truly independent.

This Cayman Islands-based fund is being liquidated and it is uncertain whether there will be any recovery for the victims whose pensions were invested in it.

Nearly 250 STM Fidecs QROPS members stand to lose £25 million.

Given the uncertainty of recovery by the liquidator, we felt it was essential to issue proceedings so that the victims’ interests would be protected.

STM Fidecs – a QROPS provider in Gibraltar – has issued the following update to the Trafalgar Multi Asset victims:

“Following an investigation into the status of the Fund’s investments, the Company’s directors determined that it would be in the best interests of the Shareholders to wind down the Fund and to focus on the recovery of assets and the distribution of such assets to those entitled to have recourse.”

STM Fidecs appointed Stephen Doran of Doran + Minehane as liquidator.

The update issued by STM Fidecs has given victims very limited information relating to the current status of the liquidation of the fund or the prospects of recovery. However, it has made it clear that there was “misappropriation of funds” and that there were investigations ongoing.

STM Fidecs has stated that it has recently commenced litigation against “various parties” and a claim has been issued against thirteen defendants in respect of misappropriated monies.

Whether the guilty parties will be brought to justice, or whether there will be any money left over for the victims after the the liquidator has been paid in full, remains to be seen.

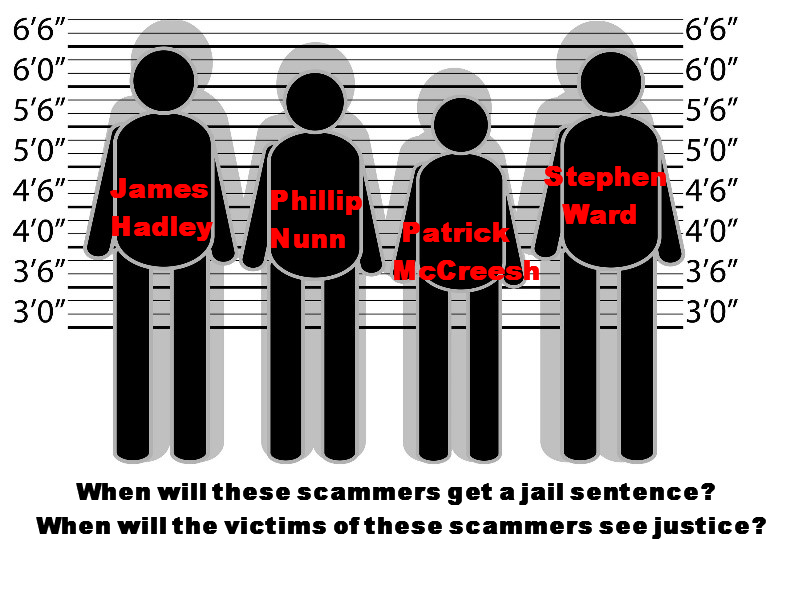

It is well known that the Trafalgar Multi Asset scam has been under investigation by the Serious Fraud Office. This was announced by the SFO on 22 May 2017. Other schemes promoted by the same team of scammers included the Capita Oak and Henley pension scams which were promoted by Sycamore Crown Ltd, Jackson Francis Ltd, Portia Financial and Nunn McCreesh.

It is also known that the same scammers who were promoting Capita Oak, Henley and Trafalgar Multi Asset Fund were also promoting the Blackmore Global Fund run by Phillip Nunn and Patrick McCreesh. Nunn and McCreesh’s Blackmore Bond is currently in the hands of administrators Duff and Phelps.

Victims of all of these scams are still invited to contact the Serious Fraud Office if they have any evidence they wish to provide in order to help bring the fraudsters to justice: hazel@sfo.gov.uk

Forsters – the firm which Pension Life is working with – have liaised with the Trafalgar Multi Asset Fund investor committee (which currently includes a doctor and a police officer). Forsters and Pension Life are working towards bringing about the best possible outcome for the victims.

There may be serious doubts over whether the liquidation by Doran + Minehane will result in any meaningful returns for the victims. However, this litigation will give them a decent chance to get a large proportion of their pensions back.

Forsters LLP is a leading law firm with an exceptional track record of successful dispute resolution. It is not a no-win-no-fee firm, and it has no connection with any claims management companies.

The Kiwis were grass and England was a lawnmower. For a couple of hours we forgot Brexit and remembered our national pride.

In a Week that saw an inconclusive result in the UK v Europe match (yet again), at least England taught New Zealand how to play rugby.

And the battle against pension scams moved up a gear as the press reported on the first round in the victims v scammers tournament.

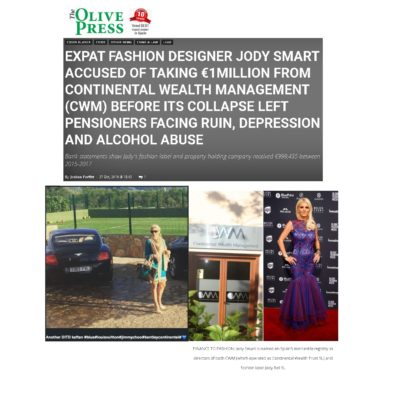

Olive Press journalist Joshua Parfitt reported on the first round of the criminal proceedings in Denia on the Costa not so Blanca. His surprisingly well-written article pulled no punches as it exposed the one million Euros that Continental Wealth Management boss Jody Smart Bell Kirby Pearson took out of the business in the two years before it collapsed in September 2017.

Former cleaner Jody claims she was only a “non-active” director of Continental Wealth and that the company was run by former boyfriend Darren Kirby. She also claims that her property company Mercurio Compro S.L. (which received 670k of the million) was just a front for Darren’s property dealings and that he used the company bank account because he didn’t have his own personal bank account.

Jody’s fashion business – Jody Bell – received 326k of the million. At least she hasn’t tried to claim that this was Darren’s business in reality (and that he had taken to designing frilly frocks between scamming 1,000 investors out of their life savings).

Whichever way you look at it, however, Jody paid herself 1 million Euros on top of her salary of 280,000 Euros. But this was only during the last two years of the life of doomed Continental Wealth – we still don’t know how many millions she paid herself prior to that – at the height of the structured note/insurance bond scam operated by Darren and his team.

There’s an interesting comment on the Olive Press article: English naivete is amazing given any chance for a quick return. Doesn’t anybody do due diligence when it comes to investment? This is like episodes on ” L’l Britain”.

