Pension scammers have a “code”. Rather like pirates, they are not to be trusted. They pick their words carefully, revealing little; they are sneaky and lack any morals. They are good at disguises and if they fear they may be rumbled, they will disappear over the horizon, never to be seen again. They certainly won’t hang around to help pick up the pieces after their victims have been ruined. Rest assured, they will take as much as they can get and show no remorse. Living the Life of Riley on your hard-earned money is their reward.

“Yo ho, yo, ho! A scammer’s life for me”.

Those of you who follow Pension Life, will know that we want to put a stop to pension scammers and are trying our hardest to get as much information as possible out to the public about how to avoid being scammed. We want to educate the masses and stop pension scammers worldwide.

Those of you who are new readers, may not be aware of how common pension and investment scams are, or how easily you could fall victim to a pension scam. But never fear, we have constructed a series of blogs, videos and cartoons for you to read and watch, so you can swot up on the dos and don’ts when it comes to safeguarding your precious pension fund.

This video has been constructed to show you the pension scammers’ code of conduct. By familiarising yourself with their techniques, you will be better prepared to spot the scammers and avoid falling victim to their schemes.

Please look through our archives and read about past scams, serial scammers and failures of the regulators and police to bring them to justice for their crimes. Make sure you know all there is to know about the evil and seemingly unstoppable world of pension scammers.

Above all, read the Trolley’s guide, and see how scammers learn their highly-profitable and destructive trade. Scammers learn from the best – including theauthor of this guide. And then they bring their own individual touch to the art of scamming.

Katar Investments say they give UK and overseas investment advice in a simple way. However, the types of investment opportunities they are offering are, unfortunately, once again, making my red beacon flash. So, with Déjà vu, let me tell you why. Please make sure you are comfy, this might take a while!

Firstly, I had a quick look into their team. In my opinion, you would hope that some of the people advertising about giving you advice on investments would hold some sort of financial qualification. However, out of the five team members listed only one mentions a background in finance, the others only list sales experience.

I had a quick check on the registers to see if the one team member who states she has 10 years´ experience in the financial sector, holds any qualifications with the CII, CISI etc. – she did not appear to have any registered financial qualifications.

Now, forgive me if I am slightly biased and ever so critical when it comes to firms giving investment advice, but I would hope that any firm giving me advice on what to invest in, would have a team of fully qualified financial advisers. Not just sales experts. Or am I just being fussy?

Katar Investments state:

“Whether you are looking for a steady income investment, a property investment with high capital growth and a quick turn around of your capital or an opportunity in the latest emerging market, we have something to offer you.

We are highly committed to our investors and are focussed (their spelling mistake – not mine) on delivering a level of customer service which is above and beyond. So rest assured our agents will strive to provide you a class A service when you Invest with Katar Investments.”

I feel that the salespeople who work for Katar Investments may well be driven solely by earning high commissions when it comes to offering class A services. But, again, maybe I am biased! Let’s move on to what investments they offer.

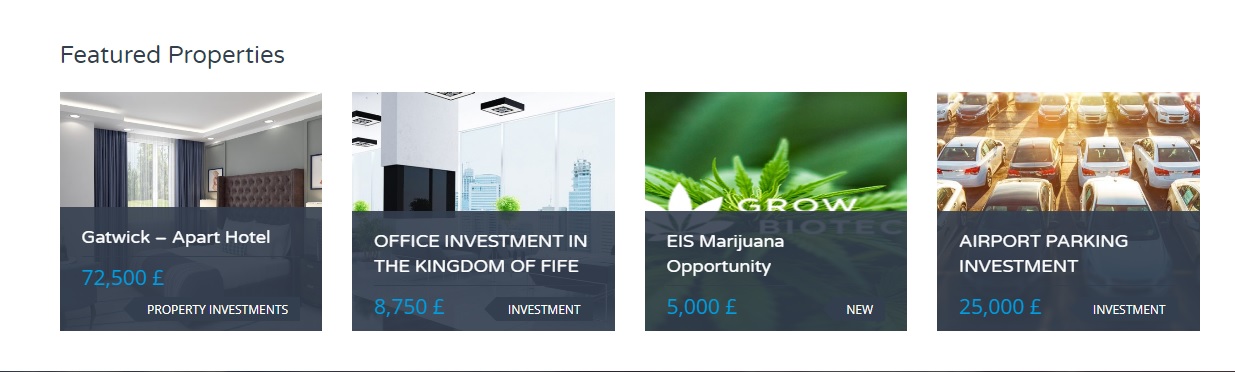

Gatwick – Apart Hotel – This is a serviced apartment/Hotel investment with a minimum investment of 72,500 GBP. The figure states “from”, so I assume you can throw a bit more in for good measure. The promised outcomes:

12 Months rental paid in advance

Rental protected by Insurance

5 Years Rental 8%

2% profit paid on exchange deposit during refurbishment

7 days free stay subject to 1 months notice

Buy back at 110% after 10 years

40% Finance on units over £140,000

Luxury furniture pack included with every purchase

Completion date: March 2019

This is a fixed term investment of 10 years and it has not been built yet (check the completion date). To me, an investment like this would ring alarm bells, as you are purchasing property that has yet to be completed. All sorts of hiccups could occur before the investment was up and running. An illiquid, high-risk investment, only for those who can afford a potential loss on the funds used.

This means your money is trapped for an awfully long time. If the market sways, you could be set for a loss and often with fixed-term structured investments there are fees and charges. Investments like this can, if they go wrong, result in you, the investor, falling into negative equity.

EIS marijuana opportunity – Grow Biotec, there is a lot of press going around at the moment into the medical uses of marijuana and possibilities of a change in legislation in the UK. In many states of America, the use of marijuana for medical use has been decriminalized. As an avid supporter of natural remedies and healing through nature, the use of CBD extracted from the marijuana plant interests me immensely, the idea of investing in this potentially lifesaving product does have a certain draw.

But, there is always a but! Since working for Pension Life, any investment opportunity that quotes the word ´bio´ gives me the heebie-jeebies. We have only to look back and remember the Elysian Bio Fuels liberation scam promoted by James Hay. The victims of this scam have been left penniless AND with huge tax bills from HMRC.

Another ´bio´investment disaster was Sustainable Agroenergy (SAE) Plc, investors were told their investments were in biofuel products, that land was owned in Cambodia and planted with Jatropha trees – a tree with highly toxic fruit that could be used to produce biofuel. Unfortunately, the Jatropa trees were not as fruitful as originally thought. The perpetrators, were thankfully convicted of fraud and bribery offenses.

The reasons I doubt this as a good investment are the vague promises and the over promises.

´It is a private offer raising £5 million to develop one of the world’s most valuable portfolios of cannabis-IP assets by 2022.´

What will be the outcome should this £5 million not be made? A possibility of loss of all or part of your investment.

´We are seeking to develop one of the world’s most valuable portfolios of cannabis-IP assets by 2022.´

Meaning this is a fixed-term investment, with potentially no return for at least 4 years, if not longer, AND only if successful.

Projected high returns: Target return of £50 per £1 invested (not guaranteed)

EIS Tax relief: up to 50% income tax and capital gains tax relief. Remember tax rules can change and benefits depend on circumstances.

If it sounds too good to be true – it probably is. Plus this figure is not guaranteed and seems to me like it was just plucked out of the sky, nice and high, to lure investors in.

These investments are what we in the industry call illiquid. Once your money is in, then it´s pretty hard to get it out quick AND unless the venture does well there will be no return. With regards to pension investments, these are the very worst, toxic assets to invest in.

Unfortunately, they are often the assets which pay handsome investment introduction commissions to the salesperson, and this is why serial scammers, like Ward, love them. They go in with the ´eco-bio´ sale pitch or the glamorous property ownership – withholding the high-risk, fixed-term rules surrounding the investment.

A pension fund is a retail investment that should be placed in a low to medium-risk asset. Fixed terms, high-risk and illiquid investments should be avoided at all costs.

The types of investments offered by Katar Investments are high-risk and illiquid, if you have a spare five grand that you can afford to lose, then go for it: have a cheeky punt on Bio Grow. You may be pleasantly surprised and get the target return of £50 per £1 invested (just remember to duck smartly when those pink things with curly tails fly a bit too close!). However, if your money is dear to you and you cannot afford to lose it, please stay away from shiny pink and green investments like this.

When it comes to your precious pension fund it is always best to air on the side of caution and go for the safe bet. It might not pay the highest interest, however, slow and steady wins the race. Meaning you will be able to enjoy your hard earned pennies in your retirement – stress free.

