If it was easy to stop pension scams, everyone would be doing it. Clearing up the mess left behind a pension scam is a huge challenge. This is why clear international standards need to be recognised and adopted. The scammers are like flocks of vultures. If people only used regulated firms, they could avoid a lot of scams.

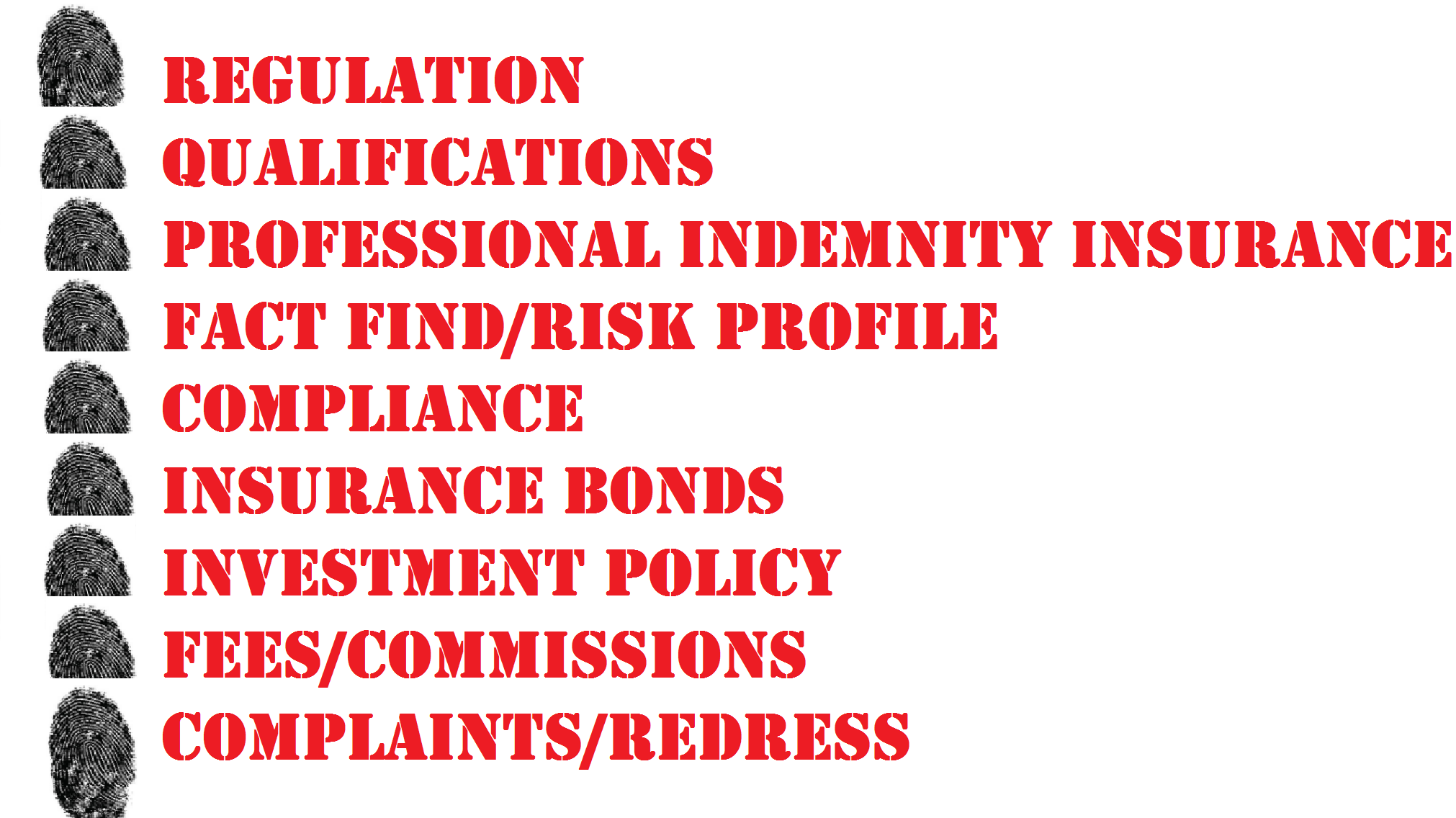

Firm must be fully regulated – with licenses for insurance and investment advice

Advisers must be qualified to the right standard

Firm must have Professional Indemnity Insurance

Clients must have comprehensive fact finds and risk profiles

Firm must operate adequate compliance procedures

Advisers must not abuse insurance bonds

Clients must understand the investment policy

All fees, charges and commissions must be disclosed

Investors must know how their investments are performing

Firm must keep a log of all customer complaints

Why is regulation so important?:

If a firm sells insurance, it must have an insurance license.

If a firm gives investment advice, it must have an investment license.

Many advisers will claim that if they only have an insurance license, they can advise on investments if an insurance bond is used. This practice must be outlawed, because this is how so many scams happen.

Most countries have an insurance and an investment regulator. They provide licenses to firms. Some regulators are better than others. Most regulators do some research and only give licenses to decent firms.

History tells us that most pension scams start with unlicensed firms. Here are some examples:

Continental Wealth Management invested 1,000 clients’ funds in high-risk structured notes. Investors started with £100 million. Most have lost at least half. Some have lost everything. Continental Wealth Management had no license from any regulator in any country.

Serial scammers such as Peter Moat, Stephen Ward, Phillip Nunn, and XXXX XXXX all ran unlicensed firms. Peter Moat operated the Fast Pensions scam which cost victims over £21 million. Stephen Ward operated the Ark, Evergreen, Capita Oak, Westminster and London Quantum pension scams which cost victims over £50 million. XXXX XXXX operated the Trafalgar pension scam which cost victims over £21 million.

Phillip Nunn operates the Blackmore Global Fund which has cost victims over £40 million. Serial scammer David Vilka has been promoting this fund. Over 1,000 people may have lost their pensions.

Firms that give unlicensed advice are breaking the law. Unlicensed advisers often use insurance bonds. These bonds pay high commissions. The funds these advisers use also pay high commissions. The advisers get rich. The clients get fleeced. The funds get destroyed. Insurance bonds such as OMI, FPI, SEB and Generali are full of worthless unregulated funds, bonds and structured notes.

Unlicensed firms hide charges from their clients. Most victims say they would never have invested had they known how expensive it was going to be.

Hidden charges can destroy a fund – even without investment losses. Licensed advisers normally disclose all fees and commissions up front. This way, the client knows exactly how much the advice is going to cost.

People can avoid being victims of pension scammers. Using properly regulated firms is one way. An advisory firm should have both an insurance license and an investment license. Don’t fall for the line: “we don’t need an investment license if we use an insurance bond”. Bond providers such as OMI, FPI, SEB and Generali still offer high-risk investments. The insurance bond provides zero protection. And the bond charges will make investment losses much worse.

The ongoing war against pension scammers continues with no sign that the end is near. The authorities stand idly by – facilitating mis-selling and outright fraud.

The only conclusive way to stop scammers is to ensure there are no victims for them to scam. AND the only way to do this is to educate consumers and drum the TEN STANDARDS into them.

PENSION SCAMMERS MUST BE STOPPED!

Ten Essential Standards For Pension Advice:

Do you know what a pension scammer looks like? The unfortunate answer is, he looks like any other Tom, Dick or Harry (or James, Stephen or Darren) walking down the street. Not only is he good at disguises, he also has the gift of the gab and he will have you convinced that the pension transfer he is offering you will pave the rest of your life with gold. In reality though, the gold will be short lived (or non-existent), and some or all of your fund will probably go poof! (along with the adviser).

Much as a master illusionist takes your breath away with his magic, a master scammer takes your money away with his silver tongue. You will be left wondering just how this smart-looking, sleek-talking ‘adviser’ managed to leave your pension – and probably your life – in tatters.

