Fighting pension scams needs to be done logically and methodically. Decent advisers need to use high standards to help fight scams. If these standards become the norm, the scammers won’t survive and flourish so easily.

Fighting pension scams – Qualifications

Most qualified advisers want nothing to do with pension scams. Many offshore firms employ advisers who have not passed the required exams. Even if an adviser has qualified, he or she must still be registered. We recently surveyed a number of offshore advisory firms:

The Chartered Institute for Securities & Investment (CISI) is the largest and most widely respected professional body for those who work in the securities. The Chartered Insurance Institute (CII) is a professional body dedicated to building trust in the insurance and financial planning profession.

All financial advisory firms should list their advisers, provide clear details of each adviser’s qualifications and a link to the institute’s register showing evidence of the qualifications.

“Qualifications are not the be all/end all. A certificate does not prove professional competence in the field , ethics or experience. But the public have to start their due diligence somewhere.”

and many others such as Westminster and London Quantum – ruining thousands of lives. Several of his schemes are under investigation by the Serious Fraud Office. He also provided the transfer advice in the Continental Wealth scam.

Any decent adviser will want to be fully qualified. And registered. The rest should go back to selling snake oil. But consumers must remember there are exceptions. Some regulated firms get it wrong. Qualified advisers can get it wrong.

Clients must have comprehensive fact finds and risk profiles

Firm must operate adequate compliance procedures

Advisers must not abuse insurance bonds

Clients must understand the investment policy

All fees, charges and commissions must be disclosed

Investors must know how their investments are performing

Firm must keep a log of all customer complaints

Fighting pension scams – why qualifications are so essential

If clients used only firms that tick all ten Standards boxes, it would be harder for the scammers to get business. Decent firms who care about their reputation should make sure there are clear links to all advisers’ qualifications. Make it easy for the consumer to understand how to check that the stated qualifications are genuine. And help educate people to understand what qualifications are required.

All too often, advisers claim to have qualifications that don’t exist – or that aren’t appropriate for investment advice. For example, some advisers who are assuring clients they can advise on pensions and investments, only have qualifications suitable for mortgages. Or worse still, no qualifications at all. Whatever the adviser says his qualifications are, the client must be able to double check.

You wouldn’t go to an unqualified solicitor would you? So don’t use an unqualified financial adviser. Being qualified goes hand in hand with being regulated.

If it was easy to stop pension scams, everyone would be doing it. Clearing up the mess left behind a pension scam is a huge challenge. This is why clear international standards need to be recognised and adopted. The scammers are like flocks of vultures. If people only used regulated firms, they could avoid a lot of scams.

Firm must be fully regulated – with licenses for insurance and investment advice

Advisers must be qualified to the right standard

Firm must have Professional Indemnity Insurance

Clients must have comprehensive fact finds and risk profiles

Firm must operate adequate compliance procedures

Advisers must not abuse insurance bonds

Clients must understand the investment policy

All fees, charges and commissions must be disclosed

Investors must know how their investments are performing

Firm must keep a log of all customer complaints

Why is regulation so important?:

If a firm sells insurance, it must have an insurance license.

If a firm gives investment advice, it must have an investment license.

Many advisers will claim that if they only have an insurance license, they can advise on investments if an insurance bond is used. This practice must be outlawed, because this is how so many scams happen.

Most countries have an insurance and an investment regulator. They provide licenses to firms. Some regulators are better than others. Most regulators do some research and only give licenses to decent firms.

History tells us that most pension scams start with unlicensed firms. Here are some examples:

Continental Wealth Management invested 1,000 clients’ funds in high-risk structured notes. Investors started with £100 million. Most have lost at least half. Some have lost everything. Continental Wealth Management had no license from any regulator in any country.

Serial scammers such as Peter Moat, Stephen Ward, Phillip Nunn, and XXXX XXXX all ran unlicensed firms. Peter Moat operated the Fast Pensions scam which cost victims over £21 million. Stephen Ward operated the Ark, Evergreen, Capita Oak, Westminster and London Quantum pension scams which cost victims over £50 million. XXXX XXXX operated the Trafalgar pension scam which cost victims over £21 million.

Phillip Nunn operates the Blackmore Global Fund which has cost victims over £40 million. Serial scammer David Vilka has been promoting this fund. Over 1,000 people may have lost their pensions.

Firms that give unlicensed advice are breaking the law. Unlicensed advisers often use insurance bonds. These bonds pay high commissions. The funds these advisers use also pay high commissions. The advisers get rich. The clients get fleeced. The funds get destroyed. Insurance bonds such as OMI, FPI, SEB and Generali are full of worthless unregulated funds, bonds and structured notes.

Unlicensed firms hide charges from their clients. Most victims say they would never have invested had they known how expensive it was going to be.

Hidden charges can destroy a fund – even without investment losses. Licensed advisers normally disclose all fees and commissions up front. This way, the client knows exactly how much the advice is going to cost.

People can avoid being victims of pension scammers. Using properly regulated firms is one way. An advisory firm should have both an insurance license and an investment license. Don’t fall for the line: “we don’t need an investment license if we use an insurance bond”. Bond providers such as OMI, FPI, SEB and Generali still offer high-risk investments. The insurance bond provides zero protection. And the bond charges will make investment losses much worse.

The ceding providers have something significant in common with the scammers. When we expose some of the scammers, their lawyers swing into action. I once had letters from Carter Ruck, Mishcon de Reya and DWF land on my desk all in one day. The scammers’ lawyers bleat loudly about their “poor” clients’ reputations.

Every pension scam starts with a negligent transfer

But the ceding providers are just as bad: their lawyers think it is fine to facilitate financial crime. Here’s an extract from recent letter from one of them:

“You state you have “hard evidence” that our customers “have suffered serious loss because of our negligence”. You have not provided any such evidence. Please therefore produce such ‘hard evidence’ by return.”

This lawyer went on to request evidence that the provider ought to have known that the receiving scheme in

question was a scam. She went on to state that my allegations were “wholly unfounded” and to demand that I take down this blog:

But this pension provider has given me no reason to take the blog down – and no justification for the claim that the firm is “innocent” of handing over victims’ pensions to obvious scammers. Back in 2010, the Pensions Regulator warned providers about transferring pension funds to scams:

“Any administrator who simply ticks a box and allows a transfer post July 2010 is failing in their duty as a trustee and as such are liable to compensate the beneficiary.”

But the providers have studiously ignored the regulator’s warning for nine years. And thousands have lost their pensions as a result of this sickening negligence.

Transferring pensions to scammers

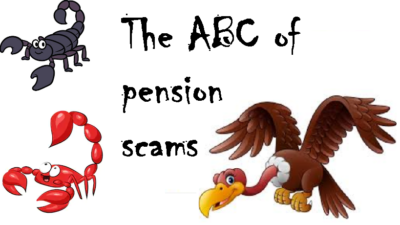

Here is an “A to Z” of the pensions industry’s negligence in handing over thousands of pensions in defiance of numerous warnings since 2010. Note: to my knowledge not a single administrator has voluntarily compensated their victims – and all have emphatically denied they did anything wrong.

Transferring pensions to scammers – the ABC of shame

Aviva: Second only to Aegon in our list of shame, Aviva transferred numerous pensions from October 2013 onwards. This was well after the Pensions Regulator’s “Scorpion” warning. The largest of these was £258,684.05 at the request of well-known scammer Stephen Ward of Premier Pension Solutions. Ward had been behind the £27 million Ark liberation scam in 2010. On 21st January 2015, Aviva’s Robert Palmer told me they needed no help or advice with avoiding negligent transfers to obvious scams. One month later, Aviva handed over £23,500 to the GFS scam.

British Steel: Long before the much-publicised handing over of multiple members to scammers in 2018, British Steel was handing over pensions to the Hong Kong GFS QROPS scam in 2014 . Mainly advised by serial scammer David Vilka of Square Mile International Financial Services in the Czech Republic, the GFS scam invested hundreds of victims’ funds in UCIS funds such as Blackmore Global.

