When we buy certain products, they have a warning on them. Cigarette packets, for instance, state that smoking is bad for your health. The wrappers show hideous images of what might happen to you if you use tobacco.

However, when it comes to investments, the ‘advisers’ selling dangerous investments are able to disguise the risks and costs. Offshore, there seems to be no effective code of conduct, or regulation as to what they must disclose and what they can conceal.

When selling their investments, these firms are really good at omitting details of the full charges that will apply – not only initially – but on an ongoing annual basis as well. These hidden charges put your investment in danger.

The FCA has stated:

“In one case it found an asset manager had omitted a 4 per cent a year transaction cost from the UCITS Key Investor Information Document (KIID).”

In so many pension scams, we hear that the victims were sold a ‘free pension review’; they were not told about the transfer costs; that they were not told about annual fees either. In many cases, the transfer costs and fees work out to be considerably higher than if they had paid a proper fee for the review in the first place. These hidden costs put a huge strain on the fund and sometimes victims can lose up to 25% of their fund to hidden charges.

What worries us most is the lack of regulatory concern or control in respect of expensive and risky investment products. You can’t buy cigarettes without a stern health warning. The same goes for alcohol: bottles and cans clearly state how many units are in the container, and how many units men and women can safely drink per day. They also state that alcohol should not be consumed by pregnant women.

Alcohol companies manage to fit all this info about the dangers of drinking on a tiny label. And this poses the essential question as to why financial advisory firms are able to sell risky investments again and again – omitting clear warnings about the dangerous aspects of them.

“The FCA reserved its fiercest criticism for asset managers, saying it found instances where asset manager fact sheets or websites did not mention costs. When they did, they often gave the ongoing charge figure, which omitted transaction costs, performance fees and borrowing charges which are shown in the Key Information Document (KID). In one example, total charges in the PRIIPs KID equated to around 3 per cent per annum – but the only costs given in the fact sheet was the 1.2 per cent annual management charge (AMC).”

This is not news to us at Pension Life. It is something we have been writing about for sometime – and we have a great deal of evidence that hidden, excessive charges are a terrible blight on the face of financial services internationally. It is indeed excellent news that the FCA has finally highlighted the dangers of such hidden charges, but now we need to make sure these dangers are highlighted to the public. CLEARLY AND VISIBLY.

You can’t buy a gun without going to a registered shop and having a licence. (Although, I guess on the black market you can). If you buy a gun on the black market, it is going to be ‘hot’. The person you buy it from is going to be dodgy and it certainly won’t come with the correct paperwork.

So if you are a normal, law-abiding citizen (and cautious investor), you would want a legitimate investment which fits your risk profile – and full paperwork disclosing ALL the charges. Make sure you pick the right adviser who will give you evidence of all these essential details.

Dodgy advisers are still getting away with selling ‘hot’ investments: funds that are clearly toxic and dangerous to your pension fund. These advisers manage to do this very successfully by wrapping them in a fluffy cover and selling them with an array of unrealistic promises of high returns and alleged capital protection to reel the victims in.

When considering a pension transfer, we urge you to familiarise yourself with our ten standards. Your adviser ought to adhere to these standards anyway – and if he doesn’t then walk away. Number eight covers what we have talked about in this blog: CHARGES.

Your adviser MUST GIVE YOU: Full disclosure of fees, charges and commissions on all products and services in writing, before you commit. So before you sign anything regarding a pension transfer and subsequent investment, please ensure you know exactly what charges will be applied to your fund: before, during AND after. It is also imperative to know if there is a lock-in period and early exit penalty and to make sure you are comfortable with that.

Excessive and concealed fees can ruin a once healthy and happy pension fund – just like smoking can ruin your lungs and drinking can ruin your liver. Hidden charges can put your funds in danger and ruin your retirement savings beyond repair.

Here is a list of our ten standards.

STANDARDS ACCREDITATION CHECKLIST FOR FINANCIAL ADVISERS:

Proof of regulation for all services provided by the firm and individual advisers in the jurisdiction(s) where advice is given and the clients are based.

Verifiable evidence of appropriate, registered qualifications and CPD for all advisers. (Where there are insufficient qualifications, there must be clear evidence of plans and preparation to achieve required goals within a reasonable, stated time frame).

Professional Indemnity Insurance

Details of how fact finds are carried out, how clients’ risk profiles are determined and adhered to.

Details of the firm’s compliance procedures – assuring clients of the highest possible standards and assurance that risk profiles are always accurately and faithfully respected.

Clear and consistent explanation and justification of the use of insurance bonds for investments.

Unambiguous policy on structured notes, UCIS funds, in-house funds, non-standard assets and any ongoing commission-paying investments. Report of all investment recommendations for all clients and evidence as to how these match individual risk profiles.

Disclosure of fees, charges and commissions on all products and services at time of sale, in writing, before clients commit.

Account of how clients are updated on fund/portfolio performance.

Public evidence of complaints made, rejected or upheld and redress paid.

For more in depth explanation check out our other blog on the ten standards:

Every year we are seeing an increase in the number of victims falling for pension and investment scams. Despite warnings in the public domain and a huge array of information about how to avoid falling victim to a scam, it seems the scammers are so skilled at their sales techniques, that even the cleverest of people can fall for their slick pitches. Often the scammers use cold-calling techniques to initiate these pitches: using emails, texts, mail shots and the good ol’ phone.

We finally saw the introduction of the cold calling ban come into place in January 2019, with huge fines being threatened to firms using these techniques to promote pension sales. We have already written about the firms who have changed their scripts to escape the fines: Cadde Wealth Management is one of these firms. On top of this, we now find that the cold-calling ban has just encouraged the scammers to divert their efforts to British expats.

BBC4 You and Yours recently discussed how the cold-calling ban in the UK has seen a change in the scammers’ behaviour. Unfortunately, this is not a change for the better. As the ban only applies to the UK, scammers are targeting expats instead. This means UK pension holders are still the main target for pension scammers and are at greater risk than ever.

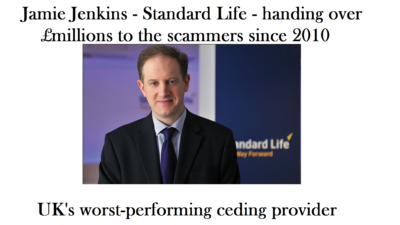

Interviewed in the programme, Jamie Jenkins says he has noticed this change. He is Head of Global Saving Policy at Standard Life. He states in the report, “In recent months we have known that the cold-calling ban is coming in and criminals know that too. So we have seen a switch from cold calls originating in the UK to UK customers, to overseas calls to expat customers living abroad.”

Ironically, Standard Life has been one of the worst performers in terms of ceding pension providers who have recklessly and negligently handed over millions of pounds’ worth of pensions to the scammers. Completely ignoring the Pensions Regulator’s warnings in 2010, they shoveled £millions across to pension scams such as Ark, Capita Oak, Westminster, Continental Wealth Management, Global Fiduciary Services and many other QROPS scams.

Here at Pension Life, we know that expats are not just a new target of cold callers – many expats have already fallen victim to horrific pension scams, like those who lost large chunks of their pension funds to CWM. Continental Wealth Management fraudsters like Darren Kirby, cold-called victims, then followed through with repeat house calls and persuaded around 1,000 UK pension holders to transfer out of safe DB pensions into QROPS and illegally-sold life insurance bonds (such as OMI, Generali, SEB, RL360). With promises of high returns, a lump sum in cash and greater freedoms, many professional and well-educated people fell for the scam.

Here is our cartoon video reconstruction of how the Continental Wealth Management scam worked:

The BBC programme also talks to a Continental Wealth Management victim, Rebecca Cooke, who lost £75,000 after transferring out of an NHS pension and other secure investments.