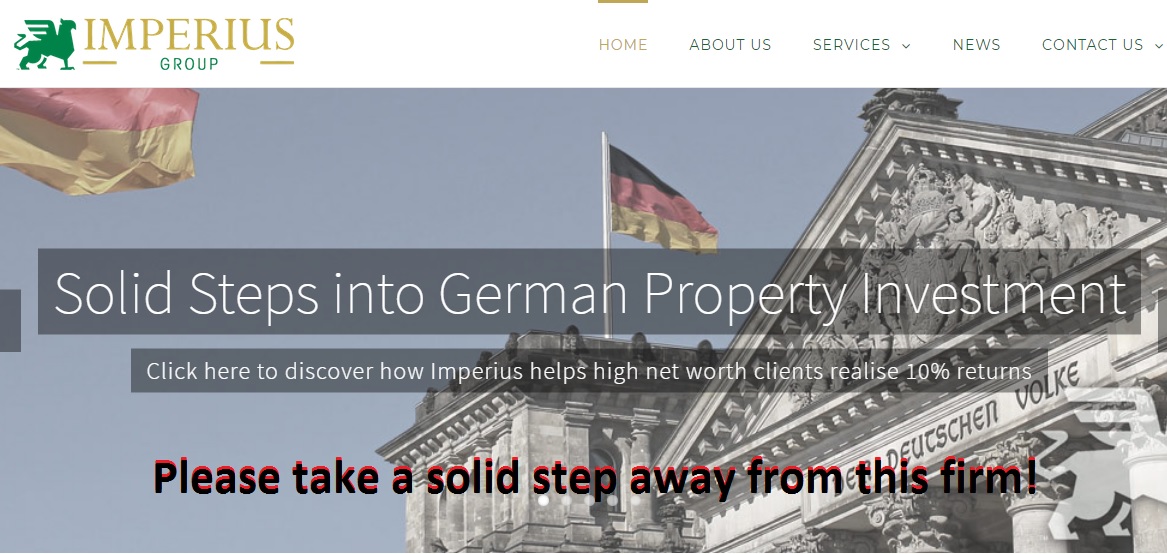

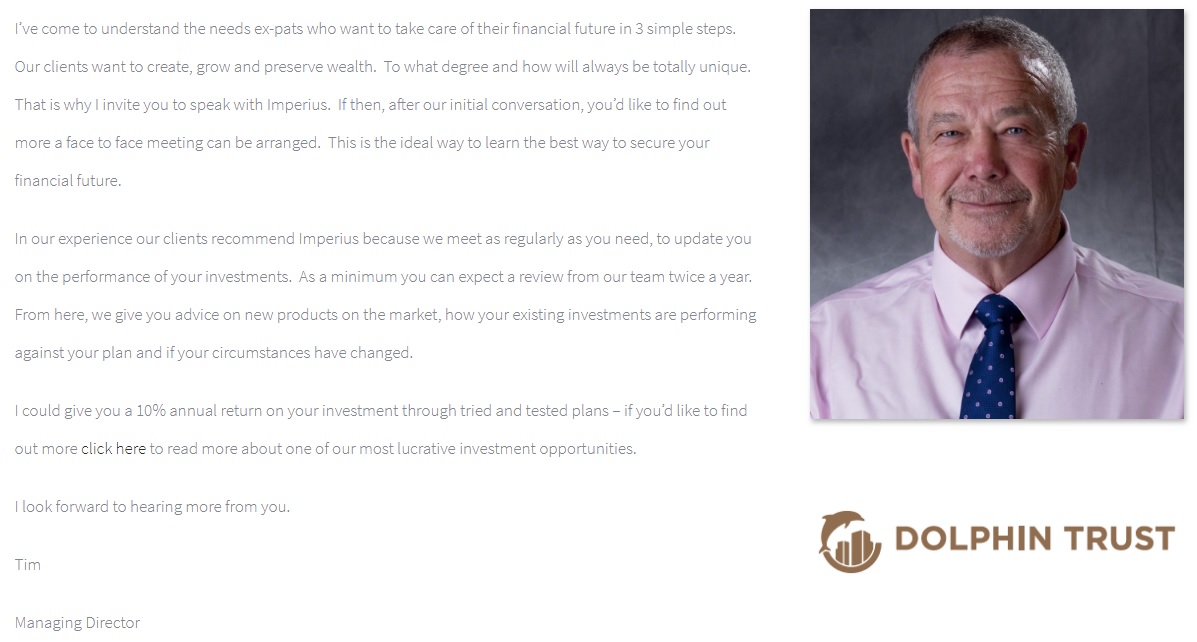

In my weekly hunt for the next firm to feature in my ´qualified and registered?´ blog series, I came across an advisory company that caught my attention: The Imperius Group, run by a fella named Tim Blogg, who claims to have retrained 25 years ago to offer pension and investment advice to expats.

The reason Tim Blogg´s company, The Imperius Group, flashed up on my red beacon radar was the fact that he listed his company in partnership with various life assurance offices including OMI (Old Mutual International) and Generali. Links to these companies, a well-read Pension Life blog follower will know, is not a good thing. They are also linked to RL360 and Hansard Global.

Tim Blogg also has a bright and shiny Dolphin Trust logo underneath the mug shot of him and a promise of:

“I could give you a 10% annual return on your investment through tried and tested plans – if you’d like to find out more click here to read more about one of our most lucrative investment opportunities.”

Tim Blogg offers “strong steps into German property investment”, through Dolphin Trust (loan notes).

Ring any bells?

British Steelworkers were duped into investing their DB pension schemes into – yes, you´ve got it – into an unregulated fund: Dolphin Trust (in Germany). Celtic Wealth Management acted as the introducers to this investment and Active Wealth – now collapsed – acted as the advisory company. This investment scam has left British Steelworkers trapped and at risk in this totally unsuitable, unregulated investment.

Dolphin Trust IS NOT regulated and there is no evidence to show The Imperius Group is either.

Tim Blogg, founder of The Imperius Group, DOES NOT APPEAR ON ANY REGISTER as a qualified and registered financial adviser.

Aside from Tim Blogg, the only other person who claims to work for The Imperius Group is a lady called Emma Allen, listing herself as, ´Employed as a Personal Assistant by iBOS working for the Managing Director of The Imperius Group Limited.´ The Imperius Group website quotes the term ´us´ regularly, but from what I have found, it would seem this company is pretty much a one-man unqualified band.

Once again, I am left wringing my hands in despair at the state of the offshore financial sector and at purported financial advisers like Tim Blogg.

However, at least I will sleep soundly tonight knowing that another financial advisory firm has been outed. The Imperius Group and Dolphin Trust are not the company to trust with your precious pension fund.

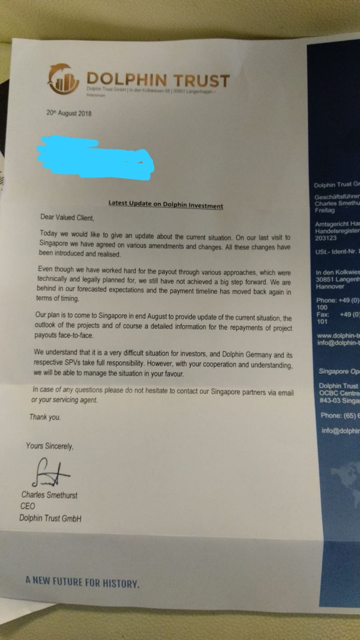

To demonstrate the serious concerns about investments in Dolphin Trust, this is a copy of a letter sent by Charles Smethurst CEO of Dolphin Trust to investors. It would seem that although some investments have reached their maturity, other investors are still waiting for their funds to be released. This raises questions about the liquidity of funds and also the possibility of Dolphin Trust going bankrupt. Maybe the victims will have a claim over the properties, if indeed the German properties they think they have invested in actually exist.

In the Royal London v Hughes case, Royal London suspected an attempted transfer was destined to go into a scam and blocked it. The member, Ms Hughes, complained to the Pensions Ombudsman – but he did not uphold her complaint. He said that Royal London was quite right to block the transfer. But Ms Hughes appealed the matter to the High Court and the judge overturned the Ombudsman’s determination.

The industry was, naturally, appalled. But this matter left many questions unanswered:

Why was a singing teacher so desperate to transfer her £8,000 pension and have it invested in Cape Verde property? (Had she developed a passion for collapsible flats?)

Where did she get the many thousands of pounds it must have cost her to have a barrister represent her in the High Court? (Considerably more than eight thousand quid I reckon).

How come the mighty Fenner Moeran QC (for Royal London) got so soundly defeated by a public access barrister? (Was his sharp stick a bit blunt that day?)

What happened to the several hundred people queuing up behind Ms Hughes to have their pensions invested in Cape Verde flats? (“Flat” being the operative word).

I could ask loads more pertinent and searching questions – like why did Ms Hughes’ public access barrister, Frances Ratcliffe of Radcliffe Chambers, think it was a good use of her considerable skills to defend an obvious pension scam? How drunk was the judge on the day? How many more people got scammed out of their pensions because of this abomination – and proof the law is not just an ass but a whole donkey farm?

Anyway, enough already. The damage was done in the Royal London v Hughes case. And now, hopefully, the door to justice has been opened in the Police Authority v Mr N case – as eloquently reported by Henry Tapper in his blog on 2.8.18. But there is a great deal more work to be done on this now: the scammers who organised and promoted the London Quantum scam need to be prosecuted and jailed; and the FCA-regulated firm – Gerard Associates – which gave the advice to the police officer (Mr N) needs to be sanctioned by the FCA. Gerard Associates – run by Stephen Ward’s associate Gary Barlow – also needs to refund the £5k they charged Mr N – and indeed all of the £220k they charged the 98 London Quantum victims.

Now is the time to bring to justice not only the pension scammers, but also the negligent ceding pension trustees who allowed the scammers to succeed – and facilitated financial crime.

At the time Mr N was scammed by Stephen Ward; Viva Costa International (the “introducers”); and FCA-regulated advisers Gerard Associates, the Pensions Regulator’s “Scorpion” campaign was in full flow. But it was unbelievably inept. It only really talked about liberation and ignored the many other kinds of fraud being perpetrated at the time – i.e. investment fraud.

The London Quantum pension scam came hard on the heels of the Capita Oak and Henley scams – which straddled the Scorpion watershed of February 2013. The transfer administration for Capita Oak was done by Stephen Ward of Premier Pension Solutions (Spain) and Premier Pension Transfers (Worsley, Manchester). Ward knew from first-hand experience how ceding trustees were starting – albeit agonisingly slowly and gradually – to resist transfer requests.