Due diligence would, indeed, have revealed that Continental Wealth operated without a license and that the staff were not qualified.

Until 2015, Continental Wealth claimed to be an “agent” of a firm in Cyprus called Inter Alliance – and that this allowed the CWM scammers to use the Cyprus license. However, this was entirely untrue as Inter Alliance never had any license and had in fact been fined by the Cyprus regulator for falsely claiming to be licensed.

Interestingly, when I click on the Olive Press Article, an irritating advert for Abbey Wealth keeps popping up. The ad offers the same old same old scammers’ trick: “free pension review”. So, coming from the same “stable” as Jody and Darren’s Continental Wealth scam, let’s do our due diligence on Abbey Wealth.

According to the Abbey Wealth website, there are 17 “Senior Wealth” Managers. Most of these have no verifiable evidence of any qualifications, and quite a few are former mortgage brokers. Despite there being no investment license for the firm, several mention investments:

Ben Noifeld: “investment solutions”; Christian Holbrook: “providing highly-regulated, tax-efficient investment solutions”; Mark Smith: “portfolio management and investment planning”; Michael Chambers: “making clients comfortable with their investments”.

In Spain, all these “Senior Wealth Managers” are committing a criminal offence by promoting investment advice without a license”.

There’s one chap – Craig Allanson – who claims to be a Senior International Pensions Adviser, despite no evidence of any qualifications. And the Managing Partner – Victor France – has no evidence of any qualifications (as well as being ex Old Mutual – the kiss of death as far as most Continental Wealth victims are concerned).

However, there is one adviser who is indeed Chartered: Ian Boden. But why on earth would a man who states he “holds the highest level of qualification of Fellowship and Chartered Financial Planner status with the Chartered Insurance Institute (CII)” work for a firm with no investment license? He, of all people, should know better. He’s either desperate or has some dark skeleton lurking in his cupboard.

The final nail in the coffin is that the firm’s insurance license is from the Central Bank of Ireland. So there’s no protection for any of the clients if anything goes wrong. The Irish Ombudsman is hopeless, never upholds any victims’ complaints and is clearly bent towards Irish-licensed firms and against their victims. The Ombudsman’s determinations against SEB and OMI victims are clear evidence of this. And talking of SEB, Abbey’s “Senior Wealth Manager” Iwan Thomas (with no evidence of any qualifications) is ex SEB.

Abbey Wealth – will they altar their insurance bond salesmen’s approach to “wealth management”?

The comment on the Olive Press article by “Chas” does indeed raise the essential issue of due diligence. DD isn’t hard – it is just a question of knowing the questions to ask and understanding the answers. Finding out about regulation (license) is easy – you just start with the firm’s own website. The licensing bit is usually at the bottom on the website. Then you look at each of the advisers and check on the CII and CISI websites to see if they are listed on the register. Then, most important of all, do a Google search.

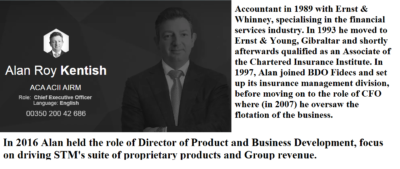

So here’s a prime example: QROPS provider STM is now trying to force members to use an IoM advisory firm called Creechurch Capital. STM is headed up by Alan Kentish (below) who is no stranger to handcuffs himself, and has a penchant for working with scammers.

A quick Google search reveals that a “whistleblower” had exposed Creechurch for falsifying client records. If you would still want to have this firm as your financial adviser, consider that it is based in the Isle of Man (where many scammers, and Old Mutual International, are based). The Isle of Man has a rubbish regulator and ombudsman and – like Ireland and Gibraltar – seems to positively encourage scams and scammers and treat victims as irrelevant.

You can tell a lot about a firm by the pictures on their website. In the case of Creechurch Capital, it is a bottle of wine. Does that suggest a client would need to be drunk to use Creechurch? Drunk or sober, any potential client should check out the people behind the firm.

Managing Director Jim Dolan claims to be qualified with the Chartered Institute of Securities and Insurance. And indeed he shows up on the CISI register as being Chartered FCSI – only not with Creechurch but with a firm in London called Sentient Capital. Nothing particularly suspicious about that, I suppose, but how can a person be Managing Director of two firms simultaneously? (I thought it was only women who can multi-task).

Miles Ashworth, Creechurch’s Head of Private Wealth, appears on the CISI register as claimed. And the rest of the senior management team seem to be a reasonable bunch. Also, the company was sold to Nayyar Group in March 2019. So somebody must have done their due diligence on the firm and paid good money for it.

But the question remains: why would a decent bunch of qualified and experienced financial services professionals be seen dead working on the Isle of Man along with so many dodgy, unregulated fund houses such as Blackmore Group and rogue life offices like Old Mutual International and Friends Provident?

And, even more important, why on earth would the guys at Creechurch want to be associated with STM? Don’t they know that STM has a history of working with scammers and that they facilitated the Trafalgar Multi-Asset Fund scam by investing all 400 victims’ pensions in XXXX XXXX’s own fund?

So back to the real World: rugby; Brexit; Halloween and the end of the decade looming. It really has been a dreadful decade for pension scams: thousands of people scammed out of £ billions. Let’s hope the scammers at Continental Wealth Management will all get hefty jail sentences and that this will force any advisory firms operating the same business model to turn away from the dark side.

So what exactly is the “dark side”? In a nutshell:

Providing services without a license

Having unqualified “advisers”

Mis-using insurance bonds (purely for the commissions)

Putting low-risk investors in high-risk investments (purely for the commissions)

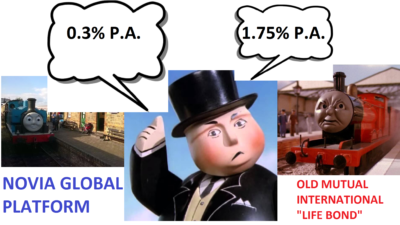

The problem with money is that it blows away if you don’t hold it down, tie it up or stuff it down your knickers. That’s why you need to put it somewhere safe: in a shoe box on top of the wardrobe; under your mattress; in the safe or – if you’re feeling really brave – in the bank. Trouble is, left in cash, money shrinks (inflation, charges, moths). This is why so many advisers recommend a platform – aka “somewhere safe” to keep your money.

I’ve met Bill Vasilieff who runs Novia Global. He serves Earl Grey and nice biscuits. A man of few words, and even fewer syllables, he gave me a quick rundown on how the Novia Global platform works – and how much it costs.