“We were approached in 2012/13 by a company based in Spain (Continental Wealth Management) who were offering us advice about moving our private pension from the UK into another investment scheme based in the EU. We went with them, but it became blatantly obvious that we had suffered catastrophic losses in our pension and chased them up about what was happening. They had actually invested our funds badly and put them in high-risk rather in low to medium risk funds. Consequently, we had lost that amount of money (£75,000).”

She said she feels stupid for falling for the scam, but she is not alone in believing the shiny sales pitch of these scamming criminals.

It seems the only way to escape the scammers – anywhere in the world – is not to fall for their lies. But the challenge is to know what is true and what is false. And that isn’t easy – the scammers are very clever and can adapt quickly to invalidate public warnings and even use them to their advantage. In addition to the scammers, there are now offshore claims management companies circling like vultures and conning people into believing that complaints against offshore firms can be upheld by UK-based ombudsmen – and that claims can be made against the FSCS (Financial Services Compensation Scheme) in respect of Maltese trustees.

Another victim of Berkeley Burke SIPPS investments into Store First storage pods has come forward. 55-year-old factory worker Robert McCarthy, of Ebbw Vale, said he has lost more than £30,000 through a Self-Invested Personal Pension (SIPP). He was duped into the transfer and investment by unregulated firm Jackson Francis which was liquidated in 2014. His investment may or may not be worthless – depending on whether Store First is wound up later in 2019.

Robert McCarthy – who is one of 500 Store First investors who used Berkeley Burke as their SIPP provider – made a serious complaint against Berkeley Burke – and spoke to BBC News on the matter.

McCarthy said:

“Basically I’ve lost my private pension. Thirteen years of hard work, they’ve taken it, it’s gone.

I’ll never trust anyone again. And I can’t believe that they can get away with what they’ve done.”

The BBC has reported Store First as saying that: “In McCarthy’s case, Berkeley Burke failed to instruct Store First on how to manage the pods they purchased as part of a SIPPS. This means that the store pods have stood empty since their purchase. With returns based on rent paid for using the pods purchased, no returns have been made on these empty pods.”

This scam follows the same path as so many other scams we see: an unregulated advisory firm, Liverpool-based company Jackson Francis, introduced the victims to Berkely Burke and the Store First investment. (Jackson Francis was wound up in 2014). With promises of the investment being ‘the next best thing’ and also guaranteed high returns, 500 people signed their pensions over to the SIPPS provider Berkeley Burke.

Berkeley Burke then invested the SIPPS into the store pods, but failed to give permission for Store First to rent the pods out on behalf of the investors – meaning they stood empty. Store First said they were never contracted to manage, advertise or let the storage pods. That responsibility, they say, lies with the pension trustee, Berkeley Burke.

This is not the first time Berkeley Burke have been accused of negligence. In the High Court last October, Berkeley Burke was found to have failed to show due diligence in vetting unregulated investments for another client. The company are currently seeking to appeal against the decision. But with a further 14 individuals, based in Wales alone, making complaints against them, there is definitely no smoke without fire.

Whilst Capita Oak tuned out to be a scam (currently under investigation by the Serious Fraud Office) and victims have lost huge chunks of their pensions, the initial presentation they were given made the scheme look 100% genuine.

I spend a lot of time sharing our blogs over Facebook into different groups, trying to get the message across about pension scams. Interestingly, many of my posts are met with negative comments.

Last week in a comment on an expat forum, I was told that my blog about expats being targeted by scammers was “irrelevant”. I have also had comments like: “I would never fall for a scam.” However, there is clear evidence that falling for a scam doesn´t make you stupid or naive – especially when the scammers are so good at disguising their sham schemes as genuine investments.

Therefore, when it comes to the crunch, it is incredibly easy to fall for a pension scam – especially when it is registered by HMRC and promoted by a qualified financial adviser. It is hard to tell the difference between the good guys and the bad guys (who are so good at clever disguises). Pension scam victims include airline pilots, doctors and nurses, teachers, scientists, bankers and even a solicitor or two. Anyone can fall for a cleverly-sold scam – and they frequently do.

Toby Whittaker, owner of Store First, as you can see from his Twitter page, is still promoting Group First and Store First as going concerns. He is also fighting the winding-up petition by the Insolvency Service against Store First.

Despite the fact that the Capita Oak scam now lies in the hands of Dalriada Trustees (appointed by the Pensions Regulator) and the ongoing petition to have Store First wound up (purportedly in the “public interest”), Toby Whittaker still stands proud and says he had no idea that his company was being used as part of a scam.

No one knows where the money went, but it certainly didn´t go to the victims of this scam. We can bet it lined the pockets of the scamming salesmen who incorrectly invested over 1,000 victims’ pensions into Store First.

If the UK government succeeds in its petition to wind Store First up, the hundreds of victims will lose all the funds in their pensions.

By far the best US crime thriller series (IMHO) on Netflix has got to be Blacklist. Utterly mesmerising is the star Raymond Reddington (played by the superb James Spader). Reddington manages to be simultaneously as camp as a row of tents, and macho as the All Blacks.

The rest of the cast – both cops and robbers – are all excellent with intriguing sub-plots, endearing romances and lots of buttock-clenching suspense as the FBI race against time to catch the bad guys, recover the sniffing/folding stuff and save the victims from torture and painful deaths.

So inspired was I by taking up Blacklist binge-watching, that I decided to write an episode to submit to NBC (just in case the writers run out of ideas). My plot was hatched because every Blacklist episode contains all the ingredients that we need to tackle pension scams: the minute the crime (or intended crime) is identified, the FBI Special Agents swing into action, and SWAT teams are warmed up; the criminals’ mobiles are tracked and their computers hacked.

By the time I’ve cracked open the Snickers, Special Agents Wrestler and Mossad are on the scene and closing in fast on the bad guys. As I’m warming up my cocoa, the contraband has been uncovered; the bombs have been defused (with two seconds to spare); the bad guys are all either full of holes or in handcuffs; the full details of the dastardly criminal plot are laid bare. Most important, the lost $millions are recovered in full, and the valiant Red Reddington flies off into the sunset in his private jet with his trusty Dembe clucking at him for taking too many risks.

So here’s my humble attempt at the script for a Blacklist episode “The Pension Scam (No 69)” – script:

Arch pension criminal (and mastermind of the Capita Oak and Henley cases) XXXX XXXX – dressed in bright purple (to offset his flaming red hair) and driving a black Ferrari – struts into the offices of various QROPS trustees around the Med and meets cheery Irishman Justin Caffrey of Harbour Pensions. XXXX tells Caffrey of his plot to make millions out of scamming hundreds (or preferably thousands) of victims out of their pensions. His plan is to con hundreds of UK residents into transferring their pensions into a QROPS. And then (and this is the clever bit) XXXX, who is acting as the victims’ financial adviser, invests all their money in his own fund: the Trafalgar Multi-Asset Fund.

Being a particularly canny Irishman, Caffrey sees straight through XXXX’s dastardly plan and sends him and his (borrowed) Ferrari packing. Caffrey clocks XXXX as an outright spiv straight away. Caffrey is, anyway, already up to his ears in Phillip Nunn’s Blackmore Global investment scam, promoted by vile David Vilka, so he really can’t handle more than one scam at a time (being male, he can’t multi-task).

Way too thick-skinned, determined and greedy to be discouraged, XXXX heads across the Mediterranean to Gibraltar and the offices of STM Fidecs. There he meets CEO Alan Kentish who listens to XXXX’s offering with keen interest. Already under investigation for “tax irregularities”, Kentish is no stranger to “bending the rules” and is keen to learn more about how XXXX’s scam is going to work – and, of course, what is in it for Kentish himself.