Here is evidence of the first tentative – and very inconsistent – moves to do some long-overdue diligence on pension transfer requests – as reported by Stephen Ward’s team of transfer administration scammers:

24.4.2013 – ReAssure Pensions – “The scheme now want the client’s application and new-dated screenshot emailed to Alan (Fowler – Ward’s pension lawyer chum) – on hold at Tom’s (Biggar – XXXX XXXX’s mate) request”.

11.4.2013 – Prudential – “Transfer canceled as per XXXX (XXXX XXXX’s wife)”

26.4.2013 – Zurich – “Unwilling to process – not sure why – need to cancel”

11.7.2013 – Zurich – “On hold as there may be an issue with Scorpion”

26.4.2013 – Friends Life – “Awaiting trust scheme rules – with Anthony (Salih – Ward’s mate) – need to cancel”

30.5.2013 – Aviva, NHS, Co-op, Friends Life – “Schemes are refusing to transfer”

11.6.2013 – Scottish Life – “Scheme contacting client – believed not transferring”

However, during this same period, there were plenty of transfers being made in defiance or ignorance of Scorpion. These included ceding schemes NHS (£43k), Scottish Widows (£25k), LGPS Newham (£47k), Aviva (£54k), Xerox £92k, Zurich (£21k), Prudential (£25k) and Standard Life (£53k).

But the most worrying was the Firefighters Pension Scheme: £69K after the following notes were made:

“Advised that the trustees committee are meeting to discuss cases and we are awaiting a call back next week. Transfer sent today 2.7.13 and paid on 16.8.13. Statement sent to XXXX and Tom (Biggar)”.

So the Firefighters were no better than the Police Authority in terms of ignoring the Scorpion warning.

And here is what the Scorpion warning was saying from 2013 onwards – and, indeed, was still saying in 2016 when the last couple of hundred Continental Wealth Management victims were in the process of being scammed:

Predators Stalk Your Pension

Companies are singling out savers like you and claiming that they can help you cash in your pension early. If you agree to this you could face a tax bill of more than half your pension savings.

Don’t let your pension become prey.

Pension loans or cash incentives are being used alongside misleading information to entice savers as the number of pension scams increases. This activity is known as ‘pension liberation fraud’ and it’s on the increase in the UK.

In rare cases – such as terminal illness – it is possible to access funds before age 55 from your current pension scheme. But for the majority, promises of early cash will be bogus and are likely to result in serious tax consequences.

What to watch out for?

Being approached out of the blue, over the phone or via text message

Pushy advisers or ‘introducers’ who offer upfront cash incentives

Companies that offer a ‘loan’, ‘savings advance’ or cash back’ from your pension

Not being informed about the potential tax consequences

Five steps to avoid becoming a victim

Never give out financial or personal information to a cold caller

Find out about the company’s background through information online. Any financial advisers should be registered with the FCA

Ask for a statement showing how your pension will be paid at retirement and question who will look after your money until then

Speak to an adviser that is not associated with the proposal you’ve received, for unbiased advice

Never be rushed into agreeing to a pension transfer

If you think you may have been made an offer, contact Action Fraud.

But, the Scorpion warning failed tragically in so many different ways:

The warning only talked about liberation. Many victims thought this warning didn’t apply to them as they had no intention of liberating their pension fund

No information was given on how to find out about a company’s background – and how to establish whether it was regulated

The warning talked about advisers being FCA regulated – but ignored the question of offshore advisers who obviously wouldn’t be FCA regulated

The public was advised to contact Action Fraud – but did not disclose that Action Fraud would do absolutely nothing

In 2015, we went to see the Pensions Regulator to talk about the failings of the Scorpion campaign – as well as the failings of the Regulator. Two Ark victims and I met the then Executive Director for Regulatory Policy – Tinky Winky. Our intention was to explain to him how the Scorpion campaign had failed and how it needed to be made more robust and comprehensive.

Tinky Winky, flanked by two lawyers and a paralegal, told us to “hop it” – and warned us that if we tried to interfere with the authority of the powers of the regulator, our arse would be grass and he’d be a lawnmower. A year later the Scorpion warning had still not been updated or improved and hundreds more victims lost their life savings.

The Pensions Ombudsman is, naturally, the hero of the hour in the Mr N v Police Authority case. And hopefully, he will find for the rest of the victims if they all now bring complaints against their negligent ceding trustees in the London Quantum case. But we must remember that, contrary to what the Ombudsman’s service has said for the past few years, the industry did know about pension scams long before the Scorpion Campaign in February 2013.

In fact, a clear warning had been given in 2010. The Pensions Regulator had been fully aware that since 1999 pension scams were on the increase, and yet did not make it clear to ceding pension trustees what their statutory obligations were in respect of transferring victims into scams. On 13.7.2010, tPR Chair David Norgrove stated that: “Any administrator who simply ticks a box and allows the transfer, post July 2010, is failing in their duty as a trustee and as such are liable to compensate the beneficiary.”

But pension trustees claim they never read that message (let alone heeded it) and that it was neither publicised nor distributed. Further, in the same year Tony King, the Pensions Ombudsman, reported that he had “found that pension trustees failed in carrying out serious fiduciary responsibilities to others in circumstances in which the law specifically states that they should not be protected from liability.” And still tPR did nothing. And the Pension Schemes Act 1993 was not amended to reflect the urgent need to protect the public.

The Pensions Regulator’s predecessor – OPRA (Occupational Pensions Regulatory Authority) had warned about the dangers of pension scams years before 2013 – as had HMRC. The last thing I want to do is criticise the Ombudsman – as this must be his hour of glory and we must all be hugely grateful to him. Especially Mr N and his fellow London Quantum victims. But we must remember that the industry in general, and pension trustees in particular, should have been alert to pension scams long before Scorpion.

Now is the time to bring to justice not only the pension scammers, but also the negligent ceding pension trustees who allowed the scammers to succeed – and facilitated financial crime.

Among the flood of apathy, laziness and callousness by ceding pension trustees since at least 2010, we now have a Pensions Ombudsman’s determination which will hopefully result in more trustees being brought to account – and more victims getting justice.

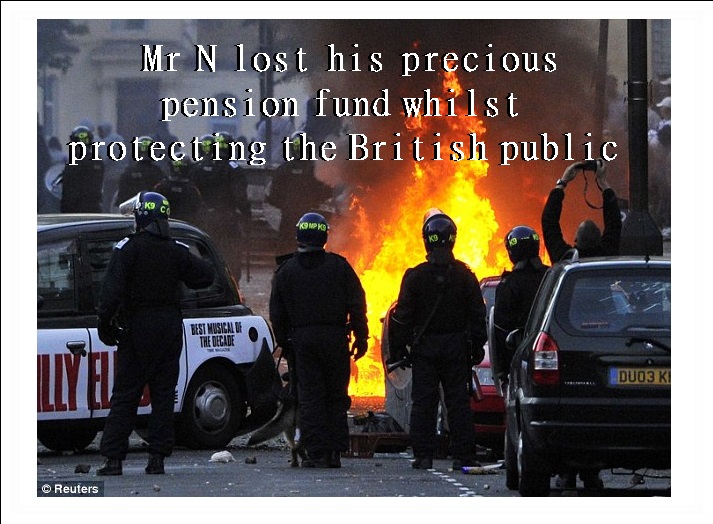

The London Quantum victim who made the complaint to the Pensions Ombudsman – Mr. N – is a serving police officer with the Northumbria Police Authority. In October 2014, he was scammed out of his Police final salary pension scheme and into Stephen Ward’s pension scam: London Quantum.