Clerical Medical: Another disgraceful firm with a long history of handing over pensions to Ark, Capita Oak, Westminster and GFS in 2014.

This A to Z of shame goes on and on – and includes all the big names (who should have known better):

In many pension scam cases, we find victims telling us that they were not informed about the hidden charges that were applied to their fund. This is why it is essential to warn the public about the hidden dangers of charges that ruin your pension investments. These charges often take a huge chunk out of the fund before and during its new investments. Scammers lie about these charges, and victims never find out about them until it is too late.

The investments the scammers use are often high-risk and totally unsuitable for a pension fund. Pensions should be invested in diverse, low-to-medium risk assets which are prudent and liquid. And pensions don’t need an insurance wrapper at all, especially since the wrapper pays a whopping 8% commission to the scammers. And, sadly, much of the offshore advisory industry relies entirely on commissions – so the unethical advisers always chose the investments that pay the highest commissions. Unfortunately for the victims, the sweet-talking “advisers” are very good at concealing these hidden charges (commissions). They lure victims away from the small print and flash the promise of high – often “guaranteed” – returns.

Scammers – entirely reliant on commissions – are very good at blinding their victims from the risks they are inadvertently taking by putting their hard-earned cash into investments that pay the highest commissions. These scammers are pure salesmen, rather than proper financial advisers. Many of them are notQUALIFIED to give financial advice and they are only out for their “cut” of their victims’ hard-earned life savings. The hidden charges (commissions), paid unknowingly by the victims, buy the scammers their lavish lifestyle. Once the victims have signed on the dotted line, the scammers have no interest in what happens to the remainder of the funds after the commissions have been taken out.

So how does this illicit commission work? And how do the hidden charges damage a victim’s fund?

Let us assume a victim has a fund of £100,000. And he is transferring from a UK pension to an offshore QROPS.

First, a transfer specialist will charge a fee for the transfer advice. Then the offshore adviser will charge a setup fee. Then the QROPS provider will charge a setup fee. So, now we don’t have £100,000 any more – we probably only have £95,000 if we are lucky.

Then the scammer will put the victim into an insurance bond – such as OMI or RL360. The scammer will earn 8% on this (i.e. £8,000). But the victim won’t see this, because the insurance bond provider (OMI, RL360 etc) will claw this back over a ten-year period.

The scammers at OMI or RL360 will always keep a fat chunk of the fund in cash to pay their own fees – usually via hidden charges.

But let’s say they allow £80,000 of the remaining £95,000 to be invested, and let’s say the scammer at the advisory firm invests £40,000 in structured notes and £40,000 in “dirty” funds (i.e. the funds that pay the biggest commissions). This could be a further 10% in commission – so the victim will think he is getting £80,000 worth of investment, but in reality he is only getting £72,000 worth of investment. He simply can’t see the £8,000 in commissions because they are carefully hidden.

Eventually, the victim will realise that his fund is only shrinking, and that it will never have a chance to grow. Growth will be mathematically impossible, because of the constant, hidden fees/commissions. Some victims realise how they have been shafted quite quickly and are able to take positive action to move away from the rogue adviser. But for many, it is too late and too much damage has been done. Their funds will never have a chance to recover to anywhere near where they started. They would have been much better off sticking their retirement savings under the mattress. Because, of course, the “advisers” don’t care – they are long gone in their fancy sports cars and designer suits, sipping champagne at the local exclusive golf club.

In the UK we have regulations in place that prevent financial advisers from taking commissions. This works fine for the ethical, regulated sector of the financial advisory profession. But the unregulated offshore spivs who masquerade as “advisers” – and are, in reality, nothing more than silver-tonged salesmen – still do untold damage to the reputation of the industry by promoting unsuitable, high-risk, illiquid investments to low-risk pension savers (including those resident in the UK).

Many of the scammers are keen to get their UK-based victims’ pensions offshore to escape the protection of the British regulations. This, of course, prevents victims from having access to the FSCS and the ombudsmen.

A prime example of this is the dastardly duo: Phillip Nunn and Patrick McCreesh. This pair of scammers received £ millions promoting the Capita Oak, Thurlstone Loans, Henley Retirement Benefits Scheme and Berkeley Burke SIPPS scams – leaving 1,200 victims worried sick about facing poverty in retirement.

The Nunn/McCreesh double act has gone on to promote their own toxic investment fund: the Blackmore Global Fund. This is a UCIS fund (Unregulated Collective Investment Scheme), which is illegal to promote to UK residents. Yet Phillip Nunn and Patrick McCreesh sold these investments with the help of David Vilka of Square Mile Financial Services. (David Vilka is NOT a qualified financial adviser and Square Mile is not regulated to provide investment advice). Nobody knows where the Blackmore Global victims’ funds have gone – as Nunn and McCreesh will not have the fund audited (the last thing they want is anyone knowing what they have invested their victims’ life savings in). But one thing we can guarantee is that the scammers Nunn, McCreesh and Vilka made a pocket full of cash through hidden charges.

In all leading expat jurisdictions – most notably Spain and Dubai – the scammers are beavering away grinding the commission machines. They take their hidden charges with no remorse.

In the time it took the gentle reader to read this blog, at least one victim will have lost their life savings. And one scammer will have earned 8% commission out of selling a useless, pointless, expensive insurance bond – such as OMI, Generali or RL360 – and up to 10% (or even more) on the underlying investments. On top of this, the scammer – masquerading as an “adviser” – will also charge a 1% “advisory” fee. And probably a setup fee. And then there are the QROPS charges.

Henry Tapper wrote an excellent blog on this very subject – he called it FRACTIONAL SCAMMING. I do hope that all offshore advisory firms will read this carefully. The excuse that they didn’t really understand the impact of hidden charges and commissions – and were only copying what they thought the industry was already doing successfully – is simply not going to wash any more. The damage caused by this toxic practice has been widely published and exposed.

The only way forward is to go fee-based. And to outlaw commissions and hidden charges altogether. The scammers won’t do it – but decent, ethical firms will. The hard part will be to warn expats against vultures. Ethical firms will help with this initiative. Obviously, the scammers won’t.

Intro written by Kim: ‘This week Angie travelled for work (yet again): she had to fly from Granada to Barcelona. Disaster struck – her baggage sadly did not make the full journey -it’s sitting in the triangle of lost luggage no doubt. The airline – Vueling – whilst only providing the flight, was still happy to take responsibility for the loss of her bag and its contents, and compensate her. That got her thinking: if an airline can take full responsibility for a loss, why are life offices like OMI turning a blind eye to the massive losses they have caused to thousands of pension scam victims’ funds?

Over to Angie:

The financial services industry (especially offshore) has a lot to learn from the airline industry. Aviation stakeholders internationally provide the highest possible levels of safety for air travellers. This due diligence is constantly reviewed, updated and improved. The same standard of responsibility routinely happens in all jurisdictions. Regulators, as well as air crash investigators, work together when things go right. As well as when they don’t.

The work of the air industry regulators, investigators and safety trainers never ceases with all parties constantly striving to maintain the highest possible standards of performance and safety. And when something goes wrong, everybody swings into action like the A-team, International Rescue and Tom Cruise combined.

I know all this because one of my members is a Captain with a well-known airline (probably quite easy to guess which one!). He also trains pilots from a variety of other airlines in simulators – and this includes Vueling pilots. I will call him Captain BJ.

BJ is a thoroughly decent bloke and has a rather endearing fondness for chickens. He has devoted his professional life to the business of safety in travel. And behind him is a comprehensive and robust system of regulation – internationally. Financial services regulators, on the other hand, stand by and watch (with their hands firmly in their pockets – and their fingers compulsively searching for something with which to fiddle) as the equivalent of hundreds of passenger planes crash every month. The regulators stare blankly at the charred remains of the passengers’ life savings and shrug carelessly at the huge scale of human misery caused so routinely. With such flaccid regulatory regimes in so many jurisdictions, these chocolate-teapot regulators de facto facilitate and encourage losses caused by negligence and scams.