I haven’t met Peter Kenny of Old Mutual International (OMI) – although I have spoken to him several times. As broadly Irish as Bill is Scottish, Peter Kenny also comes across as a softly-spoken and sincere chap. But there the similarity seems to end. Peter stood me up – I got a view of his office waiting room but wasn’t offered a cup of tea (let alone a biscuit).

Mind you, there isn’t much I don’t know about the Old Mutual International bonds. I’ve seen thousands of their policyholders’ statements – and they are frighteningly ugly and depressing. They accurately, faithfully and unemotionally report the destruction of their victims’ atrocious losses. And OMI regularly (like clockwork!) take their quarterly fees – irrespective of how deep the destruction of the policyholders’ funds is. In fact, some victims even find themselves in negative figures as OMI continue to account for their fees long after the whole blooming lot has gone.

Anyway, back to Bill and his welcoming teapot….I can’t really compare him to Pete but I can compare the two products. So here is a brief and brutal side-by-side line up of what the two “platforms” offer. And how much they cost. And how difficult they are to get out of. And how much financial crime they are associated with.

So the OMI “life bond” costs almost six times as much as the Novia Global platform. But that is if you are locked in for five years. You can get it cheaper – 1.15% – if you get locked in for ten years. But you must remember that if you are scammed, then OMI will have paid the scammer an 8% commission and you could get stuck with paying the quarterly fees for the next ten years, even if you’ve figured out you’ve been scammed. And the quarterly fees are based on your original investment – not on the impaired amount. If you’ve been scammed, and your fund value drops inexorably, the 1.15% will become bigger and bigger. And even if you lose your whole fund, OMI will keep taking their charges and pushing you further and further into debt.

A bit like the lyrics to Hotel California, with an OMI “bond”, you can’t check out any time you want, and you can only leave after between five and ten years. OMI will take that number of years to claw back the commission paid to your adviser – even if you have long since learned that your adviser was an unregulated scammer and has conned you into unsuitable, high-risk, high-commission investments that have badly damaged your fund. You are stuck with paying the quarterly fees to OMI – even after your whole fund has gone. One victim went from plus £300k to minus £25k – and counting. As your funds inside the OMI bond shrink, the 1.15% grows and helps destroy what is left of your fund even faster. But with the Novia Global platform, you can leave any time you want. No exit penalties. No hard feelings.

In Spain, the Supreme Court has ruled that bogus life assurance policies – such as those provided by Old Mutual International – used to hold investments are illegal. This is because they are neither proper insurance policies (which take risk in the interests of the consumer) nor are they proper investment platforms. The Spanish aren’t stupid – they can spot a scam much more easily than other jurisdictions and take action to prevent them from ruining future victims. This is in stark contrast to the likes of the Isle of Man and Gibraltar – which seem to revel in encouraging scams and protecting firms such as Old Mutual International (and STM Group) which facilitate financial crime on a massive scale.

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

As is the case with many scams, the victims are unlikely to recoup any of the funds they entrusted to him. Bartlett is said to have spent the hard-earned funds on prostitutes, escorts and expensive holidays. The victims, all of whom knew him on a personal level, are disgusted at his behaviour and were glad to see this scammer jailed.

Here in the Pension Life office, we are always pleased to hear that a scammer has been jailed. The only shame, is that we just don´t hear the words enough. It would be great if we could write blogs that contain the words SCAMMER JAILED on a daily basis. But sadly it is just not the case.

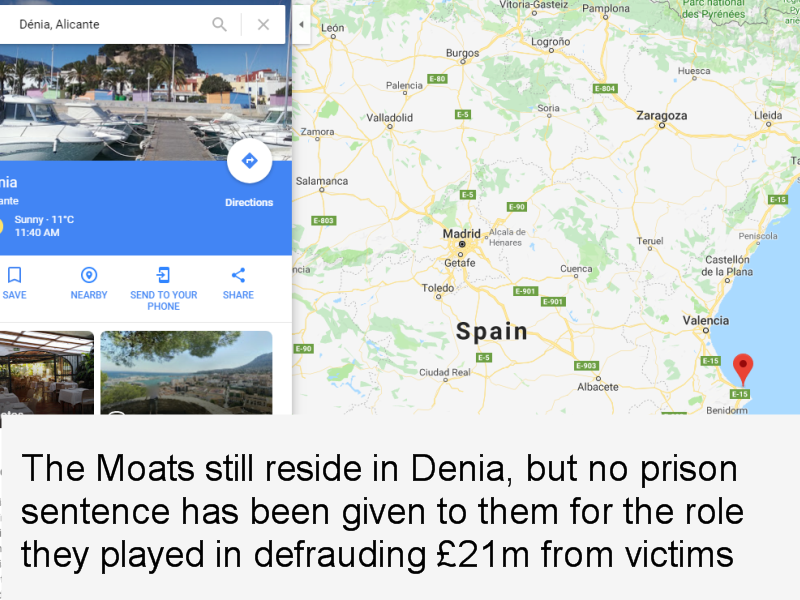

An example of this is Peter and Sara Moat of Fast Pensions – which was wound up back in May 2018. We know they fraudulently took £21m from their victims. We know they did not invest it in the interest of their victims. We know they invested the funds into other businesses they own. We know that they reside in Denia, where their daughter goes to a private school. We know all this – AND the SFO knows all this – yet the Moats are still free to live a lavish lifestyle whilst their victims go without a pension and some face losing their homes as well as bankruptcy.

I´m sure the victims of the Fast Pensions and Blu loans scams would find some solace in reading the words – “scammer jailed” in relation to both Peter Moat and Sara Moat. But I´m not sure if they ever will – and that makes us sad and bloody angry.

Thousands of victims and hundreds of thousands of pounds’ worth of pension money has been fraudulently taken from the victims of scam schemes sold by the above-named scammers. Schemes like Capita Oak, Blackmore Global Fund and the Trafalgar Multi Asset Fund.

All we can do is make a very loud suggestion that STM Group Gibraltar – STM Fidecs – Alan Kentish – should all be given a VERY wide berth when considering a change of pension trustee – as from past evidence they are not to be trusted!

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors Old Mutual International, or a marketing machine. I read with interest the recent IA Industry Most Influential Top 100 described by IA thus: “we at International Adviser decided to shine a light on the movers and shakers that have helped this industry get to where it is today”.

