April 2019 sees the battle between Store First and the Insolvency Service. On April 15th, the High Court proceedings will kick off. As a result, the Store First v Insolvency Service will determine how many people will lose their pensions permanently. Two sets of very expensive lawyers – DWF and Eversheds Sutherland – will battle it out to see if Store First can continue trading. In the end, if the Insolvency Service wins the war, then both law firms and an insolvency practitioner will get rich.

As a result of the Insolvency Service winning, 1,200 pension scam victims will probably lose the majority of their investments in Store First. In most insolvencies, there is little left after the various snouts in the insolvency trough have had their fill. Investors will be lucky to get 10p in the pound. If there’s an “R” in the month. And if it is snowing. And if Brexit has a “happy ever after” ending.

The Insolvency Service says it is “in the public interest” to wind up Store First. But are they right? Isn’t winding up the company going to do even more unnecessary damage?

One very important issue is that the Insolvency Service’s witness statement dated 27.5.2015 (by Leonard Fenton) is so full of inaccuracies, misunderstandings, incomplete facts and an obvious failure to understand how the scam worked – as to be utterly laughable. The Insolvency Service and the High Court will rely heavily on this witness statement – and yet it has so many holes and errors that it is misleading, incomplete and meaningless. I asked the Insolvency Service questions about the incorrect and incomplete statements and made numerous comments on the failings contained within the statement. But the Insolvency Service did not even have the courtesy to reply or even acknowledge my contribution. In my view, this is arrogance and incompetence in the extreme.

This impending legal battle (which will cost the taxpayer £millions) is riddled with many more questions than answers. Here are a couple of my questions:

QUESTIONS RE STORE FIRST V INSOLVENCY SERVICE BATTLE

Why did HMRC and tPR register Capita Oak and Henley Retirement Benefits Scheme as pension schemes in the first place?

How many of the many scammers behind Capita Oak and Henley have been prosecuted?

The reason for my questions is that both HMRC and tPR were negligent in registering the two occupational pension schemes. This was because the schemes were obvious scams from the outset. They both had non-existent sponsoring employers which had never traded or employed anybody. And they weren’t even in the UK.

HMRC was blind, stupid and lazy at the start – when these two schemes were registered by known scammers. But several years later, HMRC woke up pretty smartly and sent out tax demands for the “loans” the victims received. The Store First v Insolvency Service Battle is probably doomed to ignore HMRC’s negligence in causing this disaster in the first place.

James Hay and Suffolk Life had been facilitating the Elysian Fuels investment scam at around the same time. And this was with the considerable “help” of serial scammer Stephen Ward. So, this was a prime time for scams and scammers. However, both HMRC and tPR failed the public back then and have continued to do so ever since.

In 2015, the Insolvency Service identified and interviewed most of the scammers behind the Store First pension scam. In their witness statement dated 27th May 2015, Insolvency Service Investigator Leonard Fenton cited statements and evidence from all the key players.

KEY PLAYERS IN THE STORE FIRST PENSION SCAM:

Ben Fox

Stuart Chapman-Clarke

Michael Talbot

Sarah Duffell

Bill Perkins

XXXX XXXX

Alan Fowler

Jason Holmes

Karl Dunlop

Christopher Payne

Keith Ryder

Craig Mason

Patrick McCreesh (of Nunn McCreesh – along with Phillip Nunn)

Tom Biggar

Paul Cooper (Metis Law Solicitors)

That is fifteen scammers who have never been prosecuted. They have not only never been brought to justice, but many of them went on to operate further scams and ruin thousands more lives – destroying more £ millions of hard-earned pension funds.

And what of Toby Whittaker’s Store First? There is no question that store pods are not suitable investments for pension fund investments. Car parking spaces are unsuitable for pensions as well. There are, in fact, a long list of inappropriate investments for pensions – including anything high-risk, illiquid and expensive or commission-laden.

All the above are routinely used and abused by pension scammers as “investments” for some dodgy scheme. Invariably, the above investments come with pension liberation fraud and/or huge introduction commissions and hidden charges. However, it is rarely the fault of the artist, wine maker, start-up entrepreneur, truffle farmer or property developer that the scammers profit so handsomely from abusing their products.