I know all this because Captain BJ is also a pension scam victim – courtesy of Stephen Ward’s Ark £27 million pension scam. Despite the extreme stress of losing his pension, he has to keep a stiff upper lip and continue with his daily routine of flying thousands of passengers safely around the skies of Europe.

My recent experience on a Vueling flight provides an interesting parallel with the “financial services” provided by Old Mutual International. Vueling sells flights. They provide the aircraft; the pilots and the cabin crew. They offer a selection of routes, food and drink, duty free goods, toilets and the expertise to get many thousands of passengers from one destination to another safely and on time; day after day after day.

What Vueling doesn’t do is operate a baggage handling service – this is provided by the airport you travel through. However, no matter how enjoyable a flight has been (if such a thing is possible!) and how punctual the take-off and landing are, the whole experience can be badly marred by the loss of a passenger’s luggage. While Vueling is responsible for the safety of the passengers, it is NOT responsible for the safety of the passengers’ luggage when it is not in the bowels of the aircraft. However, Vueling goes to extraordinary lengths to help people whose luggage has been delayed or lost. Vueling take full responsibility for a loss of luggage, luckily for me.

Earlier this week, it was the baggage handlers at either Granada airport or Barcelona airport who were responsible for my medium-sized, black, tatty suitcase. And they lost it. The case had been full of clothing typically worn by a slightly fat, grey-haired woman on the wrong side of something ending in a nought. So no desirable or valuable designer totty wear, expensive perfume or sparkly jewellery.

But Vueling provide people like me (who end up wearing the same orange jumper and purple socks two days in a row) with an easy to use, online complaints and redress facility. It wasn’t Vueling’s fault that my luggage got lost, but they take responsibility for it anyway because it is part of the whole flight “package”.

Contrast this with Old Mutual International (OMI) and the IoM regulator. And thank your lucky stars that they don’t try to run an airline (because if they did, it is unlikely any passengers or luggage would ever survive). OMI provides “insurance bonds” or bogus life assurance policies. These products serve no purpose except to pay fat commissions to rogue IFAs. And they feature a selection of risky investment products for the IFAs to earn even more commission. What OMI does not provide is financial advice – that is the job of someone else (i.e. the IFAs). But when the IFAs do the equivalent of losing the baggage, OMI takes no interest or responsibility other than to record the loss.

In the air industry, there are two things that can go wrong that can cause customers financial damage: flight delays and loss of luggage. A comprehensive complaints and redress system is routinely provided by all leading airlines. In the financial services industry, there are two things that can go wrong that can cause customers financial damage: investment failures and disproportionately high charges. No complaints and redress system is provided by life offices such as OMI and no one takes full responsibility for a loss.

If an airline experiences a crash, a huge machine swings into action to investigate the cause and take immediate remedial action to prevent the same or similar event from ever causing another accident. If a life office such as OMI experiences a crash, it pretends nothing has happened. Pension scam victims? No pension scam victims here! OMI denies all responsibility. And blames the IFA. Or the weather. Or Brexit. And keeps charging the victims the same disproportionately high fees based on the huge commissions they originally paid to the IFA that caused the crash.

Here are some examples of OMI’s crashes in the past six years:

* Axiom Litigation Fund – this was a PROFESSIONAL-INVESTOR-ONLY fund which was routinely used by rogue IFAs for ordinary, retail investors (and from which the IFAs earned fat commissions). OMI offered the Axiom fund on the bogus “life assurance” platform. And when the fund went into administration in December 2012, OMI shrugged its shoulders and said “not our problem“. And kept charging the victims the same fees as if the £120 million loss hadn’t happened.

OMI knew that many of the IFAs had been neither regulated nor qualified and that the investors were unsophisticated, low-risk, retail customers.

* LM Australian Property Fund – this was a PROFESSIONAL-INVESTOR-ONLY fund which was routinely used by rogue IFAs for ordinary, retail investors (and from which the IFAs earned fat commissions). OMI offered the LM fund on the bogus “life assurance” platform. And when the fund went into administration in March 2013, OMI shrugged its shoulders and said “not our problem“. And kept charging the victims the same fees as if the £240 million loss hadn’t happened.

* Premier New Earth Recycling Fund – this was a PROFESSIONAL-INVESTOR-ONLY fund which was routinely used by rogue IFAs for ordinary, retail investors (and from which the IFAs earned fat commissions). OMI offered the PNER fund on the bogus “life assurance” platform. And when the fund went into administration in June 2016, OMI shrugged its shoulders and said “not our problem“. And kept charging the victims the same fees as if the £800 million loss hadn’t happened.

OMI knew that many of the IFAs had been neither regulated nor qualified and that the investors were unsophisticated, low-risk, retail customers. That is £1.16 billion worth of fund losses in just over six years, but they take no responsibility for loss of funds and the pension scam victim gets no redress.

(Note – if you read the above three examples, you will see that although the funds, dates and amounts were different, the circumstances were EXACTLY the same!)

Add to this the £ billions lost through toxic, risky structured notes, and that adds up to quite a cricket score that OMI “wasn’t responsible for“.

The causes were all the same:

UNREGULATED ADVISORY FIRMS

UNQUALIFIED ADVISERS

FUNDS OFFERING HUGE COMMISSIONS

FUNDS SUITABLE FOR HIGH-RISK, PROFESSIONAL INVESTORS SOLD TO LOW-RISK, RETAIL INVESTORS

NO DUE DILIGENCE BY OMI

We know that OMI bought:

£200 million worth of failed Leonteq structured notes

between 2012 and 2016 as OMI is claiming to be suing Leonteq. But this does little to distract attention from OMI’s multiple, long-term failures for allowing such toxic investments in the first place and causing many people to become pension scam victims.

If I give my car keys to someone who is so drunk they can barely stand up – and certainly can’t spell either OMI or IOM – and there is a serious accident, whose fault is it? The drunk’s or mine?

OMI’s CEO is a bloke called Peter Kenny who used to work for the IoM regulator. So he should know better. But he doesn’t. So we must assume he would be happy to hand his car keys over to a drunk or let an unqualified pilot fly a plane with a broken wing. And he would still claim it wasn’t his fault, despite the number of pension scam victims.

The moral of this blog is: never wear orange and purple on a flight; never use an OMI life bond; always use a qualified, regulated and insured IFA. Don’t become the next pension scam victim.

My next dilemma is what to buy with my Vueling compensation. I feel a trip to Marks and Sparks coming on. (I needed a bigger size anyway!).

(Huge thanks to Captain BJ – to whom I owe my sanity).

PS – since we wrote and published this blog, my luggage has been found. Apparently, it never left Granada airport. I suspect somebody pinched it – then found the clothes inside were so dull that they didn’t think it was worth taking it after all.

If you have read our other blog you will already know that we have been waiting several years for a cold calling ban to be put in place. It is more than irritating to see that instead of a blanket ban on all cold calling they have imposed a fine on certain cold calls.

This also begs the question of how they had time to pass the legislation for the fine, but not the legislation to simply just ban all cold calling – FULL STOP – no ifs no buts. I also wonder how they are going to track down the cold callers and enforce the fines onto them. Will it be the people making the cold calls that get the fines? or will it be the companies setting up the call centres, or god forbid will it be the masterminds and serial scammers who continue to set up toxic, high-risk funds to lure in their victims?

The victims of the Continental Wealth management scam were cold called, see their story here.

An article written by the Telegraph confirms my fears about the lack of ability the regulators have in enforcing the fines they have already issued. The ICO has been fining companies for nuisance calls since 2015, it is estimated that nearly half of all land line calls are cold calls made to the elderly!

´The ICO has issued more than £5.7m in fines to cold call companies for breaching nuisance rules since 2015, but of the 27 fines issued only nine have been paid in full, recently published government figures revealed.´

The sad truth from these figures clearly shows that despite fines being made they are not being imposed, the companies are simply not paying them. If companies are happy to ignore the fines then they are probably happy to ignore the threat of a fine and continue to make cold calls. Figures from Ofgem have shown that consumers were bombarded with 3.9 billion nuisance phone calls and texts last year but only 27 fines were issued and just nine of those actually paid in full!