We have compiled a list of ten standards that EVERY firm offering pension advice should adhere to. Every qualified adviser working for an advisory firm should also be able to meet all of these standards. On Facebook recently, one reader stated: “Why would anyone respond to an unsolicited offer to manage their money from a complete stranger?” The answer is, “I don’t know, but they do!“. So, get to know a financial adviser long before you let them anywhere near your finances.

In the case of Capita Oak, for example, we saw many targeted victims who were struggling financially. So, the offer of a lump sum release and the opportunity of an investment that promised “guaranteed returns” was music to their ears.

Many of the victims didn’t stop to think; didn’t pause to ask the right questions; or do any research to make sure the pension offer came from a viable, credible, regulated firm. The victims just said “yes” as they thought the transfer would make life easier.

For example, with the awful benefit of hindsight – six years on – the Capita Oak victims are grappling with tax demands from HMRC and the possibility that the investment they are trapped in will go into liquidation. These people all wish they had stopped and thought before going ahead.

Sadly, the Capita Oak members who were defrauded by a bunch of scammers, (many of which are under investigation by the Serious Fraud Office) such as XXXX, Stuart Chapman-Clarke and Stephen Ward, are not alone. Thousands of other victims of both UK-based and offshore scams and mis-selling are facing similar regrets: these include victims of scams such as Evergreen New Zealand QROPS; Fast Pensions, Trafalgar Multi Asset Fund/STM Fidecs; Blackmore Global Fund; and Continental Wealth Management.

Mastermind serial scammer Stephen Ward has orchestrated a whole array of different scams over the last nine years. One of the biggest ones was Continental Wealth Management – a 1,000-victim scam. Ward was once a fully qualified and registered adviser and a pension trustee. He has destroyed dozens of pensions funds and thousands of victims’ lives. Yet he has never been prosecuted or forced to pay back even one penny of his victims’ losses. Only at the end of 2018 was he finally banned from being a pension trustee.

Most of the known scams used cold-calling techniques to reel in their victims. Whilst we saw a cold-calling ban on pension sales in 2019, we have already had reports that sneaky firms have changed their scripts to avoid fines. AND we are now seeing scammers focus their targets back onto expats. Which makes us worry there will be more QROPS disasters in the pipeline from now on.

Just a few minutes of research – as well as knowing the right questions to ask and understanding what standards an adviser and firm should adhere to – could have prevented past victims from losing so much of their precious pension pots. We can’t change what happened in the past – other than to take action against the scammers and negligent advisers – but we can help consumers understand what they should be looking for in an adviser:

STANDARDS ACCREDITATION CHECKLIST FOR FINANCIAL ADVISERS:

Proof of regulation for all services provided by the firm and individual advisers in the jurisdiction where advice is given

Evidence of appropriate qualifications and CPD for all advisers

Professional Indemnity Insurance

Details of how fact finds are carried out, and how clients’ risk profiles are determined and adhered to

Details of the firm’s compliance procedures – assuring clients of the highest possible standards

Clear and consistent explanation and justification of the use of insurance bonds for pensions and investments

Clear policy on structured notes, UCIS and in-house funds, non-standard assets and commission-paying investments

Full disclosure of all fees, charges and commissions on all products and services at time of sale, in writing

Account of how clients are updated on fund/portfolio performance

Evidence of customer complaints made, rejected or upheld and redress paid

If the firm you are thinking about using for your pension transfer do not adhere to all of these standards, find one that does. Your pension pot is your life savings – so don’t entrust it to any old unregulated firm or dishonest scammer. Remember, thousands of victims have already failed to ask the above ten questions – and will regret it for the rest of their lives.

ALL PENSION SCAMS START WITH A TRANSFER BY A CEDING PENSION PROVIDER.

It is interesting that PSIG chose three particular providers to give their answers to the questionnaire sent out: XPS Pensions Group, Phoenix Life Assurance Company and Standard Life Assurance Company. I have no doubt they chose these three providers because of their extensive first-hand expertise at facilitating financial crime. In the Capita Oak and Westminster scams – distributed and administered by serial scammers XXXX and Stephen Ward – and now under investigation by the Serious Fraud Office – Phoenix Life and Standard Life handed over dozens of pensions to the scammers. In Phoenix Life’s case, the total came to nearly half a million pounds’ worth, and in Standard Life’s case it was well over one million.

While there is, of course, substantial hard evidence that both the Pensions Regulator (formerly OPRA) and HMRC had been giving the industry plenty of warnings about scams long before the Scorpion Campaign was published on Valentine’s Day in 2013, it is also true that providers such as Phoenix Life, Standard Life – and other favourite financial crime facilitators such as Aegon, Friends Life, Legal & General, Prudential, Royal London, Scottish Life and Scottish Widows – carried on handing over millions to the scammers well into 2014, 2015 and beyond. And, in fact, they are still at it today.

The “Key Findings” do throw up some interesting facts:

“Information on scams is not readily available at an organisational level”.

Seriously? Don’t these organisations know how to do research? Do they really not know what to look for? They’ve had enough experience over the years – and have had enough examples of spending vast amounts of time trying to cook up reasons to deny complaints against their incompetence for handing over pensions to scammers – to write a whole encyclopedia about scams.

Organisations (such as Phoenix Life and Standard Life) could try talking to TPAS, or tPR, or the FCA, or the SFO, or Dalriada Trustees, or regulators in Malta, the IoM, Gibraltar, Dubai or Hong Kong. Or some of the thousands of victims – who have lost their pensions due to the incompetence and callousness of the ceding providers – who would readily fill in the blanks. There really is no shortage of readily-available, free information. They just need to take the time and trouble to ask for it. It really isn’t difficult. They just have to put their box-ticking pencils down for a few minutes.

“The Scams Code is seen as a good basis for due diligence”

I agree – it is really great. But it is also 78 pages long. Few people have to the time to read, understand or remember such long documents (with too many long words and not enough pictures). What would be helpful would be to get a few of the worst offenders: Aegon, Aviva, Friends Life, Legal & General, Phoenix, Prudential, Royal London, Scottish Life, Scottish Widows, Standard Life and Zurich, in a room at the same time – and bang their heads together. And threaten them that if they don’t get their acts together and stop handing over pensions to the scammers, they will be made to read and memorise the 78-page Scams Code and recite it every morning before coffee break. Twice. Then snap all their box-ticking pencils in half, and JOB DONE! It really isn’t rocket science – there are usually some hints which are as subtle as a brick, such as: the sponsoring employer doesn’t exist; or the member lives in Scunthorpe and is transferring to a scheme whose sponsoring employer is based in Cyprus. Or Hong Kong. Now, I know there was a bit of a hiccup with the Royal London v Hughes case when Justice Morgan overturned the Ombudsman’s determination. But dear old Hughes had probably had a few Babychams too many – and it had slipped his mind that the law is supposed to be about justice and common sense. And that just because a particular piece of legislation has been written by an ass, it doesn’t have to be interpreted with stupidity.

“Significant time and effort goes into protecting members from scams”

This, of course, may be true. I only get to see the cases where the negligent ceding providers dohand over the pensions to the scammers. I rarely get to see the ones that have a narrow escape. But what worries me is that I am in the process of making complaints to the ceding providers who have handed over pensions to the scammers, and not a single one of them thinks they have done anything wrong. So, if they do spend “significant time and effort” doing the protecting bit, how come so many of them still fail so badly? And then try to deny they failed. These providers spend very significant amounts of time and effort writing long, boring letters about how they did nothing wrong – letters which must have taken them at least an hour to write. And yet they won’t spent two minutes checking – and stopping – transfers to obvious scams.

“The more detailed the due diligence, the more suspicious traits are identified”

I am a bit suspicious that this indicates a touch of porky pies here. I’ve never seen any evidence of ANY due diligence by the ceding providers. A bloke at Aviva once told me that they spent thousands on research and due diligence – but I see no evidence of it. The problem is, the ceding providers don’t know what they don’t know. And, to coin one of my favourite phrases: “they don’t know the questions to ask, and even if they did then they wouldn’t understand the answers”.