But where exactly is the industry today? And have the so-called top 100 moved and shaken the industry in a helpful way or a detrimental way? To find out, why don’t we have a look at a few of the “influencers”. To get the measure of them, let’s put them into a game of “Have I Got News For You”:

Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based Investors Trust until recently appointed chair of the Association of International Life Offices, the trade body for international life offices. During his 35 years of experience in financial services, he facilitated the scam run by Phillip Nunn of Blackmore Global and David Vilka of Square Mile International Financial Services. Investors Trust accepted over 1,000 investments into illegal UCIS funds for UK-based victims scammed into QROPS with Integrated Capabilities and Harbour (now STM).

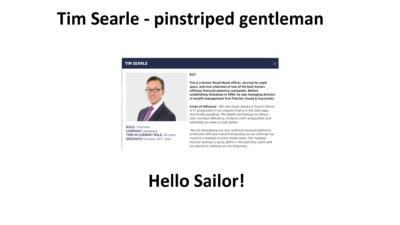

As Captain of the Navel Team, let’s have dashing Tim Searle – Chairman of Dubai-based Globaleye. With his eight-year Naval history, he should make an ideal leader and would come in particularly useful in the event of icebergs, torpedos or sharks.

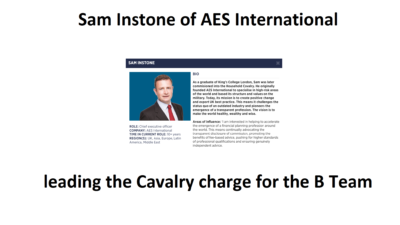

Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

On the Army Team, we’ll have international wealth and regulatory specialist, Phil Billingham. Phil must be utterly disgusted with the likes of Stephen Ward (another fully-qualified adviser) messing up the reputation of the profession by running a long series of pension scams and ruining thousands of lives.

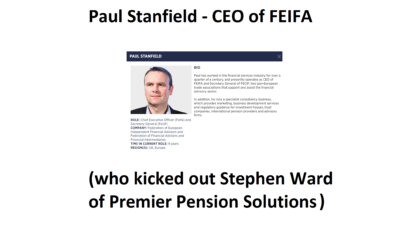

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated Stephen Ward of Premier Pension Solutions from FEIFA to loud cheers from victims and industry professionals alike. (My only gripe with him would be that he still hasn’t kicked out Square Mile Financial Services run by scammers John Ferguson and David Vilka).

On the Navel Team we’ll have Geraint Davies of Montfort International – an expert IFA specialising in international financial services, and Roger Berry of Concept Group Trustees in Guernsey. These two chaps also have, between them, extensive experience of Stephen Ward in their own ways and will, no doubt, have much to talk about.

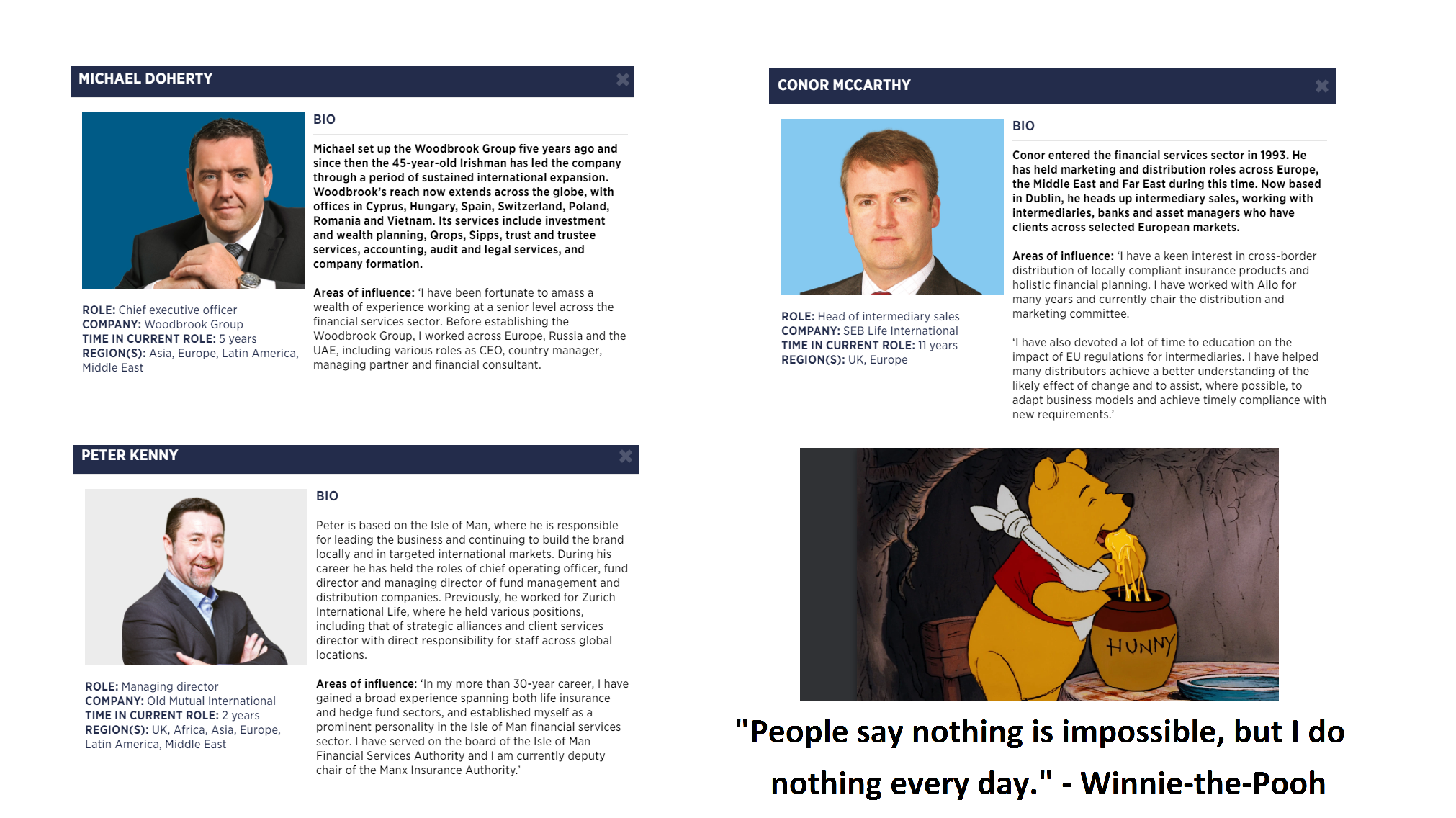

The contest will be to spot the “odd one out”: Michael Doherty of Woodbrook Group, Conor McCarthy of SEB, Peter Kenny of OMI and Winnie-the-Pooh.

