Another victim of Berkeley Burke SIPPS investments into Store First storage pods has come forward. 55-year-old factory worker Robert McCarthy, of Ebbw Vale, said he has lost more than £30,000 through a Self-Invested Personal Pension (SIPP). He was duped into the transfer and investment by unregulated firm Jackson Francis which was liquidated in 2014. His investment may or may not be worthless – depending on whether Store First is wound up later in 2019.

Robert McCarthy – who is one of 500 Store First investors who used Berkeley Burke as their SIPP provider – made a serious complaint against Berkeley Burke – and spoke to BBC News on the matter.

McCarthy said:

“Basically I’ve lost my private pension. Thirteen years of hard work, they’ve taken it, it’s gone.

I’ll never trust anyone again. And I can’t believe that they can get away with what they’ve done.”

The BBC has reported Store First as saying that: “In McCarthy’s case, Berkeley Burke failed to instruct Store First on how to manage the pods they purchased as part of a SIPPS. This means that the store pods have stood empty since their purchase. With returns based on rent paid for using the pods purchased, no returns have been made on these empty pods.”

This scam follows the same path as so many other scams we see: an unregulated advisory firm, Liverpool-based company Jackson Francis, introduced the victims to Berkely Burke and the Store First investment. (Jackson Francis was wound up in 2014). With promises of the investment being ‘the next best thing’ and also guaranteed high returns, 500 people signed their pensions over to the SIPPS provider Berkeley Burke.

Berkeley Burke then invested the SIPPS into the store pods, but failed to give permission for Store First to rent the pods out on behalf of the investors – meaning they stood empty. Store First said they were never contracted to manage, advertise or let the storage pods. That responsibility, they say, lies with the pension trustee, Berkeley Burke.

This is not the first time Berkeley Burke have been accused of negligence. In the High Court last October, Berkeley Burke was found to have failed to show due diligence in vetting unregulated investments for another client. The company are currently seeking to appeal against the decision. But with a further 14 individuals, based in Wales alone, making complaints against them, there is definitely no smoke without fire.

Whilst Capita Oak tuned out to be a scam (currently under investigation by the Serious Fraud Office) and victims have lost huge chunks of their pensions, the initial presentation they were given made the scheme look 100% genuine.

I spend a lot of time sharing our blogs over Facebook into different groups, trying to get the message across about pension scams. Interestingly, many of my posts are met with negative comments.

Last week in a comment on an expat forum, I was told that my blog about expats being targeted by scammers was “irrelevant”. I have also had comments like: “I would never fall for a scam.” However, there is clear evidence that falling for a scam doesn´t make you stupid or naive – especially when the scammers are so good at disguising their sham schemes as genuine investments.

Therefore, when it comes to the crunch, it is incredibly easy to fall for a pension scam – especially when it is registered by HMRC and promoted by a qualified financial adviser. It is hard to tell the difference between the good guys and the bad guys (who are so good at clever disguises). Pension scam victims include airline pilots, doctors and nurses, teachers, scientists, bankers and even a solicitor or two. Anyone can fall for a cleverly-sold scam – and they frequently do.

Toby Whittaker, owner of Store First, as you can see from his Twitter page, is still promoting Group First and Store First as going concerns. He is also fighting the winding-up petition by the Insolvency Service against Store First.

Despite the fact that the Capita Oak scam now lies in the hands of Dalriada Trustees (appointed by the Pensions Regulator) and the ongoing petition to have Store First wound up (purportedly in the “public interest”), Toby Whittaker still stands proud and says he had no idea that his company was being used as part of a scam.

No one knows where the money went, but it certainly didn´t go to the victims of this scam. We can bet it lined the pockets of the scamming salesmen who incorrectly invested over 1,000 victims’ pensions into Store First.

If the UK government succeeds in its petition to wind Store First up, the hundreds of victims will lose all the funds in their pensions.

The Spanish Insurance Regulator – the DGS (Dirección General de Seguros y Fondos de Pensiones) – has made a most welcome judgment. This outlaws the mis-selling of bogus life assurance policies as investment “platforms” – aka “life bonds”. Read the translated summary below.

The iniquitous practice of scamming victims into these expensive, pointless bonds – so beloved by the “chiringuitos” (scammers) on the Costa Blanca and Costa del Sol for many years – will now result in criminal convictions for the peddlers of these toxic products.

The DGS’ judgment has provided reinforcement to the earlier Spanish Supreme Court’s ruling that life assurance contracts used to hold “single-premium” investments are invalid. This heralds a huge step forward in cleaning up the filthy scams which have for so long proliferated in popular British expat communities – making the victims poor and the perpetrators rich. This evil practice came to a head when scammers Continental Wealth Management collapsed in a pile of debris in September 2017. The main perps: Darren Kirby, Dean Stogsdill, Anthony Downs, Richard Peasley, Alan Gorringe, Neil Hathaway, Antony Poole all ran for the hills. Other scammers who played supporting roles – including Stephen Ward, Martyn Ryan and Paul Clarke – slithered away quietly to ply their scams elsewhere.

The DGS ruling has opened the way for criminal prosecutions against all those at Continental Wealth Management who profited so handsomely from flogging “life bonds” by Old Mutual International (aka OMI and Royal Skandia), Generali and SEB. While it goes without saying there will be a hearty cheer about the jailing of Darren Kirby and his merry men, they will soon be joined by other individuals who have joined in the bogus life insurance fest just as enthusiastically. And, of course, the life offices – from OMI, Generali and SEB, to Friends Provident and RL360 – will be treated to a proceeds-of-crime party.

Guest of honour will, of course, be Peter Kenny of OMI. But just to make sure nobody feels left out, Hansard and Investors Trust will certainly get their invites. Maybe Wormwood Scrubs will set up their own wing for life-office scammers.

It has long seemed curious that such a delightful part of Spain as the Costa Blanca should have fostered such an evil industry. From the arch scammer himself – Stephen Ward of Premier Pension Solutions, and his many associates including Paul Clarke who was helping him flog Ark before he joined CWM to learn to scam on a much larger scale. But anywhere along that delightful stretch of coastline running from Valencia to Alicante there are dozens of firms giving the life bond machine plenty of welly.

So popular is the use of life bonds among the seedier sector of the financial services industry, that multi-national firm Blevins Franks have their own their “exclusive” offering of bogus Lombard bonds. And you can see why: these scammers earn 8% from flogging these bogus life assurance policies. That’s 8% for doing nothing – and for trapping their victims into paying back this commission over up to ten years. Often long after the victims have worked out that the bond serves no purpose except to prevent the funds from ever growing.

The victims themselves – hundreds of which lost most (or in some cases all) of their life savings to Continental Wealth Management – will indeed see the DGS’ ruling as wonderful news. They will certainly celebrate the fact that justice has at last prevailed and that the law in Spain has made it clear that selling life assurance policies the traditional scamming way is illegal.

Continental Wealth Management (CWM – “sister company” to Stephen Ward’s Premier Pension Solutions) was set up initially to provide the cold calling and lead generation services to support Ward’s many scams – including the Evergreen (New Zealand) QROPS scam. Evergreen was swiftly followed by the Capita Oak and Westminster scams (now under investigation by the Serious Fraud Office). Unregulated, and staffed by unqualified salesmen who took it in turns to sport grand titles such as “Managing Director” and “Investment Director”, most of these spivs had been car salesmen or estate agents before flogging QROPS and life assurance contracts used to hold the toxic structured notes which destroyed so many millions of pounds’ worth of the victims’ life savings. Many of these bonds were supplied by Old Mutual International, who despite the huge losses on the funds, continued to take their fees monthly.

Back in April 2018, OMI and the IOM were defeated by Spanish courts ruling that the jurisdiction in litigation against them for facilitating financial crime should be in Spain. This was a welcomed victory for the victims in the face of so much corruption and fraud in Spain for many years. It is certainly a turning point in the quest for justice by the thousands of victims of scammers such as Continental Wealth Management and life offices such as Old Mutual International, Generali and SEB.

I will be writing to all advisory firms who are selling life bonds to victims in Spain to advise them that this is now a criminal matter and to warn them that they will be reported to the DGS.

General Directorate of Insurance and Pension Funds (DGS)

Complaints service file number 268/2016

COMPLAINT BY A CONTINENTAL WEALTH CLIENT IN RESPECT OF HEAVY LOSSES INCURRED ON HIS PENSION TRANSFERRED TO A BOURSE QROPS AND PLACED IN A GENERALI INSURANCE BOND.

The Directorate General of Insurance and Pension Funds is competent under the powers conferred on it by Article 46 of Law 26/2006 of 17 July, on the mediation of private insurance and reinsurance, to examine the claim formulated for the purpose of determining non-compliance with current regulations on the mediation of private insurance and reinsurance, and whether this is decisive for the adoption of any of the relevant administrative control measures, particularly those of administrative sanction, which contravene the aforementioned Law.