Store First v Insolvency Service Battle

I hope Store First defeats the Insolvency Service in the forthcoming battle in the High Court this month. And I hope that the public and British government will finally get to see what embarrassingly inept, corrupt, lazy regulators and government agencies we have. I will publish the Insolvency Service’s witness statement separately for anyone who wants to read the Full Monty.

Let us not forget that the solicitors acting for the Insolvency Service – DWF LLP – also act for serial scammer Stephen Ward. It was Ward who was responsible for the pension transfers which subsequently invested in Store First. Had it not been for him, 1,200 victims’ pensions totaling £120 million wouldn’t now be at risk. But, somehow, DWF LLP doesn’t think that is a conflict of interest?!?

Let us be clear: if the Insolvency Service wins the court case, the investors will get nothing. This will mean that, yet again, the victims will get punished. If Store First wins, the investors will get at the very least half their money back. If they are patient, they may even get it all back.

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

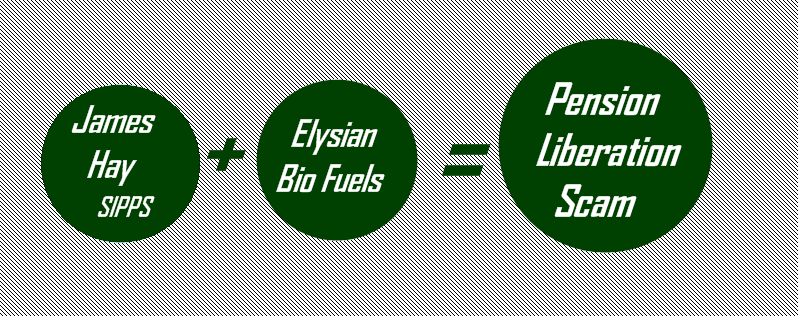

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

Katar Investments say they give UK and overseas investment advice in a simple way. However, the types of investment opportunities they are offering are, unfortunately, once again, making my red beacon flash. So, with Déjà vu, let me tell you why. Please make sure you are comfy, this might take a while!

Firstly, I had a quick look into their team. In my opinion, you would hope that some of the people advertising about giving you advice on investments would hold some sort of financial qualification. However, out of the five team members listed only one mentions a background in finance, the others only list sales experience.

I had a quick check on the registers to see if the one team member who states she has 10 years´ experience in the financial sector, holds any qualifications with the CII, CISI etc. – she did not appear to have any registered financial qualifications.

Now, forgive me if I am slightly biased and ever so critical when it comes to firms giving investment advice, but I would hope that any firm giving me advice on what to invest in, would have a team of fully qualified financial advisers. Not just sales experts. Or am I just being fussy?

Katar Investments state:

“Whether you are looking for a steady income investment, a property investment with high capital growth and a quick turn around of your capital or an opportunity in the latest emerging market, we have something to offer you.

We are highly committed to our investors and are focussed (their spelling mistake – not mine) on delivering a level of customer service which is above and beyond. So rest assured our agents will strive to provide you a class A service when you Invest with Katar Investments.”

I feel that the salespeople who work for Katar Investments may well be driven solely by earning high commissions when it comes to offering class A services. But, again, maybe I am biased! Let’s move on to what investments they offer.

