On the web of pension scams It seems as though criminal convictions against pension scammers might be getting popular. More than a decade has gone by with virtually none of the usual suspects getting jailed – despite a few criminal investigations (that, so far, have not resulted in convictions). Is the system really that hopeless or do these criminals just know how to work it? Probably, both. But is it getting any better?

Almost all scammers and scams are, in some way, related or connected. If the earliest scammers (circa 2010) had been prosecuted and put behind bars, much of today’s damage could have been prevented.

Now that there is an intricate web of them passing around their tricks of the trade, it’s no wonder they’ve all been able to bypass the laws and regulations.

Two scammers have, however, recently been brought to justice:

Much of the £13m ended up in the hands of well-known scammer David Austin – who committed suicide after being caught in another pension scam (using his daughter Camilla as the “front man”).

Susan Dalton & Alan Barratt

The Barratt and Dalton scheme, was also promoted by Julian Hanson – one of the main promoters of the £27m Ark pension scam in 2010/11. Hanson’s vigorous promotion efforts resulted in £5.5m worth of Ark victims (100 in total). One of Hanson’s co-scammers was the notorious Stephen Ward of Premier Pension Solutions who was the “architect” behind the Ark scheme – along with Andrew Isles of Isles and Storer Accountants. Hanson, Ward and Isles were never prosecuted and so went on to operate and promote millions of pounds’ worth of further pension scams – ruining many thousands more lives.

Ryan Playford

Sue Dalton, after moving on from the Barratt and Dalton scheme, went to work at Continental Wealth Management in Spain – reporting to head scammer Darren Kirby and his partner Jody Smart (who was the sole director of the company). Dalton’s extensive experience in pension scamming made her a hit at CWM. Ironically, Hanson has not been jailed along with Barratt and Dalton.

Playford got 15 years for supplying cocaine and canabis. Clearly a wrong-un, and someone who has no respect for the law or for the wellbeing of people’s lives who would inevitably be ruined by drug abuse.

But what does Playford’s drug conviction have to do with pension scams – you may ask? We have to go back a decade to discover the answer:

In 2008, Playford and an associate – Natasha Beesley – registered a drug company inCyprus:R. P. Med Plant. Presumably, the authorities were convinced that by “drugs”, this meant legitimate drugs for medicinal purposes.

Stephen Ward

In 2012, however, the pension scammers pounced on this Cyprus company as being the ideal sponsoring employer for another one of Stephen Ward’s pension scams: Capita Oak. Ward and his pension-lawyer friend Alan Fowler, used R. P. Med Plant Limited (Cyprus) as the so-called employer for an occupational scheme – registered by HMRC and the Pensions Regulator.

Ward and Fowler forged signatures on a trust deed for their new pension scam, and slightly changed the name of the employer to R. P. Medplant Limited (so that nobody could find it easily on the Cyprus Companies House register). It seems likely that Ward and Fowler must have known Ryan Playford somehow, in order to be able to get their hands on his drug company.

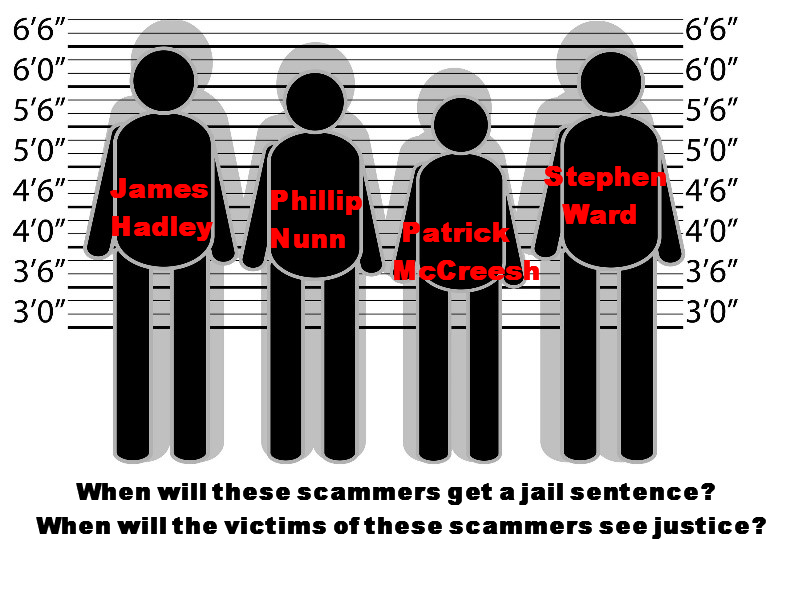

Patrick McCreesh

Capita Oak then became the vehicle for the scamming of 300 victims into investing their entire pensions in Store First store pods. Ward took charge of all the victims’ pension transfers, while another group of scammers took care of the cold calling of thousands of potential victims and signing up of the actual 300 victims.

Capita Oak’s 300 members were not the only victims invested in Store First store pods. There were thousands more in the Henley Retirement Benefits Scheme and various SIPPS including Carey (now Options and owned by STM), as well as Berkeley Burke and Rowanmoor. There have so far been no convictions – other than Playford’s for drug dealing.

This interconnected web of lies and deceit will keep on spreading unless these criminals actually fear the consequences of their actions. Let’s keep the convictions coming and not just save them for drug lords.

Blackmore is two scams for the price of one: Blackmore Bond and Blackmore Global Fund. Both run by Phillip Nunn and Patrick McCreesh of Blackmore Group. Blackmore Bond is a “loan” scheme (bond) which has conned £25 million out of hundreds of victims and is now in default. Blackmore Global is an “investment” scam which has never provided any evidence as to where the money has gone and what it is invested in. It is thought that more than £40 million is invested in the fund. Both scams have left hundreds of investors worried sick that they may never see their money again.

Blackmore Scam by Nunn & McCreesh

Much has been written about both scams – by interested observers, bloggers, journalists, distressed investors/lenders and by me.

Investors of Blackmore is a closed Facebook group run by Mat Noakes. Mat created the group for Blackmore Bond victims, and makes sure that those who apply to join are genuine investors. He has strict rules about conduct on the group (as he is entitled to). Mat is raising funds to take legal action against Blackmore and has provided a substantial amount of information and evidence on this scam. Most revealing of all is that the so-called property development projects which victims have funded are incomplete and bound to be difficult (or impossible) to sell. Blackmore has run out of cash and is in default. Nunn and McCreesh are using a series of lame delaying tactics to try to assuage the victims’ fears. As with most Ponzi-style scams, once new money dries up, existing lenders/investors don’t get their promised returns and can’t get their money out.

Blackmore Bond and Global Fund is an open group run by me. I created it for both Blackmore Bond and Blackmore Global victims. Anyone can join – even the scammers if they want to (although I doubt they’d have the balls – scammers are almost always spineless cowards). There are no rules – anyone can say whatever they want. Especially me. I say openly and publicly that both Blackmore Bond and Blackmore Global are scams run by Phillip Nunn and Patrick McCreesh who have used a series of other known scammers to promote and distribute these two scams.

Blackmore Bond was promoted by Surge Group run by Paul Careless. He has been arrested and is under investigation by the Serious Fraud Office. Surge earned £6 million out of promoting this high-risk, illiquid, unregulated bond to low-risk investors. Surge also earned £60 million out of promoting the London Capital & Finance bond scam which is now being wound up by Finbarr O’Connell of Smith & Williamson.

Blackmore Global was promoted by two spivs: David Vilka and John (Gus) Ferguson of Square Mile Financial Services. Another spiv – Charlie Goldsmith – lurks in the background and appears to make even more money out of promoting Blackmore than Vilka and Ferguson.