Article 6 of Law 26/2006, of 17 July, on private insurance and reinsurance mediation, which regulates the general obligations of insurance intermediaries, states:

“Insurance intermediaries shall provide truthful and sufficient information in the promotion, supply and underwriting of insurance contracts, and, in general, in all their advisory activity….”

Article 26 paragraphs 2 and 3 of Law 26/2006, of 17 July, on private insurance and reinsurance mediation, which refers to insurance brokers, establishes the following:

“Insurance brokers must inform the person who tries to take out the insurance about the conditions of the contract which, in their opinion, it is appropriate to take out and offer the cover which, according to their professional criteria, is best adapted to the needs of the former. The broker must ensure the client’s requirements will be met effectively by the insurance policy.”

Article 42 of the Private Insurance and Reinsurance Mediation Act, which refers to the information to be provided by the insurance intermediary prior to the conclusion of an insurance contract, provides:

“Before an insurance contract is concluded, the insurance intermediary must, as a minimum, provide the customer with the following information:

a) The broker’s identity and address.

b) The Register in which the broker is registered, as well as the means of verifying such registration.”

Insurance agents must inform the customer of the names of the insurance companies with which they can carry out the mediation activity in the insurance product offered.

In order for the client to be able to exercise the right to information about the insurance entities for which they mediate, insurance agents must notify the client of the right to request such information.

Banking and insurance operators, in addition to the provisions of the previous letter, must inform their clients that the advice given is provided for the purpose of taking out an insurance policy and not any other product that the credit institution may market.

Insurance brokers must inform the client that they provide advice in accordance with the following obligations:

“Insurance brokers are obliged to carry out and provide (to the customer) an objective analysis on the basis of a comparison of a sufficient number of insurance contracts offered on the market for the risks to be covered. Brokers must do this so that they can formulate an objective recommendation.”

On the basis of information provided by the customer, insurance intermediaries shall specify the requirements and needs of the customer, as well as the reasons justifying any advice they may have given on a particular insurance. The intermediary must answer all questions raised by the client regarding the function and complexity of the proposed insurance contract.

All intermediaries operating in Spain must comply with the rules laid down for reasons of general interest and the applicable rules on the protection of the insured, in accordance with the provisions of Article 65 of the Law on the Mediation of Private Insurance and Reinsurance.

Every insurance intermediary is obliged, before the conclusion of the insurance contract, to provide full disclosure. In the event that a mediator was an Insurance Broker or independent mediator, he is also obliged to give advice in accordance with the obligation to carry out an objective analysis. This must be provided on the basis of the analysis of a sufficient number of insurance contracts offered on the market for the risks to be covered. The mediator can then formulate a recommendation, using professional criteria, in respect of the insurance contract that would be appropriate to the needs of the client.

In the case in question, there is no evidence that the aforementioned information was provided to the client before the investment product was contracted. Therefore, Article 42 of the regulations has been breached.

Therefore, this Claims Service concludes that the mediator must justify the information and prior advice given to his client, so that the obligations imposed by the Law of Mediation can be understood to be fulfilled with the aim of protecting the insured. Failure to comply with their obligations could be considered as one of the causes of the damage that would have occurred to their client.

The claim is understood to be founded. In the opinion of this Claims Service, the mediating entity has committed a breach of the regulations regulating the mediation activity – specifically of the provisions of articles 6 and 42 of Law 26/2006 of Mediation of Private Insurance and Reinsurance.

The DGS requires the mediating entity to account to this Service, within a period of one month from the notification of this report, for the decision adopted in view of it, for the purposes of exercising the powers of surveillance and control that are the responsibility of the Ministry of Economy and Enterprise.

The interested parties are informed that there is no appeal to this judgment. Both the claimant and the mediating entity are made aware of their right to resort to the Courts of Justice to resolve any differences that may arise between them regarding the interpretation and compliance with the regulations in force regarding the mediation of private insurance and reinsurance, in accordance with the provisions of articles 24 and 117 of the Constitution.

Chief Inspector of Unit

Ministry of Economy and Enterprise

Secretary of State for the Economy and Business Support

Another day, another voluntary ban taken by pension scammers, this time by those involved in the Henley Retirement Benefits and Capita Oak Pension Schemes. It seems there is still no justice for the victims of these financial crimes and there are no consequences for the directors of Transeuro Worldwide Holdings nor Imperial Trustee Services.

These scammers take a voluntary slap on the wrist and are still free to move on to their next venture.

“A ban from being involved in pension transfers is not a strong enough deterrent for other pension scammers. We need to see tougher penalties such as hefty monetary fines to make it clear that this behaviour will not be tolerated.”

We couldn´t agree more, as stated in a previous article, “The wheels of the law don´t seem to turn at all“, where we highlighted that a mere ban is pointless. Also, the time frame it took for this ban to be enforced is laughable.

Capita Oak was registered by HMRC on 23.7.2012 (PSTR 00785484RM) by Stephen Ward of Premier Pension Transfers of 31 Memorial Road, Worsley and Premier Pension Solutions of Moraira, Spain.

Capita Oak was wound up in the High Court in 2015.

2018 voluntary bans taken.

So, it took all this time for (some, NOT ALL) of the scammers involved in the Henley Retirement Benefits and Capita Oak Pension Schemes, to just get a ban. They have not been prosecuted and some of the main players are still at large. None of them have been ordered to pay back the funds they stole in larger than normal commissions – funds which were originally promised to the victims.

As always, there is a string of firms connected through this case, so bear with me whilst I outline the long list:

The directors connected with Transeuro Worldwide Holdings were the focus of this investigation

Transeuro helped fund three introducer firms: Sycamore Crown, Nunn McCreesh and Jackson Francis

Victims were transferred into SIPPS and pension schemes operated by Omni and Imperial Trustees

More than £100m was paid into SIPPS, more than £10m into Capita Oak Pension Scheme and more than £8m to Henley Retirement Benefit Scheme

The funds were then invested in assets which paid the scammers 46% in commission

Victims of Henley Retirement Benefit Scheme and Capita Oak Pension Scheme were cold called and given the hard sell, with promises of high returns. The usual spiel which – if you are considering a pension transfer – should not be believed.

Bans were given to:

Sycamore Crown director Stuart Greehan (also known as Stuart Chapman-Clarke) agreed to a nine-year voluntary ban

Karl Dunlop, director of Imperial Trustee Services, agreed to voluntary bans of nine years

Ian Dunsford, director of Omni Trustees agreed to a voluntary ban of seven years

Stephen Talbot accepted a nine-year disqualification undertaking for failing to explain what happened to millions pounds’ worth of assets

The words ¨accept¨ and ¨agreed¨ are used here, which gives the impression they all sat down to a nice lunch and “agreed” that they may have made a mistake and therefore “accepted” their bans! These people are financial criminals who left many lives ruined. The victims – many of which were already in financial hardship – now have no pension fund to look forward to.

The Serious Fraud office opened their investigations into the Capita Oak Pension and Henley Retirement Benefits Schemes, as well as Westminster and XXXX’s Trafalgar Multi-Asset Fund, back in May 2017. It is, however, anyone´s guess when this case might be pushed through the high court.

In the Pension Life office, we have been wondering how to get the information about pension scams more widely seen, heard and taken on board. We’d like to ensure the masses are educated and aware that pension scammers can strike from many angles, and with a variety of “deals”. Pension scammers must be stopped and together we can work towards this.

A quick Google search of the phrase “Pension Scam” shows no end of advice available, so why is this information not being spread to the public more widely and effectively?

Why was 2017 the WORST year for pension scams?

Google’s current top-ranking search return for the phrase “pension scam” is How to avoid a pension scam by Pension Wise. This site offers simple and basic information on how to spot a scam and how to report it.

This is followed by The Pensions Regulator (tPR) which, offers 5-step advice to protect a pension from pension scammers.

In third place, the Money Advice Service offers information on “How to spot a pension scam”. Money Advice highlight that scammers can be very good at disguising themselves as bona fide, regulated companies.

The FCA’s website comes in fourth, with their information on smart scams, advising people to be aware that the offer of a free pension review is often cause for concern and suspicion.

But, even with all this information out there, 2017 was still the worst year ever for pension scams. It seems that despite changes to regulations, scammers seem to come out on top nine times out of ten. Serial scammers are able to move onward and upward, scam after scam after scam. Officials, like the regulators, ombudsmen, arbiters and HMRC just stand idly by letting it happen again and again and again.

Maybe the problem is that the scammers are ever evolving in their behavior and tactics – and the authorities just can’t keep up. Pension Life came about because of the Ark pension liberation scam. But scamming tactics have moved on considerably.