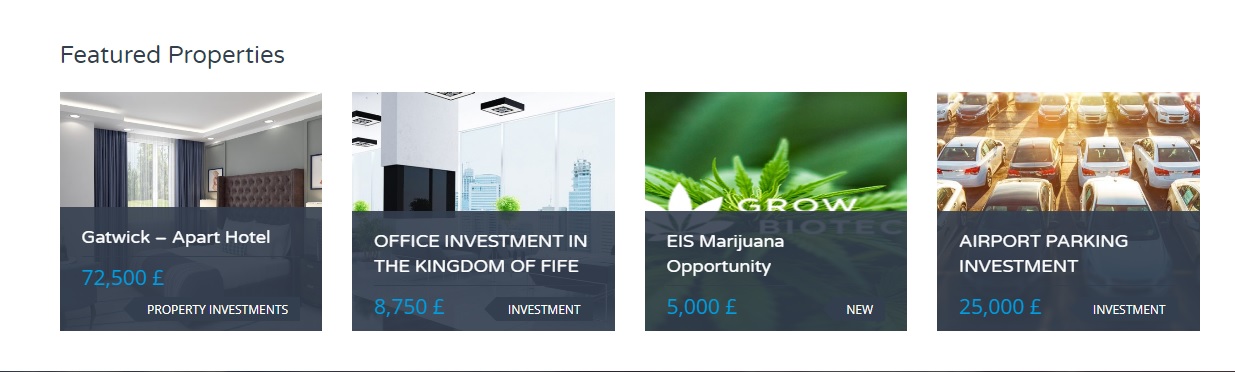

Gatwick – Apart Hotel – This is a serviced apartment/Hotel investment with a minimum investment of 72,500 GBP. The figure states “from”, so I assume you can throw a bit more in for good measure. The promised outcomes:

12 Months rental paid in advance

Rental protected by Insurance

5 Years Rental 8%

2% profit paid on exchange deposit during refurbishment

7 days free stay subject to 1 months notice

Buy back at 110% after 10 years

40% Finance on units over £140,000

Luxury furniture pack included with every purchase

Completion date: March 2019

This is a fixed term investment of 10 years and it has not been built yet (check the completion date). To me, an investment like this would ring alarm bells, as you are purchasing property that has yet to be completed. All sorts of hiccups could occur before the investment was up and running. An illiquid, high-risk investment, only for those who can afford a potential loss on the funds used.

This means your money is trapped for an awfully long time. If the market sways, you could be set for a loss and often with fixed-term structured investments there are fees and charges. Investments like this can, if they go wrong, result in you, the investor, falling into negative equity.

EIS marijuana opportunity – Grow Biotec, there is a lot of press going around at the moment into the medical uses of marijuana and possibilities of a change in legislation in the UK. In many states of America, the use of marijuana for medical use has been decriminalized. As an avid supporter of natural remedies and healing through nature, the use of CBD extracted from the marijuana plant interests me immensely, the idea of investing in this potentially lifesaving product does have a certain draw.

But, there is always a but! Since working for Pension Life, any investment opportunity that quotes the word ´bio´ gives me the heebie-jeebies. We have only to look back and remember the Elysian Bio Fuels liberation scam promoted by James Hay. The victims of this scam have been left penniless AND with huge tax bills from HMRC.

Another ´bio´investment disaster was Sustainable Agroenergy (SAE) Plc, investors were told their investments were in biofuel products, that land was owned in Cambodia and planted with Jatropha trees – a tree with highly toxic fruit that could be used to produce biofuel. Unfortunately, the Jatropa trees were not as fruitful as originally thought. The perpetrators, were thankfully convicted of fraud and bribery offenses.

The reasons I doubt this as a good investment are the vague promises and the over promises.

´It is a private offer raising £5 million to develop one of the world’s most valuable portfolios of cannabis-IP assets by 2022.´

What will be the outcome should this £5 million not be made? A possibility of loss of all or part of your investment.

´We are seeking to develop one of the world’s most valuable portfolios of cannabis-IP assets by 2022.´

Meaning this is a fixed-term investment, with potentially no return for at least 4 years, if not longer, AND only if successful.

Projected high returns: Target return of £50 per £1 invested (not guaranteed)

EIS Tax relief: up to 50% income tax and capital gains tax relief. Remember tax rules can change and benefits depend on circumstances.

If it sounds too good to be true – it probably is. Plus this figure is not guaranteed and seems to me like it was just plucked out of the sky, nice and high, to lure investors in.

These investments are what we in the industry call illiquid. Once your money is in, then it´s pretty hard to get it out quick AND unless the venture does well there will be no return. With regards to pension investments, these are the very worst, toxic assets to invest in.

Unfortunately, they are often the assets which pay handsome investment introduction commissions to the salesperson, and this is why serial scammers, like Ward, love them. They go in with the ´eco-bio´ sale pitch or the glamorous property ownership – withholding the high-risk, fixed-term rules surrounding the investment.

A pension fund is a retail investment that should be placed in a low to medium-risk asset. Fixed terms, high-risk and illiquid investments should be avoided at all costs.

