April 2019 sees the battle between Store First and the Insolvency Service. On April 15th, the High Court proceedings will kick off. As a result, the Store First v Insolvency Service will determine how many people will lose their pensions permanently. Two sets of very expensive lawyers – DWF and Eversheds Sutherland – will battle it out to see if Store First can continue trading. In the end, if the Insolvency Service wins the war, then both law firms and an insolvency practitioner will get rich.

As a result of the Insolvency Service winning, 1,200 pension scam victims will probably lose the majority of their investments in Store First. In most insolvencies, there is little left after the various snouts in the insolvency trough have had their fill. Investors will be lucky to get 10p in the pound. If there’s an “R” in the month. And if it is snowing. And if Brexit has a “happy ever after” ending.

The Insolvency Service says it is “in the public interest” to wind up Store First. But are they right? Isn’t winding up the company going to do even more unnecessary damage?

One very important issue is that the Insolvency Service’s witness statement dated 27.5.2015 (by Leonard Fenton) is so full of inaccuracies, misunderstandings, incomplete facts and an obvious failure to understand how the scam worked – as to be utterly laughable. The Insolvency Service and the High Court will rely heavily on this witness statement – and yet it has so many holes and errors that it is misleading, incomplete and meaningless. I asked the Insolvency Service questions about the incorrect and incomplete statements and made numerous comments on the failings contained within the statement. But the Insolvency Service did not even have the courtesy to reply or even acknowledge my contribution. In my view, this is arrogance and incompetence in the extreme.

This impending legal battle (which will cost the taxpayer £millions) is riddled with many more questions than answers. Here are a couple of my questions:

QUESTIONS RE STORE FIRST V INSOLVENCY SERVICE BATTLE

Why did HMRC and tPR register Capita Oak and Henley Retirement Benefits Scheme as pension schemes in the first place?

How many of the many scammers behind Capita Oak and Henley have been prosecuted?

The reason for my questions is that both HMRC and tPR were negligent in registering the two occupational pension schemes. This was because the schemes were obvious scams from the outset. They both had non-existent sponsoring employers which had never traded or employed anybody. And they weren’t even in the UK.

HMRC was blind, stupid and lazy at the start – when these two schemes were registered by known scammers. But several years later, HMRC woke up pretty smartly and sent out tax demands for the “loans” the victims received. The Store First v Insolvency Service Battle is probably doomed to ignore HMRC’s negligence in causing this disaster in the first place.

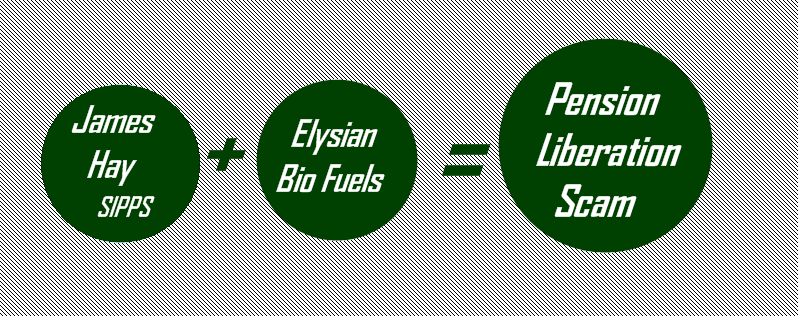

James Hay and Suffolk Life had been facilitating the Elysian Fuels investment scam at around the same time. And this was with the considerable “help” of serial scammer Stephen Ward. So, this was a prime time for scams and scammers. However, both HMRC and tPR failed the public back then and have continued to do so ever since.

In 2015, the Insolvency Service identified and interviewed most of the scammers behind the Store First pension scam. In their witness statement dated 27th May 2015, Insolvency Service Investigator Leonard Fenton cited statements and evidence from all the key players.

KEY PLAYERS IN THE STORE FIRST PENSION SCAM:

Ben Fox

Stuart Chapman-Clarke

Michael Talbot

Sarah Duffell

Bill Perkins

XXXX XXXX

Alan Fowler

Jason Holmes

Karl Dunlop

Christopher Payne

Keith Ryder

Craig Mason

Patrick McCreesh (of Nunn McCreesh – along with Phillip Nunn)

Tom Biggar

Paul Cooper (Metis Law Solicitors)

That is fifteen scammers who have never been prosecuted. They have not only never been brought to justice, but many of them went on to operate further scams and ruin thousands more lives – destroying more £ millions of hard-earned pension funds.

And what of Toby Whittaker’s Store First? There is no question that store pods are not suitable investments for pension fund investments. Car parking spaces are unsuitable for pensions as well. There are, in fact, a long list of inappropriate investments for pensions – including anything high-risk, illiquid and expensive or commission-laden.

All the above are routinely used and abused by pension scammers as “investments” for some dodgy scheme. Invariably, the above investments come with pension liberation fraud and/or huge introduction commissions and hidden charges. However, it is rarely the fault of the artist, wine maker, start-up entrepreneur, truffle farmer or property developer that the scammers profit so handsomely from abusing their products.

Store First v Insolvency Service Battle

I hope Store First defeats the Insolvency Service in the forthcoming battle in the High Court this month. And I hope that the public and British government will finally get to see what embarrassingly inept, corrupt, lazy regulators and government agencies we have. I will publish the Insolvency Service’s witness statement separately for anyone who wants to read the Full Monty.

Let us not forget that the solicitors acting for the Insolvency Service – DWF LLP – also act for serial scammer Stephen Ward. It was Ward who was responsible for the pension transfers which subsequently invested in Store First. Had it not been for him, 1,200 victims’ pensions totaling £120 million wouldn’t now be at risk. But, somehow, DWF LLP doesn’t think that is a conflict of interest?!?

Let us be clear: if the Insolvency Service wins the court case, the investors will get nothing. This will mean that, yet again, the victims will get punished. If Store First wins, the investors will get at the very least half their money back. If they are patient, they may even get it all back.

In the run up to the High Court proceedings to hear the Insolvency Service’s petition to wind up Store First, here is some background. This is an abridged version of the Insolvency Service’s witness statement regarding the Store First pension investment scam. It involved two bogus occupational pension schemes set up and administered by Stephen Ward of Premier Pension Solutions: Capita Oak and Henley Retirement Benefit Scheme. Ward also administered the transfers from the ceding schemes. In addition to Capita Oak and Henley, there were hundreds of transfers from SIPPS such as Berkeley Burke and Carey Pensions.

One very important issue is that the below Insolvency Service’s witness statement dated 27.5.2015 (by Leonard Fenton) is so full of inaccuracies, misunderstandings, incomplete facts and an obvious failure to understand how the scam worked – as to be utterly laughable. The Insolvency Service and the High Court will rely heavily on this witness statement – and yet it has so many holes and errors that it is misleading, incomplete and meaningless. I asked the Insolvency Service questions about the incorrect and incomplete statements and made numerous comments on the failings contained within the statement. But the Insolvency Service did not even have the courtesy to reply or even acknowledge my communication. In my view, this is arrogance and incompetence in the extreme.

Let us hope that justice will prevail, and the appalling failings of the Insolvency Service will be publicly laid bare. My comments and questions are in RED CAPS.

Petitioner: Leonard Fenton – Date: 27.5.2015

High Court of Justice, Chancery Division, Manchester District Registry

Transeuro Worldwide Holdings Ltd and Imperial Trustee Services Ltd in the matter of the Insolvency Act 1986

WITNESS STATEMENT

(SUMMARIZED TO CONCENTRATE ON CAPITA OAK AND WITH COMMENTS/QUESTIONS IN RED BY AB):

The scheme was offered to members of the public as an opportunity to transfer their pension funds into a new pension vehicle, CAPITA OAK, of which IMPERIAL was appointed as trustee and administrator. Members of the public have been misled into transferring their pension funds into the occupational scheme on the basis that they would receive a guaranteed return for a fixed period of time and, if eligible, be entitled to immediately access funds and receive an inducement payment of 5% of the transferred fund which would be treated as a non-repayable loan. There has been no transparency as to the investment or the administration of the occupational pension scheme, fees and charges have been deducted of which members were not aware and for which there has been no apparent benefit and members’ funds have not received the guaranteed return. READING YOUR WITNESS STATEMENT WILL FILL ANY VICTIM OR PERSON INVOLVED IN THE RESCUE OF THE ARK SCHEMES WITH REVULSION SINCE CAPITA OAK IS MERELY A RE-RUN OF THE ARK DISASTER – WITH MANY OF THE SAME PERPETRATORS BEHIND ARK HAVING PLAYED PIVOTAL ROLES IN CAPITA OAK. THE POINT MUST BE MADE THAT WHOEVER THE CAPITA OAK “SALES ENTITIES” WERE, IT WAS INCUMBENT UPON THE TRUSTEE I.E. IMPERIAL TRUSTEE SERVICES LTD TO ENSURE THAT THE SCHEME WAS OPERATED DILIGENTLY IN ACCORDANCE WITH HMRC AND TPR REGULATIONS. THIS INCLUDED THE TRUST DEED BEING MADE PROPERLY; THE SPONSORING EMPLOYER BEING A PROPER COMPANY WITH DUE DILIGENCE ON THE ACCOUNTS AND DIRECTORS; A STATEMENT OF INVESTMENT PRINCIPLES THAT INCLUDED DUE OBSERVANCE OF LIQUIDITY AND DIVERSITY; THE TRUSTEE (AND ANY DIRECTORS, DE FACTO DIRECTORS OR OFFICERS OF IMPERIAL) MEETING FIT-AND-PROPER REQUIREMENTS; SCHEME AND MEMBER ACCOUNTS; PROPER REPORTING TO MEMBERS; DUE DILIGENCE ON ANY INVESTMENTS; STRICT AVOIDANCE OF UNAUTHORISED PAYMENTS; PROPER SUPERVISION OF ANY PROMOTION OR SALES ACTIVITIES OR BROCHURES; TRANSPARENCY REGARDING FEES.

The sales entities were JACKSON FRANCIS, SANDERSON CLARKE and BARNCROFT ASSOCIATES. JACKSON FRANCIS and SANDERSON CLARKE were incorporated on 6.9.11 and 10.4.12 respectively, with STUART CHAPMAN-CLARKE being recorded as the sole registered director of both companies. JACKSON FRANCIS and SANDERSON CLARKE are not the subject of petitions by the Secretary of State and both companies are in Creditors Voluntary Liquidation.

I sent out a total of 753 questionnaires to members of the public who “invested” their monies in CAPITA OAK and Henley and of those some 289 were returned completed. From consideration of those questionnaires returned, it is noted that members of the public were initially cold called by JACKSON FRANCIS/SANDERSON CLARKE and other introducers in an attempt to persuade the potential client to make an appointment for a representative of JACKSON FRANCIS to visit them at home. During that visit the members of the public were offered a transfer of their pension into CAPITA OAK which invested only in Store First storage pods. YOU HAVE NOT MENTIONED JP STERLING WHO WERE INVOLVED IN PROMOTING CAPITA OAK TO MANY VICTIMS. IT HAS NEVER BEEN DISCOVERED WHO JP STERLING ACTUALLY WAS.

JACKSON FRANCIS and SANDERSON CLARKE informed prospective clients that an 8% return would be guaranteed for the first two years, with subsequent rates predicted to be 10% or more.

Investors of CAPITA OAK were also informed they could receive an inducement payment of 5% of the transferred fund value. This was treated as a-non repayable loan from the company called Thurlstone, a company purportedly registered in Gibraltar, but I have been unable to confirm the existence of a company with this name.

From the questionnaire responses I became aware that employees of SANDERSON CLARKE had been contacting members of the public stating they were calling on behalf of SANDERSON CLARKE and BARNCROFT ASSOCIATES in an attempt to persuade members of the public to transfer their pension into CAPITA OAK. SANDERSON CLARKE and BARNCROFT ASSOCIATES were dissolved on 7.1.14 and 26.3.13 respectively and the directors were Ben Fox and STUART CHAPMAN-CLARKE respectively.

An analysis of SANDERSON CLARKE’s bank account with Barclays shows that between 21.6.12 and 29.5.13, SANDERSON CLARKE received the following funds:

£3,390,275 from TRANSEURO

£501,000 from ADVANTAGE ACCOUNTING on behalf of TRANSEURO

£50,000 from Store First

£51,596 in deposits

These funds were used to meet the operating costs of SANDERSON CLARKE and subsequently JACKSON FRANCIS. SANDERSON CLARKE and JACKSON FRANCIS were almost entirely financed by TRANSEURO which operated as the facilitator of the Scheme, funding SANDERSON CLARKE and JACKSON FRANCIS almost entirely and providing the sales leads.

On 17.6.14, MSB Solicitors, on behalf of STUART CHAPMAN-CLARKE informed me that JACKSON FRANCIS and SANDERSON CLARKE had ceased to trade on 22.5.14 (ten days after the commencement of the investigation).

While I have been frustrated in my attempts to obtain information from TRANSEURO or those who are in control of the company, I note that:

TOBY WHITTAKER, MD of Store First, advised me that he had been approached by MICHAEL TALBOT and STUART CHAPMAN-CLARKE acting for TRANSEURO to purchase storage on behalf of their own “super” fund, CAPITA OAK. The conditions of the agreement was that payment of the two years’ 8% guaranteed return had to be paid up front to TRANSEURO plus rent earned on the store pods. TOBY WHITTAKER confirmed that the 8% guaranteed return due on the funds invested via CAPITA OAK was paid to TRANSEURO. In total TRANSEURO has received 46% of the total sales made to the CAPITA OAK scheme by Store First. There is no evidence that prospective members of CAPITA OAK were told of the commission payment or that TRANSEURO was funding the companies which had cold called the member in order to persuade them to transfer their pension fund. IT IS CLEAR THAT TALBOT, CHAPMAN-CLARK AND XXXX WERE ALL 100% AWARE THAT THE 8% “GUARANTEED RENTAL” WAS ALREADY SPOKEN FOR UNDER THE TERMS OF THE AGREEMENTS ENTERED IN TO BETWEEN STORE FIRST AND TRANSEURO. AND, FURTHER, WHY HAVE TALBOT, CHAPMAN-CLARKE AND XXXX NOT BEEN PROSECUTED YET – SINCE THIS WAS CLEAR FRAUD?

TRANSEURO entered into a number of marketing and sales agreements with Store First. TRANSEURO was entitled to a commission of either 30% or 46% on any sales that it introduced to Store First. The aggregate value of business transacted by Whittaker, Store First and TRANSEURO, as at 25.2.14, was £97,166,914. From this TRANSEURO received commissions in excess of £33m. AN EXPLANATION IS REQUIRED AS TO HOW AND WHY THE DISTINCTION WAS MADE BETWEEN 30% AND 46% COMMISSION AND UPON WHAT BASIS IT WAS DECIDED THAT A PURCHASE WOULD BE SUBJECT TO A SUB-LEASE OR NOT AS THIS APPEARS TO HAVE DETERMINED THE COMMISSION LEVEL. FURTHER EXPLANATION IS REQUIRED AS TO WHY THIS WAS NOT COMMUNICATED TO IMPERIAL TRUSTEES OR TO METIS LAW SOLICITORS WHEN CONTRACTS FOR PURCHASE WERE IN PROGRESS.

According to Bermans LLP acting on instructions from TRANSEURO and Octopus International Business Services, who provided nominee director services to TRANSEURO, TRANSEURO is owned by JJT Associates International Foundation a Panamanian registered company. According to Bermans, the “protector” of JJT is stated to be Stephen Michael Talbot.

In accordance with the pension scheme documentation dated 23.7.12, IMPERIAL acts as trustee and administrator of CAPITA OAK and has received £10.8m of transferred pensions into the bank account that was held in its name at Barclays. IMPERIAL subsequently transferred £10.1m to Metis Law, who, on instructions, facilitated the purchase of £9.8m of storage pods from Store First. These pods are held by IMPERIAL as the trustee of CAPITA OAK. I established that the 5% inducement payments to members who transferred to CAPITA OAK were made via the client account of ADVANTAGE ACCOUNTING into which Store First transferred £1.8m commission on behalf of TRANSEURO.

While IMPERIAL was trustee and administrator of CAPITA OAK, IMPERIAL entered into a services agreement with TKE for the provision of administration services. IMPERIAL deducted an administration fee of 5% from any pension fund transfers and provided these monies to TKE. Sarah Duffell is the sole director of TKE. She told me her duties included dealing with administration and answering the phone. She told me she worked closely with Bill Perkins who calculated the payments that were due out of TKE. Duffell told me she just did what she was told by Perkins who agreed her wages.

Of the 5% admin fee received by TKE, 2% was transferred to NATIONWIDE BENEFIT CONSULTANTS of which XXXX XXXX is sole director. The remaining 3% was used to pay Alan Fowler, Bill Perkins and Jason Holmes. IT NEEDS TO BE MADE CLEAR WHAT ROLE HOLMES PLAYED IN THIS.

In total, fees of £541,776 were transferred from IMPERIAL to TKE which were utilized to make payments as follows:

Paid to Metis Law on behalf of Hawkshead Properties in lieu of fees due to NATIONWIDE BENEFIT CONSULTANTS (XXXX XXXX) £100,873

Paid to Alan Fowler £86,632

Paid to WJP Admin and Copeland South for Bill Perkins £83,485

Paid to KE Media Services Ltd for Jason Holmes £73,811

No fee payments were made by TKE direct to NATIONWIDE BENEFIT CONSULTANTS but in addition to the payment made to Metis Law on behalf of Hawkshead Properties a payment of £100,558 was made from funds held by Metis Law to THURLSTONE on the instruction of Karl Dunlop who told me that XXXX XXXX was the person behind Thurlstone CAN YOU PLEASE CONFIRM THAT YOU HAVE SEEN INVOICES FOR ALL THE ABOVE PAYMENTS?

On 12.5.14 I was authorised pursuant to Section 447 and S463A of the Companies Act 1985 in respect of TRANSEURO. TRANSEURO provided the funding to the sales operation of the scheme and received funds by way of a sales commission from Store First. In total TRANSEURO has received in excess of £30m from Store First. CAN YOU PLEASE EXPLAIN HOW, WHEN AND WHY YOU WERE AUTHORISED IN RESPECT OF IMPERIAL? ONE OF THE CAPITA OAK MEMBERS HAD BEEN REPORTING THE CAPITA OAK SCAM TO TPR FOR MORE THAN A YEAR AND ALSO I HAD HANDED EVIDENCE OF CAPITA OAK BEING A PENSION LIBERATION SCAM TO HMRC IN JUNE 2014, BUT NO ACTION HAD BEEN TAKEN BY EITHER TPR OR HMRC.

On 9.10.14 I was authorised in respect of IMPERIAL, trustee of CAPITA OAK. AS ABOVE.

On 28.1.15 I was authorised in respect of TKE Admin which purportedly provided administration services to IMPERIAL. AS ABOVE.

TRANSEURO was incorporated in Gibraltar on 19.4.10. BY WHOM WAS TRANSEURO REGISTERED? THERE MUST BE A RECORD OF THIS AT THE GIBRALTAR COMPANIES HOUSE SURELY?

According to the annual return made up to 19.4.13, the issued share capital of TRANSEURO is £12 comprising 1 ordinary share of £1 held by Toc Nominees Ltd in Nevis, West Indies.

According to the Registrar of Companies, Gibraltar, the sole director of TRANSEURO on incorporation was Octopus International Business Services Ltd (Octopus Gibraltar who resigned on 20.4.10 and was replaced by Tosca Nominees of the Nevis address). SOMEBODY HAS OBVIOUSLY GONE TO A LOT OF TROUBLE TO OBSCURE THE BENEFICIAL OWNER/DIRECTOR OF TRANSEURO. THIS SMELLS OF TAX EVASION AND MONEY LAUNDERING. WHAT ACTION HAS BEEN TAKEN TO REPORT THIS TO THE SFO?

No trading address in the UK has been disclosed for TRANSEURO. However, I have been informed by Toby Whittaker, MD of Group First, Store First and Business First, that TRANSEURO has been based at B1 Business Centre, 25 Goodlass Road, Liverpool L24 9HJ.

On 15.10.14 TRANSEURO applied to Companies House Gibraltar to be struck off the Company Register.

On 19.5.14 I served the S447 authority relating to TRANSEURO on Stephen Michael Talbot at Apt 518 at the Quebec address.

On 18.6.14 I served the S447 authority relating to TRANSEURO on Keith Ryder at his home address of 14 Norton Vale, Thornton Cleveleys, Lancashire FY5 5QB.

I served the authorities relating to Sycamore and TRANSEURO on Deborah Smith of D. Smith Associates at 14 Yellow House Lane, Southport PR8 1ER.

According to the Registrar of Companies, the directors of JACKSON FRANCIS have been Ben Fox and Stuart Chapman-Clark. The registered office of JACKSON FRANCIS was Apt 518 Quebec Building, Bury Street, Salford, Greater Manchester M3 7DU (the Quebec address) until 6.9.14 when it was changed to Station House, Midland Drive, Sutton Coldfield, W. Midlands B72 1TU.

On 11.9.14 Gerald Irwin was appointed liquidator. The statement of affairs of JACKSON FRANCIS as at 11.9.14 shows JACKSON FRANCIS to have no assets and liabilities of £6,321.

ADVANTAGE ACCOUNTING was incorporated on 16.6.2008 with share capital of 1,000 ordinary shares of £1 each and the issued shares are one ordinary share, one ordinary A share and one ordinary B share issued to the subscriber, Online Nominees Ltd., Carpenter Court, Maple Road, Bramhall, Stockport SK7 2DH

According to the Registrar of Companies, the directors of ADVANTAGE ACCOUNTING since incorporation have been Keith John Ryder and Helen Mary Ryder. ADVANTAGE ACCOUNTING was struck off the Company Register and dissolved on 28.9.10. On the application of a creditor who had been a client of ADVANTAGE ACCOUNTING who had a claim for £580,400 plus interest for funds misappropriated from ADVANTAGE ACCOUNTING’s client accounts, ADVANTAGE ACCOUNTING was subsequently restored to the Company Register and wound up on 3.12.13.

Imperial was incorporated on 6.7.12 (8133190) with issued share capital of £1 which has been issued to Roger Chant. THE ORIGINAL DIRECTOR AND SOLE SHAREHOLDER WAS CHRISTOPHER PAYNE. HAS HE BEEN QUESTIONED AS TO WHO INSTRUCTED HIM TO SET IMPERIAL UP AND WHY? IT IS OBVIOUS FROM THE HISTORY OF THE CLASS ACTION’S INVESTIGATIONS AND FROM YOUR WITNESS STATEMENT THAT HE WAS MERELY A “PUPPET” AND THAT PERKINS AND FOWLER WERE THE DE FACTO DIRECTORS AS WELL AS XXXX. HOWEVER, EVIDENCE SUGGESTS THERE WAS A DISPUTE BETWEEN XXXX AND PERKINS OVER FEES AND OTHER ARRANGEMENTS.

The directors of Imperial have been as follows:

Christopher Payne 6.7.12 to 15.10.12

Christopher Payne 1.10.14 to 24.10.14

Karen Burton 15.10.12 to 16.11.12

Karl Dunlop 16.11.12 to 1.2.13

Maria Orolfo 18.10.13 to 25.8.14

Angela Brooks 1.10.14 to 13.10.14

Roger Chant 24.10.14 to present

Although termination of Karl Dunlop’s appointment is recorded as 1.2.13, notice of the termination of his appointment was not filed at Companies House until 10.6.13 and he appears to have continued to act as director until July 2013. XXXX XXXX appears to have acted as a de facto director of Imperial which does not have a company secretary. XXXX MAY HAVE ACTED AS DE FACTO DIRECTOR OF IMPERIAL, BUT WHY HAVE YOU NOT MENTIONED THAT BOTH PERKINS AND FOWLER WERE ALSO CLEARLY DE FACTO DIRECTORS AND THAT NONE OF THE OTHERS MENTIONED WERE MORE THAN “PUPPETS” AND TOOK NO ACTIONS IN RELATION TO IMPERIAL WITHOUT SPECIFIC INSTRUCTIONS AND PERMISSION FROM PERKINS AND FOWLER? IN FACT, MARIA OROLFO WAS APPOINTED BY XXXX BUT RESIGNED WHEN SHE REALISED SHE WAS A NOMINEE DIRECTOR OF A PENSION SCAM. OROLFO WAS ALSO APPOINTED AT THE SAME TIME TO THAMES TRUSTEES (WESTMINSTER SCAM) AND HIGHGATE TRUSTEES (REGENT SCAM). SHE RESIGNED FROM ALL THREE IN OR AROUND AUGUST 2014 AND I APPOINTED MYSELF AS DIRECTOR OF ALL THREE IN ORDER TO TRY TO PROTECT THE VICTIMS (MEMBERS OF CAPITA OAK, WESTMINSTER AND REGENT PENSION SCHEMES) AS COMPANIES HOUSE WAS ON THE POINT OF STRIKING ALL THREE COMPANIES OFF.

On 15.5.14, when I exercised the JACKSON FRANCIS authority I was informed that Stuart Chapman-Clark was not at the office so I asked to speak to whoever was in charge. Eventually, a man attended reception who declined to provide his name or position within JACKSON FRANCIS and he would only take from me a letter addressed to Stuart Chapman-Clark. I have subsequently identified that individual from photographs as being Michael Talbot. The fact that he was on the premises on the day of my visit and was the person who came to speak to me in Chapman-Clark’s absence would appear to be consistent with Melyssa Green’s description of him as a “big boss” and her statement that he shared an office with Chapman-Clark.

Chapman-Clark told me that he had instigated the Store First product and that he had always had a good relationship with Toby Whittaker, the MD of Store First. He said that Sycamore received the loan when money had been tight and that he believed that the loan had been repaid, although I have been unable to identify any loan repayments and no documentation has been produced to verify this loan.

Toby Whittaker, MD of Group First and Store First, told me that he was approached by Mike Talbot and Chapman-Clark acting for TRANSEURO to purchase storage on behalf of their own “super” fund (CAPITA OAK and Henley) but with conditions attached including the payment of the two years 8% guaranteed return upfront to TRANSEURO plus rent earned on the store pods. Toby Whittaker confirmed that the 8% guaranteed return due on the funds invested via CAPITA OAK was paid to TRANSEURO and the 8% guaranteed return due on the funds invested via Henley was paid to a Delaware, USA registered company called Graylaw International.

TRANSEURO is registered in Gibraltar. The sole director of TRANSEURO on incorporation was Octopus International Business Services (Octopus Gibraltar who resigned on 20.4.2010 and was replaced by Tosca Nominees Ltd of the Nevis address. The joint secretaries are Toc Nominees and R.E. Services of 13/1 Line Wall Road, Gibraltar, both of which were appointed on 20.4.14.

According to enquiries made with Octopus on 13.5.14, I was initially informed by Sharron Smith, CEO of Octopus Gibraltar, that whilst the director of TRANSEURO was a Nevis registered company, Tosca Nominees, their client was Stephen Michael Talbot of Quebec Buildings, Bury St, Salford M3 7DU, who gave instructions to Toc Nominees and Tosca Nominees in relation to TRANSEURO and who was introduced to them by Keith Ryder. In spite of my concerted attempts, Mike Talbot has declined to be interviewed in relation to TRANSEURO.

Octopus Gibraltar subsequently provided their Know Your Client information which showed that a Panamanian company JJT Associates International Foundation was the beneficial owner of TRANSEURO from 18.7.11 which appears to be the date on which JJT was incorporated and that their representative was Mr. Ryder.

In an email dated 9.6.14, Ms. Smith of Octopus Gibraltar indicated, contrary to the information supplied on 13.5.14, that it was Mr. Ryder who was their client and that Mr. Talbot only had rights to speak to them regarding TRANSEURO in the absence of Keith Ryder.

Notwithstanding what I was told by Octopus, I note an Owners Declaration document signed by Keith Ryder confirming that instructions to them would be in writing and that the same document empowered Octopus to contact the founder/protector of JJT in the event of a breakdown in communications with Ryder and that the protector of JJT is said to be Talbot. Octopus also provided an Owners Indemnity signed by Ryder as the “intermediary” and in which he is identified as the representative of the owners of JJT. Further confirmation of Ryder’s role is contained in the Bermans correspondence with the liquidator of ADVANTAGE ACCOUNTING in which they state “our clients were introduced to Keith Ryder of Advantage in or around July 2011…Mr. Ryder was engaged to incorporate Transeuro and JJT” and also “Mr. Ryder and Advantage acted, effectively, as Transeuro’s accountant”.

Although Sycamore and JACKSON FRANCIS have been mainly financed by TRANSEURO, Chapman-Clark initially declined to provide me with details of the persons responsible for the management of TRANSEURO without, he said, speaking to the people involved and seeking advice. He eventually provided the name of a Marthinus Joubert with a contact email of mjj@transeuroworldwideholdings.com and the names of a Felix and Fiona whose surnames he could not remember. When I asked where Mr. Joubert was from, Mr. Chapman-Clark said that he was from “everywhere” but he had met him in Malaga and in South Africa. When I subsequently asked him on 7.8.14 about flights paid for by Sycamore for Chapman-Clark, he told me that he sometimes travelled to Spain to meet with “the guys from TRANSEURO”. I received no response to an enquiry email sent on 26.8.14 to the email address provided for Mr. Joubert although I note that the same email address was subsequently used to send an email, purportedly from Mr. Joubert, to Metis Law on 9.12.14.

I have been provided with a number of marketing and sale agreements between TRANSEURO and Store First under which TRANSEURO was to act as Store First’s agent for which they would receive commission on all sales of store pods to the pension schemes.

Enquiries I have made with the liquidator of ADVANTAGE ACCOUNTING, Tony Murphy of Harrisons Business Recovery of London revealed that he has been advised by Bermans Solicitors acting for TRANSEURO that Store First transferred funds, being commissions due to TRANSEURO to an ADVANTAGE ACCOUNTING client deposit a/c at the request of TRANSEURO due to the Cypriot banking crisis. Bermans produced to Mr. Murphy a marketing and sale agreement between TRANSEURO and Store First dated 5.9.11 for a term of 12 months which showed that the rate of commission to be paid to TRANSEURO by Store First was 30%.

In response to enquiries I made with Store First concerning the non-payment of the 8% return guaranteed for two years to CAPITA OAK, Ruth Almond explained to me that there were different marketing and sale agreements depending on whether the store pods were sold either with or without a sub-lease which would be managed by Store First. In the event of the pods being sold with a sub-lease, the commission to be paid to TRANSEURO was to be 30% whilst if the store pod was sold without a sub-lease, the commission to be paid to TRANSEURO was 46%. Toby Whittaker produced to me a printout from Sage of Store First’s supplier activity summary dating from 23.9.11 to 29.9.14 which shows that Store First has paid in excess of £33m to TRANSEURO.

The liquidator of ADVANTAGE ACCOUNTING, Tony Murphy of Harrisons Business Recovery, revealed that he has been advised by Bermans Solicitors instructed by TRANSEURO that Store First transferred funds, being commissions due to TRANSEURO, to an ADVANTAGE ACCOUNTING client deposit a/c at the request of TRANSEURO due to the Cypriot banking crisis. Regarding ownership of these funds, Bermans explained the trading relationship between Store First and TRANSEURO and stated that TRANSEURO is “owned by JJT Associates International Foundation – the protector of which is Stephen Michael Talbot”.

TRANSEURO banked with FBME Bank of Nicosia, Cyprus and during the Cypriot banking crisis of 2013 it obtained a banking facility via a client deposit a/c of ADVANTAGE ACCOUNTING of which Mr. Ryder was director.

Extracts from that ADVANTAGE ACCOUNTING client deposit account 13664368 show a number of transactions which are related to the transfer of funds between Store First, TRANSEURO, Sycamore and CAPITA OAK as follows:

3.13 to 26.4.13 Store First transferred £1,822,127 and on 10.4.13 Store First transferred £6,270. According to the Bermans correspondence, TRANSEURO has a claim in the liquidation of ADVANTAGE ACCOUNTING for a sum of £677,427 representing the balance of these funds.

On 28.3.13 JJT transferred £2.5m to this account and on 2.4.13 an identical amount was transferred to Stirling Law Solicitors of Manchester.

Between 3.4.13 and 6.9.13, £501,000 was transferred to SANDERSON CLARKE on specific instruction from TRANSEURO.

Between 8.4.13 and 23.8 2013, £175,738 was paid to members of CAPITA OAK purportedly on behalf of Thurlstone as inducements to transfer their pension funds to CAPITA OAK and as such represent unauthorised payments from the pension scheme. I note that these payments were made during the hiatus period when Karl Dunlop was seeking to have his resignation filed at Companies House and yet, when I asked him about them on 17.12.14 he told me that he was not aware that ADVANTAGE ACCOUNTING’s bank account had been used to make payments on behalf of CAPITA OAK. THIS REINFORCES THE POINT THAT DUNLOP WAS MERELY A PUPPET AND HAD NEITHER DAY-TO-DAY AUTHORITY NOR RESPONSIBILITY. ALTHOUGH CLEARLY HE WAS PAID BY XXXX, HE DIDN’T APPEAR TO HAVE HAD ANY RECOGNITION OF HIS LEGAL RESPONSIBILITIES TOWARDS IMPERIAL FOR WHICH HE WAS ACCOUNTABLE.

A request was made on 15.10.14 by TOC Nominees who are named as the secretary of the company (Companies House Gibraltar) for the company to be struck off.

Documents and information received from four members of CAPITA OAK indicated they were initially contacted by Craig Mason or Patrick McCreesh of Nunn McCreesh of Its Your Pension Ltd and offered pension review services prior to them being referred to JACKSON FRANCIS or Sycamore for the transfer of their pension to CAPITA OAK.

On 3.3.15 I received an undated letter in which it was stated that Its Your Pension had not traded and was a dormant company and that Nunn McCreesh had traded as an insurance brokerage between 2009 and 2012 when they entered into a verbal arrangement with TRANSEURO where in return for providing pension leads to JACKSON FRANCIS they received a commission from TRANSEURO.

Nunn McCreesh provided JACKSON FRANCIS with 100-200 leads per month which were provided by email and/or telephone for which they received £899,829.86 from TRANSEURO during the period 26.3.12 to 14.5.14.

Chapman-Clark produced a spreadsheet containing details of 921 clients who had transferred pensions totaling at least £16.3m to SIPP providers.

The SIPP providers that Sycamore/JACKSON FRANCIS dealt with include Berkeley Burke, Rowanmoor Pensions, Carey Pensions, London & Colonial and Stadia Trustees. HAVE THESE FIRMS BEEN REPORTED TO THE FCA?

Andy Dibley of Archer Wealth Management produced a list of 118 clients referred by JACKSON FRANCIS who transferred into a SIPP invested in Store First HAS ARCHER WEALTH BEEN REPORTED TO THE FCA?

Alfie Morrison of Moneywise produced a list of 104 clients referred by JACKSON FRANCIS who transferred their pensions into a SIPP invested in Store First. 76 clients transferred to a Berkeley Burke SIPP and 28 clients to a Rowanmoor SIPP. HAS MONEYWISE BEEN REPORTED TO THE FCA?

Capita Oak Pension Scheme

Alan Fowler states he was approached by XXXX XXXX in March 2012 and requested by XXXX “to assist in establishing the Scheme”. Fowler informed me that RP Medplant, a company registered in Cyprus, established a pension scheme the membership of which was made available to persons other than employees and that it accommodated the requirements of XXXX. Fowler states he does not know the individuals responsible for the management and control of RP Medplant. Fowler produced a copy of the “governing document of the scheme” dated 23.7.12 between RP Medplant, the scheme sponsor, and Imperial who was appointed to be the administrator of the scheme. IT STRIKES ME FOWLER IS MAKING A POOR EFFORT TO COVER UP THE TRUTH. HOW DO YOU “ASSIST IN ESTABLISHING A SCHEME”? IT TAKES ONE PERSON TO REGISTER A SCHEME WITH HMRC AND TPR. NOT ONE PERSON TO OPERATE THE MOUSE AND AN ASSISTANT TO OPERATE THE KEYBOARD. HOW CAN RP MEDPLANT HAVE ESTABLISHED A PENSION SCHEME? FIRSTLY, RP MEDPLANT DOESN’T EXIST (ALTHOUGH THERE IS A COMPANY REGISTERED IN CYPRUS CALLED RP MED PLANT) AND SECONDLY IF FOWLER STATES HE DOES NOT KNOW THE INDIVIDUALS RESPONSIBLE FOR THE MANAGEMENT AND CONTROL OF RP MEDPLANT, HOW COULD ANY OFFICER OF THE COMPANY (EVEN IF IT HAD EXISTED) HAVE COMMUNICATED WITH FOWLER TO TELL HIM THAT THEY JUST HAPPENED TO HAVE SET UP A PENSION SCHEME? IS FOWLER SERIOUSLY EXPECTING YOU TO BELIEVE THAT JUST WHEN HE HAD BEEN ASKED TO “ASSIST” IN ESTABLISHING A PENSION SCHEME THAT SOME PERSON IN CYPRUS CALLED HIM OUT OF THE BLUE AND BY SHEER COINCIDENCE INFORMED HIM THEY HAD A SPARE PENSION SCHEME? BUT THEN NOT LEAVE A NAME.

ACCORDING TO THE CAPITA OAK TRUST DEED, RP MEDPLANT APPOINTED IMPERIAL AS THE TRUSTEE/ADMINISTRATOR. AND SOMEONE WHOSE SIGNATURE LOOKS LIKE IT MIGHT BE ALAN FOWLER SIGNED ON BEHALF OF RP MEDPLANT. CAN YOU CHECK THE SIGNATURE ON THE TRUST DEED PLEASE AND COMPARE IT TO ALAN FOWLER’S SIGNATURE? ALSO, SOMEONE WHOSE SIGNATURE LOOKS LIKE “KAREN BURTON” SIGNED ON BEHALF OF IMPERIAL. HOWEVER, IT IS NOTHING LIKE THE SIGNATURE ON VARIOUS COMMUNICATIONS I HAVE SEEN WHICH WERE SIGNED BY THE REAL KAREN BURTON (PRESUMABLY) BUT IS EERILY SIMILAR TO THE HANDWRITING OF ANTHONY SALIH OF PREMIER PENSION TRANSFERS OF 31 MEMORIAL ROAD, WORSLEY WHICH WAS THE ORIGINAL ADDRESS OF CAPITA OAK AND WHERE THE PENSION TRANSFERS WERE CARRIED OUT.

FURTHERMORE, RP MEDPLANT SET UP A SUBSEQUENT PENSION SCHEME CALLED WESTMINSTER, WHOSE TRUSTEE WAS THAMES AND TO WHICH IMPERIAL WAS APPOINTED AS ADMINISTRATOR. THIS SCHEME WAS ANOTHER ONE OF XXXX’S AND THE SAME “TEAM” CARRIED OUT THE ADMINISTRATION I.E. “ANTHONY, BILL, SARAH AND ALAN” (SALIH, PERKINS, DUFFELL AND FOWLER). THE TRANSFER RECORDS OF BOTH CAPITA OAK AND WESTMINSTER WERE KEPT IN THE SAME FORMAT AND COLOURS AND HAD THE SAME SPELLING AND GRAMMAR MISTAKES. ERGO, IT IS CLEAR BOTH SCHEMES WERE OPERATED BY THE SAME “TEAM” – ALTHOUGH THIS HAS BEEN EMPHATICALLY DENIED BY BRIAN DOWNS (ACCOUNTANT).

It is noted that the CAPITA OAK scheme documentation has been signed by unidentified individuals whose signatures have not been witnessed. Fowler states he has no knowledge of who signed the document on behalf of RP Medplant or Imperial and he states he did not sign the document in any capacity. AS ABOVE, PLEASE CHECK FOWLER’S SIGNATURE. IF FOWLER REALLY DID NOT SIGN THE DEED, WHY DID HE NOT CHECK THE DOCUMENT TO MAKE SURE IT DID NOT HAVE FORGED SIGNATURES? FOWLER WAS PAID £86K TO “ASSIST” IN SETTING UP CAPITA OAK AND HE IS A QUALIFIED, EXPERIENCED PENSIONS LAWYER, SO HE COULD HARDLY HAVE GOT THIS WRONG – COULD HE?

The scheme document appears as if it may have been signed on behalf of Imperial by “K Burton”, however she was not appointed until 15.10.12. Burton has not responded to my enquiries. Payne, who was the sole director of Imperial at the date of the scheme document, told me that he had not signed the scheme document and he guessed that the document had been signed by Burton on behalf of Imperial. Payne said he didn’t know who had signed the document on behalf of RP Medplant. SO PAYNE IS ASKING YOU TO BELIEVE THAT HE WAS SOLE SHAREHOLDER AND DIRECTOR OF IMPERIAL WHICH WAS APPOINTED AS TRUSTEE/ADMINISTRATOR TO A PENSION SCHEME BUT HE DID NOT CHECK THE DEED OR VERIFY WHO HAD SIGNED THE DOCUMENT ON BEHALF OF RP MEDPLANT? THIS IS STRETCHING CREDIBILITY BEYOND THE LIMIT.

Payne told me he is an accountant who supplies clients with incorporated companies and that he incorporated Imperial, of which he was at one time a director, at the request of Fowler who he described as a “one off client” and legal advisor to CAPITA OAK and who, Payne said, also requested the incorporation of TKE. IF FOWLER REQUESTED THE INCORPORATION OF BOTH IMPERIAL AND TKE, AND WAS “LEGAL ADVISOR” TO CAPITA OAK, THEN IT IS CLEAR FOWLER WAS RESPONSIBLE IN A “SHADOW” CAPACITY FROM THE VERY BEGINNING BUT FOR REASONS OF HIS OWN NEVER APPEARED AS A DIRECTOR FOR EITHER. HE OBVIOUSLY “PULLED THE STRINGS” OF PAYNE AND SUBSEQUENT DIRECTORS (ALONG WITH XXXX IN THE CASE OF DUNLOP) BUT OPERATED IN THE SHADOWS. FOWLER USED TO PRACTICE AS A PENSIONS LAWYER WITH THE FIRM STEVENS & BOLTON IN GUILDFORD SO HE KNEW ABOUT THE LEGAL REQUIREMENTS FOR A PENSION SCHEME, SO WHY DID HE NOT ENSURE THAT THE SCHEME WAS LEGITIMATELY SET UP AND RUN?

Payne informed me he resigned as director of Imperial on 15.10.12 in favour of Burton at the request of Fowler as, according to Payne, Burton had experience of acting as a trustee. Although Payne had resigned as director of Imperial he told me that he continued to act as Imperial’s accountant and signatory to Imperial’s bank account. He also retained the Companies House authentication (pin). Payne told me that he arranged for the 5% administration fees to be transferred from Imperial to TKE after the receipt of pension transfers and arranged the transfer of funds to Metis Law on the authorisation of Dunlop who was director of Imperial at the relevant time. IF PAYNE CONTINUED TO ACT AS IMPERIAL’S ACCOUNTANT AND SIGNATORY TO IMPERIAL’S BANK ACCOUNT, WHY DID HE NOT ENSURE THAT ALL TRANSACTIONS WERE COMPLIANT? HE KNEW FULL WELL THAT IMPERIAL WAS BEING USED TO RUN A PENSION SCHEME AND WAS HANDLING MILLIONS OF POUNDS’ WORTH OF MEMBERS’ FUNDS BUT DID NOTHING TO CHECK THAT THE SCHEME WAS BEING OPERATED IN A COMPLIANT AND LEGAL MANNER. THE ANSWER, UNDOUBTEDLY, IS THAT HE ONLY EVER ACTED ON THE INSTRUCTIONS OF FOWLER WHO WAS THE DE FACTO DIRECTOR OF IMPERIAL.

Payne was also director of TKE from incorporation until 1.4.14 when he was replaced by Sarah Duffell and he told me it was an oversight that she had not been appointed in his place much earlier as it was Duffell who was in control of TKE’s bank account. PAYNE CLAIMS TO BE AN ACCOUNTANT WHO SPECIALIZES IN COMPANY INCORPORATION. HOW CAN THIS POSSIBLY HAVE BEEN AN “OVERSIGHT”?

Burton has not responded to my enquiries, however I note she resigned on 16.11.12 on the same day Dunlop was appointed.

Dunlop was appointed director of Imperial on 16.11.12. He told me he was asked by XXXX to take on the role on a temporary basis and that he did not receive any payment from Imperial as he was just doing a favour for XXXX. From other documents I have seen it appears that Dunlop’s statement regarding payment was factually correct but, nonetheless, misleading. Specifically, I have been sent copies of emails by Perkins and while it is clear they have been extracted from a string of messages and while Perkins has ignored my request for copies of the entire conversation, I nevertheless note the contents of those messages. I AM CURIOUS AS TO WHY YOU HAVE NEVER ASKED ME FOR ANY EVIDENCE DURING YOUR INVESTIGATIONS, AS YOU KNEW I HAD BEEN INVESTIGATING CAPITA OAK AND IMPERIAL. HAD YOU ASKED ME, I WOULD HAVE BEEN ABLE TO PROVIDE YOU WITH COMPLETE EMAIL STRINGS, RATHER THAN CROPPED ONES PROVIDED BY PERKINS WHO WAS CLEARLY TRYING TO BE SELECTIVE ABOUT THE EVIDENCE HE GAVE YOU IN ORDER TO PROTECT HIMSELF AND FOWLER.

On 22.5.13 Dunlop sent an email to Perkins, principally in connection with his removal as a director of Imperial. He states: “James pays my fees directly himself from his own fees sent by yourselves. I now have remaining fees to collect from him. Can you deal with his fees immediately please so I can complete my tenure as director of Imperial”.

Later the same day, in a further email to Perkins, Dunlop stated: “it is approximately 4 weeks since I requested removal as director of Imperial, I charge £2k per month for my services”. As director of Imperial, Dunlop gave instructions to Perkins, Holmes, Duffell and Payne to transfer funds to Metis Law for the investment in store pods with Store First. I SUGGEST THIS IS PURE NONSENSE. DUNLOP WOULD NOT HAVE KNOWN WHAT TRANSFERS HAD BEEN RECEIVED INTO THE IMPERIAL BANK ACCOUNT WHICH WAS SET UP AND CONTROLLED BY PAYNE, SO WOULD NOT HAVE KNOWN HOW MUCH TO TRANSFER OR WHEN. HE MAY HAVE SIGNED A MANDATE FOR METIS LAW PURPOSES BUT THAT WOULD HAVE BEEN THE EXTENT OF HIS INVOLVEMENT.

Dunlop, upon appointment, authorised the transfer of funds to Metis Law for the purpose of purchasing store pods from Store First. DUNLOP MAY HAVE SIGNED SOMETHING AT SOME POINT, BUT TO BE HONEST I CAN’T SEE HOW HIS INVOLVEMENT IN THE FUND TRANSFER PROCESS WAS ANYTHING OTHER THAN A FRONT TO PROTECT PERKINS AND FOWLER AS THEY CLEARLY WISHED TO REMAIN “ANONYMOUS” IN THE PROCESS.

In total Imperial received some £10.8m of transferred pensions into its Barclays a/c and some £10.1m was transferred to Metis Law who facilitated the purchase of some £9.8m of store pods which are held by Imperial as the trustee of CAPITA OAK.

Dunlop told me that Bill Perkins and his organisation, including Jason Holmes and Sarah Duffell, controlled Imperial’s bank account and the administration of CAPITA OAK. When I asked how members of the public were introduced to CAPITA OAK, Dunlop said he didn’t know in detail other than that it was done via Chapman-Clark and Mike Talbot’s company, neither of whom he had ever met. THIS DEMONSTRATES THAT HE WAS NOTHING MORE THAN A PUPPET, ANSWERABLE TO XXXX/PERKINS/FOWLER.

Although Companies House records Dunlop resigning as director of Imperial on 1.2.13, notice of his termination of office was not filed until 10.6.13 and he appears to have continued to authorise payments to Metis Law up to 5.7.13. Dunlop said he had instructed Perkins to remove him as director of Imperial but he failed to file the form TM01 so he continued to authorise the transfers and provide instructions to Metis Law. I SUGGEST PERKINS DID THIS DELIBERATELY TO AVOID THE NECESSITY OF FINDING ANOTHER PUPPET DIRECTOR. HOW CAN DUNLOP CLAIM THAT HE DID NOT WANT TO CONTINUE TO ACT AS A DIRECTOR IF HE CONTINUED TO AUTHORISE TRANSFERS TO METIS LAW? IT JUST DOESN’T MAKE SENSE, UNLESS HIS “AUTHORISATION” WAS MERELY A SIGNATURE WHICH REMAINED ON A MANDATE.

Dunlop produced copies of extracts of emails dealing with the matter of his resignation and involving Dunlop, Perkins, Fowler and XXXX. From those which are dated between 23rd and 31st May 2013, it seems clear Dunlop was keen to have his resignation actioned but was unable to process this without input from others, specifically from those involved in the email exchanges, who, for reasons which are not clear to me, were delaying matters. Further in this regard, I note that, when I saw Dunlop on 17.12.14 he confirmed to me that he first asked Perkins to remove him as a director in a telephone call and that it took something like 8 weeks for Perkins to file the form. DUNLOP ONLY HAD TO DOWNLOAD A FORM FROM THE COMPANIES HOUSE WEBSITE AND RESIGN HIMSELF. HE DIDN’T NEED PERKINS OR ANYONE ELSE TO “ACTION” THIS – ALTHOUGH HE CLEARLY BELIEVED THAT HE DIDN’T HAVE THE AUTHORITY TO DO SO HIMSELF WITHOUT PERKINS’ “PERMISSION”. THIS FURTHER CONFIRMS THAT PERKINS (ALONG WITH FOWLER) WAS A DE FACTO DIRECTOR OF IMPERIAL.

Dunlop was succeeded as director by Maria Orolfo (who resides in Spain). XXXX told me that he “sourced” Orolfo as a nominee director of Imperial from Europe Emirates who supply a nominee director service. He said that following Dunlop’s resignation, Imperial was left without a director which he feared may result in advance tax charges on the pension scheme. He said that as Orolfo was an employee of Europe Emirates, he can only assume that she consented to act as director. OROLFO DOES NOT RESIDE IN SPAIN. SHE IS BASED IN DUBAI. SHE WAS APPOINTED AS A NOMINEE DIRECTOR OF THREE PENSION TRUSTEE COMPANIES BY XXXX: IMPERIAL (CAPITA OAK); THAMES (WESTMINSTER) AND HIGHGATE (REGENT). OROLFO DID NOT REALISE (ACCORDING TO HER BOSS, ADRIAN OTON OF EUROPE EMIRATES) THAT ANY OF THE THREE COMPANIES WERE PENSION TRUSTEES OF FRAUDULENTLY-RUN SCHEMES AND SHE RESIGNED FROM ALL THREE IN AUGUST 2014. OTON ALSO INFORMED ME THAT HIS COMPANY HAD SET UP A PREMIER PENSION SOLUTIONS FOR STEPHEN WARD IN RAK A YEAR OR SO EARLIER.

I have seen copies of email exchanges between XXXX, Fowler and Tom Biggar between 17 and 30 October 2013 from which it appears Orolfo was only appointed to prevent Companies House from dissolving Imperial. THEY OBVIOUSLY FAILED TO FIND ANY OTHER MUG WILLING TO TAKE ON THIS POISONED CHALICE.

XXXX said he did not file form TM01 notifying Maria Orolfo’s termination of appointment with Companies House and that his signature on that document is a forgery. THIS CONFIRMS THAT OROLFO AND PREVIOUS DIRECTORS OF IMPERIAL WERE MERELY PUPPETS AND THAT PERKINS AND FOWLER WERE THE DE FACTO DIRECTORS BEHIND THE ENTIRE CAPITA OAK OPERATION, ALONG WITH XXXX TO SOME EXTENT. HOWEVER, WHILE XXXX WAS AT THE “SHARP END” I.E. RUNNING THE PROMOTION AND DISTRIBUTION OF CAPITA OAK, PERKINS AND FOWLER WERE “RUNNING THE ENGINE ROOM” I.E. THE PENSION AND BANK TRANSFERS.

I have not attempted contact with Orolfo because I understand she is not present at the London address given for her at Companies House and have not sought to contact Europe Emirates as it is based in Dubai. YOU ARE RIGHT AS SHE HAS NEVER BEEN TO THE LONDON ADDRESS.

While Orolfo resigned on 25.8.14 (though XXXX claims the signature on the document submitted to the registrar of Companies is a forgery) I note she was not replaced until Payne appointed himself director on 1.10.14. PAYNE DID THIS OUT OF DESPERATION AS IT WAS CLEAR FROM THE WHOCALLSME WEBSITE THAT UNREST WAS GROWING AT THE DISAPPEARANCE OF THE FUNDS, THE 16% “GUARANTEED RENT”, AND THE FACT THAT NONE OF THE MEMBERS WAS RECEIVING RESPONSES TO THEIR DESPERATE PLEAS FOR INFORMATION. PAYNE WAS HIMSELF DODGING CALLS FROM THE BBC AND ME AT THE TIME, ALTHOUGH HE WAS COMMUNICATING TO A LIMITED EXTENT WITH METIS LAW AT THE TIME.

At that same time it would appear Angela Brooks appointed herself director from 1.10.14. I am aware that she is chairman of a group which operates under the title of Ark Class Action and which was set up to deal with the “Ark pension liberation fraud”. I APPOINTED MYSELF DIRECTOR OF IMPERIAL IN CONSULTATION WITH METIS LAW BECAUSE OF PAYNE’S FAILURE TO RESPOND TO COMMUNICATIONS. METIS LAW REALISED THEY THEMSELVES WERE IN A “TIGHT SPOT” AND WANTED TO BE ABLE TO WORK WITH SOMEBODY WHO COULD HELP UNRAVEL THE MESS SINCE THE PENSIONS REGULATOR HAD FAILED TO TAKE ANY ACTION DESPITE REPEATED REQUESTS BY MEMBERS WHO FEARED THEY HAD LOST THEIR PENSIONS TO A SCAM. METIS LAW SAID THAT AS SOON AS I WAS APPOINTED DIRECTOR, THEY WOULD GIVE ME ALL THE INFORMATION AND DOCUMENTATION ON THE CAPITA OAK/STORE FIRST TRANSACTIONS ONCE MY APPOINTMENT WAS PUBLISHED ON THE COMPANIES HOUSE WEBSITE. I WARNED PARTNERS COOPER AND SHARMA OF METIS LAW THAT AS SOON AS PAYNE REALISED I WAS A DIRECTOR HE WOULD REMOVE ME AS HE HAD THE COMPANIES HOUSE PIN NUMBER AND THEY MIGHT ONLY HAVE A FEW MINUTES TO ACT. THEY DID SEND ME THEIR IMPERIAL/CAPITA OAK ACCOUNTING RECORDS BUT MINUTES LATER PAYNE REMOVED ME AND THEY WERE UNABLE TO PROVIDE ME WITH ANY FURTHER INFORMATION.

On 13.10.14 Brooks was immediately removed by Payne who then resigned on 24.10.14 allegedly due to threats made on social media. PAYNE HAD DELIBERATELY IGNORED THE DESPERATE PLEAS OF NUMEROUS CAPITA OAK VICTIMS IN SEPTEMBER AND OCTOBER 2014. I HAVE BEEN THROUGH THE WHOLE WHOCALLSME THREAD FOR SEPTEMBER AND OCTOBER 2014 BUT THERE ARE NO THREATS WHATSOEVER. THE ONLY POSTS OF ANY SIGNIFICANCE CONCERNING PAYNE WERE INFORMATION ABOUT HIS FIRM, PHOENIX ACCOUNTING AND THE FACT THAT LYNN PAYNE OF FJP INVESTMENTS WAS PROMOTING STORE FIRST.

From 24.10.14 the director of Imperial has been Roger Chant, a Bromley businessman (butcher) and associate of Payne. I am not aware that Chant has any experience in being a director of a company which acts as a trustee of a pension fund. CHANT WAS PAID £100 A WEEK TO BE A PUPPET DIRECTOR AND SIMPLY KEEP QUIET AND SIGN LETTERS WRITTEN BY FOWLER.

Chant told me he accepted his appointment in place of Payne as Payne was being “bullied” on the whocallsme website and he didn’t like bullies and to find out on behalf of members of CAPITA OAK what had happened to their investments and their due returns. Nevertheless, I am aware from Brian Downs that Payne first approached him with a suggestion that he become director and that he declined whilst agreeing to provide assistance, which was formalized in the form of an appointment letter signed by Payne on 2.10.14. CHANT HAS NEVER DONE ANYTHING OTHER THAN THE BARE MINIMUM OF SIGNING LETTERS WRITTEN BY PERKINS/FOWLER/DOWNS. HE HAS NEVER REPLIED TO ANY EMAILS OR PHONE CALLS FROM ME OR MEMBERS.

Chant told me he had been in business for over 20 years but he did not have any experience in dealing with pension schemes. He has been assisted by Downs, Adrian Gilan of Bark & Co Solicitors, and Perkins and Fowler in making enquiries of Imperial’s activities and CAPITA OAK’s assets on behalf of members and making announcements in the form of letters issued to members. IF CHANT CLAIMS HE HAS BEEN “ASSISTED” BY DOWNS, PERKINS AND FOWLER HE IS LYING. HE IS THE LAST IN A LONG LINE OF PUPPETS MANIPULATED AND CONTROLLED BY PERKINS AND FOWLER.

Since taking office Chant has caused announcements to be issued to all CAPITA OAK members on 8 and 23 January 2015 and has caused what he refers to as a “detailed financial report” to be prepared. Whilst the information from this report has not been communicated to members, I have seen a copy and note that it is no more than an unaudited analysis of Imperial’s Barclays bank statements for the period from 30.7.12 to 13.9.13. From other correspondence I have received from Chant it appears clear he had no prior knowledge of the scheme and was having to piece together information from a variety of sources. HOW DOES A PERSON “CAUSE” A REPORT TO BE PREPARED? ESPECIALLY WHEN THAT PERSON HAS ZERO KNOWLEDGE OF PENSIONS OR ACCOUNTS. THE REPORT HE IS REFERRING TO WAS A BRIEF BANK RECONCILIATION PRODUCED BY BRIAN DOWNS (WHO BECAME THE “MOUTHPIECE” FOR IMPERIAL) OF DOWNS & CO ACCOUNTANTS IN JANUARY 2015, THREE MONTHS AFTER DOWNS HAD PROMISED THE MEMBERS HE WOULD PRODUCE ACCOUNTS FOR THE CAPITA OAK SCHEME. DOWNS DOGGEDLY REFUSED TO INCLUDE THE METIS LAW ACCOUNTS IN HIS “REPORT” DESPITE REPEATED REQUESTS BY ME TO DO SO. DOWNS CLAIMED HE COULD NOT INCLUDE THE METIS ACCOUNTS BECAUSE HE “DID NOT KNOW THE SOURCE OF THE DATA” DESPITE ME PROVIDING PROOF TO PAUL THOMAS (AN IFA WHO HAS BEEN WORKING CLOSELY WITH DOWNS AND PERKINS BY HIS OWN ADMISSION) THAT METIS SENT ME THE ACCOUNTS BY EMAIL. FURTHER, DOWNS REFUSED TO PROVIDE ME WITH COPIES OF IMPERIAL’S BANK STATEMENTS AND ALSO REFUSED TO ALLOW AN INDEPENDENT AUDIT OF THE ACCOUNTING RECORDS BY BRADBURY STELL ACCOUNTANTS WHOM I HAD ASKED TO CARRY OUT AN AUDIT ON BEHALF OF THE CAPITA OAK MEMBERS.

There is correspondence which has been written on behalf of Imperial in an attempt to locate the missing money and seeking information. I note the responses received have been unhelpful for example this investigation has been used as an excuse to not provide information. DOWNS CLAIMED TO HAVE WRITTEN TWO LETTERS TO TOBY WHITTAKER AT STORE FIRST WHICH HE STATED WERE IGNORED. THIS IS HARDLY THE “DETAILED” INVESTIGATION HE REPEATEDLY CLAIMED TO HAVE CARRIED OUT.

There is a series of emails which document a struggle between parties such as Chant, Payne, Downs, Metis Law and Brooks to gain control/retain control of Imperial. THERE WAS NO “STRUGGLE” AS YOU HAVE STATED. METIS LAW WANTED ME TO BE THE DIRECTOR OF IMPERIAL SO THAT TOGETHER WE COULD ATTEMPT TO UNTANGLE THE MESS LEFT BEHIND BY IMPERIAL PREVIOUS DIRECTORS/SHADOW DIRECTORS AND FULLY EXPOSE THEM FOR THE NEGLIGENCE AND FRAUD THEY HAD BEEN INVOLVED IN. INDEED, AT ONE POINT THEY SAID PAYNE WAS “WARMING” TO THE IDEA, BUT THEN PERKINS AND FOWLER INSTRUCTED PAYNE TO REMOVE ME AS DIRECTOR AS THEY DID NOT WANT ME UNCOVERING AND EXPOSING THEIR INVOLVEMENT IN IMPERIAL/CAPITA OAK. I note that currently there would appear to be £9.8m of illiquid assets namely store pods being held in the name of Imperial as trustee of CAPITA OAK with no one with experience being involved in the management of the investment on behalf of members and the payment of pensions due to those members. Furthermore, from correspondence I have received from Chant, I am aware that a small number of members have sought to transfer their investment out of the scheme but that Chant has determined it would be inappropriate of him to authorise such transfers while he conducts further enquiries. THERE HAVE BEEN FOUR PENSIONS OMBUDSMAN’S DETERMINATIONS IN RESPECT OF MR. X AND THREE OTHER MEMBERS. NEITHER CHANT NOR ANYBODY ELSE COULD HAVE AUTHORISED THE DETERMINED TRANSFERS BECAUSE THERE WAS NO MONEY LEFT TO TRANSFER AND NO SCHEME WOULD HAVE ACCEPTED IN SPECIE TRANSFERS OF THE ASSETS SINCE THEY WERE NON-STANDARD (ACCORDING TO THE FCA).

There is a spreadsheet setting out responses received from members of the public who became members of CAPITA OAK. The questionnaires and responses are discussed further below. There is evidence that the lack of management of Imperial has directly affected the members of CAPITA OAK and there is evidence of members being unable to receive the payment of pensions due to them. IT IS INDISPUTABLE THAT PERKINS, FOWLER AND XXXX – AS DE FACTO DIRECTORS OF IMPERIAL – KNEW THAT 100% OF THE CAPITA OAK MEMBERS’ £10M FUNDS WERE INVESTED IN STORE FIRST STORE PODS; THAT THE PROMISED 8% “GUARANTEED RENT” HAD ALREADY BEEN PAID TO TRANSEURO, AND THAT NO PROPER ACCOUNTS (EITHER FOR THE SCHEME OR THE MEMBERS INDIVIDUALLY) HAD BEEN KEPT. CALLING THIS “LACK OF MANAGEMENT” IS SURELY A BIT LIKE REFERRING TO NIAGARA FALLS AS A STREAM?

Whittaker, MD of Group First and Store First, told me he was approached by Talbot and Chapman-Clark acting for TRANSEURO to purchase storage on behalf of their own “super” fund (CAPITA OAK and Henley) but with conditions attached including the payment of the two years’ 8% guaranteed return up front to TRANSEURO plus rent earned on the store pods. Whittaker confirmed that the 8% guaranteed return due on the funds invested via CAPITA OAK was paid to TRANSEURO.

XXXX told me it was the members of CAPITA OAK who decided to invest in Store First as there was a written instruction in the application pack that the client wanted to invest in Store First. THIS IS AN EXTRAORDINARY STATEMENT! NONE OF THE MEMBERS HAD EVER HEARD OF STORE FIRST UNTIL IT WAS PRESENTED TO THEM AS A “DONE DEAL” AND SOLD TO THEM AS AN EXCELLENT INVESTMENT OPPORTUNITY FOR THEIR PENSIONS ON THE BASIS OF THE GUARANTEED 8% RETURN AND THE 5% “CASHBACK”. NOT A SINGLE MEMBER CAME TO IMPERIAL AND ASKED TO TRANSFER TO CAPITA OAK BECAUSE THEY WERE SO ENTHUSIASTIC ABOUT STORE FIRST AS THEY HAD DISCOVERED IT THEMSELVES AND WERE DESPERATE TO INVEST THEIR PENSIONS IN IT. THEY WERE CONVINCED BY JP STERLING OR WHOEVER THEIR INTRODUCER WAS THAT THERE WERE SIGNIFICANT ADVANTAGES TO BE GAINED FROM TRANSFERRING TO CAPITA OAK WHICH HAD ONLY ONE SINGLE INVESTMENT (STORE FIRST) AND NO ALTERNATIVES WERE OFFERED. THEY WERE ALSO “SWEETENED” WITH THE PROMISE OF THE “NON-REPAYABLE” 5% THURLSTONE “LOANS”.

Dunlop told me that in relation to CAPITA OAK, he acted on clients’ instructions as were recorded in the application documentation to invest in commercial property. When I asked who made the decision to invest in storage with Store First, Dunlop suggested I ask XXXX or the promoters of the scheme, Talbot and Chapman-Clark. When I put the question to XXXX on 4.12.14 he said it was the client’s decision and that there were individual written instructions in the membership application pack. I am aware from documents and information obtained during the course of my investigation that clients were not offered any alternative to Store First. IT APPEARS THERE WAS A CONCERTED “PARTY LINE” BETWEEN DUNLOP AND XXXX. THE EXTRAORDINARY THING THAT APPEARS TO EMERGE FROM RESPONSES TO YOUR ENQUIRIES IS THAT DUNLOP AND XXXX ARE BLAMING THE CAPITA OAK MEMBERS THEMSELVES FOR WHAT WAS SO CYNICALLY, AGGRESSIVELY AND DISHONESTLY PROMOTED TO THEM.

When asked whose decision it was that 100% of the available assets of the scheme should be invested in Store First as opposed to other alternative and more liquid assets, Fowler informed me that “all decisions as to investments were, to the best of my knowledge, made solely by the directors in office at the material time such investments were made. I believe that Dunlop and Orolfo were the directors at the material times”. THIS RESPONSE IS PURE NONSENSE. FOWLER KNEW PERFECTLY WELL THAT DUNLOP AND OROLFO WERE MERE PUPPETS AND SIMPLY DID AS THEY WERE TOLD BY XXXX FOR “MINIMAL” (IN THE GRAND SCHEME OF THINGS) REMUNERATION. IN FACT, FOWLER HIMSELF ADMITTED TO XXXX THAT THE STORE FIRST INVESTMENT WAS THE SUBJECT OF COUNSEL’S OPINION. FOWLER IS BEING DELIBERATELY EVASIVE AND MISLEADING IN HIS ANSWER TO THIS PARTICULAR ENQUIRY.

Fowler advised me that he had not at any time “directed, influenced or controlled the investment of CAPITA OAK’ assets and that all decisions regarding investments were to the best of his knowledge made solely by the directors in office at the material time i.e. Dunlop and Orolfo. THIS MAY INDEED BE TRUE. HOWEVER, FOWLER KNOWINGLY SET UP CAPITA OAK WITH STEPHEN WARD AND ANTHONY SALIH IN THE FULL KNOWLEDGE THAT ALL THOSE WHO TRANSFERRED TO THE SCHEME WERE DOOMED TO HAVE THEIR ENTIRE PENSION TRANSFER INVESTED IN ONE SINGLE ILLIQUID, SPECULATIVE, HIGH-RISK PROPERTY INVESTMENT. AS A PENSIONS LAWYER, HE KNEW FULL WELL THE RISKS TO WHICH HE WAS EXPOSING THE VICTIMS.

I asked Perkins about the decision to invest in Store First and he said it was first suggested by XXXX, who also made the decision to instruct Metis Law at the same time as he, XXXX, decided that Dunlop should replace Burton as director of Imperial. Perkins added that Fowler had sought counsel’s advice on the investment but I have never seen such advice and it has not been mentioned to me by Fowler. FOWLER “MENTIONED” IT IN AN EMAIL TO XXXX. I SIMPLY CANNOT IMAGINE WHAT “COUNSEL’S ADVICE” WOULD HAVE SAID ABOUT THE RISKS OF SUCH AN INVESTMENT, BUT HAD COUNSEL BEEN COMPETENT OR KNOWN THE FIRST THING ABOUT PENSIONS HE/SHE WOULD SURELY HAVE SAID SOMETHING ALONG THE LINES OF “MAKE SURE THE SCHEME’S INVESTMENTS ARE DIVERSE, PRUDENT AND LIQUID”.

Perkins produced a copy of an email between XXXX and Fowler dated 30.10.12 which states the following: “I hope you don’t mind but I’ve taken the lead and appointed my guys, Metis Law. We had a conference call with their tax chap in the early days of structuring the holding vehicle. They’re sensible chargers and know what they’re doing as they’re purely a commercial firm. I will need assistance from you in gathering the necessary DD for their regulatory compliance please. This matter is really pressing. We need to complete a purchase this week. With regard to the instruction letter from the client, we can get this done but we have not been advised when this needs to be done. Bill rather unhelpfully said “at the end” when first discussed but other than that nothing has been said.” METIS LAW INFORMED ME THAT THEY WERE “INVITED TO TENDER AGAINST SOME LARGE FIRMS”. I SUBMIT THEY WERE SPECIFICALLY CHOSEN BY XXXX AND THAT THIS WAS ACCEPTED BY FOWLER PURELY BECAUSE THEY WERE A SMALL, INEXPERIENCED AND NAÏVE FIRM WHO WERE UNLIKELY TO ASK ANY QUESTIONS AND WERE DESPERATE FOR THE BUSINESS. THEY CERTAINLY DIDN’T KNOW ANYTHING ABOUT PENSIONS AND DIDN’T DO ANY DUE DILIGENCE EITHER ON THE SCHEME, THE TRUSTEES, OR THE ASSETS PURCHASED. ANY EXPERIENCED FIRM WOULD HAVE INSISTED ON VALUATIONS AND WOULD HAVE ENSURED THAT THE SCHEME’S ASSETS WERE PURCHASED IN ACCORDANCE WITH PENSION INVESTMENT REGULATIONS AND GUIDELINES RATHER THAN JUST ACCEPTING THEIR CLIENT’S INSTRUCTIONS. METIS LAW TOLD ME THAT THEY PURCHASED A VARIETY OF PROPERTY ASSETS FOR THEIR CLIENTS AND THAT IT WAS NOTHING TO DO WITH THEM IF THE PURCHASES WERE IMPRUDENT OR RESULTED IN THE CLIENT LOSING THEIR MONEY BECAUSE THE ASSET TURNED OUT TO BE WORTHLESS. THIS MAY OR MAY NOT BE TRUE (ALTHOUGH I SUSPECT NOT) BUT IN THE CASE OF A PENSION SCHEME’S ASSETS WHERE THE TRUSTEE IS PURCHASING ASSETS IN TRUST FOR A PENSION SCHEME IT MOST CERTAINLY IS NOT TRUE AND METIS LAW WERE UNDOUBTEDLY NEGLIGENT.

This is an apparent contradiction of Fowler’s assertion above. I have also seen other email correspondence dated 19.11.13 involving Fowler, XXXX and Dunlop and the authorisation of a payment to Metis Law, from which it appears that the first named believes Dunlop will follow instructions from XXXX. THIS FURTHER CONFIRMS THE FACT THAT FOWLER AND XXXX WERE DE FACTO DIRECTORS OF IMPERIAL AND CONTROLLERS OF THE WHOLE CAPITA OAK SET UP. HOWEVER, I REITERATE THAT FOWLER WAS CONTROLLING THE “ENGINE ROOM” AND XXXX WAS AT THE “SHARP END” I.E. PROMOTION AND DISTRIBUTION (AS HE HIMSELF ADMITTED TO ME).

XXXX told me he suggested to Fowler that Metis Law could deal with the conveyancing for the acquisition of store pods by CAPITA OAK. However, as shown above according to Fowler and Perkins it was XXXX’s decision to invest 100% of CAPITA OAK funds in Store First and to instruct Metis Law. IT MAY HAVE BEEN XXXX’S DECISION TO INVEST 100% OF CAPITA OAK FUNDS IN STORE FIRST AND TO INSTRUCT METIS LAW, BUT THIS DECISION WAS ACCEPTED BY FOWLER AND REMAINED UNQUESTIONED AND UNCHALLENGED (BY A PENSIONS LAWYER WHO CERTAINLY SHOULD HAVE KNOWN BETTER).

Paul Cooper of Metis Law told me that Metis Law were approached in October 2012 by XXXX to act for CAPITA OAK and acquire store pods on its behalf. XXXX subsequently approached Metis Law to also act for Henley to acquire store pods. COOPER TOLD ME THAT METIS LAW WERE INVITED TO TENDER AGAINST LARGER FIRMS. WHETHER THIS IS TRUE OR NOT, METIS LAW CLEARLY MADE NO ATTEMPT TO ESTABLISH WHAT THE INVESTMENT PRINCIPLES OF A PENSION SCHEME WERE SUPPOSED TO BE. HAD THEY DONE SO, THEY WOULD SURELY HAVE QUESTIONED THE WISDOM OF INVESTING 100% OF A PENSION SCHEME’S ASSETS IN STORE PODS.

Although Dunlop was the director of Imperial and trustee of CAPITA OAK, and nominally authorised all acquisitions of store pods, Cooper of Metis Law said that Dunlop shared information with XXXX. Cooper described XXXX as “shadow director” of Imperial and as “project manager” of the scheme as he gave day to day instructions and chased things up. He said that whilst Dunlop made the key decisions Metis Law considered that he did so on XXXX’s instructions. I SUBMIT THAT DUNLOP MADE NO DECISIONS BUT WAS ONLY ACTING ON INSTRUCTIONS – WHETHER FROM FOWLER OR XXXX. HE HAD CLEARLY BECOME NERVOUS ABOUT THE WHOLE SET UP EARLY ON, BUT CONTINUED NEVERTHELESS. IT IS NOT HARD TO CONCLUDE THAT DUNLOP – ALONG WITH ALL THE REST OF THE PUPPETS INVOLVED IN IMPERIAL/CAPITA OAK – WERE INTIMIDATED BY THE DE FACTO DIRECTORS AND MEEKLY DID AS THEY WERE TOLD.

XXXX told me that he did not agree with Cooper’s description of him as “project manager” and he did not agree that he instructed Dunlop. He said that he may have spoken to Dunlop but there was no need for him to instruct Dunlop. Although XXXX disputes Cooper’s description of him, Dunlop was paid by XXXX and he was accustomed to acting as XXXX’s nominee. In an email sent by XXXX to Fowler on 4.1.13 he states: “re the below, can you shed some light on this please? It was my understanding that after putting in my own director to Imperial (and paying him) and setting up a loan company and loan agreements etc., that the headline rate of fee was dropping to 2%”. THERE HAS BEEN MUCH HEATED DEBATE ON WHOCALLSME AS TO WHETHER IMPERIAL/CAPITA OAK WAS RUN BY THOSE “NORTH OR SOUTH OF THE BORDER”. DOWNS HAS TRIED TO CLAIM THAT THE “BAD GUYS” WERE THE NORTHERNERS WHILE THE “GOOD GUYS” WERE THE SOUTHERNERS. HE WAS CLEARLY REFERRING TO XXXX (NORTHERNER) AND FOWLER (SOUTHERNER). IN MY HUMBLE OPINION, THEY WERE BOTH AS BAD AS EACH OTHER. ALTHOUGH THEY EACH HAD DIFFERENT ROLES, FOWLER FACILITATED XXXX’S ACTIONS AND VICE VERSA.

On 5.2.13 Dunlop instructed Metis Law to settle, from the funds held in their Imperial Client a/c an invoice of the same date raised by Thurlstone for £100,557.58 in respect of management services in respect of CAPITA OAK. Dunlop told me he believed that XXXX was the person behind Thurlstone. DOWNS HAS DOGGEDLY REFUSED TO ANSWER QUESTIONS REGARDING THIS TRANSACTION AND, INDEED, I BELIEVE PART OF THE REASON WHY HE SO DESPERATELY WANTED TO SUPPRESS THE METIS LAW ACCOUNTS WAS THAT HE DID NOT WANT THIS THURLSTONE TRANSACTION TO BE EXPOSED. FOWLER WAS CLEARLY THE “CONTROLLING MIND” BEHIND THE CONTROL OF IMPERIAL AND THE BARCLAYS BANK ACCOUNT, AND IT IS INCONCEIVABLE THAT HE DID NOT KNOW OF THE THURLSTONE LOANS WHICH WERE PART OF THE CAPITA OAK “PACKAGE” (AND INDEED HAD ACKNOWLEDGED THIS IN AN EMAIL TO XXXX). WHETHER HE CONSCIOUSLY OR ACTIVELY PARTICIPATED IN THE INSTRUCTION TO PAY THURLSTONE FROM THE METIS LAW IMPERIAL CLIENT ACCOUNT, OR WHETHER HE ACQUIESCED TO THE PAYMENT IS IRRELEVANT. FOWLER KNEW THAT THE THURLSTONE LOANS WERE USED TO ENCOURAGE MEMBERS TO TRANSFER TO CAPITA OAK AND DOWNS HAS DESPERATELY TRIED TO CLAIM THERE WAS NO CONNECTION BETWEEN THE PENSION TRANSFERS AND THE THURLSTONE LOANS IN ORDER TO HIDE FOWLER’S ACTIVE INVOLVEMENT IN PENSION LIBERATION FRAUD.

Metis Law wrote to Chant on 5.2.15 expressing concern over “serious issues and concerns that have arisen from 2014 concerning Imperial’s purported management of CAPITA OAK”. Metis were instructed by Imperial on 21.10.12 having been introduced to Dunlop by XXXX. Metis understood Imperial were taking advice concerning their trustee function from specialist lawyers and that as such Metis’ role would be restricted to commercial property work purchasing store pods. BEARING IN MIND CHANT WAS APPOINTED AS DIRECTOR OF IMPERIAL IN OCTOBER 2014, I AM SOMEWHAT (BUT NOT ENTIRELY) SURPRISED THAT METIS DID NOT WRITE TO A DIRECTOR OF IMPERIAL “EXPRESSING CONCERN” UNTIL FEBRUARY 2015. THE “SPECIALIST” LAWYERS CONSULTED BY IMPERIAL (I.E. PERKINS AND FOWLER) WERE BARK & CO WHO PROUDLY ADVERTISE ON THEIR WEBSITE THAT THEY ACT FOR THIEVES, FRAUDSTERS, HACKERS, MURDERERS AND ASSORTED SCAMMERS. BARK & CO DO NOT APPEAR TO HAVE ANY PROFESSIONAL EXPERTISE IN PENSIONS.

Metis advised they were not involved in the negotiations between Imperial and Store First. Metis were advised that the purchase of store pods were pursuant to an investment strategy formulated by Imperial upon which it had taken its own independent advice. No mention of any such advice has been made to me during the course of my investigation. IN A RHETORICAL FASHION, I WONDER WHETHER METIS SOUGHT CONFIRMATION OF THE “INDEPENDENT ADVICE ON THE INVESTMENT STRATEGY”. THE ANSWER IS, OF COURSE, THAT THEY DID NOT AND CARED NOT.

Metis noted that no site inspection had been undertaken and that Imperial were acquiring assets without permitting Metis sight of any valuations “we were advised that Imperial had already procured RICS valuations and we should get on with the job”. METIS WERE DESPERATE FOR THE WORK. THEY MAY HAVE BEEN INSTRUCTED TO GET ON WITH THE JOB, BUT ANY CONSCIENTIOUS, RESPECTABLE AND RESPONSIBLE FIRM WOULD HAVE INSISTED ON SEEING THE ALLEGED RICS VALUATIONS BEFORE GOING AHEAD WITH THE PURCHASES.

Metis noted that “we have now come to understand, following subsequent events that a rent/income/return may have been due back to the scheme pursuant to Imperial’s acquisition of the store pods. None of the purchase contracts supplied by or agreed with Store First references any obligation on the part of Store First to pay a return due back to the scheme, albeit it is accepted that Store First have subsequently confirmed that such a return was owed and paid to a company based in Gibraltar known as Transeuro Worldwide Holdings Ltd.” METIS EXECUTED THE PURCHASE CONTRACTS AND HAD AN OBLIGATION TO DO THEIR OWN DUE DILIGENCE AS TO THE TERMS OF THE CONTRACTS. THE STORE FIRST DRAFT CONTRACTS WERE AT THE TIME OF PURCHASE IN THE PUBLIC DOMAIN, AND THE STORE FIRST WEBSITE LOUDLY AND PROUDLY PROCLAIMED THAT THERE WAS A TWO-YEAR 8% GUARANTEED RENTAL AS PART OF THE PURCHASE PACKAGE. I THEREFORE SEE NO EXCUSE FOR METIS HAVING FAILED TO ENSURE THIS WAS PART OF THE PURCHASE CONDITIONS.

Metis confirmed that Imperial was the legal owner of the store pods as they had been advised the scheme possessed “no legal personality”. WHEN A PERSON STUDIES LAW, ONE OF THE ASPECTS OF LAW IS “TRUST”. CAPITA OAK MAY HAVE HAD NO “LEGAL PERSONALITY” BUT IT HAD A TRUST DEED AND IT WOULD HAVE BEEN CLEAR (HAD METIS BOTHERED TO INSPECT THE TRUST DEED) THAT THE ASSETS PURCHASED BY IMPERIAL WERE IN TRUST TO THE CAPITA OAK PENSION SCHEME. SURELY, THIS SHOULD HAVE RAISED QUESTIONS AS TO THE WISDOM OF INVESTING A PENSION SCHEME’S ASSETS IN ONE SINGLE PROPERTY ASSET WHICH WAS ILLIQUID AND CONTRAVENED ALL THE LEGAL REQUIREMENTS OF A PENSION SCHEME?

Metis advised they had been instructed by Imperial to send letters before action to Store First in order to seek the payment of the return and the rent due to CAPITA OAK. THIS IS COMPLETELY UNTRUE. METIS TOOK THEIR OWN DECISION TO SEND A LETTER BEFORE ACTION TO CRAIG HOLLINGDRAKE, STORE FIRST’S SOLICITOR, WITHOUT INSTRUCTION FROM IMPERIAL AS PAYNE WAS DECLINING TO DO OR SAY ANYTHING AT THE TIME. METIS TOLD HOLLINGDRAKE THAT I, DURING MY SHORT TENURE (BEFORE BEING REMOVED BY PAYNE WITHIN FIVE MINUTES OF THE APPEARANCE OF MY DIRECTORSHIP ON THE COMPANIES HOUSE WEBSITE) HAD INSTRUCTED METIS TO ISSUE A LETTER BEFORE ACTION. HOWEVER, WHEN QUESTIONED BY HOLLINGDRAKE AS TO WHETHER I HAD ISSUED SUCH AN INSTRUCTION I HAD NO ALTERNATIVE THAN TO CONFIRM THAT I HAD NOT. THIS RESULTED IN A TERMINATION OF THE PREVIOUSLY COOPERATIVE RELATIONSHIP BETWEEN ME AND METIS LAW. BOTH WHITTAKER AND HOLLINGDRAKE HAD PREVIOUSLY ASSURED ME OF THEIR “EVERY COOPERATION” AND HOLLINGDRAKE HAD EVEN INFORMED ME THAT WHITTAKER WAS PREPARED TO FLY OUT TO SPAIN TO HELP SORT THINGS OUT. BUT AT THIS POINT, HOLLINGDRAKE TOLD ME THAT THEY WERE “PULLING UP THE DRAWBRIDGE”. Metis further advised they had attempted to enter into correspondence with TRANSEURO and that “we have subsequently received correspondence directly from TRANSEURO verifying that they have never received any return owed to the scheme.” Clearly this is at odds with the statements made by Store First. AT THE END OF THE DAY, IT WAS THE RESPONSIBILITY OF THE TRUSTEE TO ENSURE THE CONTRACTS WERE CORRECT FROM THE BEGINNING. HOWEVER, SINCE IT IS ESTABLISHED THAT THE “TRUSTEE” WAS A SERIES OF PUPPET DIRECTORS, AND THE DE FACTO DIRECTORS – XXXX XXXX AND ALAN FOWLER – WERE HIDING BEHIND A FENCE OF ANONYMITY, IT IS HARD TO SEE HOW IT COULD HAVE BEEN POSSIBLE FOR THE TRUSTEE TO DO A PROPER JOB AND TO ENSURE THAT METIS LAW ALSO DID A PROPER JOB.

Metis provided me on 18.2.15 with an email purportedly from Marthinus Joubert dated 9.12.14 as well as a letter from a law firm called Liburd Dash who were stated to be acting for TRANSEURO stating: “the only payments received by TRANSEURO were in respect of commissions in accordance with the agreement in place with Store First. We can also state the Company has never received any payments which would been due to the scheme” AGAIN, THIS MIGHT BE TRUE. IT DEPENDS HOW THE AGREEMENTS WERE SET UP. IT IS CLEAR THERE WERE TWO “FACTIONS”: XXXX RUNNING THE PROMOTION/DISTRIBUTION END; FOWLER RUNNING THE TRANSFER END; NEITHER OF THEM TAKING RESPONSIBILITY FOR OVERSEEING THE PUPPET DIRECTORS OR METIS LAW PROPERLY. HOWEVER, XXXX’S CLAIM THAT METIS LAW WERE “SENSIBLE CHARGERS” PROBABLY MEANS IT WAS CONSIDERED THAT METIS WERE A “CHEAP AND CHEERFUL” OUTFIT WHO WOULDN’T LOOK TOO CLOSELY AT THE PURCHASE CONTRACTS OR ASK TOO MANY AWKWARD QUESTIONS.

I am also aware that similar concerns to those pursued by Metis have surfaced elsewhere, such as on the whocallsme website and in media coverage of the matter and that a sum of £1.6m has commonly been mentioned in respect of the returns payable by Store First on sums invested via CAPITA OAK. When I spoke to Whittaker on 26.1.15 he stated all sums representing guaranteed returns on monies invested by both CAPITA OAK and Henley has been paid and that they had been paid to TRANSEURO on the basis of the terms of sale negotiated with Store First by Talbot and Chapman-Clark. AGAIN, THIS IS PROBABLY TRUE. HOLLINGDRAKE TOLD ME THAT THE RENT WAS (PROPERLY) PAID TO THOSE WHO WERE RUNNING THE SCHEME IN ACCORDANCE WITH THE CONTRACT. IT WAS UP TO THE “TRUSTEE” TO ENSURE THAT THE PROMISES MADE TO THE MEMBERS WERE HONOURED, AND TO ENSURE THAT WHEN THE PODS WERE PURCHASED THE 8% X 2 YEARS WAS WRITTEN INTO THE CONTRACT. FOWLER AND XXXX WERE TOO BUSY HIDING BEHIND PUPPETS TO NOTICE OR CARE, AND METIS LAW WERE TOO NAÏVE AND INEXPERIENCED TO ASK QUESTIONS.

However, on 9.3.15 I was contacted by email by Ruth Almond, director of Store First, who advised me that, contrary to what had earlier been said by Whittaker, payment of the guaranteed returns in respect of Henley had been paid to a company by the name of Graylaw International which was owned by the same people as TRANSEURO. Attached to the email was an invoice from Graylaw dated 20.9.13 addressed to Store First in respect of “commission due” on the sum of £3.5m invested by Henley which appears to represent virtually the entire sum invested in store pods. Whilst the printed sum claimed is difficult to read from the scanned copy, the invoice has been annotated to indicate it was settled by way of a payment of £1,711.850, representing a little under 49% of the sum invested. Graylaw is a company also owned by the same directors as Transeuro”. I note that the Wilmington address is also used by Quantum Global Associates Capital LLC which has as its majority beneficial owner the same as that of TRANSEURO. PERHAPS A COINCIDENCE THAT A SUBSEQUENT SCAM OPERATED BY STEPHEN WARD (AND OBVIOUSLY ASSISTED BY FOWLER) WAS CALLED “LONDON QUANTUM”?

TRANSEURO is described as the agent, that its Gibraltar registered office is cited and that the following clause is included: “with effect from the date of this agreement the agent is to become the non-exclusive selling agent of Store First, with rights to sell the product” and that TRANSEURO was entitled to receive commission at the rate of 30% of the total purchase price of the products sold. The total value of sales transacted by TRANSEURO is £97,166,914

TRANSEURO has raised invoices in respect of sales made via CAPITA OAK totaling £5,164,500 and has received 16% of that sum (£826,320) which I believe should properly have gone back into the scheme. CAN YOU PLEASE CLARIFY THIS? THE TOTAL PAID BY IMPERIAL/CAPITA OAK FOR STORE PODS WAS £9.8M SO WHY DO TRANSEURO’S INVOICES ONLY TOTAL £5.1M? THIS DOESN’T MAKE SENSE.

The service agreement between Imperial and TKE details the services to be provided by TKE as follows:

To deduct specified amounts on entry to membership from transfer payments to the scheme and to apply the same as directed by Imperial. Imperial directs that the amount to be deducted on transfer shall be 5%; 3% of the amount deducted shall be retained by TKE and 2% shall be paid to Nationwide Benefit Consultants (XXXX).

To arrange/provide banking and related arrangements for the scheme

To arrange or assist with the keeping of financial records

To make payments from the scheme as directed by Imperial

To provide/arrange administrative services specified by Imperial

To distribute documents/information as directed by Imperial

To engage other service providers where directed by Imperial

To provide additional services not specified above as directed by Imperial