There are also so many loopholes these companies – who operate the call centers – can leap through. People must opt out of being cold called, if they have not done this, then companies can claim they were happy to receive the calls.

For instance, if you are online – say on a compare website – and you do not tick the box to state you do not want to be contacted by third parties, you are giving your permission to be contacted. This then means that your data is sold on and the company that calls you about the pension scheme transfer can claim that you were happy to be contacted. It wasn´t a cold call as they had opted in.

The loophole enables them to potentially escape any fine, as technically the receiver of the call had agreed to being contacted via a third party. The company making the calls can claim that they were not making a “cold call”. It feels like this legislation has been made after the horse has bolted from the stable. Hundreds of people have been scammed through the use of cold calling and hundreds more will continue to be scammed with the use of cold calling techniques, through loopholes.

Pension scams involving cold calls such as Capita Oak, Continental Wealth Management, Trafalgar Multi Asset Fund have left hundreds of victims with out a decimated pension fund. These unregulated, shameless firms and their snake salesmen are not going to acknowledge the treat of a fine, nor the administer of a fine. AND if they are fined do the government really think they will pay it?

Serial scammers like Stephen Ward who started out on the ARK pension scam, went on to scam again AND again, despite the scams being shut down by HMRC and the tPR again and again! None of the scammers who promoted these scam have been put behind bars and no money has been paid back to the victims. The scammers show no remorse for their actions. These blatant financial criminals aren´t going to pay a fine for cold calling if they aren´t going to admit the pension scheme´s they set up were fraudulent.

A quick google search of cold call gives untold amounts of advice on how to do it efficiently in 2019! Whilst some of these companies aren´t UK based, the evidence is clear. Cold calling pays and the companies that benefit from cold calling are not going to suddenly stop making them.

The regulators are really going to have to step up and do some serious regulating and enforcing if these fines are to be issued, actually followed up and collected.

The sad truth is that whilst the fines sound great on paper, they will do little to protect the public from being scammed.

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

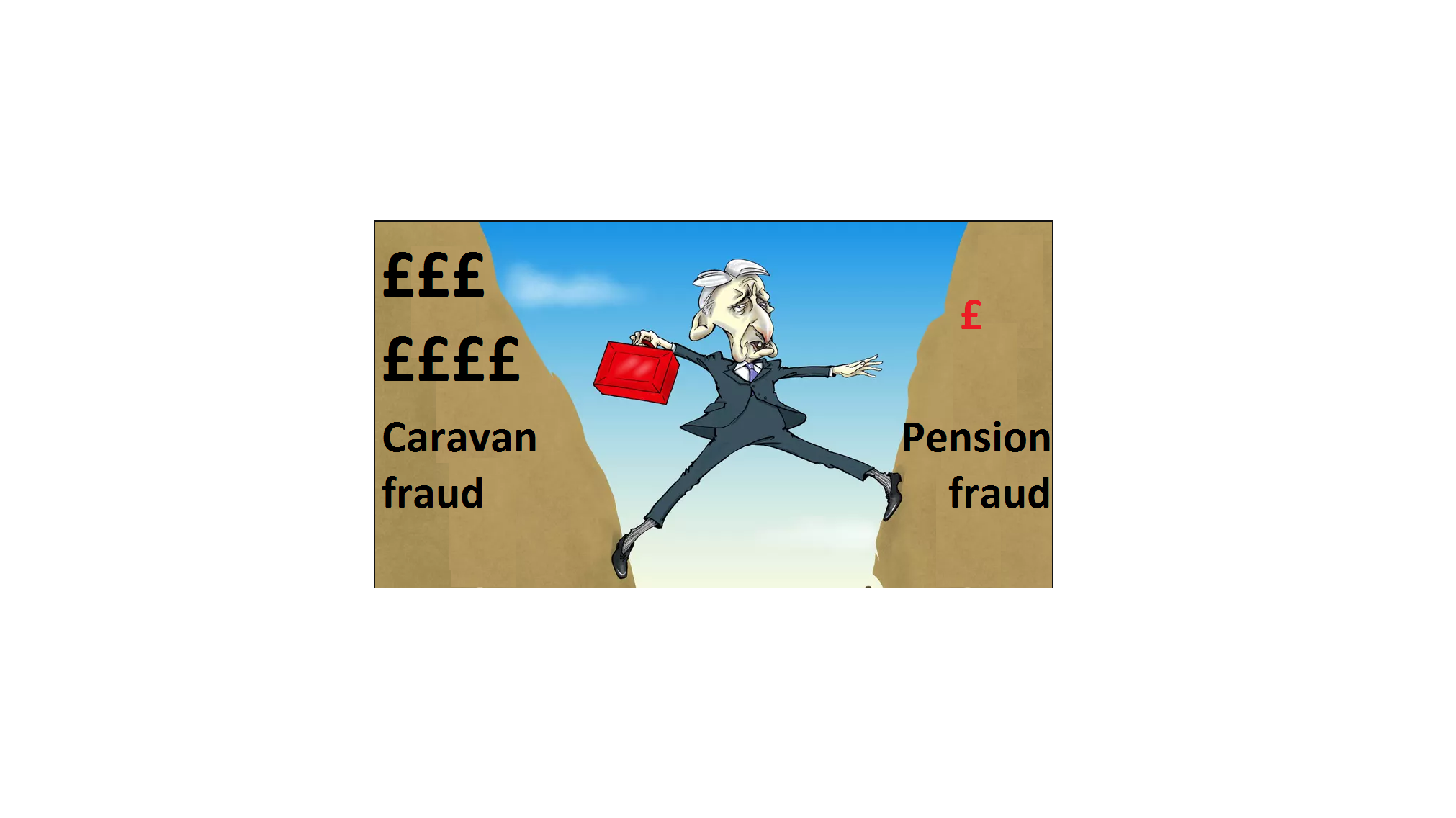

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

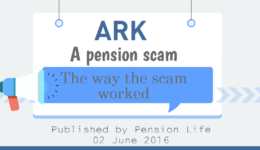

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

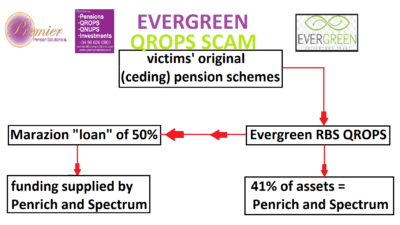

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

TPR has been neither coy nor shy in its published determination against Ward and Salih – and has openly called the London Quantum pension scheme, and the risky investments which Ward made, a “scam”.

But to any reasonable person’s mind, tPR’s determination in relation to Ward and London Quantum raises more questions than it answers. In fact, I would go even further and say that HMRC’s and tPR’s incompetence – as well as Dalriada Trustees‘ own failings – should be examined in parallel with Ward’s multiple frauds.

Because, make no mistake, London Quantum was only one of many.

It all started long before the Ark Pensions scam. Ward set out his stall transferring pensions to New Zealand and liberating 100% “tax free”. He boasted in the local Costa Blanca press that he had “helped” thousands of clients liberate their pensions (legally). Of course, this may have been free of tax in New Zealand, but when the Spanish tax authorities catch up with these clients, there will be a very expensive disaster.

It is extremely worrying that IVCM – a “phoenix” of the Brooklands disaster – is also offering the same New Zealand liberation facility today. It always worries me when firms fail to learn the lessons of past scams and expose unsuspecting victims to the same catastrophes that past scammers orchestrated. Add to this the fact that IVCM is regulated out of Gibraltar – the jurisdiction of choice for scammers such as XXXX XXXX and STM Fidecs – and I think it is well worth giving IVCM a very wide berth.

Prior to 2010, Ward was a tied agent of Inter Alliance – a company based in Cyprus which had an insurance license. For Inter Alliance in Cyprus, Ward successfully created the illusion that this gave his company Premier Pension Solutions some sort of license. But, in reality, it did not – as the Cyprus license was only for Inter Alliance and not for any other entity. Plus tied agents were (and still are) illegal in Spain.