The types of investments offered by Katar Investments are high-risk and illiquid, if you have a spare five grand that you can afford to lose, then go for it: have a cheeky punt on Bio Grow. You may be pleasantly surprised and get the target return of £50 per £1 invested (just remember to duck smartly when those pink things with curly tails fly a bit too close!). However, if your money is dear to you and you cannot afford to lose it, please stay away from shiny pink and green investments like this.

When it comes to your precious pension fund it is always best to air on the side of caution and go for the safe bet. It might not pay the highest interest, however, slow and steady wins the race. Meaning you will be able to enjoy your hard earned pennies in your retirement – stress free.

Here at Pension Life, we are well aware of QROPS and SIPPs providers being a favorite of the serial pension scammers and are very pleased to report that there is positive news of better protection against this, on the horizon.

Three years ago the Pension Liberation Industry Group (PLIG) launched a code of practice to protect retail investors from serial scammers. Whilst the code of practice managed to help towards the eradication of the big occupational scams, the serial scammers altered their gameplay and continued to score. Serial scammers are focusing on using SIPPS and QROPS providers as a way to lure unsuspecting victims into toxic, high risk investments. Legal “envelopes” with corrupt contents.

Fortunately, the PLIG has finally recognised this change of tactic and has now announced that it will be updating the code of practice to reflect the new tactics of scammers, with the hope of reducing the number of pension scam victims.

Despite this welcome positive news, I still can’t shake the idea that this updated code of practice by PLIG, is possibly too little too late. The situation with James Hay springs to mind. James Hay – the UK´s largest SIPP provider – has announced losses in 2017. James Hay was also involved in the pension liberation scam with Elysian, in which around 500 clients put £55m into Elysian Bio Fuels. The business failed in 2015.

The business failed in 2015 after SIPPS – including James Hay – had already been misused to lure in pension scam victims. This is just one of many such scams (off the top of my head). Believe me, there are many, many more similar to this – that have scammed unsuspecting victims out of millions of pounds’ worth of pension funds and into crippling tax charges.

He was quoted as saying: “The new Qrops legislation that was introduced in the budget [last year] has reduced scams a bit. So, to some extent, revisions are a little behind the curve. I actually think scammers are switching back to using SIPPS and [small self-administered schemes] SSAS again.”

We welcome this new code from the PLIG, however we can’t agree more with Darren Cooke who also stated, that the FCA needs to regulate the products and not just the advisers.

“As soon as the FCA [starts] regulating the product, it would stop regulated advisers recommending unregulated products. That would stop 99 per cent of scams.”

A small step in the right direction, where a huge leap needs to be made.

Dear FCA,

If you really want to stop pension scamming in its tracks:

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

James Hay, the first UK SIPPS provider, could face tax charges of up to £20 million from HMRC, related to the Elysian Bio Fuel investment scam (sorry: scheme). Elysian Bio Fuels, which owned a bioethanol plant in the US and a renewable fuels refinery in the UK, was also used by other SIPPS providers such as Suffolk Life.

Money Marketing states : “Sipp investors are facing millions in write downs on a high-risk bio fuel investment, which has also been linked to a suspected pension liberation scam.”

Unsurprisingly, James Hay has launched an appeal against the tax charges AND as of January, has also slipped in a ban on non-standard investments including overseas commercial property, storage pods and carbon credits to be bought through its SIPPS platform.

We say to James Hay, “too little, too late, mate!”

Through SIPPS provided by James Hay, around 500 clients put £55m in to Elysian Bio Fuels. Yes, that´s 500 retail investors, placed into high-risk toxic investments, totally unsuitable for pensions. The business failed in 2015. James Hay claim that they did not advise their members AND limited their role to pension administration. Whilst they may not have directly advised their members, they did, however, allow crooked advisers to buy shares in Elysian Bio Fuels for the purpose of Pension Liberation.

The sheer act of letting crooked advisers advise their trusting members, whilst turning a blind eye to fraud, makes James Hay guilty in anybody´s book. How long can so called legitimate SIPPS providers continue to get away with this sheer negligence of their members´ funds?

Below is an email exchange between Stephen Ward of Premier Pension Solutions, his lawyer Alan Fowler and Angela South of Magna Wealth. This thread describes exactly how the Elysian Bio Fuels/James Hay liberation scam worked.