Behind the lies, deception and undoubted fraud perpetrated by Nunn and McCreesh, let’s look at their history in some depth. In 2012/13, they were running a firm called Nunn McCreesh which was an appointed agent of Sage Financial Services. Their legal permission was to sell (mediate) insurance. But clearly they didn’t earn enough out of doing legitimate business, so they turned to financial crime.

Joining the string of scammers behind the Capita Oak, Henley, SIPPS scam led by XXXX XXXX, Nunn McCreesh set out to help scam hundreds of victims into bogus occupational pension schemes and have their life savings invested in store pods (out of which the scammers earned 46% in commission).

The scam was investigated by the Insolvency Service in 2014 (and later by the Serious Fraud Office). Here’s what the Insolvency Service’s witness had to say about Nunn McCreesh on 27.5.2015:

Documents received from members of CAPITA OAK indicated they were initially contacted by Patrick McCreesh of Nunn McCreesh and Its Your Pension Ltd and offered pension review services.

Its Your Pension had not traded and was a dormant company.

Nunn McCreesh had traded as an insurance brokerage between 2009 and 2012 when they entered into a verbal arrangement where in return for providing pension leads they received a commission.

Nunn McCreesh provided 100-200 leads per month which were provided by email and/or telephone for which they received £899,829.86 during the period 26.3.12 to 14.5.14.

It is important to understand the pedigree and psychology of Phillip Nunn and Patrick McCreesh to understand why they should never have been allowed to handle anybody’s money. And why they would have been better off in prison rather than being left free to put what looks like over £65 million worth of victims’ money at risk.

The Insolvency Service’s own research established that the pair had been masquerading as trading legitimately from a non-trading company. This establishes their dishonesty.

“Pension reviews” have been a classic feature of many pension scams in the past ten years. They are a way of conning victims into handing over their pensions to bogus schemes such as Capita Oak and Henley – and placing them into the hands of serial scammers such as XXXX XXXX and Stephen Ward.

Nunn McCreesh was mainly interested in the lucrative business of commissions. This in itself is a dishonest and toxic practice since it is deliberately hidden from the investors – who have no idea that large portions of their hard-earned life savings are being handed over to the scammers.

Over a period of more than two years, Nunn McCreesh provided around 5,000 “leads” to the other firm of scammers involved: Jackson Francis. These leads would, inevitably, have been obtained illegally. As a result of this industrial-scale scamming, Nunn McCreesh gave potential victims’ contact details to Jackson Francis. It is known that at least 1,200 of these resulted in the contacts losing their entire pensions.

During this two-year period, Nunn and McCreesh obviously learned a great deal from the other scammers. They also saw XXXX XXXX making a fortune out of this particular scam – and then watched him go on to make an even bigger fortune out of the Trafalgar Multi Asset Fund scam. Seeing XXXX XXXX boasting a magnificent country house, Ferrari and champagne lifestyle, they obviously realised they were only in the “little league” and needed to move up a gear. And thus Blackmore was born.

Nunn and McCreesh then teamed up with the scammers behind Aspinall Chase and Aktiva Wealth Management, later renamed Square Mile International, then Michalska Holding and now called Planet Pensions. The firm has just been wound up.

These scammers – Gus Ferguson, David Vilka and Charlie Goldsmith – then proceeded to scam many hundreds of victims into the Blackmore Global Fund. They duped UK residents into transferring their pensions into QROPS in the IoM, Malta and Hong Kong: Kreston, Optimus, Harbour and GFS. After all the scammers shared out the huge commissions, there would have been very little actual cash left – and what there was would have been invested in worthless rubbish which paid more commissions. These sub funds would have included Swan and GRRE – also run by known scammers.

Nunn and McCreesh claim on their website that they invest part of the Blackmore Global fund in commercial property. My worry is that some of this may be the same or similar commercial property to the worthless rubbish held in the Blackmore Bond. Of course, there have never been any audited accounts – despite many repeated assurances for the past four years they they are “working on it”.

My biggest worry is: why was this allowed to happen? Why weren’t Phillip Nunn and Patrick McCreesh prosecuted back in the days when they were under investigation by both the Insolvency Service and the Serious Fraud Office? Why weren’t they put safely behind bars so they couldn’t scam any more victims? And where was the FCA? Nunn and McCreesh were clearly running an unregulated collective investment scheme without permission. We know the FCA has the power to take action against firms they suspect of running such schemes because they’ve done so with Park First doggedly for the past three years.

The Blackmore Group website claims to be: “a Real Estate Investment House, built to be an institutional yet dynamic company capable of maximising market opportunities by combining a blend of investment management experience and real estate expertise”. Yet Nunn and McCreesh only have a track record of miserable failure and scams. Their company, Nunn McCreesh, only operated for one year from 2012 to 2013. During this twelve month period it somehow managed to chalk up £351,000 worth of debts and loans. Neither Nunn nor McCreesh has ever demonstrated any investment management experience – other than what they may have gleaned about investment scams from XXXX XXXX. The Companies House accounts paint a bleak picture. The last published accounts – 2017 – show the company being barely solvent and with debts of over one million pounds. And no sign of the 2018 accounts.

The Blackmore Global website spouts similar disingenuous nonsense claiming: “expertise of specialists and regulated Investment Managers, along with a robust due diligence process”. This is clearly downright lies. The Blackmore Global brochure claimed that a company in Barcelona – Meridan Capital – was the Investment Manager. And yet, when I spoke to Meridan Capital they said they most certainly were not. Had there been any due diligence done, the underlying assets would most certainly not have been accepted into the fund. These included Swan and GRRE – run by known scammers.

The Blackmore Bond website is full of similar lies and rubbish. It claims Blackmore is a property development company. It isn’t. It claims to have: “a wealth of property insight and a proven track record in delivering quality developments”. But according to the published accounts for 2017, it has £1.1 million worth of assets and £1.1 million worth of debts. And to have made £6,000 profit. I would say that is anything but a proven track record – and in fact shows that they have no experience or success in property development since they set the company up in 2016.

This whole episode shows the dangers of known scammers such as Phillip Nunn and Patrick McCreesh being left free to set up unregulated investment companies, bonds and funds with no professional qualifications or expertise. The only track record this pair has is a well-documented track record of success in selling illegally-obtained contact databases and of promoting bogus pension schemes which are under investigation by the Serious Fraud Office.

Meghan and Harry – the Duke and Duchess of Sussex – are having a tough time (and are running away from home). Their sadness and confusion is because they have no purpose or passion in life. So I am offering them an interesting and satisfying challenge: taking on and championing the cause of pension scam victims. Harry’s Mum knew a thing or too about adopting worthy causes and had no problem jumping on a plane to far away, war-torn places full of the most appalling human suffering and landmines. Meghan and Harry don’t even have to travel as far as the airport to find victims whose cause desperately needs championing.

Poor Duke and Duchess of Sussex – what an awful time they’re having: posh clothes; flash cars; sumptuous “cottage” in Windsor Park. They needn’t be bored and aimless any longer. They can become patrons of the plight of the thousands of British citizens who have lost £ billions to pension and investment scams.

Just as the Late Princess Diana confronted the horrific dangers of land mines, Meghan and Harry can confront the huge tide of appalling human misery caused by scammers Stephen Ward of Premier Pension Solutions; Paul Clarke of Roebuck Wealth; Dennis Radford of Spectrum IFA Group; Darren Kirby of CWM; Gus Ferguson and David Vilka of Square Mile; XXXX XXXX of Nationwide Benefit Consultants; Phill Pennick of Pennick Blackwell; Peter and Sara Moat of Fast Pensions; Paul Baxendale-Walker; Patrick McCreesh and Phillip Nunn of Blackmore Group; Paul Careless of Surge Group.