As a sideline, Ward was flogging EEA Life Settlements as he had discovered the delights of making huge commissions out of dodgy, risky, illiquid investments to his unsuspecting victims. In 2010, Ward was working closely with Concept Trustees in Guernsey – run by Roger Berry. Initially happy to see Concept Trustees’ QROPS members have 100% of their pensions invested by Ward in EEA, Berry eventually realised that Ward’s firm was not regulated as it had been dumped by Inter Alliance. Of course, even before it had been dumped, Premier Pension Solutions wasn’t regulated anyway. But Concept Trustees was too stupid to realise that.

Concept then wrote to all the members who were clients of Ward’s Premier Pension Solutions and warned them that Ward’s firm was neither regulated nor had any professional indemnity insurance cover. Berry claimed he would not be accepting any further investment instructions from Ward, but this was basically just a load of hot air (aka lying) as he continued to accept investment instructions into EEA by Ward.

In September 2010, Premier Pension Solutions was appointed as a tied agent of AES International – a firm based in London and Dubai. The agency agreement covered PPS for investment and insurance business – but not pension transfer business. Ward’s PPS letterheaded paper claimed that it was a “partner” of AES and that it was regulated by the DGS (Spanish insurance regulator) and CNMV (Spanish investment regulator). PPS also became a member of FEIFA – the Federation of European Independent Financial Advisers (although he was later dumped by them). You can understand why so many victims thought that PPS was a bona fide advisory firm.

Then came the first of Ward’s major pension scams: Ark. It is worth looking at the history of Ark because this sets the scene for how nearly 500 victims came to lose their pensions and face tax liabilities – as well as the dozens of further scams operated by Ward (including London Quantum).

A famous footballer and his mate – a football club owner – bought a plot of land in Larnaca in Cyprus with a view to turning it into a golf resort. They paid £1.1 million for the property, but then realised it wasn’t big enough for a whole golf course (neither of them was bright enough to be able to count up to 18) and so they tried to find some other investors. The chumps they tried to con into buying more land adjacent to the original plot either couldn’t come up with the money or were frightened off such a high-risk, illiquid investment.

So the sporty pair went to see the footballer’s accountant – Andrew Isles of Isles and Storer (now owned by LB Group). Isles soothed the sporty pair’s worries by telling them that securing more investors was simple: just start a pension fund! He introduced them to what he called “two leading pension experts”: Craig Tweedley and Stephen Ward. Tweedley was already operating the KJK Investments/G Loans pension liberation scam (later to be placed in the hands of Dalriada Trustees by the Pensions Regulator) and Ward was a highly-qualified pensions expert, examiner and author.

The rest is history as nearly 500 victims lost their pensions to the Ark scam. But the sporty pair did very nicely – they sold the land in Cyprus to the Ark scheme for £4 million and pocketed the profit. The footballer tried to hide the money in Dubai but got caught and turned Queens Evidence. He and the other original investor (the football club owner) fell out and they ended up in court against each other – with the footballer triumphing. Andrew Isles also did very nicely as he sold introductions to a number of his clients and earned fat commissions in doing so.

As Ark unfolded – between mid 2010 and mid 2011 – Ward initially acted as an introducer. There were various introducers – many recruited by Ward when he ran a series of seminars in various parts of the UK. But Ward himself was the biggest introducer – accounting for more than a third of the whole £27 million fund and earning approaching three quarters of a million pounds in fees (the Pensions Regulator’s report of £350k was way off the mark).

Ward and his sidekick – bent lawyer Alan Fowler of Stevens and Bolton Solicitors – acted as the controlling minds behind Ark. The scheme documentation and the “loan” contracts were drawn up and explained by Ward and Fowler. Of the 5% commission charged by Craig Tweedley, Ward got at least 2% plus a transfer fee. But Ward had his eye on a much bigger proportion of the fees. Towards the end of the life of Ark, Ward was preparing to take Ark over from Tweedley – along with an associate of his: Peter Moat (another pension crook who went on to operate the Fast Pensions scam – now also in the hands of Dalriada Trustees). In a way, it was a shame that didn’t happen, as Tweedley did at least try to help the Ark victims, whereas Ward never lifted a finger. In fact, he simply told the Ark victims to throw the tax demands away as “HMRC would never pursue them”.

In February 2011, HMRC met with Tweedley and Ward to discuss the “loans” – so HMRC knew perfectly well that Ward was the main brain behind the scam. It is, therefore, astonishing that they did nothing to stop him operating so many further pension scams.

Ark came to a shuddering halt on 31st May 2011, when tPR appointed Dalriada Trustees and the scheme was suspended. Dalriada went up to Yorkshire to confront Crag Tweedley and relieve him of all the evidence and files relating to the scam. Tweedley told Dalriada that all the records were held down at Ward’s Manchester office at 31, Memorial Road and he drove down to collect them from Anthony Salih. He arrived to find Salih removing all the Premier Pension Solutions fee agreements on the instructions of Ward (he managed to shred most of them – but did missed a few which I now have).

After Ark, Ward went on to run the Evergreen Retirement Benefits QROPS scam with accompanying 50% “loans” and a further 300 victims lost £10 million worth of pensions. HMRC removed Evergreen from the QROPS list when they realised it was a liberation scam and Ward fell back on two more UK-based, bogus occupational schemes: Southlands and Headforte. Plus, he registered a number of new schemes – including Capita Oak.

The Capita Oak scheme was another bogus occupational scheme registered by Ward with a fictitious sponsoring employer: RP Medplant (Cyprus). There is, however, a firm called RP Med Plant in Cyprus. The Capita Oak trust deed was written by Ward’s bent lawyer Alan Fowler. Ward took responsibility for the transfer administration – transferring valuable personal and final salary occupational pensions into this scam – in the full knowledge that he was condemning hundreds of victims to certain financial ruin and poverty in retirement. Capita Oak is now also in the hands of Dalriada Trustees.

Other pension scams that Ward was operating – in addition to Southlands and Headforte – from 2012 onwards included Feldspar, Hammerley, Meribel, Halkin, Randwick, Bollington Wood and Westminster. And, of course, Dorrixo Alliance which was the trustee for many of these scams. Capita Oak and Westminster are both under investigation by the Serious Fraud Office.

How much more evidence do they need?

In May 2014, HMRC was given evidence of all of Ward’s various scams – including Dorrixo Alliance. They were also given detailed testimony by me and a number of victims of what Ward had been up to in the pension liberation fraud industry since Ark. It would have been very easy for HMRC to look up to see what other pension schemes Dorrixo was trustee to. Had they done this, they would have seen that Dorrixo was the trustee for the London Quantum scheme. If HMRC had taken any action, they could have prevented Mr. N – a serving police officer – and 96 other victims from losing their pensions to Ward and his various dodgy, inappropriate investments (including loans to Dolphin Trust).

If we add to the above catalogue of scams the Continental Wealth Management scam – 1,000 victims facing the loss of £100 million worth of life savings – Ward has been responsible for the destruction of thousands of people’s pensions this past eight years. Plus several suicides and deaths from stress-related medical conditions.

SERIOUS QUESTIONS ARISING FROM THE PENSIONS REGULATOR’S DETERMINATION RE:

Mr Stephen Alexander Ward – The Pensions Regulator case ref: C46205159

Ward was a director of Dorrixo from 13 October 2011 to 28 April 2015. A company called Quantum Investment Management Solutions LLP (“QIMS”) has at all material times been the sole sponsoring employer of the Scheme. Dorrixo became the sole trustee of the Scheme on 19 April 2014. Dorrixo is also recorded as being the Scheme administrator.

HMRC AND TPR WERE GIVEN EVIDENCE OF WARD’S COMPANY, DORRIXO, IN MAY 2014. THEY WERE ALSO GIVEN EVIDENCE OF A LARGE NUMBER OF SCAMS WARD OPERATED AFTER ARK – ALL INVOLVING LIBERATION FRAUD. WHY WASN’T ACTION TAKEN TO PREVENT LONDON QUANTUM? ALL 97 VICTIMS – INCLUDING A SERVING POLICE OFFICER – COULD HAVE BEEN PREVENTED.

On 18 June 2015 the Regulator appointed Dalriada Trustees Limited (“Dalriada”) as an independent trustee to the Scheme, with exclusive powers.

HAS ONE SINGLE PENNY EVER BEEN RETURNED TO ANY OF THE PENSION SCAMS PLACED IN THE HANDS OF DALRIADA TRUSTEES? THERE ARE DOZENS OF THEM, AND FEW – IF ANY – OTHER INDEPENDENT TRUSTEES ARE EVER APPOINTED BY TPR. BUT THERE SEEMS TO BE NO RECORD OF ONE SINGLE MEMBER EVER GETTING ANY RETURN FROM ANY OF THE SCHEMES IN THE PAST EIGHT YEARS – DESPITE THE MANY MILLIONS DALRIADA HAVE PAID THEMSELVES FROM THESE SCHEMES.

Following its appointment Dalriada discovered that there were approximately 609 files on record relating to potential new members, each at various stages of progression towards becoming a new member.

AS THIS EVIDENCES THAT THIS SCAM COULD EASILY HAVE DWARFED ARK IN A VERY SHORT SPACE OF TIME, DON’T HMRC AND TPR RECOGNISE THAT THEIR LAZINESS AND NEGLIGENCE NEED TO BE ADDRESSED? THEY LEARNED NOTHING FROM ARK – AND WHILE THERE ARE VALID CRITICISMS OF WARD FOR HAVING LEARNED NOTHING, HE IS JUST A COMMON SPIV WHILE HMRC AND TPR ARE SUPPOSED TO BE GOVERNMENT DEPARTMENTS WITH A RESPONSIBILITY TO PROTECT THE PUBLIC. THE SCALE OF THIS SCAM SHOWS THESE TWO ORGANISATIONS ARE NOTHING BUT HOPELESSLY INEPT AND AMATEURISH IN THEIR APPROACH TO DILIGENCE AND PUBLIC RESPONSIBILITY.

The Scheme was promoted to potential new members by introducers. These included the following entities: GoBMV; Baird Dunbar; What Partnership; the Resort Group PLC; Friendly Investments; Premier Mark Consultants and Quantum Wealth Management Solutions Limited.

THE DANGERS OF THE SCOURGE OF “INTRODUCERS” SHOULD HAVE BEEN LEARNED FROM THE ARK SCAM IN 2011. WARD RECRUITED DOZENS OF THEM ALL OVER THE COUNTRY. AND YET NONE OF THEM HAS EVER BEEN BROUGHT TO JUSTICE FOR THEIR PART IN ARK, AND HAVE GONE ON TO OPERATE AS INTRODUCERS AND EVEN HOLD KEY CENTRAL ROLES IN LATER SCAMS. THIS INCLUDES FRIENDLY INVESTMENTS AND JULIAN HANSON – WHOSE SCHEMES ARE NOW ALSO IN THE HANDS OF DALRIADA TRUSTEES.

Gerard was responsible for producing template risk letters, member application forms, pro forma declarations stating that the person signing them was a self-certified sophisticated investor, member booklets and the statement of investment principles (of which there were four versions). Gerard sent these documents to members once they had been introduced to the Scheme by an introducer.

GERARD ASSOCIATES, RUN BY GARY BARLOW, HAD ACTED AS AN INTRODUCER TO WARD IN THE ARK SCAM. AND YET HE WAS LEFT FREE TO OPERATE IN THE SAME CAPACITY IN THE LONDON QUANTUM SCAM – AND EVEN TAKE ON A MORE CENTRAL ROLE. GERARD ASSOCIATES WAS AT THE TIME AN FCA-REGULATED FIRM – AND REMAINS SO TO THIS DAY. THE FCA HAS TAKEN NO ACTION TO REMOVE THIS FIRM OR TAKE ANY ACTION AGAINST GARY BARLOW.

GERARD ASSOCIATES’ GARY BARLOW WAS PAID £253,000 FROM THE LONDON QUANTUM SCHEME FOR DEFRAUDING VICTIMS INTO SIGNING AGREEMENTS THAT THEY WERE “SOPHISTICATED” INVESTORS. SO WHY HASN’T BARLOW BEEN PROSECUTED AND JAILED – AND MADE TO PAY THIS MONEY BACK TO THE VICTIMS?

A material number of the new members had a low or medium appetite for investment risk and, in any event, were unaware that the Scheme’s investments were high-risk investments. The Panel was troubled by the apparent disconnect between members’ appetite for risk and the high risk nature of the investments made by Dorrixo. Mr Ward accepted that the Scheme’s investments were high risk, but claimed this was made clear to new members in the Member Booklet.

I DON’T KNOW WHAT SORT OF DRUNKEN DUMMIES MADE UP TPR’S “PANEL”, BUT DID THEY SERIOUSLY THINK THAT ANY PENSION FUNDS SHOULD EVER INVEST IN HIGH-RISK CRAP? INDIVIDUAL MEMBERS’ APPETITE FOR INVESTMENT RISK IS IRRELEVANT – THIS WAS A PENSION FUND, NOT A CASINO.

The case against Ward was based on failures of competence and capability, and also a lack of honesty and integrity as well as Ward’s involvement with “pension liberation” as an introducer of members to the “Ark” schemes.

BUT TPR AND HMRC KNEW ALL ABOUT THIS BACK IN 2010 AND 2011. WHY DID THEY DO NOTHING TO PREVENT WARD FROM SCAMMING MORE VICTIMS OUT OF MORE MILLIONS OF POUNDS. THEY STOOD BACK AND WATCHED – DESPITE HAVING HARD EVIDENCE THAT HE WAS STILL UP TO HIS CRIMINAL MISCHIEF.

Mr Ward did not dispute that a company of his (Premier Pensions Solutions SL) was involved in introducing members to the Ark Schemes, but states that the relevant activity pre-dated any finding by the courts of pensions liberation and that Mr Ward had no knowledge that the schemes were being used for such activity.

BUT HMRC, TPR AND DALRIADA ALL KNOW THIS ISN’T TRUE. THEY HAVE ALL SEEN EVIDENCE THAT WARD AND HIS BENT LAWYER ALAN FOWLER ACTUALLY PRODUCED THE “LOAN” (MPVA) DOCUMENTATION AND EXPLAINED THE LOANS IN SOME CONSIDERABLE DETAIL TO THE VICTIMS. THE MPVA CONTRACTS WERE DRAWN UP BY FOWLER. IS IT REALLY CREDIBLE THAT NEITHER HMRC NOR TPR WOULD HAVE OBJECTED TO THIS STATEMENT?

The Panel did not consider there was sufficient evidence of Ward having actual knowledge of, or turning a blind eye to, the illegal nature of the activity of the Ark Schemes when carrying out his role as introducer before.

SERIOUSLY? I HAVE GIVEN EVIDENCE OF THIS TO BOTH HMRC AND TPR ON MANY OCCASIONS. THIS HAS BEEN DISCUSSED AT MEETINGS WITH DALRIADA TRUSTEES ON MANY OCCASIONS. EVIDENCE OF THIS HAS BEEN GIVEN TO THE SERIOUS FRAUD OFFICE ON MANY OCCASIONS BY VARIOUS VICTIMS AND ME. WHAT FURTHER EVIDENCE DID THE PANEL WANT? EVERY ARK MEMBER’S FILE WAS FULL OF SUCH EVIDENCE. EITHER TPR IS LYING OR IT IS INCOMPETENT. OR BOTH.

The Case Team also relied on certain alleged failures in relation to other pension schemes (called Headforte and Halkin), of which Mr Ward was a trustee. These are denied by him (e.g. an allegation of failure to appoint an auditor to those schemes) and the Panel did not consider it necessary to make findings in respect of them.

SO WHAT ACTION HAS TPR TAKEN IN RELATION TO HEADFORTE AND HALKIN? BOTH WERE BEING USED FOR PENSION LIBERATION FRAUD BY WARD – AND YET THE VICTIMS PROBABLY STILL HAVE NO IDEA WHAT HAS HAPPENED TO THEIR MONEY. IT IS ABSOLUTELY ASTONISHING THAT NO ACTION HAS BEEN TAKEN IN RELATION TO THESE TWO SCHEMES, PLUS ALL THE OTHERS WARD HAS BEEN OPERATING OVER THE YEARS.

Stephen Alexander Ward (date of birth 11 July 1955) is hereby prohibited from being a trustee of trust schemes in general. This order has the effect of removing the above-named individual from all or any schemes of which he is a trustee. By section 6 of the Pensions Act 1995, any person who purports to act as a trustee of a trust scheme whilst prohibited under section 3 is guilty of an offence and liable (a) on summary conviction to a fine not exceeding the statutory maximum, and (b) on conviction on indictment to a fine or imprisonment or both.

SO, WARD CAN STILL OPERATE AS A PENSIONS ADMINISTRATOR? CAN STILL DO PENSION TRANSFERS? HE IS BASICALLY FREE TO CARRY ON AS BEFORE. THIS MAKES HMRC AND TPR COMPLICIT IN WARD’S MANY CRIMES.

THIS IS NOT JUST THE DEATH OF TRUST, BUT OF ANY CONFIDENCE IN THE GOVERNMENT, REGULATORS AND CRIME PREVENTION AGENCIES TO PREVENT OR DEAL WITH PENSION SCAMS AND SCAMMERS.

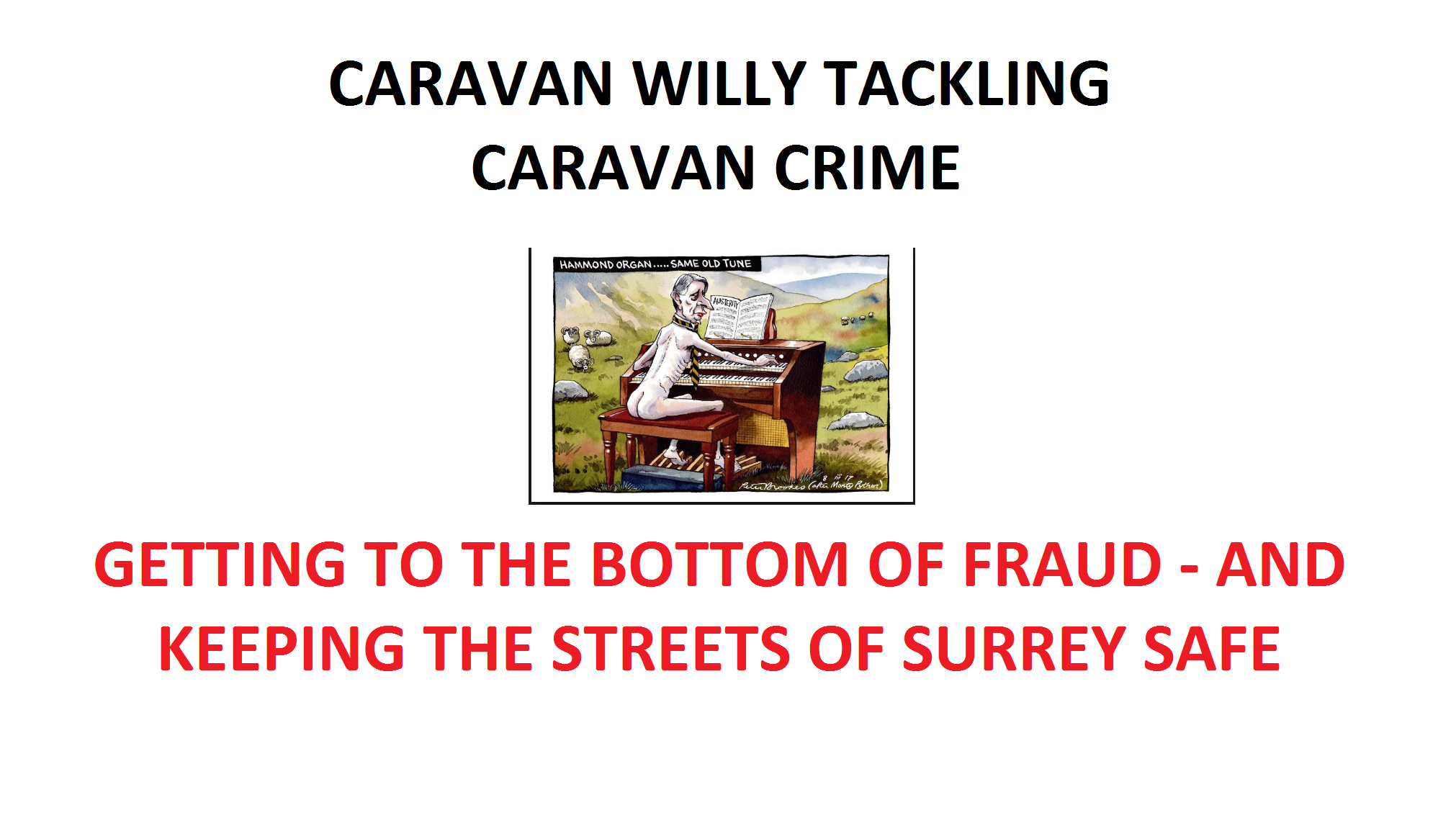

Tackling Caravan Crime – Chancellor Philip Hammond. Victims of pension fraud in scams such as Ark, Capita Oak, Westminster, London Quantum, Friendly Pensions and Salmon Enterprises – will not be surprised to hear that even the Crown Prosecution Service acknowledges that the fraudsters have defeated the system. Alison Saunders, head of the CPS, has stated publicly that the British justice system can’t cope. She is stepping down and is clearly disheartened by Britain’s failure to tackle crime – especially fraud. She has vented her frustration in an interview:

But look hard enough, and you will see how tackling crime can be done successfully. As someone who constantly writes about the failure of our police and courts to bring criminals to justice, I was surprised to hear of a spectacular success story in leafy Surrey recently.

Mr. and Mrs. Shore of Thorpe, in Surrey, were successfully prosecuted and jailed for proceeds of crime. Residing in Runnymede Borough Council – presided over by Chancellor Phillip Hammond – this dastardly pair (in their sixties) were both sent down for a heinous crime under the Proceeds of Crime Act 2002 (“POCA”).

After many years of detailed investigation, the successful prosecution will send out a resounding warning to all such criminals and will no doubt discourage others from profiting from the same hideous crimes. And the crime was…….?

Housing homeless families in caravans without planning consent.

Let that sink in for a moment – vulnerable people with young children who had a choice between living on the streets or living in a caravan. And this crime was committed in Runnymede Borough where there was insufficient housing for the many poor families who could not afford private accommodation and had not been offered council homes.

This spectacular success story on the part of Hammond, Runnymede Borough Council and the CPS has left the good citizens of Surrey relieved that these dangerous caravan owners are now behind bars and dozens of homeless families are now living on the streets. Jobdone; justice served; well done Cutty Sark!

Hailing from Surrey myself, I am pleased that the county will now be a safer place. The successful prosecution was in respect of 14 breaches of six enforcement notices issued since 1999 by Runnymede Borough Council, following a seven-day trial at Guildford Crown Court. The jury heard how the farm owners had not only stationed the caravans on their own land, but had also failed to demolish a shower room. Unbelievable!

Hammond must be strutting the halls of Westminster bursting with pride and patrolling the fields of Runnymede with a sense of upholding the social and civil justice with which King John would have been delighted. In the House of Commons bar, Chancellor Hammond is probably boasting that there is a reason why he is named after a large organ. In fact, after his spectacular success with the Shores’ caravans, he will probably go down in history as “Caravan Willy” for presiding over such a coup.

I am sure that the many thousands of people who have lost millions of pounds’ worth of life savings to scammers such as Stephen Ward, Julian Hanson, George Frost, XXXX XXXX, Phillip Nunn, Patrick McCreesh, Stuart Chapman-Clarke, David Vilka, David Austin, Darren Kirby, Dean Stogsdill, Anthony Downs and James Lau will now understand why the CPS couldn’t dedicate any resources to prosecuting them. And they will, no doubt, be glad that the priority of the judiciary was removing unauthorised caravans in Surrey.

As in most of my blogs, there is an important postscript: Caravan Willy is a keen property owner and is reported to be worth over £9 million. The Shores’ land has now been confiscated by Runnymede Borough Council. And it is worth at least £27 million once planning permission for a housing estate is granted. I wonder who will be lucky enough to scoop that one up?………

Pension scammers have a “code”. Rather like pirates, they are not to be trusted. They pick their words carefully, revealing little; they are sneaky and lack any morals. They are good at disguises and if they fear they may be rumbled, they will disappear over the horizon, never to be seen again. They certainly won’t hang around to help pick up the pieces after their victims have been ruined. Rest assured, they will take as much as they can get and show no remorse. Living the Life of Riley on your hard-earned money is their reward.

“Yo ho, yo, ho! A scammer’s life for me”.

Those of you who follow Pension Life, will know that we want to put a stop to pension scammers and are trying our hardest to get as much information as possible out to the public about how to avoid being scammed. We want to educate the masses and stop pension scammers worldwide.

Those of you who are new readers, may not be aware of how common pension and investment scams are, or how easily you could fall victim to a pension scam. But never fear, we have constructed a series of blogs, videos and cartoons for you to read and watch, so you can swot up on the dos and don’ts when it comes to safeguarding your precious pension fund.

This video has been constructed to show you the pension scammers’ code of conduct. By familiarising yourself with their techniques, you will be better prepared to spot the scammers and avoid falling victim to their schemes.

Please look through our archives and read about past scams, serial scammers and failures of the regulators and police to bring them to justice for their crimes. Make sure you know all there is to know about the evil and seemingly unstoppable world of pension scammers.

Above all, read the Trolley’s guide, and see how scammers learn their highly-profitable and destructive trade. Scammers learn from the best – including theauthor of this guide. And then they bring their own individual touch to the art of scamming.

John Rodges had a pension pot of £202,000. He was cold called by a salesman called Dean Stogsdill and persuaded to transfer his pension fund to a QROPS (Qualifying Recognised Overseas Pension Scheme) with Continental Wealth Management (CWM pension scam using high-risk, professional-investor-only structured notes which Stogsdill referred to as “Blue Chip Notes”).

With false promises of greater flexibility, better growth and a 25% tax-free cash lump sum, the transfer seemed like a good opportunity. In reality, it was an offer too good to be true – it was a pension scam- in which the CWM salesmen, Dean Stogsdill and Anthony Downs would reap high commissions. The victims – like John Rogers – would be left with heavy losses.

67 year old John Rodgers, a former research and development chemist, had a collection of occupational and private pensions in the UK. As he had moved to Spain 11 years previously, he had the opportunity of consolidating his pension into a QROPS.

Stogsdill – Chief Executive of CWM, assured John Rodgers that he had been evaluated as a low-medium risk investor, and that the costs would be 1.75% a year over a period of five years – or 1.5% for ten years. This would be based on the original value of the investment, so the promised growth of 8% would not incur any further costs. He was also promised that life assurance would be ‘thrown in’. Unfortunately, John was to become the next victim of the CWM pension scam.

What actually happened was John Rodger’s pension fund was invested into a selection of high-risk structured notes from Royal Bank of Canada – “Blue Chip Notes”. John was told that these “Blue Chip Notes”, were capital protected inside a life bond which would give him life assurance. No real explanation of what a structured note actually was, was given to John.

Structured notes are generally high-risk, FOR PROFESSIONAL INVESTORS ONLY. Therefore, these “Blue Chip Notes” had no place in a pension fund. This investment strategy was part of the CWM pension scam – earning salesmen like Stogsdill big bucks while destroying innocent victims’ pension funds.

Stogsdill also failed to disclose the commissions they were going to earn from the life assurance bond and the “Blue Chip Notes” so even before John’s funds were placed in the toxic high-risk investements – they had incurred a significant loss.

It took just two years for John’s fund to plummet to half of its original value. However, CWM assured him that it was just a “paper loss”, and that the fund would go back up at maturity.

Today John’s pension fund is worth just £60,000 (if he is lucky).

Pension Life has reconstructed John’s story and we would like to share it, in the hope that other people can spot the signs of a pension scam like CWM and avoid falling victim to the scammers – the only ones who profit from investments like these.

It is estimated that up to 1,000 people fell victim to the CWM pension scam and that around 40 million pounds was lost to these high-risk, toxic investments with providers such as

Royal Bank of Canada, Nomura Commerzbank and Leonteq.

The CWM pension scam was promoted by unqualified, unregulated salesmen posing as financial advisers. People who were not legally allowed to provide this kind of financial advice. The scam was promoted with outright lies and undisclosed fees and costs.

Stephen Ward of Premier Pension Solutions

A financial adviser that can be linked to not just the CWM pension scam, but also many others including Ark, is a man called STEPHEN WARD (pictured). He IS fully qualified AND registered with the CII. However, he does not have a conscience when it comes to destroying hard-earned pension funds – check out another of Pension Life’s videos:

If the name Stephen Ward appears on any pension transfer you are offered, make sure you say no and walk away – Pete and Val – another couple who were victims of the CWM pension scam – wish they had.

When considering transferring your pension fund, please make sure you check all the facts and fully understand all of the costs. Ensure your pension is going into a suitable retail investment – not a structured note.

Kim – a member of the Pension Life team is writing a series of blogs about pensions and we would love it if everyone would read and share these. Let’s stop pension scammers in their tracks worldwide by educating the masses on pension rules and regulations.

International Investment interview with Angie Brooks, founder of Pension Life this week. This blog is written by Kim, Angie´s Assistant. Here´s the interview video which explains how Pension Life works to help victims of pension and investment scams. The interview also raises the question as to why pension and investment scams are so prolific – despite Angie’s hard work to bring them into the public eye – and bring scammers to justice.

As Angie states in the video, Pension Life was originally founded to help victims of the ARK pension scam with their tax liabilities. However, four years on and Pension Life has evolved. Angie is now involved in helping 34 different groups of victims of pension and investment scams. Angie regularly goes to the regulators and ombudsmen in different jurisdictions and makes complaints on their behalf.

Pension Life is based in Spain, and Angie works with clients all over the world. Pension and investment scammers have no boundaries or borders and will weave their evil mischief wherever they can find British expats.

Angie offers her members a fixed membership fee, meaning “people know exactly what they are going to pay in advance”. Using privately-funded solicitors can be pricey and sometimes even non-starterer. Angie has, over the past four years, educated herself in pension and investment scams – how they work and how they are (constantly) evolving. Members can rest assured that they are being represented by a leading expert in the area of pension and investment scams.

If it were up to Angie, the people and firms responsible for pension and investment scams would all be sent to jail and the keys thrown away. With her weekly blogs and videos on the Pension Life website, and with the use of social media, Angie is hoping to get the word out there and warn both the public and the industry.

Angie stands up for the masses, where their single complaints are lost in a pile of excuses by the firms responsible for the destruction of their funds. She meets and speaks to as many victims as she can. Each victim has his or her own tragedy – often involving serious health issues and terrible financial hardship as a result of being scammed out of their life savings.

Some of Angie´s blogs are very hard hitting towards the firms and advisors who condone the use of pension and investment scams. The role Angie plays in uncovering the crooks of the industry is not without risk and often her outspoken words attract negative attention. Angie often receives threats of being sued by the lawyers who represent the companies she blogs about.

Angie states, “But If I was frightened I wouldn´t do it.”

Its not just solicitors who bombard her in outrage about the clearly-evidenced facts that Angie reports, she also has a herd of internet trolls who target her incessantly.

Angie says with reference to her blog trolls: