I have enormous respect for FT Adviser. Their articles are written by proper journalists and they generally write competently and professionally. FT Adviser puts International Adviser to shame with their thinly-disguised promotional shows and Micky Mouse “articles” which only ever promote their own sponsors – Old Mutual International and their ilk.

It was really interesting to read FT Adviser’s recent “Top 100 Financial Advisers 2018“. I had, however, never heard of most of the advisory firms. But that is hardly surprising because nobody ever comes to me and says “guess what, I’ve got a really good adviser and am making good returns on my investments”. And I presume that all the advisory firms listed by FT Adviser are full of happy clients who never need to complain about being scammed into unsuitable investments and losing money due to a combination of high, undisclosed charges and trading losses within insurance bonds (particularly OMI’s).

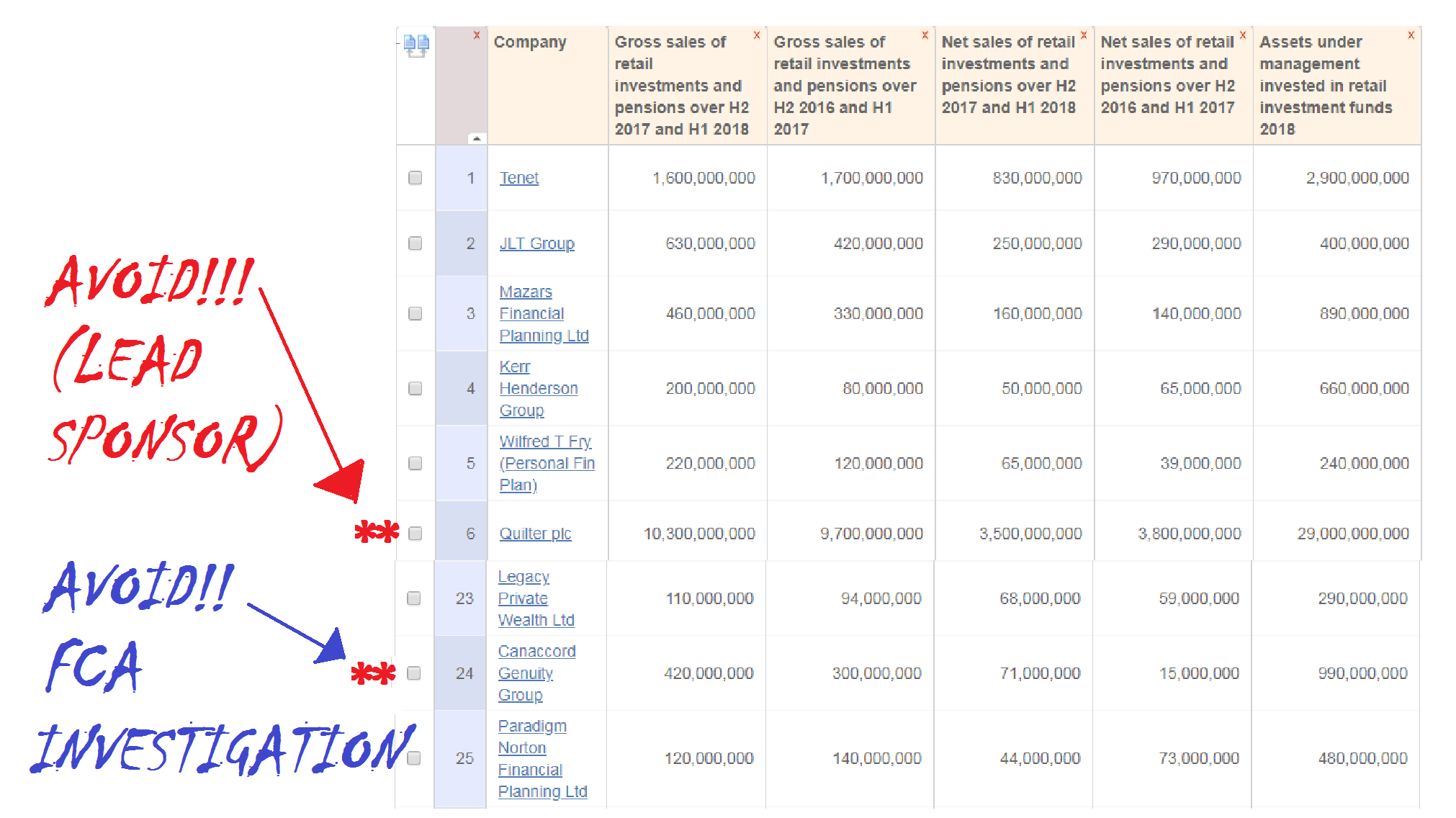

However, and it is a big “however”, there are a couple of firms on the list which should have had big red asterisks against them – largely because they discredit the rankings, the other firms on the list and FT Adviser’s reputation. These are Quilter PLC and Canaccord Genuity Group.

Canaccord Genuity Group is under investigation by the FCA for non-disclosure of investment charges. Coming 24th in the top 100 list, it is very worrying that an advisory firm that lies about how much investments cost should have £990,000,000 worth of assets under management. I wonder what the investment charges are on that little lot and how much non-disclosure of related charges has gone on. Let us not forget that “non-disclosure” means lying – and with almost one billion under management that is very serious indeed.

However, Canaccord Genuity Group’s porky pies do pale into a degree of insignificance when compared to Quilter plc which came sixth with £10.3 billion worth of sales and £29 billion worth of assets under management. Quilter plc is Old Mutual International, which is the life office which helped scam hundreds of victims out of their life savings. So surely FT Adviser should have put a really bright double red asterisk against this firm on the league table? (Or perhaps they didn’t care, as Quilter was the lead sponsor?).

If Quilter is managing £29 billion worth of assets – presumably on behalf of thousands of investors – I wonder how much of this has been used to buy toxic, high-risk structured notes. As Old Mutual International seems to be claiming there is nothing wrong with destroying millions of pounds’ worth of clients’ funds by making inappropriate investments, the same must be true of Quilter plc.

Old Mutual International was buying many millions of pounds’ worth of structured notes provided by Commerzbank, Royal Bank of Canada, Nomura and Leonteq between 2010 and 2017. OMI has disclosed that at least £94 million worth of the Leonteq notes were fraudulent, and is now suing Leonteq.

I have to confess, if I were a client of Quilter plc, I would be inclined to change advisers sharpish – although most certainly not to Canaccord Genuity. Mind you, that still seems to leave 98 other firms worth considering.

But, despite the embarrassing inclusion of these two dud firms, congratulations to FT Adviser for the hard work which must have gone into producing this hit parade. This is definitely one in the eye for the hopeless nitwits at International Adviser.

Long-term savings plans by Friends Provident, Generali, Zurich, Hansard and RL360. These have been around for years and are typically mis-sold by seedy, unregulated advisory firms. Why don’t we come up with an alternative? THE LONG-TERM SAVINGS PIG!

Roughly speaking, the con artists at Friends Provident, Generali, Zurich, Hansard and RL360 structure these products so that for every two pounds saved, one pound goes to the life office and the spiv who sold the plan to the victim in the first place.

The adviser earns a packet by selling these useless plans and few victims continue saving for more than a few years – long before the end of the term. Pretty quickly, the con artists’ clients realise they’ve been scammed and that they’ve inadvertently signed up to an expensive, unworkable plan with no flexibility. They really would have been better off sticking their money under the mattress.

So here’s my suggested alternative: the LONG-TERM SAVINGS PIG:

You see, the problem with most long-term savings plans is that you are locked in and there is no flexibility. Plus there are heavy penalties and half of what you save goes in fees and commissions.

Imagine being able to save what you want, when you want, for free! All you have to do is be strict with yourself and save as much as you can, regularly and generously.

The problem is, of course, that so many offshore advisory firms sell products – rather than provide advice. Advisers earn huge commissions from mis-selling these appalling long-term savings plans – and ruin their clients in the process.

After as little as a year or two, the victims realise they’ve been conned and that they are simply pouring their hard-earned money into the pockets of the adviser and the life office.

In a perfect world, these dreadful products should be banned. All the advisers who have conned so many victims into believing they are paying into a flexible plan which is good value for money should be prohibited from ever working in financial services again. And the rogue life offices should be brought to justice and made to refund the victims’ money.

The reasons why these savings products don’t work are:

Few people can guarantee they will be able to save the contracted amount each month for the agreed period. People’s earnings do fluctuate and circumstances change.

Few people actually realise what they are signing up to. The advisers don’t tell them how expensive and inflexible the plans are.

Few people understand that half of what they save will be eaten up by fees and commissions.

Most people who get conned into these plans end up abandoning them and writing off what they have lost.

Remember, it’s your money and your life. Don’t get conned into giving half your savings to the scammer and the life office.

Just to make things crystal clear, if you sign up to a 25-year savings plan with one of the leading life offices, you will pay the following amount of fees over the life of the plan:

46.64% Friends Provident Premier 47.80% Generali Vision 48.07% Zurich Vista 51.28% Hansard Vantage 51.68% RL360 Quantum

So, if you save a total of £366,600 over 25 years with RL360, you will pay them (and your adviser) £189,460 in fees and commissions.

Integrated Capabilities – a Trust Company based in Malta have created their own Pension Scheme – Azure Pensions. On the face of it, however, the management team do not appear to have learned anything from their previous experience with Optimus Retirement Benefit Scheme No.1 and their association with David Vilka of Square Mile International Financial. It appears they have now teamed up with some very dubious friends – the result of which is very likely to create more victims of UK pension scams.

I AM GRATEFUL TO STEVE – ONE OF THE BLACKMORE GLOBAL/DAVID VILKA VICTIMS – FOR RE-WRITING THIS BLOG AT THE REQUEST OF INTEGRATED CAPABILITIES’ LAWYER.

The Azure website states: “We believe that trust is built and earned. As such we have an ingrained and sustained desire to develop long-term relationships with our clients”. These are just words and words are easy. It’s what you do that counts.

In 2015, the Optimus scheme started out with 26 members and by the end finished up with 1,176 – that’s a gain of almost 100 new members per month! I was one such member conned into transferring my pension by fraudulent misrepresentations made by David Vilka of Square Mile Financial Services.

This new pension arrangement locked me in for 10 years – definitely a “long-term relationship” – giving all parties the opportunity to drain my pension dry in fees. Credit where credit is due, however. Once I discovered I was in a scam, the director Andy Dawson (bottom row, 3rd from the left) did make an extraordinary effort not only to redeem the investments but successfully persuaded most parties to waive their early exit penalties and refund their fees. Only the greedy Symphony Fund chose to keep the penalties and that’s after mysteriously dropping in value 30% just before redemption. Thanks to Andy Dawson and his team, I did manage to get back 92% of my pension. But the BIG QUESTION is what has happened to the other 1,100+ members? It is inconceivable I was the only one transferred into this scheme via Vilka et al.

Another claim made by Azure Pensions is: “Our people are highly experienced, knowledgeable and motivated to do their utmost to ensure that they deliver a superior, professional and hassle-free service.” But this firm, and the people in it, have a history of working with scammers and investing members’ retirement funds in investment scams such as Phillip Nunn’s Blackmore Global and Richard Reinert’s Symphony Fund. So I would take issue with claims like “highly experienced” and “knowledgeable”.

If they were highly experienced and knowledgeable they would have known that, at the time I was being advised by Vilka in January 2015, Aktiva Wealth Management (later changed to Square Mile and now called Michalska Holding) was NOT regulated by the Czech National Bank. According to the CNB records, this didn’t happen until 5th May 2015 and then, only for insurance mediation and not for transferring pensions!

If Integrated Capabilities had been “highly experienced and knowledgeable” then they would have known the Symphony Fund – regulated in their own jurisdiction by their own regulator, the MFSA – was NOT permitted to be offered to me, a retail client. And they knew this because they had the Symphony documentation which clearly prohibited its promotion to UK retail clients.

I complained to the MFSA but they didn’t care and Malta’s “Ombudsman” equivalent – what they call the Office of the Arbiter for Financial Services – deters complaints because they have this small print that says if you lose, the other side can be awarded legal costs!

If Integrated Capabilities had been “highly experienced and knowledgeable” they would have known the Blackmore Global fund had never published audited accounts and still hasn’t to this day (December 2018). Something that in January 2015 caused Kreston (pension provider on the Isle of Man) to write to its members explaining their concerns over Blackmore Global and also stopped taking new members from Vilka.

So if they were “highly experienced and knowledgeable” then why did they allow all this to happen? It certainly had nothing to do with “motivation to do their utmost”. It is clear their only motivation was to take on as many members as possible – irrespective of which scammer introduced them and what unsuitable investments were made for them. Also, they claim to have a “long history and proven track record of providing expert and value for money multi-jurisdictional fiduciary solutions, so our clients and partners can have great peace of mind in the knowledge that our board of directors has over 100 years combined expertise in this field.” The proven track record is that they have taken on hundreds of new members per month from a known scammer – and the last thing their members have is peace of mind – far from it.

Angie has referred to these people at Integrated Capabilities/Azure Pensions as a “bunch of cowboys” and their lawyer recently wrote to her and objected to the phrase. You make your own mind up.

How do they earn trust when they have accepted transfers and investment instructions from known unregulated scammers Square Mile and David Vilka? Why would victims “desire” to have a long-term relationship with Azure when funds were previously placed in an unnecessary, expensive insurance bond by Investors Trust in the Cayman Islands (the only purpose for which is to pay commission to the scammers)?

Azure Pensions also claims that one of its partners is Carey Pensions UK LLC. Carey is facing a legal battle for investing a member into unregulated collectives in Australia through a Carey Pensions SIPP.

Carey is in hot water for allowing investments into high-risk scams, and is also now part of STM – undoubtedly the biggest scammers in the offshore pension trust industry. It would seem the Azure team have not learned anything from their previous experience.

If, as they say “We believe that trust is built and earned …”, then you actually have to do some “trust building” with actions – not just weasel words. The indisputable facts seem to indicate “business as usual” but with a different name.

It is highly probable that Integrated Capabilities still has at least 1,100 victims invested in scam funds such as Blackmore Global by scammers such as David Vilka of Square Mile. It looks like most – if not all – of these victims were UK residents who should never have gone into a QROPS at all in the first place. The only reason for transferring these pension funds to a QROPS was to get the money away from UK regulation so that the scammers could invest them in commission-paying UCIS funds – such as Blackmore Global.

The public should be very wary of Azure in the first instance, do a lot of due diligence and make sure their pension funds don’t go anywhere near offshore unregulated collectives wrapped in an assurance bond that can suck your pension dry.

Azure states on their website that: “Notwithstanding your appointment of a Financial Adviser, ICML has an overriding right to refuse to make investments, or to disinvest, where it believes that a particular investment proposal may not be consistent with the Scheme’s Investment Policy or any investment restriction applicable under Retirement Scheme Law.”

Is this a change in policy? Are they going to put their “knowledge and experience” to meaningful use by exercising some due diligence? Is this a statement that means they have sorted the 1,100+ members in the Optimus Scheme that are most likely locked into “investments … not consistent with the Scheme’s … Policy?” Or are these just more weasel words with no substance?

Reformed management team or a “bunch of cowboys”? The jury is still out. The association with Carey & STM doesn’t appear to show a reformed team. What has happened to the 1,100+ members in the previous Optimus Scheme? Has anything been done to remedy the situation?

I believed, and still do, that this team was unwittingly drawn into facilitating a scam by David Vilka of Square Mile, and that in essence Integrated Capabilities/Azure Pensions are a respectable team. However, if they want to be seen as having learned from their past failings they could take some actions. First, help the 1,100+ members to avoid financial ruin and secondly assist in the prosecution of the architects of the scam facilitated by Integrated Capabilities. I am sure they will have a considerable body of evidence that could be used to show fraudulent misrepresentation and thirdly drop the association with companies with an already poor reputation for their involvement with scams or unregulated collectives being promoted to retail clients.

TPR has been neither coy nor shy in its published determination against Ward and Salih – and has openly called the London Quantum pension scheme, and the risky investments which Ward made, a “scam”.

But to any reasonable person’s mind, tPR’s determination in relation to Ward and London Quantum raises more questions than it answers. In fact, I would go even further and say that HMRC’s and tPR’s incompetence – as well as Dalriada Trustees‘ own failings – should be examined in parallel with Ward’s multiple frauds.

Because, make no mistake, London Quantum was only one of many.

It all started long before the Ark Pensions scam. Ward set out his stall transferring pensions to New Zealand and liberating 100% “tax free”. He boasted in the local Costa Blanca press that he had “helped” thousands of clients liberate their pensions (legally). Of course, this may have been free of tax in New Zealand, but when the Spanish tax authorities catch up with these clients, there will be a very expensive disaster.

It is extremely worrying that IVCM – a “phoenix” of the Brooklands disaster – is also offering the same New Zealand liberation facility today. It always worries me when firms fail to learn the lessons of past scams and expose unsuspecting victims to the same catastrophes that past scammers orchestrated. Add to this the fact that IVCM is regulated out of Gibraltar – the jurisdiction of choice for scammers such as XXXX XXXX and STM Fidecs – and I think it is well worth giving IVCM a very wide berth.

Prior to 2010, Ward was a tied agent of Inter Alliance – a company based in Cyprus which had an insurance license. For Inter Alliance in Cyprus, Ward successfully created the illusion that this gave his company Premier Pension Solutions some sort of license. But, in reality, it did not – as the Cyprus license was only for Inter Alliance and not for any other entity. Plus tied agents were (and still are) illegal in Spain.

As a sideline, Ward was flogging EEA Life Settlements as he had discovered the delights of making huge commissions out of dodgy, risky, illiquid investments to his unsuspecting victims. In 2010, Ward was working closely with Concept Trustees in Guernsey – run by Roger Berry. Initially happy to see Concept Trustees’ QROPS members have 100% of their pensions invested by Ward in EEA, Berry eventually realised that Ward’s firm was not regulated as it had been dumped by Inter Alliance. Of course, even before it had been dumped, Premier Pension Solutions wasn’t regulated anyway. But Concept Trustees was too stupid to realise that.

Concept then wrote to all the members who were clients of Ward’s Premier Pension Solutions and warned them that Ward’s firm was neither regulated nor had any professional indemnity insurance cover. Berry claimed he would not be accepting any further investment instructions from Ward, but this was basically just a load of hot air (aka lying) as he continued to accept investment instructions into EEA by Ward.

In September 2010, Premier Pension Solutions was appointed as a tied agent of AES International – a firm based in London and Dubai. The agency agreement covered PPS for investment and insurance business – but not pension transfer business. Ward’s PPS letterheaded paper claimed that it was a “partner” of AES and that it was regulated by the DGS (Spanish insurance regulator) and CNMV (Spanish investment regulator). PPS also became a member of FEIFA – the Federation of European Independent Financial Advisers (although he was later dumped by them). You can understand why so many victims thought that PPS was a bona fide advisory firm.

Then came the first of Ward’s major pension scams: Ark. It is worth looking at the history of Ark because this sets the scene for how nearly 500 victims came to lose their pensions and face tax liabilities – as well as the dozens of further scams operated by Ward (including London Quantum).

A famous footballer and his mate – a football club owner – bought a plot of land in Larnaca in Cyprus with a view to turning it into a golf resort. They paid £1.1 million for the property, but then realised it wasn’t big enough for a whole golf course (neither of them was bright enough to be able to count up to 18) and so they tried to find some other investors. The chumps they tried to con into buying more land adjacent to the original plot either couldn’t come up with the money or were frightened off such a high-risk, illiquid investment.

So the sporty pair went to see the footballer’s accountant – Andrew Isles of Isles and Storer (now owned by LB Group). Isles soothed the sporty pair’s worries by telling them that securing more investors was simple: just start a pension fund! He introduced them to what he called “two leading pension experts”: Craig Tweedley and Stephen Ward. Tweedley was already operating the KJK Investments/G Loans pension liberation scam (later to be placed in the hands of Dalriada Trustees by the Pensions Regulator) and Ward was a highly-qualified pensions expert, examiner and author.

The rest is history as nearly 500 victims lost their pensions to the Ark scam. But the sporty pair did very nicely – they sold the land in Cyprus to the Ark scheme for £4 million and pocketed the profit. The footballer tried to hide the money in Dubai but got caught and turned Queens Evidence. He and the other original investor (the football club owner) fell out and they ended up in court against each other – with the footballer triumphing. Andrew Isles also did very nicely as he sold introductions to a number of his clients and earned fat commissions in doing so.

As Ark unfolded – between mid 2010 and mid 2011 – Ward initially acted as an introducer. There were various introducers – many recruited by Ward when he ran a series of seminars in various parts of the UK. But Ward himself was the biggest introducer – accounting for more than a third of the whole £27 million fund and earning approaching three quarters of a million pounds in fees (the Pensions Regulator’s report of £350k was way off the mark).

Ward and his sidekick – bent lawyer Alan Fowler of Stevens and Bolton Solicitors – acted as the controlling minds behind Ark. The scheme documentation and the “loan” contracts were drawn up and explained by Ward and Fowler. Of the 5% commission charged by Craig Tweedley, Ward got at least 2% plus a transfer fee. But Ward had his eye on a much bigger proportion of the fees. Towards the end of the life of Ark, Ward was preparing to take Ark over from Tweedley – along with an associate of his: Peter Moat (another pension crook who went on to operate the Fast Pensions scam – now also in the hands of Dalriada Trustees). In a way, it was a shame that didn’t happen, as Tweedley did at least try to help the Ark victims, whereas Ward never lifted a finger. In fact, he simply told the Ark victims to throw the tax demands away as “HMRC would never pursue them”.

In February 2011, HMRC met with Tweedley and Ward to discuss the “loans” – so HMRC knew perfectly well that Ward was the main brain behind the scam. It is, therefore, astonishing that they did nothing to stop him operating so many further pension scams.

Ark came to a shuddering halt on 31st May 2011, when tPR appointed Dalriada Trustees and the scheme was suspended. Dalriada went up to Yorkshire to confront Crag Tweedley and relieve him of all the evidence and files relating to the scam. Tweedley told Dalriada that all the records were held down at Ward’s Manchester office at 31, Memorial Road and he drove down to collect them from Anthony Salih. He arrived to find Salih removing all the Premier Pension Solutions fee agreements on the instructions of Ward (he managed to shred most of them – but did missed a few which I now have).

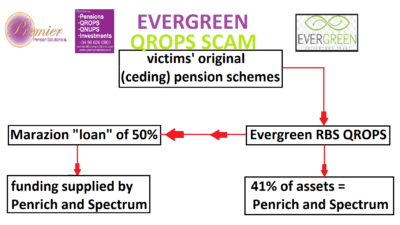

After Ark, Ward went on to run the Evergreen Retirement Benefits QROPS scam with accompanying 50% “loans” and a further 300 victims lost £10 million worth of pensions. HMRC removed Evergreen from the QROPS list when they realised it was a liberation scam and Ward fell back on two more UK-based, bogus occupational schemes: Southlands and Headforte. Plus, he registered a number of new schemes – including Capita Oak.

The Capita Oak scheme was another bogus occupational scheme registered by Ward with a fictitious sponsoring employer: RP Medplant (Cyprus). There is, however, a firm called RP Med Plant in Cyprus. The Capita Oak trust deed was written by Ward’s bent lawyer Alan Fowler. Ward took responsibility for the transfer administration – transferring valuable personal and final salary occupational pensions into this scam – in the full knowledge that he was condemning hundreds of victims to certain financial ruin and poverty in retirement. Capita Oak is now also in the hands of Dalriada Trustees.

Other pension scams that Ward was operating – in addition to Southlands and Headforte – from 2012 onwards included Feldspar, Hammerley, Meribel, Halkin, Randwick, Bollington Wood and Westminster. And, of course, Dorrixo Alliance which was the trustee for many of these scams. Capita Oak and Westminster are both under investigation by the Serious Fraud Office.

How much more evidence do they need?

In May 2014, HMRC was given evidence of all of Ward’s various scams – including Dorrixo Alliance. They were also given detailed testimony by me and a number of victims of what Ward had been up to in the pension liberation fraud industry since Ark. It would have been very easy for HMRC to look up to see what other pension schemes Dorrixo was trustee to. Had they done this, they would have seen that Dorrixo was the trustee for the London Quantum scheme. If HMRC had taken any action, they could have prevented Mr. N – a serving police officer – and 96 other victims from losing their pensions to Ward and his various dodgy, inappropriate investments (including loans to Dolphin Trust).

If we add to the above catalogue of scams the Continental Wealth Management scam – 1,000 victims facing the loss of £100 million worth of life savings – Ward has been responsible for the destruction of thousands of people’s pensions this past eight years. Plus several suicides and deaths from stress-related medical conditions.

SERIOUS QUESTIONS ARISING FROM THE PENSIONS REGULATOR’S DETERMINATION RE:

Mr Stephen Alexander Ward – The Pensions Regulator case ref: C46205159

Ward was a director of Dorrixo from 13 October 2011 to 28 April 2015. A company called Quantum Investment Management Solutions LLP (“QIMS”) has at all material times been the sole sponsoring employer of the Scheme. Dorrixo became the sole trustee of the Scheme on 19 April 2014. Dorrixo is also recorded as being the Scheme administrator.

HMRC AND TPR WERE GIVEN EVIDENCE OF WARD’S COMPANY, DORRIXO, IN MAY 2014. THEY WERE ALSO GIVEN EVIDENCE OF A LARGE NUMBER OF SCAMS WARD OPERATED AFTER ARK – ALL INVOLVING LIBERATION FRAUD. WHY WASN’T ACTION TAKEN TO PREVENT LONDON QUANTUM? ALL 97 VICTIMS – INCLUDING A SERVING POLICE OFFICER – COULD HAVE BEEN PREVENTED.

On 18 June 2015 the Regulator appointed Dalriada Trustees Limited (“Dalriada”) as an independent trustee to the Scheme, with exclusive powers.

HAS ONE SINGLE PENNY EVER BEEN RETURNED TO ANY OF THE PENSION SCAMS PLACED IN THE HANDS OF DALRIADA TRUSTEES? THERE ARE DOZENS OF THEM, AND FEW – IF ANY – OTHER INDEPENDENT TRUSTEES ARE EVER APPOINTED BY TPR. BUT THERE SEEMS TO BE NO RECORD OF ONE SINGLE MEMBER EVER GETTING ANY RETURN FROM ANY OF THE SCHEMES IN THE PAST EIGHT YEARS – DESPITE THE MANY MILLIONS DALRIADA HAVE PAID THEMSELVES FROM THESE SCHEMES.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

AS THIS EVIDENCES THAT THIS SCAM COULD EASILY HAVE DWARFED ARK IN A VERY SHORT SPACE OF TIME, DON’T HMRC AND TPR RECOGNISE THAT THEIR LAZINESS AND NEGLIGENCE NEED TO BE ADDRESSED? THEY LEARNED NOTHING FROM ARK – AND WHILE THERE ARE VALID CRITICISMS OF WARD FOR HAVING LEARNED NOTHING, HE IS JUST A COMMON SPIV WHILE HMRC AND TPR ARE SUPPOSED TO BE GOVERNMENT DEPARTMENTS WITH A RESPONSIBILITY TO PROTECT THE PUBLIC. THE SCALE OF THIS SCAM SHOWS THESE TWO ORGANISATIONS ARE NOTHING BUT HOPELESSLY INEPT AND AMATEURISH IN THEIR APPROACH TO DILIGENCE AND PUBLIC RESPONSIBILITY.

The Scheme was promoted to potential new members by introducers. These included the following entities: GoBMV; Baird Dunbar; What Partnership; the Resort Group PLC; Friendly Investments; Premier Mark Consultants and Quantum Wealth Management Solutions Limited.

THE DANGERS OF THE SCOURGE OF “INTRODUCERS” SHOULD HAVE BEEN LEARNED FROM THE ARK SCAM IN 2011. WARD RECRUITED DOZENS OF THEM ALL OVER THE COUNTRY. AND YET NONE OF THEM HAS EVER BEEN BROUGHT TO JUSTICE FOR THEIR PART IN ARK, AND HAVE GONE ON TO OPERATE AS INTRODUCERS AND EVEN HOLD KEY CENTRAL ROLES IN LATER SCAMS. THIS INCLUDES FRIENDLY INVESTMENTS AND JULIAN HANSON – WHOSE SCHEMES ARE NOW ALSO IN THE HANDS OF DALRIADA TRUSTEES.

Gerard was responsible for producing template risk letters, member application forms, pro forma declarations stating that the person signing them was a self-certified sophisticated investor, member booklets and the statement of investment principles (of which there were four versions). Gerard sent these documents to members once they had been introduced to the Scheme by an introducer.

GERARD ASSOCIATES, RUN BY GARY BARLOW, HAD ACTED AS AN INTRODUCER TO WARD IN THE ARK SCAM. AND YET HE WAS LEFT FREE TO OPERATE IN THE SAME CAPACITY IN THE LONDON QUANTUM SCAM – AND EVEN TAKE ON A MORE CENTRAL ROLE. GERARD ASSOCIATES WAS AT THE TIME AN FCA-REGULATED FIRM – AND REMAINS SO TO THIS DAY. THE FCA HAS TAKEN NO ACTION TO REMOVE THIS FIRM OR TAKE ANY ACTION AGAINST GARY BARLOW.

GERARD ASSOCIATES’ GARY BARLOW WAS PAID £253,000 FROM THE LONDON QUANTUM SCHEME FOR DEFRAUDING VICTIMS INTO SIGNING AGREEMENTS THAT THEY WERE “SOPHISTICATED” INVESTORS. SO WHY HASN’T BARLOW BEEN PROSECUTED AND JAILED – AND MADE TO PAY THIS MONEY BACK TO THE VICTIMS?

A material number of the new members had a low or medium appetite for investment risk and, in any event, were unaware that the Scheme’s investments were high-risk investments. The Panel was troubled by the apparent disconnect between members’ appetite for risk and the high risk nature of the investments made by Dorrixo. Mr Ward accepted that the Scheme’s investments were high risk, but claimed this was made clear to new members in the Member Booklet.

I DON’T KNOW WHAT SORT OF DRUNKEN DUMMIES MADE UP TPR’S “PANEL”, BUT DID THEY SERIOUSLY THINK THAT ANY PENSION FUNDS SHOULD EVER INVEST IN HIGH-RISK CRAP? INDIVIDUAL MEMBERS’ APPETITE FOR INVESTMENT RISK IS IRRELEVANT – THIS WAS A PENSION FUND, NOT A CASINO.

The case against Ward was based on failures of competence and capability, and also a lack of honesty and integrity as well as Ward’s involvement with “pension liberation” as an introducer of members to the “Ark” schemes.

BUT TPR AND HMRC KNEW ALL ABOUT THIS BACK IN 2010 AND 2011. WHY DID THEY DO NOTHING TO PREVENT WARD FROM SCAMMING MORE VICTIMS OUT OF MORE MILLIONS OF POUNDS. THEY STOOD BACK AND WATCHED – DESPITE HAVING HARD EVIDENCE THAT HE WAS STILL UP TO HIS CRIMINAL MISCHIEF.

Mr Ward did not dispute that a company of his (Premier Pensions Solutions SL) was involved in introducing members to the Ark Schemes, but states that the relevant activity pre-dated any finding by the courts of pensions liberation and that Mr Ward had no knowledge that the schemes were being used for such activity.

BUT HMRC, TPR AND DALRIADA ALL KNOW THIS ISN’T TRUE. THEY HAVE ALL SEEN EVIDENCE THAT WARD AND HIS BENT LAWYER ALAN FOWLER ACTUALLY PRODUCED THE “LOAN” (MPVA) DOCUMENTATION AND EXPLAINED THE LOANS IN SOME CONSIDERABLE DETAIL TO THE VICTIMS. THE MPVA CONTRACTS WERE DRAWN UP BY FOWLER. IS IT REALLY CREDIBLE THAT NEITHER HMRC NOR TPR WOULD HAVE OBJECTED TO THIS STATEMENT?

The Panel did not consider there was sufficient evidence of Ward having actual knowledge of, or turning a blind eye to, the illegal nature of the activity of the Ark Schemes when carrying out his role as introducer before.

SERIOUSLY? I HAVE GIVEN EVIDENCE OF THIS TO BOTH HMRC AND TPR ON MANY OCCASIONS. THIS HAS BEEN DISCUSSED AT MEETINGS WITH DALRIADA TRUSTEES ON MANY OCCASIONS. EVIDENCE OF THIS HAS BEEN GIVEN TO THE SERIOUS FRAUD OFFICE ON MANY OCCASIONS BY VARIOUS VICTIMS AND ME. WHAT FURTHER EVIDENCE DID THE PANEL WANT? EVERY ARK MEMBER’S FILE WAS FULL OF SUCH EVIDENCE. EITHER TPR IS LYING OR IT IS INCOMPETENT. OR BOTH.

The Case Team also relied on certain alleged failures in relation to other pension schemes (called Headforte and Halkin), of which Mr Ward was a trustee. These are denied by him (e.g. an allegation of failure to appoint an auditor to those schemes) and the Panel did not consider it necessary to make findings in respect of them.

SO WHAT ACTION HAS TPR TAKEN IN RELATION TO HEADFORTE AND HALKIN? BOTH WERE BEING USED FOR PENSION LIBERATION FRAUD BY WARD – AND YET THE VICTIMS PROBABLY STILL HAVE NO IDEA WHAT HAS HAPPENED TO THEIR MONEY. IT IS ABSOLUTELY ASTONISHING THAT NO ACTION HAS BEEN TAKEN IN RELATION TO THESE TWO SCHEMES, PLUS ALL THE OTHERS WARD HAS BEEN OPERATING OVER THE YEARS.

Stephen Alexander Ward (date of birth 11 July 1955) is hereby prohibited from being a trustee of trust schemes in general. This order has the effect of removing the above-named individual from all or any schemes of which he is a trustee. By section 6 of the Pensions Act 1995, any person who purports to act as a trustee of a trust scheme whilst prohibited under section 3 is guilty of an offence and liable (a) on summary conviction to a fine not exceeding the statutory maximum, and (b) on conviction on indictment to a fine or imprisonment or both.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

THIS IS NOT JUST THE DEATH OF TRUST, BUT OF ANY CONFIDENCE IN THE GOVERNMENT, REGULATORS AND CRIME PREVENTION AGENCIES TO PREVENT OR DEAL WITH PENSION SCAMS AND SCAMMERS.

Tackling Caravan Crime – Chancellor Philip Hammond. Victims of pension fraud in scams such as Ark, Capita Oak, Westminster, London Quantum, Friendly Pensions and Salmon Enterprises – will not be surprised to hear that even the Crown Prosecution Service acknowledges that the fraudsters have defeated the system. Alison Saunders, head of the CPS, has stated publicly that the British justice system can’t cope. She is stepping down and is clearly disheartened by Britain’s failure to tackle crime – especially fraud. She has vented her frustration in an interview:

But look hard enough, and you will see how tackling crime can be done successfully. As someone who constantly writes about the failure of our police and courts to bring criminals to justice, I was surprised to hear of a spectacular success story in leafy Surrey recently.

Mr. and Mrs. Shore of Thorpe, in Surrey, were successfully prosecuted and jailed for proceeds of crime. Residing in Runnymede Borough Council – presided over by Chancellor Phillip Hammond – this dastardly pair (in their sixties) were both sent down for a heinous crime under the Proceeds of Crime Act 2002 (“POCA”).

After many years of detailed investigation, the successful prosecution will send out a resounding warning to all such criminals and will no doubt discourage others from profiting from the same hideous crimes. And the crime was…….?

Housing homeless families in caravans without planning consent.

Let that sink in for a moment – vulnerable people with young children who had a choice between living on the streets or living in a caravan. And this crime was committed in Runnymede Borough where there was insufficient housing for the many poor families who could not afford private accommodation and had not been offered council homes.

This spectacular success story on the part of Hammond, Runnymede Borough Council and the CPS has left the good citizens of Surrey relieved that these dangerous caravan owners are now behind bars and dozens of homeless families are now living on the streets. Jobdone; justice served; well done Cutty Sark!

Hailing from Surrey myself, I am pleased that the county will now be a safer place. The successful prosecution was in respect of 14 breaches of six enforcement notices issued since 1999 by Runnymede Borough Council, following a seven-day trial at Guildford Crown Court. The jury heard how the farm owners had not only stationed the caravans on their own land, but had also failed to demolish a shower room. Unbelievable!

Hammond must be strutting the halls of Westminster bursting with pride and patrolling the fields of Runnymede with a sense of upholding the social and civil justice with which King John would have been delighted. In the House of Commons bar, Chancellor Hammond is probably boasting that there is a reason why he is named after a large organ. In fact, after his spectacular success with the Shores’ caravans, he will probably go down in history as “Caravan Willy” for presiding over such a coup.

I am sure that the many thousands of people who have lost millions of pounds’ worth of life savings to scammers such as Stephen Ward, Julian Hanson, George Frost, XXXX XXXX, Phillip Nunn, Patrick McCreesh, Stuart Chapman-Clarke, David Vilka, David Austin, Darren Kirby, Dean Stogsdill, Anthony Downs and James Lau will now understand why the CPS couldn’t dedicate any resources to prosecuting them. And they will, no doubt, be glad that the priority of the judiciary was removing unauthorised caravans in Surrey.

As in most of my blogs, there is an important postscript: Caravan Willy is a keen property owner and is reported to be worth over £9 million. The Shores’ land has now been confiscated by Runnymede Borough Council. And it is worth at least £27 million once planning permission for a housing estate is granted. I wonder who will be lucky enough to scoop that one up?………

Sadly, Spain – the leading British expat destination in Europe – is rife with scams and scammers. The Costa Blanca, Costa del Sol, Costa Brava and everything in between are crawling with what the Spanish regulator calls “chiringuitos” – literally “bar flies”. And you can see why: wherever there is food – whether fresh or rotting – they congregate in large swarms. They are not proud – they will nibble your chips while still on your fork; sip your sangria off your straw; suck the sweat off your shirt and crawl into your underpants to see if there is anything tasty in there.

At least the flies have a little more dignity and respect.

Becoming an expat in Spain is fraught with difficulty. First, you have to learn to drive on the wrong side of the road, then you have to learn Spanish – or Valenciano or Catalan (you can see why so few Brits bother). Then you have to come to terms with the heat: long, hot summers with temperatures well up into the 30s and 40s are fine if all you have to do is lounge beside the pool, drink beer and plan your next outing to the local chippy. But if you are working, being too hot all day is no fun.

Many Brits are naturally suspicious of the Spanish and seek out British professionals whenever they can: builders, plumbers, pool maintainers, car mechanics and manicurists. And you can understand why – most Brits can barely manage things like “my loo won’t flush”, “the pool’s turned green”, “our car won’t start (or stop)” and “I want nails like Kim Kardashian”. So when it comes to “how do I invest my life savings” they don’t really stand a chance.

The problem is that most Brits in Spain are outside their comfort zone. They are in a foreign country and so they cosy up to other Brits because that makes them feel safe – and they don’t quite trust the natives anyway. Quite apart from the language barrier, Spanish bureaucracy can seem somewhat intimidating and, well, foreign. So when it comes to managing their life savings and retirement provisions, the Brits either actively seek out British advisory firms or feel relieved and happy when they are cold-called by them.

There’s no shortage of “advisers” – they lurk everywhere: bars, supermarkets, golf and sailing clubs. They are typically charming, well-dressed, friendly and fall over themselves to sell financial advice or what they call “wealth management”. Only that isn’t what they are selling: they are actually selling products. These products are basically insurance bonds (that you don’t need) and investments (that you don’t want). And huge fees for selling you things that you neither need nor want.

With appealing adverts and websites showing happy, good-looking couples with nice teeth, expensive yachts and fast cars. These chiringuitos sell the idea that somehow they can make people wealthy and happy in retirement.

The reality is that the chiringuitos make themselves rich by fleecing their victims and destroying their funds.

Before the industry cries “unfair, unfair!!”, let me just mention a couple of examples that prove my point:

Premier Pension Solutions (Costa Blanca) – Ark £27 million; Evergreen £10 million; Capita Oak £10 million; London Quantum £3 million

Continental Wealth Management (Costa Blanca) – £100 million

That’s at least a couple of thousand people financially ruined. There are plenty more examples:

There’s quite a wide spectrum – ranging from out and out scammers like Premier Pension Solutions and Continental Wealth Management, to firms that are just plain dodgy, expensive, dishonest and irresponsible. You may ask what the difference is: in practice NONE. Both ends of the spectrum cause damage to the funds – and distress to the victims.

Let’s look at the reality and examine what many advisory firms (chiringuitos) do and don’t do. We will take the don’ts first:

they don’t disclose all the fees up front

they don’t disclose how much commission they will earn from your funds

they don’t respect your risk profile – and can invest you in high-risk stuff when you are a low-risk investor

they don’t tell you when the answer to the question “do I need a QROPS” is “no”

they don’t respect the basic principles of diversity, risk, liquidity and cost

they don’t disclose whether the firm is regulated

they don’t disclose whether they are qualified

and now what they do:

they transfer your pension into a QROPS whether that is in your interests or not

they put your funds into an insurance bond even though you don’t need one

they invest you in what they have already decided they want to sell you – irrespective of whether that is what you need

they churn your investments to maximise their commissions

they lie about your losses (only “paper” losses)

they stick you in an expensive insurance bond which will cost you a fortune to get out of

There are, of course, multiple variations on this theme – including things like flogging you whatever fund pays them the most commission that month; flogging you their own fund; flogging you your own grandmother – twice. They flog funds with entry fees, exit fees, ongoing fees and lousy performance. Basically, these advisers have no interest in keeping their clients long term – they are only interested in the initial fees. Once the client realised they have been fleeced, he can take his business elsewhere – unless the firm is Blevins Franks, in which case the victim is stuck with them.

I am often asked the question: “are there any firms you can recommend which won’t rip me off?”. The answer to this question is a resounding “maybe”.

There are a few I can categorically recommend against:

Watch out – Blevins Franks will probably sell you a pup if you’re not careful!

Blevins Franks – a so-called financial advisory firm in Spain and other places around the Med – might (hopefully) offer me a job. I quite fancy trying my hand at being a financial adviser, so I’m practicing cheesy smiles and earnest but friendly poses. Over the weekend I’m going to rehearse some elevator pitches and killer closing offers for my interview with Blevins Franks:

“Any fund you like – as long as its a Russell fund”

“Shall I Russell up some coffee while you browse through our catalog of funds (it won’t take you long – we only sell one fund!)”

“Autumn is my favourite time of year – I just love the Russell of fallen leaves”

“I adore your Jack Russell (the one that slobbered on my new trousers) – I might just Russell him on my way out”

While I’m on a roll, I might try a real joke or two:

“What do you call a man under a pile of leaves? Russell! What do you call a man under a pile of leaves for a thousand years? Pete!”

(I just hope my prospective clients aren’t called Russell and Pete).

I’m sure I’ll be able to think up plenty more jolly quips, and I reckon I’ll soon have dozens of potential clients eating out of my hand and desperate for the chance to invest their life savings in Russell funds. The only thing I’m not sure of, is how to sell them on the concept of going into a Lombard bond. What do I say the benefits are? Of course, I know what the benefits are to me: I will earn 8% commission – but what line do I spin the client?

* It will give you capital protection (by protecting your capital from growing too fat)

* It will give you the best and widest selection of funds (as long as they start with a Rus and end with a Sell)

* It will help reduce the appearance of wrinkles and fine lines (and growth)

* It will pay me lots of commission (oops – better not say that!)

I’m going to do some homework before my interview so I know the Russell funds inside out – so over to good ol’ Morningstar.

Let’s start with the Russell Real Assets Fund. I won’t mention that it is down 3.8% this year (2018) or that it is performing way below the benchmark, but I will stress that this fund is a bargain at just 3% to buy into and a mere 2.01% a year ongoing. (Probably best not to mention that if somebody bought it direct they could get it for free and pay only 1.26% a year).

Then I’ll move on to the Russell Openworld Global High Dividend Equity Fund (better stay sober to get that one right) – a steal at only 5% to buy into and 2.02% a year once you’re in. Then, just to show I know what I’m talking about, I’ll give ’em the killer Russell Asia Pacific Ex Japan Fund – another steal at 5% to get in, and 2.8 a year to stay in. I won’t mention that both these funds are half the price if you buy them direct – because this is after all about my commission and not about trying to sell them something cheap or suitable.

If I really want to impress my prospective victims, I could go on and on: “Russell Emerging Markets Equity Fund, Russel US Equity Fund, Russell Global Real Estate Securities Fund….”. I could even invent some of my own: “Russell Falling Leaves Fund, Russell Falling Value Fund, Russell Falling For It Fund…”

The best thing about working for Blevins Franks, of course, is that you get paid twice: once for flogging the Lombard bond, and then again for flogging the Russell fund – a “double hussle” (or even a “Russell hussle”!). I can’t wait.

But what, you may ask, if Russell and Pete suss out that I’ve conned them after they see their funds stuck in this useless, pointless, expensive bond and realise they could have bought the Russell funds way cheaper elsewhere – or could have just bought better funds to start with? The answer is simple – just listen to my favourite song: Hotel California by The Eagles: “You can check out any time, but you can never leave”.

You see, clients in Spain don’t realise that when they get conned into a Lombard Insurance Bond they have to stay with Blevins Franks no matter how badly the funds inside the bond perform? No other IFA in Spain is allowed to take over managing the funds if an investor is not satisfied with Blevins Franks. So Russell and Pete will be stuck with me forever – unless they fancy paying a huge exit penalty (so it will cost them a fortune to get rid of me!).

Never mind treating customers fairly – we’ll lock them into a cripplingly-expensive insurance bond which is illegal in Spain and fleece them with expensive, poor-performing funds they could buy way cheaper anywhere else. And Russell and Pete can do nothing about it.

In the words of the best band in the world: “On a dark desert highway, cool wind in my hair, I was thinking to myself this could be heaven and this could be hell, such a lovely place to listen to the Russell of crumpled pound notes….”

Just goes to show, even with a load of qualified advisers, victims can still get scammed.

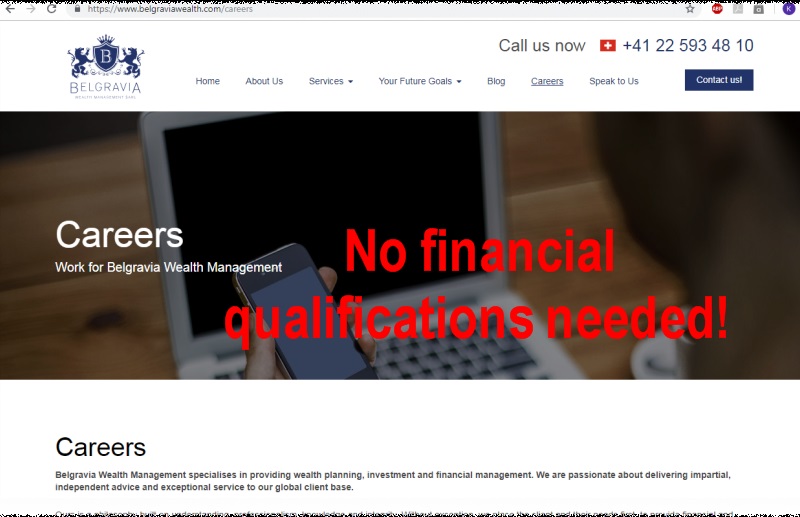

Back due to popular demand, qualified and registered company blogs. Today, I am looking into Belgravia Wealth, a Swiss based company. Belgravia Wealth – qualified and registered? Lets see if you are.

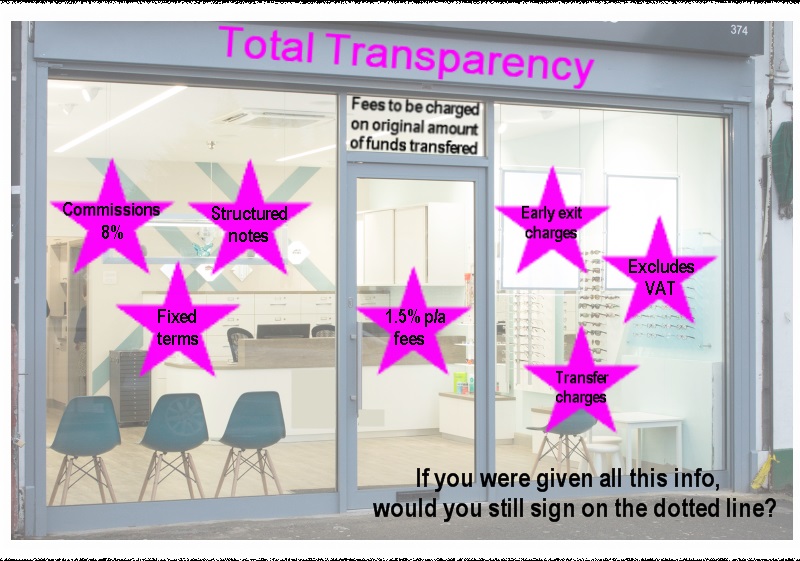

Belgravia Wealth has an impressive list of services offered. However, those who follow our blogs will know that the terms “structured products” and pensions together, makes us shudder with horror. We have seen so many pensions ruined by being invested in high-risk, fixed-term, for-professional- investor-only structured products.

“Belgravia Wealth Management is a Swiss-established and regulated company founded to fill the advice gap that currently exists between the retail financial companies and the services available to the UHNW clients. As an independent company, we ensure that you benefit from impartial advice and access to offerings from all the financial providers available in the market.”

It is great to read that Belgravia Wealth is regulated. Many firms I have written about fail to meet this simple – but essential – requirement. They claim to be independent and suggest that their advice is impartial. I wonder, though, with all this transparency in their blurb – are their staff qualified and registered to give this “impartial” advice?

Whilst their website offers a tab entitled “Careers”, it does not offer a list of staff that actually work for Belgravia Wealth. So, over to Linkedin to see if Belgravia Wealth staff advertise their employment with the company.

As with all these blogs, we only go by the information we can find, which is the same information potential clients would be able to access.

IFAs and their clients are invited to add to this blog, correct it, improve it. We will gladly edit our information if proof of qualification certificates can be supplied. Here’s a link to the three registers if you want to double check for yourself:

Spencer Freeman-Haynes – Director Zurich and Basel region at Belgravia Wealth Management – claims CISI – DOES not appear on the register

Emmanuel Obi, Jr. LL.M – Head of Compliance – Switzerland at Belgravia Wealth Management – no financial qualifications claimed (but how can he oversee the compliance function if he isn’t qualified?)

Mark Saunders – Regional Manager – Geneva Area, Switzerland – lists various CII qualifications – DOES NOT appear on the register

Ian Crompton – Director at Belgravia Wealth Management SARL – Claims CISI – DOES NOT appear on the register

Mystery Man (I do not have access to the profile) – Manager of Business Development – Belgravia Wealth Management – without a name I can not check his qualifications

Belgravia Wealth Switzerland has 6 members of staff listed as working for them, and from what I can tell NONE of them are qualified or registered to give financial advice.

The financial services industry has failed with flyingcolours to achieve transparency – both offshore and in the UK. The single most important thing about any product or service is transparency – aka honesty. This is where the profession has tolerated – and even encouraged – bare-faced lying for years and continues to do so today.

There is nothing intrinsically wrong with overcharging – as long as the overcharger makes it clear he is openly trying to rip his customers off and the victim is consciously happy to be ripped off. Personally, I’d love to be able to sell my car for 25,000 EUR – but with its age, condition and mileage I know I’d struggle to get 5,000. However, a crafty, clever person could give it a makeover, a clockover, tell a few convincing porky pies – and some poor fool might pay over the odds for it.

Most of the victims I deal with tell me the same story:

the adviser said the “review” would be free

the adviser said the only charge I would pay would be 1.5% a year

the adviser said my fund would grow at 8% a year net of charges

the adviser never told me about the insurance bond

the adviser never told me he was going to invest my funds in high-risk, illiquid funds or structured notes

Most people describe their offshore adviser as being about as transparent as a pork chop and the “flying colours” of their achievements to be fifty shades of brown.

Champion campaigner against this sort of dishonesty is international king of transparency Andy Agathangelou – Founding Chair of the Transparency Task Force, the collaborative, campaigning community dedicated to driving up levels of transparency in financial services around the world. Andy writes for Investment Week and calls for total transparency from offshore advisory firms.

One of Andy’s key statements is: “the financial services industry as a whole has a moral, ethical and professional duty to behave transparently”. But I wonder if that is a bit like asking for World peace, an end to pollution, a cure for cancer or a reversal of global warming (and a solution to the Brexit problem).

In the UK, advisers are not allowed to charge commissions on the products they sell, meaning that they will (hopefully) choose the best investment for their client – as there is no financial incentive to chose one product over another. However, offshore advisers do not have these restrictions, meaning that when they are selling an investment they will inevitably choose the one that pays the most commission.

But are things really that squeaky clean in the UK? Does the “beady” eye of the FCA have any effect or is it merely a masking mechanism to cloak lack of transparency (aka lying) in a thin veneer of false security? Henry Tapper’s recent blog on the subject of the FCA’s investigation into 34 firms suspected of non-disclosure of investment charges reports:

and quotes SCM Direct as saying “Its time for the chief executive of the FCA, Andrew Bailey, to demonstrate that he is willing to be the industry enforcer rather than the industry lapdog.”

One example was cited: Canaccord Genuity claimed its annual management fee was 1.25% plus a transaction commission of £30. But it turned out the 1.25% was just the beginning – then there were VAT and fund charges bringing the true cost nearer to 2.75%. Now, I know we women sometimes stretch the truth when it comes to our age, weight or clothes size – but Canaccord’s porky pie was that the real charges were actually twice what was claimed. That’s not just lack of transparency – that is naked dishonesty.

I had a browse through Canaccord’s funds and got bewildered by the range of costs – the annual charges seemed to range from 2.1% up to a whopping 4.34%. I’m just wondering whether an investor prepared to pay 4.34% for one of these funds might like to buy my car as well? After all, if they can throw their money away so easily, they surely can’t be bright enough to realise my rusty old heap isn’t worth 25k.

While I was in a browsing mood, I thought I’d have a wee look at Flying Colours. The company aims to provide super low-cost advice and investment funds and “negate the hidden costs in the market”. The website claims “I’m building a network of independent financial advisers with a shared vision – to improve the returns of UK investors. Join us.” But now I’ve got alarm bells ringing: a network? And who exactly is in the network?

A list of firms scattered across England from Bristol and Godalming to Liverpool and Skelmersdale – plus a few one-man bands. But they all claim to be “independent” financial advisers. How can they be independent if they are tied agents of Flying Colours? We are back to the “Wild West” offshore culture where members of a network are effectively “feral” and get up to all sorts of mischief due to lack of independence. And let us not forget that tied agents are illegal in Spain – and for good reason because the Spanish government knows that advisers simply cannot be independent if they are tied to one provider.

The Flying Colours network includes All Things Financial, Arch Financial Planning, CBG Financial Planning, Cullen Wealth Management, E-Crunch, Fit Financial Services, JAV Financial Planning, JBD Financial Planning, JRF Financial Planning, Lavelle Financial Services, Layfield Wealth Management, Mathew Burrows Financial Planning, NTW Financial Planning, Pepperells Wealth, S Fox Wealth Management, Sterling Financial Planning, The Royall Wealth Partnership and Tyrone Peters Financial Planning.

But how on earth does a coherent and effective compliance function work with 18 different firms scattered all across the country? (All of which are lying about their independence).

The Flying Colours website boasts: “We’re transparent about the charges you’ll pay for advice and investments. And there’ll be no hidden fees, ever.” But where are the fees and charges? I searched the whole website but couldn’t find out what they were. Because they were hidden.

Flying Colours recently made an ill-fated, abortive attempt to enter the offshore market (leaving considerable embarrassment and expense in its wake). Far from the claim of “starting strong relationships with a cultural fit and starting friendships“, Flying Colours ended up dumping the failure and retreating to UK-based “DIY” advice. Once Flying Colours’ offshore mess is cleared up, there will – no doubt – be a sigh of relief since Flying Colours was actually offering a more expensive version of the “cheap” investment advice process at 2% for investors with complex investments (so back to the same old, same old offshore “sophisticated” confidence trick).

What is there in Britain to protect consumers from lies; scams; lack of independence and transparency; weak compliance and unworkable investment offerings? Forget the FCA – they are permanently on a coffee break.

But what about the Insolvency Service? Isn’t that there to help protect victims from investment scams? More than a year ago, the IS commenced winding up proceedings against Store First for selling store pods to rogue SIPPS providers such as Berkeley Burke, Carey Pensions, Rowanmoor Pensions, London & Colonial and Stadia Trustees. So, we have thousands of victims of pension and investment fraud all left hanging – not knowing whether their investments are worthless or not. And this, of course, includes the Capita Oak and Henley scheme victims.

The lack of transparency about the store pods was, arguably, not the fault of Store First itself, but caused by the lies of the rogue promoters and “advisers” and the negligence of the SIPPS providers. A store pod is a great investment if the investor has a burning desire to invest in an illiquid, speculative asset – with the added benefit that he can also put his granny’s knick-knacks in there free of charge. While any honest adviser would have told the investors to invest their life savings in a low-cost, liquid, prudent fund – and any competent pension trustee or administrator would have refused to accept store pods as pension investments – the fact is that the backhanders set aside any common sense entirely.

Personally, I think the UK has a long way to go before it can claim to be entirely transparent. To get there, some sort of regulator would be helpful (forget the FCA – obviously) and an effective insolvency service would contribute to achieving meaningful reform. But while firms are still lying, obfuscating and cheating, we can’t really say that pension and investment scams only happen offshore. They are still very much on our doorstep.

Andy Agathangelou’s important work addresses many of the ills which blight offshore financial services. But he could do with a team of several hundred helpers to cover all the key expat jurisdictions. Offshore advisers – as well as UK-based firms – need to be 100% committed to their clients and take into consideration the future of the investments they make. They need to give their clients total transparency, not just on the commissions that will be applied but also on all other fees and charges.

Total transparency on all fees and commissions, before any transfers are made, would mean investors know exactly what they are getting into.The truth, the whole truth and nothing but the truth, is needed from day one! But it would also be exceedingly helpful if ALL UK-based advisers and fund managers adhered to this model.

Going back to Canaccord Genuity’s opacity in the case of a client with a £700k portfolio, their non-disclosure of the VAT charges alone led to an additional cost of £10,500. £10,500 over 10 years amounts to £105,000 – quite a sizable chunk of the fund. You would have to have some very good investments to cover these costs AND increase the amount of the fund. Which, of course, is (or ought to be) the main aim of an investment!

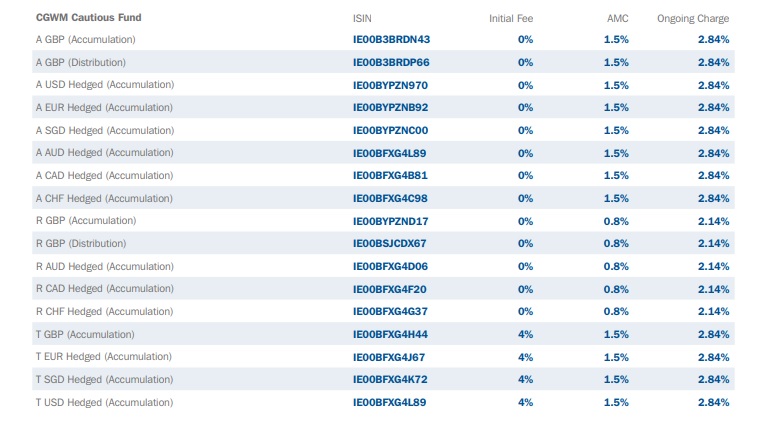

Just for a laugh, have a look on Canaccord´s website at their list of fees, in particular, their cautious fund. 4.34% a year in charges. I wondered if this included VAT (being a “cautious” investor!).

So I decided I´d give them a call, just to clear up the confusion.

I was passed around various departments and ended up talking to a woman, who was – to put it plainly – pretty unhelpful. I asked about the charges and was told I would need to talk to a fund manager. I was asked how much I wanted to invest. I replied I´d need more information before I could commit to an amount. I was told there was a minimum investment of £250,00, but she still couldn´t tell me about the fees and charges.

I was put on hold, after she implied she might find out the answers to my questions. However, she must have forgotten me as no one came back and I was simply left hanging – listening to the sound of silence. Hopefully, Canaccord won’t forget me in the future.

Mind you, I didn’t have much luck with Flying Colours either. I chatted to their online “can I help you?” chap, Stephen Murphy, and asked him what the fund and advisory charges were. Murphy wanted to know why I wanted to know. I explained I was writing an article on Flying Colours’ fees. His reply was: “In regards to you writing an article around fund charges – we are not interested in featuring in an article as you are based in Spain – however, if you need further information around this you could contact Dani Greenfield on dgreenfield@flyingcolourswealth.com – she deals with the marketing side of our business.” Why so secretive I wonder?

Offshore advisers should be forced to put labels like these on their investments!

All this leaves us with a number of pressing, unanswered questions:

Is it acceptable that the financial services industry has failed with flyingcolours?

Is it tolerable that in some ways it is as bad in the UK as it is offshore?

Should consumers continue to tolerate unacceptably high charges from providers?

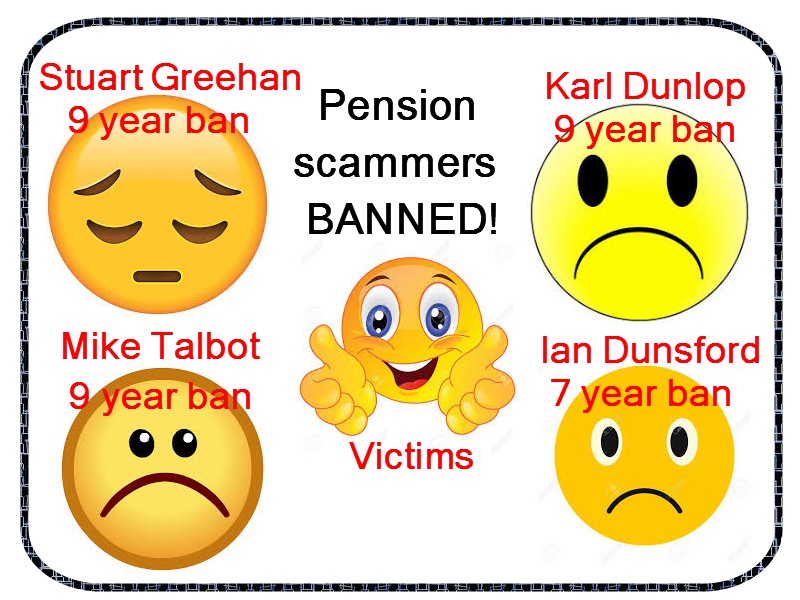

Articles like New Model Adviser’s report on some of the scammers behind the Capita Oak/Henley/Store First scam getting banned always makes me smile. Knowing that a few pension scammers (four in this case), are being named and shamed – as well as banned from being directors – motivates me to share information about these evil scams with the public.

“An investigation led by the Insolvency Service revealed the directors were connected with Transeuro Worldwide Holdings, which helped fund two introducer firms Sycamore Crown and Jackson Francis. The firms were involved in the transfer of £57 million of pension savings.

Sycamore Crown director Stuart Greehan agreed to a nine-year voluntary ban as a result of false and misleading statements to encourage investors to transfer their pensions.

Karl Dunlop, director of Imperial Trustee Services, and Ian Dunsford, director of Omni Trustees, agreed to bans of nine and seven years, respectively, for failing to act in the best interests of members and ‘failing to ensure investments were adequately diverse’.

While not a formally appointed director of Transeuro Worldwide Holdings, Mike Talbot (AKA Stephen Talbot) accepted a nine-year disqualification undertaking for failing to disclose what happened to the millions of pounds of pension assets.”

BUT, IN ADDITION TO THESE EVIL SCAMMERS, THERE WERE OTHER PLAYERS IN THIS APPALLING TRAGEDY AND THEY WERE NOT MENTIONED. SO HERE ARE THE OTHER PEOPLE WHO PLAYED LEADING PARTS IN THIS FOUL PLAY:

Stephen Ward of Premier Pension Solutions SL and Premier Pension Transfers Ltd – he handled the transfer administration from the original (ceding) pension providers. He was, apparently, paid £300 per Capita Oak transfer – and would have known that he was condemning each member to certain loss of his or her pension.

XXXX XXXX of Nationwide Benefit Consultants, The Pension Reporter, Victory Asset Management and Tourbillon, was clearly the “controlling mind” behind Capita Oak. He also ran the Thurlstone loan scheme which paid 5% in cash to the Capita Oak victims as a “bonus” or “thank you”. HMRC is now taxing these payments at 55% as they qualify as unauthorised payments. XXXX XXXX then went on to launch the successful Trafalgar Multi Asset Fund scam which saw over 400 victims lose their pensions to high-risk toxic loans to Dolphin Trust in an STM Fidecs Gibraltar QROPS. XXXX – as with most pension scammers – subsequently ignores the plight of the victims when the schemes eventually and inevitably collapse. XXXX is under investigation by the Serious Fraud Office and was also responsible for the Westminster pension scam.

Mark Manley of Manleys Solicitors – acting for XXXX XXXX.

Stuart Chapman-Clarke, Christopher Payne, Ben Fox, Bill Perkins, Alan Fowler, Karen Burton, Tom Biggar, Sarah Duffell, Jason Holmes, Metis Law Solicitors, Roger Chant, Brian Downs, Phillip Nunn and Patrick McCreesh all played further prominent roles in this series of scams and profited to a greater or lesser degree.

It is believed that cold calling techniques were used to lure unsuspecting victims into this series of unregulated investment scams. Victims’ pension savings were transferred into bogus occupational pension schemes whose trustees/administrators were Omni Trustees and Imperial Trustee Services. The schemes were Henley Retirement Benefit Scheme (HRBS) and Capita Oak Pension Scheme (COPS). But the scammers also used a variety of SIPPS which included Berkeley Burke, Careys Pensions, Rowanmoor, London and Colonial and Stadia Trustees.

As is often the case in scams like these, the victims were lured in with promises of so-called guaranteed high returns by spivs masquerading as advisers, who were also unqualified and unregulated to give financial advice.

The unqualified advisers were able to transfer millions of pounds’ worth of pension savings into these schemes which included investments in unregulated storage units and over £10 million into COPS (Capita Oak) and over £8 million into HRBS (Henley). The promised high returns were never paid to the investors – but handed over to the scammers instead. The pension funds are now suspended with the funds trapped in these illiquid investments.

The company directors have received a total ban of 34 years collectively. Here at Pension Life we would have liked to have seen lifetime bans all round.

The Serious Fraud Office (SFO) is now moving forward with their investigations against Omni and Imperial. They urge people who are members of HRBS (Henley) and COPS (Capita Oak) to contribute to criminal evidence against the scammers via a questionnaire.

As always, the team at Pension Life urges pension holders to be wary of pension scammers. Never accept a cold call offer, be aware that scammers lurk everywhere and if it seems to good to be true it probably is!

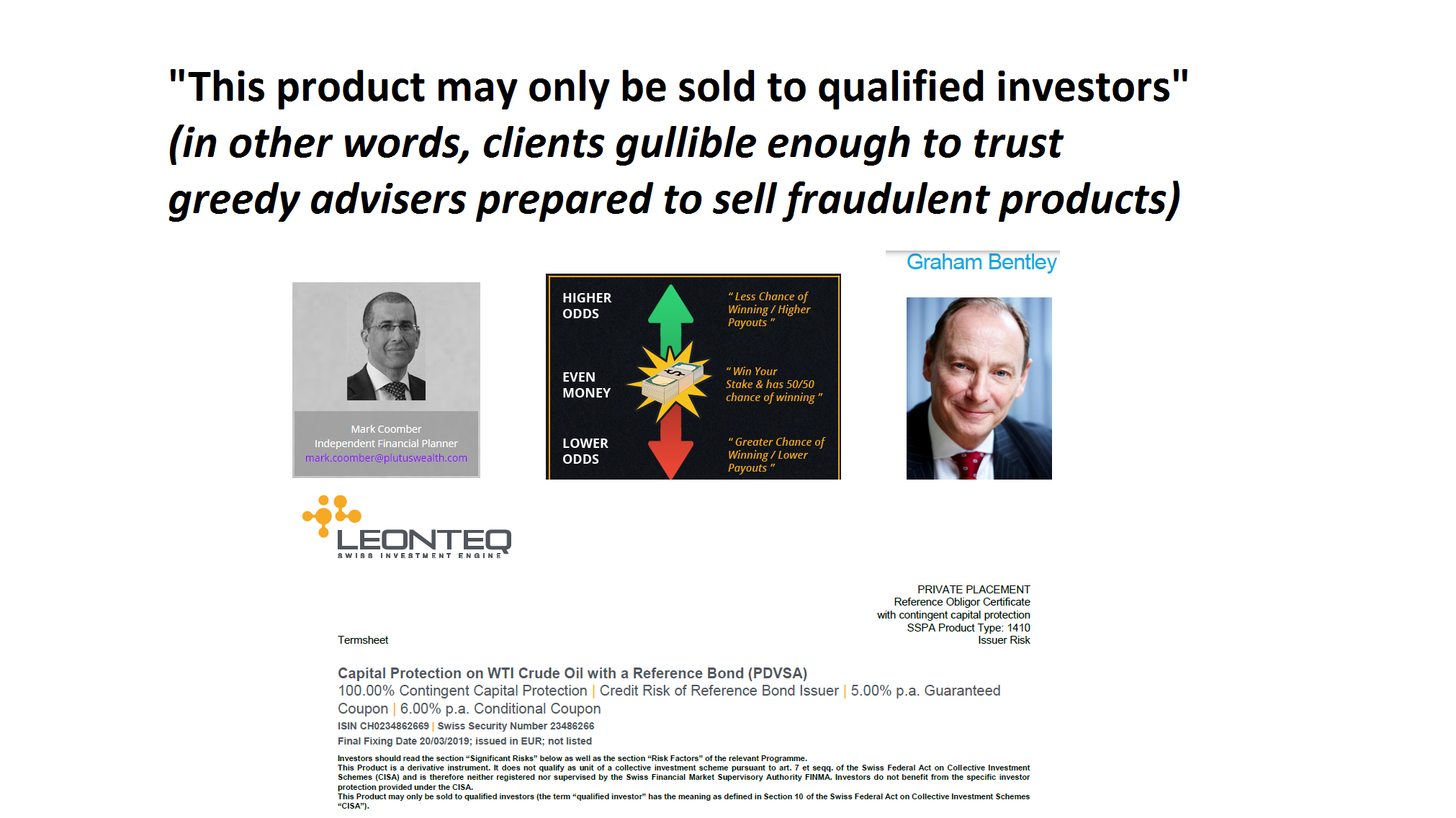

Nitwit or Dragonfly? Gambling or Investing? Are investment losses as a result of a bad adviser or a bad investment? Or both? The real question is: how does the consumer tell the difference? A favourite episode of Fawlty Towers involved Basil’s ill-fated bet on a racehorse called Dragonfly. Confusion sets in – fuelled by the easily-confused Manuel – and “Dragonfly” gets muddled up with “Nitwit”. And that is how clients get confused just as easily: by advisers who spout the usual rubbish: capital protected; guaranteed returns; blue-chip investments; solid providers etc. They just leave out the three most important things: the fat commissions paid to the adviser; the high-risk nature of the “investment” and the fact that structured notes are FOR PROFESSIONAL INVESTORS ONLY (and not for retail investors).

Bentley has suggested that structured products are an option that advisers could consider including in their portfolio of investment solutions. If he is talking about outright scammers, then – of course – he is right. Structured products pay juicy commissions of up to 8%, so naturally they are a favoured product for these criminals to sell. Plus, if the clients themselves have so much money they are desperate to get rid of as much of it as possible, as quickly as possible, then structured products are ideal.

But Bentley is missing the point entirely. Structured products have, for years, been sold enthusiastically and aggressively by the usual suspects: Leonteq, Nomura, Commerzbank, Royal Bank of Canada and BNP Paribas; bought by scammers such as Continental Wealth Management for the juicy commissions; harboured by crooked life offices such as Old Mutual International. And the result has been huge losses for hundreds of victims. In some cases, total destruction of a victim’s life savings.

Most advisers who sell these toxic products are too thick to understand how they work – and indeed anything beyond the amount of commission they earn out of flogging them is way too tricky to get their simple minds around. And why should they even bother? They just sell them, collect their 8% and then move on to the next victim. What’s to understand? They know that life offices love them – and indeed Old Mutual International bought £94 million worth of the fraudulent Leonteq ones alone. It is a delightful circle for all concerned: the scammers get rich, the bent life offices get fat and the structured product providers do very nicely thank you. And not a single one of them gives a second thought for the victims.

One cheerful idiot on the Linkedin thread has enthusiastically supported Bentley’s idiotic view:

“Continue to use structured products (as part of portfolios) both personally and for clients with great success. Most of the negative comments I read about them are born out of ignorance and sheer laziness of some advisers who cannot be bothered to either learn the topic matter or undertake the relevant due diligence.”

And this guy is chartered! As a member of the CISI he should know better than to spout such rubbish – and I feel deeply sorry for any clients of Plutus Wealth Management as they are clearly in danger of being sold these toxic products. In fact, I would go further and suggest the public should be warned about the dangers of using this firm, as Coomber clearly has every intention of flogging his victims these high-risk products. If he is stupid enough to use them for his own gambling fun, good luck to him. But he has no right to inflict them on retail clients.

One of the fraudulent structured notes sold by Leonteq (for 8% commissions to the scammers) was:

Capital Protection on WTI Crude Oil with a Reference Bond (PDVSA)

100.00% Contingent Capital Protection | Credit Risk of Reference Bond Issuer | 5.00% p.a. Guaranteed

Coupon | 6.00% p.a. Conditional Coupon

ISIN CH0234862669 | Swiss Security Number 23486266

Final Fixing Date 20/03/2019

The term sheet did, to be fair, give a clear warning:

“Given the complexity of the terms and conditions of this Product an investment is suitable only for experienced Investors who understand and are in a position to evaluate the risks associated with it.”

Sadly, we have to wait until March 2019 to find out how many victims have lost their shirts on this particular lame horse.

And this is the problem: most advisers don’t understand structured products themselves – all they understand (and care about) is the fat commission. They certainly don’t care that the products are fraudulent. But, more importantly, none of these rogue advisers’ clients are experienced investors. If they were, they wouldn’t be paying a greedy and irresponsible financial adviser to risk their hard-earned life savings for them.

STRUCTURED NOTES ARE GAMBLING – NOT INVESTING!

So my message to Coomber and Bentley is this: read Leonteq’s term sheet:

“Products involve a high degree of risk, including the potential risk of expiring worthless. Potential Investors should be prepared in certain circumstances to sustain a total loss of the capital invested to purchase this Product.” And then try to decide which horse is going to win: Dragonfly or Nitwit.

All pension and investment scams have one thing in common: if the pension scam victims had asked the offshore advisers some or all of these 10 essential questions, they might not have lost their life savings to the scammers.

Here at Pension Life, we are working hard to help educate the masses and stop pension scammers in their tracks worldwide. By arming and informing the public, and teaching them how to spot the scammers and avoid being scammed, we can help put a stop to these crimes.

With the scammers outsmarted, there will hopefully be fewer pension scam victims!

We have put together this cartoon which provides you, the investor, with 10 essential questions to ask your offshore adviser before you sign your precious pension fund over. Knowing what questions to ask could mean you do not become the next pension scam victim.

1. Pension Life has covered what qualifications your adviser needs to give pension advice. The adviser should also be able to show you their certificates and be registered with the governing body that awarded them – typically CII or CISI qualifications. We have created a series of blogs “firm name – qualified and registered?” which cover many offshore advisory firms and their team members. They show the firms that list employees who claim qualifications but are not registered and have failed to supplied proof and which firms are transparent. Some firms are happy to work with us and be 100% transparent and demonstrate that their team of advisers are fully qualified and registered.

2. Many offshore companies are regulated with an insurance licence ONLY and this is not sufficient to give pension and investment advice. They must have a licence to give advice on pensions and investments.

4. Insurance bonds are an expensive and unnecessary double wrapper on your pension. If it has already been invested in a SIPPS or a QROPS, insurance bonds are not needed. Insurance bonds are another way for the scammers to skim more commissions from your fund, putting a dent in your start and end value. Life offices such as Old Mutual International, Generali and RL360 are among the firms (known as life offices) to be avoided.

5. Structured note providers such as Leonteq, Nomura, Royal Bank of Canada and Commerzbank should be avoided. These companies are linked to previous pension scams and many victims have seen their pension funds destroyed with these high-risk, fixed-term notes, that are totally unsuitable for a pension fund. Often these structured notes have high commissions that make the ‘adviser’ big bucks.

6. Holding a DB pension puts you in good stead for your retirement. With a pension fund like this you are often better to ‘just do nothing’ and leave it as it is. Transferring it can lead to heavy charges and fees, meaning your fund becomes worth much less than before.

7. A pension is classed as a retail investment and needs to be invested in low to medium risk investments with a steady increase in value. Offers of high returns, especially in investments that use words like “renewable energies” or “property”, are illiquid and high risk. These types of investments are not safe for your pension. An example of this is the Elysian bio-fuels pension scam, facilitated by James Hay and Dolphin Trust – a German housing investment scheme – promoted to British steelworkers.

8. Time and time again, we see pension scam victims receiving the paperwork on the pension transfer ‘deal’ they have signed, only to realise that large fees and charges have been applied. The scammers are experts at hiding the charges and often quote the term: ‘free pension review’. Whilst they do not charge for all their visits and advice before you sign on the dotted line, they make up for this in transfer fees, commissions and often quarterly charges too! The quarterly charges will be applied no matter how your fund is doing. We have seen pension scam victims´ funds end up in negative equity due to being placed into an inappropriate fund which causes losses and second, continuing fees being applied. (Fees are normally based on the start value of the fund).

9. With the technology we have today, like smart phone apps, many firms are offering instant access to the progress of your pension fund through their own app. Options exist to add funds or change your investments and total transparency of investments and progress; a company that offers this service is Pension Bee. You should also get quarterly statements and annual reviews so you can track the progress of your fund.

10. We have seen pension scam victims repeatedly contacting their so-called advisers to try to get information on the demise of their fund, only to meet dead end after dead end. Again, ensure you are using a fully licensed firm that has an admin, compliance and support team. Ensure you are able to get a set of contact details (if not two!) and that there is a ‘real’ address and a landline – scammers often use PO boxes and mobile numbers.

Remember, it is your pension and your investment; you are entitled to ask as many questions as you like. These essential questions to ask offshore advisers should be simple for any trustworthy and transparent adviser to answer quickly and effortlessly. If your adviser is in any way cagey, vague or tries to avoid the question altogether, just walk away. An adviser who is unwilling to be totally transparent could well be a scammer.

I have enormous respect for FT Adviser. Their articles are written by proper journalists and they generally write competently and professionally. FT Adviser puts International Adviser to shame with their thinly-disguised promotional shows and Micky Mouse “articles” which only ever promote their own sponsors – Old Mutual International and their ilk.