This is now becoming a very high-profile topic – especially in the light of the multiple, dismal failings of the FCA and a recent series of hard-hitting articles published by Tom Kelly of the Daily Mail. Kelly, an engaging and open-minded young man (who I am sure the Sussexes will like) has written about a wide array of pension and investment disasters which have befallen thousands of victims since 2010. I would urge Meghan and Harry to contact him: Tom’s email address is: Tom.Kelly@dailymail.co.uk and his editor’s address is: Geordie.greg@dailymail.co.uk

As the disillusioned Royals are bound to ask whether pension scam victims have anything to do with them (or whether they should even care about people who have lost their life savings or pensions), they might like to consider the following:

If Frogmore Cottage catches fire, Meghan and Harry will have to call the Fire Brigade. The sumptuous property cost £2.4 million to refurbish to the highest possible standard, but even the best sparks do sometimes make the odd mistake. The Royals’ home – and even their lives – will be in the hands of the firemen. These brave firefighters will risk their own lives running into the burning building; then will rescue the people and (hopefully) save the building.

If Meghan and Harry’s baby son Archie is unwell after inhaling smoke, they will rush him to hospital – where he will be tended to by nurses and doctors.

If a therapeutic trip to Canada is required (to get over the upset of their home being damaged by fire), the plane will be flown by two pilots.

Pension and investment scammers target people from all works of life – including firemen, doctors, nurses and airline pilots. Next time the Sussexes place their hands into the lives of any of these professionals, they might like to consider whether these people are victims of scams and are worried sick about their financial losses.

Scammers don’t care what their victims do for a living: sparks, chippies, builders, gardeners, taxi and bus drivers, soldiers, care workers, architects, scientists, accountants, artists, police officers…the list is endless – and includes airline pilots.

Meghan and Harry need not think that going to Canada will get them far away from the world of pension and investment scams. These criminals have long arms and can easily reach as far as North America – and well beyond. The long list of highly-organised scams includes schemes in the UK and all expat jurisdictions across the globe – including Canada.

Coming from a privileged background where Harry’s Mum gets paid more than £8 million a year (and Meghan and Harry are reportedly worth around £30 million), it is going to be hard to get their heads round the poverty thousands of victims are facing. Perhaps cutting the purse and apron strings will teach Meghan and Harry just how hard it is to earn a crust – and save for a retirement that isn’t handed to them on a plate.

While the Duke and Duchess of Sussex fly backwards and forwards between the UK and Canada, perhaps they might like to ponder a few things:

How to keep the plight of pension and investment scam victims in the headlines

How to encourage the government to make financial regulation effective

How to provide a law-enforcement system that ensures all scammers are jailed

How to get the law changed to ensure HMRC pursues the perps rather than the victims

Whether the pilot of their plane has lost his pension and hasn’t got his mind entirely on the job

If Meghan and Harry do accept this challenge, they will have to accept that it won’t be easy. The scammers are determined, hard-nosed and hard-hearted criminals; the regulators are lazy and mostly asleep at the wheel; the police are over-stretched and under-resourced; the government hasn’t got a Scooby – and anyway can’t think beyond Brexit. This is evidenced by the fact that the moronic Chancellor Sajid Javid appointed arch FCA failure Andrew Bailey to govern the Bank of England. Boris Johnson was just as bonkers to endorse this ridiculous decision. When he told the Queen of the appointment, she should have given him a good slap round the earhole. (Mind you – she was probably a bit preoccupied about the company Uncle Andrew was keeping at the time, and she probably thought “oh well, at least Bailey isn’t a paedophile”).

The biggest challenge in fighting pension and investment scams is how to help prevent further victims. The best way to do this is to keep the topic firmly in the public eye – and that means encouraging the press to keep the subject in the headlines (and not let it get shoved out of sight by trivia). The other important role that Meghan and Harry could play would be to ensure that politicians keep their promises. A couple of years ago Boris Johnson promised a group of his constituents that he would tackle pension scams. But nothing happened and now he is ignoring them. We all know he’s been a little busy recently, but leaving his own constituents hanging after promising he would help them is not acceptable.

I remember being with two Ark victims at least five years ago and begging journalists at The Sunday Times and The Sun to run an article on the Ark scam. They all said it wasn’t “sexy enough”. Mark Atherton of The Times wrote a very good piece in The Times in 2014, but he was severely threatened and never wrote about pension scams again. https://www.thetimes.co.uk/article/pension-scam-leaves-victims-in-debt-k33rlcs25wc

Just think how many victims could have been prevented had the media done their duty and fully exposed the parties who caused and facilitated these scams since 2010. Then think how many suicides and stress-related deaths could have been prevented. Consider how much money could have been saved from destruction – and how many people could have been looking forward to a well-earned and comfortable retirement rather than abject poverty and misery.

In October 2019, The Mail’s Tom Kelly came to my office in Spain and spent several days with me. I went through the whole history of Stephen Ward and Ark (followed by Capita Oak and more than a dozen others), as well as James Lau and Salmon Enterprises, Paul Baxendale-Walker, Peter Moat and Darren Kirby’s Continental Wealth Management. I explained to Tom in detail how the flow of money works from the ceding pension providers: Aviva, Standard Life, Prudential, NHS, Police and Local Authorities etc., to the receiving schemes; what the difference between personal and DB pensions is and how the whole bogus occupational scheme fraud worked. Most important, we went through how hidden commissions and high-risk, toxic investments often destroy victims’ funds – as well as the life bonds such as OMI, SEB, Generali, Friends Provident, RL360 which lock investors in to entirely unnecessary, inflexible and expensive offshore bonds – AND PAY FAT COMMISSIONS TO THE UNQUALIFIED, UNREGULATED SCAMMERS.

In case Meghan and Harry are still unsure whether patronage of an initiative to outlaw pension and investment scams is their cup of tea, I will share, yet again, the video which features the death of CWM victim Mark Davison:

Laura Shannon of The Mail On Sunday attended Mark’s memorial service and interviewed dozens of further CWM victims in September 2019. While five months pregnant, Laura made the journey to Denia, Alicante, in fierce heat – putting all other so-called investigative journalists who write about financial services (or not, as the case may be) to shame. Not even stopping to recover from an arduous bus journey from the airport, she got stuck straight in and wrote an excellent piece: https://pension-life.com/continental-wealth-management-plunder-in-paradise/

Responsibility for reforming financial services and bringing culpable parties to justice may lie with governments, regulators, police and HMRC. But Royals could do their part too. Meghan and Harry: get stuck in to a worthy cause. Find out what the real world is really like for ordinary, decent, hard-working victims of pension and investment scams.

Finally, I am enormously grateful to Shadow Chancellor John McDonnell for calling out our idiot Chancellor Sajid Javid over the appalling appointment of Andrew Bailey as Governor of the Bank of England. Anyone who fancies dropping him a line can reach him here: mcdonnellj@parliament.uk or here: lowderh@parliament.uk

April 2019 sees the battle between Store First and the Insolvency Service. On April 15th, the High Court proceedings will kick off. As a result, the Store First v Insolvency Service will determine how many people will lose their pensions permanently. Two sets of very expensive lawyers – DWF and Eversheds Sutherland – will battle it out to see if Store First can continue trading. In the end, if the Insolvency Service wins the war, then both law firms and an insolvency practitioner will get rich.