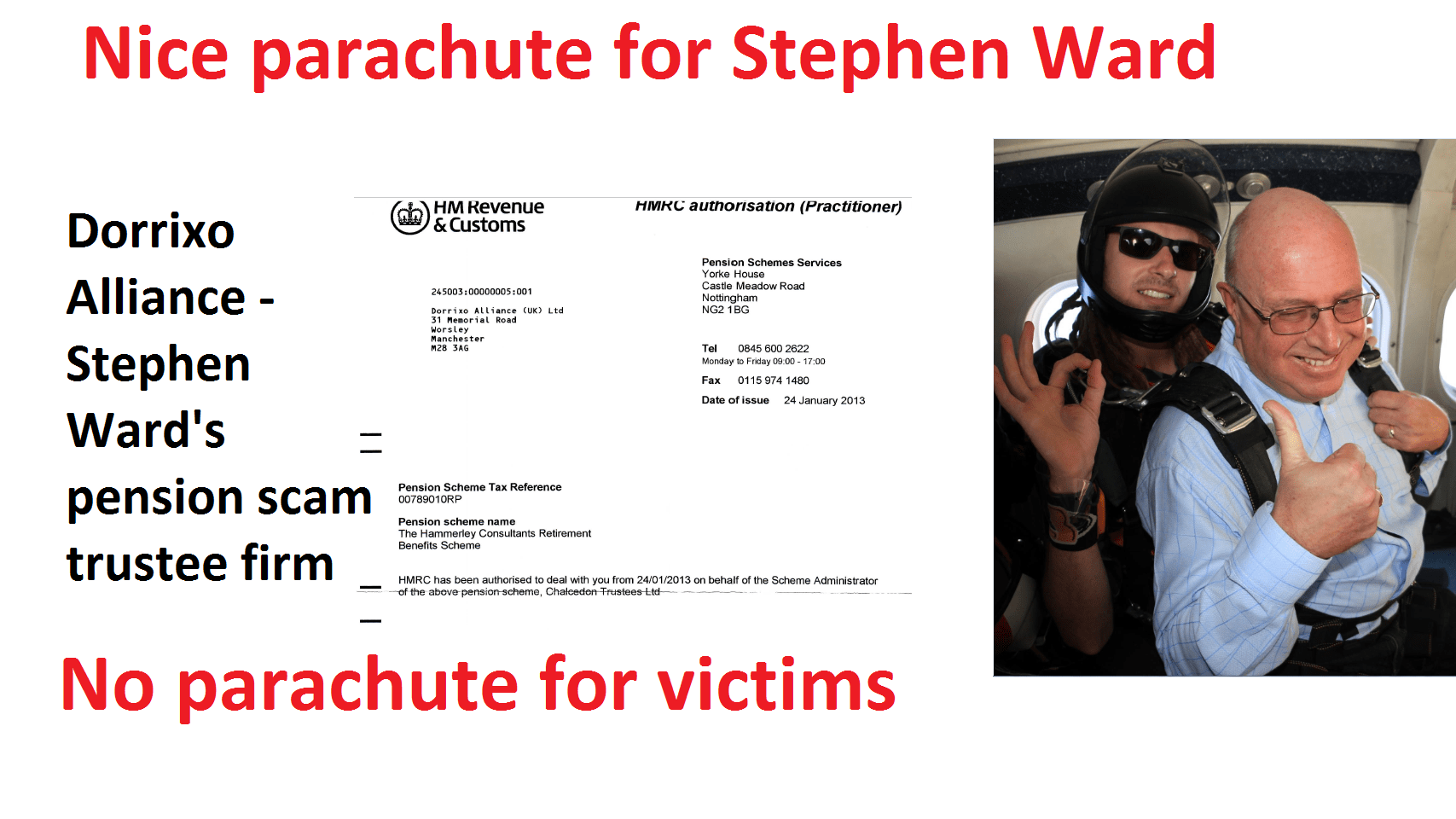

It is worth noting that, in May of 2014, I went to London and handed HMRC evidence of Stephen Ward’s various pension scams – including his pension administration and trustee firm: Dorrixo Alliance (the trustee for London Quantum). But HMRC did nothing – and hence Mr N (along with 97 other victims) got scammed into London Quantum just a few months later. The fact that if HMRC had done its job this would have been prevented is an absolute disgrace.

It is also worth noting that HMRC met with Stephen Ward in February 2011 to discuss the Ark pension scam – so they were fully aware back then that Ward was heavily involved with pension fraud. And yet they cheerfully registered pension schemes such as Hammerley for his firm Dorrixo Alliance which was registered at his UK address: 31 Memorial Road, Worsley.

We have warned about the significant dangers of unregulated firms, unqualified advisers, bogus occupational schemes, toxic investments and liberation fraud for years. Yet still, the ceding trustees have stubbornly ignored us – and also ignored the Pensions Regulator’s Scorpion campaign (published in February 2013).

And now the chickens have come home to roost thanks to the Pensions Ombudsman’s determination in Mr N’s favour – and hopefully this will bring to justice to more victims of negligence by similarly lazy trustees.

Highlights from the Pensions Ombudsman’s determination are quoted below – with my comments in bold. First, however, it is important to understand the background and put the Police Authority’s negligence into context.

In 2010/11, dozens of trustees handed over £ millions to the Ark scam. The worst offender in the personal pension sector was Standard Life; the worst offender in the DB sector was Royal Mail – by a royal mile. We were denied permission to bring complaints to the Pensions Ombudsman as the Ark transfers were effected prior to February 2013 – the date the Pensions Regulator’s “Scorpion” warning was published.

And this, of course, was a great shame. Because Standard Life and Royal Mail – along with dozens of other negligent trustees – went on to hand over more £ millions and ruin thousands more lives. Three of the other worst-performing personal pension trustees in the subsequent Capita Oak and Westminster scams (now under investigation by the Serious Fraud Office) were Scottish Widows and Prudential.

None of these lazy, box-ticking ceding providers has ever paid redress to their victims (to our knowledge). Further, in the case of Royal Mail, PASA (Pension Administration Standards Association) has given Royal Mail trustees not one but two accreditations – despite the fact that they have never compensated any of their members for handing over their pensions to the scammers.

Before we look at the determination, let us look at a depressingly common thread which runs through these pension scams.

In 2010/11, Stephen Ward (Level 6 qualified, former pensions examiner) was promoting and administering the Ark pension liberation scam. 486 victims lost £27 million worth of pensions and face £ millions in tax charges. The schemes are now in the hands of Dalriada Trustees and Stephen Ward has never been prosecuted. Dozens of ceding providers handed over hundreds of personal and occupational pensions without question.

In 2012, Stephen Ward was promoting and administering the Evergreen New Zealand QROPS/Marazion liberation scam. 300 victims lost £10 million worth of pensions and face £ millions in tax charges. The scheme is now being wound up and Stephen Ward has never been prosecuted. Dozens of ceding providers handed over hundreds of personal and occupational pensions without question.

In 2012/13, Stephen Ward was administering the Capita Oak liberation scam (now under investigation by the Serious Fraud Office). 300 victims lost £10 million worth of pensions and face £ millions in tax charges. The scheme is now in the hands of Dalriada Trustees and Stephen Ward has never been prosecuted. Dozens of ceding providers handed over hundreds of personal and occupational pensions without question.

In 2013, Stephen Ward was administering the Westminster liberation scam (now under investigation by the Serious Fraud Office). 200 victims lost £7 million worth of pensions and face £ millions in tax charges. The scheme is now in the hands of Dalriada Trustees and Stephen Ward has never been prosecuted. Dozens of ceding providers handed over hundreds of personal and occupational pensions without question.

In 2014, Stephen Ward was promoting and administering the London Quantum pension scam. 100 victims lost £3 million worth of pensions. The scheme is now in the hands of Dalriada Trustees and Stephen Ward has never been prosecuted. Dozens of ceding providers handed over hundreds of personal and occupational pensions without question.

I apologise if the above is somewhat repetitive. I did omit the dozen or so other schemes that Stephen Ward was also promoting which might have mixed it up a bit – as none of these is in the hands of Dalriada (yet).

Ombudsman’s Determination Applicant Mr N Scheme The Police Pension Scheme (the Scheme) Respondent Northumbria Police Authority (the Authority) Complaint Summary

“Mr N” (a serving Police officer) complained that the (Police) Authority transferred his pension fund to a new pension scheme (the London Quantum scam) without having conducted adequate checks in relation to the receiving scheme, and failed to provide him with a sufficient warning as required by the Pensions Regulator.

Mr N did indeed complain – and has been complaining for four years. To put his complaint into context, he was advised to make the transfer by a regulated advisory firm: Gerard Associates – run by Gary Barlow. Both the firm and Mr Barlow are on the FCA register. Barlow is also Level 4 qualified with the CII http://www.cii.co.uk/web/app/membersearch/MemberSearch.aspx?endstem=1&q=n&n=gary+barlow&c=&ch=0&p=0

The complaint is upheld against the Authority because it failed to conduct adequate checks and enquiries in relation to Mr N’s new pension scheme; to send Mr N the Pensions Regulator’s transfer fraud warning leaflet; and to engage directly with Mr N regarding the concerns it should have had with his transfer request, had it properly assessed it.

The ceding provider in Mr N’s case – the Police Authority – has been denying for almost four years that they were negligent (well they would – wouldn’t they!). But surely, of all providers, the Police pension trustee ought to have known better. The Police were involved in Project Bloom – the multi-agency project including regulators, police authorities and HMRC that aimed to combat pension fraud.

In February 2013, the Pensions Regulator issued an action pack for pension professionals headed “Pension liberation fraud – The predators stalking pension transfers”. This said that: “Government enforcement agencies and advisory services have worked to produce a short leaflet that you (the ceding pension trustee) can use to help pension scheme members understand the risks and warning signs of pension liberation fraud.

But, of course, the Police Authority – along with hundreds of other ceding providers – totally ignored this warning and doomed thousands of victims to financial ruin by cheerfully handing over victims’ pensions to the scammers.

Mr N received a phone call from Viva Costa International, an unregulated introducer of work to independent financial advisers, and was referred to Gerard Associates Limited (Gerard), a firm of financial advisers.

The unregulated “introducer” has been the scourge of financial services in the UK and offshore for years. They con victims into believing they are some kind of qualified and regulated “adviser”, but in fact they are nothing more than slimy salesmen chasing commission. Of even greater concern, however, was the fact that there was an FCA-regulated firm – Gerard Associates – involved in this scam. Gerard Associates, run by CII qualified Gary Barlow, had a track record of working with Stephen Ward of Premier Pension Solutions – helping him with his various pension scams.

The London Quantum Retirement Benefit Scheme (London Quantum) was subsequently recommended to Mr N. Based on the information available, London Quantum appears to be a defined contribution occupational pension scheme established in 2012. The sole sponsoring employer of London Quantum was Quantum Investment Management Solutions LLP, based in offices in London. That company is now in liquidation. London Quantum was originally administered by Dorrixo Alliance (UK) Limited (Dorrixo). Dorrixo became the trustee of London Quantum in 2014.

London Quantum was, in fact, a bogus occupational scheme. Dorrixo Alliance was a firm run by Stephen Ward of Premier Pension Solutions and used for a variety of his pension scams.