XXXX explains that he has found an “umbrella” fund called the Nascent Fund run by Custom House Global Fund Services and a handsome but menacing-looking chap called Richard Reinert. This outwardly respectable-looking outfit allows wannabee fund “managers” (such as XXXX) to set up their own investment funds in the dodgy jurisdiction of the Cayman Islands – far from the eagle eye of the FCA.

Kentish is eager to know how much money can be made out of this plot. XXXX explains that 46% was earned out of his Capita Oak and Henley scams and that he hopes to make at least as much out of this one. With Kentish’s “help” (nudge nudge, wink wink). Of course, the proceeds could be split and plenty of brown envelopes used to disguise the handing over of the proceeds.

Things get off to a cracking start, with XXXX’s two trusted assistants: Tom Biggar and Paul Garner. But cracks start to appear early on. The success of the mission depends on the highest-risk assets being purchased with the funds – as these pay the highest “commissions”. But Biggar is a bad guy with a bit of a conscience, and he insists that some proper, prudent investments should also be made. This, of course, impacts on XXXX’s profits, so pretty soon Biggar “disappears” – never to be heard of again. Garner is seriously rattled and doesn’t want to end up the same way, so he heads off to work for the Gibraltar regulator – where he knows he’ll be safe as houses, as they’ll never take an interest in this crime. After all, STM Fidecs is one of the biggest employers in Gibraltar (after Betfred, Stan James, Paddy Power, William Hill, Bet 365 and 888 Holdings) – so there’s no risk of any of the perps doing porridge.

XXXX is now free to invest the whole fund (now well over £20 million) in whatever he pleases. So he sticks most of it in the German Dolphin (derelict property loan notes) Fund and cleans up. Trouble is, Richard Reinert of Custom House starts to get suspicious and starts sniffing around – after the worrying sudden disappearances of Biggar and Garner. He lifts the skirts of XXXX’s Trafalgar scam, and finds something rather more sinister than skid marks.

The FBI are a bit busy that day (yet another Blacklist case) so the SFO swings into action. XXXX is arrested. His office searched. The Gibraltar FSC twitches because XXXX’s third in command, Garner, is now working for them, so they turn a blind eye. Avoiding embarrassment, they get friendly local book cookers Deloittes to pop in to inspect STM Fidecs’ books. When Deloittes find out what a load of crap the STM QROPS is filled with, they wag their fingers sternly. Kentish is thoroughly upset (so much so, that he almost – but not quite – passes the fags round).

Now that the Trafalgar Multi-Asset Fund has been suspended – thanks to the hero of the hour: Reinert – Kentish decides to buy Caffrey’s QROPS firm, Harbour (which is full of Phillip Nunn’s Blackmore Global investment scam). Caffrey swans off into the sunset with £1 million burning a hole in his pocket, quietly humming “Oh Danny Boy”.

In the end, the handsome Reinert turns out to be a good guy after all, and gets some of the victims’ money back. (But only just enough to pay the liquidators’ fees!)

I submitted my carefully-typed script to NBC and waited with bated breath. A couple of weeks later their response arrived:

“Dear Miss Brooks, thank you for submitting your script for Blacklist episode “The Pension Scam (No 69)”. We have read your work with interest (and fell about laughing), but we do not feel it would be suitable for our series. Unfortunately, the plot is too far fetched and we do not consider that our viewers would find the story-line plausible. This sort of thing simply doesn’t happen in real life. However, we wish you all the best with your future writing efforts – but just suggest you try to stick to more believable plots.”

Sadly, of course, it was real life. As more than 400 victims will attest. So no more script-writing for me. I will stick to blogs in the future.

Scammers who act as financial advisers and operate pension scams, don’t wear a badge to identify themselves – nor do they pay any redress for the devastation they cause. Oh no, of course they don’t! The scammers dress in snazzy suits, drive go-faster cars, sport posh briefcases and speak with a silky sales tune floating out of their mouths. All this lulls victims into a false sense of security. Promises of guaranteed high returns and capital protection, as well as tax efficiency – and then… POOF! – there goes your whole life savings.

This poem was passed over to us by a twitter friend. We think it wonderfully sums up the way scammers work:

Poem

Above the calming waves, you spot a dorsal fin,

Is it that greedy shark who’s gonna take you in?

So you dip your toes to test and out pops friendly Flipper,

He’s so adorable but…

did you know his snout can also be a killer?

You listen to his clicking sounds that dull out your senses,

You write those cheques then wish you hadn’t been so careless,

As you wave goodbye to Flipper, you feel like all those lemmings,

The wistful trail of your pension and POOF!

there goes your whole life savings.

Don’t fall for the silky-voiced salesman´s tune. Follow the guidance in our ten standards to safeguard your pension from the scammers.

Ten standards for a financial adviser

1 – The firm that a trustworthy financial adviser works for will have the correct licences to advise you on your pension. It will be fully licensed (regulated) for both insurance and investment, and the adviser will not hesitate to give you proof of this.

2 – A trustworthy financial adviser will be fully qualified to the correct level and be happy to show you their certificates. A certified adviser will work to a correct code (not a scammer’s code) and never use silky sales techniques to get you to sign over your life savings.

3 – A trustworthy firm and their fully qualified advisers will have all the correct paperwork and this includes professional indemnity insurance.

4 – A financial adviser who wants to help your pension grow steadily – with safe and suitable investments – will never throw sky-high promises of super fat returns at you. Scammers love this too-good-to-be-true sales technique. Remember, if it sounds too good to be true it probably is! And it is a sign that they are working for commission benefits that will line their pockets and probably not suit your risk profile. A pension risk profile is usually a low-medium risk which will grow steadily. High commission investments are often high risk and also often fail – causing devastating losses.

5 – A financial adviser that works for your benefit and that alone will never expose you to a hard sales pitch. Repeat phone calls and pressure to sign – “for fear of missing out” – are often a tell-tale sign they are working for commission. Scam advisers – working for fat commissions at the expense of customer satisfaction – will rarely respect your risk profile. They will rarely observe any compliance ethics either.

6 – A financial adviser that you can trust should NEVER up-sell you with ‘extra’ investments like insurance bonds. Often these are a double wrapper that will make a scammer extra commissions. These ‘extra’ investments will often simply drain your pension pot, not contribute to it.

8 – An adviser you can trust will be happy to disclose ALL fees, charges and commissions, in writing: no ifs or buts. If the adviser you are using skims round this VERY IMPORTANT information, he probably isn’t a trustworthy adviser. Hidden charges are often how scammers line their pockets and destroy your pension fund.

9 – A trustworthy firm and adviser will ensure you have full access to accounts of how you are updated on your pension fund and portfolio performance. This should be outlined to you at the time of transfer, usually a quarterly statement AND a yearly review. If your financial adviser cannot offer this information readily – just walk away.

10 – A firm you can trust will have all their company history readily available. This should include public evidence of complaints made, rejected or upheld and redress paid.

A firm with advisers who are unwilling to answer all of the questions you ask them is clearly a firm to be avoided.

If the firm you choose and the adviser they assign to you cannot attain all ten of the standards listed – find one that can.

Don’t risk your life savings to the tune of a silky-voiced salesman. He may look the part, but appearances can so easily fool.

Scam victims will tell you they wish they had ensured their pension transfer had adhered to all ten of these standards.

Another day, another voluntary ban taken by pension scammers, this time by those involved in the Henley Retirement Benefits and Capita Oak Pension Schemes. It seems there is still no justice for the victims of these financial crimes and there are no consequences for the directors of Transeuro Worldwide Holdings nor Imperial Trustee Services.

These scammers take a voluntary slap on the wrist and are still free to move on to their next venture.

“A ban from being involved in pension transfers is not a strong enough deterrent for other pension scammers. We need to see tougher penalties such as hefty monetary fines to make it clear that this behaviour will not be tolerated.”