Tim Searle: “They’re all Irish, except Winnie-the-Pooh who’s English?”

Geraint Davies: “They all hate Angie except Winnie-the-Pooh who’s never heard of her?”

Roger Berry: “They all love Angie except Winnie-the-Pooh who’s never heard of her?”

Sam Instone: “They’ve all got names that end in Y except Winnie-the-Pooh?”

Phil Billingham: “They’re all involved in money except Winnie-the-Pooh who’s involved in honey?”

Paul Stanfield: “None of them have applied to be members of FEIFA except Winnie-the-Pooh?”

Bob Pain: “No, you’re all wrong. The answer is Peter Kenny of OMI. The other three have been doing “nothing”: Michael Doherty was employing ex CWM scammers Dean Stogsdill and Neil Hathaway (known as Dog Kill and Hadaway) but claimed he was paying them nothing; Conor McCarthy of SEB has been asked numerous times for his comments on why SEB allowed the scammers at CWM to invest most of their victims’ funds in toxic structured notes, but McCarthy is saying nothing and won’t reply; and Winnie-the-Pool is doing nothing all the time.

The odd one out is Peter Kenny who is doing “something” and is suing Leonteq for the £94 million worth of fraudulent structured notes they sold to OMI.

I have read the report about what happened to the scammers at STM Fidecs in the wake of the Gibraltar FSC’s investigation and Deloitte’s so-called “expert report”.

Frankly, I am stunned. I have members who are victims of the Trafalgar Multi-Asset Fund and STM Fidecs and they are, understandably, stunned as well. I have met the people at the Gibraltar FSC and they had seemed decent guys |(but WTF do I know?!). Maybe they’ve all left, because the people I met appeared enthusiastic and conscientious. But perhaps they’ve been replaced by a bunch of malfunctioning robots, or ex-scammers or – much worse – ex STM Fidecs employees.

Serious Fraud Office investigating XXXX XXXX

The bottom line is that STM Fidecs scammed hundreds of victims out of their pensions. STM Fidecs took business from unlicensed scammer XXXX XXXX of Global Partners Limited (only had an insurance license with Marcus Groombridge’s firm Joseph Oliver) and then invested 100% of the victims’ funds into an illegal UCIS fund – run by XXXX XXXX (now under investigation by the Serious Fraud Office – although I really don’t know what they are playing at because XXXX still isn’t behind bars).

The rest is history. The Trafalgar Multi-Asset Fund is being wound up, and after paying the liquidation costs to Stephen Doran, of Doran + Minehane, there is unlikely to be much – if anything – left. Deloittes spent weeks supposedly investigating STM Fidecs’ books. I reckon the chumps at Deloittes probably spent most of that time on the golf course with Alan Kentish having a chuckle and a side bet about how feeble the Gibraltar FSC was likely to be. And, of course, they were right.

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.

Neither STM Fidecs nor the Gibraltar FSC has said a word about redress for the Trafalgar Multi-Asset Fund victims.

The only words spoken are that the Gibraltar Regulator has told STM Fidecs to “improve its compliance”. Improve?? How can you improve something that doesn’t even exist at all? We know that one victim (of scammers Holborn Assets) was bullied by STM Fidecs for trying to improve compliance and harassed for trying to stop obviously non-compliant transactions when she was employed by them. She was subsequently “paid off” and threatened with a gagging order.

“STM is now expected to engage with the Gibraltar FSC in order to discuss the Recommendations of the report, and agree a plan of action to implement them.” (according to the report by FT Adviser). Recommendations? Where are the sanctions? Where are the appropriate fines? Where are the bans to stop Alan Kentish and David Easton from ever practising in financial services again? Where is the cancellation of STM Fidecs‘ license?

With this in mind, here are some idiots’ guides as to how to become a pension trustee, and how to become a regulator. Both are equally easypeasylemonsqueasy – any old idiot or scammer could do it.

HOW TO BE A PENSION TRUSTEE IN EASY STEPS

Think of a catchy name: obviously inspired by the acronym STD, Alan Kentish came up with the name STM. FIDEC is an acronym for “Fighting Infectious Diseases in Emerging Countries”. Here’s my suggestion: Trussed4U – wadya fink?

Think of a jurisdiction with the most ineffective, pathetic and corrupt regulation – such as Gibraltar

Find an unlicensed scammer like XXXX XXXX who will transfer lots of UK-resident victims into an offshore QROPS and invest their life savings in whatever crap will pay him the highest commissions

Sit back and rake in the profits

Forget fiduciary obligations or anything with the word “trust” in it – only concentrate on the word “trussed“

Play golf with the regulator

HOW TO BE A REGULATOR

Join a golf club (that isn’t too picky about who it lets in)

Give licenses to as many scammers as possible – the more the merrier

Buy lots of blindfolds (to help turn a blind eye to scams and scammers)

Play lots of golf with the scammers and bent pension trustees who facilitate financial crime

When an advisory firm or a trustee firm gets caught scamming, slap a few people on the wrist with a wet fish

Write meaningless reports about robust compliance

HOW TO BE A SCAMMER

Find yourself a bent jurisdiction (such as Gibraltar)

Find a bent trustee who will accept business from any old unlicensed scammer (such as STD FIDEC)

Find a bent “umbrella” fund which will facilitate financial crime – such as Richard Reinert’s Nascent Fund

Find a Ponzi scheme such as Dolphin Trust which will issue “loan notes” at 10% interest per annum (and up to 25% in introduction commission)

Transfer hundreds of UK residents to a Gibraltar QROPS scam

Get the trustee to agree to invest 100% of 100% of the victims’ retirement savings in … your own fund!

See how easy it is to be either a trustee, a regulator or a scammer? But, equally, remember how easy it is to be a victim!

Quite frankly, Gibraltar should be towed out to sea and sunk. It is a disgrace to the British nation. Just give it back to the Spanish and let them clean it up – they would soon kick the likes of STM Fidecs out and stop any further scams and scammers from operating on Spanish soil. Soil being the operating word.