As a result of the Insolvency Service winning, 1,200 pension scam victims will probably lose the majority of their investments in Store First. In most insolvencies, there is little left after the various snouts in the insolvency trough have had their fill. Investors will be lucky to get 10p in the pound. If there’s an “R” in the month. And if it is snowing. And if Brexit has a “happy ever after” ending.

The Insolvency Service says it is “in the public interest” to wind up Store First. But are they right? Isn’t winding up the company going to do even more unnecessary damage?

One very important issue is that the Insolvency Service’s witness statement dated 27.5.2015 (by Leonard Fenton) is so full of inaccuracies, misunderstandings, incomplete facts and an obvious failure to understand how the scam worked – as to be utterly laughable. The Insolvency Service and the High Court will rely heavily on this witness statement – and yet it has so many holes and errors that it is misleading, incomplete and meaningless. I asked the Insolvency Service questions about the incorrect and incomplete statements and made numerous comments on the failings contained within the statement. But the Insolvency Service did not even have the courtesy to reply or even acknowledge my contribution. In my view, this is arrogance and incompetence in the extreme.

This impending legal battle (which will cost the taxpayer £millions) is riddled with many more questions than answers. Here are a couple of my questions:

QUESTIONS RE STORE FIRST V INSOLVENCY SERVICE BATTLE

Why did HMRC and tPR register Capita Oak and Henley Retirement Benefits Scheme as pension schemes in the first place?

How many of the many scammers behind Capita Oak and Henley have been prosecuted?

The reason for my questions is that both HMRC and tPR were negligent in registering the two occupational pension schemes. This was because the schemes were obvious scams from the outset. They both had non-existent sponsoring employers which had never traded or employed anybody. And they weren’t even in the UK.

HMRC was blind, stupid and lazy at the start – when these two schemes were registered by known scammers. But several years later, HMRC woke up pretty smartly and sent out tax demands for the “loans” the victims received. The Store First v Insolvency Service Battle is probably doomed to ignore HMRC’s negligence in causing this disaster in the first place.

James Hay and Suffolk Life had been facilitating the Elysian Fuels investment scam at around the same time. And this was with the considerable “help” of serial scammer Stephen Ward. So, this was a prime time for scams and scammers. However, both HMRC and tPR failed the public back then and have continued to do so ever since.

In 2015, the Insolvency Service identified and interviewed most of the scammers behind the Store First pension scam. In their witness statement dated 27th May 2015, Insolvency Service Investigator Leonard Fenton cited statements and evidence from all the key players.

KEY PLAYERS IN THE STORE FIRST PENSION SCAM:

Ben Fox

Stuart Chapman-Clarke

Michael Talbot

Sarah Duffell

Bill Perkins

XXXX XXXX

Alan Fowler

Jason Holmes

Karl Dunlop

Christopher Payne

Keith Ryder

Craig Mason

Patrick McCreesh (of Nunn McCreesh – along with Phillip Nunn)

Tom Biggar

Paul Cooper (Metis Law Solicitors)

That is fifteen scammers who have never been prosecuted. They have not only never been brought to justice, but many of them went on to operate further scams and ruin thousands more lives – destroying more £ millions of hard-earned pension funds.

And what of Toby Whittaker’s Store First? There is no question that store pods are not suitable investments for pension fund investments. Car parking spaces are unsuitable for pensions as well. There are, in fact, a long list of inappropriate investments for pensions – including anything high-risk, illiquid and expensive or commission-laden.

All the above are routinely used and abused by pension scammers as “investments” for some dodgy scheme. Invariably, the above investments come with pension liberation fraud and/or huge introduction commissions and hidden charges. However, it is rarely the fault of the artist, wine maker, start-up entrepreneur, truffle farmer or property developer that the scammers profit so handsomely from abusing their products.

Store First v Insolvency Service Battle

I hope Store First defeats the Insolvency Service in the forthcoming battle in the High Court this month. And I hope that the public and British government will finally get to see what embarrassingly inept, corrupt, lazy regulators and government agencies we have. I will publish the Insolvency Service’s witness statement separately for anyone who wants to read the Full Monty.

Let us not forget that the solicitors acting for the Insolvency Service – DWF LLP – also act for serial scammer Stephen Ward. It was Ward who was responsible for the pension transfers which subsequently invested in Store First. Had it not been for him, 1,200 victims’ pensions totaling £120 million wouldn’t now be at risk. But, somehow, DWF LLP doesn’t think that is a conflict of interest?!?

Let us be clear: if the Insolvency Service wins the court case, the investors will get nothing. This will mean that, yet again, the victims will get punished. If Store First wins, the investors will get at the very least half their money back. If they are patient, they may even get it all back.

Much like a black hole in Space, the Blackmore Global Fund and Blackmore Bond will swallow up victims’ savings – and never spit them out again.

20% Black Hole in Blackmore Global

It is no secret that we have little confidence in the Blackmore Global Group run by Phillip Nunn and Patrick McCreesh – two of the scammers who promoted Capita Oak and earned nearly £1 million from providing “leads” for the cold callers. Capita Oak is now under investigation by the Serious Fraud Office, and Nunn McCreesh’s nefarious activities were investigated and reported on by the Insolvency Service.

To confirm our suspicions that Nunn and McCreesh’s Blackmore Global Fund and Bond are not just high-risk and illiquid crap (and – of course – totally unsuitable for pensions or anyone with less money than sense), they have announced that 20% of your money could go towards paying for the “costs of the investment”. To put that into plain English, any of the unregulated scammers who promote and distribute the Blackmore investments are earning 20% in commission.

This new-found “transparency” by Blackmore is neither a courtesy to their customers, nor evidence of voluntary honesty. Rather, it is a reaction to the FCA´s new rules for being “clear, fair and not misleading” .

“Capital Protection” and “Income Certainty”. Immediately below these phrases, in letters half the size, were the words:

“Capital at risk | Please read our risk section. Illiquid and non-transferable. Not FSCS”

This change is in connection with Nunn and McCreesh’s Blackmore Global Bond. Their Blackmore Global Fund has already featured heavily in the press with criticisms about its costs and unsuitability for pensions. BBC 4 You and Yours did a feature on the fund back in January 2018, finding that an unregulated adviser – David Vilka of Square Mile International Financial Services – invested many of his QROPS clients into this unsuitable fund – which undoubtedly will have paid him fat commissions.

THE BLACKMORE GLOBAL FUND IS A UCIS (UNREGULATED, COLLECTIVE, INVESTMENT SCHEME) WHICH IS ILLEGAL TO PROMOTE TO UK RESIDENTS. Yet, David Vilka – who had no investment license – promoted it and Nunn and McCreesh accepted the many investments into it from him.

What is similar in both the Blackmore Global Fund and Bond, is the lack of transparency from the start. With the fund, there was also a ten-year lock-in, which was in the small print and not mentioned to the pension investors at the time of signing over their pensions to the scammers. Some of the members were nearly 60, meaning that they were unable to access their money when they retired.

The Bond, up until now, has had no transparency on its charges – and the risk factors were most definitely hidden.

The confirmation of a 20% commission charge (to the scammers who promote and distribute this risky, expensive, opaque investment) comes as a welcome dribble of transparency. However, it is still unclear as to how – after this huge payment – Blackmore investors will ever be able to recoup the initial costs and then start to make some headway on their investment.

Bond Review explains this well:

“In slightly simplified terms, if Blackmore raises £10,000 from an investor in its 3 year bonds paying 7.9% per year, and pays out 20% in commission, it now needs to turn £8,000 into £12,370 to repay the investor in full, representing a 55% return over 3 years – or 15.6% per year.

For its 5 year bonds paying 9.9%, the return required to turn £8,000 into £14,950 is 87% over 5 years, or 13.3% a year.

Any investment targeting a return of 15.6% or 13.3% a year will inevitably be extremely high risk – and while Blackmore can diversify over many such projects, some of its projects will fail, which will lower the overall return.”

This is not an investment to enter into lightly (or at all). Blackmore Global showed net liabilities of £7 million on assets of £18 million in its last accounts – December 2017. Finances and accounts can dramatically shift in the short space of one year: a well-run, professional and ethical company could turn things around. But with Blackmore Global failing for three years to even produce audited accounts on their fund, and lying about who their Investment Manager is, this hardly inspires any confidence at all.

Another worrying thing about Blackmore Global is that they use Surge Financial to promote their toxic wares – and has paid this firm £5.1 million in one year for “marketing services”. Surge Financial is run by Paul Careless, and was promoting the failed London Capital & Finance fund, which paid out an eye-watering 25% to the scammers who promoted and distributed their toxic wares. Having conned thousands of victims into investing £236,000,000 into London Capital and Finance, the whole lot is now probably lost as the company has gone into liquidation. But Surge Financial pocketed £60,000,000 in marketing this toxic fund – and is still promoting Blackmore Global. The FCA declared that the marketing blurb was misleading, unfair and unclear – and it is obvious that the lies told in the glossy brochures duped thousands of people into losing their life savings.

So, with Blackmore Global also using Surge Financial to source victims, and succeeding at the rate of £1.5m a month, it is a serious worry that there will be thousands more victims when the Blackmore Global shit hits the fan.

Bond Review is quoted as saying:

“That Blackmore Bond paid out up to 20% in commission is already known from Blackmore’s December 2017 accounts, which disclosed that £25.4m had been raised in the period (July 2016 to December 2017) and that £5.1m had been paid to Surge Financial for “sourcing investors loans and front and back office operations” (almost exactly 20%).

Could Blackmore Global go the same way as London Capital Finance? We already know that the Blackmore Global fund has been used to scam hundreds of UK-resident victims out of their pensions using QROPS. We also know that few of these victims have had their money back – and that there is zero disclosure as to where the money has gone.

Just remember: there are perfectly-good, regulated funds out there – with extremely low charges, zero commissions to scammers, and excellent performance history (openly reported in the public domain). People don’t need to put their hard-earned savings in black holes such as Blackmore which don’t even disclose what the underlying assets are.

When we buy certain products, they have a warning on them. Cigarette packets, for instance, state that smoking is bad for your health. The wrappers show hideous images of what might happen to you if you use tobacco.

However, when it comes to investments, the ‘advisers’ selling dangerous investments are able to disguise the risks and costs. Offshore, there seems to be no effective code of conduct, or regulation as to what they must disclose and what they can conceal.

When selling their investments, these firms are really good at omitting details of the full charges that will apply – not only initially – but on an ongoing annual basis as well. These hidden charges put your investment in danger.

The FCA has stated:

“In one case it found an asset manager had omitted a 4 per cent a year transaction cost from the UCITS Key Investor Information Document (KIID).”

In so many pension scams, we hear that the victims were sold a ‘free pension review’; they were not told about the transfer costs; that they were not told about annual fees either. In many cases, the transfer costs and fees work out to be considerably higher than if they had paid a proper fee for the review in the first place. These hidden costs put a huge strain on the fund and sometimes victims can lose up to 25% of their fund to hidden charges.

What worries us most is the lack of regulatory concern or control in respect of expensive and risky investment products. You can’t buy cigarettes without a stern health warning. The same goes for alcohol: bottles and cans clearly state how many units are in the container, and how many units men and women can safely drink per day. They also state that alcohol should not be consumed by pregnant women.

Alcohol companies manage to fit all this info about the dangers of drinking on a tiny label. And this poses the essential question as to why financial advisory firms are able to sell risky investments again and again – omitting clear warnings about the dangerous aspects of them.

“The FCA reserved its fiercest criticism for asset managers, saying it found instances where asset manager fact sheets or websites did not mention costs. When they did, they often gave the ongoing charge figure, which omitted transaction costs, performance fees and borrowing charges which are shown in the Key Information Document (KID). In one example, total charges in the PRIIPs KID equated to around 3 per cent per annum – but the only costs given in the fact sheet was the 1.2 per cent annual management charge (AMC).”

This is not news to us at Pension Life. It is something we have been writing about for sometime – and we have a great deal of evidence that hidden, excessive charges are a terrible blight on the face of financial services internationally. It is indeed excellent news that the FCA has finally highlighted the dangers of such hidden charges, but now we need to make sure these dangers are highlighted to the public. CLEARLY AND VISIBLY.

You can’t buy a gun without going to a registered shop and having a licence. (Although, I guess on the black market you can). If you buy a gun on the black market, it is going to be ‘hot’. The person you buy it from is going to be dodgy and it certainly won’t come with the correct paperwork.

So if you are a normal, law-abiding citizen (and cautious investor), you would want a legitimate investment which fits your risk profile – and full paperwork disclosing ALL the charges. Make sure you pick the right adviser who will give you evidence of all these essential details.

Dodgy advisers are still getting away with selling ‘hot’ investments: funds that are clearly toxic and dangerous to your pension fund. These advisers manage to do this very successfully by wrapping them in a fluffy cover and selling them with an array of unrealistic promises of high returns and alleged capital protection to reel the victims in.

When considering a pension transfer, we urge you to familiarise yourself with our ten standards. Your adviser ought to adhere to these standards anyway – and if he doesn’t then walk away. Number eight covers what we have talked about in this blog: CHARGES.

Your adviser MUST GIVE YOU: Full disclosure of fees, charges and commissions on all products and services in writing, before you commit. So before you sign anything regarding a pension transfer and subsequent investment, please ensure you know exactly what charges will be applied to your fund: before, during AND after. It is also imperative to know if there is a lock-in period and early exit penalty and to make sure you are comfortable with that.

Excessive and concealed fees can ruin a once healthy and happy pension fund – just like smoking can ruin your lungs and drinking can ruin your liver. Hidden charges can put your funds in danger and ruin your retirement savings beyond repair.

Here is a list of our ten standards.

STANDARDS ACCREDITATION CHECKLIST FOR FINANCIAL ADVISERS:

Proof of regulation for all services provided by the firm and individual advisers in the jurisdiction(s) where advice is given and the clients are based.

Verifiable evidence of appropriate, registered qualifications and CPD for all advisers. (Where there are insufficient qualifications, there must be clear evidence of plans and preparation to achieve required goals within a reasonable, stated time frame).

Professional Indemnity Insurance

Details of how fact finds are carried out, how clients’ risk profiles are determined and adhered to.

Details of the firm’s compliance procedures – assuring clients of the highest possible standards and assurance that risk profiles are always accurately and faithfully respected.

Clear and consistent explanation and justification of the use of insurance bonds for investments.

Unambiguous policy on structured notes, UCIS funds, in-house funds, non-standard assets and any ongoing commission-paying investments. Report of all investment recommendations for all clients and evidence as to how these match individual risk profiles.

Disclosure of fees, charges and commissions on all products and services at time of sale, in writing, before clients commit.

Account of how clients are updated on fund/portfolio performance.

Public evidence of complaints made, rejected or upheld and redress paid.

For more in depth explanation check out our other blog on the ten standards:

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

As is the case with many scams, the victims are unlikely to recoup any of the funds they entrusted to him. Bartlett is said to have spent the hard-earned funds on prostitutes, escorts and expensive holidays. The victims, all of whom knew him on a personal level, are disgusted at his behaviour and were glad to see this scammer jailed.

