As the decade comes to a close, it is clearer than ever that victims of investment fraud need justice. The dirtiest stain on society is that of pension and investment fraud. Scammers have made fortunes out of pension and investment scams in the UK and across the globe – in all leading expat jurisdictions. With little sign of this international crime abating, scammers continue making fortunes out of relieving people of their life savings.

The FCA managed to get out of bed (briefly) to bring to justice the scammer behind the Dynamic £600k investment scam. But completely overlooked over £1 billion worth of other investment scams.

Meanwhile, the very authorities which should be preventing financial crime – regulators; law enforcement agencies; HMRC; Insolvency Service; government; courts – stand around clueless and helpless. Their inaction is embarrassing and disgusting – especially in the wake of the appalling announcement that Andrew Bailey has been appointed governor of the Bank of England.

Manraj Singh Virdee of Dynamic UK Trades Ltd conned 24 victims out of more than £600,000. His method was to promise returns of 100% for investing in his forex trading and spread betting “expertise”. The FCA brought a case against this criminal who was convicted by Southwark Crown Court. The sentence was only a suspended prison sentence for running an unauthorised investment scheme. However, the court made a confiscation order against Singh Virdee of £171,913 – to be used to compensate the victims. If he doesn’t pay, he will be sentenced to two years in prison.

It is indeed good to know that during a prolonged period of being asleep at the wheel, the FCA can do a wee bit of regulating. But why does Manraj Singh Virdee deserve to be sentenced for defrauding 24 victims out of £600,000 when so many other scammers have got away with defrauding many thousands of victims out of many £ millions?

Victims of Investment Fraud need Justice: In 2020, pressure must be brought to bear on the inattentive, lazy and negligent authorities who have done nothing. It is simply not acceptable to turn a blind eye to so much financial crime. This is especially true when cases like the Singh Virdee one clearly demonstrate that if only they could be bothered, they could actually clean up the scamming industry. But, first, they have to want to do it. And as things stand, there is no evidence that they really do want to.

While this would-be forex trader and spread better faces a couple of years behind bars, the rest of the scammers are still out there scamming away merrily and profitably. Shouldn’t 2020 be the year to make pension and investment scamming illegal? Because as things stand, the scammers know they can get away with it easily.

I “borrowed” this blog from my Twitter friend in Singapore who clearly understands and cares about investment scams – and the inability of the inept authorities to do anything about them. This is true not just in Singapore but throughout the world – particularly the UK, the Isle of Man, Gibraltar, the Cayman Islands, Guernsey, Ireland, Dubai, and Hong Kong.

I could not improve upon his excellent blog, but I have put some comments in red in the body of the text (with apologies to Lee!).

This is a story about how scammers have used the loopholes within the law to fleece hundreds of millions of dollars (and pounds and Euros in other jurisdictions) from an unsuspecting public. Many of whom are retirees and young people venturing into alternative investments for the first time in their lives.

In Singapore, there are two primary agencies that are set up to ensure a safe investment environment for its people. The Monetary Authority of Singapore (MAS) that regulates the financial industry and the Commercial Affairs Department (CAD) of the Singapore Police Force that investigates commercial crime and Fraud.

Just wanted to add a few more: chia seeds, eucalyptus plantations, truffle trees, forex trading, life assurance policies, football betting, property loans, rubbish recycling, litigation funding, timeshares, films, claims management companies etc.

In support of innovation (Lee uses the word “innovation” – but I would have used the word “opportunism”) in the financial industry, Alternative Investment Offers have been allowed to thrive. Non-traditional Products are being offered to the lay public, advertised widely on social media and even in the mainstream media with barely any restrictions. (In the UK, we would refer to many of these as UCIS – unregulated collective investment schemes – which are illegal to promote to retail investors). Many vendors of these make wild claims of double-digit percentage returns per annum, sometimes coupled with apparent full capital protection that targetted investors would just swallow wholesale.

These companies are not regulated by MAS and will often be listed as such in the MAS-issued Investor Alert List. But being on the Investor Alert List simply means Caveat Emptor … nothing more. Legitimate companies, as well as unscrupulous ones, are similarly listed there without distinction. So in most cases, the attractive returns and false assurance of safety are just too irresistible to the average investors who would be pulled in by the hundreds, if not thousands. I reckon few people ever think to look at the MAS website – just as few ever look at the FCA website where well-hidden warnings lurk deep below the surface.

While not all Alternative Investments are dodgy, many of them are because the current law offers a fairly wide window (between 3 to 8 years) for them to operate before the law catches up. Why? Because the law enforcement agency that investigates fraud only starts to investigate after many victims have reported their loss. There are victims who do not report because of fear, because of embarrassment, because of unrealistic, hopeful optimism and a variety of other reasons so by the time CAD gets involved, it would have added more years and more new victims. A lot more people, sadly, would have been hurt by then. This is the most significant factor in stopping financial fraud – if the first whistle were to prompt action by the authorities, more victims could be prevented. The feet of clay by regulators and law enforcers help the scammers and facilitate the crimes.

Ponzi schemes are chief among these and as with all Ponzis, the early investors are taken in by the promised high returns being achieved. This pool of satisfied investors will go on to sink in additional funds. But more than that, they are often trotted out on stage at investment seminars to be the best spokespersons for their “safe and profitable” investments. Some are even recruited to be sub-agents who earn referral commissions.

A very common scam I see over recent years involves companies that may own some land in a distant country, directly or indirectly via their selected “Developer Partners” who have cleared their “rigorous” due diligence process and deemed safe. Money is borrowed from the lay public by an intermediary set up for that specific fundraising purpose. This intermediary is supposed to channel the funds out to the said Developers for the purpose of infrastructure development or some construction activities on the property. In return, the intermediary company, freshly created, probably a limited liability entity registered in some opaque tax-free haven, signs an IOU agreement with the investor detailing scheduled repayments of interests and full capital at the end of 2 or 3 or 4-year terms. He’s just described Dolphin Trust and similar investment “loan-note” scams perfectly.

The IOU agreement or promissory note does not accord the investors (or more accurately the lenders), any say on how the funds are utilised. There is also nothing to stop these unscrupulous vendors from using that same plot of land as their “collateral” to draw in funds from other investors in other markets.

Theoretically, that same piece of land could be used multiple times to borrow new money as long as the investors were not aware of it and had no legal title on that property. The number of times this “asset” is leveraged is limited only to the diabolical ingenuity of those vendors and the trusting innocence of an investing client pool. Am getting a bit worried now, as I think some of the scammers – who hadn’t already thought of this – might be getting very excited!

Other fundraising schemes can be created… perhaps through the issuance of minibonds in countries like the UK or in Europe. Or through commercial paper described as Development Funds that pay generous coupon rates over medium term, offered to selected high net worth clients. (And low-net-worth clients – the scammers aren’t fussy!).

Different company names are formed but the directors may be the same. The product brief is almost always similar and the advertising media material professionally done and is always flashy. Invariably these vendors will hold charity events and engage media celebrities or host politicians to lend credibility to their cause. They would list fake awards and renowned organisations as their business partners on their websites. All these with the sole intent of creating an image of legitimacy. This perfectly describes Phillip Nunn and his Blackmore Global investment scams – promoted by David Vilka.

Sometimes they may even attempt to raise public funds via a back door listing through an acquisition of a public listed entity that had fallen under judicial management.

Who are these people who are capable of such an elaborate scheme that spans international borders? Will the law catch up with them before they escape with their ill-gotten loot? Will justice be served in time and make an example of how fraud should not be excused as business failure?

Alas, only time will tell. Lee doesn’t seem optimistic. And I most certainly am not. The scammers make far too much money from such investment scams – and pension savers are ridiculously easy targets. The cold-calling ban will have negligible effect, and the ceding pension providers will keep on keeping on handing over pensions to the scammers willy-nilly.

I must admit, I had always been under the impression that regulation and law enforcement in Singapore were superb. But reading Lee’s blog, and learning how UOB bank has stolen £ millions from one customer, I think Singapore is probably as hopeless at challenging scams and financial fraud as the rest of the World.

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

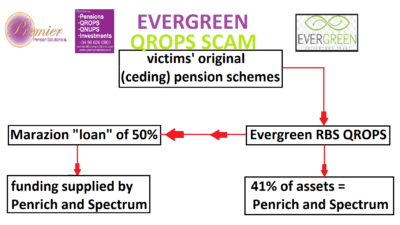

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

Having the highest possible regard for lawyers in general, and JMW Solicitors in particular, it is good to report that there is now a dialogue in progress which will hopefully result in Dolphin Trust producing a copy of the audited accounts. An excellent outcome would also be the repayment of the loan notes.

JMW Solicitors appears to be a promising outfit – especially as their website states: “No matter who you are or what you need, you can be assured of a great personal service from us.” As we need a copy of the Dolphin Trust audited accounts and the return of the money that Dolphin Trust borrowed (unsecured) from hundreds of pension and investment scam victims, I hope this promised great personal service will extend to a prompt and hassle-free resolution to the Dolphin Trust lenders’ problem.

The lawyer from JMW acting for Dolphin Trust – Nick McAleenan – has championed the cause of the supermarket chain: Morrisons.

MORRISONS DATA LEAK CASE – MORRISONS HELD LIABLE IN LANDMARK COURT RULING

JMW is representing thousands of claimants in a legal action for compensation against Morrisons Supermarkets.

The case is the leading legal case in the UK concerning “data breach”. It relates to the unauthorised copying and disclosure of Morrisons payroll information by a disgruntled ex-employee. In 2017, the High Court ruled that Morrisons is legally responsible for the data breach. In 2018, Morrisons appealed the High Court’s judgment, but the Court of Appeal dismissed Morrisons’ appeal. Further legal proceedings will take place to determine what compensation must be paid to the victims.

Nick McAleenan clearly has genuine empathy for the awful ordeal suffered by the Morrisons victims who had to undergo the trauma of having their privacy violated.

I sincerely hope this will translate into similar empathy for scam victims whose life savings have been “loaned” to his clients: Dolphin Trust.

If Nick (interesting name!) wants any clarification about how these scam victims compare to the Morrisons supermarket victims, he might want to have a chat with some of the victims of the STM Fidecs Trafalgar Multi-Asset Fund scam.

TPR has been neither coy nor shy in its published determination against Ward and Salih – and has openly called the London Quantum pension scheme, and the risky investments which Ward made, a “scam”.

But to any reasonable person’s mind, tPR’s determination in relation to Ward and London Quantum raises more questions than it answers. In fact, I would go even further and say that HMRC’s and tPR’s incompetence – as well as Dalriada Trustees‘ own failings – should be examined in parallel with Ward’s multiple frauds.

Because, make no mistake, London Quantum was only one of many.

It all started long before the Ark Pensions scam. Ward set out his stall transferring pensions to New Zealand and liberating 100% “tax free”. He boasted in the local Costa Blanca press that he had “helped” thousands of clients liberate their pensions (legally). Of course, this may have been free of tax in New Zealand, but when the Spanish tax authorities catch up with these clients, there will be a very expensive disaster.

It is extremely worrying that IVCM – a “phoenix” of the Brooklands disaster – is also offering the same New Zealand liberation facility today. It always worries me when firms fail to learn the lessons of past scams and expose unsuspecting victims to the same catastrophes that past scammers orchestrated. Add to this the fact that IVCM is regulated out of Gibraltar – the jurisdiction of choice for scammers such as XXXX XXXX and STM Fidecs – and I think it is well worth giving IVCM a very wide berth.

Prior to 2010, Ward was a tied agent of Inter Alliance – a company based in Cyprus which had an insurance license. For Inter Alliance in Cyprus, Ward successfully created the illusion that this gave his company Premier Pension Solutions some sort of license. But, in reality, it did not – as the Cyprus license was only for Inter Alliance and not for any other entity. Plus tied agents were (and still are) illegal in Spain.

As a sideline, Ward was flogging EEA Life Settlements as he had discovered the delights of making huge commissions out of dodgy, risky, illiquid investments to his unsuspecting victims. In 2010, Ward was working closely with Concept Trustees in Guernsey – run by Roger Berry. Initially happy to see Concept Trustees’ QROPS members have 100% of their pensions invested by Ward in EEA, Berry eventually realised that Ward’s firm was not regulated as it had been dumped by Inter Alliance. Of course, even before it had been dumped, Premier Pension Solutions wasn’t regulated anyway. But Concept Trustees was too stupid to realise that.

Concept then wrote to all the members who were clients of Ward’s Premier Pension Solutions and warned them that Ward’s firm was neither regulated nor had any professional indemnity insurance cover. Berry claimed he would not be accepting any further investment instructions from Ward, but this was basically just a load of hot air (aka lying) as he continued to accept investment instructions into EEA by Ward.

In September 2010, Premier Pension Solutions was appointed as a tied agent of AES International – a firm based in London and Dubai. The agency agreement covered PPS for investment and insurance business – but not pension transfer business. Ward’s PPS letterheaded paper claimed that it was a “partner” of AES and that it was regulated by the DGS (Spanish insurance regulator) and CNMV (Spanish investment regulator). PPS also became a member of FEIFA – the Federation of European Independent Financial Advisers (although he was later dumped by them). You can understand why so many victims thought that PPS was a bona fide advisory firm.

Then came the first of Ward’s major pension scams: Ark. It is worth looking at the history of Ark because this sets the scene for how nearly 500 victims came to lose their pensions and face tax liabilities – as well as the dozens of further scams operated by Ward (including London Quantum).

A famous footballer and his mate – a football club owner – bought a plot of land in Larnaca in Cyprus with a view to turning it into a golf resort. They paid £1.1 million for the property, but then realised it wasn’t big enough for a whole golf course (neither of them was bright enough to be able to count up to 18) and so they tried to find some other investors. The chumps they tried to con into buying more land adjacent to the original plot either couldn’t come up with the money or were frightened off such a high-risk, illiquid investment.

So the sporty pair went to see the footballer’s accountant – Andrew Isles of Isles and Storer (now owned by LB Group). Isles soothed the sporty pair’s worries by telling them that securing more investors was simple: just start a pension fund! He introduced them to what he called “two leading pension experts”: Craig Tweedley and Stephen Ward. Tweedley was already operating the KJK Investments/G Loans pension liberation scam (later to be placed in the hands of Dalriada Trustees by the Pensions Regulator) and Ward was a highly-qualified pensions expert, examiner and author.

The rest is history as nearly 500 victims lost their pensions to the Ark scam. But the sporty pair did very nicely – they sold the land in Cyprus to the Ark scheme for £4 million and pocketed the profit. The footballer tried to hide the money in Dubai but got caught and turned Queens Evidence. He and the other original investor (the football club owner) fell out and they ended up in court against each other – with the footballer triumphing. Andrew Isles also did very nicely as he sold introductions to a number of his clients and earned fat commissions in doing so.

As Ark unfolded – between mid 2010 and mid 2011 – Ward initially acted as an introducer. There were various introducers – many recruited by Ward when he ran a series of seminars in various parts of the UK. But Ward himself was the biggest introducer – accounting for more than a third of the whole £27 million fund and earning approaching three quarters of a million pounds in fees (the Pensions Regulator’s report of £350k was way off the mark).

Ward and his sidekick – bent lawyer Alan Fowler of Stevens and Bolton Solicitors – acted as the controlling minds behind Ark. The scheme documentation and the “loan” contracts were drawn up and explained by Ward and Fowler. Of the 5% commission charged by Craig Tweedley, Ward got at least 2% plus a transfer fee. But Ward had his eye on a much bigger proportion of the fees. Towards the end of the life of Ark, Ward was preparing to take Ark over from Tweedley – along with an associate of his: Peter Moat (another pension crook who went on to operate the Fast Pensions scam – now also in the hands of Dalriada Trustees). In a way, it was a shame that didn’t happen, as Tweedley did at least try to help the Ark victims, whereas Ward never lifted a finger. In fact, he simply told the Ark victims to throw the tax demands away as “HMRC would never pursue them”.

In February 2011, HMRC met with Tweedley and Ward to discuss the “loans” – so HMRC knew perfectly well that Ward was the main brain behind the scam. It is, therefore, astonishing that they did nothing to stop him operating so many further pension scams.

Ark came to a shuddering halt on 31st May 2011, when tPR appointed Dalriada Trustees and the scheme was suspended. Dalriada went up to Yorkshire to confront Crag Tweedley and relieve him of all the evidence and files relating to the scam. Tweedley told Dalriada that all the records were held down at Ward’s Manchester office at 31, Memorial Road and he drove down to collect them from Anthony Salih. He arrived to find Salih removing all the Premier Pension Solutions fee agreements on the instructions of Ward (he managed to shred most of them – but did missed a few which I now have).

After Ark, Ward went on to run the Evergreen Retirement Benefits QROPS scam with accompanying 50% “loans” and a further 300 victims lost £10 million worth of pensions. HMRC removed Evergreen from the QROPS list when they realised it was a liberation scam and Ward fell back on two more UK-based, bogus occupational schemes: Southlands and Headforte. Plus, he registered a number of new schemes – including Capita Oak.

The Capita Oak scheme was another bogus occupational scheme registered by Ward with a fictitious sponsoring employer: RP Medplant (Cyprus). There is, however, a firm called RP Med Plant in Cyprus. The Capita Oak trust deed was written by Ward’s bent lawyer Alan Fowler. Ward took responsibility for the transfer administration – transferring valuable personal and final salary occupational pensions into this scam – in the full knowledge that he was condemning hundreds of victims to certain financial ruin and poverty in retirement. Capita Oak is now also in the hands of Dalriada Trustees.

Other pension scams that Ward was operating – in addition to Southlands and Headforte – from 2012 onwards included Feldspar, Hammerley, Meribel, Halkin, Randwick, Bollington Wood and Westminster. And, of course, Dorrixo Alliance which was the trustee for many of these scams. Capita Oak and Westminster are both under investigation by the Serious Fraud Office.

How much more evidence do they need?

In May 2014, HMRC was given evidence of all of Ward’s various scams – including Dorrixo Alliance. They were also given detailed testimony by me and a number of victims of what Ward had been up to in the pension liberation fraud industry since Ark. It would have been very easy for HMRC to look up to see what other pension schemes Dorrixo was trustee to. Had they done this, they would have seen that Dorrixo was the trustee for the London Quantum scheme. If HMRC had taken any action, they could have prevented Mr. N – a serving police officer – and 96 other victims from losing their pensions to Ward and his various dodgy, inappropriate investments (including loans to Dolphin Trust).

If we add to the above catalogue of scams the Continental Wealth Management scam – 1,000 victims facing the loss of £100 million worth of life savings – Ward has been responsible for the destruction of thousands of people’s pensions this past eight years. Plus several suicides and deaths from stress-related medical conditions.

SERIOUS QUESTIONS ARISING FROM THE PENSIONS REGULATOR’S DETERMINATION RE:

Mr Stephen Alexander Ward – The Pensions Regulator case ref: C46205159

Ward was a director of Dorrixo from 13 October 2011 to 28 April 2015. A company called Quantum Investment Management Solutions LLP (“QIMS”) has at all material times been the sole sponsoring employer of the Scheme. Dorrixo became the sole trustee of the Scheme on 19 April 2014. Dorrixo is also recorded as being the Scheme administrator.

HMRC AND TPR WERE GIVEN EVIDENCE OF WARD’S COMPANY, DORRIXO, IN MAY 2014. THEY WERE ALSO GIVEN EVIDENCE OF A LARGE NUMBER OF SCAMS WARD OPERATED AFTER ARK – ALL INVOLVING LIBERATION FRAUD. WHY WASN’T ACTION TAKEN TO PREVENT LONDON QUANTUM? ALL 97 VICTIMS – INCLUDING A SERVING POLICE OFFICER – COULD HAVE BEEN PREVENTED.

On 18 June 2015 the Regulator appointed Dalriada Trustees Limited (“Dalriada”) as an independent trustee to the Scheme, with exclusive powers.

HAS ONE SINGLE PENNY EVER BEEN RETURNED TO ANY OF THE PENSION SCAMS PLACED IN THE HANDS OF DALRIADA TRUSTEES? THERE ARE DOZENS OF THEM, AND FEW – IF ANY – OTHER INDEPENDENT TRUSTEES ARE EVER APPOINTED BY TPR. BUT THERE SEEMS TO BE NO RECORD OF ONE SINGLE MEMBER EVER GETTING ANY RETURN FROM ANY OF THE SCHEMES IN THE PAST EIGHT YEARS – DESPITE THE MANY MILLIONS DALRIADA HAVE PAID THEMSELVES FROM THESE SCHEMES.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

AS THIS EVIDENCES THAT THIS SCAM COULD EASILY HAVE DWARFED ARK IN A VERY SHORT SPACE OF TIME, DON’T HMRC AND TPR RECOGNISE THAT THEIR LAZINESS AND NEGLIGENCE NEED TO BE ADDRESSED? THEY LEARNED NOTHING FROM ARK – AND WHILE THERE ARE VALID CRITICISMS OF WARD FOR HAVING LEARNED NOTHING, HE IS JUST A COMMON SPIV WHILE HMRC AND TPR ARE SUPPOSED TO BE GOVERNMENT DEPARTMENTS WITH A RESPONSIBILITY TO PROTECT THE PUBLIC. THE SCALE OF THIS SCAM SHOWS THESE TWO ORGANISATIONS ARE NOTHING BUT HOPELESSLY INEPT AND AMATEURISH IN THEIR APPROACH TO DILIGENCE AND PUBLIC RESPONSIBILITY.

The Scheme was promoted to potential new members by introducers. These included the following entities: GoBMV; Baird Dunbar; What Partnership; the Resort Group PLC; Friendly Investments; Premier Mark Consultants and Quantum Wealth Management Solutions Limited.

THE DANGERS OF THE SCOURGE OF “INTRODUCERS” SHOULD HAVE BEEN LEARNED FROM THE ARK SCAM IN 2011. WARD RECRUITED DOZENS OF THEM ALL OVER THE COUNTRY. AND YET NONE OF THEM HAS EVER BEEN BROUGHT TO JUSTICE FOR THEIR PART IN ARK, AND HAVE GONE ON TO OPERATE AS INTRODUCERS AND EVEN HOLD KEY CENTRAL ROLES IN LATER SCAMS. THIS INCLUDES FRIENDLY INVESTMENTS AND JULIAN HANSON – WHOSE SCHEMES ARE NOW ALSO IN THE HANDS OF DALRIADA TRUSTEES.

Gerard was responsible for producing template risk letters, member application forms, pro forma declarations stating that the person signing them was a self-certified sophisticated investor, member booklets and the statement of investment principles (of which there were four versions). Gerard sent these documents to members once they had been introduced to the Scheme by an introducer.

GERARD ASSOCIATES, RUN BY GARY BARLOW, HAD ACTED AS AN INTRODUCER TO WARD IN THE ARK SCAM. AND YET HE WAS LEFT FREE TO OPERATE IN THE SAME CAPACITY IN THE LONDON QUANTUM SCAM – AND EVEN TAKE ON A MORE CENTRAL ROLE. GERARD ASSOCIATES WAS AT THE TIME AN FCA-REGULATED FIRM – AND REMAINS SO TO THIS DAY. THE FCA HAS TAKEN NO ACTION TO REMOVE THIS FIRM OR TAKE ANY ACTION AGAINST GARY BARLOW.

GERARD ASSOCIATES’ GARY BARLOW WAS PAID £253,000 FROM THE LONDON QUANTUM SCHEME FOR DEFRAUDING VICTIMS INTO SIGNING AGREEMENTS THAT THEY WERE “SOPHISTICATED” INVESTORS. SO WHY HASN’T BARLOW BEEN PROSECUTED AND JAILED – AND MADE TO PAY THIS MONEY BACK TO THE VICTIMS?

A material number of the new members had a low or medium appetite for investment risk and, in any event, were unaware that the Scheme’s investments were high-risk investments. The Panel was troubled by the apparent disconnect between members’ appetite for risk and the high risk nature of the investments made by Dorrixo. Mr Ward accepted that the Scheme’s investments were high risk, but claimed this was made clear to new members in the Member Booklet.

I DON’T KNOW WHAT SORT OF DRUNKEN DUMMIES MADE UP TPR’S “PANEL”, BUT DID THEY SERIOUSLY THINK THAT ANY PENSION FUNDS SHOULD EVER INVEST IN HIGH-RISK CRAP? INDIVIDUAL MEMBERS’ APPETITE FOR INVESTMENT RISK IS IRRELEVANT – THIS WAS A PENSION FUND, NOT A CASINO.

The case against Ward was based on failures of competence and capability, and also a lack of honesty and integrity as well as Ward’s involvement with “pension liberation” as an introducer of members to the “Ark” schemes.

BUT TPR AND HMRC KNEW ALL ABOUT THIS BACK IN 2010 AND 2011. WHY DID THEY DO NOTHING TO PREVENT WARD FROM SCAMMING MORE VICTIMS OUT OF MORE MILLIONS OF POUNDS. THEY STOOD BACK AND WATCHED – DESPITE HAVING HARD EVIDENCE THAT HE WAS STILL UP TO HIS CRIMINAL MISCHIEF.

Mr Ward did not dispute that a company of his (Premier Pensions Solutions SL) was involved in introducing members to the Ark Schemes, but states that the relevant activity pre-dated any finding by the courts of pensions liberation and that Mr Ward had no knowledge that the schemes were being used for such activity.

BUT HMRC, TPR AND DALRIADA ALL KNOW THIS ISN’T TRUE. THEY HAVE ALL SEEN EVIDENCE THAT WARD AND HIS BENT LAWYER ALAN FOWLER ACTUALLY PRODUCED THE “LOAN” (MPVA) DOCUMENTATION AND EXPLAINED THE LOANS IN SOME CONSIDERABLE DETAIL TO THE VICTIMS. THE MPVA CONTRACTS WERE DRAWN UP BY FOWLER. IS IT REALLY CREDIBLE THAT NEITHER HMRC NOR TPR WOULD HAVE OBJECTED TO THIS STATEMENT?

The Panel did not consider there was sufficient evidence of Ward having actual knowledge of, or turning a blind eye to, the illegal nature of the activity of the Ark Schemes when carrying out his role as introducer before.

SERIOUSLY? I HAVE GIVEN EVIDENCE OF THIS TO BOTH HMRC AND TPR ON MANY OCCASIONS. THIS HAS BEEN DISCUSSED AT MEETINGS WITH DALRIADA TRUSTEES ON MANY OCCASIONS. EVIDENCE OF THIS HAS BEEN GIVEN TO THE SERIOUS FRAUD OFFICE ON MANY OCCASIONS BY VARIOUS VICTIMS AND ME. WHAT FURTHER EVIDENCE DID THE PANEL WANT? EVERY ARK MEMBER’S FILE WAS FULL OF SUCH EVIDENCE. EITHER TPR IS LYING OR IT IS INCOMPETENT. OR BOTH.

The Case Team also relied on certain alleged failures in relation to other pension schemes (called Headforte and Halkin), of which Mr Ward was a trustee. These are denied by him (e.g. an allegation of failure to appoint an auditor to those schemes) and the Panel did not consider it necessary to make findings in respect of them.

SO WHAT ACTION HAS TPR TAKEN IN RELATION TO HEADFORTE AND HALKIN? BOTH WERE BEING USED FOR PENSION LIBERATION FRAUD BY WARD – AND YET THE VICTIMS PROBABLY STILL HAVE NO IDEA WHAT HAS HAPPENED TO THEIR MONEY. IT IS ABSOLUTELY ASTONISHING THAT NO ACTION HAS BEEN TAKEN IN RELATION TO THESE TWO SCHEMES, PLUS ALL THE OTHERS WARD HAS BEEN OPERATING OVER THE YEARS.

Stephen Alexander Ward (date of birth 11 July 1955) is hereby prohibited from being a trustee of trust schemes in general. This order has the effect of removing the above-named individual from all or any schemes of which he is a trustee. By section 6 of the Pensions Act 1995, any person who purports to act as a trustee of a trust scheme whilst prohibited under section 3 is guilty of an offence and liable (a) on summary conviction to a fine not exceeding the statutory maximum, and (b) on conviction on indictment to a fine or imprisonment or both.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

THIS IS NOT JUST THE DEATH OF TRUST, BUT OF ANY CONFIDENCE IN THE GOVERNMENT, REGULATORS AND CRIME PREVENTION AGENCIES TO PREVENT OR DEAL WITH PENSION SCAMS AND SCAMMERS.

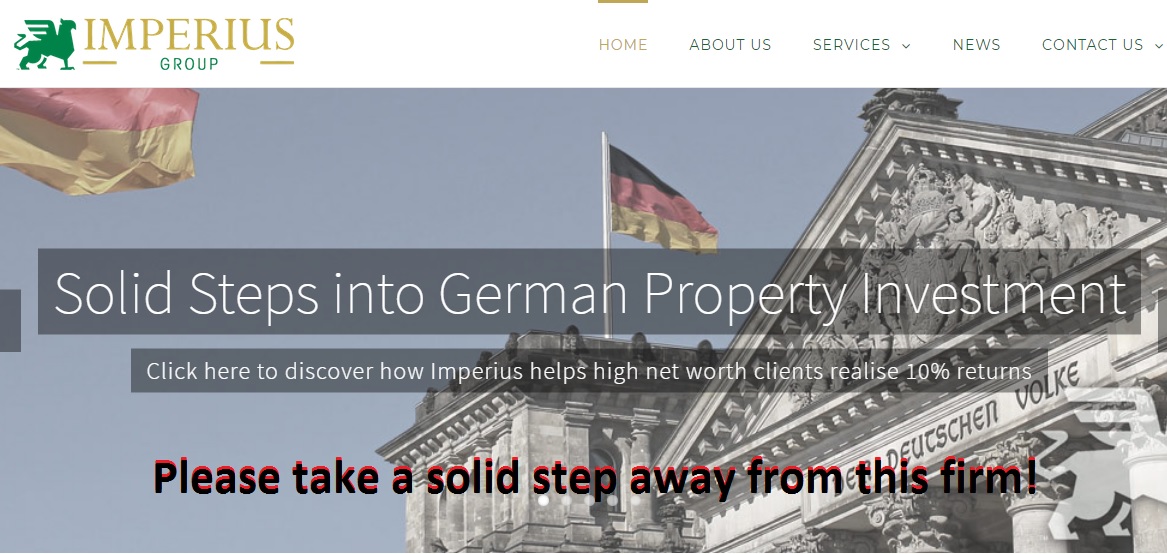

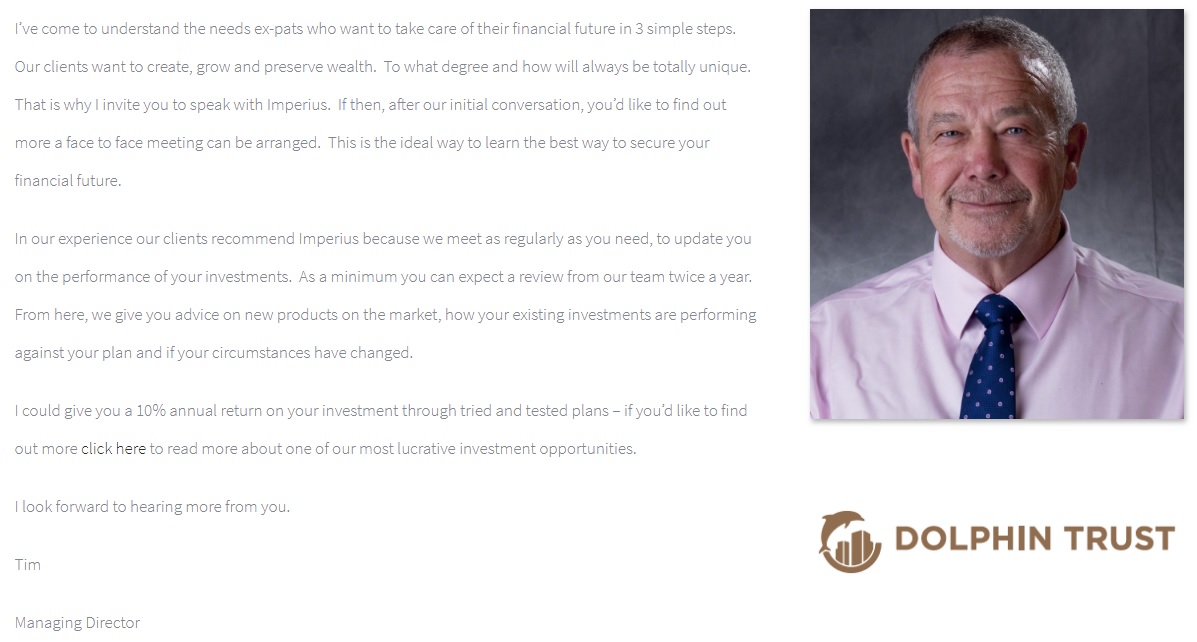

In my weekly hunt for the next firm to feature in my ´qualified and registered?´ blog series, I came across an advisory company that caught my attention: The Imperius Group, run by a fella named Tim Blogg, who claims to have retrained 25 years ago to offer pension and investment advice to expats.

The reason Tim Blogg´s company, The Imperius Group, flashed up on my red beacon radar was the fact that he listed his company in partnership with various life assurance offices including OMI (Old Mutual International) and Generali. Links to these companies, a well-read Pension Life blog follower will know, is not a good thing. They are also linked to RL360 and Hansard Global.

Tim Blogg also has a bright and shiny Dolphin Trust logo underneath the mug shot of him and a promise of:

“I could give you a 10% annual return on your investment through tried and tested plans – if you’d like to find out more click here to read more about one of our most lucrative investment opportunities.”

Tim Blogg offers “strong steps into German property investment”, through Dolphin Trust (loan notes).

Ring any bells?

British Steelworkers were duped into investing their DB pension schemes into – yes, you´ve got it – into an unregulated fund: Dolphin Trust (in Germany). Celtic Wealth Management acted as the introducers to this investment and Active Wealth – now collapsed – acted as the advisory company. This investment scam has left British Steelworkers trapped and at risk in this totally unsuitable, unregulated investment.

Dolphin Trust IS NOT regulated and there is no evidence to show The Imperius Group is either.

Tim Blogg, founder of The Imperius Group, DOES NOT APPEAR ON ANY REGISTER as a qualified and registered financial adviser.

Aside from Tim Blogg, the only other person who claims to work for The Imperius Group is a lady called Emma Allen, listing herself as, ´Employed as a Personal Assistant by iBOS working for the Managing Director of The Imperius Group Limited.´ The Imperius Group website quotes the term ´us´ regularly, but from what I have found, it would seem this company is pretty much a one-man unqualified band.

Once again, I am left wringing my hands in despair at the state of the offshore financial sector and at purported financial advisers like Tim Blogg.

However, at least I will sleep soundly tonight knowing that another financial advisory firm has been outed. The Imperius Group and Dolphin Trust are not the company to trust with your precious pension fund.

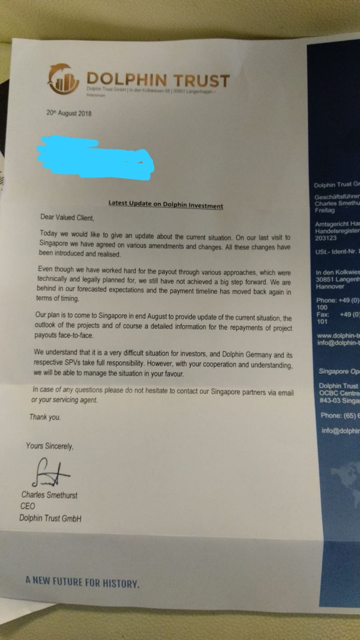

To demonstrate the serious concerns about investments in Dolphin Trust, this is a copy of a letter sent by Charles Smethurst CEO of Dolphin Trust to investors. It would seem that although some investments have reached their maturity, other investors are still waiting for their funds to be released. This raises questions about the liquidity of funds and also the possibility of Dolphin Trust going bankrupt. Maybe the victims will have a claim over the properties, if indeed the German properties they think they have invested in actually exist.

I’ve been very concerned about Dolphin Trust GmbH for some time. There’s an awful lot of pension money being loaned to this company – and I don’t get to hear of many (in fact any) people who have had their loans repaid. That doesn’t mean they haven’t been repaid – it just means I haven’t heard about it.

The things that bothers me about Dolphin Trust are:

“Introducers” get paid eye-watering commissions of up to 25%

If the assets and projects are so good, why pay private lenders 10% interest (on top of the 25% commission) – why not just go to the bank?

I have recently heard that Dolphin and some of their dodgy “introducers” are now trying to convince lenders to take their loans back in the form of shares in the company

But the biggest concern I have is that Dolphin Trust formed a major part of the underlying investments in the Trafalgar Multi-Asset Fund scam – run by XXXX XXXX of Global Partners Limited and STM Fidecs in Gibraltar. This fund is now being wound up by Stephen Doran, of Doran + Minehane.

The Trafalgar Multi-Asset Fund and XXXX XXXX are currently under investigation by the Serious Fraud Office. Ironically, Justin Caffrey of Harbour Pensions once told me that XXXX came to see him to try to flog the obviously dodgy Trafalgar fund. Caffrey claimed he could see XXXX was an obvious spiv straight away and that Trafalgar was clearly bad news – so he sent the ginger scammer packing.

And then STM Group bought out Harbour Pensions and got custody of some of Caffrey’s Blackmore Global Fund worthless crap to keep the Trafalgar Multi Asset Fund worthless crap company. You couldn’t make it up! A bunch of toxic rubbish flogged by scammers Phillip Nunn and XXXX XXXX.

STM Fidecs had notified the hundreds of victims that there would be a distribution in early 2018 once Doran + Minehane had got rid of some of the Dolphin Trust loan notes. But then STM did a U-turn and announced there wouldn’t be a distribution at all. Clearly, getting shot of the loan notes was more difficult (or impossible) than Mr Doran first imagined. Or perhaps he did get rid of them – but got shares in Dolphin Trust or Vordere instead (and this is the reason for the lack of distribution by STM Fidecs).

Any way you look at it, Dolphin Trust is looking dodgier than ever now it is well known that there are £21 million worth of Trafalgar Multi Asset Fund loan notes out there looking for a warm and cosy (and gullible) home.

Quite apart from the fact that no self-respecting introducer or financial adviser should EVER be caught selling high-risk, unregulated, non-standard “assets” in the first place, surely nobody would ever want to be caught flogging the same stuff that the likes of XXXX XXXX and Stephen Ward were making a fortune out of.

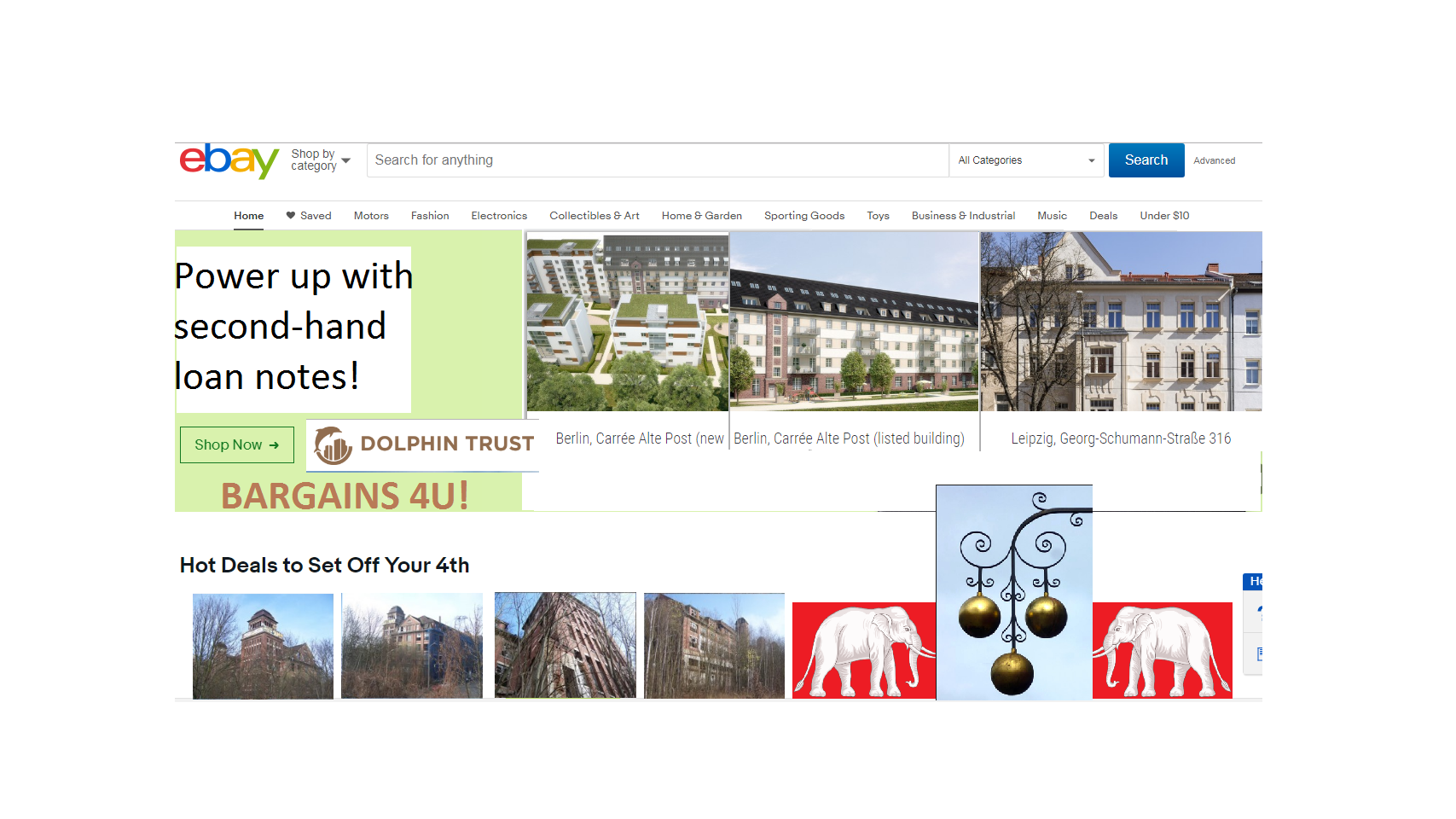

I did try to call Dolphin Trust, but they don’t answer their phone. Maybe they don’t like cold calls (which is how most victims get scammed into lending them money in the first place).

Without the benefit of any assurances from the nice men at Dolphin Trust – Charles Smethurst, Helmut Freitag, Axel Krechberger and Matthias Ruhl – we will just have to hope that Mr Doran manages to offload the second-hand loan notes that STM Fidecs allowed 400+ victims’ life savings to be invested in. Perhaps I’ll drop him a friendly note and suggest he tries ebay.

I am saddened to write about the first (but probably not the last) British Steelworker who has fallen victim to an investment scam as well as a pension scam. The British Steelworker was persuaded to transfer his DB pension AND invest £35,000 of his personal saving into an unregulated fund – Dolphin Trust (in Germany).

More and more, we are seeing innocent, hardworking individuals falling victim to pension scams due to their pension funds being invested in unregulated, high-risk, illiquid investments. It is just a matter of time before these unsuitable investments leave victims’ pension funds in tatters.

Mike Pickett, a British Steelworkers, had his savings loaned to an unregulated German property development company called Dolphin Trust. This was courtesy of (now collapsed) IFA firm Active Wealth. Mike not only transferred his pension fund, but also his life savings. His pension funds went into a SIPPS which then found their way to Gallium Fund Solutions.

Mike’s non-pension savings then went through Active Wealth into Dolphin Trust GmbH, which specialises in the development of German-listed buildings and promises 10% returns on investment. He says he was unaware that he was signed up to a fixed term payment (minimum 2 years) and of the associated 5% exit penalty to withdraw money from Gallium early.

Dolphin Trust IS NOT regulated by the Financial Conduct Authority.

The way victims were lured into this scheme is more than a little questionable. It is also somewhat confusing as to who was actually responsible for investing Mike’s funds. Much little like an traditional fable, the storyline seems to shift to ensure the blame can be passed where necessary.

It all started with a presentation made to British Steel Workers via Celtic Wealth. How on earth are these people were able to make a presentation to innocent victims-to-be for an UNREGULATED investment is beyond me. Especially when Celtic Wealth was not authorised to provide investment advice.

And here’s where Active Wealth came in. Celtic Wealth claimed “All regulated advice in relation to pensions and investments is given by Active Wealth (UK) Ltd.”

After the presentation by Celtic Wealth, Mike Pickett claims to have spoken to Active Wealth adviser Andrew Deeney, and says he was visited at his home shortly thereafter by Deeney and a representative of Celtic Wealth. He had three meetings with Active Wealth in total – two of which he said were with Deeney.

Active Wealth has now surrendered its pension transfer permissions following FCA action in relation to advice given to steelworkers. Andrew Deeney, now sole director and shareholder of regulated IFA firm Fidelis Wealth Management, claims he has no relation to these investments.

No one wants to take the blame for these mis-sold investments. Yet all involved would have contributed to the demise of the pension funds – and earned fees and commissions along the way.

Transfers into self-invested personal pensions (SIPPS) dominated the pension transfer market in 2017, accounting for 51 percent of all transfers. It is worrying to consider what percentage of that figure is being transferred into unregulated, toxic investments.

The problem with pension scammers is that they are very good at disguising themselves. They wear smart clothes, they are friendly, knowledgeable and very very persuasive. They have a series of different scams disguised as a great investment – when one collapses they move onto another, just as Andrew Deeney has and the infamous Stephen Ward.

The first way of avoiding a possible scam is to reject all cold calling.

Never take a ‘free’ review on your pension.

Always check that the advisers and companies are regulated

Make sure you know ALL the facts

Low-risk high return investment – THEY DO NOT EXIST

Too good to be true – it probably is

******************************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

STM Fidecs, the Gibraltar-based trustee firm used for the Trafalgar Multi Asset Scam, is now the subject of large numbers of complaints to the Gibraltar authorities. Hundreds of victims of XXXX XXXX’s unlicensed “advice” transferred safe UK pensions to a Gibraltar STM Fidecs QROPS and then he invested 100% of their funds into his own fund – Trafalgar Multi Asset (now under investigation by the Serious Fraud Office). These victims have now submitted evidence and testimony. These reports and complaints are against both XXXX XXXX and STM Fidecs for their part in this scam.

STM Fidecs are also being reported to the Gibraltar Financial Services Commission for the attention of:

Annette Perales, Head of Financial Crime

and

Zoe Westwood, Head of Enforcement, Legal, Enforcement and Policy

The Serious Fraud Office has been investigating this scam – in which STM Fidecs played an integral and crucial part – for some months. XXXX XXXX and one of the STM Fidecs directors have been arrested. XXXX’s office was searched and no doubt STM Fidecs’ offices were also searched. Obviously, the victims all want those responsible for this scam to serve maximum prison sentences.

The STM Fidecs website makes the following grand-sounding claim:

“The backbone of STM is its staff. We have people who have worked for us for 20 years who are the heart and soul of our business. If we didn’t have outstanding staff, we wouldn’t be able to do what we do.”

The only thing “outstanding” would be an immediate admission of their guilt and negligence, as well as an undertaking by STM Fidecs to compensate their victims for the £ millions of losses they are facing due to STM Fidecs’ complicity with this scam. Let’s examine some of these staff and see how much backbone they really have.

Alan Roy Kentish ACA ACII AIRM Role: Chief Executive Officer

Alan Kentish, CEO, claims to be a qualified chartered accountant specialising in the financial services industry. So you would have thought he would have known not to accept business from an unlicensed firm – XXXX XXXX’s Global Partners Limited (now Tourbillon). He ought to have known that UK residents should not be transferred to a QROPS at all. He would have known that members’ funds should not be 100% invested in one UCIS fund (illegal to be promoted to UK residents). And he should have recognised that it is a clear conflict of interest for members to be invested in a fund for which their adviser was also the investment manager.

What has Alan Kentish done to put this right? How much compensation has he offered to the hundreds of distressed investors? Has he engaged with the victims and assured them that STM Fidecs acknowledges their responsibility, liability and culpability? No – Alan Kentish has done nothing except pull up the drawbridge-like a spineless coward.

David Easton, Head of Pensions at STM Group PLC

“David Easton, Head of Pensions for STM Group PLC joined STM in October 2014 as Managing Director of the Gibraltar pensions business and is also a board member of the pensions businesses in Malta and the UK. Since 1990 David has worked in the financial services arena specialising in pensions administration. David is responsible for driving the expansion of STM Group’s international pensions division as well as personal and occupational pension schemes in Gibraltar and personal pensions in the UK.”

So, responsible for driving the expansion of STM’s pension business into an investment scam run by a known serial scammer? Well done David. Your “primary focus” was very clear: put UK residents into a QROPS and then allow all of them to be 100% invested into an illegal UCIS. And to what extent has he engaged with the hundreds of distressed victims of this scam? Zero. Another spineless coward who refuses to speak to these people. He will neither explain nor apologise.

A former employee of STM Fidecs sent me the following statement:

“We were told not to go to the Pension Life website so as not to give her any traffic and SEO rankings. I believed them. More fool me. This is why I am now checking it out and am amazed at what’s on there.

I was asked to dig the dirt on Angela Brooks and I did, believing STM had not been aware of the Trafalgar stuff but had instead been duped. It’s more than apparent now that they fully knew what they were doing. They have sent Angela lawyers letters insisting she cease from mentioning them on her website or will take legal action against her.

Glynis Broadfoot (a victim of Holborn Assets and Gower Pensions) who also used to work for STM Fidecs, was marched out. We had no anti-bullying policy in place at the time and Glynis was being bullied. They marched her out on trumped up charges.

If I had known this at the time I would have objected. Glynis won’t speak though. They must have frightened her to death.

Outstanding staff? I think not. The only thing the STM Fidecs staff excel at is bullying. And bullies are, of course, the biggest cowards of all.

Dolphin Trust – a UCIS which was illegal to be sold to UK residents

The Trafalgar Multi Asset Fund liquidators say this is the most obvious scam they have ever seen. Purely designed through ‘layering’ to misappropriate funds, the liquidators are just glad the administrators pulled the plug at £21m and not later. At the height of the success of this scam, STM Fidecs was accepting more than £1 million a month from UK residents (none of whom should have transferred into a QROPS at all) and allowing it all to be invested in XXXX XXXX’s illegal UCIS.

Apparently, Dolphin Trust (the German fund which borrows money to refurbish derelict government and listed buildings) has “cooperated” and the liquidators have found some other assets as well, although getting them may prove tricky since they will have been vigorously hidden. Dolphin Trust is typically found alongside car parking spaces, store pods, eucalyptus plantations, truffle trees and other toxic crap peddled by the scammers.

The liquidators reckon the victims might get 50% back less costs, so after the liquidators’ costs that would be nearer 30% net. But STM Fidecs know all this, but have deliberately hidden it from the victims.

It is human to err, and STM Fidecs is staffed by humans (albeit spineless ones). But what is not forgivable is to fail to come to the table and assure the victims they will be compensated for their losses and profound distress. STM Group has been bragging that it has plenty of money and will be buying up other trust companies to make their business bigger and more profitable.

None so blind….

STM Fidecs’ victims feel they shouldn’t be in the pension trustee business at all since they are clearly incompetent, dishonest and dishonorable. This belief is clearly correct since STM Fidecs also accepted transfers from Continental Wealth Management (unlicensed “chiringuitos”) and then allowed the victims’ pensions to be 100% invested in high-risk, professional-investor-only structured notes. As a result, the STM members are facing heavy losses.

Hundreds of victims have reported both XXXX XXXX and STM Fidecs to the SFO and the GFSC for fraud

The Gibraltar authorities must now show how “highly regulated and transparent” Gibraltar is. As things stand, the evidence is that Gibraltar is full of thieves, scammers and scoundrels. The chiringuitos love being there because the regulation is widely accepted as being as spineless as the staff and directors at STM Fidecs.

**********************************

As always, Pension Life would like to remind you that if you are planning to transfer any pension funds, make sure that you are transferring into a legitimate scheme. To find out how to avoid being scammed, please see our blog:

Beddoe proceedings: arguably (apparently) Dalriada could have been pursued by Ark victims without MPVAs for not pursuing repayment from those with MPVAs and conversely could have been pursued by Ark victims with MPVAs. So, to be on the safe side, they spent a quarter of a million quid of the victims’ funds on the Beddoe proceedings in the High Court.

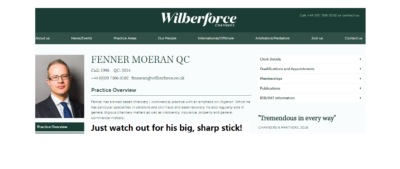

And here we need to look at the meaning of the terms – MPVA and sharp stick:

Sharp Stick: Fenner Moeran’s extremely offensive statement that Ark victims should be beaten with a sharp stick (upon which neither the judge, Sarah Asplin, admonished him nor upon which Keith Bryant, the Ark victims’ QC, challenged him)

MPVA

MPVA is an anacronym for “Maximising Pension Value Arrangements” – a euphemism for pension liberation. The rules are that if a person is under the age of 55, he or she can’t access any part of their pension without incurring an unauthorised payment tax charge of up to 55%. So all pension liberation scammers think up clever ways of fooling potential victims into believing there is a legal “loophole” to circumvent this rule.

The point of a pension liberation scam is not to provide members with a bona fide pension scheme designed to provide an income in retirement, but to make the scammers loads of money. First there is the transfer fee: in the Ark case it was relatively low at 5% – although Stephen Ward was charging an extra fee on top of that of up to £2k per transfer.

And then there are the investment kick-backs. We still don’t know how much the Ark scammers earned out of the speculative, illiquid, high-risk properties they purchased in various dodgy offshore jurisdictions. But it will have been very lucrative. In subsequent scams, the scammers earned huge commissions such as 20% from Dolphin Trust; 30% from Park First; 46% from Store First.

By the time the Ark victims realised they’d been scammed it was too late and there was no parachute

The scammers always promise spectacularly high returns on the investments with assurances such as “guaranteed 8% per annum”. In the case of Ark, the victims were told they would receive up to 9% a year on the growth of the value of “high-end London residential properties” in which the pensions would be invested. This, of course, was a lie. But by the time alarms started to ring and the victims realised there was no way out of this toxic flight with no parachute, it was too late.

But let us revert to the portion of a transfer which is liberated. This can range from 5% to 85% depending on the structure of the scam. And it is given various names or labels such as “cashback”; “thank you”; “refund of fees”; “trousers”; “loan”. The favourite word used is “loan” because the scammers claim that “loans are not taxable”. There is no intention for the money ever to be paid back – that isn’t the point of the exercise. The scammers know the victims would never be able to repay the funds.

The use of the word “loan” in some schemes is merely a marketing term used to fool people into believing they won’t be taxed on the money. And the scammers have no interest in whether the victims ever get taxed or not – because by the time HMRC gets around to sending out tax demands, the scheme will have collapsed and the scammers will be long gone and far ahead on their next scams. They never stick around to help mop up the train wreck left behind.

Often, the victims are surprised when they receive “loan” documentation and alarm bells start ringing. But the scammers assure the victims that this is “just a paper exercise” or “administration to make sure HMRC don’t try to tax the money – because loans aren’t taxable“.

In the Ark scheme, the victims were told the amounts liberated would not be taxable because they didn’t come from the members’ own scheme, but from another scheme. And this is why 14 schemes were set up to work in pairs so that up to 99 people in each pair of schemes could swap cash from their transfers. So this was an artificial mechanism structured purely to operate the liberation – using the label “MPVA” to dress the payments up as something more glamorous and bona fide than just a dollop of unauthorised cash in a person’s trousers.

Very few of the victims were told their cash would ever have to be paid back. The MPVA agreements never once mentioned the word “loan” but did mention the word “discharge” and suggested that the MPVA would be automatically “discharged” after a period of years.

Some victims were told the MPVA would be settled or repaid out of the growth that the Ark pension would enjoy (because of the wonderful investments!). It was explained that the MPVA would grow at 3% a year but the pension fund would grow at 9%. But the member would never have to pay the MPVA off out of their own pocket.

Other victims were told the MPVAs would never have to be paid at all because of the reciprocal nature of the transfer/payment structure. It was explained thus: two “paired” members in different schemes would each have a reciprocal MPVA of – say – £50k. If they both decided they never wanted to pay the MPVAs back, they would just treat them like equal IOUs and agree to simply tear them up.

The Tolleys authoritative manual on pensions taxation by Stephen Ward

Now remember, the victims weren’t told these things by any old spivs – they were told them by Stephen Ward of Premier Pension Solutions and his various accomplices (e.g. Fraser Collins, Terry Tunmore, Paul Clarke etc). Stephen Ward was back then – and still is now – a regulated financial adviser of many years’ experience, as well as the author of the Tolleys Pensions Taxation Manual, (and Level 6 CII qualified).

The same assurances were also given to numerous victims by George Frost, of Frost Financial, a regulated mortgage and insurance broker. And the victims who received the advice on the merits of entering into the Ark scheme believed they had every right to believe and trust professional, qualified and regulated advisers who assured them the MPVAs would never have to be repaid and that their pensions would be safe and secure.

HMRC does not care whether a sum of money accessed from a pension before the age of 55 is called a loan, thank you, cash back, fee refund, MPVA or any other euphemism for “liberation”. They don’t care whether it is repayable or whether it is ever repaid or not. They don’t care whether it comes directly from the member’s pension scheme, or from somebody else’s pension scheme, or via some convoluted arrangement designed to conceal the source of the money – such as Stephen Ward’s Evergreen/Marazion pension/loan scam. If a member makes a pension transfer and receives a sum of money as a result – irrespective of where it comes from – HMRC will issue a tax demand of up to 55%.

To illustrate how pension liberation scams range from the very simple and transparent to the highly complex and opaque, here is an example of one arrangement which Stephen Ward and his merry men, Alan Fowler and Bill Perkins, were involved with in 2013 – after Ark, Evergreen, Capita Oak and Westminster pension scams had all been suspended:

Thanks to you both for your understanding…. Am unused to non delivery! The arrangement I heard about today works like this as an example (ignoring fees) and this is the simplistic version …

Client borrows 16k or thereabouts (this is available in the package)

He gets a non recourse loan (which will not be repaid) of £84k

He buys shares in Xco for £100k. These are listed on the CISX (name is Elysian)

Transfers £100k to James Hay SIPP

SIPP pays member £100k for the shares

Member repays the 16k and trousers £84k

My IFA connection has done 40 of them so far. Advice to transfer to the SIPP is from an FCA regulated IFA. James Hay and Suffolk Life know the full structure and are happy with it.

Regards Stephen

The FCA-regulated IFA to whom he was referring was Angela South of Magna Wealth. She soon made a hasty exit from the collaboration with Stephen Ward when victims realised this was a scam and threatened to report her to the Serious Fraud Office. Victims who participated in this scam have now received tax demands from HMRC and Elysian Fuels is now worthless.

SHARP STICK

Dalriada’s QC, Fenner Moeran, seemed like a very sharp cookie. His skeleton argument (which we never got to see), and his opening speeches, started with the assumption that the MPVAs were definitely loans; that there was no question that they were loans and that the members knew and accepted that they were loans.

The judge, Sarah Asplin, accepted this without question and there was no debate on the subject. Kim Goldsmith’s QC, Keith Bryant, sat as quiet as a corpse and made not one single interjection or objection – even though he was sitting next to Kim who knew perfectly well – and must have told him – that the victims were not aware the MPVAs were loans. Indeed, they were categorically assured that the MPVAs would never have to be repaid.

Even more astonishing was the fact that Dalriada was aware the victims never knew the MPVAs were loans. Dalriada’s Sean Browes and Brian Spence, as well as Pinsent Masons’Ben Fairhead and Ian Hyde, had attended various meetings with the Ark Class Action and gone through this issue numerous times. They were also fully aware that one victim was horrified when she was subsequently told the MPVA was a loan and she immediately called Dalriada and asked to repay it. But Dalriada had refused.

Furthermore, dozens of Ark Class Action members had completed HMRC’s 10-point questionnaire (the Q10) which specifically asked about the arrangements and what they had been told about the need to repay the MPVAs. This is evidenced at HMRC’s question 8:

8: “DETAILS OF WHAT YOU WERE TOLD ABOUT THE NEED TO REPAY THE LOAN”

Here is a typical response to this question by one of the victims:

“I was told that although on paper it would be an official 25 year loan, that because of the nature of the way the loans were set up, i.e. the quid pro quo arrangement, whereby as one person received their monies from the other members scheme and vice versa, if there was a request for any monies to be repaid in the future from each member, each would tear up each other`s IOU and be quits, so to speak, as already stated.”

Stephen Ward – BA (Econ), ACII, APFS, APMI, ex examiner for the pensions management institute and for the CII, confirmed that the Ark scheme was designed by specialist pensions lawyer Alan Fowler – head of pensions at Stevens and Bolton.

Ward went on to explain how the MPVAs worked: “The best way to understand this is in terms of my lending you £100 and you lending me £100. If I do not repay you and you do not repay me then we are both in an equal position. Conversely, if I repay you and you repay me then the position is identical to that which would arise if neither party had repaid the other”.

These statements have been made to HMRC by Ark victims on countless occasions – and Dalriada has always been perfectly well aware of this. And yet Fenner Moeran used his sharp stick to knock these evidenced facts completely off the table – so that the judge was never made aware of them. Mind you, Keith Bryant QC was no better – because he didn’t bring them to the judge’s attention either.

I would go so far as to observe that Fenner Moeran should have used his sharp stick to point the judge to these evidenced facts – and Dalriada should have made sure he did so. By omitting to do so, both Fenner Moeran and Keith Bryant allowed the judge to come to the incorrect conclusion that:

“members who received the MPVA loans agreed to repay them. That’s the point of a loan. It’s not a gift. They cannot now complain about having to repay them. They can complain about having to repay them earlier, but that’s a cashflow issue which is vastly overwritten by the capital harm that is suffered by the non-recipient members”

Fenner Moeran merely leaned on his sharp stick and did nothing to correct the judge. As I was sitting behind him, I couldn’t see whether he was smirking – but I have a feeling he might have been. The judge was wrong on three counts:

The members with MPVAs did not agree to repay them – they were told they would never have to

They can most certainly now complain about being asked to repay them as they were never told they would have to and did not budget to do so

The capital harm suffered by members without MPVAs was mostly caused by Dalriada who did not reject their transfers after 31.5.11 but allowed transfers to continue right up until the end of August 2011

Having glossed over the facts smoothly, and directed the judge to her incorrect conclusion, Fenner Moeran then addressed the issue of ascertaining whether the Ark victims were in a position to be able to afford to repay the MPVAs. And then he produced, with a confident flourish, his pièce de résistance:

“The chances of getting ascertainably or enforceably more accurate information increases when you have the sharp stick of litigation behind it. If we want to see if we’re actually going to get any of this money back, the chances are that we’re going to have to wave a very large stick“

Fenner Moeran ought to be an intelligent person. In the full knowledge that a few feet to his right sat Kim Goldsmith, an Ark victim who had gone through six years of hell courtesy of Stephen Ward and George Frost and all the other scammers, and that a number of other victims were sitting at the back of the courtroom, he still made such an unbelievably stupid and offensive statement. He apologised later “I deeply and sincerely apologise for any misunderstanding or upset caused”.

But the damage had already been done – and you can’t un-say what has been said – especially when every word is recorded and transcribed. On behalf of Dalriada Trustees, he had deliberately misled the judge, and then proceeded to demonstrate clear contempt for the suffering of the Ark victims.

Interestingly, the judge had not remonstrated with Moeran for his crass comments – and Keith Bryant had not objected to the stupid and insensitive words. Throughout the rest of the proceedings, the judge remained – in my view – dominated and steered by Moeran. No attempt was ever made to disclose the truth about what the victims were told about repayment of the MPVAs by Stephen Ward, George Frost, Andrew Isles or Alan Fowler. And no explanation was ever given as to why Dalriada had not pursued these parties for having duped, misled and defrauded the Ark members.