Rather than going on about how utterly disgusted I am with the Gibraltar regulator, I will leave it to the eloquent words of one of the STM Fidecs/Trafalgar Multi-Asset victims to put this sickening disgrace into perspective.

Firstly, do Gibraltar FSC actually realise over 1,000 individuals and their families are affected by the Trafalgar fiasco, who will potentially all suffer negatively in many different ways during their retirement years? On a personal level, I should haveknown better but was caught out by cleverness at a weak moment in my life, but many others I have spoken to had no understanding at all of financial affairs and put all of their trust in the hands of STM and all connected parties due to their apparent convincing knowledge and lies – shocking!!!!!

Due to my own personal research, I know of several other financial institutions who were offered and were involved in discussions regarding Trafalgar. But due to having correct procedures in place (unlike STM), they clearly ”smelled a rat”, and were far more ”ROBUST” in their approach. The only rat STM smelled was some form of hopeful ”Magic Money Tree” with no concern for its clients’ wellbeing – apart from its own pound note signs.

As you already know I have previously discussed this matter with my local MP and with your permission would like to highlight again the manner in which Gibraltar FSC have dealt with and inadequately reacted to STM’s performance. STM’s website highlights their glowing history and expertise, but at no point mentions their clearly poor basic audit and compliance mechanisms.

Hopefully, at some point in the future all the evil parties – including STM – in this matter are dragged through the courts, eventually embarrassed and humiliated by the press, and made to pay both financially and personally for their hideous crimes – I can only dream.

Still angry and in despair.

STM Fidecs/Trafalgar Multi Asset Fund Victim

That victim may well have lost her entire life savings thanks to XXXX XXXX and STM Fidecs. I am sickened and disgusted with our own onshore regulator’s pathetic failings: the FCA. But, quite frankly, the Gibraltar FSC makes the FCA look like Superman with TWO pairs of pants on outside their tights!

Interestingly, Justin Caffrey – who used to run Harbour Pensions in Malta – told me a year or so ago that he had been approached by XXXX XXXX who wanted to flog his toxic Trafalgar Multi Asset crap.

Caffrey claimed to have sent XXXX packing with a flea in his ear because he twigged straight away that XXXX was a no-good spiv. However, he had no such ethics when he invested victims’ pensions in Phillip Nunn’s Blackmore Global crap.

But now STD FIDEC has bought Harbour and Caffrey has been given the heave-ho. You couldn’t make it up!

QROPS provider STM Group’s Alan Kentish, is delighted to deliver reports of record profits for 2017. I wonder how delighted the victims of his previous scam, the Trafalgar Multi Asset Fund, are to hear this. I think we’d be more delighted to hear that Kentish planned to pay all the victims of this investment fraud (currently under investigation by the Serious Fraud Office) full compensation for their losses.

The company, STM Fidecs, which has recently moved its head office to the UK from Gibraltar, says its annual profits grew last year by 43% after the introduction of a new SIPPS.

Kentish went on to say,

“Moving into 2018, we have a solid recurring revenue platform on which to look to launch new products and to expand our distribution network as part of a strategy to make our business even more robust.”

In our opinion, there is nothing robust about Kentish and his various dodgy products. And the Gibraltar regulator shares our opinion as well as our concerns. In a letter dated 6.11.2017, the GFSC wrote to the directors of STM Fidecs about their concerns following a series of onsite visits:

“COMPLIANCE: effectiveness and oversight of the company’s internal compliance functions; high turnover of staff in compliance officer and money laundering regulatory officer roles; general suitability and experience of compliance staff.

PROFESSIONAL TRUSTEE SERVICES: level and nature of due diligence when accepting new QROPS business and whether legal and regulatory obligations were being met; nature of investments e.g. the Trafalgar Multi Asset Fund linked to serious customer detriment and fraud”

The Gibraltar regulator appointed three partners of forensic investigators CVR Global LLP to inspect and investigate the affairs of STM Fidecs. The deadline for completion of this inspection is end of March 2018 and the GFSC has warned that:

a person who wilfully makes a statement or furnishes information knowing it to be untrue;

a person who refuses to supply information or cooperate with an inspector

is guilty of an offence and is liable on conviction to imprisonment.

I wonder if any of STM’s fat profits will be used to help balance the heavy losses made by the company’s past “mistakes”. At the height of the success of the Trafalgar Multi Asset investment scam, STM Fidecs was accepting more than £1 million a month from UK residents (none of whom should have transferred into a QROPS at all) and allowing it all to be invested in XXXX XXXX’s illegal UCIS.

I find it very hard to swallow that Kentish can continue to offer his “products” to unsuspecting future victims – given his murky past record. Kentish has stated “I look forward to updating the market on our developments during the year.” But has he updated the Trafalgar victims about the development of their lost funds being recouped? No he has not. He has just scraped his past misdemeanors under the carpet and hoped they will be forgotten.

After his arrest in October 2017, Kentish was released without charge and was fully backed by the STM board. (They are obviously a load of crooked clowns who are no better than Kentish himself). He has, also, been given the green light to further his venture into offering legal SIPPS wrappers to clients, that have the potential to contain high-risk, toxic investments. The results of which may well leave even more unsuspecting victims’ pension funds in tatters.

******************************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

STM Fidecs has played its “get out of jail free” card, avoided January’s court hearing and agreed to “cooperate” with the Gibraltar Financial Services Commission (GFSC) – allowing auditors Deloitte to probe STM’s dirty books.

I was more than a little miffed because I was looking forward to a nice day out in Gibraltar. I had my packed lunch all planned – spam sandwiches, hard-boiled eggs and ripe tomatoes (with a few spares in case I got a chance to lob one or two at Alan Kentish and David Easton).

Instead, Deloittes are going to “probe” STM’s undoubtedly cooked books. Fraudsters Alan Kentish and David Easton might try to hide some of the dirtiest stuff. (And in case some eager defamation lawyer is reading this, “fraudsters” is what Kentish and Easton called themselves on Facebook).

I will, of course, be more than happy to help Deloittes see the whole picture – rather than just what the Fraudsters want them to see. I will happily buy a whole shed full of spades as well as several boxes of latex gloves and surgical masks. However, the most important way in which I can assist them is to give them details of the various scams which the Fraudsters have operated and facilitated.

