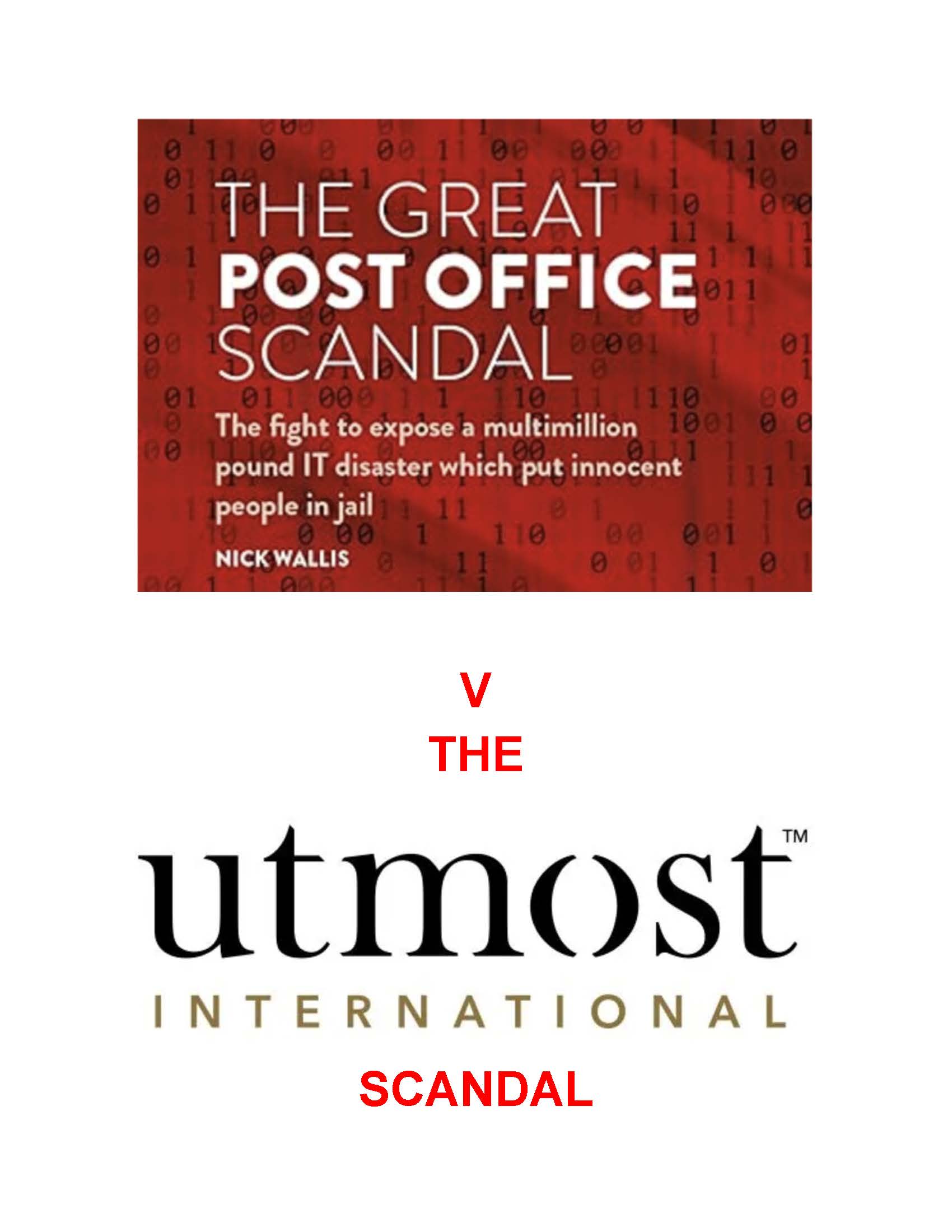

The Post Office scandal is routinely referred to as being the worst betrayal of justice in British history. It is hard to argue that there could be anything worse than what the liars and fraudsters at Post Office Limited and Fujitsu (and their various lawyers) did to hundreds of innocent sub postmasters. But the Life Offices – including Utmost International – and many of the brokers with whom they have terms of business – certainly come a close second.

The Post Office scam was led by Paula Vennells – an ordained Anglican Minister. She was CEO from 2012 to 2019. It is hard to figure out which bit of the Ten Commandments she omitted to read, especially “Thou shalt not steal” and “Thou shalt not bear false witness”.

Listening to the testimonies in the Post Office Horizon Enquiry led by Sir Wyn Williams, it is clear there is a sub-group of human beings who have little right to call themselves “human”. This includes the bosses at Post Office Limited and Fujitsu (as well as their various lawyers) who knowingly sent hundreds of innocent victims to prison (including a pregnant woman). Having extorted money from their victims to repay the “shortages” falsely reported by the Horizon software, the Post Office bosses then paid themselves whopping bonuses.

There is a great deal of information, background and commentary on the Post Office scandal – including Nick Wallis’ excellent book “The Great Post Office Cover Up“; Computer Weekly’s excellent, comprehensive coverage; the British government’s own report; and even a television docudrama which reconstructed the appalling events in Mr. Bates vs The Post Office.

The Post Office/Fujitsu scandal was the subject of a public enquiry which exposed the appalling events and profound negligence and criminality by Post Office and Fujitsu bosses and staff. Thanks to the exceptional diligence of the barristers who represented the victims and expertly dragged the truths, half truths and lies out of the perpetrators, the public can finally see the truth.

What remains to be seen, however, is what compensation the victims of the Post Office and Fujitsu fraud will receive. Hundreds of sub postmasters were wrongly convicted of false accounting and theft, and in numerous cases made to pay back the money they had never stolen, and often sent to prison. Hundreds of lives were ruined and some victims committed suicide because of the shame of being viewed in their close-knit communities as guilty of theft and false accounting. Taking into account the wider interests of the families of the victims, however, this atrocity has ruined thousands of lives.

The Post Office has, reportedly, spent hundreds of millions on legal fees – to defend its position, deny responsibility and culpability, and delay paying out compensation to its victims. Figures vary, but it is clear the Post Office has spent way more on its own fees than it would have done had it simply paid fair compensation to its victims.

While the Post Office/Fujitsu enquiry is now complete, the civil litigation against the Life Offices is currently going through the Isle of Man courts. And, like the Post Office, the Life Offices are throwing millions of pounds at their lawyers to try to evade paying their victims the redress they deserve.

There are numerous similarities and differences between the Post Office scandal and the Life Office scandal (Utmost International, SEB, RL360, Investors Trust etc). The bosses at the Post Office and Fujitsu had a limited, finite pool of victims in the UK – whereas the Life Offices had – and still have – an unlimited pool of victims globally. Plus, the Life Offices did not falsely prosecute their victims or send them to prison. But they still ruined their lives nonetheless.

Let’s compare some of the tragic similarities between both scandals:

| The Post Office was headed up by an ordained Anglican minister (Paul Vennells). She should have known better. | Quilter (Old Mutual) (leading player in the Life Office scandal) was headed up by a former Isle of Man regulator (Peter Kenny). He should have known better. |

| The Post Office knew that Fujitsu’s “Horizon” accounting software was full of bugs and could not be relied upon. Horizon would inevitably report false statistics and financials. | The Life Offices knew many assets offered on their investment platforms were high-risk, high-commission and bound to fail. These investments would inevitably cause severe losses. |

| Fujitsu is a key “strategic supplier” to the UK government, making £100m a year from this work, and has won 150 new contracts worth £2.04bn since the 2019 court ruling that Fujitsu’s Horizon IT system caused accounting errors that were blamed on the sub-postmasters. | The Life Offices (Utmost, RL360, Hansard etc) are still to this day used extensively by virtually all offshore brokers and QROPS providers. Posting eye-watering profits and AUM, the Life Offices continue to flourish but offer to pay no compensation to their victims. |

| Fujitsu’s clients for these lucrative contracts include the Home Office, HMRC, the Foreign Office, the MoD, and the DWP. Plus the £2.4bn lifetime contract Fujitsu still has with the Post Office for the Horizon system. | Life Offices continue to provide unnecessary insurance bonds for virtually the entire offshore financial services market. These products serve only to pay undisclosed commissions to the brokers and provide no benefit to the investors. |

| Fujitsu and The Post Office have jointly caused millions of pounds’ worth of financial losses and damage to hundreds of sub postmasters. Still only pitifully small amounts of compensation have been paid to the victims. | Life Offices have caused many hundreds of millions of pounds’ worth of financial losses to thousands of investors. Still no compensation has been paid or received. |

| The Post Office continues to pay a herd of lawyers millions of pounds to fight against paying just compensation to the sub postmasters who were victims of this scandalous crisis. | Life Offices Utmost International and Friends Provident are paying lawyers in the IoM to fight against paying compensation to the victims of investment fraud and undisclosed commissions. |

WHICH IS WORSE? THE POST OFFICE SCANDAL OR THE LIFE OFFICE SCANDAL?

It really is hard to say. In both cases, thousands of people’s lives have been ruined. Marriages have been destroyed, homes and businesses lost and unnecessary deaths have occurred. The Post Office (and Fujitsu) had a limited and finite pool of victims (only the sub postmasters and their families in the UK) – whereas the Life Offices have an infinite pool of victims across the globe. And this scandal continues to this very day – entirely unsanctioned.

Save for the outstanding justice and compensation due to the sub postmasters, and the impending criminal proceedings against those responsible at The Post Office and Fujitsu (and possibly some of the lawyers who helped cover up their fraud), this matter is over bar the shouting. By contrast, the Life Offices are continuing full blast with the same business model which has destroyed countless lives, families, marriages and life savings.

The Post Office/Fujitsu victims will still have to wait many years for their rightful compensation – while the lawyers continue to get rich and the government prevaricates feebly. There are faint signs that Paula Vennells and Nick Read may yet serve time behind bars. But at least something is being done, and there is a legal process in place. However, the Isle of Man and Irish governments and regulators have shown zero interest in the fraud committed and facilitated by the Life Offices.