Here in the Pension Life office, we are always pleased to hear that a scammer has been jailed. The only shame, is that we just don´t hear the words enough. It would be great if we could write blogs that contain the words SCAMMER JAILED on a daily basis. But sadly it is just not the case.

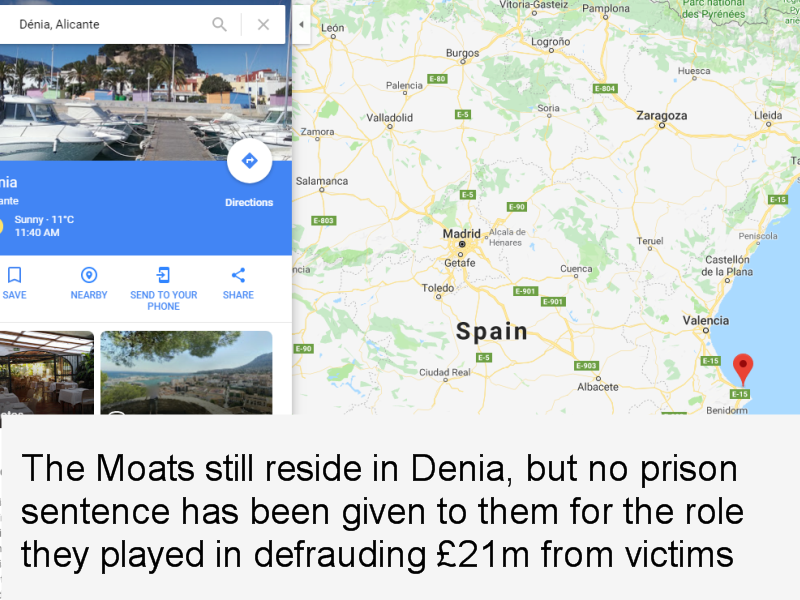

An example of this is Peter and Sara Moat of Fast Pensions – which was wound up back in May 2018. We know they fraudulently took £21m from their victims. We know they did not invest it in the interest of their victims. We know they invested the funds into other businesses they own. We know that they reside in Denia, where their daughter goes to a private school. We know all this – AND the SFO knows all this – yet the Moats are still free to live a lavish lifestyle whilst their victims go without a pension and some face losing their homes as well as bankruptcy.

I´m sure the victims of the Fast Pensions and Blu loans scams would find some solace in reading the words – “scammer jailed” in relation to both Peter Moat and Sara Moat. But I´m not sure if they ever will – and that makes us sad and bloody angry.

Thousands of victims and hundreds of thousands of pounds’ worth of pension money has been fraudulently taken from the victims of scam schemes sold by the above-named scammers. Schemes like Capita Oak, Blackmore Global Fund and the Trafalgar Multi Asset Fund.

All we can do is make a very loud suggestion that STM Group Gibraltar – STM Fidecs – Alan Kentish – should all be given a VERY wide berth when considering a change of pension trustee – as from past evidence they are not to be trusted!

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

Integrated Capabilities – a Trust Company based in Malta have created their own Pension Scheme – Azure Pensions. On the face of it, however, the management team do not appear to have learned anything from their previous experience with Optimus Retirement Benefit Scheme No.1 and their association with David Vilka of Square Mile International Financial. It appears they have now teamed up with some very dubious friends – the result of which is very likely to create more victims of UK pension scams.

I AM GRATEFUL TO STEVE – ONE OF THE BLACKMORE GLOBAL/DAVID VILKA VICTIMS – FOR RE-WRITING THIS BLOG AT THE REQUEST OF INTEGRATED CAPABILITIES’ LAWYER.

The Azure website states: “We believe that trust is built and earned. As such we have an ingrained and sustained desire to develop long-term relationships with our clients”. These are just words and words are easy. It’s what you do that counts.

In 2015, the Optimus scheme started out with 26 members and by the end finished up with 1,176 – that’s a gain of almost 100 new members per month! I was one such member conned into transferring my pension by fraudulent misrepresentations made by David Vilka of Square Mile Financial Services.

This new pension arrangement locked me in for 10 years – definitely a “long-term relationship” – giving all parties the opportunity to drain my pension dry in fees. Credit where credit is due, however. Once I discovered I was in a scam, the director Andy Dawson (bottom row, 3rd from the left) did make an extraordinary effort not only to redeem the investments but successfully persuaded most parties to waive their early exit penalties and refund their fees. Only the greedy Symphony Fund chose to keep the penalties and that’s after mysteriously dropping in value 30% just before redemption. Thanks to Andy Dawson and his team, I did manage to get back 92% of my pension. But the BIG QUESTION is what has happened to the other 1,100+ members? It is inconceivable I was the only one transferred into this scheme via Vilka et al.

Another claim made by Azure Pensions is: “Our people are highly experienced, knowledgeable and motivated to do their utmost to ensure that they deliver a superior, professional and hassle-free service.” But this firm, and the people in it, have a history of working with scammers and investing members’ retirement funds in investment scams such as Phillip Nunn’s Blackmore Global and Richard Reinert’s Symphony Fund. So I would take issue with claims like “highly experienced” and “knowledgeable”.

If they were highly experienced and knowledgeable they would have known that, at the time I was being advised by Vilka in January 2015, Aktiva Wealth Management (later changed to Square Mile and now called Michalska Holding) was NOT regulated by the Czech National Bank. According to the CNB records, this didn’t happen until 5th May 2015 and then, only for insurance mediation and not for transferring pensions!

If Integrated Capabilities had been “highly experienced and knowledgeable” then they would have known the Symphony Fund – regulated in their own jurisdiction by their own regulator, the MFSA – was NOT permitted to be offered to me, a retail client. And they knew this because they had the Symphony documentation which clearly prohibited its promotion to UK retail clients.

I complained to the MFSA but they didn’t care and Malta’s “Ombudsman” equivalent – what they call the Office of the Arbiter for Financial Services – deters complaints because they have this small print that says if you lose, the other side can be awarded legal costs!

If Integrated Capabilities had been “highly experienced and knowledgeable” they would have known the Blackmore Global fund had never published audited accounts and still hasn’t to this day (December 2018). Something that in January 2015 caused Kreston (pension provider on the Isle of Man) to write to its members explaining their concerns over Blackmore Global and also stopped taking new members from Vilka.

So if they were “highly experienced and knowledgeable” then why did they allow all this to happen? It certainly had nothing to do with “motivation to do their utmost”. It is clear their only motivation was to take on as many members as possible – irrespective of which scammer introduced them and what unsuitable investments were made for them. Also, they claim to have a “long history and proven track record of providing expert and value for money multi-jurisdictional fiduciary solutions, so our clients and partners can have great peace of mind in the knowledge that our board of directors has over 100 years combined expertise in this field.” The proven track record is that they have taken on hundreds of new members per month from a known scammer – and the last thing their members have is peace of mind – far from it.

Angie has referred to these people at Integrated Capabilities/Azure Pensions as a “bunch of cowboys” and their lawyer recently wrote to her and objected to the phrase. You make your own mind up.

How do they earn trust when they have accepted transfers and investment instructions from known unregulated scammers Square Mile and David Vilka? Why would victims “desire” to have a long-term relationship with Azure when funds were previously placed in an unnecessary, expensive insurance bond by Investors Trust in the Cayman Islands (the only purpose for which is to pay commission to the scammers)?

Azure Pensions also claims that one of its partners is Carey Pensions UK LLC. Carey is facing a legal battle for investing a member into unregulated collectives in Australia through a Carey Pensions SIPP.

Carey is in hot water for allowing investments into high-risk scams, and is also now part of STM – undoubtedly the biggest scammers in the offshore pension trust industry. It would seem the Azure team have not learned anything from their previous experience.