The Gibraltar regulator has for some time been trying to expose STM’s various nefarious activities – while Kentish and Easton have doggedly and desperately wriggled and slithered out of reach. The Deloitte investigation will finally expose the company’s internal compliance failures and conflicts of interest.

Deloittes will need to concentrate on at least three main areas: Trafalgar Multi-Asset Fund; Cornerstone Friendly Society and Blackmore Global. They will also need to liaise closely with the Serious Fraud Office which is investigating the Trafalgar fund scam and the West Yorkshire and Humber Police which is investigating the Cornerstone scam.

If Deloittes are going to be able to conclude their investigations into STM by the end of March 2018, they will have to ask many probing questions to establish the extent of STM’s “compliance failures” (aka facilitation of financial crime).

Why did STM accept business from serial scammer XXXX XXXX’s unlicensed firm Global Partners Limited?

Why did STM accept hundreds of transfers from UK residents in whose interests it was NOT to swap their British pension arrangements for an expensive QROPS?

Why did STM allow these victims to have funds invested in XXXX XXXX’s own fund – Trafalgar Multi-Asset (a UCIS which is illegal to promote to UK residents)?

Did STM not consider it to be a conflict of interest for the “adviser” and fund manager to be one and the same person? Especially a person with a sordid track record of operating pension scams such as Capita Oak, Henley, and Westminster?

Chief executive Alan Kentish has described the Deloitte “deal” as a workable solution and is jolly pleased to have avoided January’s court hearing. He has also said that the hearing wasn’t in either STM’s or the GFSC’s interests.

I suspect both STM and the GFSC knew it was very likely that quite a few STM victims whose pensions are in tatters were likely to turn up and that the hail of ripe tomatoes was likely to make quite a mess of the Supreme Court’s wallpaper.

Meanwhile, Alan Kentish and another STM Fraudster are still being investigated by the Gibraltar Police Money Laundering Unit. I just hope they don’t get hauled off to jail before Deloitte get to finish their digging and probing – as that might delay the publication of the report.

So what has prompted all this recent flurry of action? In November 2017, the GFSC wrote to STM Fidecs and outlined their concerns. These included – among other things:

Effectiveness and oversight of STM Fidecs’ internal compliance functions

High turnover of staff in Compliance Officer and Money Laundering Regulatory Officer roles

General suitability and experience of compliance staff

Exercise of corporate governance across all of the STM companies

Compliance with legal and technical requirements in relation to the operation of client accounts

Level and nature of due diligence undertaken when accepting new QROPS business and whether legal and regulatory obligations are/were being met

Nature of investments made in relation to QROPS e.g. the Trafalgar Multi-Asset Fund – linked to serious customer detriment and alleged fraud

I think Deloittes also ought to look into why STM Fidecs’ own staff were bullied into “looking the other way” when they were worried about compliance issues (and then paid off to keep them quiet).

Finally, STM Fidecs has now announced it will be moving from Gibraltar to the UK. This move comes after what Alan Kentish has described as “unexpected challenges”. Kentish remains bullish, however, about the company’s profitability. However, he still fails to express any concern for the hundreds of STM Fidecs’ victims who will inevitably see heavy losses in their pension funds and will suffer poverty in retirement. Shame on this callous character.

*************************************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Quilter – Old Mutual International – new name to try to hide past crimes

QUILTER – A NEW HOBBY FOR OMI? OMI – Old Mutual International – needs to compensate thousands of victims of financial crime which they facilitated. I can’t make up my mind whether they are adopting the brand “Quilter” to attempt to shake off their sordid and toxic past, or whether they are actually taking up quilting.

If OMI really is going to become a quilter, it needs to make a quilt depicting all the criminals whose crimes it has facilitated for so many years. And all the victims who have lost part of or all of their life savings.

What OMI really needs to do is to get firmly behind the prosecution of the criminals – from whom they profited for many years. OMI must contribute to the cost of denouncing these criminals and ensuring they are given maximum prison sentences.

Also, OMI – Old Mutual – must stop allowing toxic, professional-investor-0nly structured notes in their bonds. Typically, these were provided by Commerzbank, Nomura, Leonteq and RBC. If Old Mutual International wants to gamble away its own money on these crap products, then be my guest. But don’t expose retail pension savers to these sordid, high-risk instruments – used by the scammers as mere tiles in a game of Scrabble.

Al Rush championing the British Steelworkers who have been scammed

Al Rush has suggested the wording which victims can use to report those who scammed – or attempted to scam – them. And all of what Al and his colleagues have done has been done at their own expense and out of a sense of decency.

Hard to tell the difference between OMI and Quilter and Jabba The Hut

This is in stark and stinky contrast to OMI – Old Mutual International. Since 2011, OMI has sat and watched – like a cross between Jabba The Hut and a Black Widow Spider – while thousands of victims have seen their life savings dwindle away to very little or even nothing. And all the while, taking extortionate fees and paying commissions to the very scammers who ruined the victims in the first place.

So does OMI really think that adopting the name “Quilter” will make future victims fail to make the connection – that this is the same firm that took business from dozens of unregulated scammers such as Continental Wealth Management, Abbey Financial Solutions, Holborn Assets, Guardian Wealth Management, and other “chiringuitos”?

Perhaps the worst crime committed by OMI is not that they took business from unlicensed scammers; not that they allowed 100% of victims’ pension funds to be invested in professional-investor-only, high-risk structured notes; not that they sat there idly and negligently while the clients’ pensions and investments shrank inexorably……

Old Mutual International – the rubbish end of financial services

the worst of OMI’s crimes has been that when there are only a few crumbs left of a life-time’s retirement savings, they will still charge crippling early-exit penalties. OMI, or Skandia, or Quilter or Jabba The Hut or whatever the hell this toxic, evil shower call themselves, have no place in financial services. They have facilitated and profited from financial crime for years and benefited from the misery and ruin of thousands of victims.

In an attempt to emulate Al Rush’s suggested police report for British Steel victims at the hands of the various scammers who targeted, stalked and scammed them, here is my suggested report for OMI victims to make to the police and the regulators. Naturally, this will work equally well for victims of Generali, SEB, RL360, Friends Provident, Hansard, Investors Trust etc.

OMI must be sanctioned for facilitating financial crime

‘I was advised to transfer out of my personal/occupational (delete as appropriate) pension scheme and was lied to when I asked about how much money would be taken from me. I think, over time especially, I will lose/have already lost many tens of thousands of pounds (probably, hundreds of thousands of pounds) in fees which were hidden from me.