We now we have noticeably less liberation and more investment scams where the introducer heads for the investment with the highest commissions, with no regard for the risk or fees that are applied to the fund.

Furthermore, if someone does approach you via a cold call claiming to be a viable company with a convincing sales pitch – how do you know if what they are saying is genuine? How do you know if they are a qualified financial adviser? Unfortunately, in the business of pensions and finance, the sad truth is that you need to: trust slowly; question quickly.

In the CWM case, victims saw unqualified, unregulated advisers placing low to medium risk investors’ entire funds into high-risk, fixed-term structured notes.

Fractional scamming is also on the up. Unqualified, unregulated firms posing as financial advisers act as “introducers” – and often introduce thousands of victims to outright scams. The funds then go through various other parties’ hands to ensure everyone gets their piece of the pie. Each party involved along the chain, creams their bit off the top of the pension fund, until the fund is a fraction of its former self. This means it will take years to get the pension back to its original state, let alone to start showing a profit.

Perhaps one of the most iniquitous aspects of pension and investment scams is the routine use of insurance bonds. (a significant part of the fractional scam and an unnecessary second “wrapper”). The life offices themselves are a big part of the pension scam industry.

Firms such as OMI, SEB, RL360 and Generali accept business repeatedly from unlicensed firms and known scammers. These so-called “life offices” (although they really ought to be called “death offices”) sit back and watch while these scammers gamble away the victims’ life savings on toxic structured notes and high-risk investments. Despite reporting on the inexorable destruction of the funds, firms like Generali et al just keep on taking their fees every quarter – and will sometimes do so until there is nothing left in the fund.

The best advice we can give, is to ensure you know exactly who you are dealing with and where your money will be going – every penny of it.

There is no such thing as “free”, and there will ALWAYS be commissions and fees on any pension transfer, legitimate or not. But however much it is – as in REALLY IS – the client needs to know and accept these costs. Many advisory firms conceal the real costs and the clients only find out what they are when it is too late, and the damage has been done.

Make sure you have everything in writing AND read it all – at least three times, if not more!

Make sure you understand everything: the costs, fixed terms, the risk level of investments – and if you don´t, then ask more questions.

Keep a regular eye on your fund; don´t trust any company 100%; make sure you know exactly what your fund is doing and do not ever be fobbed off with the explanation that any losses are “just paper losses”.

If in doubt – JUST SAY NO!!

I am writing a series of blogs about pensions, pension scammers and how to safeguard your pension fund from fraudsters. Please make sure you read as many as possible and ensure you know everything you should about your pension transfer. You only get one shot at getting it right – if you get it wrong, the damage may never be undone.

If we can ensure the masses are educated about pension scammers and financial fraud, we can help stop the scammers in their tracks – globally.

In many pension scam cases, we find victims telling us that they were not informed about the hidden charges that were applied to their fund. This is why it is essential to warn the public about the hidden dangers of charges that ruin your pension investments. These charges often take a huge chunk out of the fund before and during its new investments. Scammers lie about these charges, and victims never find out about them until it is too late.

The investments the scammers use are often high-risk and totally unsuitable for a pension fund. Pensions should be invested in diverse, low-to-medium risk assets which are prudent and liquid. And pensions don’t need an insurance wrapper at all, especially since the wrapper pays a whopping 8% commission to the scammers. And, sadly, much of the offshore advisory industry relies entirely on commissions – so the unethical advisers always chose the investments that pay the highest commissions. Unfortunately for the victims, the sweet-talking “advisers” are very good at concealing these hidden charges (commissions). They lure victims away from the small print and flash the promise of high – often “guaranteed” – returns.

Scammers – entirely reliant on commissions – are very good at blinding their victims from the risks they are inadvertently taking by putting their hard-earned cash into investments that pay the highest commissions. These scammers are pure salesmen, rather than proper financial advisers. Many of them are notQUALIFIED to give financial advice and they are only out for their “cut” of their victims’ hard-earned life savings. The hidden charges (commissions), paid unknowingly by the victims, buy the scammers their lavish lifestyle. Once the victims have signed on the dotted line, the scammers have no interest in what happens to the remainder of the funds after the commissions have been taken out.

So how does this illicit commission work? And how do the hidden charges damage a victim’s fund?

Let us assume a victim has a fund of £100,000. And he is transferring from a UK pension to an offshore QROPS.

First, a transfer specialist will charge a fee for the transfer advice. Then the offshore adviser will charge a setup fee. Then the QROPS provider will charge a setup fee. So, now we don’t have £100,000 any more – we probably only have £95,000 if we are lucky.

Then the scammer will put the victim into an insurance bond – such as OMI or RL360. The scammer will earn 8% on this (i.e. £8,000). But the victim won’t see this, because the insurance bond provider (OMI, RL360 etc) will claw this back over a ten-year period.

The scammers at OMI or RL360 will always keep a fat chunk of the fund in cash to pay their own fees – usually via hidden charges.

But let’s say they allow £80,000 of the remaining £95,000 to be invested, and let’s say the scammer at the advisory firm invests £40,000 in structured notes and £40,000 in “dirty” funds (i.e. the funds that pay the biggest commissions). This could be a further 10% in commission – so the victim will think he is getting £80,000 worth of investment, but in reality he is only getting £72,000 worth of investment. He simply can’t see the £8,000 in commissions because they are carefully hidden.

Eventually, the victim will realise that his fund is only shrinking, and that it will never have a chance to grow. Growth will be mathematically impossible, because of the constant, hidden fees/commissions. Some victims realise how they have been shafted quite quickly and are able to take positive action to move away from the rogue adviser. But for many, it is too late and too much damage has been done. Their funds will never have a chance to recover to anywhere near where they started. They would have been much better off sticking their retirement savings under the mattress. Because, of course, the “advisers” don’t care – they are long gone in their fancy sports cars and designer suits, sipping champagne at the local exclusive golf club.

In the UK we have regulations in place that prevent financial advisers from taking commissions. This works fine for the ethical, regulated sector of the financial advisory profession. But the unregulated offshore spivs who masquerade as “advisers” – and are, in reality, nothing more than silver-tonged salesmen – still do untold damage to the reputation of the industry by promoting unsuitable, high-risk, illiquid investments to low-risk pension savers (including those resident in the UK).

Many of the scammers are keen to get their UK-based victims’ pensions offshore to escape the protection of the British regulations. This, of course, prevents victims from having access to the FSCS and the ombudsmen.

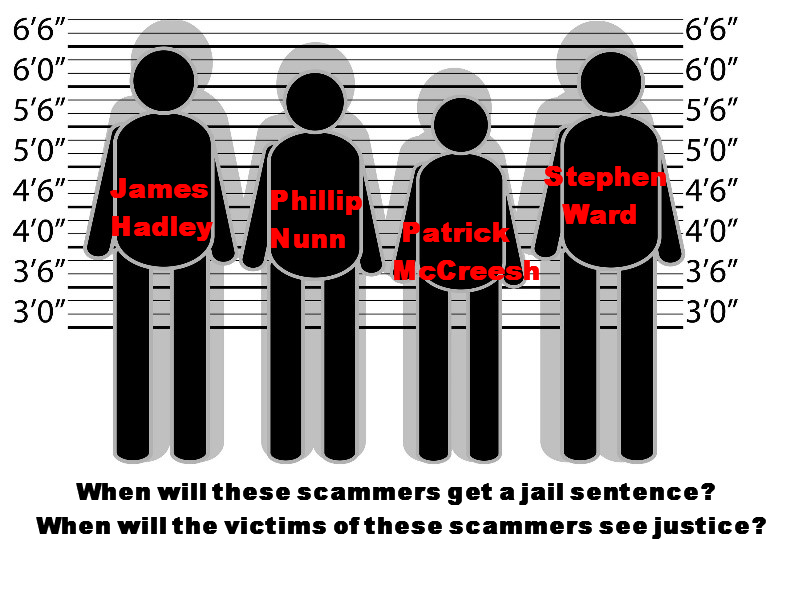

A prime example of this is the dastardly duo: Phillip Nunn and Patrick McCreesh. This pair of scammers received £ millions promoting the Capita Oak, Thurlstone Loans, Henley Retirement Benefits Scheme and Berkeley Burke SIPPS scams – leaving 1,200 victims worried sick about facing poverty in retirement.

The Nunn/McCreesh double act has gone on to promote their own toxic investment fund: the Blackmore Global Fund. This is a UCIS fund (Unregulated Collective Investment Scheme), which is illegal to promote to UK residents. Yet Phillip Nunn and Patrick McCreesh sold these investments with the help of David Vilka of Square Mile Financial Services. (David Vilka is NOT a qualified financial adviser and Square Mile is not regulated to provide investment advice). Nobody knows where the Blackmore Global victims’ funds have gone – as Nunn and McCreesh will not have the fund audited (the last thing they want is anyone knowing what they have invested their victims’ life savings in). But one thing we can guarantee is that the scammers Nunn, McCreesh and Vilka made a pocket full of cash through hidden charges.