If, as they say “We believe that trust is built and earned …”, then you actually have to do some “trust building” with actions – not just weasel words. The indisputable facts seem to indicate “business as usual” but with a different name.

It is highly probable that Integrated Capabilities still has at least 1,100 victims invested in scam funds such as Blackmore Global by scammers such as David Vilka of Square Mile. It looks like most – if not all – of these victims were UK residents who should never have gone into a QROPS at all in the first place. The only reason for transferring these pension funds to a QROPS was to get the money away from UK regulation so that the scammers could invest them in commission-paying UCIS funds – such as Blackmore Global.

The public should be very wary of Azure in the first instance, do a lot of due diligence and make sure their pension funds don’t go anywhere near offshore unregulated collectives wrapped in an assurance bond that can suck your pension dry.

Azure states on their website that: “Notwithstanding your appointment of a Financial Adviser, ICML has an overriding right to refuse to make investments, or to disinvest, where it believes that a particular investment proposal may not be consistent with the Scheme’s Investment Policy or any investment restriction applicable under Retirement Scheme Law.”

Is this a change in policy? Are they going to put their “knowledge and experience” to meaningful use by exercising some due diligence? Is this a statement that means they have sorted the 1,100+ members in the Optimus Scheme that are most likely locked into “investments … not consistent with the Scheme’s … Policy?” Or are these just more weasel words with no substance?

Reformed management team or a “bunch of cowboys”? The jury is still out. The association with Carey & STM doesn’t appear to show a reformed team. What has happened to the 1,100+ members in the previous Optimus Scheme? Has anything been done to remedy the situation?

I believed, and still do, that this team was unwittingly drawn into facilitating a scam by David Vilka of Square Mile, and that in essence Integrated Capabilities/Azure Pensions are a respectable team. However, if they want to be seen as having learned from their past failings they could take some actions. First, help the 1,100+ members to avoid financial ruin and secondly assist in the prosecution of the architects of the scam facilitated by Integrated Capabilities. I am sure they will have a considerable body of evidence that could be used to show fraudulent misrepresentation and thirdly drop the association with companies with an already poor reputation for their involvement with scams or unregulated collectives being promoted to retail clients.

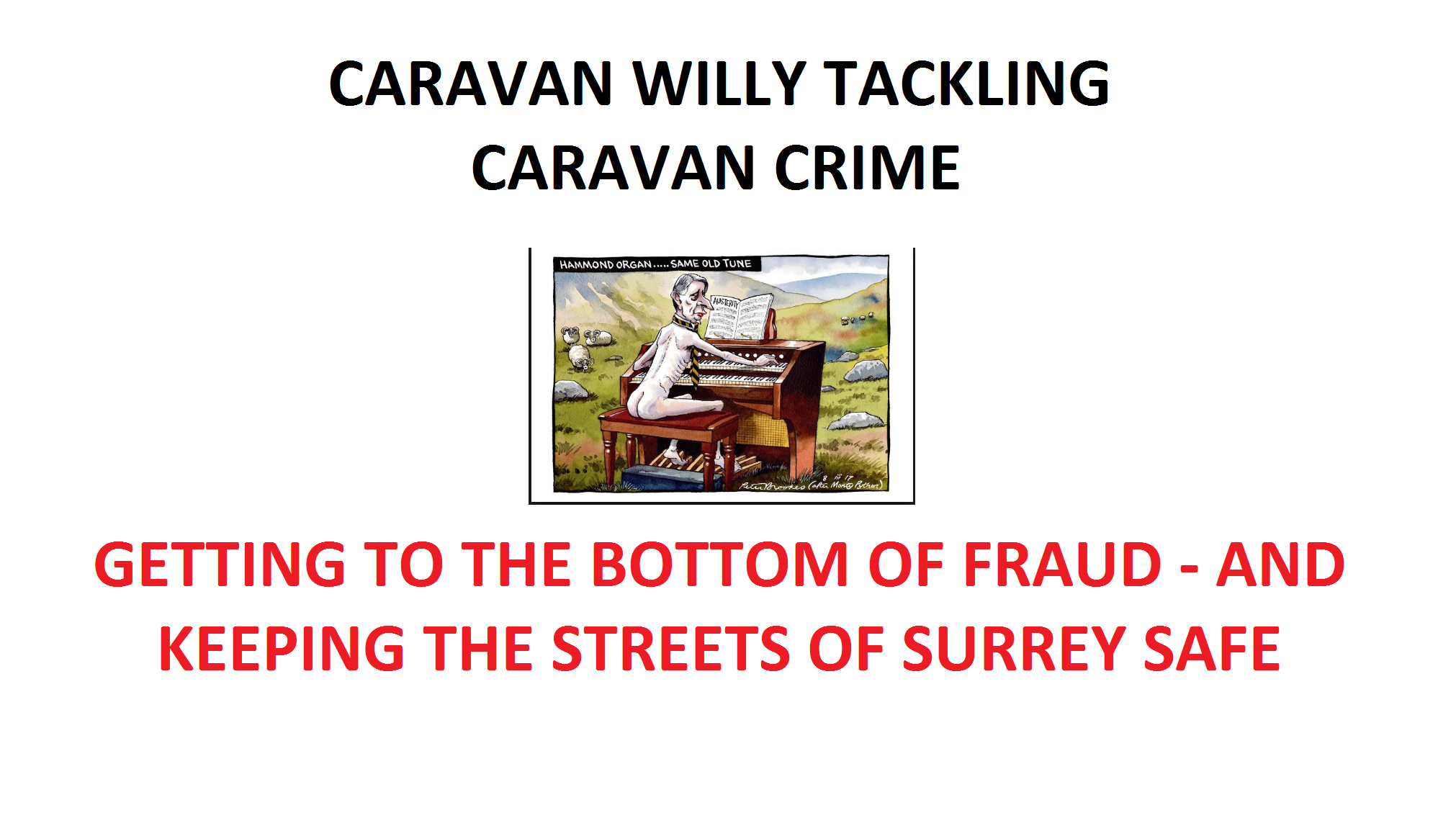

Tackling Caravan Crime – Chancellor Philip Hammond. Victims of pension fraud in scams such as Ark, Capita Oak, Westminster, London Quantum, Friendly Pensions and Salmon Enterprises – will not be surprised to hear that even the Crown Prosecution Service acknowledges that the fraudsters have defeated the system. Alison Saunders, head of the CPS, has stated publicly that the British justice system can’t cope. She is stepping down and is clearly disheartened by Britain’s failure to tackle crime – especially fraud. She has vented her frustration in an interview:

But look hard enough, and you will see how tackling crime can be done successfully. As someone who constantly writes about the failure of our police and courts to bring criminals to justice, I was surprised to hear of a spectacular success story in leafy Surrey recently.

Mr. and Mrs. Shore of Thorpe, in Surrey, were successfully prosecuted and jailed for proceeds of crime. Residing in Runnymede Borough Council – presided over by Chancellor Phillip Hammond – this dastardly pair (in their sixties) were both sent down for a heinous crime under the Proceeds of Crime Act 2002 (“POCA”).

After many years of detailed investigation, the successful prosecution will send out a resounding warning to all such criminals and will no doubt discourage others from profiting from the same hideous crimes. And the crime was…….?

Housing homeless families in caravans without planning consent.

Let that sink in for a moment – vulnerable people with young children who had a choice between living on the streets or living in a caravan. And this crime was committed in Runnymede Borough where there was insufficient housing for the many poor families who could not afford private accommodation and had not been offered council homes.

