High Court Rules in Trafalgar Multi Asset Fund Case against James Hadley and associates.

In a recent High Court judgment, Judge Mr. Nicholas Thompsell found that the Cayman-Islands based Trafalgar Multi Asset Fund (TMAF) was involved in an illegal conspiracy to “extract commissions from the investments.” The defendants, who were also behind the 2013 Store First pension investment scam, were found guilty of acting together to establish TMAF and deceive investors.

The claimant, Doran & Minehane, the liquidator of TMAF, argued that the investments were uncommercial transactions, potentially fictitious, or involved undisclosed self-dealing benefiting the conspirators. The investments were designed to exploit and misappropriate pension funds for the defendants’ benefit.

The judge determined a deliberate intention to harm TMAF, stating that the arrangements aimed to generate commissions for the conspirators at the fund’s expense. The accused faced a range of serious accusations, including breach of financial services regulation, fiduciary duties, and involvement in unlawful means conspiracy.

The victims, who suffered significant losses due to these schemes, have our sympathy. The court’s judgment establishes solid principles of liability, which may lead to a faster receipt of claimed monies and reduced legal costs for the defendants.

For the full judgment, click here: High Court Rules in Trafalgar Multi Asset Fund Case against James Hadley and associates.

This is a helpful lesson for victims and potential victims of pension and investment scams. The FSCS compensation payments will be funded by levies on the decent, qualified and ethical IFAs who don’t operate scams. Justice and education combined in one bitter pill.

Covid 19 is having a terrible effect on millions of people across the globe. All walks of life are being affected. One important aspect of life in general is that of investments – life savings and pensions in particular.

Fraudsters are now using the Covid 19 pandemic as a weapon to encourage investors to fall for investment scams. The tactics used are similar to those deployed as scare tactics over Brexit:

“get your pensions out of the UK so you have more investment choice and control”

(What the scammers meant by this, of course, was that they would have choice and control – and fat commissions. The victims would just have less money).

There are many lessons to be learned from the pandemic – including the way different countries have dealt with lockdown procedures. But the lesson I want to examine, in parallel, is how governments deal with pension and investment fraud.

We’ve now seen that laws can be changed swiftly when there is an international crisis threatening millions of lives. Yet, for more than a decade, pension and investment scams have threatened even more lives, while laws and regulations have barely budged. Police can jump into action when a couple of people take a stroll in the park without observing social distancing laws, yet armies of scammers steal of millions of pounds from thousands of victims, and nobody in a police uniform lifts a finger.

The Covid 19 crisis will inevitably contribute to the effects of inappropriate investments – which teeter on the narrow verge between mis-selling and fraud. Where commission is king and investments have been chosen purely for the hidden (from the consumer) introduction revenue, the effects of this will now be felt acutely by many victims.

It has long been deeply frustrating that so many scammers can offend repeatedly – often for years on end – without any sanction. Victims of pension scams such as Ark, Capita Oak, Henley, Westminster, Evergreen, London Quantum, Fast Pensions and Continental Wealth Management have lost their pensions to the same scammers over a seven-year period.

Regulators, police and government ministers have taken not a bit of notice other than sometimes handing the pension schemes over to Dalriada Trustees – who also fail to report the blindingly-obvious frauds to the police authorities.

Mind you, I have some (limited) sympathy with Dalriada. They obviously know it is a complete waste of their precious (and very expensive) time reporting the scammers. Dalriada clearly knows full well that the Police, Insolvency Service and Serious Fraud Office are worse than useless.

Behind this failed law-enforcement network lies an even bigger scam: Action Fraud. This is a cynical effort to fool scam victims into believing that some action will be taken when fraud takes place. However, the reality is that Action Fraud is just a call centre which deliberately ignores the desperate pleas for help by fraud victims. In fact, the Action Fraud call centres are no different in nature than the boiler-room cold calling centres used by the scammers – the purpose is the same: to deceive victims.

We have now seen the hard evidence that whole continents can jump into radical action when necessary. So there is no longer any excuse for allowing the pension and investment scam pandemic to continue unchallenged.

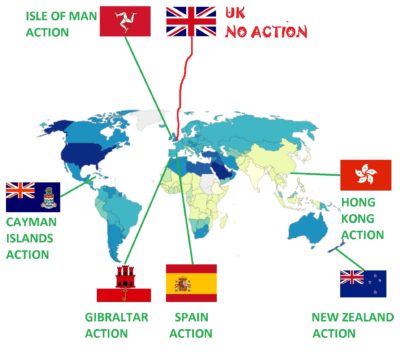

Every country – especially ones where lots of British expats live – needs to recognise that pension and investment scams are – and always have been – a global pandemic. The apathy and laziness of regulators, law enforcement agencies and governments need to cease. And Britain’s shameful, embarrassing track record of ignoring – and even facilitating – scams needs to be reformed.

The early signs of a wind of change in the pension and investment scamming world are there. Spain and New Zealand are now actively progressing criminal proceedings against scammers. There are early signs that other jurisdictions are starting to wake up as well.

The scammers at Premier Pension Solutions and Continental Wealth Management are facing fraud and falsification charges in Spain.

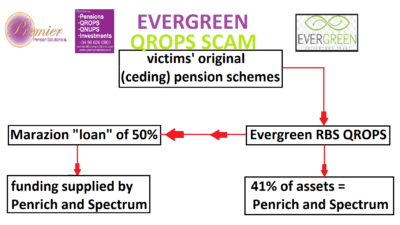

The SFO in New Zealand is investigating the scammers in the $100m Penrich Macro Global investment fraud which was also linked to the Evergreen QROPS scam (run by Stephen Ward and promoted by Continental Wealth Management).

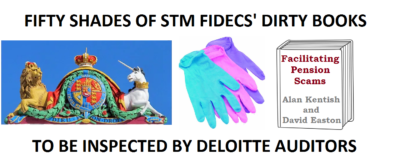

STM Fidecs in Gibraltar has issued a claim against thirteen defendants for the return of “misappropriated” money in the Trafalgar Multi Asset Fund case (also under investigation by the British SFO).

Police in the Cayman Islands are investigating a fraudulent investment company – and has warned potential investors into any companies in Cayman to carry out proper research and due diligence

The Isle of Man courts are preparing for a raft of civil proceedings against leading life offices which have facilitated financial crime on a massive scale internationally.

The Hong Kong fraud squad is taking a keen interest in the GFS Blackmore Global pension/investment scam.

Back home in the UK, there are serious complaints being filed against HMRC and the Pensions Regulator for facilitating pension scams and failing to warn the public. And a growing body of victims and professionals is looking at bringing the FCA to justice for their multiple failures.

Even if the tide is beginning to turn, it is – of course – way too late for thousands of victims whose lives have already been ruined by the scammers. Just as Covid 19 has killed hundreds of thousands of victims in just a few months, pension and investment scams have ruined hundreds of thousands of hard-working victims’ lives in the past decade.

While more than 200 countries are fighting against the spread of Coronavirus and trying to save the 300,000+ people who are sick, we now need key financial services jurisdictions to take the pension and investment scam pandemic seriously.

Renowned English Author James Hadley Chase once famously wrote:

“It’s better to be sick of life than not have a life”.

Pension and scam victims are not just sick of life, but they are also sick of the lack of action by authorities internationally – but above all in Britain. Let’s hope that current actions in place in Spain, Gibraltar, Cayman Islands, Isle of Man, Hong Kong and New Zealand will be replicated as swiftly and effectively as the Covid 19 protection measures.

This Cayman Islands-based fund is being liquidated and it is uncertain whether there will be any recovery for the victims whose pensions were invested in it.

Nearly 250 STM Fidecs QROPS members stand to lose £25 million.

Given the uncertainty of recovery by the liquidator, we felt it was essential to issue proceedings so that the victims’ interests would be protected.

STM Fidecs – a QROPS provider in Gibraltar – has issued the following update to the Trafalgar Multi Asset victims:

“Following an investigation into the status of the Fund’s investments, the Company’s directors determined that it would be in the best interests of the Shareholders to wind down the Fund and to focus on the recovery of assets and the distribution of such assets to those entitled to have recourse.”

STM Fidecs appointed Stephen Doran of Doran + Minehane as liquidator.

The update issued by STM Fidecs has given victims very limited information relating to the current status of the liquidation of the fund or the prospects of recovery. However, it has made it clear that there was “misappropriation of funds” and that there were investigations ongoing.

STM Fidecs has stated that it has recently commenced litigation against “various parties” and a claim has been issued against thirteen defendants in respect of misappropriated monies.

Whether the guilty parties will be brought to justice, or whether there will be any money left over for the victims after the the liquidator has been paid in full, remains to be seen.

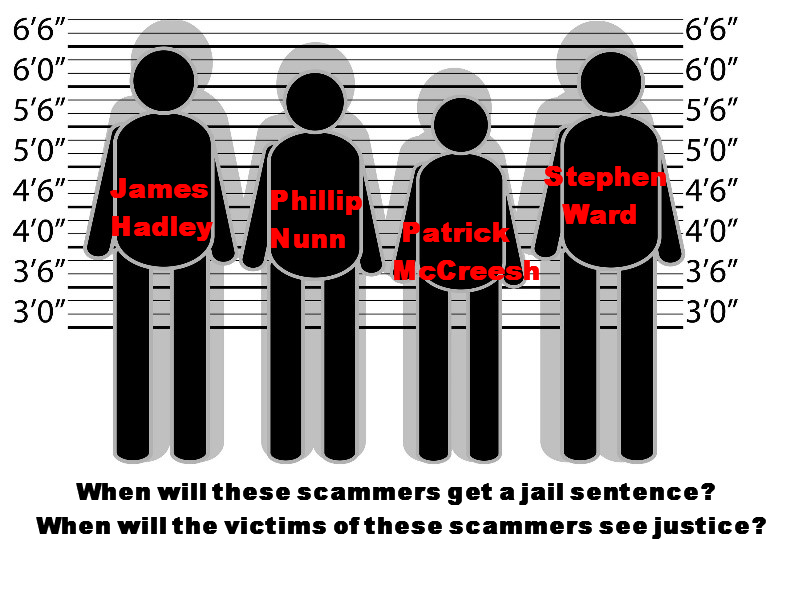

It is well known that the Trafalgar Multi Asset scam has been under investigation by the Serious Fraud Office. This was announced by the SFO on 22 May 2017. Other schemes promoted by the same team of scammers included the Capita Oak and Henley pension scams which were promoted by Sycamore Crown Ltd, Jackson Francis Ltd, Portia Financial and Nunn McCreesh.

It is also known that the same scammers who were promoting Capita Oak, Henley and Trafalgar Multi Asset Fund were also promoting the Blackmore Global Fund run by Phillip Nunn and Patrick McCreesh. Nunn and McCreesh’s Blackmore Bond is currently in the hands of administrators Duff and Phelps.

Victims of all of these scams are still invited to contact the Serious Fraud Office if they have any evidence they wish to provide in order to help bring the fraudsters to justice: hazel@sfo.gov.uk

Forsters – the firm which Pension Life is working with – have liaised with the Trafalgar Multi Asset Fund investor committee (which currently includes a doctor and a police officer). Forsters and Pension Life are working towards bringing about the best possible outcome for the victims.

There may be serious doubts over whether the liquidation by Doran + Minehane will result in any meaningful returns for the victims. However, this litigation will give them a decent chance to get a large proportion of their pensions back.

Forsters LLP is a leading law firm with an exceptional track record of successful dispute resolution. It is not a no-win-no-fee firm, and it has no connection with any claims management companies.

The ongoing war against pension scammers continues with no sign that the end is near. The authorities stand idly by – facilitating mis-selling and outright fraud.

The only conclusive way to stop scammers is to ensure there are no victims for them to scam. AND the only way to do this is to educate consumers and drum the TEN STANDARDS into them.

PENSION SCAMMERS MUST BE STOPPED!

Ten Essential Standards For Pension Advice:

Do you know what a pension scammer looks like? The unfortunate answer is, he looks like any other Tom, Dick or Harry (or James, Stephen or Darren) walking down the street. Not only is he good at disguises, he also has the gift of the gab and he will have you convinced that the pension transfer he is offering you will pave the rest of your life with gold. In reality though, the gold will be short lived (or non-existent), and some or all of your fund will probably go poof! (along with the adviser).

Much as a master illusionist takes your breath away with his magic, a master scammer takes your money away with his silver tongue. You will be left wondering just how this smart-looking, sleek-talking ‘adviser’ managed to leave your pension – and probably your life – in tatters.

We have compiled a list of ten standards that EVERY firm offering pension advice should adhere to. Every qualified adviser working for an advisory firm should also be able to meet all of these standards. On Facebook recently, one reader stated: “Why would anyone respond to an unsolicited offer to manage their money from a complete stranger?” The answer is, “I don’t know, but they do!“. So, get to know a financial adviser long before you let them anywhere near your finances.

In the case of Capita Oak, for example, we saw many targeted victims who were struggling financially. So, the offer of a lump sum release and the opportunity of an investment that promised “guaranteed returns” was music to their ears.

Many of the victims didn’t stop to think; didn’t pause to ask the right questions; or do any research to make sure the pension offer came from a viable, credible, regulated firm. The victims just said “yes” as they thought the transfer would make life easier.

For example, with the awful benefit of hindsight – six years on – the Capita Oak victims are grappling with tax demands from HMRC and the possibility that the investment they are trapped in will go into liquidation. These people all wish they had stopped and thought before going ahead.

Sadly, the Capita Oak members who were defrauded by a bunch of scammers, (many of which are under investigation by the Serious Fraud Office) such as XXXX, Stuart Chapman-Clarke and Stephen Ward, are not alone. Thousands of other victims of both UK-based and offshore scams and mis-selling are facing similar regrets: these include victims of scams such as Evergreen New Zealand QROPS; Fast Pensions, Trafalgar Multi Asset Fund/STM Fidecs; Blackmore Global Fund; and Continental Wealth Management.

Mastermind serial scammer Stephen Ward has orchestrated a whole array of different scams over the last nine years. One of the biggest ones was Continental Wealth Management – a 1,000-victim scam. Ward was once a fully qualified and registered adviser and a pension trustee. He has destroyed dozens of pensions funds and thousands of victims’ lives. Yet he has never been prosecuted or forced to pay back even one penny of his victims’ losses. Only at the end of 2018 was he finally banned from being a pension trustee.

Most of the known scams used cold-calling techniques to reel in their victims. Whilst we saw a cold-calling ban on pension sales in 2019, we have already had reports that sneaky firms have changed their scripts to avoid fines. AND we are now seeing scammers focus their targets back onto expats. Which makes us worry there will be more QROPS disasters in the pipeline from now on.

Just a few minutes of research – as well as knowing the right questions to ask and understanding what standards an adviser and firm should adhere to – could have prevented past victims from losing so much of their precious pension pots. We can’t change what happened in the past – other than to take action against the scammers and negligent advisers – but we can help consumers understand what they should be looking for in an adviser:

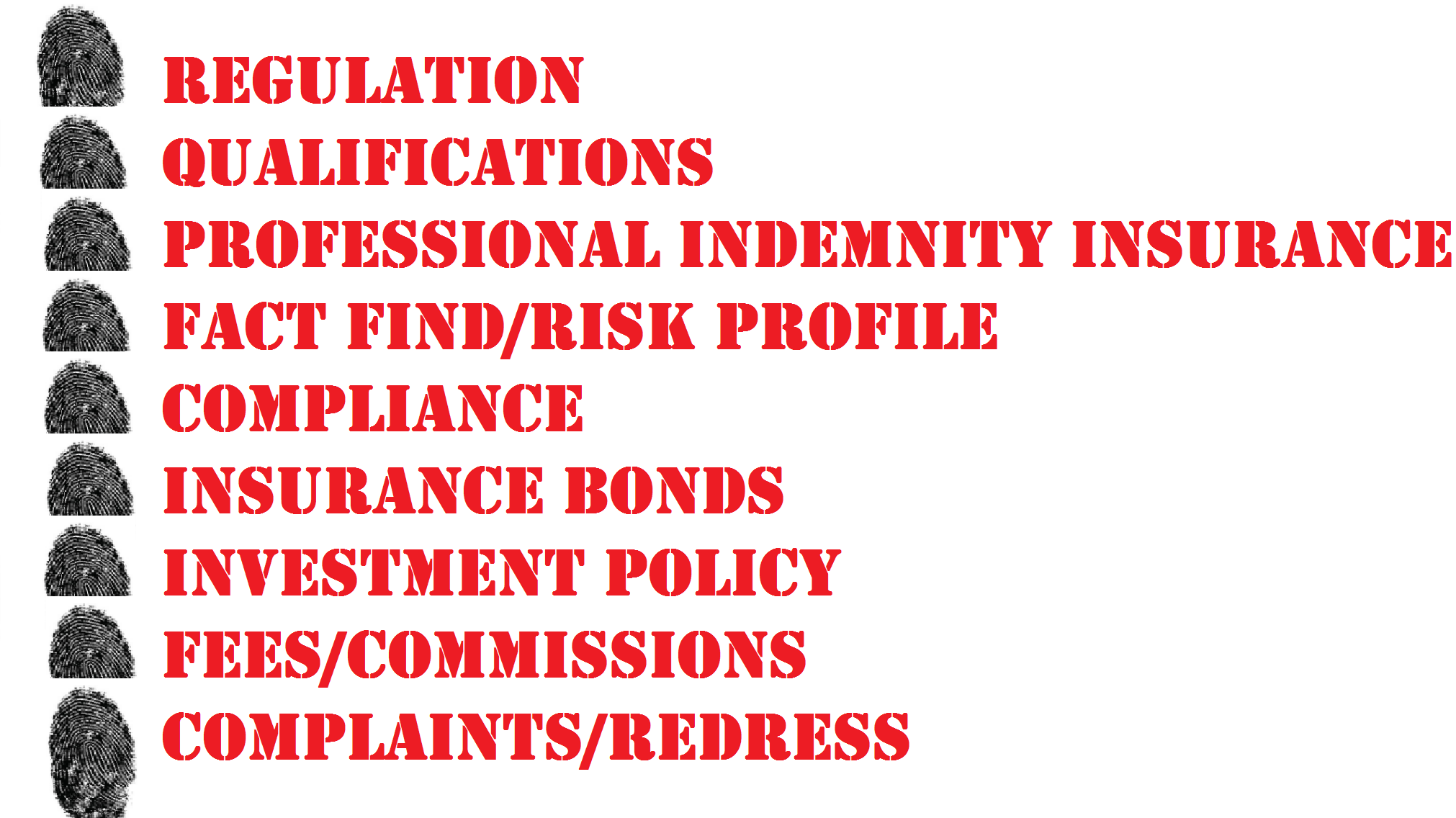

STANDARDS ACCREDITATION CHECKLIST FOR FINANCIAL ADVISERS:

Proof of regulation for all services provided by the firm and individual advisers in the jurisdiction where advice is given

Evidence of appropriate qualifications and CPD for all advisers

Professional Indemnity Insurance

Details of how fact finds are carried out, and how clients’ risk profiles are determined and adhered to

Details of the firm’s compliance procedures – assuring clients of the highest possible standards

Clear and consistent explanation and justification of the use of insurance bonds for pensions and investments

Clear policy on structured notes, UCIS and in-house funds, non-standard assets and commission-paying investments

Full disclosure of all fees, charges and commissions on all products and services at time of sale, in writing

Account of how clients are updated on fund/portfolio performance

Evidence of customer complaints made, rejected or upheld and redress paid

If the firm you are thinking about using for your pension transfer do not adhere to all of these standards, find one that does. Your pension pot is your life savings – so don’t entrust it to any old unregulated firm or dishonest scammer. Remember, thousands of victims have already failed to ask the above ten questions – and will regret it for the rest of their lives.

By far the best US crime thriller series (IMHO) on Netflix has got to be Blacklist. Utterly mesmerising is the star Raymond Reddington (played by the superb James Spader). Reddington manages to be simultaneously as camp as a row of tents, and macho as the All Blacks.

The rest of the cast – both cops and robbers – are all excellent with intriguing sub-plots, endearing romances and lots of buttock-clenching suspense as the FBI race against time to catch the bad guys, recover the sniffing/folding stuff and save the victims from torture and painful deaths.

So inspired was I by taking up Blacklist binge-watching, that I decided to write an episode to submit to NBC (just in case the writers run out of ideas). My plot was hatched because every Blacklist episode contains all the ingredients that we need to tackle pension scams: the minute the crime (or intended crime) is identified, the FBI Special Agents swing into action, and SWAT teams are warmed up; the criminals’ mobiles are tracked and their computers hacked.

By the time I’ve cracked open the Snickers, Special Agents Wrestler and Mossad are on the scene and closing in fast on the bad guys. As I’m warming up my cocoa, the contraband has been uncovered; the bombs have been defused (with two seconds to spare); the bad guys are all either full of holes or in handcuffs; the full details of the dastardly criminal plot are laid bare. Most important, the lost $millions are recovered in full, and the valiant Red Reddington flies off into the sunset in his private jet with his trusty Dembe clucking at him for taking too many risks.

So here’s my humble attempt at the script for a Blacklist episode “The Pension Scam (No 69)” – script:

Arch pension criminal (and mastermind of the Capita Oak and Henley cases) XXXX XXXX – dressed in bright purple (to offset his flaming red hair) and driving a black Ferrari – struts into the offices of various QROPS trustees around the Med and meets cheery Irishman Justin Caffrey of Harbour Pensions. XXXX tells Caffrey of his plot to make millions out of scamming hundreds (or preferably thousands) of victims out of their pensions. His plan is to con hundreds of UK residents into transferring their pensions into a QROPS. And then (and this is the clever bit) XXXX, who is acting as the victims’ financial adviser, invests all their money in his own fund: the Trafalgar Multi-Asset Fund.

Being a particularly canny Irishman, Caffrey sees straight through XXXX’s dastardly plan and sends him and his (borrowed) Ferrari packing. Caffrey clocks XXXX as an outright spiv straight away. Caffrey is, anyway, already up to his ears in Phillip Nunn’s Blackmore Global investment scam, promoted by vile David Vilka, so he really can’t handle more than one scam at a time (being male, he can’t multi-task).

Way too thick-skinned, determined and greedy to be discouraged, XXXX heads across the Mediterranean to Gibraltar and the offices of STM Fidecs. There he meets CEO Alan Kentish who listens to XXXX’s offering with keen interest. Already under investigation for “tax irregularities”, Kentish is no stranger to “bending the rules” and is keen to learn more about how XXXX’s scam is going to work – and, of course, what is in it for Kentish himself.

XXXX explains that he has found an “umbrella” fund called the Nascent Fund run by Custom House Global Fund Services and a handsome but menacing-looking chap called Richard Reinert. This outwardly respectable-looking outfit allows wannabee fund “managers” (such as XXXX) to set up their own investment funds in the dodgy jurisdiction of the Cayman Islands – far from the eagle eye of the FCA.

Kentish is eager to know how much money can be made out of this plot. XXXX explains that 46% was earned out of his Capita Oak and Henley scams and that he hopes to make at least as much out of this one. With Kentish’s “help” (nudge nudge, wink wink). Of course, the proceeds could be split and plenty of brown envelopes used to disguise the handing over of the proceeds.

Things get off to a cracking start, with XXXX’s two trusted assistants: Tom Biggar and Paul Garner. But cracks start to appear early on. The success of the mission depends on the highest-risk assets being purchased with the funds – as these pay the highest “commissions”. But Biggar is a bad guy with a bit of a conscience, and he insists that some proper, prudent investments should also be made. This, of course, impacts on XXXX’s profits, so pretty soon Biggar “disappears” – never to be heard of again. Garner is seriously rattled and doesn’t want to end up the same way, so he heads off to work for the Gibraltar regulator – where he knows he’ll be safe as houses, as they’ll never take an interest in this crime. After all, STM Fidecs is one of the biggest employers in Gibraltar (after Betfred, Stan James, Paddy Power, William Hill, Bet 365 and 888 Holdings) – so there’s no risk of any of the perps doing porridge.

XXXX is now free to invest the whole fund (now well over £20 million) in whatever he pleases. So he sticks most of it in the German Dolphin (derelict property loan notes) Fund and cleans up. Trouble is, Richard Reinert of Custom House starts to get suspicious and starts sniffing around – after the worrying sudden disappearances of Biggar and Garner. He lifts the skirts of XXXX’s Trafalgar scam, and finds something rather more sinister than skid marks.

The FBI are a bit busy that day (yet another Blacklist case) so the SFO swings into action. XXXX is arrested. His office searched. The Gibraltar FSC twitches because XXXX’s third in command, Garner, is now working for them, so they turn a blind eye. Avoiding embarrassment, they get friendly local book cookers Deloittes to pop in to inspect STM Fidecs’ books. When Deloittes find out what a load of crap the STM QROPS is filled with, they wag their fingers sternly. Kentish is thoroughly upset (so much so, that he almost – but not quite – passes the fags round).

Now that the Trafalgar Multi-Asset Fund has been suspended – thanks to the hero of the hour: Reinert – Kentish decides to buy Caffrey’s QROPS firm, Harbour (which is full of Phillip Nunn’s Blackmore Global investment scam). Caffrey swans off into the sunset with £1 million burning a hole in his pocket, quietly humming “Oh Danny Boy”.

In the end, the handsome Reinert turns out to be a good guy after all, and gets some of the victims’ money back. (But only just enough to pay the liquidators’ fees!)

I submitted my carefully-typed script to NBC and waited with bated breath. A couple of weeks later their response arrived:

“Dear Miss Brooks, thank you for submitting your script for Blacklist episode “The Pension Scam (No 69)”. We have read your work with interest (and fell about laughing), but we do not feel it would be suitable for our series. Unfortunately, the plot is too far fetched and we do not consider that our viewers would find the story-line plausible. This sort of thing simply doesn’t happen in real life. However, we wish you all the best with your future writing efforts – but just suggest you try to stick to more believable plots.”

Sadly, of course, it was real life. As more than 400 victims will attest. So no more script-writing for me. I will stick to blogs in the future.

The problem with money is that it blows away if you don’t hold it down, tie it up or stuff it down your knickers. That’s why you need to put it somewhere safe: in a shoe box on top of the wardrobe; under your mattress; in the safe or – if you’re feeling really brave – in the bank. Trouble is, left in cash, money shrinks (inflation, charges, moths). This is why so many advisers recommend a platform – aka “somewhere safe” to keep your money.

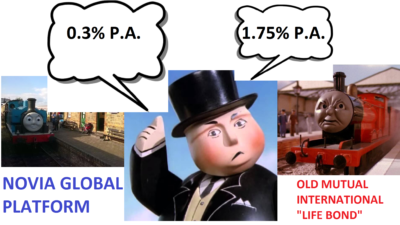

I’ve met Bill Vasilieff who runs Novia Global. He serves Earl Grey and nice biscuits. A man of few words, and even fewer syllables, he gave me a quick rundown on how the Novia Global platform works – and how much it costs.

I haven’t met Peter Kenny of Old Mutual International (OMI) – although I have spoken to him several times. As broadly Irish as Bill is Scottish, Peter Kenny also comes across as a softly-spoken and sincere chap. But there the similarity seems to end. Peter stood me up – I got a view of his office waiting room but wasn’t offered a cup of tea (let alone a biscuit).

Mind you, there isn’t much I don’t know about the Old Mutual International bonds. I’ve seen thousands of their policyholders’ statements – and they are frighteningly ugly and depressing. They accurately, faithfully and unemotionally report the destruction of their victims’ atrocious losses. And OMI regularly (like clockwork!) take their quarterly fees – irrespective of how deep the destruction of the policyholders’ funds is. In fact, some victims even find themselves in negative figures as OMI continue to account for their fees long after the whole blooming lot has gone.

Anyway, back to Bill and his welcoming teapot….I can’t really compare him to Pete but I can compare the two products. So here is a brief and brutal side-by-side line up of what the two “platforms” offer. And how much they cost. And how difficult they are to get out of. And how much financial crime they are associated with.

So the OMI “life bond” costs almost six times as much as the Novia Global platform. But that is if you are locked in for five years. You can get it cheaper – 1.15% – if you get locked in for ten years. But you must remember that if you are scammed, then OMI will have paid the scammer an 8% commission and you could get stuck with paying the quarterly fees for the next ten years, even if you’ve figured out you’ve been scammed. And the quarterly fees are based on your original investment – not on the impaired amount. If you’ve been scammed, and your fund value drops inexorably, the 1.15% will become bigger and bigger. And even if you lose your whole fund, OMI will keep taking their charges and pushing you further and further into debt.

A bit like the lyrics to Hotel California, with an OMI “bond”, you can’t check out any time you want, and you can only leave after between five and ten years. OMI will take that number of years to claw back the commission paid to your adviser – even if you have long since learned that your adviser was an unregulated scammer and has conned you into unsuitable, high-risk, high-commission investments that have badly damaged your fund. You are stuck with paying the quarterly fees to OMI – even after your whole fund has gone. One victim went from plus £300k to minus £25k – and counting. As your funds inside the OMI bond shrink, the 1.15% grows and helps destroy what is left of your fund even faster. But with the Novia Global platform, you can leave any time you want. No exit penalties. No hard feelings.

In Spain, the Supreme Court has ruled that bogus life assurance policies – such as those provided by Old Mutual International – used to hold investments are illegal. This is because they are neither proper insurance policies (which take risk in the interests of the consumer) nor are they proper investment platforms. The Spanish aren’t stupid – they can spot a scam much more easily than other jurisdictions and take action to prevent them from ruining future victims. This is in stark contrast to the likes of the Isle of Man and Gibraltar – which seem to revel in encouraging scams and protecting firms such as Old Mutual International (and STM Group) which facilitate financial crime on a massive scale.

BREXIT is the question on everybody’s lips at the moment. BREXIT: will we? won´t we? deal? no deal? So many unanswered questions and so much scaremongering. We would like to offer some helpful words and hopefully protect you from making rash decisions. This could help you to safeguard your pension. Many scammers are trying to cash in on Brexit – make sure sure you’re not their next victim.

Remember I am not a financial adviser. I am a blogger, and I write about financial crime. I provide information about past scams and on how to avoid falling victim to new scams – especially pension scams. The words I write are aimed to help you safeguard your pension from the many offshore scammers.

So, Expats, what does Brexit mean for your pension rights? The short answer is that we really do not know! There are currently lots of “coulds” and “mights” being thrown around, but no certainties. And herein lies the risk that you and your pension could fall victim to a scam with all this scaremongering.

Firstly, despite Spectrum IFA advertising themselves as “international financial advisers”, with some digging we were able to find out that they DO NOT in fact have an investment licence. This means they are not legally allowed to advise on pensions or investments. Secondly, they scored rather poorly on the qualified and registered percentage too. Out of the 16 advisers we checked up on, only four were registered with the appropriate institutes. The rest came up red – meaning the institute had no record of them.

Worrying isn´t it? Offshore companies can try to claim they are international financial advisers, but actually be unregulated and unqualified to carry out the very service they offer! The “advisory” firms have flash websites, and some have several offices around Europe and beyond. Their PR is great at scaremongering expats about their pension investments in the lead up to Brexit.

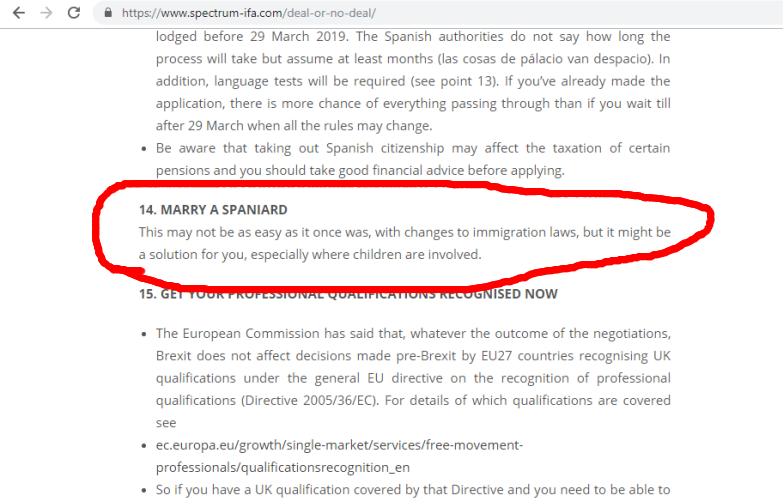

In Spectrum’s ´Deal or no deal´ article number 14, they suggest you marry a Spaniard in order to prepare for Brexit. I´m not sure about you, but I feel that getting hitched to a native to be able to stay in Spain is a pretty drastic measure and definitely more than a little illegal.

Spectrum IFA is just one example of a firm that probably ought to be given a wide berth when transferring your precious pension fund offshore. Safeguard your pension by avoiding unregulated and unqualified firms like this one.

********

It may seem daunting when you read that your UK pension could be subjected to extra taxes if we leave the EU on a no-deal basis. You may be thinking that you should transfer into a QROPS quickly, to save on these taxes. But what you really need to know is that a QROPS is not without punitive costs of its own. They can be expensive and unless you have a good lump sum to transfer you could see a huge chunk of your pension pot taken in transfer and set-up fees anyway! Potentially making you worse off.

Unfortunately, until we make a deal or actually go through with Brexit, nothing is very clear for expats. Which leaves us in an uncertain time and situation. This, I understand, may be daunting for many people, but I urge you to take a deep breath before considering any speedy offshore pension transfers. Thousands of people – especially those who have already fallen victim to scammers such as Continental Wealth Management – would give you exactly the same urgent advice.

If you do want to transfer your pension, please heed this advice to safeguard your pension:

We did a series of blogs last year on offshore companies and their advisers. The results were extremely worrying. Aside from their blatant disregard for the necessity of these qualifications – due to being offshore – the number of unqualified advisers offshore was cause for serious concern. Many of the firms had not one single qualified and registered adviser on their team.

A reputable firm will have a fact-find procedure, and adhere to a client’s risk profile.

A reputable firm will have compliance procedure.

A reputable firm will have clear and consistent explanations and justifications for the use of insurance bonds.

Where will your funds be invested, and how will you know if this is in line with your risk profile?

A pension fund should be placed into a low-medium risk investment.

Scammers tend to go for high-risk, professional-investor-only investments as they offer them the best commissions. But a pension fund should have more protection than this. Avoid investments that involve structured notes (like CWM´s Blue Chip notes), UCIS funds (like Blackmore Global), in-house funds, non-standard assets and any ongoing commission-paying investments.

Insurance bonds – often used by scammers – are usually an unnecessary double wrapper on your fund, that costs you more in fees and charges than a straightforward platform, lining the pockets of the scammers – but making your fund smaller.

How much will the fees and charges be? Remember NO pension transfer is free.

Legitimate firms will normally have a small transfer charge and a small annual fee.

Scammers will often be vague about fees and charges, and avoid giving you a straight answer so they can cover up the true figures. These hidden figures can see your pension fund decrease by 25% or even more in some cases.

A reputable firm should offer you regular updates on the progress of your fund.

You should receive an annual review and a quarterly update showing the fees, charges and growth of your fund.

If your new firm and adviser fail to do this, alarm bells should ring loudly.

Finally, a reputable company will publish evidence to show records of complaints made, rejected or upheld and redress paid.

If the adviser cannot show you all this information, do not trust them.

If it all sounds to good to be true, it probably is – RUN!

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

As is the case with many scams, the victims are unlikely to recoup any of the funds they entrusted to him. Bartlett is said to have spent the hard-earned funds on prostitutes, escorts and expensive holidays. The victims, all of whom knew him on a personal level, are disgusted at his behaviour and were glad to see this scammer jailed.

Here in the Pension Life office, we are always pleased to hear that a scammer has been jailed. The only shame, is that we just don´t hear the words enough. It would be great if we could write blogs that contain the words SCAMMER JAILED on a daily basis. But sadly it is just not the case.

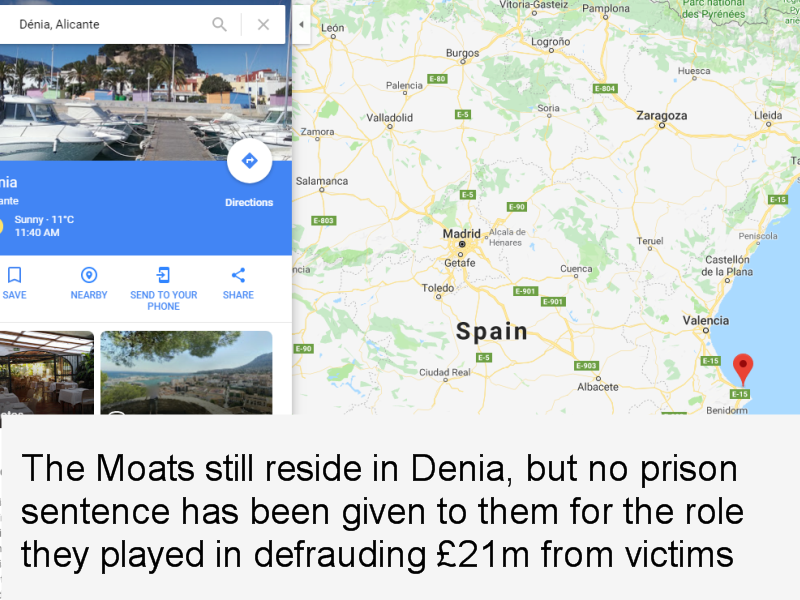

An example of this is Peter and Sara Moat of Fast Pensions – which was wound up back in May 2018. We know they fraudulently took £21m from their victims. We know they did not invest it in the interest of their victims. We know they invested the funds into other businesses they own. We know that they reside in Denia, where their daughter goes to a private school. We know all this – AND the SFO knows all this – yet the Moats are still free to live a lavish lifestyle whilst their victims go without a pension and some face losing their homes as well as bankruptcy.

I´m sure the victims of the Fast Pensions and Blu loans scams would find some solace in reading the words – “scammer jailed” in relation to both Peter Moat and Sara Moat. But I´m not sure if they ever will – and that makes us sad and bloody angry.

Thousands of victims and hundreds of thousands of pounds’ worth of pension money has been fraudulently taken from the victims of scam schemes sold by the above-named scammers. Schemes like Capita Oak, Blackmore Global Fund and the Trafalgar Multi Asset Fund.

All we can do is make a very loud suggestion that STM Group Gibraltar – STM Fidecs – Alan Kentish – should all be given a VERY wide berth when considering a change of pension trustee – as from past evidence they are not to be trusted!

Premier New Earth Recycling and Renewables PLC (in liquidation) is being wound up by Deloittes. Joint liquidators Alexander Cameron Adam and David Peter Craine have written to shareholders to say the directors of NERR aren’t being terribly helpful. Apparently, they are refusing to cooperate with the investigation into why the company failed and are insisting they will only answer questions put to them in writing. Disappointing, perhaps, but not really surprising – scammers rarely “cooperate”.

NERR was a typical investment scam from the outset. The fund was highly speculative, with underlying assets mostly made up of smoke and mirrors, and a bit more smoke (plus quite a bit of rubbish). But to be fair, the published accounts did draw attention to the inherent high risks of the venture failing.

The fund’s assets were equity and unsecured loans in three UK companies:

1. New Earth Solutions Group Limited (“NESGL”)

2. New Earth Solutions Facilities Management Limited (“NESFM”)

3. New Earth Energy Facilities Management Limited (“NEEFM”)

When the liquidators got called in, they valued the investments at “close to nil”. In fact, the only value was probably the paper that the depressing accounts were printed on. Deloittes will, apparently, be trying to uncover why NERR was NEVER going to do anything other than collapse. So that will require a bit of sleuthing to find out who and what was responsible. The liquidators have applied to the court to have the directors questioned under oath. But the directors – who have undoubtedly made a packet out of this scam – will be able to afford top-class lawyers who will help them muddy the waters.

Deloittes have made the usual “we are limited in what information we can share so that we do not prejudice any potential claims” disclaimer to the distressed shareholders. But I find it worrying that Deloittes is being used at all for this job. Deloittes was used to inspect the books and records of STM Fidecs in Gibraltar – and they must surely have uncovered the massive fraud involved in the Trafalgar Multi-Asset Fund (under investigation by the Serious Fraud Office). But no action was ever taken against STM Fidecs. So I am not optimistic that Deloittes will do anything other than push a bit of paper around a desk and submit eye-watering fee invoices.

The Isle of Man Financial Services Authority is paying Deloittes’ fees for the liquidation. For now. However, if the IoM regulator had done its job properly in the first place, they could – and should – have prevented this scam and avoided so many thousands of investors losing their shirts.

Read the published accounts for the NERR Group of companies – and I think you’ll agree this was obviously a dodgy investment right from the start. These accounts were prepared by BDO Stoy Hayward – and you’d have thought they would have known better than to fail to blow the whistle on this collection of companies which was, quite frankly, always bound to fail (at best) and an outright scam (at worst). The writing was always on the public domain wall.

2008 Turnover £3.5mCost of Sales £3.8mAdmin Costs £1.8m

2010 Turnover £6.4mCost of Sales £8.7mAdmin Costs £5m

2012 Turnover £24.8mCost of Sales £25mAdmin Costs £5.8m

2014 Turnover £31.9mCost of Sales £39mAdmin Costs £1.7m

However noble, environmentally friendly and ethical the concept of turning rubbish into clean energy may sound in theory, this commercial venture was never commercially viable. In fact, looking at the ever-increasing gross losses from 2008 to 2014: from £0.3m in 2008 to £7m in 2014 – and a total spent on “admin costs” of £14.3m – any half-decent accountant or auditor would have blown the whistle long before 2016.

Pumping more and more investment into this hopeless venture was only ever going to prolong the inevitable. An unprofitable venture is an unprofitable venture – no more and no less. The directors will, naturally, have got fat and rich, but the investors will have lost large chunks of their life savings.

The name “Premier” will, of course, strike a chord with victims of Stephen Ward’s Premier Pension Solutions. Since at least 2010, thousands of victims have lost their pensions to Ward. However, in this case there seems to be no link between the Premier Group investment scam, and Ward’s Premier Pension scam. However, one of Premier Group’s other scams – in addition to the recycling scam – was the Eco Resources Fund which invested in bamboo plantations in Nicaragua. Which sounds awfully similar to the Reforestation Group fund that Ward was peddling in the London Quantum pension scam. This fund was purportedly based on Brazilian eucalyptus trees and land used for plantations. Only it seems there were no eucalyptus trees. And no land.

In total, around 3,250 investors lost almost £300m in the Premier Group investment scam. A great shame it took the Isle of Man regulator eight years to figure out what was going on under its own nose. But then the regulator has a long track record of ignoring financial crime and those who facilitate it – and ignoring it is the same thing as encouraging it. Personally, I would put the IoM regulator in the same category as the Gibraltar regulator: inept and bent – taking no action against scammers or those who facilitate scams.

And, of course, Old Mutual International had a big hand in helping to facilitate the Premier Group scam as this fund was offered on the OMI platform. Had Old Mutual International done even the most basic bit of due diligence, they would have seen it was an obvious scam and more than likely to result in investors losing their money.

The Premier Shareholder’s Group, a campaign group for investors, said Premier Group had paid large commissions to “unqualified and unlicensed” introducers to target pensioners by promoting their funds to low-risk investors. This campaigning group also claims investors were locked in with “punitive” exit fees, often as high as 30%, which they were not told about when they signed up.

Former director of Premier Group – John Bourbon – has apparently denied accusations of mis-selling and mis-representation and is quoted as saying: “It is highly unlikely that anybody could have a significant investment in Premier Group without understanding the risk”. He has also insisted all fees and charges were clearly set out in the offer document that investors were required to sign to confirm their status as “experienced investor”. Bourbon has also moaned that the regulatory action was “something of a witch hunt”.

So, in summary, you’ve got all the same old same old symptoms of yet another scam:

Hopeless, commercially-unviable venture which hasn’t a hope of ever succeeding

Bent introducers and unregulated advisers flogging the high-risk investment to low-risk clients

Huge commissions and punitive exit penalties

Victims conned into signing up as “experienced investors”

Until and unless regulators and crime enforcement agencies make an example out of the scammers who operate such investment scams, nothing is going to change. And until and unless life offices such as Old Mutual International are sanctioned for offering such scams, unscrupulous and commission hungry “advisers” are going to keep on peddling such toxic wares to unsuspecting victims.

The one thing that could stop these kinds of scams from getting off the ground would be to ban commissions offshore and mirror the principles of British RDR. Financial advice can never be truly independent if commissions are payable – whether for useless, expensive insurance bonds, or toxic, expensive investment funds such as Premier New Earth Recycling and Renewables (NERR).

USEFUL CONTACT DETAILS:

nerrenquiries@deloitte.co.uk.

http://www.deloitte-insolvencies.co.uk/kr/new-earth-recycling-and-renewables-(infrastructure)-plc.aspx

Alex Adam: acadam@deloitte.co.uk

David Craine: dcraine@burleigh.co.im

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors Old Mutual International, or a marketing machine. I read with interest the recent IA Industry Most Influential Top 100 described by IA thus: “we at International Adviser decided to shine a light on the movers and shakers that have helped this industry get to where it is today”.

But where exactly is the industry today? And have the so-called top 100 moved and shaken the industry in a helpful way or a detrimental way? To find out, why don’t we have a look at a few of the “influencers”. To get the measure of them, let’s put them into a game of “Have I Got News For You”:

Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based Investors Trust until recently appointed chair of the Association of International Life Offices, the trade body for international life offices. During his 35 years of experience in financial services, he facilitated the scam run by Phillip Nunn of Blackmore Global and David Vilka of Square Mile International Financial Services. Investors Trust accepted over 1,000 investments into illegal UCIS funds for UK-based victims scammed into QROPS with Integrated Capabilities and Harbour (now STM).

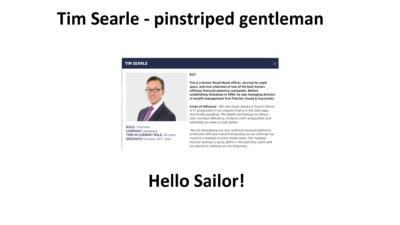

As Captain of the Navel Team, let’s have dashing Tim Searle – Chairman of Dubai-based Globaleye. With his eight-year Naval history, he should make an ideal leader and would come in particularly useful in the event of icebergs, torpedos or sharks.

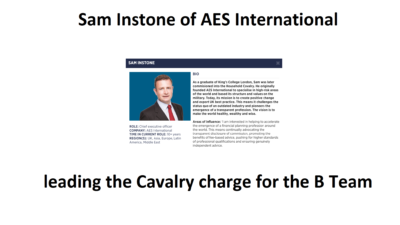

Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

On the Army Team, we’ll have international wealth and regulatory specialist, Phil Billingham. Phil must be utterly disgusted with the likes of Stephen Ward (another fully-qualified adviser) messing up the reputation of the profession by running a long series of pension scams and ruining thousands of lives.

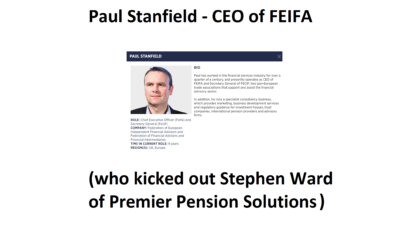

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated Stephen Ward of Premier Pension Solutions from FEIFA to loud cheers from victims and industry professionals alike. (My only gripe with him would be that he still hasn’t kicked out Square Mile Financial Services run by scammers John Ferguson and David Vilka).

On the Navel Team we’ll have Geraint Davies of Montfort International – an expert IFA specialising in international financial services, and Roger Berry of Concept Group Trustees in Guernsey. These two chaps also have, between them, extensive experience of Stephen Ward in their own ways and will, no doubt, have much to talk about.

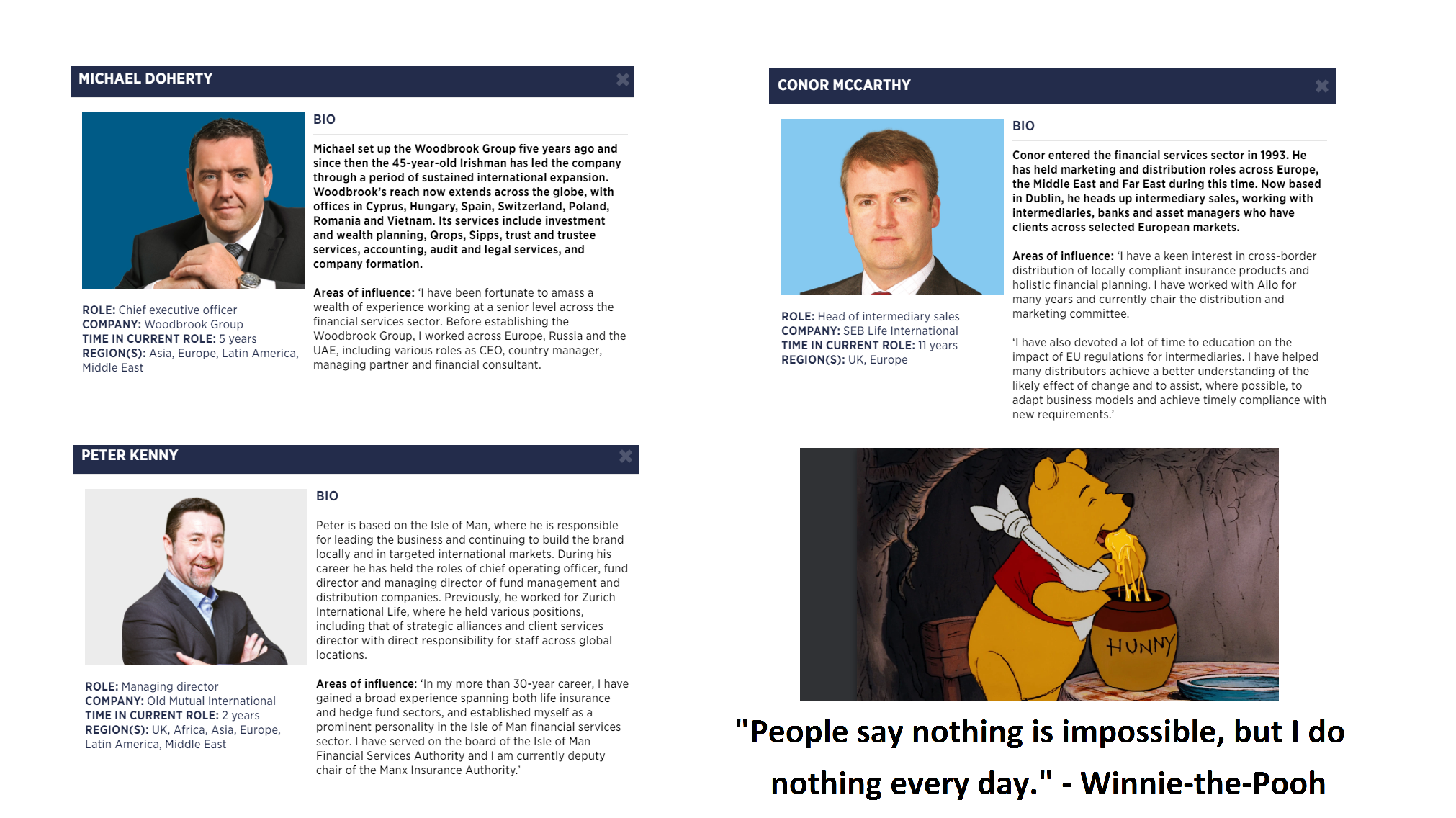

The contest will be to spot the “odd one out”: Michael Doherty of Woodbrook Group, Conor McCarthy of SEB, Peter Kenny of OMI and Winnie-the-Pooh.

Tim Searle: “They’re all Irish, except Winnie-the-Pooh who’s English?”

Geraint Davies: “They all hate Angie except Winnie-the-Pooh who’s never heard of her?”

Roger Berry: “They all love Angie except Winnie-the-Pooh who’s never heard of her?”

Sam Instone: “They’ve all got names that end in Y except Winnie-the-Pooh?”

Phil Billingham: “They’re all involved in money except Winnie-the-Pooh who’s involved in honey?”

Paul Stanfield: “None of them have applied to be members of FEIFA except Winnie-the-Pooh?”

Bob Pain: “No, you’re all wrong. The answer is Peter Kenny of OMI. The other three have been doing “nothing”: Michael Doherty was employing ex CWM scammers Dean Stogsdill and Neil Hathaway (known as Dog Kill and Hadaway) but claimed he was paying them nothing; Conor McCarthy of SEB has been asked numerous times for his comments on why SEB allowed the scammers at CWM to invest most of their victims’ funds in toxic structured notes, but McCarthy is saying nothing and won’t reply; and Winnie-the-Pool is doing nothing all the time.

The odd one out is Peter Kenny who is doing “something” and is suing Leonteq for the £94 million worth of fraudulent structured notes they sold to OMI.

Having the highest possible regard for lawyers in general, and JMW Solicitors in particular, it is good to report that there is now a dialogue in progress which will hopefully result in Dolphin Trust producing a copy of the audited accounts. An excellent outcome would also be the repayment of the loan notes.

JMW Solicitors appears to be a promising outfit – especially as their website states: “No matter who you are or what you need, you can be assured of a great personal service from us.” As we need a copy of the Dolphin Trust audited accounts and the return of the money that Dolphin Trust borrowed (unsecured) from hundreds of pension and investment scam victims, I hope this promised great personal service will extend to a prompt and hassle-free resolution to the Dolphin Trust lenders’ problem.

The lawyer from JMW acting for Dolphin Trust – Nick McAleenan – has championed the cause of the supermarket chain: Morrisons.

MORRISONS DATA LEAK CASE – MORRISONS HELD LIABLE IN LANDMARK COURT RULING

JMW is representing thousands of claimants in a legal action for compensation against Morrisons Supermarkets.

The case is the leading legal case in the UK concerning “data breach”. It relates to the unauthorised copying and disclosure of Morrisons payroll information by a disgruntled ex-employee. In 2017, the High Court ruled that Morrisons is legally responsible for the data breach. In 2018, Morrisons appealed the High Court’s judgment, but the Court of Appeal dismissed Morrisons’ appeal. Further legal proceedings will take place to determine what compensation must be paid to the victims.

Nick McAleenan clearly has genuine empathy for the awful ordeal suffered by the Morrisons victims who had to undergo the trauma of having their privacy violated.

I sincerely hope this will translate into similar empathy for scam victims whose life savings have been “loaned” to his clients: Dolphin Trust.

If Nick (interesting name!) wants any clarification about how these scam victims compare to the Morrisons supermarket victims, he might want to have a chat with some of the victims of the STM Fidecs Trafalgar Multi-Asset Fund scam.

TPR has been neither coy nor shy in its published determination against Ward and Salih – and has openly called the London Quantum pension scheme, and the risky investments which Ward made, a “scam”.

But to any reasonable person’s mind, tPR’s determination in relation to Ward and London Quantum raises more questions than it answers. In fact, I would go even further and say that HMRC’s and tPR’s incompetence – as well as Dalriada Trustees‘ own failings – should be examined in parallel with Ward’s multiple frauds.

Because, make no mistake, London Quantum was only one of many.

It all started long before the Ark Pensions scam. Ward set out his stall transferring pensions to New Zealand and liberating 100% “tax free”. He boasted in the local Costa Blanca press that he had “helped” thousands of clients liberate their pensions (legally). Of course, this may have been free of tax in New Zealand, but when the Spanish tax authorities catch up with these clients, there will be a very expensive disaster.

It is extremely worrying that IVCM – a “phoenix” of the Brooklands disaster – is also offering the same New Zealand liberation facility today. It always worries me when firms fail to learn the lessons of past scams and expose unsuspecting victims to the same catastrophes that past scammers orchestrated. Add to this the fact that IVCM is regulated out of Gibraltar – the jurisdiction of choice for scammers such as XXXX XXXX and STM Fidecs – and I think it is well worth giving IVCM a very wide berth.

Prior to 2010, Ward was a tied agent of Inter Alliance – a company based in Cyprus which had an insurance license. For Inter Alliance in Cyprus, Ward successfully created the illusion that this gave his company Premier Pension Solutions some sort of license. But, in reality, it did not – as the Cyprus license was only for Inter Alliance and not for any other entity. Plus tied agents were (and still are) illegal in Spain.

As a sideline, Ward was flogging EEA Life Settlements as he had discovered the delights of making huge commissions out of dodgy, risky, illiquid investments to his unsuspecting victims. In 2010, Ward was working closely with Concept Trustees in Guernsey – run by Roger Berry. Initially happy to see Concept Trustees’ QROPS members have 100% of their pensions invested by Ward in EEA, Berry eventually realised that Ward’s firm was not regulated as it had been dumped by Inter Alliance. Of course, even before it had been dumped, Premier Pension Solutions wasn’t regulated anyway. But Concept Trustees was too stupid to realise that.

Concept then wrote to all the members who were clients of Ward’s Premier Pension Solutions and warned them that Ward’s firm was neither regulated nor had any professional indemnity insurance cover. Berry claimed he would not be accepting any further investment instructions from Ward, but this was basically just a load of hot air (aka lying) as he continued to accept investment instructions into EEA by Ward.

In September 2010, Premier Pension Solutions was appointed as a tied agent of AES International – a firm based in London and Dubai. The agency agreement covered PPS for investment and insurance business – but not pension transfer business. Ward’s PPS letterheaded paper claimed that it was a “partner” of AES and that it was regulated by the DGS (Spanish insurance regulator) and CNMV (Spanish investment regulator). PPS also became a member of FEIFA – the Federation of European Independent Financial Advisers (although he was later dumped by them). You can understand why so many victims thought that PPS was a bona fide advisory firm.

Then came the first of Ward’s major pension scams: Ark. It is worth looking at the history of Ark because this sets the scene for how nearly 500 victims came to lose their pensions and face tax liabilities – as well as the dozens of further scams operated by Ward (including London Quantum).

A famous footballer and his mate – a football club owner – bought a plot of land in Larnaca in Cyprus with a view to turning it into a golf resort. They paid £1.1 million for the property, but then realised it wasn’t big enough for a whole golf course (neither of them was bright enough to be able to count up to 18) and so they tried to find some other investors. The chumps they tried to con into buying more land adjacent to the original plot either couldn’t come up with the money or were frightened off such a high-risk, illiquid investment.

So the sporty pair went to see the footballer’s accountant – Andrew Isles of Isles and Storer (now owned by LB Group). Isles soothed the sporty pair’s worries by telling them that securing more investors was simple: just start a pension fund! He introduced them to what he called “two leading pension experts”: Craig Tweedley and Stephen Ward. Tweedley was already operating the KJK Investments/G Loans pension liberation scam (later to be placed in the hands of Dalriada Trustees by the Pensions Regulator) and Ward was a highly-qualified pensions expert, examiner and author.

The rest is history as nearly 500 victims lost their pensions to the Ark scam. But the sporty pair did very nicely – they sold the land in Cyprus to the Ark scheme for £4 million and pocketed the profit. The footballer tried to hide the money in Dubai but got caught and turned Queens Evidence. He and the other original investor (the football club owner) fell out and they ended up in court against each other – with the footballer triumphing. Andrew Isles also did very nicely as he sold introductions to a number of his clients and earned fat commissions in doing so.

As Ark unfolded – between mid 2010 and mid 2011 – Ward initially acted as an introducer. There were various introducers – many recruited by Ward when he ran a series of seminars in various parts of the UK. But Ward himself was the biggest introducer – accounting for more than a third of the whole £27 million fund and earning approaching three quarters of a million pounds in fees (the Pensions Regulator’s report of £350k was way off the mark).

Ward and his sidekick – bent lawyer Alan Fowler of Stevens and Bolton Solicitors – acted as the controlling minds behind Ark. The scheme documentation and the “loan” contracts were drawn up and explained by Ward and Fowler. Of the 5% commission charged by Craig Tweedley, Ward got at least 2% plus a transfer fee. But Ward had his eye on a much bigger proportion of the fees. Towards the end of the life of Ark, Ward was preparing to take Ark over from Tweedley – along with an associate of his: Peter Moat (another pension crook who went on to operate the Fast Pensions scam – now also in the hands of Dalriada Trustees). In a way, it was a shame that didn’t happen, as Tweedley did at least try to help the Ark victims, whereas Ward never lifted a finger. In fact, he simply told the Ark victims to throw the tax demands away as “HMRC would never pursue them”.

In February 2011, HMRC met with Tweedley and Ward to discuss the “loans” – so HMRC knew perfectly well that Ward was the main brain behind the scam. It is, therefore, astonishing that they did nothing to stop him operating so many further pension scams.

Ark came to a shuddering halt on 31st May 2011, when tPR appointed Dalriada Trustees and the scheme was suspended. Dalriada went up to Yorkshire to confront Crag Tweedley and relieve him of all the evidence and files relating to the scam. Tweedley told Dalriada that all the records were held down at Ward’s Manchester office at 31, Memorial Road and he drove down to collect them from Anthony Salih. He arrived to find Salih removing all the Premier Pension Solutions fee agreements on the instructions of Ward (he managed to shred most of them – but did missed a few which I now have).

After Ark, Ward went on to run the Evergreen Retirement Benefits QROPS scam with accompanying 50% “loans” and a further 300 victims lost £10 million worth of pensions. HMRC removed Evergreen from the QROPS list when they realised it was a liberation scam and Ward fell back on two more UK-based, bogus occupational schemes: Southlands and Headforte. Plus, he registered a number of new schemes – including Capita Oak.

The Capita Oak scheme was another bogus occupational scheme registered by Ward with a fictitious sponsoring employer: RP Medplant (Cyprus). There is, however, a firm called RP Med Plant in Cyprus. The Capita Oak trust deed was written by Ward’s bent lawyer Alan Fowler. Ward took responsibility for the transfer administration – transferring valuable personal and final salary occupational pensions into this scam – in the full knowledge that he was condemning hundreds of victims to certain financial ruin and poverty in retirement. Capita Oak is now also in the hands of Dalriada Trustees.

Other pension scams that Ward was operating – in addition to Southlands and Headforte – from 2012 onwards included Feldspar, Hammerley, Meribel, Halkin, Randwick, Bollington Wood and Westminster. And, of course, Dorrixo Alliance which was the trustee for many of these scams. Capita Oak and Westminster are both under investigation by the Serious Fraud Office.

How much more evidence do they need?

In May 2014, HMRC was given evidence of all of Ward’s various scams – including Dorrixo Alliance. They were also given detailed testimony by me and a number of victims of what Ward had been up to in the pension liberation fraud industry since Ark. It would have been very easy for HMRC to look up to see what other pension schemes Dorrixo was trustee to. Had they done this, they would have seen that Dorrixo was the trustee for the London Quantum scheme. If HMRC had taken any action, they could have prevented Mr. N – a serving police officer – and 96 other victims from losing their pensions to Ward and his various dodgy, inappropriate investments (including loans to Dolphin Trust).

If we add to the above catalogue of scams the Continental Wealth Management scam – 1,000 victims facing the loss of £100 million worth of life savings – Ward has been responsible for the destruction of thousands of people’s pensions this past eight years. Plus several suicides and deaths from stress-related medical conditions.

SERIOUS QUESTIONS ARISING FROM THE PENSIONS REGULATOR’S DETERMINATION RE:

Mr Stephen Alexander Ward – The Pensions Regulator case ref: C46205159

Ward was a director of Dorrixo from 13 October 2011 to 28 April 2015. A company called Quantum Investment Management Solutions LLP (“QIMS”) has at all material times been the sole sponsoring employer of the Scheme. Dorrixo became the sole trustee of the Scheme on 19 April 2014. Dorrixo is also recorded as being the Scheme administrator.

HMRC AND TPR WERE GIVEN EVIDENCE OF WARD’S COMPANY, DORRIXO, IN MAY 2014. THEY WERE ALSO GIVEN EVIDENCE OF A LARGE NUMBER OF SCAMS WARD OPERATED AFTER ARK – ALL INVOLVING LIBERATION FRAUD. WHY WASN’T ACTION TAKEN TO PREVENT LONDON QUANTUM? ALL 97 VICTIMS – INCLUDING A SERVING POLICE OFFICER – COULD HAVE BEEN PREVENTED.

On 18 June 2015 the Regulator appointed Dalriada Trustees Limited (“Dalriada”) as an independent trustee to the Scheme, with exclusive powers.

HAS ONE SINGLE PENNY EVER BEEN RETURNED TO ANY OF THE PENSION SCAMS PLACED IN THE HANDS OF DALRIADA TRUSTEES? THERE ARE DOZENS OF THEM, AND FEW – IF ANY – OTHER INDEPENDENT TRUSTEES ARE EVER APPOINTED BY TPR. BUT THERE SEEMS TO BE NO RECORD OF ONE SINGLE MEMBER EVER GETTING ANY RETURN FROM ANY OF THE SCHEMES IN THE PAST EIGHT YEARS – DESPITE THE MANY MILLIONS DALRIADA HAVE PAID THEMSELVES FROM THESE SCHEMES.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

AS THIS EVIDENCES THAT THIS SCAM COULD EASILY HAVE DWARFED ARK IN A VERY SHORT SPACE OF TIME, DON’T HMRC AND TPR RECOGNISE THAT THEIR LAZINESS AND NEGLIGENCE NEED TO BE ADDRESSED? THEY LEARNED NOTHING FROM ARK – AND WHILE THERE ARE VALID CRITICISMS OF WARD FOR HAVING LEARNED NOTHING, HE IS JUST A COMMON SPIV WHILE HMRC AND TPR ARE SUPPOSED TO BE GOVERNMENT DEPARTMENTS WITH A RESPONSIBILITY TO PROTECT THE PUBLIC. THE SCALE OF THIS SCAM SHOWS THESE TWO ORGANISATIONS ARE NOTHING BUT HOPELESSLY INEPT AND AMATEURISH IN THEIR APPROACH TO DILIGENCE AND PUBLIC RESPONSIBILITY.

The Scheme was promoted to potential new members by introducers. These included the following entities: GoBMV; Baird Dunbar; What Partnership; the Resort Group PLC; Friendly Investments; Premier Mark Consultants and Quantum Wealth Management Solutions Limited.

THE DANGERS OF THE SCOURGE OF “INTRODUCERS” SHOULD HAVE BEEN LEARNED FROM THE ARK SCAM IN 2011. WARD RECRUITED DOZENS OF THEM ALL OVER THE COUNTRY. AND YET NONE OF THEM HAS EVER BEEN BROUGHT TO JUSTICE FOR THEIR PART IN ARK, AND HAVE GONE ON TO OPERATE AS INTRODUCERS AND EVEN HOLD KEY CENTRAL ROLES IN LATER SCAMS. THIS INCLUDES FRIENDLY INVESTMENTS AND JULIAN HANSON – WHOSE SCHEMES ARE NOW ALSO IN THE HANDS OF DALRIADA TRUSTEES.

Gerard was responsible for producing template risk letters, member application forms, pro forma declarations stating that the person signing them was a self-certified sophisticated investor, member booklets and the statement of investment principles (of which there were four versions). Gerard sent these documents to members once they had been introduced to the Scheme by an introducer.

GERARD ASSOCIATES, RUN BY GARY BARLOW, HAD ACTED AS AN INTRODUCER TO WARD IN THE ARK SCAM. AND YET HE WAS LEFT FREE TO OPERATE IN THE SAME CAPACITY IN THE LONDON QUANTUM SCAM – AND EVEN TAKE ON A MORE CENTRAL ROLE. GERARD ASSOCIATES WAS AT THE TIME AN FCA-REGULATED FIRM – AND REMAINS SO TO THIS DAY. THE FCA HAS TAKEN NO ACTION TO REMOVE THIS FIRM OR TAKE ANY ACTION AGAINST GARY BARLOW.

GERARD ASSOCIATES’ GARY BARLOW WAS PAID £253,000 FROM THE LONDON QUANTUM SCHEME FOR DEFRAUDING VICTIMS INTO SIGNING AGREEMENTS THAT THEY WERE “SOPHISTICATED” INVESTORS. SO WHY HASN’T BARLOW BEEN PROSECUTED AND JAILED – AND MADE TO PAY THIS MONEY BACK TO THE VICTIMS?

A material number of the new members had a low or medium appetite for investment risk and, in any event, were unaware that the Scheme’s investments were high-risk investments. The Panel was troubled by the apparent disconnect between members’ appetite for risk and the high risk nature of the investments made by Dorrixo. Mr Ward accepted that the Scheme’s investments were high risk, but claimed this was made clear to new members in the Member Booklet.

I DON’T KNOW WHAT SORT OF DRUNKEN DUMMIES MADE UP TPR’S “PANEL”, BUT DID THEY SERIOUSLY THINK THAT ANY PENSION FUNDS SHOULD EVER INVEST IN HIGH-RISK CRAP? INDIVIDUAL MEMBERS’ APPETITE FOR INVESTMENT RISK IS IRRELEVANT – THIS WAS A PENSION FUND, NOT A CASINO.

The case against Ward was based on failures of competence and capability, and also a lack of honesty and integrity as well as Ward’s involvement with “pension liberation” as an introducer of members to the “Ark” schemes.

BUT TPR AND HMRC KNEW ALL ABOUT THIS BACK IN 2010 AND 2011. WHY DID THEY DO NOTHING TO PREVENT WARD FROM SCAMMING MORE VICTIMS OUT OF MORE MILLIONS OF POUNDS. THEY STOOD BACK AND WATCHED – DESPITE HAVING HARD EVIDENCE THAT HE WAS STILL UP TO HIS CRIMINAL MISCHIEF.

Mr Ward did not dispute that a company of his (Premier Pensions Solutions SL) was involved in introducing members to the Ark Schemes, but states that the relevant activity pre-dated any finding by the courts of pensions liberation and that Mr Ward had no knowledge that the schemes were being used for such activity.

BUT HMRC, TPR AND DALRIADA ALL KNOW THIS ISN’T TRUE. THEY HAVE ALL SEEN EVIDENCE THAT WARD AND HIS BENT LAWYER ALAN FOWLER ACTUALLY PRODUCED THE “LOAN” (MPVA) DOCUMENTATION AND EXPLAINED THE LOANS IN SOME CONSIDERABLE DETAIL TO THE VICTIMS. THE MPVA CONTRACTS WERE DRAWN UP BY FOWLER. IS IT REALLY CREDIBLE THAT NEITHER HMRC NOR TPR WOULD HAVE OBJECTED TO THIS STATEMENT?

The Panel did not consider there was sufficient evidence of Ward having actual knowledge of, or turning a blind eye to, the illegal nature of the activity of the Ark Schemes when carrying out his role as introducer before.

SERIOUSLY? I HAVE GIVEN EVIDENCE OF THIS TO BOTH HMRC AND TPR ON MANY OCCASIONS. THIS HAS BEEN DISCUSSED AT MEETINGS WITH DALRIADA TRUSTEES ON MANY OCCASIONS. EVIDENCE OF THIS HAS BEEN GIVEN TO THE SERIOUS FRAUD OFFICE ON MANY OCCASIONS BY VARIOUS VICTIMS AND ME. WHAT FURTHER EVIDENCE DID THE PANEL WANT? EVERY ARK MEMBER’S FILE WAS FULL OF SUCH EVIDENCE. EITHER TPR IS LYING OR IT IS INCOMPETENT. OR BOTH.

The Case Team also relied on certain alleged failures in relation to other pension schemes (called Headforte and Halkin), of which Mr Ward was a trustee. These are denied by him (e.g. an allegation of failure to appoint an auditor to those schemes) and the Panel did not consider it necessary to make findings in respect of them.

SO WHAT ACTION HAS TPR TAKEN IN RELATION TO HEADFORTE AND HALKIN? BOTH WERE BEING USED FOR PENSION LIBERATION FRAUD BY WARD – AND YET THE VICTIMS PROBABLY STILL HAVE NO IDEA WHAT HAS HAPPENED TO THEIR MONEY. IT IS ABSOLUTELY ASTONISHING THAT NO ACTION HAS BEEN TAKEN IN RELATION TO THESE TWO SCHEMES, PLUS ALL THE OTHERS WARD HAS BEEN OPERATING OVER THE YEARS.

Stephen Alexander Ward (date of birth 11 July 1955) is hereby prohibited from being a trustee of trust schemes in general. This order has the effect of removing the above-named individual from all or any schemes of which he is a trustee. By section 6 of the Pensions Act 1995, any person who purports to act as a trustee of a trust scheme whilst prohibited under section 3 is guilty of an offence and liable (a) on summary conviction to a fine not exceeding the statutory maximum, and (b) on conviction on indictment to a fine or imprisonment or both.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

THIS IS NOT JUST THE DEATH OF TRUST, BUT OF ANY CONFIDENCE IN THE GOVERNMENT, REGULATORS AND CRIME PREVENTION AGENCIES TO PREVENT OR DEAL WITH PENSION SCAMS AND SCAMMERS.

Much as a master illusionist takes your breath away with his magic, a

Much as a master illusionist takes your breath away with his magic, a

Blacklist – “The Pension Scam (No 69)”

Blacklist – “The Pension Scam (No 69)” than one scam at a time (being male, he can’t multi-task).

than one scam at a time (being male, he can’t multi-task). Kentish is eager to know how much money can be made out of this plot. XXXX explains that 46% was earned out of his Capita Oak and Henley scams and that he hopes to make at least as much out of this one. With Kentish’s “help” (nudge nudge, wink wink). Of course, the proceeds could be split and plenty of brown envelopes used to disguise the handing over of the proceeds.

Kentish is eager to know how much money can be made out of this plot. XXXX explains that 46% was earned out of his Capita Oak and Henley scams and that he hopes to make at least as much out of this one. With Kentish’s “help” (nudge nudge, wink wink). Of course, the proceeds could be split and plenty of brown envelopes used to disguise the handing over of the proceeds. Now that the Trafalgar Multi-Asset Fund has been suspended – thanks to the hero of the hour: Reinert – Kentish decides to buy Caffrey’s QROPS firm, Harbour (which is full of Phillip Nunn’s Blackmore Global investment scam). Caffrey swans off into the sunset with £1 million burning a hole in his pocket, quietly humming “Oh Danny Boy”.

Now that the Trafalgar Multi-Asset Fund has been suspended – thanks to the hero of the hour: Reinert – Kentish decides to buy Caffrey’s QROPS firm, Harbour (which is full of Phillip Nunn’s Blackmore Global investment scam). Caffrey swans off into the sunset with £1 million burning a hole in his pocket, quietly humming “Oh Danny Boy”. Sadly, of course, it was real life. As more than 400 victims will attest. So no more script-writing for me. I will stick to blogs in the future.

Sadly, of course, it was real life. As more than 400 victims will attest. So no more script-writing for me. I will stick to blogs in the future.

The problem with money is that it blows away if you don’t hold it down, tie it up or stuff it down your knickers. That’s why you need to put it somewhere safe: in a shoe box on top of the wardrobe; under your mattress; in the safe or – if you’re feeling really brave – in the bank. Trouble is, left in cash, money shrinks (inflation, charges, moths). This is why so many advisers recommend a platform – aka “somewhere safe” to keep your money.

The problem with money is that it blows away if you don’t hold it down, tie it up or stuff it down your knickers. That’s why you need to put it somewhere safe: in a shoe box on top of the wardrobe; under your mattress; in the safe or – if you’re feeling really brave – in the bank. Trouble is, left in cash, money shrinks (inflation, charges, moths). This is why so many advisers recommend a platform – aka “somewhere safe” to keep your money.

A bit like the lyrics to Hotel California, with an OMI “bond”, you can’t check out any time you want, and you can only leave after between five and ten years. OMI will take that number of years to claw back the commission paid to your adviser – even if you have long since learned that your adviser was an unregulated scammer and has conned you into unsuitable, high-risk, high-commission investments that have badly damaged your fund. You are stuck with paying the quarterly fees to OMI – even after your whole fund has gone. One victim went from plus

A bit like the lyrics to Hotel California, with an OMI “bond”, you can’t check out any time you want, and you can only leave after between five and ten years. OMI will take that number of years to claw back the commission paid to your adviser – even if you have long since learned that your adviser was an unregulated scammer and has conned you into unsuitable, high-risk, high-commission investments that have badly damaged your fund. You are stuck with paying the quarterly fees to OMI – even after your whole fund has gone. One victim went from plus  In Spain, the Supreme Court has ruled that bogus life assurance policies – such as those provided by

In Spain, the Supreme Court has ruled that bogus life assurance policies – such as those provided by

Worrying isn´t it? Offshore companies can try to claim they are international financial advisers, but actually be unregulated and unqualified to carry out the very service they offer! The “advisory” firms have flash websites, and some have several offices around Europe and beyond. Their PR is great at scaremongering expats about their pension investments in the lead up to Brexit.

Worrying isn´t it? Offshore companies can try to claim they are international financial advisers, but actually be unregulated and unqualified to carry out the very service they offer! The “advisory” firms have flash websites, and some have several offices around Europe and beyond. Their PR is great at scaremongering expats about their pension investments in the lead up to Brexit.

Know all the correct questions to ask an adviser before you sign on the dotted line.

Know all the correct questions to ask an adviser before you sign on the dotted line.  How much will the fees and charges be? Remember NO pension transfer is free.

How much will the fees and charges be? Remember NO pension transfer is free.

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

AND to rub salt into the wounds of the Trafalgar victims,

AND to rub salt into the wounds of the Trafalgar victims,

1. New Earth Solutions Group Limited (“NESGL”)

1. New Earth Solutions Group Limited (“NESGL”) Deloittes have made the usual “we are limited in what information we can share so that we do not prejudice any potential claims” disclaimer to the distressed shareholders. But I find it worrying that Deloittes is being used at all for this job. Deloittes was used to inspect the books and records of

Deloittes have made the usual “we are limited in what information we can share so that we do not prejudice any potential claims” disclaimer to the distressed shareholders. But I find it worrying that Deloittes is being used at all for this job. Deloittes was used to inspect the books and records of  However noble, environmentally friendly and ethical the concept of turning rubbish into clean energy may sound in theory, this commercial venture was never commercially viable. In fact, looking at the ever-increasing gross losses from 2008 to 2014: from £0.3m in 2008 to £7m in 2014 – and a total spent on “admin costs” of £14.3m – any half-decent accountant or auditor would have blown the whistle long before 2016.

However noble, environmentally friendly and ethical the concept of turning rubbish into clean energy may sound in theory, this commercial venture was never commercially viable. In fact, looking at the ever-increasing gross losses from 2008 to 2014: from £0.3m in 2008 to £7m in 2014 – and a total spent on “admin costs” of £14.3m – any half-decent accountant or auditor would have blown the whistle long before 2016. The name “Premier” will, of course, strike a chord with victims of

The name “Premier” will, of course, strike a chord with victims of  And, of course,

And, of course,

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors

International Adviser really can’t make up its mind whether it is organising a piss-up in a brewery, a news roundup carefully slewed in favour sponsors Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based

Bob Pain in the chair as quiz master. A bloke who ran Cayman Islands-based  Capabilities and Harbour (n

Capabilities and Harbour (n Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

Captain of the Army Team I nominate as Sam Instone of AES International. His experience as an Army officer should give him the leadership skills to oppose the Navel Team. Sam’s track record as the “enemy of traditional financial services” should give him the basis for a sound battle plan.

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated

And the final member of the Army team will be Paul Stanfield, CEO of FEIFA (Federation of European Independent Financial Advisers). Another real gentleman – and handsome to boot – and one who understands the importance of outlawing scammers. Several years ago he excommunicated

The lawyer from JMW acting for Dolphin Trust – Nick McAleenan – has championed the cause of the supermarket chain: Morrisons.