We couldn´t agree more, as stated in a previous article, “The wheels of the law don´t seem to turn at all“, where we highlighted that a mere ban is pointless. Also, the time frame it took for this ban to be enforced is laughable.

Capita Oak was registered by HMRC on 23.7.2012 (PSTR 00785484RM) by Stephen Ward of Premier Pension Transfers of 31 Memorial Road, Worsley and Premier Pension Solutions of Moraira, Spain.

Capita Oak was wound up in the High Court in 2015.

2018 voluntary bans taken.

So, it took all this time for (some, NOT ALL) of the scammers involved in the Henley Retirement Benefits and Capita Oak Pension Schemes, to just get a ban. They have not been prosecuted and some of the main players are still at large. None of them have been ordered to pay back the funds they stole in larger than normal commissions – funds which were originally promised to the victims.

As always, there is a string of firms connected through this case, so bear with me whilst I outline the long list:

The directors connected with Transeuro Worldwide Holdings were the focus of this investigation

Transeuro helped fund three introducer firms: Sycamore Crown, Nunn McCreesh and Jackson Francis

Victims were transferred into SIPPS and pension schemes operated by Omni and Imperial Trustees

More than £100m was paid into SIPPS, more than £10m into Capita Oak Pension Scheme and more than £8m to Henley Retirement Benefit Scheme

The funds were then invested in assets which paid the scammers 46% in commission

Victims of Henley Retirement Benefit Scheme and Capita Oak Pension Scheme were cold called and given the hard sell, with promises of high returns. The usual spiel which – if you are considering a pension transfer – should not be believed.

Bans were given to:

Sycamore Crown director Stuart Greehan (also known as Stuart Chapman-Clarke) agreed to a nine-year voluntary ban

Karl Dunlop, director of Imperial Trustee Services, agreed to voluntary bans of nine years

Ian Dunsford, director of Omni Trustees agreed to a voluntary ban of seven years

Stephen Talbot accepted a nine-year disqualification undertaking for failing to explain what happened to millions pounds’ worth of assets

The words ¨accept¨ and ¨agreed¨ are used here, which gives the impression they all sat down to a nice lunch and “agreed” that they may have made a mistake and therefore “accepted” their bans! These people are financial criminals who left many lives ruined. The victims – many of which were already in financial hardship – now have no pension fund to look forward to.

The Serious Fraud office opened their investigations into the Capita Oak Pension and Henley Retirement Benefits Schemes, as well as Westminster and XXXX’s Trafalgar Multi-Asset Fund, back in May 2017. It is, however, anyone´s guess when this case might be pushed through the high court.

In many pension scam cases, we find victims telling us that they were not informed about the hidden charges that were applied to their fund. This is why it is essential to warn the public about the hidden dangers of charges that ruin your pension investments. These charges often take a huge chunk out of the fund before and during its new investments. Scammers lie about these charges, and victims never find out about them until it is too late.

The investments the scammers use are often high-risk and totally unsuitable for a pension fund. Pensions should be invested in diverse, low-to-medium risk assets which are prudent and liquid. And pensions don’t need an insurance wrapper at all, especially since the wrapper pays a whopping 8% commission to the scammers. And, sadly, much of the offshore advisory industry relies entirely on commissions – so the unethical advisers always chose the investments that pay the highest commissions. Unfortunately for the victims, the sweet-talking “advisers” are very good at concealing these hidden charges (commissions). They lure victims away from the small print and flash the promise of high – often “guaranteed” – returns.

Scammers – entirely reliant on commissions – are very good at blinding their victims from the risks they are inadvertently taking by putting their hard-earned cash into investments that pay the highest commissions. These scammers are pure salesmen, rather than proper financial advisers. Many of them are notQUALIFIED to give financial advice and they are only out for their “cut” of their victims’ hard-earned life savings. The hidden charges (commissions), paid unknowingly by the victims, buy the scammers their lavish lifestyle. Once the victims have signed on the dotted line, the scammers have no interest in what happens to the remainder of the funds after the commissions have been taken out.

So how does this illicit commission work? And how do the hidden charges damage a victim’s fund?

Let us assume a victim has a fund of £100,000. And he is transferring from a UK pension to an offshore QROPS.

First, a transfer specialist will charge a fee for the transfer advice. Then the offshore adviser will charge a setup fee. Then the QROPS provider will charge a setup fee. So, now we don’t have £100,000 any more – we probably only have £95,000 if we are lucky.

Then the scammer will put the victim into an insurance bond – such as OMI or RL360. The scammer will earn 8% on this (i.e. £8,000). But the victim won’t see this, because the insurance bond provider (OMI, RL360 etc) will claw this back over a ten-year period.

The scammers at OMI or RL360 will always keep a fat chunk of the fund in cash to pay their own fees – usually via hidden charges.

But let’s say they allow £80,000 of the remaining £95,000 to be invested, and let’s say the scammer at the advisory firm invests £40,000 in structured notes and £40,000 in “dirty” funds (i.e. the funds that pay the biggest commissions). This could be a further 10% in commission – so the victim will think he is getting £80,000 worth of investment, but in reality he is only getting £72,000 worth of investment. He simply can’t see the £8,000 in commissions because they are carefully hidden.

Eventually, the victim will realise that his fund is only shrinking, and that it will never have a chance to grow. Growth will be mathematically impossible, because of the constant, hidden fees/commissions. Some victims realise how they have been shafted quite quickly and are able to take positive action to move away from the rogue adviser. But for many, it is too late and too much damage has been done. Their funds will never have a chance to recover to anywhere near where they started. They would have been much better off sticking their retirement savings under the mattress. Because, of course, the “advisers” don’t care – they are long gone in their fancy sports cars and designer suits, sipping champagne at the local exclusive golf club.

In the UK we have regulations in place that prevent financial advisers from taking commissions. This works fine for the ethical, regulated sector of the financial advisory profession. But the unregulated offshore spivs who masquerade as “advisers” – and are, in reality, nothing more than silver-tonged salesmen – still do untold damage to the reputation of the industry by promoting unsuitable, high-risk, illiquid investments to low-risk pension savers (including those resident in the UK).

Many of the scammers are keen to get their UK-based victims’ pensions offshore to escape the protection of the British regulations. This, of course, prevents victims from having access to the FSCS and the ombudsmen.

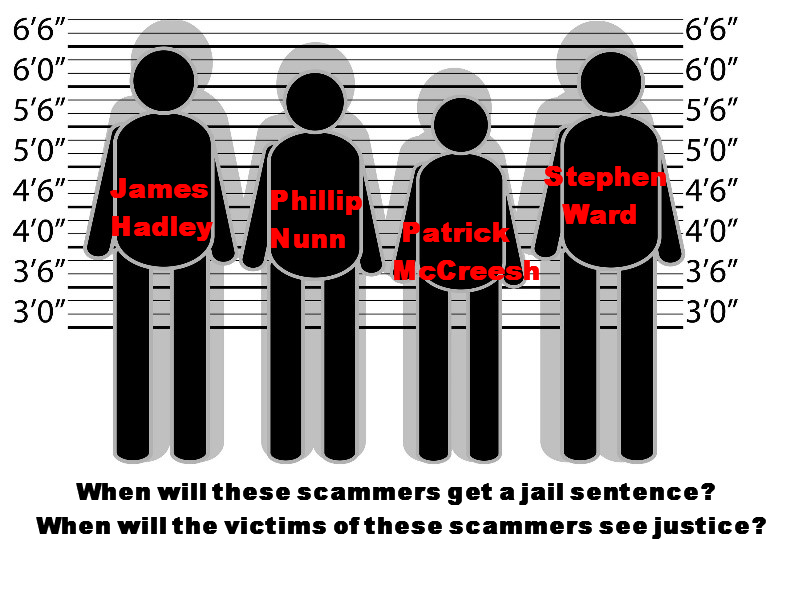

A prime example of this is the dastardly duo: Phillip Nunn and Patrick McCreesh. This pair of scammers received £ millions promoting the Capita Oak, Thurlstone Loans, Henley Retirement Benefits Scheme and Berkeley Burke SIPPS scams – leaving 1,200 victims worried sick about facing poverty in retirement.