Gerard took a fee of nearly £5,000 out of the transfer payment. On 11 November 2014, Mr N received confirmation that the transferred funds had been invested. In 2015, Mr N looked again at the documents that he had been given in 2014, and was concerned to note that he had signed up to a high risk investment as a sophisticated investor. He was unable to obtain satisfactory responses from Gerard or Dorrixo about this.

(Note: Gerard have never refunded the £5,000 to Mr N – and, presumably, have held on to the fees charged to the other 97 victims). This is entirely typical of how pension scams work. Mr N was in fact invested in high-risk, toxic, illiquid, speculative funds which were totally unsuitable for a pension fund. The only parties who benefited from this transaction were the scammers themselves, as they would have received high investment introduction commissions. The investments included:

Quantum PYX Management FX Fund – risky and illiquid forex trading

Park First – UK airport car parking spaces

Best Asset Management – Dubai car parking spaces

The Resort Group – holiday properties in Cape Verde

Reforestation Group – eucalyptus plantations

Colonial Capital (three-year bonds in distressed US property)

ABC Alpha (four-year bonds in business centres)

Most of these assets would have paid commissions to the scammers of up to 30%.

I note that Mr N’s transfer request was received by the Authority in November 2013, nine months after the Pensions Regulator’s pension liberation fraud guidance of February 2013 was issued, and his transfer was completed in August 2014. The pensions industry was aware of pension scams before the scorpion warning was published.

It is ironic – as well as extremely sad – that the Police Authority took no notice of the regulator’s fraud warning. And the victim who paid the price for this disgusting negligence was a serving police officer.

The Authority has admitted that it did not send Mr N a copy of the scorpion warning. The scorpion warnings were designed to be sent individually to scheme members. So, I am satisfied that maladministration has occurred.

It is indeed utterly disgusting that the Police Authority failed to send one of their own officers (who was indeed contemplating a transfer) a copy of the scorpion warning.

The next question is whether the Authority only had to send the scorpion warning to Mr N, or should have done more. I consider that it should have done more. I accept that when Mr N made his transfer request London Quantum was not a new scheme. However, the Authority ignored a number of features which other pension schemes identified as potential ‘red flags’ and accordingly refused transfer requests to that arrangement. These included that London Quantum was sponsored by a dormant company that was registered at an address far removed from the scheme member.

It has long been a disgrace that ceding providers have allowed members to transfer to a bogus occupational scheme – the sponsor of which neither traded nor employed anybody (or ever intended to do so). Justice Morgan’s overturning of a Pensions Ombudsman’s determination in the Hughes v Royal London case appalled the industry and the public. Morgan determined that a member only had to have earnings – rather than earnings with the sponsor of the scheme.

The Authority was fully aware, however, that although Mr N was a deferred member of the Scheme he was still employed as a policeman in Northumberland and he was still living in that county. The question of why he was requesting a transfer to an occupational pension scheme sponsored by a company that he did not work for, and based at the other end of the country, appears not to have concerned the Authority. I consider that the Authority should have had concerns about London Quantum, even the name might have rung alarm bells for a North-Eastern employer, and therefore it should have made some enquiries about London Quantum before it allowed the transfer to be made. Unfortunately, it failed to do so.

The Authority took the view that Mr N’s proposed transfer had none of the features of a potential pension transfer scam. However, I do not agree. In several previous determinations, we set out the type of due diligence expected of transferring schemes.

Within 28 days of the date of this Determination the Authority shall reinstate Mr N’s accrued benefits in the Scheme and pay Mr N £1,000 to reflect the materially significant distress and inconvenience that he has suffered as a result of the Authority not making appropriate checks in respect of London Quantum, and not giving Mr N the appropriate warnings.

Hopefully, now the Ombudsman will find in favour of thousands of other victims of pension scams facilitated by negligent, lazy, box-ticking ceding providers. However, the £1,000 “compensation” (for distress and inconvenience) order by the determination does not scratch the surface in terms of making up for the ordeal that Mr N has gone through. And he has suffered this profound torment while protecting the British public in the North East of England this past few years.

I’ve been very concerned about Dolphin Trust GmbH for some time. There’s an awful lot of pension money being loaned to this company – and I don’t get to hear of many (in fact any) people who have had their loans repaid. That doesn’t mean they haven’t been repaid – it just means I haven’t heard about it.

The things that bothers me about Dolphin Trust are:

“Introducers” get paid eye-watering commissions of up to 25%

If the assets and projects are so good, why pay private lenders 10% interest (on top of the 25% commission) – why not just go to the bank?

I have recently heard that Dolphin and some of their dodgy “introducers” are now trying to convince lenders to take their loans back in the form of shares in the company

But the biggest concern I have is that Dolphin Trust formed a major part of the underlying investments in the Trafalgar Multi-Asset Fund scam – run by XXXX XXXX of Global Partners Limited and STM Fidecs in Gibraltar. This fund is now being wound up by Stephen Doran, of Doran + Minehane.

The Trafalgar Multi-Asset Fund and XXXX XXXX are currently under investigation by the Serious Fraud Office. Ironically, Justin Caffrey of Harbour Pensions once told me that XXXX came to see him to try to flog the obviously dodgy Trafalgar fund. Caffrey claimed he could see XXXX was an obvious spiv straight away and that Trafalgar was clearly bad news – so he sent the ginger scammer packing.

And then STM Group bought out Harbour Pensions and got custody of some of Caffrey’s Blackmore Global Fund worthless crap to keep the Trafalgar Multi Asset Fund worthless crap company. You couldn’t make it up! A bunch of toxic rubbish flogged by scammers Phillip Nunn and XXXX XXXX.

STM Fidecs had notified the hundreds of victims that there would be a distribution in early 2018 once Doran + Minehane had got rid of some of the Dolphin Trust loan notes. But then STM did a U-turn and announced there wouldn’t be a distribution at all. Clearly, getting shot of the loan notes was more difficult (or impossible) than Mr Doran first imagined. Or perhaps he did get rid of them – but got shares in Dolphin Trust or Vordere instead (and this is the reason for the lack of distribution by STM Fidecs).

Any way you look at it, Dolphin Trust is looking dodgier than ever now it is well known that there are £21 million worth of Trafalgar Multi Asset Fund loan notes out there looking for a warm and cosy (and gullible) home.

Quite apart from the fact that no self-respecting introducer or financial adviser should EVER be caught selling high-risk, unregulated, non-standard “assets” in the first place, surely nobody would ever want to be caught flogging the same stuff that the likes of XXXX XXXX and Stephen Ward were making a fortune out of.

I did try to call Dolphin Trust, but they don’t answer their phone. Maybe they don’t like cold calls (which is how most victims get scammed into lending them money in the first place).

Without the benefit of any assurances from the nice men at Dolphin Trust – Charles Smethurst, Helmut Freitag, Axel Krechberger and Matthias Ruhl – we will just have to hope that Mr Doran manages to offload the second-hand loan notes that STM Fidecs allowed 400+ victims’ life savings to be invested in. Perhaps I’ll drop him a friendly note and suggest he tries ebay.

Since 2010, £millions have been lost to pension scams, thousands of victims have lost their retirement savings, large-scale misery and poverty are the terrible results. One common factor connects many of these scams: one man – Stephen Ward.

Here at Pension Life we have made a video – based on the Mastermind quiz. Lessons must be learned from the dozens of scams, headed by Stephen Ward, which ruined thousands of lives and destroyed hundreds of millions of pounds’ worth of pensions.

Premier Pension Solutions, Stephen Ward’s company in Moraira on the Costa Blanca, was responsible for the Ark pension liberation scam. Ward had advised 160 victims to transfer £10m worth of secure pensions into this scheme on the promise of having 50% of their pensions paid to them in cash. 2011 saw the Pensions Regulator place the scheme in the hands of Dalriada Trustees. The High Court called the Ark scheme a “fraud on the power of investment”.

Ward then went on to his next scam: Evergreen New Zealand QROPS and the Marazion “loans”. The “sister company”, Continental Wealth Management, was running the cold-calling operation to lure victims in – and some of the CWM salesmen were hanging around outside supermarkets to try to trap people into this scam. When Evergreen was removed from the QROPS list, Ward continued to work with CWM. It is not known how many other Stephen Ward/Premier Pension Solutions scams CWM was involved in.

Mastermind – Stephen Ward

1. Who is the owner and director of the Spanish firm Premier Pension Solutions based in Moraira on the Costa Blanca in Spain?

Stephen Ward

2. In 2010, who was running road shows in the United Kingdom to promote the Ark pension liberation schemes and recruit introducers?

Stephen Ward

3. In the Ark pension scam, which operated in 2010/11, who was the biggest introducer with more than £10m worth of transfers?

Stephen Ward

4. Who is the author of the Tolley’s Pensions Taxation Manual described as an essential reference source for all tax practitioners?

Stephen Ward

5. Who administered the pension transfer administration in the Capita Oak scam which saw 300 victims lose £10m worth of pensions and is now under investigation by the Serious Fraud Office?

Stephen Ward

6. Who handled the pension transfer administration of the Westminster pension scam which saw 79 victims lose over £3.3 million pounds to worthless investments: now also under investigation by the Serious Fraud Office?

Stephen Ward

7. Who was the trustee for the London Quantum pension scheme now in the hands of Dalriada Trustees and invested in high-risk, illiquid investments such as Dolphin Trust which paid investment introduction commissions of up to 30%?

Stephen Ward

8. Which Level 6 qualified former pensions examiner and IFA in 2014 was famously quoted as saying: “The schemes with which we are involved are completely above board. The Ark thing is history now.”

Stephen Ward

9. Who was promoting the Elysian Fuels SIPPS liberation scheme which he described as allowing members to “trouser” most of their pension fund in cash?

Stephen Ward

10. Who was the owner of the loan company Marazion which operated pension liberation loans in the Evergreen QROPS scam which saw around 300 people lose £10 million worth of pension funds?

The BSPS dilemma for steelworkers is clearly difficult with very little time to consider options and make a wise decision which will affect them for the rest of their lives.

There’s a whole team of willing voluntary professional advisers trying to provide some guidance to help people avoid making the wrong decision. This team includes eminent pensions experts including Henry Tapper (The Pension Ploughman), Al Rush, Darren Cooke and many more.

I’d like to contribute to this excellent initiative to help the scheme members – but I can’t advise how to do things right; I can only advise how not to do things wrong.

Henry Tapper, Al Rush and Darren Cooke – plus other qualified, licensed advisers generously giving their time to help the BSPS members – will give sound guidance as to the right decision to make. The Pensions Advisory Service will also help.

Here are some pointers from me – someone who represents hundreds of victims of pensions scams and has seen all the tricks, lies, false promises and smoke/mirrors in the pension scamming business.

Check that a proper adviser is licensed – in other words: regulated. You can check this out on the FCA register. Here is an example: check out Darren Cooke’s firm, Red Circle. You will see that his firm is regulated (or licensed by the FCA – Financial Conduct Authority) to carry out personal pension and stakeholder pension advice. Remember, unregulated means SNAKE OIL SALESMAN. And beware the “introducer” – which is another word for snake oil salesman. If you find the so-called adviser is not regulated – run like hell!

Beware “free” financial advice. Go to Tesco and ask if they have any free milk. Go to the Post Office and ask if there are any free stamps. Go to an accountant and ask if he will do your accounts for free. Go to your local car dealer and ask if there are any free cars. There ain’t no such thing as free. Everything has to be paid for – but make sure that all the charges, fees, commissions etc., are openly declared. If someone promises you free financial advice – run like hell!

Run a mile from “get rich quick” investment schemes. Your pension has to be invested in boring, safe, traditional assets which will grow steadily and safely. If you are offered something exciting and sexy – like eucalyptus plantations; car parks; football betting; overseas property “opportunities” and truffle trees – run like hell. If you are told that your pension will get “guaranteed returns” of 8%, 10% or 12% – run like hell!

If you are told you can have some cash out of your pension other than your 25% tax free at age 55 – or the rest at the marginal tax rate – run like hell!

If you are cold called – run like hell!

Remember, you are a sitting duck – and it is open season. Also remember, the good guys like Henry Tapper, Darren Cooke and Al Rush – as well as all the other decent, honourable, ethical advisers who are volunteering their time free to help you avoid the scammers – can give you some invaluable, generic guidance. But someone who is offering to transfer your pension into another scheme is giving you advice.

So what is the difference between actual advice and general guidance? Let us take the example of a medical practitioner: you know a doctor – say a GP – at your local tennis club. You are concerned about your health in general and the fact that you are putting on weight and get breathless going upstairs. The doctor might suggest – as in suggest – that you consider going on a diet and taking some exercise, but that you also consult your GP. That is an informal and friendly (as well as well-meaning and common sense) suggestion. But it does not constitute formal advice. A specialist would look for deeper issues such as blood pressure, signs of diabetes and any other underlying conditions to be investigated – and would prescribe specific treatment.

If all else fails, drop me an email and I will try to help: angiebrooks@pension-life.com – but meanwhile, please buy some good running shoes!

Meanwhile, take a look at just a few of the schemes for which Pension Life is representing groups of victims who have lost their life savings to the same – or very similar – scammers who will inevitably be targeting you now:

Pension and investment scams and scandals are a blight on financial services and saving for retirement. The energetic and inspired campaign by Darren Cooke of Red Circle successfully raised awareness of the problems of cold calling. But the snap general election scuppered serious traction on this and the most the government has achieved so far is to make a vague promise to talk about talking about it. But still it is not illegal, and still the scammers are scamming away merrily.

Chair of The Transparency Task Force

The Scams and Scandals team was formed as a result of inspiration by the Transparency Task Force’s Andy Agathangelou. It has attracted a group of like-minded professionals who believe passionately that a concerted effort should go into coordinating a zero-tolerance approach to scams and scandals. All members of the team are committed to producing a White Paper which can focus the minds of government ministers, regulators and law enforcement agencies on the whole problem – not just the cold calling bit.

Irrespective of which version of which political party we are talking about, the ultimate object of a successful and fulfilled life is to be happy, healthy and solvent. And this includes getting a decent education, leading a responsible and law-abiding life, and saving for a comfortable retirement. Millions of British citizens manage to achieve this goal, but sadly many thousands of them lose part of all of their retirement savings to the armies of scammers.

XXXX XXXX, one of the many pension scammers ruining thousands of victims’ lives

All these scams and scammers have caused thousands of victims to lose hundreds of millions of pounds’ worth of retirement savings. And caused untold misery – in many cases exacerbated by HMRC punishing the victims rather than the perpetrators.

The Scams and Scandals Team has a clear five-point goal:

Ban UK cold calling and fraudulent calling

We must not let this disappear off the agenda and must keep up pressure on MPs and Ministers – as well as the regulators. But this must also be extended to overseas as we already know that the UK-based cold calling outfits have made arrangements to move their operations or merely facilitate re-routing of phone numbers. However, the twilight industry of “introducing” must also be examined as this is a serious source of scam facilitation.

Support Lesley Titcomb “Scammers are Criminals”

Ms Titcomb has publicly declared scammers to be criminals

We must work with the regulators, government and law enforcement agencies to enhance existing and introduce new regulation and legislation to prevent new scams, close down known existing scams and bring those involved in conceiving, operating and promoting both to account.

Revitalise Scorpion Campaign

Fundamental to preventing scams is communication to the public of the dangers of cold calls and pension/investment scams which would include the Scorpion Campaign – but so much more as well. A key part of this exercise is the use of social media and the plan to produce a documentary and Youtube channel giving real-life examples of past and current scams. Explaining the mechanics of a scam is one thing – but showing an actual example of a victim and the scammer is bound to have even greater impact.

Write off HMRC debt where scams are proven

HMRC celebrating the tax they collect from victims of pension liberation fraud

We need the help of the government here and could do with an actuary to help us work out what the cost to the State is of taxing victims of scams. If we can demonstrate that by ruining a scam victim (who has already probably lost part or all of his pension) with the tax charge, the long-term cost of supporting the victim and his family will far outstrip the tax collected. This is especially well demonstrated in the Ark case where the victims have got to both repay the “loans” and pay the 55% tax even if the loans are repaid.

Ensure AML regs include pension scamming

TOBY WHITTAKER’S TOXIC EMPIRE WILL FINALLY BE HUFFED AND PUFFED AWAY

I would widen this to include investment scams. This is because at the heart of every pension scam there is a fraudulent investment (and/or loan). The actual pension itself is harmless as it is essentially just a box with a label on it and only becomes toxic and dangerous once you put the scorpions, snakes and cockroaches inside it. You could equally put fluffy kittens in it. It is the mis-use of the pension “box” which is the scam.

Blackmore Global is a UCIS (unregulated collective investment scheme) which is illegal to be promoted to retail, UK investors. The fund is run by Philip Nunn and Patrick McCreesh (formerly of Nunn McCreesh – the lead generation and cold calling firm which introduced around 8,000 victims to the scammers who were running the Capita Oak and Henley pension scams in 2012/13).

It is perhaps more than a little ironic that a pair of cold-callers who were facilitating hundreds of victims being transferred into schemes 100% invested in Store First store pods are now running their own investment fund – Blackmore Global.

Slater and Gordon is a very large firm of no-win-no-fee solicitors with an office in Manchester. I met their National Practice Group Leader and specialist in financial litigation and pension mis-selling in April 2015. His name is Craig McAdam. After going through the various scams I was handling at the time, and the appalling damage done by the scammers to thousands of victims, Craig was thoroughly up to speed on how the scams worked. He was also deeply committed to helping the Ark Class Action and other group actions.

Nunn McCreesh was the introducer of contacts for the pension scammers

Craig McAdam confirmed by email on 16.4.15 that he was looking forward to working with me. A week later he sent a draft engagement letter and confirmed that Slater & Gordon’s success fee would be 15% – although he did revise this up to 18% a couple of days later.

The following month Craig McAdam confirmed he would be attending a meeting with Dalriada Trustees and Pinsent Masons with members of the Ark Class Action. He also confirmed he would be talking to one of Stephen Ward’s many victims: a member of the London Quantum scheme whose trustee was Ward’s firm Dorrixo Alliance.

A month later, Craig McAdam was examining the Capita Oak pension scam run by XXXX XXXX and administered by Stephen Ward, and asked me to put forward one of the victims as a creditor. The Insolvency Service had wound up the trustee of Capita Oak: Imperial Trustees Ltd. Craig then asked me if I was happy for Grant Thornton to be appointed as the insolvency practitioner and I confirmed that indeed I was. I felt that Grant Thornton was a competent and ethical firm and could finally unscramble the mess created by the scammers behind Capita Oak and bring some form of resolution to the victims who were all introduced and/or cold called by Nunn McCreesh.

I was delighted that the same day, one of the Capita Oak victims put herself forward willingly and eagerly as a creditor and Craig McAdam confirmed this to Grant Thornton the following day. At the same time, Craig confirmed that one of the London Quantum victims was a client of Slater and Gordon and made a complaint to FCA-regulated Gerard Associates who had acted as the adviser in that case.

Later in June 2015, Craig McAdam confirmed that Slater and Gordon was instructed by the Capita Oak victim who had volunteered to be the creditor in the liquidation of the trustee of the Capita Oak scam. Craig also sent out letters of engagement to other victims.

In July 2015 I sent a copy of the Insolvency Service’s Capita Oak/Imperial Trustee Services witness statement to Craig McAdam. This statement confirmed that Philip Nunn and Patrick McCreesh’s firm Nunn McCreesh had supplied up to 300 leads a month (for 28 months) to the scammers who promoted and operated the Capita Oak scam: Jackson Francis, Sycamore Crown, Sanderson Clarke, Barncroft Associates, Nationwide Benefits Consultants, Speke Admin, Timoran Capital.

The Insolvency Service witness statement mentioned Nunn McCreesh several times:

“Members of Capita Oak indicated they were initially contacted by Patrick McCreesh of Nunn McCreesh and referred to Jackson Francis or Sycamore for the transfer of their pension to Capita Oak. I wrote to Mr. McCreesh to request a copy of any sales and marketing agreement with Jackson Francis or Sycamore and details of commission received.” Nunn McCreesh and their solicitors admitted they had been involved with the scammers and also Transeuro Worldwide Holdings – one of the main operators of the Capita Oak and Henley scams.

However, Nunn McCreesh was unable to produce copies of invoices or sales ledgers for the money received for their part in these scams. Their solicitors also confirmed that Nunn McCreesh received a commission of 8% of sales and the Insolvency Service stated that there was a “lack of transparency” by Nunn McCreesh.

The Insolvency Service also confirmed that some of the victims had been cold called directly by Nunn McCreesh.

Being in possession of the Insolvency Service’s witness statement clearly galvanised Craig McAdam into an enthusiastic confidence to take on the Capita Oak case and asked me to send him through contact details of all the members. He obviously realised that now the scam was clearly documented and the promoters – including Nunn McCreesh – were now identified without any question of doubt. It was also documented in the witness statement that Nunn McCreesh had earned £900k out of providing at least 8,000 leads for the scam – 300+ of which ended up in Capita Oak and 200+ of which ended up in Henley. It is not clear whether the 8% sales commission was on top of this. 8% of £10.8 million would have been a handsome sum indeed.

I provided Craig McAdam with contact details for the Capita Oak Class Action members and on 21.7.15 he confirmed that cases were “being opened up smoothly”. At the end of 2015, Craig attended a meeting of Class Action members and got to meet a group of victims in person. There can be no doubt that Craig, by now, thoroughly understood the wickedness of the scammers and the profound distress and impending financial ruin of the victims.

So for most of 2015, it looked like Slater and Gordon was going to represent the Capita Oak members – all of whom were initially introduced by Nunn McCreesh. And it looked like Grant Thornton was going to be appointed as insolvency practitioner to Capita Oak’s trustee – Imperial Trustee Services Ltd.

In the event, neither happened. But Capita Oak is now in the hands of Dalriada Trustees – appointed by the Pensions Regulator. And the organisers, promoters and administrators of Capita Oak are all under investigation by the Serious Fraud Office.

Slater and Gordon now represents Nunn McCreesh

In a very curious twist, Philip Nunn and Patrick McCreesh are now running the Blackmore Global UCIS. They are doing the cold calling and the pension administration, as well as running the fund. And you will never guess who their solicitor is: Steve Kunziewicz of Slater and Gordon (Manchester office). And you will never guess who their auditor is: Grant Thornton. You really couldn’t make it up.

Victims of Blackmore Global are indeed extremely distressed. They have either managed to redeem out of the fund at a loss after a protracted struggle, or they are stuck in the fund with no prospect of getting out of it any time soon (if ever).

A year ago, the underlying assets of the fund were confirmed to one victim by Optimus Fiduciaries Ltd, an IoM domiciled company managing the Optimus Retirement Benefits #1 QROPS. Further research discovered these underlying assets were a load of toxic, illiquid, high-risk crap.

Neither Slater and Gordon nor Grant Thornton will confirm what the assets are or how much they are worth – despite Nunn and McCreesh claiming the fund has “£17m under management”. However, £17m is nothing more than a meaningless figure on a piece of paper until such time as the assets are independently verified and audited. Nunn & McCreesh have promised to publish audited accounts for over 12 months now, but failed to do so. One can only assume that to do so would instantly crystallise a true value far below the imaginary £17m and result in a sudden collapse of the fund.

Nunn and McCreesh claim Meriden Capital Partners are the investment manager to the fund

I have asked Steve Kunziewicz of Slater and Gordon on numerous occasions this past couple of months to tell me what the assets are, but presumably Nunn and McCreesh won’t tell their own solicitor – any more than they will tell their own auditors. Perhaps they told the Blackmore Global investment manager, Meriden Capital Partners in Barcelona? The trouble is that Meriden Capital Partners deny that they were ever investment manager to the fund and that Nunn and McCreesh are lying.

I hope the irony of this situation is not lost on the gentle reader: Slater and Gordon solicitors and Grant Thornton being “gamekeepers turned poachers”. My suggestion to both firms is that they should choose their clients carefully and protect their public image diligently. Both firms should decide whether they want to be like Bark and Co who openly represent fraudsters, murderers, insider dealers, hackers, race fixers and other criminals. Or whether they want to be on the side of justice for victims of pension and investment scammers. Because they can’t do both.

Regulators have got to do some effective regulating

Regulators and scammers; cops and robbers; cowboys and indians. Each has their role: cowboys fire their six shooters and dodge the injuns’ arrows valiantly; cops drive their police cars at breakneck speed to corner the robbers in a dark alley; regulators waggle their flaccid willies and watch the scammers walk all over them.

In the week my great friend had his appendix out (somewhat hurriedly as it happens) I thought I would write a slight variation on the Three Sausages poem:

Regulation, regulation, regulation, Three scammers went to the station, One got crushed, one got killed, And one got a huge operation.

The sizzling scammers need to be put behind bars – and the keys need to be thrown away.

Now, I am not suggesting I want the scammers crushed or killed – nor even that they suffer the same pain and discomfort that my mate has gone through in hospital this past week. But I do want them stopped from harming more victims and destroying more life savings. And, of course, put behind bars where the only thing they can scam is the soap on a rope.

WHAT DO REGULATORS NEED TO DO AS A MATTER OF URGENCY?

All regulators in all jurisdictions where has been a history of scamming and mis-selling need to work closely with governments, tax authorities, financial crime units, ombudsmen and the press. There has to be a “zero tolerance” attitude to scams and scammers – and all those responsible have to be brought to justice. And publicly so. It is clear that most regulators – including the FCA – are limp, lazy and useless and this has to change. Here are some examples of regulators’ failures in each jurisdiction:

Allowing unregulated firms to provide financial, pension and investment advice freely and without sanction in the UK. Sometimes these firms have an insurance license – sometimes none at all

Not sanctioning regulated firms for clear breaches and/or fraud – such as Gerard Associates which was introducing Ark victims to Stephen Ward of Premier Pension Solutions as far back as 2010, and was then providing “advice” to Ward’s London Quantum victims

Ignoring firms such as Fast Pensions who have defied 37 Pensions Ombudsmen’s determinations

Failing to coordinate criminal prosecutions against the scammers behind numerous scams who ruined thousands of lives and cost hundreds of millions of pounds’ worth of life savings

Failing to use existing legislation provided by FSMA 2000 to prosecute advisors (regulated and/or unregulated) overtly contravening the ban on communicating invitations to retail clients to invest in Unregulated Collective Investment Schemes

Announcing ineffective crack-down plans by newly-appointed government minsters who have failed to grasp the enormity of the pension scamming industry and the desperate plight of thousands of pension scam victims

Failing to police and sanction negligent pension trustees such as STM Fidecs for accepting members introduced by an unlicensed adviser: XXXX XXXX of Global Partners Ltd/The Pension Reporter – who was also the fund manager for the UCIS that all the victims had their pensions invested in and which is now being wound up

Refusing to communicate with members on the progress of the winding up of the Trafalgar Multi Asset Fund which had been run by XXXX XXXX

Omitting to take action against STM Fidecs for its role in the Cornerstone Friendly Society investment scam

Taking no action against Trustees, Integrated Capabilities Malta Ltd (ICML) for accepting retail members from an unlicensed firm in the Czech Republic and knowingly permitting investments in Nunn McCreesh’s UCIS: Blackmore Global, as well as Malta-licensed fund Symphony – a sub-fund of the Nascent Platform that is licensed only for professional investors

Not sanctioning Customs House Global, that runs the Nascent Platform, for inadequate due diligence and accepting unscrupulous sub-fund managers (such as XXXX XXXX, investment manager of failed TMAF and later, the recently wound up Symphony Fund) that exploit the platform for the sole purpose of pension scamming

Allowing an unlicensed firm – Square Mile Financial Services – to operate freely in the EU, providing pension and investment advice with only an insurance mediation license

Ignoring insurance companies which accept investments in UCIS funds and professional-investor-only instruments for retail investors

Failing to recognise those registered Closed-Ended Investment Companies whose true nature is as a Collective Investment irrespective of their form, such as Blackmore Global (registered number 010221V), that intentionally circumvent the stricter regulations imposed on collective investments, specifically to hide their financial accounts and the sub-funds which invariably include unsigned loan notes and high-risk hare-brained projects

Failing to act against a pension liberation scam – Evergreen Retirement Benefits Scheme – run by Simon Swallow who was working with Stephen Ward of Premier Pension Solutions and operating Marazion “loans”

Ignoring Concept Trustees (Guernsey) who offered retail investors the EEA Life Settlements UCIS and then accepted investment instructions from unlicensed, un-insured Stephen Ward of Premier Pension Solutions

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

London Quantum is a pension scheme whose trustee was a firm called Dorrixo Alliance run by our old friend Stephen Ward. That name will, of course, send a chill down the spines of many pension scam victims. Since 2010, Ward had been involved – either at the top or the bottom of the pond – in numerous pension scams. He eventually decided to “go straight” and declared that Ark was history – although Ark was far from history for his hundreds of victims who are now facing financial ruin.

Ward’s version of “going straight” was London Quantum. He had learned from the Capita Oak and Westminster scams that the value in getting involved in a pension scam comes from the investment introduction commissions. So he set about building a portfolio for the London Quantum victims which was based purely on how much wonga he could earn – rather than what was right, prudent and appropriate for an occupational pension scheme.

So what were the investments and why weren’t they right for a pension scheme?

The Scheme purchased shares in a unitised currency investment fund which traded in the top ten major currencies. The fund was regulated by the Central Bank of Ireland.

The fund was regulated but according to a regulated investment advisor the fund was inappropriate in terms of risk for the Scheme.

The fund prospectus did not specify a predicted rate of capital growth. However the scheme sponsor had previously stated a predicted return of 12%-15% per annum – an astonishing amount by any stands. But in practice, the fund performed poorly and fell over the period of the investment.

Dalriada Trustees (who replaced Stephen Ward’s Dorrixo Alliance and was appointed by the Pensions Regulator) received advice that, due to the high-risk nature of the fund and, notwithstanding the fall in the value of the investment, the Trustee should exit the fund at the earliest opportunity – irrespective of potentially heavy losses.

In 2014/15, the Scheme purchased nine corporate loan notes. Dolphin specialise in the purchasing of derelict and listed German property. The property is then sold off plan to German investors who take advantage of a specific German tax relief which allows for the recovery of renovation costs through tax allowances when purchasing units within a listed building.

The corporate loan notes were for a period of 5 years with no early exit options. The loans were due to be repaid at various dates between 9 October 2019 to 27 April 2020 depending on when the loans were made.

The loan notes had varied rates of return ranging from 12% to 13.8% per annum. All interest is rolled forward and paid at the end of the 5 year period.

This is an unregulated investment and is high risk in nature. There is no guarantee that the capital and interest will be fully repaid at the end of the relevant 5 year period. Dalriada had received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

London Quantum One Limited

The Scheme had purchased shares in London Quantum One Limited (“LQOL”). LQOL holds rights to a social media application called VIP Greetings which provides personalised messages with the use of celebrity endorsement. The original trustees paid for the LQOL shares from the scheme funds.

The underlying investment in VIP Greetings was long term and no returns were expected for several years. No early exit options exist and there is no evidence of a secondary market to sell the investment.

The returns from VIP Greeting application are highly speculative. These is no guaranteed minimum return or definitive payment date. Investors hold no security over any physical asset.

A number of valuations in relation to the VIP Greetings investment were received prior to the appointment of Dalriada Trustees. The valuations appeared highly speculative. In addition, the valuations were not made at the time that the Scheme purchased the investment.

Dalriada suspects that the investment holds little, or more likely, no value. They are not confident that any return will be made to the Scheme.

Between 2014 and 2015 the Scheme purportedly invested in 17 car parking spaces in a car park near Glasgow Airport. The investment was offered by Park First Glasgow Limited who lease parking spaces to investors, in this case the London Quantum, and then sub lease the parking space back.

The investor enters a lease for a period of 175 years (the maximum allowed under Scottish law). The parking spaces are then sub-leased back for a period of 6 years. The sub-leases can be terminated by Park First after 2 or 4 years, or at any time with not less than 10 days notice if it has found a substitute sub-tenant.

There is a ‘guaranteed buy back’ policy which outlines under what circumstance Park First will buy back the parking spaces. Park First has full discretion in this regard and is under no obligation to buy back the spaces at any point. In short, there is no guaranteed exit option.

The investment offers a guaranteed rate of return of 8% per annum for the first 2 years. To date payment in line with the 8% return had been received. £27,200 was received in February 2015 and a further £27,200 was received in February 2016. No payment was received for February 2017.

This is an unregulated investment. Park First operate the car parking space on behalf of the investor for an annual fee. The parking spaces generate income which is ultimately passed back to the investor each year.

Dalriada received advice that the investment was illiquid and inappropriate for the Scheme and early exit was recommended.

Dalriada have tried to recover the monies paid to Park First arguing that the legal documentation was never fully completed by the previous trustee and that the contracts were ineffective. Park First has rejected this request and is insisting that the contracts are valid and that there is no scope for Dalriada to be refunded.

On 20 August 2013 the Scheme invested in an unsecured loan note issued by the law firm Malletts Solicitors Limited.

The loan note had an investment period of 6 years with an obligation for the note holder to redeem 25% of the note per annum after year 2. No early exit options existed.

The loan note purported to return 8% per annum payable half yearly.

Interest or redemption payment have not been made by Mallets. To date the Scheme should have received payments totalling £3,280.00 as per the contractual documentation.

Loan notes have been issued by Mallets in an attempt to raise funding for an internal ‘legal hub’ project. The loan note was unsecured.

Dalriada contacted Malletts to obtain additional information in relation to the investment. Mallets have refused to explain how the Scheme came to be invested with them and have only provided minimum details

Dalriada had received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended. They sent Malletts a number of formal requests to exit the investment however Malletts did not respond.

Malletts Solicitors Limited went in liquidation on 11 November 2016. Dalriada submitted a proof of debt respect of the loan note but the fact it has gone into liquidation suggests prospects of recovery are poor.

On 31 January 2015 the Scheme invested in a corporate bond with Colonial Capital Group Plc. Colonial operates in the distressed US social housing market and have issued a number of bonds.

The corporate bond is for a period of 3 years. No early exit options exist. The bond has a fixed return of 12% per annum. Interest will be rolled forward and paid at the end of the 3 year investment period.

This is an unregulated investment. Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

Dalriada sent Colonial a formal request to exit the investment. Colonial responded and confirmed that an early exit was not available as Colonial may only redeem all or part of the bonds on a pro rata basis for all investors. It would therefore not be possible to facilitate an early exit for the Scheme.

Colonial Capital Group Plc was then placed into administration on 8 March 2017. Dalriada has issued a proof of debt in relation to the corporate bond but, again, the fact the company has gone into administration suggests prospects of recovery are unpromising.

The investment is in hotel rooms in a hotel development by The Resort Group. The hotel has recently been completed in Cape Verde and investors purchase a right to benefit from the profits and interests of specific pieces of the development. Investors do not own the land nor do they have a charge over it. An investor has simply a right to share in any profit generated from the hotel rooms.

The investment could not be exited prior to completion of the hotel rooms. Now that these have been completed they can be sold on the secondary market.

Before completion of the hotel rooms a guaranteed return is paid. After completion the return is based on room occupancy. The expected returns have been paid to the Scheme.

This is an unregulated investment. Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

The Resort Group offered to repay the amount transferred to it by the Scheme. That offer was to release one plot every two months from 31 October 2016 subject to completion of legal agreements. Dalriada agreed to this offer and signed the agreements in December 2016.

The Reforestation Group Limited

The purported nature of this investment is that the Scheme has purchased ‘land rights’ to 21 plots of Brazilian farm land that is to be used for growing eucalyptus trees. The investment term is 21 years as it covers three cycles of seven years, which is the projected time period to grow and harvest the trees. The investment purportedly offers returns of 28-32% compounded over each seven year cycle.

The crop cycle of the eucalyptus tree is seven years. Accordingly, with the investment being made in 2014, the first return on any of the Land Rights Agreements (”LRA”) would not be realised until around 2021.

The estimated return after 7 years is £19,000 per hectare, which is a 90% return. There are a number of issues with this development which Dalriada finds concerning and are being investigated.

Dalriada has received advice that the investment is illiquid and inappropriate for the Scheme and early exit is recommended.

Dalriada, through the Scheme’s legal advisers, has written to Reforestation to seek further details regarding this investment and to seek justification for the apparent high level of returns promised.

The investment consists of 11 Bonds over three different series and made between 27 October 2014 and 15 May 2015. The Bonds mature after four years from issue but can be redeemed early after three years (upon six months’ notice) or otherwise with ‘the express consent of the directors of ABC Alpha Business Centres Limited’.

Investment returns depend on the series of the Bond and range from 8.11% to 8.25% with and additional bonus if the Bonds are not redeemed early.

In relation to the two series of Bonds, the Scheme has elected not to have ‘rolled up’ interest. This means that interest is due and payable to the Scheme on a quarterly basis. These payments were made until Q4 2016 but stopped when ABC Alpha Business Centres UK Limited and ABC Alpha Business Centres VI UK Limited went into administration on 20 January 2017.

The Bonds are corporate bonds in ANC UK Limited. ABC UK Limited is the capital raising vehicle for the investments. ABC UK Limited is wholly owned by a United Arab Emirates (UAE) entity, ABC LLC. ABC LLC owns and operates the investment portfolio of real estate investments.