Interestingly, if – instead of repeatedly spending hours denying they did anything wrong when they handed over millions of pounds’ worth of pensions to the scammers – they spent some time talking to me and the victims trying to learn what went wrong and what due diligence should have gone into preventing a dodgy transfer, they might learn how to stop failing so badly.

SIPPS (including international SIPPS) are the vehicle of choice by scammers

Agreed. But the scammers still love the good old QROPS. But whether it is a SIPPS or a QROPS – both of which are just “wrappers” at the end of the day, it is about what goes inside the wrappers. Where the scammers make their money is in the kickbacks: 8% on the pointless, expensive insurance bond from OMI, SEB, Generali, RL360, Friends Provident etc., and then more fat commissions on the expensive funds or structured notes.

“Quality of adviser tops the list of practitioner concerns, with member awareness a close second”

And hereby lies one of the main problems: ceding providers don’t know who the good guys are and who the bad guys are. And that is because they don’t ask. And they don’t learn from their mistakes when they get it wrong. And they don’t care when they hand the pensions over to the bad guys and their former member is now financially ruined and contemplating suicide. Instead of trying to use their appalling mistakes to improve their performance and understand what “quality” actually means, and how to tell the difference between good and bad quality, they only care about avoiding responsibility for their own failings.

The problem about “member awareness” is that most people assume their ceding provider will do some sort of due diligence. They think that words like “Phoenix Life”, “Prudential” and “Standard Life” convey some sort of professionalism or duty of care. Most members are simply unaware of the appalling track record of these providers – and the extraordinary and exhaustive lengths to which they will go to avoid being brought to justice for their negligence and laziness.

“Sharing of intelligence would help avoid duplication of effort”

Oh, how heartily I agree! I remember a year or so ago, I shared some intelligence and a few beers with a nice chap from Scottish Widows. We met at one of Andy Agathangelou’s symposiums in London – the subject of which was pension scams. The Pensions Regulator was there, Dalriada Trustees were there, Pension Bee were there, lots of interested parties were there (including an American insurer from Singapore), and a couple of victims. I gave a joint presentation with one of the victims who described how he had been scammed and how his provider had handed over his pension so easily – well after the Scorpion watershed. The nice chap from Scottish Widows asked the victim why he hadn’t called the Police. The victim replied: “I am the Police”.

It was very telling that the room wasn’t full of delegates from Aviva, Phoenix Life, Prudential, Standard Life etc. None of them were interested.

Not a single provider has ever phoned me up to ask for advice, or to arrange to speak to some victims to learn something about how they were scammed and how and why their ceding providers had failed them so badly. There are so many victims all over the UK and the rest of the world. And what they all share is a passion to try to prevent other people from being scammed by the bad guys and failed by the bad pension providers. So this invaluable intelligence is freely available.

Until and unless the providers develop a conscience, they are going to continue to fuel the pension scam industry – and nothing will change. And the 79-page code might just as well be consigned to the bathrooms of Aegon, Aviva, Friends Life, Legal & General, Phoenix, Prudential, Royal London, Scottish Life, Scottish Widows, Standard Life and Zurich.

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

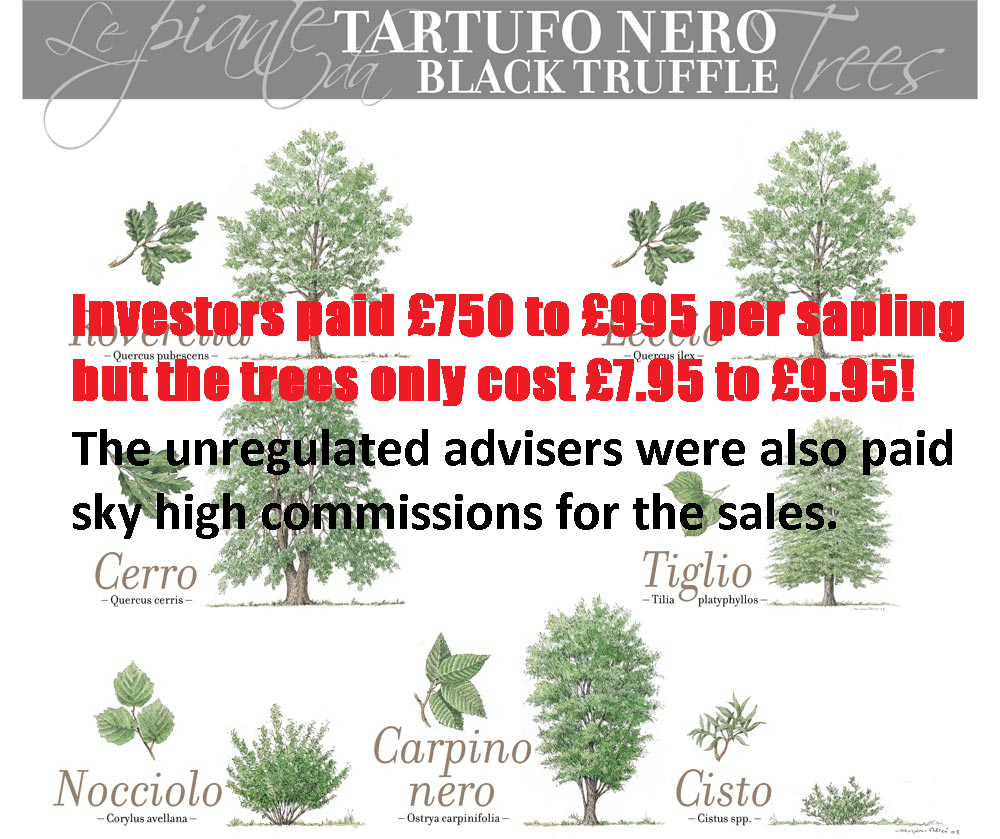

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

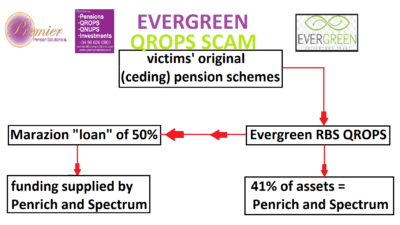

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

This could possibly be described as wonderful news for the victims of Viceroy Jones New Tech Ltd, Viceroy Jones Overseas PCC Limited, Westcountrytruffles Limited, Truffle Sales Ltd and Credit Free Limited. Or maybe not. The whereabouts of the funds is unknown. This pension liberation and investment scam saw 100 investors conned out of £9m of their pension savings.

In short, Viceroy Jones used unregulated financial advisory firms to persuade victims to invest in ‘high-value truffles for commercial sales’. With the promise of high returns on this fixed-term investment (lasting 15 years), investors believed they would reap the benefits once the truffles were harvested.

No truffles were ever harvested.

In reality, the investment saw most of the £9m of funds invested being paid into offshore bank accounts. These funds were then paid out in high commissions to the unregulated advisers who mis-sold the scheme. No supporting documents have been found regarding these investments, so the whereabouts of any remaining funds is unknown.

As I said above, it is only possibly wonderful news for the victims. Whilst the company has been wound up, the victims have been promised no compensation and do not know where their money is. This is a not an uncommon situation in scams like these. The victims of Peter Moat’s company –Fast Pensions, also do not know where their funds have gone.

Cheryl Lambert, Chief Investigator for the Insolvency Service, said:

“We take the matter of unregulated pension liberation investment schemes very seriously and will take action to stop any such schemes who have acted unscrupulously.”

However, I feel I have to disagree.

What message does the Insolvency Service send?!?

Are the perpetrators behind bars?NO!

Are the perpetrators having all their assets frozen and liquidated to pay the victim’s back? NO!

Are the perpetrators facing life without a pension?I DOUBT IT!

Are the perpetrators sorry for what they did?I DOUBT IT!

There is a long list of other pensions scammers who have scammed millions out of the public and still walk freely, creating new scam after new scam.

Winding up these companies is often of little help to the scam victims. What is left of their funds (if any) is passed on to another trustee (often Dalriada) to deal with the ‘clean up’. This action, however, is not without cost and often the funds just sit there doing nothing.

Take the Ark victims whose schemes were transferred to Dalriada – they have not had any compensation in the seven and a half years Dalriada has acted as their trustees. Dalriada, however, has continued – without fail – to charge their yearly fees and costs, further decimating the victims’ funds. AND without any suggestion of what will happen next!

Furthermore, victims that fell prey to these scams, face more stress as they are also contending with HMRC. The Taxman is sending out demands for huge tax bills, as they claim the money the victims liberated (“borrowed”) from the Ark schemes was not tax free. 55% tax is applied to money that was liberated from pension funds – this is deemed an “unauthorised payment charge” by HMRC.

The High Court needs to do a lot more than this, to send a clear message to these scammers. Prosecutions, jail sentences and large fines would be a good start.

All enquiries concerning the affairs of the companies should be made to: The Official Receiver, Public Interest Unit, 4 Abbey Orchard Street, London, SW1P 2HT. Telephone: 0207 637 1110, Email: piu.or@insolvency.gsi.gov.uk.

TPR has been neither coy nor shy in its published determination against Ward and Salih – and has openly called the London Quantum pension scheme, and the risky investments which Ward made, a “scam”.

But to any reasonable person’s mind, tPR’s determination in relation to Ward and London Quantum raises more questions than it answers. In fact, I would go even further and say that HMRC’s and tPR’s incompetence – as well as Dalriada Trustees‘ own failings – should be examined in parallel with Ward’s multiple frauds.

Because, make no mistake, London Quantum was only one of many.

It all started long before the Ark Pensions scam. Ward set out his stall transferring pensions to New Zealand and liberating 100% “tax free”. He boasted in the local Costa Blanca press that he had “helped” thousands of clients liberate their pensions (legally). Of course, this may have been free of tax in New Zealand, but when the Spanish tax authorities catch up with these clients, there will be a very expensive disaster.

It is extremely worrying that IVCM – a “phoenix” of the Brooklands disaster – is also offering the same New Zealand liberation facility today. It always worries me when firms fail to learn the lessons of past scams and expose unsuspecting victims to the same catastrophes that past scammers orchestrated. Add to this the fact that IVCM is regulated out of Gibraltar – the jurisdiction of choice for scammers such as XXXX XXXX and STM Fidecs – and I think it is well worth giving IVCM a very wide berth.

Prior to 2010, Ward was a tied agent of Inter Alliance – a company based in Cyprus which had an insurance license. For Inter Alliance in Cyprus, Ward successfully created the illusion that this gave his company Premier Pension Solutions some sort of license. But, in reality, it did not – as the Cyprus license was only for Inter Alliance and not for any other entity. Plus tied agents were (and still are) illegal in Spain.

As a sideline, Ward was flogging EEA Life Settlements as he had discovered the delights of making huge commissions out of dodgy, risky, illiquid investments to his unsuspecting victims. In 2010, Ward was working closely with Concept Trustees in Guernsey – run by Roger Berry. Initially happy to see Concept Trustees’ QROPS members have 100% of their pensions invested by Ward in EEA, Berry eventually realised that Ward’s firm was not regulated as it had been dumped by Inter Alliance. Of course, even before it had been dumped, Premier Pension Solutions wasn’t regulated anyway. But Concept Trustees was too stupid to realise that.

Concept then wrote to all the members who were clients of Ward’s Premier Pension Solutions and warned them that Ward’s firm was neither regulated nor had any professional indemnity insurance cover. Berry claimed he would not be accepting any further investment instructions from Ward, but this was basically just a load of hot air (aka lying) as he continued to accept investment instructions into EEA by Ward.

In September 2010, Premier Pension Solutions was appointed as a tied agent of AES International – a firm based in London and Dubai. The agency agreement covered PPS for investment and insurance business – but not pension transfer business. Ward’s PPS letterheaded paper claimed that it was a “partner” of AES and that it was regulated by the DGS (Spanish insurance regulator) and CNMV (Spanish investment regulator). PPS also became a member of FEIFA – the Federation of European Independent Financial Advisers (although he was later dumped by them). You can understand why so many victims thought that PPS was a bona fide advisory firm.

Then came the first of Ward’s major pension scams: Ark. It is worth looking at the history of Ark because this sets the scene for how nearly 500 victims came to lose their pensions and face tax liabilities – as well as the dozens of further scams operated by Ward (including London Quantum).

A famous footballer and his mate – a football club owner – bought a plot of land in Larnaca in Cyprus with a view to turning it into a golf resort. They paid £1.1 million for the property, but then realised it wasn’t big enough for a whole golf course (neither of them was bright enough to be able to count up to 18) and so they tried to find some other investors. The chumps they tried to con into buying more land adjacent to the original plot either couldn’t come up with the money or were frightened off such a high-risk, illiquid investment.

So the sporty pair went to see the footballer’s accountant – Andrew Isles of Isles and Storer (now owned by LB Group). Isles soothed the sporty pair’s worries by telling them that securing more investors was simple: just start a pension fund! He introduced them to what he called “two leading pension experts”: Craig Tweedley and Stephen Ward. Tweedley was already operating the KJK Investments/G Loans pension liberation scam (later to be placed in the hands of Dalriada Trustees by the Pensions Regulator) and Ward was a highly-qualified pensions expert, examiner and author.

The rest is history as nearly 500 victims lost their pensions to the Ark scam. But the sporty pair did very nicely – they sold the land in Cyprus to the Ark scheme for £4 million and pocketed the profit. The footballer tried to hide the money in Dubai but got caught and turned Queens Evidence. He and the other original investor (the football club owner) fell out and they ended up in court against each other – with the footballer triumphing. Andrew Isles also did very nicely as he sold introductions to a number of his clients and earned fat commissions in doing so.

As Ark unfolded – between mid 2010 and mid 2011 – Ward initially acted as an introducer. There were various introducers – many recruited by Ward when he ran a series of seminars in various parts of the UK. But Ward himself was the biggest introducer – accounting for more than a third of the whole £27 million fund and earning approaching three quarters of a million pounds in fees (the Pensions Regulator’s report of £350k was way off the mark).

Ward and his sidekick – bent lawyer Alan Fowler of Stevens and Bolton Solicitors – acted as the controlling minds behind Ark. The scheme documentation and the “loan” contracts were drawn up and explained by Ward and Fowler. Of the 5% commission charged by Craig Tweedley, Ward got at least 2% plus a transfer fee. But Ward had his eye on a much bigger proportion of the fees. Towards the end of the life of Ark, Ward was preparing to take Ark over from Tweedley – along with an associate of his: Peter Moat (another pension crook who went on to operate the Fast Pensions scam – now also in the hands of Dalriada Trustees). In a way, it was a shame that didn’t happen, as Tweedley did at least try to help the Ark victims, whereas Ward never lifted a finger. In fact, he simply told the Ark victims to throw the tax demands away as “HMRC would never pursue them”.

In February 2011, HMRC met with Tweedley and Ward to discuss the “loans” – so HMRC knew perfectly well that Ward was the main brain behind the scam. It is, therefore, astonishing that they did nothing to stop him operating so many further pension scams.

Ark came to a shuddering halt on 31st May 2011, when tPR appointed Dalriada Trustees and the scheme was suspended. Dalriada went up to Yorkshire to confront Crag Tweedley and relieve him of all the evidence and files relating to the scam. Tweedley told Dalriada that all the records were held down at Ward’s Manchester office at 31, Memorial Road and he drove down to collect them from Anthony Salih. He arrived to find Salih removing all the Premier Pension Solutions fee agreements on the instructions of Ward (he managed to shred most of them – but did missed a few which I now have).

After Ark, Ward went on to run the Evergreen Retirement Benefits QROPS scam with accompanying 50% “loans” and a further 300 victims lost £10 million worth of pensions. HMRC removed Evergreen from the QROPS list when they realised it was a liberation scam and Ward fell back on two more UK-based, bogus occupational schemes: Southlands and Headforte. Plus, he registered a number of new schemes – including Capita Oak.

The Capita Oak scheme was another bogus occupational scheme registered by Ward with a fictitious sponsoring employer: RP Medplant (Cyprus). There is, however, a firm called RP Med Plant in Cyprus. The Capita Oak trust deed was written by Ward’s bent lawyer Alan Fowler. Ward took responsibility for the transfer administration – transferring valuable personal and final salary occupational pensions into this scam – in the full knowledge that he was condemning hundreds of victims to certain financial ruin and poverty in retirement. Capita Oak is now also in the hands of Dalriada Trustees.

Other pension scams that Ward was operating – in addition to Southlands and Headforte – from 2012 onwards included Feldspar, Hammerley, Meribel, Halkin, Randwick, Bollington Wood and Westminster. And, of course, Dorrixo Alliance which was the trustee for many of these scams. Capita Oak and Westminster are both under investigation by the Serious Fraud Office.

How much more evidence do they need?

In May 2014, HMRC was given evidence of all of Ward’s various scams – including Dorrixo Alliance. They were also given detailed testimony by me and a number of victims of what Ward had been up to in the pension liberation fraud industry since Ark. It would have been very easy for HMRC to look up to see what other pension schemes Dorrixo was trustee to. Had they done this, they would have seen that Dorrixo was the trustee for the London Quantum scheme. If HMRC had taken any action, they could have prevented Mr. N – a serving police officer – and 96 other victims from losing their pensions to Ward and his various dodgy, inappropriate investments (including loans to Dolphin Trust).

If we add to the above catalogue of scams the Continental Wealth Management scam – 1,000 victims facing the loss of £100 million worth of life savings – Ward has been responsible for the destruction of thousands of people’s pensions this past eight years. Plus several suicides and deaths from stress-related medical conditions.

SERIOUS QUESTIONS ARISING FROM THE PENSIONS REGULATOR’S DETERMINATION RE:

Mr Stephen Alexander Ward – The Pensions Regulator case ref: C46205159

Ward was a director of Dorrixo from 13 October 2011 to 28 April 2015. A company called Quantum Investment Management Solutions LLP (“QIMS”) has at all material times been the sole sponsoring employer of the Scheme. Dorrixo became the sole trustee of the Scheme on 19 April 2014. Dorrixo is also recorded as being the Scheme administrator.

HMRC AND TPR WERE GIVEN EVIDENCE OF WARD’S COMPANY, DORRIXO, IN MAY 2014. THEY WERE ALSO GIVEN EVIDENCE OF A LARGE NUMBER OF SCAMS WARD OPERATED AFTER ARK – ALL INVOLVING LIBERATION FRAUD. WHY WASN’T ACTION TAKEN TO PREVENT LONDON QUANTUM? ALL 97 VICTIMS – INCLUDING A SERVING POLICE OFFICER – COULD HAVE BEEN PREVENTED.

On 18 June 2015 the Regulator appointed Dalriada Trustees Limited (“Dalriada”) as an independent trustee to the Scheme, with exclusive powers.

HAS ONE SINGLE PENNY EVER BEEN RETURNED TO ANY OF THE PENSION SCAMS PLACED IN THE HANDS OF DALRIADA TRUSTEES? THERE ARE DOZENS OF THEM, AND FEW – IF ANY – OTHER INDEPENDENT TRUSTEES ARE EVER APPOINTED BY TPR. BUT THERE SEEMS TO BE NO RECORD OF ONE SINGLE MEMBER EVER GETTING ANY RETURN FROM ANY OF THE SCHEMES IN THE PAST EIGHT YEARS – DESPITE THE MANY MILLIONS DALRIADA HAVE PAID THEMSELVES FROM THESE SCHEMES.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

AS THIS EVIDENCES THAT THIS SCAM COULD EASILY HAVE DWARFED ARK IN A VERY SHORT SPACE OF TIME, DON’T HMRC AND TPR RECOGNISE THAT THEIR LAZINESS AND NEGLIGENCE NEED TO BE ADDRESSED? THEY LEARNED NOTHING FROM ARK – AND WHILE THERE ARE VALID CRITICISMS OF WARD FOR HAVING LEARNED NOTHING, HE IS JUST A COMMON SPIV WHILE HMRC AND TPR ARE SUPPOSED TO BE GOVERNMENT DEPARTMENTS WITH A RESPONSIBILITY TO PROTECT THE PUBLIC. THE SCALE OF THIS SCAM SHOWS THESE TWO ORGANISATIONS ARE NOTHING BUT HOPELESSLY INEPT AND AMATEURISH IN THEIR APPROACH TO DILIGENCE AND PUBLIC RESPONSIBILITY.

The Scheme was promoted to potential new members by introducers. These included the following entities: GoBMV; Baird Dunbar; What Partnership; the Resort Group PLC; Friendly Investments; Premier Mark Consultants and Quantum Wealth Management Solutions Limited.

THE DANGERS OF THE SCOURGE OF “INTRODUCERS” SHOULD HAVE BEEN LEARNED FROM THE ARK SCAM IN 2011. WARD RECRUITED DOZENS OF THEM ALL OVER THE COUNTRY. AND YET NONE OF THEM HAS EVER BEEN BROUGHT TO JUSTICE FOR THEIR PART IN ARK, AND HAVE GONE ON TO OPERATE AS INTRODUCERS AND EVEN HOLD KEY CENTRAL ROLES IN LATER SCAMS. THIS INCLUDES FRIENDLY INVESTMENTS AND JULIAN HANSON – WHOSE SCHEMES ARE NOW ALSO IN THE HANDS OF DALRIADA TRUSTEES.

Gerard was responsible for producing template risk letters, member application forms, pro forma declarations stating that the person signing them was a self-certified sophisticated investor, member booklets and the statement of investment principles (of which there were four versions). Gerard sent these documents to members once they had been introduced to the Scheme by an introducer.

GERARD ASSOCIATES, RUN BY GARY BARLOW, HAD ACTED AS AN INTRODUCER TO WARD IN THE ARK SCAM. AND YET HE WAS LEFT FREE TO OPERATE IN THE SAME CAPACITY IN THE LONDON QUANTUM SCAM – AND EVEN TAKE ON A MORE CENTRAL ROLE. GERARD ASSOCIATES WAS AT THE TIME AN FCA-REGULATED FIRM – AND REMAINS SO TO THIS DAY. THE FCA HAS TAKEN NO ACTION TO REMOVE THIS FIRM OR TAKE ANY ACTION AGAINST GARY BARLOW.

GERARD ASSOCIATES’ GARY BARLOW WAS PAID £253,000 FROM THE LONDON QUANTUM SCHEME FOR DEFRAUDING VICTIMS INTO SIGNING AGREEMENTS THAT THEY WERE “SOPHISTICATED” INVESTORS. SO WHY HASN’T BARLOW BEEN PROSECUTED AND JAILED – AND MADE TO PAY THIS MONEY BACK TO THE VICTIMS?

A material number of the new members had a low or medium appetite for investment risk and, in any event, were unaware that the Scheme’s investments were high-risk investments. The Panel was troubled by the apparent disconnect between members’ appetite for risk and the high risk nature of the investments made by Dorrixo. Mr Ward accepted that the Scheme’s investments were high risk, but claimed this was made clear to new members in the Member Booklet.

I DON’T KNOW WHAT SORT OF DRUNKEN DUMMIES MADE UP TPR’S “PANEL”, BUT DID THEY SERIOUSLY THINK THAT ANY PENSION FUNDS SHOULD EVER INVEST IN HIGH-RISK CRAP? INDIVIDUAL MEMBERS’ APPETITE FOR INVESTMENT RISK IS IRRELEVANT – THIS WAS A PENSION FUND, NOT A CASINO.

The case against Ward was based on failures of competence and capability, and also a lack of honesty and integrity as well as Ward’s involvement with “pension liberation” as an introducer of members to the “Ark” schemes.

BUT TPR AND HMRC KNEW ALL ABOUT THIS BACK IN 2010 AND 2011. WHY DID THEY DO NOTHING TO PREVENT WARD FROM SCAMMING MORE VICTIMS OUT OF MORE MILLIONS OF POUNDS. THEY STOOD BACK AND WATCHED – DESPITE HAVING HARD EVIDENCE THAT HE WAS STILL UP TO HIS CRIMINAL MISCHIEF.

Mr Ward did not dispute that a company of his (Premier Pensions Solutions SL) was involved in introducing members to the Ark Schemes, but states that the relevant activity pre-dated any finding by the courts of pensions liberation and that Mr Ward had no knowledge that the schemes were being used for such activity.

BUT HMRC, TPR AND DALRIADA ALL KNOW THIS ISN’T TRUE. THEY HAVE ALL SEEN EVIDENCE THAT WARD AND HIS BENT LAWYER ALAN FOWLER ACTUALLY PRODUCED THE “LOAN” (MPVA) DOCUMENTATION AND EXPLAINED THE LOANS IN SOME CONSIDERABLE DETAIL TO THE VICTIMS. THE MPVA CONTRACTS WERE DRAWN UP BY FOWLER. IS IT REALLY CREDIBLE THAT NEITHER HMRC NOR TPR WOULD HAVE OBJECTED TO THIS STATEMENT?

The Panel did not consider there was sufficient evidence of Ward having actual knowledge of, or turning a blind eye to, the illegal nature of the activity of the Ark Schemes when carrying out his role as introducer before.

SERIOUSLY? I HAVE GIVEN EVIDENCE OF THIS TO BOTH HMRC AND TPR ON MANY OCCASIONS. THIS HAS BEEN DISCUSSED AT MEETINGS WITH DALRIADA TRUSTEES ON MANY OCCASIONS. EVIDENCE OF THIS HAS BEEN GIVEN TO THE SERIOUS FRAUD OFFICE ON MANY OCCASIONS BY VARIOUS VICTIMS AND ME. WHAT FURTHER EVIDENCE DID THE PANEL WANT? EVERY ARK MEMBER’S FILE WAS FULL OF SUCH EVIDENCE. EITHER TPR IS LYING OR IT IS INCOMPETENT. OR BOTH.

The Case Team also relied on certain alleged failures in relation to other pension schemes (called Headforte and Halkin), of which Mr Ward was a trustee. These are denied by him (e.g. an allegation of failure to appoint an auditor to those schemes) and the Panel did not consider it necessary to make findings in respect of them.

SO WHAT ACTION HAS TPR TAKEN IN RELATION TO HEADFORTE AND HALKIN? BOTH WERE BEING USED FOR PENSION LIBERATION FRAUD BY WARD – AND YET THE VICTIMS PROBABLY STILL HAVE NO IDEA WHAT HAS HAPPENED TO THEIR MONEY. IT IS ABSOLUTELY ASTONISHING THAT NO ACTION HAS BEEN TAKEN IN RELATION TO THESE TWO SCHEMES, PLUS ALL THE OTHERS WARD HAS BEEN OPERATING OVER THE YEARS.

Stephen Alexander Ward (date of birth 11 July 1955) is hereby prohibited from being a trustee of trust schemes in general. This order has the effect of removing the above-named individual from all or any schemes of which he is a trustee. By section 6 of the Pensions Act 1995, any person who purports to act as a trustee of a trust scheme whilst prohibited under section 3 is guilty of an offence and liable (a) on summary conviction to a fine not exceeding the statutory maximum, and (b) on conviction on indictment to a fine or imprisonment or both.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

THIS IS NOT JUST THE DEATH OF TRUST, BUT OF ANY CONFIDENCE IN THE GOVERNMENT, REGULATORS AND CRIME PREVENTION AGENCIES TO PREVENT OR DEAL WITH PENSION SCAMS AND SCAMMERS.

This week Henry Tapper wrote a blog entitled, “The wheels of the law turn (too) slowly”. He exposes the fact that when it comes to financial crime the justice system in place just isn´t enough. I think he was being generous with his title. The wheels of the law don’t just turn slowly – they just don’t turn at all. Friendly Pensions has been in the news this week.

In the case of Friendly Pensions, we know ringleader David Austin is guilty of setting up 11 fake schemes, with toxic investments including a truffle farm. We know that he and his partners in crime, Susan Dalton, Alan Barratt and Julian Hanson (also connected to the Ark Scam), are guilty of scamming 245 pension savers out of £13.7 million. We knew all of this back in January 2018, yet no arrests have been made!

“David Austin, 52, has been banned from serving as a pension trustee and disqualified from working as a company director for 12 years. His business partners Susan Dalton, Alan Barratt, and Julian Hanson have also been barred from trustee roles.

David Austin’s daughter, 25-year-old Camilla, has been banned from serving as a director for four years for helping him with the scheme.”

They have been asked to pay the money back but by the looks of their social media accounts, I don´t think there is much left. Camilla’s Facebook and Instagram accounts show her sunning herself on beaches and yachts around the world, and posing at luxury alpine ski resorts. David Austin is pictured on a gondola in Venice. They certainly got to enjoy the proceeds of their many victims’ pensions.

Camilla Austin was a central part of the operational side of the Friendly Pensions scam. She and a number of her girlfriends went into nursing homes and approached elderly, frail and vulnerable elderly people. They easily conned them into signing transfer request forms – all that is required to get their hands on millions of pounds’ worth of pension funds. And, of course, we all know that the ceding providers do nothing to stop fraudulent transfers.

As Henry points out, banning these people from acting as trustees or directors, does little to deter past, present and future pension scammers. A ban is barely a slap on the wrist as far as we are concerned; these scammers can still launch any number of future dodgy schemes by simply finding the next crooked stooge – just as XXXX XXXX used the idiotic Karl Dunlop to be a director in the Capita Oak scam.

Keeping pension savers safe from financial crime should be at the top of the list – but, instead, it is at the bottom. Pension scammers are left free to commit their crimes over and over again. Take Julian Hanson: he was busily scamming dozens of Ark victims out of more than £5.3 million worth of pensions back in 2011 and 2012, yet he was not prosecuted or jailed. Hence, he was still able to get “friendly” with David Austin and go on to scam hundreds more victims out of their pensions.

Despite investigations being made into these schemes, Ward was still able to go on and create the CWM monster scheme that saw around 1,000 victims conned out of their pension funds. Ward is hovering somewhere between his collection of luxury villas in Florida and the Spanish Costa Blanca – but at least he is no longer doing pension transfers. Over the past nine years, Ward can be linked to dozens more pension scams that have left thousands of victims’ funds decimated.

These cases are just the tip of the iceberg. We must not forget Philip Nunn and Patrick McCreesh´s investment scam Blackmore Global. This was in the wake of them doing the lead generation for the Capita Oak and Henley Retirement Fund scams. The Insolvency Service has wound up these schemes, yet Nunn and McCreesh remain free to defraud more victims as they have never been brought to justice.

David Vilka of Square Mile International was one of the main promoters of the Blackmore Global Fund scam. He “advised” dozens – possibly hundreds – of victims to invest their pensions in this scam (despite the fact that he is neither qualified nor regulated to give investment advice). Again, he has never been prosecuted or jailed, so still remains at large – free to continue scamming people out of their pensions.

You can see a depressing pattern here: these words are about cold, hard facts. The authorities are leaving known scammers free to keep scamming.

Victims of these scams have been left in misery and financial ruin. Some have taken their own lives. Yet the perpetrators, those guilty of these repeated financial crimes, are free to do as they please.

This area of financial crime really is where the wheels of the law don´t seem to turn. Shame there aren’t any regulators capable of doing any regulating, or law enforcement agencies capable of enforcing the law.

Fast Pensions – Slow Law Enforcement – Stationary Regulators – same old, same old. Looks like the embarrassment of our hopeless, lazy and impotent regulators and limp law enforcement when it comes to financial crime has struck yet another blow for justice and another goal for the scammers in this case the Moats of Fast Pensions.

his case the Moats of Fast Pensions.

The Fast Pensions scam couldn’t have been much more obvious: a known scammer – Peter Moat of Blu Debt Management (one of the promoters of the Ark Pension scam and associate of Stephen Ward) had set up a very clumsy pension liberation scam. It was loosely modeled on Ward’s Ark scam, but as Moat was clearly nowhere near as intelligent and crafty as Ward, it was screamingly obvious from square one that it was an outright fraud.

In fact, if you think about how the Moats got this scam got off the ground, it was the usual routine:

HMRC registered 15 occupations pension schemes (whereas with Ark it was 14)

The sponsoring employer had never traded, nor had any prospect of ever trading or employing anyone

The trustee firm, FP Scheme Trustees, had a sole director: Jane Wright. A young woman who worked as Peter Moat’s bookkeeper – with no experience in being a pension trustee and was only paid to be a “stooge” to keep Peter Moat’s name out of the scheme

Peter Moat’s main business was loans – personal and bridging

HMRC and the Pensions Regulator did nothing to check this obvious scam out. All the might of Britain’s regulators and law enforcement stood by while, courtesy of the Moats, more than 400 people were defrauded out of their life savings – FAST PENSIONS – SLOW LAW ENFORCEMENT – STATIONARY REGULATORS.

Between November 2016 and May 2017, there were 18 complaints by Fast Pensions victims to the Pensions Ombudsman. All 18 were upheld. It was clear from the complaints and the Ombudsman’s determinations that the scheme was a scam and that the Moats, Peter and his wife Sara, were out and out fraudsters.

Still, neither the regulators nor law enforcement agencies lifted a finger to stop the Moats: FAST PENSIONS – SLOW LAW ENFORCEMENT – STATIONARY REGULATORS, is the basis of this case.

The Moats remain living in luxury in their palatial villa in Javea on the Costa Blanca – driving around in their flash cars. What paid for this gorgeous lifestyle was £millions stolen from innocent, hard-working British citizens – while the callous, lazy, impotent regulators and law-enforcement agencies stood by and watched.

As the great parliamentarian Edmund Burke said, “The only thing necessary for the triumph of evil is for good men to do nothing.” In my humble view, what is even worse is for hopeless and uncaring men to do worse than nothing: to pretend to be good men.

On this sad and disgusting topic, I will write no more – but leave this blog’s words to the son of one of the victims who attended the High Court hearing in the matter of the winding up petition by the Insolvency Service against Peter and Sara Moat, Fast Pensions, FP Scheme Trustees, the 15 bogus occupational pension schemes and Moat’s various loan companies.

Fast Pensions Victim Vs Fast Pensions Ltd.

Claimant: Fast Pensions Victim (Fast Pensions Ltd DM1 Scheme member) Defendant: Fast Pensions Ltd

Manchester Court of Justice Date: 30th May 2018 Time: 14:00. Case Reference: Claim No XXXX of 2018.

Case:

In 2012 my father had a personal pension fund which had accumulated to over £XXXX as a result of him working hard and saving over a number of years.

In September of that year my father took a “cold call” from a gentleman representing a consultancy firm called Capital Consulting. He was informed that by transferring his pension funds from the existing scheme to another pension scheme he would benefit in as much that he could withdraw 25% of his pension fund (tax-free) on the transfer and sign up to a Five-Year Fixed Plan giving my father a fixed 5% bonus each year over the 5 years, and at the end of the 5 years could have a payout without any fixed penalties.

My father thought through this proposal, as there had been and still were serious issues with the Equitable regarding pension schemes, so my father arranged to have a home visit from Capital Consulting.

He listened to their proposals and then decided to accept the proposal. My father signed into the DM1 Retirement Plan on the 4th. October 2012, the administrators were to be AC. Management & Administration Ltd, who at that time were based in Gorseinon, South Wales. A sum of over £XXXX was then transferred into the ACMA Client Account of Barclays Bank Cardiff.

On the 26th October 2012 my father received a letter from a Jane Wright (Pension Processor) stating that the 5 Year Plan had now started with Fast Pensions. Soon after signing up to the scheme some of the initial promises of the scheme did not materialise so my father made numerous phone calls on the one phone no. that was available 08453730569 which would transfer onto answerphone on most occasions.

My father’s main concern related to the following. “We have just recently developed a client login area and this should be available shortly. This will enable you to track your pension.”

My father phoned regarding this facility and on the few occasions he managed to receive an answer he spoke to Jane Wright who stated that there was IT issues but it would be up and running shortly. My father is still waiting.

My father received annual statements for his DMI Retirement Plan for 2013/2014/2015. My father did not contact Fast Pensions Ltd again until June 2015, when he applied for a Flexi Drawdown Payment of £XXXX. The drawdown application was made on the 20th June 2015. Legislation had been introduced in April 2015, whereby a member of a pension scheme had the option of using this legislation to withdraw an amount from their pension fund, so my father took up this option from Fast Pensions.

The drawdown application was made on the 20th June 2015. It was eventually paid out as two payments. The first payment of £XXXX was paid in October 2015 as an interim payment and the balance was paid on the 9th November 2015.

There are number of reasons why this took so long and for the money to be received. The main reason was the total lack of communication from Fast Pensions.

Fast Pensions Ltd had, as already mentioned, one contact number which was an 0845 number which would obviously cost more than the standard rate to call often to be met by an answering machine, and incidentally cost my father a large amount of money. When my father did manage to succeed, it was from a Paul Bennett (Pension Administrator) who was so unhelpful and uncooperative towards my father’s questions. He would often be met with “I will have to speak to my manager Mr Gary Henderson and get him to come back to you”

During these months I personally spoke to Paul Bennett as he would often ignore calls from my father’s mobile and found if I called from a withheld number he would accept the call. I personally found Mr Bennett to be constantly unable to answer questions often just finding excuses to the questions in which he was presented with. Mr Bennett on one occasion told me he could not speak to me as I was not the policy holder. Mr Bennett was provided with a letter of authority from my father to enable me to act on his behalf.

Owing to the lack of responses, my father asked Paul Bennett for Mr Henderson’s email or telephone number but was told” it was not company policy to issues clients with direct contact details.”

Throughout the period of time dealing with Mr Bennett there would be long delays between his emails and responses so again adding to a further delay of dealing with the drawdown application.

My father was asked to return the completed application forms to the registered address in London (being a “virtual address”). He duly sent the paperwork to this address to have it returned to sender, so my father sent it again, this time by recorded delivery which was also returned by the Royal Mail stating “no one is available to sign for it”. My father actually spoke to Head of Operations at the Westminster sorting office to verify this. Mr. Bennett on the rare occasion my father actually spoke to him, stated there had been problems but had now been rectified. It certainly had not.

This was further evidence of a total breakdown of communication and excuses for not dealing with my father’s request. Eventually Mr Bennett responded to this issue and issued the forms again which were this time sent by e-mail. My father was then informed by Mr Bennett that he had missed the deadline for the end of August pay run and he would not receive it that month. The delays were simply down to lack of cooperation and communication from Mr Bennett and Fast Pensions Ltd. At this point Fast Pensions paid an interim payment of £XXXX as my father had repeatedly told Paul Bennett that he was struggling financially.

He was later quoted by Mr Bennett that the balance of the drawdown payment would reach his account by 30th September 2015, not surprisingly this did not happen. He did although receive a payment slip with the current amounts of the drawdown, £XXXX gross and £XXXX net. My father received the notification from the HMRC that Fast Pensions Ltd had informed them of the payment, which my father finally received in full as already mentioned by the 9thNovember 2015. I will point out at this time, that this transaction to the HMRC will have been completed with an RTI. Note what occurs when Fast Pensions try to send the RTI for the second drawdown payment.

On several occasions my father requested an explanation and apology for the total lack of communication, payment delays, mal-administration, and mismanagement from Fast Pensions Ltd. This was never received.

Owing to the serious issues concerning Fast Pensions my father decided to seek advice from an independent regulated Financial Advisor. They highlighted various issues, including the way the transfer from the Equitable to Fast Pensions had been organised.

At this time my father requested the paperwork from both Fast Pensions Ltd and the Equitable Life regarding the transfer of funds. One of the main questions which came out of the independent advice and requested from Fast Pensions Ltd was details of the pension fund and the fund portfolio. My father never received this information.

Over the previous few months the worry, financial distress and health issues caused by Fast Pensions Ltd was having an effect on my father, so he took a break before he applied for his next drawdown payment.

On the 29th January 2016 my father contacted Fast Pensions Ltd to apply for his next drawdown. He requested the payment after the 5th April 2016. This was to give Fast Pensions enough time to process the application and fall into the 2016/2017 tax year.

At this point we were aware of Fast Pensions Ltd being under investigation by South Wales Fraud Squad. My father had provided South Wales Fraud Squad with several pieces of evidence in relation to his dealings with Fast Pensions Ltd.

In February 2016 my father received several emails from Paul Bennet quoting that the request was received and would be processed, but it was becoming evident that from the end of February 2016, there was no answer from Fast Pensions Ltd and all communication ceased. No emails or telephone calls were received from Mr Bennett from the end of February 2016. On 23rd March 2016, my father received an email from DC. Andy Holmes of the Economic Crime Unit who informed my father that Paul Bennett had terminated all links with Fast Pensions Ltd and had left at the end of February 2016.

Mr. Bennett had quoted on his LinkedIn profile that he was employed by a company called Jackson Wood from August 2014 until February 2016. (No mention of Fast Pensions) I then decided to enquire about Jackson Wood Ltd and found a familiar name as the Director. Mr Ian Stuart Chapman, who is also the director of

My father was later made aware by DC Andy Holmes (Economic Crime Unit, Wales) that Paul Bennett had been helping with enquiries in relation to Fast Pensions Ltd. He also informed my father that Paul Bennet had left Fast Pensions Ltd without informing him. From the period of Paul Bennet ceasing communication at the end of February my father could not contact anyone at Fast Pensions.

My father, at a later date checked Mr Bennett’s profile and noted that he had moved to a company called Silverene Administration of 50, Chorley Road, Bolton, BL1 4AP, (company no 09088060). He has again moved on and is now employed by a company called Cranfords, Pension Administrators.

The Director of Silverene Administration Ltd is a Merle Oper who was also the founder of Umbrella Loans Ltd from 2010-April 2014.

Mr Bennett provided my father with an email to contact Sara Moat (sara.moat@blupropertygroup.com) surprisingly Sara Moat never replied to any of my father’s emails.

My father did not receive any communication from Fast Pensions from February 2016 until May 2016. This was when he received a letter from Sara Moat informing my father that Paul Bennett had left Fast Pensions (it had only taken three months for Fast Pensions to mention this)) and due to his departure, they had experienced difficulties and delays. Sara Grace Moat quoted in this letter that the ongoing request had been sent to payroll department, and my father would receive confirmation of this within 14 days. My father is still waiting for that confirmation.

It was now becoming a very serious situation as all communication with Fast Pensions had ceased and this was continuing to cause my father further stress, financial difficulties, and ongoing health issues.

“If you believe that a firm has promoted or sold you a UCIS that is not suitable for you, sold a UCIS to you unlawfully or without fully explaining the risks, you should make a complaint to the firm involved”. (www.fca.org.uk)

Regarding the above reference from the FCA website, the amount of times me and my father have complained about the conduct of Fast Pensions – it is all recorded and has also being made available to those requesting it, i.e. Economic Crime Unit, Serious Fraud Office and others.

After several requests for information on my father’s investment, including the investment portfolio, and an up to date statement, I do believe that the reason you have not made it available, is that it was put into a UCIS.

Therefore, I find myself alongside my father reading peoples experiences, comments and consequences resulting from Fast Pensions. Not to mention the contact with the Serious Fraud Unit and Economic Crime Unit who are all actively investigating Fast Pensions. Hence the reason why my father and I openly and transparently discuss all emails to them relating to Fast Pensions Limited.

Angie Brooks’ is also against the miss-selling of Pension Schemes which are sold by introducers or untrustworthy IFA’s. In the case of my father was ill-informed and misled as to the DM1 pension scheme and the fact is being an unregulated scheme, of which you have admitted to in your IDRP response. I am only too aware of the risks with unregulated schemes after several hours of research, because of my father’s experience with Fast Pensions Ltd.

I am also aware of the relationship Angie Brooks has with the Pension Regulator, HMRC, Insolvency Services and the FCA, and the assistance my father is giving to the Serious Fraud Office. At this moment in time Fast Pensions Ltd and its Trustees have stated nothing to defend or deny these comments, in fact they are simply adding to the negative experiences the members are having with Fast Pensions.

The appellant’s statement descibed above is followed by more than 30,000 words describing the catalog of lies and obfuscation by the Moats and their associates, and the deterioration in his vicim’s health. During this whole time, there were no arrests and no action by the regulators – FAST PENSIONS – SLOW LAW ENFORCEMENT – STATIONARY REGULATORS – disgusting all round!

The Insolvency Service has now, finally, placed the various entities involved into liquidation. It remains to be seen whether any money will ever be traced and recovered from this scam.

I would like to thank Michael Gibbon, the son of one of the Fast Pensions members, for attending the hearing and representing Pension Life and the 400 victims. Michael has been enormously supportive of our work behind the scenes – although this has clearly been hindered by the obfuscation of the Moats.

Michael has kindly summarised the details of the proceedings – and I have added some further information and thoughts.

I will now be asking all the Fast Pensions members to provide their documentation to my Assistant who will be collating as much evidence as possible for the Insolvency Service, insolvency practitioner and/or independent trustees.

The six companies originally placed into provisional liquidation by the Insolvency Service on 29th March 2018 were:

Fast Pensions Ltd – company registration number 08121954 – was incorporated on 28 June 2012. The company’s registered office is at Crown House, 27 Old Gloucester Street, London WC1N 3AX

FP Scheme Trustees Ltd – company registration number 09126225 – was incorporated on 11 July 2014. The company’s registered office is at 20-22 Wenlock Road, London N1 7GU

Blu Debt Management Ltd – company registration number 06699233 – was incorporated on 16 September 2008. The company’s registered office is at Gilbert Wakefield House, 67 Bewsey Street, Warrington WA2 7JQ

Blu Financial Services Ltd – company registration number 05912973 – was incorporated on 22 August 2006. The company’s registered office is at Gilbert Wakefield House, 67 Bewsey Street, Warrington WA2 7JQ

Blu Personal Finance Ltd – company registration number 07758290 – was incorporated on 31 August 2011. The company’s registered office is at Gilbert Wakefield House, 67 Bewsey Street, Warrington WA2 7JQ

Umbrella Loans Ltd – company registration number 07331044 – was incorporated on 30 July 2010. The company’s registered office is at Gilbert Wakefield House, 67 Bewsey Street, Warrington WA2 7JQ

The fifteen occupational schemes run by Peter and Sara Moat were:

Broughton Retirement Plan

DM1 Retirement Plan

Elphinstone Retirement Plan

EP1 Retirement Plan

Fleming Retirement Plan

FP1 Retirement Plan

FP2 Retirement Plan

FP3 Retirement Plan

Galileo Retirement Plan

Golden Arrow Retirement Plan

Leafield Retirement Plan

Springdale Retirement Plan

Talisman Retirement Plan

Templar Retirement Plan

VRSEB Retirement Plan