In all leading expat jurisdictions – most notably Spain and Dubai – the scammers are beavering away grinding the commission machines. They take their hidden charges with no remorse.

In the time it took the gentle reader to read this blog, at least one victim will have lost their life savings. And one scammer will have earned 8% commission out of selling a useless, pointless, expensive insurance bond – such as OMI, Generali or RL360 – and up to 10% (or even more) on the underlying investments. On top of this, the scammer – masquerading as an “adviser” – will also charge a 1% “advisory” fee. And probably a setup fee. And then there are the QROPS charges.

Henry Tapper wrote an excellent blog on this very subject – he called it FRACTIONAL SCAMMING. I do hope that all offshore advisory firms will read this carefully. The excuse that they didn’t really understand the impact of hidden charges and commissions – and were only copying what they thought the industry was already doing successfully – is simply not going to wash any more. The damage caused by this toxic practice has been widely published and exposed.

The only way forward is to go fee-based. And to outlaw commissions and hidden charges altogether. The scammers won’t do it – but decent, ethical firms will. The hard part will be to warn expats against vultures. Ethical firms will help with this initiative. Obviously, the scammers won’t.

Intro written by Kim: ‘This week Angie travelled for work (yet again): she had to fly from Granada to Barcelona. Disaster struck – her baggage sadly did not make the full journey -it’s sitting in the triangle of lost luggage no doubt. The airline – Vueling – whilst only providing the flight, was still happy to take responsibility for the loss of her bag and its contents, and compensate her. That got her thinking: if an airline can take full responsibility for a loss, why are life offices like OMI turning a blind eye to the massive losses they have caused to thousands of pension scam victims’ funds?

Over to Angie:

The financial services industry (especially offshore) has a lot to learn from the airline industry. Aviation stakeholders internationally provide the highest possible levels of safety for air travellers. This due diligence is constantly reviewed, updated and improved. The same standard of responsibility routinely happens in all jurisdictions. Regulators, as well as air crash investigators, work together when things go right. As well as when they don’t.

The work of the air industry regulators, investigators and safety trainers never ceases with all parties constantly striving to maintain the highest possible standards of performance and safety. And when something goes wrong, everybody swings into action like the A-team, International Rescue and Tom Cruise combined.

I know all this because one of my members is a Captain with a well-known airline (probably quite easy to guess which one!). He also trains pilots from a variety of other airlines in simulators – and this includes Vueling pilots. I will call him Captain BJ.

BJ is a thoroughly decent bloke and has a rather endearing fondness for chickens. He has devoted his professional life to the business of safety in travel. And behind him is a comprehensive and robust system of regulation – internationally. Financial services regulators, on the other hand, stand by and watch (with their hands firmly in their pockets – and their fingers compulsively searching for something with which to fiddle) as the equivalent of hundreds of passenger planes crash every month. The regulators stare blankly at the charred remains of the passengers’ life savings and shrug carelessly at the huge scale of human misery caused so routinely. With such flaccid regulatory regimes in so many jurisdictions, these chocolate-teapot regulators de facto facilitate and encourage losses caused by negligence and scams.

I know all this because Captain BJ is also a pension scam victim – courtesy of Stephen Ward’s Ark £27 million pension scam. Despite the extreme stress of losing his pension, he has to keep a stiff upper lip and continue with his daily routine of flying thousands of passengers safely around the skies of Europe.

My recent experience on a Vueling flight provides an interesting parallel with the “financial services” provided by Old Mutual International. Vueling sells flights. They provide the aircraft; the pilots and the cabin crew. They offer a selection of routes, food and drink, duty free goods, toilets and the expertise to get many thousands of passengers from one destination to another safely and on time; day after day after day.

What Vueling doesn’t do is operate a baggage handling service – this is provided by the airport you travel through. However, no matter how enjoyable a flight has been (if such a thing is possible!) and how punctual the take-off and landing are, the whole experience can be badly marred by the loss of a passenger’s luggage. While Vueling is responsible for the safety of the passengers, it is NOT responsible for the safety of the passengers’ luggage when it is not in the bowels of the aircraft. However, Vueling goes to extraordinary lengths to help people whose luggage has been delayed or lost. Vueling take full responsibility for a loss of luggage, luckily for me.

Earlier this week, it was the baggage handlers at either Granada airport or Barcelona airport who were responsible for my medium-sized, black, tatty suitcase. And they lost it. The case had been full of clothing typically worn by a slightly fat, grey-haired woman on the wrong side of something ending in a nought. So no desirable or valuable designer totty wear, expensive perfume or sparkly jewellery.

But Vueling provide people like me (who end up wearing the same orange jumper and purple socks two days in a row) with an easy to use, online complaints and redress facility. It wasn’t Vueling’s fault that my luggage got lost, but they take responsibility for it anyway because it is part of the whole flight “package”.

Contrast this with Old Mutual International (OMI) and the IoM regulator. And thank your lucky stars that they don’t try to run an airline (because if they did, it is unlikely any passengers or luggage would ever survive). OMI provides “insurance bonds” or bogus life assurance policies. These products serve no purpose except to pay fat commissions to rogue IFAs. And they feature a selection of risky investment products for the IFAs to earn even more commission. What OMI does not provide is financial advice – that is the job of someone else (i.e. the IFAs). But when the IFAs do the equivalent of losing the baggage, OMI takes no interest or responsibility other than to record the loss.

In the air industry, there are two things that can go wrong that can cause customers financial damage: flight delays and loss of luggage. A comprehensive complaints and redress system is routinely provided by all leading airlines. In the financial services industry, there are two things that can go wrong that can cause customers financial damage: investment failures and disproportionately high charges. No complaints and redress system is provided by life offices such as OMI and no one takes full responsibility for a loss.

If an airline experiences a crash, a huge machine swings into action to investigate the cause and take immediate remedial action to prevent the same or similar event from ever causing another accident. If a life office such as OMI experiences a crash, it pretends nothing has happened. Pension scam victims? No pension scam victims here! OMI denies all responsibility. And blames the IFA. Or the weather. Or Brexit. And keeps charging the victims the same disproportionately high fees based on the huge commissions they originally paid to the IFA that caused the crash.

Here are some examples of OMI’s crashes in the past six years:

* Axiom Litigation Fund – this was a PROFESSIONAL-INVESTOR-ONLY fund which was routinely used by rogue IFAs for ordinary, retail investors (and from which the IFAs earned fat commissions). OMI offered the Axiom fund on the bogus “life assurance” platform. And when the fund went into administration in December 2012, OMI shrugged its shoulders and said “not our problem“. And kept charging the victims the same fees as if the £120 million loss hadn’t happened.

OMI knew that many of the IFAs had been neither regulated nor qualified and that the investors were unsophisticated, low-risk, retail customers.

* LM Australian Property Fund – this was a PROFESSIONAL-INVESTOR-ONLY fund which was routinely used by rogue IFAs for ordinary, retail investors (and from which the IFAs earned fat commissions). OMI offered the LM fund on the bogus “life assurance” platform. And when the fund went into administration in March 2013, OMI shrugged its shoulders and said “not our problem“. And kept charging the victims the same fees as if the £240 million loss hadn’t happened.

* Premier New Earth Recycling Fund – this was a PROFESSIONAL-INVESTOR-ONLY fund which was routinely used by rogue IFAs for ordinary, retail investors (and from which the IFAs earned fat commissions). OMI offered the PNER fund on the bogus “life assurance” platform. And when the fund went into administration in June 2016, OMI shrugged its shoulders and said “not our problem“. And kept charging the victims the same fees as if the £800 million loss hadn’t happened.

OMI knew that many of the IFAs had been neither regulated nor qualified and that the investors were unsophisticated, low-risk, retail customers. That is £1.16 billion worth of fund losses in just over six years, but they take no responsibility for loss of funds and the pension scam victim gets no redress.

(Note – if you read the above three examples, you will see that although the funds, dates and amounts were different, the circumstances were EXACTLY the same!)

Add to this the £ billions lost through toxic, risky structured notes, and that adds up to quite a cricket score that OMI “wasn’t responsible for“.