This will bleed my pot dry, leave me exposed to poverty in old age and create a burden on the local council.

I was specifically told there would be no penalties or lock-in periods.

Can you help me please, I would like to make a formal statement and help you bring charges against those who did this, and those who helped them’.

It is rare for me to say nothing. On this occasion, STM Group has stated they are going to stick their heads in the sand and zip their lips. They have facilitated a financial crime…….OK, enough said. For now. I will leave it to STM Group/Fidecs to decide what goes into this blog. They have until close of play tomorrow, Friday 26th May. Then we can either deal with this discreetly and privately – or we can do it all publicly. With every sordid detail exposed in the public domain, to the regulators, the police (who are already investigating, with victims making their reports to the Serious Fraud Office) and the press. And, of course, the Stock Market. Your call STM. Silence is not golden. It is distinctly brown. Get your lawyers to talk to me if you want, but let these victims have some answers if you have any conscience.

Seriously–is this yet another wind up? STM want to be voted as “National Public Champion”?

All of STM’s allegedly world-leading people will have known that it was illegal to promote a UCIS to retail UK residents. Unless STM’s claims about their excellent pensions team are just a wind up?

After International Investor’s expose of the wind up of the failed £21 millionTrafalgar Multi-Asset fund:

not many of the hundreds of victims who may stand to lose part or all of their pensions will be voting for STM. International Investment’s Helen Burggraf reported that the Trafalgar fund’s investors were advised of the wind up on 13th January 2017 by Richard Reinert of the Nascent Fund (an umbrella fund containing the Trafalgar fund).

STM, who failed to provide details about how the wind-up is likely to work, have apparently whined that they had been “unfairly singled out” as a well-known trustee because they had kept their victims “informed about the fund’s problems”

STM, whose stake in Trafalgar accounted for 75% of the total fund value, failed to answer urgent questions about their role in the victims’ impending losses in the fund which, according to International Investment was “managed by Victory Asset Management, run by two of the people involved in the Capita Oak pension scam.”

.

STM claim to have over 50 “dedicated and highly-skilled” people in their pensions team and that their level of expertise has made them world leaders in the field of QROPS. Perhaps one of these wonderful people can explain why hundreds of UK-domiciled investors were transferred into a Gibraltar QROPS on the advice of an unregulated adviser who was also the Trafalgar fund manager into which 100% of these pensions were invested.

STM will surely have no trouble providing an explanation as to why victims’ pensions were 100% invested into one UCIS which was 100% invested in loans to a German property developer.

All of STM’s allegedly world-leading people will have known that it was illegal to promote a UCIS to retail UK residents. Unless STM’s claims about their excellent pensions team are just a wind up?

The problem with money is that it blows away if you don’t hold it down, tie it up or stuff it down your knickers. That’s why you need to put it somewhere safe: in a shoe box on top of the wardrobe; under your mattress; in the safe or – if you’re feeling really brave – in the bank. Trouble is, left in cash, money shrinks (inflation, charges, moths). This is why so many advisers recommend a platform – aka “somewhere safe” to keep your money.

The problem with money is that it blows away if you don’t hold it down, tie it up or stuff it down your knickers. That’s why you need to put it somewhere safe: in a shoe box on top of the wardrobe; under your mattress; in the safe or – if you’re feeling really brave – in the bank. Trouble is, left in cash, money shrinks (inflation, charges, moths). This is why so many advisers recommend a platform – aka “somewhere safe” to keep your money.

A bit like the lyrics to Hotel California, with an OMI “bond”, you can’t check out any time you want, and you can only leave after between five and ten years. OMI will take that number of years to claw back the commission paid to your adviser – even if you have long since learned that your adviser was an unregulated scammer and has conned you into unsuitable, high-risk, high-commission investments that have badly damaged your fund. You are stuck with paying the quarterly fees to OMI – even after your whole fund has gone. One victim went from plus

A bit like the lyrics to Hotel California, with an OMI “bond”, you can’t check out any time you want, and you can only leave after between five and ten years. OMI will take that number of years to claw back the commission paid to your adviser – even if you have long since learned that your adviser was an unregulated scammer and has conned you into unsuitable, high-risk, high-commission investments that have badly damaged your fund. You are stuck with paying the quarterly fees to OMI – even after your whole fund has gone. One victim went from plus  In Spain, the Supreme Court has ruled that bogus life assurance policies – such as those provided by

In Spain, the Supreme Court has ruled that bogus life assurance policies – such as those provided by

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

AND to rub salt into the wounds of the Trafalgar victims,

AND to rub salt into the wounds of the Trafalgar victims,

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based

Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based  Capabilities and Harbour (n

Capabilities and Harbour (n Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.

Now, of course, Deloittes and STM Fidecs are celebrating, as the GFSC has done nothing to stop this iniquitous, dishonest, incompetent and negligent firm from trading. Whether STM Fidecs bribed the Gibraltar FSC, or merely got them drunk on the golf course, we will never know. And it makes no difference. But certainly the matter has been brusquely brushed under the carpet and the hundreds of ruined lives have been conveniently ignored and forgotten.

QROPS provider

QROPS provider  In our opinion, there is nothing robust about Kentish and his various dodgy products. And the Gibraltar regulator shares our opinion as well as our concerns. In a letter dated 6.11.2017, the GFSC wrote to the directors of STM Fidecs about their concerns following a series of onsite visits:

In our opinion, there is nothing robust about Kentish and his various dodgy products. And the Gibraltar regulator shares our opinion as well as our concerns. In a letter dated 6.11.2017, the GFSC wrote to the directors of STM Fidecs about their concerns following a series of onsite visits:

I will, of course, be more than happy to help Deloittes see the whole picture – rather than just what the Fraudsters want them to see. I will happily buy a whole shed full of spades as well as several boxes of latex gloves and surgical masks. However, the most important way in which I can assist them is to give them details of the various scams which the Fraudsters have operated and facilitated.

I will, of course, be more than happy to help Deloittes see the whole picture – rather than just what the Fraudsters want them to see. I will happily buy a whole shed full of spades as well as several boxes of latex gloves and surgical masks. However, the most important way in which I can assist them is to give them details of the various scams which the Fraudsters have operated and facilitated. Deloittes will need to concentrate on at least three main areas: Trafalgar Multi-Asset Fund;

Deloittes will need to concentrate on at least three main areas: Trafalgar Multi-Asset Fund;