Interesting….but I’m amazed that reputable SIPP providers will countenance this. Who’s making the loans? I’m not sure I see how the SIPP pays the member (or anyone for that matter) £100k – with what/who’s money? And won’t the SIPP need to verify that the shares in Xco are actually worth £100k. That said, if the IFA is doing these, it seems the process works………..

From: Stephen Ward [mailto:SWard@ppsespana.com] Sent: 18 October 2013 10:01 To: Angela (South – Magna Wealth) Subject: FW: QROPS opportunity Importance: High

Morning Angela

I was not expecting such a fast green light !

But it seems to me that a green light is what we have

The next step is a test case I guess ….. ? I may have one but just need to check his fund value.

Putting my provider hat on I do not need to understand the details of the back end engineering, the fact its OK with James Hay is good enough for me.

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Pension and investment scams and scandals are a blight on financial services and saving for retirement. The energetic and inspired campaign by Darren Cooke of Red Circle successfully raised awareness of the problems of cold calling. But the snap general election scuppered serious traction on this and the most the government has achieved so far is to make a vague promise to talk about talking about it. But still it is not illegal, and still the scammers are scamming away merrily.

Chair of The Transparency Task Force

The Scams and Scandals team was formed as a result of inspiration by the Transparency Task Force’s Andy Agathangelou. It has attracted a group of like-minded professionals who believe passionately that a concerted effort should go into coordinating a zero-tolerance approach to scams and scandals. All members of the team are committed to producing a White Paper which can focus the minds of government ministers, regulators and law enforcement agencies on the whole problem – not just the cold calling bit.

Irrespective of which version of which political party we are talking about, the ultimate object of a successful and fulfilled life is to be happy, healthy and solvent. And this includes getting a decent education, leading a responsible and law-abiding life, and saving for a comfortable retirement. Millions of British citizens manage to achieve this goal, but sadly many thousands of them lose part of all of their retirement savings to the armies of scammers.

XXXX XXXX, one of the many pension scammers ruining thousands of victims’ lives

All these scams and scammers have caused thousands of victims to lose hundreds of millions of pounds’ worth of retirement savings. And caused untold misery – in many cases exacerbated by HMRC punishing the victims rather than the perpetrators.

The Scams and Scandals Team has a clear five-point goal:

Ban UK cold calling and fraudulent calling

We must not let this disappear off the agenda and must keep up pressure on MPs and Ministers – as well as the regulators. But this must also be extended to overseas as we already know that the UK-based cold calling outfits have made arrangements to move their operations or merely facilitate re-routing of phone numbers. However, the twilight industry of “introducing” must also be examined as this is a serious source of scam facilitation.

Support Lesley Titcomb “Scammers are Criminals”

Ms Titcomb has publicly declared scammers to be criminals

We must work with the regulators, government and law enforcement agencies to enhance existing and introduce new regulation and legislation to prevent new scams, close down known existing scams and bring those involved in conceiving, operating and promoting both to account.

Revitalise Scorpion Campaign

Fundamental to preventing scams is communication to the public of the dangers of cold calls and pension/investment scams which would include the Scorpion Campaign – but so much more as well. A key part of this exercise is the use of social media and the plan to produce a documentary and Youtube channel giving real-life examples of past and current scams. Explaining the mechanics of a scam is one thing – but showing an actual example of a victim and the scammer is bound to have even greater impact.

Write off HMRC debt where scams are proven

HMRC celebrating the tax they collect from victims of pension liberation fraud

We need the help of the government here and could do with an actuary to help us work out what the cost to the State is of taxing victims of scams. If we can demonstrate that by ruining a scam victim (who has already probably lost part or all of his pension) with the tax charge, the long-term cost of supporting the victim and his family will far outstrip the tax collected. This is especially well demonstrated in the Ark case where the victims have got to both repay the “loans” and pay the 55% tax even if the loans are repaid.

Ensure AML regs include pension scamming

TOBY WHITTAKER’S TOXIC EMPIRE WILL FINALLY BE HUFFED AND PUFFED AWAY

I would widen this to include investment scams. This is because at the heart of every pension scam there is a fraudulent investment (and/or loan). The actual pension itself is harmless as it is essentially just a box with a label on it and only becomes toxic and dangerous once you put the scorpions, snakes and cockroaches inside it. You could equally put fluffy kittens in it. It is the mis-use of the pension “box” which is the scam.

“James Hay was ONLY the pension administrator”. My hat!

JAMES HAY AND ELYSIAN BIOFUELS SCAM

I always say that pension and investment scams happen because people, firms and authorities allow them to happen. This was very true in the Elysian Fuels pension liberation scam. Jack Gilbert of New Model Adviser broke the news today, 9.5.2017, of James Hay’s involvement in this:

Sipp and platform provider James Hay is facing an HM Revenue & Customs tax charge of £1.8 million over the non-standard biofuel investment Elysian Fuels. James Hay today said it has 500 clients who have invested around £55 million in Elysian Fuels and HMRC is investigating this scheme.

And the firm added it is now appealing a tax charge from HMRC over this investment.

‘James Hay did not advise investors in relation to these investments; it acted solely as pension administrator. James Hay has received, in April 2017, assessment notices for sanction charges from HMRC for the tax years 2011/2012 and 2012/2013 in total for £1.8 million. These have been appealed and are the subject of ongoing discussions with HMRC.’

The investors themselves, whose SIPP investments are now worthless, will undoubtedly be interested to know the real story behind this disgraceful scam – which also involved other FCA-regulated SIPP providers such as Suffolk Life:

The arrangement I heard about today works like this as an example ( ignoring fees) and this is the simplistic version

Client borrows 16k or thereabouts (this is available in the package)

He gets a non-recourse loan (which will not be repaid) of £84k

He buys shares in Xco for £100k. These are listed on the CISX (name is Elysian)

Transfers £100k to James Hay SIPP

SIPP pays member £100k for the shares .,,,

Member repays the 16k and trousers £84k

My IFA connection has done 40 of them so far. Advice to transfer to the SIPP is from an FCA regulated IFA. James Hay and Suffolk Life know the full structure and are happy with it ….Fees ….. On transfer to SIPP (need to agree the commercials with the IFA)

Regards

Stephen

The FCA-registered IFA was Angela South’s Magna Wealth. We’ve had quite a good old chin-wag over this and while she said she did suspect I had hacked her emails, she denied she had done 40 of these transactions. In fact, the only hacking I have ever done was plodding round Windsor Great Park on an elderly horse when I was a teenager.

But don’t you just love James Hay’s protestation: “we acted solely as pension administrator”? Solely? Pull the other one. Come on FCA – wake up! Perhaps we could have a competition between tPR and FCA to see which one could start doing some actual regulating first? Tortoise and tortoise race?

Email to Michael Bridges, Compliance, HMRC from Angie Brooks, ARK Class Action – re pension liberation loans.

11 November 2015

Dear Mr. Bridges,

Re: Pension Liberation “Loans”

Thank you for calling me yesterday and for discussing the various aspects of the pension transfers and “loans”. Some important points arose from our discussion, and I feel it would be valuable to get these recorded and addressed.

The first issue was whether any of the members/victims ever asked their existing/ceding providers if they could provide a loan. It has never occurred to me to ask this question so – by copying in a number of members to this email – I am reaching out to ask them this specific question:

“Did you ever ask or consider asking your original pension provider – e.g. Standard Life, Aviva, Royal Mail, NHS etc. – whether they could provide a loan?”

If I get any replies I will let you know. I suggest the answer will be a resounding “no” – but rather than assume the response I will leave it to the experts, i.e. the victims themselves, to answer this question. (I think you will find the answer in the Q10’s anyway.)

How do Pension Liberation “Loans” work?

Victims of different scams were told different things, and the “loans” were structured in different ways. Some were told the loans were repayable; some that they were not repayable; some received elaborate loan documentation; some received nothing. However, the common fact is that they were all told in no uncertain terms that the “loans” were not taxable. Many of the scammers went to great lengths to try to create the illusion that there was no connection between the loans and the transfers and that it was entirely a coincidence that they both happened at the same time.

Elysian Fuels

In fact, in a recently-published case: Elysian Fuels (£240 million now valued at £zero) the participants were told by financial advisers that the 84% “loans” were not taxable and that regulated SIPP providers James Hay and Suffolk Life were fully aware of and “happy” with the “loan” structure. I have copied and pasted the emails outlining this scheme below for your information.

Tax Compliance

The point I am trying to make is that if an “ordinary man in the street” is assured by an IFA, a solicitor and a SIPP provider that a transaction is tax compliant, there is no reason for him to question that assurance. What makes matters worse for the victims (and better for the scammers) is that the vehicles for the scams – whether an occupational scheme, QROPS or SIPP,- are registered by HMRC in the first place. This gives the illusion that there is something “safe” or “approved” about the entire structure and indeed the scammers often use the term “HMRC approved” to dupe the victims.

I have copied James Hay into this email and hopefully – as a regulated SIPP provider – they will come back with some further professional and regulated views on how and why pension liberations/loans/maximising arrangements (or whatever “label” is used to describe the liberation mechanism) are so easy to sell as “tax free” transactions. Hopefully someone at James Hay will be able to provide some enlightening “inside” information and views on the subject.

I could tell that you felt impatient with the fact that so many people believed these various liberation scams were legitimate and tax compliant. With the greatest of respect, I would point out that as you work for HMRC in Compliance, it is your job to be an expert on pensions taxation. But the victims don’t tend to have that knowledge or education and won’t have read Tolley’s Pensions Taxation (420 pages) http://www.amazon.com/Tolleys-Pensions-Taxation-2014-2015-Stephen/dp/0754549356.

You also pointed out that if there was no loan agreement or contract, then there was no loan. Each scam worked differently, and as far as I can see the only one with a proper, enforceable loan contract was the Evergreen QROPS/Marazion loan scheme run by Stephen Ward from Spain. The word “loan” was merely a four-letter word – sometimes accompanied by the term “non recourse” as in the James Hay/Elysian example below. We could debate “when is a loan not a loan?” all day long, but the bottom line is that the victims were misled and defrauded. In some cases by a government consultant on pensions; and in some cases an added layer of apparent respectability enhanced the illusion that the transaction was safe and compliant by involving FCA-regulated IFAs and SIPP providers.

Another scheme for pension liberation was Salmon Enterprises which worked with the trustees Tudor Capital Management.

All in all, it is a disgraceful state of affairs, and I am afraid HMRC themselves have played their own part in helping facilitate these scams for the past five years – resulting in ruin for many thousands of victims while lining the pockets of the scammers.

Interesting….but I’m amazed that reputable SIPP providers will countenance this. Who’s making the loans? I’m not sure I see how the SIPP pays the member (or anyone for that matter) £100k – with what/who’s money? And won’t the SIPP need to verify that the shares in Xco are actually worth £100k. That said, if the IFA is doing these, it seems the process works………..

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “ Neither Garry Williams nor Sue Huxley has ever been convicted or jailed.

Neither Garry Williams nor Sue Huxley has ever been convicted or jailed.

Fast Pensions

Fast Pensions

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm  116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

Rental protected by Insurance

Rental protected by Insurance But, there is always a but! Since working for Pension Life, any investment opportunity that quotes the word ´bio´ gives me the heebie-jeebies. We have only to look back and remember the

But, there is always a but! Since working for Pension Life, any investment opportunity that quotes the word ´bio´ gives me the heebie-jeebies. We have only to look back and remember the

The types of investments offered by Katar Investments are high-risk and illiquid, if you have a spare five grand that you can afford to lose, then go for it: have a cheeky punt on Bio Grow. You may be pleasantly surprised and get the target return of £50 per £1 invested (just remember to duck smartly when those pink things with curly tails fly a bit too close!). However, if your money is dear to you and you cannot afford to lose it, please stay away from shiny pink and green investments like this.

The types of investments offered by Katar Investments are high-risk and illiquid, if you have a spare five grand that you can afford to lose, then go for it: have a cheeky punt on Bio Grow. You may be pleasantly surprised and get the target return of £50 per £1 invested (just remember to duck smartly when those pink things with curly tails fly a bit too close!). However, if your money is dear to you and you cannot afford to lose it, please stay away from shiny pink and green investments like this.