The causes were all the same:

UNREGULATED ADVISORY FIRMS

UNQUALIFIED ADVISERS

FUNDS OFFERING HUGE COMMISSIONS

FUNDS SUITABLE FOR HIGH-RISK, PROFESSIONAL INVESTORS SOLD TO LOW-RISK, RETAIL INVESTORS

NO DUE DILIGENCE BY OMI

We know that OMI bought:

£200 million worth of failed Leonteq structured notes

between 2012 and 2016 as OMI is claiming to be suing Leonteq. But this does little to distract attention from OMI’s multiple, long-term failures for allowing such toxic investments in the first place and causing many people to become pension scam victims.

If I give my car keys to someone who is so drunk they can barely stand up – and certainly can’t spell either OMI or IOM – and there is a serious accident, whose fault is it? The drunk’s or mine?

OMI’s CEO is a bloke called Peter Kenny who used to work for the IoM regulator. So he should know better. But he doesn’t. So we must assume he would be happy to hand his car keys over to a drunk or let an unqualified pilot fly a plane with a broken wing. And he would still claim it wasn’t his fault, despite the number of pension scam victims.

The moral of this blog is: never wear orange and purple on a flight; never use an OMI life bond; always use a qualified, regulated and insured IFA. Don’t become the next pension scam victim.

My next dilemma is what to buy with my Vueling compensation. I feel a trip to Marks and Sparks coming on. (I needed a bigger size anyway!).

(Huge thanks to Captain BJ – to whom I owe my sanity).

PS – since we wrote and published this blog, my luggage has been found. Apparently, it never left Granada airport. I suspect somebody pinched it – then found the clothes inside were so dull that they didn’t think it was worth taking it after all.

BREXIT is the question on everybody’s lips at the moment. BREXIT: will we? won´t we? deal? no deal? So many unanswered questions and so much scaremongering. We would like to offer some helpful words and hopefully protect you from making rash decisions. This could help you to safeguard your pension. Many scammers are trying to cash in on Brexit – make sure sure you’re not their next victim.

Remember I am not a financial adviser. I am a blogger, and I write about financial crime. I provide information about past scams and on how to avoid falling victim to new scams – especially pension scams. The words I write are aimed to help you safeguard your pension from the many offshore scammers.

So, Expats, what does Brexit mean for your pension rights? The short answer is that we really do not know! There are currently lots of “coulds” and “mights” being thrown around, but no certainties. And herein lies the risk that you and your pension could fall victim to a scam with all this scaremongering.

Firstly, despite Spectrum IFA advertising themselves as “international financial advisers”, with some digging we were able to find out that they DO NOT in fact have an investment licence. This means they are not legally allowed to advise on pensions or investments. Secondly, they scored rather poorly on the qualified and registered percentage too. Out of the 16 advisers we checked up on, only four were registered with the appropriate institutes. The rest came up red – meaning the institute had no record of them.

Worrying isn´t it? Offshore companies can try to claim they are international financial advisers, but actually be unregulated and unqualified to carry out the very service they offer! The “advisory” firms have flash websites, and some have several offices around Europe and beyond. Their PR is great at scaremongering expats about their pension investments in the lead up to Brexit.

In Spectrum’s ´Deal or no deal´ article number 14, they suggest you marry a Spaniard in order to prepare for Brexit. I´m not sure about you, but I feel that getting hitched to a native to be able to stay in Spain is a pretty drastic measure and definitely more than a little illegal.

Spectrum IFA is just one example of a firm that probably ought to be given a wide berth when transferring your precious pension fund offshore. Safeguard your pension by avoiding unregulated and unqualified firms like this one.

********

It may seem daunting when you read that your UK pension could be subjected to extra taxes if we leave the EU on a no-deal basis. You may be thinking that you should transfer into a QROPS quickly, to save on these taxes. But what you really need to know is that a QROPS is not without punitive costs of its own. They can be expensive and unless you have a good lump sum to transfer you could see a huge chunk of your pension pot taken in transfer and set-up fees anyway! Potentially making you worse off.

Unfortunately, until we make a deal or actually go through with Brexit, nothing is very clear for expats. Which leaves us in an uncertain time and situation. This, I understand, may be daunting for many people, but I urge you to take a deep breath before considering any speedy offshore pension transfers. Thousands of people – especially those who have already fallen victim to scammers such as Continental Wealth Management – would give you exactly the same urgent advice.

If you do want to transfer your pension, please heed this advice to safeguard your pension:

We did a series of blogs last year on offshore companies and their advisers. The results were extremely worrying. Aside from their blatant disregard for the necessity of these qualifications – due to being offshore – the number of unqualified advisers offshore was cause for serious concern. Many of the firms had not one single qualified and registered adviser on their team.

A reputable firm will have a fact-find procedure, and adhere to a client’s risk profile.

A reputable firm will have compliance procedure.

A reputable firm will have clear and consistent explanations and justifications for the use of insurance bonds.

Where will your funds be invested, and how will you know if this is in line with your risk profile?

A pension fund should be placed into a low-medium risk investment.

Scammers tend to go for high-risk, professional-investor-only investments as they offer them the best commissions. But a pension fund should have more protection than this. Avoid investments that involve structured notes (like CWM´s Blue Chip notes), UCIS funds (like Blackmore Global), in-house funds, non-standard assets and any ongoing commission-paying investments.

Insurance bonds – often used by scammers – are usually an unnecessary double wrapper on your fund, that costs you more in fees and charges than a straightforward platform, lining the pockets of the scammers – but making your fund smaller.

How much will the fees and charges be? Remember NO pension transfer is free.

Legitimate firms will normally have a small transfer charge and a small annual fee.

Scammers will often be vague about fees and charges, and avoid giving you a straight answer so they can cover up the true figures. These hidden figures can see your pension fund decrease by 25% or even more in some cases.

A reputable firm should offer you regular updates on the progress of your fund.

You should receive an annual review and a quarterly update showing the fees, charges and growth of your fund.

If your new firm and adviser fail to do this, alarm bells should ring loudly.

Finally, a reputable company will publish evidence to show records of complaints made, rejected or upheld and redress paid.

If the adviser cannot show you all this information, do not trust them.

If it all sounds to good to be true, it probably is – RUN!

SCAMMER JAILED! Hip hip hooray! we say. What a great start to the new year. Neil Bartlett, 53, of Delamere Road, Ainsdale, used £4.5m of his victims’ money to fund an extravagant lifestyle of foreign travel, top hotels and gambling.

As is the case with many scams, the victims are unlikely to recoup any of the funds they entrusted to him. Bartlett is said to have spent the hard-earned funds on prostitutes, escorts and expensive holidays. The victims, all of whom knew him on a personal level, are disgusted at his behaviour and were glad to see this scammer jailed.

Here in the Pension Life office, we are always pleased to hear that a scammer has been jailed. The only shame, is that we just don´t hear the words enough. It would be great if we could write blogs that contain the words SCAMMER JAILED on a daily basis. But sadly it is just not the case.

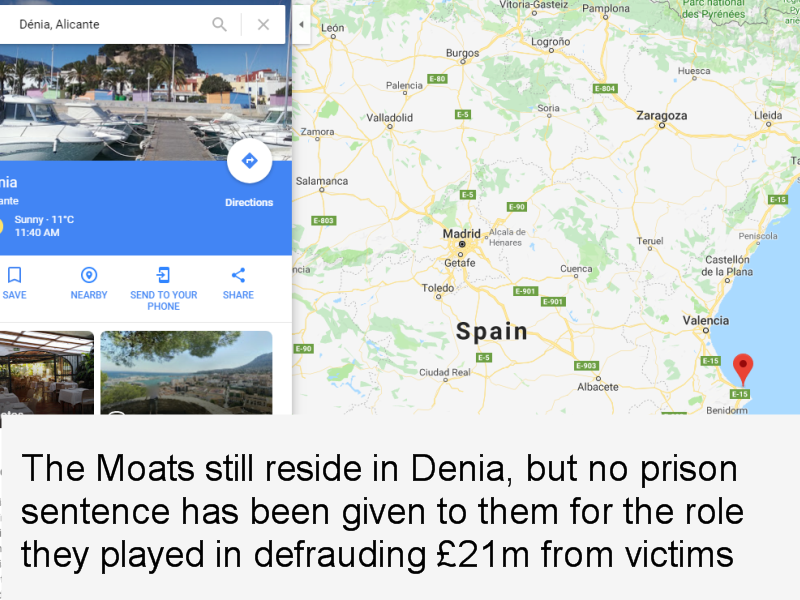

An example of this is Peter and Sara Moat of Fast Pensions – which was wound up back in May 2018. We know they fraudulently took £21m from their victims. We know they did not invest it in the interest of their victims. We know they invested the funds into other businesses they own. We know that they reside in Denia, where their daughter goes to a private school. We know all this – AND the SFO knows all this – yet the Moats are still free to live a lavish lifestyle whilst their victims go without a pension and some face losing their homes as well as bankruptcy.

I´m sure the victims of the Fast Pensions and Blu loans scams would find some solace in reading the words – “scammer jailed” in relation to both Peter Moat and Sara Moat. But I´m not sure if they ever will – and that makes us sad and bloody angry.

Thousands of victims and hundreds of thousands of pounds’ worth of pension money has been fraudulently taken from the victims of scam schemes sold by the above-named scammers. Schemes like Capita Oak, Blackmore Global Fund and the Trafalgar Multi Asset Fund.

All we can do is make a very loud suggestion that STM Group Gibraltar – STM Fidecs – Alan Kentish – should all be given a VERY wide berth when considering a change of pension trustee – as from past evidence they are not to be trusted!

If you have read our other blog you will already know that we have been waiting several years for a cold calling ban to be put in place. It is more than irritating to see that instead of a blanket ban on all cold calling they have imposed a fine on certain cold calls.

This also begs the question of how they had time to pass the legislation for the fine, but not the legislation to simply just ban all cold calling – FULL STOP – no ifs no buts. I also wonder how they are going to track down the cold callers and enforce the fines onto them. Will it be the people making the cold calls that get the fines? or will it be the companies setting up the call centres, or god forbid will it be the masterminds and serial scammers who continue to set up toxic, high-risk funds to lure in their victims?

The victims of the Continental Wealth management scam were cold called, see their story here.

An article written by the Telegraph confirms my fears about the lack of ability the regulators have in enforcing the fines they have already issued. The ICO has been fining companies for nuisance calls since 2015, it is estimated that nearly half of all land line calls are cold calls made to the elderly!

´The ICO has issued more than £5.7m in fines to cold call companies for breaching nuisance rules since 2015, but of the 27 fines issued only nine have been paid in full, recently published government figures revealed.´

The sad truth from these figures clearly shows that despite fines being made they are not being imposed, the companies are simply not paying them. If companies are happy to ignore the fines then they are probably happy to ignore the threat of a fine and continue to make cold calls. Figures from Ofgem have shown that consumers were bombarded with 3.9 billion nuisance phone calls and texts last year but only 27 fines were issued and just nine of those actually paid in full!

There are also so many loopholes these companies – who operate the call centers – can leap through. People must opt out of being cold called, if they have not done this, then companies can claim they were happy to receive the calls.

For instance, if you are online – say on a compare website – and you do not tick the box to state you do not want to be contacted by third parties, you are giving your permission to be contacted. This then means that your data is sold on and the company that calls you about the pension scheme transfer can claim that you were happy to be contacted. It wasn´t a cold call as they had opted in.

The loophole enables them to potentially escape any fine, as technically the receiver of the call had agreed to being contacted via a third party. The company making the calls can claim that they were not making a “cold call”. It feels like this legislation has been made after the horse has bolted from the stable. Hundreds of people have been scammed through the use of cold calling and hundreds more will continue to be scammed with the use of cold calling techniques, through loopholes.

Pension scams involving cold calls such as Capita Oak, Continental Wealth Management, Trafalgar Multi Asset Fund have left hundreds of victims with out a decimated pension fund. These unregulated, shameless firms and their snake salesmen are not going to acknowledge the treat of a fine, nor the administer of a fine. AND if they are fined do the government really think they will pay it?

Serial scammers like Stephen Ward who started out on the ARK pension scam, went on to scam again AND again, despite the scams being shut down by HMRC and the tPR again and again! None of the scammers who promoted these scam have been put behind bars and no money has been paid back to the victims. The scammers show no remorse for their actions. These blatant financial criminals aren´t going to pay a fine for cold calling if they aren´t going to admit the pension scheme´s they set up were fraudulent.

A quick google search of cold call gives untold amounts of advice on how to do it efficiently in 2019! Whilst some of these companies aren´t UK based, the evidence is clear. Cold calling pays and the companies that benefit from cold calling are not going to suddenly stop making them.

The regulators are really going to have to step up and do some serious regulating and enforcing if these fines are to be issued, actually followed up and collected.

The sad truth is that whilst the fines sound great on paper, they will do little to protect the public from being scammed.

As 2018 draws to a close, a recap is in order to review the year’s progress in the war against pension scammers. Let us not forget – in the immortal words of the Pensions Regulator’s Lesley Titcombe: “scammers are criminals“. However, the sad truth is that most of them have not been prosecuted or jailed.

The vast majority of the well-known pension scammers are still roaming free, busy thinking up yet more life-destroying schemes to make them rich and the victims poor. Whilst the scammers enjoy champagne this New Year’s Eve, many victims will be worrying themselves sick about their bleak financial future.

The Pensions Regulator, the Serious Fraud Office, the Insolvency Service, crime enforcement agencies and courts all seem to drag their feet when it comes to actually bringing charges against these criminals. Yet we see people being locked up for renting out caravans to help vulnerable homeless families! I would love it if this was a short and sweet blog, with many happy endings. But, alas, the scams are plentiful and the victims are left uncompensated for their losses.

Let’s have a quick round up of where we are with the scams and scammers. And remember: all the thousands of victims want to see the scammers sent to jail and the keys thrown away so they can’t ruin any more innocent people’s lives.

5G Futures

5G Futures: in May 2013 Garry John Williams and Susan Lynn Huxley were suspended as trustees of the 5G Futures pension scheme, and from trust schemes in general. Pi Consulting was appointed as the new trustee by the Pensions Regulator.

About 400 people had invested a total of £20m into the 5G Futures scheme – which was invested in high-risk, illiquid off-shore investments, with insufficient diversification making them completely unsuitable for pension scheme investments. There was no due diligence exercised by Williams and Huxley – and the scheme records were a mess.

The scheme operated pension liberation through ‘loans’ to members. Williams and Huxley were found to have taken very high commissions on the investments – taking nearly £900,00 in one year alone.

One of the most worrying things, however, is that the pension scammers don’t just leave the pensions industry and dedicate themselves to helping their many distressed victims – they start up all over again:

Stephen Ward: (this will not be the last time you hear this name in this blog) was the mastermind behind this scam (dating back to 2010). It was his first known scam – but by no means his last one. What is left of the Ark fund, stands still frozen, in the hands of Dalriada Trustees, who continue to take their yearly costs and fees from what little is left. Dalriada has done nothing to ensure the scammers are prosecuted – saying it is “not within their remit”. The victims of the Ark scam also have the heavy hand of HMRC hanging over them. And let us not forget that it was HMRC who happily registered this scam and failed to withdraw the registration when they discovered that Stephen Ward was operating pension liberation fraud.

Dalriada has never reported Stephen Ward to the police as it is not “within their remit” to ensure the scammers are prosecuted.

In 2018 we saw Stephen Ward being banned from acting as a pension trustee. Eight years after his first scam, he has still not been imprisoned for the millions of pounds’ worth of life savings he has destroyed and the thousands of lives he has ruined.

Other prominent figures in the Ark scam were Julian Hanson – who went on to play a key role in the Friendly Pensions scam; George Frost who went on to operate a new pension liberation scam using truffle trees as investments; Andrew Isles who went on to sell his accountancy business, Isles and Storer to LB Group; Peter Moat of Blu Debt Management who went on to operate the Fast Pensions scam. None of these scammers has ever been convicted or jailed.

Axiom

Another pension liberation scam, which saw victims with HMRC tax demands of 55%. Rex Ashcroft of Wealth Protection International was one of the main introducers of this scam. According to his Linkedin profile, he offers business development strategy planning for the UK, Spain, Portugal and France. He also offers “day-to-day application of wealth protection strategies”. Ashcroft lied to Axiom victims telling them they could access part of their pensions and not pay tax on the cash they took out.

David Vilka, Phillip Nunn and Patrick McCreesh have never been convicted or jailed. Blackmore Global Group is still being promoted by Phillip Nunn! Nunn and McCreesh had been the main lead generators in the Capita Oak scam – earning nearly £1 million in the process.

This was another of Stephen Ward´s scams – on which he worked closely with his pensions lawyer Alan Fowler (ex Stevens and Bolton Solicitors) and his sidekick Bill Perkins. Ward carried out the transfer administration for this scam which was mainly operated by XXXX XXXX who offered victims 5% Thurlston “loans”. Over 300 victims are facing the partial or total loss of their pensions and are also now being pursued by HMRC for tax liabilities on the “loans”.

Capita Oak – like Ark – was placed in the hands of Dalriada Trustees. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward, Alan Fowler, Bill Perkins and XXXX XXXX have never been convicted or jailed (although XXXX XXXX is under investigation by the Serious Fraud Office).

Stephen Ward’s firm Premier Pension Solutions (in Moraira, Spain) was the “sister” firm of Continental Wealth Management, run by scammer Darren Kirby. This was one of the biggest single scams – known as CWM – with around 1,000 victims losing part or all of their life savings. Other scammers involved were Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway.

This scam was promoted by cold-calling victims and promising unrealistically high returns and “capital protection”. Darren Kirby and Anthony Downs used the victims’ funds to invest in totally unsuitable, high-risk, fixed-term structured notes. This scam saw huge commissions paid by the life offices – Old Mutual International, SEB, and Generali – as well as by the structured note providers: Leonteq, Commerzbank, Royal Bank of Canada, and BNP Paribas to this unregulated firm. Let us not forget that this was without question financial crime and was facilitated by the life offices.

Old Mutual International, run by ex IoM regulator Peter Kenny, was the leading life office which facilitated the CWM scam. Generali and SEB also routinely accepted business from these known scammers and unlicensed advisers.

Stephen Ward, Darren Kirby, Anthony Downs, Dean Stogsdill, Alan Gorringe, Richard Peasley, and Neil Hathaway have never been convicted or jailed.

James Hay and Suffolk Life were accepting Elysian shares for liberation purposes

Another Stephen Ward creation which was operating 80% liberation with the full cooperation of the SIPPS providers James Hay and Suffolk Life. The SIPPS providers and the victims could face tax charges of up to £20 million from HMRC.

Despite clear evidence that Stephen Ward pushed this scam in emails to Alan Fowler and Bill Perkins, neither Ward nor Fowler nor Perkins have ever been prosecuted or jailed.

A New Zealand QROPS scam with Marazion pension loans

When Ark got shut down, Stephen Ward went straight to New Zealand to set up his next pension liberation scam with Simon Swallow of Charter Square. A further 300 victims were scammed out of over £10 million and conned into Marazion “loans” AND locked into the Evergreen scheme for five years. After the five years victims were told: ´Despite our best efforts, Evergreen has not been as successful as we had originally hoped.´ Evergreen was wound up April 208.

This scam was promoted by Darren Kirby’s Continental Wealth Management which cold called the victims.

Stephen Ward, Darren Kirby, and Simon Swallow have never been convicted or jailed.

It was determined that there is no doubt this was a scam.

Peter and Sara Moat and their accomplices have never been convicted or jailed.

Friendly Pensions Limited (FPL)

Back in January of 2018, the Pensions Regulator asked the High Court to act on their behalf in the Friendly Pensions matter. Scammers: David Austin, Susan Dalton, Alan Barratt and Julian Hanson (also involved in ARK) were ordered to pay back £13.7 million they took from their victims and banned from being pension trustees. However, Dalriada the independent trustee appointed by TPR to take over the running of the schemes, is in charge of confiscating the scammers’ assets for the benefit of their victims. (Who knows how long this could take: how long is a piece of string?) As yet, no compensation has been offered to the victims.

David Austin, Susan Dalton, Alan Barratt and Julian Hanson and their accomplices have never been convicted or jailed. However, there have recently been some arrests – so let us hope this results in maximum sentences.

Two bogus “occupational pension schemes” set up for pension liberation fraud by Stephen Ward after the Evergreen QROPS scam hit the rocks (when HMRC removed Evergreen from the QROPS list). Victims have no idea where or how their pensions are invested. The pensions are allegedly invested in “The Treasury Plus Fund” (whatever that might be – and it is not likely to be anything good) and the trustee is Ward’s bogus trustee firm Dorrixo Alliance.

Nobody knows the total aggregate value of lost pensions and tax liabilities Ward has caused – we hazard a guess at a figure in the region of £100 million +.

Another double act by Stephen Ward and XXXX XXXX. This was the “sister” scheme to Capita Oak. Ward did the transfer administration – from safe, well-known and regulated pension providers to this bogus occupational scheme run by XXXX.

Neither Stephen Ward nor XXXX XXXX has ever been convicted or jailed.

Another pension liberation scam – placed in the hands of Dalriada Trustees by the Pensions Regulator.

Incartus was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported the scammers to the police as it is not “within their remit” to ensure the scammers are prosecuted.

None of the Incartus or Bluefin trustees scammers has ever been convicted or jailed.

£11.9 million worth of transfers were made, with the victims receiving approximately 50% of their pension as a loan and the promise of the rest being invested into a high-interest generating SIPPS. The loans were made from the pensions and therefore the victims have the usual HMRC tax demand letters. Further to the victims’ misery, the other 50% of the funds was not invested as promised. Most of the funds were swallowed by high commissions paid to the scammers.

None of the KJK Investments/G Loans scammers has ever been convicted or jailed.

Another of Stephen Ward’s many pension scams, this one was courtesy of his bogus pension trustee firm Dorrixo Alliance, his accomplice Gary Barlow at Gerard Associates, and introducers at Viva Costa International. Like Ward´s other scams, London Quantum scam was never set up for the benefit of the victims, but in the interests of Stephen Ward and his team of scammers to earn the maximum amount of commission out of the toxic, illiquid, high-risk investments.

The London Quantum scam is now in the hands of Dalriada Trustees.

London Quantum – like Ark, Capita Oak and Fast Pensions – was placed in the hands of Dalriada Trustees by the Pensions Regulator. But Dalriada has never reported Stephen Ward – or any of the other scammers – to the police as it is not “within their remit” to ensure the scammers are prosecuted.

Stephen Ward and Gary Barlow have never been convicted or jailed.

This pension liberation scam dating back to 2013 and 2014, involved around £1m of victims pension funds. Anthony Locke, was sentenced to a five-year jail term and Ray King, 54, who was employed by Lock, was given a three-year jail sentence.

It is great that these two crooks received jail terms, however, they are relatively “small fry” in comparison to the other serial scammers who are still walking free! The question remains: why have two minor players such as Locke and King been convicted and jailed while the “big fish” remain free to keep on scamming?

116 victims were scammed out of their pensions by James Lau of FCA-regulated Wightman Fletcher McCabe. Victims were assured the loans they were given did not come from their pension funds and would not be taxable by HMRC. The trustees of the scheme – Peter Bradley and Andrew Meeson (both ex HMRC) of Tudor Capital Management – were jailed for eight years for cheating the Public Revenue. James Lau is currently under criminal investigation by the Insolvency Service. The victims are awaiting a verdict on whether they will still have to pay the tax penalties.

James Lau has not yet been convicted or jailed – although he is clearly a wanted man.

This scam was facilitated by STM Fidecs in Gibraltar – one of Europe’s biggest QROPS providers. The regulator did order Deloittes to carry out an inspection into STM Fidecs’ books, but no action was taken against STM Fidecs for their part in this scam.

STM Fidecs accepted transfers into the QROPS by UK-resident victims “advised” by XXXX XXXX – even though he was not licensed to give financial advice. And then XXXX’s clients were 100% invested in XXXX’s own fund.

XXXX XXXX has not yet been convicted or jailed – although he is clearly under investigation by the Serious Fraud Office.

Another of the schemes under investigation by the SFO. This liberation scam with more than £3 million worth of (now worthless) investments was registered and administered by Stephen Ward.

Windsor Pensions

A no-frills pension liberation scam run by Florida-based Steve Pimlott. This scam has been going on for years and there is no sign of any let up – despite the fact that the regulators and ombudsman are well aware of Pimlott’s modus operandi. Pimlott doesn’t bother with any attempt to conceal the loans with fancy “loans” or complex mechanisms to try to “distance” the liberation from the pension transfer. He uses QROPS and a fraudulently-set-up bank account in the Isle of Man (of course!). HMRC catches many of the victims and charges them 55% tax on the liberated amount. Pimlott charges around 15% for the liberation.

Steve Pimlott has not yet been convicted or jailed

What a sorry state of affairs that out of all the pension schemes I have mentioned here, only one of them has seen the scammers jailed. Serial scammers like Stephen Ward and XXXX XXXX seem to slip the noose of justice again and again.

Berkeley Burke SIPPS – A SLIP OF THE TICK WITH THE SIPPS

We talk about the so-called “independent advisers” who sell scams to unwitting victims; we talk about the firms, introducers, cold-callers, lead generators, closers, couriers and transfer administrators. Many of the Pension Life blogs mention good old Stephen Ward – one of the leading scammers since 2010 – and we often try to make sure XXXX XXXX doesn’t feel left out either.

However, there is another link in the pension scam chain that is often forgotten about – the trustees. A pension scam always starts with two sets of trustees: the ceding trustee which hands over the funds to the scammers and the receiving trustee which allows the scammers to do their work successfully.

Ceding trustees have been ticking boxes and handing out thousands of victims’ life savings for years – in complete defiance of warnings by HMRC, the Pensions Regulator and the Scorpion campaign. It really is too much trouble for ceding trustees to look for the blindingly obvious signs of a scam – and the people these firms employ are obviously not that bright. Rather than actually doing anything which involves the magic word “trust” (or the four-letter word “work”), it is much easier – and cheaper – just to hand the millions over to the scammers.

I dread to think how much the lazy, negligent ceding trustees spend on pencils every year for ticking boxes, and blindfolds for making sure the transfer admin staff don’t ever see the scam warnings. The worst performers are always the same old same old names:

Aegon, Aon, Aviva, DHL, Friends Provident, Legal & General, Norwich Union, Pearl Assurance, Prudential, Royal London, Royal Mail, Scottish Widows, Standard Life and Zurich.

Since the Ark and Salmon Enterprises pension scams back in 2010, these lazy box-ticking trustees must have got through thousands of pencils and blindfolds. In fact, one ceding provider – Nationwide – deliberately handed over a pension even after they had received confirmation that the receiving trustees had been arrested for fraud and money laundering (and were later jailed for eight years).

However, this blog is written to address the equally damning and disgusting behaviour of negligent trustees who are at the receiving end of a transfer by the scammers – and allow victims’ pension funds to be invested in toxic, high-risk crap which only serves to pay eye-watering commissions to the scammers. We must remember that if such trustees are negligent, the scammers are able to succeed – and financial crime is inevitably facilitated.

One such negligent trustee is Berkeley Burke SIPPS Administration Ltd. At the end of October 2018, Berkeley Burke appeared in the High Court at the behest of the Financial Ombudsman. The matter involved a complaint by one of their victims: Wayne Charlton – a gardener. I have never met Mr. Charlton, so know little or nothing about him. But I have met a few gardeners in my time – and I wouldn’t say that any of them came close to being sophisticated investors. So I think it is highly unlikely that Mr. Charlton knew anything about investing or had any experience of the highly complex world of investment strategies.

In 2011, Mr. Charlton applied to transfer his existing personal pension to Berkeley Burke and to use the money for investment in an investment scheme run by scammers. Of course, he didn’t know the scheme was a scam at the time – although it was unquestionably a UCIS fund which should not have been promoted to a retail pension saver at all (and Berkeley Burke ought to have known this). Over 600 other victims were also scammed into investing around £ 12,250,000 in SIPPs operated by Berkeley Burke. However, it transpired that the investment scheme was a scam. And all the money was lost – all because Berkeley Burke was too lazy, selfish, stupid and careless to carry out any basic due diligence. Not just in respect of Mr. Charlton, but in respect of all the other 600+ victims.

There were a few basic warning signs that Berkeley Burke deliberately ignored:

The introducer was Mr. Stones of Big Pebble Limited. You would have thought that just the name: Big Pebble might have triggered at least a raised eyebrow. The firm was newly incorporated and had never traded.

The core question that was considered in the High Court by Justice Jacobs, was whether Berkeley Burke acted fairly and reasonably by accepting Mr. Charlton’s SIPPS investment into non-existent Cambodian land and Jatropha trees.

The judge decided it was blooming obvious that this was an unsuitable investment for a pension fund. Whilst Berkeley Burke could not give financial advice, they did, however, have a duty of care to their client. Justice Jacobs concluded that Berkeley Burke “did not act fairly and reasonably” with regards to Mr. Charlton’s investment. The point was made that they should have questioned the investment and made further investigations into it, and that had they done so they would have deemed that the investment was totally unsuitable.

But of course, it was much easier to go “tick” and let Mr. Charlton and more than 600 other victims lose over £12 million worth of life savings.

So my motto for pension trustees for 2019 is: Don’t be a Berk or a Burke – put those ticks away!

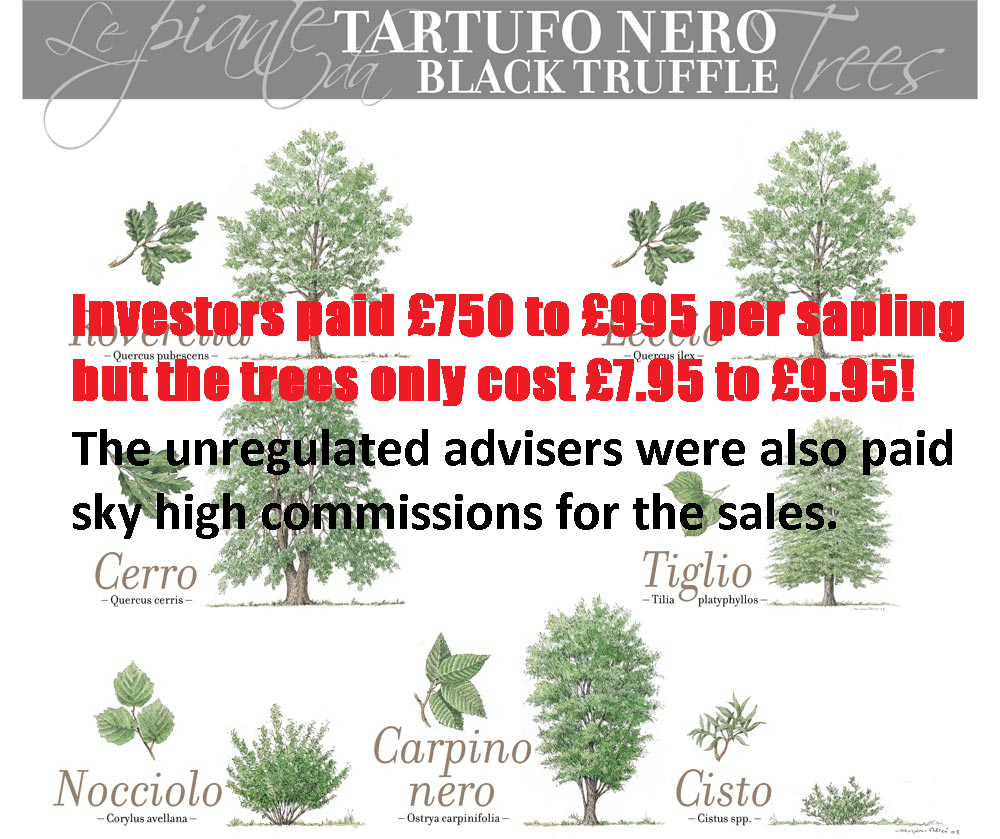

This could possibly be described as wonderful news for the victims of Viceroy Jones New Tech Ltd, Viceroy Jones Overseas PCC Limited, Westcountrytruffles Limited, Truffle Sales Ltd and Credit Free Limited. Or maybe not. The whereabouts of the funds is unknown. This pension liberation and investment scam saw 100 investors conned out of £9m of their pension savings.

In short, Viceroy Jones used unregulated financial advisory firms to persuade victims to invest in ‘high-value truffles for commercial sales’. With the promise of high returns on this fixed-term investment (lasting 15 years), investors believed they would reap the benefits once the truffles were harvested.

No truffles were ever harvested.

In reality, the investment saw most of the £9m of funds invested being paid into offshore bank accounts. These funds were then paid out in high commissions to the unregulated advisers who mis-sold the scheme. No supporting documents have been found regarding these investments, so the whereabouts of any remaining funds is unknown.

As I said above, it is only possibly wonderful news for the victims. Whilst the company has been wound up, the victims have been promised no compensation and do not know where their money is. This is a not an uncommon situation in scams like these. The victims of Peter Moat’s company –Fast Pensions, also do not know where their funds have gone.

Cheryl Lambert, Chief Investigator for the Insolvency Service, said:

“We take the matter of unregulated pension liberation investment schemes very seriously and will take action to stop any such schemes who have acted unscrupulously.”

However, I feel I have to disagree.

What message does the Insolvency Service send?!?

Are the perpetrators behind bars?NO!

Are the perpetrators having all their assets frozen and liquidated to pay the victim’s back? NO!

Are the perpetrators facing life without a pension?I DOUBT IT!

Are the perpetrators sorry for what they did?I DOUBT IT!

There is a long list of other pensions scammers who have scammed millions out of the public and still walk freely, creating new scam after new scam.

Winding up these companies is often of little help to the scam victims. What is left of their funds (if any) is passed on to another trustee (often Dalriada) to deal with the ‘clean up’. This action, however, is not without cost and often the funds just sit there doing nothing.

Take the Ark victims whose schemes were transferred to Dalriada – they have not had any compensation in the seven and a half years Dalriada has acted as their trustees. Dalriada, however, has continued – without fail – to charge their yearly fees and costs, further decimating the victims’ funds. AND without any suggestion of what will happen next!

Furthermore, victims that fell prey to these scams, face more stress as they are also contending with HMRC. The Taxman is sending out demands for huge tax bills, as they claim the money the victims liberated (“borrowed”) from the Ark schemes was not tax free. 55% tax is applied to money that was liberated from pension funds – this is deemed an “unauthorised payment charge” by HMRC.