This spectacular success story on the part of Hammond, Runnymede Borough Council and the CPS has left the good citizens of Surrey relieved that these dangerous caravan owners are now behind bars and dozens of homeless families are now living on the streets. Jobdone; justice served; well done Cutty Sark!

Hailing from Surrey myself, I am pleased that the county will now be a safer place. The successful prosecution was in respect of 14 breaches of six enforcement notices issued since 1999 by Runnymede Borough Council, following a seven-day trial at Guildford Crown Court. The jury heard how the farm owners had not only stationed the caravans on their own land, but had also failed to demolish a shower room. Unbelievable!

Hammond must be strutting the halls of Westminster bursting with pride and patrolling the fields of Runnymede with a sense of upholding the social and civil justice with which King John would have been delighted. In the House of Commons bar, Chancellor Hammond is probably boasting that there is a reason why he is named after a large organ. In fact, after his spectacular success with the Shores’ caravans, he will probably go down in history as “Caravan Willy” for presiding over such a coup.

I am sure that the many thousands of people who have lost millions of pounds’ worth of life savings to scammers such as Stephen Ward, Julian Hanson, George Frost, XXXX XXXX, Phillip Nunn, Patrick McCreesh, Stuart Chapman-Clarke, David Vilka, David Austin, Darren Kirby, Dean Stogsdill, Anthony Downs and James Lau will now understand why the CPS couldn’t dedicate any resources to prosecuting them. And they will, no doubt, be glad that the priority of the judiciary was removing unauthorised caravans in Surrey.

As in most of my blogs, there is an important postscript: Caravan Willy is a keen property owner and is reported to be worth over £9 million. The Shores’ land has now been confiscated by Runnymede Borough Council. And it is worth at least £27 million once planning permission for a housing estate is granted. I wonder who will be lucky enough to scoop that one up?………

This week Henry Tapper wrote a blog entitled, “The wheels of the law turn (too) slowly”. He exposes the fact that when it comes to financial crime the justice system in place just isn´t enough. I think he was being generous with his title. The wheels of the law don’t just turn slowly – they just don’t turn at all. Friendly Pensions has been in the news this week.

In the case of Friendly Pensions, we know ringleader David Austin is guilty of setting up 11 fake schemes, with toxic investments including a truffle farm. We know that he and his partners in crime, Susan Dalton, Alan Barratt and Julian Hanson (also connected to the Ark Scam), are guilty of scamming 245 pension savers out of £13.7 million. We knew all of this back in January 2018, yet no arrests have been made!

“David Austin, 52, has been banned from serving as a pension trustee and disqualified from working as a company director for 12 years. His business partners Susan Dalton, Alan Barratt, and Julian Hanson have also been barred from trustee roles.

David Austin’s daughter, 25-year-old Camilla, has been banned from serving as a director for four years for helping him with the scheme.”

They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

Camilla Austin was a central part of the operational side of the Friendly Pensions scam. She and a number of her girlfriends went into nursing homes and approached elderly, frail and vulnerable elderly people. They easily conned them into signing transfer request forms – all that is required to get their hands on millions of pounds’ worth of pension funds. And, of course, we all know that the ceding providers do nothing to stop fraudulent transfers.

As Henry points out, banning these people from acting as trustees or directors, does little to deter past, present and future pension scammers. A ban is barely a slap on the wrist as far as we are concerned; these scammers can still launch any number of future dodgy schemes by simply finding the next crooked stooge – just as XXXX XXXX used the idiotic Karl Dunlop to be a director in the Capita Oak scam.

Keeping pension savers safe from financial crime should be at the top of the list – but, instead, it is at the bottom. Pension scammers are left free to commit their crimes over and over again. Take Julian Hanson: he was busily scamming dozens of Ark victims out of more than £5.3 million worth of pensions back in 2011 and 2012, yet he was not prosecuted or jailed. Hence, he was still able to get “friendly” with David Austin and go on to scam hundreds more victims out of their pensions.

Despite investigations being made into these schemes, Ward was still able to go on and create the CWM monster scheme that saw around 1,000 victims conned out of their pension funds. Ward is hovering somewhere between his collection of luxury villas in Florida and the Spanish Costa Blanca – but at least he is no longer doing pension transfers. Over the past nine years, Ward can be linked to dozens more pension scams that have left thousands of victims’ funds decimated.

These cases are just the tip of the iceberg. We must not forget Philip Nunn and Patrick McCreesh´s investment scam Blackmore Global. This was in the wake of them doing the lead generation for the Capita Oak and Henley Retirement Fund scams. The Insolvency Service has wound up these schemes, yet Nunn and McCreesh remain free to defraud more victims as they have never been brought to justice.

David Vilka of Square Mile International was one of the main promoters of the Blackmore Global Fund scam. He “advised” dozens – possibly hundreds – of victims to invest their pensions in this scam (despite the fact that he is neither qualified nor regulated to give investment advice). Again, he has never been prosecuted or jailed, so still remains at large – free to continue scamming people out of their pensions.

You can see a depressing pattern here: these words are about cold, hard facts. The authorities are leaving known scammers free to keep scamming.

Victims of these scams have been left in misery and financial ruin. Some have taken their own lives. Yet the perpetrators, those guilty of these repeated financial crimes, are free to do as they please.

This area of financial crime really is where the wheels of the law don´t seem to turn. Shame there aren’t any regulators capable of doing any regulating, or law enforcement agencies capable of enforcing the law.

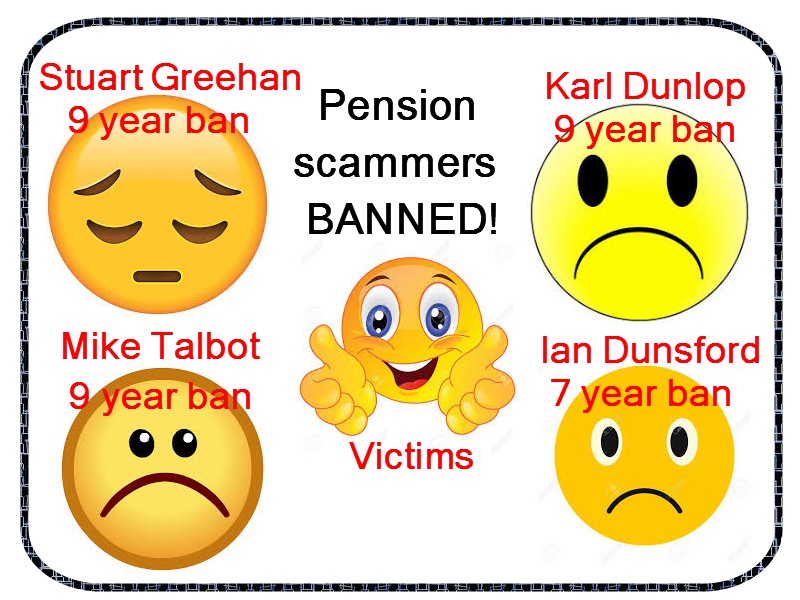

Articles like New Model Adviser’s report on some of the scammers behind the Capita Oak/Henley/Store First scam getting banned always makes me smile. Knowing that a few pension scammers (four in this case), are being named and shamed – as well as banned from being directors – motivates me to share information about these evil scams with the public.

“An investigation led by the Insolvency Service revealed the directors were connected with Transeuro Worldwide Holdings, which helped fund two introducer firms Sycamore Crown and Jackson Francis. The firms were involved in the transfer of £57 million of pension savings.

Sycamore Crown director Stuart Greehan agreed to a nine-year voluntary ban as a result of false and misleading statements to encourage investors to transfer their pensions.