The Nunn/McCreesh double act has gone on to promote their own toxic investment fund: the Blackmore Global Fund. This is a UCIS fund (Unregulated Collective Investment Scheme), which is illegal to promote to UK residents. Yet Phillip Nunn and Patrick McCreesh sold these investments with the help of David Vilka of Square Mile Financial Services. (David Vilka is NOT a qualified financial adviser and Square Mile is not regulated to provide investment advice). Nobody knows where the Blackmore Global victims’ funds have gone – as Nunn and McCreesh will not have the fund audited (the last thing they want is anyone knowing what they have invested their victims’ life savings in). But one thing we can guarantee is that the scammers Nunn, McCreesh and Vilka made a pocket full of cash through hidden charges.

In all leading expat jurisdictions – most notably Spain and Dubai – the scammers are beavering away grinding the commission machines. They take their hidden charges with no remorse.

In the time it took the gentle reader to read this blog, at least one victim will have lost their life savings. And one scammer will have earned 8% commission out of selling a useless, pointless, expensive insurance bond – such as OMI, Generali or RL360 – and up to 10% (or even more) on the underlying investments. On top of this, the scammer – masquerading as an “adviser” – will also charge a 1% “advisory” fee. And probably a setup fee. And then there are the QROPS charges.

Henry Tapper wrote an excellent blog on this very subject – he called it FRACTIONAL SCAMMING. I do hope that all offshore advisory firms will read this carefully. The excuse that they didn’t really understand the impact of hidden charges and commissions – and were only copying what they thought the industry was already doing successfully – is simply not going to wash any more. The damage caused by this toxic practice has been widely published and exposed.

The only way forward is to go fee-based. And to outlaw commissions and hidden charges altogether. The scammers won’t do it – but decent, ethical firms will. The hard part will be to warn expats against vultures. Ethical firms will help with this initiative. Obviously, the scammers won’t.

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

As is the case with many scams, the victims are unlikely to recoup any of the funds they entrusted to him. Bartlett is said to have spent the hard-earned funds on prostitutes, escorts and expensive holidays. The victims, all of whom knew him on a personal level, are disgusted at his behaviour and were glad to see this scammer jailed.

Here in the Pension Life office, we are always pleased to hear that a scammer has been jailed. The only shame, is that we just don´t hear the words enough. It would be great if we could write blogs that contain the words SCAMMER JAILED on a daily basis. But sadly it is just not the case.

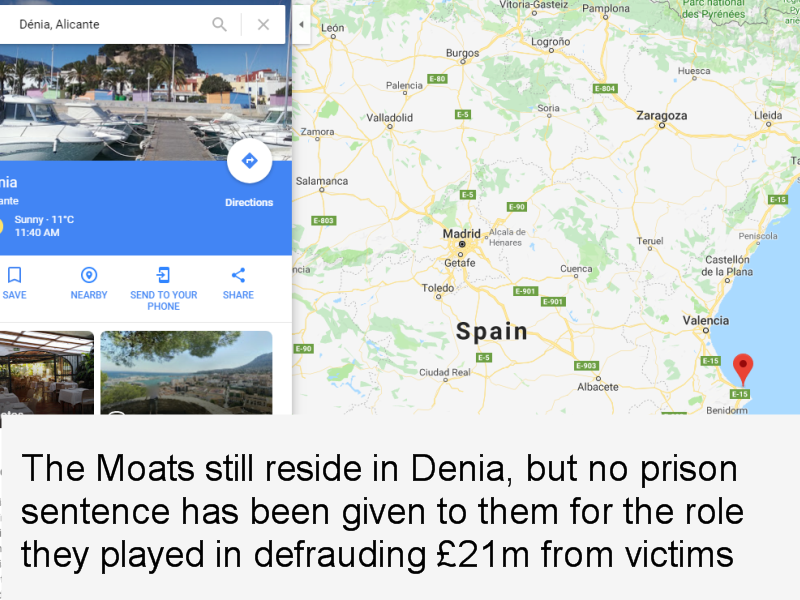

An example of this is Peter and Sara Moat of Fast Pensions – which was wound up back in May 2018. We know they fraudulently took £21m from their victims. We know they did not invest it in the interest of their victims. We know they invested the funds into other businesses they own. We know that they reside in Denia, where their daughter goes to a private school. We know all this – AND the SFO knows all this – yet the Moats are still free to live a lavish lifestyle whilst their victims go without a pension and some face losing their homes as well as bankruptcy.

I´m sure the victims of the Fast Pensions and Blu loans scams would find some solace in reading the words – “scammer jailed” in relation to both Peter Moat and Sara Moat. But I´m not sure if they ever will – and that makes us sad and bloody angry.

Thousands of victims and hundreds of thousands of pounds’ worth of pension money has been fraudulently taken from the victims of scam schemes sold by the above-named scammers. Schemes like Capita Oak, Blackmore Global Fund and the Trafalgar Multi Asset Fund.

All we can do is make a very loud suggestion that STM Group Gibraltar – STM Fidecs – Alan Kentish – should all be given a VERY wide berth when considering a change of pension trustee – as from past evidence they are not to be trusted!

If you have read our other blog you will already know that we have been waiting several years for a cold calling ban to be put in place. It is more than irritating to see that instead of a blanket ban on all cold calling they have imposed a fine on certain cold calls.

This also begs the question of how they had time to pass the legislation for the fine, but not the legislation to simply just ban all cold calling – FULL STOP – no ifs no buts. I also wonder how they are going to track down the cold callers and enforce the fines onto them. Will it be the people making the cold calls that get the fines? or will it be the companies setting up the call centres, or god forbid will it be the masterminds and serial scammers who continue to set up toxic, high-risk funds to lure in their victims?

The victims of the Continental Wealth management scam were cold called, see their story here.

An article written by the Telegraph confirms my fears about the lack of ability the regulators have in enforcing the fines they have already issued. The ICO has been fining companies for nuisance calls since 2015, it is estimated that nearly half of all land line calls are cold calls made to the elderly!

´The ICO has issued more than £5.7m in fines to cold call companies for breaching nuisance rules since 2015, but of the 27 fines issued only nine have been paid in full, recently published government figures revealed.´

The sad truth from these figures clearly shows that despite fines being made they are not being imposed, the companies are simply not paying them. If companies are happy to ignore the fines then they are probably happy to ignore the threat of a fine and continue to make cold calls. Figures from Ofgem have shown that consumers were bombarded with 3.9 billion nuisance phone calls and texts last year but only 27 fines were issued and just nine of those actually paid in full!

There are also so many loopholes these companies – who operate the call centers – can leap through. People must opt out of being cold called, if they have not done this, then companies can claim they were happy to receive the calls.

For instance, if you are online – say on a compare website – and you do not tick the box to state you do not want to be contacted by third parties, you are giving your permission to be contacted. This then means that your data is sold on and the company that calls you about the pension scheme transfer can claim that you were happy to be contacted. It wasn´t a cold call as they had opted in.

The loophole enables them to potentially escape any fine, as technically the receiver of the call had agreed to being contacted via a third party. The company making the calls can claim that they were not making a “cold call”. It feels like this legislation has been made after the horse has bolted from the stable. Hundreds of people have been scammed through the use of cold calling and hundreds more will continue to be scammed with the use of cold calling techniques, through loopholes.

Pension scams involving cold calls such as Capita Oak, Continental Wealth Management, Trafalgar Multi Asset Fund have left hundreds of victims with out a decimated pension fund. These unregulated, shameless firms and their snake salesmen are not going to acknowledge the treat of a fine, nor the administer of a fine. AND if they are fined do the government really think they will pay it?

Serial scammers like Stephen Ward who started out on the ARK pension scam, went on to scam again AND again, despite the scams being shut down by HMRC and the tPR again and again! None of the scammers who promoted these scam have been put behind bars and no money has been paid back to the victims. The scammers show no remorse for their actions. These blatant financial criminals aren´t going to pay a fine for cold calling if they aren´t going to admit the pension scheme´s they set up were fraudulent.

A quick google search of cold call gives untold amounts of advice on how to do it efficiently in 2019! Whilst some of these companies aren´t UK based, the evidence is clear. Cold calling pays and the companies that benefit from cold calling are not going to suddenly stop making them.

The regulators are really going to have to step up and do some serious regulating and enforcing if these fines are to be issued, actually followed up and collected.

The sad truth is that whilst the fines sound great on paper, they will do little to protect the public from being scammed.

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

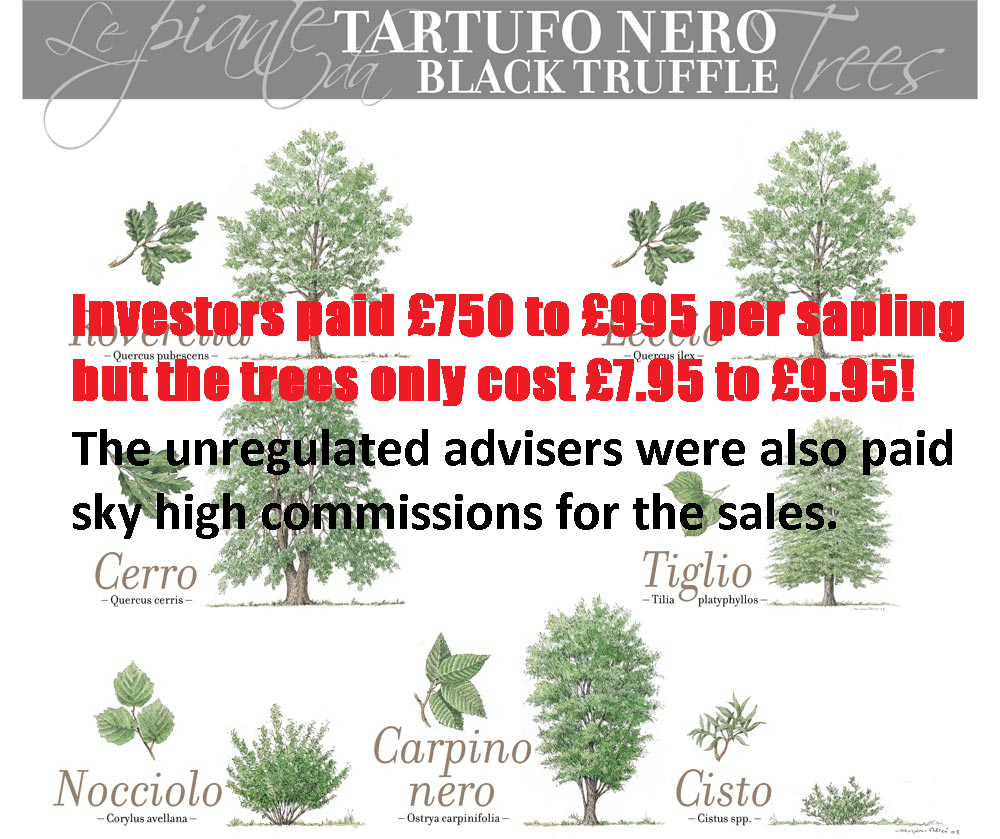

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

This could possibly be described as wonderful news for the victims of Viceroy Jones New Tech Ltd, Viceroy Jones Overseas PCC Limited, Westcountrytruffles Limited, Truffle Sales Ltd and Credit Free Limited. Or maybe not. The whereabouts of the funds is unknown. This pension liberation and investment scam saw 100 investors conned out of £9m of their pension savings.

In short, Viceroy Jones used unregulated financial advisory firms to persuade victims to invest in ‘high-value truffles for commercial sales’. With the promise of high returns on this fixed-term investment (lasting 15 years), investors believed they would reap the benefits once the truffles were harvested.

No truffles were ever harvested.

In reality, the investment saw most of the £9m of funds invested being paid into offshore bank accounts. These funds were then paid out in high commissions to the unregulated advisers who mis-sold the scheme. No supporting documents have been found regarding these investments, so the whereabouts of any remaining funds is unknown.

As I said above, it is only possibly wonderful news for the victims. Whilst the company has been wound up, the victims have been promised no compensation and do not know where their money is. This is a not an uncommon situation in scams like these. The victims of Peter Moat’s company –Fast Pensions, also do not know where their funds have gone.

Cheryl Lambert, Chief Investigator for the Insolvency Service, said:

“We take the matter of unregulated pension liberation investment schemes very seriously and will take action to stop any such schemes who have acted unscrupulously.”

However, I feel I have to disagree.

What message does the Insolvency Service send?!?

Are the perpetrators behind bars?NO!

Are the perpetrators having all their assets frozen and liquidated to pay the victim’s back? NO!

Are the perpetrators facing life without a pension?I DOUBT IT!

Are the perpetrators sorry for what they did?I DOUBT IT!

There is a long list of other pensions scammers who have scammed millions out of the public and still walk freely, creating new scam after new scam.

Winding up these companies is often of little help to the scam victims. What is left of their funds (if any) is passed on to another trustee (often Dalriada) to deal with the ‘clean up’. This action, however, is not without cost and often the funds just sit there doing nothing.

Take the Ark victims whose schemes were transferred to Dalriada – they have not had any compensation in the seven and a half years Dalriada has acted as their trustees. Dalriada, however, has continued – without fail – to charge their yearly fees and costs, further decimating the victims’ funds. AND without any suggestion of what will happen next!

Furthermore, victims that fell prey to these scams, face more stress as they are also contending with HMRC. The Taxman is sending out demands for huge tax bills, as they claim the money the victims liberated (“borrowed”) from the Ark schemes was not tax free. 55% tax is applied to money that was liberated from pension funds – this is deemed an “unauthorised payment charge” by HMRC.

The High Court needs to do a lot more than this, to send a clear message to these scammers. Prosecutions, jail sentences and large fines would be a good start.

All enquiries concerning the affairs of the companies should be made to: The Official Receiver, Public Interest Unit, 4 Abbey Orchard Street, London, SW1P 2HT. Telephone: 0207 637 1110, Email: piu.or@insolvency.gsi.gov.uk.

DWF’s clever PR chaps have come up with some impressive words to sell this law firm’s services: “We connect expert services with innovative thinkers across diverse sectors wherever our clients do business.”

DWF is clearly a big firm (albeit, size isn’t everything). However, one of their most senior litigation teams (twenty senior lawyers) upped and left a couple of years ago to join rival law firm Trowers and Hamlins. These guys obviously didn’t make the leap because things were going swimmingly at DWF – and clearly, they felt no loyalty to their previous employers. Either they were leaving a ship with a hole in the hull the size of Manchester, or they didn’t want to be associated with a firm that happily represented fraudsters.

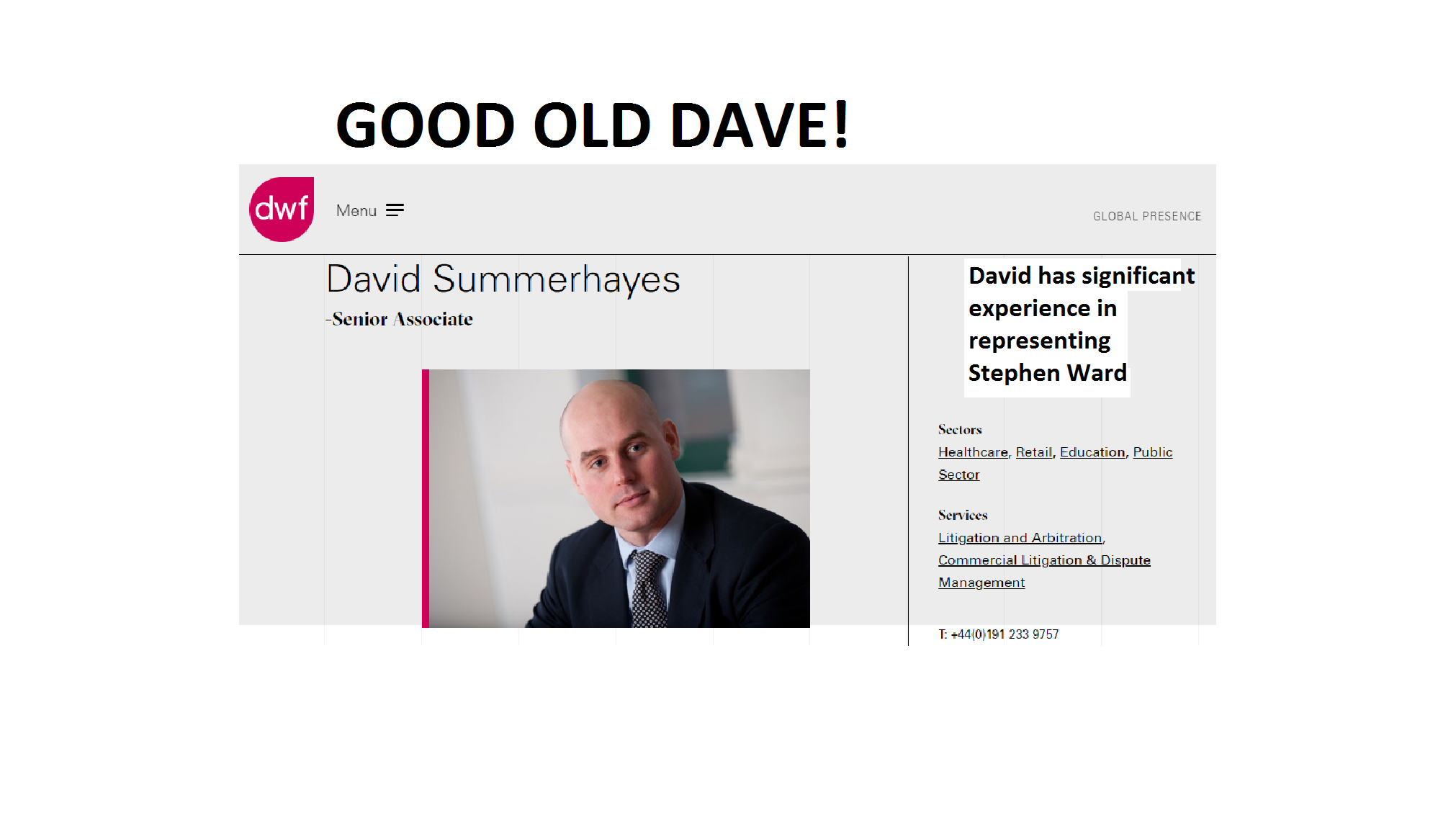

So how do I know DWF? One of their nice lawyers, David Summerhayes, threatened to sue me for defamation when I exposed some of the frauds perpetrated by his client, Stephen Ward of Premier Pension Solutions. Dear Dave got straight to the point in a letter to me on 8.5.2014:

“We act on behalf of Mr. Ward, who trades as Premier Pension Solutions (“PPS”). Our client has become aware of many statements in which he is identified, both personally and through PPS, which contain false and defamatory allegations about him and his conduct. Of particular concern are the statements which convey an imputation of criminal conduct and fraud. The statements our client complains about convey the imputation that our client is guilty of criminal conduct and fraud. This is wholly false and highly defamatory of our client. The publication of these words has caused and is likely to cause serious harm to the reputation of our client.

In light of the above, we now require urgently from you:

1. Identification of where else you have published defamatory statements or similar allegations 2. Your agreement to withdraw the defamatory allegations and undertake not to repeat them 3. Your agreement to provide our client with an apology which shall be published on Facebook 4. Your proposals to pay an appropriate sum of damages to compensate our client for injury to his reputation

In light of the seriousness of the matter, the on-going damage which is being caused to our client’s reputation and the simplicity in which these issues can be redressed, we require that you remove the defamatory allegations and respond with your suggested wording of apology by 4 pm on 22 May 2014.

To be fair to Dave, he probably wasn’t aware at that point just how many thousands of lives his client Stephen Ward had ruined or how many £ millions worth of life savings he had destroyed. But in the intervening four and a half years, you’d have thought that Dave might have done a bit of research on his client. And told some of his mates at DWF what Ward has been up to.

Three hundred victims of the Capita Oak pension scheme were defrauded into transferring their pensions and having them 100% invested in Store First store pods. A bunch of crooks – many of which are now under investigation by the Serious Fraud Office – set up this scam and mercilessly relieved the victims of their life savings.

Store First is a company based Up North where they talk funny. They make buildings that store stuff (kind of does what it says what it says on the tin). Funny thing is, when you put your stuff in a Store First store pod, you can take it out again whenever you like. However, when you put your pension in one of Stephen Ward’s pension schemes, that’s the last you ever see of it.

So just to show Dave Summerhayes there are no hard feelings about his unfriendly threats to me back in 2014, I’m going to give DWF a few friendly hints as to how they might approach their case in the High Court in April 2019. I’m going to be generous because I wouldn’t want them to look silly – so here are some points they might want to mention to the judge:

Q: Who registered the Capita Oak occupational pension scheme with HMRC?

A: DWF’s client Stephen Ward

Q: Who produced the Capita Oak trust deed and rules?

A: DWF’s client Stephen Ward

Q: Who handled the transfer of 300 victims into Capita Oak – at £300 a pop?

A: DWF’s client Stephen Ward

Q: Who knew for certain that all 300 Capita Oak victims were doomed to lose their pensions?

A: DWF’s client Stephen Ward

Q: Who advised XXXX XXXX on how to operate the Capita Oak pension liberation fraud (Thurlstone loans)?

A: DWF’s client Stephen Ward

Q: Who advised XXXX XXXX how to deal with ceding provider reluctance after the Pensions Regulator’s Scorpion warning?

A: DWF’s client Stephen Ward

Q: Who registered the “sister” scheme to Capita Oak – Westminster (now under investigation by the SFO)?

A: DWF’s client Stephen Ward

I am beginning to wonder if DWF stands for: “Defending Ward’s Fraud”. Conflict of interest anyone?

When we buy certain products, they have a warning on them. Cigarette packets, for instance, state that smoking is bad for your health. The wrappers show hideous images of what might happen to you if you use tobacco.

When we buy certain products, they have a warning on them. Cigarette packets, for instance, state that smoking is bad for your health. The wrappers show hideous images of what might happen to you if you use tobacco. What worries us most is the lack of regulatory concern or control in respect of expensive and risky investment products. You can’t buy cigarettes without a stern health warning. The same goes for alcohol: bottles and cans clearly state how many units are in the container, and how many units men and women can safely drink per day. They also state that alcohol should not be consumed by pregnant women.

What worries us most is the lack of regulatory concern or control in respect of expensive and risky investment products. You can’t buy cigarettes without a stern health warning. The same goes for alcohol: bottles and cans clearly state how many units are in the container, and how many units men and women can safely drink per day. They also state that alcohol should not be consumed by pregnant women. You can’t buy a gun without going to a registered shop and having a licence. (Although, I guess on the black market you can). If you buy a gun on the black market, it is going to be ‘hot’. The person you buy it from is going to be dodgy and it certainly won’t come with the correct paperwork.

You can’t buy a gun without going to a registered shop and having a licence. (Although, I guess on the black market you can). If you buy a gun on the black market, it is going to be ‘hot’. The person you buy it from is going to be dodgy and it certainly won’t come with the correct paperwork.

Every year we are seeing an increase in the number of victims falling for pension and investment scams. Despite warnings in the public domain and a huge array of information about how to avoid falling victim to a scam, it seems the scammers are so skilled at their sales techniques, that even the cleverest of people can fall for their slick pitches. Often the scammers use cold-calling techniques to initiate these pitches: using emails, texts, mail shots and the good ol’ phone.

Every year we are seeing an increase in the number of victims falling for pension and investment scams. Despite warnings in the public domain and a huge array of information about how to avoid falling victim to a scam, it seems the scammers are so skilled at their sales techniques, that even the cleverest of people can fall for their slick pitches. Often the scammers use cold-calling techniques to initiate these pitches: using emails, texts, mail shots and the good ol’ phone. Listen to the show here:

Listen to the show here: Ironically, Standard Life has been one of the worst performers in terms of ceding pension providers who have recklessly and negligently handed over millions of pounds’ worth of pensions to the scammers. Completely ignoring the Pensions Regulator’s warnings in 2010, they shoveled £millions across to pension scams such as Ark, Capita Oak, Westminster, Continental Wealth Management, Global Fiduciary Services and many other QROPS scams.

Ironically, Standard Life has been one of the worst performers in terms of ceding pension providers who have recklessly and negligently handed over millions of pounds’ worth of pensions to the scammers. Completely ignoring the Pensions Regulator’s warnings in 2010, they shoveled £millions across to pension scams such as Ark, Capita Oak, Westminster, Continental Wealth Management, Global Fiduciary Services and many other QROPS scams. It seems the only way to escape the scammers – anywhere in the world – is not to fall for their lies. But the challenge is to know what is true and what is false. And that isn’t easy – the scammers are very clever and can adapt quickly to invalidate public warnings and even use them to their advantage. In addition to the scammers, there are now

It seems the only way to escape the scammers – anywhere in the world – is not to fall for their lies. But the challenge is to know what is true and what is false. And that isn’t easy – the scammers are very clever and can adapt quickly to invalidate public warnings and even use them to their advantage. In addition to the scammers, there are now

Another victim of Berkeley Burke SIPPS investments into Store First storage pods has come forward. 55-year-old factory worker Robert McCarthy, of Ebbw Vale, said he has lost more than £30,000 through a Self-Invested Personal Pension (SIPP). He was duped into the transfer and investment by unregulated firm Jackson Francis which was liquidated in 2014. His investment may or may not be worthless – depending on whether Store First is wound up later in 2019.

Another victim of Berkeley Burke SIPPS investments into Store First storage pods has come forward. 55-year-old factory worker Robert McCarthy, of Ebbw Vale, said he has lost more than £30,000 through a Self-Invested Personal Pension (SIPP). He was duped into the transfer and investment by unregulated firm Jackson Francis which was liquidated in 2014. His investment may or may not be worthless – depending on whether Store First is wound up later in 2019.

Victims were also invested into the Store First storage pods via

Victims were also invested into the Store First storage pods via  Stephen Ward

Stephen Ward

Blacklist – “The Pension Scam (No 69)”

Blacklist – “The Pension Scam (No 69)” than one scam at a time (being male, he can’t multi-task).

than one scam at a time (being male, he can’t multi-task). Kentish is eager to know how much money can be made out of this plot. XXXX explains that 46% was earned out of his Capita Oak and Henley scams and that he hopes to make at least as much out of this one. With Kentish’s “help” (nudge nudge, wink wink). Of course, the proceeds could be split and plenty of brown envelopes used to disguise the handing over of the proceeds.

Kentish is eager to know how much money can be made out of this plot. XXXX explains that 46% was earned out of his Capita Oak and Henley scams and that he hopes to make at least as much out of this one. With Kentish’s “help” (nudge nudge, wink wink). Of course, the proceeds could be split and plenty of brown envelopes used to disguise the handing over of the proceeds. Now that the Trafalgar Multi-Asset Fund has been suspended – thanks to the hero of the hour: Reinert – Kentish decides to buy Caffrey’s QROPS firm, Harbour (which is full of Phillip Nunn’s Blackmore Global investment scam). Caffrey swans off into the sunset with £1 million burning a hole in his pocket, quietly humming “Oh Danny Boy”.

Now that the Trafalgar Multi-Asset Fund has been suspended – thanks to the hero of the hour: Reinert – Kentish decides to buy Caffrey’s QROPS firm, Harbour (which is full of Phillip Nunn’s Blackmore Global investment scam). Caffrey swans off into the sunset with £1 million burning a hole in his pocket, quietly humming “Oh Danny Boy”. Sadly, of course, it was real life. As more than 400 victims will attest. So no more script-writing for me. I will stick to blogs in the future.

Sadly, of course, it was real life. As more than 400 victims will attest. So no more script-writing for me. I will stick to blogs in the future.

A firm with advisers who are unwilling to answer all of the questions you ask them is clearly a firm to be avoided.

A firm with advisers who are unwilling to answer all of the questions you ask them is clearly a firm to be avoided.

The words ¨accept¨ and ¨agreed¨ are used here, which gives the impression they all sat down to a nice lunch and “agreed” that they may have made a mistake and therefore “accepted” their bans! These people are financial criminals who left many lives ruined. The victims – many of which were already in financial hardship – now have no pension fund to look forward to.

The words ¨accept¨ and ¨agreed¨ are used here, which gives the impression they all sat down to a nice lunch and “agreed” that they may have made a mistake and therefore “accepted” their bans! These people are financial criminals who left many lives ruined. The victims – many of which were already in financial hardship – now have no pension fund to look forward to.

In many pension scam cases, we find victims telling us that they were

In many pension scam cases, we find victims telling us that they were  So how does this illicit commission work? And how do the hidden charges damage a victim’s fund?

So how does this illicit commission work? And how do the hidden charges damage a victim’s fund? The only way forward is to go fee-based. And to outlaw commissions and hidden charges altogether. The scammers won’t do it – but decent, ethical firms will. The hard part will be to warn expats against vultures. Ethical firms will help with this initiative. Obviously, the scammers won’t.

The only way forward is to go fee-based. And to outlaw commissions and hidden charges altogether. The scammers won’t do it – but decent, ethical firms will. The hard part will be to warn expats against vultures. Ethical firms will help with this initiative. Obviously, the scammers won’t.

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

AND to rub salt into the wounds of the Trafalgar victims,

AND to rub salt into the wounds of the Trafalgar victims,  In follow up to our blog ´

In follow up to our blog ´

A quick google search of cold call gives untold amounts of advice on how to do it efficiently in 2019! Whilst some of these companies aren´t UK based, the evidence is clear. Cold calling pays and the companies that benefit from cold calling are not going to suddenly stop making them.

A quick google search of cold call gives untold amounts of advice on how to do it efficiently in 2019! Whilst some of these companies aren´t UK based, the evidence is clear. Cold calling pays and the companies that benefit from cold calling are not going to suddenly stop making them.

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “